A Discussion on Recent Risk Measures with Application to Credit Risk: Calculating Risk Contributions and Identifying Risk Concentrations

Abstract

:1. Introduction and Motivation

2. Credit Risk and Credit Portfolio Modeling

3. Risk Measures beyond VaR: A Comparative Analysis

3.1. Desirable Requirements to Risk Measures

- monotonicity: with

- cash invariance: for

- positive homogeneity: for

- subadditivity: .

- 5.

- convex: for

- 6.

- comonotonic additivity: for comonotonic random losses with non-decreasing functions and a positive random variable Z.

- 7.

- law invariance: .

- 8.

- elicitability: .

- 9.

- robustness:

3.2. Classes of Risk Measures

3.3. Risk Measures beyond VaR

4. Risk Contribution and Euler Allocation

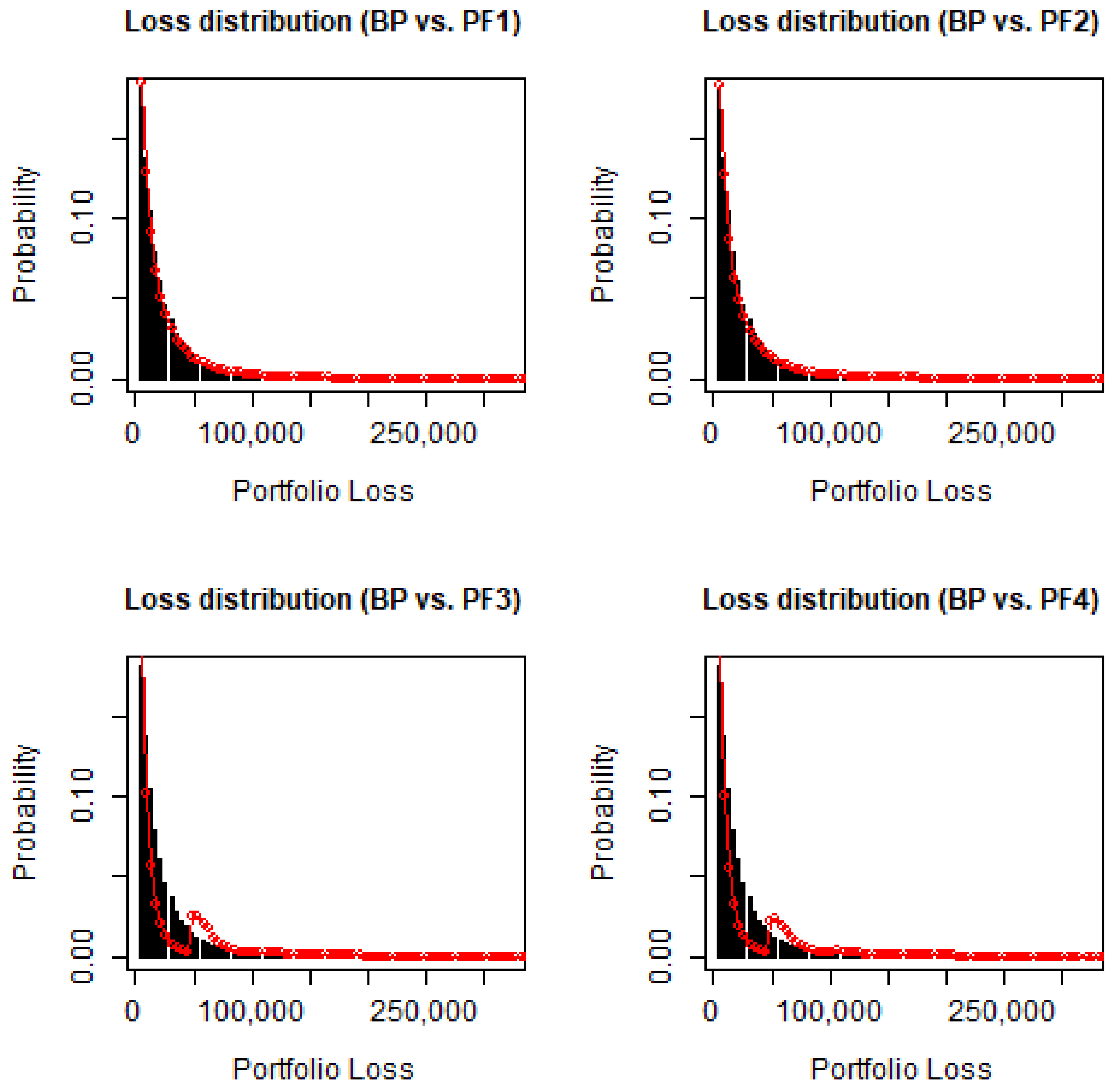

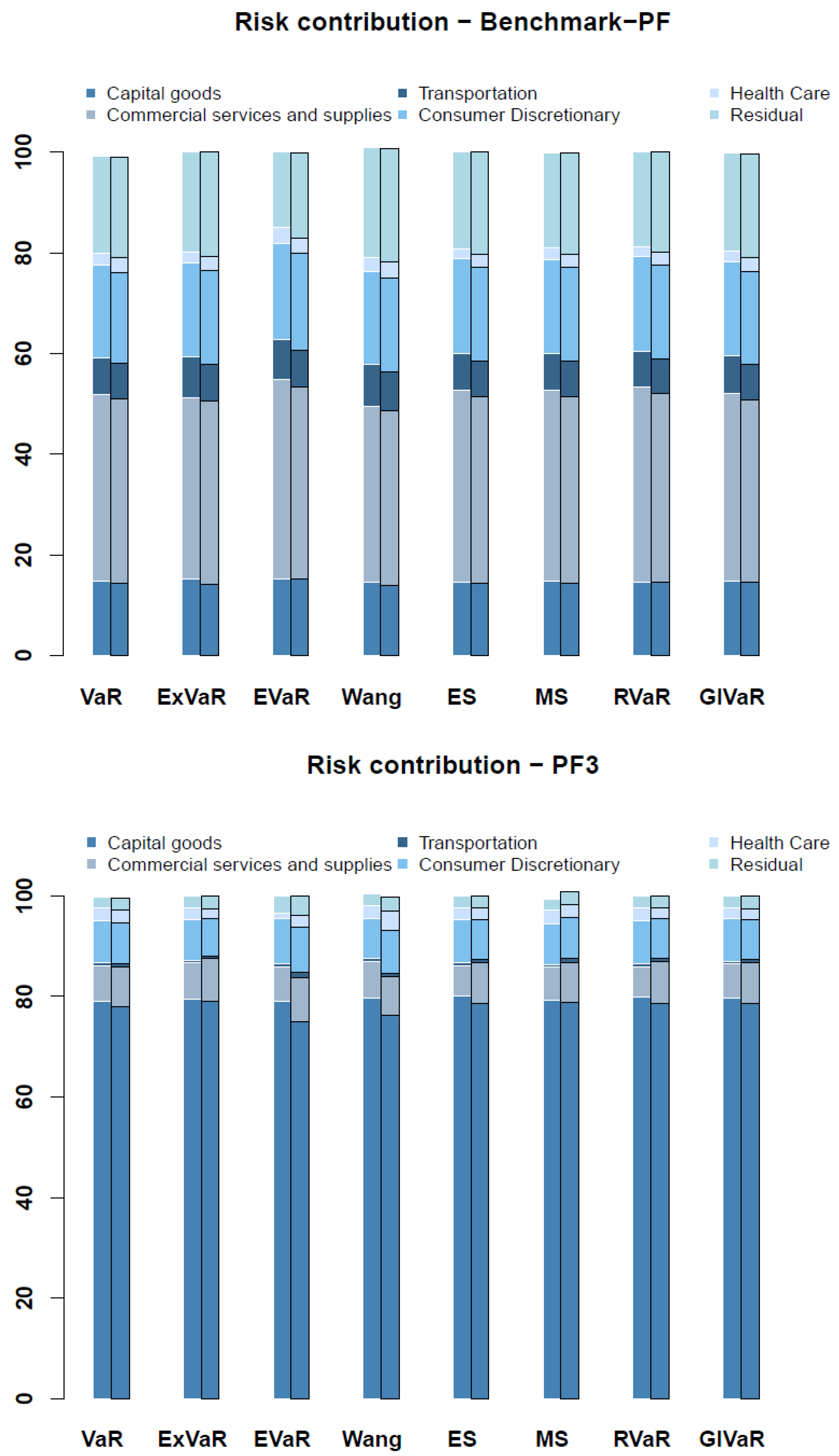

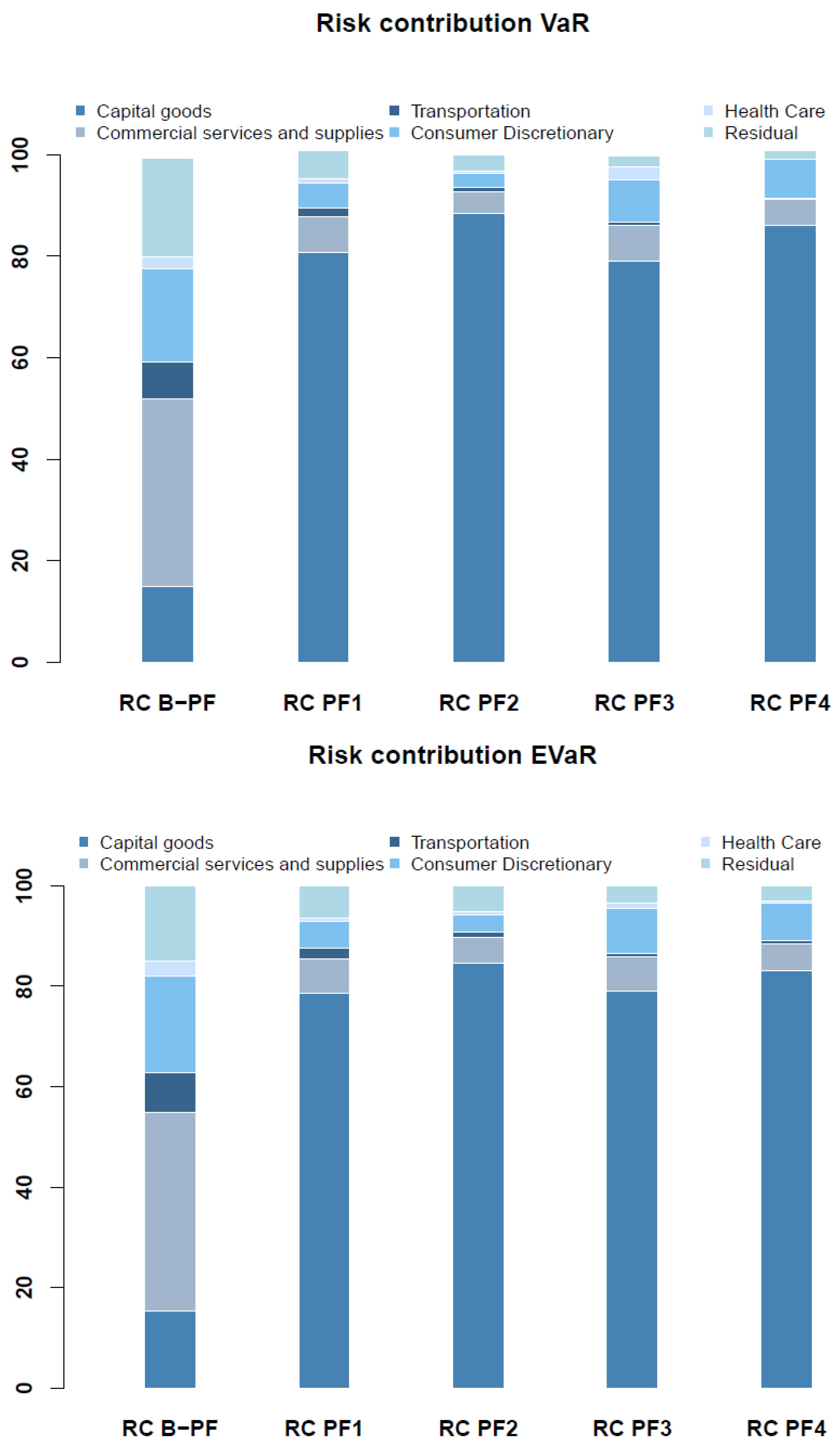

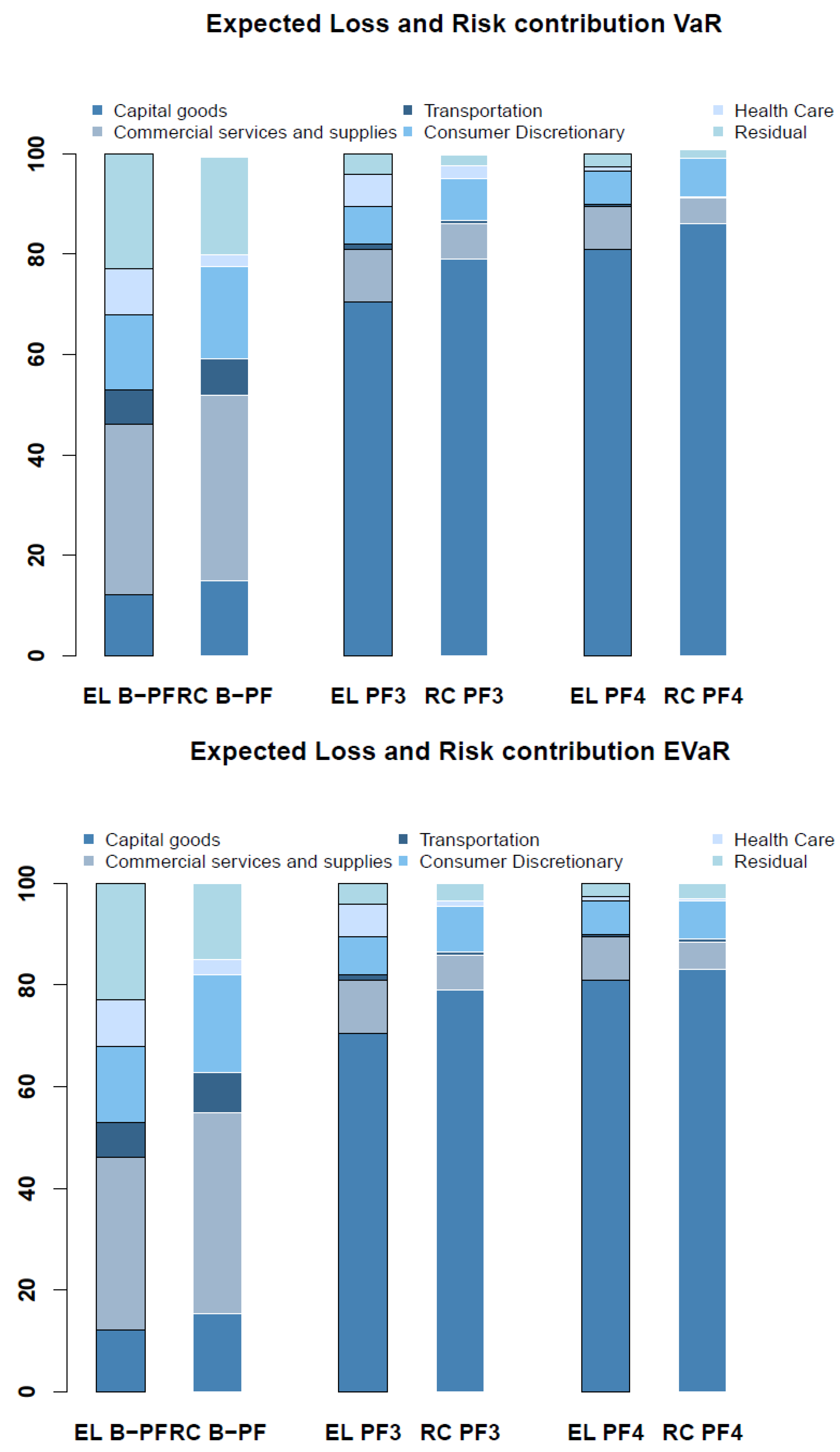

5. Application to Credit Risk

5.1. Data Description and Portfolio Structure

5.2. Research Questions and Calibration of the Risk Measures

- How sensitive is the overall portfolio risk w.r.t. changes of the credit quality across the risk measures under consideration?

- How sensitive are the risk contributions w.r.t. sector and name concentrations across the risk measures under consideration?

- Are there differences between the risk measures under consideration w.r.t. capital allocation?

5.3. Empirical Results

6. Conclusions

Author Contributions

Acknowledgments

Conflicts of Interest

References

- Acerbi, Carlos. 2002. Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking and Finance 26: 1505–18. [Google Scholar] [CrossRef]

- Acerbi, Carlos. 2004. Coherent representations of subjective risk aversion. In Risk Measures for the 21th Century. Edited by Giorgio Szergo. New York: John Wiley and Sons. [Google Scholar]

- Acerbi, Carlos, and Dirk Tasche. 2002. On the coherence of expected shortfall. Journal of Banking and Finance 26: 1487–503. [Google Scholar] [CrossRef]

- Acerbi, Carlo, and Balazs Szekely. 2017. General Properties of Backtestable Statistics. Available online: http://0-dx-doi-org.brum.beds.ac.uk/10.2139/ssrn.2905109 (accessed on 4 December 2018).

- Ahmadi-Javid, Amir. 2011. An information-theoretic approach to constructing coherent risk measures. Paper presented at the IEEE International Symposium on Information Theory, St. Petersburg, Russia, July 31–August 5; pp. 2125–27. [Google Scholar]

- Ahmadi-Javid, Amir. 2012a. Entropic value-at-risk: A new coherent risk measure. Journal of Optimization Theory and Appications 155: 1105–23. [Google Scholar] [CrossRef]

- Ahmadi-Javid, Amir. 2012b. Addendum to: Entropic value-at-risk: A new coherent risk measure. Journal of Optimization Theory and Appications 155: 1124–28. [Google Scholar] [CrossRef]

- Ahmadi-Javid, Amir. 2012c. Application of information-type divergences to constructing multiple-priors and variational preferences. Paper presented at the IEEE International Symposium on Information Theory, Cambridge, MA, USA, July 1–6; pp. 538–40. [Google Scholar]

- Ahmadi-Javid, Amir, and Alois Pichler. 2017. An Analytical Study of norms and Banach Spaces Induced by the Entropic Value-at-Risk. Mathematics and Financial Economics 11: 527–50. [Google Scholar] [CrossRef]

- Albanese, Claudio, and Stephan Lawi. 2004. Spectral Risk Measures for Credit Portfolios. In Risk Measures for the 21st Century. Edited by Giorgio Szegö. Chichester: John Wiley & Sons, p. 209. [Google Scholar]

- Artzner, Philippe, Freddy Delbaen, Jean-Marc Eber, and David Heath. 1999. Coherent measures of risk. Mathematical Finance 9: 203–28. [Google Scholar] [CrossRef]

- Assa, Hirbod, Manuel Morales, and Hassan Omidi Firouzi. 2016. On the Capital Allocation Problem for a New Coherent Risk Measure in Collective Risk Theory. Risks 4: 30. [Google Scholar] [CrossRef]

- Bauer, Daniel, and George Zanjani. 2015. The marginal cost of risk, risk measures, and capital allocation. Management Science 62: 1431–57. [Google Scholar] [CrossRef]

- Belles-Sampera, Jaume, Montserrat Guillén, and Miguel Santolino. 2014a. Beyond Value-at-Risk: GlueVaR Distortion Risk Measures. Risk Analysis 34: 121–34. [Google Scholar] [CrossRef]

- Belles-Sampera, Jaume, Montserrat Guillén, and Miguel Santolino. 2014b. GlueVaR risk measures in capital allocation applications. Insurance: Mathematics and Economics 58: 132–37. [Google Scholar] [CrossRef]

- Belles-Sampera, Jaume, Montserrat Guillén, and Miguel Santolino. 2014c. The use of flexible quantile-based measures in risk assessment. Communications in Statistics Theory and Methods 45: 1670–81. [Google Scholar] [CrossRef]

- Bellini, Fabio, Bernhard Klar, Alfred Müller, and Emanuela Rosazza Gianin. 2014. Generalized quantiles as risk measures. Insurance Mathematics & Economics 54: 41–48. [Google Scholar]

- Bellini, Fabio, and Valeria Bignozzi. 2015. On elicitable risk measures. Quantitative Finance 15: 725–33. [Google Scholar] [CrossRef]

- Bellini, Fabio, and Elena Di Bernardino. 2017. Risk management with expectiles. The European Journal of Finance 23: 487–507. [Google Scholar] [CrossRef]

- Bignozzi, Valeria, Matteo Burzoni, and Cosimo Munari. 2018. Risk Measures Based on Benchmark Loss Distributions. Working Paper. Milan, Italy: University of Milan. [Google Scholar]

- Brandtner, Mario, Wolfgang Kürsten, and Robert Rischau. 2018. Entropic risk measures and their comparative statics in portfolio selection: Coherence vs. convexity. European Journal of Operational Research 264: 707–16. [Google Scholar] [CrossRef]

- Breckling, Jens, and Ray Chambers. 1988. M-quantiles. Biometrika 75: 761–72. [Google Scholar] [CrossRef]

- Buch, Arne, Gregor Dorfleitner, and Maximilian Wimmer. 2011. Risk capital allocation for RORAC optimization. Journal of Banking & Finance 35: 3001–9. [Google Scholar]

- Burzoni, Matteo, Ilaria Peri, and Chiara M. Ruffo. 2017. On the properties of the Lambda value at risk: Robustness, elicitability and consistency. Quantitative Finance 17: 1735–43. [Google Scholar] [CrossRef]

- Chen, Rongda, Ze Wang, and Lean Yu. 2017. Importance Sampling for Credit Portfolio Risk with Risk Factors Having t-Copula. International Journal of Information Technology & Decision Making 16: 1101–24. [Google Scholar]

- Cont, Rama, Romain Deguest, and Giacomo Scandolo. 2010. Robustness and sensitivity analysis of risk measurement procedures. Quantitative Finance 10: 593–606. [Google Scholar] [CrossRef] [Green Version]

- Cousin, Areski, and Elena Di Bernardino. 2013. On multivariate extensions of value-at-risk. Journal of Multivariate Analysis 119: 32–46. [Google Scholar] [CrossRef]

- Cousin, Areski, and Elena Di Bernardino. 2014. On multivariate extensions of conditional-tail-expectation. Insurance Mathematics & Economics 55: 272–82. [Google Scholar]

- CSFP. 1997. CreditRisk+: A Credit Risk Management Framework. Technical Paper. Zurich: Credit Suisse First Boston. [Google Scholar]

- Delbaen, Freddy. 2000. Draft: Coherent risk measures. Paper presented at Lecture Notes, Pisa, Italy, February 28–March 8. [Google Scholar]

- Delbaen, Freddy. 2018. Remark on the Paper “Entropic value-at-risk: A new coherent risk measure”. In Risk and Stochastics. Edited by Pauline Barrieu. Singapore: World Scientific. [Google Scholar]

- Denault, Michel. 2001. Coherent allocation of risk capital. Journal of Risk 4: 1–34. [Google Scholar] [CrossRef] [Green Version]

- Denneberg, Dieter. 1994. Non-Additiv Risk Measure and Integral. Dordrecht: Kluwer Academic Publisher. [Google Scholar]

- Dhaene, Jan, Mark J. Goovaerts, and Rob Kaas. 2003. Economic capital allocation derived from risk measures. North American Actuarial Journal 7: 44–59. [Google Scholar] [CrossRef]

- Dhaene, Jan, Steven Vanduffel, Qihe Tang, Marc Goovaerts, Rob Kaas, and David Vyncke. 2004. Solvency Capital, Risk Measures and Comonotonicity: A Review. DTEW Research Report 0416. Leuven: Departement Toegepaste Economische Wetenschappen. [Google Scholar]

- Dhaene, Jan, Luc Henrard, Zinoviy Landsman, Antoine Vandendorpe, and Steven Vanduffel. 2008. Some results on the CTE-based capital allocation rule. Insurance: Mathematics and Economics 42: 855–63. [Google Scholar] [CrossRef]

- Dhaene, Jan, Andreas Tsanakas, Emiliano A. Valdez, and Steven Vanduffel. 2012. Optimal capital allocation principles. Journal of Risk and Insurance 79: 1–28. [Google Scholar] [CrossRef] [Green Version]

- Dorfleitner, Gregor, Matthias Fischer, and Marco Geidosch. 2012. Specification risk and calibration effects of a multifactor credit portfolio model. Journal of Fixed Income 22: 7–24. [Google Scholar] [CrossRef]

- Duellmann, Klaus, and Nancy Masschelein. 2007. A tractable model to measure sector concentration risk in credit portfolios. Journal of Financial Services Research 32: 55–79. [Google Scholar] [CrossRef]

- Dutta, Santanu, and Suparna Biswas. 2018. Nonparametric estimation of expected shortfall: p → 0 as sample size is increased. Communications in Statistics Simulation and Computation 47: 271–91. [Google Scholar] [CrossRef]

- Eckert, Johanna, Kevin Jakob, and Matthias Fischer. 2016. A Credit Portfolio Framework under Dependent Risk Parameters PD, LGD and EAD. Journal of Credit Risk 12: 97–119. [Google Scholar] [CrossRef]

- Embrechts, Paul, Haiyan Liu, and Ruodu Wang. 2016. Quantile-based Risk Sharing. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2744142 (accessed on 4 December 2018).

- Emmer, Susanne, Marie Kratz, and Dirk Tasche. 2015. What is the best risk measure in practice? A comparison of standard measures. Journal of Risk 18: 31–60. [Google Scholar] [CrossRef] [Green Version]

- Farinelli, Simone, and Mykhaylo Shkolnikov. 2012. Two models of stochastic loss given default. The Journal of Credit Risk 8: 3–20. [Google Scholar] [CrossRef] [Green Version]

- Fischer, Matthias, and Kevin Jakob. 2015. Copula-Specific Credit Portfolio Modeling. In Innovations in Quantitative Risk Management. Springer Proceedings in Mathematics & Statistics. Berlin and Heidelberg: Springer, pp. 129–46. [Google Scholar]

- Föllmer, Hans, and Alexander Schied. 2011. Stochastic Finance: An Introduction in Discrete Time, 3rd ed. Berlin: Walter de Gruyter. [Google Scholar]

- Föllmer, Hans, and Alexander Schied. 2008. Convex and Conherent Risk Measures. Working Paper. Berlin, Germany: Humboldt University. [Google Scholar]

- Föllmer, Hans, and Thomas Knispel. 2011. Entropic risk measures: Coherence vs. convexity, model ambiguity, and robust large deviations. Stochastics and Dynamics 11: 333–51. [Google Scholar] [CrossRef]

- Frittelli, Marco, Marco Maggis, and Ilaria Peri. 2014. Risk Measures on P(R) and value at risk with probability/loss function. Mathematical Finance 24: 442–63. [Google Scholar] [CrossRef]

- Frye, Jon. 2008. Correlation and asset correlation in the structural portfolio model. Journal of Credit Risk 4: 75–96. [Google Scholar] [CrossRef]

- Geidosch, Marco, and Matthias Fischer. 2016. Application of Vine Copulas to Credit Portfolio Risk Modeling. Journal of Risk and Financial Management 9: 1–15. [Google Scholar] [CrossRef]

- Glasserman, Paul, and Jingyi Li. 2005. Importance Sampling for Portfolio Credit Risk. Management Science 51: 1593–732. [Google Scholar] [CrossRef]

- Glasserman, Paul. 2005. Measuring Marginal Risk Contributions in Credit Portfolios. Journal of Computational Finance 9: 1–41. [Google Scholar] [CrossRef]

- Gneiting, Tilmann. 2011. Making and Evaluating Point Forecasts. Journal of the American Statistical Association 106: 746–62. [Google Scholar] [CrossRef]

- Gzyl, Henryk, and Silvia Mayoral. 2008. On a relationship between distorted and spectral risk measures. Revista de Economía Financiera 15: 8–21. [Google Scholar]

- Gupton, Greg M., Christopher C. Finger, and Mickey Bhatia. 1997. Credit Metrics. Technical Document. New York: J.P. Morgan. [Google Scholar]

- Haaf, Hermann, and Dirk Tasche. 2002. Calculationg Value-at-Risk Contributions in Credit Risk+. Available online: https://arxiv.org/abs/cond-mat/0112045 (accessed on 4 December 2018).

- Hainaut, Donatien, and David Colwell. 2016. A structural model of credit risk with switching processes and synchronous. The European Journal of Finance 20: 1040–62. [Google Scholar] [CrossRef]

- Hitaj, Asmerilda, and Ilaria Peri. 2015. Lambda vAlue at Risk: A New Backtestable Alternative to VaR. Working Paper. Milan, Italy: University of Milan. [Google Scholar]

- Hitaj, Asmerilda, Cesario Mateus, and Ilaria Peri. 2017. Lambda Value at Risk and Regulatory Capital: A Dynamic Approach to Tail Risk. Working Paper. Milan, Italy: University of Milan. [Google Scholar]

- Hougaard, Jens Leth, and Aleksandrs Smilgins. 2011. Risk capital allocation with autonomous subunits: The Lorenz set. Insurance: Mathematics and Economics 67: 151–57. [Google Scholar] [CrossRef]

- Jakob, Kevin, and Matthias Fischer. 2014. Quantifying the impact of different copulas in a general CreditRisk+ framework. Dependence Modeling 2: 1–21. [Google Scholar] [CrossRef]

- Jakob, Kevin, and Matthias Fischer. 2016. GCPM: A flexible package to explore credit portfolio risk. Austrian Journal of Statistics 45: 25–44. [Google Scholar] [CrossRef]

- Jones, M. Chris. 1994. Expectiles and M-quantiles are quantiles. Statistic and Probability Letters 20: 149–53. [Google Scholar] [CrossRef]

- Jovan, Matej, and Aleš Ahčan. 2017. Default prediction with the Merton-type structural model based on the NIG Lévy process. Journal of Computational and Applied Mathematics 3: 414–22. [Google Scholar] [CrossRef]

- Kalkbrener, Michael, Hans Lotter, and Ludger Overbeck. 2004. Sensible and efficient capital allocation. Risk 1: 19–24. [Google Scholar]

- Kalkbrenner, Michael. 2005. An axiomatic approach to capital allocation. Mathematical Finance 15: 425–37. [Google Scholar] [CrossRef]

- Kaposty, Florian, Matthias Löderbusch, and Jakob Maciag. 2017. Stochastic loss given default and exposure at default in a structural model of portfolio credit risk. The Journal of Credit Risk 13: 93–123. [Google Scholar] [CrossRef]

- Kealhofer, Stephen, and Jeffrey R. Bohn. 2001. Portfolio Management of Default Risk. Technical Paper. San Fransisco: J.P. Morgan. [Google Scholar]

- Kim, Joseph H. T. 2010. Bias correction for estimated distortion risk measure using the bootstrap. Insurance: Mathematics and Economics 47: 198–205. [Google Scholar] [CrossRef] [Green Version]

- Kou, Steven, and Xianhua Peng. 2014. Expected shortfall or median shortfall. Journal of Financial Engineering 1: 145–47. [Google Scholar] [CrossRef]

- Kou, Steven, Xianhua Peng, and Christian Heyde. 2013. External risk measures and Basel accords. Mathematics of Operation Research 38: 393–417. [Google Scholar] [CrossRef]

- Kou, Steven, and Xianhua Peng. 2014. On the measurement of economic tail risk. Available online: https://arxiv.org/pdf/1401.4787v2.pdf (accessed on 4 December 2018).

- Koyluoglu, Ugur, and James Stoker. 2002. Honour your contribution. Risk 15: 90–94. [Google Scholar]

- Krätschmer, Volker, Alexander Schied, and Zähle Hendryk. 2014. Comparative and quanlitative robustness for law-invariant risk measures. Finance and Stochastics 18: 271–95. [Google Scholar] [CrossRef]

- Kurth, Alexandre, and Dirk Tasche. 2003. Contributions to credit risk. Risk 16: 84–88. [Google Scholar]

- Lucas, André, Pieter Klaassen, Peter Spreij, and Stefan Straetmans. 2002. Extreme tails for linear portfolio credit risk models. In Committee on the Global Financial System: Risk Measurement and Systemic Risk. Paper presented at the Third Joint Central Bank Research Conference, Basel, Switzerland, March 7–8. Basel: Bank for International Settlements, pp. 271–84. [Google Scholar]

- Lucas, André, Pieter Klaassen, Peter Spreij, and Stefan Straetmans. 2003. Tail Behavior of Credit Loss Distributions for General Latent Factor Models. Applied Mathematical Finance 10: 337–57. [Google Scholar] [CrossRef]

- Martin, Richard. 2014. Expectiles behave as expected. Risk 2014: 79. [Google Scholar]

- Martin, Richard, and Dirk Tasche. 2007. Shortfall: A tail of two parts. Risk 20: 84–89. [Google Scholar]

- Maume-Deschamps, Véronique, Didier Rullière, and Khalil Said. 2017. Multivariate extensions of expectiles risk measures. Dependence Modeling 5: 20–44. [Google Scholar] [CrossRef] [Green Version]

- McKinsey & Company Inc. 1999. CreditPortfolioView. Technical Report. New York: McKinsey & Company, Inc. [Google Scholar]

- Merton, Robert C. 1974. On the pricing of corporate debt: The risk structure of interest rates. Journal of Finance 29: 449–70. [Google Scholar]

- Micocci, Marco. 2000. M.A.R.C: An actuarial model for credit risk. Paper presented at the XXXIth International Astin Colloquium, Porto Cervo, Italy, September 17–20. [Google Scholar]

- Moser, Thorsten. 2016. Jenseits von Value-at-Risk und Expected Shortfall: Alternativen und Neuere Ansätze mit Anwendungen auf Kreditrisiken. Master’s Thesis, University Erlangen-Nuremberg, Erlangen, Germany. [Google Scholar]

- Nadarajah, Saralees, Bo Zhang, and Stephen Chan. 2014. Estimation methods for expected shortfall. Quantitative Finance 14: 271–91. [Google Scholar] [CrossRef]

- Nadarajah, Saralees. 2016. Estimation methods for Value at risk. In Extreme Events in Finance: A Handbook of Extreme Value Theory and its Applications. Edited by Francois Longin. Hoboken: John Wiley & Sons, pp. 303–73. [Google Scholar]

- Newey, Whitney K., and James L. Powell. 1987. Asymmetric least squares estimation and testing. Econometrica 55: 819–47. [Google Scholar] [CrossRef]

- Patrik, Gary, Stefan Bernegger, and Marcel Beat Rüegg. 1999. The use of risk adjusted capital to support business decision making. Paper presented at Casualty Actuarials Society Forum, Baltimore, MD, USA, June 6–8. [Google Scholar]

- Pfeuffer, Marius, Maximilian Nagl, Matthias Fischer, and Daniel Rösch. 2018. Parameter Estimation, Bias Correction and Uncertainty Quantification in the Vasicek Credit Portfolio Model. Working Paper (submitted). Erlangen, Germany: University Erlangen-Nuremberg. [Google Scholar]

- Pichler, Alois, and Ruben Schlotter. 2018. Entropy Based Risk Measures. Working Paper. Chemnitz, Germany: University of Chemnitz. [Google Scholar]

- Rassoul, Abdelaziz. 2014. An Improved Estimator of the Distortion Risk Measure for Heavy-Tailed Claims. Working Paper. Blida, Algeria: Ecole Nationale Supérieure d’Hydraulique. [Google Scholar]

- Rockafellar, R. Tyrrell, and Stanislav Uryasev. 2002. Conditional value at risk for general loss distributions. Journal of Banking & Finance 7: 1443–71. [Google Scholar]

- Siller, Thomas. 2013. Measuring marginal risk contributions in credit portfolios. Quantitative Finance 13: 1915–23. [Google Scholar] [CrossRef]

- Stahl, Gerhard, Jinsong Zheng, Ruediger Kiesel, and Robin Rülicke. 2012. Conceptualizing Robustness in Risk Management. Working Paper. Campus Essen, Germany: University of Duisburg-Essen. [Google Scholar]

- Tasche, Dirk. 1999. Risk Contributions and Performance Measurement. Working Paper. Munich, Germany: Munich University of Technology. [Google Scholar]

- Tasche, Dirk. 2001. Conditional Expectation as Quantile Derivative. Working Paper. Munich, Germany: Munich University of Technology. [Google Scholar]

- Tasche, Dirk. 2004. Allocating portfolio economic capital to sub-portfolios. In Economic Capital: A Practitioner Guide. London: Risk Books, pp. 275–302. [Google Scholar]

- Tasche, Dirk. 2007. Euler Allocation: Theory and Practice. Technical Document. London: Fitch Ratings. [Google Scholar]

- Tasche, Dirk. 2008. Capital Allocation to Business Units and Sub-Portfolios: The Euler Principle. In Pillar II in the New Basel Accord: The Challenge of Economic Capital. Edited by Andrea Resti. London: Risk Books. [Google Scholar]

- Tasche, Dirk. 2016. Fitting a Distribution to Value-at-Risk and Expected Shortfall, With an Application to Covered Bonds. Journal of Credit Risk, 12: 77–111. [Google Scholar] [CrossRef]

- Tsaig, Yaakov, Amnon Levy, and Yashan Wang. 2011. Analyzing the impact of credit migration in a portfolio setting. Journal of Banking and Finance 35: 3145–57. [Google Scholar] [CrossRef]

- Tsanakas, Andreas, and Christopher Barnett. 2003. Risk capital allocation and cooperative pricing of insurance liabilities. Insurance: Mathematics and Economics 33: 239–54. [Google Scholar] [CrossRef]

- Tsukahara, Hideatsu. 2014. Estimation of Distortion Risk Measures. Journal of Financial Econometrics 12: 213–35. [Google Scholar] [CrossRef]

- Urban, Michael, Jörg Dittrich, Claudia Klüppelberg, and Rolf Stölting. 2003. Allocation of risk capital to insurance portfolios. Blätter der DGVFM 26: 389–406. [Google Scholar] [CrossRef]

- Van Gulick, Gerwals, Anja De Waegemaerre, and Henk Norde. 2012. Excess based capital allocation of risk capital. Insurance: Mathematics and Economics 50: 26–42. [Google Scholar] [CrossRef]

- Wang, Shaun. 1995. Insurance pricing and increased limits ratemaking by proportional hazard transforms. Insurance: Mathematics and Economics 17: 43–54. [Google Scholar] [CrossRef]

- Wang, Shaun. 1996. Premium calculation by transforming the layer premium density. ASTIN Bulletin 26: 71–92. [Google Scholar] [CrossRef]

- Wang, Shaun. 1998. An Actuarial Index of Right-Tail Risk. North American Actuarial Journal 2: 88–101. [Google Scholar] [CrossRef]

- Wang, Shaun S. 2000. A Class of Distortion Operators for Pricing Financial and Insurance Risks. The Journal of Risk and Insurance 67: 15–36. [Google Scholar] [CrossRef]

- Wang, Shaun S. 2001. A risk measure that goes beyond coherence. Working paper. Itasca, IL, USA: SCOR Reinsurance Co. [Google Scholar]

- Zanjani, George. 2010. An economic approach to capital allocation. Journal of Risk and Insurance 77: 523–49. [Google Scholar] [CrossRef]

- Zheng, Chengli, and Yan Chen. 2012. Coherent risk measure based on relative entropy. Applied Mathematics & Information Sciences 6: 233–38. [Google Scholar]

- Zheng, Chengli, and Yan Chen. 2014a. The comparisons for three kinds of quantile-based risk measures. Information Technology Journal 13: 1147–53. [Google Scholar] [CrossRef]

- Zheng, Chengli, and Yan Chen. 2014b. Portfolio selection based on relative entropy coherent risk measure. Systems Engineering Theory & Practice 34: 648–55. [Google Scholar]

- Zheng, Chengli, and Yan Chen. 2015. Allocation of Risk Capital Based on Iso-Entropic Coherent Risk Measure. Journal of Industrial Engineering and Management 8: 530–53. [Google Scholar] [CrossRef]

- Zhou, Rongxi, Xiao Liu, Mei Yu, and Kyle Huang. 2017. Properties of Risk Measures of Generalized Entropy in Portfolio Selection. Entropy 19: 657. [Google Scholar] [CrossRef]

- Ziegel, Johanna, and Ruodu Wang. 2015. Elicitable distortion risk measures: A concise proof. Statistic and Probability Letters 100: 172–75. [Google Scholar]

| 1 | In a broader sense, losses may also arise from rating migrations if the rating of the counterparty changes; see, for instance, Tsaig et al. (2011). |

| 2 | Eckert et al. (2016) discuss a credit portfolio framework that allows for dependence between PD, LGD and EAD; see also Kaposty et al. (2017) and Farinelli and Shkolnikov (2012). |

| 3 | Typically, counterparties are assigned to predefined industry and/or country sectors. |

| 4 | A technical implementation (see, in particular, Algorithm 1 from Jakob and Fischer (2016)) can be found in the R package GCPM, which was used to generate the loss distribution for the hypothetical portfolios in the empirical part. |

| 5 | If the confidence level is high and losses from the tail of the distribution are of special interest, Importance Sampling (IS) might came to application in order to increase the speed of the calculation. With IS, the future economic scenarios are not generated randomly, but the “bad” scenarios have a higher chance of being selected than the “good” scenarios and the bias that is thus introduced is corrected later, see Glassermann (2005), Glassermann and Li (2005) or Chen et al. (2017). |

| 6 | For a multivariate extensions of the VaR, we refer to Cousin and Di Bernardino (2013). |

| 7 | |

| 8 | Newey and Powell (1987) and Breckling and Chambers (1988) have already introduced a similar notion of generalized quantiles in a different context. For the choice , the generalized quantile is an expectile. |

| 9 | Except for a correction term for a discontinuity in the distribution, the ES equals the conditional Expectation . It is also well known as Average-VaR, Tail-VaR and Conditional-VaR. |

| 10 | Cousin and Di Bernardino (2014) discuss multivariate extensions of ES. |

| 11 | |

| 12 | Maume-Deschamps et al. (2017) discuss multivariate extensions of expectiles. |

| 13 | and . |

| 14 | Wang (2000) pointed out that this distortion function combines four different approaches: (1) Classical insurance premium calculation; (2) Theory of distortion risk measures; (3) Capital-Asset-Pricing-Model; (4) Option pricing (Black-Scholes). Furthermore, Wang (2001) has showed that for a normal or log-normal distributed loss this distortion function results in a normal or log-normal distribution. |

| 15 | The forcing conditions for the parameters such that the two presented inequalities hold are listed in Belles-Sampera et al. (2014a). |

| 16 | Belles-Sampera et al. (2014a) calculate some useful analytical closed forms of the GlueVaR for Normal, Log-normal, Exponential, Pareto and Type-II Pareto distributions. Furthermore, they deliver conditions under which the GlueVaR fulfills the special property of tail-subadditivity also introduced in the same paper. |

| 17 | The contribution discusses different approaches for capital allocation methods for the GlueVaR. |

| 18 | Alternative allocation methods: Shapley, Aumann-Shapley, Euler, Activity based, beta method, incremental method, cost gap method, Nucleonlus method |

| 19 | The axiomatic approach follows three key properties of the allocation principle: (1) complete allocation; (2) diversification; (3) continuity with respect to the allocation principle. |

| 20 | We take this portfolio size to guarantee efficient simulations and avoid working memory problems. |

| 21 | The MSCI EMU Index (European Economic and Monetary Union) captures large and mid cap representation across the 10 Developed Markets countries in the EMU. |

| 22 | |

| 23 | The simulation results are generated with a simulation number of 100,000. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| RM | Coherence | Convex | Comonotonic Add. | Law Invariant | Elicitability | Robustness |

|---|---|---|---|---|---|---|

| VaR | x | x | ✓ | ✓ | ✓ | Weak Topology |

| ES | ✓ | ✓ | ✓ | ✓ | x | Wasserstein |

| MS | x | x | ✓ | ✓ | ✓ | Weak Topology |

| ExVaR | ✓ | ✓ | x | ✓ | ✓ | Wasserstein |

| LVaR | x | x | x | ✓ | ✓ | -robust |

| RMBLD | x | x | x | ✓ | x | -robust |

| RVaR | x | x | ✓ | ✓ | x | -robust |

| Wang | ✓ | ✓ | ✓ | ✓ | x | |

| GlueVaR | x | x | ✓ | ✓ | x | Wasserstein |

| EVaR | ✓ | ✓ | ✓ | ✓ | x |

| RM | Source | ||

|---|---|---|---|

| VaR | Tasche (1999) | ||

| ES | Tasche (1999) | ||

| MS | Moser (2016) | ||

| ExVaR | Emmer et al. (2015) | ||

| RVaR | Moser (2016) | ||

| Wang | Tsanakas and Barnett (2003) | ||

| GlueVaR | Tsanakas and Barnett (2003) | ||

| EVaR | Zheng and Chen (2015) | ||

| LVaR | x | x | not positive homogeneous |

| BLD | x | x | not positive homogeneous |

| Sector | Benchmark-PF | PF 1 | PF 2 | PF 3 | PF 4 |

|---|---|---|---|---|---|

| Energy | 0 | 0 | 0 | 0 | 0 |

| Materials | 6 | 2 | 1 | 2 | 1 |

| Capital goods | 12 | 71 | 82 | 71 | 82 |

| Commercial services and supplies | 34 | 11 | 7 | 11 | 7 |

| Transportation | 7 | 2 | 1 | 2 | 1 |

| Consumer Discretionary | 15 | 5 | 3 | 5 | 3 |

| Consumer staples | 6 | 2 | 1 | 2 | 1 |

| Health Care | 9 | 3 | 2 | 3 | 2 |

| Information technology | 3 | 1 | 1 | 1 | 1 |

| Telecommunication.services | 1 | 1 | 1 | 1 | 1 |

| Utilities | 7 | 2 | 1 | 2 | 1 |

| Number of Counterparties | 200 | 200 | 200 | 100 | 100 |

| HHI | 17.86 | 52.15 | 67.92 | 52.15 | 67.92 |

| Risk Measures | Benchmark-PF | PF1 | PF2 | Risk Measures | Benchmark-PF | PF1 | PF2 |

|---|---|---|---|---|---|---|---|

| VaR (PD 2.0) | 9.23 | +24 | +32 | BLD (PD 2.0) | 9.23 | +24 | +32 |

| VaR (PD 3.5) | 12.83 | +25 | +28 | BLD (PD 3.5) | 12.83 | +25 | +28 |

| VaR (Mixed PD) | 6.98 | +26 | +32 | BLD (Mixed PD) | 6.98 | +26 | +32 |

| ExVaR (PD 2.0) | 10.47 | +27 | +34 | ES (PD 2.0) | 11.01 | +27 | +35 |

| ExVaR (PD 3.5) | 14.10 | +23 | +28 | ES (PD 3.5) | 14.83 | +25 | +29 |

| ExVaR (Mixed PD) | 8.02 | +25 | +33 | ES (Mixed PD) | 8.49 | +25 | +32 |

| EVaR (PD 2.0) | 8.72 | +31 | +36 | MS (PD 2.0) | 10.80 | +27 | +33 |

| EVaR (PD 3.5) | 13.74 | +22 | +27 | MS (PD 3.5) | 14.85 | +21 | +29 |

| EVaR (Mixed PD) | 6.98 | +23 | +30 | MS (Mixed PD) | 8.10 | +25 | +33 |

| Wang (PD 2.0) | 9.57 | +29 | +34 | RVaR (PD 2.0) | 10.76 | +26 | +33 |

| Wang (PD 3.5) | 13.11 | +22 | +27 | RVaR (PD 3.5) | 14.44 | +25 | +29 |

| Wang (Mixed PD) | 7.46 | +29 | +37 | RVaR (Mixed PD) | 8.20 | +24 | +33 |

| LVaR (PD 2.0) | 9.45 | +26 | +31 | GlueVaR (PD 2.0) | 10.82 | +27 | +34 |

| LVaR (PD 3.5) | 13.05 | +26 | +33 | GlueVaR (PD 3.5) | 14.71 | +24 | +29 |

| LVaR ( Mixed PD) | 6.75 | +33 | +47 | GlueVaR (Mixed PD) | 8.34 | +26 | +33 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fischer, M.; Moser, T.; Pfeuffer, M. A Discussion on Recent Risk Measures with Application to Credit Risk: Calculating Risk Contributions and Identifying Risk Concentrations. Risks 2018, 6, 142. https://0-doi-org.brum.beds.ac.uk/10.3390/risks6040142

Fischer M, Moser T, Pfeuffer M. A Discussion on Recent Risk Measures with Application to Credit Risk: Calculating Risk Contributions and Identifying Risk Concentrations. Risks. 2018; 6(4):142. https://0-doi-org.brum.beds.ac.uk/10.3390/risks6040142

Chicago/Turabian StyleFischer, Matthias, Thorsten Moser, and Marius Pfeuffer. 2018. "A Discussion on Recent Risk Measures with Application to Credit Risk: Calculating Risk Contributions and Identifying Risk Concentrations" Risks 6, no. 4: 142. https://0-doi-org.brum.beds.ac.uk/10.3390/risks6040142