ICO vs. Equity Financing under Imperfect, Complex and Asymmetric Information

Adam Smith Business School, College of Social Science, University of Glasgow, Glasgow G128QQ, UK

FinTech 2024, 3(1), 17-39; https://0-doi-org.brum.beds.ac.uk/10.3390/fintech3010002

Submission received: 30 October 2023

/

Revised: 9 December 2023

/

Accepted: 15 December 2023

/

Published: 27 December 2023

Abstract

:This paper offers a game-theoretic model of a firm that raises funds for financing an innovative business project and chooses between ICO (initial coin offering) and equity financing. The model is based on information problems associated with both ICO and equity financing well-documented in the literature. Several new features are introduced, for example, information complexity, which is analyzed along with a more traditional imperfect information and an asymmetric information approach. The model provides several implications that have not yet been tested. For example, we find that the message complexity can be beneficial for firms conducting ICOs. Also, high-quality projects can use ICO as a signal of quality. Thirdly, the average size of projects undertaking equity financing is larger than that of firms conducting ICO.

Keywords:

asymmetric information; complex information; initial coin offering (ICO); equity financing; signalingJEL Classification:

D82; G32; L11; L26; M131. Introduction

The importance of imperfect information for firms raising funds for their investment projects is well recognized in theory and practice. For example, the pecking-order theory of capital structure [1] predicts that under asymmetric information, firms should use internal funds to avoid information-related cost associated with external financing and in the absence of internal funds they should use debt. Equity should only be used as a last resort when no other options are available and high-quality firms should not issue equity. This theory can be applied to public issues of securities as well as to other forms of financing such as entrepreneurial finance including venture capital finance (see, for example, [2,3]).

Imperfect information is also very important for newly created ways of raising funds such as initial coin offerings (ICOs) (see, for example, [4]). Interestingly though, emerging papers on ICO find differences between empirical evidence surrounding equity financing and ICOs. For example, in the case of an ICO, buyers of tokens enjoy on average higher rates of return after issue [5]—see also [6,7]—that focuses on connections between token returns and volatility than in the case of IPO (initial public offering) and we do not observe a long-term underperformance of ICO firms as compared to IPO firms, at least to the same extent. For IPO evidence see, e.g., a review by [8]. The average rates of return for ICO investors are higher than the rates of return on venture capital. Ref. [5] found that the average rate of return for an ICO is 78% while the average required rates of return for VC investors are between 20 and 40% (see, for example, [9]).

In this paper, we take a closer look at a comparison of equity financing and ICO under asymmetric information and aim to analyze the following research question: can the concept of information complexity be helpful in analyzing the entrepreneur’s choice of financing? First, the ICO is a much more recent phenomenon than traditional equity financing, so most investors are less familiar with it; secondly, ICOs require that the firm is connected to a blockchain which is often argued to be one of the most sophisticated business innovations of 21st century and further industries or sectors that raise most funds using ICOs are related to fintech/hightech known for employing/developing most progressive and innovative products and services; for example, in [10] the top four sectors are blockchain platform and services, finance, trading and investing, data, AI and machine learning and payments, wallets and cryptocurrencies. Finally, from a pure financial theory point of view, an ICO is not only a new way of financing per say, but it is also quite different from traditional ways of financing in some of its core features, for example the right of using tokens for both creating capital gains and also purchasing firm future products and services. Further recent work by [11] conducts surveys among entrepreneurs considering an ICO and finds that in their opinion investors indeed lack an understanding of modern technologies related to ICO: “Simply because they [VC (venture capitalists)] lack the understanding of how blockchain technology works. Even today, still, they do not understand it.” [11] (p. 1047). Furthermore, Ref. [12] measure the degree of ICO complexity and find that complexity does indeed matter for ICOs and affects their outcome. So, in this paper, we aim to understand if the model which is based on imperfect, asymmetric and complex information can provide new insights into our understanding of an entrepreneur’s choice of financing and shed new light on some empirical evidence discussed in the previous paragraph. We also aim to explore if it helps to explain signaling opportunities for entrepreneurs using ICOs since they have been one of the most important topics in financing literature; as we know, in traditional financing literature, a signaling equilibrium usually does not exist because low quality firms mimic high-quality firms.

We argue that significant differences exist between pecking-order theory and theories of ICO. In particular, we argue that high-quality firms can use an ICO as a signal. The reason is that prices, production decisions and other parameters arising in equilibrium for a high-quality firm may not be suitable for a bad quality firm if the latter decides to mimic the high-quality firm. An ICO is a more complex phenomenon than an equity issue. Under equity issue, mimicking happens because the market relationship/negotiations between a firm and investors are strongly dominated by one parameter, i.e., the firm share price, where a higher share price of high-quality firm attracts low-quality firms. Under ICO, equilibrium parameters of the market relationship between the firm and investors are multi-dimensional and are strongly affected by at least two parameters: token price and product price. Regarding ICO complexities note that ref. [13] mentioned that an ICO is a complex phenomenon. We show that in these conditions, mimicking a good firm might not necessarily be profitable for a bad quality firm even if one of the parameters may have a higher value for high-quality firm.

Blockchain-based ICOs promised to provide a new source of financing for innovative firms. The ICO phenomenon dates back to 2013. Since then, the number and funding of projects have been growing exponentially, with over $20 billion raised by December 2018 [14]. ICO research is also quickly growing; for theoretical papers on ICOs see, among others, [15,16,17,18,19,20,21,22,23]. Including the choice between ICO and traditional equity financing seems to be a very important issue for many entrepreneurs. See, for example, https://blog.polymath.network/minthealth-and-polymath-bring-the-first-healthcare-security-token-to-revolutionize-healthcare-a36884f17e4e; https://www.theblockcrypto.com/2019/06/04/a-conversation-with-carlos-domingo-ceo-and-co-founder-securitize/ (accessed on 1 December 2023). Several directions seem to be emerging, including models based on agency cost and moral hazard (see, e.g., [14,24,25]); network effects of tokens (see, e.g., [16,26]). In this article, we offer a model of a choice between ICO and equity financing under imperfect information and analyze what drives firms to use ICO and issue tokens as compared to more traditional equity financing and what empirical predictions can be generated from this analysis. The closest paper to ours is probably that of [27]. In that paper, firms choose between ICO and venture capital financing. It is assumed that asymmetric information between entrepreneurs and investors exists only in the case of ICO but not in the case of venture capital financing. When the extent of asymmetric information is relatively small, there exists a separating equilibrium, in which the low types choose ICO on better terms than high types that retain a larger portion of tokens than they would under perfect information. The entrepreneur uses the number of retained tokens as a costly signal of firm quality. If the degree of asymmetric information is relatively large, some high-quality entrepreneurs, who would prefer an ICO in a low-information-asymmetry environment, prefer venture capital financing. This implies that in the presence of high information asymmetry, ICOs are expected to be less prevalent and of lower quality on average. Ref. [27] use a similar idea to [28], where an entrepreneur signals their quality by retaining a larger fraction of equity in the firm and reducing external issue of equity and respectively increasing debt. In [27], an entrepreneur retains a larger fraction of tokens and reduces external issue of tokens. Our model takes more ideas from [1] pecking-order theory. Asymmetric information and signaling effect differ for different types of financing (debt vs. equity in [1]; ICO vs. equity in our model) because of different payoff structures for investors. Also in contrast to [27], in the present paper, asymmetric information exists under both ICO and equity financing that is consistent with the spirit of empirical evidence. In addition, we introduce information uncertainty (demand uncertainty) where firms can use tokens to learn market demand and also consider information complexity.

In our model, an entrepreneur with an innovative idea considers launching a web-based platform for an infinite number of periods. The demand for the product is highly uncertain. Tokens give the right to purchase a product or service on the platform. Issuing tokens (ICO) helps the firm learn the demand and improve its decision-making including production (pricing) decisions. It is similar to learning market demand ideas from reward-based crowdfunding (see, e.g., [29,30,31]); it is also similar to acquiring new customers ideas behind complimentary currencies (see, e.g., [32]). The success of the campaign also depends on the demand shock that reflects the public perception of the message provided by the firm. Given the blockchain nature of ICOs, their message to investors is typically more complex than traditional equity financing that is more familiar for the majority of investors. So the shortcoming of tokens is a higher degree of complexity compared to traditional equity financing. If the public does not understand some aspects of blockchain technology or some aspects of ICO offered by the firm or if the message seems to be too complex, it can result in market mistrust towards the firm that ultimately leads to the campaign failure. This is in line with, for example, Refs. [33,34] who find that ICOs with higher levels of transparency are more likely to succeed.

We first analyze firm choice between ICO and equity financing under symmetric information. We find that the [35] proposition holds, i.e., the firm is indifferent between ICO and equity financing if the amount of start-up investments is not large enough. Otherwise the firm should prefer equity financing. The reason is that, in contrast to tokenholders, equityholders can count on firm long-term profit. We also find that the token price increases after the initial issue of tokens. We then analyze the case with demand uncertainty and show that the choice between ICO and equity financing depends on the trade-off between the degree of demand uncertainty (higher uncertainty favors ICO since in this case it provides more benefits for entrepreneurs in terms of learning market demand) and the message complexity. A higher level of complexity and risk of campaign failure makes an ICO less desirable. Finally, we analyze the case with asymmetric information and argue that unlike traditional equity financing, ICO can be used by high-quality firms as a signal of quality.

Our model provides several predictions, most of which have not been tested as of yet. For example, we find that the message complexity can be beneficial for firms conducting ICOs. Although a detailed empirical analysis of this prediction has not been performed, it is consistent with the spirit of [12] that find that the whitepaper (analogous to a prospectus of the issue in the case of an IPO) complexity is positively related to the amount raised during an ICO. Also, high-quality projects can use an ICO as a signal of quality. Thirdly, the average size of projects undertaking equity financing is larger than that of firms conducting ICOs. Forth, our model predicts that signaling opportunities exist when the degree of complexity associated with ICO is not too small nor too large. Fifth, under an ICO, the token’s market price significantly increases shortly after the issue as compared to the initial token price. Finally, we show that ICO will be preferred if the degree of uncertainty regarding market demand is relatively high. Most of these predictions have not been directly tested.

The rest of the paper is organized as follows. Section 2 describes the basic model and some preliminary results. Section 3 provides an analysis for the model with imperfect information and demand uncertainty. Section 4 considers the case with asymmetric information. Section 5 discusses the consistency of the model’s predictions with observed empirical evidence. Section 6 discusses the model’s robustness and its potential extensions and Section 7 provides a conclusion to the study.

2. Basic Model

An innovative firm seeks funds to create a website platform for selling a product/service for an infinite number of periods. The initial start-up fixed cost equals I. During the operational stages of the platform, if the firm produces units, it costs in total. c equals with probability or with probability , . means that the cost of production is low (high-quality firm) and means that the cost of production is high (bad-quality firm). c is the entrepreneur’s private information. The demand for the product in period n is expected to be driven by the following demand function: , where is the price at period n. equals with probability or with probability , . means that the demand is high and means that the demand is low. Let be the firm’s operational profit in period n and is the discount factor. Additionally, is the present value of the firm’s earnings. The calculations of as well as the way the firm’s earnings will be distributed depend on the firm’s financing strategy. The firm needs funds to cover its start-up costs and chooses between equity financing (we do not focus on any specific form of equity financing, e.g., venture capital, friends’ investments, IPO, etc., but rather use just general aspects of equity financing. In Section 6 we discuss the model predictions with regard to specific forms of equity financing) and ICO.

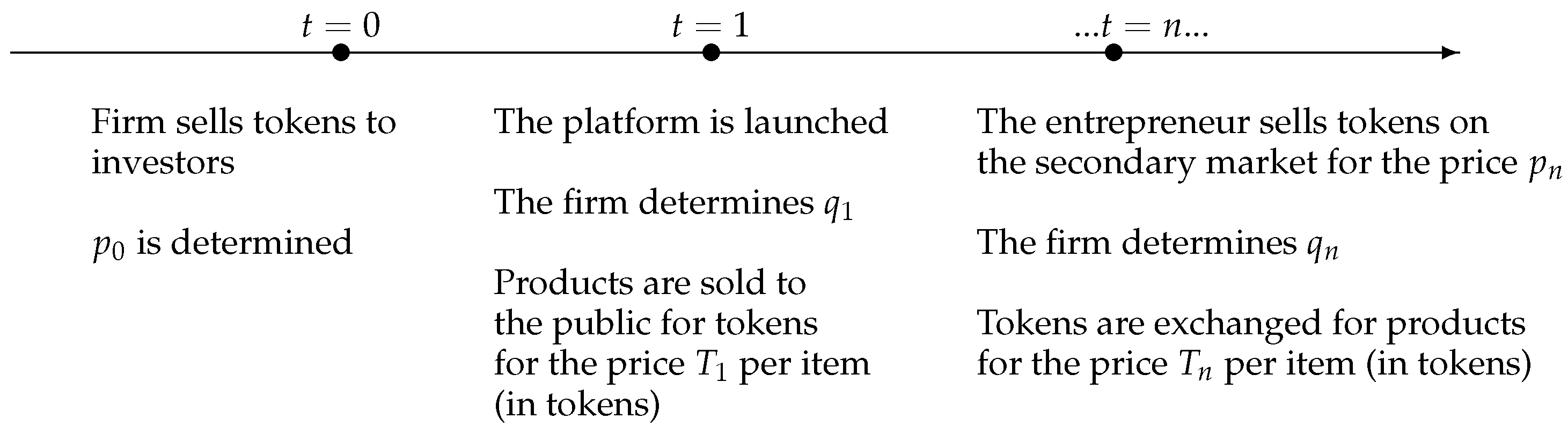

Under ICO, the firm sells tokens for the price . (They can be paid for with fiat money and cryptocurrencies such as Bitcoin, Ether, etc.) The total number of tokens is normalized to unity without the loss of generality. After tokens are sold, the entrepreneur receives information about the demand in period 1 and uses the proceeds from selling to cover firm start-up costs and the first-period production costs. The platform is launched. In each period, the entrepreneur sells tokens received for selling the product in the previous period. After that the firm makes its production decision . ICO participants buy products offered by the firm using tokens. We assume that in period 1 (after the initial sale of tokens) demand is as follows: , where with probability and 0 with probability . is the demand ”demand shock”, “information quality shock” or “complexity shock”, etc. If , the product is considered as too complex by the market and the demand for the firm’s product does not exist.

Under equity financing, the firm sells a fraction of the firm. After that the platform is launched for an infinite number of periods. In each period, the firm produces its products/services and sells them to the public. The firm’s earnings are distributed pro-rata according to the number of shares owned by each shareholder.

All variables are described in Table 1.

Initially, the firm is owned by an entrepreneur. Investors/funders and entrepreneurs are assumed to be risk-neutral and the risk-free interest rate is 0.

First consider the symmetric information case without demand uncertainty, i.e., suppose that a is known and that market participants are able to perfectly read the firm message if ICO is chosen, i.e., . Also, c is public knowledge.

2.1. ICO

The timing of events is presented in Figure 1.

We begin the solution by working backwards. Consider the operational stage. In period n, the entrepreneur sells tokens for the price . Theoretically, the firm can also spot sale products and stop reselling tokens. One can show that is not an optimal strategy when the market demand is uncertain (see Section 4). Under symmetric information, this strategy would lead to same outcome as with tokens so we omit it for brevity. This strategy becomes important to consider under asymmetric information. We will discuss it in Section 5. After tokens are sold, the firm determines . Tokenholders then use their tokens to buy products. Equilibrium is determined by the following conditions: (1) after selling tokens the firm maximizes its profit, which equals (production-incentive constraint)

(2) demand equilibrium:

where is the cost of the product for the public:

(i.e., the cost of tokens for consumers () equals the cost of products offered by the entrepreneur taking into account the demand function). Taking into account (1) and (2), the entrepreneur’s objective function can be written as . The optimal equals

and the entrepreneur’s profit (in tokens) equals:

From (1) and (3) we have:

From (2) we obtain:

Token market equilibrium (supply equals demand) is described by the following condition:

This implies:

The present value of the firm’s profits equals and the present value of the entrepreneur’s earnings equals

The second term is substructed because the entrepreneur does not sell tokens during period 1 (it is performed in period 0 because the entrepreneur needs to cover investment cost I as well as the production cost in period 1).

In period 1, equilibrium is determined by the following conditions: (1) the firm maximizes its profit, which equals (production-incentive constraint)

(2) demand equilibrium:

where is the cost of the product for the buyers of tokens in period 0:

The second term reflects the need of the firm to cover its start-up cost. It equals and not I because initial buyers of tokens will not be able to consume firm products at the same period but at the next period so the real cost for them is higher and takes into account the discount factor. Taking into account (6) and (7), the entrepreneur’s objective function can be written as . The optimal equals

From (6) and (8) we have:

From (7) we obtain:

Token market equilibrium (supply equals demand) is described by the following condition:

This implies:

Note that the initial value of tokens is lower (comparing (4) and (9)) compared to further periods. Also note that an ICO is only feasible if

Otherwise we will have a corner solution with ( should be non-negative).

Note that we assume that tokens will be exchanged for products next period after they purchased by buyers. One can assume that buyers hold their tokens longer. It will not change our result qualitatively but quantitatively the condition (10) may change depending on assumption about the average velocity of tokens.

2.2. Equity Financing

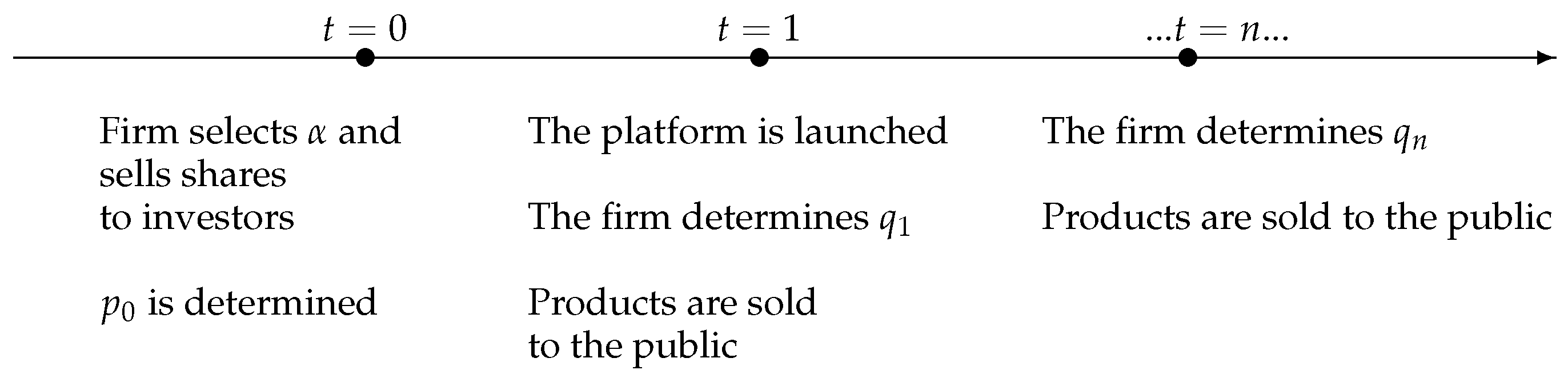

The timing of events is presented in Figure 2.

Consider the operational stage. In period n there are items produced. The firm’s objective function can be written as . The optimal q equals

and the entrepreneur’s profit equals:

The present value of the entrepreneur’s profits equals

The investors’ expected earnings should cover their investment cost or:

Under optimal solution the condition (14) will be binded because the firm can always make as small as necessary to satisfy them. Then we have:

Substituting this into (13), we find that the entrepreneur’s expected profit equals:

As we can see, this is the same amount as in (12). This is not surprising given that in the absence of any financial market imperfections every type of financing should have the same result (similar to [35]) as long as they fit into the budget constraints.

Lemma 1.

(1) If

the firm is indifferent between ICO and equity financing; (2) if , the firm should select equity financing; (3) if , the project is worthless.

Proof.

Lemma 1 shows that equity financing has a “technical” advantage for large projects (high fixed costs I and high variable costs c). Since our focus is on the role of market imperfections, we will usually assume that condition (15) holds. In this case, both types of financing are feasible.

Lemma 1 has several empirical implications. If (15) does not hold, equity financing will be chosen. The likelihood of this condition to hold decreases with larger I, larger c, smaller a and higher . It means that the likelihood of using an ICO decreases with the size of the project, the cost of production, and time value of money, inflation rate, etc. and increases with demand. Firms select equity financing mostly for the possibility of collecting large amounts of capital.

Lemma 2.

Under an ICO, token’s market price is higher in period 2 compared to period 1.

3. Imperfect Information

In the previous section, the demand function was known with certainty. In this section, information about demand is imperfect, i.e., the firm faces demand uncertainty where a can have either low or high value and secondly, in the case of ICO a complexity shock is possible. If the latter is the case, the demand for tokens is absent and the campaign fails.

3.1. ICO

The timing of events is similar to that on Figure 1. The difference is that after issuing tokens the firm learns about the demand.

We begin the solution by working backwards. Consider the operational stage. In period n, the entrepreneur sells tokens for the price . After tokens are sold, the firm determines . Tokenholders then use their tokens to buy products. Equilibrium is determined by the following conditions: (1) after selling tokens the firm maximizes its profit, which equals (production-incentive constraint)

(2) demand equilibrium:

where is the cost of the product for the public:

Taking into account (16) and (17), the entrepreneur’s objective function can be written as . The optimal equals (note that by the time the production decision should be made, tokens are sold and is determined)

and the entrepreneur’s profit (in tokens) equals:

From (16) and (18) we have:

This implies a non-arbitrage condition for consumers (i.e., the cost of tokens for consumers () equals the cost of products offered by the entrepreneur taking into account the demand function):

Token market equilibrium (supply equals demand) is described by the following condition:

This implies:

The expected value of firm’s profit in period n, is

The present value of the firm’s profits in periods equals

The second term is substructed because we have not counted firm profit in period that is considered below.

In period 1 the demand is as follows: , where with probability and 0 with probability . is the demand “shock”. If , the demand for the firm’s product does not exist. Equilibrium is determined by the following conditions: (1) the firm maximizes its profit, which equals (production-incentive constraint)

(2) demand equilibrium:

where is the cost of the product for the buyers of tokens in period 0:

Taking into account (21) and (22), the entrepreneur’s objective function can be written as . The optimal equals (note that by the time the production decision should be made, tokens are sold and is determined)

From (21) and (8) we have:

This implies a non-arbitrage condition for consumers (i.e., the cost of tokens for consumers () equals the cost of products offered by the entrepreneur taking into account the demand function plus the amount of investments multiplied by because it takes into account that tokens were sold in period 0):

Token market equilibrium (supply equals demand) is described by the following condition:

This implies:

The present value of the firm’s profits equals the sum of (20) and the present value of (24):

3.2. Equity Financing

The timing of events is similar to that in Figure 2.

Consider the operational stage. In period n there are items produced. The firm’s objective function can be written as . The optimal q equals

and the entrepreneur’s profit equals:

The present value of the entrepreneur’s profits equals

The investors’ expected earnings should cover their investment cost or:

Under the optimal solution, condition (28) will be binded because the firm can always make as small as necessary to satisfy them. Then we have:

Substituting this into (27), we find that the entrepreneur’s expected profit equals:

Proposition 1.

When information is imperfect and complex (demand uncertainty; complexity shock) but symmetric, the firm prefers ICO to equity financing if

Corollary 1.

The likelihood of using ICO/using IPO increases/decreases with .

Proof.

The derivative of RHS of (31) in c is negative implying that a higher c implies a lower value of RHS which in turns implies that it is more likely that RHS is smaller than LHS and an ICO is more likely than an IPO. □

Proposition 1 and Corollary 1 imply that the likelihood of using ICO vs. equity financing increases with lower probability of complexity shock (higher ), and increases/decreases with firm cost c/profitability.

4. Asymmetric Information

Signaling by Selecting ICO

In this section, asymmetric information exists regarding the cost of production. (In Section 6, an extension will be considered where asymmetric information concerns the cost of production). In particular, we assume that, unlike outside investors, firm owners know the value of c (production cost of their firm). There are two types of firms: for type h and for type b, where .

The timing of events is as previously except that at the beginning the firm’s type is revealed to the entrepreneur.

Proposition 2.

If , where

and

a separating equilibrium exists, where type selects ICO and type selects equity financing. An equilibrium where type selects equity financing does not exist.

Proof.

Consider a situation where type b selects equity financing and type g selects ICO. First we have

where is the equilibrium profit of type j (all calculations are based on the symmetric information case for each type described in the previous section). Suppose that b mimics g and chooses ICO. Since it is a multiperiod game, we have to consider different strategies of a firm when it decides to deviate from its equilibrium strategy and mimic another type. One approach is when the firm mimics the decisions of another firm in each period. Another strategy is when firm sells products directly to the public without issuing/reselling tokens. We start with the analysis of the first case. Since it is a separating equilibrium, the participants of the game (tokens buyers) continue to believe that the type is g when observing issue of tokens in any period. In this case, the profit of firm b in each period equals

for , where , and . Here, , and are exactly the same as they if type g uses ICO but in (34) is different from the profit of type g in equilibrium because the cost of production is different for type b. It implies:

and

Also

where , and . It implies:

□

Therefore the present value of the firm’s profits equals and the present value of the entrepreneur’s earnings equals

Comparing this with (33) we find that the latter is greater if

If it holds, b has no incentive to deviate.

Suppose that g mimics b and chooses equity financing. We have

where is determined by (29) and equals because the investors think that the type is b when observing equity financing. Using this in (36), we obtain:

Note that conditions (35) and (37) do not contradict each other. It is because the right side of (37) is smaller than that of (35). An example is illustrated in Figure 3.

One can see there is an area where both non-mimicking conditions hold. The analysis of other strategies is in fact very similar. In each period the firm’s decision to resell tokens or spot sell depends on the comparison of and . b will select the latter if

It is the same condition as (35) when . Two cases are possible. First, . In this case a separating equilibrium does not exist because b deviates and mimics g by issuing tokens each period. Second, . In this case it is more profitable for b to continue to resell tokens in each period. A separating equilibrium exists if (35) and (37) hold as discussed above. Third,

In this case, spot sales are more profitable for b than reselling tokens. So firm b would select spot sale in any which is the same payoff as under equity financing. So to compare profit from deviations and its equilibrium payoff we just need to compare its period 1 profits. In equilibrium it is and it deviates it is . The latter is smaller because (38) holds, so b does not deviate. To summarize: the crucial condition is (35). If it holds the analysis of all deviation strategies gives the same conclusion.

Now let us analyze a potential equilibrium where g selects equity financing and type b selects ICO. Similarly to the analysis above we find that non-mimicking conditions are:

An example is illustrated in Figure 4.

One can see that the the area where both non-mimicking conditions hold does not exist.

The right side of the inequality in Proposition 2 puts an upper bound on the probability of ICO success. The intuition behind this result is as follows. ICO is very costly if the probability that the ICO message is too complex is relatively high. In this case the low-quality firm will not mimic the high-quality firm. If, on the contrary, is very large, the low-quality firm would mimic the high-quality firm and benefit from the market’s optimistic belief about the quality of firms that use ICO. The left side of the inequality in Proposition 2 places a lower bound on the probability of ICO success. If, on the contrary, the probability that demand is absent is very high, it would be beneficial for the high-quality firm to not use ICO and deviate to equity financing. (Pooling equilibrium analysis is available upon request. It does not bring ay significant new results qualitatively).

5. Implications

Our paper has several implications for an entrepreneurial firm’s choice of financing.

Lemma 1 implies that the average size of ICO should be smaller than that of equity financing. For example, as documented in [4], the average size of ICO is between 13 and 16 mln $US while for example the average size of IPO is 108 million $US. (https://0-www-statista-com.brum.beds.ac.uk/statistics/251149/median-deal-size-of-ipos-in-the-united-states/ (accessed on 1 December 2023)).

Proposition 2 implies that high-quality projects may use ICO as a signal of quality. This prediction has not been directly tested but seems to be consistent with the spirit of [4,5,33,34] that suggest that in order to be successful, an ICO should meet high-quality standards including the quality of “whitepapers” (technical documentation describing ICO), good level of transparency, etc. It is also consistent with an idea that ICO are more likely to succeed if they use KYC or DAICO procedures that reduce the chances of fraud and ultimately increase the campaign quality. (KYC means “know-your-customer” procedure. It requires potential investors to disclosure their identity before letting them particpate in the campaign (see [4,6]). DAICO means Decentralized Autonomous ICO. It repesents a type of ICO with a smart contract that improves the control of token circulation and reduces the chances of fraud by founders (see [36]). To some extent this result is also similar to some results about reward-based crowdfunding which is similar to ICO in that investors have rights to purchase firm’s future product and also in that firms can use it to analyze market demand for their product, etc. [37,38] find that it can serve as a signal of a project’s quality. Furthermore, the entrepreneur’s larger fraction of equity is associated with a higher project quality [28]. In our case, ICO implies a higher fraction of ownership held by the entrepreneur. Similar results have been found with regard to equity-based crowdfunding. [37] examine the effectiveness of the signals used by entrepreneurs to induce (small) investors to commit financial resources in an equity-based crowdfunding context. They found that retaining equity is an effective signal and can therefore strongly impact the probability of a funding’s success. This result contrasts one in [27] where the signal is the fraction of tokens retained by the entrepreneur. In our case, issuing external tokens is a positive signal of firm’s quality rather than a negative one as in [27].

Lemma 2 implies that under an ICO, a token’s market price significantly increases shortly after issue compared to the initial token price. The interpretation of this result is as follows. The first issue of tokens should cover both fixed start-up cost and period 1 variable cost while all subsequent issues/resales of tokens will only cover variable costs in a given period. From the token buyers point of view, the amount of utility is the same in any period and is related to the quantity of products produced by the firm. This leads to a lower token price in period 1 that assures higher demand for tokens and compensates the firm for additional costs in period 1. Obviously, total net profit of the firm in period 1 will be lower as well, which is intuitive since it is a start-up firm. The prediction that the token price significantly increases from period 1 to period 2 has not been directly tested although it seems to be consistent with some evidence in [4,5] that show the token price growth after the initial issue (see also [36]). Interestingly, even though the price of tokens is lower in period 1 but the product price remains the same (in real terms) and the product price in tokens can be lower. It is interesting to compare product prices under ICO and equity financing. Our analysis predicts that if a signaling equilibrium exists then the real product price will be higher under ICO than under equity financing (comparing (19) and (26) and taking into account that good-quality firm uses ICO). The results of Lemma 2 can be tested by comparing the rates of return for ICO and equity financing. Although precise testing would include finding comparable firms, etc., some indirect evidence seems to be consistent with the predictions of Lemma 2. For example, it seems like in the case of an ICO buyers of tokens enjoy on average higher rates of return after issue [5] than in the case of IPO (initial public offering) and we do not observe long-term underperformance of ICO firms as compared to IPO firms [8] at least to the same extent. The average rates of return for ICO investors seem to be higher than for rates of return on venture capital. Ref. [5] find that the average rate of return for ICO is 78% while the average required rates of treturn for VC investors is between 20 and 40% (see, for example, [9]). Further evidence include [39] that finds a very significant underpricing of ICOs and comparatively higher levels of short-term return for investors.

With regard to other forms of equity financing, it is worth mentioning STO. Fintech companies started to use STOs to finance their projects in 2017. In contrast to utility tokens, security tokens are regulated. The legal structures continue to evolve. In the US, for example, the Securities and Exchange Commission (SEC) applies the Howey test to determine whether an asset qualifies as a security. Essentially, investments are considered securities if money is invested, the investment is expected to yield a profit, the money is invested in a common enterprise and any profit comes from the efforts of a promoter or third party (Ante and Fiedler (2019)). In security token offerings (STOs), companies sell tokenized traditional financial instruments, like, for example, equity where tokenholders receive rights on a firm’s future profits (see, e.g., [40]). The number of STOs is quickly growing. In January 2018, five STOs were conducted (monthly) while in November/December 2018 there were more than 20 per month and it continues to grow. (https://hackernoon.com/will-2019-be-the-year-of-the-sto-understanding-stos-security-tokens-market-potential-over-icos-4d2502227220 (accessed on 1 December 2023)). We have not found any research that directly compares the rates of return on ICO and STO. The following points are worth mentioning. First, the total amount of funds raised using ICO is much higher than that using STO (see, for example, https://www.pwc.ch/en/publications/2020/Strategy&_ICO_STO_Study_Version_Spring_2020.pdf (accessed on 1 December 2023)) that is consistent with the spirit of our findings (Proposition 2) that signaling opportunities prevail in ICO and that high-quality firms should not use equity financing including STO. Secondly, some research shows that low-quality signals are relevant in STO (see, for example, [40]).

Proposition 2 suggests that the existence of separating equilibrium is related to the value of . It implies that if the level of complexity/probability of ICO success should not be very low or very high. It means that some degree of risk/complexity can be beneficial. If signaling equilibrium does not exist, then equilibrium is pooling and as we know under pooling the payoff of high-quality type is significantly reduced because of underpricing. It can happen if complexity is absent/very low (very high ). However, if is in the range determined by Proposition 2 and signaling equilibrium exist, the payoff of the high-quality type can be higher. To some extent the result that some degree of risk of campaign failure is beneficial is also consistent with the spirit of the results in some empirical papers on crowdfunding in that higher targets do not necessarily signal a better quality. For example, Refs. [38,41] found that setting higher thresholds does not lead to higher campaign rates of success. Further research is required. Also we find that the message complexity can be beneficial for firms conducting ICOs. As was mentioned previously, this is consistent with the spirit of findings in [12]. Future research might be related to identifying and measuring the average level of complexity in different industries that may help generating some industry-specific predictions. Finally we show, for example, that the utility tokens will be preferred if the degree of uncertainty regarding market demand is higher (it increases the learning value of utility tokens). For example, if (the maximal level of demand uncertainty) RHS of condition (31) decreases and it is more likely to hold while when or (in either case there is no demand uncertainty), RHS equals 1 and so condition (31) does not hold.

Previous results are mostly related to ICO. With regard to equity issues, several interesting points are worth mentioning. Consider for example the link between equity issues and firm’s quality. A firm’s IPO decision has been one of the top issues in corporate finance theory. Over the years financial economists have formulated and tested various theories of IPO, including models based on asymmetric information, market timing, and many others. Despite the tireless efforts, this issue has not been completely resolved. Pecking-order theory [1], for example, predicts that only firms with low expected performance may issue equity. Therefore one should expect a negative correlation between the size of equity issues including IPO and post-offer performance. Signaling theory usually suggests that debt issues can be used as a positive signal of firms performance [28] as opposite to equity issues (negative signal). Refs. [42,43,44] analyze the long-run operating underperformance of equity issuing firms compared to non-issuing firms. This literature usually suggests that firms issuing equity underperform (at least in long term) that is indirectly consistent with negative correlation between IPO size and firm’s operating performance. Our model predicts that the likelihood of equity issue is positively correlated with firm performance (according to Proposition 1 and Corollary 1 if c decreases firms are more likely to issue equity) that is not directly consistent with traditional theories. It also provides an explanation for negative correlation between debt and profitability (a lower c increases the firm profitability/performance and increases the likelihood of IPO/equity issue which in turn (for a gven level of debt) leads to a lower debt/equity ratio) that is not consistent with standard theories of financing such as the trade-off theory (see, e.g., [45]) or mentioned above signaling theory. In standard models a signaling equilibrium usually does not exist (see, e.g., [1] or [46]) because a good quality firm is mimicked by a low quality firm. In our model a high quality firm will not necessarily be mimicked by a low quality firm. It may happen if a high-quality firm conducts an ICO campaign with some level of complexity/risk of failure making mimicking this firm unprofitable even for a low-quality firm.

6. The Model Extensions and Robustness

Asymmetric information about demand. Suppose that firms have the same cost, i.e., but receive a private signal about future demand for their products. One firm knows that and for another one . This is a less intuitive extension since a lot of informational aspects of the problems become unimportant in this setting but the main results remain. The high-quality firm will not be able to signal its quality by using equity financing and one the other hand if is low enough it should be able to signal its quality by using an ICO. A low-quality firm may find it unprofitable to mimic the high-quality firm in some cases.

Different demand functions. Our focus in this article is to analyze the role of asymmetric information for an ICO. That is why we adopt a relatively simple demand function. In the ICO literature (see, for example, [15]) or dynamic monopoly pricing literature, this approach is not unusual (see, for example, [47]). The intuitions behind our results (such as Propositions 1, 2, etc.) are general enough and will hold if mathematically different demand functions are used. Alternatively, a significantly different approach of modelling the demand side can be taken where individual customers with different demand functions are included. This approach is often used in crowdfunding literature such as [48,49]. This approach is also often used in industrial organization or price discrimination literature. As discussed in some literature (see, for example, [50]) adopting a more complicated demand function often leads to similar results.

One can also consider different types of “complexity shock” in the demand function. When considering ICO complexity, we usually assume that has only two values: 0 or 1. In other words, managers receive an “extreme” signal: either the degree of complexity is good and demand is “normal” or it is completely non-existent. One can consider an extension of the model where the demand is as follows: , where is distributed according to some density function , e.g., one can assume that uniformly distributed on . Here, again, we find that when information about market demand is uncertain but symmetric, the firm’s expected profit earnings are lower when ICO is used than when equity financing is used. It is similar to the result in Section 3. For the case with asymmetric information we found that depending on , two outcomes are possible. Either a separating equilibrium does not exist or there is a separating equilibrium, where type h selects ICO and type l selects equity financing. A separating equilibrium where h uses equity financing does not exist. With regard to a separating equilibrium where h plays ICO, note that if is such that the small values of q prevail then h is not interested in playing ICO. If however, is such that high values of q prevail then l is not interested in mimicking l. A separating equilibrium exists under some conditions similar to the spirit of Proposition 2.

Moral hazard. One can consider the need to introduce moral hazards in the model. The entrepreneurial moral hazard takes place because, for example, the entrepreneur’s equity stake in the firm is reduced while his individual effort is costly and this cost is not shared. This approach is very common in financing literature (starting with [51,52]). There are many different ways to analyze moral hazard issues with regard to firm financing choice but usually a result is that selecting a financing strategy that provides a higher fraction of equity to the decision-maker compared to other strategies of financing will be beneficial. See for example [25] with regard to the choice between token issues and equity financing (see also [14,24]). In [20,53] STO has an advantage compared to ICO due to entrepreneurial moral hazard in a model where the success of the firm depends not only on entrepreneurial effort but on the effort of miners as well who under STO can obtain some profit rights. Our analysis shows that combining asymmetric information with moral hazard definitely complicates calculations without bringing significantly new results.

Behavioural biases. The paper assumes rational investors and issuers so a possible direction for future research would be to incorporate behavioral aspects, e.g., investor’s overreaction or entrepreneurial overconfidence. In a similar spirit, Ref. [53] for example studied the effect of entrepreneurial overconfidence on a firm’s choice between equity-based crowdfunding and reward-based crowdfunding. For example, the entrepreneurial overconfidence may change the entrepreneur’s incentive to issue equity. This may have quantitative effect on the precise conditions of existence of separating equilibrium but qualitatively the result will not change in sense that only a separating equilibrium where ICO is issued by the good quality firm may exist. The entrepreneurial overconfidence may only reduce the entrepreneur’s incentive to issue equity (e.g., [54]). With regard to ICO, the effect of overconfidence on entrepreneur’s decision-making will be moderated by the complexity factor. If the entrepreneur and market participants have the same opinion then the information complexity may actually reduce the negative effect of overconfidence because the negative impact of overconfidence in estimating the potential benefit of firm profit when using and ICO will be diminished because of factor . This may increase the incentive to use an ICO as a signal. Further analysis of behavioral factors may also include market sentiment (see, e.g., [55]).

Regulatory environment differences. One can further extend the model by including different cost of conducting ICOs vs equity issues. It is not clear at this point though if it leads to qualitatively new results so we leave it to future research. A possible interpretation of complexity may include the complexity (uncertainty) of the regulatory environment (see, e.g., [12,56]). In this sense, the paper results can be interpreted as including some aspect of regulatory differences between ICOs and equity issues.

The distribution of types. In Section 4, which deals with asymmetric information, we use two types of firms to illustrate the main ideas. This is also very typical in the literature. A natural question though is whether the results stand if one considers a case with multiple types. Our analysis shows that most conclusions remain the same: under asymmetric information, equity financing is an inferior choice compared to ICO. In the case of multiple types, however, one may have a semi-separating or even pooling equilibrium where only the type with the highest cost (speaking about Section 4) will be indifferent between the two types of financing and all other types select ICO. Our analysis shows that the results may hold even in a multiple types environment though more research is required. The main implication of our analysis holds. In particular, our results show that there is no semi-separating equilibrium where the average quality of types that choose equity financing is lower than those that choose ICO, which is consistent with our basic model. Proofs are available upon demand. Note that the calculations become much longer and technically more complicated, which is very typical for multiple types of games with asymmetric information.

Mixed financing and more types of financing. In capital structure literature, debt/equity mix is a very common strategy (as opposite to pure equity or pure debt financing). So if mixed financing is allowed in period 1, most results will stand. For example, if mixing ICO and equity financing is allowed in period 1, the spirit of the results of Section 3 remains the same. The fraction of ICO in the total amount of funds raised by the firm compared to the fraction of equity financing depends on a condition which is very similar to condition (31). In Section 4, a signaling equilibrium may still exist where a high-quality firm uses a mix of ICO and equity financing with a larger fraction of ICO compared to low-quality firm, although restricting conditions will change quantitatively. Introducing additional financing strategies such as debt is an interesting direction. Most results regarding the costs and benefits of different financing strategies found in this paper are quite general and do not depend on introduction of more options in the model. Quantitatively though, some conditions may change. It is definitely an interesting direction for future research. Note that most existing theoretical literature on ICO or equity financing does often consider them separately from debt-based crowdfunding. One of the reasons for this seems to be that the founders’ objectives are quite different in these scenarios (see, for example, [57]).

Token velocity. In our model, tokens have a 1 period velocity, i.e., tokenholders use them at the same period they purchased them. One can extend the model by considering different level of token velocity. This will not change our results qualitatively. One can also assume that different consumers have different preferences between using tokens as an investment tool or as a tool for purchasing firm products in the future. In our model, the token price increases after period 1 and remains on the same average level afterwards (i.e., there is no upward trend) but it can change from low price to high price depending on the demand for products in each period. So long-term investment strategy does not create any consistent profit long-term. One can extend the model by assuming that the firm has additional investment projects in the future that increase the firm production scale etc. This is a possible direction for future research. One can also introduce friction on the secondary market for tokens which can be based for example on some asymmetry of information between different types of investors. In our model, the main asymmetry exists between firm founders and entrepreneurs and outside investors.

The main predictions of our analysis are summarized in Table 2.

7. Conclusions

This article analyzes the role of imperfect information in the choice between an ICO and equity financing for an innovative firm looking to fund the development of its innovative business. The topic of ICO is a highly growing area in research and practice. Our model is based on two important features of innovative firms dealing with the development of Fintech-related products. Firstly, there are imperfect information problems related to the development of platforms and a high degree of uncertainty. A lot of campaigns fail or turn out to be low quality or even fraud in some cases (see, for example, [58]). Secondly, it is also well known from the literature that equity financing is usually accompanied by a good degree of information asymmetry. In contrast to traditional literature analyzing firm financing strategies under imperfect information, in this article we combine information asymmetry and information complexity, which was mentioned in several recent papers on ICOs. Empirical literature discovered some differences between features of ICO firms and equity financed firms. We study what can the choice of financing strategy reveal about firm parameters. The model provides several implications, most of which have not been yet been tested. When asymmetric information is important, high-quality firms can use an ICO to signal their quality. This is opposite to traditional theories of equity financing that should never be used by high-quality firms for signaling. Among other results, note the following. We find that the message complexity can be beneficial for firms conducting ICOs. This result is consistent with some recent evidence about ICOs and also may have some regulatory implications as well since it suggests that requiring to submit more documents by firms planning an ICO may not necessarily be socially optimal; although additional research is required in this direction, the average size of projects undertaking equity financing is larger than that of firms conducting ICOs. Thirdly, our model predicts that signaling opportunities exist when the degree of complexity associated with an ICO is not too small nor too large. Forth, under an ICO, a token’s market price significantly increases shortly after the issue as compared with the initial token price. Finally, we show that an ICO will be preferred if the degree of uncertainty regarding the market demand is relatively high.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

No new data were created or analyzed in this study. Data sharing is not applicable to this article.

Acknowledgments

I am grateful to Victor Miglo, Sajda Qureshi, Chris Yang, Vladimir Zwass, the seminar participants at Royal Economic Society annual meeting 2022, Edinburgh Napier University, University of South Bank London, University of Brighton, University of Twente and University of Salford for helpful comments and editing assistance.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Myers, S.; Majluf, N. Corporate Financing Decisions When Firms Have Information Investors Do Not Have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef]

- Cumming, D. Adverse Selection and Capital Structure: Evidence from Venture Capital. Entrep. Theory Pract. 2006, 30, 155–184. [Google Scholar] [CrossRef]

- Cosh, A.; Cumming, D.; Hughes, A. Outside Entrepreneurial Capital. Econ. J. 2009, 119, 1494–1533. [Google Scholar]

- Ofir, M.; Sadeh, I. ICO vs IPO: Empirical Findings, Information Asymmetry and the Appropriate Regulatory Framework. Vanderbilt J. Transnatl. Law, 2019; forthcoming. [Google Scholar] [CrossRef]

- Benedetti, H.; Kostovetsky, L. Digital tulips? Returns to investors in initial coin offerings. J. Corp. Financ. 2021, 66, 101786. [Google Scholar] [CrossRef]

- Lyandres, E.; Palazzo, B.; Rabetti, D. Do Tokens Behave Like Securities? An Anatomy of Initial Coin Offerings, Working Paper. 2020. Available online: https://www.idc.ac.il/en/schools/business/annual-conference/Documents/2019-annual-conference/do-tokens-behave-like-securities-lyandres.pdf (accessed on 1 December 2023).

- Lyandres, E.; Palazzo, B.; Rabetti, D. Initial Coin Offering (ICO) Success and Post-ICO Performance. Manag. Sci. 2022, 68, 8658–8679. [Google Scholar] [CrossRef]

- Ritter, J.; Welch, I. A Review of IPO Activity, Pricing, and Allocations. J. Financ. 2002, 57, 1795–1828. [Google Scholar] [CrossRef]

- Desbrières, P.; Manigart, S.; Waele, K.; Wright, M.; Robbie, K.; Sapienza, H.; Beekman, A. Determinants of required return in venture capital investments: A five country study. J. Bus. Ventur. 2002, 17, 291–312. [Google Scholar]

- Cape, F.; Ripamonte, F. An Empirical Study of the Efficiency of Initial Coin Offerings Adopting a Two-stage DEA Model. 2019. Available online: https://www.politesi.polimi.it/retrieve/a81cb05d-4176-616b-e053-1605fe0a889a/2019_07_Cap%C3%A8_Ripamonti.pdf (accessed on 1 December 2023).

- Schückes, M.; Gutmann, T. Why do startups pursue initial coin offerings (ICOs)? The role of economic drivers and social identity on funding choice. Small Bus. Econ. 2021, 57, 1027–1052. [Google Scholar] [CrossRef]

- Samieifar, S.; Baur, D.G. Read me if you can! An analysis of ICO white papers. Financ. Res. Lett. 2021, 38, 101427. [Google Scholar] [CrossRef]

- Belitski, M.; Boreiko, D. Success factors of initial coin offerings. J. Technol. Transf. 2022, 47, 1690–1706. [Google Scholar] [CrossRef]

- Chod, J.; Trichakis, N.; Yang, S.A. Platform Tokenization: Financing, Governance, and Moral Hazard. Management Science Forthcoming Coinschedule (2018). Cryptocurrency ICO Stats 2018. 2021. Available online: https://www.coinschedule.com/stats.html (accessed on 9 December 2018).

- Catalini, C.; Gans, J.S. Initial Coin Offerings and the Value of Crypto Tokens; NBER Working Paper 24418; 2018. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3137213 (accessed on 1 December 2023).

- Li, J.; Mann, W. Initial Coin Offering and Platform Building. Working Paper. 2018. Available online: https://pdfs.semanticscholar.org/309e/f98741d5da2003df8317fd605e1ac83d6fb9.pdf (accessed on 1 December 2023).

- Govindan, S.; Wilson, R. On Forward Induction. Econometrica 2009, 77, 1–28. [Google Scholar] [CrossRef]

- Bakos, Y.; Hałaburda, H. The Role of Cryptographic Tokens and ICOs in Fostering Platform Adoption. SSRN Electron. J. 2018. [Google Scholar] [CrossRef]

- Cong, L.W.; Li, Y.; Wang, N. Token-based platform finance. J. Financ. Econ. 2021, 144, 972–991. [Google Scholar] [CrossRef]

- Miglo, A. STO vs ICO: A Theory of Token Issues Under Moral Hazard and Demand Uncertainty. J. Risk Financ. Manag. 2021, 14, 232. [Google Scholar] [CrossRef]

- Garratt, R.; van Oordt, M. Entrepreneurial Incentives and the Role of Initial Coin Offerings, Bank of Canada, Staff Working Paper. 2019. Available online: https://www.bankofcanada.ca/2019/05/staff-working-paper-2019-18/ (accessed on 1 December 2023).

- Lee, J.; Parlour, C. Consumers as Financiers: Crowdfunding, Initial Coin Offerings and Consumer Surplus, Working Paper. 2019. Available online: https://www.chapman.edu/research/institutes-and-centers/economic-science-institute/_files/ifree-papers-and-photos/parlour-lee-consumers-as-financiers-2019.pdf (accessed on 1 December 2023).

- Gan, J.; Tsoukalas, G.; Netessine, S. Initial Coin Offerings, Speculation, and Asset Tokenization. Manag. Sci. 2020, 67, 914–931. [Google Scholar] [CrossRef]

- Gryglewicz, S.; Mayer, S.; Morellec, E. Optimal financing with tokens. J. Financ. Econ. 2021, 142, 1038–1067. [Google Scholar] [CrossRef]

- Malinova, K.; Park, A. Tokenomics: When Tokens Beat Equity. 2018. Available online: https://ssrn.com/abstract=3286825 (accessed on 1 December 2023).

- Halaburda, H.; Haeringer, G.; Gans, J.S.; Gandal, N. The microeconomics of cryptocurrencies. J. Econ. Lit. 2020, 60, 971–1013. [Google Scholar] [CrossRef]

- Chod, J.; Lyandres, E. A theory of icos: Diversification, agency, and information asymmetry. Manag. Sci. 2021, 67, 5969–6627. [Google Scholar] [CrossRef]

- Leland, H.E.; Pyle, D.H. Information asymmetries, financial structure, and financial Intermediation. J. Financ. 1977, 32, 371–387. [Google Scholar] [CrossRef]

- Baber, H. A Framework for Crowdfunding Platforms to Match Services between Funders and Fundraisers. Int. J. Ind. Bus. 2019, 10, 25–31. [Google Scholar]

- Chemla, G.; Tinn, K. Learning Through Crowdfunding. Manag. 2020, 66, 1783–1801. [Google Scholar] [CrossRef]

- Baber, H.; Fanea-Ivanovici, M. Motivations behind backers’ contributions in reward-based crowdfunding for movies and web series. Int. J. Emerg. Mark. 2021, 18, 666–684. [Google Scholar] [CrossRef]

- Stępnicka, N.; Zimon, G.; Brzozowiec, D. The Complementary Currency Zielony in Poland and Its Importance for the Development of Local Economy Entities during the COVID-19 Pandemic Lockdown. Sustainability 2021, 13, 9184. [Google Scholar] [CrossRef]

- de Jong, A.; Roosenboom, P.; van der Kolk, T. What Determines Success in Initial Coin Offerings? Available online: https://ssrn.com/abstract=3250035 (accessed on 1 December 2023).

- Bourveau, T.; De George, E.; Ellahie, A.; Macciocchi, D. Initial Coin Offerings: Early Evidence on the Role of Disclosure in the Unregulated Crypto Market; Working Paper; 2018. Available online: https://web.archive.org/web/20190507061340id_/https://www.marshall.usc.edu/sites/default/files/2019-03/thomas_bourveau_icos.pdf (accessed on 1 December 2023).

- Modigliani, F.; Miller, M. The Cost of Capital, Corporation Finance and the Theory of Investment. Am. Econ. Rev. 1958, 48, 261–297. [Google Scholar]

- Myalo, A. Comparative Analysis of ICO, DAOICO, IEO and STO. Case Study. Financ. Theory Pract. 2019, 23, 6–25. [Google Scholar] [CrossRef]

- Ahlers, G.; Cumming, D.; Guenther, C.; Schweizer, D. Signaling in Equity Crowdfunding. Entrep. Theory Pract. 2015, 39, 955–980. [Google Scholar] [CrossRef]

- Mollick, M. The dynamics of crowdfunding: An exploratory study. J. Bus. Ventur. 2014, 29, 1–16. [Google Scholar] [CrossRef]

- Hsieh, H.-C.; Oppermann, J. Initial coin offerings and their initial returns. Asia Pac. Manag. Rev. 2021, 26, 1–10. [Google Scholar] [CrossRef]

- Ante, L.; Fiedler, I. Cheap Signals in Security Token Offerings (STOs). Brl Work. Pap. Ser. 2020, 4, 608–639. [Google Scholar] [CrossRef]

- Cordova, A.; Dolci, J.; Procedia, G. The Determinants of Crowdfunding Success: Evidence from Technology Projects. Soc. And Behavioral Sci. 2015, 181, 115–124. [Google Scholar] [CrossRef]

- Jain, B.; Kini, O. The Post-Issue Operating Performance of IPO Firms. J. Financ. 1994, 69, 1699–1726. [Google Scholar]

- Mickelson, W.; Partch, M.; Shah, K. Ownership and Operating Performance of Companies that go public. J. Financ. Econ. 1997, 44, 281–307. [Google Scholar] [CrossRef]

- Loughran, T.; Ritter, J. The Operating Performance of Firms Conducting Seasoned Equity Offerings. J. Financ. 1997, 52, 1823–1850. [Google Scholar] [CrossRef]

- Titman, S.; Wessels, R. The Determinants of Capital Structure Choice. J. Financ. 1988, 43, 1–19. [Google Scholar] [CrossRef]

- Nachman, D.C.; Noe, T.H. Optimal Design of Securities Under Asymmetric Information. Rev. Financ. Stud. 1994, 7, 1–44. [Google Scholar] [CrossRef]

- Demichelis, S.; Tarola, O. Capacity expansion and dynamic monopoly pricing. Res. Econ. 2006, 60, 169–178. [Google Scholar] [CrossRef]

- Belleflamme, P.; Lambertz, T.; Schwienbacher, A. Crowdfunding: Tapping the Right Crowd. J. Bus. Ventur. 2014, 29, 585–609. [Google Scholar] [CrossRef]

- Strausz, R. A Theory of Crowdfunding—A Mechanism Design Approach with Demand Uncertainty and Moral Hazard. CEPR Discussion Paper No. DP11222. 2016. Available online: http://ssrn.com/abstract=2766550 (accessed on 1 December 2023).

- Miglo, A.; Miglo, V. Market Imperfections and Crowdfunding. Small Bus. Econ. 2019, 53, 51–79. [Google Scholar] [CrossRef]

- Jensen, M.; Meckling, W. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Innes, R. Limited liability and incentive contracting with ex-ante action choices. J. Econ. Theory 1990, 52, 45–67. [Google Scholar] [CrossRef]

- Miglo, A. Crowdfunding Under Market Feedback, Asymmetric Information And Overconfident Entrepreneur. Entrep. Res. J. 2021, 11, 2019018. [Google Scholar] [CrossRef]

- Malmendier, U.; Tate, G.; Yanv, J. Overconfidence and Early-Life Experiences: The Effect of Managerial Traits on Corporate Financial Policies. J. Financ. 2011, 66, 1687–1733. [Google Scholar] [CrossRef]

- Aslan, A.; Şensoy, A.; Akdeniz, L. Determinants of ICO success and post-ICO performance. Borsa Istanb. Rev. 2023, 23, 217–239. [Google Scholar] [CrossRef]

- Andrieu, G.; Sannajust, A. ICOs after the decline: A literature review and recommendations for a sustainable development. Ventur. Cap. 2023. [Google Scholar] [CrossRef]

- Hildebrand, T.; Puri, M.; Rocholl, J. Adverse Incentives in Crowdfunding. 2014. Available online: http://ssrn.com/abstract=1615483 (accessed on 1 December 2023).

- OECD. Initial Coin Offerings (ICOs) for SME Financing. 2019. Available online: www.oecd.org/finance/initial-coin-offerings-for-sme-financing.htm (accessed on 1 December 2023).

Figure 1.

The sequence of events for an ICO.

Figure 2.

The sequence of events for equity financing.

Figure 3.

, , , , , . Area below thin solid line: non-mimicking condition for g. Area above thick solid line: non-mimicking condition for b.

Figure 3.

, , , , , . Area below thin solid line: non-mimicking condition for g. Area above thick solid line: non-mimicking condition for b.

Figure 4.

, , , , , . Area below thin solid line: non-mimicking condition for g. Area above dash line: non-mimicking condition for b.

Figure 4.

, , , , , . Area below thin solid line: non-mimicking condition for g. Area above dash line: non-mimicking condition for b.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Variables and notations description.

| Variable | Description |

|---|---|

| a | parameter in the demand function |

| parameter in the demand function for the level of demand in a model with demand uncertainty | |

| probability that demand is high | |

| I | start-up fixed cost |

| c | unit production cost |

| unit production cost for firm in the model with asymmetric information | |

| discount factor | |

| quantity produced in period n | |

| token price | |

| product price | |

| product price in tokens | |

| firm profit in period n | |

| demand complexity shock in period 1, | |

| probability that |

Table 2.

The model’s results and testable empirical predictions.

| The Model’s Predictions |

| The message complexity can be beneficial for firms conducting ICOs. |

| High-quality projects can use an ICO as a signal of quality. |

| Average size of projects undertaking equity financing is larger than that of firms conducting an ICO. |

| Signaling opportunities exist when the degree of complexity associated with an ICO is not too small nor too large |

| Under an ICO, token’s market price significantly increases shortly after the issue as compared with initial token price. |

| An ICO will be preferred if the degree of uncertainty regarding market demand is relatively high. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Miglo, A. ICO vs. Equity Financing under Imperfect, Complex and Asymmetric Information. FinTech 2024, 3, 17-39. https://0-doi-org.brum.beds.ac.uk/10.3390/fintech3010002

AMA Style

Miglo A. ICO vs. Equity Financing under Imperfect, Complex and Asymmetric Information. FinTech. 2024; 3(1):17-39. https://0-doi-org.brum.beds.ac.uk/10.3390/fintech3010002

Chicago/Turabian StyleMiglo, Anton. 2024. "ICO vs. Equity Financing under Imperfect, Complex and Asymmetric Information" FinTech 3, no. 1: 17-39. https://0-doi-org.brum.beds.ac.uk/10.3390/fintech3010002