Are Environmentally Innovative Companies Inclined towards Integrated Environmental Disclosure Policies?

Abstract

:1. Introduction

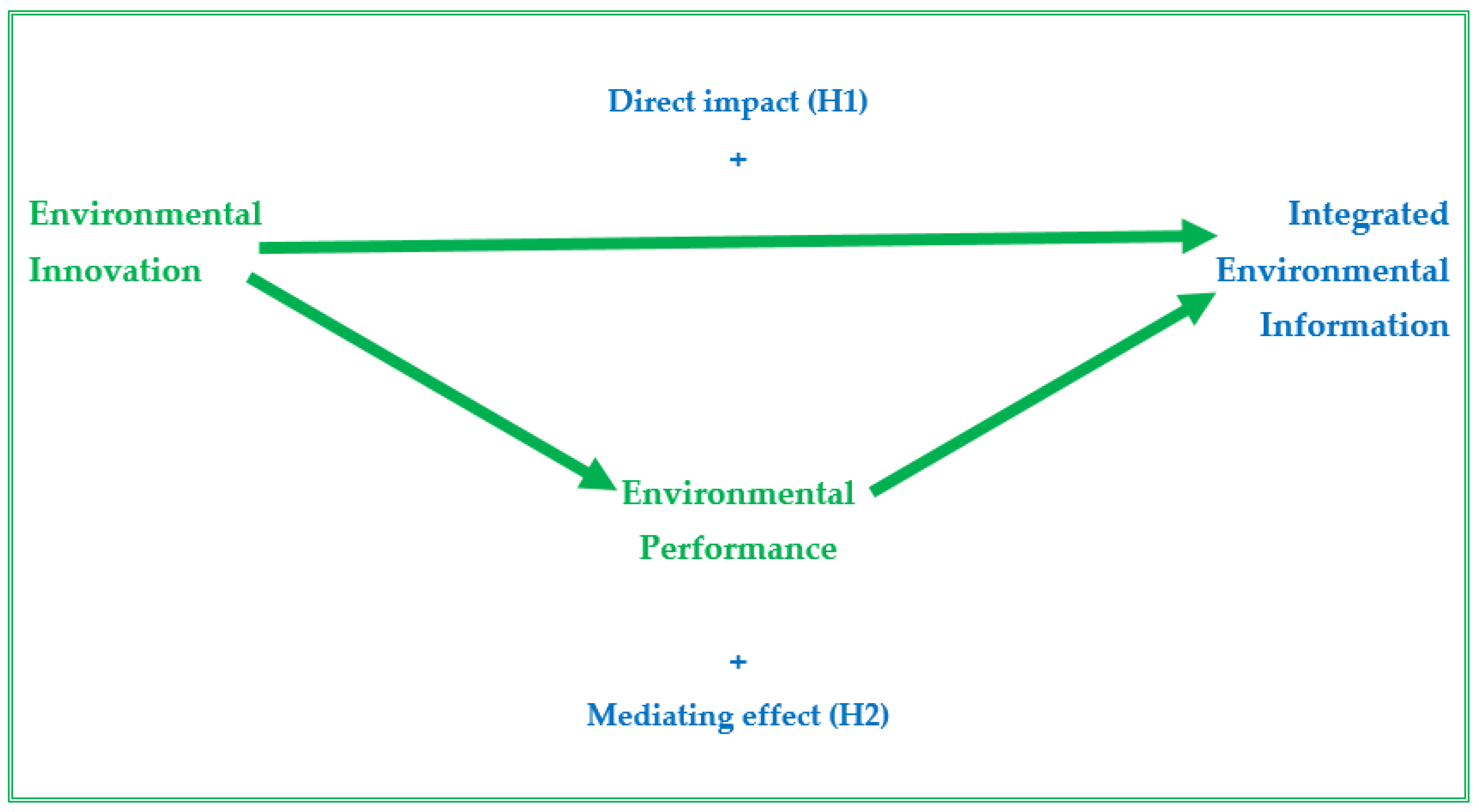

2. Background, Theory and Research Hypotheses

2.1. Environmental Innovation and Environmental Disclosure

2.2. Theory and Hypotheses Development

3. Methodology

3.1. Sample

3.2. Empirical Models

4. Results and Discussion

4.1. Descriptive Statistics

4.2. Basic Model Results

4.3. Complementary Analysis

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Alazzani, Abdulsamad, and Wan Nordin Wan-Hussin. 2013. Global Reporting Initiative’s environmental reporting: A study of oil and gas companies. Ecological Indicators 32: 19–24. [Google Scholar] [CrossRef]

- Albino, Vito, Azzurra Balice, and Rosa Maria Dangelico. 2009. Environmental strategies and green product development: An overview on sustainability-driven companies. Business Strategy and the Environment 18: 83–96. [Google Scholar] [CrossRef]

- Al-Tuwaijri, Sulaiman A., Theodore E. Christensen, and K. E. Hughes II. 2004. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Accounting, Organizations and Society 29: 447–71. [Google Scholar] [CrossRef]

- Ambec, Stefan, and Paul Lanoie. 2008. Does it pay to be green? A systematic overview. The Academy of Management Perspectives 22: 45–62. [Google Scholar]

- Amorelli, María-Florencia, and Isabel-María García-Sánchez. 2020. Trends in the dynamic evolution of board gender diversity and corporate social responsibility. Corporate Social Responsibility and Environmental Management 28: 537–54. [Google Scholar] [CrossRef]

- Amor-Esteban, Victor, María Purificación Galindo-Villardón, and Isabel-María García-Sánchez. 2018. Useful information for stakeholder engagement: A multivariate proposal of an Industrial Corporate Social Responsibility Practices Index. Sustainable Development 26: 620–37. [Google Scholar] [CrossRef]

- Amor-Esteban, Victor, María Purificación Galindo-Villardón, Isabel-María García-Sánchez, and Fátima David. 2019. An extension of the industrial corporate social responsibility practices index: New information for stakeholder engagement under a multivariate approach. Corporate Social Responsibility and Environmental Management 26: 127–40. [Google Scholar] [CrossRef]

- Baalouch, Fatma, Salma Damak Ayadi, and Khaled Hussainey. 2019. A study of the determinants of environmental disclosure quality: Evidence from French listed companies. Journal of Management and Governance 23: 939–971. [Google Scholar] [CrossRef] [Green Version]

- Bennett, Martin, and Peter James. 1998. The Green Bottom Line: Current Practice and Future Trends in Environmental Management Accounting. Sheffield: Greenleaf Publishing. [Google Scholar]

- Bewley, Kathryn, and Yue Li. 2000. Disclosure of environmental information by Canadian manufacturing companies: A voluntary disclosure perspective. In Advances in Environmental Accounting & Management. Bingley: Emerald Group Publishing Limited, pp. 201–26. [Google Scholar]

- Blättel-Mink, Birgit. 1998. Innovation towards sustainable economy-the integration of economy and ecology in companies. Sustainable Development 6: 49–58. [Google Scholar] [CrossRef]

- Brammer, Stephen, and Stephen Pavelin. 2008. Factors influencing the quality of corporate environmental disclosure. Business Strategy and the Environment 17: 120–36. [Google Scholar] [CrossRef]

- Buniamin, Sharifah. 2010. The quantity and quality of environmental reporting in annual report of public listed companies in Malaysia. Issues in Social and Environmental Accounting 4: 115–35. [Google Scholar] [CrossRef]

- Burritt, Roger L. 2002. Environmental reporting in Australia: Current practices and issues for the future. Business Strategy and the Environment 11: 391–406. [Google Scholar] [CrossRef]

- Carrión-Flores, Carmen E., and Robert Innes. 2010. Environmental innovation and environmental performance. Journal of Environmental Economics and Management 59: 27–42. [Google Scholar] [CrossRef]

- Cecere, Grazia, Nicoletta Corrocher, Cédric Gossart, and Muge Ozman. 2014. Lock-in and path dependence: An evolutionary approach to eco-innovations. Journal of Evolutionary Economics 24: 1037–65. [Google Scholar] [CrossRef]

- Chen, Yu-Shan. 2008. The driver of green innovation and green image–green core competence. Journal of Business Ethics 81: 531–43. [Google Scholar] [CrossRef]

- Chiou, Tzu-Yun, Hing Kai Chan, Fiona Lettice, and Sai Ho Chung. 2011. The influence of greening the suppliers and green innovation on environmental performance and competitive advantage in Taiwan. Transportation Research Part E: Logistics and Transportation Review 47: 822–36. [Google Scholar] [CrossRef]

- Clarkson, Peter M., Yue Li, Gordon D. Richardson, and Florin P. Vasvari. 2008. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organizations and Society 33: 303–27. [Google Scholar] [CrossRef]

- Cormier, Denis, Michel Magnan, and Barbara Van Velthoven. 2005. Environmental disclosure quality in large German companies: Economic incentives, public pressures or institutional conditions? European Accounting Review 14: 3–39. [Google Scholar] [CrossRef]

- Dawkins, Cedric E., and John W. Fraas. 2011. Erratum to: Beyond acclamations and excuses: Environmental performance, voluntary environmental disclosure and the role of visibility. Journal of Business Ethics 99: 383–97. [Google Scholar] [CrossRef]

- Del Río, Pablo, Javier Carrillo-Hermosilla, and Totti Könnölä. 2010. Policy strategies to promote eco-innovation: An integrated framework. Journal of Industrial Ecology 14: 541–57. [Google Scholar] [CrossRef]

- Delmas, Magali A., and Vanessa Cuerel Burbano. 2011. The drivers of greenwashing. California Management Review 54: 64–87. [Google Scholar] [CrossRef] [Green Version]

- Dye, Ronald A. 1985. Disclosure of nonproprietary information. Journal of Accounting Research 23: 123–45. [Google Scholar] [CrossRef]

- Dye, Ronald A. 2001. An evaluation of “essays on disclosure” and the disclosure literature in accounting. Journal of Accounting and Economics 32: 181–235. [Google Scholar] [CrossRef]

- Dyllick, Thomas, and Kai Hockerts. 2002. Beyond the business case for corporate sustainability. Business Strategy and the Environment 11: 130–41. [Google Scholar] [CrossRef]

- Eco-Innovation Observatory. 2016. Policies and Practices for Eco-Innovation Up-Take and Circular Economy Transition. Available online: https://ec.europa.eu/environment/ecoap/policies-and-practices-eco-innovation-uptake-and-circular-economy-transition_en (accessed on 15 February 2021).

- Eiadat, Yousef, Aidan Kelly, Frank Roche, and Hussein Eyadat. 2008. Green and competitive? An empirical test of the mediating role of environmental innovation strategy. Journal of World Business 43: 131–45. [Google Scholar] [CrossRef]

- Epstein, Marc J., and Martin Freedman. 1994. Social disclosure and the individual investor. Accounting, Auditing & Accountability Journal 7: 94–109. [Google Scholar]

- Esty, Daniel C., and Micheal E. Porter. 2001. Ranking national environmental regulation and performance: A leading indicator of future competitiveness? The Global Competitiveness Report 2002: 78–100. [Google Scholar]

- Esty, Daniel C., and Andrew Winston. 2009. Green to Gold: How Smart Companies Use Environmental Strategy to Innovate, Create Value, and Build Competitive Advantage. Hoboken: John Wiley & Sons. [Google Scholar]

- Flammer, Caroline. 2013. Corporate social responsibility and shareholder reaction: The environmental awareness of investors. Academy of Management Journal 56: 758–81. [Google Scholar] [CrossRef] [Green Version]

- Fondevila, Miguel Marco, José M. Moneva, and Sabina Scarpellini. 2019. Environmental disclosure and Eco-innovation interrelation. The case of Spanish firms. Revista de Contabilidad-Spanish Accounting Review 22: 73–87. [Google Scholar]

- Forsman, Helena. 2013. Environmental innovations as a source of competitive advantage or vice versa? Business Strategy and the Environment 22: 306–20. [Google Scholar] [CrossRef]

- Frías-Aceituno, José-Valeriano, and Beatriz Aibar-Gúzman. 2021. Is It Necessary to Centralize Power in The CEO To Ensure Environmental Innovation? Administrative Sciences. forthcoming. [Google Scholar]

- Frías-Aceituno, José-Valeriano, Lázaro Rodríguez-Ariza, and Isabel-María García-Sánchez. 2013a. Is integrated reporting determined by a country’s legal system? An exploratory study. Journal of Cleaner Production 44: 45–55. [Google Scholar] [CrossRef]

- Frías-Aceituno, José-Valeriano, Lázaro Rodriguez-Ariza, and Isabel-María García-Sánchez. 2013b. The role of the board in the dissemination of integrated corporate social reporting. Corporate Social Responsibility and Environmental Management 20: 219–33. [Google Scholar] [CrossRef]

- Frías-Aceituno, José-Valeriano, Lázaro Rodríguez-Ariza, and Isabel-María García-Sánchez. 2014. Explanatory factors of integrated sustainability and financial reporting. Business Strategy and the Environment 23: 56–72. [Google Scholar] [CrossRef]

- Frondel, Manuel, Jens Horbach, and Klaus Rennings. 2007. End-of-pipe or cleaner production? An empirical comparison of environmental innovation decisions across OECD countries. Business Strategy and the Environment 16: 571–84. [Google Scholar] [CrossRef] [Green Version]

- Frondel, Manuel, Jens Horbach, and Klaus Rennings. 2008. What triggers environmental management and innovation? Empirical evidence for Germany. Ecological Economics 66: 153–60. [Google Scholar] [CrossRef] [Green Version]

- Garcés-Ayerbe, Concepción, Sabina Scarpellini, Jesus Valero-Gil, and Pilar Rivera-Torres. 2016. Proactive environmental strategy development: From laggard to eco-innovative firms. Journal of Organizational Change Management 29: 1118–34. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, and Ligia Noguera-Gámez. 2017a. Integrated reporting and stakeholder engagement: The effect on information asymmetry. Corporate Social Responsibility and Environmental Management 24: 395–413. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, and Ligia Noguera-Gámez. 2017b. Integrated information and the cost of capital. International Business Review 26: 959–75. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, and Ligia Noguera-Gámez. 2018. Institutional investor protection pressures versus firm incentives in the disclosure of integrated reporting. Australian Accounting Review 28: 199–219. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Lázaro Rodríguez-Ariza, and José-Valeriano Frías-Aceituno. 2013. The cultural system and integrated reporting. International Business Review 22: 828–38. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Jennifer Martínez-Ferrero, and María Antonia García-Benau. 2019. Integrated reporting: The mediating role of the board of directors and investor protection on managerial discretion in munificent environments. Corporate Social Responsibility and Environmental Management 26: 29–45. [Google Scholar] [CrossRef] [Green Version]

- García-Sánchez, Isabel-María, Nicola Raimo, and Filippo Vitolla. 2020a. CEO power and integrated reporting. Meditari Accountancy Research. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Nazim Hussain, Sana-Akbar Khan, and Jennifer Martínez-Ferrero. 2020b. Do Markets Punish or Reward Corporate Social Responsibility Decoupling? Business & Society. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Cristina Aibar-Guzmán, and Beatriz Aibar-Guzmán. 2020c. The effect of institutional ownership and ownership dispersion on eco-innovation. Technological Forecasting and Social Change 1158: 120173. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Isabel Gallego-Álvarez, and José-Luis Zafra-Gómez. 2020d. Do the ecoinnovation and ecodesign strategies generate value added in munificent environments? Business Strategy and the Environment 29: 1021–33. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Beatriz Aibar-Guzmán, Cristina Aibar-Guzmán, and Tânia-Cristina Azevedo. 2020e. CEO ability and sustainability disclosures: The mediating effect of corporate social responsibility performance. Corporate Social Responsibility and Environmental Management 27: 1565–77. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Nicola Raimo, Arcangelo Marrone, and Filippo Vitolla. 2020f. How does integrated reporting change in light of COVID-19? A Revisiting of the content of the integrated reports. Sustainability 12: 7605. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel-María, Lázaro Rodríguez-Ariza, and María-del-Carmen Granada-Abarzuza. 2021. The Influence of Female Directors and Institutional Pressures on Corporate Social Responsibility in Family Firms in Latin America. Journal of Risk and Financial Management 14: 28. [Google Scholar] [CrossRef]

- Giannarakis, Grigoris, George Konteos, Nikolaos Sariannidis, and George Chaitidis. 2017. The relation between voluntary carbon disclosure and environmental performance: The case of S&P 500. International Journal of Law and Management 59: 784–803. [Google Scholar]

- Giannarakis, Grigoris, Andreas Andronikidis, and Nikolaos Sariannidis. 2019. Determinants of environmental disclosure: Investigating new and conventional corporate governance characteristics. Annals of Operations Research 294: 87–105. [Google Scholar] [CrossRef]

- Healy, Paul M., and Krishna G. Palepu. 2001. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics 31: 405–40. [Google Scholar] [CrossRef]

- Herremans, Irene M., Parporn Akathaporn, and Morris McInnes. 1993. An investigation of corporate social responsibility reputation and economic performance. Accounting, Organizations and Society 18: 587–604. [Google Scholar] [CrossRef]

- Ho, Elaine, Sondra Eger, and Simon C. Courtenay. 2018. Assessing current monitoring indicators and reporting for cumulative effects integration: A case study in Muskoka, Ontario, Canada. Ecological Indicators 95: 862–76. [Google Scholar] [CrossRef]

- Hojnik, Jana, and Mitja Ruzzier. 2016. What drives eco-innovation? A review of an emerging literature. Environmental Innovation and Societal Transitions 19: 31–41. [Google Scholar] [CrossRef]

- Huang, Rongbing, and Danping Chen. 2015. Does environmental information disclosure benefit waste discharge reduction? Evidence from China. Journal of Business Ethics 129: 535–52. [Google Scholar] [CrossRef]

- Huang, Cheng-Li, and Fan-Hua Kung. 2010. Drivers of environmental disclosure and stakeholder expectation: Evidence from Taiwan. Journal of Business Ethics 96: 435–51. [Google Scholar] [CrossRef]

- Jitmaneeroj, Boonlert. 2016. Reform priorities for corporate sustainability. Management Decision 54: 1497–521. [Google Scholar] [CrossRef]

- Junior, Flavio Hourneaux, Barbara Galleli, Dolores Gallardo-Vázquez, and Maria Isabel Sánchez-Hernández. 2017. Strategic aspects in sustainability reporting in oil & gas industry: The comparative case-study of Brazilian Petrobras and Spanish Repsol. Ecological Indicators 72: 203–14. [Google Scholar]

- Kaplan, Steven N., and Luigi Zingales. 1997. Do investment-cash flow sensitivities provide useful measures of financing constraints? The Quarterly Journal of Economics 112: 169–215. [Google Scholar] [CrossRef] [Green Version]

- Kemp, René, and Vanessa Oltra. 2011. Research insights and challenges on eco-innovation dynamics. Industry and Innovation 18: 249–53. [Google Scholar] [CrossRef]

- Kemp, René, and Peter Pearson. 2007. Final Report MEI Project about Measuring Eco-Innovation. Maastricht: UM Merit, vol. 10. [Google Scholar]

- Kemp, René, and Serena Pontoglio. 2011. The innovation effects of environmental policy instruments—A typical case of the blind men and the elephant? Ecological Economics 72: 28–36. [Google Scholar] [CrossRef]

- Konadu, Renata, Samuel Owusu-Agyei, Theophilus A. Lartey, Albert Danso, Samuel Adomako, and Joseph Amankwah-Amoah. 2020. CEOs’ reputation, quality management and environmental innovation: The roles of stakeholder pressure and resource commitment. Business Strategy and the Environment 29: 2310–23. [Google Scholar] [CrossRef]

- Kuo, Lopin, and Vivian Yi-Ju Chen. 2013. Is environmental disclosure an effective strategy on establishment of environmental legitimacy for organization? Management Decision 51: 1462–87. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert W. Vishny. 1998. Law and finance. Journal of Political Economy 106: 1113–55. [Google Scholar] [CrossRef]

- Lee, Ki-Hoon, and Byung Min. 2015. Green R&D for eco-innovation and its impact on carbon emissions and firm performance. Journal of Cleaner Production 108: 534–42. [Google Scholar]

- Li, Yue, Gordon D. Richardson, and Daniel B. Thornton. 1997. Corporate disclosure of environmental liability information: Theory and evidence. Contemporary Accounting Research 14: 435–74. [Google Scholar] [CrossRef]

- Liao, Zhongju. 2016. Temporal cognition, environmental innovation, and the competitive advantage of enterprises. Journal of Cleaner Production 135: 1045–53. [Google Scholar] [CrossRef]

- Long, Xingle, Yaqiong Chen, Jianguo Du, Keunyeob Oh, and Insoo Han. 2017. Environmental innovation and its impact on economic and environmental performance: Evidence from Korean-owned firms in China. Energy Policy 107: 131–37. [Google Scholar] [CrossRef]

- Luo, Le, and Qingliang Tang. 2014. Does voluntary carbon disclosure reflect underlying carbon performance? Journal of Contemporary Accounting & Economics 10: 191–205. [Google Scholar]

- Martínez-Ferrero, Jennifer, David Ruiz-Cano, and Isabel-María García-Sánchez. 2016. The causal link between sustainable disclosure and information asymmetry: The moderating role of the stakeholder protection context. Corporate Social Responsibility and Environmental Management 23: 319–32. [Google Scholar] [CrossRef]

- Mirata, Murat, and Tareq Emtairah. 2005. Industrial symbiosis networks and the contribution to environmental innovation: The case of the Landskrona industrial symbiosis programme. Journal of Cleaner Production 13: 993–1002. [Google Scholar] [CrossRef]

- Nyquist, Siv. 2003. The legislation of environmental disclosures in three Nordic countries—A comparison. Business Strategy and the Environment 12: 12–25. [Google Scholar] [CrossRef]

- O’Dwyer, Brendan. 2003. The ponderous evolution of corporate environmental reporting in Ireland. Recent evidence from publicly listed companies. Corporate Social Responsibility and Environmental Management 10: 91–100. [Google Scholar] [CrossRef]

- Odoemelam, Ndubuisi, and Regina G. Okafor. 2018. The influence of corporate governance on environmental disclosure of listed non-financial firms in Nigeria. Indonesian Journal of Sustainability Accounting and Management 2: 25–49. [Google Scholar] [CrossRef]

- Oltra, Vanessa, and Maïder Saint Jean. 2005. The dynamics of environmental innovations: Three stylised trajectories of clean technology. Economics of Innovation and New Technology 14: 189–212. [Google Scholar] [CrossRef]

- Parra-Domínguez, Javier, Fátima David, and Tânia-Cristina Azevedo. 2021. Family firms and coupling among CSR disclosures and performance. Administrative Sciences. forthcoming. [Google Scholar]

- Porter, Micheal E., and Claas van der Linde. 1995. Toward a new conception of the environment-competitiveness relationship. Journal of Economic Perspectives 9: 97–118. [Google Scholar] [CrossRef]

- Qiu, Lu, Xiaowen Jie, Yanan Wang, and Minjuan Zhao. 2020. Green product innovation, green dynamic capability, and competitive advantage: Evidence from Chinese manufacturing enterprises. Corporate Social Responsibility and Environmental Management 27: 146–65. [Google Scholar] [CrossRef]

- Radu, Camélia, and Claude Francoeur. 2017. Does innovation drive environmental disclosure? A new insight into sustainable development. Business Strategy and the Environment 26: 893–911. [Google Scholar] [CrossRef]

- Raimo, Nicola, Marianna Zito, and Alessandra Caragnano. 2019. Does national culture affect integrated reporting quality? A focus on GLOBE dimensions. Paper presented at 9th International Symposium on Natural Resources Management, Zaječar, Serbia, May 31; pp. 383–392. [Google Scholar]

- Raimo, Nicola, Elbano de Nuccio, Anastasia Giakoumelou, Felice Petruzzella, and Filippo Vitolla. 2020a. Non-financial information and cost of equity capital: An empirical analysis in the food and beverage industry. British Food Journal 123: 49–65. [Google Scholar] [CrossRef]

- Raimo, Nicola, Alessandra Ricciardelli, Michele Rubino, and Filippo Vitolla. 2020b. Factors affecting human capital disclosure in an integrated reporting perspective. Measuring Business Excellence 24: 575–92. [Google Scholar] [CrossRef]

- Raimo, Nicola, Filippo Vitolla, Arcangelo Marrone, and Michele Rubino. 2020c. The role of ownership structure in integrated reporting policies. Business Strategy and the Environment 29: 2238–50. [Google Scholar] [CrossRef]

- Raimo, Nicola, Alessandra Caragnano, Marianna Zito, Filippo Vitolla, and Massimo Mariani. 2021a. Extending the benefits of ESG disclosure: The effect on the cost of debt financing. Corporate Social Responsibility and Environmental Management. [Google Scholar] [CrossRef]

- Raimo, Nicola, Filippo Vitolla, Arcangelo Marrone, and Michele Rubino. 2021b. Do audit committee attributes influence integrated reporting quality? An agency theory viewpoint. Business Strategy and the Environment 30: 522–34. [Google Scholar] [CrossRef]

- Rao, Kathyayini Kathy, Carol A. Tilt, and Laurence H. Lester. 2012. Corporate governance and environmental reporting: An Australian study. Corporate Governance: The International Journal of Business in Society 12: 143–63. [Google Scholar]

- Rennie, Susannah C. 2016. Providing information on environmental change: Data management, discovery and access in the UK Environmental Change Network Data Centre. Ecological Indicators 68: 13–20. [Google Scholar] [CrossRef] [Green Version]

- Salvi, Antonio, Filippo Vitolla, Nicola Raimo, Michele Rubino, and Felice Petruzzella. 2020a. Does intellectual capital disclosure affect the cost of equity capital? An empirical analysis in the integrated reporting context. Journal of Intellectual Capital 21: 985–1007. [Google Scholar] [CrossRef]

- Salvi, Antonio, Filippo Vitolla, Anastasia Giakoumelou, Nicola Raimo, and Michele Rubino. 2020b. Intellectual capital disclosure in integrated reports: The effect on firm value. Technological Forecasting and Social Change 160: 120228. [Google Scholar] [CrossRef]

- Scarpellini, Sabina, Alfonso Aranda, Juan Aranda, Eva Llera, and Miguel Marco. 2012. R&D and eco-innovation: Opportunities for closer collaboration between universities and companies through technology centers. Clean Technologies and Environmental Policy 14: 1047–58. [Google Scholar]

- Sharif, Mehmoona, and Kashif Rashid. 2014. Corporate governance and corporate social responsibility (CSR) reporting: An empirical evidence from commercial banks (CB) of Pakistan. Quality & Quantity 48: 2501–21. [Google Scholar]

- Singhvi, Surendra S., and Harsha B. Desai. 1971. An empirical analysis of the quality of corporate financial disclosure. The Accounting Review 46: 129–38. [Google Scholar]

- Skordoulis, Michalis, Stamatios Ntanos, Grigorios L. Kyriakopoulos, Garyfallos Arabatzis, Spyros Galatsidas, and Miltiadis Chalikias. 2020. Environmental Innovation, Open Innovation Dynamics and Competitive Advantage of Medium and Large-Sized Firms. Journal of Open Innovation: Technology, Market, and Complexity 6: 195. [Google Scholar] [CrossRef]

- Trireksani, Terri, and Hadrian Geri Djajadikerta. 2016. Corporate governance and environmental disclosure in the Indonesian mining industry. Australasian Accounting, Business and Finance Journal 10: 18–28. [Google Scholar] [CrossRef] [Green Version]

- Verrecchia, Robert E. 1983. Discretionary disclosure. Journal of Accounting and Economics 5: 179–94. [Google Scholar] [CrossRef]

- Vitolla, Filippo, and Nicola Raimo. 2018. Adoption of integrated reporting: Reasons and benefits—A case study analysis. International Journal of Business and Management 13: 244–50. [Google Scholar] [CrossRef] [Green Version]

- Vitolla, Filippo, Nicola Raimo, and Elbano De Nuccio. 2018. Integrated reporting: Development and state of art—The Italian case in the international context. International Journal of Business and Management 13: 233–40. [Google Scholar] [CrossRef] [Green Version]

- Vitolla, Filippo, Nicola Raimo, and Michele Rubino. 2019a. Appreciations, criticisms, determinants, and effects of integrated reporting: A systematic literature review. Corporate Social Responsibility and Environmental Management 26: 518–28. [Google Scholar] [CrossRef]

- Vitolla, Filippo, Nicola Raimo, Michele Rubino, and Antonello Garzoni. 2019b. How pressure from stakeholders affects integrated reporting quality. Corporate Social Responsibility and Environmental Management 26: 1591–606. [Google Scholar] [CrossRef]

- Vitolla, Filippo, Nicola Raimo, Michele Rubino, and Antonello Garzoni. 2019c. The impact of national culture on integrated reporting quality. A stakeholder theory approach. Business Strategy and the Environment 28: 1558–71. [Google Scholar] [CrossRef]

- Vitolla, Filippo, Nicola Raimo, and Michele Rubino. 2020a. Board characteristics and integrated reporting quality: An agency theory perspective. Corporate Social Responsibility and Environmental Management 27: 1152–63. [Google Scholar] [CrossRef]

- Vitolla, Filippo, Nicola Raimo, Arcangelo Marrone, and Michele Rubino. 2020b. The role of board of directors in intellectual capital disclosure after the advent of integrated reporting. Corporate Social Responsibility and Environmental Management 27: 2188–200. [Google Scholar] [CrossRef]

- Vitolla, Filippo, Nicola Raimo, Michele Rubino, and Antonello Garzoni. 2020c. The determinants of integrated reporting quality in financial institutions. Corporate Governance: The International Journal of Business in Society 20: 429–44. [Google Scholar] [CrossRef]

- Vitolla, Filippo, Nicola Raimo, Michele Rubino, and Giovanni Maria Garegnani. 2021a. Do cultural differences impact ethical issues? Exploring the relationship between national culture and quality of code of ethics. Journal of International Management 27: 100823. [Google Scholar] [CrossRef]

- Vitolla, Filippo, Nicola Raimo, Michele Rubino, and Antonello Garzoni. 2021b. Broadening the horizons of intellectual capital disclosure to the sports industry: Evidence from top UEFA clubs. Meditari Accountancy Research. [Google Scholar] [CrossRef]

- Vormedal, Irja, and Audun Ruud. 2009. Sustainability reporting in Norway—An assessment of performance in the context of legal demands and socio-political drivers. Business Strategy and the Environment 18: 207–22. [Google Scholar] [CrossRef]

- Winn, Monica L., and Linda C. Angell. 2000. Towards a process model of corporate greening. Organization Studies 21: 1119–47. [Google Scholar] [CrossRef]

- World Economic Forum. 2020. The Global Risks Report 2020. Available online: http://www3.weforum.org/docs/WEF_Global_Risk_Report_2020.pdf (accessed on 10 January 2021).

- Yin, Jianhua, and Sen Wang. 2018. The effects of corporate environmental disclosure on environmental innovation from stakeholder perspectives. Applied Economics 50: 905–19. [Google Scholar] [CrossRef]

- Zhang, Yue-Jun, Yu-Lu Peng, Chao-Qun Ma, and Bo Shen. 2017. Can environmental innovation facilitate carbon emissions reduction? Evidence from China. Energy Policy 100: 18–28. [Google Scholar] [CrossRef]

{kind=link}

| Panel A. Sample Distribution by Geographic Zone | |||

|---|---|---|---|

| Country | % | Country | % |

| Argentina | 0.11 | Netherlands | 0.88 |

| Australia | 6.59 | New Zealand | 0.55 |

| Austria | 0.39 | Nigeria | 0.02 |

| Bahrein | 0.05 | Norway | 0.48 |

| Belgium | 0.67 | Oman | 0.08 |

| Bermuda | 0.39 | Panama | 0.01 |

| Brazil | 1.59 | Papua New Guinea | 0.02 |

| Canada | 6.31 | Peru | 0.17 |

| Cayman Islands | 0.04 | Philippines | 0.44 |

| Chile | 0.50 | Poland | 0.55 |

| China | 2.42 | Portugal | 0.27 |

| Colombia | 0.24 | Puerto Rico | 0.01 |

| Cyprus | 0.02 | Qatar | 0.15 |

| Czech Republic | 0.08 | Russia | 0.72 |

| Denmark | 0.63 | Saudi Arabia | 0.19 |

| Egypt | 0.19 | Singapore | 1.16 |

| Finland | 0.64 | South Africa | 2.08 |

| France | 2.31 | Spain | 1.10 |

| Germany | 2.03 | Sri Lanka | 0.02 |

| Gibraltar | 0.02 | Sweden | 1.27 |

| Greece | 0.40 | Switzerland | 1.66 |

| Guernsey | 0.03 | Taiwan | 2.45 |

| Hong Kong | 2.83 | Thailand | 0.58 |

| Hungary | 0.08 | Turkey | 0.53 |

| India | 1.64 | Ukraine | 0.01 |

| Indonesia | 0.63 | United Arab Emirates | 0.16 |

| Ireland | 0.62 | United Kingdom | 7.84 |

| Isle Of Man | 0.01 | United States | 29.52 |

| Israel | 0.32 | Panel B. Sample distribution by Industry | |

| Italy | 1.21 | Industry | % |

| Japan | 9.98 | Oil and Gas | 6.99 |

| Jersey | 0.07 | Basic Materials | 9.98 |

| Jordan | 0.02 | Industry | 18.22 |

| Korea (South) | 2.10 | Consumer goods | 10.52 |

| Kuwait | 0.13 | Health | 6.02 |

| Luxemburg | 0.15 | Consumer services | 12.95 |

| Macau | 0.03 | Telecommunications | 2.65 |

| Malaysia | 0.92 | Public services | 4.53 |

| Mexico | 0.62 | Financial and Real Estate | 21.37 |

| Morocco | 0.07 | Technology | 6.77 |

| Variable | Measure | Relative Frequency | |

|---|---|---|---|

| AC_Exp | Dummy if a financial expert is on the audit committee | 0.49 | |

| Civil_Law | Dummy if the firm is located in a civil law country | 0.38 | |

| Mandatory | Dummy if the firm is located in South Africa | 0.02 | |

| Mean | Std.Dev | ||

| EnvI.Inf | Integrated level of environmental information (0–4 points) | 1.21 | 1.16 |

| EnvInno | Environmental innovation projects (0–3 values) | 0.6 | 0.89 |

| EnvPerf | Environmental performance score | 49.64 | 31.97 |

| F_Size | Logarithm of total assets by firm size measure | 16.69 | 2.82 |

| F_Age | Age of the company since its establishment | 37.39 | 31.86 |

| ROA | Ratio Return on Assets | 4.85 | 15.19 |

| Growth | Sales mean value in the last five years | 2.97 | 0.32 |

| Error | Forecast error (Martínez-Ferrero et al. 2016) | 0.09 | 1.54 |

| KZIndex | KZ index of Kaplan and Zingales (1997) | 0.01 | 0.08 |

| Leverage | Ratio Total Debt to Total Equity | 0.14 | 0.17 |

| WorCap | Working capital | 0.92 | 0.01 |

| Divid | Dividends paid by the company | 61.89 | 74.44 |

| F_Intern | Investment in total assets in other countries | 17.68 | 26.82 |

| Analysts | Analysts follow the company | 13.09 | 8.98 |

| CPI | CEO Power Index (García-Sánchez et al. 2020a) | 1.92 | 0.73 |

| B_Size | Number of directors on the board | 10.07 | 3.53 |

| B_Activity | Annual meetings of the board | 18.41 | 10.87 |

| B_Women | Percentage of female directors on the board | 0.12 | 0.11 |

| IENVPI | Industry Environmental Index (Amor-Esteban et al. 2018, 2019) | 0.02 | 0.91 |

| ERRI | National environmental regulations index (Esty and Porter 2001) | 0.93 | 0.64 |

| TranspIndex | Disclosure legal requirement at country level | 0.56 | 0.82 |

| LOIndex | The index of law and order from La Porta et al. (1998) | 8.89 | 1.68 |

| JEIndex | The index of judicial efficiency from La Porta et al. (1998) | 9.18 | 1.55 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |||

| 1 | EnvI.Inf | 1 | ||||||||

| 2 | EnvInno | 0.40 *** | 1 | |||||||

| 3 | EnvPerf | 0.50 *** | 0.29 *** | 1 | ||||||

| 4 | F_Size | 0.30 *** | 0.28 *** | 0.18 *** | 1 | |||||

| 5 | F_Age | 0.20 *** | 0.23 *** | 0.13 *** | 0.18 *** | 1 | ||||

| 6 | ROA | 0.03 *** | 0.00 | 0.02 *** | 0.04 *** | 0.04 *** | 1 | |||

| 7 | Growth | 0.00 | 0.00 | 0.01 | 0.00 | −0.01 * | 0.00 | 1 | ||

| 8 | Error | −0.02 *** | −0.01 ** | −0.01 * | −0.03 *** | −0.02 *** | −0.10 *** | 0.00 | 1 | |

| 9 | KZIndex | 0.07 *** | 0.07 *** | 0.03 *** | 0.34 *** | 0.02 *** | −0.01 | 0.00 | 0.00 | |

| 10 | Leverage | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | −0.01 | 0.00 | 0.42 *** | |

| 11 | WorCap | 0.04 *** | 0.03 *** | 0.02 *** | 0.18 *** | 0.01 | 0.02 *** | 0.00 | −0.01 | |

| 12 | Divid | −0.01 | 0.01 *** | 0.01 * | 0.15 *** | −0.01 * | 0.00 | 0.00 | 0.00 | |

| 13 | F_Intern | 0.14 *** | 0.08 *** | 0.07 *** | −0.03 *** | 0.06 *** | 0.01 * | 0.00 | 0.00 | |

| 14 | Analysts | 0.30 *** | 0.21 *** | 0.17 *** | 0.24 *** | 0.05 *** | 0.09 *** | −0.01 * | −0.01 | |

| 15 | CPI | 0.04 *** | −0.01 | 0.02 *** | 0.10 *** | −0.02 ** | −0.01 ** | 0.01 | −0.01 | |

| 16 | B_Size | 0.21 *** | 0.10 *** | 0.29 *** | 0.19 *** | 0.08 *** | 0.02 *** | 0.02 *** | −0.02 *** | |

| 17 | B_Activity | 0.14 *** | 0.03 *** | 0.15 *** | 0.04 *** | 0.03 *** | −0.01 | 0.00 | −0.02 *** | |

| 18 | B_Women | 0.12 *** | 0.02 *** | 0.15 *** | −0.13 *** | 0.04 *** | 0.02 *** | −0.01 | −0.01 | |

| 19 | AC_Exp | 0.08 *** | −0.02 *** | −0.07 *** | −0.13 *** | −0.02 *** | 0.00 | 0.01 | 0.00 | |

| 20 | IENVPI | 0.13 *** | 0.20 *** | 0.09 *** | −0.04 *** | 0.07 *** | −0.03 *** | 0.00 | 0.00 | |

| 21 | ERRI | −0.08 *** | 0.05 *** | 0.03 *** | −0.41 *** | 0.03 *** | −0.05 *** | 0.00 | 0.01 | |

| 22 | Civil_Law | 0.20 *** | 0.24 *** | 0.15 *** | 0.53 *** | 0.10 *** | 0.01 * | 0.01 ** | −0.02 *** | |

| 23 | TranspIndex | 0.10 *** | −0.03 *** | 0.03 *** | −0.35 *** | 0.00 | −0.01 *** | 0.01 | −0.01 * | |

| 24 | LOIndex | −0.19 *** | −0.03 *** | −0.05 *** | −0.44 *** | −0.05 *** | −0.08 *** | 0.00 | 0.01 *** | |

| 25 | JEIndex | −0.17 *** | −0.04 *** | −0.04 *** | −0.34 *** | −0.03 *** | −0.05 *** | 0.00 | 0.00 | |

| 26 | Mandatory | 0.13 *** | −0.04 *** | 0.00 | 0.01 | 0.04 *** | 0.03 *** | 0.00 | 0.00 | |

| 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | |||

| 9 | KZIndex | 1 | ||||||||

| 10 | Leverage | 0.01 | 1 | |||||||

| 11 | WorCap | 0.26 *** | 0.00 | 1 | ||||||

| 12 | Divid | 0.22 *** | 0.00 | 0.13 *** | 1 | |||||

| 13 | F_Intern | −0.02 *** | −0.01 | −0.03 *** | −0.03 *** | 1 | ||||

| 14 | Analysts | 0.05 *** | −0.01 | 0.07 *** | 0.01 *** | 0.08 *** | 1 | |||

| 15 | CPI | 0.03 *** | 0.00 | 0.02 *** | 0.01 ** | 0.01 ** | −0.06 *** | 1 | ||

| 16 | B_Size | 0.00 | 0.01 | 0.00 | −0.03 *** | 0.03 *** | 0.12 *** | 0.05 *** | 1 | |

| 17 | B_Activity | 0.02 ** | 0.00 | 0.00 | 0.01 | 0.08 *** | −0.04 *** | 0.33 *** | −0.10 *** | |

| 18 | B_Women | −0.07 *** | 0.01 ** | −0.03 *** | −0.05 *** | −0.02 *** | 0.05 *** | −0.16 *** | 0.08 *** | |

| 19 | AC_Exp | −0.05 *** | 0.00 | −0.03 *** | −0.04 *** | 0.00 | 0.04 *** | −0.19 *** | 0.02 *** | |

| 20 | IENVPI | 0.05 *** | −0.01 ** | 0.02 *** | −0.01 * | 0.16 *** | −0.05 *** | 0.02 *** | −0.02 *** | |

| 21 | ERRI | −0.20 *** | 0.00 | −0.12 *** | −0.08 *** | 0.13 *** | 0.00 | −0.15 *** | −0.06 *** | |

| 22 | Civil_Law | 0.15 *** | 0.00 | 0.08 *** | 0.10 *** | 0.05 *** | 0.02 *** | 0.11 *** | 0.12 *** | |

| 23 | TranspIndex | −0.08 *** | −0.01 | −0.04 *** | −0.05 *** | 0.23 *** | −0.06 *** | 0.09 *** | −0.07 *** | |

| 24 | LOIndex | −0.25 *** | 0.00 | −0.14 *** | −0.10 *** | 0.01 ** | −0.02 *** | −0.17 *** | −0.07 *** | |

| 25 | JEIndex | −0.26 *** | −0.01 | −0.16 *** | −0.08 *** | 0.02 *** | −0.03 *** | −0.11 *** | −0.09 *** | |

| 26 | Mandatory | −0.02 *** | 0.01 | −0.01 * | −0.01 *** | 0.00 | −0.11 *** | 0.05 *** | 0.01 ** | |

| 17 | 18 | 19 | 20 | 21 | 22 | 23 | 24 | 25 | ||

| 17 | B_Activity | 1 | ||||||||

| 18 | B_Women | −0.01 | 1 | |||||||

| 19 | AC_Exp | −0.12 *** | 0.28 *** | 1 | ||||||

| 20 | IENVPI | 0.06 *** | −0.06 *** | −0.02 *** | 1 | |||||

| 21 | ERRI | −0.0 7*** | 0.11 *** | 0.04 *** | −0.05 *** | 1 | ||||

| 22 | Civil_Law | 0.11 *** | −0.13 *** | −0.19 *** | 0.05 *** | −0.21 *** | 1 | |||

| 23 | TranspIndex | 0.24 *** | 0.11 *** | 0.05 *** | 0.05 *** | 0.28 *** | −0.04 *** | 1 | ||

| 24 | LOIndex | −0.11 *** | 0.09 *** | 0.06 *** | −0.02 *** | 0.87 *** | −0.28 *** | 0.16 *** | 1 | |

| 25 | JEIndex | −0.08 *** | 0.05 *** | 0.07 *** | −0.03 *** | 0.75 *** | −0.42 *** | 0.12 *** | 0.77 *** | 1 |

| 26 | Mandatory | 0.04 *** | 0.05 *** | 0.04 *** | −0.01 | −0.22 *** | −0.11 *** | −0.10 *** | −0.39 *** | −0.30 *** |

| Equation (2) | Equation (1) | Robust 1 | Robust 2 | |

|---|---|---|---|---|

| EnvPerf | EnvI.Inf | EnvI.Inf1 | EnvI.Inf2 | |

| Coeff. (Std. Error) | Coeff. (Std. Error) | Coeff. (Std. Error) | Coeff. (Std. Error) | |

| EnvInno | 2.385 ** | 0.361 *** | 0.556 *** | 0.189 *** |

| −1.035 | (0.0318) | (0.0510) | (0.0319) | |

| EnvPerf | 0.00584 *** | 0.00625 *** | 0.00569 *** | |

| (0.000711) | (0.00111) | (0.000754) | ||

| F_Size | 3.117 * | 0.359 *** | 0.680 *** | 0.203 *** |

| −1.696 | (0.0255) | (0.0484) | (0.0232) | |

| F_Age | 1.764 *** | 0.00630 *** | 0.0137 *** | 0.00242 ** |

| (0.225) | (0.00121) | (0.00219) | (0.00107) | |

| ROA | −0.0392 | 0.00591 *** | 0.0126 *** | 0.00303 |

| (0.0547) | (0.00206) | (0.00363) | (0.00206) | |

| Growth | −0.0776 | −0.00265 | −0.167 * | −0.00155 |

| (0.0566) | (0.00305) | (0.0961) | (0.00251) | |

| Error | −0.183 | −0.00717 | 0.0152 | −0.0151 |

| (0.374) | (0.0182) | (0.0290) | (0.0198) | |

| KZIndex | −35.82 | −5.001 *** | −9.378 *** | −2.112 ** |

| (59.31) | −1.020 | −1.701 | (0.934) | |

| Leverage | 0.000239 | 7.66e−06 | 3.11e−06 | 6.67e−06 |

| (0.000197) | (9.99e−06) | (1.51e−05) | (1.09e−05) | |

| WorCap | 2.93e−09 ** | −1.15e−09 *** | −2.20e−09 *** | −3.63e−10 |

| (1.17e−09) | (2.78e−10) | (4.59e−10) | (2.55e−10) | |

| Divid | −0.0380 | −0.000200 | −0.000191 | −0.000211 |

| (0.0250) | (0.000153) | (0.000296) | (0.000135) | |

| F_Intern | 0.0146 | 0.000671 | 0.00313 * | −0.000757 |

| (0.0345) | (0.00114) | (0.00180) | (0.00113) | |

| Analysts | 0.164 | 0.0475 *** | 0.0682 *** | 0.0268 *** |

| (0.140) | (0.00395) | (0.00658) | (0.00379) | |

| CPI | −1.471 ** | −0.0762 *** | −0.111 ** | −0.0477 |

| (0.730) | (0.0293) | (0.0458) | (0.0310) | |

| B_Size | 0.0164 | 0.00444 | −0.00682 | 0.00948 |

| (0.170) | (0.00738) | (0.0116) | (0.00773) | |

| B_Activity | 0.0746 | 0.00672 *** | 0.00661 ** | 0.00727 *** |

| (0.0473) | (0.00194) | (0.00299) | (0.00206) | |

| B_Women | 0.0793 * | −0.00202 | −0.00125 | −0.00326 |

| (0.0472) | (0.00190) | (0.00297) | (0.00200) | |

| AC_Exp | 0.0188 | −0.0130 | 0.0507 | −0.0265 |

| −1.444 | (0.0604) | (0.0936) | (0.0649) | |

| IENVPI | 0.334 *** | 0.679 *** | 0.157 *** | |

| (0.0550) | (0.0997) | (0.0489) | ||

| ERRI | 1.146 | 0.848 *** | 1.280 *** | 0.617 *** |

| −9.001 | (0.160) | (0.266) | (0.145) | |

| Civil_Law | −0.0528 | −0.189 | −0.00231 | |

| (0.144) | (0.253) | (0.128) | ||

| TranspIndex | 0.850 *** | 1.765 *** | 0.332 *** | |

| (0.0611) | (0.116) | (0.0534) | ||

| LOIndex | −0.327 *** | −0.410 *** | −0.256 *** | |

| (0.0622) | (0.107) | (0.0556) | ||

| JEIndex | −0.159 *** | −0.357 *** | −0.0603 | |

| (0.0600) | (0.107) | (0.0533) | ||

| Mandatory | 1.334 *** | 2.255 *** | 0.698 ** | |

| (0.345) | (0.608) | (0.310) | ||

| Zone, Industry and Year included | ||||

| R2 | 0.9067 *** | |||

| Log-Likelihood | −7533.5816 | −3809.8896 | −5522.8182 | |

| LR test | 2873.07 *** | 3730.89 *** | 1568.36 *** | |

| Dummy Silent Green Disclosures | |

|---|---|

| Coeff. (Std. Error) | |

| EnvInno | 2.128 *** |

| (0.503) | |

| F_Size | −0.435 *** |

| (0.140) | |

| F_Age | 0.00432 |

| (0.00668) | |

| ROA | −0.0132 |

| (0.0168) | |

| Growth | 0.0449 |

| (0.194) | |

| Error | 0.287 |

| (0.745) | |

| KZIndex | 9.993 |

| (24.28) | |

| Leverage | −0.000124 |

| (0.000256) | |

| WorCap | −8.74e−10 |

| (1.12e−09) | |

| Divid | −0.000494 |

| (0.000708) | |

| F_Intern | 0.00771 |

| (0.00767) | |

| Analysts | 0.0507 ** |

| (0.0252) | |

| CPI | −0.414 * |

| (0.236) | |

| B_Size | 0.0104 |

| (0.0570) | |

| B_Activity | 0.0202 |

| (0.0156) | |

| B_Women | 0.00207 |

| (0.0154) | |

| AC_Exp | 0.869 * |

| (0.448) | |

| IENVPI | 0.402 |

| (0.309) | |

| ERRI | 1.254 |

| (0.927) | |

| Civil_Law | −1.576 ** |

| (0.733) | |

| TranspIndex | −0.730 ** |

| (0.333) | |

| LOIndex | −0.220 |

| (0.343) | |

| JEIndex | −0.439 |

| (0.302) | |

| Mandatory | −2.937 ** |

| −1.408 | |

| Zone, Industry and Year included | |

| Log-Likelihood | −305.85377 |

| LR test | 49.80 *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

García-Sánchez, I.-M.; Raimo, N.; Vitolla, F. Are Environmentally Innovative Companies Inclined towards Integrated Environmental Disclosure Policies? Adm. Sci. 2021, 11, 29. https://0-doi-org.brum.beds.ac.uk/10.3390/admsci11010029

García-Sánchez I-M, Raimo N, Vitolla F. Are Environmentally Innovative Companies Inclined towards Integrated Environmental Disclosure Policies? Administrative Sciences. 2021; 11(1):29. https://0-doi-org.brum.beds.ac.uk/10.3390/admsci11010029

Chicago/Turabian StyleGarcía-Sánchez, Isabel-María, Nicola Raimo, and Filippo Vitolla. 2021. "Are Environmentally Innovative Companies Inclined towards Integrated Environmental Disclosure Policies?" Administrative Sciences 11, no. 1: 29. https://0-doi-org.brum.beds.ac.uk/10.3390/admsci11010029