Firm Heterogeneities, Multi-Dimensional Proximities, and Systematic Dynamics of M&A Partnering: Evidences from Transitional China

Key Laboratory of Watershed Geographic Sciences, Nanjing Institute of Geography and Limnology, Chinese Academy of Sciences, Nanjing 210008, China

Systems 2022, 10(2), 32; https://0-doi-org.brum.beds.ac.uk/10.3390/systems10020032

Submission received: 26 January 2022

/

Revised: 21 February 2022

/

Accepted: 27 February 2022

/

Published: 8 March 2022

(This article belongs to the Section Systems Practice in Social Science)

Abstract

:Corporate investment strategies and decision-making processes are crucial for understanding the operation and evolution of socioeconomic systems. Mergers and acquisitions (M&As) have been the main mode of corporate investment, growth, and upgrading, deeply affecting corporate reorganization, regional industrial restructuring, and economic globalization. By building a database including 5543 M&A partnerings and 1.89 million M&A non-partnerings, this study aims to uncover the systematic dynamics of M&A partnering in regional China during different phases since the mid-1990s, with particular attention given to the effects of firm heterogeneities and multi-dimensional proximities. Although geographical, cognitive, organizational, and institutional proximity dimensions are significantly influential for M&A partnering, we find that the effects of multi-dimensional proximities differ across M&A types and involving firms. Specifically, organizational proximity matters more for large- and medium-sized acquirers, while institutional proximity plays a more vital role in the acquisition target selection of private-owned and small-sized acquirers. Cognitive proximity measured by industrial and technical relatedness is more crucial for horizontal, vertical, and conglomerate M&As that are tightly associated with the corporate product, technical, and functional upgrading. The results indicate that the benefits of cognitive proximity may offset the risks and costs resulting from long-distance M&As, demonstrating the interactive dynamics between proximity dimensions. Our findings suggest that firm heterogeneities, proximity dynamics, and contextual factors should be focused on when explaining the investment decision-making processes of individual corporations in emerging and transitional economies such as China.

1. Introduction

The variegated investment activities of corporations are an important component of the real economic world [1,2,3]. Demystifying the processes of corporate diversified strategies and investment behaviors will contribute to our understanding of the driving forces behind the operation and evolution of the socioeconomic system [4,5,6]. Particularly, a large body of literature has illustrated that corporate investment and relevant choices should be considered as a complex decision-making process, which is sensitive to contextual factors [7,8], place-specific attributes [1,9,10], organizational structures [11,12], and entrepreneurial behaviors [13,14]. Furthermore, there exist significant differences in decision-making mechanisms and locational implications of various investment modes, including greenfield investment (GI) and mergers and acquisitions (M&As), of individual corporations [15,16,17]. With the increasingly vital role played by M&As in corporate performance [18,19], industrial dynamics [20,21], and socioeconomic system [22,23], the contextual influences, corporate motivations, and geographical outcomes of M&A transactions have been hotly discussed by disciplines such as economics, management, accountancy, and geography [8,24,25].

The linchpin of M&As is the partnering of the acquirer and the target, and this is different from the optimized choice of location in the process of corporate GI [26,27]. In addition to the firm- and place-specific attributes, previous studies have also explained the determinants of M&As from the perspective of inter-firm and inter-place relations [28,29]. Particularly, a multi-dimensional proximity framework, including geographical, cognitive, organizational, institutional, and cultural proximity, has been widely used in relevant research [30,31,32]. However, there are several research gaps in the systematic dynamics behind M&A partnering due to data availability and limited case locations (mainly in Europe and the USA). First, more scholarly efforts should be devoted to comprehensively examining the effects of firm heterogeneities (e.g., size, industrial attribute, ownership structure) on acquisition target selection. Research on differences in M&A partnerings of manufacturing and service sectors, as well as state-, foreign-, and private-owned corporations, is quite limited.

Second, we know little about the variegated role played by proximities when M&A activities are grouped into different types according to acquirers’ business purposes. Corporations may pursue market/product extension, forward/backward integration, and diversification through horizontal, vertical, and conglomerate M&As, respectively [23]. The preferences of acquisition target selection would differ across corporations with various investment goals and strategies [23,33,34]. The relationships between multi-dimensional proximities, which affect the fit of targets to acquirers, and M&A partnering would also vary across types. Empirical studies considering M&A types will advance our understanding of the systematic dynamics of M&A partnering.

Third, the impact of various proximities on M&A partnering in emerging economies (EEs) remains a deeply neglected topic in the literature. During the last decade, EEs (e.g., China and India) have been experiencing rapid growth of the amount of cross-border and domestic M&As, deeply reshaping economic geography on global, national, and regional scales [35,36]. According to the Zephyr database, the number of China’s domestic M&As has surpassed that of Germany, Canada, and France combined in 2016 [23]. It should be noted that the market environment and regulatory policies for corporate activities in EEs are significantly different from those in developed economies (DEs) [37,38,39]. The impacts of proximity dynamics on M&A partnering in EEs’ contexts call for more scholarly attention. Furthermore, whereas research on M&As from a geographical perspective is extensive, the number of empirical studies investigating corporate M&As on a finer spatial scale (e.g., regional scale) is still relatively small [26].

To fill the aforementioned research gaps, this paper is conducted to examine the effects of corporate heterogeneity and proximity dynamics on M&A partnering driven by various business purposes in the Yangtze River Delta (YRD), one of the emerging global-city regions in China. By building a database including 5543 M&A partnerings and 1.89 million M&A non-partnerings, we focus on three related research questions: (1) How do multi-dimensional proximities at the firm level affect M&A partnering? (2) How do acquiring preferences vary by corporations with different attributes? (3) How do the influences of proximities differ across M&A types? This study aims to advance our understanding of the socioeconomic system by uncovering the driving mechanisms behind corporate investment strategy (i.e., M&A). By highlighting the impacts of firm heterogeneities and multi-dimensional proximities on M&A transactions differentiated by business goals, our findings will also contribute to the literature about corporate investment decisions, networked economy, and management systems. Moreover, we provide an alternative perspective and a case study for readers to better understand corporate M&As in EEs such as China.

In the next section, we review the literature and develop a conceptual framework. Section 3 presents the dataset and methodologies used in this study. Empirical results related to the effects of firm heterogeneities and multi-dimensional proximities on M&A partnering are reported in the Section 4. Then, we discuss and conclude.

2. Literature Review and Conceptual Framework

2.1. Literature Review: Motives and Determinants of Corporate M&As

Why corporations engage in M&A activities and which corporations could become M&A partners have been the subject of heated debates in relevant literature [8,26,27]. Existing research has illustrated that the general nature of M&As is that corporate organizations achieve costs/risks controlling and shareholder wealth increasing through outward investment and strategic integration [23,33]. However, the seminal works investigated the motives and determinants both from the perspectives of corporate organizations and from the perspectives of the evolved places [8,22,40]. The roles played by corporate heterogeneities and inter-firm linkages, by contrast with place-specific attributes and inter-regional relations, remain central to M&A decisions and partnering [31,41,42].

2.1.1. Corporate Heterogeneities of M&A Activities

There is a consensus that corporations, especially acquirers, engage in M&A events out of motivations such as financial enticements [24,43], market expansion [18], and access to scarce resources and localized assets [13,29]. Certainly, the specific pursuits related to M&A activities would differ across individual corporations with various sizes, industrial attributes, and ownership structures [32,44,45]. Some studies on M&As have uncovered the preferences of acquisition target selection carried out by corporations with different attributes [44,46].

Specifically, traditional manufacturers are more likely to acquire targets based on criteria such as raw materials, labor, and market proximity, while buyers that belong to the “new economy” (e.g., knowledge-intensive industries) would be attracted by distance-transcending assets such as tacit knowledge and emerging technologies [45]. With few exceptions [21,34,47], research on the spatial merger behaviors and acquiring predilections of service firms, as well as the relevant differences between manufacturing and services, is relatively limited. Existing studies have also indicated that the acquiring preferences would vary across corporations with different ownership structures (e.g., domestic and foreign-owned) [32,42]. Multinational enterprises (MNEs) frequently execute partial acquisitions rather than full acquisitions to reduce their liability of foreignness and to maintain an effective local partner [46]. Furthermore, the spatial merger behaviors will diverge among acquirers with different sizes [44,48]. Larger corporations, such as MNEs and listed firms, are considered more capable of initiating long-distance and inter-industry M&As, while small- and medium-sized enterprises (SMEs) tend to become acquiring targets of large ones [40].

2.1.2. Multi-Dimensional Proximities and M&A Partnering

The proximity framework has been increasingly used in examining the determinants of M&A partnering on regional, national, and global scales [31,32]. Particularly, a more comprehensive framework, including geographical, technological, organizational, and institutional proximity, generated by Boschma et al. (2016), has proven to be effective in previous studies [32]. Scholars have reached a consensus on the role played by multi-dimensional proximities in promoting M&A partnering, although there are still some mixed findings in the literature.

The importance of geographical proximity for capital mobility, knowledge spillover, cooperation, and learning has been documented in vast literature [49,50,51]. Decreasing spatial distance between the acquirer and the target will help inhibit the influences of information asymmetry, and then reduce searching costs and transaction risks in the process of M&A partnering [26,52]. Spatial closeness can also facilitate the face-to-face exchange of tacit knowledge and the sharing of fixed assets [49,50], which will contribute to the success of post-M&A integration. With the increased information revolution, the effects of geographical proximity or “home bias” on M&A partnering, especially that initiated by large acquirers (e.g., MNEs and listed firms) with a stronger ability to internalize long-distance resources, would weaken to a certain extent [53].

Most of the literature suggested that cognitive proximity, which is usually measured by industrial and technological relatedness [26], has positive effects on M&A partnering. The acquirer and the target in related sectors and technological fields are complementary in aspects of strategy, product, and market, and this is important to reduce cognitive bias and access synergy effects in M&A decisions [26,32]. Searching targets within familiar industries or supply chains will help acquirers pursue economies of scale/scope, as well as internalize transaction costs.

Organizational proximity is mainly manifested in that the acquirer and the target belong to the same group (have the same actual controller), and the similarity of corporate size and internal structure. Existing studies indicated that organizational proximity driver M&A partnering is not only because of less uncertainty and opportunistic behavior among group members but also related to the easier and more effective integration between corporations with similar size and office structure [31,40]. Institutional proximity (e.g., similar corporate culture and management/financial system), as well as social and cultural proximity resulting from geographical closeness, have also been verified as a crucial source for information symmetry and synergy effect promoting M&A partnering [30,31].

In addition, empirical results have implied that there exist interaction effects among different proximity dimensions [49,50,51]. Geographical proximity can increase the degree of other proximity dimensions through facilitating information and knowledge exchange among individual agents; cognitive proximity, especially industrial and technical relatedness, may, in turn, make up for the potential costs and risks in the process of long-distance investment or cooperation [51]. Recent studies have suggested that multi-dimensional proximities would present variegated effects on M&A decision and partnering differentiated by the size, industrial attribute, and ownership structure of acquirers/targets [32]. Some seminal scholarly works have also indicated that individual characteristics of the engaged corporations, as well as the influences of proximities on horizontal, vertical, and conglomerate M&As, are different due to various business strategies and purposes [23,34].

2.2. Conceptual Framework: Partnership Dynamics of M&As in the Chinese Context

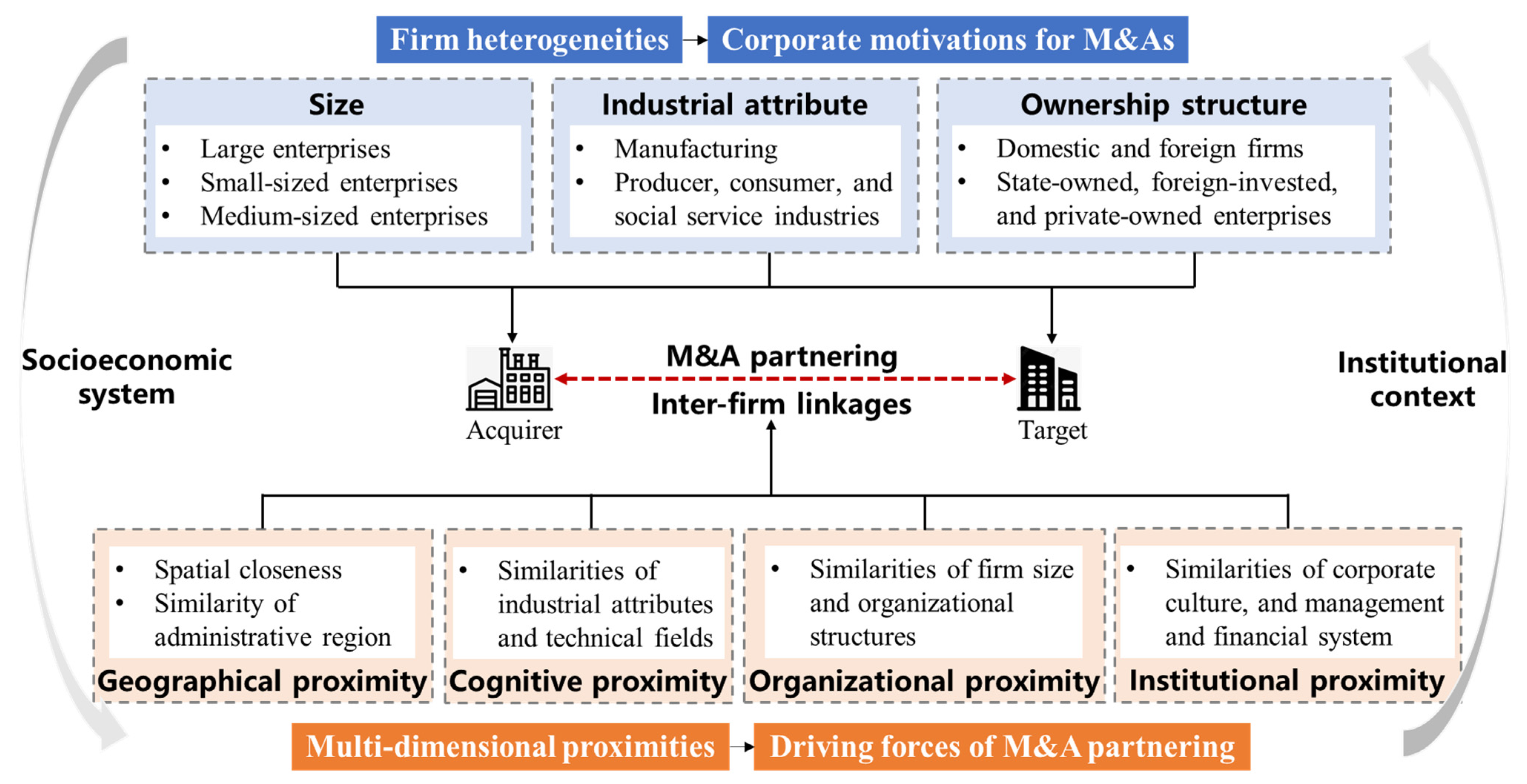

As economic activities led by individual corporations, China’s domestic M&A transactions also follow the general nature of M&A partnering that is drawn from the Western literature. However, China, one of the largest developing and transitional economies all over the world, provides a special economic structure, regulatory policy, and institutional setting for corporate M&As [35,37]. Before the reform and opening-up, corporate shutdowns, mergers, and transformations were dominated by China’s central and local governments due to the planned economic system and public ownership. In the late 1990s, the deepening of market-oriented reform led to the rise of corporate M&As in China. Since the early 2010s, the number of China’s M&A events increased drastically due to rapid industrialization, corporate expansion, and encouraging policies [53,54]. Based on previous findings and the unique contexts, we develop a conceptual framework to explain the variations of the impacts of corporate heterogeneities and proximities on M&A partnering in transitional China (see Figure 1).

On the one hand, there is an extensive literature underlining the role played by firm heterogeneities, particularly differences in corporate sizes, industrial attributes, and ownership structures, on M&A decisions and acquisition target selection. We should re-examine the distinct or changing characteristics of China’s domestic M&A activities initiated by corporations with variegated sizes, industrial attributes, and ownership structures. There is a long tradition of local governments favoring large corporations (e.g., the Fortune Global 500 and listed firms) that have positive effects on the achievements in one’s official career in China. These large corporations are more accessible to financing and incentive policies, which enforce their dominant position in China’s M&A market. Unlike the original resource-intensive and low-end growth model, China has increasingly pursued industrial upgrading, especially the development of high-tech manufacturing and producer services. This will result in more active investment activities including M&A in relevant sectors. Moreover, quite a number of studies have discussed the differences in business strategies and spatial investment behaviors of corporations with various ownership structures (e.g., state-, foreign-, and private-owned) in China [55,56]. Investment choices of state-owned enterprises (SOEs), which are controlled by the central and local governments, will give priority to industrial monopoly, local protectionism, and appreciation of state assets. Foreign-invested enterprises (FIEs) enter China mainly for the emerging market and low-cost factors, although some of them have gradually embedded in the host region due to local linkages [57]. FIEs will carefully choose entry and expand modes for avoiding potential risks in the process of cross-border investment. Private-owned enterprises (POEs) are still the main force of the Chinese market. As the business environment of POEs improves, their investment for the product, technological, and functional upgrading will become more active. It should also be noted that the deepening reform of SOEs aiming at mixed-ownership would promote cross-ownership M&As in China.

On the other hand, following the general nature of proximity dynamics of M&A partnering, we hypothesize that geographical, cognitive, organizational, and institutional proximity at the firm level would significantly promote M&A partners in transitional China. However, the impacts of multi-dimensional proximities on M&A partnering will change due to the unique socioeconomic system and institutional context in China. The transition from a planned economy to a socialist market economy has greatly promoted resource reallocation and corporate investment between administrative regions in China [58,59]. However, local protectionism and regional competition that resulted from fiscal decentralization make officials more concerned about local economic growth [60], and they try their best to prevent the loss of corporate control and high-quality assets to the outside. Incentive policies also encourage acquirers to expand or transform through buying and internalizing local targets. The so-called “administrative region economy” would affect the roles played by proximities in China’s domestic M&A partnering. Particularly, the effect of geographical proximity measured by the similarity of the administrative region on M&A partnering might be reinforced.

Furthermore, the process of China’s market-oriented reform and economic transition has gone through several periods with distinctive features [61]. In the 1990s, the Chinese government’s interference with economic activities was still significant, and China’s domestic M&A market has not yet developed. Joining the World Trade Organization (WTO) in 2001 has accelerated the process of China’s reform and opening-up, the status of individual corporations as the main force of market resource allocation has been established. The advanced management experience brought by FIEs has also made China’s domestic corporations aware of the importance of capital operations, such as M&As related to product and market expansion. Since the early 2010s (the post-financial crisis-era), China has done more efforts to deepen reform, expand opening, and promote economic transition. M&A activities that are conducive to corporate reorganization and industrial upgrading have increasingly been encouraged by China’s central and local governments. Therefore, the spatial merger behaviors of corporations, as well as the effects of multi-dimensional proximities on M&A partnering, may vary over time in transitional China.

3. Study Area and Data Description

3.1. The Yangtze River Delta (YRD): An Emerging Global-City Region

Existing studies have documented that corporate M&As would be more active in China’s coastal regions dominating the national M&A network [53]. The YRD, one of the coastal urban agglomerations with a higher level of economic development and regional integration in China [62,63], was selected for the case study because the following reasons: First, as the frontier of China’s reform and opening-up, the YRD provides a wide range of research samples and cases for studying the national economic structure and corporate behavior. A higher level of economic system development has also resulted in a more active M&A market involving various acquirers and targets in the YRD. Second, industrial upgrading has been increasingly promoted in major cities of the YRD, where traditional industrialization trajectories first started [64]. A series of developmental plans that were implemented by the Chinese central government for regional integration of the YRD has also enforced corporate linkages through encouraging inter-regional labor division, industrial coordination, and market unification. The processes of economic transition and regional integration will make M&A partnering and its determinants in the YRD present obvious periodical features. Third, the YRD, led by Shanghai, has a similar economic output as acknowledged global-city regions led by London, New York, and Tokyo. An empirical investigation on the YRD will draw attention to corporate M&As in emerging global-city regions on the one hand, and contribute to the comparison of M&A studies in EEs with those in DEs on the other hand. The YRD is divided into 4 province-level, 41 city-level, and 210 county/urban district-level regions in this study (see Figure 2).

3.2. Data Source and Processing

Domestic M&A events analyzed in this paper are derived from the database of WIND, which is a lead firm of financial data service in China. We collected 6413 announced M&A events where both the total involved acquirers and targets were located in the YRD from 1996 to 2016. Events that failed or were forced to be discontinued were excluded in our analysis. Then, we identified acquirers’ and targets’ characteristics, such as registered capital, industrial attribute, listed status, outside investment situation, ownership structure, and address, in the inquiry system of corporate information built by Qichacha. We eliminated M&A events with incomplete information of relevant acquirers and targets. Moreover, for M&A events involving larger groups of corporations (M&A events with multiple acquirers or targets), we split them into one-to-one deals initiated by different buyers. Finally, we obtained 5543 M&A partners for this study.

The completed and announced M&A partnerings are still rare events among potential corporate partners in the YRD from 1996 to 2016. Investigation on the microcosmic mechanism of corporate M&As needs to consider the peer group of non-partnerings in the same place or period. According to the methods applied in the literature [26,44,52], we built the peer group of non-partnerings from the perspective of acquirers. We assume that only acquirers and targets engaged in above mentioned 5543 M&A partnerings could act as potential acquirers and targets in the peer group of non-partnerings. A time window of one year before and after the year of event announcement was used in the allocation of potential targets to the known acquirers. For instance, all acquirers of M&A events announced in 2015 could buy all relevant targets from 2014 to 2016. After accomplishing the aforementioned processes, we then construct the peer group of non-partnerings, including over 1.89 million potential transactions in the YRD from 1996 to 2016.

4. Model Setting and Variable Specification

M&A partnering, which represents firm dyads related to the announced M&A deals, is typical behavior of binary choice. Based on the previous studies [31], the dependent variable in our empirical model, namely , is constructed as a binary variable (1 for an M&A deal between any two corporations, 0 when the potential acquirer and target could but did not set up an M&A deal). We apply logistic regression to examine the determinants of M&A partnering between any two corporations in the YRD, as methods such as OLS are invalid for binary dependent variables. The equation including of logistic regression model can be constructed as follows:

where is an intercept term, and represent the independent variable and its regression coefficient, respectively, and refers to the probability when takes the value 1, while indicates the probability when takes a value of 0. According to the cumulative logistic distribution and Equation (1), can be calculated as follows:

Based on the existing studies and our database, independent variables are identified in aspects of geographical, cognitive, organizational, and institutional proximity (see Table 1). We take the straight-line distance calculated in ArcGIS between the acquiring and target corporations (Dist), which has been widely used in the literature [30] as one of the proxies of geographical proximity. Three dummy variables (i.e., Intra_P, Intra_C, and Intra_D) have also been introduced to measure the spatial closeness between corporations and the effects of China’s administrative region economy in our analysis. Specifically, Intra_P, Intra_C, and Intra_D take a value of 1 when the acquirer and target engaged in an M&A partnering are respectively located in the same province, city, and county/urban district.

We follow the previous studies in measuring cognitive proximity from the perspective of industrial/technological relatedness between the corporations, that is to say, whether the acquirer and target operate in the same sector [32]. We introduce two dummy variables (i.e., Intra_I and Intra_G) to test the effects of cognitive proximity. Intra_I and Intra_G take a value of 1 if the involved corporations of an M&A partnering operate in the same industrial division and major sectors. In our analysis, industrial divisions indicate manufacturing, producer services, and consumer and social services; 20 major sectors are identified as the National Economy Classification Codes GB/T 4754-2017 in China. Compared with the seminal works, our analysis failed to obtain more detailed industrial attributes of corporations due to data availability.

Two dummy variables (i.e., Multi_L and Same_S) have been applied to account for the impacts of organizational proximity. Multi_L takes a value of 1 if both the acquiring and target corporations have at least one outside investment event (partly/totally controlled company). Same_S takes a value of 1 if the two corporations are grouped into the same size, which is measured by corporate registered capital. Corporations with registered capital of more than 100 million yuan, 10 million to 100 million yuan, and less than 10 million yuan are, respectively, defined as being of large, medium, and small size.

The degree of similarity in ownership structure and listed status between corporations has been used to test the effects of institutional proximity in this study. We introduce three dummy variables, namely Same_Ins, List, and Nonlist. Same_Ins takes a value of 1 if both the acquirer and target belong to the same ownership structure, including the SOEs, POEs, FIEs, and joint venture. In our analysis, FIEs include corporations controlled by investors from foreign countries, as well as Hong Kong, Macao, and Taiwan in China. List (Nonlist) takes a value of 1 if both the acquirer and target are listed (unlisted) on any stock exchange. The description of the partnerings and non-partnerings of M&As in the YRD is presented in Table 2.

Furthermore, there are some estimation issues that should be explained before running models and presenting results. First, in order to deal with various estimated errors resulting from the huge discrepancy between 1.89 million M&A non-partnerings and only 5543 M&A partnerings, we follow the previous studies in using endogenous stratification to split all observations into a group of events and a group of non-events [26]. We then import all partnering observations and randomly selected non-partnering observations into models as dependent variables. One announced M&A partnering matched with five potential partnerings (27,721 non-partnerings have been randomly drawn) in our analysis, and this rule has been verified to be effective by existing research [31]. Second, China and its M&A market have been undergoing several developmental phases since the late 1990s. The period from 1996 to 2016 has been divided into four ranges (i.e., 1996–2000, 2001–2005, 2006–2010, and 2011–2016) to investigate how do the effects of multi-dimensional proximities change over time. This division of period is based on the time windows of the 9th, 10th, 11th, and 12th plan for national economic and social development, which largely released new signals of market regulation and incentive policies in China. Considering the comparability of each research period, the year 2016 was included in the time window of the 12th plan for national economic and social development in China. Third, in addition to horizontal, vertical, and conglomerate M&As identified in the literature [23], we introduce financial investment and recapitalization as the other two types of M&A activities according to our database. Corporations are more likely to access the added value of the purchased equity/asset, and to promote the reallocation and overall listing of group assets through initiating M&A deals featured as financial investment and recapitalization. In total, 206 M&A partnerings were excluded from the models considering different business strategies due to an unclear M&A type in our analysis.

5. Empirical Results

5.1. Overall Effects of Proximities on China’s Domestic M&A Partnering

Independent variables (i.e., LnDistance and Intra_P/Intra_C/Intra_D, Inra_I, and Intra_G) with higher Pearson correlation coefficients were separately tested in models to avoid possible multicollinearity. The regression results on the overall impacts of multi-dimensional proximities on M&A partnering in the YRD during various periods are present in Table 3. The descriptive results of M&A partnerings during different periods are reported in Table 4 to help understand the changing effects of multi-dimensional proximities.

5.1.1. Effects of Geographical Proximity

The coefficients for LnDistance in all models, and that for Intra_P/Intra_C/Intra_D, are significantly negative and positive, respectively. This may imply that spatial closeness, especially located in the same administrative region, would promote corporate M&A partnering in the YRD. However, the average geographical distance between the acquirer and the target increased from 45.69 km during 1996–2000 to 79.99 km during 2011–2016. Although there more than 75%, 60%, and 45% of corporate partnerings, respectively, took place in the same province, city, and county (urban district) in the YRD during 2011–2016, the relevant proportions have been declining over time. These results indicate an obvious growth in interregional and long-distance M&As on the one hand, and the gradually weakened role played by geographical proximity in acquisition target selection of some corporations in the YRD on the other.

5.1.2. Effects of Cognitive Proximity

The coefficients for Inra_I and Intra_G are significantly positive in all models, suggesting that M&A deals would be more likely to succeed between corporations belonging to the same industrial provisions and major sectors. This signifies the importance of closer industrial and technological relatedness for M&A partnering. However, the share of M&A partnerings achieved by firms that belong to the same industrial provisions and major sectors has decreased from 53.89% and 42.50% during 2006–2010 to 47.70% and 35.65%, respectively. More than 20% of manufacturing acquirers tended to buy service targets to achieve business goals. This embodies a significant growth in cross-industry M&As related to industrial upgrading and amalgamation in the YRD since the early 2010s.

5.1.3. Effects of Organizational Proximity

The coefficients of Multi_L are significantly negative in most models, implying that multi-plants/locations acquirers might tend to buy targets with a single plant location to minimize the costs or risks of post-acquisition integration. In contrast, Same_S has significantly positive coefficients during 2006–2010 and 2011–2016, suggesting that the relatively similar size of the acquirer and the target would be vital for M&A partnering in the YRD. However, Table 4 presents a decreasing proportion of M&A partnerings that occurred between corporations with similar size during 2011–2016. Specifically, the capability of large enterprises to buy and internalize SMEs has been enhanced, while it is still very difficult for SMEs to merge the larger ones in the YRD. Considering the significance level of the relevant variables, the decisive influences of organizational proximity on M&A partnerings in the YRD may be weaker than that of geographical and cognitive dimensions.

5.1.4. Effects of Institutional Proximity

The coefficients for Same_Ins are significantly positive in all models, suggesting that acquiring corporations might prefer targets with a similar ownership structure. The results shown in Table 4 indicate that partners between POEs were the main force of the M&A market in the YRD. In contrast, List and Nonlist have negative and significant signs in most models, signifying that the similarity in corporate culture and governance of both (un)listed firms did not significantly promote corporate M&A partnerings in the YRD. M&A transactions between listed firms may be difficult due to complex processes of price negotiation and post-acquisition integration. Table 4 shows that the proportion of M&A partnerings between the listed acquirers and the unlisted targets accounted for 59.61% of the total in the YRD during 2011–2016. This result is in line with the preferences of large acquirers for small- and medium-sized targets in the YRD.

5.2. Acquiring Preferences of Corporations Differentiated by Attributes

Based on our conceptual framework, we explore the acquiring preferences of corporations with different industrial attributes, ownership structures, and sizes in the YRD during 1996–2016. The descriptive results can be found in Table 5.

5.2.1. Acquiring Preferences of Corporations with Different Industrial Attributes

The average geographical distances of M&A partnerings initiated by acquirers in manufacturing, producer services, and consumer and social services were 83.27 km, 61.08 km, and 57.73 km, respectively. Acquirers in service industries are more likely to search and purchase targets within the same administrative region in the YRD. These results indicate that M&A decisions of service corporations might be, compared with that of manufacturing ones, more sensitive to the effects of “home bias” related to geographical proximity. Although industrial and technological relatedness matter, manufacturing acquirers have shown a stronger inclination to merge across sectors, especially in producer services. This is probably because of the upgrading trend of manufacturing servitization in the YRD. The descriptive results also suggest that organizational proximity measured by locational patterns and institutional proximity measured by listed status have more significant impacts on M&A decisions of acquirers in service sectors.

5.2.2. Acquiring Preferences of Corporations with Different Ownership Structures

About 95% of M&A partnerings launched by SOEs occurred within the administrative regions. This is probably because investment behaviors and locational strategies of SOEs are profoundly affected by the intervention of local governments. Moreover, more than 65% of M&A partnerings initiated by SOEs occurred between corporations of comparable size. These results indicate that the administrative region economy related to geographical proximity, as well as organizational proximity measured by the similarity of firm size, have more significant impacts on M&A decisions of SOEs in the YRD. By contrast, the foreign- and private-owned acquirers tend to pay more attention to industrial and technological relatedness when searching and internalizing targets. The results also suggest that institutional proximity measured by the similarity of corporate ownership structures might be a key determinant of M&A partnering of POEs.

5.2.3. Acquiring Preferences of Corporations with Different Sizes

The average distance of acquisition target selection of SMEs in the YRD was shorter than that of large corporations, implying the sensitive response of M&A decisions of SMEs to geographical proximity or “home bias”. Large corporations may be more capable of carrying out long-distance or interregional M&As due to their experiences in cost/risk controlling and information searching. The results also signify that M&As of SMEs in service sectors to manufacturing targets would be more active, while large manufacturers showed a more obvious tendency of servitization through M&As. Institutional proximity, particularly the similarity in ownership structure, matters more for M&A partnerings launched by medium- and small-sized acquirers. We also find that large- and medium-sized acquirers might prefer to buy and internalize targets of the same size as their own, suggesting a trend of alliance between giants on the M&A market in the YRD.

5.3. Multi-Dimensional Proximities and M&A Partnering Differentiated by Types

For the third research question, we further examine the variegated roles of multi-dimensional proximities on M&A partnerings differentiated by corporate business goals, with particular attention given to financial investment, recapitalization, horizontal, vertical, and conglomerate M&A. The regression results are presented in Table 6.

5.3.1. Geographical Proximity and Different Types of M&A Partnering

Although the coefficients for variables related to geographical proximity are significantly positive in all models, the average geographical distance of M&A partnerings featured as financial investment or recapitalization was shorter than that of horizontal, vertical, and conglomerate M&As (see Figure 3). This partly indicates that the extents of roles played by spatial closeness and the administrative region economy in partnering would vary across M&A types in the YRD. With regard to financial investment and recapitalization M&As, corporations tend to invest in local high-quality corporate assets or equities through M&As to avoid unknown risks impeding capital appreciation.

5.3.2. Cognitive Proximity and Different Types of M&A Partnering

The coefficients for Inra_I and Intra_G have positive and significant signs in the models related to recapitalization, horizontal, vertical, and conglomerate M&A, while the effect of industrial and technological relatedness on the group of financial investment is insignificant in the YRD. This signifies that corporations might pay more attention to the potential of assets accretion, rather than industrial chain linkages or post-acquisition synergy, in capital managing or financial investment activities related to M&As. In contrast, recapitalization, as well as horizontal and vertical M&As, is mainly carried out between corporations whose products, technologies, and functions are interrelated; corporations will also take the costs and risks of post-acquisition integration into account when conducting conglomerate M&As related to diversification strategies. Cognitive proximity matters more for recapitalization, horizontal, vertical, and conglomerate M&As.

5.3.3. Organizational Proximity and Different Types of M&A Partnering

The coefficients of Multi_L are insignificant for financial investment and recapitalization, but significantly negative for horizontal and vertical M&As. This is probably because multi-plants/locations targets are more difficult to be internalized by acquirers, especially in horizontal and vertical M&As related to corporate control transfer and post-acquisition integration. On the contrary, the coefficients of Same_S are significantly positive for financial investment and recapitalization, but insignificant for horizontal, vertical, and conglomerate M&A. This is perhaps because most large acquiring corporations tend to merge SMEs in order to control the costs and risks of the post-acquisition integration in the YRD.

5.3.4. Institutional Proximity and Different Types of M&A Partnering

The coefficients of Same_Ins are positive and significant in all models, implying that institutional proximity measured by the similarity of corporate ownership structure plays a critical role in M&A partnering differentiated by various business goals. However, the influences of the similarity of listed status (i.e., List and Nonlist) are mixed. The coefficients of List and Nonlist are significantly negative for horizontal, vertical, and conglomerate M&As. This is perhaps because most relevant M&A partnerings involved both the large listed enterprise and the unlisted SMEs in the YRD. It should be noted that the coefficients of List and Nonlist are significantly negative and positive for recapitalization, respectively. This is probably because more than 55% of M&A partnerings related to recapitalization consisted of unlisted corporations in the YRD during 1996–2016 (see Figure 3).

6. Discussion: Proximity Dynamics of M&A Partnering in the Chinese Context

Although the administrative region economy related to “home bias” matters for corporate investment activities including M&As in China, the growing interregional M&As may indicate the weakened role played by spatial distance in M&A partnering over time. This is probably because of the enhancement of corporate capabilities of long-distance acquisition target selection on the one hand, and the improved infrastructure and socioeconomic linkages between regions in the YRD on the other [62]. The regression results also indicate that geographical proximity would have more significant effects on M&A decisions made by producer service, state-owned, and small-sized corporations, in comparison with that of manufacturing, private-owned, and listed ones.

Cognitive proximity measured by industrial and technological relatedness plays a crucial role in promoting M&A transactions between the acquirer and the target in transitional China. Corporations with a higher degree of cognitive proximity are even more likely to make long-distance M&A negotiation and integration, suggesting the benefits of industrial and technological relatedness might offset the potential risks and costs (e.g., information asymmetry) of acquisition target selection. We also find that cross-industry M&A partnerings experienced rapid growth since the early 2010s in the YRD. Particularly, private-owned and foreign-invested manufacturers have been increasingly acquiring targets in financial, business, and science and technical service industries. This is probably because of functional upgrading pursued by manufacturing firms and the economic transition pursued by the government in the YRD.

The effects of organizational and institutional proximity on M&A partnering are mixed in the Chinese context. Although M&A-related alliances between large and multi-plant corporations are an important way for acquirers in the YRD to promote organizational and spatial expansion, there were many private-owned and foreign-invested corporations that choose to acquire SMEs in order to control the costs of post-acquisition integration. Our analysis implies that it is more difficult for small-sized acquirers to merge large- and medium-sized targets. Institutional proximity measured by corporate ownership structure has significant impacts on acquisition target selection, especially for private-owned and small-sized acquiring corporations in the YRD. The descriptive results imply that state-owned acquirers might tend to carry out cross-ownership M&As, which is probably because of the reform of introducing mixed ownership to SOEs in transitional China.

Our findings also indicate the interactive dynamics between proximity dimensions, which is consistent with the hypotheses proposed by seminal works [49,51]. The average geographical distance between the acquirers and the targets with the similar industrial sector, locational pattern, or ownership structure is longer than the mean level of all M&A partnerings in the YRD during 2011–2016. Relevant descriptive results may indicate that cognitive, organizational, and institutional proximity would profoundly affect the effects of geographical proximity on M&A partnering. Specifically, the closer industrial and technical relatedness and similar management system between the acquirer and the target will partly offset the negative effects, such as information asymmetry largely resulting from the long distance.

Additionally, the role played by proximity dynamics in M&A partnering differs between M&A types based on corporate business strategies in the YRD. In order to ensure asset appreciation and control investment risks, acquirers in financial investment and recapitalization M&As are more sensitive to the effect of “home bias”, and pay more attention to the size, organizational network, and ownership structure of the targets. In contrast, acquiring corporations, which pursue product, technological, and functional upgrading in horizontal, vertical, and conglomerate M&As, are capable of internalizing long-distance targets, and show more concern about cognitive proximity measured by industrial and technical relatedness in acquisition target selection.

7. Conclusions

M&A activities have been increasingly reshaping corporate organizations, regional industrial dynamics, and the globalized socioeconomic systems, especially since the 1990s [8,29,40]. Although there is a large body of literature on the decision-making process, spatial pattern, and locational implication of corporate M&As [30,36,37], we know little about the driving forces of domestic M&As in emerging or transitional economies [64]. Particularly, research on the effects of firm-level attributes and inter-firm relations on M&As, which have been fully discussed in DEs, is quite limited under the contexts of EEs. Exploring the impacts of firm heterogeneities and multi-dimensional proximities on corporate M&A partnering in the YRD, one of the emerging global-city regions, this study aims to fill the aforementioned research gaps. We also investigate the variegated role of proximity dynamics in M&A partnering differentiated by business goals, such as financial investment, as well as horizontal/vertical integration and diversified development. The results underline the importance of geographical, cognitive, organizational, and institutional proximity between corporations for M&A partnerings, and this is in line with the findings generated by previous research on corporate M&As [26,31,32].

Specifically, “home bias” related to geographical proximity profoundly affected M&A decisions in the YRD; however, the capability of corporations to acquire long-distance targets has also significantly improved. Cognitive proximity and institutional proximity, particularly the similarity in industrial attributes and ownership structures, matter more for corporate M&A partnering in the YRD. In contrast, the effects of organizational proximity on M&A partnering were mixed in the YRD during different time periods. There exists interactive dynamics, which may differ across various phases of regional development, between multi-dimensional proximities in the process of acquisition target selection in the YRD. We also find that the acquiring preferences varied across corporations differentiated by attributes, and the response to multi-dimensional proximities differed across partnerings differentiated by M&A types.

This study will advance our understanding of the internal operating mechanism of the socioeconomic system through uncovering firm heterogeneities, proximity dynamics, and typological differentiation of M&As, one of the important corporate investment strategies, in regional China. On the one hand, the variegated inter-firm linkages, such as geographical, cognitive, organizational, and institutional proximity, are important for explaining the reshaping forces of the corporate networked economy and the decision process of corporate strategic behaviors. The governmental intervention embodied by local protectionism (or the administrative region economy) and incentive policies should be given more attention when investigating regional industrial dynamics and corporate investment activities in transitional and emerging economies such as China. On the other hand, our findings related to the effects of multi-dimensional proximities on five types of M&As (i.e., financial investment, recapitalization, horizontal, vertical, and conglomerate M&As) in the YRD would complement the existing literature on the determinants of M&A partnering. Furthermore, the systematic dynamics of M&A partnering, especially the periodical, interregional, and typological differences, in EEs call for more scholarly investigations. Corporate decision processes and management systems related to M&A partnering could also be focused on in further research from multiple disciplinary perspectives.

Funding

This work was funded by the National Natural Science Foundation of China (42001138), and the Scientific Research Foundation of Nanjing Institute of Geography and Limnology; Chinese Academy of Sciences (NIGLAS2019QD006).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Dicken, P.; Malmberg, A. Firms in territories: A relational perspective. Econ. Geogr. 2001, 77, 345–363. [Google Scholar] [CrossRef]

- Alcácer, J.; Cantwell, J.; Piscitello, L. Internationalization in the information age: A new era for places, firms, and international business networks? J. Int. Bus. Stud. 2016, 47, 499–512. [Google Scholar] [CrossRef]

- Sigler, T.; Martinus, K.; Loginova, J. Socio-spatial relations observed in the global city network of firms. PLoS ONE 2021, 16, e0255461. [Google Scholar] [CrossRef] [PubMed]

- Isaksen, A.; Jakobsen, S.E.; Njøs, R.; Normann, R. Regional industrial restructuring resulting from individual and system agency. Innov. Eur. J. Soc. Sci. Res. 2019, 32, 48–65. [Google Scholar] [CrossRef]

- MacKinnon, D. Beyond strategic coupling: Reassessing the firm-region nexus in global production networks. J. Econ. Geogr. 2012, 12, 227–245. [Google Scholar] [CrossRef]

- Seddighi, H.R.; Mathew, S. Innovation and regional development via the firm’s core competence: Some recent evidence from North East England. J. Innov. Knowl. 2020, 5, 219–227. [Google Scholar] [CrossRef]

- Hirshleifer, J. Investment Decision under Uncertainty: Choice—Theoretic approaches. Q. J. Econ. 1965, 79, 509–536. [Google Scholar] [CrossRef]

- Chapman, K. Cross-border mergers/acquisitions: A review and research agenda. J. Econ. Geogr. 2003, 3, 309–334. [Google Scholar] [CrossRef]

- Wang, J.; Wei, Y.D.; Lin, B. Functional division and location choices of Chinese outward FDI: The case of ICT firms. Environ. Plan. A Econ. Space 2021, 53, 937–957. [Google Scholar] [CrossRef]

- Knight, E.; Kumar, V.; Wójcik, D.; O’Neill, P. The competitive advantage of regions: Economic geography and strategic management intersections. Reg. Stud. 2020, 54, 591–595. [Google Scholar] [CrossRef]

- Brenes, E.R.; Ciravegna, L.; Woodside, A.G. Constructing useful models of firms’ heterogeneities in implemented strategies and performance outcomes. Ind. Mark. Manag. 2017, 62, 17–35. [Google Scholar] [CrossRef]

- Myles Shaver, J.; Flyer, F. Agglomeration economies, firm heterogeneity, and foreign direct investment in the United States. Strateg. Manag. J. 2000, 20, 1175–1193. [Google Scholar] [CrossRef]

- Seth, A.; Song, K.P.; Pettit, R. Synergy, managerialism or hubris? An empirical examination of motives for foreign acquisitions of US firms. J. Int. Bus. Stud. 2000, 31, 387–405. [Google Scholar] [CrossRef]

- Harré, M.S.; Eremenko, A.; Glavatskiy, K.; Hopmere, M.; Pinheiro, L.; Watson, S.; Crawford, L. Complexity Economics in a Time of Crisis: Heterogeneous Agents, Interconnections, and Contagion. Systems 2021, 9, 73. [Google Scholar] [CrossRef]

- Görg, H. Analysing foreign market entry—The choice between greenfield investment and acquisitions. Econ. Tech. Pap. 2000, 27, 165–181. [Google Scholar] [CrossRef] [Green Version]

- Raff, H.; Ryan, M.; Stähler, F. The choice of market entry mode: Greenfield investment, M&A and joint venture. Int. Rev. Econ. Financ. 2009, 18, 3–10. [Google Scholar]

- Harms, P.; Méon, P.G. Good and useless FDI: The growth effects of greenfield investment and mergers and acquisitions. Rev. Int. Econ. 2018, 26, 37–59. [Google Scholar] [CrossRef]

- Hansen, U.E.; Fold, N.; Hansen, T. Upgrading to lead firm position via international acquisition: Learning from the global biomass power plant industry. J. Econ. Geogr. 2016, 16, 131–153. [Google Scholar] [CrossRef]

- Moretti, F.; Biancardi, D. Inbound open innovation and firm performance. J. Innov. Knowl. 2020, 5, 1–19. [Google Scholar] [CrossRef]

- Chapman, K.; Edmond, H. Mergers/acquisitions and restructuring in the EU chemical industry: Patterns and implications. Reg. Stud. 2000, 34, 753–767. [Google Scholar] [CrossRef]

- Boschma, R.; Hartog, M. Merger and Acquisition Activity as Driver of Spatial Clustering: The Spatial Evolution of the Dutch Banking Industry, 1850–1993. Econ. Geogr. 2014, 90, 247–266. [Google Scholar] [CrossRef] [Green Version]

- Leigh, R.; North, D.J. Regional aspects of acquisition activity in British manufacturing industry. Reg. Stud. 1978, 12, 227–245. [Google Scholar] [CrossRef]

- Green, M.B. Mergers and acquisitions. In The International Encyclopedia of Geography; Richardson, D., Castree, N., Goodchild, M.F., Kobayashi, A., Liu, W., Marston, R.A., Eds.; John Wiley & Sons: New York, NY, USA, 2018. [Google Scholar]

- Rao, N.V.; Reddy, K. The impact of the global financial crisis on cross-border mergers and acquisitions: A continental and industry analysis. Eurasian Bus. Rev. 2015, 5, 309–341. [Google Scholar] [CrossRef]

- Gunessee, S.; Hu, S. Chinese cross-border mergers and acquisitions in the developing world: Is Africa unique? Thunderbird Int. Bus. Rev. 2021, 63, 27–41. [Google Scholar] [CrossRef]

- Ellwanger, N.; Boschma, R. Who Acquires Whom? The Role of Geographical Proximity and Industrial Relatedness in Dutch Domestic M&As between 2002 and 2008. Tijdschr. Econ. Soc. Geogr. 2015, 106, 608–624. [Google Scholar]

- Schildt, H.A.; Laamanen, T. Who buys whom: Information environments and organizational boundary spanning through acquisitions. Strateg. Organ. 2006, 4, 111–133. [Google Scholar] [CrossRef]

- Böckerman, P.; Lehto, E. Geography of Domestic Mergers and Acquisitions (M&As): Evidence from Matched Firm-level Data. Reg. Stud. 2006, 40, 847–860. [Google Scholar]

- Zademach, H.-M.; Rodríguez-Pose, A. Cross-Border M&As and the Changing Economic Geography of Europe. Eur. Plan. Stud. 2009, 17, 765–789. [Google Scholar]

- Di Guardo, M.C.; Marrocu, E.; Paci, R. The Concurrent Impact of Cultural, Political, and Spatial Distances on International Mergers and Acquisitions. World Econ. 2016, 39, 824–858. [Google Scholar] [CrossRef]

- Boschma, R.; Marrocu, E.; Paci, R. Symmetric and asymmetric effects of proximities. The case of M&A deals in Italy. J. Econ. Geogr. 2016, 16, 505–535. [Google Scholar]

- Kvĕtoň, V.; Bĕlohradský, A.; Blažek, J. The variegated role of proximities in acquisitions by domestic and international companies in different phases of economic cycles. Pap. Regi. Sci. 2020, 99, 583–602. [Google Scholar] [CrossRef]

- Green, M.B.; Cromley, R.G. The horizontal merger: Its motives and spatial employment impacts. Econ. Geogr. 1982, 58, 358–370. [Google Scholar] [CrossRef]

- Rozen-Bakher, Z. Comparison of merger and acquisition (M&A) success in horizontal, vertical and conglomerate M&As: Industry sector vs. services sector. Serv. Ind. J. 2018, 38, 492–518. [Google Scholar]

- Duysters, G.; Cloodt, M.; Schoenmakers, W.; Jacob, J. Internationalisation efforts of Chinese and Indian companies: An empirical perspective. Tijdschr. Econ. Soc. Geogr. 2015, 106, 169–186. [Google Scholar] [CrossRef]

- Lebedev, S.; Peng, M.W.; Xie, E.; Stevens, C.E. Mergers and acquisitions in and out of emerging economies. J. World Bus. 2015, 50, 651–662. [Google Scholar] [CrossRef]

- Buckley, P.J.; Yu, P.; Liu, Q.; Munjal, S.; Tao, P. The institutional influence on the location strategies of multinational enterprises from emerging economies: Evidence from China’s cross-border mergers and acquisitions. Manag. Organ. Rev. 2016, 12, 425–448. [Google Scholar] [CrossRef] [Green Version]

- Bruhn, N.C.P.; Calegário, C.L.L.; de Melo Carvalho, F.; Campos, R.S.; dos Santos, A.C. Mergers and acquisitions in Brazilian industry: A study of spillover effects. Int. J. Product. Perform. Manag. 2017, 66, 51–77. [Google Scholar] [CrossRef]

- Zheng, Y.; Yan, D.; Ren, B. Institutional distance, firm heterogeneities, and FDI location choice of EMNEs. Nankai Bus. Rev. Int. 2016, 7, 192–215. [Google Scholar] [CrossRef]

- Hossain, M.S. Merger & Acquisitions (M&As) as an important strategic vehicle in business: Thematic areas, research avenues & possible suggestions. J. Econ. Bus. 2021, 116, 106004. [Google Scholar]

- Ascani, A. The takeover selection decisions of multinational enterprises: Empirical evidence from European target firms. J. Econ. Geogr. 2018, 18, 1227–1252. [Google Scholar] [CrossRef]

- Kim, S.J. Networks, scale, and transnational corporations: The case of the South Korean seed industry. Econ. Geogr. 2006, 82, 317–338. [Google Scholar] [CrossRef]

- Clark, G.L. Costs and prices, corporate competitive strategies and regions. Environ. Plan. A 1993, 25, 5–26. [Google Scholar] [CrossRef]

- Hussinger, K. On the importance of technological relatedness: SMEs versus large acquisition targets. Technovation 2010, 30, 57–64. [Google Scholar] [CrossRef]

- Rodríguez-Pose, A.; Zademach, H.M. Industry dynamics in the German merger and acquisitions market. Tijdschr. Econ. Soc. Geogr. 2006, 97, 296–313. [Google Scholar] [CrossRef] [Green Version]

- Mariotti, S.; Piscitello, L.; Elia, S. Local externalities and ownership choices in foreign acquisitions by multinational enterprises. Econ. Geogr. 2014, 90, 187–211. [Google Scholar] [CrossRef]

- Barattieri, A.; Borchert, I.; Mattoo, A. Cross-border mergers and acquisitions in services: The role of policy and industrial structure. Can. J. Econ. 2016, 49, 1470–1501. [Google Scholar] [CrossRef] [Green Version]

- Weitzel, U.; McCarthy, K.J. Theory and evidence on mergers and acquisitions by small and medium enterprises. Int. J. Entrep. Innov. Manag. 2011, 14, 248–275. [Google Scholar] [CrossRef] [Green Version]

- Balland, P.; Boschma, R.; Frenken, K. Proximity and Innovation: From Statics to Dynamics. Reg. Stud. 2015, 49, 907–920. [Google Scholar] [CrossRef]

- Caragliu, A.; Nijkamp, P. Space and knowledge spillovers in European regions: The impact of different forms of proximity on spatial knowledge diffusion. J. Econ. Geogr. 2016, 16, 749–774. [Google Scholar] [CrossRef]

- Boschma, R. Proximity and Innovation: A Critical Assessment. Reg. Stud. 2005, 39, 61–74. [Google Scholar] [CrossRef]

- Chakrabarti, A.; Mitchell, W. The persistent effect of geographic distance in acquisition target selection. Organ. Sci. 2013, 24, 1805–1826. [Google Scholar] [CrossRef] [Green Version]

- Wu, J.; Wei, Y.D.; Chen, W. Spatial proximity, localized assets, and the changing geography of domestic mergers and acquisitions in transitional China. Growth Chang. 2020, 51, 954–976. [Google Scholar] [CrossRef]

- PwC 2021. China M&A 2020 Review and 2021 Outlook. Available online: https://www.pwccn.com/en/services/deals-m-and-a/publications/ma-2020-review-and-2021-outlook.html (accessed on 1 October 2021).

- Wei, G. Ownership structure, corporate governance and company performance in China. Asia Pac. Bus. Rev. 2007, 13, 519–545. [Google Scholar] [CrossRef]

- Li, L.; McMurray, A.; Sy, M.; Xue, J. Corporate ownership, efficiency and performance under state capitalism: Evidence from China. J. Policy Model. 2018, 40, 747–766. [Google Scholar] [CrossRef]

- Wei, Y.H.D. Network linkages and local embeddedness of foreign ventures in China: The case of Suzhou municipality. Reg. Stud. 2015, 49, 287–299. [Google Scholar] [CrossRef]

- Wei, Y.D. Decentralization, marketization, and globalization: The triple processes underlying regional development in China. Asian Geogr. 2001, 20, 7–23. [Google Scholar] [CrossRef]

- Wei, Y.D.; Bi, X.; Wang, M.; Ning, Y. Globalization, economic restructuring, and locational trajectories of software firms in shanghai. Prof. Geogr. 2016, 68, 211–226. [Google Scholar] [CrossRef]

- He, C.; Pan, F.; Chen, T. Research progress of industrial geography in China. J. Geogr. Sci. 2016, 26, 1057–1066. [Google Scholar] [CrossRef]

- Fan, G.; Ma, G.; Wang, X. Institutional reform and economic growth of China: 40-year progress toward marketization. Acta Oecon. 2019, 69, 7–20. [Google Scholar] [CrossRef]

- Chen, W.; Yenneti, K.; Wei, Y.D.; Yuan, F.; Wu, J.; Gao, J. Polycentricity in the Yangtze River Delta Urban Agglomeration (YRDUA): More cohesion or more disparities? Sustainability 2019, 11, 3106. [Google Scholar] [CrossRef] [Green Version]

- Ye, C.; Zhu, J.; Li, S.; Yang, S.; Chen, M. Assessment and analysis of regional economic collaborative development within an urban agglomeration: Yangtze River Delta as a case study. Habitat Int. 2019, 83, 20–29. [Google Scholar] [CrossRef]

- Wu, J.; Wei, Y.; Li, Q.; Yuan, F. Economic transition and changing location of manufacturing industry in china: A study of the yangtze river delta. Sustainability 2018, 10, 2624. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Conceptual framework of relationships among firm heterogeneity, proximity, and M&A partnering.

Figure 1.

Conceptual framework of relationships among firm heterogeneity, proximity, and M&A partnering.

Figure 2.

The location of the Yangtze River Delta, China.

Figure 3.

Descriptive results of M&A partnerings differentiated by corporate business goals.

{kind=link}

{kind=link}

{kind=link}

Table 1.

The definition of independent variables.

| Category | Description | Abbreviation | |

|---|---|---|---|

| Geographical proximity | Spatial distance | Spatial distance (km) calculated by ArcGIS between the acquirer and the target | LnDistance |

| Same province | Dummy variable, 1 when the acquirer and the target are co-located in the same province | Intra_P | |

| Same city | Dummy variable, 1 when the acquirer and the target are co-located in the same city | Intra_C | |

| Same county/urban district | Dummy variable, 1 when the acquirer and the target are co-located in the same county or urban district | Intra_D | |

| Cognitive proximity | Same industrial division | Dummy variable, 1 when the highest degree of industrial and technical relatedness is at industrial division | Inra_I |

| Same major sector | Dummy variable, 1 when the highest degree of industrial and technical relatedness is at major sector | Intra_G | |

| Organizational proximity | Same locational pattern | Dummy variable, 1 when both the acquirer and the target have at least one outside investment event | Multi_L |

| Same size | Dummy variable, 1 when the acquirer and the target are grouped in the same size measured by registered capital | Same_S | |

| Institutional proximity | Same ownership structure | Dummy variable, 1 when the acquirer and the target are featured by the same ownership structure (i.e., SOEs, POEs, and FIEs) | Same_Ins |

| Same listed status | Dummy variable, 1 when both the acquirer and the target are listed corporations | List | |

| Dummy variable, 1 when both the acquirer and the target are unlisted firms | Nonlist | ||

Table 2.

Description of the partnerings and non-partnerings of M&A in the YRD.

| Category | M&A Partnerings | M&A Non-Partnerings | |

|---|---|---|---|

| Geographical proximity | Distance mean | 69.83 km | 187.43 km |

| Same province | 80.34% | 29.34% | |

| Same city | 68.00% | 14.78% | |

| Same county/urban district | 49.01% | 5.44% | |

| Cognitive proximity | Same industrial division | 48.88% | 32.70% |

| Same major sector | 37.16% | 17.85% | |

| Organizational proximity | Same locational pattern | 56.04% | 57.28% |

| Same size | 46.39% | 41.79% | |

| Institutional proximity | Same ownership structure | 70.26% | 69.99% |

| Both listed | 1.77% | 3.78% | |

| Both unlisted | 38.08% | 43.91% | |

| Number of M&A deals | 5543 | 1,890,104 | |

Note: “Distance mean” is the average distance between the acquirer and the target in our dataset.

Table 3.

Regression results for the effects of proximities on M&As in the YRD.

| Variables | 1996–2016 | 1996–2000 | 2001–2005 | 2006–2010 | 2011–2016 |

|---|---|---|---|---|---|

| LnDistance | −0.855 *** | −0.559 *** | −0.812 *** | −0.903 *** | −0.886 *** |

| Intra_P | (1.128 ***) | (1.492 ***) | (1.411 ***) | (1.440 ***) | (0.978 ***) |

| Intra_C | (0.731 ***) | (1.648 ***) | (0.629 ***) | (0.750 ***) | (0.786 ***) |

| Intra_D | (1.496 ***) | (0.631 ***) | (1.435 ***) | (1.441 ***) | (1.597 ***) |

| Inra_I | 0.601 *** | 0.620 *** | 0.594 *** | 0.794 *** | 0.518 *** |

| Intra_G | (0.981 ***) | (0.694***) | (0.972 ***) | (1.126 ***) | (0.934 ***) |

| Multi_L | −0.077 ** | 0.079 | −0.194 * | −0.128 * | −0.101 ** |

| Same_S | 0.100 *** | 0.001 | 0.139 | 0.144 * | 0.094 ** |

| Same_Ins | 0.401 *** | 0.579 *** | 0.352 *** | 0.382 *** | 0.357 *** |

| List | −1.515 *** | −1.124 ** | −1.247 *** | −1.564 *** | −1.400 *** |

| Nonlist | −0.546 *** | −0.231 | −0.306 *** | −0.471 *** | −0.626 *** |

| _cons | 1.627 *** (−3.131 ***) | −0.106 (−3.043 ***) | 1.324 (−3.399 ***) | 1.643 *** (−3.504 ***) | 1.945 *** (−2.963 ***) |

| No. of partnerings | 5543 | 124 | 696 | 1413 | 3310 |

| No. of non-partnerings | 27,715 | 620 | 3480 | 7065 | 16,550 |

| -Log likelihood | 11,137.1 (11,050.5) | 289.5 (299.7) | 1395.1 (1367.5) | 2661.6 (2658.4) | 6730.7 (6658.4) |

| LR chi2 | 7700.7 *** (7874.0 ***) | 91.5 *** (71.0 ***) | 978.3 *** (1033.6 ***) | 2316.5 *** (2322.9 ***) | 4434.8 *** (4579.6 ***) |

| Pseudo R2 | 0.257 (0.263) | 0.137 (0.106) | 0.260 (0.274) | 0.303 (0.304) | 0.248 (0.256) |

Note: ***, **, and * denote statistical significance at 1%, 5%, and 10%, respectively. The coefficients for the highly correlated variables that are respectively tested in the model are presented in the parentheses.

Table 4.

Descriptive results of M&A partnerings in the YRD during different phases.

| 1996–2000 | 2001–2005 | 2006–2010 | 2011–2016 | |

|---|---|---|---|---|

| Distance mean | 45.69 km | 53.37 km | 56.30 km | 79.99 km |

| Same province | 86.29% | 85.26% | 85.22% | 76.92% |

| Same city | 83.06% | 76.39% | 74.47% | 62.84% |

| Same county/urban district | 44.35% | 52.65% | 52.48% | 46.89% |

| Same industrial division | 43.55% | 45.06% | 53.89% | 47.70% |

| Same major sector | 30.65% | 34.48% | 42.50% | 35.65% |

| Acquirer services, target manufacturing | 25.00% | 17.60% | 13.65% | 11.45% |

| Acquirer manufacturing, target producer services | 0.81% | 4.43% | 5.30% | 14.83% |

| Acquirer manufacturing, target consumer and social services | 8.06% | 8.15% | 5.59% | 6.10% |

| Both multi-locations/plants corporations | 6.45% | 63.38% | 56.58% | 56.07% |

| Same size | 36.29% | 48.78% | 51.49% | 44.05% |

| Acquirer large-sized, target medium-sized | 37.90% | 29.61% | 30.13% | 36.65% |

| Acquirer large-sized, target small-sized | 15.32% | 9.01% | 8.13% | 10.15% |

| Acquirer SMEs, target large-sized | 0.00% | 7.87% | 6.08% | 4.56% |

| Same ownership structure | 54.84% | 64.23% | 62.80% | 75.26% |

| Both listed corporations | 6.45% | 2.58% | 1.70% | 1.45% |

| Acquirer listed, target unlisted | 50.81% | 38.20% | 44.48% | 59.61% |

Table 5.

Descriptive results of M&A partnerings initiated by acquirers with different attributes in the YRD.

Table 5.

Descriptive results of M&A partnerings initiated by acquirers with different attributes in the YRD.

| Manufacturing | Producer Services | Consumer and Social Services | SOEs | POEs | FIEs | Large-Sized | Medium-Sized | Small-Sized | |

|---|---|---|---|---|---|---|---|---|---|

| Distance mean | 83.27 km | 61.08 km | 57.73 km | 32.64 km | 69.26 km | 75.59 km | 72.61 km | 55.37 km | 57.87 km |

| Same province | 78.74% | 80.52% | 82.90% | 94.69% | 80.35% | 77.22% | 79.62% | 83.96% | 84.36% |

| Same city | 62.86% | 71.60% | 71.62% | 87.55% | 66.78% | 67.41% | 66.79% | 74.26% | 73.74% |

| Same county/urban district | 48.50% | 49.61% | 50.76% | 61.22% | 50.63% | 43.34% | 48.18% | 53.64% | 51.40% |

| Same industrial division | 51.78% | 47.11% | 50.04% | 40.41% | 49.10% | 54.44% | 48.66% | 50.67% | 47.49% |

| Same major sector | 51.78% | 23.24% | 36.79% | 25.51% | 37.10% | 46.26% | 37.71% | 35.98% | 27.93% |

| Acquirer services, target manufacturing | — | 25.89% | 16.83% | 22.86% | 14.49% | 8.06% | 11.88% | 19.14% | 18.99% |

| Acquirer manufacturing, target producer services | 28.44% | — | — | 3.27% | 9.88% | 11.80% | 12.27% | 2.96% | 5.03% |

| Acquirer manufacturing, target consumer and social services | 16.55% | — | — | 3.27% | 5.46% | 9.23% | 6.95% | 3.10% | 2.23% |

| Both multi-locations/plants corporations | 51.78% | 63.40% | 50.94% | 64.29% | 55.29% | 52.80% | 56.82% | 50.94% | 57.54% |

| Same size | 42.08% | 49.81% | 45.93% | 66.73% | 44.29% | 45.91% | 47.51% | 45.28% | 22.35% |

| Acquirer large-sized, target medium-sized | 41.80% | 27.77% | 32.59% | 23.47% | 30.41% | 37.50% | 40.96% | — | — |

| Acquirer large-sized, target small-sized | 11.27% | 8.39% | 8.50% | 4.90% | 8.84% | 10.86% | 11.53% | — | — |

| Acquirer SMEs, target large-sized | 2.47% | 7.47% | 7.07% | 2.65% | 8.76% | 3.50% | — | 32.61% | 27.37% |

| Same ownership structure | 70.66% | 67.89% | 74.49% | 9.80% | 88.43% | 18.22% | 68.37% | 79.38% | 81.56% |

| Both listed corporations | 1.95% | 1.45% | 1.43% | 0.41% | 0.62% | 3.04% | 2.12% | 0.00% | 0.00% |

| Both unlisted corporations | 21.49% | 51.83% | 45.57% | 58.16% | 52.75% | 23.95% | 27.52% | 90.97% | 91.62% |

| Acquirer listed, target unlisted | 74.18% | 33.08% | 47.72% | 14.69% | 38.29% | 71.14% | 63.22% | 1.35% | 0.00% |

| Acquirer unlisted, target listed | 2.38% | 13.65% | 5.28% | 26.73% | 8.34% | 1.87% | 7.14% | 7.68% | 8.38% |

Table 6.

Regression results for the effects of proximities on different types of M&As in the YRD.

| Variables | Financial Investment M&As | Recapitalization M&As | Horizontal M&As | Vertical M&As | Conglomerate M&As |

|---|---|---|---|---|---|

| LnDistance | −0.858 *** | −0.988 *** | −0.868 *** | −0.849 *** | −0.829 *** |

| Intra_P | (1.571 ***) | (1.272 ***) | (1.060 ***) | (1.116 ***) | (1.114 ***) |

| Intra_C | (0.278) | (1.099 ***) | (0.807 ***) | (0.716 ***) | (0.583 ***) |

| Intra_D | (1.630 ***) | (1.464 ***) | (1.416 ***) | (1.399 ***) | (1.563 ***) |

| Inra_I | 0.085 | 0.402 *** | 0.519 *** | 0.864 *** | 0.462 *** |

| Intra_G | (0.092) | (0.619 ***) | (1.118 ***) | (1.359 ***) | (0.857 ***) |

| Multi_L | −0.036 | −0.084 | −0.390 ** | −0.158 *** | −0.025 |

| Same_S | 0.402 *** | 0.544 *** | −0.075 | 0.045 | −0.094 |

| Same_Ins | 0.613 *** | 0.513 *** | 0.321 * | 0.342 *** | 0.340 *** |

| List | −0.494 | −1.051 *** | −1.964 ** | −1.588 *** | −1.917 *** |

| Nonlist | 0.147 | 0.323 *** | −0.848 *** | −1.009 *** | −0.529 *** |

| _cons | 1.109 *** (−3.122 ***) | 1.446 *** (−3.369 ***) | 2.205 *** (−3.117 ***) | 1.763 *** (−3.215 ***) | 1.681 *** (−3.028 ***) |

| No. of partnerings | 465 | 792 | 247 | 2522 | 1311 |

| No. of non-partnerings | 2325 | 3960 | 1235 | 12,610 | 6555 |

| -Log likelihood | 952.4 (945.9) | 1458.4 (1469.2) | 502.3 (492.6) | 4959.4 (4970.1) | 2686.6 (2678.5) |

| LR chi2 | 625.6 *** (638.6 ***) | 1367.2 *** (1345.5 ***) | 331.0 *** (350.2) | 3716.9 *** (3695.6 ***) | 1718.7 *** (1734.8 ***) |

| Pseudo R2 | 0.247 (0.252) | 0.319 (0.314) | 0.249 (0.262) | 0.273 (0.271) | 0.242 (0.245) |

Note: ***, **, and * denote statistical significance at 1%, 5%, and 10%, respectively. The coefficients for the highly correlated variables that are respectively tested in the model are presented in parentheses.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Wu, J. Firm Heterogeneities, Multi-Dimensional Proximities, and Systematic Dynamics of M&A Partnering: Evidences from Transitional China. Systems 2022, 10, 32. https://0-doi-org.brum.beds.ac.uk/10.3390/systems10020032

AMA Style

Wu J. Firm Heterogeneities, Multi-Dimensional Proximities, and Systematic Dynamics of M&A Partnering: Evidences from Transitional China. Systems. 2022; 10(2):32. https://0-doi-org.brum.beds.ac.uk/10.3390/systems10020032

Chicago/Turabian StyleWu, Jiawei. 2022. "Firm Heterogeneities, Multi-Dimensional Proximities, and Systematic Dynamics of M&A Partnering: Evidences from Transitional China" Systems 10, no. 2: 32. https://0-doi-org.brum.beds.ac.uk/10.3390/systems10020032

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.