Effect of Psychological Factors on Credit Risk: A Case Study of the Microlending Service in Mongolia

,

,  ,

,

and

and

Abstract

:1. Introduction

2. Theoretical Background

2.1. Psychological Variables

2.1.1. Effective Financial Decision-Making

2.1.2. Self-Control

2.1.3. Conscientiousness

2.1.4. Selflessness and Giving (Charitable) Attitude

2.1.5. Neuroticism

2.1.6. Attitude towards Money

3. Methodology

3.1. Data Collection

3.2. Test Developing Steps

3.2.1. Establish Expert Committee

3.2.2. Identify Dimensionality of Construct

3.2.3. Item Development

3.2.4. Review and Revise Initial Item Pool

3.2.5. Pilot Testing

- Focus group discussion

- 2.

- Pilot testing

3.2.6. Reliability/Validity Check

3.3. Statistics for the Sampled Data

3.4. Economic Categories

- Salary—What is your monthly income?

- Extra income—What is the amount of your extra income?

- Salary loan—Do you have a salary loan?

- NBFI loan—Do you repay loans at banks and NBFIs?

- Previous NBFI loan—Have you ever received loans from banks and NBFIs?

- Mortgage loan—Do you have a mortgage loan?

- Monthly payment—How much money do you spend on servicing loans each month?

- Real estate—Do you have an immovable property under your name?

- Real estate price—What is the current market price of your immovable property?

- Car—Do you own a car?

- Car price—What is the current market price of your car?

- Life year—How long have you lived at your current address?

3.5. Measure

4. Results

4.1. Factor Analysis

4.2. Analysis of Psychological Variables

4.3. Analysis on Psychological Variables through Economic Factors

5. Findings and Discussion

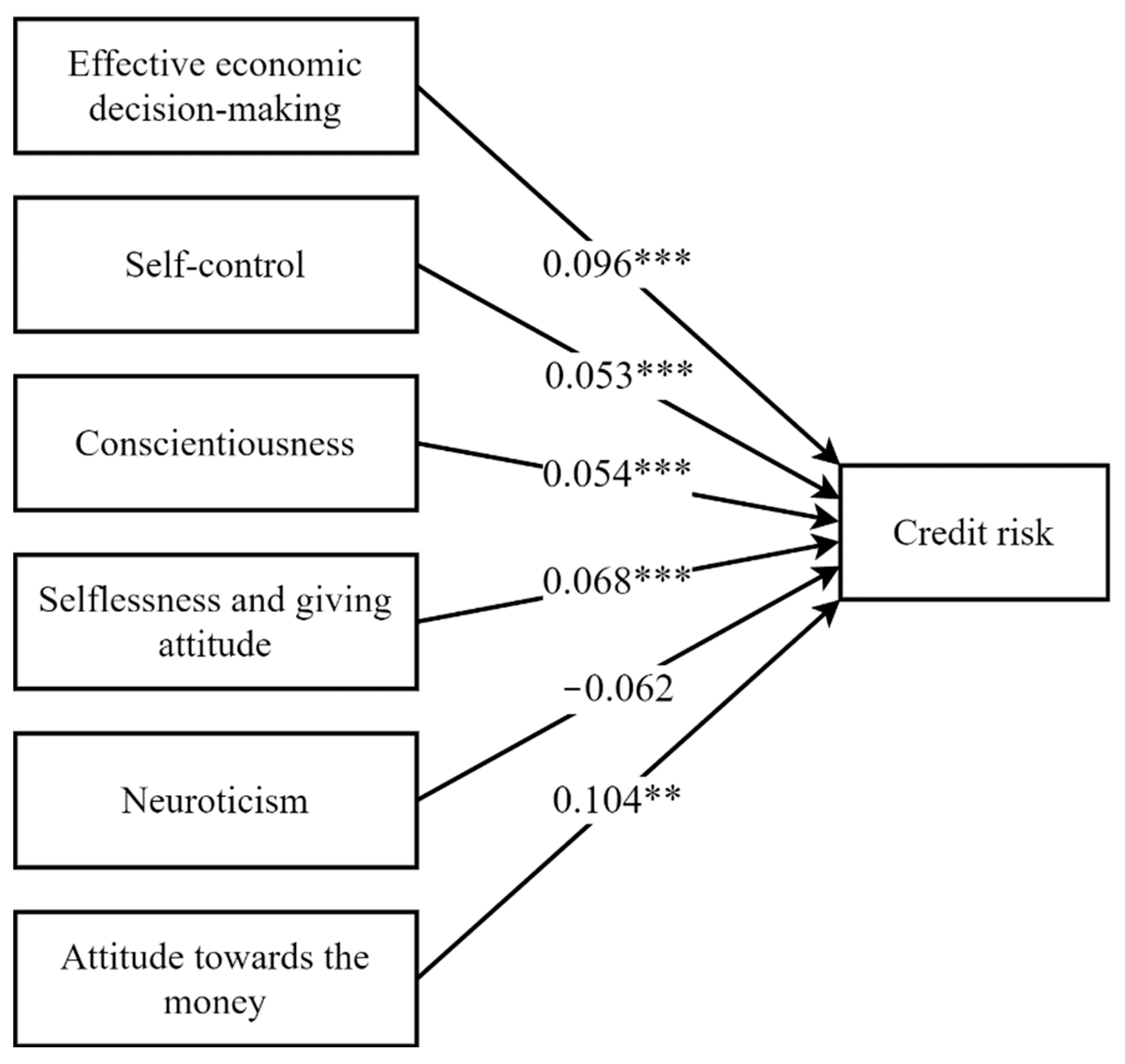

- As shown in H1, protecting oneself from acting on a whim and making a budget and purchase decisions are based on logic and analysis and essentially enables one to practice proper money management and to be left with sufficient money for the loan repayment. This result supports the findings that rational decision-making is a prominent characteristic of responsible borrowers [1].

- H2 reveals that poor self-control leads to overspending and unnecessary purchases, thus leaving no room for servicing one’s loans. This result supports the idea that lack of self-control and a low level of financial literacy are positively correlated with defaults on consumer loans and self-reports of excessive debt burden [34].

- As reflected in H3, a conscientious person has better financial control, holds savings, and ensures timely debt servicing. This result supports some research findings which state that responsible borrowers have a higher level of conscientiousness and rational debt behavior than risky borrowers [21]. Additionally, researchers stated that conscientious individuals are responsible, attentive, careful, persistent, orderly, and planful, while those people who score low on this trait are irresponsible, unreliable, careless, and distractible [58].

- As shown in H4, a generous and selfless individual with a mission to serve others tends to repay loans. This result supports the theory which says that people who are unable to spend money on others tend to lack soul to pay the loan back [38].

- As reflected in H5, the hypothesis of the psychological factor, neuroticism, was not supported. As compared against the other indicators, neuroticism is volatile and cannot serve as an indicator to predict a consistent outcome. This finding supports the result of a previous survey [21]. However, this result is in disagreement with Nyhus and Webley (2001) [12], who found that emotional instability (i.e., neuroticism) is a predictor of loan default. The reason for this result needs to be re-examined, and we assume that there are differences in national characteristics.

- As demonstrated in H6, the possibility to service loans on time is increased when one neither worships nor denies money. Conversely, worshipping or fearing money has a propensity to lead one to either deny using money or emotionally spend to accommodate one’s psychological issues. This leaves one to have no money to spend on servicing loans.

6. Conclusions, Implications and Limitations

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Özşahin, M.; Yürür, S.; Coşkun, E. A Field Research to Identify Psychological Factors Influencing the Debt Repayment Behavior in Turkey. EMAJ Emerg. Mark. J. 2019, 8, 26–33. [Google Scholar] [CrossRef] [Green Version]

- LenddoEFL. Available online: https://lenddoefl.com (accessed on 17 March 2021).

- National Centre for Lifelong Education of Mongolia. 2018. Available online: https://www.ncle.mn (accessed on 17 March 2021).

- Central Bank of Mongolia. Financial Stability Report of Mongolia. 2019. Available online: https://www.mongolbank.mn (accessed on 17 March 2021).

- National Statistics Office of Mongolia. Mongolian Statistical Yearbook. 2019. Available online: https://www.1212.mn (accessed on 17 March 2020).

- Fernandes, D.; Lynch, J.G., Jr.; Netemeyer, R.G. Financial literacy, financial education, and downstream financial behaviors. Manag. Sci. 2014, 60, 1861–1883. [Google Scholar] [CrossRef]

- Klinger, B.; Khwaja, A.I.; Del Carpio, C. Enterprising Psychometrics and Poverty Reduction; Springer: Berlin/Heidelberg, Germany, 2013; Volume 860. [Google Scholar]

- Kahneman, D.; Tversky, A. Prospect Theory. An Analysis of Decision Making Under Risk. In Prospect Theory. An Analysis of Decision Making Under Risk; Defense Technical Information Center: Fort Belvoir, VA, USA, 1977; pp. 99–127. [Google Scholar]

- Rahman, M.; Azma, N.; Masud, M.; Kaium, A.; Ismail, Y. Determinants of indebtedness: Influence of behavioral and demo-graphic factors. Int. J. Financ. Stud. 2020, 8, 8. [Google Scholar] [CrossRef] [Green Version]

- Davies, S.; Finney, A.; Collard, S.; Trend, L. Borrowing behaviour. In A Systematic Review for the Standard Life Foundation Report; Personal Finance Research Centre, University of Bristol: Bristol, UK, 2019. [Google Scholar]

- Gagarina, M.; Nestik, T.; Drobysheva, T. Social and Psychological Predictors of Youths’ Attitudes to Cryptocurrency. Behav. Sci. 2019, 9, 118. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Nyhus, E.K.; Webley, P. The role of personality in household saving and borrowing behaviour. Eur. J. Pers. 2001, 15, S85–S103. [Google Scholar] [CrossRef]

- Gutiérrez-Nieto, B.; Serrano-Cinca, C.; De La Cuesta, M. A multivariate study of over-indebtedness’ causes and consequences. Int. J. Consum. Stud. 2017, 41, 188–198. [Google Scholar] [CrossRef]

- Sukheja, G.M. Behavioral biases in financial decision making. Int. J. Mark. Financ. Serv. Manag. Res. 2016, 5, 60–69. [Google Scholar]

- Kahneman, D.; Tversky, A. Intuitive Prediction: Biases and Corrective Procedures; Cambridge University Press (CUP): Cambridge, UK, 1982; pp. 414–421. [Google Scholar]

- Kahneman, D. Thinking, Fast and Slow; Macmillan: New York, NY, USA, 2011. [Google Scholar]

- Wang, L.; Lu, W.; Malhotra, N.K. Demographics, attitude, personality and credit card features correlate with credit card debt: A view from China. J. Econ. Psychol. 2011, 32, 179–193. [Google Scholar] [CrossRef]

- Robb, C.A.; Sharpe, D.L. Effect of personal financial knowledge on college students’ credit card behavior. J. Financ. Couns. Plan. 2009, 20, 25–43. [Google Scholar]

- Hampson, S.E. Personality processes: Mechanisms by which personality traits “get outside the skin”. Annu. Rev. Psychol. 2012, 63, 315–339. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Gathergood, J. Self-control, financial literacy and consumer over-indebtedness. J. Econ. Psychol. 2012, 33, 590–602. [Google Scholar] [CrossRef] [Green Version]

- Gagarina, M.A.; Shantseva, A.A. Socio-psychological peculiarities and level of financial literacy of Russian debtors. Rev. Bus. Econ. Stud. 2017, 5, 5–22. [Google Scholar]

- Atkinson, A. Measuring Financial Literacy: Results of the OECD INFE Pilot Study [Electronic Resource]; OECD Working Papers on Finance, Insurance and Private Pensions; OECD Publishing: Paris, France, 2012; Available online: https://www.oecd.org/about/ (accessed on 17 March 2021).

- Bhattacherjee, A. Social Science Research: Principles, Methods, and Practices; University of South Florida: Tampa, FL, USA, 2012. [Google Scholar]

- Luksander, A.; Németh, E.; Zsótér, B. Financial personality types and attitudes that affect financial indebtedness. Int. J. Soc. Sci. Educ. Res. 2017, 2, 4687–4704. [Google Scholar]

- Hirshleifer, D. Don’t Hide Your Light Under a Bushel: Innovative Originality and Stock Returns; University Library of Munich: Munich, Germany, 2014; Available online: http://www.vwl.uni-muenchen.de/ (accessed on 17 March 2021).

- Dennett, D.C. Consciousness Explained; Little Brown and Company: Boston, MA, USA, 1991. [Google Scholar]

- Fehr, E. The economics of impatience. Nat. Cell Biol. 2002, 415, 269–272. [Google Scholar] [CrossRef]

- Heidhues, P.; Kőszegi, B. Exploiting Naïvete about Self-Control in the Credit Market. Am. Econ. Rev. 2010, 100, 2279–2303. [Google Scholar] [CrossRef] [Green Version]

- Laibson, D. Golden Eggs and Hyperbolic Discounting. Q. J. Econ. 1997, 112, 443–478. [Google Scholar] [CrossRef] [Green Version]

- Strömbäck, C.; Lind, T.; Skagerlund, K.; Västfjäll, D.; Tinghög, G. Does self-control predict financial behavior and financial well-being? J. Behav. Exp. Financ. 2017, 14, 30–38. [Google Scholar] [CrossRef]

- Ameriks, J.; Caplin, A.; Leahy, J. Wealth Accumulation and the Propensity to Plan. Q. J. Econ. 2003, 118, 1007–1047. [Google Scholar] [CrossRef]

- Ameriks, J.; Caplin, A.; Leahy, J.; Tyler, T. Measuring Self-Control Problems. Am. Econ. Rev. 2007, 97, 966–972. [Google Scholar] [CrossRef] [Green Version]

- Achtziger, A.; Hubert, M.; Kenning, P.; Raab, G.; Reisch, L. Debt out of control: The links between self-control, compulsive buying, and real debts. J. Econ. Psychol. 2015, 49, 141–149. [Google Scholar] [CrossRef] [Green Version]

- Gathergood, J.; Disney, R.F. Financial Literacy and Indebtedness: New Evidence for U.K. Consumers. SSRN Electron. J. 2011. [Google Scholar] [CrossRef]

- Donnelly, G.; Iyer, R.; Howell, R.T. The Big Five personality traits, material values, and financial well-being of self-described money managers. J. Econ. Psychol. 2012, 33, 1129–1142. [Google Scholar] [CrossRef]

- Duckworth, A.L.; Quinn, P.D.; Tsukayama, E. What No Child Left Behind leaves behind: The roles of IQ and self-control in predicting standardized achievement test scores and report card grades. J. Educ. Psychol. 2012, 104, 439–451. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Donnellan, M.B.; Conger, K.J.; McAdams, K.K.; Neppl, T.K. Personal Characteristics and Resilience to Economic Hardship and Its Consequences: Conceptual Issues and Empirical Illustrations. J. Pers. 2009, 77, 1645–1676. [Google Scholar] [CrossRef] [Green Version]

- Science of Generosity Initiative. 2012. Available online: https://generosityresearch.nd.edu (accessed on 17 March 2021).

- Moll, J.; Krueger, F.; Zahn, R.; Pardini, M.; de Oliveira-Souza, R.; Grafman, J. Human fronto–mesolimbic networks guide de-cisions about charitable donation. Proc. Natl. Acad. Sci. USA 2006, 103, 15623–15628. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Walumbwa, F.O.; Schaubroeck, J. Leader personality traits and employee voice behavior: Mediating roles of ethical leadership and work group psychological safety. J. Appl. Psychol. 2009, 94, 1275–1286. [Google Scholar] [CrossRef]

- Britt, S.L.; Canale, A.; Fernatt, F.; Stutz, K.; Tibbetts, R. Financial Stress and Financial Counseling: Helping College Students. J. Financial Couns. Plan. 2015, 26, 172–186. [Google Scholar] [CrossRef]

- Sages, R.A.; Griesdorn, T.S.; Gudmunson, C.G.; Archuleta, K.L. Assessment in Financial Therapy. In Financial Therapy; Springer: Cham, Switzerland, 2015; pp. 69–85. [Google Scholar]

- Klontz, B.; Klontz, T. Mind over Money: Overcoming the Money Disorders that Threaten Our Financial Health, 1st ed.; Crown Business: New York, NY, USA, 2009. [Google Scholar]

- Goldfayn, O.; Vellekoop, N. Borrowing from Family and Friends: Preferences, Peers and Personality. Think Forward Initiative Research Challenge. 2018. Available online: https://www.thinkforwardinitiative.com (accessed on 17 March 2021).

- Hornyák, A. Attitűdök és Kompetenciák a Középiskolás Diákok, Mint Potenciális Banki Ügyfelek Körében. Ph.D. Thesis, University of Sopron, Sopron, Hungary, 2015. [Google Scholar] [CrossRef]

- Furnham, A.; Kirkcaldy, B.D.; Lynn, R. National Attitudes to Competitiveness, Money, and Work Among Young People: First, Second, and Third World Differences. Hum. Relat. 1994, 47, 119–132. [Google Scholar] [CrossRef]

- Schervish, P.G.; Furnham, A.; Argyle, M. The Psychology of Money. Contemp. Sociol. A J. Rev. 2001, 30, 166. [Google Scholar] [CrossRef]

- Ivan, B.; Dickson, L. Consumer Economic Socialization. In Handbook of Consumer Finance Research; Metzler, J.B., Ed.; Springer: Cham, Switzerland, 2008; pp. 83–102. [Google Scholar]

- Furnham, A.; Wilson, E.; Telford, K. The meaning of money: The validation of a short money-types measure. Pers. Individ. Differ. 2012, 52, 707–711. [Google Scholar] [CrossRef]

- Tang, T.L.-P. The development of a short Money Ethic Scale: Attitudes toward money and pay satisfaction revisited. Pers. Individ. Differ. 1995, 19, 809–816. [Google Scholar] [CrossRef]

- Tsang, S.; Royse, C.F.; Terkawi, A.S. Guidelines for developing, translating, and validating a questionnaire in perioperative and pain medicine. Saudi J. Anaesth. 2017, 11, S80–S89. [Google Scholar] [CrossRef] [PubMed]

- Irwing, P.; Hughes, D.J. Test development. In The Wiley Handbook of Psychometric Testing: A Multidisciplinary Reference on Survey, Scale and Test Development; Wiley-Blackwell: Hoboken, NJ, USA, 2018; pp. 1–47. [Google Scholar]

- De Andrade, F.W.M.; Thomas, L.C. Structural Models in Consumer Credit. SSRN Electron. J. 2004, 183, 1569–1581. [Google Scholar] [CrossRef]

- Belas, J.; Smrcka, L.; Gavurova, B.; Dvorsky, J. The Impact of Social and Economic Factors in The Credit Risk Management of Sme. Technol. Econ. Dev. Econ. 2018, 24, 1215–1230. [Google Scholar] [CrossRef] [Green Version]

- Dirick, L.; Bellotti, T.; Claeskens, G.; Baesens, B. Macro-Economic Factors in Credit Risk Calculations: Including Time-Varying Covariates in Mixture Cure Models. J. Bus. Econ. Stat. 2017, 37, 40–53. [Google Scholar] [CrossRef]

- Arslan, Ö.; Karan, M.B. Consumer Credit Risk Characteristics: Understanding Income and Expense Differentials. Emerg. Mark. Financ. Trade 2010, 46, 20–37. [Google Scholar] [CrossRef]

- Connelly, L. Logistic regression. Medsurg. Nurs. 2020, 29, 353–354. [Google Scholar]

- Caspi, A.; Roberts, B.W.; Shiner, R.L. Personality Development: Stability and Change. Annu. Rev. Psychol. 2005, 56, 453–484. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Test Developing Method 1 [51] | Test Developing Method 2 [52] |

|---|---|

| Construct definition, specification of test need, test structure. Overall planning. Item development. Construct definition. Item generation: theory versus sampling. Item review. Piloting of items. Scale construction-factor analysis and Item Response Theory (IRT). Reliability. Validation. Test scoring and norming. Test specification. Implementation and testing. Technical Manual. |

| Subscales | Number of Items | Cronbach’s Alpha |

|---|---|---|

| EDM | 21 | 0.913 |

| SCR | 16 | 0.763 |

| CON | 18 | 0.698 |

| SGA | 16 | 0.694 |

| NRT | 15 | 0.677 |

| ATM | 25 | 0.873 |

| Hypothesis | Question | Answer | Point |

|---|---|---|---|

| Effective financial Decision-Making | |||

| H1 |

|

| −2 |

| −1 | ||

| 1 | ||

| 2 | ||

|

| −2 | |

| −1 | ||

| 1 | ||

| 2 | ||

| Self-control | |||

| H2 |

|

| −2 |

| −1 | ||

| 1 | ||

| 2 | ||

|

| −2 | |

| −1 | ||

| 1 | ||

| 2 | ||

| Conscientiousness | |||

| H3 |

|

| −2 |

| −1 | ||

| 1 | ||

| 2 | ||

|  | −2 | |

| −1 | ||

| 1 | ||

| 2 | ||

| Selflessness and giving (charitable) attitude | |||

| H4 |

|

| −2 |

| −1 | ||

| 1 | ||

| 2 | ||

|

| −2 | |

| −1 | ||

| 1 | ||

| 2 | ||

| Neuroticism | |||

| H5 |

|

| −2 |

| −1 | ||

| 1 | ||

| 2 | ||

|

| −2 | |

| −1 | ||

| 1 | ||

| 2 | ||

| Attitude towards the money | |||

| H6 |

|

| −2 |

| −1 | ||

| 1 | ||

| 2 | ||

|

| −2 | |

| −1 | ||

| 1 | ||

| 2 | ||

| Variables | Mean | Std. Dev. | Min | 25% | 50% | 75% | Max |

|---|---|---|---|---|---|---|---|

| Dependent variable | |||||||

| Credit Risk | 0.75 | 0.43 | 0 | 1 | 1 | 1 | 1 |

| Psychological variables | |||||||

| EDM | 3.38 | 3.31 | −7 | 1.5 | 4 | 6 | 9.5 |

| SCR | 3.33 | 4.83 | −10 | 0 | 2.5 | 7.5 | 10 |

| CON | 3.65 | 4.53 | −10 | 0 | 5 | 7.5 | 10 |

| SGA | 2.46 | 3.77 | −7 | −0.5 | 3.5 | 6 | 7 |

| NRT | −0.23 | 2.17 | −4 | −2 | 0 | 1 | 4 |

| ATM | 1.20 | 1.89 | −4 | 0 | 1 | 3 | 4 |

| Items | Loading | Items | Loading | Items | Loading | |||

|---|---|---|---|---|---|---|---|---|

| EDM | SCR | CON | ||||||

| Q101 | 0.748 | 0.559 | Q201 | 0.705 | 0.497 | Q301 | 0.811 | 0.658 |

| Q102 | 0.754 | 0.568 | Q202 | 0.733 | 0.537 | Q302 | 0.779 | 0.607 |

| Q103 | 0.791 | 0.626 | Q203 | 0.722 | 0.521 | Q303 | 0.809 | 0.655 |

| Q104 | 0.779 | 0.606 | Q204 | 0.790 | 0.624 | Q304 | 0.768 | 0.590 |

| Q105 | 0.808 | 0.654 | Q205 | 0.664 | 0.441 | Q305 | 0.689 | 0.475 |

| Q106 | 0.796 | 0.634 | Q206 | 0.756 | 0.572 | Q306 | 0.715 | 0.512 |

| Q107 | 0.785 | 0.616 | Q207 | 0.731 | 0.534 | Q307 | 0.694 | 0.481 |

| Q108 | 0.862 | 0.743 | Q208 | 0.750 | 0.562 | Q308 | 0.806 | 0.650 |

| Q109 | 0.781 | 0.610 | Q209 | 0.758 | 0.574 | Q309 | 0.793 | 0.629 |

| Q110 | 0.864 | 0.746 | Q210 | 0.717 | 0.514 | Q310 | 0.738 | 0.545 |

| Q111 | 0.809 | 0.654 | Q211 | 0.736 | 0.541 | Q311 | 0.778 | 0.606 |

| Q112 | 0.799 | 0.639 | Q212 | 0.770 | 0.593 | Q312 | 0.770 | 0.593 |

| Q113 | 0.882 | 0.777 | Q213 | 0.768 | 0.590 | Q313 | 0.782 | 0.611 |

| Q114 | 0.776 | 0.602 | Q214 | 0.752 | 0.566 | Q314 | 0.789 | 0.623 |

| Q115 | 0.877 | 0.769 | Q215 | 0.720 | 0.519 | Q315 | 0.744 | 0.553 |

| Q116 | 0.771 | 0.595 | Q216 | 0.712 | 0.506 | Q316 | 0.775 | 0.601 |

| Q117 | 0.797 | 0.635 | Q317 | 0.716 | 0.513 | |||

| Q118 | 0.777 | 0.604 | Q318 | 0.787 | 0.619 | |||

| Q119 | 0.671 | 0.451 | ||||||

| Q120 | 0.796 | 0.633 | ||||||

| Q121 | 0.786 | 0.617 | ||||||

| SGA | NRT | ATM | ||||||

| Q401 | 0.722 | 0.522 | Q501 | 0.745 | 0.555 | Q601 | 0.801 | 0.641 |

| Q402 | 0.742 | 0.550 | Q502 | 0.823 | 0.677 | Q602 | 0.836 | 0.699 |

| Q403 | 0.650 | 0.422 | Q503 | 0.624 | 0.390 | Q603 | 0.808 | 0.653 |

| Q404 | 0.766 | 0.586 | Q504 | 0.825 | 0.681 | Q604 | 0.767 | 0.588 |

| Q405 | 0.754 | 0.568 | Q505 | 0.737 | 0.544 | Q605 | 0.840 | 0.705 |

| Q406 | 0.775 | 0.601 | Q506 | 0.818 | 0.670 | Q606 | 0.786 | 0.618 |

| Q407 | 0.771 | 0.595 | Q507 | 0.681 | 0.463 | Q607 | 0.804 | 0.647 |

| Q408 | 0.743 | 0.552 | Q508 | 0.586 | 0.343 | Q608 | 0.777 | 0.604 |

| Q409 | 0.652 | 0.425 | Q509 | 0.720 | 0.518 | Q609 | 0.856 | 0.733 |

| Q410 | 0.786 | 0.618 | Q510 | 0.695 | 0.484 | Q610 | 0.773 | 0.598 |

| Q411 | 0.779 | 0.606 | Q511 | 0.790 | 0.624 | Q611 | 0.819 | 0.671 |

| Q412 | 0.728 | 0.530 | Q512 | 0.599 | 0.359 | Q612 | 0.805 | 0.648 |

| Q413 | 0.729 | 0.532 | Q513 | 0.788 | 0.621 | Q613 | 0.850 | 0.723 |

| Q414 | 0.715 | 0.511 | Q514 | 0.620 | 0.384 | Q614 | 0.850 | 0.722 |

| Q415 | 0.731 | 0.535 | Q515 | 0.649 | 0.422 | Q615 | 0.854 | 0.729 |

| Q416 | 0.732 | 0.536 | Q616 | 0.860 | 0.739 | |||

| Q617 | 0.851 | 0.723 | ||||||

| Q618 | 0.850 | 0.722 | ||||||

| Q619 | 0.825 | 0.681 | ||||||

| Q620 | 0.852 | 0.727 | ||||||

| Q621 | 0.844 | 0.713 | ||||||

| Q622 | 0.846 | 0.716 | ||||||

| Q623 | 0.859 | 0.738 | ||||||

| Q624 | 0.841 | 0.708 | ||||||

| Q625 | 0.856 | 0.733 | ||||||

| Variable | B | S.E. | Wald | Significance | Low Conf. | High Conf. |

|---|---|---|---|---|---|---|

| EDM | 0.096 | 0.017 | 5.670 | 0.000 | 0.062 | 0.129 |

| SCR | 0.053 | 0.013 | 4.125 | 0.000 | 0.028 | 0.078 |

| CON | 0.054 | 0.013 | 4.135 | 0.000 | 0.029 | 0.08 |

| SGA | 0.068 | 0.016 | 4.155 | 0.000 | 0.036 | 0.100 |

| NRT | −0.062 | 0.032 | −1.955 | 0.051 | −0.125 | 0.000 |

| ATM | 0.104 | 0.034 | 3.067 | 0.002 | 0.037 | 0.170 |

| Hypothesis | Relationship | Result |

|---|---|---|

| H1 | The ability to make efficient economic decisions is significant in predicting the borrower’s risk. | Supported |

| H2 | Self-control has a significant impact on timely debt payment. | Supported |

| H3 | A conscientious personality significantly reduces the risk of having overdue credit. | Supported |

| H4 | Charitable attitude and selfless personality significantly/positively affect the loan risk. | Supported |

| H5 | Neurosis significantly affects loan defaults. | Not supported |

| H6 | A positive attitude towards money positively affects the loan risk. | Supported |

| Category | EDM | SCR | CON | SGA | NRT | ATM |

|---|---|---|---|---|---|---|

| Salary ≤ 800 K | 0.082 * | 0.058 * | 0.026 | 0.091 ** | −0.12 | 0.094 |

| 800 K < Salary ≤ 1.2 M | 0.122 *** | 0.063 ** | 0.103 *** | 0.036 | −0.071 | 0.054 |

| 1.2 M < Salary ≤ 2 M | 0.069 * | 0.033 | 0.036 | 0.081 ** | 0.001 | 0.137 * |

| Salary > 2 M | 0.135 | 0.102 | 0.040 | 0.138 | −0.178 | 0.304 |

| Extra income = 0 | 0.051 | 0.019 | 0.092 *** | 0.124 *** | −0.066 | 0.230 ** |

| Extra income ≤ 400 K | 0.113 *** | 0.055 ** | 0.044 * | 0.044 | −0.071 | 0.065 |

| 400 K < Extra income ≤ 800 K | 0.125 *** | 0.036 | 0.059 * | 0.061 | −0.028 | 0.032 |

| Extra income > 800 K | 0.089 | 0.17 *** | 0.009 | 0.037 | −0.167 | 0.245 * |

| Salary loan = No | 0.101 *** | 0.042 * | 0.069 *** | 0.059 ** | −0.061 | 0.139 ** |

| Salary loan = Yes | 0.088 *** | 0.068 *** | 0.036 | 0.082 *** | −0.065 | 0.057 |

| NBFI loan = No | 0.109 *** | 0.052 * | 0.055 * | 0.061 * | −0.039 | 0.122 * |

| NBFI loan = Yes | 0.087 *** | 0.055 *** | 0.054 ** | 0.071 *** | −0.076 | 0.094 * |

| Previous NBFI loan = No | 0.100** | 0.027 | 0.088 ** | 0.020 | −0.017 | 0.159 * |

| Previous NBFI loan = Yes | 0.095 *** | 0.062 *** | 0.043 ** | 0.082 *** | −0.081 * | 0.090 * |

| Mortgage loan = No | 0.067 | 0.060 | 0.102 * | 0.067 | −0.095 | 0.159 |

| Mortgage loan = Yes | 0.098 *** | 0.053 *** | 0.05 *** | 0.067 *** | −0.061 | 0.100 ** |

| Monthly payment = 0 | 0.091 ** | 0.013 | 0.067 ** | 0.055 | −0.068 | 0.16 * |

| Monthly payment ≤ 300 K | 0.107 ** | 0.086 *** | 0.046 | 0.093 ** | −0.15 * | 0.062 |

| 300 K < Monthly payment ≤ 500 K | 0.114 *** | 0.072 ** | 0.055 * | 0.049 | −0.028 | 0.140 * |

| Monthly payment > 500 K | 0.073 * | 0.049 | 0.056 * | 0.092 ** | −0.013 | 0.018 |

| Real estate = No | 0.091 *** | 0.052 *** | 0.055 *** | 0.062 *** | −0.078 * | 0.105 ** |

| Real estate = Yes | 0.275 ** | 0.031 | 0.034 | 0.166 * | 0.397 | 0.170 |

| Real estate price ≤ 20 M | 0.090 *** | 0.059 *** | 0.058 *** | 0.087 *** | −0.126 ** | 0.106 * |

| 20 M < Real estate price ≤ 50 M | 0.130 *** | 0.045 | 0.039 | 0.023 | 0.084 | 0.148 |

| 50 M < Real estate price ≤ 80 M | 0.028 | 0.043 | 0.076 * | 0.055 | −0.061 | 0.172 |

| Real estate price > 80 M | 0.159 ** | 0.033 | 0.044 | 0.093 | −0.027 | 0.050 |

| Car = No | 0.027 | 0.073 | 0.080 | 0.006 | −0.205 | 0.067 |

| Car = Yes | 0.102 *** | 0.052 *** | 0.051 *** | 0.074 *** | −0.048 | 0.112 ** |

| Car price ≤ 8 M | 0.089 *** | 0.059 ** | 0.056 ** | 0.060 ** | −0.137 ** | 0.064 |

| 8 M < Car price ≤ 13 M | 0.095 ** | 0.031 | 0.039 | 0.111 *** | −0.028 | 0.144 * |

| 13 M < Car price ≤ 18 M | 0.097 | 0.040 | 0.079 | 0.042 | 0.082 | 0.135 |

| Car price > 18 M | 0.212 * | 0.114 | 0.054 | −0.093 | 0.017 | 0.253 |

| Life year ≤ 3 | 0.071 | 0.098 * | 0.066 | 0.031 | 0.003 | 0.212 * |

| 3 < Life year ≤ 6 | 0.074 * | 0.038 | 0.068 ** | 0.061 * | −0.023 | 0.083 |

| 6 < Life year ≤ 10 | 0.15 *** | 0.039 | 0.000 | 0.083* | −0.057 | 0.139 |

| Life year > 10 | 0.095 *** | 0.059 ** | 0.062 ** | 0.074 ** | −0.091 | 0.075 |

| Age ≤ 22 | 0.505 | 0.319 | −0.028 | −0.001 | 0.192 | −0.659 |

| 22 < Age ≤ 30 | 0.033 | 0.112 ** | 0.058 | 0.071 | −0.183 * | 0.158 |

| 30 < Age ≤ 50 | 0.106 *** | 0.030 * | 0.053 *** | 0.074 *** | −0.047 | 0.088 * |

| Age > 50 | 0.102 * | 0.111 ** | 0.050 | 0.014 | 0.032 | 0.196 * |

| Sex = Female | 0.106 *** | 0.078 *** | 0.037 | 0.058 * | −0.091 | 0.114 * |

| Sex = Male | 0.088 *** | 0.028 | 0.073 *** | 0.076 *** | −0.044 | 0.091 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ganbat, M.; Batbaatar, E.; Bazarragchaa, G.; Ider, T.; Gantumur, E.; Dashkhorol, L.; Altantsatsralt, K.; Nemekh, M.; Dashdondog, E.; Namsrai, O.-E. Effect of Psychological Factors on Credit Risk: A Case Study of the Microlending Service in Mongolia. Behav. Sci. 2021, 11, 47. https://0-doi-org.brum.beds.ac.uk/10.3390/bs11040047

Ganbat M, Batbaatar E, Bazarragchaa G, Ider T, Gantumur E, Dashkhorol L, Altantsatsralt K, Nemekh M, Dashdondog E, Namsrai O-E. Effect of Psychological Factors on Credit Risk: A Case Study of the Microlending Service in Mongolia. Behavioral Sciences. 2021; 11(4):47. https://0-doi-org.brum.beds.ac.uk/10.3390/bs11040047

Chicago/Turabian StyleGanbat, Mandukhai, Erdenebileg Batbaatar, Ganzul Bazarragchaa, Togtuunaa Ider, Enkhjargalan Gantumur, Lkhamsuren Dashkhorol, Khosgarig Altantsatsralt, Mandakhbayar Nemekh, Erdenebaatar Dashdondog, and Oyun-Erdene Namsrai. 2021. "Effect of Psychological Factors on Credit Risk: A Case Study of the Microlending Service in Mongolia" Behavioral Sciences 11, no. 4: 47. https://0-doi-org.brum.beds.ac.uk/10.3390/bs11040047