Value and Sustainability of Emerging Social Commerce Professions: An Exploratory Study

Department of Computer Science and Software Engineering, School of Engineering, Auckland University of Technology, Auckland 1010, New Zealand

*

Author to whom correspondence should be addressed.

Information 2022, 13(4), 178; https://0-doi-org.brum.beds.ac.uk/10.3390/info13040178

Submission received: 3 January 2022

/

Revised: 17 March 2022

/

Accepted: 29 March 2022

/

Published: 31 March 2022

(This article belongs to the Special Issue Information Technology and Consumer Behavior: Challenges and Opportunities)

Abstract

:Recent advances in social commerce and mobile technology have led to the emergence of new professions such as vlogging, blogging and virtual pop-up store owning. Starting initially as hobbies, the services provided by these ‘new professionals’ have become ubiquitous and are being used by customers from many different countries and backgrounds. This paper reports on a study that first explored the views and opinions of new professionals from several fields (using a qualitative approach), and then the views of their potential customers (a quantitative study informed by UTAUT2—the extended Unified Theory of Acceptance and Use of Technology). The results indicated that new professionals both create and co-create value with their customers, peers, and some existing, traditionally established professions. The results also indicated that the intended audience/customers of the new professional businesses had a positive perception of their long-term commercial sustainability. Customers’ intention to use the new professional services in the future were predicted mostly by the behavioral characteristics of hedonic motivation and habit. The research contributes by empirically investigating the value creation and co-creation processes in a context that is yet to attract academic interest. It proposes a value creation and co-creation framework that draws on the interactions of the main players.

Keywords:

blogging; vlogging; pop-up store; sCommerce; mCommerce; social media; UTAUT2; content analysis; customer survey; value co-creation1. Introduction

With their ubiquitous presence, improved functionality and a variety of information access features, mobile devices today play a natural role in everyday life [1]. The use of smart phone connection to the Internet and mobile applications (apps) to buy and sell products and services over mobile networks is referred to as mobile commerce (mCommerce) [2]. MCommerce is growing fast: in recent years, the number of mCommerce transactions across the globe has significantly surpassed the number of transactions concluded through personal computers [3]. Mobile access to the Internet has also facilitated an explosive growth in the use of social networking services (SNS) offered by Facebook, Twitter, Instagram, BlogSpot and others social media platforms [4]. Similarly to mobile devices, SNSs are omnipresent in individuals’ daily lives, especially in the lives of younger generations [5].

As mobile technology and in particular, mobile apps, have caused changes in customer behavior, so have businesses transformed and refocused their strategies to include developing and maintaining networks with current and potential customers [6]. These include the use of SNSs for creating social media-based shopping outlets, which is known as social commerce (sCommerce). In sCommerce, businesses utilize social media outlets as a means of assisting customer communication and other social activities to support buying and selling services and goods online, and to draw on consumer recommendations and other customer generated content to support business growth and financial stability [7,8,9].

While businesses operating is traditional areas such as banking and retail have added mCommerce and sCommerce initiatives to their brick-and-mortar professional offerings, mCommerce and sCommerce have also helped create some entirely new professions. For example, Australia’s first professional Instagram photographer, Lauren Bath gave up her day job as a chef to become a vlogger—a profession she says she ‘invented’ herself. A large and growing number of followers on Instagram allowed Bath to make it a new career pathway [10]. A new profession with a relatively longer history is that of bloggers, who write about topics that they are passionate about, and thrive in the virtual communities of similar-minded individuals who follow their blogs [11]. In the sub-genre of micro blogging, individuals and businesses use SNSs for informal sharing of ideas and collaboration [12]. Professional bloggers and vloggers meet and socialize at conferences and other social events such as DigiMarCon [13] and VidCon [14]. Yet, another category of new professionals are the virtual pop-up store-owners. Unlike brick-and-mortar businesses which also sell and advertise their goods on social media alongside their own website or at an Amazon storefront, virtual pop-up store owners are small-scale sellers of goods and services who use only social media sites such as Instagram and Etsy [15], with no other presence on the web. Their products are often handmade, e.g., jewelry or baked goods.

Recognized profession classifications can be found at government web sites such as the Bureau of Labor Statistics (USA) and the Office of National Statistics (UK). Prior to 2020, none of the new professions above were included in the Standard Occupational Classification (SOC) lists published by these two organizations [16,17]. Recently, a mention of ‘blogger’ was added to the description of the category ‘writers and authors’ in the SOC published by the Bureau of Labor Statistics. (Further in the text, professions/occupations listed in the SOCs published by the Bureau of Labor Statistics and the Office of National Statistics prior to 2020 are referred to as’ traditional’ or ‘established’, in the sense that these professions/occupations have been recognized and accepted by society.)

According to Crosby [18], new professions usually emerge when people need businesses to do tasks that have never or rarely been carried out before. Factors influencing the process include both technological advances and societal changes. Crosby defines a new occupation as ‘one that is not included in the most current occupational classification system’, while an emerging occupation is ‘one that has small employment numbers but is expected to get larger in the future’. Applying Crosby’s definition, vlogging and virtual pop-up store owing can be classified as new professions/occupations, while blogging can be tentatively classified as an emerging profession/occupation; the change factor leading to the emergence of these new professions is the opportunity to use new media for authoring content (web sites).

Current research considering blogging, vlogging and pop-up store owning as new professions or occupations is scarce. Most of the prior work in related areas includes investigations of specific aspects of blogging and vlogging as social interactions, rather than as professional activities. For example, Nistor et al. [19] investigated how new communication channels such as blogging can be used to enhance information exchange in online learning. Other studies explored the impact of blogging on consumer behavior. Ing and Ming [20] found that consumer attitude towards blogger recommendations was highly influenced by the perceived trustworthiness of the blogger, and had an impact on the intention to purchase the goods recommended. A similar result was reported in an empirical study of vlog content and vlogger characteristics [21]. Arieta et al. [22] identified blogger’s social influence and customer experience as the determinants of customer loyalty towards the blogger.

The broad impact of using digital platforms including social media on the way goods and services are created and distributed was investigated by Kenney and Zysman [23]. The authors propose a work and value creation taxonomy according to which the new professionals can be construed as ‘consignment content’ creators who monetize their products and services through the use of social media platforms. The customers of the new professions are ‘non-compensated’ value creators; they generate data from which value can be derived. The taxonomy provides a useful view of the new professional services as a manifestations of the emerging ‘platform economy’; however, it does not consider explicitly the interactions between the participants in the platform-mediated content creation activities that are an essential part of the new professional services. More recently, Törhönen et al. [24] identified video creation for commercial gain as an entrepreneurial activity; they also highlighted the need for further research into how and where value was formed, and into the interactions of the participating entities including video content creators and their audiences.

This research addresses the literature gaps identified above. It investigates how new and emerging professions take advantage of the opportunities offered by the fast developing communication channels and platforms to achieve a transition from being personal hobbies to economically and socially sustainable occupations that successfully leverage the advances in mobile technology and the changing society dynamics (recently accelerated by the ongoing global COVID-19 pandemic [25]). The research explores the value creation processes and social interaction flows that occur, and attempts to obtain a measure of the long-term sustainability of the new professional businesses.

In the industrial era, value creation attempts to increase revenue and profits in the form of improving the value of products and services to the consumer; however, the value creation process was mostly asymmetrical in the sense that decisions about the value proposition were made by the business, with little direct input from customers. When a customer accepted a product, they paid for its face value, even if they could not realize it (i.e., if the product did not meet some of their specific needs) [26]. However, control over value creation has since shifted to include more customer input obtained through customer–provider interaction much earlier in the value creation process [27]. Customers and service providers become engaged in value-cocreation—a symbiotic relationship between the two parties whose actions contribute to each other’s benefit [28]. For customers, this means receiving serviced/products that satisfy their specific needs as they can easily find and consider other customers’ opinions on social media outlets such as Twitter, Facebook and Instagram; there are companies that are built exclusively on rating and reviewing business by customers (e.g., TripAdvisor). For businesses, value co-creation contributes towards their economic and social sustainability [29]. For example, Starbucks launched the ‘My Starbucks Idea’ platform, where customers presented their views about the company’s practices and gave new ideas regarding future steps that the company should take [30]. Value co-creation also requires effective interaction between the participating parties [31].

The new professionals (bloggers, vloggers and virtual pop-up store owners) use social media and mobile technology to create new professional content and commercialize it. They use social networking to promote and maintain a transparent dialogue between new professionals and their audience/customers, and facilitate a mutually beneficial value creation and co-creation processes, and thus may add to the social capital of the society by creating sustainable value [32]. As the research aims to identify and investigate the value creation processes and social interaction flows that occur, the first research question was formulated as:

- How do the new professionals leverage mobile technology and social media to create value?

Rashid et al. [33] propose that customer’s experience and motivation shared within the online user community may impact positively on value co-creation and innovation. Furthermore, successful vale co-creation depend on the mutual understanding of the needs and actions of each participant [34]. In particular, shared customer experiences, satisfaction and expectations have an impact of the perceived value of the new professional services and thus, on the viability of the new professional businesses. Therefore, the second research question guiding the study was formulated as:

- 2.

- How do the intended audience/customers of the new professions perceive their services?

To address the research questions, the study followed a mixed method approach, aiming to achieve meaningful results by combining the strengths of the quantitative and qualitative research techniques and conceptualizations [35]. Subsequently, the empirical investigation was conducted as a sequence of two studies (Study 1 and Study 2). The theoretical underpinning of the empirical investigations draws on prior research in the areas of value creation and co-creation, and on user acceptance of technology.

2. Materials and Methods

Study 1 conducted a qualitative investigation of the views and opinions of the new professionals by surveying a selection of new profession representatives, while Study 2 explored quantitively the perceptions of the audience/customers of these new professions through a survey. The theories and methods used in each study are described below.

2.1. Study 1: The Perspective of the New Professionals

The qualitative component of the research investigated how the new professionals established their respective businesses and how they perceived their roles as value creators. The study considers the new professional services from the perspective of service dominant logic (SDL). SDL conceptualizes value as a ‘co-creative endeavor’ (rather than something created by a single entity); value creation/co-creation is seen not as a linear processes, but as a service ecosystem comprising dynamic and contextually grounded processes and information flows [36]. SDL posits that value co-creation occurs only when the customer is an active participant in the service exchange; thus, co-created value is determined by the customer’s use of the service or the service interaction experience (value-in-use) rather by the service provider’s value proposition (value-in-exchange) [37]. Furthermore, service ecosystems are often complex; they may include multiple participants and their interrelationships and communication flows, through which value-co-creation is coordinated [28]. The service ecosystem view provides a service-based theoretical perspective for the study of emerging business models, which leverage social connectivity and networks support active customer engagement [38]. Therefore, an SDL perspective is suitable for the study of the new professional services as rely exclusively on social media to promote and offer their services, and on customer-to-customer communication flow to gauge customer perceptions about their experiences and service acceptance, and benefit from customer generated ideas.

Considering the impact of technology on value co-creation, service ecosystems are socio-technical systems that enable value co-creation through integrating participant resources including the information and communication technologies involved in the service exchange [39]. Therefore, new technologies such as mobile technologies have a critical role in the value co-creation ecosystem; they not only support but partner with social media. By providing multiple communication channels and flexible access to SNN platforms, they may act as value co-creation catalyzers [40]. This is another important consideration, as the new professional services studied in this research are delivered predominantly through mobile channels and depend on customer access to the mobile apps of the respective social media platforms.

2.1.1. Participant Selection

The use of sCommerce and mCommerce in creating their professional identity was the primary criterion for selecting the research participants in Study 1. The authors used their personal networks and searched the web in order to identify potential research participants. Twelve invitations were issued, and six new professionals were recruited (two participants from each new profession described below).

Bloggers create content such as small articles or essays and publish them on their own websites or on dedicated platforms such as WordPress, InstaBlogs and BlogSpot. According to Target Internet, the most financially successful bloggers in 2021 earned up to a million a month [41]. Figure 1 shows the website of the top earner Tim Sykes, who trades in ‘penny stocks’, and also teaches his audience how to trade.

Vlogs are videos published by individuals on video hosting and sharing social media outlets such as YouTube. Vlogs range from video tutorials on various fields such as programming, fashion, gaming, photography, music and life experiences, to entertainment videos like comedy sketches, talk shows and social or other experiments. Recognizing vlogger business success, the Forbes magazine started releasing the list of the highest paid YouTube vloggers [42]. In 2020, the top earner’s income was estimated as $29.5 million (Ryan Kaji, who reviews children’s toys and other merchandise—Figure 2).

Lastly, virtual pop-up store owning entails goods/services being sold by individuals on outlets like Facebook and Instagram. Virtual pop-up stores are not hosted as commercial retail websites; rather just a phone number, an email address or a social media profile is used to contact the seller. An example is shown in Figure 3.

2.1.2. Data Gathering through Semi-Structured Interviews

Qualitative data were gathered through semi-structured interviews following the guidelines provided in [43]. The 17 indicative questions asked participants to describe their respective professions, and to elaborate on how they used mCommerce and sCommerce to start their businesses, and to create ongoing value. The questions also attempted to investigate the skills required for their profession, the level of preparedness and prior knowledge they felt were needed, and the complications and benefits of using mobile technology and social media. Also of interest were participant views about their audience/customer base, and any other in-sights they were willing to share.

The interviews (lasting from 20 to 49 min) were conducted over Skype and/or Facebook Messenger; the audio data were recorded and transcribed. The transcription process rendered a fully anonymized document containing about 20,000 words of text. To support the subsequent coding, the text was first interpreted and structured as a collection of data segments, with each segment containing one or more sentences related by topic [44].

2.1.3. Interview Data Coding

Coding plays an important role in qualitative data analysis as codes are developed to bring out the primary content of the data collected [45]. In Study 1, descriptive coding was used as the primary means of summarizing participants’ responses as the descriptive code emerging from a unit of qualitative data gives a succinct representation of its topi [46]. Coding was performed iteratively, with all segments re-checked every time a new descriptive code was defined. The final set of descriptive codes comprised 44 codes; an example of a descriptive code is provided in Table 1.

2.2. Study 2: The Customer Perspective

To develop a customer perspective on the perceived value of the services offered by the new professionals, the study draws on one of the most widely used models for the study of customer acceptance and continuous use of technology—the extended Unified Theory of Acceptance and Use of Technology (UTAUT2) [47,48]. Introduced by Venkatesh et al. [49], UTAUT2 builds on the earlier version named UTAUT [50] and combines constructs from previously developed and validated technology adoption models. UTAUT2 postulates that the factors influencing user intention to use new technology include expectations about technology performance and the level of effort needed to use it, the perceived price value balance, the perceived enjoyment (hedonic motivation), the perceived quality of the facilitating conditions, the user’s habits, and the user’s perceptions about the attitude of important others (friends, family, co-workers) towards the new technology. Age, gender and experience are moderating factors. Technology use behavior (actual use) is influenced by the user’s intention (moderated by experience), habit and facilitating conditions.

UTAUT2 was chosen as the theoretical foundation for the investigation of customer acceptance of the new professional services as its broad range of adoption factors is well suited to the exploratory nature of this research. Furthermore, UTAUT2t explicitly includes variables related to social influence, perceived value and actual use that may provide an insight into the sustainability of the new professional services. In addition, the model allows us to adapt the variable definitions to reflect the context of this research, and has been used in studies in related areas such as mCommerce acceptance, e-service adoption, mobile Internet usage and blog adoption [48]. For example, Muhammad et al. [51] adapted UTAUT2 for the investigation of customer willingness to generate sizeable social media content. In this research, the model was expanded by adding a new construct (Participation), which was supported by the findings of Study 1. The new construct reflects the importance of customer participation [26].

2.2.1. Research Design

The outcomes of Study 1 informed the research design of the subsequent quantitative Study 2. Quantitative data were gathered through an anonymous public online survey and analyzed statistically. The survey questions explored the views and opinions of the audience/customers of the new professions on the use of the products and services offered by the new professions and on the new professions’ commercial sustainability. The survey questions were based on the constructs defined below.

The themes identified in Study 1 were examined through an UTAUT2 lens to gauge the support provided for the UTAUT2 constructs. It was established first that the themes did not refer explicitly to performance expectancy, effort expectancy and facilitating conditions; therefore, these constructs were considered outside the scope of Study 2 and were not investigated through the survey. The definitions of the supported constructs (social influence, hedonic motivation, price value, and habit) were adapted to the context of the study, as explained next.

- Social influence (SI): The extent to which an individual perceives that ‘important others’ believe he or she can accept the services of the new professions. For example, an individual may watch a vlog because their family, friends, peers, colleagues, superiors or role-models are also doing so. The findings of the qualitative Study 1 supported the inclusion of this construct. As shown in theme 15, the content of a vlog could ‘go viral’ with the help of messenger applications sending it to the extended ‘family and friends’ network. Additionally, the interviewees themselves were susceptible to social influence when it came to selecting social media outlets. As seen in themes 2 and 17, participants acceded to using certain social media outlets only because they had friends, family and peers using them. Since the selection of social media outlets because of social influence was common in the new professionals themselves, it was considered of interest to also investigate the items in this construct with respect to their intended audience.

- Hedonic motivation (HM): The level to which the customer enjoys or gains pleasure from leveraging the goods and services provided by the new professions. For instance, being able to order handmade products targeting niche markets. As seen in theme 16, customers and audience enjoyed the services offered, as they left positive comments and reviews of the content, along with requests for more content.

- Price value (PV): The cost and pricing structure. These may have a significant impact on the acceptance of the new professions. For example, some vlogs and blogs may be free, while others require a paid subscription. As seen in theme 16, participants described their customers as proactively requesting new and customized content and products; this may be interpreted as satisfaction with the price and the corresponding value of the services provided.

- Habit (H): The extent to which people tend to stick to a learned routine, for example regularly ordering merchandise from a particular online pop-up store. Again, in theme 16, participants indicated the existence of a loyal customer base, with some regularly following from the very start, ‘liking’ and commenting on the content. This may be interpreted as the development of a customer habit, such as regularly reading a particular blog.

Further examination of the interview data and especially theme 16 indicated that according to interviewees, customer participation was paramount to the success of the new professions. The importance of customers’ comments and criticism, their informed insight, compliments and requests, and the engagement with the audience were often mentioned and highlighted by all participants. For example, participants reiterated the importance and impact of audience participation and talked about how valuable the interactions with customers were in themes 1, 9, 15 and 17. To capture customer participation, a new construct (Participation) was developed.

- 5.

- Participation (P) reflects customer trust in the products and services provided by new professionals, giving positive or negative feedback on services and products and engaging proactively with the new professional in the form of requests or suggestions.

Finally, use intention and behavior were investigated through questions related to continual intention to use, and actual use (adapted from UTAUT2). The survey also included a question exploring customer views on the long-term commercial sustainability of the new professions.

- 6.

- Continual intention to use (CI) refers to the intention of the customers/audience to continue using the products/services offered by the new professions in future (e.g., one may intend to watch vlogs, read blogs or buy products from pop-up stores in future).

- 7.

- Actual use (AU) refers to the way customers actually use the goods and services offered by the new professionals (e.g., the actual frequency of watching vlogs, reading blogs or purchasing from pop-up stores).

- 8.

- Sustainability (SU) refers to customer perceptions of the long-term commercial viability of the new professions, i.e., the expected future availability of the services and the products offered.

2.2.2. Survey Instrument

The relevant UTAUT2 items were adapted to the research context and included as survey questions (Appendix A, Table A1). A five-point Likert scale was used to measure the items associated with SI, HM, PV, H, CI and SU (1—strongly disagree to 5—strongly agree). The scale for measuring P was defined as 1—never, 2—rarely, 3—sometimes, 4—frequently and 5—always. The e items associated with AU were measured on the scale 1—never, 2—every year, 3—every month, 4—every week and 5—every day.

The survey questionnaire comprised three sections (one each for the professions of vlogging, blogging, and virtual pop-store owing). The respondents could fill in either one or more of the them depending on their knowledge and actual use. In addition, respondents were asked questions about age, gender and online experience (hours spent online per day). The questionnaire was designed using the online tool ‘Qualtrics’ and pilot tested by the researchers and a layman with no vested personal interest in the research. In its final version, the survey was advertised on several social media sites.

2.2.3. Study Sample

A total of 290 responses were received, out of which 178 responses were found acceptable (two respondents clicked on ‘Do Not Consent’ in the consent form and were removed from the survey, 14 skipped all three sections and were removed and 15 were removed because they did not complete the survey). Overall, 135 individuals completed the vlogging section of the survey, 129 completed the blogging section, and 89 completed the pop-up store owning section. A total of 56 respondents completed all three sections, and 63 completed two sections.

Out of the 178 respondents, 111 were female (62.36%), 66 were male (37.08%) and one person preferred not to disclose their gender. There were no respondents above 55 years of age and minority were 35 or older (7 participants were in the 35–44 age group and 10 participants were in the 45–54 age group). Most respondents (124) belonged to the 18–24 age group followed by the 25–34 age group (37). Thus, respondents in the 18–34 age group dominated the Study 2 sample.

With regard to time spent online per day, a majority of respondents (106 out of 178, or 59.55%) spent more than four hours a day online, 21 (11.8%) spent about three to four hours online, 22 (12.46%) spent two to three hours, 26 (14.61%) spent between one or two hours and only three (1.69%) spent less than one hour on the Internet. Overall, a majority of respondents (71.35%), spent three or more hours online each day. Out of the dominant group (18–34 years of age), 72.67% of respondents spent more than three hours online every day. Furthermore, 61.54% of the respondents in the dominant group (18–34 years of age) were female, thereby indicating that in the sample, there were more young, female new profession customers, compared to young male new profession customers.

3. Results

3.1. Thematic Analsysy of the Views and Opinions of the New Professionals

The higher-level analysis of the qualitative data started with a search for associations amongst the descriptive codes, which led to organizing the descriptive codes into five broad categories as shown in Table 2. This categorization simplified the code structure and highlighted emerging themes and concepts from the qualitative data.

To complete the analysis, the data represented by each code category were systematically re-examined and interpreted further to identify coherent themes that captured the key points made by the research participants. The 20 themes that emerged are summarized below (organized by code category).

3.1.1. Themes around ‘Social Media and sCommerce’

- 1.

- Use of multiple social media channels

The increased popularity and outreach of their services and goods were due to the strong reliance on advertising and promoting themselves through multiple outlets, looking for a channel where potential customers may be more active. Being active on several outlets enabled creating audience awareness, which may lead to attracting more viewers/readers/customers.

- 2.

- Criteria used when choosing social media channels

The selection criteria for social media outlets specific to their professions depend on a variety of reasons, including search results on the Internet and the social influence from friends, family and peers. In fact, peer influence often leads to the audience/customers transitioning into becoming new professionals themselves. This influx of ‘newer’ new professionals because of the increased outreach of the goods and services offered by these professions suggests a favorable outlook for long-term commercial sustainability.

- 3.

- Perpetual learning and professional development along with adaptation to innovations in the features of SNS

New professionals actively branch out to acquire new knowledge and attempt new features. Improving their skills (e.g., using analytics) benefit their professions and help develop the services and products suggested by customers. New professionals exhibit flexibility in the adoption of new features introduced by SNS as well as their understanding and utilization of existing features in their effort to add value to the goods/services they offered.

- 4.

- Leveraging new features—hashtags

The practice of using hashtags increases the audience reach and thereby attracts more customers and/or a higher quality audience. Using hashtags relevant to their field or topic of discussion leads to improved search results for prospective customers who may be interested in the goods/services offered by them.

- 5.

- The importance of planning

Planning their social media posts both in terms of the frequency of the posts as well as the specific timing of the post uploads helps not only to ensure optimal visibility of their posts and attract new viewers/customers, but also to retain their existing audience. In fact, being an infrequent uploader can alienate one’s existing audience and customers.

- 6.

- Drawbacks of social media outlets and new professionals’ suggestions for improvement

Even though social media outlets are the facilitators of their professions, they had faults and limitations, such as inadequate rating systems or unhelpfully presented analytics. Due to their experience and familiarity with operating these outlets, new professionals were able to suggest improvements to existing features, as well as create new features (such as an option to buy on Facebook sites—recently implemented), or even new outlets.

- 7.

- The effect of social media outlet policies

The new professionals are completely reliant on the content policies of these outlets, which could change without much warning. This may put their professions in danger if an outlet’s policy change decreases the visibility of their posts (for example, a policy that changes the order in which posts are displayed). Even worse would be the impact of a major social media outlet being shut down for a period of time.

- 8.

- Cyberbullying

Cyberbullying, even though brought up by just one of the new professionals interviewed may pose a serious threat to the mental well-being of the new professionals. Different from posting negative or unfavorable feedback addressed to brands/companies, commenters may launch harassment or personal attacks against a new professional as individuals, regardless of the professional content or the customer service.

3.1.2. Themes around ‘Mobile Technology and mCommerce’

- 9.

- Usage of mobile devices and technology

The usage of mobile devices and technology by the new professionals was prevalent due to their enhanced operability and portability and also because they facilitated instantaneous interaction with their customers. Additionally, the high-end cameras in the smart phones were critical to producing good quality visuals. Moreover, there seem to be applications used by the new professionals that are available on mobile platforms only (i.e., Snapchat).

- 10.

- Limitations of mobile devices

There are limitations of using mobile devices and technology, which perhaps need to be addressed by developers (e.g., high battery drain when producing high quality videos, and inadequate video editing tools). However, these reasons did not seem to deter the new professionals from making use of mobile devices. This was partly because, as stated in Theme 9, certain applications had only been created for, and thus could only be accessed through, mobile devices.

3.1.3. Themes around ‘Personal Ambition and Incentives’

- 11.

- New-professionals’ backgrounds

Even though the new professionals came from different backgrounds that were not necessarily related to their current field or even topic of blogging or vlogging or may have no prior experience of selling goods, they evolved and adapted themselves to fit their new professions. This was done by a combination of having some prior interest in the field and developing skills that helped them be effective in their new occupations. Particularly important was that the social media platforms offered ample opportunities and support for newcomers in the field. Additionally, being self-employed and having autonomy over the goods and services they supplied to their customers was advantageous and satisfying, according to participants.

- 12.

- Income and taxes

It may be hard for newcomers in the field to have consistent or regular income through just one channel, but there is an availability of supplementary channels through which they get additional paid work that is related to their skills as bloggers, vloggers and pop-up store owners. New professional services are usually treated as businesses for taxation purposes, which recognizes their value to society.

- 13.

- Supplemental skills required

The main factors influencing the specific additional skills to be learnt before starting in one of the new professions depended on the genre of the new profession being considered. Bloggers needed expertise in writing, vloggers in video editing and content creation, and pop-up store owners—in creating and selling their products. However, these genres had further specificities: food bloggers needed to know about food styling and culinary photography, beauty bloggers needed to be adept at makeup and assessing beauty products, and lifestyle vloggers needed excellent camera presence and had to research for new ideas for their log. Product-specific skills were required for pop-up store owned; for example, an online patisserie must have an expert pastry chef, whereas an apothecary owner should be accomplished in creating products that did not present health and safety risks.

- 14.

- Supplemental equipment required

Similar to supplemental skills, the additional equipment required was specific to the profession. Bloggers and vloggers may require camera equipment in general, but more specifically, beauty bloggers and vloggers may require make-up and clothes to review. Similarly, pop-up store owners would require particular equipment related to their field, such as an adequate kitchen.

- 15.

- Expertise and social media presence

A consistent presence on social media and ongoing innovation were the essential factors in sustaining a new profession and gradually becoming a recognized expert, irrespective of the genre. Moreover, this may lead to progression to the next level in their professions because of the increased business opportunities, such as a pop-up store owner opening an online class or developing a profitable side business line such as selling goods in a physical market.

3.1.4. Themes around ‘Society’s Response and Influence’

- 16.

- Value co-creation with the customers/audience

There is a notable presence of value co-creation activities between the new professionals and their customers. The audience/customers are not just static/passive entities; in fact, they make demands and provide suggestions in the form of direct interaction with the content provider through comments (for example, on the blog or post advertising a product for sale by a virtual store, and also by tagging the new professionals in personal posts and reviews on social media outlets). There has always been a two-way, symmetrical dialogue and interaction between new professionals and their customers. In fact, the new professionals attribute their success to their customers; new professionals try to engage with customers in a meaningful relationship by customizing content, adjusting services and products according to customer feedback and requests, and replying to customer comments. Audience support of new professionals in the form of positive feedback, loyalty and the continual use of the goods and services offered by the new professionals is extremely important. The direct interaction with the audience means that the new professionals are seen as individuals rather than as corporate entities; customers and new professionals perceive and trust each other at a personal level. Responding to comments was how one inherently understood the needs of the customer that led to new ideas and customized content created for the audience; a participant considered her audience base to be her best ‘analytical tool’ because of their fearless approach of saying what they wanted/did not want or what they liked/disliked. Customers reacted positively to being more involved; for example, posting videos and images of the creation of her products made the audience of pop-store owners feel they were to part of the entire process, from creation to delivery. Some ‘bigger’ vloggers and bloggers (the ones with a larger audience base) have expanded to become entrepreneurs by collaborating with traditionally established companies; this was made possible by the support and participation of their audiences.

- 17.

- Social influence

The popularity and use of certain social media outlets by friends, family and their circle of social interactions had also prompted new professionals to adopt them for the purposes of their professions. When new social media outlets were introduced, the participants again sought the opinions of their wider group of social contacts.

- 18.

- Professional outreach—traditional businesses and ‘newer’ professions

New professionals hire other professionals (for example, professional photographers) to support their professions and, in turn, get hired by traditionally established companies to promote their products and services; this contributes to their sustainability and promotes growth.

3.1.5. Themes around ‘New Professional Peer Influence’

- 19.

- Collaborating with peers

New professionals collaborated with peers for mutual benefit, for example to achieve an ‘exchange of audience’. Collaborations with the ‘right’ peer were beneficial, but the opportunities were somewhat limited; as a participant put it, it would be futile to collaborate with someone who had fewer subscribers than herself, while vloggers with a viewership larger than hers may not want to collaborate for the same reason. However, support from their peers and mentors has helped newer professionals to enter the field; participants pointed out that there were better and more easily available opportunities for newcomers in their field compared to the difficulty of entering certain traditionally accepted professions.

- 20.

- Competition and inequity

There are different sets of new professionals within each particular genre (e.g., micro-bloggers and micro-vloggers who produce short blogs and videos on Instagram or Twitter), and also across genres (e.g., aggregate bloggers or vloggers). This leads to competition and rivalry, and possibly to financial loss (for example, the audience of a blogger switching to an aggregator). Potential copyright breaches and unethical use of others’ content was an additional issue raised. There was also a certain inequity between the professionals who were relatively new to the field and already established professionals who had already captured large audiences.

3.2. Statistical Analysis of the Views and Opinions of the Customers of the New Pprofessioaml Services

3.2.1. Actual Use of New Professional Services

Actual use data indicated that blogs were accessed most frequently (69% of the respondents read a blog daily or weekly); similarly, vlogs were viewed every day or every week by 65.93% of the respondents (Table 3). A majority of customers (88.77%), shopped from pop-up stores only monthly or yearly possibly because shopping from pop-up stores entailed the purchase of tangible and possibly more expensive goods, unlike the intangible services offered by vloggers and bloggers. It also appeared that a very small proportion of the responses were provided by individuals who did not use the goods and services offered by the professions, but answered the questionnaire because of their familiarity with the new professions. This may imply that the popularity of new professions is growing and that these particular respondents may become customers in the future. A similar trend was observed in the dominant customer group (18–34 years of age), where 68.84% read blogs and 65.60% watched vlogs at least weekly. Furthermore, 87.18% of these respondents shopped at least yearly from pop-up stores future.

3.2.2. Customer Participation in New Professional Services

In line with the findings of Study 1, the data gathered in Study 2 indicated that customers left ample feedback and constructive suggestions regarding the content that they watched, read, or bought. As shown in Table 4, a relatively high number of customers left positive feedback at least once for each of the three new professions, with blogging attracting the highest response rate (77.5% overall, and 76.3% for the 18–34 years of age group). A smaller but still significant number of respondents left negative feedback at least once; pop-up stores had the highest response rate (55.1% overall and also for the 18–34 years of age group).

The proportion of customers who left positive or negative feedback frequently (always or often—Table 5) was not high (blogging customers left positive feedback most frequently—22.5%, while vlogging and pop-up store customers left negative feedback most frequently—2.2%). While about 50% of the customers left positive feedback regularly (always, often, or sometimes—Table 4), the proportion of customers who regularly left negative feedback was relatively low (the higher number of customers regularly leaving negative feedback was 27%, for pop-up stores). However, 1.1% of the pop-up store customers had indicated that they always gave negative comments. This may be construed as a form of cyberbullying, as mentioned in the findings of Study 1 (theme 8).

The results for leaving negative and positive feedback for the 18–34 years of age group were similar to the results for the whole sample (Table 4, Table 5 and Table 6). In addition, more than half of the vlogging and blogging customers and 44.87% of the pop-up store customers in this age group had never left any negative feedback. This may indicate that at least half of customers in the 18–34 years of age group did not appear to be indulging in cyberbullying with malicious intent against the new professionals.

With regard to requesting content change or suggesting new content options, the highest level of participation was observed in the pop-up store customer segment (57.3%), followed by blogger customers (45.5%) (Table 4). However, the customers in the sample did not post requests for new content or for content change either frequently or regularly (Table 5 and Table 6). The most regularly active customer segment was the pop-up store audience (39.3% posted content requests always often, or sometimes). The customers in the 18–34 years of age group were only slightly more active, and even less active as pop-up store content contributors: 35.9% compared to 39.3% for the whole sample (Table 6).

Overall, the majority of the respondents, irrespective of their age, seemed not to prefer direct engagement with any of the new professional genres, highlighting a relatively weak communication flow from customer to new professional service provider. The results also indicate that in this sample, respondents aged 35 and above were willing to engage in value co-creation digitally despite being potentially less digitally literate compared to the 18–34 years of age group.

In terms of customer trust, 87.6% of the respondents trusted reviews by bloggers, followed by 77.0% who trusted vlogger reviews and 76.4% of customers who trusted products advertised by pop-up store owners (Table 4). However, the number of customers who regularly or frequently trusted new professionals were lower (Table 5 and Table 6). The ‘lack of trust’ in some of the customers may be explained by perceptions about the quality of the service and the personalities of the new professionals and also by external factors such as the influence of friends and associates [52]. The results for the 18–24 years of age group were similar (Table 4, Table 5 and Table 6).

In summary, although the Study 2 sample contained a large group of customers who trusted the new professionals and frequently or regularly contributed comments, requests and suggestions, there was also a group of customers who did not participate directly in value co-creation interactions. However, these customers may still provide value to the new professionals through viewing and/or ‘liking’ the content: as also indicated in the findings is of Study 1 (theme 3), new professionals can access such data through the social medium’s data analytics tools.

3.2.3. Sustainability of New Professional Services

The respondents’ views on new profession sustainability indicated that virtual pop-up store owning was the profession most expected to last long-term (Table 7). A relatively high number of respondents believed that blogging and vlogging will continue to exist (45.7% and 42.2%, respectively), while more than half (64%) were confident that pop-up stores will continue to exist. While a relatively high number of respondents were undecided on the future of the new professions, only a relative minority perceived each of these professions as unsustainable. The views of the respondents from the 18–24 years of age group were similarly distributed, with pop-up store owning again considered most sustainable (62.82%), and 23% with no opinion on the matter. The perceptions of these younger customers are significant, as they will increasingly become the dominant customer group in the long term.

3.2.4. Continual Intention to Use New Professional Services

As shown in the preceding section, a relatively high proportion of customers believed in the continued sustainability of the new professions. These customers may intend to use these services in the future. The findings of this study presented so far suggest that continual intention to use new professional services may be driven by social influence, habit, enjoyment and the perceived value of the service or product.

An exploratory factor analysis was conducted to investigate whether the factor structure of the relevant data aligned with the UTAUT2 constructs used to inform the survey questionnaire (SI, HM, PV and H), and to obtain a measure of the internal reliability of the dataset. Each new profession was considered separately. The software used was IBM SPSS Statistics 24. The complete output of the statistical analysis is available online (Supplementary Materials).

All measurement items (as listed in Appendix A, Table A1) for SI, HM, PV and H were found to be acceptable as none of the correlation coefficients was greater than 0.9, and the determinant of the R matrix for each new profession was greater than 0.00001 (0.001 for blogging, 0.004 for vlogging, and between 0.00001 and 0.001 for pop-up store owning; see Supplementary Materials, Parts SM1, SM2 and SM3). The Bartlett’s measure of sphericity was 0.000 for all new professions, indicating that there was no item redundancy [53]. The Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy (blogging—0.783, vlogging—0.790, and pop-up stores—0.797) was also acceptable or ‘good’, according to Hutcheson and Sofroniou’s [54] recommendations.

Following Stevens [55], factors with loadings below 0.512 (for vlogging and blogging) and below 0.650 (for pop-up stores), were discarded, based on the sample size for these new professions (129. 135, and 89, respectively). The four extracted factors (factors with Eigenvalues greater than one) were considered final as the respective scree plots showed a flattening of the curve after the fourth factor, for all three professions (Supplementary Materials, Parts SM1, SM2 and SM3). Orthogonal rotation (varimax rotation) was used as the factors were assumed to be independent on each other [53].

The factors and the item loadings are shown in Appendix A, Table A2, Table A3 and Table A4. Each of the factors identified corresponded to one of the independent constructs of UTAUT2, that is, hedonic motivation, habit, price–value and social influence. However, social influence contained only three items (SI1, SI2, and SI4) in the case of blogging and vlogging, and only two items (SI1 and SI2) in the case of pop-up stores. In pop-up stores, SI4 became part of the factor corresponding to hedonic motivation. Item SI3 was dropped from blogging and pop-up store owning because it did not have a significant enough factor loading. Regression analysis was used to investigate the factors as potential predictors of the continual intention to use the new professional services.

The quantitative measures of the dependent variables representing SI, HM, PV and H in the regression analysis were computed as the means of the items in each of the extracted factors (for each new profession individually). As the correlation matrices of the two items related to CI showed a high degree of internal consistency (Supplementary Material, Part SM4), the dependent variable CI was measured similarly.

The complete results of the multiple regression analysis for each profession are provided in Supplementary Material, Parts SM5–SM7. Even though some of the one-tail p-values were not less than 0.001 (especially for SI, with p-values higher than the threshold for all three professions), the variables were found acceptable as the correlation coefficients were small, indicating no collinearity [53].

The variables identified as predictors of CI are shown in Table 8. The values of R2 (indicating how much of the variance in the outcome variable CI is explained by the predictor variables s) was 0.487 for blogging, 0.468 for vlogging and 0.412 for pop-up stores. H was a significant predictor for all three professions SI was not a predictor of CI for any of the new professions (with the exception of SI4 mentioned earlier) even though the new professions existed on social media outlets.

4. Discussion

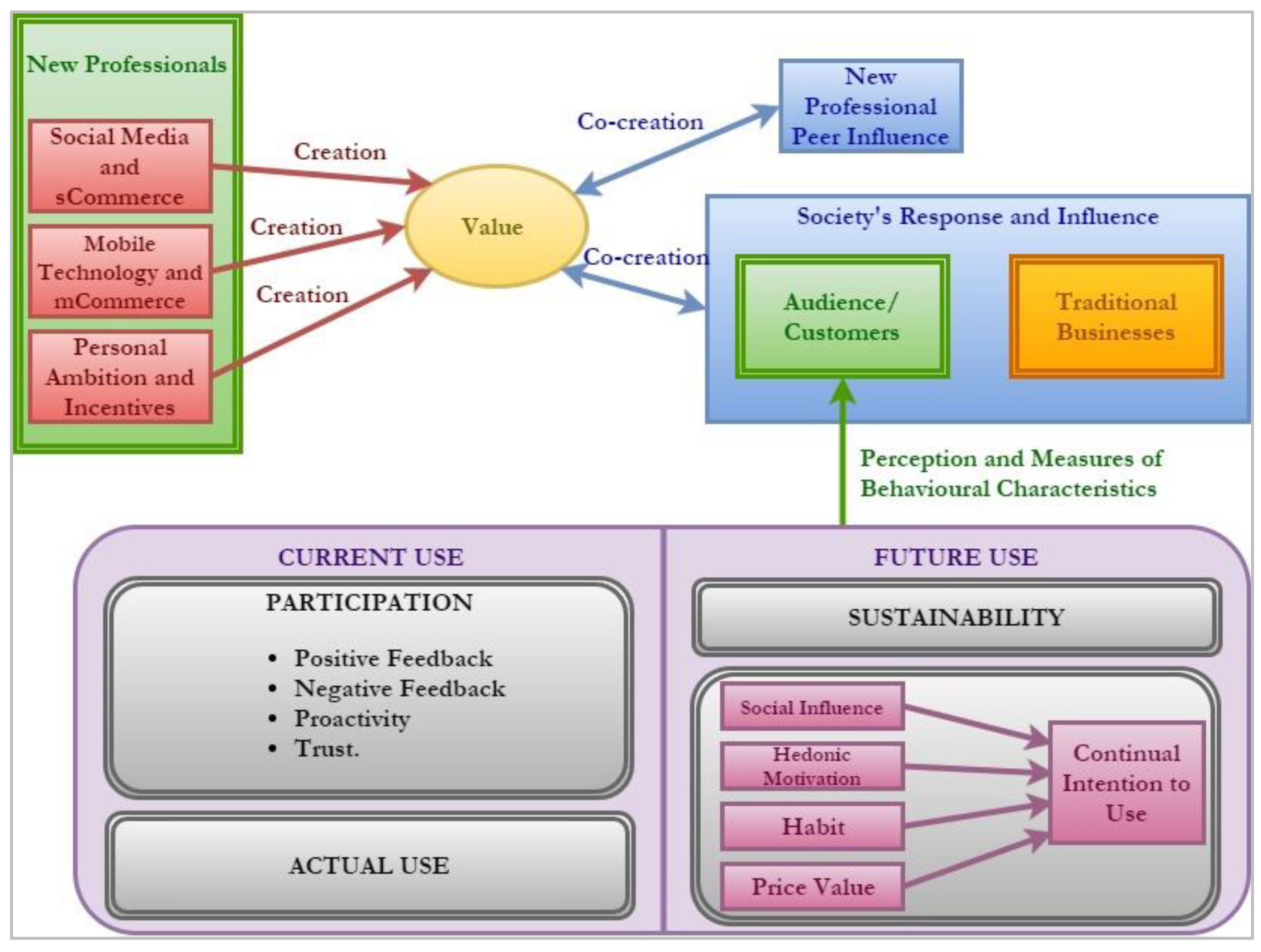

The preceding sections showed that the new professionals build their occupation by using social media and mobile technology to create, promote, establish and make available the goods and services offered by their respective professions. The themes emerging from the qualitative data gathered in Study 1 indicate that according to participants, both their audience/customers and peers (including traditional businesses and companies) provide important contributions to their success. The results of the statistical analysis of the quantitative data gathered in Study 2 provide insights into how customers perceived the value and the commercial sustainability of the new professions, and how they participated in a value co-creation process along with the providers of the new professional products and services. The interactions between the players involved, the resources they use to create and co-create value and the behavior-driving motivators identified in this research are depicted in the top half of Figure 4.

As shown, the new professionals use a combination of social media, mobile technology and their personal ambition to create value from their occupation. Both their peers (other new professionals) and society including their audience/customers and traditionally established professions play roles as value co-creators. Current use (at the bottom half of Figure 4) includes the frequency of the use of the service (actual use) and various aspects of participation, such as feedback, interactions with the service providers in the form of proactively requesting content, and trust, which involves trusting the reviews and recommendations made by new professionals. Additionally, at the bottom half of Figure 4, future use includes customers’ predictions of the sustainability of the new professions and the behavioral characteristics that may influence continual intention to use the goods/services provided.

Returning to the research questions guiding the study, the next sections discuss in more depth the specific value creation interactions in each of the three new professions, and the audience/customers’ acceptance of the new professions and their services.

4.1. Value Creation and Co-Creation Interactions

The network of interactions in Figure 4 allows us to address the first research question (“How do the new professionals leverage mobile technology and social media to create value”) by showing the processes involved in value creation and co-creation and the factors motivating participants’ behavior.

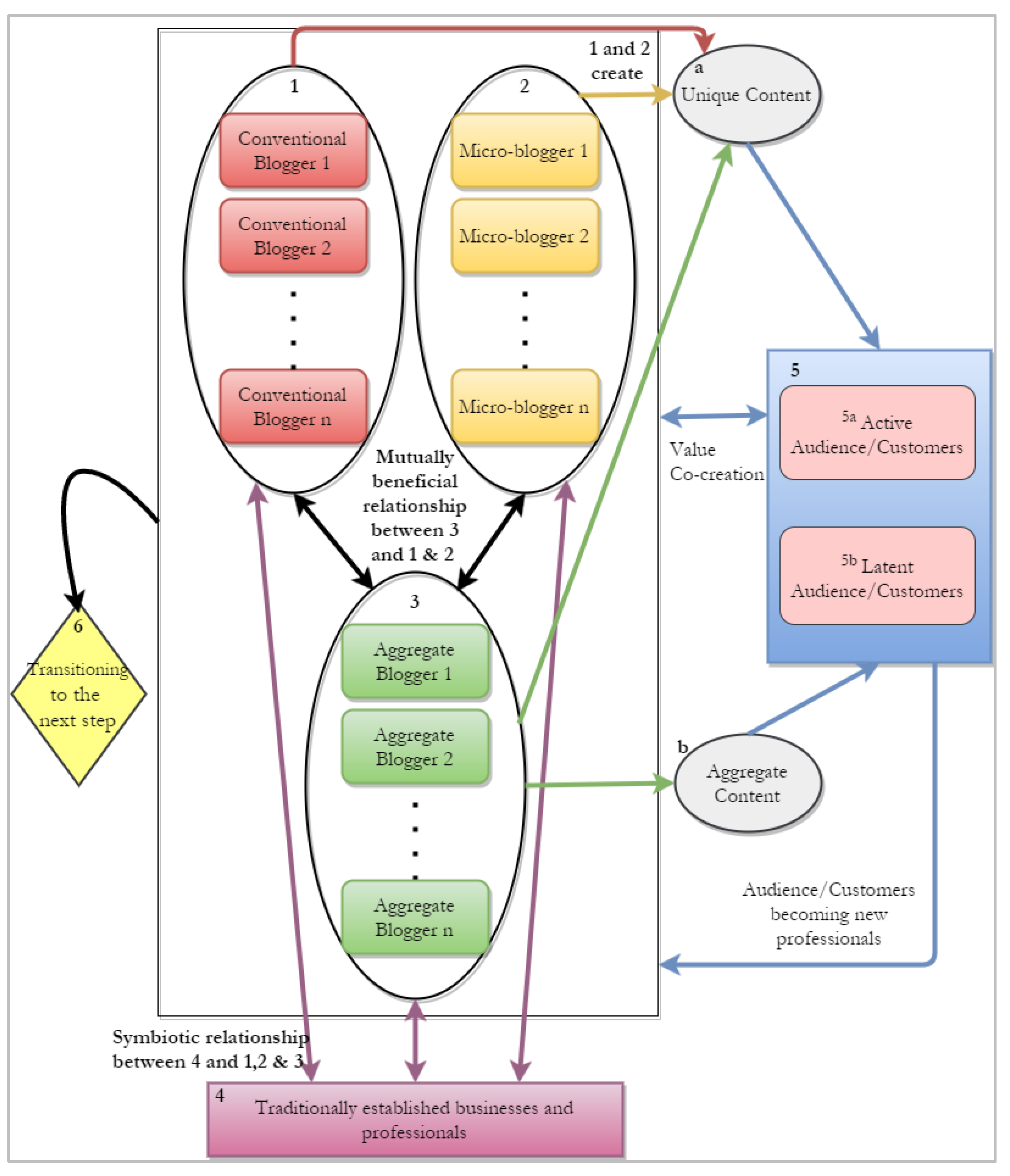

4.1.1. Blogging

Figure 5 shows the players and interactions involved in creating and co-creating value in the case of blogging. Bloggers include ‘conventional’ bloggers (1) who write articles and blogs on web pages, ‘micro’ bloggers (2), who use social media outlets like Twitter and Instagram to write a one sentence/paragraph with an accompanied image, and ‘aggregate’ bloggers (3) who collate the other bloggers’ content and post it (giving credit to the original authors). Therefore, value is first created by conventional and micro-bloggers who create unique content, as seen in the themes around social media and sCommerce, mobile technology and mCommerce, and personal ambition and incentive (Study 1). Customers realize the value by enjoying their favorite blogs (Section 3.2.4).

There is also a value co-creation relationship amongst bloggers: between aggregate bloggers and the other two blogger groups (Study 1, theme 20). While aggregate bloggers sustain their profession by leveraging the unique content created by conventional and micro-bloggers, the latter may increase their own readership due to the exposure. A value co-creation relationship is revealed in theme 18 of Study 1: between bloggers and the representatives of traditionally established companies (4) who send bloggers products to review, invite them to their establishments to rate and write about their services, and sponsor blog posts, giveaways and events for the bloggers’ audience. Bloggers gain support from the traditional firms for the creation of new content and may benefit from increased popularity and customer trust in the traditionally established business [52] while traditional firms achieve their publicity and promotional goals.

Finally, the active audience/customers (5a) of the bloggers participate in the value co-creation process by consuming both the unique and the aggregated content and through active interaction with the bloggers (as noted in Study 1, theme 16 and in the replies to the questions about participation in Study 2). Customers may explain what they liked and did not like, request customized content, and express their trust in the bloggers’ content by means of commenting positively and/or agreeing to follow the bloggers’ suggestions. The bloggers gain ideas for new content and create posts that aim to meet their target audience’s needs. However, there is a latent part of the audience/customers (5b) who do not engage in direct interaction with new professionals (as discussed in sub Section 3.2.2). While they do not leave feedback, nor actively ask for customized content, the may still add to the number of ‘reads’ and ‘views’ of the bloggers’ content, which the blogger has access to (Study 1, theme 3). While customers may become bloggers themselves, bloggers may ‘transition to the next step’—for example becoming vloggers to supplement their posts with video content, or even launching their own line of products for sale through a pop-up store (Study 1, theme 15).

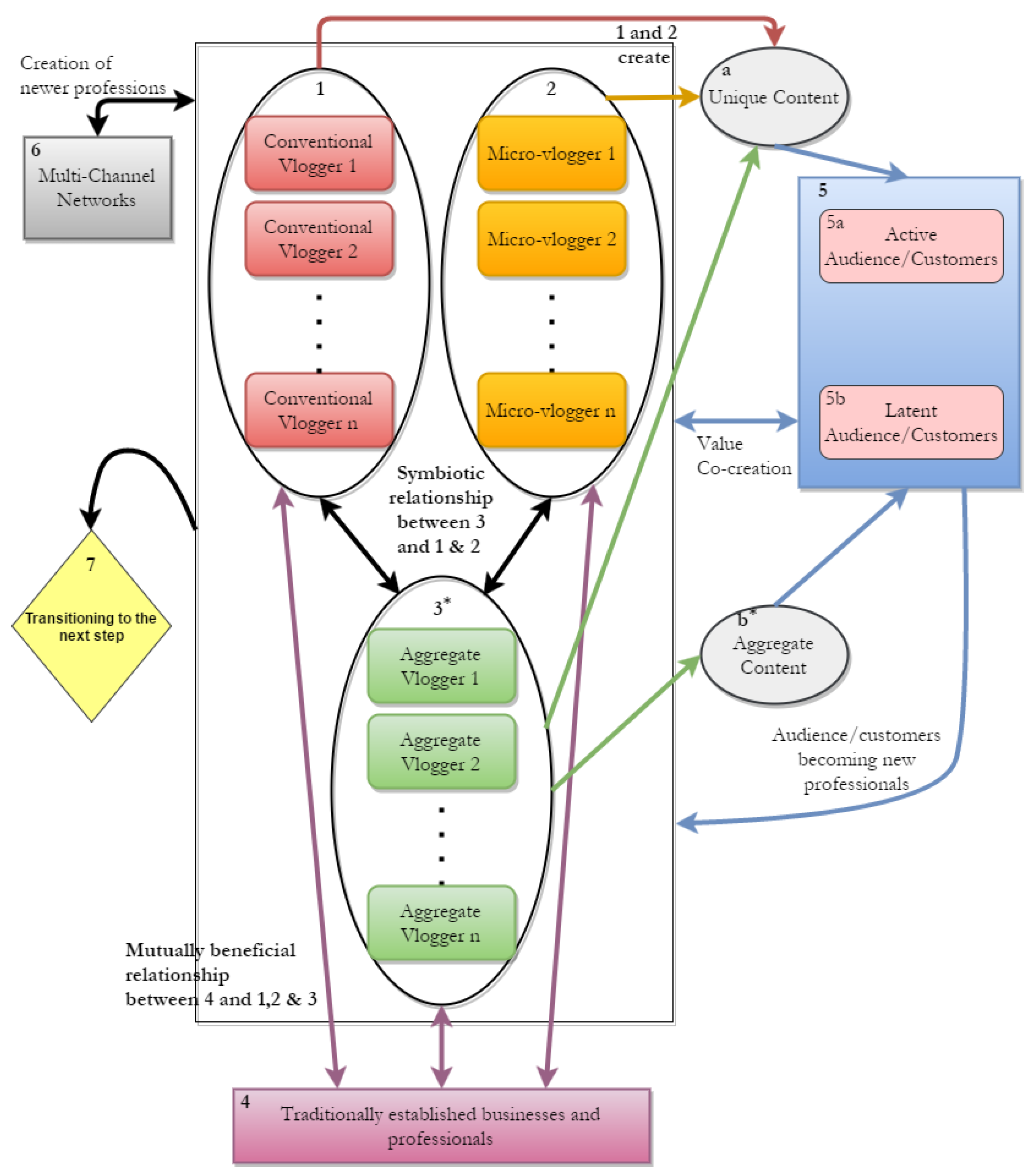

4.1.2. Vlogging

As shown in Figure 6, the value creation and co-creation interactions in vlogging are very similar to those described for blogging above, except for a few specific characteristics highlighted below. The types of vloggers also include conventional vloggers (1) who publish videos on streaming social media sites like YouTube, micro vloggers (2) who film short videos (under a minute) and publish them on micro-social media networks such as Instagram and Twitter, and ‘aggregate’ vloggers (3), who either aggregate video content and repost micro vlogs on social media with due credit to the creator, or edit video content and publish it on streaming/video publishing sites. Customers realize the value as they satisfy the habit they have developed for watching videos, and by enjoying the videos they watch. For vlogger customers, habit seems to be more important than enjoyment (Section 3.2.4).

There is a symbiotic relationship between the conventional and micro vloggers who create value through their own unique content, and the aggregate vloggers. However, aggregate vloggers cannot directly monetize aggregated videos on social media outlets like YouTube (Study 1, theme 20) as they first need to resolve copyright issues and obtain permission for creating the added production value. Similarly to blogging, traditionally established professions (4) play a role supporting vloggers (Study 1—Theme 18). In addition, another new profession has emerged—multi-channel networks (MCN) (6), whose main job is to handle vlogging channels for other vloggers. MCN add value by increasing a vlogger’s following and charging a percentage of the vlogging channel’s profits.

The vlogging audience (5) engages in value co-creation with the vloggers in the same way as in blogging; in addition, the interaction may involve customers creating a response video, which becomes part of the unique content on the vlogger’s site (Study 1, theme 16). In other words, customers may become co-producers and eventually may become vloggers themselves (Study 1, theme 11).

Vloggers use their audience’s comments and the findings from data analytics (Study 1, theme 3) to produce new vlogs. Again, there is a significant proportion of ‘silent’ customers who do not visibly participate in the value co-creation process (Section 3.2.2). As in blogging, vloggers may still derive value from the data on the number of views. As indicted in theme 15 of Study 1, there seems to be a transition (7) from vlogging to entrepreneurship.

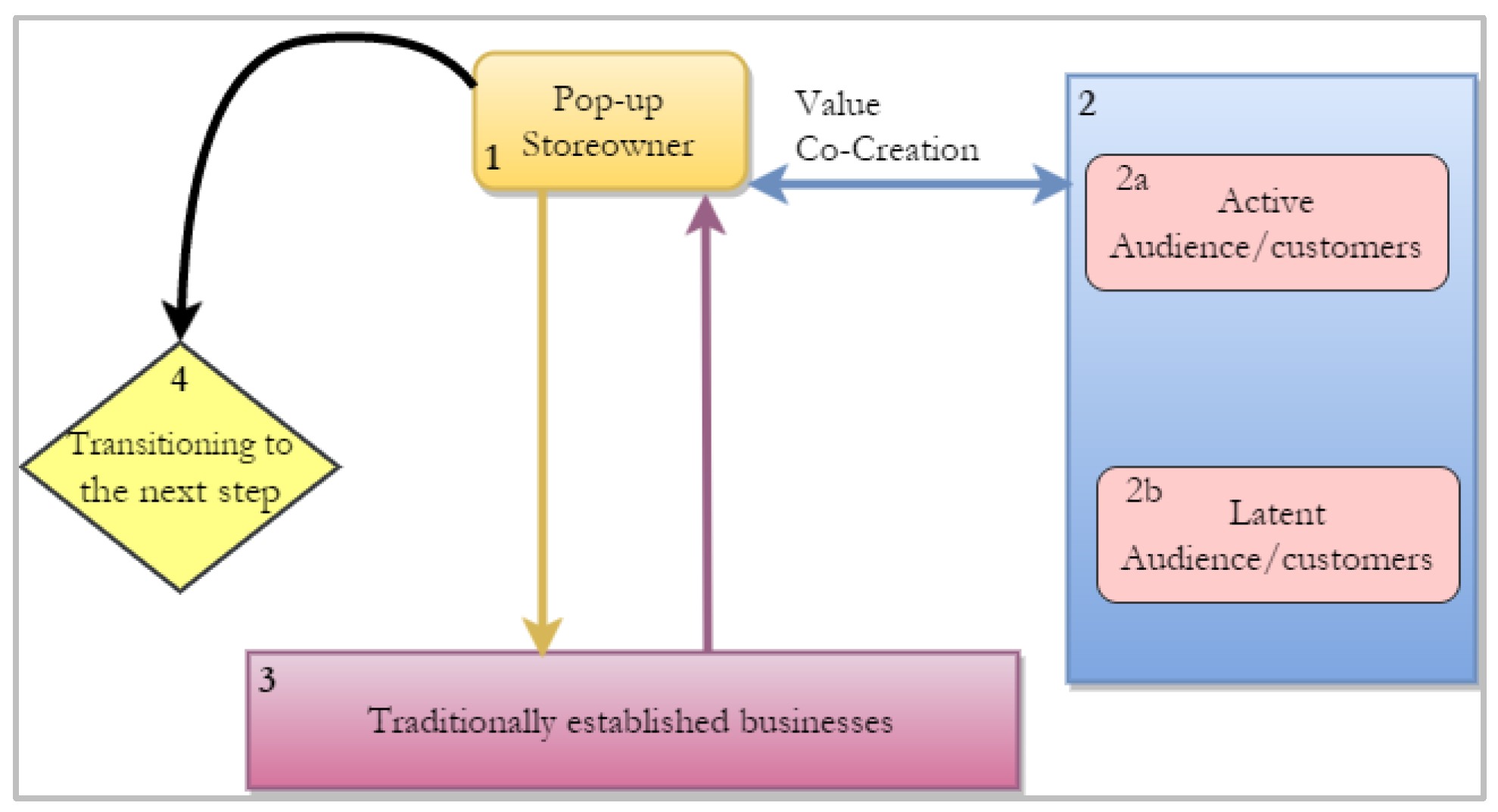

4.1.3. Pop-Up Stores

As shown in Figure 7, the value creation and co-creation network of virtual pop-up store owning emerging from the data in this research is relatively simple. There are no sub-genres in this profession, as all pop-up storeowners (1) deal in tangible, physical products. Traditionally established businesses (3) may want to invest in pop-up stores as a business opportunity or to collaborate with pop-up store owners by providing products to sell and thus co-create value (Study 1, theme 18). While pop-up store customers are driven by hedonic motivation and habit factors (similar to blogger/vlogger customers), the price–value balance is also considered. This is not surprising, as pop-up stores very rarely offer free products, while a significant amount of the content provided by bloggers/vloggers can be accessed free of charge.

The active customers of the pop-up store owners (2a) co-create value in the same way as the customers of bloggers and vloggers—through proactive participation (Study 1, theme 16). There is a similar presence of a latent section of customers (2b) who do not visibly engage in the value co-creation process. They do not leave feedback, do not ask for personalized products, and do not offer recommendations to the pop-up store owners; however, they may still provide value and indirect feedback to pop-up store owners through their purchases. Lastly, according to theme 15 in Study 1, pop-up store owners may, in the future, progress to opening brick-and-mortar stores instead of just virtual ones, indicating a ‘transition into the next step’ (4).

4.2. Audience/Customer Acceptance

These findings about current and possible future use of the new professional services and the summary in Figure 4 allow us to address the second research question (“How do the intended audience/customers of these new professions perceive their services?”). Among the respondents to the customer survey, 18–34 year old females who spent more than three hours online every day were the most prominent customers of the new professionals. Furthermore, a majority of customers also watch vlogs and read blogs regularly, ranging from daily to weekly. A majority also bought products from pop-up stores monthly or yearly, which can be considered as a relatively frequent buying when shopping online for tangible goods [56]. However, in terms of interaction and participation, in all three professions a majority of customers did not interact proactively with the new professionals frequently or on a regular basis. Additionally, most customers appeared to leave feedback only occasionally (whether positive or negative). As already mentioned, this indicates the presence of a silent, or ‘latent’ section of customers in the sample: customers who use the services but did not engage in any apparent way with the service providers. Additionally, only approximately half of the customers appeared to frequently trust the reviews and recommendations of the new professionals for buying other products.

Excluding the responses that were ‘neutral’, the customers’ views on the commercial sustainability of the professions were positive with only a small minority indicating doubt about the long-term sustainability of the service. Subsequently, the findings of the regression analysis indicated the significant predictors of continual intention to use for all three professions were hedonic motivation and habit. It indicated that the customers may have a proclivity for buying goods and services based on their sense of enjoyment and whether they were already habituated to shop in this way. Even though the new professions existed on social media outlets, the influence of customers’ social circles had an insignificant impact on the intention to use the services provided by bloggers and vloggers, with co-workers being marginally influential when purchasing products from pop-up stores. While this result is aligned with findings from previous research suggesting that co-workers’ opinions on shopping are more influential than family’s [57], the absence of social influence as a predictor of future use intention contradicts the views of the new professionals about the importance of family and friends’ opinions.

The effect of price value was not significant for bloggers and vloggers, potentially because most blogs and vlogs are free to read and watch, being available on websites which do not require a payment. However, price value played a significant role, albeit not as significant as hedonic motivation and habit, for pop-up stores. This was possibly because of the presence of tangible goods that need to be paid for to use. Nevertheless, price value could be a significant predictor for blogging and vlogging in future because of the recent advent of paid streaming services like YouTube Red where vloggers have their own contracted shows.

Due to the regular current usage and the claimed intention to use the new professional services in the future and the optimistic customer views about new professional service sustainability, it may be concluded that customers presently perceive the new professions positively. Furthermore, it may be suggested that the new professions have a sustainable future, as long as the value creation and co-creation processes remain stable.

4.3. Contributions, Implications, Limitations and Further Research

This research contributes to the body of knowledge in several ways. First, it undertook the investigation of the processes of value co-creation and creation and future use of the services of the three newly established professions, which have not yet attracted significant interest. Second, for each of the three new professions, the study proposes a value creation and co-creation framework that includes the main players and their interactions. Third, the study identified specific customer behavioral characteristics that influenced customer’s acceptance of the new professions.

According to [58], loyal customers contribute to a profession’s growth by recommending its services to others; however, recommendations also mean that individuals are putting their reputation on the line. Thus, to ensure the possible future growth of their professions through a loyal and trusting customer base and not to alienate the silent customer base, it seems prudent for the new professionals to be aware of all their customers’ needs and not just of the ones who are vocal about it. Therefore, they need to seek new ways of involving customers in visible interactions [59]. This may also leverage the role of social influence as customers may be more comfortable participating on sites also used by their respective social circles.

The study has important limitations, some of which could be overcome by attempting further research in this field. First, only a small sample of six new professionals were interviewed. However, each new professional genre was represented by two participants, from different countries. Similarly, only 209 individuals responded to the invitation to complete the online survey.

Further research may use the results to construct a model for the empirical investigation of the acceptance and use of a larger scope of new sCommerce/mCommerce professional services. Of specific interest would be to create a more comprehensive view of the latent customer base and to investigate in depth the phenomenon of using the products and services offered by the new professionals, but not engaging in visible participation and interactions, and the factors causing lack of trust [52]. This may in turn reveal some so far undetected factors that may also influence the continual intention to use. Similarly. when investigating the effect of social influence, it may be of interest to include the influence of strangers who have social media presence.

Furthermore, an in-depth study of the two other players involved in value co-creation, the traditionally established professions and the new professional peers, may provide useful insights. For example, it has been reported that editors from Vogue (a traditionally established magazine) had made disparaging remarks about the bloggers seated in the front row of Milan Fashion week [60]. This may point at potential tensions in the relationship between the traditional and new professionals.

Supplementary Materials

The following supporting information can be downloaded at: https://0-www-mdpi-com.brum.beds.ac.uk/article/10.3390/info13040178/s1. IBM SPSS Statistics24 output including Part SM1: Factor analysis (Blogging), Part SM2: Factor analysis (Vlogging), Part SM3: Factor analysis (Pop-up Stores), Part SM4: Correlation Matrices for Continual Intention to Use, Part SM5: Multiple regression (Blogging), Part SM6: Multiple regression (Vlogging), Part SM7: Multiple regression (Pop-up Stores).

Author Contributions

Conceptualization, S.D. and K.P.; methodology, K.P. and S.D.; data analysis: S.D. and K.P.; investigation, S.D.; resources, K.P.; data curation, K.P.; writing—original draft, S.D. and K.P.; writing—review and editing, K.P.; visualization, S.D.; supervision, K.P.; project administration, S.D. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

The study was conducted according to the guidelines of the Declaration of Helsinki and approved by the Ethics Committee of Auckland University of Technology (AUTEC 16/84).

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Data supporting reported results may be obtained by a special request.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table A1.

Survey questionnaire items.

| Label | Vlogging | Blogging | Virtual Pop-Up Stores |

|---|---|---|---|

| SI1. | People who influence my behaviour (peers, role models, etc.) think that I should watch vlogs | People who influence my behaviour (peers, role models, etc.) think that I should read blogs | People who influence my behaviour (peers, role models, etc.) think that I should shop from pop-up stores. |

| SI2. | People who are important to me (friends, family, etc.) think that I should watch vlogs | People who are important to me (friends, family, etc.) think that I should read blogs | People who are important to me (friends, family, etc.) think that I should shop from pop-up stores |

| SI3. | The video sharing/hosting site has been helpful in using their site/application by including things like a simplified design/user interface with easy separation and searching of different genres of vlogs | The blogging social media site has a robust and simple application and responds to any problems I have with it | The social media site which hosts the pop-up store has a robust and simple application and responds to any problems I have with it |

| SI4. | Colleagues at my workplace have been encouraging in the watching of vlogs for help with my job | Colleagues at my workplace have been encouraging in the reading of blogs for help with my job | Colleagues at my workplace have recommended shopping from pop-up stores |

| HM1. | Watching vlogs is fun | Reading blogs is fun | Shopping from pop-up stores is fun |

| HM2. | Watching vlogs is enjoyable | Reading blogs is enjoyable | Shopping from pop-up stores is enjoyable |

| HM3. | Watching vlogs is entertaining | Reading blogs is entertaining | Shopping from pop-up stores is entertaining |

| PV1. | Watching vlogs online is reasonably priced | Reading blogs online is reasonably priced | Shopping from pop-up stores online is reasonably priced |

| PV2. | Watching vlogs online is good value for money | Reading blogs online is good value for money | Shopping from pop-up stores online is good value for money |

| PV3. | At the current price, watching vlogs provides a good value | At the current price, reading blogs provides a good value | At the current price, shopping from pop-up stores provides a good value |

| H1. | Watching vlogs has become a habit for me | Reading blogs has become a habit for me | Shopping from pop-up stores has become a habit for me |

| H2. | I am addicted to watching vlogs | I am addicted to reading blogs | I am addicted to shopping from pop-up stores |

| H3. | Watching vlogs has become natural to me | Reading blogs has become natural to me | Shopping from pop-up stores has become natural to me |

| CI1. | I intend to keep watching vlogs in future | I intend to keep reading blogs in future | I intend to keep shopping from pop-up stores in future |

| CI2. | I plan to continue watching vlogs in future | I plan to continue watching blogs in future | I plan to continue shopping from pop-up stores in future |

| SU1. | I predict that vlogging as a profession is sustainable long term | I predict that blogging as a profession is sustainable long term | I predict that pop-up store owning as a profession is sustainable long term |

| AU1. | I normally watch vlogs as frequently as: | I normally read blogs as frequently as: | I normally shop from pop-up stores as frequently as: |

| P1. | I leave positive comments on vlogs | I leave positive comments on blogs | I leave positive feedback after shopping from pop-up stores online |

| P2. | I leave negative comments on vlogs | I leave negative comments on blogs | I leave negative feedback after shopping from pop-up stores online |

| P3. | I have requested for specific content on vlogs | I have requested for specific content on blogs | I have requested for specific products from pop-up storeowners online |

| P4. | I buy products reviewed/recommended by vloggers | I buy products reviewed/recommended by bloggers | I buy new products advertised and advocated by pop-up storeowners |

Table A2.

Rotated component matrix for blogging (for the purposes of distinguishing between the professions, a prefix ‘B’ was added to the item identifiers).

Table A2.

Rotated component matrix for blogging (for the purposes of distinguishing between the professions, a prefix ‘B’ was added to the item identifiers).

| Component | ||||

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |

| BHM2 | 0.913 | |||

| BHM1 | 0.866 | |||

| BHM3 | 0.853 | |||

| BPV2 | 0.876 | |||

| BPV3 | 0.874 | |||

| BPV1 | 0.797 | |||

| BH1 | 0.845 | |||

| BH2 | 0.832 | |||

| BH3 | 0.797 | |||

| BSI2 | 0.902 | |||

| BSI1 | 0.862 | |||

| BSI4 | 0.522 | |||

| BSI3 | ||||

Table A3.

Rotated component matrix for vlogging (for the purposes of distinguishing between the professions, a prefix ‘V’ was added to the item identifiers).

Table A3.

Rotated component matrix for vlogging (for the purposes of distinguishing between the professions, a prefix ‘V’ was added to the item identifiers).

| Component | ||||

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |

| VHM2 | 0.887 | |||

| VHM1 | 0.876 | |||

| VHM3 | 0.854 | |||

| VH2 | 0.875 | |||

| VH1 | 0.800 | |||

| VH3 | 0.665 | |||

| VPV1 | 0.809 | |||

| VPV3 | 0.768 | |||

| VPV2 | 0.725 | |||

| VSI4 | 0.746 | |||

| VSI1 | 0.684 | |||

| VSI2 | 0.670 | |||

| VSI3 | 0.571 | |||

Table A4.

Rotated component matrix for pop-up stores (for the purposes of distinguishing between the professions, a prefix ‘P’ was added to the item identifiers).

Table A4.

Rotated component matrix for pop-up stores (for the purposes of distinguishing between the professions, a prefix ‘P’ was added to the item identifiers).

| Component | ||||

|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |

| PHM1 | 0.860 | |||

| PHM2 | 0.845 | |||

| PHM3 | 0.809 | |||

| PSI4 | 0.692 | |||

| PH2 | 0.887 | |||

| PH1 | 0.840 | |||

| PH3 | 0.830 | |||

| PPV2 | 0.844 | |||

| PPV1 | 0.841 | |||

| PPV3 | 0.701 | |||

| PSI3 | ||||

| PSI1 | 0.861 | |||

| PSI2 | 0.827 | |||

References

- Cavalinhos, S.; Marques, S.H.; Salgueiro, M.D.F. The use of mobile devices in-store and the effect on shopping experience: A systematic literature review and research agenda. Int. J. Consum. Stud. 2021, 45, 1198–1216. [Google Scholar] [CrossRef]