Drought Shocks and Gearing Impacts on the Profitability of Sheep Farming

, , , , and

, , , , and

Abstract

:1. Introduction

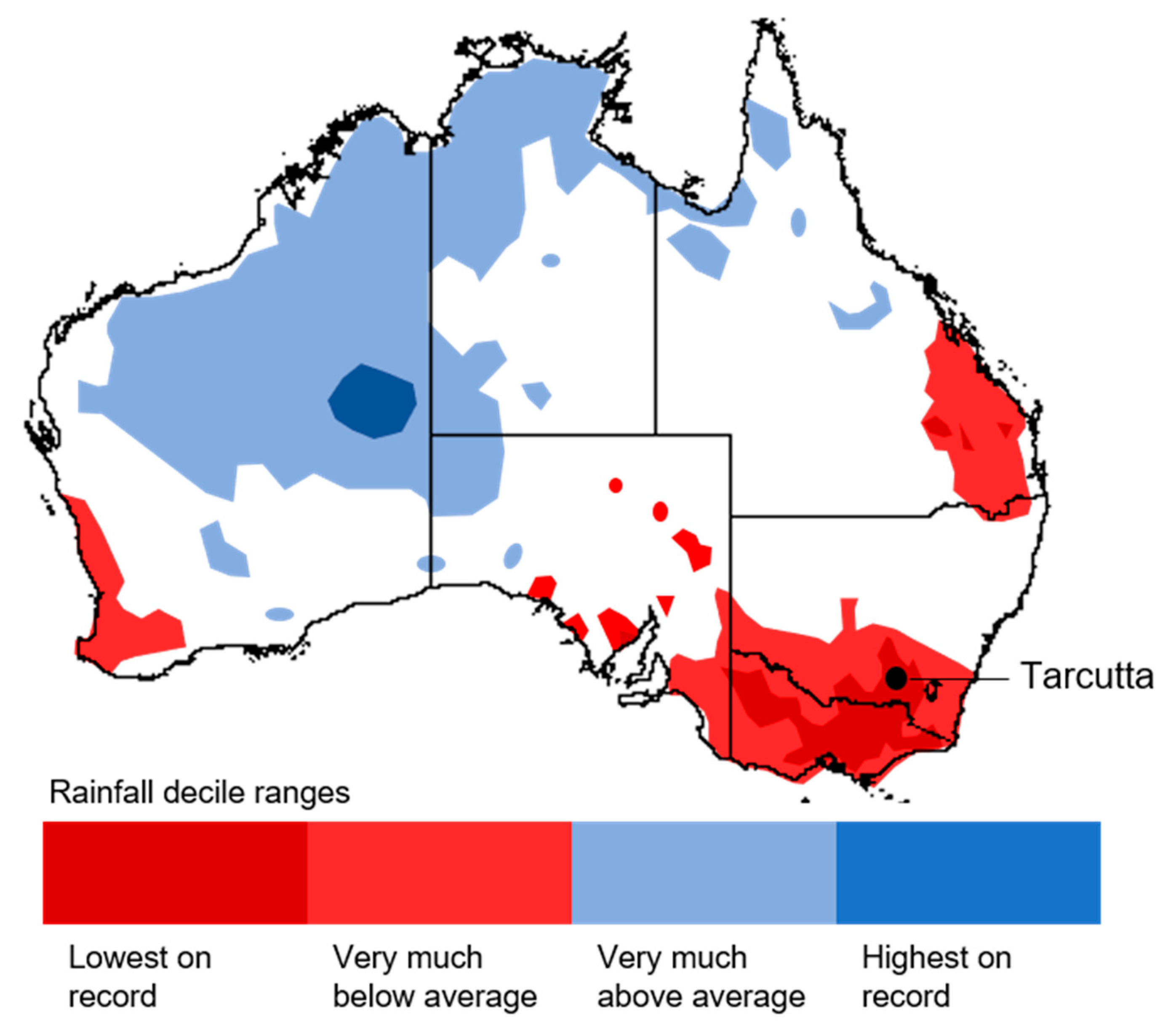

2. Materials and Methods

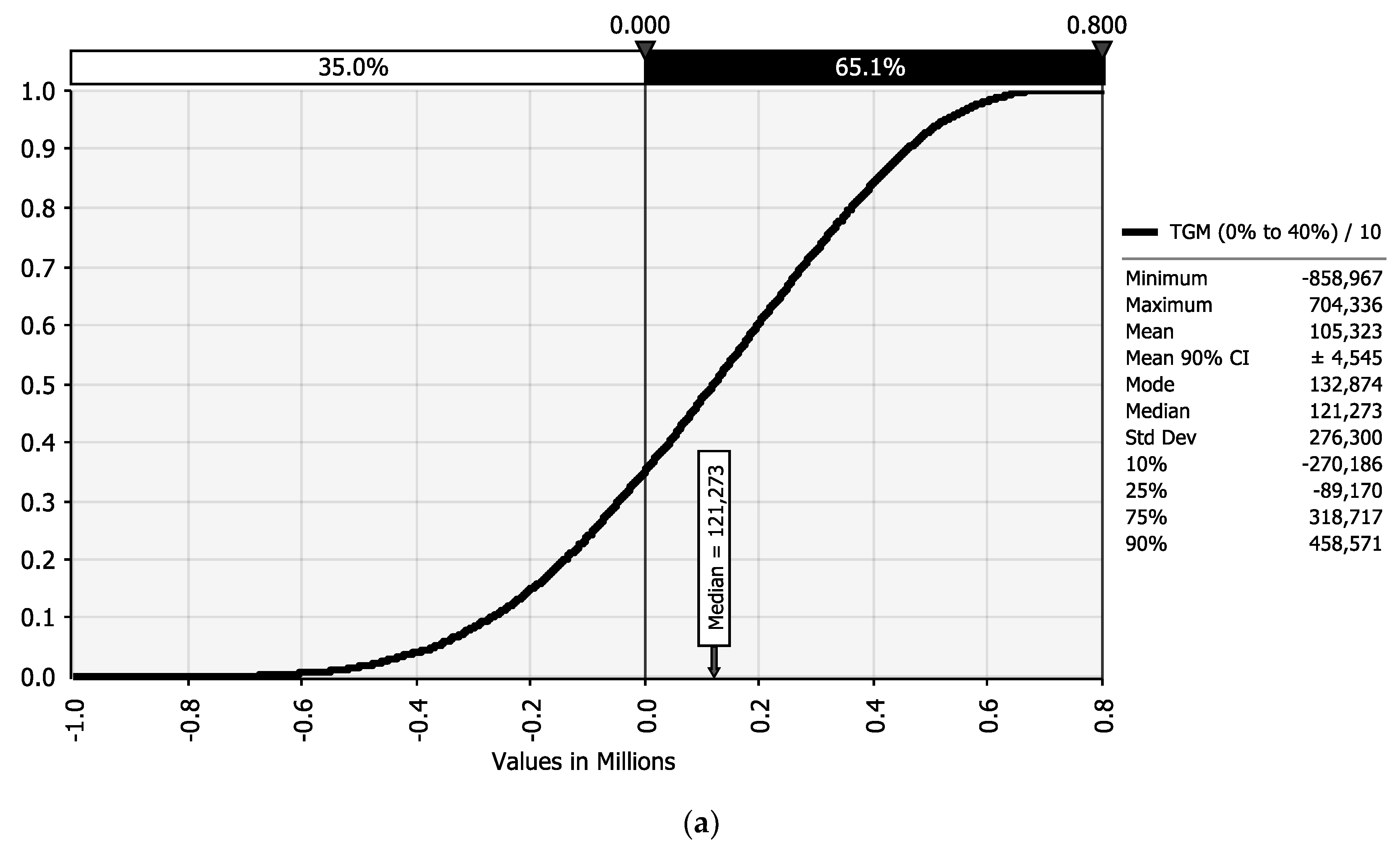

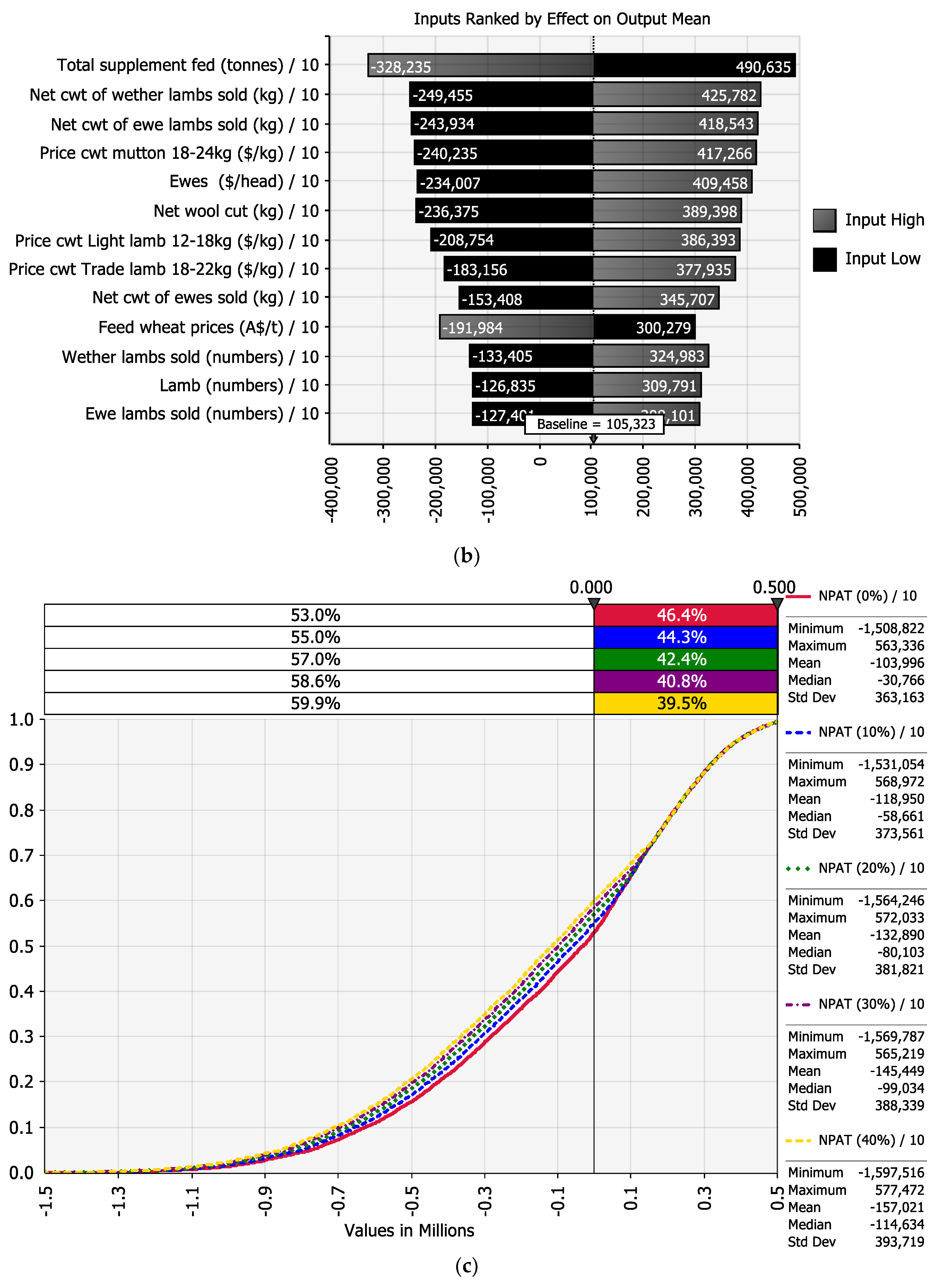

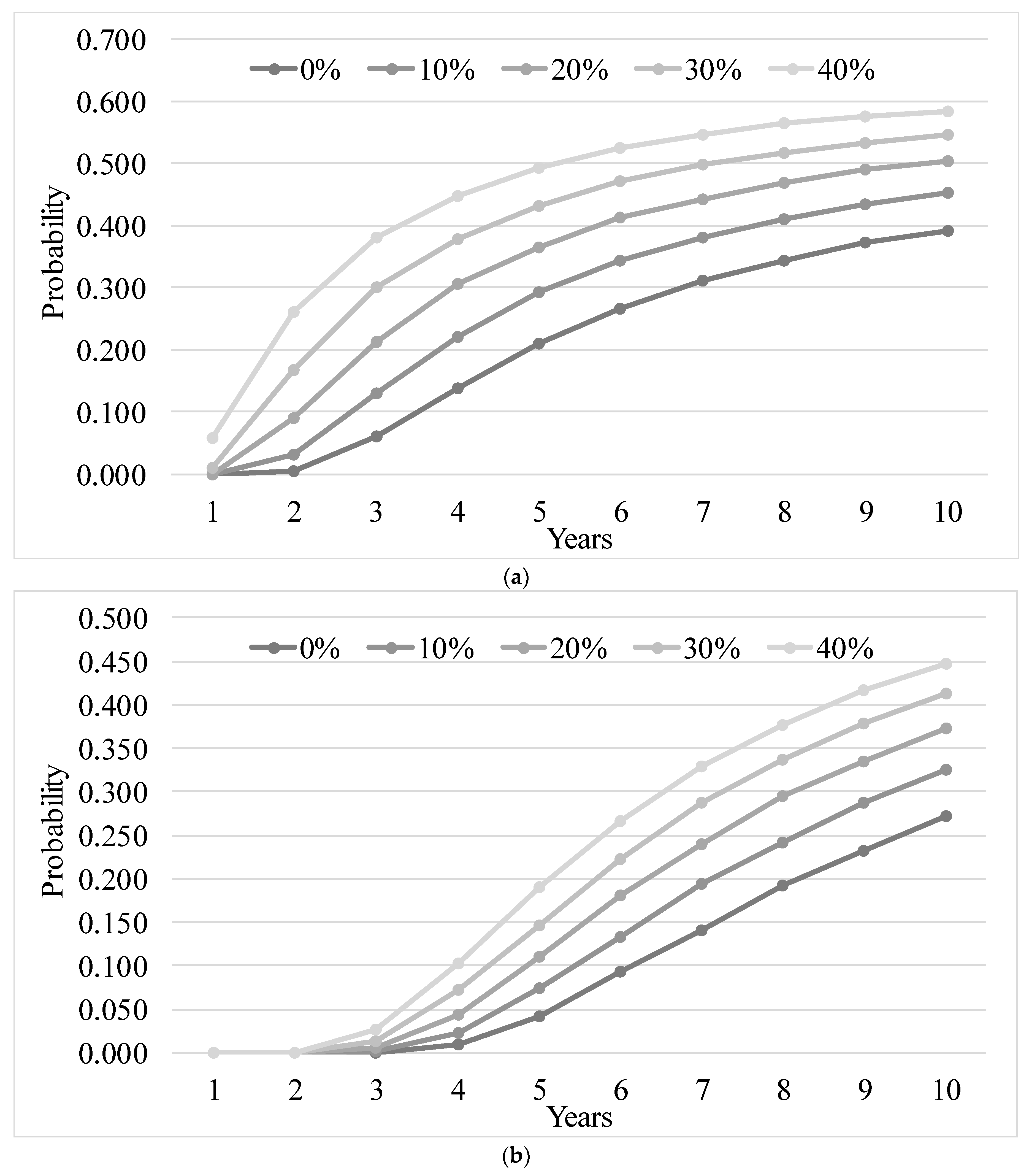

3. Results

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

| Year | Wool Clean 20 µm ($/kg) | Net Wool Cut (kg) | Price cwt Mutton 18–24 kg ($/kg) | Price Merino Sheep Skin 24.1 kg + 1.5″–2″ ($/skin) | Ewes Sold Cast for Age (no.) | Net cwt of ewes Sold (kg) | Price cwt Trade Lamb 18–22 kg ($/kg) | Price cwt Light Lamb 12–18 kg ($/kg) | Price Lamb Skin 16.1–20 kg 1″–2″ ($/skin) | Wether Lambs Sold (no.) | Net cwt of Wether Lambs Sold (kg) | Ewe Lambs Sold (no.) | Net cwt of ewe Lambs Sold (kg) | Total shorn (no.) | Ewe (no.) | Lamb (no.) | Ewes ($/hd) | Ewes Bought (no.) | Feed Wheat Prices (AUD/t) | Total Supplement Fed (Tonnes) | Rams Bought (no.) | Total ha |

| 2002 | 15.4 | 16611 | 2.3 | 18.4 | 814 | 27.4 | 4.8 | 4.0 | 13.4 | 2660 | 13.1 | 2655 | 12.0 | 4912 | 4872 | 5315 | 96 | 1070 | 307 | 432 | 16.7 | 1000 |

| 2003 | 14.9 | 16189 | 2.9 | 15.3 | 835 | 28.3 | 5.5 | 4.9 | 11.5 | 2588 | 6.7 | 2583 | 6.7 | 4900 | 4873 | 5171 | 123 | 1110 | 435 | 1274 | 16.7 | 1000 |

| 2004 | 12.1 | 14950 | 2.7 | 19.1 | 921 | 28.3 | 5.4 | 4.7 | 15.0 | 2499 | 8.5 | 2505 | 8.4 | 4922 | 4862 | 5004 | 130 | 1124 | 306 | 826 | 16.7 | 1000 |

| 2005 | 10.5 | 15332 | 2.4 | 12.5 | 834 | 29.2 | 4.8 | 4.2 | 7.9 | 2749 | 9.0 | 2738 | 8.9 | 4935 | 4901 | 5487 | 116 | 1202 | 262 | 760 | 16.7 | 1000 |

| 2006 | 10.9 | 16656 | 1.9 | 14.1 | 804 | 24.1 | 4.4 | 3.5 | 10.1 | 2733 | 10.8 | 2739 | 10.0 | 4917 | 4901 | 5472 | 100 | 1087 | 251 | 1073 | 16.7 | 1000 |

| 2007 | 13.3 | 11938 | 2.0 | 13.4 | 825 | 27.5 | 4.1 | 3.4 | 9.7 | 2549 | 11.7 | 2540 | 10.9 | 4920 | 4892 | 5089 | 94 | 1052 | 363 | 1095 | 16.7 | 1000 |

| 2008 | 11.5 | 15605 | 2.4 | 12.5 | 871 | 27.9 | 4.8 | 3.9 | 9.0 | 2834 | 14.4 | 2839 | 13.0 | 4916 | 4883 | 5673 | 104 | 1078 | 522 | 499 | 16.7 | 1000 |

| 2009 | 9.9 | 15457 | 3.0 | 8.0 | 939 | 28.7 | 5.3 | 4.4 | 4.5 | 2694 | 15.9 | 2700 | 14.1 | 4918 | 4896 | 5394 | 116 | 1137 | 389 | 776 | 16.7 | 1000 |

| 2010 | 11.2 | 15644 | 4.4 | 16.5 | 846 | 29.1 | 5.9 | 5.4 | 12.6 | 2718 | 17.6 | 2731 | 15.8 | 4908 | 4896 | 5449 | 155 | 1173 | 275 | 315 | 16.7 | 1000 |

| 2011 | 15.4 | 17173 | 4.7 | 23.3 | 791 | 29.3 | 6.3 | 6.2 | 18.0 | 2863 | 18.1 | 2856 | 16.2 | 4930 | 4880 | 5719 | 177 | 1110 | 298 | 21 | 16.7 | 1000 |

| 2012 | 13.6 | 16672 | 2.8 | 15.8 | 820 | 28.9 | 4.6 | 4.4 | 11.7 | 2860 | 15.7 | 2866 | 13.9 | 4908 | 4880 | 5726 | 123 | 1095 | 250 | 123 | 16.7 | 1000 |

| 2013 | 12.8 | 15359 | 2.2 | 14.3 | 858 | 28.9 | 4.6 | 3.9 | 10.8 | 2809 | 16.1 | 2822 | 14.5 | 4904 | 4881 | 5631 | 104 | 1104 | 330 | 634 | 16.7 | 1000 |

| 2014 | 12.2 | 16557 | 3.3 | 9.5 | 899 | 28.6 | 5.4 | 4.8 | 6.3 | 2623 | 15.6 | 2603 | 13.6 | 4907 | 4876 | 5226 | 125 | 1121 | 325 | 349 | 16.7 | 1000 |

| 2015 | 13.2 | 16236 | 3.7 | 12.4 | 813 | 28.6 | 5.7 | 5.3 | 8.4 | 2765 | 16.8 | 2756 | 15.0 | 4913 | 4892 | 5521 | 140 | 1175 | 304 | 601 | 16.7 | 1000 |

| 2016 | 14.5 | 16162 | 3.6 | 15.2 | 851 | 29.4 | 5.8 | 5.6 | 9.5 | 2392 | 18.6 | 2394 | 16.5 | 4919 | 4889 | 4786 | 149 | 1082 | 285 | 516 | 16.7 | 1000 |

| 2017 | 16.1 | 16322 | 4.5 | 15.4 | 844 | 27.6 | 6.3 | 6.2 | 11.5 | 2828 | 11.0 | 2827 | 9.8 | 4923 | 4891 | 5655 | 168 | 1112 | 228 | 758 | 16.7 | 1000 |

| Shearing ($/hd) | Husbandry per ewe ($) | Husbandry per lamb ($) | Purchase cost per ram ($) | Pasture costs ($/ha) | Pasture establishment costs ($/ha) | |||||||||||||||||

| Min | 11.4 | 7.8 | 7.8 | 500 | 35.6 | 0.0 | ||||||||||||||||

| Most Likely | 11.9 | 9.0 | 9.0 | 746 | 38.9 | 26.5 | ||||||||||||||||

| Max | 12.1 | 10.6 | 10.6 | 2500 | 40.5 | 0.0 |

Appendix B

References

- Kimura, S.; Antón, J.; Lethi, C. Farm Level Analysis of Risk and Risk Management Strategies and Policies: Cross Country Analysis. In OECD Food, Agriculture and Fisheries No. 26; OECD Publishing: Paris, France, 2010. [Google Scholar]

- Kimura, S.; Antón, J. Risk Management in Agriculture in Australia. In OECD Food, Agriculture and Fisheries Papers, No. 39; OECD Publishing: Paris, France, 2011. [Google Scholar]

- Blackburn, A.; Rod, A. Financing Your Farm: A Practical Guide to Financial Growth, 4th ed.; Australian Bankers’ Association in conjunction with Grain Growers Association: Sydney, Australia, 2006. [Google Scholar]

- Australian Bureau of Statistics. Agricultural Commodities, Australia, 2016–2017, Catalogue No. 7121.0. Available online: http://www.abs.gov.au/AUSSTATS/[email protected]/DetailsPage/7121.02016-17?OpenDocument (accessed on 17 December 2018).

- Frilay, J.; van Dijk, J.; Ashton, D. Financial Performance of Lamb Producers, 2014–2015 to 2016–2017; Australian Bureau of Agricultural and Resource Economics and Sciences: Canberra, Australia, 2017.

- Malcolm, B. Financing Matters. AFBM J. 2011, 8, 11–18. [Google Scholar]

- Warn, L.; Ware, J.B.; Salmon, L.; Donnelly, J.; Alcock, D. Analysis of the Profitability of Sheep Wool and Meat Enterprises in Southern Australia. Final Rep. Proj. 1.2.6; Sheep Co-Operative Research Centre: Melbourne, Australia, 2006. [Google Scholar]

- Holmes Sackett. Prime Lamb Situation Analysis; Meat & Livestock Australia Limited: Sydney, Australia, 2010. [Google Scholar]

- Hutchings, T.R.; Nordblom, T.L. A Financial Analysis of the Effect of the Mix of Crop and Sheep Enterprises on the Risk Profile of Dryland Farms in South-Eastern Australia. AFBM J. 2011, 8, 19–41. [Google Scholar]

- Sklar, A. Fonctions De Répartition À N Dimensions Et Leurs Marges. Publ. Inst. Stat. Univ Paris 1959, 8, 229–231. [Google Scholar]

- Nelsen, R.B. An Introduction to Copulas, 2nd ed.; Springer: New York, NY, USA, 2006. [Google Scholar]

- Hardaker, J.B.; Lien, G.; Anderson, J.R.; Huirne, R.B.M. Coping with Risk in Agriculture; CABI: Wallingford, UK, 2015. [Google Scholar]

- Nguyen-Huy, T.; Deo, R.C.; Mushtaq, S.; Kath, J.; Khan, S. Copula-Based Agricultural Conditional Value-at-Risk Modelling for Geographical Diversifications in Wheat Farming Portfolio Management. Weather Clim. Extem. 2018, 21, 76–89. [Google Scholar] [CrossRef]

- Ji, Q.; Bouri, E.; Roubaud, D.; Shahzad, S.J.H. Risk Spillover between Energy and Agricultural Commodity Markets: A Dependence-Switching Covar-Copula Model. Energy Econ. 2018, 75, 14–27. [Google Scholar] [CrossRef]

- Vergni, L.; Todisco, F.L.; Mannocchi, F. Analysis of Agricultural Drought Characteristics through a Two-Dimensional Copula. Water Resour. Manag. 2015, 29, 2819–2835. [Google Scholar] [CrossRef]

- Riberiro, A.F.S.; Russo, A.; Gouveia, C.M.; Páscoa, P. Copula-Based Agricultural Drought Risk of Rainfed Cropping Systems. Agric. Water Manag. 2019, 223, 2795–2809. [Google Scholar]

- Moore, A.D.; Donnelly, J.R.; Freer, M. Grazplan: Decision Support Systems for Australian Grazing Enterprises. Iii. Pasture Growth and Soil Moisture Submodels, and the Grassgro Dss. Agric. Syst. 1997, 55, 535–582. [Google Scholar] [CrossRef]

- Lehman, D.; Groenendaal, H. Practical Spreadsheet Modeling Using @Risk; CRC Press: Boca Raton, FL, USA, 2020. [Google Scholar]

- Bureau of Meteorology. Previous Droughts; Australian Government, Bureau of Meteorology: Melbourne, Australia, 2021. [Google Scholar]

- Behrendt, K.; Weeks, P. How Are Global and Australian Sheepmeat Producers Performing? Global agri benchmark network results 2017. In MLA Market Information; Meat and Livestock Australia Ltd.: North Sydney, Australia, 2018. [Google Scholar]

- Nuthall, P.L. Farm Business Management Analysis of Farming Systems; CABI: Wallingford, UK, 2011. [Google Scholar]

- Robertson, S.M.; Broster, J.C.; Friend, M.A. Performance of Sheep Systems Grazing Perennial Pastures. 1. Pasture Persistence and Enterprise Productivity. Anim. Prod. Sci. 2019, 60, 388–405. [Google Scholar] [CrossRef]

- Australian Bureau of Agricultural and Resource Economics and Sciences. Agricultural Commodity Statistics 2018. ABARES. Available online: https://www.agriculture.gov.au/abares/research-topics/agricultural-outlook/data#agricultural-commodities (accessed on 20 December 2018).

- Meat and Livestock Australia. Saleyard Sheep and Lamb Indicators: New South Wales, Australia. Available online: http://statistics.mla.com.au/Report/List (accessed on 10 January 2019).

- Meat and Livestock Australia. Sheepskin Prices: Merino Sheep: New South Wales, Australia. Available online: http://statistics.mla.com.au/Report/List (accessed on 10 January 2019).

- Ridge, H.; (Australian Wool Innovation Limited, Sydney, Australia). Personal Communication, 2018.

- Martin, P. Cost of Sheep Production; Australian Bureau of Agricultural and Resource Economics and Sciences: Canberra, Australia, 2018.

- Malcolm, B.; Makeham, J.; Wright, V. The Farming Game: Agricultural Management and Marketing, 2nd ed.; Cambridge University Press: Melbourne, Australia, 2005. [Google Scholar]

- Behrendt, K.; Malcolm, B.; Jackson, T. Beef Business Management. In Beef Cattle Production and Trade; Cottle, D., Kahn, L., Eds.; CSIRO Publishing: Collingwood, Australia, 2014. [Google Scholar]

- Amidy, M.R.; Behrendt, K.; Badgery, W.B. Assessing the Profitability of Native Pasture Grazing Systems: A Stochastic Whole-Farm Modelling Approach. Anim. Prod. Sci. 2017, 57, 1859–1868. [Google Scholar] [CrossRef] [Green Version]

- Barry, P.J.; Ellinger, P.N. Financial Management in Agriculture, 7th ed.; Prentice Hall: Boston, MA, USA, 2012. [Google Scholar]

- Sarykalin, S.; Serraino, G.; Uryasev, S. Value-at-Risk Vs. Conditional Value-at-Risk in Risk Management and Optimisation. In State-of-the-Art Decision-Making Tools in the Information-Intensive Age; INFORMS Tutorials in Operations Research: Catonsville, MD USA, 2014; pp. 270–294. [Google Scholar]

- Rockafellar, R.T.; Uryasev, S. Conditional Value-at-Risk for General Loss Distributions. J. Bank. Financ. 2002, 26, 1443–1471. [Google Scholar] [CrossRef]

- Szegö, G. Measures of Risk. J. Bank. Financ. 2002, 26, 1253–1272. [Google Scholar] [CrossRef]

- Rees, M. Business Risk and Simulation Modelling in Practice: Using Excel, VBA and @Risk, 1st ed.; Wiley Finance Series: Newark, NJ, USA, 2015. [Google Scholar]

- @Risk, Decision Tools Suite 8. Palisade Corporation; Palisade Decision Tools: Ithaca, NY, USA, 2021.

- Buxton, R.; Smith, M.S. Managing Drought in Australia’s Rangelands: Four Weddings and a Funeral. Rangel. J. 1996, 18, 292–308. [Google Scholar] [CrossRef]

- Krause, M. Farming the Business Sowing for Your Future; Grains Research & Development Corporation (GRDC): Canberra, Australia, 2014. [Google Scholar]

- Fantazzini, D. The Effects of Misspecified Marginals and Copulas on Computing the Value at Risk: A Monte Carlo Study. Comput. Stat. Data Anal. 2009, 53, 2168–2188. [Google Scholar] [CrossRef]

- Delignette-Muller, M.L.; Dutang, C. fitdistrplus: An R Package for Fitting Distributions. J. Stat. Softw. 2015, 64, 34. [Google Scholar] [CrossRef] [Green Version]

- Zwick, D.S. A Hybrid Method for Fitting Distributions to Data and its Use in Computing Process Capability Indices. Qual. Eng. 1995, 7, 601–613. [Google Scholar] [CrossRef]

- Godfrey, S.; Nordblom, T.; Ip, R.; Robertson, S.; Hutchings, T. Using GrassGro® with @Risk®: Merino Ewe/First-Cross Lamb Enterprise Risk Profiles with Variable Prices and Weather; Australasian Agricultural and Resource Economics Society (AARES): Melbourne, Australia, 2019. [Google Scholar]

- Hutchings, T.R. Financial Risk on Dryland Farms in South-Eastern Australia. Ph.D. Thesis, Charles Sturt University, Wagga Wagga, Australia, 2013. [Google Scholar]

- Australian Bankers’ Association. Agriculture in Australia: Activity and Financing, Economic Report; Australian Bankers’ Association Inc.: Sydney, Australia, 2016. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Assets | Liabilities |

|---|---|

| Land $2,500,000 @$2500/ha × 1000 Hectares 1 | Five opening debt to equity (D:E) ratio scenarios:

|

| Machinery $500,000 | |

| Livestock $674,965 approximately according to the market value of ewes 2 | |

| Total Assets: $3,674,965 | Total Liabilities: $0; $333,000; $613,000; $847,000; $1,050,000 |

| Historical Prices and Quantities | |||||||

|---|---|---|---|---|---|---|---|

| Input | Minimum | Maximum | Mean | Median | SD | Distribution | Parameter |

| Wool clean 20 µm ($/kg) | 9.5 | 16.5 | 13.0 | 13.0 | 2.0 | Uniform | (9.5, 16.5) |

| Net wool cut (kg) | 8695.2 | 17,173.3 | 15,760.2 | 16,075.8 | 1194.2 | Pert | (8695.2, 17,173, 17,173) |

| Price cwt mutton 18–24 kg ($/kg) | 1.7 | 4.9 | 3.3 | 3.3 | 0.9 | Uniform | (1.7, 4.9) |

| Price merino sheep skin 24.1 kg + 1.5″–2″ ($/skin) | 6.6 | 24.6 | 15.1 | 14.9 | 3.7 | Triangle | (6.5, 14.1, 24.6) |

| Ewes sold cast for age (numbers) | 791.0 | 961.6 | 847.9 | 841.0 | 40.2 | Triangle | (791, 791, 961.6) |

| Net cwt of ewes sold (kg) | 23.7 | 29.4 | 27.5 | 27.8 | 1.4 | Triangle | (23.7, 29.4, 29.4) |

| Price cwt Trade lamb 18–22 kg ($/kg) | 4.0 | 6.4 | 5.2 | 5.2 | 0.7 | Uniform | (4, 6.4) |

| Price cwt Light lamb 12–18 kg ($/kg) | 3.2 | 6.4 | 4.8 | 4.8 | 0.9 | Uniform | (3.2, 6.4) |

| Price lamb skin 16.1–20 kg 1″–2″ ($/skin) | 3.4 | 19.3 | 10.8 | 10.5 | 3.3 | Triangle | (3.4, 9.7, 19.3) |

| Wether lambs sold (numbers) | 2332.6 | 2863.0 | 2686.2 | 2707.6 | 125.0 | Triangle | (2332.6, 2863, 2863) |

| Net cwt of wether lambs sold (kg) | 4.6 | 18.6 | 13.9 | 14.5 | 3.3 | Triangle | (4.6, 18.6, 18.6) |

| Ewe lambs sold (numbers) | 2332.4 | 2866.0 | 2688.1 | 2709.7 | 13.1 | Triangle | (2332.4, 2866, 2866) |

| Net cwt of ewe lambs sold (kg) | 5.0 | 16.5 | 12.7 | 13.1 | 2.7 | Triangle | (5.1, 16.5, 16.5) |

| Historical Total Variable Costs and Quantities | |||||||

| Total shorn (numbers) | 4897.5 | 4939.9 | 4915.1 | 4913.9 | 9.0 | Triangle | (4897.5, 4908, 4940) |

| Ewe (numbers) | 4855.8 | 4900.6 | 4885.7 | 4887.5 | 10.5 | Triangle | (4855.8, 4900.6, 4900.6) |

| Lamb (numbers) | 4666.2 | 5726.0 | 5372.7 | 5415.6 | 249.8 | Triangle | (4666.2, 5726, 5726) |

| Ewes ($/head) | 93.8 | 190.9 | 126.1 | 122.2 | 22.9 | Triangle | (93.8, 93.8, 190.9) |

| Ewes bought (numbers) | 1042.0 | 1221.9 | 1115.3 | 1109.7 | 38.6 | Triangle | (1042.1, 1082, 1221.9) |

| Feed wheat prices (AUD/t) | 228.4 | 771.2 | 318.8 | 298.6 | 76.5 | Pert | (228.4, 228.4, 771.2) |

| Total supplement fed (tonnes) * | 0.0 | 1357.5 | 647.5 | 647.5 | 409.0 | Uniform | (0.0,1357.5) |

| Inputs without Historical Data | Minimum | Most Likely | Maximum | ||||

| Shearing ($/head) | 11.4 | 11.9 | 12.1 | Pert | (11.4, 11.9, 12.1) | ||

| Husbandry ($/ewe) | 7.8 | 9.0 | 10.6 | Pert | (7.8, 9.0, 10.6) | ||

| Husbandry ($/lamb) | 500 | 746 | 2500 | Pert | (7.8, 9.0, 10.6) | ||

| Rams replacement ($/ram) | 35.6 | 38.9 | 40.5 | Pert | (500, 746, 2500) | ||

| Pasture costs ($/ha) | 26.5 | 26.5 | 26.5 | Pert | (35.6, 38.9, 40.5) | ||

| Pasture establishment costs ($/ha) | 11.4 | 11.9 | 12.1 | Pert | (24.2, 26.5, 27.6) | ||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | 19 | 20 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1. Wool clean 20µm ($/kg) | 1.0 | |||||||||||||||||||

| 2. Net wool cut (kg) | 0.5 | 1.0 | ||||||||||||||||||

| 3. Price cwt mutton 18–24 kg ($/kg) | 0.4 | 0.4 | 1.0 | |||||||||||||||||

| 4. Price merino sheep skin 24.1 kg + 1.5″–2″ $/skin) | 0.6 | 0.3 | 0.2 | 1.0 | ||||||||||||||||

| 5. Ewes sold cast for age (numbers) | −0.4 | −0.6 | 0.0 | −0.4 | 1.0 | |||||||||||||||

| 6. Net cwt of ewes sold (kg) | 0.0 | 0.0 | 0.6 | 0.1 | 0.1 | 1.0 | ||||||||||||||

| 7. Price cwt Trade lamb 18–22 kg ($/kg) | 0.4 | 0.3 | 0.9 | 0.3 | 0.0 | 0.5 | 1.0 | |||||||||||||

| 8. Price cwt Light lamb 12–18 kg ($/kg) | 0.5 | 0.4 | 1.0 | 0.3 | 0.0 | 0.5 | 1.0 | 1.0 | ||||||||||||

| 9. Price lamb skin 16.1–20 kg 1″–2″ ($/skin) | 0.6 | 0.3 | 0.2 | 1.0 | −0.4 | 0.0 | 0.3 | 0.2 | 1.0 | |||||||||||

| 10. Wether lambs sold (numbers) | 0.1 | 0.5 | 0.2 | 0.1 | −0.4 | 0.1 | 0.1 | 0.1 | 0.2 | 1.0 | ||||||||||

| 11. Net cwt of wether lambs sold (kg) | 0.1 | 0.3 | 0.5 | 0.0 | −0.1 | 0.6 | 0.4 | 0.3 | 0.0 | 0.2 | 1.0 | |||||||||

| 12. Ewe lambs sold (numbers) | 0.1 | 0.5 | 0.2 | 0.1 | −0.4 | 0.0 | 0.1 | 0.1 | 0.2 | 1.0 | 0.2 | 1.0 | ||||||||

| 13. Net cwt of ewe lambs sold (kg) | 0.1 | 0.3 | 0.4 | 0.0 | −0.1 | 0.6 | 0.3 | 0.3 | 0.0 | 0.2 | 1.0 | 0.2 | 1.0 | |||||||

| 14. Total shorn (numbers) | 0.0 | −0.1 | 0.2 | 0.1 | −0.2 | 0.2 | 0.2 | 0.2 | 0.1 | 0.1 | 0.0 | 0.0 | 0.0 | 1.0 | ||||||

| 15. Ewe (numbers) | −0.5 | −0.2 | −0.1 | −0.5 | −0.2 | 0.0 | −0.2 | −0.2 | −0.5 | 0.2 | 0.2 | 0.2 | 0.2 | 0.3 | 1.0 | |||||

| 16. Lamb (numbers) | 0.1 | 0.5 | 0.2 | 0.1 | −0.4 | 0.1 | 0.1 | 0.1 | 0.2 | 1.0 | 0.2 | 1.0 | 0.2 | 0.1 | 0.2 | 1.0 | ||||

| 17. Ewes ($/head) | 0.4 | 0.4 | 0.9 | 0.4 | 0.0 | 0.6 | 0.9 | 1.0 | 0.3 | 0.2 | 0.4 | 0.2 | 0.4 | 0.2 | −0.1 | 0.2 | 1.0 | |||

| 18. Ewes bought (numbers) | −0.4 | −0.1 | 0.5 | −0.2 | 0.2 | 0.4 | 0.5 | 0.5 | −0.2 | 0.1 | 0.0 | 0.1 | 0.0 | 0.2 | 0.3 | 0.1 | 0.5 | 1.0 | ||

| 19. Feed wheat prices (AUD/t) | −0.2 | −0.4 | −0.3 | −0.3 | 0.4 | −0.2 | −0.2 | −0.4 | −0.3 | −0.3 | −0.1 | −0.3 | −0.1 | −0.4 | −0.3 | −0.3 | −0.4 | −0.3 | 1.0 | |

| 20. Total supplement fed (tonnes) | −0.2 | −0.6 | −0.5 | −0.3 | 0.2 | −0.5 | −0.4 | −0.4 | −0.3 | −0.6 | −0.7 | −0.5 | −0.7 | −0.1 | 0.0 | −0.5 | −0.5 | −0.1 | 0.3 | 1.0 |

| KPIs | 0% Opening D:E Ratio | 10% Opening D:E Ratio | 20% Opening D:E Ratio | 30% Opening D:E Ratio | 40% Opening D:E Ratio | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Year 0 | Year 10 | Year 0 | Year 10 | Year 0 | Year 10 | Year 0 | Year 10 | Year 0 | Year 10 | |

| Assets | $3,674,965 | $3,301,968 | $3,674,965 | $3,251,363 | $3,674,965 | $3,229,824 | $3,674,965 | $3,218,557 | $3,674,965 | $3,211,812 |

| Debt | $0 | $332,822 | $333,000 | $1,047,099 | $613,000 | $1,652,257 | $847,000 | $2,155,493 | $1,050,000 | $2,594,351 |

| Equity | $3,674,965 | $2,868,199 | $3,341,965 | $2,146,854 | $3,061,965 | $1,536,122 | $2,827,965 | $1,043,859 | $2,624,965 | $597,946 |

| Gearing D:E * | 0% | 12% | 10% | 49% | 20% | 108% | 30% | 206% | 40% | 434% |

| Equity E:A * | 100% | 87% | 91% | 66% | 83% | 48% | 77% | 32% | 71% | 19% |

| Solvency D:A * | 0% | 10% | 9% | 32% | 17% | 51% | 23% | 67% | 29% | 81% |

| Year 1 | Year 10 | Year 1 | Year 10 | Year 1 | Year 10 | Year 1 | Year 10 | Year 1 | Year 10 | |

| ROC * | −0.1% | 0.5% | −0.2% | 0.5% | −0.1% | 0.5% | −0.2% | 0.5% | −0.2% | 0.5% |

| ROE * | −1.1% | −1.1% | −1.7% | −2.7% | −2.2% | −5.2% | −2.7% | −9.5% | −3.2% | −19.2% |

| TGM | $99,749 | $121,273 | $99,035 | $120,453 | $99,570 | $120,642 | $99,053 | $120,693 | $99,185 | $121,345 |

| EBIT | −$5251 | $16,273 | −$5965 | $15,453 | −$5430 | $15,642 | −$5947 | $15,693 | −$5815 | $16,345 |

| NP | −$41,251 | −$30,766 | −$55,285 | −$58,661 | −$65,950 | −$80,103 | −$75,827 | −$99,034 | −$83,815 | −$114,634 |

| Year 0 | Year 0 | Year 0 | Year 0 | Year 0 | ||||||

| NPV | −$1,328,092 | −$1,333,242 | −$1,332,017 | −$1,327,591 | −$1,331,184 | |||||

| MIRR | −0.5% | −0.5% | −0.5% | −0.5% | −0.5% | |||||

| Year 10 | Year 10 | Year 10 | Year 10 | Year 10 | ||||||

| CVaR10 | −$4,927,658 | −$5,119,387 | −$5,281,562 | −$5,416,217 | −$5,535,020 | |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Godfrey, S.S.; Nordblom, T.; Ip, R.H.L.; Robertson, S.; Hutchings, T.; Behrendt, K. Drought Shocks and Gearing Impacts on the Profitability of Sheep Farming. Agriculture 2021, 11, 366. https://0-doi-org.brum.beds.ac.uk/10.3390/agriculture11040366

Godfrey SS, Nordblom T, Ip RHL, Robertson S, Hutchings T, Behrendt K. Drought Shocks and Gearing Impacts on the Profitability of Sheep Farming. Agriculture. 2021; 11(4):366. https://0-doi-org.brum.beds.ac.uk/10.3390/agriculture11040366

Chicago/Turabian StyleGodfrey, Sosheel S., Thomas Nordblom, Ryan H. L. Ip, Susan Robertson, Timothy Hutchings, and Karl Behrendt. 2021. "Drought Shocks and Gearing Impacts on the Profitability of Sheep Farming" Agriculture 11, no. 4: 366. https://0-doi-org.brum.beds.ac.uk/10.3390/agriculture11040366