The Activity-Based Costing System Applied in Higher Education Institutions: A Systematic Review and Mapping of the Literature

Abstract

:1. Introduction

2. Literature Review

2.1. Activity-Based Costing (ABC)

2.2. Application of the ABC Model in HEIs

3. Research Methodology

Method

4. Results

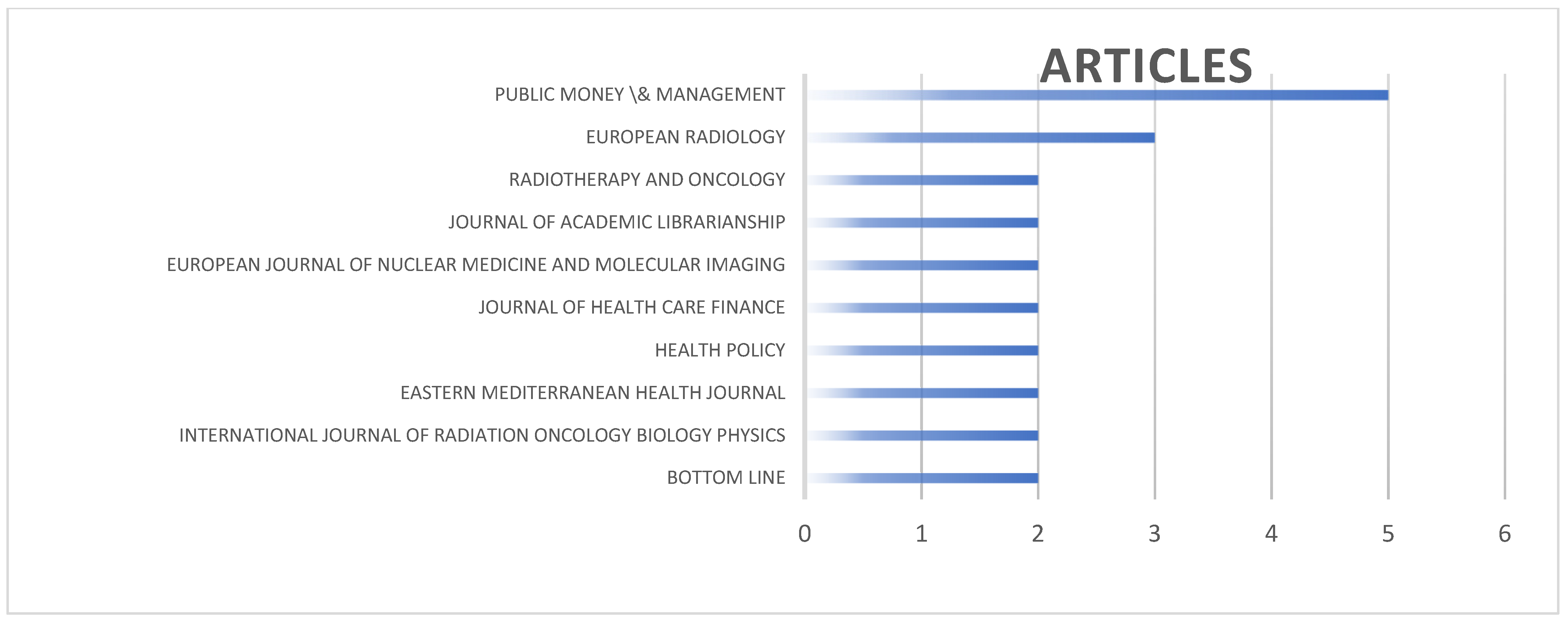

4.1. Data Base Information

4.2. Analysis of Co-Citations: Multidimensional Scales, Cluster Analysis, and Factor Analysis

4.3. ABC Applied in HEIs

5. Theoretical and Managerial Implications

6. Conclusions, Contributions, and Research Agenda

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Anthony, J.C.; Yoshizawa, F.; Anthony, T.G.; Vary, T.C.; Jefferson, L.S.; Kimball, S.R. Leucine stimulates translation initiation in skeletal muscle of postabsorptive rats via a rapamycin-sensitive pathway. J. Nutr. 2000, 130, 2413–2419. [Google Scholar] [CrossRef]

- Johnson, H.T.; Kaplan, R.S. The rise and fall of management accounting. IEEE Eng. Manag. Rev. 1987, 15, 36–44. [Google Scholar] [CrossRef]

- Hardan, A.S.; Shatnawi, T.M. Impact of applying the ABC on improving the financial performance in Telecom companies. Int. J. Bus. Manag. 2013, 8, 48–61. [Google Scholar] [CrossRef]

- Krishnan, A. An Application of Activity Based Costing in Higher Learning Institution: A local Case Study. Contemp. Manag. Res. 2007, 2, 75–90. [Google Scholar] [CrossRef]

- Sorros, J.; Karagiorgos, A.; Mpelesis, N. Adoption of Activity-Based Costing: A Survey of the Education Sector of Greece. Int. Adv. Econ. Res. 2017, 23, 309–320. [Google Scholar] [CrossRef]

- Améstica-Rivas, L.; Llinas-Audet, X.; Oriol Escardíbul, J. Costos de la renovación curricular: Una propuesta metodológica para la valorización económica de carreras universitarias. Form. Univ. 2017, 10, 89–100. [Google Scholar] [CrossRef]

- Ríos, M.; Rodríguez, L. Sistema de custeio baseado em atividades um instrumento viável para pequenas e médias empresas no caso do México. Manag. Stud. 2014, 220–232. [Google Scholar] [CrossRef]

- López, M.; Rodríguez, J.A. Peculiaridades de custo nas universidades. Sci. J. Account. 2018, 21, 103–115. [Google Scholar] [CrossRef]

- Parra, J.F.; Peña, Y.C. The Theory of Hidden Performance Preserves: A Theoretical Approach. Cad. Contab. 2014, 12, 15–39. [Google Scholar] [CrossRef]

- Zanievicz, M.; Beuren, I.; Santos, P.; Kloeppel, N. Métodos de Custeio: Uma metaanálise dos artigos apresentados no Congresso Brasileiro de Custos no período 1994–2010. Rev. Bras. Gestão Negócios 2013, 15, 601–616. [Google Scholar]

- Mutschke, P.; Mayr, P.; Schaer, P.; Sure, Y. Science models as value-added services for scholarly information systems. Scientometrics 2011, 89, 349–364. [Google Scholar] [CrossRef]

- Hawkins, D.T. Unconventional uses of on-line information retrieval systems: Online bibliometric studies. J. Am. Soc. Inf. Sci. 1977, 28, 13–18. [Google Scholar] [CrossRef]

- Using Bibliometrics: A Guide to Evaluating Research Performance with Citation Data; Thomsom Reuters: Toronto, ON, Canada, 2008.

- Altawati, N.; Kim-Soon, N.; Ahmad, A.; Elmabrok, A. A Review of Traditional Cost System versus Activity Based Costing Approaches. Adv. Sci. Lett. 2018, 24, 4688–4694. [Google Scholar] [CrossRef]

- Akyol, D.; Tuncel, G.; Bayhan, G. A comparative analysis of activity-based costing and traditional costing. Int. J. Ind. Manuf. Eng. 2005, 1, 136–139. [Google Scholar]

- Kaplan, R.S.; Cooper, R. Cost and Effect: Using Integrated Cost Systems to Drive Profitability and Performance; Harvard Business School: Boston, MA, USA, 1998. [Google Scholar]

- Bornia, A.C. Análise Gerencial de Custos: Aplicação em Empresas Modernas, 3rd ed.; Atlas: São Paulo, Brazil, 2019. [Google Scholar]

- Catânio, A.R.; Pizzo, J.C.M.; Moraes, R.O. Time-Driven Activity-Based Costing (TDABC): Um estudo bibliométrico das publicações nacionais. In Anais do Congresso Brasileiro de Custos; Anais do Congresso Brasileiro de Custos Foz do Iguaçu, Brazil. 2015, p. 22. Available online: https://anaiscbc.emnuvens.com.br/anais/article/view/3913 (accessed on 10 November 2023).

- Khodadadzadeh, T. A state-of-art review on activity-based costing. Accounting 2015, 1, 89–94. [Google Scholar] [CrossRef]

- Cooper, R.; Slagmulder, R. Strategic cost management: Expanding scope and boundaries. Cost Manag. 2003, 17, 23–30. [Google Scholar]

- Kalicanin, D. Activity-Based Costing as an Information Basis for an Efficient Strategic Management Process. Econ. Ann. 2013, 58, 95–119. [Google Scholar] [CrossRef]

- da Costa, C.V.; de Sene Carvalho, M.; Pinto, D.A.; Visentin, I.C.; de Souza, F.M.A. Contabilidade de Custos Aplicada à Gestão Hospitalar Uma Revisão Teórica. Cost Accounting Applied to Hospital Management: A Theoretical Review. Humanidades Tecnol. Finom 2021, 29. Available online: http://revistas.icesp.br/index.php/FINOM_Humanidade_Tecnologia/article/view/1589 (accessed on 14 January 2024).

- Kaplanog, V. Application of activity-based costing to a land transportation company: A case study. Int. J. Prod. Econ. 2008, 116, 308–324. [Google Scholar]

- Quesado, P.; Silva, R. Activity-based costing (ABC) and its implication for open innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 41. [Google Scholar] [CrossRef]

- Pietrzak, Z.; Wnuk-Pel, T.; Christauskas, C. Problems with Activity-Based Costing Implementation in Polish and Lithuanian Companies. Eng. Econ. 2020, 31, 26–38. [Google Scholar] [CrossRef]

- Stratton, W.; Desroches, D.; Lawson, R.; Hatch, T. Activity-based costing: Is it still relevant? Manag. Account. Q. 2009, 10, 31–40. [Google Scholar]

- Askarany, D.; Yazdifar, H. Why ABC is Not Widely Implemented? Int. J. Bus. Res. 2007, 7, 93–98. [Google Scholar]

- Bornia, A. Análise Gerencial de Custos em Empresas Modernas; Bookman: Porto Alegre, Brazil, 2002. [Google Scholar]

- Kaplan, R.; Anderson, S. Time-Driven Activity Based Costing; Campus: Rio de Janeiro, Brazil, 2007. [Google Scholar]

- Fito, A.; Llobet, J.; Cuguero, N. The activity-based costing model trajectory: A path of lights and shadows. Intang. Cap. 2018, 14, 146–161. [Google Scholar] [CrossRef]

- Ouassini, I. An analysis of Panasonic Group in Terms of Activity—Based Costing, Justin-Time Production and Quality and Environment Costing. J. Oper. Manag. 2019, 18, 49–65. [Google Scholar]

- Gosselin, M. A Review of Activity-Based Costing: Technique, Implementation and Consequences. Handb. Manag. Account. Res. 2007, 2, 641–674. [Google Scholar]

- Rankin, R. The Predictive Impact of Contextual Factors on Activity-Based Costing Adoption. J. Account. Financ. 2020, 20, 66–81. [Google Scholar]

- Wegmann, G. A typology of cost accounting practices based on activity-based costing—A strategic cost management approach. Pac. Manag. Account. J. 2019, 14, 161–184. [Google Scholar] [CrossRef]

- Järvinen, J.; Väätäjä, K. Customer Profitability Analysis Using Time-Driven Activity-Based Costing: Three Interventionist Case Studies. Nord. J. Bus. 2018, 67, 27–47. [Google Scholar]

- Major, M.; Vieira, R. Activity-Based Costing/Management. In Contabilidade e Controlo de Gestão: Teoria, Metodologia e Prática; Major, M.J., Vieira, R., Eds.; Escolar Editora: Lisbon, Portugal, 2017; pp. 297–329. [Google Scholar]

- Major, M.; Hoque, Z. Activity-Based Costing: Concepts, Issues and Practice. In Handbook of Cost and Management Accounting; Hoque, Z., Ed.; Spiramus: London, UK, 2005; pp. 83–103. [Google Scholar]

- Foster, G.; Swenson, D. Measuring the success of activity-based cost management and its determinants. J. Manag. Account. Res. 1997, 9, 109–141. [Google Scholar]

- Stefano, N.; Lisbôa, M.; Casarotto Filho, N. Activity-Based Costing: Estado da Arte Proposta pelo Pesquisador e Revisão Bibliométrica da Literatura. Iberoam. J. Proj. Manag. 2012, 3, 1–22. [Google Scholar]

- Diehl, C.; Souza, M. Publicações Sobre o Custeio Baseado em Atividades (ABC) em Congressos Brasileiros de Custos no Período de 1997 a 2006. Rev. Contab. Vista E Rev. 2008, 1, 39–57. [Google Scholar]

- Barsanti, H.; Souza, A. Método de Custeio Baseado em Atividades: Uma Pesquisa Bibliométrica. Pensar Contábil 2018, 20, 44–54. [Google Scholar]

- Souza, A.; Avelar, E.; Boina, T. Custeio Baseado em Atividades: Uma Análise das Pesquisas Brasileiras Desenvolvidas na Primeira Década do Século XXI. Rev. De Informação Contábil 2016, 10, 1–19. [Google Scholar]

- Baldvinsdottir, G.; Mitchell, F.; Nørreklit, H. Issues in the relationship between theory and practice in management accounting. Manag. Account. Res. 2010, 21, 79–82. [Google Scholar] [CrossRef]

- Scapens, R.W. Understanding management accounting practices: A personal journey. Br. Account. Rev. 2006, 38, 1–30. [Google Scholar] [CrossRef]

- Spicer, B.H. The resurgence of cost and management accounting: A review of some recent developments in practice, theories and case research methods. Manag. Account. Res. 1992, 3, 1–37. [Google Scholar] [CrossRef]

- Bromwich, M.; Scapens, R.W. Management accounting research: 25 years on. Manag. Account. Res. 2016, 31, 1–9. [Google Scholar] [CrossRef]

- Kurunmäki, L. Management accounting, economic reasoning and the new public management reforms. In Handbook of Management Accounting Research; Chapman, C., Hopwood, A.G., Shields, M.D., Eds.; Elsevier Science: Amsterdam, The Netherlands, 2009; Volume 3, pp. 1371–1383. [Google Scholar]

- Peralta, H.; Costa, F.A. Competência e confiança dos professores no uso das TIC. Síntese de um estudo internacional. Sísifo 2016, 3, 77–86. [Google Scholar]

- Lutilsky, I.D.; Dragija, M. Activity based costing as a means to full costing—Possibilities and constraints for European universities. J. Contemp. Manag. Issues 2012, 1, 33–57. [Google Scholar]

- Carvalho, J.; Costa, T.C.; Macedo, N. A contabilidade analítica ou de custos no sector público administrativo. Rev. OTOC 2008, 96, 30–41. [Google Scholar]

- Valderrama, T.G.; Sanchez, R.D. Development and implementation of a university costing model. J. Public Money Manag. 2006, 26, 251–255. [Google Scholar] [CrossRef]

- Hernández, A.L.; Díaz, D.C.; Toledano, D.S.; Ramos, D.Á.; Angulo, J.G.; Armenteros, J.H.; Martínez, V.J. Livro Blanco de Los Costes en Las Universidades, 3rd ed.; Oficina de Cooperación Universitaria, S.A.: Madrid, Spain, 2010. [Google Scholar]

- Keel, G.; Savage, C.; Rafiq, M.; Mazzocato, P. Time-driven activity-based costing in health care: A systematic review of the literature. Health Policy 2017, 121, 755–763. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Porter, M.E. How to solve the cost crisis in health care. Harv. Bus. Rev. 2011, 89, 47–64. Available online: https://www.vbhc.nl/wp-content/uploads/2021/10/Robert-S.-Kaplan-Michael-E.-Porter-How-to-Solve-The-Cost-Crisis-In-Health-Care-Harvard-Business-Review-2011.pdf (accessed on 10 November 2023).

- Small, H. Co-citation in the scientific literature: A new measure of the relationship between two documents. J. Assoc. Inf. Sci. Technol. 1973, 24, 265–269. [Google Scholar] [CrossRef]

- Smiraglia, R.P. ISKO 11’s diverse bookshelf: An editorial. Knowl. Organ. 2011, 38, 179–186. [Google Scholar] [CrossRef]

- Bellardo, T. The use of co-citations to study science. Libr. Res. 1980, 2, 231–237. [Google Scholar]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E.; Tatham, R.L. Análise Multivariada de Dados; Bookman: Porto Alegre, Brazil, 2009. [Google Scholar]

- Cooper, R.; Kaplan, R.S. Measure costs right: Make the right decisions. Harv. Bus. Rev. 1988, 66, 96–103. [Google Scholar]

- Pernot, E.; Roodhooft, F.; Van den Abbeele, A. Time-Driven Activity-Based Costing for Inter-Library Services: A Case Study in a University. J. Acad. Librariansh. 2007, 33, 551–560. [Google Scholar] [CrossRef]

- Siguenza-Guzman, L.; den Abbeele, A.; Vandewalle, J.; Verhaaren, H.; Cattrysse, D. Using time-driven activity-based costing to support library management decisions: A case study for lending and returning processes. Libr. Q. 2014, 84, 76–98. [Google Scholar] [CrossRef]

- Kont, K.R.; Jantson, S. Cost accounting and managerial accounting for reducing the impacts of financial crisis in university libraries: The case of the Baltic states. Soc. Sci. 2012, 77, 88–96. [Google Scholar] [CrossRef]

- Coney, D. Management in college and university libraries. Libr. Trends 1952, 1, 83–94. [Google Scholar]

- Gupta, M.; Galloway, K. Activity-based costing/management and its implications for operations management. Technovation 2003, 23, 131–138. [Google Scholar] [CrossRef]

- Cooper, R.; Kaplan, R.S. Activity-based systems: Measuring the costs of resource usage. Account. Horiz. 1992, 6, 1–13. [Google Scholar]

- Kaplan, R.S.; Anderson, S.R. Time-driven activity-based-costing. Havard Bus. Rev. 2004, 82, 131–138, 150. [Google Scholar] [CrossRef]

- McLaughlin, N.; Burke, M.A.; Setlur, N.P.; Niedzwiecki, D.R.; Kaplan, A.L.; Saigal, C.; Mahajan, A.; Martin, N.A.; Kaplan, R.S. Time-driven activity-based costing: A driver for provider engagement in costing activities and redesign initiatives. Neurosurg. Focus 2014, 37, E3. [Google Scholar] [CrossRef]

- Chan, Y.C.L. Improving hospital cost accounting with activity-based costing. Health Care Manag. Rev. 1993, 18, 71–77. [Google Scholar] [CrossRef]

- Laurila, J.; Suramo, I.; Brommels, M.; Tolppanen, E.-M.; Koivukangas, P.; Lanning, P.; Standertskjöld-Nordenstam, C.-G. Activity-based costing in radiology: Application in a pediatric radiological unit. Acta Radiológica 2000, 41, 189–195. [Google Scholar] [CrossRef]

- Cohen, M.D.; Hawes, D.R.; Hutchins, G.D.; McPhee, W.D.; LaMasters, M.B.; Fallon, R.P. Activity-based cost analysis: A method of analyzing the financial and operating performance of academic radiology departments. Radiology 2000, 215, 708–716. [Google Scholar] [CrossRef]

- Suthummanon, S.; Omachonu, V.K.; Akcin, M. Applying activity-based costing to the nuclear medicine unit. Health Serv. Manag. Res. 2005, 18, 141–150. [Google Scholar] [CrossRef]

- Baker, J.J. Activity-Based Costing and Activity-Based Management for Health Care; Jones & Bartlett Learning: Burlington, MA, USA, 1998. [Google Scholar]

- Lievens, Y.; van den Bogaert, W.; Kesteloot, K. Activity-based costing: A practical model for cost calculation in radiotherapy. Int. J. Radiat. Oncol. Biol. Phys. 2003, 57, 522–535. [Google Scholar] [CrossRef]

- Edbrooke, D.L.; Stevens, V.G.; Hibbert, C.L.; Mann, A.J.; Wilson, A.J. A new method of accurately identifying costs of individual patients in intensive care: The initial results. Intensive Care Med. 1997, 23, 645–650. [Google Scholar] [CrossRef]

- Laviana, A.A.; Ilg, A.M.; Veruttipong, D.; Tan, H.J.; Burke, M.A.; Niedzwiecki, D.R.; Kupelian, P.A.; King, C.R.; Steinberg, M.L.; Kundavaram, C.R.; et al. Utilizing time-driven activity-based costing to understand the short-and long-term costs of treating localized, low-risk prostate cancer. Cancer 2016, 122, 447–455. [Google Scholar] [CrossRef]

- Ellis-Newman, J. Activity-based costing in user services of an academic library. Libr. Trends 2003, 51, 333–348. [Google Scholar]

- Marlina, E.; Tjahjadi, B.; Ningsih, S. Factors affecting student performance in e-learning: A case study of higher education institutions in Indonesia. J. Asian Financ. Econ. Bus. 2021, 8, 993–1001. [Google Scholar]

- Kawamoto, T.; Ura, T.; Nittono, H. Intrapersonal and interpersonal processes of social exclusion. Front. Neurosci. 2015, 9, 62. [Google Scholar] [CrossRef]

- Van de Werf, E.; Verstraete, J.; Lievens, Y. The cost of radiotherapy in a decade of technological evolution. Radiother. Oncol. 2012, 102, 148–153. [Google Scholar] [CrossRef]

- Mitchell, G.J. Clarifying the contributions of qualitative research findings. Nurs. Sci. Q. 1996, 9, 143–144. [Google Scholar] [CrossRef]

- Cropper, P.; Cook, R. Developments: Activity-Based Costing in Universities—Five Years On. Public Money Manag. 2000, 20, 61–68. [Google Scholar] [CrossRef]

- Goddard, A.; e Ooi, K. Custeio baseado em atividades e alocação central de custos indiretos em universidades: Um estudo de caso. Dinheiro Público Gestão 1998, 18, 31–38. [Google Scholar]

- Kont, K.-R. How to optimize the cost and time of the procurement process? Collect. Build. 2015, 34, 41–50. [Google Scholar] [CrossRef]

- Kont, K. How much does it cost to catalog a document? A case study in Estonian university libraries. Cat. Classif. Q. 2015, 53, 825–850. [Google Scholar] [CrossRef]

- Kont, K.-R. What do acquisition activities really cost? A case study in Estonian university libraries. Libr. Manag. 2015, 36, 511–534. [Google Scholar] [CrossRef]

- Kont, K.-R. To buy or to borrow? Evaluating the cost of an eBook in TalTech library. Bottom Line 2020, 33, 74–93. [Google Scholar] [CrossRef]

- Kont, K.-R. If Time and Money Matters: EBook Program Challenges in Tallinn University of Technology Library. Slav. East Eur. Inf. Resour. 2021, 22, 170–196. [Google Scholar] [CrossRef]

- Kont, K.R.; Jantson, S. Activity-based costing (ABC) and time-driven activity-based costing (TDABC): Applicable methods for university libraries? Evid. Based Libr. Inf. Pract. 2011, 6, 107–119. [Google Scholar] [CrossRef]

- Declerck, B.; Swaak, M.; Martin, M.; Kesteloot, K. Activity-based cost analysis of laboratory tests in clinical chemistry. Clin. Chem. Lab. Med. 2021, 59, 1369–1375. [Google Scholar] [CrossRef]

- Lievens, Y.; Kesteloot, K.; Van den Bogaert, E. Charting in lung cancer: Economic evaluation and incentives for implementation. Radiother. Oncol. 2005, 75, 171–178. [Google Scholar] [CrossRef]

- Demoulin, L.; Kesteloot, K.; Penninckx, F. A cost comparison of disposable vs reusable instruments in laparoscopic cholecystectomy. Surg. Endosc. 1996, 10, 520–525. [Google Scholar] [CrossRef]

- Tseng, P.; Kaplan, R.S.; Richman, B.D.; Shah, M.A.; Schulman, K.A. Administrative Costs Associated with Physician Billing and Insurance-Related Activities at an Academic Health Care System. JAMA 2018, 319, 691–697. [Google Scholar] [CrossRef]

- Haas, D.A.; Kaplan, R.S. Variation in the cost of care for primary total knee arthroplasties. Arthroplast. Today 2017, 3, 33–37. [Google Scholar] [CrossRef]

- Anzai, Y.; Heilbrun, M.E.; Haas, D.; Boi, L.; Moshre, K.; Minoshima, S.; Kaplan, R.; Lee, V.S. Dissecting Costs of CT Study: Application of TDABC (Time-Driven Activity-Based Costing) in a Tertiary Academic Center. Acad. Radiol. 2017, 24, 200–208. [Google Scholar] [CrossRef]

- Bobade, R.A.; Helmers, R.A.; Jaeger, T.M.; Odell, L.J.; Haas, D.A.; Kaplan, R.S. Time-driven activity-based cost analysis for outpatient anticoagulation therapy: Direct costs in a primary care setting with optimal performance. J. Med. Econ. 2019, 22, 471–477. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Description | Results | Description | Results |

|---|---|---|---|

| Main Information about Data | Main Information about Data | ||

| Timespan | 1991:2021 | AUTHORS | |

| Sources (Journals, Books, etc.) | 121 | Authors | 502 |

| Documents | 139 | Author Appearances | 577 |

| Average years from publication | 9.59 | Authors of single-authored documents | 15 |

| Average citations per document | 8.771 | Authors of multi-authored documents | 487 |

| Average citations per year per doc | 0.9289 | AUTHORS COLLABORATION | |

| References | 3514 | Single-authored documents | 19 |

| DOCUMENT TYPES | Documents per Author | 0.279 | |

| article | 139 | Authors per Document | 3.59 |

| DOCUMENT CONTENTS | Co-Authors per Documents | 4.12 | |

| Keywords Plus (ID) | 800 | Collaboration Index | 4.02 |

| Authors Keywords (DE) | 407 |

| Article | Cluster |

|---|---|

| Cooper and Kaplan (1988) [59] | 1 |

| Pernot et al. (2007) [60] | 1 |

| Siguenza–Guzman et al. (2014) [61] | 1 |

| Kont and Jnatson (2012) [62] | 1 |

| Coney (1952) [63] | 1 |

| Gupta and Galloway (2003) [64] | 1 |

| Cooper and Kaplan (1992) [65] | 1 |

| Kaplan et al. (2004) [66] | 2 |

| Mclaughlin et al. (2014) [67] | 2 |

| Chan (1993) [68] | 3 |

| Laurila et al. (2000) [69] | 3 |

| Cohen et al. (2000) [70] | 3 |

| Suthummanon et al. (2005) [71] | 3 |

| Baker (1998) [72] | 3 |

| Lievens et al. (2003) [73] | 3 |

| Edbrooke et al. (1997) [74] | 3 |

| Article | Component 1 | Component 2 | Component 3 | Cluster |

|---|---|---|---|---|

| Cooper and Kaplan (1988) [59] | 0.968 | −0.172 | −0.106 | 1 |

| Pernot et al. (2007) [60] | 0.967 | −0.187 | −0.114 | 1 |

| Siguenza–Guzman et al. (2014) [61] | 0.964 | −0.223 | −0.101 | 1 |

| Kont and Jantson (2012) [62] | 0.959 | −0.206 | −0.095 | 1 |

| Coney (1952) [63] | 0.951 | −0.205 | −0.118 | 1 |

| Gupta and Galloway (2003) [64] | 0.947 | −0.244 | −0.114 | 1 |

| Cooper and Kaplan (1992) [65] | 0.941 | −0.189 | −0.080 | 1 |

| Chan (1993) [68] | 0.639 | −0.165 | −0.120 | 1 |

| Laurila et al. (2000) [69] | 0.627 | 0.035 | −0.113 | 1 |

| Cohen et al. (2000) [70] | −0.130 | 0.978 | −0.032 | 3 |

| Suthummanon et al. (2005) [71] | −0.172 | 0.977 | −0.021 | 3 |

| Baker (1998) [72] | −0.165 | 0.962 | −0.026 | 3 |

| Lievens et al. (2003) [73] | −0.274 | 0.936 | −0.003 | 3 |

| Edbrooke et al. (1997) [74] | −0.281 | 0.923 | 0.001 | 3 |

| Kaplan et al. (2004) [66] | −0.281 | 0.923 | 0.001 | 3 |

| Mclaughlin et al. (2014) [67] | −0.021 | 0.884 | −0.041 | 3 |

| Cooper and Kaplan (1988) [59] | −0.192 | −0.048 | 0.980 | 2 |

| Pernot et al. (2007) [60] | −0.193 | −0.048 | 0.971 | 2 |

| Siguenza–Guzman et al. (2014) [61] | −0.193 | −0.048 | 0.971 | 2 |

| Cluster 1 |

|

| |

| |

| |

| |

| |

| |

| Cluster 2 |

|

| Cluster 3 |

|

| |

| |

| |

| |

|

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Borges, P.; Alves, M.d.C.; Silva, R. The Activity-Based Costing System Applied in Higher Education Institutions: A Systematic Review and Mapping of the Literature. Businesses 2024, 4, 18-38. https://0-doi-org.brum.beds.ac.uk/10.3390/businesses4010002

Borges P, Alves MdC, Silva R. The Activity-Based Costing System Applied in Higher Education Institutions: A Systematic Review and Mapping of the Literature. Businesses. 2024; 4(1):18-38. https://0-doi-org.brum.beds.ac.uk/10.3390/businesses4010002

Chicago/Turabian StyleBorges, Pedro, Maria do Céu Alves, and Rui Silva. 2024. "The Activity-Based Costing System Applied in Higher Education Institutions: A Systematic Review and Mapping of the Literature" Businesses 4, no. 1: 18-38. https://0-doi-org.brum.beds.ac.uk/10.3390/businesses4010002