Creative Accounting Determination and Financial Reporting Quality: The Integration of Transparency and Disclosure

,

,

Abstract

:1. Introduction

- What are the effects of creative accounting determinants on financial reporting quality in the banking sector?

- To what extent do transparency and disclosure moderate the relationship between creative accounting determinants and financial reporting quality?

2. Theoretical Background

2.1. Creative Accounting Determinants and Financial Reporting Quality

2.2. The Integration of Transparency and Disclosure

3. Research Method

3.1. Study Population

3.2. Sampling Technique

3.3. Data Collection Procedures

3.4. Response Rate

3.5. Measures

3.6. Analysis and Results

3.6.1. Normality

3.6.2. Assessment of Measurement Model

3.6.3. Assessment of Structural Equation Modeling

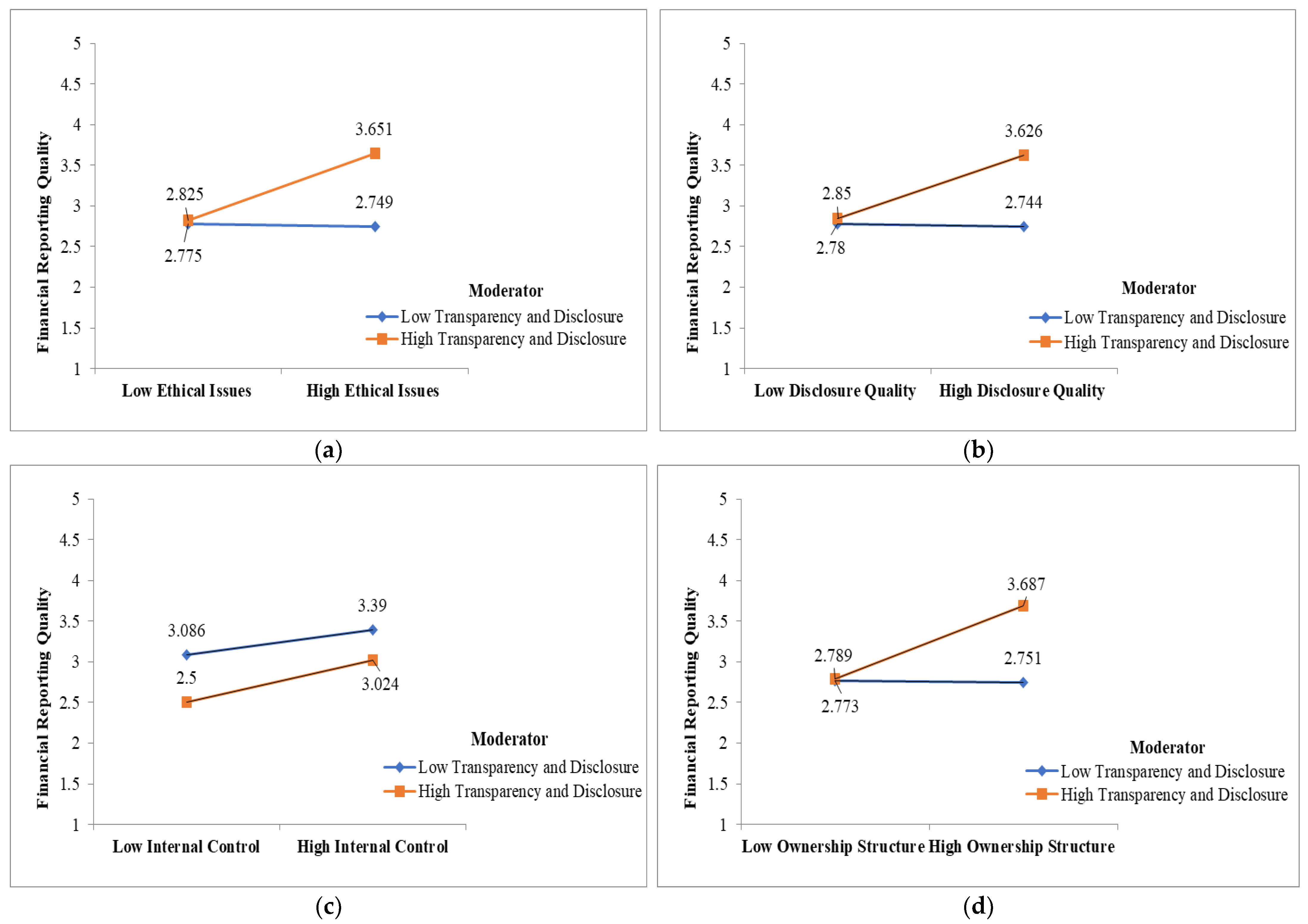

4. Discussion

5. Research Implications

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Measurement Items

| Transparency and Disclosure |

|

|

|

|

|

| Creative Accounting Determinants |

| Ethical Issues |

|

|

|

|

|

| Disclosure Quality |

|

|

|

|

|

| Internal Control |

|

|

|

|

|

| Ownership Structure |

|

|

|

|

|

| Financial Reporting Quality Dimensions |

| Relevance |

|

|

|

|

|

| Faithful Representation |

|

|

|

|

|

| Understandability |

|

|

|

|

|

| Comparability |

|

|

|

|

|

References

- Susmus, T.; Demirhan, D. Creative Accounting: A Brief History and Conceptual Framework. In Proceedings of the 3rd Balkans and Middle East Countries Conference on Accounting and Accounting History, Istanbul, Turkey, 19–22 June 2013. [Google Scholar]

- Idris, A.A.; Kehinde, J.S.; Ajemunigbohun, S.S.A.; Gabriel, J.M.O. The nature, techniques and prevention of creative accounting: Empirical evidence from Nigeria. Can. J. Account. Financ. 2012, 1, 26–31. [Google Scholar]

- Mulford, C.W.; Comiskey, E.E. Creative accounting and accounting scandals in the USA. Creat. Account. Fraud. Int. Account. Scandal. 2012, 407–424. [Google Scholar]

- Mutuc, E.B.; Lee, J.-S.; Tsai, F.-S.; Bimo, I.D.; Siregar, S.V.; Hermawan, A.A.; Wardhani, R.; Kewo, C.L.; Afiah, N.N.; Bardhan, I.; et al. Avoiding creative accounting: Corporate governance and leadership skills. SSRN Electron. J. 2019, 10, 221–246. [Google Scholar]

- Hameedi, K.S.; Al-Fatlawi, Q.A.; Ali, M.N.; Almagtome, A.H. Financial Performance Reporting, IFRS Implementation, and Accounting Information: Evidence from Iraqi Banking Sector. J. Asian Financ. Econ. Bus. 2021, 8, 1083–1094. [Google Scholar]

- Anam Ousama, A.; Fatima, A.H.; Salihin, A. An Islamic perspective on the true and fair view override principle. J. Islam. Account. Bus. Res. 2014, 5, 142–157. [Google Scholar] [CrossRef]

- Goel, S. The quality of reported numbers by the management: A case testing of earnings management of corporate India. J. Financ. Crime 2014, 21, 355–376. [Google Scholar] [CrossRef]

- Škoda, M.; Lengyelfalusy, T.; Gabrhelová, G. Creative Accounting Practicies in Slovakia after Passing Financial Crisis. Copernic. J. Financ. Account. 2017, 6, 71–86. [Google Scholar] [CrossRef]

- Ibrahim, S.S.H. The Impacts of Capital Structure on Bank Performance. Koya Univ. J. Humanit. Soc. Sci. 2019, 2, 118. [Google Scholar] [CrossRef] [Green Version]

- Alsalim, M.; Amin, H.; Youssef, A. The role of corporate governance in achieving accounting information quality (field study in the mishraq sulfur state co.). Stud. Sci. Res. Econ. Ed. 2018, 27, 2–24. [Google Scholar] [CrossRef] [Green Version]

- Uwuigbe, O.R.; Olorunshe, O.; Uwuigbe, U.; Ozordi, E.; Asiriuwa, O.; Asaolu, T.; Erin, O. Corporate Governance and Financial Statement Fraud among Listed Firms in Nigeria. In Proceedings of the IOP Conference Series: Earth and Environmental Science, Ota, Nigeria, 18–20 June 2019; Volume 331, p. 012055. [Google Scholar] [CrossRef]

- Cooray, T.; Gunarathne, A.D.N.; Senaratne, S. Does corporate governance affect the quality of integrated reporting? Sustainability 2020, 12, 4262. [Google Scholar] [CrossRef]

- Martin, R.; Yadiati, W.; Pratama, A.; Rubio-Misas, M.; Alshbili, I.; Elamer, A.A.; Beddewela, E.; Harun, M.S.; Hussainey, K.; Mohd Kharuddin, K.A.; et al. Doing Good with Creative Accounting? Linking Corporate Social Responsibility to Earnings Management in Market Economy, Country and Business Sector Contexts. Sustainability 2019, 8, 4568. [Google Scholar] [CrossRef]

- Brauweiler, H.-C.; Yerimpasheva, A.; Bagalbayeva, Z.; Lari Dashtbayaz, M.; Salehi, M.; Safdel, T.; Agyei-Mensah, B.K.; Salin, A.S.A.P.; Ismail, Z.; Smith, M.; et al. Avoiding creative accounting: Corporate governance and leadership skills. Zesz. Teor. Rachun. 2019, 12, 9–19. [Google Scholar] [CrossRef]

- Qian, W.; Hörisch, J.; Schaltegger, S.; Baalouch, F.; Ayadi, S.D.; Hussainey, K.; Agyei-Mensah, B.K.; Nagata, K.; Nguyen, P.; Daske, H.; et al. A study of the determinants of environmental disclosure quality: Evidence from French listed companies. J. Clean. Prod. 2015, 22, 1608–1619. [Google Scholar] [CrossRef] [Green Version]

- Makhaiel, N.K.B.; Sherer, M.L.J. The effect of political-economic reform on the quality of financial reporting in Egypt. J. Financ. Report. Account. 2018, 16, 245–270. [Google Scholar] [CrossRef]

- Esra, A.; Engin, D.; Atabay, E.; Dinç, E. Financial Information Manipulation and Its Effects on Investor Demands: The Case of BIST Bank. In Contemporary Issues in Audit Management and Forensic Accounting; Grima, S., Boztepe, E., Baldacchino, P.J., Eds.; Contemporary Studies in Economic and Financial Analysis; Emerald Publishing Limited: Bingley, UK, 2020; Volume 102, pp. 41–56. ISBN 978-1-83867-636-0. eISBN 978-1-83867-635-3. [Google Scholar]

- Akpanuko, E.E.; Umoren, N.J. The influence of creative accounting on the credibility of accounting reports. J. Financ. Report. Account. 2018, 16, 292–310. [Google Scholar] [CrossRef]

- Johl, S.K.; Kaur Johl, S.; Subramaniam, N.; Cooper, B. Internal audit function, board quality and financial reporting quality: Evidence from Malaysia. Manag. Audit. J. 2013, 28, 780–814. [Google Scholar] [CrossRef]

- Rozidi, M.; Nor, N.A.M.; Aziz, N.A.; Rosli, N.A.; Mohaiyadin, N.M.H. Relationship between Auditors’ Ethical Judgments, Quality of Financial Reporting and Auditors’ Attitude towards Creative Accounting: Malaysia Empirical Evidence. Int. J. Bus. Humanit. Technol. 2015, 5, 81–87. [Google Scholar]

- Abed, I.A.; Hussin, N.; Ali, M.A.; Nikkeh, N.S.; Mohammed, A. Creative Accounting Phenomenon in the Financial Reporting: A Systematic Review Classification, Challenges. Technol. Rep. Kansai Univ. 2020, 62, 1–10. [Google Scholar]

- Salome, E.N.; Ogbonna, M.I.; Marcel, E.C.; Echezonachi, O.E. The effect of creative accounting on the job performance of accountants (auditors) in reporting financial statementin Nigeria. Kuwait Chapter Arab. J. Bus. Manag. Rev. 2012, 33, 1–30. [Google Scholar]

- Kardan, B.; Salehi, M.; Abdollahi, R. The relationship between the outside financing and the quality of financial reporting: Evidence from Iran. J. Asia Bus. Stud. 2016, 10, 20–40. [Google Scholar] [CrossRef] [Green Version]

- Tri Wahyuni, E.; Puspitasari, G.; Puspitasari, E. Has IFRS improved Accounting Quality in Indonesia? A Systematic Literature Review of 2010–2016. J. Account. Invest. 2020, 21, 19–44. [Google Scholar] [CrossRef]

- Abed, I.A.; Hussin, N.; Ali, M.A.; Othman, R.; Mohammed, M.A. A Systematic Critical Review of Creative Accounting and Financial Reporting. Technol. Rep. Kansai Univ. 2020, 62, 5113–5130. [Google Scholar]

- Amat, O.; Gowthorpe, C. Creative Accounting: Nature, Incidence and Ethical Issues. 2004. Available online: https://ssrn.com/abstract=563364 (accessed on 12 July 2004).

- Engelseth, P.; Kritchanchai, D. Innovation in healthcare services-Creating a Combined Contingency Theory and Ecosystems Approach. In Proceedings of the IOP Conference Series: Materials Science and Engineering, Denpasar, Indonesia, 29–30 August 2017; Volume 337, p. 012022. [Google Scholar] [CrossRef]

- Remenarić, B.; Kenfelja, I.; Mijoč, I. Creative accounting-motives, techniques and possibilities of prevention. Ekon. Vjesn. 2018, 31, 193–199. [Google Scholar]

- Tassadaq, F.; Malik, Q.A. Creative accounting and financial reporting: Model development and empirical testing. Int. J. Econ. Financ. Issues 2015, 5, 544–551. [Google Scholar]

- Butala, A.; Khan, Z.U. Accounting Fraud at Xerox Corporation. SSRN Electron. J. 2011, 16, 81–89. [Google Scholar] [CrossRef]

- Cletus, A.; Oghoghomeh, T. Ethics of Accounting Profession in Nigeria. J. Bus. Econ. 2014, 5, 1374–1382. [Google Scholar]

- Yao, S.; Wang, Z.; Sun, M.; Liao, J.; Cheng, F. Top executives’ early-life experience and financial disclosure quality: Impact from the Great Chinese Famine. Account. Financ. 2020, 60, 4757–4793. [Google Scholar] [CrossRef]

- Gerwanski, J.; Kordsachia, O.; Velte, P. Determinants of materiality disclosure quality in integrated reporting: Empirical evidence from an international setting. Bus. Strategy Environ. 2019, 28, 750–770. [Google Scholar] [CrossRef]

- Song, D.B.; Lee, H.Y.; Cho, E.J. The association between earnings management and asset misappropriation. Manag. Audit. J. 2013, 28, 542–567. [Google Scholar] [CrossRef]

- Yasser, Q.R.; Al Mamun, A.; Ahmed, I. Quality of financial reporting in the Asia-Pacific region: The influence of ownership composition. Rev. Int. Bus. Strategy 2016, 26, 543–560. [Google Scholar] [CrossRef]

- Paolone, F.; Magazzino, C. Earnings manipulation among the main industrial sectors. evidence from Italy. Evid. Italy 2014, 253–261. [Google Scholar]

- Pakurár, M.; Haddad, H.; Popp, J.; Khan, T.; Oláh, J. Supply chain integration, organizational performance and balanced scorecard: An empirical study of the banking sector in Jordan. J. Int. Stud. 2019, 12, 129–146. [Google Scholar] [CrossRef]

- Ayagre, P.; Appiah-Gyamerah, I.; Nartey, J. The effectiveness of Internal Control Systems of banks. The case of Ghanaian banks. Int. J. Account. Financ. Report. 2014, 4, 377. [Google Scholar] [CrossRef]

- D’Mello, S.R.; Cruz, C.N.; Chen, M.-L.; Kapoor, M.; Lee, S.L.; Tyner, K.M. The evolving landscape of drug products containing nanomaterials in the United States. Nat. Nanotechnol. 2017, 12, 523–529. [Google Scholar] [CrossRef] [PubMed]

- Pakurár, M.; Haddad, H.; Nagy, J.; Popp, J.; Oláh, J. The impact of supply chain integration and internal control on financial performance in the Jordanian banking sector. Sustainability 2019, 11, 1248. [Google Scholar] [CrossRef] [Green Version]

- Foster, B.P.; Mcclain, G.; Shastri, T. The auditor’s report on internal control & fraud detection responsibility: A comparison of French and U.S. users’ perceptions. J. Account. Ethics Public Policy 2013, 14, 221–257. [Google Scholar]

- Bardhan, I.; Lin, S.; Wu, S.L. The quality of internal control over financial reporting in family firms. Account. Horiz. 2015, 29, 41–60. [Google Scholar] [CrossRef]

- Bimo, I.D.; Siregar, S.V.; Hermawan, A.A.; Wardhani, R. Internal control over financial reporting, organizational complexity, and financial reporting quality. Int. J. Econ. Manag. 2019, 13, 331–342. [Google Scholar]

- Abed, I.A.; Hussin, N.; Ali, M.A. Piloting the Role of Corporate Governance and Creative Accounting in Financial Reporting Quality. Technol. Rep. Kansai Univ. 2020, 62, 2–7. [Google Scholar]

- Nagata, K.; Nguyen, P. Ownership structure and disclosure quality: Evidence from management forecasts revisions in Japan. J. Account. Public Policy 2017, 36, 451–467. [Google Scholar] [CrossRef]

- Sahasranamam, S.; Arya, B.; Sud, M. Ownership structure and corporate social responsibility in an emerging market. Asia Pac. J. Manag. 2019, 37, 37–1192. [Google Scholar] [CrossRef] [Green Version]

- Haddad, H.; Alkhodari, D.; Al-Araj, R.; Aburumman, N.; Fraij, J. Review of the Corporate Governance and Its Effects on the Disruptive Technology Environment. Wseas Trans. Environ. Dev. 2021, 17, 1001–1020. [Google Scholar] [CrossRef]

- Alzoubi, E.S.S. Ownership structure and earnings management: Evidence from Portugal. Australas. Account. Bus. Financ. J. 2016, 24, 135–161. [Google Scholar] [CrossRef]

- Kao, M.-F.; Hodgkinson, L.; Jaafar, A. Ownership structure, board of directors and firm performance: Evidence from Taiwan. Corp. Gov. Int. J. Bus. Soc. 2019, 19. [Google Scholar] [CrossRef]

- Bao, S.R.; Lewellyn, K.B. Ownership structure and earnings management in emerging markets—An institutionalized agency perspective. Int. Bus. Rev. 2017, 26, 828–838. [Google Scholar] [CrossRef]

- Tommasetti, R.; da Silva Macedo, M.; Azevedo de Carvalho, F.A.; Barile, S. Better with age: Financial reporting quality in family firms. J. Fam. Bus. Manag. 2019, 10, 40–57. [Google Scholar] [CrossRef]

- Mudel, S. Creative Accounting and Corporate Governance—A Literature Review. 2015. Available online: https://ssrn.com/abstract=2708464 (accessed on 28 December 2015).

- Udin, S.; Khan, M.A.; Javid, A.Y. The effects of ownership structure on likelihood of financial distress: An empirical evidence. Corp. Gov. Int. J. Bus. Soc. 2017, 17. [Google Scholar] [CrossRef]

- Abdallah, A.A.-N.; Ismail, A.K. Corporate governance practices, ownership structure, and corporate performance in the GCC countries. J. Int. Financ. Mark. Inst. Money 2017, 46, 98–115. [Google Scholar] [CrossRef]

- Rose, J.M.; Mazza, C.R.; Norman, C.S.; Rose, A.M.; Desoky, A.M.; Mousa, G.A.; Arsov, S.; Bucevska, V.; Popa, A.; Blidi El, R.; et al. Transparency and disclosure, neutrality and balance: Shared values or just shared words? Probl. Perspect. Manag. 2017, 8, 63–87. [Google Scholar] [CrossRef]

- Ahmed, H.; Hussain, S.; Masroor, N. Transparency, CSR Disclosure and the Financial Performance of Firms: A Case of Pakistan Stock Exchange. Karachi Univ. Bus. Res. J. 2020, 1, 1–10. [Google Scholar] [CrossRef]

- Mohammadi, S.; Nezhad, B.M. The role of disclosure and transparency in financial reporting. Int. J. Account. Econ. Stud. 2015, 3, 60. [Google Scholar] [CrossRef] [Green Version]

- Zaman, R.; Bahadar, S.; Kayani, U.N. Role of media and independent directors in corporate transparency and disclosure: Evidence from an emerging economy. Corp. Gov. Int. J. Bus. Soc. 2018, 16, 593–608. [Google Scholar] [CrossRef]

- Duh, M.; Djokić, D. Transparency and Disclosure Regulations—A Valuable Component of Improving Corporate Governance Practice in Transition Economies. In Social Responsibility and Corporate Governance; Springer: Berlin/Heidelberg, Germany, 2020; pp. 193–228. [Google Scholar]

- Ejiogu, A.; Ejiogu, C.; Ambituuni, A. The dark side of transparency: Does the Nigeria extractive industries transparency initiative help or hinder accountability and corruption control? Br. Account. Rev. 2019, 51, 100811. [Google Scholar] [CrossRef]

- Lim, S.J.; White, G.; Lee, A.; Yuningsih, Y. A longitudinal study of voluntary disclosure quality in the annual reports of innovative firms. Account. Res. J. 2017, 30, 89–106. [Google Scholar] [CrossRef]

- Oh, W.Y.; Chang, Y.K.; Martynov, A.; Hicheon, K.; Heechun, K.; Peggy, M.L. Ownership structure and the relationship between financial slack and R&D investments: Evidence from Korean Firms. Organ. Sci. 2011, 19, 283–297. [Google Scholar] [CrossRef]

- Arthur, N.; Chen, H.; Tang, Q. Corporate ownership concentration and financial reporting quality: International evidence. J. Financ. Report. Account. 2019, 17, 104–132. [Google Scholar] [CrossRef]

- Krejcie, R.V.; Morgan, D.W. Determining sample size for research activities. Educ. Psychol. Meas. 1970, 30, 607–610. [Google Scholar] [CrossRef]

- Krejcie, R.V.; Morgan, D. Small-Sample Techniques. NEA Res. Bull. 1970, 30, 607–610. [Google Scholar]

- Pearlson, K.E.; Saunders, C.S.; Galletta, D.F. Managing and Using Information Systems: A Strategic Approach; John Wiley & Sons: Hoboken, NJ, USA, 2019; ISBN 111956056X. [Google Scholar]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill Building Approach; John Wiley & Sons: Hoboken, NJ, USA, 2016; ISBN 1119165555. [Google Scholar]

- DE JESUS, T.A.; PINHEIRO, P.; KAIZELER, C.; SARMENTO, M. Creative Accounting or Fraud? Ethical Perceptions Among Accountants. Int. Rev. Manag. Bus. Res. 2020, 9, 58–78. [Google Scholar] [CrossRef]

- Aifuwa, H.O.; Embele, K.; Musa, S. Ethical Accounting Practices and Financial Reporting Quality. EPRA Int. J. Multidiscip. Res. 2018, 4, 31–44. [Google Scholar]

- Salameh, R.S. What is the Impact of Internal Control System on the Quality of Banks’financial Statements in Jordan? Acad. Account. Financ. Stud. J. 2019, 23, 1–10. [Google Scholar]

- Adebiyi, W.K.; Olowookere, J.K. Ownership structure and the quality of financial reporting: Evidence from Nigerian deposit money banks. Int. J. Econ. Commer. Manag. 2016, IV, 541–552. [Google Scholar]

- Iqbal, M.; Javed, F. The moderating role of corporate governance on the relationship between capital structure and financial performance: Evidence from manufacturing sector of Pakistan. Int. J. Res. Bus. Soc. Sci. 2017, 6, 89–105. [Google Scholar]

- Rashid, M.M. Financial reporting quality and share price movement-evidence from listed companies in Bangladesh. J. Financ. Report. Account. 2020, 18, 425–458. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis Always Learning; Pearson Education Ltd.: London, UK, 2013. [Google Scholar]

- Byrne, B.M. Structural equation modeling with AMOS: Basic concepts, applications, and programming (multivariate applications series). N. Y. Taylor Fr. Gr. 2016, 396, 7384. [Google Scholar]

- Gras, E.; Palacios Manzano, M.; Hernández Fernández, J. Investigating the relationship between corporate social responsibility and earnings management: Evidence from Spain. BRQ Bus. Res. Q. 2016, 19, 289–299. [Google Scholar] [CrossRef] [Green Version]

- Shafer, W.E.; Poon, M.C.C.; Tjosvold, D. Ethical climate, goal interdependence, and commitment among Asian auditors. Manag. Audit. J. 2013, 28, 217–244. [Google Scholar] [CrossRef] [Green Version]

- Qian, W.; Hörisch, J.; Schaltegger, S.; Baalouch, F.; Ayadi, S.D.; Hussainey, K.; Agyei-Mensah, B.K.; Nagata, K.; Nguyen, P.; Daske, H.; et al. Assessing Disclosure Quality: A Methodological Issue. J. Mod. Account. Audit. 2015, 11, 466–475. [Google Scholar] [CrossRef] [Green Version]

- Mudel, S. A Study to Show the Relation between Creative Accounting and Corporate Governance. 2016. Available online: https://ssrn.com/abstract=2710567 (accessed on 4 January 2016).

- Raimo, N.; Vitolla, F.; Marrone, A.; Rubino, M. The role of ownership structure in integrated reporting policies. Bus. Strategy Environ. 2020, 29, 2238–2250. [Google Scholar] [CrossRef]

- Han, S.; Amrah, M.R.; Obaid, M.M.; Qawqzeh, H.K.; Endut, W.A.; Rashid, N.; Mustafa, M. Ownership Structure and Financial Reporting Quality: Influence of Audit Quality Evidence from Jordan. SSRN Electron. J. 2019, 8, 2212–2220. [Google Scholar] [CrossRef]

- Muraina, S.A.; Dandago, K.I. Effects of implementation of International Public Sector Accounting Standards on Nigeria’s financial reporting quality. Int. J. Public Sect. Manag. 2020, 33, 323–338. [Google Scholar] [CrossRef]

- Singla, C.; George, R.; Veliyath, R. Ownership structure and internationalization of Indian firms. J. Bus. Res. 2017, 81, 130–143. [Google Scholar] [CrossRef]

- Aguilera, R.V.; Crespi-Cladera, R. Global corporate governance: On the relevance of firms’ ownership structure. J. World Bus. 2016, 51, 50–57. [Google Scholar] [CrossRef]

- Khlif, H.; Ahmed, K.; Souissi, M. Ownership structure and voluntary disclosure: A synthesis of empirical studies. Aust. J. Manag. 2017, 42, 376–403. [Google Scholar] [CrossRef]

- Lari Dashtbayaz, M.; Salehi, M.; Safdel, T. The effect of internal controls on financial reporting quality in Iranian family firms. J. Fam. Bus. Manag. 2019, 9, 254–270. [Google Scholar] [CrossRef]

- Ibrahim, H.A.M.; Abdul Hussain, M.; Abdullah, Q.M. The Impact of Creative Accounting Methods on the Quality of Accounting Information: A Field Study on the Financial Reports of Companies Listed in the Iraq Stock Exchange. J. Manag. Sci. 2017, 10, 14. [Google Scholar]

- Ndebugri, H.; Tweneboah Senzu, E. Analyzing the Critical Effect of Creative Accounting Practice in the Corporate Sector of Ghana. 2017. Available online: https://ssrn.com/abstract=3236965 (accessed on 10 January 2020).

- Cernusca, L.; David, D.; Nicolaescu, C.; Gomoi, B.C. Empirical Study on the Creative Accounting Phenomenon. Studia Univ. Vasile Goldiș Arad Ser. Științe Econ. 2016, 26, 63–87. [Google Scholar] [CrossRef] [Green Version]

- Al-Hashemi, H.T. The effect of creative accounting practices on measuring and presenting accounting information in the financial statements—A comparative analytical study on a sample of the financial and industrial sectors listed on the Iraq Stock Exchange. J. Ma’aen 2020. [Google Scholar] [CrossRef]

- Kovalová, E.; Frajtová Michalíková, K. The creative accounting in determining the bankruptcy of Business Corporation. SHS Web Conf. 2020, 74, 1017. [Google Scholar] [CrossRef]

- Goel, S. Earnings management detection over earnings cycles: The financial intelligence in Indian corporate. J. Money Laund. Control. 2017, 20, 116–129. [Google Scholar] [CrossRef]

- Khanin, D.; Mahto, R. V Regulatory risk, borderline legality, fraud and financial restatement. Int. J. Account. Inf. Manag. 2012, 20, 377–394. [Google Scholar] [CrossRef]

- Nawaz, T.; Haniffa, R. Determinants of financial performance of Islamic banks: An intellectual capital perspective. J. Islam. Account. Bus. Res. 2017, 8, 130–142. [Google Scholar] [CrossRef] [Green Version]

- Barandak, S.; Mohammadi, F. The effect of Internal Control Weakness on the Asymmetrical Behavior of Selling, General, and Administrative Costs. J. Account. Manag. Vis. 2020, 2, 38–53. [Google Scholar]

- Maskani, M.; Abdoli, M. Investigating the Effectiveness of Tournament incentive on Relationship between CEO Behavioral Bias with Internal Control Weakness in Companies listed in the Tehran Stock Exchange. Financ. Manag. Strategy 2020, 8, 135–155. [Google Scholar]

- Ashrafi, M.; Abbasi, E.; Hosseini, S.A.; Etemadi, M.P.; Kim, H.; Lee, T.H.; Suprianto, E.; Suwarno, S.; Murtini, H.; Rahmawati, R.; et al. Client importance and earnings management: The moderating role of Audit Committees. Iran. J. Financ. 2020, 30, 125–156. [Google Scholar] [CrossRef]

- Tang, Q.; Chen, H.; Lin, Z. How to measure country-level financial reporting quality? J. Financ. Report. Account. 2016, 14, 230–265. [Google Scholar] [CrossRef]

- Muhannad; Hussein, M. Creative accounting practices and their reflection on the reliability of the data published in the financial statements An applied study on a sample of commercial banks in Iraq. AL-Dananeer Mag. 2017, 1, 12–23. [Google Scholar]

- Oprean-Stan, C.; Stan, S.; Brătian, V.; Hanash, M.K.; Abbas, H.H.; Oprean-Stan, C.; Oncioiu, I.; Iuga, I.; Stan, S.; Okoye, E.; et al. Corporate Sustainability and Intangible Resources Binomial: New Proposal on Intangible Resources Recognition and Evaluation. Sustainability 2018, 12, 4150. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Description | No. of Questionnaires | Percentage |

|---|---|---|

| Total questionnaires distributed | 500 | 100% |

| Completed questionnaires received | 392 | 78.4% |

| Questionnaires uncompleted/with missing data | 28 | 7.1% |

| Usable questionnaires | 364 | 92.9% |

| Variables | A | CR | AVE | MSV | MaxR (H) |

|---|---|---|---|---|---|

| EI | 0.978 | 0.978 | 0.901 | 0.150 | 0.981 |

| DQ | 0.970 | 0.970 | 0.866 | 0.070 | 0.973 |

| IC | 0.965 | 0.967 | 0.853 | 0.155 | 0.968 |

| OS | 0.970 | 0.972 | 0.872 | 0.167 | 0.972 |

| TD | 0.845 | 0.992 | 0.970 | 0.392 | 0.993 |

| FRQ | 0.960 | 0.883 | 0.654 | 0.392 | 0.887 |

| No. | Relationship | Beta | t-Value | p-Value | Decision |

|---|---|---|---|---|---|

| H1a | EI→FRQ | 0.200 | 3.328 | *** | Supported |

| H1b | DQ→FRQ | 0.185 | 3.427 | *** | Supported |

| H1c | IC→FRQ | 0.207 | 3.640 | *** | Supported |

| H1d | OS→FRQ | 0.219 | 3.912 | *** | Supported |

| No. | Relationship | Beta | t-Value | p-Value | Decision |

|---|---|---|---|---|---|

| H2a | TD _X_ EI→FRQ | 0.213 | 5.072 | *** | Supported |

| H2b | TD _X_ DQ→FRQ | 0.203 | 4.954 | *** | Supported |

| H2c | TD _X_ IC→FRQ | 0.055 | 1.403 | 0.161 | Unsupported |

| H2d | TD _X_ OS→FRQ | 0.230 | 5.641 | *** | Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abed, I.A.; Hussin, N.; Haddad, H.; Almubaydeen, T.H.; Ali, M.A. Creative Accounting Determination and Financial Reporting Quality: The Integration of Transparency and Disclosure. J. Open Innov. Technol. Mark. Complex. 2022, 8, 38. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc8010038

Abed IA, Hussin N, Haddad H, Almubaydeen TH, Ali MA. Creative Accounting Determination and Financial Reporting Quality: The Integration of Transparency and Disclosure. Journal of Open Innovation: Technology, Market, and Complexity. 2022; 8(1):38. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc8010038

Chicago/Turabian StyleAbed, Ibtihal A., Nazimah Hussin, Hossam Haddad, Tareq Hammad Almubaydeen, and Mostafa A. Ali. 2022. "Creative Accounting Determination and Financial Reporting Quality: The Integration of Transparency and Disclosure" Journal of Open Innovation: Technology, Market, and Complexity 8, no. 1: 38. https://0-doi-org.brum.beds.ac.uk/10.3390/joitmc8010038