Coopetition in the SoC Industry: The Case of Qualcomm Incorporated

Ewha School of Business, Ewha Womans University, 52 Ewhayeodae-gil, Seodaemun-gu, Seoul 121791, Korea

*

Author to whom correspondence should be addressed.

J. Open Innov. Technol. Mark. Complex. 2020, 6(1), 9; https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc6010009

Submission received: 3 December 2019

/

Revised: 20 January 2020

/

Accepted: 29 January 2020

/

Published: 2 February 2020

Abstract

:This study uses the lens of competitive dynamics to examine the coopetition process, which combines both cooperation and competition, employed by Qualcomm within the SoC (System on a Chip) design market related to smart devices. Qualcomm succeeded in developing the first SoC, which integrated GPS (Global Positioning System) and other software, and during the process of developing mobile chips has simultaneously cooperated and competed with competitors. In particular, Samsung, which began as a customer of the firm, has since become its competitor. By conducting descriptive case analysis, this study shows a coopetition process in the SoC industry and supplemented a coopetition study with the actual exemplary coopetition case.

1. Introduction

In a highly competitive environment, firms must continuously innovate to gain a competitive advantage over other firms. Although most of the firms seem to compete against each other to maintain their advantage continuously, firms also often cooperate with their competitors even while competing. Especially in a high-tech industry where technological innovation and change in products are fast, it is difficult to cope with global competitors with a single, static strategy. In other words, a dynamic competition and cooperation between firms is necessary to sustain a firm’s competitive advantage. This has led some researchers [1] to claim that within a complex business environment, firms should act outside of their boundaries and cooperate with other firms through “open innovation” by interacting with other firms or players in the market, as surviving alone in a competitive business environment is difficult to achieve.

Coopetition is a term that refers to the simultaneous coexistence of cooperation and competition. The term, based on game theory and popularized by Nalebuff and Brandenburger [2], was coined to reflect the reality of business management today as companies must respond rapidly to changes in their business environment [3]. The dynamics of coopetition behavior assume that firms cannot survive alone in the changing environment and that interdependencies among firms create value for those firms [3,4,5]. Coopetition has been previously discussed in various theoretical and empirical studies, which have shown, for instance, that coopetition can be a source of innovation [6,7], and there are also tensions between cooperation and competition [8]. This case study is intended to complement that literature by looking at the actual changes in competitiveness and performance created by one highly successful firm’s coopetition and demonstrating that these actions occur in complex competitive dynamics and influence the firm’s strategic behavior.

Throughout its history, Qualcomm has not only developed innovative technology but also survived with cooperation with other companies. The competitive behavior of Qualcomm thus should be understood as dynamic interactions in which Qualcomm both competes with and cooperates with its rivals. These interactions with their rivals do not occur alone but are intertwined and interrelated with one another. Interactions with a firm’s rivals affect firm’s survival and can lead to destructive or productive results [9]. This study focuses on the cooperation and competition between Qualcomm and Samsung and how firms employ coopetition to gain a competitive advantage.

Coopetition occurs in two different but interdependent ways regarding the cooperative and competitive firm activities. Although these two processes may seem distinct, simultaneous competition and cooperation exist among firms. In this study, coopetition was analyzed over time. It conducted a comparative case analysis of the two firms to examine how the coopetitive process actually evolves and changes over time.

This study contributes to coopetition research by analyzing and describing how specific firm events and external environmental changes affect competition and cooperation over time. In particular, we identified that competitive actions and reactions of firms are the key foundations of the change and evolution of the coopetitive process. The competitive actions of firms bring competition as well as cooperation reactions from their competitors. The choice of competitive and cooperative reactions depends on how other firms interpret and perceive other firm’s competitive activities.

To achieve this research goal, we first review the literature relevant to the concept of coopetition and then analyzes the case of Qualcomm’s coopetition behavior with Samsung as an example of this dynamic. By analyzing the coopetition process of Qualcomm, this paper provides deeper insights into the dynamics of coopetition behavior.

2. Literature Review

The case of Qualcomm shows the process of innovation and coopetition achieved throughout the growth of the SoC industry and thus helps to link the existing literature of coopetition to the real-life situation from this case study. This case study is established upon the competitive dynamics approach that mainly focused on the coopetitive behavior of the firm.

2.1. Competitive Dynamics

Existing research into competitive dynamics has assumed that competition is a most crucial facet of competitive dynamics, and therefore, focused on the competitive moves of a firm [10] and the specific behaviors and responses of competitors [11]. As this literature has shown, the management process of firms becomes increasingly competitive during such phases as launching new products, increasing market share, and securing customers. At the same time, as researchers have noted, firms sometimes also partner and make alliances with competitors in order to compete [12]. The key issue explored by research on competitive dynamics is how a particular competitive behavior affects a firm’s competitive advantage and competition in the long run [9].

As this body of research has demonstrated, the environment and conditions in which firms compete differ across industries and time periods. In those different conditions, competitive interactions among firms lead to certain firm performance. The action and reaction of firms are interdependent to the extent their strategic actions affect firm performance [13]. This case study, while examining the ways in which the specific industry dynamics shaped their competitive actions, also enlarges upon those findings by analyzing the ways in which that competition was affected and mediated by strategic coopetition with its rivals.

2.2. Coopetition

As globalization increases competition and the life cycle of products and technologies shorten, most tech companies can no longer effectively respond to the changes in the business environment based solely on their internal resources or abilities. Therefore, many firms have chosen to work closely with various other businesses to improve and sustain their own competitiveness [14]. In practice, alliances between firms have become widespread regardless of industry. According to a recent investigation, such a combination of competition and cooperation has led to innovative outcomes and economic growth [15]. Bengtsson et al. [16] defined this combination, coopetition, as “a process based upon simultaneous and mutual cooperative and competitive interactions between two or more actors at any level of analysis—whether individual, organizational or other entities”.

The focus on concurrent competition and cooperation is the key issue explored in the literature on coopetition. It can be understood as a cooperative strategy that is applied to a cooperative and competitive relationship between firms and their competitors. Coopetition allows companies to share resources, technology, and know-how with their competitors. It enables them to enjoy all the advantages of cooperation and competition by maintaining a cooperative system and competing with each other to improve their performance in other fields [17]. As the era of technological convergence, interfirm competition or cooperation is now considered as an inevitable means of survival in the global competitive market. Moreover, the increased interconnection between global organizations makes coopetition a vital source of a firm’s strategy.

According to Lado et al. [18], the pursuit of coopetition could lead to positive results. When firms strive to achieve balanced competition and cooperation, which delineates syncretic rent-seeking behavior, they could have various options for their strategic choice that result in having a competitive advantage.

Cooperation between competitors has multiplied during the past decade [16]. Coopetition is reinforced by the “market commonality and resource asymmetry” among global rivals [17]. The commonality within the market leads to more competitive actions while the asymmetry within resources leads to more cooperative actions. Coopetition is helpful for rival organizations to promote their internal resources while protecting them against their other competitors [19].

Collaboration with competitors enables firms to internalize their competitors’ abilities. Coopetition could also reduce the threats associated with expansions. It may be too risky or costly for a firm to enter global markets alone. Partnering with competitors may be a way to avoid the uncertainty associated with the expansion of markets. It also reduces the time that could take longer when implementing technologies and innovative behaviors alone. Moreover, coopetition helps to deal with outside stakeholders such as governments and to strengthen positioning in the market within a cooperative group. When these groups are dominant players, they collaborate to weaken the pressures from the regulations. Even if interdependence among competitors is increasing, the conflict of interest still exists. By cooperating, firms could earn a better position for bargaining their resources, processes, and performances. When these cooperations work, the return from them would be beneficial for all participants [17].

Coopetition may help firms to have broader strategic choices than through competition or cooperation alone. For global firms, with the diverse product line and wide region, coopetition leads firms to realize many competitive and cooperative choices in several areas. On the other hand, competition or cooperation alone leads to narrow strategic choices. When firms are focused only on competition, it might look for ways to dominate the market, such as strengthening barriers to entry, exerting power to deter other firm’s investments, or conspiring with incumbents to limit outputs, increase prices and manipulate supplies. It would be beneficial to the firms that exercise such powers in the short run; however, it would lead to strategic rigidity that could undermine the long-term feasibility of the firm. Being stuck in a strategic rigidity may result in organizational myopia [20]. Similarly, focusing only on the cooperation would be negative to the firm due to the difficulty to completely control the opportunistic behavior of other firms, which is a risk that their important corporate information or strategy may be leaked when firms are strategically affiliated with a competitor [17]. Likewise, coopetition is not always superior in all respects because it entails management risks and costs. Therefore, strategic success can be achieved only when cooperation with competitors is sufficient to ensure that the benefits are enough to compensate the risk, that is, an equivalent relationship that can be expected to complement each other [17]. Coopetition is a type of contract that involves collaboration to achieve common goals among competing firms, such as joint ventures, licensing, franchising, and the creation of a joint technology development team. However, it is also possible to think of intangible cooperation that does not involve special forms of contracting. Even invisible partnerships between competing firms, such as building an industrial infrastructure, pressure on governments, sharing distribution channels and suppliers, and forming industrial clusters for production and development activities, can also be within the scope of coopetition [17].

From a coopetitive perspective, for instance, Qualcomm developed a mobile application processor which became the dominant player in the market. How the process of competitive dynamic has occurred is the main concern. Qualcomm competed and cooperated with rival firms such as Samsung. In addition, firms participating in the coopetition has to face management risks to preserve their competitiveness. In order to research this process of coopetition, a case analysis was conducted.

3. Research Method

This case study describes and analyzes the coopetition process within the non-memory semiconductor industry by focusing on Qualcomm’s coopetitive relationships with other companies. This study showed the process of coopetition in the non-memory semiconductor industry, one of the representative areas of technology-intensive industry. This study reflects the phenomena and issues of technology management in the real SoC industry. This study examines the coopetition process of Qualcomm by analyzing its specific actions and reactions of other firms. Qualcomm’s case in the non-memory semiconductor industry, where strategic coopetition continues to develop despite fierce competition, could be seen as a prime example of research from a coopetition perspective. The analysis shows the changing relationship between firms in the process of forming the core technologies of the mobile AP.

For the purpose of this study, a qualitative case study was conducted. A case study approach is used when an in-depth analysis is required to explain the reasons why, how, or process of a particular situation occurred [21]. In this case, a descriptive case study method was carried out to understand the process and significance of the case [22]. It is applied when explaining the actual situation that has occurred. The growth of a firm throughout the development of the SoC industry offers an appropriate case for analyzing the industry and market situation. For this case study, data have been mainly acquired from secondary resources such as news articles and industry reports that are publicly available online. As this analysis of the SoC industry and comparison of the activities of different key players in the market shows, Qualcomm has been a major player and is now facing some challenges.

4. Qualcomm Background

4.1. History

Qualcomm was founded by Irwin M. Jacobs and six MIT (Massachusetts Institute of Technology) alumni in 1985 in La Jolla, California. It designs and manufactures multinational semiconductor and telecommunications equipment in the United States. Qualcomm applied for its first commercial patent for CDMA in 1986, continues to develop new technologies starting with this. In 1989, Qualcomm began to make use of code division multiple access (CDMA) technologies, a channel access technology that enables multiple transmitters to access a single channel simultaneously. Qualcomm succeeded in a demonstration call based on CDMA. Since then, CDMA technology has been commercialized sequentially by Qualcomm, from the first base station of mobile communication with CDMA to transfer control protocol-internet protocol (TCP-IP) service over CDMA and to CD-7000, which was the first CDMA-based cellular telephone. In July 1993, the U.S Telecommunications Industry Association established CDMA as a standard of telecommunication. CDMA went global in 1995, when Global CDMA service was launched first in Hong Kong and then in South Korea and Peru.

Although Qualcomm’s technology became the industry standard and flourished, the company continued to make technological advances. In 2000, Qualcomm succeeded in the development of the first CDMA chipset integrated with GPS and other system software, which allowed many functions, such as MP3, internet, and Bluetooth, to be pooled into just one chipset.

In November 2007, Qualcomm commercialized its CDMA-integrated chipset under the name Snapdragon as well as two chipset solutions that helped Qualcomm become the world’s leading mobile chipset provider. The speed of the two chipset solutions, QSD8250 and QSD 8650 exceeded previous gigahertz barriers and allowed users to enjoy speedy data processing and a 3G wireless environment with lower battery consumption. The Snapdragon platform has facilitated an instantly on and always connected user experience. In October 2008, Qualcomm’s chipsets were attached to G1, the world’s first Android-based mobile phone made by HTC (High Tech Computer) corporation.

Qualcomm’s technology has since undergone further advancements. In 2009, it developed the world’s first multimode 3G/LTE (Long-Term Evolution) integrated chipset solution. In 2011, Qualcomm acquired Atheros, an industry leader in wireless and wired local area networking, leading Snapdragon to be able to offer a processing speed of 2.5 GHz and 150% higher performance with 65% lower battery consumption than any other ARM (Advanced RISC Machine) - based chipset [23]. AMR based chipset is a processor that is highly capable of execution with relatively low cost and power consumption. RISC processors are often used for small scale control devices such as mobile phones [24].

Qualcomm has continued to develop the newest technologies and products. In 2016, Qualcomm introduced Snapdragon 820 and introduced the octa-core version of Snapdragon 820. Its newest chipset is Snapdragon 855, which also includes an octa-core CPU (central processing unit).

4.2. Vision and Major Products

Qualcomm’s vision statement focuses on its innovation, promising customers that it will connect the users through its wireless technologies. To fulfill this vision and connect the world, Qualcomm offers numerous products, including processors, displays, software, and wireless charging devices. The company’s products are presented in Table 1.

4.3. Snapdragon

Among these products, Qualcomm has mainly focused especially on its processor after Snapdragon has developed [25]. Snapdragon is a mobile system on a chip (SoC) and is generally considered the next-step CPU chip. SoC refers to a computer or electronic system component integrated into a single integrated circuit. SoC combines major semiconductor devices such as CPU, memory devices (DRAM, flash), and DSP (Digital Signal Processing device) into a single chip so that chips themselves become one system [26]. The advantage of SoC is its small size. If the CPU, GPU, and memory functions are handled separately, it is difficult to produce a device smaller than 10 cm (4 inches) squared. However, with a single SoC, devices can be smaller while retaining the features of that larger device. Therefore, SoC enables the functions of computers on small devices such as smartphones and tablet PCs [27].

Snapdragon offers many functions, such as internet connection, a camera, location, display, multimedia, and sensor core. It improves CPU and GPU performance, enables faster downloads, and performs multitasking with lower battery consumption. Qualcomm thus offers technological superiority in this market by enabling extraordinary processing speed and longer battery duration.

Worldwide, Snapdragon has been adopted by many devices, such as smartphones, tablets, and wearable devices. Qualcomm has sold its chipsets to numerous global mobile manufacturers, such as Samsung, LG, HTC Corporation, Motorola, and Sony [28].

4.4. Fabless Model

Qualcomm’s success is widely attributed to its fabless production model (see Appendix A) [29], which means that it designs its chips but outsources its fabrication to other companies. Accordingly, Qualcomm has placed a strong emphasis on building strong and long-lasting relationships with its partners, including manufacturers and other external stakeholders. Such relationships have enabled Qualcomm to create devices that are faster and more versatile in order to meet the needs of its customers.

Due to the fabless model, Qualcomm also has a different value chain than many of its rivals. It has sets of value chain activities that work closely with its suppliers during the manufacturing process. Table 2 highlights the activities in Qualcomm’s fabless model.

5. SoC Industry

5.1. Types of SoC Business Models

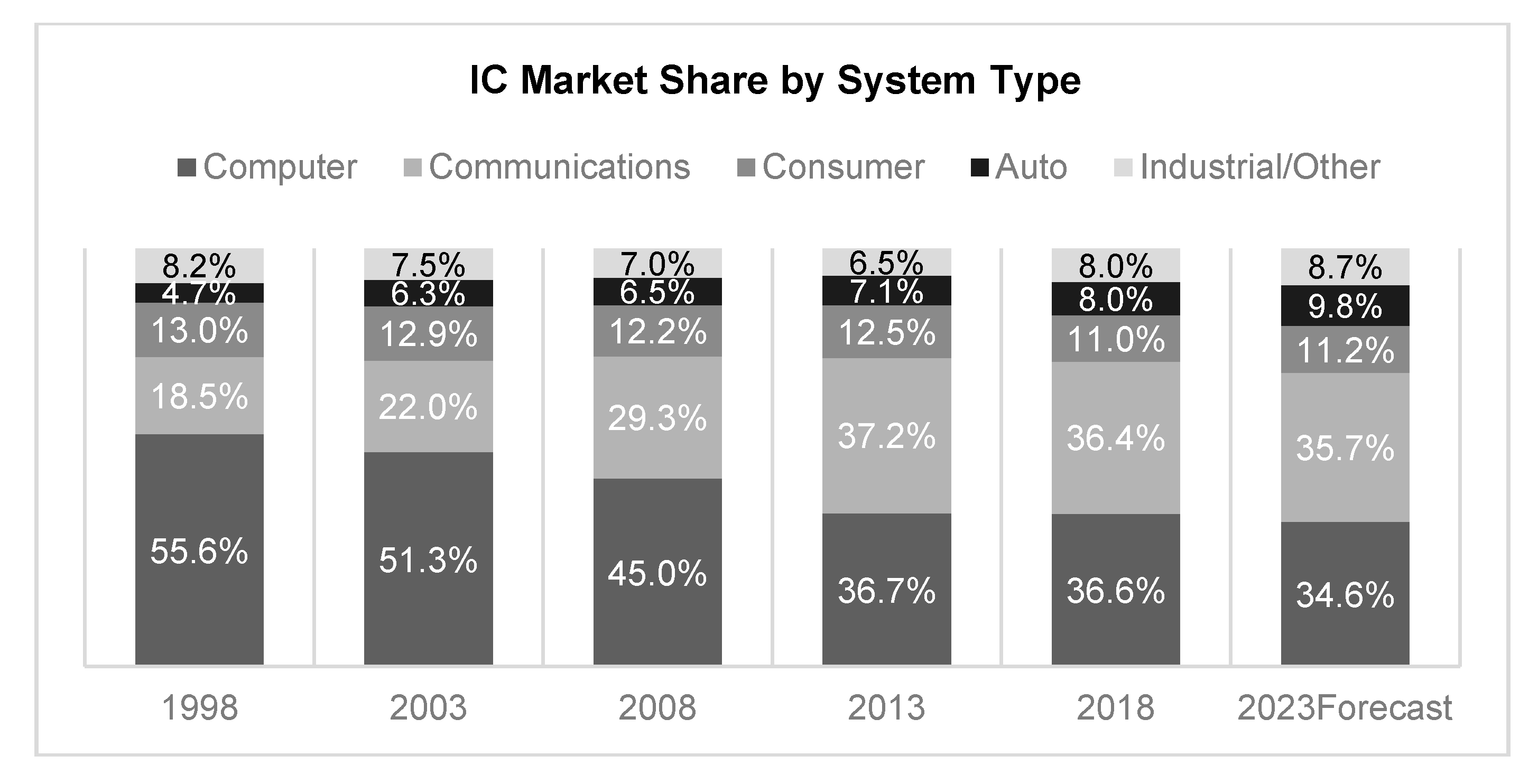

As described in Figure 1, the communication IC market appears to be the fastest-growing, and predicted to surpass computers by 2023. Therefore, this case analysis will focus on the smartphone SoC industry and companies.

There are three types of companies in SoC production. The first type includes fabless companies that only design SoC, such as Apple, Qualcomm, and MediaTek. The second type is foundry companies, which only fabricate semiconductors, such as TSMC and UMC. Finally, integrated device companies, such as Samsung and Hynix, perform all SoC processes, including design, manufacture, and selling.

Within the industry, these three types of companies interact with each other in diverse ways. For example, Apple and Qualcomm have partnerships with TSMC for fabrication. Samsung, which also produces end products, has purchased SoCs from Qualcomm because of their quality. Although Samsung and Apple are competitors, Apple has a strategic alliance with Samsung for chip fabrication and the supply of other components.

5.2. Market Situation

The demand for the SoC market is highly influenced by the demand for end products such as smartphones, tablets, and the internet of things (IoT) (According to Jacob Morgan (2014) in Forbes, the “IoT (Internet of Things) is the concept of basically connecting any device with an on and off switch to the Internet (and/or to each other). This includes everything from cellphones, coffee makers, washing machines, headphones, lamps, wearable devices, and almost anything else you can think of [31]). Within the SoC market, the telecommunication market has grown and become mature, and new segments, including the IoT, have emerged. Figure 1 presents the market share of SoC by system type, revealing that in 2018 the telecommunication sector’s market share was 36.4% [32,33].

The telecommunication sector’s high share of the SoC market has been led by the rapid growth of the smartphone market. The number of smartphones sold in 2009 was 170 million, a number that increased to 1.4 billion in 2015 [34]. Due to this rapid growth in demand, the SoC market for smartphones grew 61% in the first half of 2012 over the same period in 2011 [35].

With the help of the smartphone boom, Qualcomm has been the leader in the cellular chip market. In 2012, demand for smartphones rose in emerging markets such as China and India, and mobile technology was moving from 3G to LTE. Although late-mover companies had a chance to compete at the same level in the emerging market, Qualcomm managed to maintain its dominance by targeting high-end devices with the LTE model [35]. When Samsung launched its own cell phone SoC, Exynos, in 2011, its market share skyrocketed to position No. 2, with a 21% market share. Table 3 shows the market share of the leading companies after Samsung launched its mobile application processor for the year 2017 and 2018 [36].

Qualcomm, Samsung, and MediaTek have reaped the rewards from the growth of the mobile device market. In Q4, 2015, however, the growth rate of the smartphone market was only 9.7%, which was the first single-digit growth rate since 2008 [37]. To stimulate stalled market growth, smartphone producers have been expanding regional sales into the developing world, as they sell low- to mid-priced chips.

Although the growth rate of the smartphone market has stalled in recent years, the IoT is one of the sectors that can lead to growth in the SoC industry. It has been predicted that the demand for IoT products will increase much as the demand for smartphones did. A McKinsey 2014 report predicted that approximately 30 billion units of connected devices would be in the IoT market by 2020, which means a gradual increase of three billion per year from 2014 [38].

Moreover, the increasing demand for AI (artificial intelligence) is also expected to accelerate the growth of the semiconductor market. According to the IHS (Information Handling Service) markit, it has been estimated that AI-based SoC markets will double over the next five years due to rising demand for AI. According to a 2019 report, the global sales of the SoC industry will double every year by 2023 and that AI functions will be included in about half of SoC solutions [39].

The current SoC industry is worth about $90 billion, but less than 3 percent of these chips are compatible with AI. Artificial Intelligence will be needed for facial recognition, advanced driver-assisted systems in self-driving cars, and more powerful security features in smartphones and cameras, and that an AI embedded a new type of SoC will be required to make this possible. Therefore, it is expected that almost all major semiconductor manufacturers will introduce product lines that include artificial intelligence as a key function within a few years, increasing the SoC industry’s profits and playing an important role in AI’s innovation [39].

6. Factors in Qualcomm’s Success

6.1. R&D Investment in Advanced Technologies

We find that Qualcomm’s core competency lies within its expertise in wireless and related technologies. As shown in Table 1, Qualcomm’s product line is centered around processors such as Snapdragon and spread to other technologies such as wireless charging. Qualcomm has been the major pioneer in designing SoC by maintaining a heavy investment in research and development.

Qualcomm’s technologies are based on several attributes, the first of which is integration. Because Qualcomm can combine many functions within just one chip, it has gained a first-mover advantage in the mobile SoC market. For example, Qualcomm succeeded in developing Snapdragon in November 2007 [40], while it took Samsung 3 more years to invent SoC internally, introducing its own SoC in 2010 [41].

The second attribute is high performance. Versions of Qualcomm’s Snapdragon were the first chipsets to surpass both the 1 GHz and the 2 GHz barrier among smartphone processors [42].

The last attribute is energy efficiency. Although overload problems can lead to energy inefficiency a small chipset produces high performance, Qualcomm’s Snapdragon can produce 150% higher performance with a 2.5 GHz speed and 65% lower battery consumption than competing processors [42].

These advanced technologies result from Qualcomm’s research and development. Although competitors like Samsung and MediaTek are attempting to challenge Qualcomm with new products, Qualcomm has been able to continue to lead the development and commercialization of digital technologies through its intense dedication to R&D.

The company’s R&D intensity increased from 22% in 2016 to 25% in 2018. Table 4 shows that Apple has devoted more money to R&D but that Qualcomm has invested a much higher percentage of its profits into R&D than all of other firms and considerably more total expenditures than those creating chips for Android phones.

In addition, providing advanced technology has been crucial for Qualcomm in terms of profit. Qualcomm has two main sources of income: QCT (Qualcomm CDMA Technologies) and QTL (Qualcomm Technology Licensing). QCT is the division through which the products of its core business are sold. As seen in Table 5, QCT brought approximately 76% of Qualcomm’s revenues and QTL approximately 23% in 2018. Through QTL, Qualcomm licenses the right to use a portion of Qualcomm’s intellectual property to other companies, for which it receives fees and royalties [29]. QTL not only manages patents on technologies developed by Qualcomm but also serves to defend its intellectual property rights by buying related technologies depending on market conditions. Its competitive strategy, in other words, involves not only developing advanced technologies and producing products but also about creating barriers to other companies through steady management of its intellectual property rights. Qualcomm was able to become the largest mobile AP company in the world by taking advantage of its unrivaled market power.

6.2. Technology Acquisitions

Qualcomm’s growth has come through technology acquisitions (M&As), through which Qualcomm had been able to broaden its technology trajectories and gain complementary knowledge and technology. Table 6 reports this M&A history since 2009, during which Qualcomm has acquired 40 other companies. As the table shows, Qualcomm frequently has secured its technology competitiveness by acquiring companies that expanded their capabilities and expertise. For example, in 2009, Qualcomm acquired the mobile graphics division of AMD, an American global semiconductor company, which provided them with new technology in the graphics area that enhanced their 2D and 3D architectures [43] and differentiated its SoC from that of its competitors [44]. Similarly, in early 2011, Qualcomm acquired Atheros Communications, which was famous for producing Wi-Fi chipsets [45], thereby retaining wireless connection technology while filling technological holes in its 3G-only product portfolio.

These acquisitions are evidence of Qualcomm’s competitively strategic approach to the market. When Qualcomm has recognized technological gaps in its own offerings that emerged because of the fast-changing industry, it has tried to understand what capabilities it lacked and needed to obtain. To fill those gaps, Qualcomm has continually incorporated new capabilities, such as 3D architectures and Wi-Fi, into its established products through its technological acquisitions. Once those technological capabilities have been rapidly and successfully integrated, they have been difficult for other competitors to imitate as quickly, providing Qualcomm a competitive advantage. In other words, Qualcomm has consistently been a step ahead of its competitors, making it difficult for competitors to catch up as Qualcomm continues to strengthen its technology competitiveness [46].

7. Qualcomm’s Coopetition with Samsung

Qualcomm’s major competitors can be narrowed down to companies that are major players in the mobile device market: Apple, Samsung, MediaTek, Xiaomi, and Huawei. Within this market, there is considerable competition between mobile operating systems (OS). As the smartphone market has grown, the OS market has consolidated into two operation systems: iOS by Apple and Android by Google. Apple optimizes the SoC design for its operating system, iOS, so that its devices run smoothly. Other than Apple and Xiaomi; however, most companies have chosen Android as their operating system, which in 2019 had approximately 77% of the market share [47]. Accordingly, chips produced by companies such as Qualcomm, Samsung, and MediaTek are used mainly by devices based on the Android operating system.

Among these competitors, Qualcomm has been in a long-term relationship with Samsung since 1993, when Qualcomm provided CDMA technology to South Korea. Since then, Samsung has both paid royalties to Qualcomm for use of its telecommunication technology in its phones and provided consignment production of Qualcomm’s semiconductor, which has strengthened Qualcomm’s leadership in the SoC market. As Samsung’s own technology for telecommunication semiconductors has developed to the extent that it threatens Qualcomm; however, Qualcomm has been placed in a situation where, ironically, it has to coopete with Samsung to keep them as a customer. There exists a symbiotic relationship between the two within the SoC industry; therefore, Samsung is both one of Qualcomm’s most important customers and one of its closest competitors. Figure 2 shows the coopetition relationship between Qualcomm and Samsung. As a fabless firm, Qualcomm orders the production of semiconductor design from, and Samsung buys Qualcomm’s mobile AP and pays royalties for using Snapdragon. Samsung and Qualcomm, thus are competing to create a mobile AP while working together to provide Qualcomm with the production of semiconductors.

Samsung, unlike Qualcomm, performs both design and fabrication and produces its own SoC line, named the Exynos series. Samsung has demonstrated a fast-paced learning capability in developing SoC fabrication and design since it first obtained licenses for proprietary technology from Micron of the United States and Sharp of Japan [48,49]. After acquiring licenses from ARM, which offers the core architecture of micro-processors, Samsung was able to enter the SoC design business as well, developing Exynos 3 Single, which was inserted into the Samsung Galaxy S in 2010 [42]. Samsung has managed to build its internal production capabilities in a mere five years. Although the company performed closed innovation in developing its hardware, it deployed an open strategy platform for developing the smartphone apps, which enabled multiple players to enter the market freely and share their creations [50]. The smartphones produced by Samsung, named Galaxy, have captured a huge share of the Android market, which also represents a large portion of Qualcomm’s income. In the past, Samsung had been Qualcomm’s key customer because it used Snapdragon for its smartphones. Given that Qualcomm usually receives 2.5% to 5% of the sale price as its patent royalty for using its chips, Samsung paid Qualcomm more than $9.2 billion during the first four years after Samsung released its Galaxy S series [51]. Because Samsung currently utilizes its own technologies for both fabrication and design, however, the amount of royalties it has to pay to Qualcomm has decreased considerably.

Furthermore, Samsung encroached on Qualcomm’s competitive advantage on September 4, 2019, when it introduced Exynos 980, a 5 G mobile processor that combines a 5 G telecommunication modem chip with high-performance Mobile AP. According to Samsung, it also aims to become the global No. 1 player in the non-memory semiconductor sector by 2030 and is speeding up its efforts to chase Qualcomm, which is the top player in the market. The semiconductors that used to be equipped with modem chips separately will evolve into integrated chips. It is estimated that the market for 5 G chips will grow rapidly, from $161 million in 2019 to $3.03 billion in 2021 and $7.96 billion in 2023. In 2019, Samsung’s market share will be 7.5%, compared to Qualcomm’s 87.9%. Although Samsung’s current market share is far below Qualcomm’s, it is predicted that it will soon catch up with Qualcomm’s by 2023, increasing to 20.4% [52].

While the competition in the SoC market has intensified, Qualcomm has been daunted by the deterioration of its reputation starting in March 2015 due to the overheating issue with Snapdragon 810, which is designed by Qualcomm and manufactured by TSMC (Taiwan Semiconductor Manufacturing Company). The issue started with LG’s G Flex 2, equipped with Snapdragon 810, which was released in February 2015. ONE M9 from HTC and Xperia Z+ from Sony also suffered overheating of their mobile devices. Some benchmark tests showed that HTC ONE M9 was 10 °C to 15 °C hotter than other phones [53].

Samsung was a major customer of Qualcomm that used Snapdragon chips; however, after the overheating of Snapdragon 810, Samsung decided to use their own SoC chip, Exynos 7420, for its follow-up models, Galaxy S6 and Note 5. This decision could be interpreted as Samsung becoming not only Qualcomm’s customer but also a competitor that produce SoC chip which is equivalent to Qualcomm’s.

Although Qualcomm has not admitted to any problems in its chipset, these incidents led to poor market response, resulting in low financial performance. Although Qualcomm had expected to generate up to $28.8 billion in revenues in 2015, which would have represented a 9% revenue growth, its revenue actually fell by 5%, to $25.3 billion, after Samsung, its second-largest customer, decided not to use Snapdragon 810 for its follow-up model [54].

The overheating scandal led to a change in the relationship between Qualcomm and Samsung. As a result, revealing that Samsung has caught up with Qualcomm’s chip design capabilities.

Samsung holds a distinctive position, as it was a former customer that comprised the largest portion of Qualcomm’s revenue. Samsung dual-sourced Qualcomm’s Snapdragon and its Exynos into Galaxy S3, S4, S5, and Notes, which presumably served as a benchmark experiment for its own SoC. Although Samsung used Exynos in its smartphones, Samsung has not arisen as a direct competitor to Qualcomm. The brand power of Snapdragon surpasses that of Exynos, and Qualcomm’s revenue increased as the sales of smartphones increased. After the overheating issue, however, Samsung dropped the use of Snapdragon for the Galaxy S6, which makes it evident that Samsung has cultivated chip design as well as chip design capabilities.

Qualcomm has given Samsung an opportunity to learn the technologies of its next-generation chipset, enabling Samsung to absorb Qualcomm’s design capabilities. Based on the acquired technology of Qualcomm, Samsung can enhance the competitiveness of its SoC.

In the meantime, Samsung aggressively tested Snapdragon 820 to decide whether Samsung would turn to dual-sourcing for the next flagship smartphone, the Galaxy S7 [55]. In February 2016, Samsung released the Galaxy S7 with two chipsets versions: Snapdragon 820 and Exynos 8890.

The production of two chipsets shows that Qualcomm has to coopete with Samsung even though Samsung has to rely on Snapdragon. Exynos has been produced primarily for the internal use of Samsung business groups. However, Samsung revealed its intention to sell chipsets to external customers such as Meizu and Lenovo in 2016 [56]. Selling Exynos to other external companies suggests that Samsung is confident enough to become a direct competitor of Qualcomm as a general chipset provider in the SoC market.

It is possible that Samsung has received a key opportunity to be constantly up-to-date with Qualcomm’s internal developments by both buying Snapdragon and winning a contract for the fabrication of Snapdragon. Samsung can track Qualcomm’s moves and match the leader, producing comparable products. Moreover, Samsung has fabrication facilities that enable them to reap economies of scale [57]. In 2019, Qualcomm has decided to entrust Samsung’s foundry division to mass-produce its next-generation semiconductor called ‘Snapdragon 865’. This product will be used for 5G mobile telecommunication smartphones [58].

Samsung has developed ‘Exynos 980’, which is an integrated 5 G modem chip. Most of 5 G smartphones that have been released in markets until now are equipped with separate telecommunication semiconductors and processors, their power efficiency and performance are somewhat lower and they take up a lot of internal space of smartphones. Therefore, technologies that incorporate 5 G telecommunication semiconductor as an integral part of a processor have been considered the most important challenges for companies that develop mobile processors such as Qualcomm, Huawei, and MediaTek. After Samsung succeeded in commercializing 5 G telecommunication semiconductors that it developed with its own technologies last year, it has been working hard to secure technologies by making official plans for the development of integrated semiconductors that combine them with processors. Samsung has been using most of its own ‘Exynos’ series processors for Galaxy smartphones and has seen little success in expanding its suppliers to other smartphone manufacturers. This is because its top competitors, such as Qualcomm and China’s MediaTek, were maintaining a strong grip on the global market. However, it is likely that Exynos 980 will become the world’s first commercialized 5 G integrated semiconductor, which could provide an opportunity for Samsung to clearly show its superiority in technology to global customers and semiconductor industries [59].

Qualcomm has the ability to design SoC chips. It also still has a competitive edge in the mobile AP market, and its design capabilities will keep it competitive. Samsung, on the other hand, can design SoC chips and has the ability to manufacture them. Qualcomm faces the overheating issue of their chip, Snapdragon 820, and challenges from the competitors. To get out of this unfavorable situation in which Qualcomm faces, the firm has to keep up the coopetition with competitors. At present, Qualcomm still coopete with competitors, as in the case of Apple’s decision to receive 5 G modem chips from Qualcomm. Apple decided to yield in the patent war with Qualcomm. Qualcomm is still maintaining its top position in the semiconductor market. With the advent of the 5 G semiconductor era, Qualcomm’s market dominance persists, and Qualcomm’s share stood at 87.9 percent as of 2019 [52]. Qualcomm still has Samsung as its customer, even though Samsung has emerged as a competitor. These respective strategic differences show that while Qualcomm continues to coexist with Samsung, the relationship of global cooperation entails inherent risks. Since Qualcomm is Samsung’s largest supplier of components, the two companies are basically collaborative in that they maintain a cooperative relationship in the mobile AP market. But at the same time, Samsung is inevitably competing with Qualcomm by having the ability to produce mobile APs in-house. As a result, a global firm does not span only one industry but changes into a complex structure. In the midst of this process, a firm develops into having complex roles, such as being a competitor and a customer. Figure 3 summarizes the history of coopetition process of both firms.

8. Discussion

This study analyzed the growth process of Qualcomm with the framework of coopetition. From the case of Qualcomm, the study discovered that the growth of the SoC market and its dynamic competition is a long-term phenomenon. Qualcomm first developed CDMA technology and became the industry standard. The company seemed to succeed in retaining its first place. However, the competition is not a one-on-one rivalry, it is intertwined and dynamic. In the early days, Qualcomm led the market, but with the growth of the market, a rivalry began to emerge. While analyzing, the study offered one of competitive dynamic behavior reference, coopetition.

Qualcomm still holds the lead in the market, but the chase against latecomer Samsung continues, which marks Qualcomm’s strategic shift. In spite of increased competition, Qualcomm can be seen as collaborating with Samsung. From the case, Qualcomm provides Samsung a mobile AP chip; Snapdragon resulted from their cooperative relationship. Then, their relationship became competitive since Samsung threatened Qualcomm with its own SoC chip Exynos series. This implies that firms might evolve through cooperation and competition with competitors [60].

This case study provides an actual example of how firms are engaging in coopetition process. This study suggests that it is difficult for a firm to succeed in a competitive industry solely by competition and that it could only survive through coopetition. This study focused on the development of coopetition between firms as they simultaneously compete and cooperate. The case of Qualcomm shows that competitive actions and reactions among firms are critical to the change and evolution of coopetitive process. In terms of our case analysis, the competitive activities of firms lead to competitive reactions or cooperation with competitors. The competitive and cooperative relationship among firms depend on how other firms interpret and perceive other firm’s competitive activities.

In the global business environment, firms face conflicting issues and problems of competition, such as whether they should compete or cooperate. From the competition perspective, firms compete with each other, and it is a battle between firms. In a cooperative perspective, it is about pursuing growth through collaboration with firms in the same industry or a business sector. Competitive dynamic offers that these two perspectives do not conflict with each other or occur exclusively in reality, but coexist at the same time. The coopetition behavior of firms is necessary should a technical firm to succeed in the global market.

In terms of managerial implications for firms in the technological industry or other sectors, it is time-consuming and costly to firms that only compete with rivals. The continuation of coopetition has the effect of bringing together the complementary resources that each company has and widens the market through integrated technology. It has been shown that coopetition improves product competitiveness [60]. There also exists the risk of opportunistic behavior of other parties. The partnerships with competing firms could lead to the leakage of important corporate resources, as in the case of Qualcomm. Qualcomm offered industry-standard technology and cooperated with competitors. During those process, rivals gradually developed their technology and have attained Qualcomm’s technological level.

Managers could use this study as the representative type of behaviors of coopetition and establish innovation strategies based on it and can play an important role in determining industrial strategies through a comprehensive understanding of the ecosystem surrounding the SoC industry in the future. In addition, this study could be applied as a method for analyzing the firm’s strategy for reliable strategic choices and diagnose the coopetition process required for determining technical management and strategy. It would be possible for firms pursuing coopetition to identify the characteristics of promising technologies and technologies that should be intensively fostered through future corporate management and environmental assessments.

In the context of coopetition, during the process of growth of SoC industry, simultaneous cooperation and competition may have a positive impact on the industry as it stimulates open innovation, but there may be negative consequences for a firm [19]. Firm’s coopetition behavior offers positive innovation outcomes [6,61], although the coopeting partner could become a threat at the same time as in the case of Qualcomm. From the coopetitive relationship, firms could learn from each other, which accelerates knowledge creation that could benefit both firms. Although coopetition affects positively innovation performance of firms, it affects negatively firm’s innovation. For instance, Qualcomm entrusted Samsung to produce mobile AP chip. However, Samsung made their own mobile chip that could threaten Qualcomm. This shows that cooperative partner may turn into a competitor and threaten the other firm. The opportunistic behavior of partner firm cannot be controlled. This implies that the inherent paradox of coopetitive relationship exists among firms. Firms interact within paradoxical continuum, that is, they pursue collaborative interests while possessing opportunistic interests at the same time [8]. Qualcomm was in partnership with Samsung, but it could not prevent Samsung from developing its own chips.

While current literature offers view of the positive and negative sides of competitive dynamics, this study has showed coopetition behavior of a firm from practical case study. This paper has identified the competitive dynamic behaviors between technological firms and industry. Behind the competition, cooperation coexists, and while maintaining the tension, firms must constantly detect the potential for the competition to shift to cooperation and vice versa at any time. To this end, through case analysis, the two firms were the supplier and the customer from the perspective of cooperation, and the competition process of the two firms could be summarized from the perspective of the competition. In the coopetition, firms are dependent on each other to achieve their respective goals. Rather than focusing on one side of cooperation or competition, they represent structures that maintain cooperative relationships with rival companies in certain areas and compete with each other in other areas.

The starting point of a firm’s basic management strategies should be centered on the coopetition, and their strategic balance should be adjusted, in line with the changing business environment, sometimes by placing their strategic emphasis to the direction of competition and in the direction of cooperation. Although this study has focused on a particular firm’s behavior with a descriptive case study, the findings could be applied to other coopetition behaviors.

In conclusion, this study specifically derived the pattern of competition and cooperation among firms from a competitive dynamic perspective by further demonstrating the process of real-world coopetition case, which is the concept of simultaneous coexistence of competition and cooperation [2]. The contributions of this study are as follows. First, this study identified the process of strategic change from competition to coopetition of a particular firm through case analysis in the actual management environment. This study showed the process of forming a coopetition of entities within the SoC industry and how the entity behaves in the process. During those process, it can be concluded that firms have a coopetitive relationship by establishing supplier-customer relationships and at the same time being competitors. Second, the analysis of this coopetition process has supplemented existing studies to demonstrate the corporate trends surrounding the coopetition process. Firms are pursuing coopetition in order to create their competitiveness and to retain their value [5]. Specifically, in this study the coopetition process and strategic actions were captured in the SoC industry by demonstrating that firms are coopeting. This study depicted the dynamic aspects of interaction between firms by identifying the process of coopetition from real-life cases. By applying the competitive dynamic perspectives on this study and related methodologies from the real-world management, we can present the direction of a firm’s management strategy that considers competition and cooperation concurrently. It is valuable as a differentiated study using the latest trends from a more holistic and macroscopic perspective of actual firms’ management strategies, by focusing on information that takes into account the strategic behaviors of firms and the changing process of partners becoming competitors over time. Third, in addition to existing studies, this study apprehends the specific behaviors of cooperation and competition among firms through a case study that focused on specific coopetitive behavior. The strategic behavior of firms’ cooperation and competition-related technology management was described in detail and patterns were analyzed between them. It is also differentiated from existing research in that it captures the dynamic context of global firms’ cooperation and competitive activities in the SoC industry and identifies future direction from the perspective of coopetition. This study has not only provided examples of the coopetitive behaviors involved in the coopetition of the firms, but has also been able to show how the future behaviors would occur among global firms in a more coopetitive way.

For future research, it needs to broaden the time range of analysis to conduct research. For instance, the case of this study is descriptive rather than developing new theoretical constructs. It would be interesting for future studies to develop dynamic process of coopetition by introducing new constructs with the use of case studies. Furthermore, this study conducted a case analysis of the coopetition process of firms without quantitative analysis. For future studies, it is necessary to be reinforced with more in-depth quantitative studies that could broaden the scope of coopetition to enhance the feasibility of the analysis.

Author Contributions

Y.K., original draft preparation, review and editing, data curation, visualization; D.K., S.K., original draft preparation; S.C., supervision, corresponding author. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgments

In this section you can acknowledge any support given which is not covered by the author contribution or funding sections. This may include administrative and technical support, or donations in kind (e.g., materials used for experiments).

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Figure A1.

Business Model of Qualcomm. Source: 2009 Annual Report of Qualcomm.

References

- Tani, M.; Papaluca, O.; Sasso, P. The system thinking perspective in the open-innovation research: A systematic review. J. Open Innov. Technol. Mark. Complex. 2016, 4, 38. [Google Scholar] [CrossRef] [Green Version]

- Nalebuff, B.J.; Brandenburger, A.; Maulana, A. Co-Opetition; Harper Collins Business: London, UK, 1996. [Google Scholar]

- Afuah, A. How much do your co-opetitors’ capabilities matter in the face of technological change? Strateg. Manag. J. 2000, 21, 397–404. [Google Scholar] [CrossRef]

- Bonel, E.; Rocco, E. Coopeting to survive; surviving coopetition. Int. Stud. Manag. Organ. 2007, 37, 70–96. [Google Scholar] [CrossRef]

- Chou, H.H.; Zolkiewski, J. Coopetition and value creation and appropriation: The role of interdependencies, tensions and harmony. Ind. Mark. Manag. 2018, 70, 25–33. [Google Scholar] [CrossRef]

- Park, B.J.; Srivastava, M.K.; Gnyawali, D.R. Impact of coopetition in the alliance portfolio and coopetition experience on firm innovation. Technol. Anal. Strateg. Manag. 2014, 26, 893–907. [Google Scholar] [CrossRef]

- Yami, S.; Nemeh, A. Organizing coopetition for innovation: The case of wireless telecommunication sector in Europe. Ind. Mark. Manag. 2014, 43, 250–260. [Google Scholar] [CrossRef]

- Bengtsson, M.; Raza-Ullah, T.; Vanyushyn, V. The coopetition paradox and tension: The moderating role of coopetition capability. Ind. Mark. Manag. 2016, 53, 19–30. [Google Scholar] [CrossRef]

- Ketchen, D.J., Jr.; Snow, C.C.; Hoover, V.L. Research on competitive dynamics: Recent accomplishments and future challenges. J. Manag. 2004, 30, 779–804. [Google Scholar] [CrossRef]

- Chen, M.J.; Miller, D. Competitive dynamics: Themes, trends, and a prospective research platform. Acad. Manag. Ann. 2012, 6, 135–210. [Google Scholar] [CrossRef]

- Chen, M.J.; Miller, D. Competitive attack, retaliation and performance: An expectancy-valence framework. Strateg. Manag. J. 1994, 15, 85–102. [Google Scholar] [CrossRef]

- Silverman, B.S.; Baum, J.A. Alliance-based competitive dynamics. Acad. Manag. J. 2002, 45, 791–806. [Google Scholar]

- Nair, A.; Selover, D.D. A study of competitive dynamics. J. Bus. Res. 2012, 65, 355–361. [Google Scholar] [CrossRef]

- Luo, X.; Rindfleisch, A.; Tse, D.K. Working with rivals: The impact of competitor alliances on financial performance. J. Mark. Res. 2007, 44, 73–83. [Google Scholar] [CrossRef]

- Della Corte, V. Innovation through Coopetition: Future Directions and New Challenges. J. Open Innov. Technol. Mark. Complex. 2018, 4, 47. [Google Scholar] [CrossRef] [Green Version]

- Bengtsson, M.; Eriksson, J.; Wincent, J. Co-opetition dynamics–an outline for further inquiry. Compet. Rev. 2010, 20, 194–214. [Google Scholar] [CrossRef]

- Luo, Y. A coopetition perspective of global competition. J. World Bus. 2007, 42, 129–144. [Google Scholar] [CrossRef]

- Lado, A.A.; Boyd, N.G.; Hanlon, S.C. Competition, cooperation, and the search for economic rents: A syncretic model. Acad. Manag. Rev. 1997, 22, 110–141. [Google Scholar] [CrossRef]

- Bengtsson, M.; Kock, S. Cooperation and competition in relationships between competitors in business networks. J. Bus. Ind. Mark. 1999, 14, 178–194. [Google Scholar] [CrossRef]

- Levinthal, D.A.; March, J.G. The myopia of learning. Strateg. Manag. J. 1993, 14, 95–112. [Google Scholar] [CrossRef]

- Eisenhardt, K.M. Building theories from case study research. Acad. Manag. Rev. 1989, 14, 532–550. [Google Scholar] [CrossRef]

- Baxter, P.; Jack, S. Qualitative case study methodology: Study design and implementation for novice researchers. Qual. Rep. 2008, 13, 544–559. [Google Scholar]

- Qualcomm Announces Strategic Realignment Plan. Available online: https://www.qualcomm.com/news/releases/2015/07/22/qualcomm-announces-strategic-realignment-plan (accessed on 15 December 2015).

- Telecommunication Technology Association. Available online: http://www.tta.or.kr (accessed on 1 February 2020).

- Products. Available online: http://www.qualcomm.co.kr/products (accessed on 8 May 2015).

- Rouse, M. What is Full-Disk Encryption (FDE)?—Definition from WhatIs.Com. Available online: http://whatis.techtarget.com/definition/full-disk-encryption-FDE (accessed on 4 May 2016).

- Anthony, S. SoC vs. CPU—The Battle for the Future of Computing. Available online: http://www.extremetech.com/computing/126235-soc-vs-cpu-the-battle-for-the-future-of-computing (accessed on 4 May 2016).

- Products. Available online: https://www.qualcomm.com/snapdragon (accessed on 1 September 2019).

- 2009 Annual Report of Qualcomm. Available online: http://files.shareholder.com/downloads/QCOM/1725443717x0x349566/6D97C862-1FFD-42F1-AA36-FC416BC242BB/qualcomm_corporate_overview_09.pdf (accessed on 12 June 2016).

- Clarke, P. Qualcomm Joins IMEC Core CMOS R&D Program. Available online: http://www.eetimes.com/document.asp?doc_id=1263017 (accessed on 12 June 2016).

- Morgan, J. A Simple Explanation of ‘The Internet of Things’. Available online: https://www.forbes.com/sites/jacobmorgan/2014/05/13/simple-explanation-internet-things-that-anyone-can-understand/#2903760e1d09 (accessed on 2 June 2016).

- Communications IC Market to Again Surpass Computer IC Market. Available online: https://anysilicon.com/communications-ic-market-to-again-surpass-computer-ic-market/ (accessed on 31 August 2019).

- IC Insights. Available online: http://www.icinsights.com/news/bulletins/Communications-IC-Market-To-Again-Surpass-Computer-IC-Market/ (accessed on 2 September 2019).

- Statista. Global Smartphone Sales to End Users from 1st Quarter 2009 to 4th Quarter 2015, by Operating System (in Million Units). Available online: http://0-www-statista-com.brum.beds.ac.uk/statistics/266219/global-smartphone-sales-since-1st-quarter-2009-by-operating-system (accessed on 4 May 2016).

- Qualcomm Still Dominates the App Processor Market but EM Peers are Creeping. Available online: http://www.forbes.com/sites/greatspeculations/2012/10/19/qualcomm-still-dominates-the-app-processor-market-but-em-peers-are-creeping/#25c53c3372e3 (accessed on 5 May 2016).

- Kim, G.; Lee, S. Available online: https://www.mk.co.kr/news/business/view/2019/01/63865/ (accessed on 12 September 2019).

- Singh, S. Worldwide Smartphone Sales Grew 9.7% in Q4 2015; Iphone Declines: Gartner. Available online: http://timesofindia.indiatimes.com/tech/tech-news/Worldwide-smartphone-sales-grew-9-7-in-Q4-2015-iPhone-declines-Gartner/articleshow/51043074.cms (accessed on 4 May 2016).

- McKinsey. The Internet of Things: Sizing Up the Opportunity. Available online: http://www.mckinsey.com/industries/high-tech/our-insights/the-internet-of-things-sizing-up-the-opportunity (accessed on 4 May 2016).

- Kwon, G.Y. Available online: http://news1.kr/articles/?3642857 (accessed on 12 June 2019).

- Qualcomm Incorporated—Annual Report. Available online: http://investor.qualcomm.com/secfiling.cfm?filingID=1234452-14-320&CIK=804328#QCOM10-K2014_HTM_S51508F49E447D4D6F80EC8ED838E698A (accessed on 15 May 2015).

- Experience the Amazing Exynos by Visiting Samsung Exynos Website. Available online: http://www.samsung.com/semiconductor/minisite/Exynos/w/mediacenter.html#?v=blog_History_of_Exynos_Processors (accessed on 4 May 2016).

- 2015 Annual Report of Qualcomm. Available online: http://investor.qualcomm.com/secfiling.cfm?filingID=1234452-14-320&CIK=804328qualcomm (accessed on 12 June 2016).

- Qualcomm Acquires Handheld Graphics and Multimedia Assets from AMD. Available online: https://www.qualcomm.com/news/releases/2009/01/20/qualcomm-acquires-handheld-graphics-and-multimedia-assets-amd (accessed on 14 June 2016).

- MK Economy. Available online: http://news.mk.co.kr/v2/economy/view.php?sc=50000001&cm=%C0%FC%C3%BC%20%B1%E2%BB%E7&year=2014&no=1304838&relatedcode=&wonNo (accessed on 13 May 2016).

- Press Release. Available online: https://www.qualcomm.com/news/releases/2011/05/24/qualcomm-completes-31-billion-acquisition-atheros-communications (accessed on 13 May 2016).

- Chaudhuri, S.; Tabrizi, B. Capturing the real value in high-tech acquisitions. Harv. Bus. Rev. 2009, 77, 123. Available online: https://hbr.org/1999/09/capturing-the-real-value-in-high-tech-acquisitions (accessed on 13 June 2016).

- Mobile Operating System Market Share Worldwide. Available online: https://gs.statcounter.com/os-market-share/mobile/worldwide (accessed on 4 September 2019).

- Jordan, S.; James, C. Samsung Electronics; Harvard Business School Publishing: Boston, MA, USA, 2006; HBS No. 9-705-508. [Google Scholar]

- Yu, T.F.L.; Yan, H.D. Handbook of East Asian Entrepreneurship; Routledge: Abingdon, UK, 2014; Available online: https://books.google.co.kr/books?id=VmKvBAAAQBAJ&pg=PA339&lpg=PA339&dq=samsung+license+sharp+of+japan&source=bl&ots=NpyFH9of9z&sig=qrR2Y0Qd7rzZrXuVelo5mLrc2ck&hl=en&sa=X&ved=0ahUKEwiH45v7zaLNAhViGqYKHTL9DDYQ6AEIJjAC#v=onepage&q=technology%20licensing%20from%20California-%20based%20Zytrex%20and%20Japan%27s%20Sharp.&f=false (accessed on 6 May 2016).

- Yun, J.; Jeon, J.; Park, K.; Zhao, X. Benefits and costs of closed innovation strategy: Analysis of Samsung’s Galaxy Note 7 Explosion and withdrawal scandal. J. Open Innov. Technol. Mark. Complex. 2018, 4, 20. [Google Scholar] [CrossRef] [Green Version]

- Lucic, K. Exynos-Powered Galaxy S6 Flagships Equal Significantly Less Patent Cash for Qualcomm. Available online: http://www.androidheadlines.com/2015/04/exynos-7420-powered-galaxy-s6-flagships-equal-significantly-less-patent-cash-qualcomm.html (accessed on 4 May 2016).

- Chang, W.J. Available online: https://n.news.naver.com/article/366/0000442376 (accessed on 4 September 2019).

- Wilson, M. HTC One M9 Benchmark Shows Snapdragon 810 Overheating. Available online: http://www.kitguru.net/laptops/mobile/matthew-wilson/htc-one-m9-benchmark-shows-snapdragon-810-overheating/ (accessed on 15 December 2015).

- Sun, L. Qualcomm Inc. vs. Samsung: When a Partner Becomes a Rival. Available online: http://www.fool.com/investing/general/2015/11/16/qualcomm-inc-vs-samsung-when-a-partner-becomes-a-r.aspx (accessed on 15 December 2015).

- Qualcomm CDMA Technologies Takes Delivery of MSM6050 Chip, First Wireless Baseband IC from TSMC’s 300mm Wafer Fab Line. Available online: https://www.qualcomm.com/news/releases/2001/11/08/qualcomm-cdma-technologies-takes-delivery-msm6050-chip-first-wireless (accessed on 15 December 2015).

- Abrar. The Samsung Exynos 8870 Chipset for the External Clients. Available online: http://www.updategadgets.com/the-samsung-exynos-8870-chipset-for-the-external-clients/ (accessed on 4 May 2016).

- Ren, S. TSMC: Qualcomm is Coming Back, Jpmorgan Raises Target. Available online: http://blogs.barrons.com/asiastocks/2016/03/07/tsmc-qualcomm-is-coming-back-jpmorgan-raises-target/ (accessed on 30 May 2016).

- Kang, D.C. Available online: http://biz.chosun.com/site/data/html_dir/2019/06/11/2019061100030.html (accessed on 29 September 2019).

- Kim, Y.W. Available online: http://www.businesspost.co.kr/BP?command=article_view&num=142660 (accessed on 26 September 2019).

- Gnyawali, D.R.; Park, B.J.R. Co-opetition between giants: Collaboration with competitors for technological innovation. Res. Policy 2011, 40, 650–663. [Google Scholar] [CrossRef]

- Ritala, P.; Hurmelinna-Laukkanen, P. Incremental and radical innovation in coopetition—The role of absorptive capacity and appropriability. J. Prod. Innov. Manag. 2013, 30, 154–169. [Google Scholar] [CrossRef]

Figure 1.

IC (Integrated Chipset) market share by system type ($). Source: IC insights.

Figure 2.

Coopetitive relationship of Qualcomm and Samsung.

Figure 3.

The history of coopetition process of Qualcomm and Samsung.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

List of Qualcomm’s Products.

| Processors | Gobi, Hy-Fi, IPQ, Izat, Powerline, Snapdragon, Small Cells, VIVE, Wi-Fi Platforms |

| Displays | Mirasol, Pixtronix |

| Software | AllPlay, 2net, Brew, HealthyCircles, Qchat, Qlearn, RaptorQ, Vuforia |

| Wireless Charging | Halo, WiPower |

Source: Qualcomm Homepage.

Table 2.

Qualcomm’s Value Chain.

| Primary Activities | |

| Operations | Qualcomm collaborates closely with its manufacturers, having a say in every single feature and product, although it does not directly manufacture its products. |

| Supporting Activities | |

| Technology Development | Qualcomm invests considerable capital into the advancement of manufacturing technology. It also creates several strategic alliances with other global semiconductor research programs, such as the Complementary Metal-Oxide-Semiconductor (CMOS) Program by IMEC, a research institute for nanoelectronics, for the development of technologies regarding semiconductors and its related products [30]. |

| Procurement | Qualcomm heavily relies on third-party manufacturing for support. As such, it maintains good relationships with its suppliers, working well with them to ensure the continuous quality and reliability of its products. |

Source: Qualcomm Homepage.

Table 3.

Market share of mobile application processor in 2017 and 2018.

| Rank | Company | 2017 | 2018 |

|---|---|---|---|

| 1 | Qualcomm | 37.9% | 37% |

| 2 | MediaTek | 25.7% | 23.2% |

| 3 | Apple | 14% | 13.5% |

| 4 | Samsung | 8.2% | 11.7% |

| 5 | Spreadtrum Communications | 9.4% | 4.9% |

| 6 | Others | 4.8% | 9.7% |

| Total | 100% | 100% |

Table 4.

R&D (Research and Development) expenses and R&D intensity.

| 2016 R&D Exp($M) | 2016 R&D Intensity (R&D exp/Revenue) | 2017 R&D Exp($M) | 2017 R&D Intensity (R&D exp/Revenue) | 2018 R&D Exp($M) | 2018 R&D Intensity (R&D exp/Revenue) | |

|---|---|---|---|---|---|---|

| Qualcomm | 5151 | 22% | 5485 | 25% | 5625 | 25% |

| Samsung | 1240 | 7% | 1408 | 7% | 1563 | 7% |

| Apple | 10,045 | 5% | 11,581 | 5% | 14,236 | 5% |

| Broadcom | 2674 | 20% | 3292 | 19% | 3768 | 18% |

| MediaTek | 180 | 20% | 185 | 24% | 186 | 24% |

Source: Annual Report of Qualcomm, Samsung, Apple, Broadcom, MediaTek in 2016, 2017, and 2018.

Table 5.

Sources of Qualcomm’s Income (in millions, except percentage data).

| QCT | QTL | |

|---|---|---|

| 2016 | $15,409 | $7664 |

| As a percent of total | 65% | 33% |

| 2017 | $16,479 | $6445 |

| As a percent of total | 74% | 29% |

| 2018 | $17,282 | $5163 |

| As a percent of total | 76% | 23% |

Source: 2018 Annual report of Qualcomm.

Table 6.

Qualcomm’s M&A (Merger and Acquisition) History.

| Date | Company | Date | Company |

|---|---|---|---|

| 01/19/09 | AMD Inc-Handhale Graphics Asts | 11/25/13 | Roadnet Technologies Inc |

| 02/10/09 | Inside Secure SA | 01/10/14 | kooaba AG |

| 03/13/09 | Digital Fountain Inc | 06/01/14 | Healthvista India Private Ltd |

| 03/23/09 | Verreon Inc | 06/18/14 | Black Sand Technologies Inc |

| 05/20/09 | Higel Power LLC | 07/03/14 | Wilocity Ltd |

| 07/12/10 | Tapioca Mobile Inc | 07/30/14 | EmpoweredU |

| 10/13/10 | iSkoot Technologies Inc | 08/26/14 | Euclid Vision Technologies BV |

| 12/28/10 | Boundary Information Group | 09/15/14 | Euvision Technologies BV |

| 01/05/11 | Atheros Communications Inc | 10/15/14 | CSR PLC |

| 01/14/11 | FleetRisk Advisors LLC | 12/12/14 | Beijing Netriver Tech Co Ltd |

| 02/12/11 | Sylectus | 12/12/14 | Beijing Qixin Yiwei Info Tech |

| 08/31/11 | Bigfoot Networks Inc | 02/02/15 | Knel Robotics |

| 11/08/11 | HaloIPT Ltd | 06/12/15 | Nujira Ltd |

| 11/13/11 | Pixtronix Inc | 06/30/15 | Maxim Integrated Prod-Bus |

| 06/18/12 | Summit Microelectronics Inc | 08/06/15 | Ikanos Communications Inc |

| 08/22/12 | DesignArt Networks Ltd | 08/14/15 | Silanna Semiconductor USA Inc |

| 10/26/12 | TransCella Inc | 09/14/15 | Capsule Tech Inc |

| 11/16/12 | EPOS Dvlp-Cert Asts | 09/14/15 | Capsule Technologie SA |

| 05/06/13 | MyTeleHealth Solutions LLC | 03/02/17 | TDK Corporation |

| 10/31/13 | Arteris Inc-Certain Assets | 03/02/17 | RF360 Holdings. |

Source: Qualcomm homepage and annual reports.

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kwon, Y.; Kang, D.; Kim, S.; Choi, S. Coopetition in the SoC Industry: The Case of Qualcomm Incorporated. J. Open Innov. Technol. Mark. Complex. 2020, 6, 9. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc6010009

AMA Style

Kwon Y, Kang D, Kim S, Choi S. Coopetition in the SoC Industry: The Case of Qualcomm Incorporated. Journal of Open Innovation: Technology, Market, and Complexity. 2020; 6(1):9. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc6010009

Chicago/Turabian StyleKwon, Yona, Dahee Kang, Sinji Kim, and Seungho Choi. 2020. "Coopetition in the SoC Industry: The Case of Qualcomm Incorporated" Journal of Open Innovation: Technology, Market, and Complexity 6, no. 1: 9. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc6010009