The Misunderstanding of Social Insurance: The Inadequacy of the Basic Pension Insurance for Urban Employees (BPIUE) for the Aging Population of China

School of Public Policy and Management, University of Chinese Academy of Science, Beijing 100049, China

Soc. Sci. 2018, 7(5), 79; https://0-doi-org.brum.beds.ac.uk/10.3390/socsci7050079

Submission received: 24 February 2018

/

Revised: 24 April 2018

/

Accepted: 5 May 2018

/

Published: 13 May 2018

Abstract

:The Chinese public has shown increasing concern about the “inadequacy” of the funds available for the Basic Pension Insurance for Urban Employees (BPIUE). The government has managed the issue by balancing the program’s revenue and expenditures each year and by increasing subsidies for it from all levels. These actions have raised a number of questions, such as why the program still needs financial subsidies as the fund’s balance continues to increase. The BPIUE was initiated in 1991, and the combination model of “social pooling” and “individual accounts of employees” was established in 1995 and formally launched in 1998. Also, in 1998, reforms including the downsizing of state-owned enterprises were implemented, and tens of millions of employees of state-owned enterprises entered early retirement. Local governments used funds from the individual accounts to pay pensions to employees based on length of service, and as a result, the individual accounts have remained empty ever since. Based on the definition of social insurance and an empirical analysis of the BPIUE fund, this paper conducts a qualitative and quantitative analysis of the plan from two perspectives, striving to provide an objective explanation and assessment of the pension fund’s inadequacy. On this basis, the paper analyzes the impact of the aging population of China on the existing and future BPIUE fund gap.

1. Background and Issues

China is an aging society, and according to the National Bureau of Statistics, the working population decreased by 3.45 million in 20121. According to the UN (Population Division, DESA, United Nations 2001), China’s aging process began in 1995–2000, when the ratio of the population aged 65 and over began to exceed 7%. According to the 2010 World Population Project2, China’s aging crisis will peak in 2025–2030 when the ratio exceeds 14% and the Old Age Dependency Ratio reaches 20%, meaning that every five people in the labor force will support one person in old age. The 2010 World Population Project also states that China will join with other western countries such as Germany, Japan, and the UK to become a “super aging society”, meaning that those countries’ old age population will exceed 20% of their whole population. If we remove students of working age, unemployed young people, low-revenue employees, and retirees of working age from China’s labor force composition, the country already became a “deep aging society” in 2010 (Hu and Yang 2012). In theory, before a country becomes an aging society, it should end its pay-as-you-go pension system and build a dual pension system with a combination of a national basic pension and an individual savings pension.

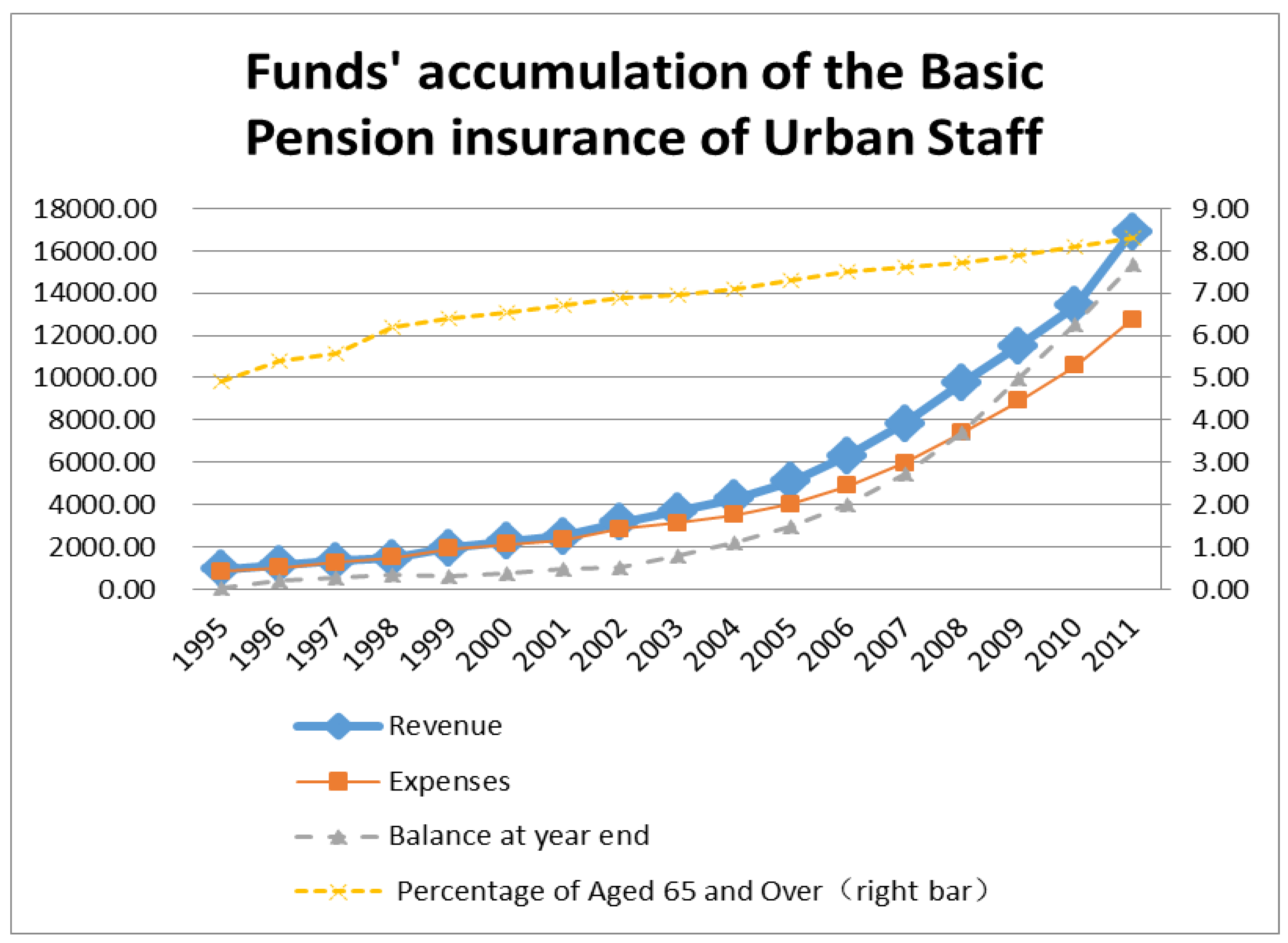

The current Basic Pension Insurance for Urban Employees (BPIUE) was initiated in 1991 and implemented nationwide in 1997 in accordance with the Decision on establishing a unified basic pension insurance system for enterprise employees by the State Council. The system required enterprises to contribute 20% of total wages to a social pooling account, and for employees, 8% of total wages were to be deposited into individual accounts. At the time, China was becoming an aging society. Between 2001 and 2011, the proportion of the population aged 65 years and over increased from 6.7% to 8.3%, and the internal alimony ratio of the BPIUE was only 3:1 (three contributing employees for one recipient). During the same time period, however, the annual cumulative balance of the pension fund rose from 9.8 billion yuan in 2001 to 1.5365 trillion yuan by the end of 2011 (Figure 1)3. Meanwhile, the financial subsidies from central and local governments increased from 40.8 trillion yuan in 2002 to 227.2 trillion yuan in 20114; as a result, funds in the individual accounts of employees were misappropriated to pay for others’ pensions, and by the end of 2011, the cumulative amount owed to the now empty accounts was more than 2 trillion yuan (Zheng 2013, p. 2). The system no longer breaks even.

In this context, the following questions are raised:

- Is the BPIUE a social insurance model? What is the nature of the individual pension savings accounts of employees?

- During the course of China’s aging, how could the BPIUE funds continue to achieve an ever-increasing cumulative balance? Why does the plan still need government subsidies despite the ever-increasing cumulative balance? Where do the government subsidies go?

- What is the impact of the China’s aging on the BPIUE, and can the BPIUE achieve sustainable development in China?

Beginning with these three questions and based on China’s social background, this paper reveals the policy mistakes of the BPIUE and the reasons for the fund balances, and then it explores the issue of sustainability for China’s pension system.

2. Theoretical Analysis: The Revenue-Expenditure Balance is the Essential Attribute of Pension Insurance

Insurance is risk savings plus a compensation contract, and it must maintain its own revenue-expenditure balance. In general, no individual or institution can guarantee insurance. Social insurance is different from social welfare (sometimes in the form of social assistance), and it should emphasize individual intergenerational transfers, not income re-distribution between groups orchestrated by the government using financial payments (Feldstein 1999). Since Bismarck founded the insurance model in 1883 (Kolmar 2007), social insurance has required employers to fulfill their obligation of contributions; employee contributions were later added. Contribution amounts from employees may be associated with their salaries; however, Germany has not yet established individual savings accounts for contributing employees. Social insurance plans emphasize contributions from both employers and employees, and contribution amounts are matched with the employee’s salary (Feldstein 2005). The biggest difference between social insurance and social welfare is that social welfare represents “civil rights”, while social insurance represents “event rights” (Feldstein 2005). Therefore, the UK’s first State Basic Pension Law requires a minimum of 45 years’ contribution to National Insurance to receive a full pension payment (the requirement for the number of contributing years is reduced for women in lieu of a family responsibility protection clause) (Blake 2003). Under the UK’s 2012 Universal Credit, those with sufficient contributions to social insurance can directly apply for unemployment insurance and family benefits and receive payments for a longer period; those who have not fulfilled their social insurance payment obligations must be means-tested by the government and are subject to numerous restrictions regarding the amount of benefits and the eligibility period. This dichotomy shows that the UK’s social safety net adheres to basic social insurance-based principles, and social welfare and social assistance are secondary5.

A successful social insurance scheme focuses on financial sustainability and requires certain actuarial calculations. It differs from commercial insurance by its compulsory nature and the financial support it receives from the government (Kolmar 2007), making the results of social insurance similar to a redistribution of wealth. However, the government’s financial investment is a limited liability to ensure the functioning of social insurance rather than the acceptance of full responsibility for the entire scheme. Otherwise, the government would face extreme political and financial pressure that would ultimately result in an unsustainable social insurance scheme (Casamatta et al. 2000; Angrisani et al. 2012).

Initially, pensions entered the market as commercial insurance and as a disguised tool for personal and family savings (Dokeland and Nordahl 2008). Pension systems distributed profits and market risks between customers and shareholders of a commercial insurance company on an actuarial basis while taking into consideration contribution amounts, asset allocation, benefit commitments, and profit sharing (Dokeland and Nordahl 2008, p. 383). Social pension insurance that developed with reference to commercial insurance emphasizes mutual social assistance, risk sharing and other factors, and unlike commercial insurance, it is impossible for a social pension insurance system to solely emphasize contributions and benefit payments (Sinn 2004; Williamson and Deitelbaum 2005; Feldstein 1999). Therefore, from the beginning of the establishment of social insurance systems, governments of various countries have chosen combination models that include pay-as-you-go (PAYG) and defined contributions. PAYG does not emphasize asset accumulation, and the system directly pays the current retired population with the current employees and employers’ contributions as payment transfer tools. As a separate fund, PAYG differs from the government transfer payment system that uses tax revenue (Feldstein 1999).

Some analysts believe that social insurance can avoid the adverse selection, moral hazard, exclusion of low-income groups, and reduction of free-rider effects of commercial insurance (Angrisani et al. 2012). Social insurance is most beneficial to the unemployed, low-income population and to the elderly who have no children to support them. As a result, social insurance plays a major role in the basic protection of an entire society based on shared risk and collective provisions and by favoring low-wage workers. For families who are unable or unwilling to have children due to family or other reasons, PAYG can offer the support that is provided by children in other families and offer some benefit from an investment in the human capital of the next generation. Therefore, PAYG is equivalent to maternity insurance (Williamson and Deitelbaum 2005). Feldstein (1999) believes that adopting PAYG reflects political needs, that is, the government gets extra-budgetary windfall to reduce its financial burden, and the cost of the system is repaid with tax revenue from future generations. As a result, the government is constantly expanding coverage to maintain public support for the system (Feldstein 1999 p. 10), which has become the government’s preferred choice for the establishment of social security.

However, there have been doubts raised about PAYG since its establishment. From the perspective of Samuelson economics, the premise for the sustainable development of a PAYG pension system is high population growth and a high growth rate of social productivity (Samuelson 1958). Since the late 20th century, the PAYG system has faced the challenge of an aging population in countries all over the world and particularly in industrialized countries, where the total fertility rate is low and life expectancy continues to rise (Cremer and Pestieau 2000; Sanz and Velázquez 2007; Williamson et al. 2012).

Since the 1980s–1990s, many countries have begun to adjust their PAYG systems. On one hand, PAYG and defined benefits (DB) are used as basic pensions to maintain low standards of living (Williamson et al. 2012). On the other hand, countries have introduced mandatory individual savings accounts (DC model) as the second pillar of pensions (Pillar II). In the 1980s, Chile changed its DB model of PAYG to the DC model with cumulative individual balances (Calvo and Williamson 2008). In the 1990s, Australia adopted the same measures. With prodding from the World Bank and other international organizations, developed countries with advanced-aging populations and developing countries that had just become aging societies have strengthened their individual savings account systems; as a result, the dual pension system structure has been implemented all over the world. The PAYG principle is preserved in the first pillar mostly through welfare and security (such as elderly, widow, and disability security payments in the US) and social assistance (such as Australia’s assistance payment), while fewer and fewer systems adhere to the German Bismarck social insurance model. The second pillar is individual savings. As noted by Peter F. Drucker (1999, p. 94), unanticipated situations include reduced coverage and decreased social insurance payments.

Individual savings accounts are personal property, and individual pension fund accounts have a greater need for specialized, market-oriented management and operations that preserve and increase the value of the accounts in the capital market (Dokeland and Nordahl 2008). The government’s role is only to establish policy and adjust the rules on taxation and the related laws and regulations, and commercial institutions or social organizations administer the specific account management, fund management, and benefit payment activities. Some scholars regard this practice as personalization (Williamson and Deitelbaum 2005) or marketization (Fanti and Gori 2012), while others regard it as a public-private partnership or public governance by the government and commercial institutions (Dong and Ye 2003).

In summary, the above theoretical analysis shows that the model and qualification determination for social insurance are different from social welfare, and social security is not merely a system of payment transfer with an emphasis on contributions, as is especially the case for pension insurance. Social security has a greater emphasis on long-term liability operations and the sustainability of sufficient contributions and other sources of funds for adequate cumulative balances. Social welfare programs do not need to consider the amount of revenue and expenditures, which are fully taken care of by the financial budget, whereas social pension insurance systems must strictly consider the sources of revenue and contributions and pursue a long-term balance of revenue and expenditures. Social insurance systems cannot shoulder high long-term levels of debt or become too large of a financial burden for the government. Meanwhile, within the PAYG pension system, the difference between pooling accounts and individual accounts with individual contributions also needs to be clarified. The PAYG system creates a public account and forms a quasi-public good; individual accounts emphasize individual contribution records and fund accumulation, and they create increased value through financial and capital markets, which reduces the need for mutual and intergenerational social support and strengthens the connection between individual responsibility and rights.

Therefore, social insurance and welfare should be divorced from PAYG and individual accounts, and although sometimes they can be integrated (e.g., in the welfare system of the UK and other European countries, social insurance contributions are a criterion for higher benefit payments, but those with no contributions can also be means-tested and receive some benefit if eligible), their boundaries should be maintained; otherwise, there will be a mismatch between responsibilities and rights, resulting in free-riding, fewer sources of funds, and difficulties in sustaining the system.

3. BPIUE Demonstrates the Transformation from Working Unit Security to Social Security

BPIUE demonstrates the transformation from working unit security to social security for the pensions of employees of Chinese enterprises. Since 1951, China’s rural areas have used the people’s commune system, and the basic livelihood of rural residents is protected by social mutual assistance (Williamson and Deitelbaum 2005). Labor insurance implemented in cities and towns is based on a model of “contribution [3% of total wages] from working units supplemented by social mutual assistance”, upon which Williamson, Dong, Feldstein, Hussain, et al. have conducted a thorough and detailed analysis (Hussain 1994; Feldstein 1999; Dong and Ye 2003; Williamson and Deitelbaum 2005; Hu and Yang 2012). During the Cultural Revolution from 1967–1976, social mutual assistance ceased to exist, pension insurance was entirely borne by working units, and pension payments were more than 80% of wages. Moreover, children could take their parents’ place and a permanent job (iron rice bowl) could be passed to the next generation. State-owned enterprises, the public sector, and government agencies implemented the same system so there was no two-tier pension system for workers at the time. However, the old industrial enterprises and state-owned enterprises bore a heavy burden of the welfare system (Hussain 1994).

In 1985, China’s state-owned enterprises implemented the labor contract system, breaking the “iron rice bowl” system of lifetime employment, and urban workers began to consider social risks such as employment, unemployment, illness, and family difficulties (Hussain 1994; Williamson and Deitelbaum 2005). In 1991, the State Council proposed the idea of social pension insurance for employees6, which ended the history of work unit insurance and adopted the social pooling and PAYG model. In 1995, the State Council stressed that based on the PAYG model and considering the aging of the population, workers’ individual savings accounts should be established, and enterprise contributions of 3% of wages should be deposited into workers’ individual accounts7. The funds in individual accounts could not be withdrawn before retirement unless the workers had settled abroad or died.

However, it has been difficult to decentralize the decision-making on how to operate the two accounts to local governments to shift the pooling responsibility. The migration of insured workers and the transfer of social insurance to other municipal governments have been difficult to manage. It was not until 1997 that the State Council required the establishment of a social pension insurance system that “combined social pooling and individual accounts” (in other words, a combination of DB and DC) for urban employees nationwide8, and according to Premier Zhu Rongji, this system was the matching measure for the reform of state-owned enterprises. During the reform of state-owned enterprises during 1997 and 1998, more than 20 million workers were laid off9, and because most of them had retired early, the average retirement age was only 4710. Prior to being laid off, the workers did not have any pension accumulation, and because of the lack of applicable laws and regulations and appropriate budgetary arrangements by the central government, local governments had to misappropriate funds in employees’ savings accounts to pay for the pensions of these “middle-aged” workers who had retired early, which began the problem of the empty individual accounts. However, even with the misappropriations, the funds were not sufficient to meet the demand for pension payments, so in the same year the central government transferred payments to local governments of approximately 10 billion yuan.

The 2005 State Council document11 directed that all of the employee contributions of 3% of wages should be deposited into social pooling accounts, and from that moment, enterprises no longer contributed to employees’ individual pension accounts. Retired workers became the responsibility of community management, and social insurance institutions were responsible for pension payments, which were issued by a bank. The traditional work unit security was transformed into social security under social management.

4. BPIUE Has Been Distorted Since 1998

4.1. Funds in Individual Accounts Were Misappropriated to Pay for Workers of State-Owned Enterprises with Early Retirement

The 1997 Urban Employees’ Pension reform was the most important one in China’s pension history. Two systems and accounts were established after the reform. The employers pay the social pooling account which is a Pay-as-you-go system and the employees pay their individual accounts as individual savings. And the unemployed and rural area people were taken out of this system to establish another pension system which is semi means-tested and semi tax financed. This paper focuses on the urban employees’ pension system.

The original intention of the 1997 reforms was to establish a model that combined SP (Social pooling) and IA (Individual Accounts), which are DB and DC (Hu and Yang 2012). It not only preserved the basic protections, transfer payments, and risk sharing of the PAYG system but also established individual savings accounts to respond to the impact of an aging population. However, the aforementioned State Council document was not ratified as law and only took effect as an administrative law in China. So far, there is still no judicial system for employees’ individual pension accounts, and there are no investment strategies or pension markets. Accounts and funds are managed by social insurance agencies of the local governments, and there are no unified national resident files. Municipal governments have set up pension insurance agencies that manage both social pooling funds and funds in individual accounts, and the balance after pension payments is turned over to the fiscal accounts of the government for the purchase of government savings bonds.

To analyze the accumulation rate at year end of the BPIUE, assuming that represents the annual fund revenue, represents the annual fund expenditures, represents the annual fund balance at year end, and , then the annual fund’s balance rate is:

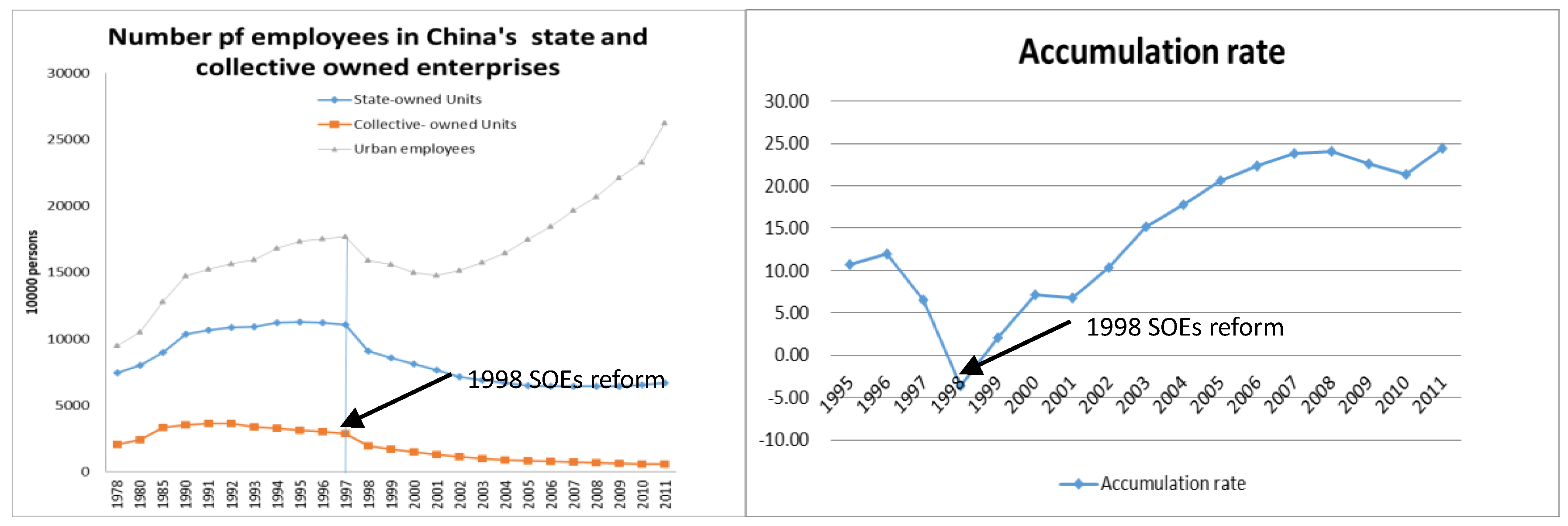

From 1996–1998, the reform of state-owned enterprises was implemented in China, and by the end of 1998, more than 20 million workers were laid off and most of them retired early, at an average age of only 47. These workers did not have any pension accumulation, but the length of their service in the state-owned enterprises was recognized by the policy of the State Council (deemed-as contributions). However, there was no budget for pension payments, so the local governments had to misappropriate funds from individual accounts. In addition, there was no legal impediment to this action because the SP and IA accounts had been mixed. From 1995–1998, the accumulation rate of the BPIUE continued to decline (Figure 2) and began to increase since 1998 to now12.

4.2. Unbalanced Regional Burden and Pension Fund Balances

For the BPIUE, the social pooling account is managed by municipal governments, and 10% is controlled by provincial governments as adjustment funds. When workers migrate to different areas, they often encounter resistance from the local government in carrying over the pension insurance relationship. Local governments are required to maintain their own balances of revenue and expenditures, and the State Council has compromised to allow local governments to retain 8% out of the 20% enterprise contribution, while the worker must carry the remaining 12% (Dong and Ye 2003).

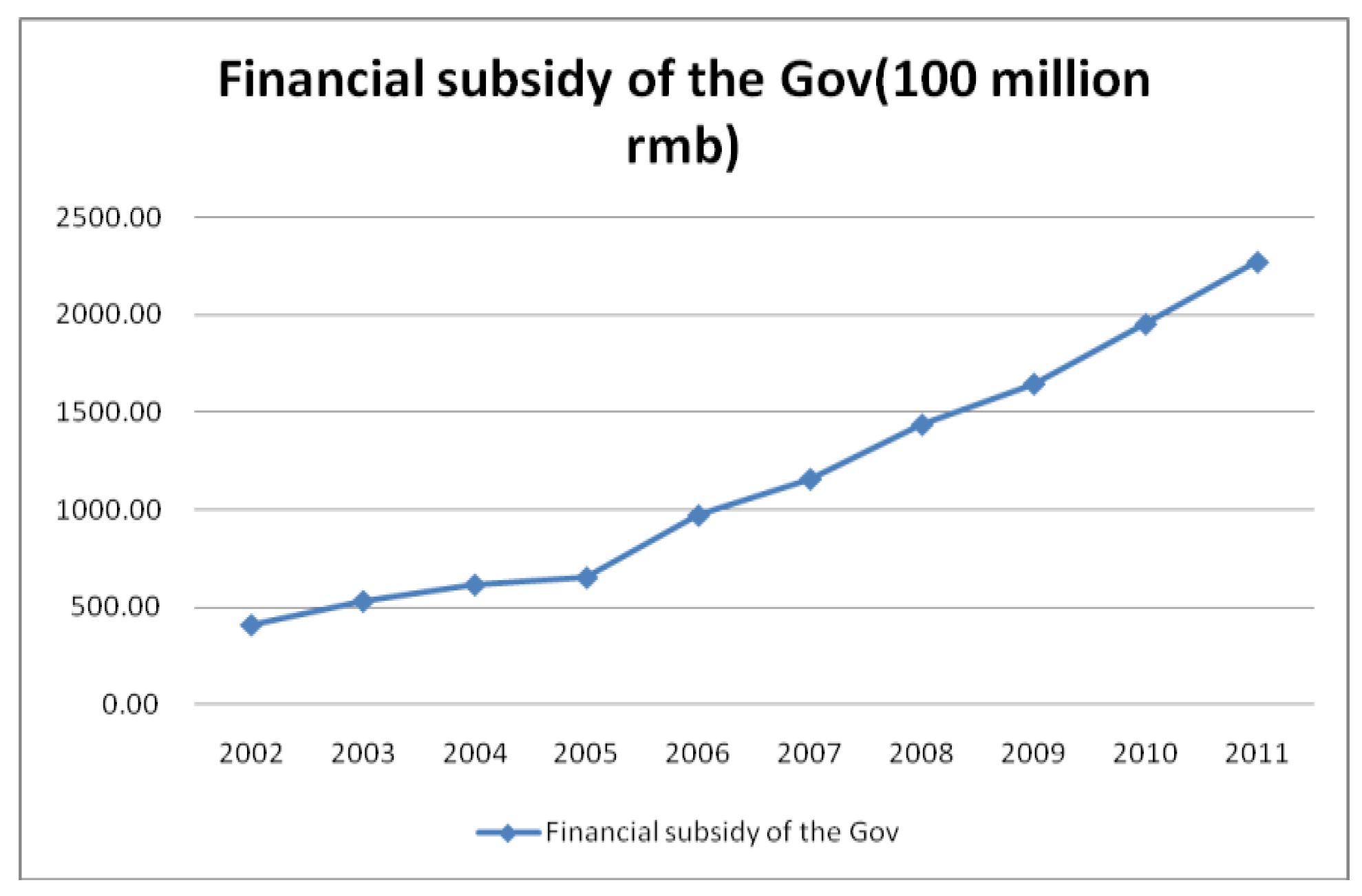

Meanwhile, in the old industrial bases of northeast and northwest China, there are a large number of laid-off workers and workers in early retirement after the implementation of the reforms of the state-owned enterprises, and the amount of the pension payments is huge; so far, there are 14 provinces that have exhausted the 20% enterprise contributions and the 8% employee contributions, yet they still cannot meet the demand to pay the pensions of the retired workers. As a result, payment transfers from the central government to local governments have continued to increase, and government financial subsidies have increased to 220 billion yuan in 2012 from 40 billion yuan in 2001 which is shown in Figure 3.

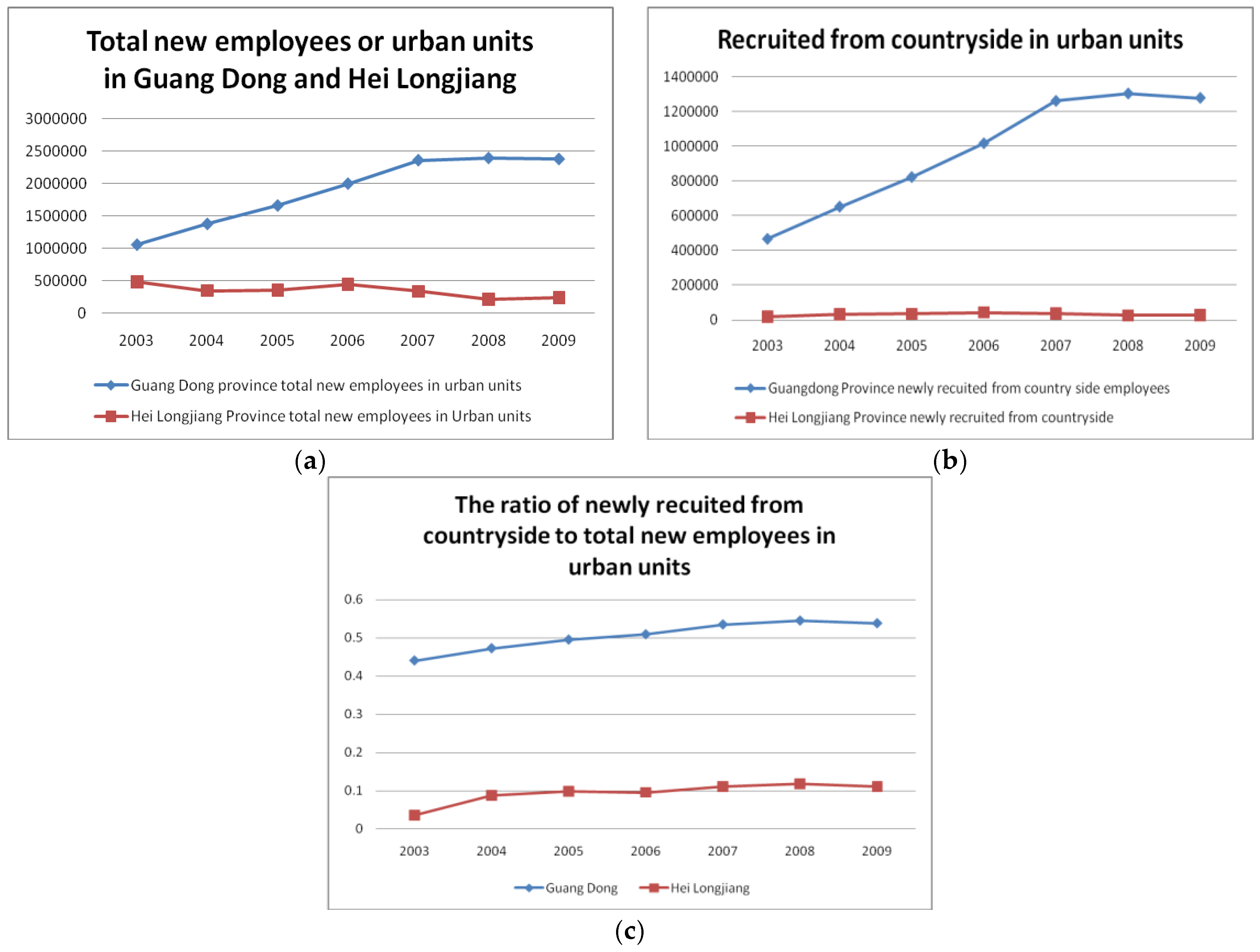

At the same time, the economically developed areas in the southeast coastal region have attracted a large amount of rural surplus labor, so these local governments have positive balances in their BPIUE funds. Currently, 17 provinces and municipalities are able to meet the payment demands and have accumulated balances before exhausting the 28% contribution. Guangdong Provincial Government can meet the payment demands with only 20% of the contribution. By the end of 2012, the cumulative balance of the BPIUE exceeded 2.3 trillion yuan.

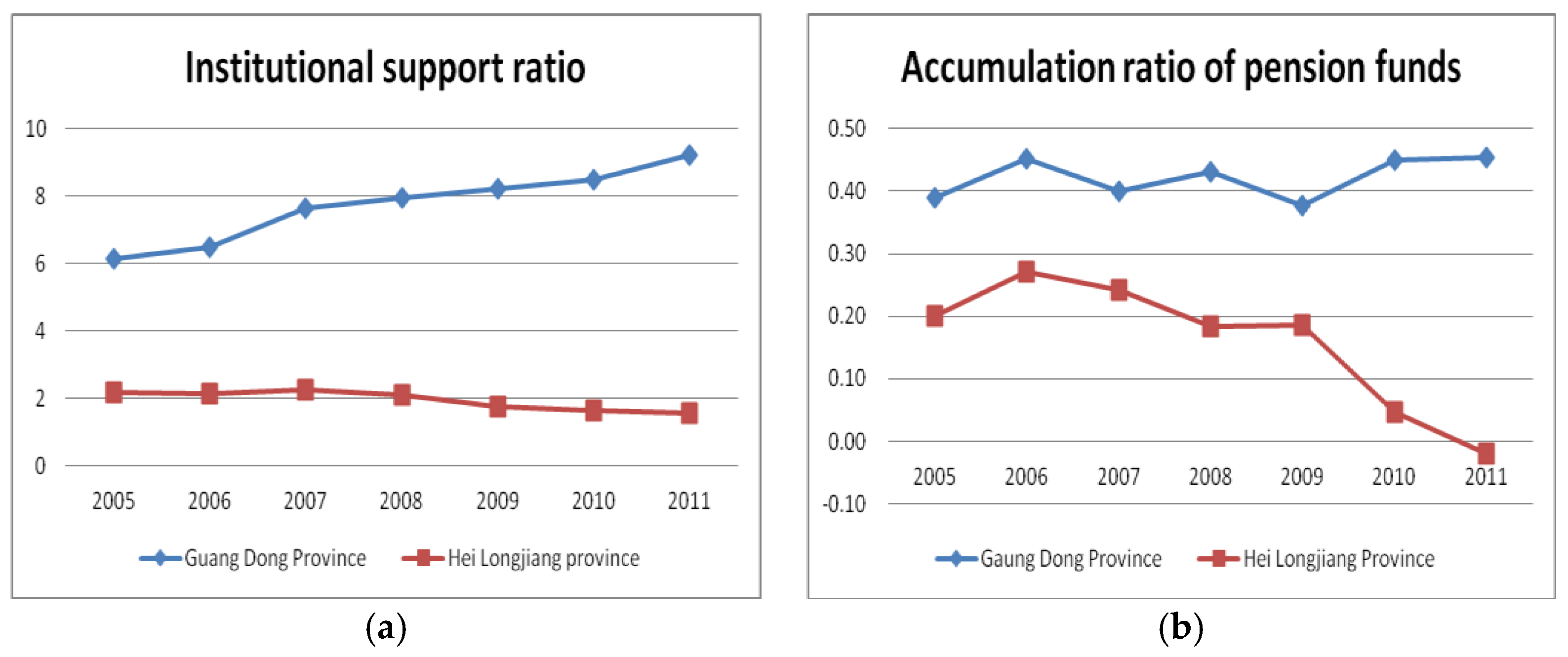

Using the examples of Guangdong and Heilongjiang provinces to examine regional differences, the results show that in 2011 the proportion of the elderly population over age 65 was 8% and 6%, respectively. Guangdong Province has been a destination for the migration of rural labor, while Heilongjiang Province is an old industrial base with many state-owned enterprises from the planned economy period. Therefore, Heilongjiang Province now has many retired older workers, with less inflow of rural labor. We compared the distribution of workers enrolled in the BPIUE and the ratio of support within the system for the two provinces in 2012. is defined as the number of workers enrolled and who contributed to the BPIUE in province during year , is defined as the number of workers who receive a pension in province during year , and the ratio of support within the system is:

The data show (Figure 4) that the ratio of support within the system in Guangdong increased from 6:1 in 2005 to 9:1 of 2011, while the ratio of support in Heilongjiang Province declined. In addition, since 2005, the balance in Guangdong Province has increased significantly and is currently close to 50%, while the balance in Heilongjiang Province is negative.

The differences in the balances are also reflected by new employees and their sources in urban work units in Guangdong Province and Heilongjiang Province over the years, as shown in Figure 5a–c. Figure 5a shows the number of new employees in urban work units in Heilongjiang Province and Guangdong Province each year; the number of new employees in Guangdong Province is higher, with approximately 2.5 million in 2011, while the number of new employees in Heilongjiang is less than 50,000. Figure 5b shows that the number of workers who migrated from the countryside to the city in Guangdong is more than 1.2 million per year, while the figure is less than 50,000 in Heilongjiang. Figure 5c shows that the reason for such a high number of new employees in Guangdong Province is that the province attracts a large amount of rural labor (from 2008–2011, more than 50% of the new labor in urban work units was from the countryside). The influx of rural labor into Guangdong Province also contributes to the balance in the province’s social insurance fund by allowing the province to maintain a higher level of fund contributions to help cope with the impact of aging. However, in some provinces, such as Heilongjiang Province, there is no influx of rural labor and the regions are old industrial bases with more retired workers; inevitably, the impact of aging is larger, so that in Heilongjiang Province, the BPIUE has been unable to meet the demands for payment using revenue from the same year since 2011. (Figure 4b).

4.3. Analysis of the Cumulative Balances of the BPIUE

China became an aging society in 2005, and the proportion of the elderly population age 65 or over is now more than 7% of the total population; therefore, the pressure for pension payments is increasing. There have been mounting demands to stop the misappropriation of funds in workers’ individual accounts and to increase their value through investment, and the 2005 State Council document on pension reform specified that the entire 20% enterprise contribution should be deposited into social pooling accounts. In terms of deposits, the social pooling accounts and the individual accounts are separated. Since 2006, considering only contributions to pooling accounts and not contributions to individual accounts, multiplying at the end of year by 20/28 should accurately reflect the revenue of the pooling fund. The annual balance of the following year is :

If contributions to individual accounts are excluded from fund revenue, then the portions of the individual accounts should likewise be excluded from fund expenditures and balances; therefore, is reduced accordingly.

However, according to the provisions of the 2005 State Council document, the BPIUE pays for the basic pension, including the basic pension of the social pooling accounts (calculated according to the average wage of the local community, the individual contribution base, and the number of years of contribution) and the pensions of the individual accounts. The pensions for the individual accounts equal the balance in the individual account divided by a specified number of months; according to the fifth census in 2000, the average life expectancy in China is 71.4 years, so people retiring at age 60 will receive a pension for 139 months, and people who survive beyond 139 months will still receive pension payments. This analysis shows that the BPIUE funds in the two accounts are mixed, the BPIUE is still a PAYG system with a defined benefit plan, and there is no separate investment or management for individual accounts.

In the formula, accumulation represents the cumulative balance of individual accounts at the time of each employee’s retirement, and m is the number of months of pension payments. m is determined according to actuarial calculations of life expectancy such that the older the retirement age is, the smaller m is, and the amount of the monthly pension payment is therefore higher.

Due to the continuous depreciation of the funds in individual accounts, the pension replacement ratio of the BPIUE has decreased from the initial 58% to below 50%, and enterprise workers are increasingly discontent. Beginning in 2006, the central government promised an increase of 10% per year in the BPIUE, and by 2012, the per capita monthly pension reached 1721 yuan.

To summarize the above analysis, the cumulative balance of the BPIUE is shown in Table 1 (1) the total accumulated amount of the two mixed accounts increased from 1.09 trillion yuan in 2007 to 1.54 trillion in 2011; (2) as of 2011, the accumulated amount in individual accounts was approximately 2.4859 trillion yuan, of which 270.3 billion yuan was commissioned to the National Social Security Fund Council for investment and management and 2.2156 trillion yuan was the amount missing from the empty pension accounts. Even if 1.53 trillion yuan was used to re-fund the empty accounts, there would still be a shortfall of 679 billion yuan; (3) in 2011, the financial subsidies were 220 billion yuan, and if the subsidies are excluded, the funding inadequacy reached 899 billion yuan.

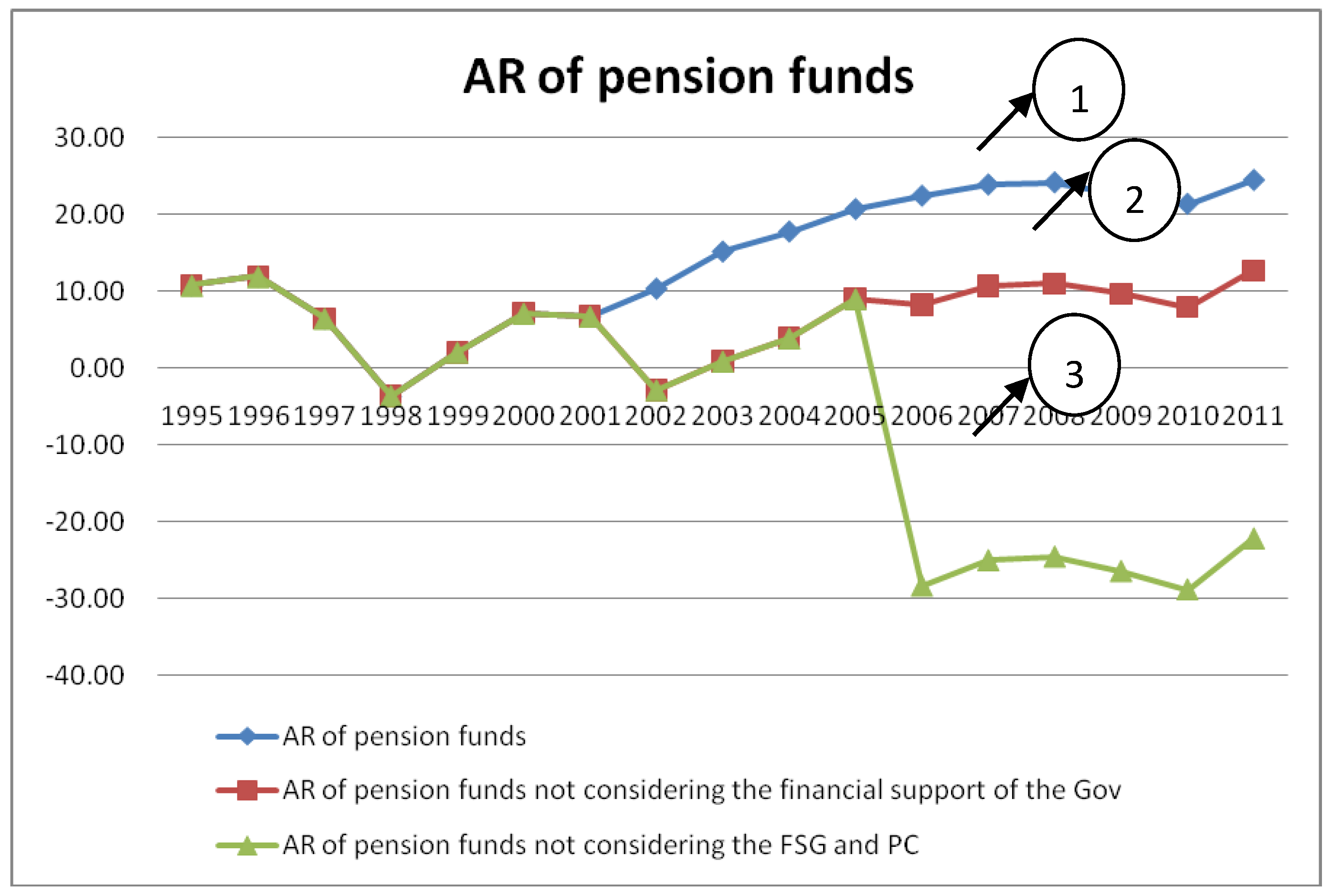

If the differences between the pooling accounts and the individual accounts are considered, and individual contributions and government subsidies are excluded from the calculation of the balance for the pooling funds, then the entire balance of the pooling funds for social pension insurance become even worse, as shown in Figure 6.

In Figure 6, Graph 1 represents the balance rate calculated in accordance with the statistics, and the current balances rate is more than 20%, but Graph 2 shows that beginning in 2003, the government financial subsidies are excluded from fund revenue (Financial support of the government). As a result, the balance rate since 2003 is only about half of Graph 1, and the balance rate for 2011 is only 10% of Graph 1. If the contributions to individual accounts and pooling accounts are strictly separated, that is, individual contributions are excluded from the annual fund revenue since 2006, then the balance rate of the entire pension fund is negative (as shown in Graph 3). This difference indicates that if the government subsidies and the contributions to individual accounts are excluded, the annual balance of China’s basic pension insurance fund will not be very high, and the cumulative balance rate of the entire fund will not increase as the population continues to age.

Figure 6 shows that the IA pensions in China are different from the model for individual savings and pension funds adopted in Chile, Australia, and for the U.S. 401 (k) system. So far, China’s concept is still not clear, and the line between a pension tax in disguise and nominal pension savings is not defined. Social pooling and individual accounts are mixed, and the BPIUE maintains PAYG characteristics.

5. The Impact of the Aging of the Population on the Balance Rate of China’s BPIUE Fund

The Sustainability of the BPIUE under China’s Aging

To examine the sustainability of the development of China’s BPIUE in a rapidly aging society, this paper uses 2012 as the starting year. is defined as the average wage for urban workers in year , is the average annual growth rate of the number of workers enrolled in the BPIUE after year , is the average growth rate of pensioners after year , is the per capita wage replacement rate of pension payments after year , is the per capita contribution to the BPIUE after year , and and are the number of workers enrolled in the BPIUE and the number of pensioners in the starting year, respectively, as shown in Formula (1):

The revenue and expenditures of the BPIUE after year are shown in Formula (2):

The difference between the revenue and expenditures of the BPIUE in future years depends on the difference between revenue and expenditures in the given year; therefore, judgment function is created, which is defined as the ratio of expenditures and revenue (4-3) and indicates the changes in the balance rate of the fund in the future.

where in,

The of each year is compared to 1; if is less than 1, then the revenue of the BPIUE is sufficient to cover the expenses for the given year. If increases to more than 1, then there is a deficit in the BPIUE in that year. Therefore, the future judgment function primarily depends on changes in certain parameters. Among these parameters, the aging of the population is an irreversible trend; the formula also accounts for changes in the judgment function for the ratio of support within the system () and (), and institutional factors (), which include the specified contribution ratio of the wages and the pension replacements.

If the pooling accounts and the individual accounts continue to be mixed, then starting in 2006, the long-term is 0.28, which is the joint contribution ratio of employers and employees, and the pension replacement ratio shows a downward trend. The parameters of , , , and for 2006–2011 are shown in Table 2:

The results show that on one hand, is greater than 1 for a considerable period, but it shows a decreasing trend; reflects the ratio of support within the system and is 0.33–0.32 in 2006–2011, showing a decreasing trend; is less than 1, suggesting that there is a balance between revenue and expenditures in the BPIUE fund prior to 2011, and shows a clear decreasing trend, with an average annual decrease of 0.01. On the other hand, three necessary conditions are needed to support the balance between revenue and expenditures in the BPIUE fund: first, high contribution rates , at 28% of total wages; second, the pension replacement ratio must decline; and third, the number of workers enrolled in the BPIUE () must grow at a certain rate.

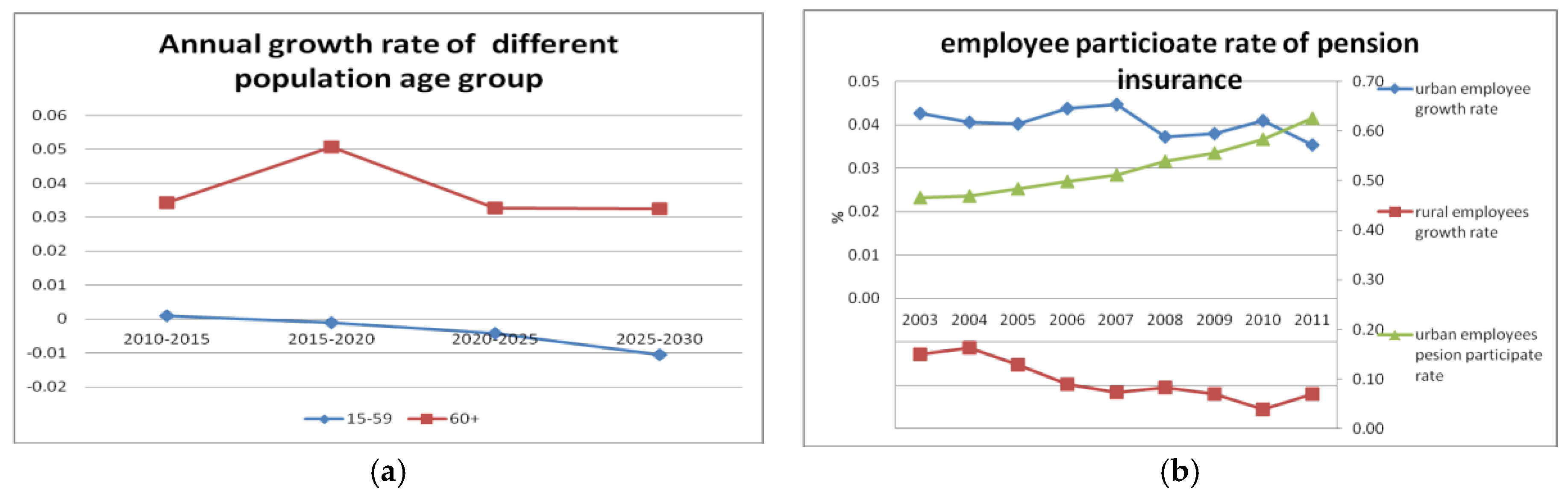

Are the above three conditions sustainable in rapidly aging China? (1) The high contribution rate , at 28% of total wages, is a heavy burden to enterprise development and personal income. This ratio is a heavy burden even for more developed countries and countries where the population is aging faster and sooner, such as the Organization for Economic Cooperation and Development (OECD) countries (Sanz and Velázquez 2007). Right now, the scope of the contribution ratio for the next 30 years has been exhausted and is not sustainable, so further increases are out of question. (2) Currently, the pension replacement ratio is as low as 42%, lower than the International Labor Organization’s (ILO) minimum security standard of 55%, suggesting that the growth rate of the pension is lower than the average wage growth rate, so continued decreases are bound to affect the living standards of retired workers. (3) Maintaining a high growth rate () of worker enrollment will be difficult. On one hand, the size of the labor force decreased by 3.45 million in 201219, and on the other hand, the level of urbanization is higher than 50%. Cai et al. show that there is not much room for an unlimited increase in the supply of labor and the migration of rural labor to urban areas (Cai 2010). The prospective population data of the United Nations show that (Figure 6a) the annual growth rate of the population age 60 or older will be maintained at 3–5% from 2015–2030, while the growth rate of the 15–59-year-old working-age population will be negative. The BPIUE coverage will be higher than 60%, and its growth rate in recent years has fluctuated approximately 4% (Figure 7b). The growth rate of rural employment will be negative.

Figure 7a,b show that the increase of the urban labor force in China in recent years is due to the migration of rural labor to urban areas and is decreasing year by year. A large number of working-age rural workers arrive in the city, and they are required to participate in the BPIUE and fulfill the contribution obligations, but when most of them return to the countryside in old age, the local governments will not pay pensions to them, other than returning their portion of the individual savings20. The current statutory retirement age in China is 50 for women and 60 for men, and with the decline of the total labor force between the ages of 15–59, a large amount of the rural labor force will stay in and build rural areas in the new round of urbanization, so in the future there will be no sustained increase in the labor force to support the growth rate of workers enrolled in the BPIUE. From 2015–2030, the growth rate of insured workers will be less than the growth rate of retired workers, and will be reduced from 0.32 to 0.2 or even lower. In addition, the function will become larger, getting closer to 1.

This so-called pension insurance system with a mixture of SP and IA virtually operates both accounts as PAYG; thus, the system can only maintain a balance for the short term and will not maintain its balance in the next decade as the aging of the population continues. The greater concern is IA misappropriation, which will leave a large liability for the Chinese government as China becomes an advanced and super-aging society in the future.

6. Conclusions and Discussion

This paper has attempted to answer three questions. The conclusions are as follows:

- (1)

- The “BPIUE” implemented since 1991 follows the customary practices of The 1951 Labor Insurance Regulations issued by the Chinese government, and the initial design of employees’ individual accounts has deviated from the insurance principles and is now a matter of individual savings; there is a lack of legal basis for the misappropriation of funds in individual accounts since 1998, and there is no policy to interpret this phenomenon. This system for workers’ contributions is different from the payroll tax in the United States and individual social insurance in Germany and is even more different from individual savings in Singapore. When individual accounts and pooling accounts are mixed and jointly used for payment, social insurance and welfare are essentially mixed, which is not the design of the policy.

- (2)

- The cumulative balance of the BPIUE fund derives from ignoring the difference between the PAYG system of the pooling accounts and the accumulation of individual accounts during calculation. Contributions from both enterprises and employees as well as from the large rural labor force that has poured into the cities since 1998 determine the system’s current revenue. The model relies on this influx of rural workers to increase social security contributions and thus reduce the burden on the government, which can be regarded as part of the dividend of a labor force with a large working-age population base. However, from the viewpoint of the overall rapid aging of China’s population, the system’s current balance is temporary and defective. Meanwhile, in some regions such as Heilongjiang Province, the current contributions are not sufficient to meet the demands for current payments because of the aging of the population and the historical burden of the reform of state-owned enterprises, requiring local government subsidies and transfer payments from the central government. Moreover, the funds in individual accounts have been misappropriated, resulting in empty accounts that need to be repaid by the government. Government subsidies are also an important source of revenue for pension insurance, and the central government subsidizes the provinces that face current payment pressures.

- (3)

- Therefore, the Chinese government has mixed social insurance and welfare, as well as PAYG and accumulation in individual accounts. The misappropriation of IA funds and the lack of specialized market-oriented management inhibit the value appreciation of the IA. Continuously increasing financial subsidies to maintain the short-term BPIUE balance is a short-term behavior that violates the long-term liability management principles of pensions, and there is an urgent need for policy adjustments in the future.

Discussion: The current pension system is mainly administrated in province level. It means that if there is surplus in a certain province, there is no formal way to transfer the surplus to the province in deficit. China must learn from the successful experience of other countries. On the one hand, China needs to establish a unified national basic pension system to achieve fairness, effectively overcome poverty in old age, and discontinue the two-tier pension system in which civil servants and public-sector employees do not participate in pension insurance but enjoy high pension subsidies with full financial support after retirement. On the other hand, China also needs to establish individual pension savings accounts, provide tax breaks, create a pension fiduciary system and pension market, achieve the goal of preserving and increasing the value of pension funds, and improve living standards in old age, which will be an important strategy for China to respond to the aging of its population.

Acknowledgments

The research in this paper was supported by 2012 National Social Science Foundation (The research on population ageing and the aged caring industry development. No. 12AGL002). We wish to express our gratitude for these supports.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Angrisani, Massimo, Anna Attias, Sergio Bianchi, and Zoltàn Varga. 2012. Sustainability of a pay-as-you-go pension system by dynamic immigration control. Applied Mathematics and Computation 219: 2442–52. [Google Scholar] [CrossRef]

- Blake, David. 2003. The UK pension system: Key issues. Pensions 8: 330–75. [Google Scholar] [CrossRef]

- Cai, Fang. 2010. Demographic Transition, Demographic Dividend, and Lewis Turning Point in China. Economic Research Journal 4: 4–13. [Google Scholar] [CrossRef]

- Calvo, Esteban, and John B. Williamson. 2008. Old-age pension reform and modernization pathways: Lessons for China from Latin America. Journal of Aging Studies 22: 74–87. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Casamatta, Georges, Helmuth Cremer, and Pierre Pestieau. 2000. Political sustainability and the design of social insurance. Journal of Public Economics 75: 341–64. [Google Scholar] [CrossRef]

- Cremer, Helmuth, and Pierre Pestieau. 2000. Reforming our pension system: Is it a demographic, financial or political problem? European Economic Review 44: 974–83. [Google Scholar] [CrossRef]

- Department for work and pension. 2010. 21st Century Welfare. In Presented to Parliament by the Secretary of State for Work and Pensions by Command of Her Majesty July 2010; London: Department for work and pension. Available online: www.dwp.gov.uk/21st-century-welfare (accessed on 5 June 2012).

- Dokeland, Trond M., and Helge A. Nordahl. 2008. Optimal pension insurance design. Journal of Banking & Finance 32: 382–92. [Google Scholar]

- Dong, Keyong, and Xiangfeng Ye. 2003. Social security system reform in China. China Economic Review 14: 417–25. [Google Scholar] [CrossRef]

- Drucker, Peter F. 1999. The Pension Fund Revolution. Transaction Publishers; Chinese Translation. Maharashtra: Oriental Press. [Google Scholar]

- Fanti, Luciano, and Luca Gori. 2012. PAYG pensions, tax-cum-subsidy and A-Pareto efficiency. Research in Economics 66: 65–71. [Google Scholar] [CrossRef] [Green Version]

- Feldstein, Martin. 1999. Social security pension reform in China. China Economic Review 10: 99–107. [Google Scholar] [CrossRef]

- Feldstein, Martin. 2005. Rethinking Social Insurance. National Bureau of Economic Research Working Paper No. 11250. Available online: http://www.nber.org/papers/w11250 (accessed on 5 June 2012).

- Hu, Naijun, and Yansui Yang. 2012. The Real Old-Age Dependency Ratio and the Inadequacy of Public Pension Finance in China. Journal of Population Ageing 5: 193–209. [Google Scholar] [CrossRef]

- Hussain, Athar. 1994. Social Security in Present-Day China and Its Reform. The American Economic Review 84: 276–80. [Google Scholar]

- Kolmar, Martin. 2007. Beveridge versus Bismarck public-pension systems in integrated markets. Regional Science and Urban Economics 37: 649–69. [Google Scholar] [CrossRef]

- Population Division, DESA, and United Nations. 2001. World Population Aging 1950–2050. New York: United Nations, p. 49. [Google Scholar]

- Samuelson, Paul A. 1958. An Exact Consumption-Loan Model of Interest with or without the Social Contrivance of Money. Journal of Political Economy 66: 467–82. [Google Scholar] [CrossRef]

- Sanz, Ismael, and Francisco J. Velázquez. 2007. The role of ageing in the growth of government and social welfare spending in the OECD. European Journal of Political Economy 23: 917–31. [Google Scholar] [CrossRef]

- Sinn, Hans-Werner. 2004. The pay-as-you-go pension system as fertility insurance and an enforcement device. Journal of Public Economics 88: 1335–57. [Google Scholar] [CrossRef]

- Williamson, John B., and Catherine Deitelbaum. 2005. Social security reform: Does partial privatization make sense for China? Journal of Aging Studies 19: 257–71. [Google Scholar] [CrossRef]

- Williamson, John B., Meghan Price, and Ce Shen. 2012. Pension policy in China, Singapore, and South Korea: An assessment of the potential value of the notional defined contribution model. Journal of Aging Studies 26: 79–89. [Google Scholar] [CrossRef]

- Zheng, Bingwen. 2013. China’s Pension Development Report (2012). Beijing: Economic Management Press. [Google Scholar]

| 1 | Press conference announcement of the National Bureau of Statistics on January 18, 2013, reproduced by Xinhua, China, at http://www.chinanews.com/gn/2013/01-18/4501813.shtml. |

| 2 | World Population Project, 2011. http://esa.un.org/. |

| 3 | The data are from the e-version of China’s National Statistical Yearbook at http://www.stats.gov.cn/tjsj/ndsj/2012/indexch.htm. |

| 4 | The data are from the annual announcement of the Ministry of Human Resources and Social Security of China at http://www.mohrss.gov.cn/SYrlzyhshbzb/zwgk/szrs. |

| 5 | See the following report for the social insurance and welfare principles and requirements, as well as the reform of the UK’s social security system: Department for work and pension (2010). |

| 6 | In June 1991, the State Council issued the document “Decision on the reform of the pension insurance system for urban enterprise employees”, introducing universal social pooling of pension insurance for urban-area employees. |

| 7 | The State Council document from March 1995, “Circular on deepening the reform of the pension insurance system for enterprise employees”, started the transition from PAYG to partial accumulation of funds and introduced the concept that employees should contribute to pension insurance either through social pooling or through individual accounts, whichever was selected by the local government. |

| 8 | Pilot projects were undertaken, and two sets of implementation schemes (the high and low contribution ratios for individual contributions) were provided from which local governments could choose. Based on the experience gained during this transitional period, in July 1997 the State Council promulgated its “Decision on establishing a unified basic pension insurance system for enterprise employees.” |

| 9 | The National Bureau of Statistics of China in 1999 |

| 10 | According to internal statistics of the Ministry of Human Resources and Social Security. |

| 11 | The 2005 State Council document “Decision to consummate the basic pension insurance system for enterprise employees” set up the whole pension insurance system as the integration of SP and IA. |

| 12 | The accumulation rate is calculated as the funds revenue minus the expenses then divided by the revenue. So, in the year 2011, the AR is 25% which means there was nearly one quarter of the revenue could be saved at that year. The AR in 1998 is below 0, which means the revenue of that year could not meet the expense demand of the same year. |

| 13 | Data source: (Zheng 2013). |

| 14 | Same as above. |

| 15 | Same as above. |

| 16 | Data source: National Statistics Year Book 2012. |

| 17 | Data source: Statistics of the Ministry of Human Resources and Social Security 2013. |

| 18 | The number of participants in the social insurance fund, the benefit levels, and workers’ wages are shown in the State Statistical Yearbook each year. |

| 19 | Press conference announcement of the National Bureau of Statistics on January 18, 2013, reproduced by Xinhua, China, at http://www.chinanews.com/gn/2013/01-18/4501813.shtml. |

| 20 | The premise for pooling at provincial levels is that there is difficulty in transferring and carrying pension insurance benefits. China’s pension insurance system for urban and rural residents was established in 2009, but improvement of the system requires more time. |

Figure 1.

Funds accumulation of the Urban Staff Pension System and the aging process in China. (The units for revenue, expenses, and balance are in 100 million RMBs).

Figure 1.

Funds accumulation of the Urban Staff Pension System and the aging process in China. (The units for revenue, expenses, and balance are in 100 million RMBs).

Figure 2.

The changes from the 1997–1998 state-owned enterprise reforms and the accumulation ratios.

Figure 2.

The changes from the 1997–1998 state-owned enterprise reforms and the accumulation ratios.

Figure 3.

Subsidies from governments at all levels for the Basic Pension Insurance for Urban Employees (BPIUE) over the years.

Figure 3.

Subsidies from governments at all levels for the Basic Pension Insurance for Urban Employees (BPIUE) over the years.

Figure 4.

Geographical differences of pension insurance funds between Heilongjiang and Guangdong Provinces. (a) is the institutional support ratio and (b) is the accumulation ration of the two provinces.

Figure 4.

Geographical differences of pension insurance funds between Heilongjiang and Guangdong Provinces. (a) is the institutional support ratio and (b) is the accumulation ration of the two provinces.

Figure 5.

New employees and their sources in Guang Dong and Hei Longjiang, (a) Total new employees of urban unit; (b) New employees of urban units recruited from the countryside; (c) Ratio of newly recruited from countryside to total new employees in urban units.

Figure 5.

New employees and their sources in Guang Dong and Hei Longjiang, (a) Total new employees of urban unit; (b) New employees of urban units recruited from the countryside; (c) Ratio of newly recruited from countryside to total new employees in urban units.

Figure 6.

Accumulation rate of pension funds (%).

Figure 7.

Annual growth rate of future age groups. (a) is the annula growth rate of different age group and (b) is the employees participate rate.

Figure 7.

Annual growth rate of future age groups. (a) is the annula growth rate of different age group and (b) is the employees participate rate.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Individual accounts are empty accounts with huge deficits.

| Year | Accumulation Record (100 Million)13 | Real Assets14 | Empty Amounts15 | Balance at Year End16 | Financial Support of the Gov17 |

|---|---|---|---|---|---|

| 2006 | 9994.00 | 9994.00 | 4041.00 | 971.00 | |

| 2007 | 11,743.00 | 786.00 | 10,957.00 | 5488.88 | 1157.00 |

| 2008 | 13,837.00 | 1100.00 | 12,737.00 | 7391.40 | 1437.00 |

| 2009 | 16,557.00 | 1569.00 | 14,988.00 | 9931.00 | 1646.00 |

| 2010 | 19,596.00 | 2039.00 | 17,557.00 | 12,526.09 | 1954.00 |

| 2011 | 24,859.00 | 2703.00 | 22,156.00 | 15,365.28 | 2272.00 |

Table 2.

Various parameters and their calculation results since 200618.

Table 2.

Various parameters and their calculation results since 200618.

| Year | |||||||

|---|---|---|---|---|---|---|---|

| 2006 | 0.08 | 0.06 | 0.46 | 0.28 | 1.66 | 0.33 | 0.55 |

| 2007 | 0.07 | 0.07 | 0.44 | 0.28 | 1.59 | 0.33 | 0.52 |

| 2008 | 0.09 | 0.07 | 0.45 | 0.28 | 1.61 | 0.32 | 0.52 |

| 2009 | 0.07 | 0.09 | 0.44 | 0.28 | 1.60 | 0.33 | 0.53 |

| 2010 | 0.09 | 0.09 | 0.44 | 0.28 | 1.57 | 0.32 | 0.50 |

| 2011 | 0.11 | 0.08 | 0.42 | 0.28 | 1.53 | 0.32 | 0.49 |

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Hu, N. The Misunderstanding of Social Insurance: The Inadequacy of the Basic Pension Insurance for Urban Employees (BPIUE) for the Aging Population of China. Soc. Sci. 2018, 7, 79. https://0-doi-org.brum.beds.ac.uk/10.3390/socsci7050079

AMA Style

Hu N. The Misunderstanding of Social Insurance: The Inadequacy of the Basic Pension Insurance for Urban Employees (BPIUE) for the Aging Population of China. Social Sciences. 2018; 7(5):79. https://0-doi-org.brum.beds.ac.uk/10.3390/socsci7050079

Chicago/Turabian StyleHu, Naijun. 2018. "The Misunderstanding of Social Insurance: The Inadequacy of the Basic Pension Insurance for Urban Employees (BPIUE) for the Aging Population of China" Social Sciences 7, no. 5: 79. https://0-doi-org.brum.beds.ac.uk/10.3390/socsci7050079

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.