1. Introduction

Environmental sustainability is one of the most critical global economic concerns. Massive energy demands are fulfilled by dominating energy commodities i.e., crude oil, natural gas, and gasoline. Meanwhile, rare earths elements are important elements for electric vehicles (

Haq et al. 2022), information technology firms (

Fishman et al. 2018), and magnet production (

Reboredo and Ugolini 2020). However, the energy consumption of rare earths results in severe climate change, carbon footprints, and air pollution issues (

Balaram 2019;

Dudley 2018;

Kihombo et al. 2022). Noticeably, the majority of REEs extraction methods from primary or secondary resources involve dirty and energy-intensive extraction processes which cause environmental issues. In the 2019 International Energy Agency, carbon dioxide (CO

2) was the most significant component of greenhouse gas emissions, which soared by 1.7 percent in 2018 (

Newell and Raimi 2020), signifying a record level of 33.1 Gt. Due to escalating effects of energy consumption and rare earths exploration on climate change and global warming, it is crucial to study the connectedness between rare earths, energy, and sustainable financial markets. In this way, economies can support the 2015 Paris Agreement and Sustainable Development Goals of the United Nations to mitigate CO

2 climate change and global warming and reform their economies to promote climate resilient global economy (

Gaustad et al. 2021;

Schulze and Buchert 2016). Additionally,

Gaustad et al. (

2021) noted that it is important to consider both environmental or social and economic or financial perspectives for investors and practitioners.

Rare earths, energy consumption, and sustainability have become major drivers of sustainable and green economic growth in the current era (

Haq et al. 2021b,

2022;

Zhou et al. 2022), which motivates this research to answer following two questions. First, is there a time-varying volatility connectedness between rare earths, energy, and sustainable financial markets in a normal period? Second, is there a time-varying volatility transmission between rare earths, energy, and sustainable financial markets during a fragile period, i.e., COVID-19?

Since that time, it has become critical for the global economy to transform its traditional energy resources into low-carbon resilient economies while maintaining environmental sustainability (

Murshed 2018). As a result, scholars and environmentalists have been increasingly concerned about global climate change and carbon footprints (

Singh and Dhadse 2021). Several studies have found that primary REEs extraction activities have degraded environmental quality and posed human health risks due to increased inorganic pollutant concentrations (

Usman et al. 2020). While other studies have concluded that it is essential to restrict unregulated rare earth elements mining and that its extraction process effect on human health and the ecosystem should be reduced (

Liang et al. 2014;

Packey and Kingsnorth 2016). Due to the severe environmental effects and high energy requirements of the processes used to extract REE, environmental sustainability has now emerged as a crucial economic criterion. Thus, this study largely focuses on exploring the financial and environmental perspective of rare earth markets and energy commodities.

Evidently, before China’s mining boom, the US held the monopoly on the global REE elements market for several decades through Mountain Pass production in 1965 (

Barakos and Mischo 2017). Unfortunately, mining activities halted in 1998, due to Chinese REE market competition and environmental issues in the mountain pass region (

Mancheri et al. 2019). As a result, the US economy has shifted its attention to REE recycling and imports a considerable quantity from several other countries (

Marques et al. 2021). Meanwhile, other countries are also focusing on recycling REE materials and restricting their mining activities through primary resources to lessen environmental effects and improve energy efficiency (

Brahim et al. 2022). These circumstances placed academics and environmentalists under immense pressure to investigate other REE sources and enhance extraction technology.

In prior research,

Beylot et al. (

2019) argued that significant investments are called for in the coming decades to achieve the objective of resilient economies with low carbon emissions. Additionally, impeding challenges including peak oil prices (

Akhtaruzzaman et al. 2021c), economic vulnerability, and geopolitical issues have already prompted the need to diversify energy portfolios to achieve a global sustainable system (

Balali and Stegen 2021). Therefore, increasing magnet use, rising global economic growth, and technological advancement are key drivers boosting demand for REEs. Global Market Insights Inc.’s 2020 research predicts that the annual growth rate of REE would be increased by 10.8% from 2022 to 2026, providing fund managers and investors throughout the world with a wide range of investment possibilities. So far, worldwide governments should undertake significant REE production plans and technology advances in REE’s mining and recycling process as expansion in REE’s market has piqued the interests of market participants. Moreover, the worsening impact of REEs on environmental quality and escalating climate challenges have spurred a global consensus to integrate global growth plans with concurrent environmental protection.

Therefore, the primary aim of our study is to reveal the dynamic volatility transmission across markets. In addition to exploring portfolio diversification or hedging opportunities across rare earths, energy, and sustainable financial markets. Generally, most portfolio managers and investors prefer higher returns at a given level of risk in their portfolios, which allows them to diversify their portfolio risk by integrating negatively or weakly correlated securities in their portfolio to obtain optimal portfolio performance (

Evans and Archer 1968). Understanding volatility transmissions allows investors to better understand dynamic risk patterns during normal and adverse market conditions.

A strand of literature has investigated the information transmission among financial markets (

Haq et al. 2022;

Pantos et al. 2019;

Papathanasiou et al. 2022b;

Samitas and Kampouris 2019;

Samitas et al. 2022b,

2022c). Energy commodities and rare earths have varying impacts across different financial markets (

Haq et al. 2021b,

2022;

Hau et al. 2022;

Zhou et al. 2022). Hence, rare earths and energy commodities inherit varying hedging or diversification properties across time and frequency and may differ across multiple financial markets and energy commodities. In overview, our research is grounded on the theoretical standing of Markowitz’s portfolio theory (

Sharpe 1964). The idea of portfolio theory suggests that investors can design a portfolio of assets considering the negative correlation patterns or moderate positively correlated assets. In addition, an investor can earn and minimize the expected volatility at a given level of risk.

This study has a potential contribution to the existing literature (

Bouri et al. 2021a;

Chen et al. 2021;

Haq et al. 2021b,

2022;

Hau et al. 2022;

Reboredo and Ugolini 2020;

Shin et al. 2019;

Song et al. 2021;

Zheng et al. 2021,

2022;

Zhou et al. 2022) in several ways. First, this study adds to the spillover and hedging literature (

Haq et al. 2022;

Pantos et al. 2019;

Papathanasiou et al. 2022b;

Reboredo and Ugolini 2020;

Samitas and Kampouris 2019;

Samitas et al. 2022b,

2022c) that rare earth elements and energy commodities, i.e., Gas, Natural Gas, and Crude Oil show heterogeneous volatility transmission toward financial markets in normal and fragile periods. Second, this research contributes to the recent body of literature (

Haq et al. 2022;

Samitas et al. 2022b,

2022d;

Zhang et al. 2021), as no recent considered the dynamic volatility spillovers among these financial markets. Due to this, the sample set covers the impact of several financially and economically fragile periods, i.e., the COVID-19 episode (

Haq and Awan 2020;

Huynh et al. 2021). Finally, we uncover the dynamic volatility spillover in major economies, i.e., China, the USA, and Australia, which are largest consumers of energy commodities, i.e., crude oil, and possess 80% the world’s REE reserves as reported in

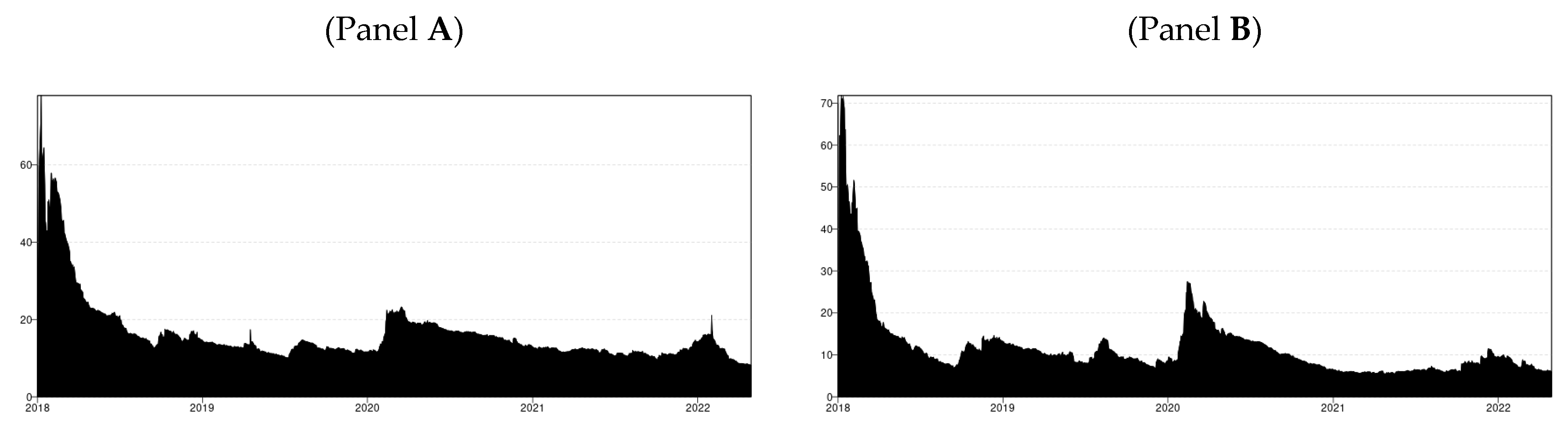

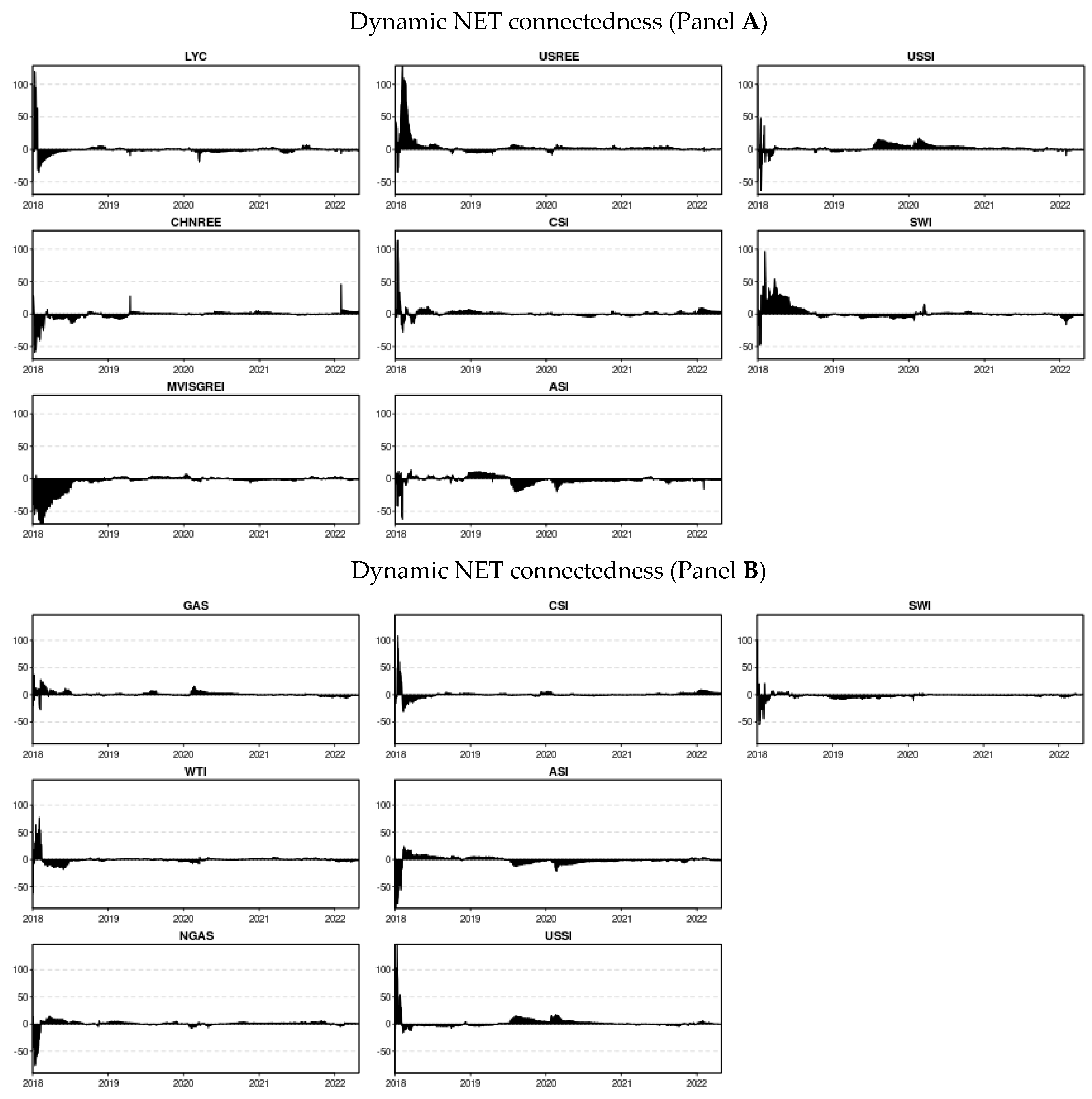

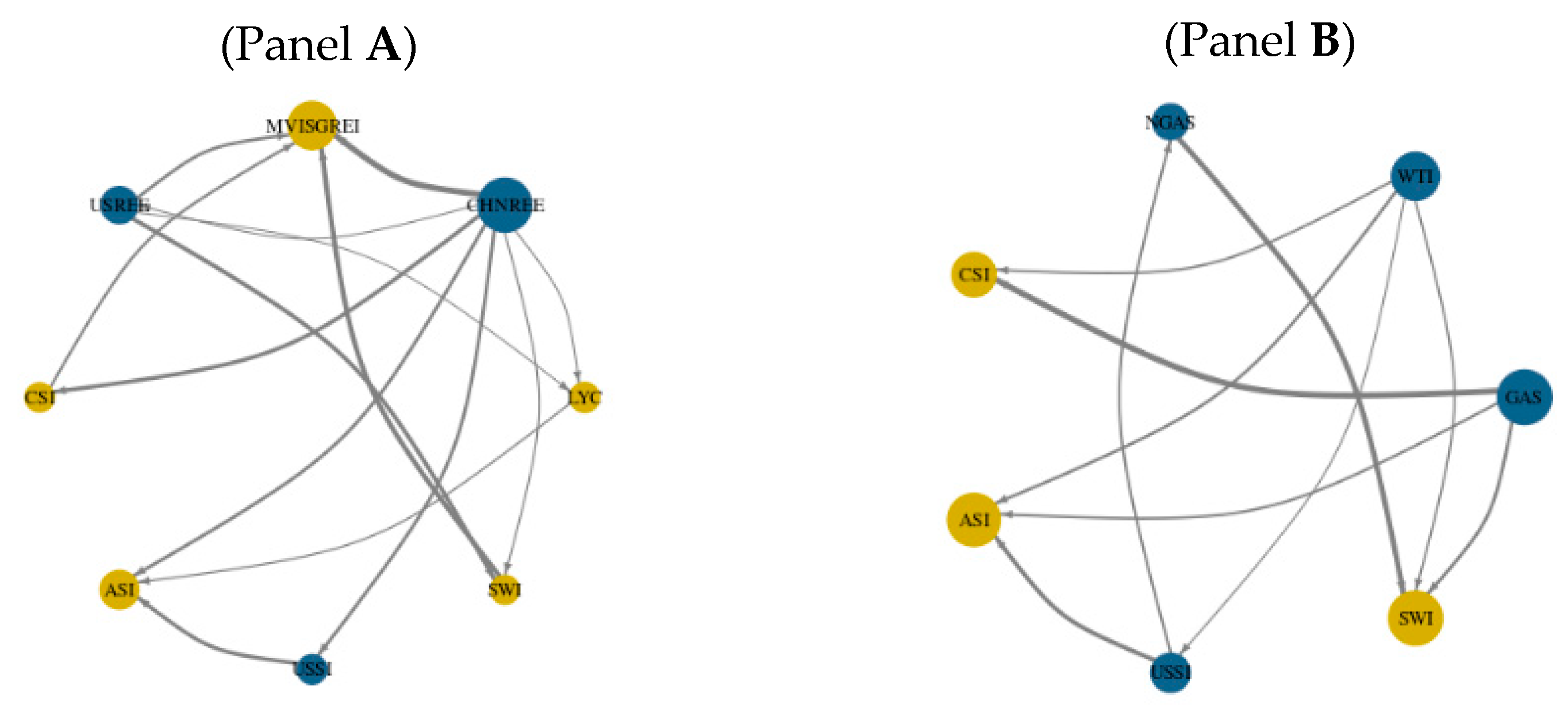

Table 1. Our empirical findings show heterogeneous volatility spillovers over time and that connectedness follows a random course over time. The volatility spillover has experienced a surge during the intense economic period, i.e., COVID-19. Total volatility spillovers present a spike around the COVID-19 outbreak, suggesting higher volatility transmission among financial markets during turbulent and crisis periods. Rare earth markets (the US and China) are net volatility transmitters and the Dow Jones Australia Sustainability Index (ASI), China Sustainability Index (CSI), Dow Jones Sustainability World Index (SWI), and MVIS Global Rare Earth Index (MVISGREI) are net recipients. Further analysis revealed that energy commodities (Crude Oil, Gasoline, and Natural Gas) are net volatility transmitters whereas ASI, CSI, and SWI are the main volatility recipients. Notably, rare earths or energy commodities failed to transmit volatility to the US sustainable financial market.

The remaining research structure of our paper is as follows:

Section 2 discusses previous literature in the current strand.

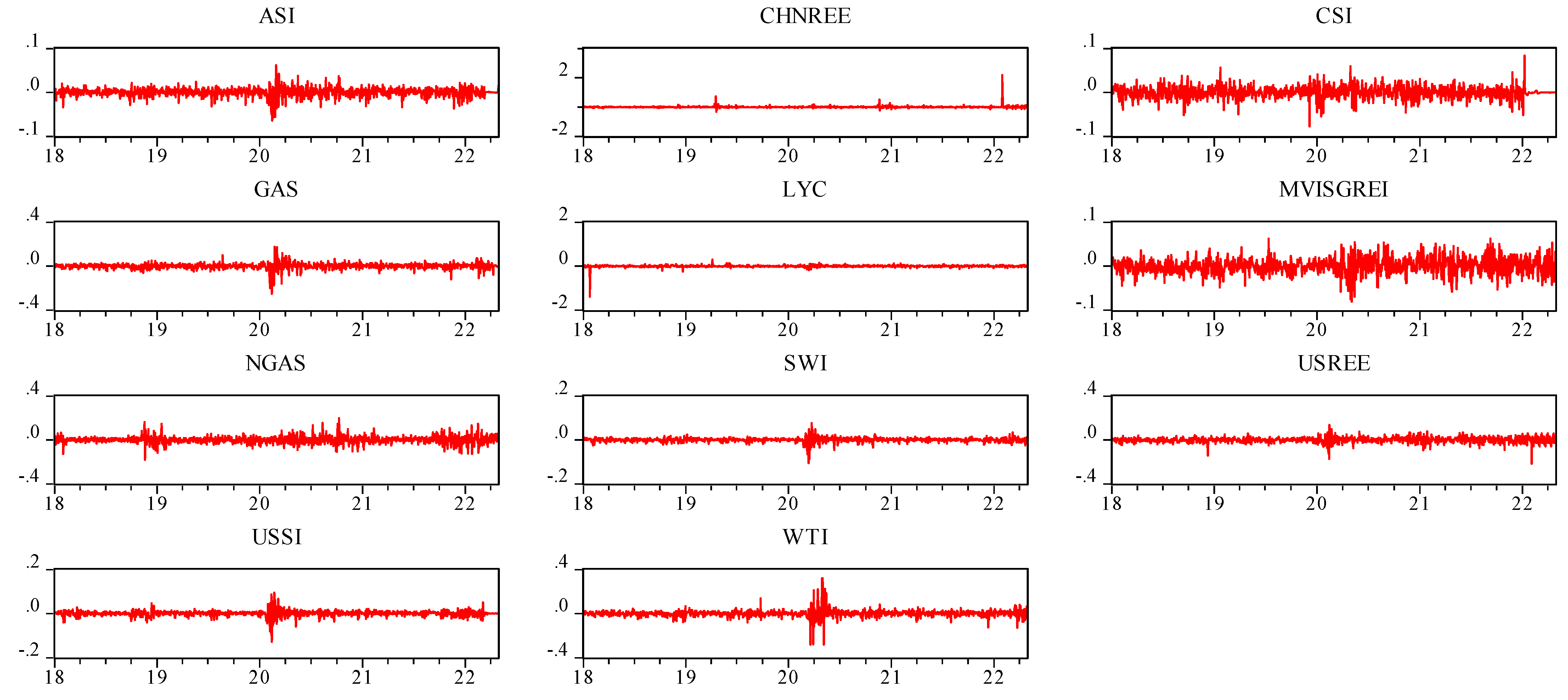

Section 3 describes the data and methodology used to analyze time-varying connectedness.

Section 4 reports results and interpretation. Finally,

Section 5 concludes our paper with policy implications.

2. Related Studies

The economic importance of rare earth elements (REEs) has thrived in the last decade. For instance, REEs have been identified as a crucial element in various environmentally sustainable technologies due to their exceptional conductive and magnetic properties (

Zhou et al. 2017). The global trend of low-carbon resilient economies has been irresistible in recent years. In addition, it has arisen in conjunction with emerging sustainable technology in which rare earth elements play a vital role and have no other substitute in the global market (

Zhao et al. 2017). Moreover, environmentally friendly technology manufacturing is largely based on REEs as these elements are essential components for manufacturing (

De Koning et al. 2018). Inherited volatility and rising demand for sustainable technologies are damaging environmental and sustainable concerns around the globe (

Haq et al. 2022;

Reboredo and Ugolini 2020) due to unsustainable extraction and mining processes of REEs (

Khorasanipour and Jafari 2018). Likewise,

Balaram (

2019);

Mancheri et al. (

2019) documented the influence of REEs occurrence, exploration, and recycling on environmental sustainability and revealed that policymakers should prioritize recycling of REE waste since it has a less severe environmental impact. Therefore, to overcome such economic and sustainable challenges, the rare earth elements industry should focus on long-run socially sustainable goals by promoting the United Nations sustainable development goals (SDGs) (

Dushyantha et al. 2020).

On the other hand, CO

2 emissions have grown due to increased energy consumption, they have also emerged as the biggest threat to sustainable development (

Nathaniel and Iheonu 2019) due to energy commodities. Unfortunately, human activities always remain the major driver of these global emissions (

Du et al. 2019). So far, an extensive set of countries have worked together under the United Nations Climate Change Conference in Paris 2015 to make their economies carbon resilient by promoting sustainable consumption (

Cai et al. 2020;

Sadiq et al. 2022). Furthermore, the Sustainable Development Goals (SDGs) emphasize that countries should reduce carbon emissions, increase energy efficiency, transition to a sustainable energy system, and ensure the supply of sustainable energy. The SDGs also emphasize the protection of biodiversity, maintenance of the ecosystem, and mitigation of environmental degradation to promote equitable human and economic growth.

The relationship between rare earths and financial markets has not yet been developed in the same way as other financial concepts. Some recent studies have examined the volatility connectedness between rare earths and financial markets. For example,

Reboredo and Ugolini (

2020) revealed that price fluctuations in the REE’s market and supply interruptions had a detrimental impact on sustainable industries, especially when REE prices increase. Further,

Song et al. (

2021) examined the connectedness of REE with financial markets by using the TVP-VAR model to uncover dynamic connectedness during the COVID-19 pandemic. The findings of the study showed that the volatile REEs market has a strong interdependence with crude oil and the clean energy market. However,

Bouri et al. (

2021a) extended this framework by using a quantile based connectedness technique to explore both tail-based and average connectedness where they revealed that interdependence of these markets varies considerably at upper and lower quantiles. Moreover, they concluded that US–China trade has little effect on return and volatility dynamics. In a similar domain,

Haq et al. (

2021b) explored the dynamic association between global rare earths and sustainable markets by employing the DCC-MGARCH model to assess the time-varying co-movements. The findings of this study showed that global rare earths exhibited safe-haven properties against economic policy uncertainty (EPU). More specifically, focusing on the impact of the 2015 Paris Agreement on sustainability,

Zhou et al. (

2022) noticed the extreme spillover effects between sustainable energy and metal markets by employing a spillover index and quantile approach. Further, the study indicated an asymmetric spillover effect among markets due to certain differences, especially in extremely negative and positive situations. Precedingly,

Zheng et al. (

2022) investigated time–frequency movements among REEs and energy markets by using the wavelet and BEKK–GARCH model. They found that REEs have a significant impact on advanced technology and sustainable energy markets and highlight potential portfolio and risk management strategies (

Haq et al. 2022). In overview, the above discussion of the literature revealed rare earths markets are a strong source of financial contagion effect toward conventional and sustainable financial markets as economies are becoming more deliberate in regard to environmental protection and carbon resilience.

The association between energy commodities and financial markets has developed in finance literature. Previous research is segregated into two parts. In the first part, researchers examined the causal effects of technological, social, and economic activities on energy consumption (

Danish and Ahmad 2018;

Shahbaz et al. 2017). The findings of these studies demonstrated that the casual association between technological, social, and economic activities and CO

2 emissions caused by drastic energy consumption varies across counties due to differences in their institutional, economic, geographical, technological, and political conditions (

Rahman and Kashem 2017). In the second part, scholars extended their analysis by adding the indicators of environmental deterioration which fostered the vulnerability of environmental sustainability, such as CO

2 emissions (

Cetin et al. 2018;

Ehigiamusoe and Lean 2019;

Pablo-Romero and De Jesús 2016). The findings showed that pollution caused by CO

2 emissions has a detrimental effect on human health and contributes to mortality (

Khan et al. 2019). To combat this threat, previous literature urges various countries to turn their attention to sustainable energy sources since they are clean, have low carbon emissions, and encourage environmental sustainability (

Shezan et al. 2017).

A strand of the literature concluded that energy commodities harm the environment due to their excessive consumption patterns, i.e., crude oil, natural gas, and gasoline throughout the world. Initially,

Managi and Okimoto (

2013) documented that increases in crude oil prices have a positive impact on other potential sustainable energy firms because escalating energy crises have driven the global economy to seek alternative energy sources.

Nathaniel et al. (

2019) explored energy consumption by applying the ARDL estimation approach and their findings reveal that economic growth and financial development have a devastating impact on the environment in the short run. Similarly (

Maghyereh et al. 2019), documented that in the last decade, the main reason for fluctuations in oil prices was environmental sustainability, as crude oil is not only a primary energy resource but also has a wide range of environmental impacts due to carbon emissions during the combustion process, which results in increased global warming. Thus, fluctuations in crude oil prices have always been a major concern for portfolio managers, global investors, and policymakers during various energy crises. As dynamic fluctuations in crude oil have a substantial impact on investor’s decisions regarding production plans, assets allocation, and implementation of regulations, it has an overall influential impact on the global economy (

Aslam et al. 2022;

Inshakov et al. 2019;

Sorknæs et al. 2020).

More specifically, a range of studies have explored volatility spillovers using the TVP-VAR approach among financial markets during the pandemic period. For instance,

Samitas et al. (

2022a) recently found instant financial contagion due to the COVID-19 financial market using network analysis. Likewise, identical spillover patterns from the fine wine market to global financial markets were uncovered (

Samitas et al. 2022d). Focusing on the COVID-19 period,

Zhang et al. (

2021) highlighted that COVID-19 has a significant impact on the financial contagion effect and that volatility connectedness heightened during the stress period. Similarly, using the TVP-VAR model,

Haq (

2022) revealed escalating volatility spillover of cryptocurrency environmental attention toward sustainable financial markets during the COVID-19 pandemic period. However, no study to date has examined the volatility spillovers of rare earths markets and energy commodities to sustainable financial markets considering pandemic episodes.

From the above discussion, we infer two observations. First, the dynamic connectedness between financial markets has been extensively developed; with heterogenous transmission patterns revealed over time. However, earlier research is inclusive and ignores empirical evidence on the volatility spillovers of rare earths, energy, and sustainable financial markets. Second, several recent studies investigated whether the dynamic connectedness and financial contagion effect of rare earths, energy commodities, and sustainable financial markets is underdeveloped, considering the COVID-19 health crisis. However, the earlier research neglected to study the dynamic connectedness between these financial markets considering the COVID-19 episode.

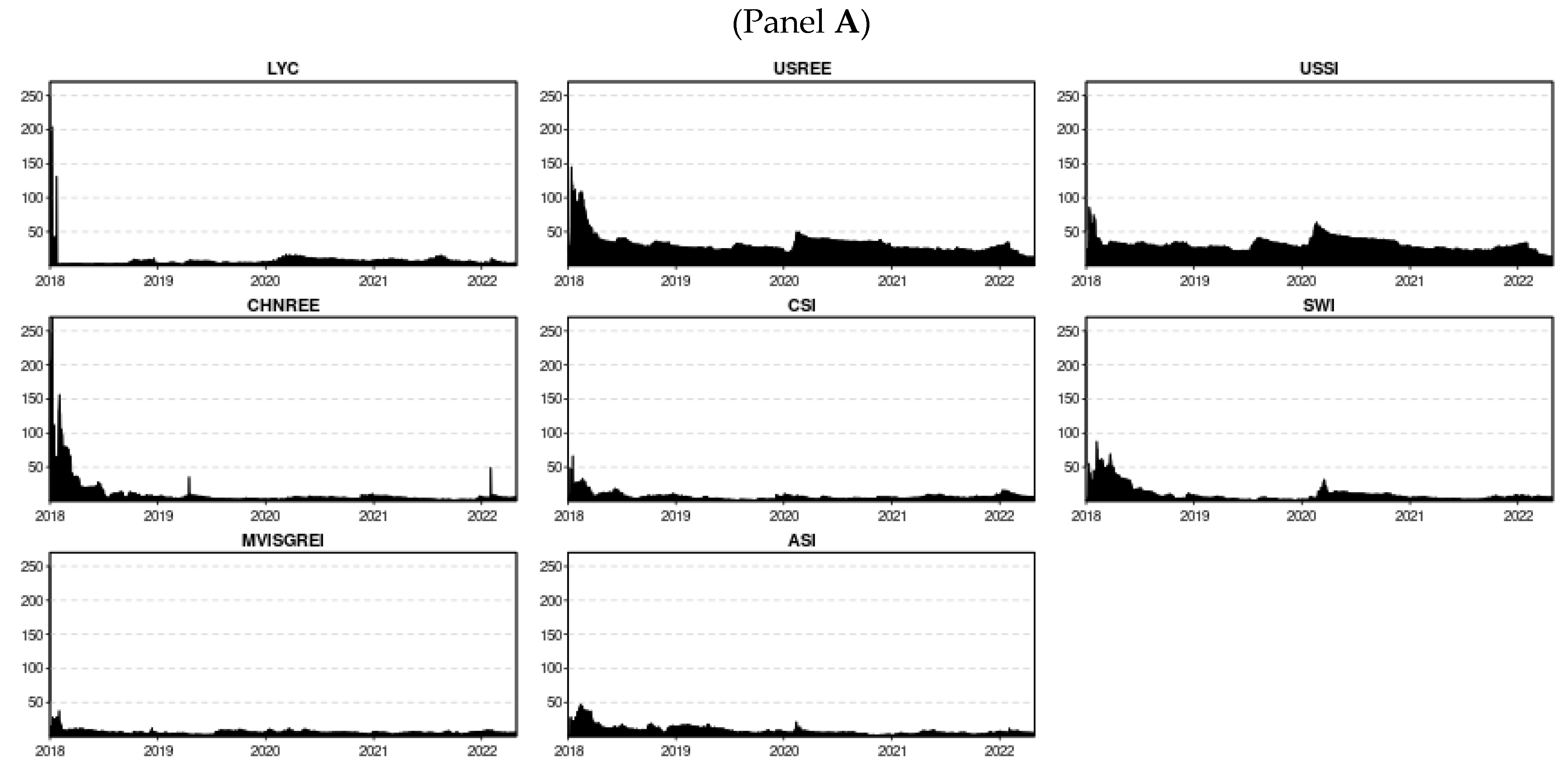

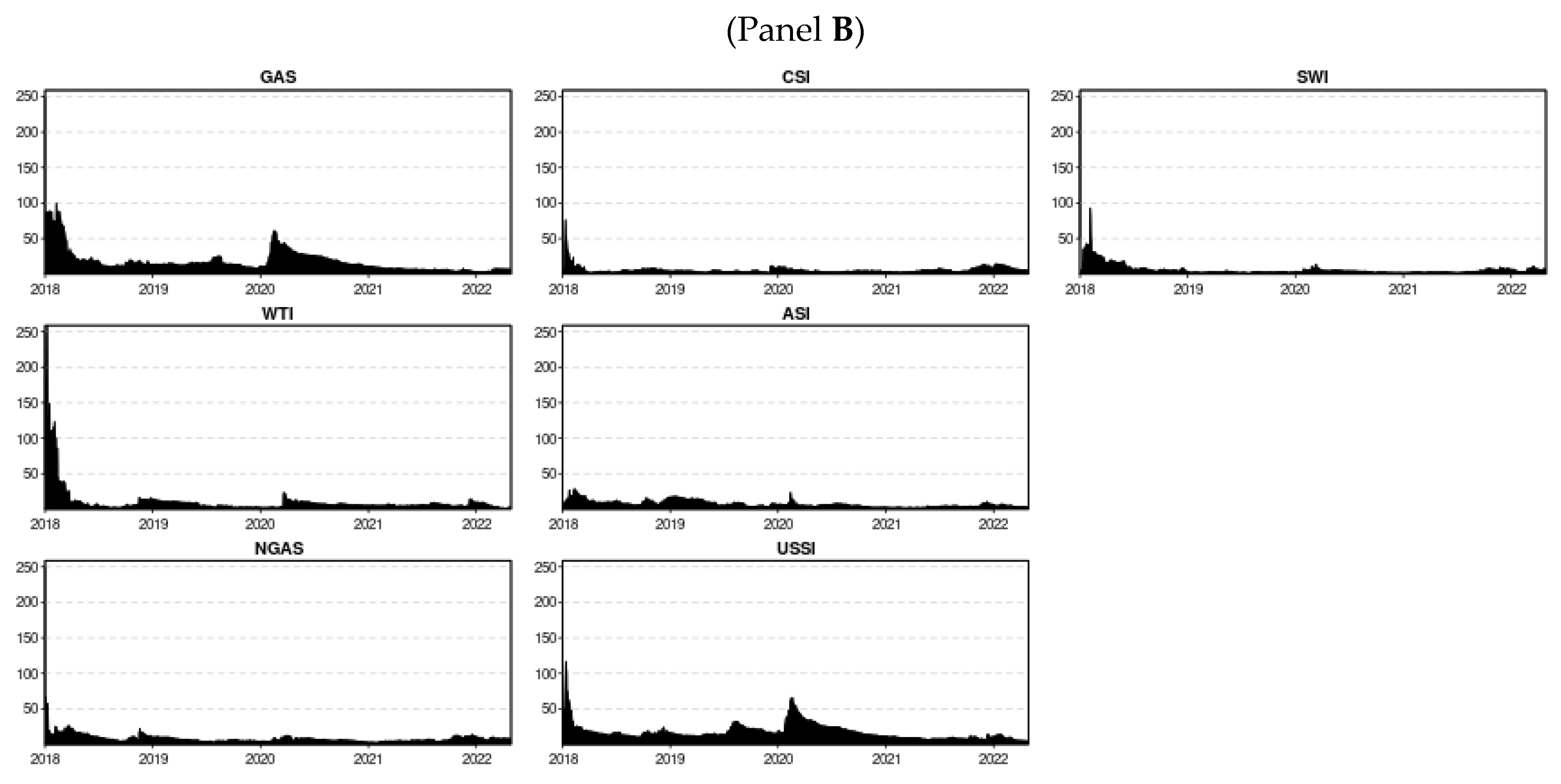

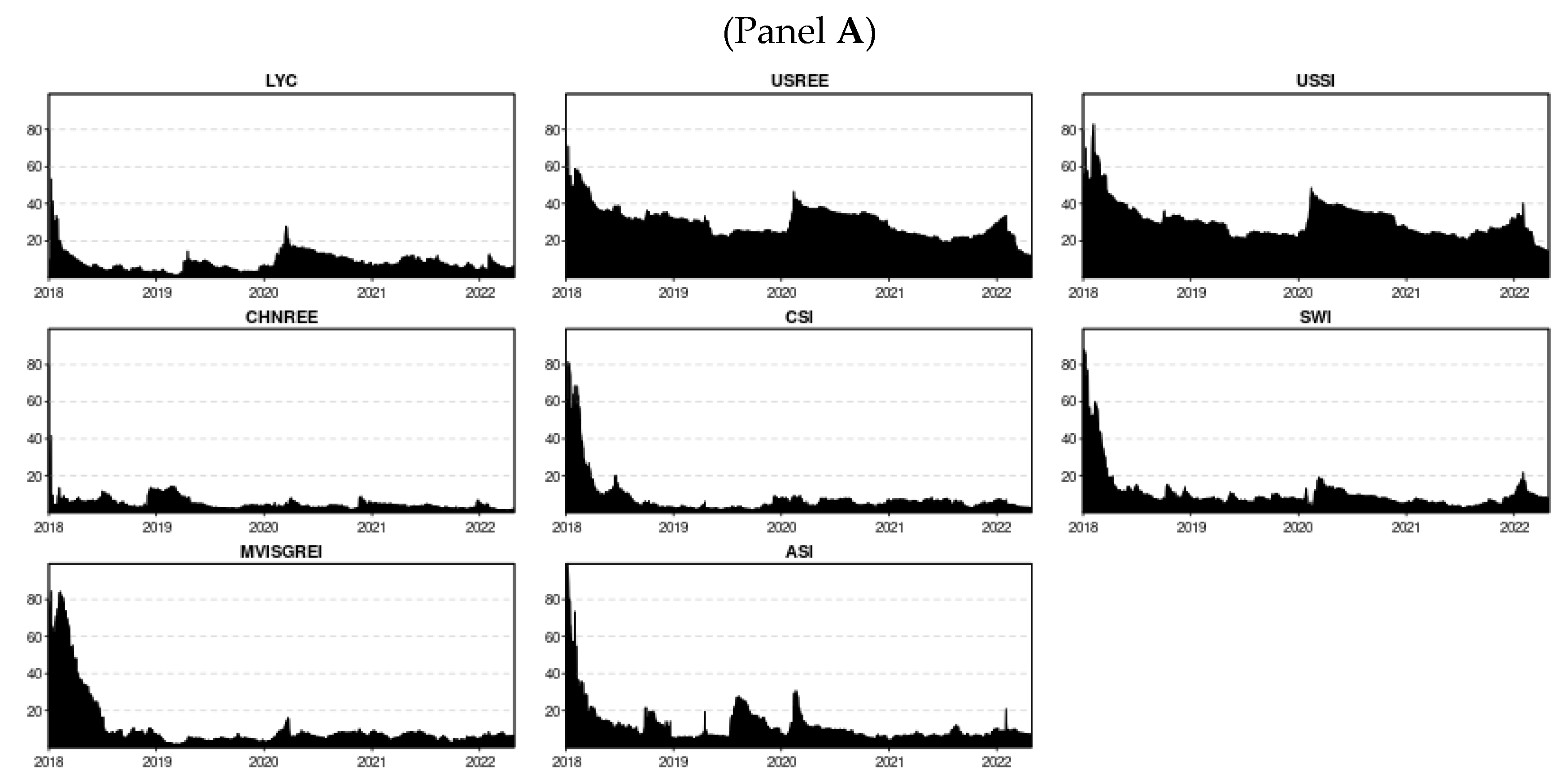

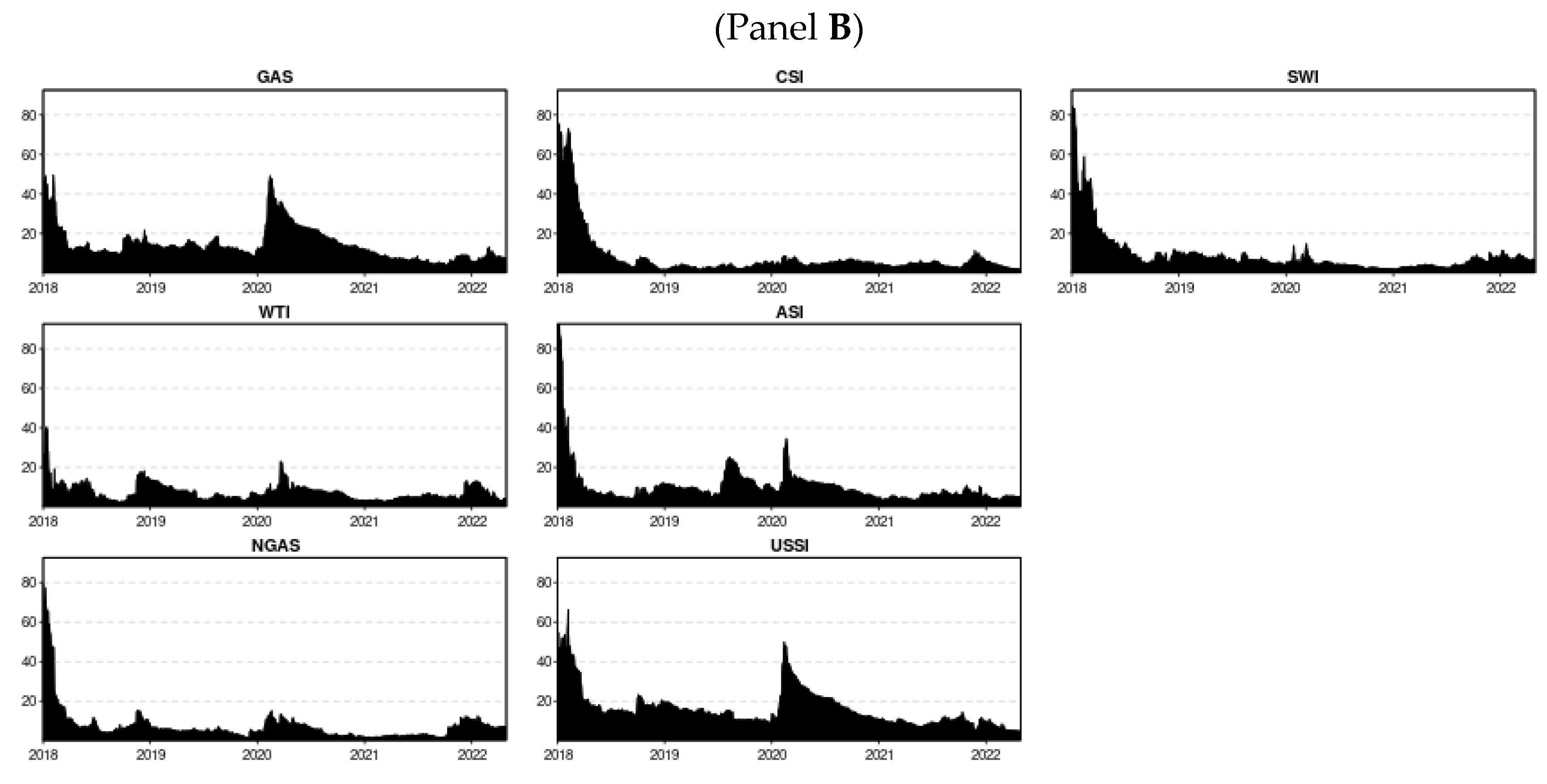

5. Conclusions and Policy Implications

Our study provides evidence of the dynamic connectedness of rare earth elements (US, China, Australia), energy commodities (Gas, Crude oil, and Natural gas), and major sustainability indices (US, China, Australia) using the TVP-VAR connectedness approach from 2018 to 2022. We further investigated the role of global rare earth elements on world sustainability. Our findings uncover that CHREE and USREE are major transmitters of volatility spillovers whereas MVISGREI, ASI, CSI, SWI, and LYC are net recipients of spillovers. Besides, Gas, WTI, and NGAS (energy commodities) are net contributors to volatility transmission, and CSI, ASI, and SWI are net receivers of volatility spillovers. The time-varying connectedness presented a spillover spike around the outbreak of the COVID-19 pandemic. The NET connectedness reiterated that CHREE and USREE are NET volatility transmitters whereas the remaining markets are presented as NET recipients. In addition, GAS, WTI, and NGAS are NET volatility transmitters however, recent the markets are demonstrated as NET recipients. In addition, MVISGREI and DJSWI are receivers of volatility from other markets. The findings stipulate intriguing implications for investors, portfolio managers, financial market participants, and policymakers. The total connectedness index suggests weak connectedness in both cases, suggesting that sustainable investments are potential sources of hedging the inherent high volatility of rare earths (

Song et al. 2021) among Australian and Chinese sustainable markets. In general, the majority of spillover of energy commodities and rare earth elements to the sustainable market is weak, suggesting the diversification opportunities of energy commodities and rare earth elements for Australia, China, and the global sustainable market. In this way, investors (institutional and individual) and portfolio managers can choose markets with greater diversification potential. The connectedness between energy commodities and sustainable markets is considerably weaker than between rare earths and sustainable financial markets. Due to this, there exist significant diversification and risk management opportunities for conventional and sustainable investors. However, energy commodities show stronger diversification potential than rare earth elements for sustainable financial assets. On the other hand, energy commodities and rare earths markets are sources of worsening sustainability and increasing volatility for the Australia sustainability index, China sustainability index, and Dow Jones sustainability world index. More specifically, global, Chinese, and Australian sustainable financial markets are most sensitive and vulnerable to carbon emissions, climate change, and circumventing environmental disasters. Hence, policymakers and regulators need to design policies and regulations to restrain the negative impact of rare earths and energy markets on the global sustainable economy and sustainable development goals. Moreover, enhancement of governance can substantially decrease the vulnerability of carbon risk (

Tran et al. 2022). The current need is encouragement of green and sustainable investments to dampen the devasting role of rare earths and energy commodities.

Our findings are basically based on the time-varying method, i.e., TVP-VAR model which can only measure volatility connectedness across time. However, conventional and sustainable investors have a diverse range of investment objectives across investment horizons, i.e., short, medium, and long (

Ul Haq et al. 2022). Therefore, future research should consider a wavelet coherence approach to examine the co-movement across both time and frequency settings. Our study explored the financial contagion effect of rare earths and energy commodities on major sustainable financial markets; however, future research could extend the sample and add clean energy stocks and green bonds (

Haq et al. 2021b), considering the COVID-19 crisis (

Akhtaruzzaman et al. 2021a). Studying the hedge or safe-haven role of gold (

Akhtaruzzaman et al. 2021b) for rare earth markets could be another possible extension of the topic.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}