The Effect of Business Legal Form on the Perception of COVID-19-Related Disruptions by Households Running a Business

Department of Corporate Finance and Insurance, Faculty of Finance, University of Economics in Katowice, 40-287 Katowice, Poland

*

Author to whom correspondence should be addressed.

Risks 2022, 10(4), 82; https://0-doi-org.brum.beds.ac.uk/10.3390/risks10040082

Submission received: 31 January 2022

/

Revised: 12 March 2022

/

Accepted: 21 March 2022

/

Published: 11 April 2022

(This article belongs to the Special Issue Main Threats of Pandemic Diseases for Financial Management in Households)

Abstract

:Recent studies uncover the lack of symmetry in COVID-19-related economic shock distributions among households. Thus, questions arise about the appropriateness of diverse risk-coping mechanisms by households. We add to this strand of research by focusing on households running a business. In particular, we analyze the role of basic legal aspects of running a business by individuals, specifically a legal form of business activity in shaping COVID-19-related business risk perception. We posit that the different legal forms allow for different risk-coping mechanisms. We incorporate analysis of variance (ANOVA) on data obtained via a survey distributed among households running a business in Poland, a country where the pandemic threatens poverty-reducing growth. We confirm that between the groups of households running a business in various legal forms, there are statistically significant differences regarding the impact of COVID-19. Thus, we conclude that the choice of business legal form affects vulnerability to COVID-19-related interruptions among households running a business.

1. Introduction

The COVID-19 outbreak has led to human tragedies, lockdowns and substantial disruptions to economic activities around the world. In this term the pandemic has generated a complex exogenous economic shock that has severely affected households. Personal financial damage is highly asymmetric which raises questions on how to design relief and recovery measures by policymakers and how to support household resilience in case of pandemic longevity. Household finance anchored studies provide in-depth insights into how severely COVID-19 impacts households’ spending, income, wealth, investment and poverty (Hanspal et al. 2020a; Baker et al. 2020; Martin et al. 2020; Chronopoulos et al. 2020). There are also studies that aim to answer the question on which groups of households were more or less vulnerable to the pandemic shock. Barrafrem et al. (2020) show that contextual factors and personal aspects shape the financial vulnerability of households during the turbulent and stressful times of the pandemic. Other studies show that the current crisis is predominantly affecting low-income households, labor-dependent households, females and the unemployed (Brewer and Gardiner 2020; Schneider et al. 2020; Albacete et al. 2021; Kansiime et al. 2021). There is also important evidence that the level of vulnerability is unevenly distributed across countries (Midões and Seré 2021). A broad conclusion that can be derived from this emerging literature is that different individuals and households have been exposed to the COVID-19 driven crisis in different ways and to varying degrees, confirming the lack of symmetry in shock distribution and the change in inequality structures that the shock has introduced. However, in the extant literature, household heterogeneity has not been fully accounted for and further studies are needed to capture the pattern of COVID-19-related distress that is experienced by diverse households. We aim to contribute to this debate by focusing on an under-researched area of the risk perception of the households involved in business activity, by setting up their own firms. In particular, we intend to analyze the role of the basic legal aspects of running a business as an individual, specifically a legal form of business activity in shaping risk perception. The legal form defines the legal status of the business venture and its main features, including the sources of capital and the liabilities of the owners. We posit that different legal forms allow households to adopt different mechanisms to cope with business risk which in turn may affect their perception of COVID-19-related disruptions.

Since the seminal paper of Hurst and Lusardi (2004), it has been widely accepted that household finance and entrepreneurship are closely intertwined. Personal savings are used to finance one’s business, while profits from this business often accrue personal assets. The current COVID-19 driven crisis has brought this issue to the forefront because of the large and rapid decline in business liquidity and profitability, in the SMEs (small and medium size enterprises) sector in particular, (Block et al. 2021; Guerini et al. 2020; Shen et al. 2020) coupled with the household income shock (Li et al. 2020; Demertzis et al. 2020; Hanspal et al. 2020b). This has magnified tensions between business goals and a private life, and has raised questions on how business owners/entrepreneurs can manage these tensions (Yue et al. 2021), especially in terms of the high volatility of health risk and strict restrictions that created/intensified the VUCA environment. Business owners/entrepreneurs may choose from the different forms of business activity and this choice has many important consequences, including their vulnerability to crisis and related concerns over their household wealth. Thus, the aim of this study is to understand how the choice of business legal form affects privately-held companies’ perception of risks related to COVID-19-related interruptions and consequently impacts the situation of the households running their own firms.

Another cognitive gap in the emerging strand of COVID-19-related literature on household finance is that few researchers have investigated the impact of this pandemic on households’ financial behaviors in emerging markets, and that existing studies focus predominantly on Asia and Africa (e.g., Yue et al. 2020; Kansiime et al. 2021). To complement previousinsights, we focus our attention on Poland—the only country from the former Soviet bloc that has recently been awarded developed status by the FTSE (Financial Times Stock Exchange). Poland and other fast-growing, large economies are believed to be the key factor in the future growth of world trade and to be critical participants in the world’s major political, economic, and social affairs. Poland is an exceptional field for researching households’ financial exposure to COVID-19-related distress for several reasons. First, Poland is best known for its economic success in the institutional transition from a command economy to a free-market system and then towards intensive Europeanisation. The reforms mobilized thousands of households to establish business ventures which enhanced the ability of the economy to generate jobs and alleviate poverty (Paci et al. 2004; Marsh and Thomas 2017; Korosteleva and Stępień-Baig 2020). The COVID-19 outbreak threatens poverty-reducing growth in Poland where a substantial number of jobs are related to self-employment. In Poland, SMEs represent 99.8% of all enterprises, they produce about 50% of GDPs (gross domestic products) and they give employment to more than 67% of the Polish workforce (European Commission 2019). The self-employed account for around three million people, that is around 20% of total number of employed people in Poland (GUS 2021a).

A second reason for researching the situation in Poland is that in this country the COVID-19-related uncertainty is exacerbated by an extremely complex legal environment for business owners. According to the Global Business Complexity Index 2021 (TMF Group 2021) Poland scores as the second most complex country in Europe for doing business. Therefore, business owners face significant uncertainty regarding their liabilities to their employees, business partners and social security as well as tax liabilities. It is well evidenced that the quality of the institutional context can have advantageous or disadvantageous effects on diverse business legal forms. In this regard, our focus on the role of the legal form on the business activity undertaken by individuals can bring about a new understanding of the patterns of households’ exposition to COVID-19.

In a methodical context, this study presents survey results. The survey was conducted in January–February 2021 on a random sample of Polish businesses, owned by households. In the period that we ran the survey, Poland was affected by the hit of the second wave of the pandemic. Thus, the surveyed household businesses were aware of the COVID-19 disruptions. They managed to familiarize themselves with these disruptions and they increased their awareness of direct and indirect impacts. We designed a questionnaire based on the previous COVID-19 survey-based barometers (Deloitte 2020; PwC 2020), aiming to capture the most important impacts that COVID-19 had on firms, including impacts on: costs, production and sales, liquidity, financing, overall threat and elasticity to react.

This study is organized as follows. In Section 2 we provide a description of business legal forms in Poland, the mechanisms of coping with the risk that a household may adopt and the related hypothesis. In Section 3 we present our research design, sample and method. In Section 4 we present our results which we discuss then in Section 5.

2. Literature Review and Hypothesis Development

2.1. Business Legal Form as a Factor of Vulnerability

In the economics and management literature there is a separate strand that is focused on constraints and opportunities relating to small ventures’ resilience and their growth in a turbulent environment. In this literature, scholars adopt three general perspectives on the types of factors that can determine such resilience:

- Personal capabilities of a business owner (e.g., Ayala and Manzano 2014; Bullough and Renko 2013; Bullough et al. 2014);

- Organizational characteristics of a venture (e.g., Smallbone et al. 2012);

- Institutional environment (Alinovi et al. 2009; Tan et al. 2020).

Our study focuses on an under researched problem of the role of a legal form, which relates to two types of above-mentioned factors: organizational (financing resources and their management) and institutional ones (law). We focus on three types of legal forms which are used to set up a venture by individuals in Poland: sole proprietorship (hereafter SP), general partnership (hereafter GP) and limited liability companies (hereafter LLC). Individuals setting up a business consider all three types of business legal forms, and they can relatively easily switch from one form to another, including LLCs.

The simplest form of business is the SP form, which is based on the single ownership of a firm. SPs can be easily founded by an individual and the owner (sole or single trader) is fully liable for debts and their liability is unlimited. This responsibility also extends to the spouse (excluding their personal property). The important feature of SPs concerning resources management is that private (also family) resources can be at any moment employed in a business venture and that business-related assets can be easily and immediately used for private purposes. There is no minimum initial capital that needs to be provided to set up a business. However, it is difficult to raise large amounts of capital as a sole trader. Thus, SPs may face financing constraints to a much bigger extent than other business legal forms. This capital gap may hamper their ability to survive in times of crisis.

Like in the case of an SP form, a GP form does not have a legal personality. This means that a GP form is not subject to the regulations concerning legal persons. It can be founded by individuals, as well as legal entities, who become partners. Rights acquired under the name of a GP and contracted liabilities become the rights and obligations of the partners of the company, who are jointly and severally liable for them. All the partners are responsible for all debts and obligations of a GP-not only with the company’s property, but also with the personal property. In Poland a GP is perceived as a less risky form of business than an SP, because the partnership’s liabilities are firstly repaid from its assets (Winnicka-Popczyk 2014). Any enforcement from the assets of a partner is viable if enforcement from the assets of the partnership proves ineffective (this solution is called subsidiary liability of a partner). However, in fact this does not protect a partner from being sued before the enforcement of the partnership’s assets has proved to be unsuccessful. Thus, although the business risk may be spread proportionally to the equity holdings of partners, the perception of a GP as less risky than an SP may stem from partners sharing responsibility rather than from a lower probability of exposing personal wealth to the enforcement According to the Polish law regulations, there are no minimum requirements for the initial capital. However, the amount of capital that can be raised by a GP depends on the joint value of partners’ personal assets, thus GPs face smaller capital constraints than the sole proprietorships (SPs).

An LLC in Poland can be launched by individuals as well as by the legal persons. The risk is limited only to the partners’ contribution (no liability with personal assets), thus partners may fully control their risk exposure. In order to establish the LLC, a minimal initial capital of PLN 5000 is required (around EUR 230). Such a requirement for a very low initial capital should not be perceived as a barrier to set up an LLC by individuals. The limited liability of partners as well as higher financial transparency makes it easier to obtain external funding. For this reason, incorporated firms grow faster than unincorporated firms (SP or GP) (Harhoff et al. (1998)).

2.2. Risk Coping Mechanisms Influencing Households’ Perceptions of Risk

Household vulnerability to shocks, and consequently their risk perception, depends on the configuration of risk-coping mechanisms adopted by a household. Well-recognized risk-coping mechanisms used by households include savings, borrowing, formal insurance, network referral, social protection system, or diverse mechanisms for sharing risks (Lee et al. 2010; Munshi 2003; Smith and Frankenberger 2018; Hallegatte 2014). In this section we focus on two types of mechanisms: the risk sharing and risk-limiting. The reason behind this is that different types of business legal forms used by households to set up a firm allow for different levels of risk sharing and risk limiting.

Informal risk sharing by households means that losses of each member of a particular group are allocated within the group based on social ties rather than contractual agreements. In general, two types of such risk-sharing are distinguished in the literature. First is intra-household (or within-household), which refers to joint decision-making by the single household members facing risk. Second is the inter-household risk-sharing, where larger communities of households take part in risk-sharing and that acts as a supplement to self-insurance via precautionary savings. It is well evidenced that intra-household risk sharing is commonly practiced and leads to the desired outcomes, e.g., lower vulnerability of households to sudden unemployment, income losses and cyclicality (Haan and Prowse 2017; Mankart and Oikonomou 2017; Wang 2019). Intra-household risk-sharing seems to be an obvious solution in face of a turbulent environment due to close ties among household-members, smooth communication and goal sharing.

Inter-household risk sharing refers to the ability of households to protect their consumption by relying on friends and the extended family, through community-level networks, and thereby to share the risk of volatile income and spending with others. It simply means that negative shocks can be covered by transfers and gifts from family and friends. Although inter-household risk sharing may appear to be a less viable solution than an intra-household risk sharing, its underlying mechanisms are solid and include extended family ties, altruism, social norms and reciprocity within broader social networks (Agarwal and Horowitz 2002; Bourlès et al. 2021; Fafchamps 2011). In addition, the evidence on inter-household risk sharing is vast. In an empirical study of the rural Philippines, Fafchamps and Lund (2003) find that inter-household risk sharing takes place through networks of relatives and friends. De Weerdt and Dercon (2006) find that in Tanzania shocks to non-food consumption are smoothed via social-networks risk sharing. Gertler and Gruber (2002) observe that in Indonesia informal insurance helps finance the expenditure needs of individuals who suffer negative health shock. For Nigeria it is evidenced that, where savings are rare, households with informal financial access (inter-household risk sharing), which experience unexpected negative income shock see consumption fall by 15% less than those without access (Carlson et al. 2015). One broad conclusion is that social networks of family and friends provide noticeable protection to individuals in an uncertain environment.

Since pooling and diversifying risk is a central function of the financial system, it is not surprising that many studies find that informal risk sharing is especially important in contexts where financial markets and insurance markets are under-developed (Fafchamps and Lund 2003; Yang and Choi 2007; Jack and Suri 2014). This effect is explained as informal risk-sharing mechanisms acting as a substitute or complementary mechanisms to formal ones (Krueger 1999; Tchamyou 2019). In this vein, Asdrubali et al. (2020) present an interesting finding that during the financial crisis in Italy, inter-household risk sharing could also be observed. Thus, not only the level of financial system development, but also the cyclicality of the financial system can determine the extent to which the households rely on informal risk-sharing mechanisms. The evidence provided by Asdrubali et al. (2020) is momentous because since the beginning of the pandemic credit markets have tightened and it is potentially more difficult for households to access new credit now than before the pandemic (Armantier et al. 2020; Horvath et al. 2021). In addition, in Poland the negative effect of COVID-19 on the banking sector resulted in the lower availability of bank loans (Łasak 2020). The tightening of credit supply and the flight-to-safety response of banks may exacerbate the role of risk-sharing among households during the pandemic. This includes households running a business.

Different types of risk sharing options are available for different business legal forms. Intra-household risk sharing is certainly practiced by SPs. Sole traders’ family members’ (e.g., spouses’, children’s, parents’) property can be easily employed in the business activities as an informal source of financing and it can substitute credit from the constrained financial system and act as an elastic cushion against the increase of operating costs. However, it has a limited effect concerning households’’ property size. In GPs and LLCs, business owners can also use their family members’ wealth inter-household risk sharing, but a co-owned business is acknowledged as a channel of inter-household risk sharing. In the GPs, any use of the personal wealth of partners for business purposes is very elastic. In LLCs, partners can reach out their personal wealth and raise additional equity to support businesses in trouble. It is claimed that since partners pool resources together to create a business, their households share business risk (Fafchamps 2011). Consequently, the wealth of several households can be used to absorb negative shocks. In this case business risks are pooled among partners and their households which results in the overall reduction of each partner’s risk exposure (Attanasio et al. 2012).

Although risk-sharing mechanisms noticeably protect households, there can be cases where mechanisms other than risk-sharing are more viable solutions. Adopting risk-sharing mechanisms by the business owners requires decisions on allocation of resources among their household members. Using private wealth as a business risk absorbing cushion reduces the amount of wealth that can be used for other purposes and by household members other than the business owners. In Becker’s (1965) famous extension of the neoclassical model of the household, all members of the household are assumed to jointly maximize some household level welfare function. In this model various types of time (good A) and consumption (good B) combine into a single household objective function with a single overall budget constraint. In this case the household is maximizing a single utility function and so it behaves in ways that are empirically indistinguishable from the behavior of a single utility maximizing individual (Thomas 1990; Chiappori and Lewbel 2015). Translating this famous model into the context of business risk management by households, one would say that households derive utility from their ability to absorb business risk shocks (intra-household risk sharing) and this substitutes for the utility a household can derive from using wealth for other purposes (e.g., consumption). Thus, each household would have a different acceptable level of within household risk-sharing depending on a particular substitution margin. The important thing is, diminishing marginal rates of substitution results in households being less and less willing to give up consumption in order to absorb rising business risk. Knowing their rates of substitutions, households would put a limit on their wealth exposure to business risk at a level that maximizes their utility from wealth used for both purposes of business risk absorption and consumption. Limiting risk as a risk-coping mechanism may thus be a valuable option for households. In practice, setting a limit on a business risk exposure is possible for LLCs where partners are held responsible for their business liabilities up to the amount of their capital invested in a company. This amount is freely decided on by each partner and can be perfectly adjusted to the level where individual utility of wealth is maximized. Formal risk limiting is impossible for SPs and GPs.

It should be stressed that in the literature there are many doubts around Becker’s model. The reason is that the internal logic of such a model obscures the significance of the intra-household dynamic (collective choices) and heterogeneity in preferences among household members (Evans 1991; Alderman et al. 1995). Since risk-taking is a collective choice, groups (household members) are required to reach a consensus on a single collective action (Davis et al. 1992). Consensus comes at a cost (Zhang et al. 2019) and it cannot be constantly renegotiated concerning household budgetary constraints. In addition, once a consensus is reached, the household members having heterogeneous preferences may use it as a reference point for their individual choices. Considering that the reference-dependent preferences are strongly evidenced as predictors of an individual’s behavior (Crawford and Meng 2011; Abeler et al. 2011), a consensus on the within-household risk-sharing limit is an important element of heterogeneous household members’ decision taking. Such consensus can be expressed as an amount of equity provided from private wealth to the LLC, further constituting a risk limit that remains unchanged until households decide to reduce or increase their exposure to business risk. Such solutions are unavailable for the households running a business as SPs or GPs. Thus, despite arguments against Becker’s model, the risk-limiting should be perceived as an important risk-coping mechanism for households.

Business legal forms differ with respect to risk-sharing and risk-limiting possibilities. SPs allow for inter-house risk sharing. GPs and LLCs allow for inter- and intra-house risk sharing. LLCs above all allow for risk limiting. The three risk-coping mechanisms may provide different levels of protection for households running a business in Poland in times of COVID-19. Thus, we hypothesize that:

Hypothesis 1 (H1).

Sole traders (SPs), general partnerships (GPs) and limited liability companies (LLCs) differ in their perception of the severity of COVID-19-related interruptions.

3. Research Design and Method

3.1. Survey Design

The first cases of the COVID-19 infections were officially confirmed in Poland on the 4 March 2020, and shortly after the first lockdown was announced. This has led to the worsening of the macroeconomic conditions in Poland, as well as to the deterioration of the financial results of Polish enterprises. The survey was run when many household firms had already been closed for over a year and were able to operate on a regular basis only within short periods. From the macroeconomic perspective, the negative impact of COVID-19 on the Polish economy is manifested for instance by the decrease in GDP (4.6%) or reduced rate of investments (10.6%) (Ministerstwo Rozwoju 2020; data for the first quarter of 2020, in comparison to the third quarter of 2019).

Inspired by the COVID-19 barometer surveys (Deloitte 2020; PwC 2020), our survey consists of several sections, where the central issues were the COVID-19 disruptions. The surveys also addressed the size of the businesses and their age.

The data were collected by the university research agency that supervised the design of the survey and organized the pilot testing of the questionnaire. The survey was distributed online, among 5005 randomly selected household businesses located in Poland. In total, 627 completed surveys were received, but 89 were excluded from the analysis (large firms, with employment over 250 persons). Based on this, we obtained a satisfactory response rate of 12.53%.

In the survey design, we have focused on the selected COVID-19 impacts, guided by the existing COVID-19 monitoring surveys. However, the channels of interruptions that we monitored are also relatively obvious, if we consider the operating activity of any type of the business. The first set of questions addressed the interruptions that were direct in nature. We addressed: limited availability of workers (a natural consequence of the growing number of infections and imposed quarantines) and additional costs (due to the implementation of the required safety measures, e.g., disinfection or the measures of workers’ protection).

Then, we considered issues that refer to financial performance and are induced by the inability to operate due to the lockdown. These covered: disruptions in supply chains and ability to continue production and sales. In our survey we also asked the respondents whether they noted the worsening of financial liquidity or faced some restrictions in the availability of funding. We also included one general question on the perception of the threat of survival (see Table 1).

For each disruptive factor considered in the survey design, the respondents were asked to answer the question “Did the COVID-19 pandemic result in difficulties in the following aspects of the firm’s performance?”. We used a seven-point Likert scale, ranging from 1 (strongly disagree) to 7 (strongly agree).

3.2. Sample Composition: Businesses Characteristics

In Table 2 we provide the sample characteristics–the businesses ownership structure, size and age. Sole proprietorships (SPs) composed 36% of our sample. General partnerships (GPs) comprised 14% of our sample. Limited liability companies (LLCs) accounted for 50% of our sample. Thus, the sample was rather imbalanced if we consider the percentage of firms where the risk is shared among household members (SPs-36%) and businesses where risk-sharing is limited (GPs and LLCs-64%). However, the sample was fully balanced if we consider firms with unlimited legal liability and the related full owner’s financial responsibility (SPs and GPs-50%) and those where this responsibility is isolated (LLCs-50%). Thus, the sample is balanced with respect to the share of risk sharing and risk limiting businesses. The sample structure does not reflect the structure of businesses operating in Poland regarding business legal form. In Poland 78% of businesses are SPs, 8% are GPs and 12% are LLCs (GUS 2021b). However, this is not relevant for the results, as we aim to understand differences between the types of business forms, not to make any conclusions regarding the whole population of businesses operating in Poland. In this context, balance between groups exhibiting differences is more important and this balance has been achieved.

Our sample was relatively balanced if we consider the size of the surveyed businesses. In total, 39% of our sample were small firms (10–49 employees), 34% were micro firms (up to nine employees) and 27% were medium firms (50–249 employees). The sample was also relatively balanced if the age of the surveyed firms is considered. As for firms in their infancy, we classified 16% of respondents. The young firms composed 25% of our sample, whereas the intermediate firms comprised35%. The mature firms (that have operated for more than 21 years) composed 24% of the respondents.

3.3. Method

Our research hypothesis states that the businesses that operate in various legal forms differ in their perceptions of the COVID-19 disruptions. Accordingly, in the empirical analysis we apply the non-parametric ANOVA to verify the statistical significance of the differences in COVID-19 perceptions between the groups (Armstrong and Hilton 2011). In other words, in our empirical study the groups are the businesses of the defined legal form (which we interpret in the context of risk-sharing or risk-limiting among the households that run a business). We employed the non-parametric ANOVA (Kruskal–Wallis test and the related pair-wise comparisons), as the variables obtained in the survey are not normally distributed (see Appendix A, Table A1) and thus cannot be subject to parametric analysis (Armstrong and Hilton 2011; Van Hecke 2012). To support the conclusions we draw, we also performed the analysis of contingencies (Chi-squared test in Appendix A Table A2 and the related contingency ratios). We also refer to descriptive statistics (Appendix A, Table A3), to better highlight the observed differences between the businesses of the legal form of our interests.

4. Results

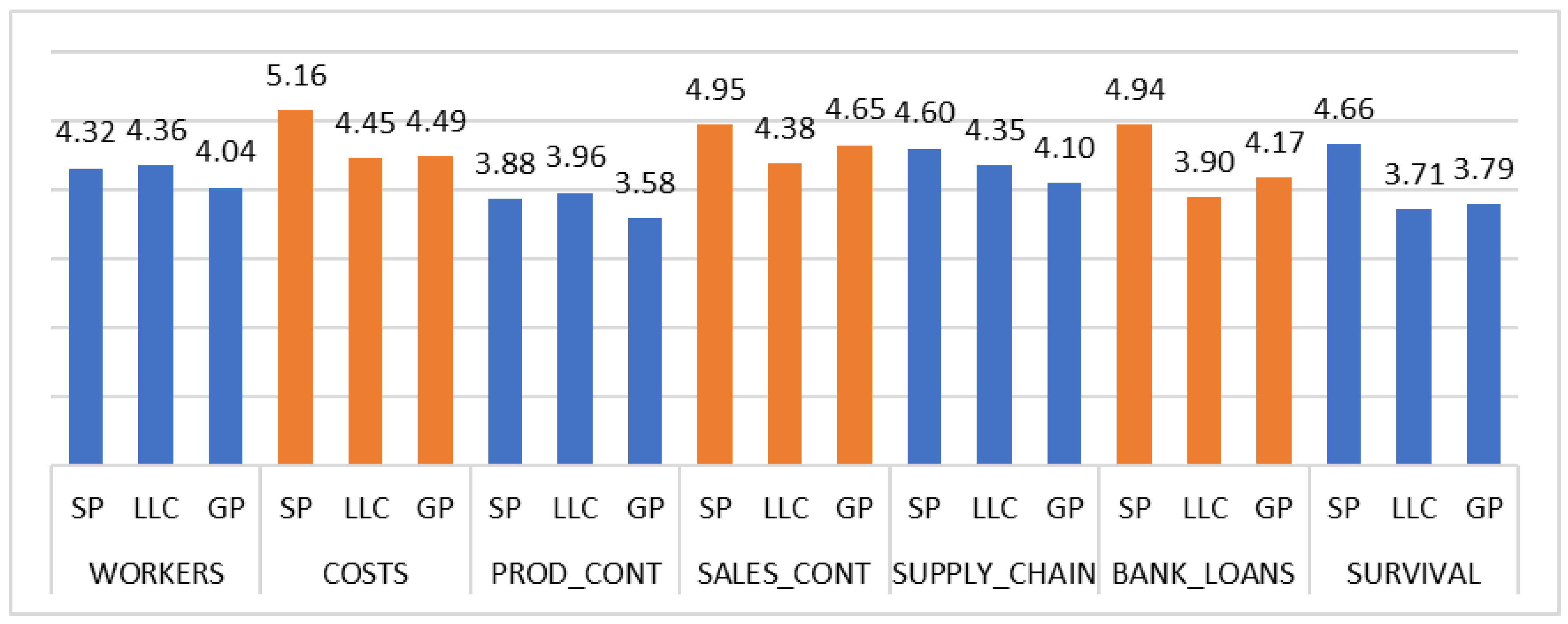

In Figure 1 we present the mean values of the analyzed COVID-19 interruptions by the type of the legal form of the business. As can be seen in Figure 1, in the case of interruptions related to costs, liquidity, bank loans and overall threat of survival, the surveyed SPs assigned visibly higher rates than the remaining types of businesses (LLCs or GPs). This observation is confirmed by the analysis of the contingencies, as the Chi-squared test and the related contingency ratios (Phi, Cramer’s V or contingency ratio) are statistically significant in each case (Table 3).

The results of non-parametric ANOVA indicate an interesting pattern. We find evidence that the businesses operating in particular legal forms differed in their perceptions of the COVID-19 interruptions. These differences were statistically significant in the case of the increase in operating costs, ability to continue sales, worsening of financial liquidity, access to bank loans and the overall threat for the businesses’ survival. All these variables are directly linked to businesses’ financial performance or capital constraints. There are no statistically significant differences for the disruptions in the limited accessibility of workers, continuity of production or the problems to maintain supply chains. This suggests that these interruptive mechanisms have equally influenced households’ firms, regardless of their legal form that approximates risk coping mechanisms adopted by their owners.

In Table 4 we also present the pair-wise comparisons (an element of Kruskal–Wallis test) for these COVID-19 interruptions that we found statistically significant. In other words, we compare which particular legal forms of businesses differ with statistical significance. Data provided in Table 4 clearly indicate that in the case of four channels of interruptions there are significant differences between SPs and other types of business legal forms (GPs and LLCs). Only for the differences in the perceptions of continuity of sales, SPs did not differ at statistically significant level from GPs. The study of the mean ranks of the Kruskal–Wallis test, provided in Table 5, indicates that in each case SPs were perceived as the given type of COVID-19 factor which was more interruptive, in comparison to LLCs or GPs. This confirms the initial observation of mean values of assigned ranks, presented in Figure 1.

We also observed that the mean ranks of the Kruskal–Wallis test for GPs are lower than for SPs, but higher than for LLCs. This means that GPs perceived these interruptions as more problematic than LLCs. However, these differences are not statistically significant, as indicated by the pair-wise comparisons presented in Table 4.

5. Discussion

The results of non-parametric ANOVA focused on businesses’ perception of diverse types COVID-19-related interruptions, allowed us to set up an interesting discussion platform. Our hypothesis stated that COVID-19 interruptions are perceived in different ways by SPs, GPs, and LLCs. This hypothesis finds some support if we consider particular channels of interruptions. SPs, GPs and LLCs differed statistically significantly if we consider their perceptions of the severity of interruptions caused by an increase in costs, continuity of sales, worsening of financial liquidity, accessibility of bank loans and the overall threat to their survival. In the in case of interruptions related to the limited accessibility of workers, ability to continue production and supply chain problems, there were no statistically significant differences between businesses operating in different legal forms. This pattern is very interesting. It indicates that the set of risks for which business legal form seem to be irrelevant and includes risks which need to be managed with physical risk control tools, rather financial risk control tools. In fact, access to financial resources can help manage workers’ availability, possibility to continue production and supply chain disruptions only to a limited extent, especially in terms of COVID-19 specific risks. Paying higher wages will not help to safeguard employees when they need or want to protect their health. Acquiring additional means of production will not allow businesses to continue technological processes when technological lines need to be disinfected often or when workers are absent. Paying higher prices for suppliers will not maintain supply continuity when suppliers cannot operate due to lack of workers or locking down their factories.

On the other hand, a set of risks for which business form appears to be important in shaping business sensitivity to COVID-19, includes risks for which financial buffering is an efficient way of control. Increase in operating costs, as well as disruption of sales, both reduce gross margins and may push a business into illiquidity, unless access to financing allows it to withstand lower or even negative gross margins. Interruptions related to payment of receivables and liquidity, can also be smoothed by financial buffering. Alternative sources of financing (reserves of funds, recapitalization by owners, loans provided by owners or family and friends) are a primary substitute for limited bank loan availability during economic crises. Finally, the overall threat of survival is related to the ability to raise and maintain capital. In other words, we find that some risks are perceived as similar for household businesses, regardless of their legal form. At the same time, some risks are perceived as more or less severe, depending on the legal form of the household business. Thus, these findings show that risk-sharing and risk-limiting mechanisms are relevant in managing only those risks that can be easily financially buffered. For other types of risks related to COVID-19, other mechanisms of risk management might be necessary. This requires further research focused on other properties of households running businesses.

The mean ranks of the Kruskal–Wallis test show that channels of interruptions have an unequal impact on businesses operating in different legal forms. Our results revealed that partnerships perceive the majority of these disruptions as less severe than sole proprietorships (which strongly supports our hypothesis). It means that risk-sharing is an efficient mechanism for managing a set of COVID-19-related risks by households running a business. This finding has important theoretical and practical implications. Theoretical implications are primarily related to whether and how social ties and close networking complement the financial market. Our results confirm that risk-sharing between households efficiently reduces business perception of risks related to exogenous shock accompanied by a tightening of credit supply. Thus, our results are in line with studies pointing to the important role of informal risk-sharing mechanisms acting as complementary mechanisms to financial services (Fafchamps and Lund 2003; Yang and Choi 2007; Jack and Suri 2014; Asdrubali et al. 2020). The theoretical implication of this finding is related to the capacity of social networks to reduce inefficiencies in the financial market. One clue for a more detailed understanding of our results can be that small businesses are perceived by banks as riskier and more informational opaque (asymmetry of information issue) (Dierkes et al. 2013). This asymmetry has been exacerbated in times of the COVID-19 pandemic and is perceived as a primary reason for “flight to safety” by banks (Corbet et al. 2020; Krukowski and DeTienne 2021; Kay 2021). Lin et al. (2009) report that stronger social ties, where social and economic relations intertwine with each other, alleviate the information asymmetry between borrowers and lenders. Following these notions, our results support that informal risk financing mechanisms and the related better access to financing by businesses which operate within strong social networks may do so by outpacing formal-ones, while resolving the asymmetry of information during COVID-19. This effect should be examined in-depth with further qualitative studies. Our results are also in line with a broader stream of research that suggests that social ties and social networks are increasingly becoming the basis of business processes (Burchardi and Hassan 2013; Carter et al. 2007; Neumeyer and Santos 2018; Dost et al. 2019).

Our results also revealed that LLCs perceive the majority of these disruptions as less severe than GPs and SPs (which provides strong support for our hypothesis). This suggests that risk-limiting is a mechanism that allows one to efficiently lower concerns over COVID-19-related interruptions. This finding has an important practical implication. Many households setting up a business have chosen SP or GP as their legal form due to the simplicity of management and the lack of capital requirements for running the business in these legal forms. Our results argue that these households should be better informed about the value of risk-limiting available under LLCs and educated about the cases where the risk-limiting options outweigh the benefits of simplicity and lack of capital requirements.

Another important theoretical implication of our study stems from revealing that different types of risk management mechanisms are of different importance for reducing business risk perception in front of diverse threats. In the case of disruptions related to costs, liquidity, bank loans availability and overall threat of survival, risk sharing helps to reduce respondents’ concerns, while risk limiting does not. We also found that risk-limiting is a valuable option for venturesome households in the case of managing risks related to continuity of sales (partial support for the hypothesis). This conclusion is driven by the observation that LLCs perceived their anxieties about continuity of sales as significantly lower than both SPs and GPs. This could be driven by the long-term effects of interruptions on continuity of sales. For a business, it takes more time and effort to rebuild one’s market position compared to finding additional sources of financing in order to protect against illiquidity, increase of costs and tightening of bank loan supply (and thus market risk is considered as strategic risk, as pointed by (Rowland et al. 2019)). In fact, market risk is perceived as posing a greater threat to small and medium size businesses, in comparison to financial risk (Kozubíková et al. 2015). Thus, putting a cap on this type of risk seems to be a desirable option for households owning a business venture. This suggests that risk limiting is better suited to manage the long-term risk of survival, while risk sharing is better suited to manage the short-term risk of survival.

Our results have important policy and managerial implications. Policy implications are related to supporting business networking, which requires consistent funding, as well as legal, technical and informational support. Managerial implications comprise implications for business owners and for banks. We show that business owners may tangibly benefit from entering into partnerships with other businesspeople, by strengthening their resilience in times of major disruptions. We also show that in the case of strategic market risk, the possibility to limit the risk brings significant value to businesses. The implication for banks is that for bank managers, a viable option could be to account for a type of business legal form in the process of evaluation of a firm’s credibility (as we observed that the business legal form determines the level of vulnerability to exogenous shocks).

Our study has several limitations. First of all, as this is based on survey results, it could result in a subjective bias. Further research on the vulnerability to COVID-19 shock of the businesses run by the households may shed some light on the results provided in this study. The second limitation stems from the timeline of the study. The survey was conducted January-February, 2021 while in the following year the situation evolved. The economy, which had already been weakened by the earlier waves of COVID-19, had to deal with the next stages of the turmoil in the markets. At the same time, a number of solutions supporting business processes in pandemic conditions were implemented. This could be influential on their perception of risk. Thus, by repeating the survey, the problem could be understood more comprehensively. Another limitation is the set of COVID-19 disruptions considered in this study. It has limited the abilities to study households’ risk-perception comprehensively, as only some specific risks have been considered (the business perspective). Thus, further inquiries should be placed to study the effect of business legal form on the perception of other types of risks (e.g., natural catastrophes) by households running a business.

6. Conclusions

Fear of the future is amongst the most important reasons why entrepreneurs do not engage in business (Cacciotti et al. 2016). This study was designed to report how the choice of business legal form affects perceptions of COVID-19-related interruptions among households running a business. This work adds primarily to the literature on household risk coping mechanisms, by revising the perceptions of COVID-19 disruptions among households running their own business in forms which vary with respect to available risk coping mechanisms. Based on the survey results on small- and medium-sized businesses operating in Poland, we provide strong evidence that COVID-19 was perceived as more disruptive by sole proprietorships than by partnerships, including general partnerships and limited liability companies. There were no significant differences between general partnerships and limited liability companies in their perception of the majority of interruptions related to COVID-19 except from interruptions related to continuity of sales. Partnerships allow for intra-household risk sharing, while only limited liability companies allow for risk limiting. Thus, our results support that intra-household risk-sharing mechanisms (as a way to cope with a shock) appear to be more important in safeguarding households running businesses in times of pandemic, than formal mechanisms of reducing the liability of individuals running a business. We conclude that strengthening social and business ties between entrepreneurs can efficiently mitigate the perception of the number of risks related to exogenous shock. We also showed that in the case of strategic market risk, the possibility to limit the risk brings significant value to the household businesses. Effective risk management by household businesses is critical for their ability to survive, as well as to generate income for households. This mechanism contributes to the development of a business itself, and at the same time to its social and market environment. In this respect, our study has a number of important practical and theoretical implications.

Author Contributions

Conceptualization, A.D. and M.W.-K.; methodology, M.W.-K.; software, M.W.-K.; validation, M.W.-K.; formal analysis, M.W.-K.; investigation, A.D. and J.B.; resources, M.W.-K.; data curation, M.W.-K.; writing—original draft preparation, A.D., J.B. and M.W.-K.; writing—review and editing, M.W.-K. and J.B.; visualization, M.W.-K.; supervision, M.W.-K.; project administration, M.W.-K. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data available on request due to privacy restrictions.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

Tests of normality distribution.

| Kolmogorov–Smirnov | Shapiro–Wilk | |||||

|---|---|---|---|---|---|---|

| Statistic | df | Sig. | Staitistc. | df | Istotność | |

| WORKERS | 0.192 | 538 | 0.000 | 0.917 | 538 | 0.000 |

| COSTS | 0.194 | 538 | 0.000 | 0.905 | 538 | 0.000 |

| PROD_CONT | 0.152 | 538 | 0.000 | 0.920 | 538 | 0.000 |

| SALES_CONT | 0.177 | 538 | 0.000 | 0.905 | 538 | 0.000 |

| SUPPLY CHAIN | 0.189 | 538 | 0.000 | 0.920 | 538 | 0.000 |

| LIQUIDITY | 0.167 | 538 | 0.000 | 0.925 | 538 | 0.000 |

| BANK LOANS | 0.168 | 538 | 0.000 | 0.936 | 538 | 0.000 |

| SURVIVAL | 0.193 | 538 | 0.000 | 0.929 | 538 | 0.000 |

Table A2.

The distribution of answers for COVID-19 interruptions by the type of the form of legal businesses (number of responses).

Table A2.

The distribution of answers for COVID-19 interruptions by the type of the form of legal businesses (number of responses).

| COVID-19 Interruptions | Legal Form of Business | Strongly Disagree | Disagree | Somewhat Disagree | Neither Agree Nor Disagree | Somewhat Agree | Agree | Strongly Agree | In Total |

|---|---|---|---|---|---|---|---|---|---|

| WORKERS | SP | 11 | 22 | 35 | 27 | 52 | 22 | 26 | 195 |

| LLC | 11 | 49 | 43 | 8 | 56 | 82 | 17 | 266 | |

| GP | 3 | 16 | 17 | 7 | 13 | 15 | 6 | 77 | |

| In total | 25 | 87 | 95 | 42 | 121 | 119 | 49 | 538 | |

| COSTS | SP | 3 | 15 | 27 | 9 | 42 | 47 | 52 | 195 |

| LLC | 0 | 41 | 53 | 21 | 69 | 59 | 23 | 266 | |

| GP | 3 | 9 | 15 | 5 | 16 | 23 | 6 | 77 | |

| In total | 6 | 65 | 95 | 35 | 127 | 129 | 81 | 538 | |

| PROD_CONT | SP | 37 | 21 | 28 | 28 | 31 | 24 | 26 | 195 |

| LLC | 14 | 60 | 50 | 24 | 48 | 56 | 14 | 266 | |

| GP | 11 | 22 | 12 | 2 | 11 | 11 | 8 | 77 | |

| In total | 62 | 103 | 90 | 54 | 90 | 91 | 48 | 538 | |

| SALES_CONT | SP | 11 | 16 | 23 | 14 | 41 | 37 | 53 | 195 |

| LLC | 3 | 47 | 60 | 19 | 42 | 63 | 32 | 266 | |

| GP | 2 | 10 | 12 | 9 | 13 | 18 | 13 | 77 | |

| In total | 16 | 73 | 95 | 42 | 96 | 118 | 98 | 538 | |

| SUPPLY CHAIN | SP | 8 | 16 | 37 | 23 | 46 | 31 | 34 | 195 |

| LLC | 2 | 38 | 72 | 15 | 58 | 53 | 28 | 266 | |

| GP | 3 | 11 | 24 | 5 | 9 | 21 | 4 | 77 | |

| In total | 13 | 65 | 133 | 43 | 113 | 105 | 66 | 538 | |

| LIQUIDITY | SP | 5 | 13 | 35 | 24 | 30 | 34 | 54 | 195 |

| LLC | 6 | 60 | 59 | 35 | 56 | 35 | 15 | 266 | |

| GP | 2 | 9 | 21 | 11 | 15 | 14 | 5 | 77 | |

| In total | 13 | 82 | 115 | 70 | 101 | 83 | 74 | 538 | |

| BANK LOANS | SP | 6 | 21 | 23 | 82 | 29 | 22 | 12 | 195 |

| LLC | 7 | 72 | 70 | 64 | 33 | 13 | 7 | 266 | |

| GP | 3 | 16 | 13 | 28 | 12 | 5 | 0 | 77 | |

| In total | 16 | 109 | 106 | 174 | 74 | 40 | 19 | 538 | |

| SURVIVAL | SP | 6 | 15 | 39 | 22 | 44 | 36 | 33 | 195 |

| LLC | 4 | 58 | 83 | 38 | 42 | 30 | 11 | 266 | |

| GP | 4 | 14 | 19 | 10 | 19 | 9 | 2 | 77 | |

| In total | 14 | 87 | 141 | 70 | 105 | 75 | 46 | 538 |

Table A3.

Descriptive statistics of the COVID-19 interruptions by the type of the legal form of the business.

Table A3.

Descriptive statistics of the COVID-19 interruptions by the type of the legal form of the business.

| SP | LCC | GP | ||||

|---|---|---|---|---|---|---|

| Mean | St.Dev. | Mean | St.Dev. | Mean | St.Dev. | |

| WORKERS | 4.318 | 1.724 | 4.365 | 1.780 | 4.039 | 1.758 |

| COSTS | 5.159 | 1.684 | 4.455 | 1.595 | 4.494 | 1.706 |

| PROD_CONT | 3.877 | 2.035 | 3.962 | 1.752 | 3.584 | 2.028 |

| SALES_CONT | 4.954 | 1.865 | 4.380 | 1.758 | 4.649 | 1.775 |

| SUPPLY CHAIN | 4.600 | 1.727 | 4.353 | 1.661 | 4.104 | 1.714 |

| LIQUIDITY | 4.944 | 1.774 | 3.902 | 1.604 | 4.169 | 1.576 |

| BANK LOANS | 4.133 | 1.404 | 3.417 | 1.344 | 3.584 | 1.271 |

| SURVIVAL | 4.656 | 1.690 | 3.714 | 1.492 | 3.792 | 1.542 |

References

- Abeler, Johannes, Armin Falk, Lorenz Goette, and David Huffman. 2011. Reference points and effort provision. American Economic Review 101: 470–92. [Google Scholar] [CrossRef] [Green Version]

- Agarwal, Reena, and Andrew W. Horowitz. 2002. Are international remittances altruism or insurance? Evidence from Guyana using multiple-migrant households. World Development 30: 2033–44. [Google Scholar] [CrossRef]

- Albacete, Nicolas, Pirmin Fessler, Fabian Kalleitner, and Peter Lindner. 2021. How has COVID-19 affected the financial situation of households in Austria? Monetary Policy and the Economy Q 4: 111–30. [Google Scholar]

- Alderman, Harold, Pierre-Andre Chiappori, Lawrence Haddad, John Hoddinott, and Ravi Kanbur. 1995. Unitary versus collective models of the household: Is it time to shift the burden of proof? The World Bank Research Observer 10: 1–19. [Google Scholar] [CrossRef]

- Alinovi, Luca, Erdgin Mane, and Donato Romano. 2009. Measuring Household Resilience to Food Insecurity: Application to Palestinian Households. Rome: EC-FAO Food Security Programme Rom, pp. 1–39. [Google Scholar]

- Armantier, Oliver, Gizem Koşar, Rachel Pomerantz, Daphne Skandalis, Kyle Smith, Giorgio Topa, and Wilbert Van der Klaauw. 2020. Coronavirus Outbreak Sends Consumer Expectations Plummeting. (No. 20200406b). New York: Federal Reserve Bank of New York. [Google Scholar]

- Armstrong, Richard A., and Anthony C. Hilton. 2011. Statistical Analysis in Microbiology: Statnotes. Hoboken: Wiley-Blackwell. [Google Scholar]

- Asdrubali, Pierfederico, Simone Tedeschi, and Luigi Ventura. 2020. Household risk-sharing channels. Quantitative Economics 11: 1109–42. [Google Scholar] [CrossRef]

- Attanasio, Orazio, Abigail Barr, Juan Camilo Cardenas, Garance Genicot, and Costas Meghir. 2012. Risk pooling, risk preferences, and social networks. American Economic Journal: Applied Economics 4: 134–67. [Google Scholar] [CrossRef] [Green Version]

- Ayala, Juan-Carlos, and Guadalupe Manzano. 2014. The resilience of the entrepreneur. Influence on the success of the business. A longitudinal analysis. Journal of Economic Psychology 42: 126–35. [Google Scholar] [CrossRef]

- Baker, Scott R., Robert A. Farrokhnia, Steffen Meyer, Michaela Pagel, and Constantine Yannelis. 2020. How does household spending respond to an epidemic? Consumption during the 2020 COVID-19 pandemic. The Review of Asset Pricing Studies 10: 834–62. [Google Scholar] [CrossRef]

- Barrafrem, Kinga, Daniel Västfjäll, and Gustav Tinghög. 2020. Financial well-being, COVID-19, and the financial better-than-average-effect. Journal of Behavioral and Experimental Finance 28: 100410. [Google Scholar] [CrossRef]

- Becker, Gary. 1965. A theory of the allocation of time. Economic Journal 75: 493–517. [Google Scholar] [CrossRef] [Green Version]

- Block, Joen H., Christian Fisch, and Mirko Hirschmann. 2021. The determinants of bootstrap financing in crises: Evidence from entrepreneurial ventures in the COVID-19 pandemic. Small Business Economics 58: 867–85. [Google Scholar] [CrossRef]

- Bourlès, Renaud, Yann Bramoullé, and Eduardo Perez-Richet. 2021. Altruism and risk sharing in networks. Journal of the European Economic Association 19: 1488–521. [Google Scholar] [CrossRef]

- Brewer, Mike, and Laura Gardiner. 2020. The initial impact of COVID-19 and policy responses on household incomes. Oxford Review of Economic Policy 36: S187–99. [Google Scholar] [CrossRef]

- Bullough, Amanda, and Maija Renko. 2013. Entrepreneurial resilience during challenging times. Business Horizons 56: 343–50. [Google Scholar] [CrossRef]

- Bullough, Amanda, Maija Renko, and Tamara Myatt. 2014. Danger zone entrepreneurs: The importance of resilience anmandad self–efficacy for entrepreneurial intentions. Entrepreneurship Theory and Practice 38: 473–99. [Google Scholar] [CrossRef]

- Burchardi, Konrad B., and Tarek A. Hassan. 2013. The economic impact of social ties: Evidence from German reunification. The Quarterly Journal of Economics 128: 1219–71. [Google Scholar] [CrossRef] [Green Version]

- Cacciotti, Gabriella, James C. Hayton, J. Robert Mitchell, and Andres Giazitzoglu. 2016. A reconceptualization of fear of failure in entrepreneurship. Journal of Business Venturing 31: 302–25. [Google Scholar] [CrossRef] [Green Version]

- Carlson, Stacy, Ms Era Dabla-Norris, Mika Saito, and Yu Shi. 2015. Household Financial Access and Risk Sharing in Nigeria. Washington, DC: International Monetary Fund. [Google Scholar]

- Carter, Craig R., Lisa M. Ellram, and Wendy Tate. 2007. The use of social network analysis in logistics research. Journal of Business Logistics 28: 137–68. [Google Scholar] [CrossRef]

- Chiappori, Pierre-Andre A., and Arthur Lewbel. 2015. Gary Becker’s a theory of the allocation of time. The Economic Journal 125: 410–42. [Google Scholar] [CrossRef] [Green Version]

- Chronopoulos, Dimitris K., Marcel Lukas, and John O. Wilson. 2020. Consumer Spending Responses to the COVID-19 Pandemic: An Assessment of Great Britain. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3586723 (accessed on 10 December 2021).

- Corbet, Shaen, Yang Hou, Yang Hu, and Les Oxley. 2020. The influence of the COVID-19 pandemic on asset-price discovery: Testing the case of Chinese informational asymmetry. International Review of Financial Analysis 72: 101560. [Google Scholar] [CrossRef]

- Crawford, Vincent P., and Juanjuan Meng. 2011. New York city cab drivers’ labor supply revisited: Reference-dependent preferences with rational-expectations targets for hours and income. American Economic Review 101: 1912–32. [Google Scholar] [CrossRef] [Green Version]

- Davis, H. James, Kameda Tatsuya, and Stasson Mark. 1992. Group Risk Taking: Selected Topics. In Risk-Taking Behavior. Edited by Frank Yates. Chichester: Wiley, pp. 163–99. [Google Scholar]

- Deloitte. 2020. Deloitte Global Cost and Enterprise Transformation Survey. Available online: https://www2.deloitte.com/us/en/pages/about-deloitte/articles/press-releases/deloitte-covid-19-survey-shifts-cost-strategies.html (accessed on 5 October 2020).

- De Weerdt, Joachim, and Stefan Dercon. 2006. Risk-sharing networks and insurance against illness. Journal of Development Economics 81: 337–56. [Google Scholar] [CrossRef] [Green Version]

- Demertzis, Maria, Marta Domínguez-Jiménez, and Annamaria Lusardi. 2020. The Financial Fragility of European Households in the Time of COVID-19. Brussels: Bruegel. [Google Scholar]

- Dierkes, Maik, Carsten Erner, Thomas Langer, and Lars Norden. 2013. Business credit information sharing and default risk of private firms. Journal of Banking and Finance 37: 2867–78. [Google Scholar] [CrossRef]

- Dost, Florian, Ulrike Phieler, Michael Haenlein, and Barak Libai. 2019. Seeding as part of the marketing mix: Word-of-mouth program interactions for fast-moving consumer goods. Journal of Marketing 83: 62–81. [Google Scholar] [CrossRef]

- European Commission. 2019. 219 SBA Fact Sheet Poland. Available online: https://ec.europa.eu/docsroom/documents/38662/attachments/22/translations/en/renditions/native (accessed on 1 July 2021).

- Evans, Alison. 1991. Evans, Alison. 1991. Gender issues in rural household economics. ids Bulletin 22: 51–59. [Google Scholar] [CrossRef] [Green Version]

- Fafchamps, Marcel, and Susan Lund. 2003. Risk-sharing networks in rural Philippines. Journal of Development Economics 71: 261–87. [Google Scholar]

- Fafchamps, Marcel. 2011. Risk Sharing between Households. Handbook of Social Economics 1: 1255–79. [Google Scholar]

- Gertler, Paul, and Jonathan Gruber. 2002. Insuring consumption against illness. American Economic Review 92: 51–70. [Google Scholar]

- Guerini, Mattia, Nesta Lionel, Xavier Ragot, and Stefano Schiavo. 2020. Firm liquidity and solvency under the Covid-19 lockdown in France. OFCE Policy Brief 76: 1–20. [Google Scholar]

- GUS. 2021a. Information Regarding the Labour Market in the Second Quarter of 2021. Warsaw: GUS. [Google Scholar]

- GUS. 2021b. Informacja o Podmiotach Gospodarki Narodowej Wpisanych do Rejestru REGON-Styczeń 2021. Warsaw: GUS. [Google Scholar]

- Haan, Peter, and Prowse Victoria. 2017. Optimal Social Assistance and Umemployment Insurance in a Life-Cycle Model of Family Labor Supply and Savings. In Purdue University Economics Working Papers 1294. West Lafayette: Department of Economics, Purdue University. [Google Scholar]

- Hallegatte, Stephane. 2014. Economic resilience: Definition and measurement. In World Bank Policy Research Working Paper (6852). Washington, DC: World Bank. [Google Scholar]

- Hanspal, Tobin, Annika Weber, and Johannes Wohlfart. 2020a. Exposure to the COVID-19 stock market crash and its effect on household expectations. The Review of Economics and Statistics 103: 994–1010. [Google Scholar]

- Hanspal, Tobin, Annika Weber, and Johannes Wohlfart. 2020b. Income and Wealth Shocks and Expectations during the COVID-19 Pandemic. (No. 8244). CESifo Working Paper. Munich: Center for Economic Studies and ifo Institute (CESifo). [Google Scholar]

- Harhoff, Dietmar, Konrad Stahl, and Michael Woywode. 1998. Legal form, growth and exit of West German firms—empirical results for manufacturing, construction, trade and service industries. The Journal of Industrial Economics 46: 453–88. [Google Scholar] [CrossRef]

- Van Hecke, Tanja. 2012. Power study of anova versus Kruskal-Wallis test. Journal of Statistics and Management Systems 15: 241–47. [Google Scholar] [CrossRef]

- Horvath, Akos, Benjamin S. Kay, and Carlo Wix. 2021. The COVID-19 Shock and Consumer Credit: Evidence from Credit Card Data. Available at SSRN 3613408. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3613408 (accessed on 15 November 2021).

- Hurst, Erik, and Annamaria Lusardi. 2004. Liquidity constraints, household wealth, and entrepreneurship. Journal of Political Economy 112: 319–47. [Google Scholar] [CrossRef] [Green Version]

- Jack, William, and Tawneet Suri. 2014. Risk sharing and transactions costs: Evidence from Kenya’s mobile money revolution. American Economic Review 104: 183–223. [Google Scholar] [CrossRef]

- Kansiime, Monika K., Justice A. Tambo, Idah Mugambi, Mary Bundi, Augustine Kara, and Charles Owuor. 2021. COVID-19 implications on household income and food security in Kenya and Uganda: Findings from a rapid assessment. World Development 137: 105199. [Google Scholar] [CrossRef]

- Kay, Benjamin S. 2021. The COVID-19 Shock and Consumer Credit: Evidence from Credit Card Data; (No. 2021-008). Washington, DC: Board of Governors of the Federal Reserve System (US).

- Korosteleva, Julia, and Paulina Stępień-Baig. 2020. Climbing the poverty ladder: The role of entrepreneurship and gender in alleviating poverty in transition economies. Entrepreneurship and Regional Development 32: 197–220. [Google Scholar] [CrossRef]

- Kozubíková, Ludmila, Jaroslav Belás, Yuriy Bilan, and Premysl Bartoš. 2015. Personal characteristics of entrepreneurs in the context of perception and management of business risk in the SME segment. Economics and Sociology 8: 41–54. [Google Scholar] [CrossRef]

- Krueger, Dirk. 1999. Risk Sharing in Economies with Incomplete Markets. Ph.D. thesis, University of Minnesota, Minneapolis, MS, USA. [Google Scholar]

- Krukowski, Kipp A., and Dawn R. DeTienne. 2021. Selling a business after the pandemic? Crisis and information asymmetry impact on deal terms. Business Horizons, in press. [Google Scholar]

- Łasak, Piotr. 2020. Wyzwania dla polskiego sektora bankowego jako skutek pandemii COVID-19. In Polityka Gospodarcza w Niestabilnym Otoczeniu–Dylematy i Wyzwania. Toruń: Wyższa Szkoła Kultury Społecznej i Medialnej, pp. 80–93. [Google Scholar]

- Lee, Soon J., Soon I. Kwon, and Seok Y. Chung. 2010. Determinants of household demand for insurance: The case of Korea. The Geneva Papers on Risk and Insurance-Issues and Practice 35: S82–S91. [Google Scholar] [CrossRef] [Green Version]

- Li, Jie, Quanlun Song, Changyan Peng, and Yu Wu. 2020. COVID-19 pandemic and household liquidity constraints: Evidence from micro data. Emerging Markets Finance and Trade 56: 3626–34. [Google Scholar] [CrossRef]

- Lin, Mingfeng, Nagpurnanand R. Prabhala, and Siva Viswanathan. 2009. Can Social Networks Help Mitigate Information Asymmetry in Online Markets? ICIS 2009 Proceedings. p. 202. Available online: https://aisel.aisnet.org/icis2009/202 (accessed on 20 November 2021).

- Mankart, Jochen, and Rigas Oikonomou. 2017. Household search and the aggregate labour market. The Review of Economic Studies 84: 1735–88. [Google Scholar] [CrossRef]

- Marsh, Dorota, and Pete Thomas. 2017. The Governance of Welfare and the Expropriation of the Common: Polish Tales of Entrepreneurship. In Critical Perspectives on Entrepreneurship. London: Routledge, pp. 225–44. [Google Scholar]

- Martin, Amory, Maryia Markhvida, Stéphane Hallegatte, and Brian Walsh. 2020. Socio-economic impacts of COVID-19 on household consumption and poverty. Economics of Disasters And Climate Change 4: 453–79. [Google Scholar] [CrossRef]

- Midões, Catarina, and Mateo Seré. 2021. Living with Reduced Income: An Analysis of Household Financial Vulnerability under COVID-19. Social Indicators Research 8: 1–25. [Google Scholar] [CrossRef]

- Ministerstwo Rozwoju. 2020. Podstawowe Wskaźniki Makroekonomiczne, Polska, Wrzesień 2020. Available online: https://www.gov.pl/attachment/bc0e9744-1fdf-475c-a137-d141df473769 (accessed on 1 July 2021).

- Munshi, Kaivan. 2003. Networks in the modern economy: Mexican migrants in the US labor market. The Quarterly Journal of Economics 118: 549–99. [Google Scholar] [CrossRef] [Green Version]

- Neumeyer, Xaver, and Susana C. Santos. 2018. Sustainable business models, venture typologies, and entrepreneurial ecosystems: A social network perspective. Journal of Cleaner Production 172: 4565–79. [Google Scholar] [CrossRef]

- Paci, Pirella, Marcin J. Sasin, and Jos Verbeek. 2004. Economic growth, income distribution, and poverty in Poland during transition. In Policy Research Working Paper. No. 3467. Washington, DC: World Bank. [Google Scholar]

- PwC. 2020. PwC Global COVID-19 CFO Pulse Report. June. Available online: https://www.pwc.com/gx/en/issues/crisis-solutions/covid-19/global-cfo-pulse.html (accessed on 2 October 2020).

- Rowland, Zuzana, Veronika Machova, Jakub Horak, and Jan Hejda. 2019. Determining the market value of the enterprise using the modified method of capitalized net incomes and Metfessel allocation of input data. AD ALTA: Journal of Interdisciplinary Research 9: 305–10. [Google Scholar]

- Schneider, Daniel, Peter Tufano, and Annamaria Lusardi. 2020. Household Financial Fragility during COVID-19: Rising Inequality and Unemployment Insurance Benefit Reductions. GFLEC WP, 4. Available online: https://www.sbs.ox.ac.uk/sites/default/files/2020-10/finfrag_workingpaper_103020%20%281%29.pdf (accessed on 18 December 2021).

- Shen, Huayu, Mengyao Fu, Hongyu Pan, Zhongfu Yu, and Yongquan Chen. 2020. The impact of the COVID-19 pandemic on firm performance. Emerging Markets Finance and Trade 56: 2213–30. [Google Scholar] [CrossRef]

- Smallbone, David, David Deakins, and Martina Battisti. 2012. Small business responses to a major economic downturn: Empirical perspectives from New Zealand and the United Kingdom. International Small Business Journal 30: 754–77. [Google Scholar] [CrossRef]

- Smith, Lisa C., and Timothy R. Frankenberger. 2018. Does resilience capacity reduce the negative impact of shocks on household food security? Evidence from the 2014 floods in Northern Bangladesh. World Development 102: 358–76. [Google Scholar] [CrossRef]

- Tan, Jin, Li Peng, and Shili Guo. 2020. Measuring Household Resilience in Hazard-Prone Mountain Areas: A Capacity-Based Approach. Social Indicators Research 152: 1153–76. [Google Scholar] [CrossRef]

- Tchamyou, Vanessa S. 2019. The role of information sharing in modulating the effect of financial access on inequality. Journal of African Business 20: 317–38. [Google Scholar] [CrossRef] [Green Version]

- Thomas, Duncan. 1990. Intra-household resource allocation: An inferential approach. Journal of Human Resources 25: 635–64. [Google Scholar] [CrossRef]

- TMF Group. 2021. Global Business Complexity Index 2021. Available online: https://www.tmf-group.com/en/news-insights/publications/2021/global-business-complexity-index/ (accessed on 20 November 2021).

- Wang, Haomin. 2019. Intra-household risk sharing and job search over the business cycle. Review of Economic Dynamics 34: 165–82. [Google Scholar] [CrossRef] [Green Version]

- Winnicka-Popczyk, Alicja. 2014. Finansowe uwarunkowania wyboru formy prawnej biznesu w firmach rodzinnych. Przedsiębiorczość i Zarządzanie 15: 249–59. [Google Scholar]

- Yang, Dean, and Hwajung Choi. 2007. Are remittances insurance? Evidence from rainfall shocks in the Philippines. The World Bank Economic Review 21: 219–48. [Google Scholar] [CrossRef]

- Yue, Pengpeng, Aslihang G. Korkmaz, Zhichao Yin, and Haigang Zhou. 2021. Household-owned Businesses’ Vulnerability to the COVID-19 Pandemic. Emerging Markets Finance and Trade 57: 1662–74. [Google Scholar] [CrossRef]

- Yue, Pengpeng, Aslihang Gizem Korkmaz, and Haigang Zhou. 2020. Household financial decision making amidst the COVID-19 pandemic. Emerging Markets Finance and Trade 56: 2363–77. [Google Scholar] [CrossRef]

- Zhang, Huanhuan, Gang Kou, and Yi Peng. 2019. Soft consensus cost models for group decision making and economic interpretations. European Journal of Operational Research 277: 964–80. [Google Scholar] [CrossRef]

Figure 1.

Comparison of means of the COVID-19 impacts by the legal form of the business.

Table 1.

Survey design: questions on COVID-19 interruptions.

| Level of Analysis | Variables | Question |

|---|---|---|

| Did the COVID-19 Pandemic Result in Difficulties in the Following Aspects of Firm’s Performance: | ||

| Operating risk factors | WORKERS | limited accessibility of workers |

| COSTS | additional costs of the implementation of required safety measures | |

| PROD_CONT | inability to continue production | |

| SALES_CONT | inability to continue sales | |

| SUPPLY CHAIN | delayed delivery of production components/materials etc., or produced goods to the customers | |

| Financial risk factors | LIQUIDITY | worsening of financial liquidity |

| BANK LOANS | limited accessibility of bank loans | |

| SURVIVAL | the overall impact of COVID-19 threatened the survival of our company |

Notes: COVID-19 interruptions were evaluated by respondents using a the seven-point Likert scale: 1—strongly disagree, 2—disagree, 3—somewhat disagree, 4—neither agree nor disagree, 5–somewhat agree, 6—agree, 7—strongly agree. Cronbach’s Alpha 0.865.

Table 2.

Sample composition and variables that explain the businesses characteristics relevant for this study.

Table 2.

Sample composition and variables that explain the businesses characteristics relevant for this study.

| Variable | N | % | |

|---|---|---|---|

| OWN_2 (owners’ responsibility, three categories) | |||

| LLC | limited, perform as limited liability companies | 195 | 36.2 |

| SP | unlimited, perform as sole proprietorship | 266 | 49.4 |

| GP | unlimited, perform as general partnerships | 77 | 14.3 |

| total | 538 | 100 | |

| SIZE (by the number of employees) | |||

| micro | up to 9 persons | 182 | 33.8 |

| small | 10–49 persons | 208 | 38.7 |

| medium | 50–249 persons | 148 | 27.5 |

| total | 538 | 100 | |

| AGE_1 (by the years of performance, four categories of business’ age) | |||

| infant | (up to 5 years) | 86 | 16.0 |

| young | (6–10 years) | 137 | 25.5 |

| intermediate | (11–20 years) | 187 | 34.8 |

| mature | (21 years or more) | 128 | 23.8 |

| total | 538 | 100 | |

Table 3.

Contingencies between the legal form of the business and the COVID-19 interruptions (Chi-squared test).

Table 3.

Contingencies between the legal form of the business and the COVID-19 interruptions (Chi-squared test).

| WORK | COSTS | PROD _CONT | SALES _CONT | SUPPLY CHAIN | LIQUIDITY | BANK LOANS | SURVIVAL | |

|---|---|---|---|---|---|---|---|---|

| Chi-squared statistic | 52.375 *** | 48.685 *** | 55.344 *** | 41.794 *** | 35.558 *** | 68.974 *** | 53.349 *** | 57.328 *** |

| Phi | 0.312 *** | 0.301 *** | 0.321 *** | 0.279 *** | 0.257 *** | 0.358 *** | 0.315 *** | 0.326 *** |

| Cramer’s V | 0.221 *** | 0.213 *** | 0.227 *** | 0.197 *** | 0.182 *** | 0.253 *** | 0.223 *** | 0.231 *** |

| Contingency ratio | 0.298 *** | 0.288 *** | 0.305 *** | 0.268 *** | 0.249 *** | 0.337 *** | 0.300 *** | 0.310 *** |

Notes: statistically significant at: *** α = 0.001.

Table 4.

Results of non-parametric ANOVA–the differences in COVID-19 risk perceptions between the business of different legal forms.

Table 4.

Results of non-parametric ANOVA–the differences in COVID-19 risk perceptions between the business of different legal forms.

| Variables | WORK | COSTS | PROD _CONT | SALES _CONT | SUPPLY CHAIN | LIQUIDITY | BANK LOANS | SURVIVAL |

|---|---|---|---|---|---|---|---|---|

| Kruskal–Wallis statistics | 2.224 | 24.623 *** | 2.646 | 12.629 ** | 5.137 | 41.779 *** | 32.177 *** | 39.205 *** |

| pair-vise comparisons | ||||||||

| LLC-GP | −7.866 | −23.017 | −24.993 | −26.159 | −9.715 | |||

| LLC-SP | 69.405 *** | 51.261 *** | 92.732 *** | 81.334 *** | 87.661 *** | |||

| GP-SP | 61.539 ** | 28.244 | 67.738 ** | 55.175 ** | 77.945 *** |

Notes: LLC–limited liability company, GP–general partnership, SP–sole proprietors; statistically significant at: *** α = 0.001; ** α = 0.05. Sample N = 538.

Table 5.

Mean ranks of the Kruskal–Wallis test.

| Legal Form of Business | COSTS | SALES _CONT | LIQUIDITY | BANK LOANS | SURVIVAL |

|---|---|---|---|---|---|

| SP | 312.62 | 298.89 | 325.04 | 317.61 | 324.00 |

| LLC | 243.22 | 247.63 | 232.31 | 236.28 | 236.34 |

| GP | 251.08 | 270.64 | 257.31 | 262.44 | 246.05 |

Notes: Sample N = 538.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Doś, A.; Wieczorek-Kosmala, M.; Błach, J. The Effect of Business Legal Form on the Perception of COVID-19-Related Disruptions by Households Running a Business. Risks 2022, 10, 82. https://0-doi-org.brum.beds.ac.uk/10.3390/risks10040082

AMA Style

Doś A, Wieczorek-Kosmala M, Błach J. The Effect of Business Legal Form on the Perception of COVID-19-Related Disruptions by Households Running a Business. Risks. 2022; 10(4):82. https://0-doi-org.brum.beds.ac.uk/10.3390/risks10040082

Chicago/Turabian StyleDoś, Anna, Monika Wieczorek-Kosmala, and Joanna Błach. 2022. "The Effect of Business Legal Form on the Perception of COVID-19-Related Disruptions by Households Running a Business" Risks 10, no. 4: 82. https://0-doi-org.brum.beds.ac.uk/10.3390/risks10040082

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.