LCC Estimation Model: A Construction Material Perspective

Faculty of Civil Engineering, Brno University of Technology, Veveří 331/95, 602 00 Brno, Czech Republic

*

Author to whom correspondence should be addressed.

Buildings 2019, 9(8), 182; https://0-doi-org.brum.beds.ac.uk/10.3390/buildings9080182

Submission received: 30 June 2019

/

Revised: 31 July 2019

/

Accepted: 6 August 2019

/

Published: 8 August 2019

(This article belongs to the Special Issue Life Cycle Prediction and Maintenance of Buildings)

Abstract

:The growing pressure to ensure sustainable construction is also associated with stricter demands on the cost-effectiveness of construction and operation of buildings and reduction of their environmental impact. This paper presents a methodology for building life cycle cost estimation that enables investors to identify the optimum material solution for their buildings on the level of functional parts. The functionality of a comprehensive model that takes into account investor requirements and links them to a construction cost estimation database and a facility management database is verified through a case study of a “façade composition” functional part, with sublevel “external thermal insulation composite system (ETICS) with thin plaster”. The results show that there is no generally applicable optimum ETICS material solution, which is caused by differing investor requirements, as well as the unique circumstances of each building and its user. The solution presented in this paper aims to aid investor decision-making regarding the choice of the building materials while taking the Life Cycle Cost (LCC) into account.

1. Introduction

Sustainable efforts are generally discussed from an environmental as well as economic perspective. On the one hand, there is a need to seek environmentally friendly solutions with minimum energy consumption and waste generation; on the other hand, there is the investor’s intention to pursue cost-effective projects. Building projects especially are marked by the fact that they are complex, are carried out over a long period of time, and face a high level of uncertainty and several risks affecting the final project outcome [1].

The building project should thus be considered in terms of its entire life cycle. In this relation, the BLCC approach (Building Life Cycle Costs) plays an important role as it focuses on cost optimisation throughout the entire life cycle [2] of a building. Zabielski and Zabielska [3] formulate LCC as a sum of the cost of purchase (project execution costs), cost of ownership (maintenance) and the cost of disposal decreased by the residual value of the property. This kind of planning of the building life cycle is crucial for informed decision-making [4], since operational costs usually significantly exceed construction costs [5]. For instance, it is estimated that about 80% of the energy use relates to the operational stage of a building’s life cycle [6].

A fundamental issue is to determine the lifespan of the building/building elements. In this regard, there is a lack of consensus in the relevant literature. Some authors consider the lifespan of 50 years [7,8,9], others use the value of 60 [10,11] years, while others even compare different service lifespans (30, 50 and 100 years) [12]. Generally speaking, the lifespan should correspond to the expected period of use, which may depend on the building’s technical parameters (wood/concrete structure) or expected time of operation (from the investor’s point of view), while it is also necessary to consider the lifespan of individual building elements. For example, Robati [13] uses 25 years as the period for replacement of glazed windows, so it is obvious that this particular element will be replaced several times during the lifespan of the building as a whole.

As a building’s lifespan ranges across decades, the prediction becomes progressively less accurate with increasing prediction time. This inaccuracy and uncertainty of costs within the operational stage is associated with several factors, e.g., predicted inflation rates (energy prices), availability of new technologies, changes in applicable legislation, inspection costs, insurance, and local tax or labour costs [14,15]. The accuracy of cost prediction depends on various aspects involving the level of information detail on the building [16] (materials, conditions under which certain activities can be carried out, e.g., the cleaning service [17]) and information about materials and related data on deterioration behaviour [18].

Within the building life cycle, a major part of the costs will be incurred at the later stages, i.e., especially in the operational stage. For future costs such as maintenance and repairs, appropriate discount rate should be applied [19]. The value of the discount rate is important [20], and the influence is more significant with lower discount rates [21], and vice versa. As a result, building investments should be evaluated in terms of the NPV (Net Present Value) indicator [9].

One of the most crucial investment decision-making issues consists of striking a balance between construction and operation costs [22]. This problem is complex, and it also involves the effect of energy prices (growing energy prices result in a more significant role played by operation energy costs in the early years of the lifespan) [10] and many other factors mentioned above. That is why many researchers apply various optimisation techniques, e.g., mixed integer linear programming [23], genetic algorithms [24], hybrid algorithms [25], and regression models [26,27]. Many researchers also apply LCC minimisation with regards to a specific natural hazard. For instance, this refers to buildings threatened by earthquakes and wind damage [7], flooding [28] or seismic risks [29]. In this regard, the LCC approach also differs in that it takes into consideration the vulnerability of buildings to a particular risk, the risk exposure in a given location, as well as refurbishment costs incurred on account of the damage. There are numerous studies providing methodologies for estimating loss caused by natural hazards (see e.g., [30] for flood risk); however, distributing these losses over the lifespan of the building is subject to uncertainty from the NPV perspective.

Recently constructed buildings have considerably improved thermal characteristics compared to older buildings. Incidentally, older buildings are often renovated with the aim of reducing energy consumption. In this regard, it should be noted that reduced consumption of energy during the operational stage of the building life-cycle usually comes with increased use of materials and the related environmental costs that may counteract its financial benefits [31]. Therefore, sustainable material cycles, recycling options and disposal costs [32,33] should be considered during the preparation of building projects.

In the area of public works, procurement is governed by applicable national legislation, which in the case of the European Union (EU) is based on Directive 2014/24/EU of the European Parliament and of the Council. According to the directive [34], “life-cycle costing shall to the extent relevant cover parts or all of the following costs over the life cycle of a product, service or works: (a) Costs, born by the contracting authority or other user (acquisition, use, maintenance and end life costs); (b) Costs imputed to environmental externalities linked to the product, service or works during its life cycle, provided their monetary value can be determined and verified”.

Unfortunately, no relevant databases of information on the expected lifetime of products, the time and extent to which they require repairs and the costs of maintenance of given structures are not available. That is why the LCC approach is rarely used in procurement practice. Nevertheless, such data should be processed in future BIM (Building Information Modelling) systems. In the future, the BIM model should serve as a source of information informing the work of the individual participants of the construction process. An approach that includes information with the BIM model will benefit from the data repository of transfer formats, allowing quick editing of the information and updating of the LCC value [35]. The integration of BIM and LCC serves to ensure better maintenance accessibility and enhanced collaboration between asset and maintenance management [36,37].

This paper therefore reflects the growing pressure to ensure sustainable construction, which is also associated with stricter demands on the cost-effectiveness of the construction and operation of buildings and reducing their environmental impact. The objective of the research is to propose a methodology enabling the selection of an optimum building material solution for the individual functional parts of a building in terms of life cycle costs. This case study involves the proposed and applied methodology for a selected functional part: “Façade—external thermal insulation composite system with thin plaster” in the context of the current state of the Czech construction sector.

The article is structured as follows: Firstly, the current state of knowledge is presented, followed by materials and methods and a description of the proposed methodology, where the methodology is then applied to the selected functional part in variant solutions and discussed. The final chapters summarise the research findings and limitations and outline future research directions.

2. Materials and Methods

A proposal for a methodology for LCC calculation with respect to construction materials requires several steps. With regard to LCC calculation standards, it is first necessary to define the required input data (see Section 2.1); specify the lifetime, the cycle and frequency of repairs, and the maintenance of the functional parts of buildings (Section 2.2); and then to propose a system for data exchange (Section 2.3).

The LCC indicator is calculated based on the formula indicated in the European ISO 15686-5:2017 [38] standard, which is based on the discounting of future costs during the examined period. Discounting means adjusting future costs (costs of reconstruction, utilities, maintenance, etc.) with respect to their present value. LCC are calculated according to following formula:

where:

- Ct denotes all costs as equivalent cash flows in year t;

- r is the discount rate;

- t is the analysed year (t = 0, 1, 2…, T);

- T is the length of the life cycle in years.

Other models, such as those published by Bromilow and Pawsey [39] or Sobanjo [40], are based on the principle of different discounting of regular and irregular costs.

2.1. Input Data Requirements for LCC Calculation

For the purposes of LCC calculation, input data are required in three main areas. Specifically, this includes determination of the length of the examined period, the value of the discount rate, and the identification of the individual types of costs arising throughout the life cycle.

The length of the examined period either corresponds to the expected lifetime of the building, or can be set as a specific period corresponding to the investor’s requirements. The expected lifetime of buildings in the Czech Republic is indicated in [41], where, e.g., a masonry building is expected to have a lifetime of 100 years.

The discount rate used when modelling LCC is up to the individual investors, but it should correspond to the rate of return of other similar projects or requirements for specific types of public projects. A 5% rate is commonly used [9,42]. Costs arising throughout the life cycle of a building then constitute the acquisition costs, operational costs (maintenance, repairs, replacement) and disposal costs. For the purposes of the present research activity, the discount rate was set at 5%.

The most complex part of the calculation consists in defining and quantifying the costs incurred in the operational stage of the building’s life cycle. It is necessary to define the scope and frequency in which the individual parts of a building have to be maintained, repaired or replaced. Each structure has different requirements when it comes to maintenance and repair, including a different expected lifetime. As a general rule, however, one of the main factors that has an impact on the expected lifespan is the material used to build a given structure. Other factors include the quality of production, quality of construction work, and maintenance frequency.

The calculation of LCC makes it desirable to divide the analysed building into functional parts (FP). It is then necessary to establish the relevant repair, maintenance and replacement cycles, and costs; this study uses the data provided in [43]. For instance, “Exterior plasters, insulation” have their FP lifetime set to 30–60 years, with a repair cycle of 30 years and the scope of repairs of 20%.

2.2. Establishing the Lifetime, Cycle and Frequency of Repairs and Maintenance of Functional Parts

The process of establishing the aforementioned values is based on a survey of already built and operated buildings included in a facility management (FM) system. In this regard, it is vital that the FM system contain data on the individual costs of repairs, maintenance and replacement (R/M/R), including the time when the given intervention took place. Using the aforementioned recorded data, it is possible to calculate the average R/M/R costs and the average length of the cycle between individual R/M/R interventions, where the average costs are calculated using the following formula:

where

- Cycle_A is the average length of the cycle between two individual activities (A), provided separately for each R/M/R component;

- DC is the date of construction;

- DA1 is the date of the 1st R/M/R activity;

- DAi is the date of the i th R/M/R activity;

- n is the number of R/M/R activities.

The concept of collecting R/M/R information and its transformation into a database of lifespans, frequencies and costs of repairs and maintenance of functional parts is introduced in [44]. Calculating LCC requires effective communication between three systems: (1) The LCC calculation system; (2) the FM system; and (3) the building cost estimation system, which is necessary to establish unit prices and other information from the price database that influence LCC calculation over the entire life cycle of a building. Another system that can be incorporated is the system for creating BIM models. A BIM model is essentially a database of all of the information on the building, which can thus serve as a source of input data for LCC calculation (e.g., surface area, materials used, dimensions, characteristics, etc.); conversely, information obtained through the LCC calculation can be transferred back into the BIM model for future use.

Each of the above systems usually operates with a different data structure and a different classification of individual building structures. Accordingly, it was necessary to find a suitable structural division of a building that would be compatible with all the component systems. The proposed connecting database is based on a division of a building into four functional units—load-bearing structures, roof structures, façade and surface treatment of interior spaces. The individual functional units are divided into functional parts (FP); a detailed division is provided in Table 1. Functional parts are further divided according to the implementation possibilities or other distinct features of the given structural part. This brings multiple benefits over the building’s life cycle, both in terms of managing its construction and cost management in the operational stage. This makes it possible to consider functional units as actual parts incorporated in a building that are supplied as a whole. Since there is no clearly available database for use in LCC calculation and the facility management system, the proposed connecting database appears to be the default option for both systems.

2.3. General Description of the System

The entire process begins with the design of a building. If the design is made using a BIM tool, it is important for the maker of the BIM model to supply information to classify all building structures into functional units and functional parts. The BIM model’s level of detail is high (LOD 200 to LOD 300) in order to include the selected construction solution, materials and dimensions, general information on the building and the size of the individual structures. If the design is made using traditional tools (2D design), the designer must input all the necessary information into the LCC calculation system manually. The required information (parameters) are dependent on the type of functional part, but generally speaking, this means its material characteristics and size. Among other information, functional parts also require information generally related to the whole building—its height, location etc.

Once a building is classified into distinctly defined functional parts, the system for LCC calculation will communicate with the building cost estimation system. Individual items of the price database carry an information on classification into functional parts, i.e., the items from which the information necessary for LCC calculation will be retrieved (e.g., unit prices, unit weight, rubble, time needed for (dis)assembly in standard hours).

The next stage consists in obtaining information for the calculation of costs in the operational stage of the building, i.e., the costs of repairs, maintenance and replacement (R/M/R). R/M/R costs information is transferred from the price framework of the building cost estimation system. As described above, there is a challenge consisting of the availability of information on the scope and frequency of R/M/R. The information can be entered into the LCC system in two ways:

- Information on the R/M/R scopes and frequencies of the individual functional parts is based on observation of already built buildings. The information is managed in the facility management system and can be transferred to the LCC calculation system via the connecting database (see Section 2.2).

- Repairs are simulated by the designer (LCC system user) based on experience or assumptions regarding the orientation or use of the building. The lifetime and maintenance can potentially be indicated by the manufacturer of the materials or can be simulated by the user as in the case of repairs. This possibility of recording can be used by users who lack data from the facility management system.

The final stage consists in entering the calculation conditions. The conditions are based on the LCC calculation formula itself—discount rate and the examined period. These parameters are dependent on the customs of the investor and the building’s character.

Once all information necessary for the LCC calculation has been entered or transferred from the individual systems, the calculation itself takes place. The entire calculation can be divided into five stages:

- calculation of acquisition costs;

- calculation of replacement costs;

- calculation of maintenance costs;

- calculation of repair costs;

- calculation of disposal costs at the end of the building’s lifetime.

The individual stages of the calculation, i.e., the structure of the calculation, differ for each functional part in terms of the manner of costing, e.g., the costing of a reinforced concrete wall differs from that of façade composition. The manner of costing is based on custom and the principles of building cost estimation.

After the calculation has been completed, an important added value of the proposed system consists in finding the most suitable solution that meets the same or better characteristics as the original solution. These properties depend on the type of the functional part and its typical characteristics, e.g., thermal insulation properties, dimensions, strength, etc. The proposed system will then calculate LCC for all alternatives and order them on the basis of various characteristics: acquisition costs, LCC, LCC minus acquisition costs, and so on. The user thus obtains a basis that will enable them to make a design based on the best possible solution.

If a BIM model is available, direct transfer of information from the LCC calculation system into the BIM model is possible. In particular, this refers to information on the acquisition price, frequency and cost of R/M/R, which benefits the planning of funding sources in the upcoming operational stage of the newly constructed building. This makes the BIM model multi-dimensional, since it contains information on costs, facility management and partially also information on time (time of assembly of the individual building structures).

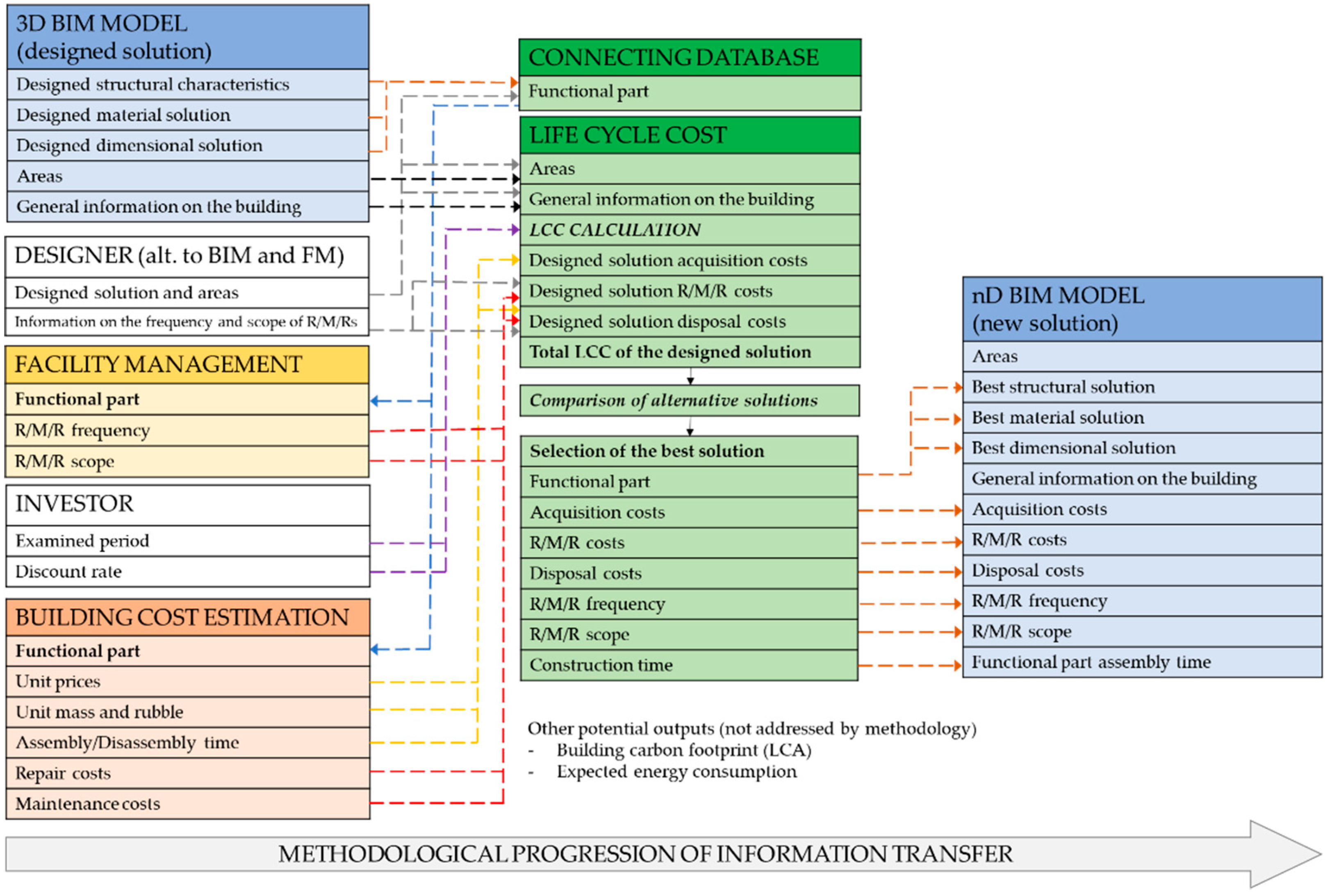

The whole process of data exchange among the individual systems is shown in Figure 1. The diagram also shows other possibilities for linking the individual systems—LCA and energy consumption—which, however, are not part of the proposed methodology. Similarly, the methodology does not address costs associated with the entire project, i.e., costs associated with project documentation and other costs borne by the investor or the contractor. The proposed methodology covers only the costs associated with the structures incorporated in the building. The methodology addresses the structure of information and its processing in the individual systems, but not its mutual systemic interconnection at the data transfer level.

3. Applying the Model: Case Study of the “Façade Composition” Functional Part

To demonstrate the functionality of the system, the chapter below presents a proposed solution for calculating LCC for the functional part designated “façade composition”. In the first stage of the process, the creator of the BIM model must define the structural, material and dimensional characteristics of the façade. The façade composition functional part can be divided into four sublevels depending on the construction solution:

- external thermal insulation composite system (ETICS) with thin plaster;

- external thermal insulation composite system (ETICS) with facing;

- plaster only;

- facing only.

The “external thermal insulation composite system (ETICS) with thin plaster” sublevel of the “façade composition” functional part, was selected for the case study. Viable types of external thermal insulation composite systems (hereinafter ETICS) and thin plasters are selected from the price database [46], which essentially contains all material and dimensional possibilities and is key for determining the costs. A total of 11 ETICS types and 13 thin plaster types were selected; a list of these, together with further details, is presented in Table 2 and Table 3. There are 143 potential combinations. The thickness of the material depends on the type of ETICS and thin plaster used.

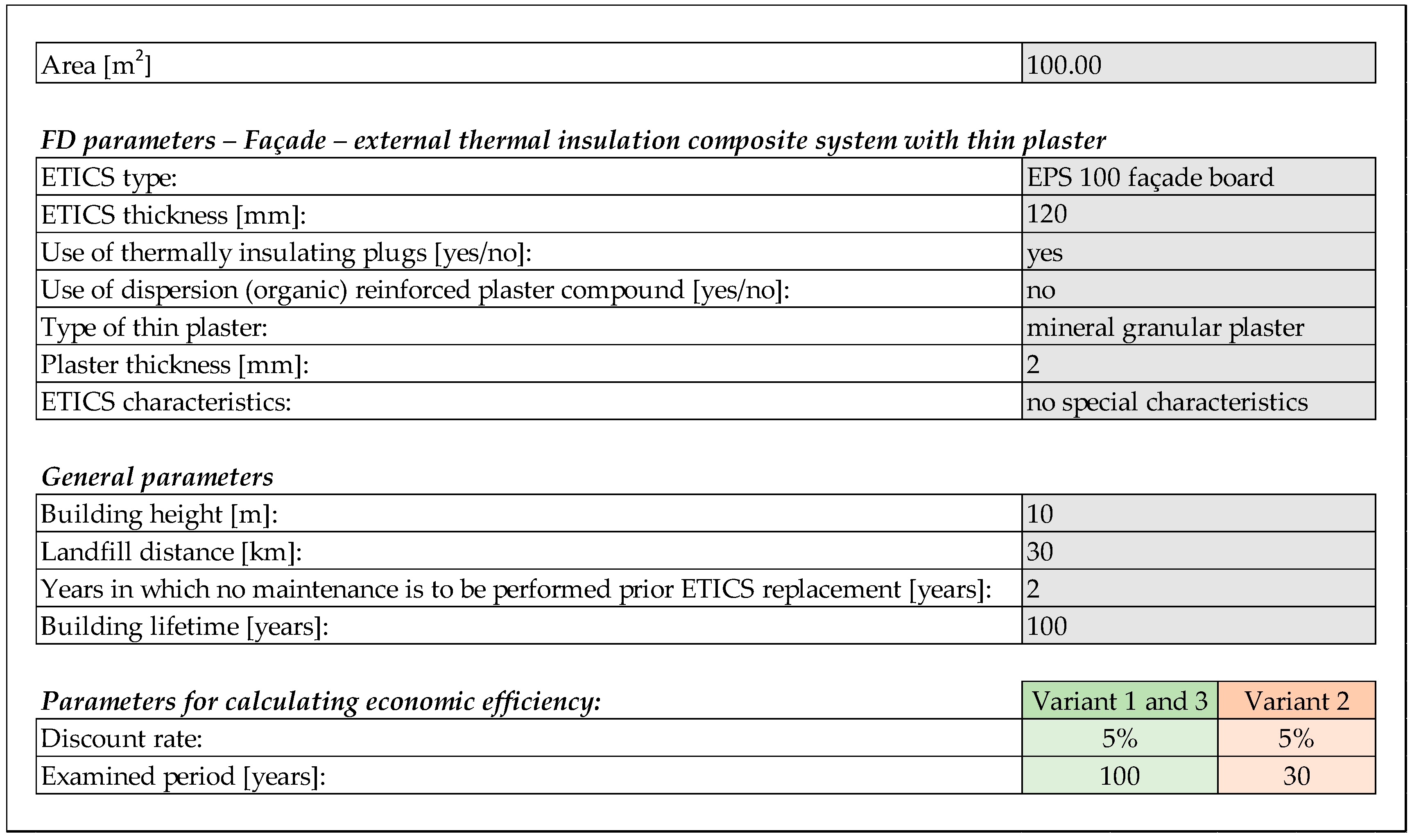

The above material and dimensional characteristics (Table 2 and Table 3) are key to the proper classification of the proposed solution and must be inputted to the BIM model by its creator. Figure 2 shows the list of input information necessary for performing the LCC calculation. Aside from the material and dimensional characteristics of the façade layers, it also includes information that must be entered for the purposes of identification of all costs associated with implementing the façade layers. For the LCC calculation itself, it is also necessary to input the investor’s requirements for LCC modelling—the discount rate and the length of the examined period based on the DCF model.

For a specific demonstration of how the proposed system works, the chosen default material solution consists of ETICS EPS 70 façade board (120 mm thick) with mineral granular plaster (2 mm thick)—see Figure 2. The input parameters of the discount rate and the examined period are modelled in three variants:

- Variant 2—The examined period is set to 30 years, i.e., the minimum lifetime of “Exterior plaster, insulation” according to [43], while the discount rate remains identical to Variant 1, i.e., 5%.

3.1. Calculation of Acquisition Costs

The calculation of acquisition costs for implementation of the façade layers consists of the items of the price database [46]. The use of the individual items of the price database depends on the type of ETICS or thin plaster used, respectively. The external thermal insulation composite system is costed separately for assembly and supply of material. Assembly of ETICS is differentiated according to the system’s type and thickness:

- assembly of polystyrene external thermal insulation boards—thickness under 40 mm, under 80 mm, under 120 mm, under 160 mm, under 200 mm, under 240 mm, over 240 mm;

- assembly of external thermal insulation mineral wool with longitudinal fibre—thickness under 40 mm, under 80 mm, under 120 mm, under 160 mm, over 160 mm;

- assembly of external thermal insulation mineral wool with perpendicular fibre—thickness under 40 mm, under 80 mm, under 120 mm, under 160 mm, under 200 mm, over 200 mm.

The price of the “ETICS assembly” item also includes the costs of assembly and supply of levelling compounds and fiberglass mesh. Each assembly item includes information not only on the unit acquisition price, but also information on the mass, which is essential for material transport calculations, and on the time demands of the work in standard hours, which is a required figure for calculating the assembly time.

The material corresponds to various types of ETICS indicated in Table 2. The thickness of the insulating material indicated by the manufacturer is distinguished. Each item of material also includes an information on the unit price and mass, where the thermal resistance is calculated according to the thermal conductivity coefficient and the insulating material thickness. Thermal resistance is important for finding variants from among the individual ETICS types with the same or improved characteristics.

ETICS costing also includes potential extra costs. The use of these extra costs is conditional on entering information into the BIM model in the form of an associated parameter. The following extra costs are included:

- for anchoring boards 22.5 m and higher above ground—determined according to the insulating material thickness;

- for use of thermally insulating plugs—determined according to ETICS type;

- for use of dispersion (organic) reinforced plaster.

The supply and assembly of thin plaster are indicated as one item in the price database. The price of the item also includes the costs of priming the substrate. As in the case of the ETICS, each item of the thin plaster includes information on the acquisition price, mass, and assembly time in standard hours. The thermal resistance of thin plaster is negligible and is disregarded.

Complete supply and assembly of the “external thermal insulation composite system with thin plaster” also carries some associated costs such as material transport, where the total mass of all the items used is added up. The items of material transport depend on the height, type and construction solution of the buildings, as well as on whether mechanisation is used fully, partially or not at all. The case study assumes full use of mechanisation in the construction process. Another cost involves the assembly, lease and removal of scaffolding and the possible use of safety nets. The price database distinguishes multiple types of scaffolding—light tubular scaffolding, heavy tubular scaffolding, light frame scaffolding, heavy frame scaffolding. Based on the calculation needs, the most commonly used type of scaffolding will be considered—light frame scaffolding with decking size of up to 1.2 m. The cost of scaffolding lease corresponds to the ETICS assembly time converted to working days. One of the user-entered parameters is the height of the building, which affects the use of items for extra costs associated with the assembly of ETICS, scaffolding and material transport.

3.2. Calculation of Replacement Costs

The replacement of a structure is assumed to occur at the end of the given functional part’s lifetime, where the replacement costs are determined by the sum of disposal costs and the acquisition costs. The proposed system assumes that the lifetime of thin plaster is the same as the ETICS lifetime. The ETICS lifetime is based on the R/M/R database and is either transferred from the facility management system or can be entered by the designer based on his experience (see Section 2.3).

The price database [46] distinguishes between disposal of polystyrene boards and mineral wool boards, where it only takes into account the thickness of the disposed insulating material. The ETICS disposal item also includes the thin plaster disposal costs. Costs associated with the transport of rubble and the disposal of waste constitute an important part of the calculation. The result depends on the mass of the disposed material (rubble). Each disposal item includes information on the mass of the building structure being disposed; however, for an exact value, the mass of items used for the calculation of acquisition costs will be used. Costs associated with rubble transport are divided into two parts—vertical transport, which depends on the height of the building and relates to transport within the building, and horizontal rubble transport associated with moving the rubble from the construction site to a landfill. The distance of the landfill from the construction site is one of the parameters that must be entered by the user. The rubble dumping fee constitutes another cost, where its amount depends on classification of the waste according to waste catalogue decree.

3.3. Calculation of Maintenance Costs

Each structure has to be maintained in some way during its operational stage. In the case of the façade functional part, maintenance concerns the layer that is in contact with the air, i.e., thin plaster. As mentioned above, it is necessary to establish what needs to be carried out and how often. Two possibilities for creating the R/M/R database include creating it based on personal observations or according to the manufacturer’s guidelines or own discretion (see Section 2.3).

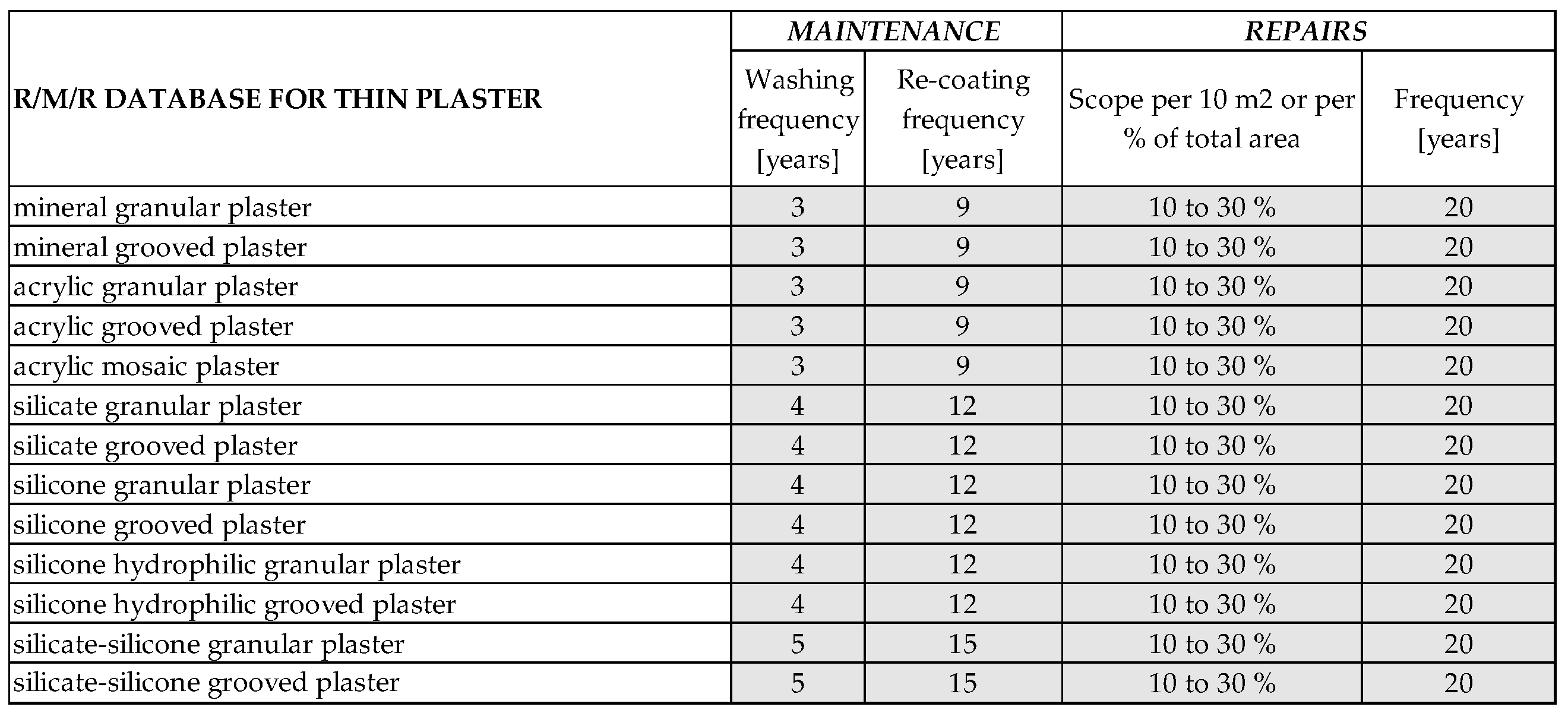

The database determines the scope and frequency of maintenance, where it is not possible to alter the data as they are the result of long-term observations. The other option consists in simulating maintenance based on the manufacturer’s recommendations and own experience. The main advantage of a simulation is the possibility to alter the inputs, since each building is exposed to different factors. Cities with high amounts of dust in the air (and thus higher dirt deposition on the façade) require a different level of maintenance than buildings in the countryside with lower traffic pollution levels. The user of the system has the manufacturer’s recommendations available and can modify them based on the user’s own experience. Based on the technical guideline of the plaster system manufacturer, it is necessary:

- to clean the façade with pressurised water every 3 to 5 years;

- to apply façade coating to plastered surfaces every 10 to 15 years.

The user can only influence the frequency of the individual stages of maintenance. The costs of the individual stages of maintenance are determined by the price database. Pressurised water cleaning has the same cost for all types of plasters. Only the coating type is determined by the plaster type. The price database [46] distinguishes 4 types of coatings for thin plasters, where the unit price is determined by the façade topography ranked 1 to 5. Topography levels 3 to 5 are practically absent in contemporary buildings because they are very costly due to the inclusion of ledges, window framing, pilasters, embedded columns, etc. Topography levels 1 and 2 are associated with the same unit price and the calculation thus need not be adjusted in any way. Table 4 shows the association of the individual types of coatings to the individual types of plasters.

The system gives the user an option to influence the calculation of the maintenance costs by enabling the user to determine when the LCC should include maintenance of thin plaster due to upcoming ETICS replacement.

3.4. Calculation of Repair Costs

The need to repair functional parts can, but does not have to, appear during their lifetime. This is the part of the LCC calculation that most relies on an own database of R/M/R and has appeared in comparable buildings that are already in operation. Nevertheless, even here, the user can set the expected scope of potential repairs based on his own experience. The only eventuality in which the ETICS with thin plaster functional part would have to be repaired during its lifetime consists of physical damage, such as perforation. From the point of view of the price database, a repair of the insulation system is determined by the ETICS type, thickness and the size of the part needing repair. Specific division is shown in Table 5.

The unit price of replacement assumes cutting out the existing insulating material, applying binding compound and inserting fiberglass mesh. Unfortunately, the price system [46] does not include the possibility of choosing different insulation types as in newly constructed structures. To facilitate LCC calculation, items from the price database were adjusted so that they correspond to newly constructed ETICS, i.e., to include the assembly and material separately.

In the event of damage to the ETICS, thin plaster has to be repaired in the same scope as the ETICS. However, the plaster itself can be repaired separately, e.g., if it crumbles away or is worn by pressurised water cleaning or otherwise. The price database determines the scope of the repaired area, either by directly inputting the repaired area or using a percentage of the repaired area. Specific division of thin plaster is shown in Table 6. Types of plaster are identical to the division for newly applied plaster.

The scope of repairs (see Table 5 and Table 6) of ETICS and thin plaster indicates the size of the damage that needs to be repaired. The scope is indicated either as a percentage of the total area or the actual area to be repaired. For the purposes of the proposed system, the scope is defined as actual area to be repaired per each 10 m2.

3.5. Calculation of Disposal Costs at the End of the Building’s Lifetime

Each building, as well as its individual parts, has a lifetime. The lifetime of the entire building is determined by the lifetime of its load-bearing parts—foundations, walls, ceilings, etc. At the end of its lifetime, the building and its individual functional parts must be disposed of (demolished). The costs of disposal are detailed in the chapter of this paper dealing with the calculation of replacement costs. Calculating this cost is dependent on making the examined period correspond to the entire lifetime of the building. When entering an examined period for the LCC calculation shorter than the lifespan of the entire building, this cost will not be counted in.

3.6. Proposed Structure of the R/M/R Database

The above LCC calculation process increases requirements for the structure of the R/M/R database. The R/M/R database, i.e., its structure for the functional part designated “façade composition—external thermal insulation composite system with thin plaster”, must indicate the ETICS and thin plaster separately. The reason for the division is the fact that it is not possible in terms of facility management to monitor all façade layers as a whole; for this functional part alone, this would be 143 possible combinations and, therefore, obtaining a relevant R/M/R information sample from facility management would not be realistic.

In the case of ETICS, the facility management system must record information on the lifetimes of the individual types of ETICS, the scope of repairs per 10 m2 of area and the frequency of the repairs. The possibility for recording the scope of repairs is based on Table 5. In case the R/M/R database from the facility management system is not available, the designer must input the information manually.

As mentioned above, the lifetime of thin plaster corresponds to the lifetime of ETICS and this is taken into account in the LCC calculation; therefore, it is not necessary for this to be included in the R/M/R database. Thin plaster chiefly requires recording and determination of the frequency of maintenance, i.e., façade washing and re-coating. As with ETICS, it is necessary to monitor, i.e., record the scopes under Table 6, and the frequency of repairs for the individual types of thin plaster (aside from ETICS repairs where plaster repairs are automatically included).

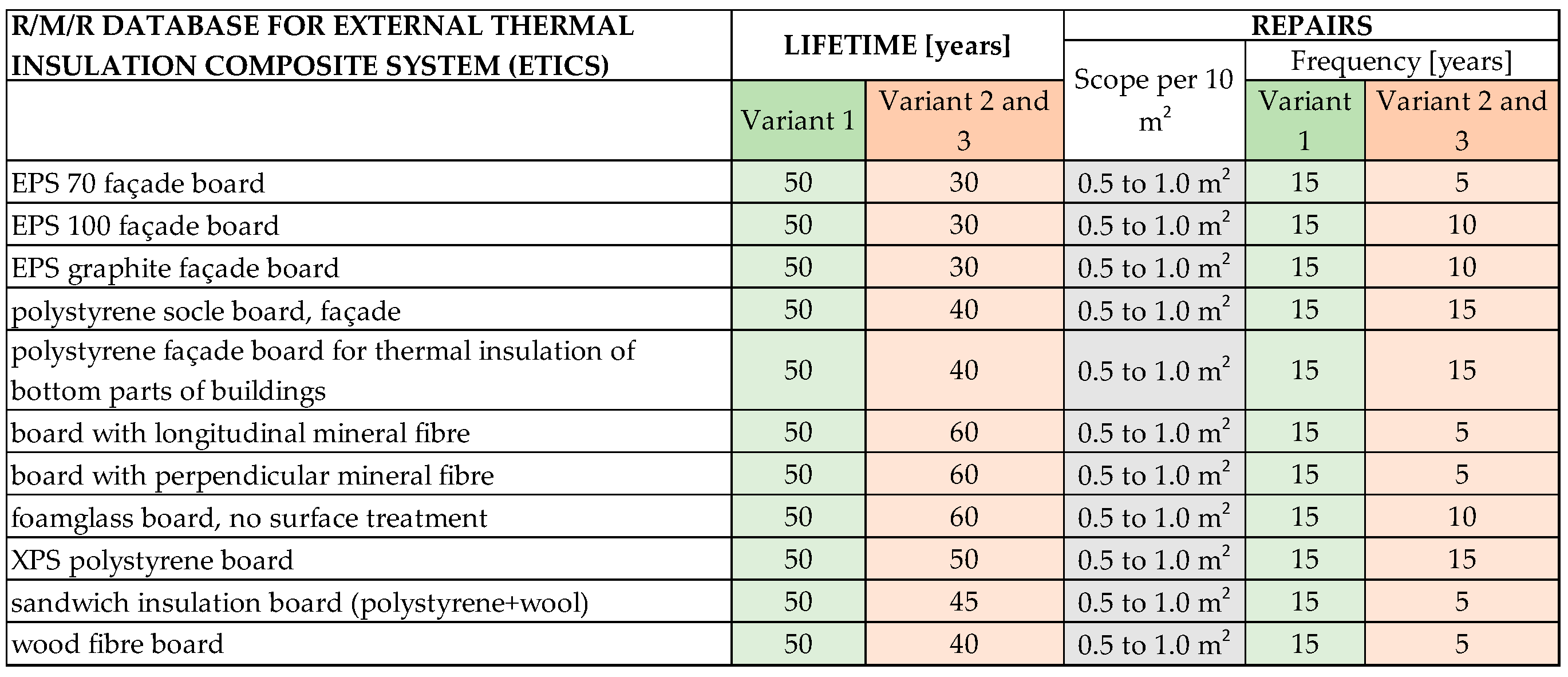

Since the Czech Republic lacks a suitable R/M/R database, the functioning of the system is showcased by manual input of information based on the manufacturers’ data or the expected lifetime and repair frequency of the individual ETICS types. The R/M/R database is modelled in three variants (see Figure 3 and Figure 4):

- Variant 1—lifetime and scope and frequency of maintenance entered based on the manufacturer of ETICS [47]. The scope and frequency of repairs corresponds to the data included in [43] (with regard to repairs of ETICS, the proposed system does not offer the possibility of repair in the scope of 20%—this is replaced by the highest possible value of the scope of repairs, i.e., from 0.5 m2 to 1.0 m2, and an increased frequency, i.e., 15 years).

- Variant 2 and 3—the R/M/R database is filled in based on the possible assumed development of the lifetime and repairs of the ETICS. In comparison to Variant 1, the lifetime of the individual types of ETICS is adjusted according to the lifetime intervals indicated in [43]. Further adjusted is the frequency of repairs which is based on the expected resistance to mechanical damage on the part of the individual ETICS types.

3.7. LCC Calculation and the Selection of the Best Variant

Previous chapters described the process of calculation and defining costs arising over the course of a building’s life cycle depending on information transferred from the BIM model and R/M/R database. An important input for the calculation consists in setting parameters for the actual LCC calculation from the point of view of the investor—the examined period and the discount rate. Individual costs of repairs, replacement, maintenance and disposal of the given FP are subsequently adequately discounted so that the investor obtains a net current value of the investment for the examined period.

The LCC calculation system simultaneously identifies alternatives to the input ETICS layers. The alternatives to the ETICS must meet the condition of identical or better thermal conductivity in order to preserve the key parameter of designing the ETICS; in thin plaster, the alternatives must be of identical or higher thickness to maintain the building’s aesthetic properties. Alternatives are subjected to the same LCC calculation as the designed solution. Subsequently, the LCC calculation system ranks the best variants of the ETICS and thin plaster in terms of acquisition costs and discounted LCC. The designer can then choose the best solution for his design.

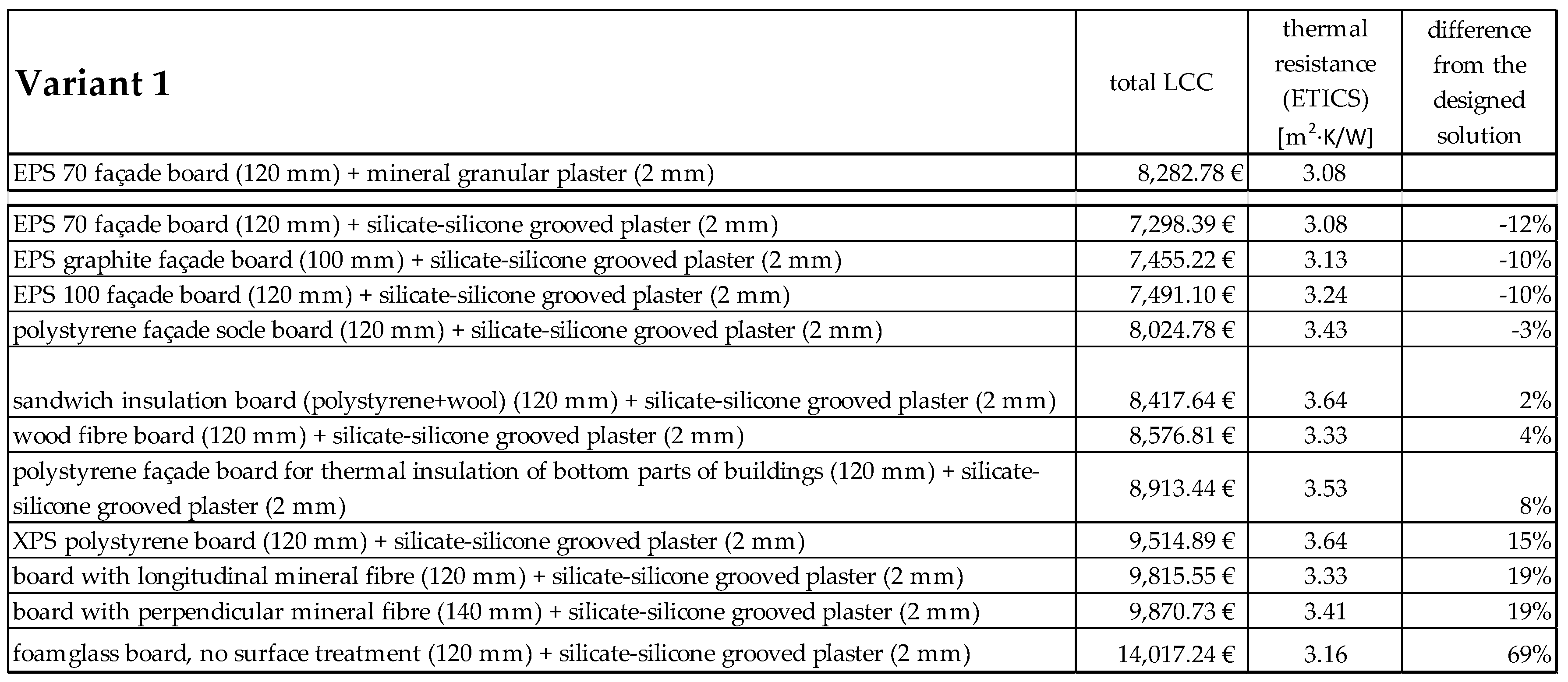

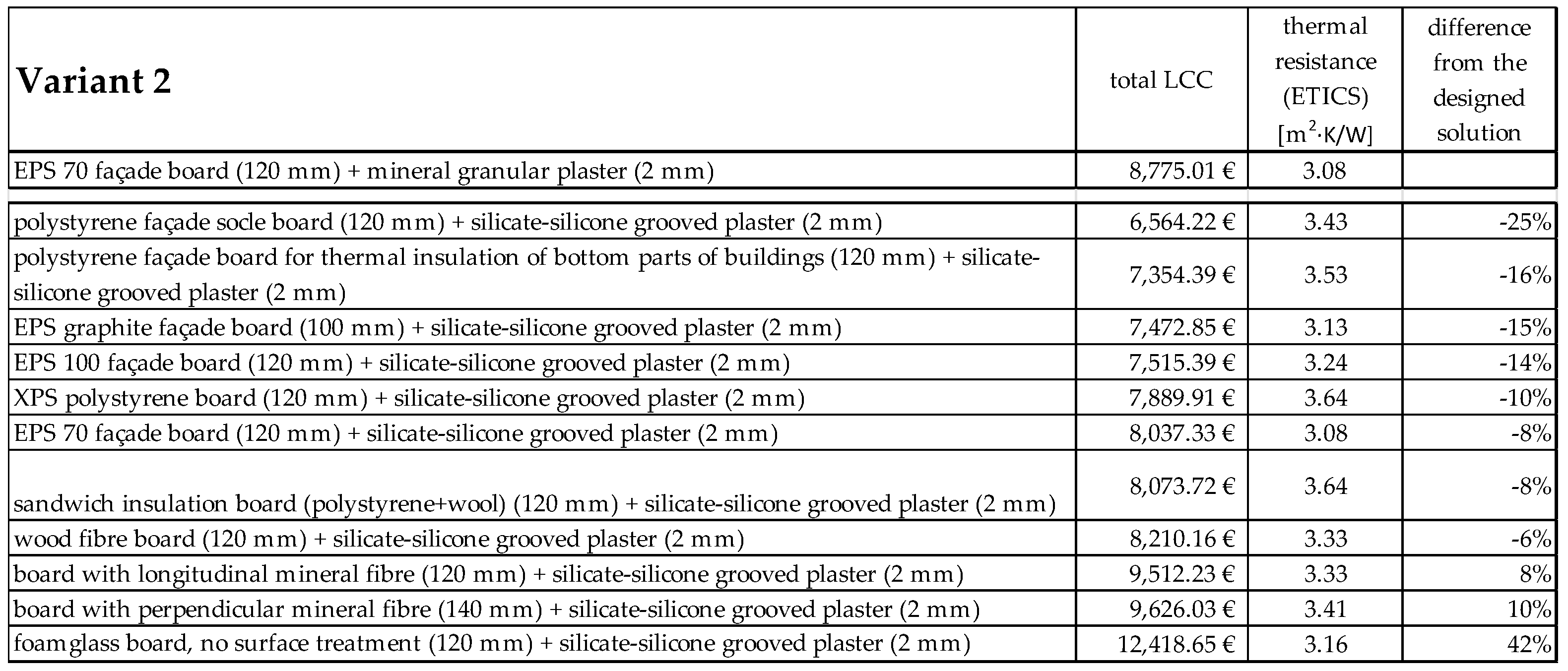

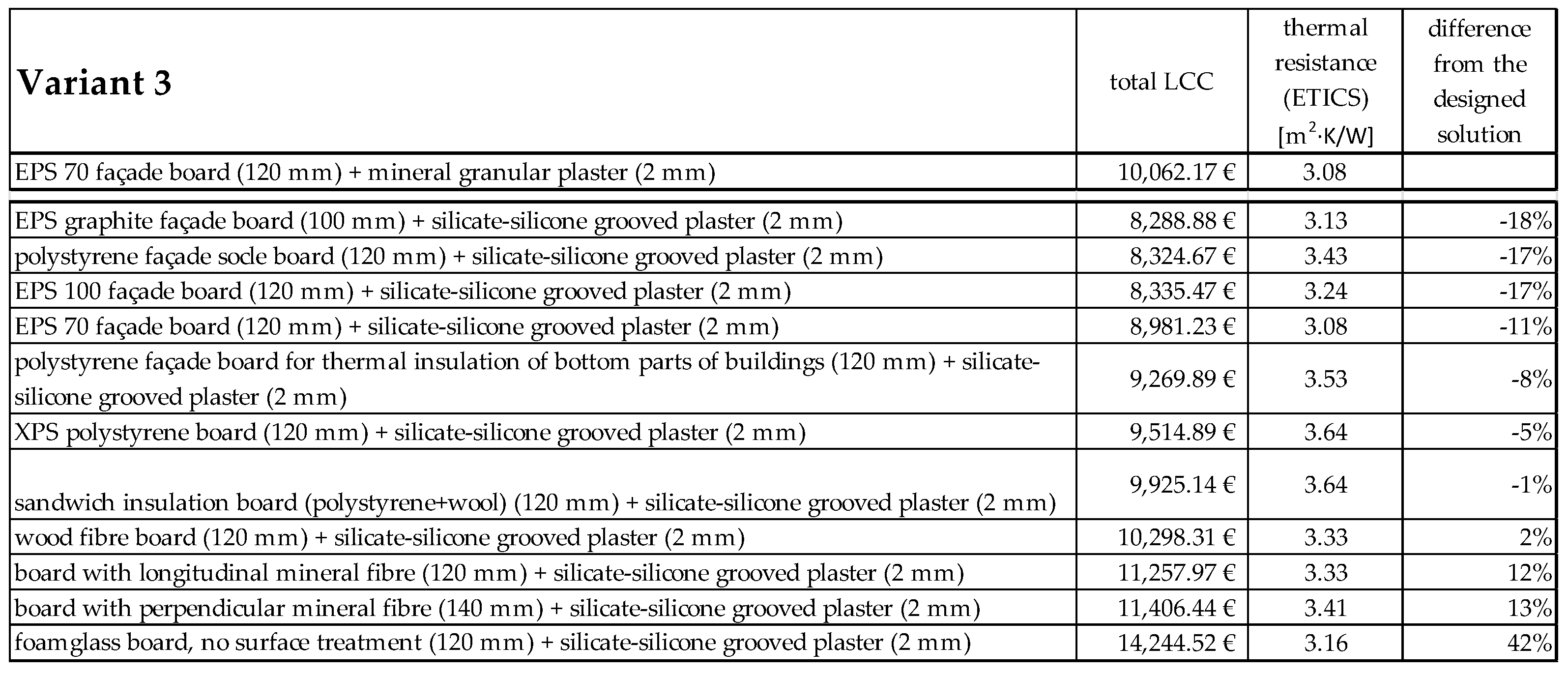

The results of the calculation for all three modelled variants of input parameters and R/M/R database are shown in Figure 5, Figure 6 and Figure 7. The first line includes the initial design variant, with the alternatives ranked below according to the lowest LCC value.

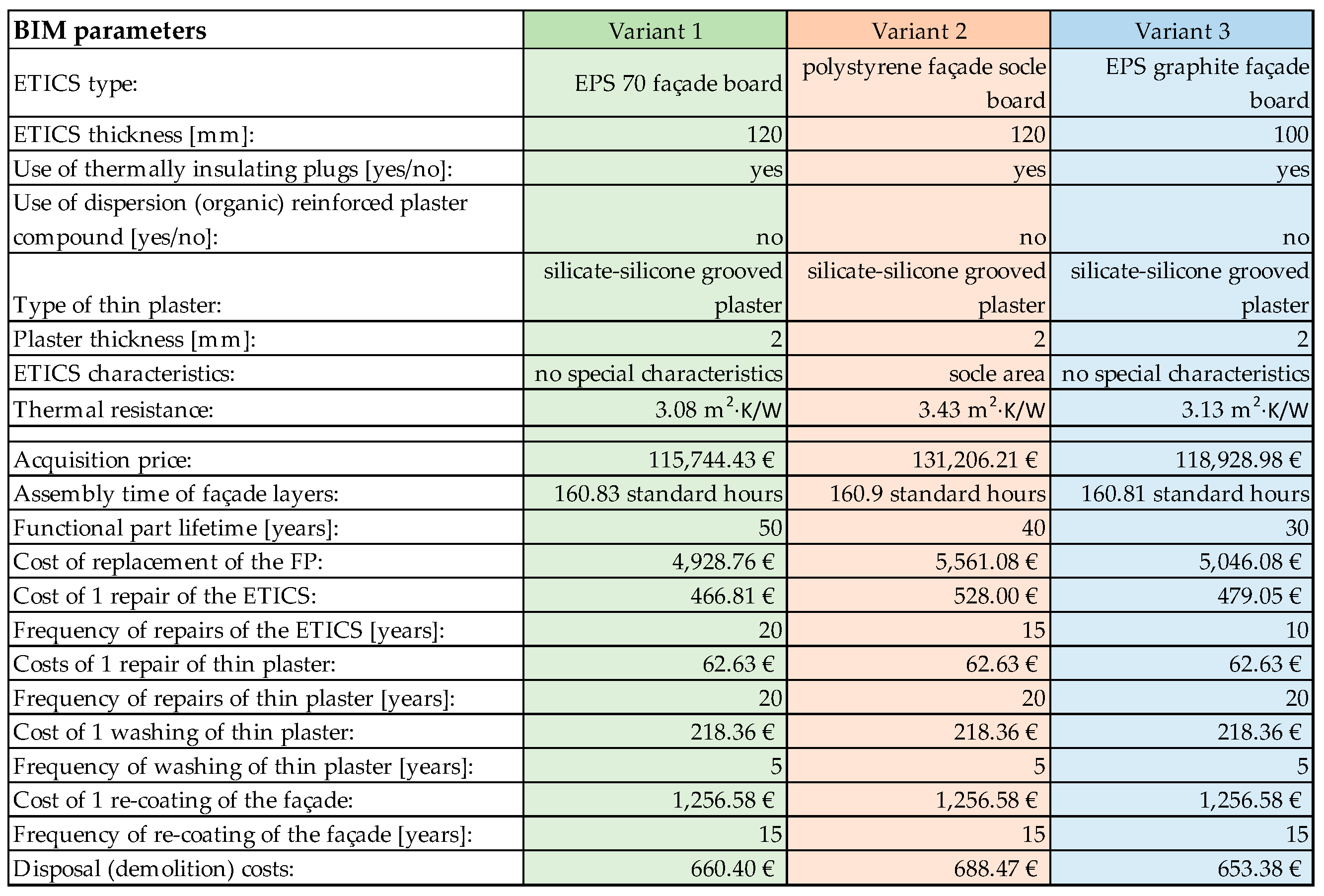

Once the designer chooses the best solution, it is possible to transfer into the BIM model the information necessary for construction—acquisition price, assembly time—as well as information for the future operational stage of the building’s life cycle—frequencies and costs of R/M/R and the disposal costs. The LCC value itself depends on the calculation parameters (the length of the examined period and the discount rate) and serves essentially as an evaluation criterion for choosing the best solution. An example of transferring selected parameters into the BIM model is shown in Figure 8.

4. Discussion

Section 3 showcased the proposed information exchange system and calculation of a building’s LCC on the example of the functional part designated “façade composition”. Multiple parameters and types of information enter the LCC calculation (see Figure 1) and influence the resulting value. As a case study, an LCC calculation was performed for an external thermal insulation composite system (ETICS) with thin plaster in three variants in terms of parameters and characteristics. The variants included different inputs of the length of the examined period (100 years in the first and third variants and 30 years in the second variant) and different input of the R/M/R database. The R/M/R database differed in the individual variants in terms of the entered lifetime and frequency of repairs of the ETICS, where in the first case, all ETICS types had the same lifetime and frequency of repairs, while different values were modelled in the second and third cases. The proposed design of façade layers included ETICS EPS 70 façade board (120 mm thick) with mineral granular plaster (2 mm thick). The system then calculated a discounted LCC design solution for the individual variants, where the result is always indicated in the first line of the resulting table (see Figure 5). The system then evaluated the other best permissible ETICS variants based on the requirement that the ETICS have the same or better thermal resistance, and thin plaster have the same or greater thickness.

The result for the ETICS type is clear in the first variant. Since all ETICS types have the same lifetime and repair frequency, the best type is also the cheapest solution (EPS 70 F), despite the fact that, e.g., the EPS graphite façade board has a higher thermal resistance (3.13 compared to 3.08 m2·K/W) while being thinner (100 mm compared to 120 mm). The differences between the best three variants of the ETICS are very small; the difference of the overall LCC is approx. 2 percentage points. The choice of thin plaster in the first variant is influenced only by the frequency of maintenance, where the silicate-silicone grooved plaster is the best option in the long term, where over the course of 100-year lifetime it will have to be washed with water 12 times and recoated 6 times. This is in contrast to the originally designed mineral plaster, which would have to be washed 22 times and recoated 10 times.

In the second variant, the input parameters and modified R/M/R database yielded the polystyrene socle façade board as the best ETICS type. This result was achieved even though the acquisition price including plaster is approx. 20% higher than the originally designed solution (Figure 5), and the thermal resistance is more than 10% higher. The lifetime of the originally designed solution was set to correspond to the examined period, i.e., 30 years, so it will have to be replaced once. By contrast, the most favourable polystyrene socle façade board has a set lifetime longer than the examined period and additionally, in contrast to other ETICS types, it has a lower set frequency of repairs as it needs to be repairs twice during the examined period. The originally designed solution would have to be repaired 5 times during the examined period.

In the third variant, where the R/M/R was identical to Variant 2, the best solution was EPS graphite façade board (100 mm thick). Considering; however, that the best solution in Variant 2 (polystyrene socle façade board) where the examined period was shorter, has almost the same resulting LCC price, despite the fact that the best solution in Variant 3 (EPS graphite façade board) will have to be replaced 3 times during the examined period, which is one replacement more than in the case of the best solution in Variant 2. The highest lifespan—60 years—was set for ETICS featuring mineral wool and foamglass. While this system would only have to be replaced once during the building lifetime, it ranked near the bottom in the comparison of the total LCC. This was because of the higher maintenance frequency of mineral fibre boards. Foamglass is also affected by its very high acquisition price.

It is clear from the overview of the results of the individual variants that the R/M/R database and the length of the examined period play a very important role. The examined period and the R/M/R database affect the results in such a way that it is impossible to determine which façade layer arrangement is generally the best, which is documented by the variable LCC efficiency of the individual construction-material solutions in the three modelled variant solutions.

5. Conclusions

This paper presented a methodology for building LCC estimation that enables investors to identify the optimum material solution for their buildings on the level of individual functional parts. From a theoretical perspective, this paper contributes to the current body of knowledge with the proposed LCC system, which takes into consideration various data inputs and interconnects the construction cost estimation database, facility management database and investors’ requirements into a comprehensive solution. Regarding managerial implications, the proposed LCC estimation system demonstrates the absence of a generally applicable optimum material solution for ETICS. Different investor requirements as well as the unique circumstances of each building and its user are a fact that underlines the need to apply comprehensive approaches to finding the best solutions. Differences between individual buildings lead to the fact that the results achieved (e.g., in the context of LCC calculations) will always be unique and, therefore, no ETICS or thin plaster type should be favoured in advance.

There are three important research limitations that should be mentioned. Firstly, the model’s division in terms of materials and structures depends on the available price database, where the proposed system presented in this paper is based on databases used in the Czech Republic. Building structures and materials not indicated in the relevant price database cannot be assigned with costs, which means no LCC value can be determined. Nevertheless, if the methodology is applied generally, it could be used—with adequate modifications—also in other regions and with different price databases. Secondly, the calculation is unique for each functional part, because it is based on its own cost estimation principles and the LCC calculation thus has to be modified for each individual functional part separately. Thirdly, this system is limited only to those life cycle costs that are related to the building’s structures and materials and omits future energy costs in the operational stage (heating, air conditioning, etc.).

Several future research directions can be outlined. It should be possible to follow up on the proposed system and the information necessary for LCA calculation in order to be able to select the best material and structural solution based on its carbon footprint as well, i.e., certainly in combination of LCC and LCA. This step would dramatically increase the potential for using the proposed system in the context of adhering to the principles of sustainable construction.

Another step could consist of incorporating utilities and energy consumption (e.g., heating, water and electricity) based on information obtained from already operated buildings and BIM model information. This would enable a more comprehensive evaluation of buildings in terms of their LCC. Finally, the information on the construction time (see Figure 5) has the potential for a broader use in creating construction time schedules or in identifying the optimum solution for a building that takes into account the construction time as one of the evaluation criteria (which can be significant in commercial development projects).

Author Contributions

Conceptualization, V.B. and T.H.; methodology, V.B. and T.H.; software, V.B.; calculation V.B. and T.H.; discussion V.B. and T.H.; resources, V.B. and T.H.; writing—original draft preparation, V.B. and T.H.; writing—review and editing, V.B. and T.H.; visualization, V.B.; supervision, T.H.; project administration, V.B.; funding acquisition, V.B.

Funding

This research was funded by Brno University of Technology, project Management of Enterprise and Investment Projects in Construction, grant number FAST-J-19-6052 and the APC was funded by FAST-J-19-6052.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Burcar Dunovic, I.; Radujkovic, M.; Vukomanovic, M. Internal and external risk based assessment and evaluation for the large infrastructure projects. J. Civ. Eng. Manag. 2016, 22, 673–682. [Google Scholar] [CrossRef]

- Korytarova, J.; Hromadka, V. Building life cycle economic impacts. In Proceedings of the International Conference on Management and Service Science, Wuhan, China, 24–26 October 2010. [Google Scholar]

- Zabielski, J.; Zabielska, I. Life Cycle of a Building (LCC) in the Investment Process-Case Study. In Proceedings of the Baltic Geodetic Congress, BGC-Geomatics, Olsztyn, Poland, 21–23 June 2018; pp. 254–259. [Google Scholar]

- Fantozzi, F.; Gargari, C.; Rovai, M.; Salvadori, G. Energy upgrading of residential building stock: Use of life cycle cost analysis to assess interventions on social housing in Italy. Sustainability 2019, 11, 1452. [Google Scholar] [CrossRef]

- Kovacic, I.; Zoller, V. Building life cycle optimization tools for early design phases. Energy 2015, 92, 409–419. [Google Scholar] [CrossRef]

- REEB Consortium. ICT Supported Energy ICT Supported Energy Efficiency in Construction. 2010. Available online: https://ec.europa.eu/information_society/activities/sustainable_growth/docs/sb_publications/reeb_ee_construction.pdf (accessed on 24 April 2019).

- Wen, Y.K.; Kang, Y.J. Minimum building life-cycle cost design criteria. II: Applications. J. Struct. Eng. 2001, 127, 338–346. [Google Scholar] [CrossRef]

- Stephan, A.; Stephan, L. Life cycle energy and cost analysis of embodied, operational and user-transport energy reduction measures for residential buildings. Appl. Energy 2016, 161, 445–464. [Google Scholar] [CrossRef]

- Lazzarin, R.M.; Busato, F.; Castelloti, F. Life cycle assessment and life cycle cost of buildings’ insulation materials in Italy. Int. J. Low Carbon Technol. 2008, 3, 44–58. [Google Scholar] [CrossRef]

- Han, G.; Srebric, J.; Enache-Pommer, E. Variability of optimal solutions for building components based on comprehensive life cycle cost analysis. Energy Build. 2014, 79, 223–231. [Google Scholar] [CrossRef]

- Anuradha, I.G.N.; Perera, B.A.K.S.; Mallawarachchi, H. Embodied carbon and cost analysis to identify the most appropriate wall materials for buildings: Whole life cycle approach. In Proceedings of the MERCon 2018 4th International Multidisciplinary Moratuwa Engineering Research Conference, Moratuwa, Sri Lanka, 30 May–1 June 2018; pp. 43–48. [Google Scholar]

- Juan, Y.; Hsing, N. BIM-based approach to simulate building adaptive performance and life cycle costs for an open building design. Appl. Sci. 2017, 7, 837. [Google Scholar] [CrossRef]

- Robati, M.; McCarthy, T.J.; Kokogiannakis, G. Integrated life cycle cost method for sustainable structural design by focusing on a benchmark office building in Australia. Energy Build. 2018, 166, 525–537. [Google Scholar] [CrossRef] [Green Version]

- Salvado, F.; Almeida, N.M.; Vale e Azevedo, A. Toward improved LCC-informed decisions in building management. Built Environ. Proj. Asset Manag. 2018, 8, 114–133. [Google Scholar] [CrossRef]

- Che-Ghani, N.Z.; Myeda, N.E.; Ali, A.S. Operations and maintenance cost for stratified buildings: A critical review. Proc. MATEC Web Conf. 2016, 66, 41. [Google Scholar] [CrossRef]

- Mong, S.G.; Mohamed, S.F.; Misnan, M.S. Key strategies to overcome cost overruns issues in building maintenance management. Int. J. Eng. Technol. 2018, 7, 269–273. [Google Scholar] [CrossRef]

- Haugbølle, K.; Raffnsøe, L.M. Rethinking life cycle cost drivers for sustainable office buildings in Denmark. Facilities 2019. [Google Scholar] [CrossRef]

- Farahani, A.; Wallbaum, H.; Dalenbäck, J. Optimized maintenance and renovation scheduling in multifamily buildings—A systematic approach based on condition state and life cycle cost of building components. Constr. Manag. Econ. 2019, 37, 139–155. [Google Scholar] [CrossRef]

- Buyle, M.; Audenaert, A.; Braet, J.; Debacker, W. Towards a more sustainable building stock: Optimizing a flemish dwelling using a life cycle approach. Buildings 2015, 5, 424–448. [Google Scholar] [CrossRef]

- Liu, L.; Rohdin, P.; Moshfegh, B. LCC assessments and environmental impacts on the energy renovation of a multi-family building from the 1890s. Energy Build. 2016, 133, 823–833. [Google Scholar] [CrossRef]

- Silvestre, J.D.; Castelo, A.M.P.; Silva, J.J.B.C.; Brito, J.M.C.L.; Pinheiro, M.D. Retrofitting a building’s envelope: Sustainability performance of ETICS with ICB or EPS. Appl. Sci. 2019, 9, 1285. [Google Scholar] [CrossRef]

- Bottinelli, A.; Louf, R.; Gherardi, M. Balancing building and maintenance costs in growing transport networks. Phys. Rev. E 2017, 96, 032316. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Milić, V.; Ekelöw, K.; Moshfegh, B. On the performance of LCC optimization software OPERA-MILP by comparison with building energy simulation software IDA ICE. Build. Environ. 2018, 128, 305–319. [Google Scholar] [CrossRef]

- Konstantinidou, C.A.; Lang, W.; Papadopoulos, A.M.; Santamouris, M. Life cycle and life cycle cost implications of integrated phase change materials in office buildings. Int. J. Energy Res. 2019, 43, 150–166. [Google Scholar] [CrossRef]

- Bandara, R.M.P.S.; Fernando, W.C.D.K.; Attalage, R.A. Optimizing life cycle cost of buildings through simulation-based optimization: A case study. In Proceedings of the Annual International Conference on Architecture and Civil Engineering, Singapore, 14–15 May 2018; pp. 363–370. [Google Scholar]

- Kim, J.; Kim, T.; Yu, Y.; Son, K. Development of a maintenance and repair cost estimation model for educational buildings using regression analysis. J. Asian Archit. Build. Eng. 2018, 17, 307–312. [Google Scholar] [CrossRef]

- Au-Yong, C.P.; Ali, A.S.; Ahmad, F. Enhancing building maintenance cost performance with proper management of spare parts. J. Qual. Maint. Eng. 2016, 22, 51–61. [Google Scholar] [CrossRef]

- Balasbaneh, A.T.; Bin Marsono, A.K.; Gohari, A. Sustainable materials selection based on flood damage assessment for a building using LCA and LCC. J. Clean. Prod. 2019, 222, 844–855. [Google Scholar] [CrossRef]

- Cheng, M.; Wei, H.; Wu, Y.; Chen, H.; Wu, C. Optimization of life-cycle cost of retrofitting school buildings under seismic risk using evolutionary support vector machine. Technol. Econ. Dev. Econ. 2018, 24, 812–824. [Google Scholar] [CrossRef]

- Zeleňáková, M.; Gaňová, L.; Purcz, P.; Horský, M.; Satrapa, L. Determination of the potential economic flood damages in Medzev, Slovakia. J. Flood Risk Manag. 2018, 11, S1090–S1099. [Google Scholar] [CrossRef]

- Blengini, G.A.; Di Carlo, T. The changing role of life cycle phases, subsystems and materials in the LCA of low energy buildings. Energy Build. 2009, 42, 869–880. [Google Scholar] [CrossRef]

- Brown, M.T.; Buranakarn, V. Emergy indices and ratios for sustainable material cycles and recycle options. Resour. Conserv. Recycl. 2003, 38, 1–22. [Google Scholar] [CrossRef]

- Fregonara, E.; Giordano, R.; Ferrando, D.G.; Pattono, S. Economic-environmental indicators to support investment decisions: A focus on the buildings’ end-of-life stage. Buildings 2017, 7, 65. [Google Scholar] [CrossRef]

- European Union. Directive 2014/24/EU of the European Parliament and of the Council of 26 February 2014 on Public Procurement and Repealing Directive 2004/18/EC; European Union: Brussels, Belgium, 2014. [Google Scholar]

- Santos, R.; Costa, A.A.; Silvestre, J.D.; Pyl, L. Integration of LCA and LCC analysis within a BIM-based environment. Autom. Constr. 2019, 103, 127–149. [Google Scholar] [CrossRef]

- Saridaki, M.; Psarra, M.; Haugbølle, K. Implementing life-cycle costing: Data integration between design models and cost calculations. J. Inf. Technol. Constr. 2019, 24, 14–32. [Google Scholar]

- Spagnolo, S.L. Information integration for asset and maintenance management. In Integrating Information in Build Environments: From Concept to Practice; Sanchez, X.A., Hampson, D.K., London, G., Eds.; Routledge: London, UK, 2018; pp. 133–149. [Google Scholar]

- ISO. Buildings and Constructed Assets-Service Life Planning; ISO 15686-5:2017; ISO: Geneva, Switzerland, 2017. [Google Scholar]

- Bromilow, F.J.; Pawsey, M.R. Life cycle cost of university buildings. Constr. Manag. Econ. 1987, 5, S3–S22. [Google Scholar] [CrossRef]

- Sobanjo, J.O. Facility Life-Cycle Cost Analysis on Fuzzy Sets Theory. Durability of Building Materials and Components 8; Institute for Research in Construction: Ottawa, ON, Canada, 1999. [Google Scholar]

- Kupilík, V. Závady a Životnost Staveb (Defects and Lifetime of Buildings); Grada: Praha, Czech Republic, 1999; p. 288. [Google Scholar]

- Korytárová, J.; Papežíková, P. Assessment of Large-Scale Projects Based on CBA. Procedia Comput. Sci. 2015, 64, 736–743. [Google Scholar] [CrossRef] [Green Version]

- Marková, L. Náklady Životního Cyklu Stavby: Náklady Investora, Celospolečenské Dopady (Building Life Cycle Costs: Investor Costs, Societal Implications); Akademické nakladatelství CERM: Brno, Czech Republic, 2011; p. 125. [Google Scholar]

- Biolek, V.; Hanak, T.; Marovic, I. Data flow in Relation to Life-Cycle Costing of Construction Projects in the Czech Republic. IOP Conf. Ser. Mater. Sci. Eng. 2017, 245, 072032. [Google Scholar] [CrossRef]

- Biolek, V.; Domansky, V.; Vyskala, M. Interconnection of construction-economic systems with BIM in the Czech environment. IOP Conf. Ser. Earth Environ. Sci. 2019, 222, 012022. [Google Scholar] [CrossRef]

- ÚRS. Katalog Stavebních Konstrukcí a Prací ÚRS, Cenová Úroveň 2019/1 (ÚRS Catalogue of Building Structures and Works; Price Level as of 2019/1); URS: San Francisco, CA, USA, 2019. [Google Scholar]

- Isover Saint-Gobaint. Katalog výrobků Isover (Isover Product Catalogue); Isover Saint-Gobaint: Ludwigshafen, Germany, 2019. [Google Scholar]

- Bachl. Fyzikální Vlastnosti Extrudovaného Polystyrenu XPS (Physical Properties of XPS Extruded Polystyrene); Karl Bachl GmbH & Co. KG: Röhrnbach, Germany, 2015. [Google Scholar]

- Foamglas. Technický List FOAMGLAS® W+F (FOAMGLAS® W+F Technical Sheet); Foamglas, Institut Bauen und Umwelt e.V.: Berlin, Germany, 2008. [Google Scholar]

- STEICO. Technický list STEICOFlex 036 (STEICOFlex 036 Technical Sheet); STEICO: Feldkirchen, Germany; Berlin, Germany, 2016. [Google Scholar]

Figure 1.

The process of exchanging information among the individual systems to ensure the best material solution of the building.

Figure 1.

The process of exchanging information among the individual systems to ensure the best material solution of the building.

Figure 2.

Overview of input parameters for calculating LCC for the individual variants.

Figure 3.

R/M/R database for the LCC calculation of the individual variants (ETICS).

Figure 4.

R/M/R database for the LCC calculation of the individual variants (thin plaster).

Figure 5.

Output of the LCC calculation for Variant 1.

Figure 6.

Output of the LCC calculation for Variant 2.

Figure 7.

Output of the LCC calculation for Variant 3.

Figure 8.

A showcase of information output transferrable to the BIM model.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Proposed connecting database with division to functional units and functional parts [45].

Table 1.

Proposed connecting database with division to functional units and functional parts [45].

| Functional unit | LOAD-BEARING STRUCTURES | ROOF STRUCTURES | FAÇADE | SURFACE TREATMENT OF INTERIOR SPACES |

| Functional part | foundations walls columns ceilings girders, (main) beams staircase load-bearing part of chimney | wooden roof frame roof covering metal sheeting of roof elements other roof elements—roof windows, skylights, antennas etc. | windows entrance door, gate façade composition exterior window sills other façade elements—covers, railing, blinds, etc. | wall plastering facings ceiling plastering suspended ceilings floor |

Table 2.

The list of individual types of ETICS with their possible thickness values, thermal conductivity coefficient and indication of special properties (none = no special properties; SO = meant for the socle area; PO = fire resistant) [46,47,48,49,50].

| Type of ETICS and Reference Products | Thickness [mm] | Thermal Conductivity Coefficient λ [W/(m·K)] | Property |

|---|---|---|---|

| EPS 70 façade board (Isover EPS 70F) | 10; 20; 30; 40; 50; 60; 80; 100; 120; 140; 150; 160; 180; 200 | 0.039 | none |

| EPS 100 façade board (Isover EPS 100F) | 30; 50; 60; 80; 100; 120; 140; 160; 180; 200 | 0.037 | none |

| EPS graphite façade board (Isover EPS GreyWall) | 20; 30; 40; 50; 60; 80; 100; 120; 140; 160; 180; 200; 220; 240; 260; 280; 300 | 0.032 | none |

| polystyrene socle board, façade (Isover EPS SOKL 3000) | 20; 30; 40; 50; 60; 80; 100; 120 | 0.035 | SO |

| polystyrene façade board for thermal insulation of bottom parts of buildings (Isover EPS PERIMETR) | 40; 50; 60; 80; 100; 120; 140 | 0.034 | SO |

| board with longitudinal mineral fibre (Isover TF PROFI) | 40; 50; 60; 70; 80; 100; 120; 140; 160; 180; 200; 220; 240; 260; 280; 300 | 0.036 | PO |

| board with perpendicular mineral fibre (Isover NF 333) | 20; 30; 40; 50; 60; 70; 80; 100; 120; 140; 160; 180; 200; 220; 240; 260; 280; 300 | 0.041 | PO |

| foamglass board, no surface treatment (FOAMGLAS®W+F) | 50; 60; 80; 100; 120; 140 | 0.038 | PO |

| XPS polystyrene board (BACHL XPS 300 G) | 30; 40; 50; 60; 80; 100; 120 | 0.036 (up to 60 mm) 0.033 (over 60 mm) | SO |

| sandwich insulation board (polystyrene+wool) (Isover TWINNER) | 100; 120; 140; 150; 160; 180; 200; 220; 240; 260; 280; 300 | 0.033 (up to 200 mm) 0.032 (over 200 mm) | PO |

| wood fibre board (STEICO Flex-wood fibre insulation) | 40; 60; 80; 100; 120; 140; 160; 180; 200 | 0.036 | none |

Table 3.

List of thin plasters with potential thickness [46].

Table 3.

List of thin plasters with potential thickness [46].

| Type of Thin Plaster | Thickness [mm] |

|---|---|

| mineral granular plaster | 1.0; 1.5; 2.0 |

| mineral grooved plaster | 2.0 |

| acrylic granular plaster | 1.0; 1.5; 2.0 |

| acrylic grooved plaster | 2.0; 3.0 |

| acrylic mosaic plaster | 1.0; 2.0; 3.0 |

| silicate granular plaster | 1.0; 1.5; 2.0; 3.0 |

| silicate grooved plaster | 2.0 |

| silicone granular plaster | 1.0; 1.5; 2.0; 3.0 |

| silicone grooved plaster | 2.0; 3.0 |

| silicone hydrophilic granular plaster | 1.0; 1.5; 2.0; 3.0 |

| silicone hydrophilic grooved plaster | 2.0; 3.0 |

| silicate-silicone granular plaster | 1.0; 1.5; 2.0; 3.0 |

| silicate-silicone grooved plaster | 2.0 |

Table 4.

Coating types associated with the individual plaster types (texture not taken into consideration).

Table 4.

Coating types associated with the individual plaster types (texture not taken into consideration).

| Type of Thin Plaster | Type of Coating |

|---|---|

| mineral plaster | lime |

| acrylic plaster | acrylic |

| silicate plaster | silicate |

| silicone and silicate-silicone plaster | silicone |

Table 5.

Division of ETICS repairs according to price database [46].

Table 5.

Division of ETICS repairs according to price database [46].

| Polystyrene Thickness | Mineral Wool Thickness | Scope of Repair for Polystyrene and Mineral Wool |

|---|---|---|

| under 40 mm | under 40 mm | under 0.1 m2 |

| 40 mm to 80 mm | 40 mm to 80 mm | 0.1 to 0.25 m2 |

| 80 mm to 120 mm | 80 mm to 120 mm | 0.25 to 0.5 m2 |

| 120 mm to 160 mm | 120 mm to 160 mm | 0.5 to 1.0 m2 |

| 160 mm to 200 mm | over 160 mm | - |

| 200 mm to 240 mm | - | - |

| over 240 mm | - | - |

Table 6.

Division of repairs of thin plaster and types of plaster.

| Repair Scope by Area | Repair Scope as a Percentage |

|---|---|

| under 0.1 m2 | under 10% |

| 0.1 to 0.25 m2 | 10 to 30% |

| 0.25 to 0.5 m2 | 30 to 50% |

| 0.5 to 1.0 m2 | - |

| 1.0 to 4.0 m2 | - |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Biolek, V.; Hanák, T. LCC Estimation Model: A Construction Material Perspective. Buildings 2019, 9, 182. https://0-doi-org.brum.beds.ac.uk/10.3390/buildings9080182

AMA Style

Biolek V, Hanák T. LCC Estimation Model: A Construction Material Perspective. Buildings. 2019; 9(8):182. https://0-doi-org.brum.beds.ac.uk/10.3390/buildings9080182

Chicago/Turabian StyleBiolek, Vojtěch, and Tomáš Hanák. 2019. "LCC Estimation Model: A Construction Material Perspective" Buildings 9, no. 8: 182. https://0-doi-org.brum.beds.ac.uk/10.3390/buildings9080182

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.