Perceived Risk as a Determinant of Propensity to Adopt Account Information Services under the EU Payment Services Directive 2

Abstract

:1. Introduction

2. Literature Review

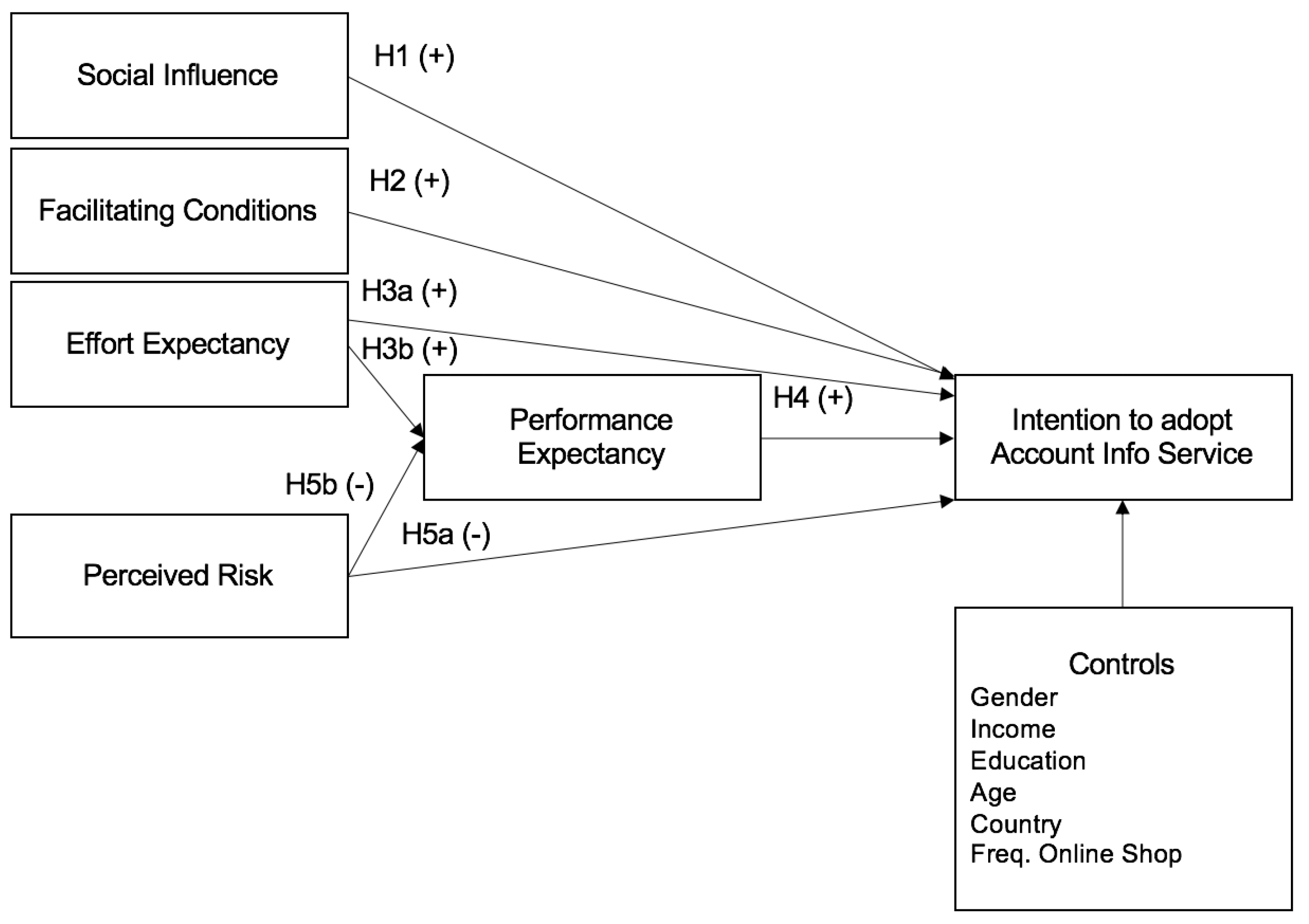

3. Research Model and Hypotheses

4. Methodology and Data Collection

5. Results

5.1. Measurement Model

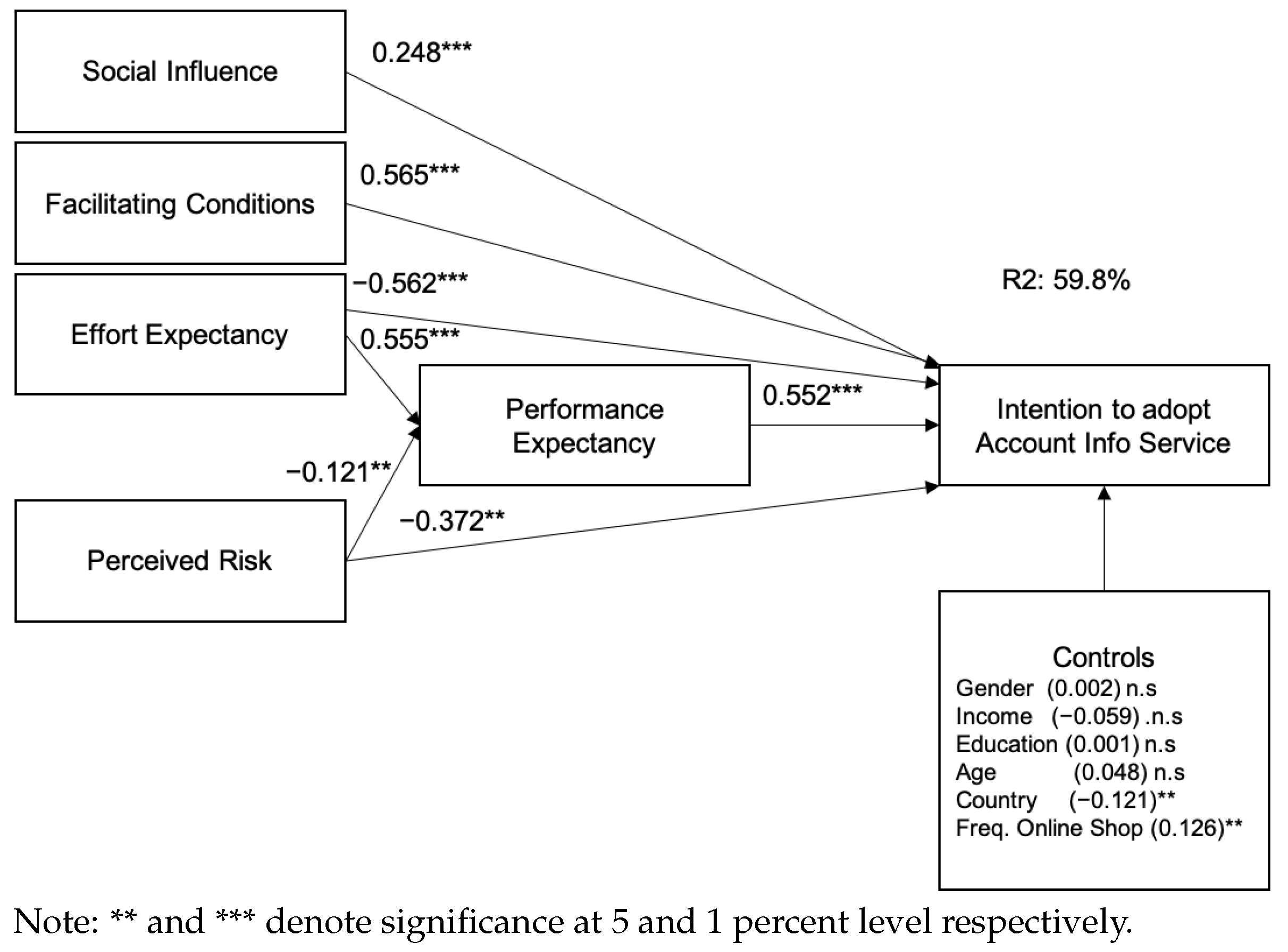

5.2. Hypothesis Testing

6. Discussion and Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Constructs | Items | Questions |

|---|---|---|

| Perceived Risk | PsyRisk1 | I think that account information services will not fit in well with my self-image or self-concept. |

| PsyRisk2 | If I use an account information service, it will negatively affect the way others think of me. | |

| FinRisk1 | The chances of losing money if I use an account information service are high. | |

| FinRisk2 | My signing up for and using an account information service would lead to a financial loss for me. | |

| PrivRisk1 | The chances of using an account information service and losing control over the privacy of my payment information is high. | |

| PrivRisk2 | My signing up and using of an account information service would lead me to a loss of privacy because my personal information may be used without my knowledge. | |

| PrivRisk3 | Internet hackers (criminals) might take control of my bank account(s) if I use an account information service. | |

| PrivRisk4 | On the whole, considering all sorts of factors combined, it would be risky if I use an account information service. | |

| TimeRisk1 | I think that if I use an account information service then I will lose time due to having to switch to a different payment method. | |

| TimeRisk2 | Using an account information service would lead to a loss of convenience for me because I would have to waste a lot of time fixing payments/information errors. | |

| TimeRisk3 | Considering the investment of my time involved to set up an account information service, it would be risky. | |

| TimeRisk4 | The possible time loss from having to set up and learn how to use an account information service is high. | |

| PerRisk1 | Account information services might not perform well and create problems with my credit. | |

| PerRisk2 | The security systems built into the account information services are not strong enough to protect my account. | |

| PerRisk3 | The probability that something’s wrong with the performance of account information services is high. | |

| PerRisk4 | Considering the expected level of performance of account information services, for me to sign up and use, it would be risky. | |

| SoRisk1 | If I use an account information service, it will negatively affect the way others think of me. | |

| SoRisk2 | My signing up for and using an account information service would lead to a social loss for me because my friends and relatives would think less highly of me. | |

| ORisk1 | On the whole, considering all sorts of factors combined, it would be risky if I use an account information service. | |

| ORisk2 | Using an account information service to control my financial information would be risky. | |

| ORisk3 | Account information services would be dangerous to use. | |

| ORisk4 | Using an account information service exposes me to an overall risk. | |

| Performance Expectancy | PE1 | An account information service is useful to carry out my tasks. |

| PE2 | I think that using an account information service would enable me to conduct tasks more quickly. | |

| PE3 | I think that using an account information service would increase my productivity. | |

| PE4 | I think that using an account information service would improve my performance. | |

| Effort Expectancy | EE1 | My interaction with an account information service would be clear and understandable. |

| EE2 | It would be easy for me to become skilful at using an account information service. | |

| EE3 | I would find account information services easy to use. | |

| EE4 | I think that learning to use an account information service would be easy for me. | |

| Social Influence | SI1 | People who influence my behaviour would think that I should use an account information service. |

| SI2 | People who are important to me would think that I should use an account information service. | |

| SI3 | People in my environment who use an account information service would have more prestige than those who do not. | |

| SI4 | People in my environment who would use an account information service have a high profile. | |

| SI5 | Using an account information service would be a status symbol in my environment. | |

| Facilitating Conditions | FC1 | I have the resources necessary to use an account information service. |

| FC2 | I have the knowledge necessary to use an account information service. | |

| Intention to Adopt | INT1 | Assuming I had access to an account information service, I would intend to use it. |

| INT2 | Given that I had access to an account information service, I predict that I would use it. |

References

- Gens, F. The 3rd Platform: Enabling Digital Transformation; IDC: Needham, MA, USA, 2013; Volume 209. [Google Scholar]

- McIntrye, A.; Skan, J.; Andre, L.C.; Francesca, C. Caterpillars, Butterflies and Unicors—Does Digital Leadership in Banking Really Matter? 2019. Available online: https://www.accenture.com/_acnmedia/PDF-102/Accenture-Banking-Does-Digital-Leadership-Matter.pdf#zoom=50 (accessed on 22 March 2022).

- Cortet, M.; Rijks, T.; Nijland, S. PSD2: The digital transformation accelerator for banks. J. Payments Strategy Syst. 2016, 10, 13–27. [Google Scholar]

- Vives, X. Digital disruption in banking. Annu. Rev. Financ. Econ. 2019, 11, 243–272. [Google Scholar] [CrossRef]

- European Commission. Frequently Asked Questions: Making Electronic Payments and Online Banking Safer and EASIER for consumers. 2019. Available online: https://ec.europa.eu/commission/presscorner/detail/en/QANDA_19_5555 (accessed on 26 September 2021).

- Brener, A. Payment Service Directive II and Its Implications. In Disrupting Finance; Lynn, T., Mooney, J., Rosati, P., Cummins, M., Eds.; Palgrave-Macmillan: Cham, Switzerland, 2019; pp. 103–119. [Google Scholar]

- Shaikh, A.A.; Karjaluoto, H. Mobile banking adoption: A literature review. Telemat. Inform. 2015, 32, 129–142. [Google Scholar] [CrossRef] [Green Version]

- Ajzen, I. From Intentions to Actions: A Theory of Planned Behavior. In Action Control; Springer: Berlin/Heidelberg, Germany, 1985; pp. 11–39. [Google Scholar]

- Tan, M.; Teo, T.S.H. Factors influencing the adoption of Internet banking. J. Arab. Islam. Stud. 2000, 1, 5. [Google Scholar] [CrossRef] [Green Version]

- Taylor, S.; Todd, P. Assessing IT usage: The role of prior experience. Manag. Inf. Syst. Q. 1995, 19, 561–570. [Google Scholar] [CrossRef] [Green Version]

- Jaruwachirathanakul, B.; Fink, D. Internet banking adoption strategies for a developing country: The case of Thailand. Internet Res. 2005, 15, 295–311. [Google Scholar] [CrossRef]

- Lee, M.C. Factors influencing the adoption of internet banking: An integration of TAM and TPB with perceived risk and perceived benefit. Electron. Commer. Res. Appl. 2009, 8, 130–141. [Google Scholar] [CrossRef]

- Lin, H.F. An empirical investigation of mobile banking adoption: The effect of innovation attributes and knowledge-based trust. Int. J. Inf. Manag. 2011, 31, 252–260. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. Manag. Inf. Syst. Q. 1989, 13, 319–340. [Google Scholar] [CrossRef] [Green Version]

- Pikkarainen, T.; Pikkarainen, K.; Karjaluoto, H.; Pahnila, S. Consumer acceptance of online banking: An extension of the technology acceptance model. Internet Res. 2004, 14, 224–235. [Google Scholar] [CrossRef] [Green Version]

- Al-Somali, S.A.; Gholami, R.; Clegg, B. An investigation into the acceptance of online banking in Saudi Arabia. Technovation 2009, 29, 130–141. [Google Scholar] [CrossRef]

- Chan, S.C.; Lu, M.T. Understanding internet banking adoption and use behavior: A Hong Kong perspective. J. Glob. Inf. Manag. 2004, 12, 21–43. [Google Scholar] [CrossRef] [Green Version]

- Wessels, L.; Drennan, J. An investigation of consumer acceptance of M-banking. Int. J. Bank Mark. 2010, 28, 547–568. [Google Scholar] [CrossRef]

- Hanafizadeh, P.; Behboudi, M.; Koshksaray, A.A.; Tabar, M.J.S. Mobile-banking adoption by Iranian bank clients. Telemat. Inform. 2014, 31, 62–78. [Google Scholar] [CrossRef]

- Lee, Y.; Kozar, K.A.; Larsen, K.R. The Technology Acceptance Model: Past, Present, and Future. Commun. Ais 2003, 12, 50. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a unified view. Manag. Inf. Syst. Q. 2003, 27, 425–478. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. Manag. Inf. Syst. Q. 2012, 36, 157–178. [Google Scholar] [CrossRef] [Green Version]

- Martins, C.; Oliveira, T.; Popovič, A. Understanding the Internet banking adoption: A unified theory of acceptance and use of technology and perceived risk application. Int. J. Inf. Manag. 2014, 34, 1–13. [Google Scholar] [CrossRef]

- Featherman, M.S.; Pavlou, P.A. Predicting e-services adoption: A perceived risk facets perspective. Int. J. Hum.-Comput. Stud./Int. J. Man-Mach. Stud. 2003, 59, 451–474. [Google Scholar] [CrossRef] [Green Version]

- Littler, D.; Melanthiou, D. Consumer perceptions of risk and uncertainty and the implications for behaviour towards innovative retail services: The case of Internet Banking. J. Retail. Consum. Serv. 2006, 13, 431–443. [Google Scholar] [CrossRef]

- Zhao, A.L.; Hanmer-Lloyd, S.; Ward, P.; Goode, M.M. Perceived risk and Chinese consumers’ internet banking services adoption. Int. J. Bank Mark. 2008, 26, 505–525. [Google Scholar] [CrossRef]

- Luo, X.; Li, H.; Zhang, J.; Shim, J.P. Examining multi-dimensional trust and multi-faceted risk in initial acceptance of emerging technologies: An empirical study of mobile banking services. Decis. Support Syst. 2010, 49, 222–234. [Google Scholar] [CrossRef]

- Chen, C. Perceived risk, usage frequency of mobile banking services. Manag. Serv. Qual. 2013, 23, 410–436. [Google Scholar] [CrossRef]

- Purwanegara, M.; Apriningsih, A.; Andika, F. Snapshot on Indonesia Regulation in Mobile Internet Banking Users Attitudes. Procedia Soc. Behav. Sci. 2014, 115, 147–155. [Google Scholar] [CrossRef] [Green Version]

- Alalwan, A.A.; Dwivedi, Y.K.; Rana, N.P. Factors influencing adoption of mobile banking by Jordanian bank customers. Int. J. Inf. Manag. 2017, 37, 99–110. [Google Scholar] [CrossRef]

- Khan, I.U.; Hameed, Z.; Khan, S.U. Understanding Online Banking Adoption in a Developing Country: UTAUT2 with Cultural Moderators. J. Glob. Inf. Manag. 2017, 25, 43–65. [Google Scholar] [CrossRef] [Green Version]

- Bijlsma, M.; van der Cruijsen, C.; Jonker, N. Consumer Propensity to Adopt PSD2 Services: Trust for Sale? De Nederlandsche Bank Working Paper. 2020. Available online: https://ssrn.com/abstract=3531010 (accessed on 24 September 2021).

- George, A. Perceptions of Internet banking users—A structural equation modelling (SEM) approach. IIMB Manag. Rev. 2018, 30, 357–368. [Google Scholar] [CrossRef]

- CBS. The Netherlands on the European Scale 2019. 2019. Available online: https://longreads.cbs.nl/european-scale-2019/internet/ (accessed on 25 September 2021).

- Thompson, R.L.; Higgins, C.A.; Howell, J.M. Personal computing: Toward a conceptual model of utilization. MIS Q. 1991, 15, 125–143. [Google Scholar] [CrossRef]

- Zhou, T.; Lu, Y.; Wang, B. Integrating TTF and UTAUT to explain mobile banking user adoption. Comput. Hum. Behav. 2010, 26, 760–767. [Google Scholar] [CrossRef]

- Karjaluoto, H.; Koenig-Lewis, N.; Palmer, A.; Moll, A. Predicting young consumers’ take up of mobile banking services. Int. J. Bank Mark. 2010, 28, 410–432. [Google Scholar]

- Wolters, P.; Jacobs, B. The security of access to accounts under the PSD2. Comput. Law Secur. Rev. 2019, 35, 29–41. [Google Scholar] [CrossRef] [Green Version]

- Oliinyk, I.; Echikson, W.; Europe’s Payments Revolution. Stimulating Payments Innovation while Protecting Consumer Privacy. CEPS Research Report No. 2018/06, September 2018. 2018. Available online: http://aei.pitt.edu/id/eprint/94533 (accessed on 20 September 2020).

- van der Cruijsen, C. Payments data: Do consumers want banks to keep them in a safe or turn them into gold? Appl. Econ. 2020, 52, 609–622. [Google Scholar] [CrossRef]

- Rogers, E.M.; Simon, S. Diffusion of Innovations, 5th ed.; Free Press: New York, NY, USA, 2003. [Google Scholar]

- Mattila, M.; Karjaluoto, H.; Pento, T. Internet banking adoption among mature customers: Early majority or laggards? J. Serv. Mark. 2003, 17, 514–528. [Google Scholar] [CrossRef] [Green Version]

- Laukkanen, T. Consumer adoption versus rejection decisions in seemingly similar service innovations: The case of the Internet and mobile banking. J. Bus. Res. 2016, 69, 2432–2439. [Google Scholar] [CrossRef]

- Riddell, W.C.; Song, X. The role of education in technology use and adoption: Evidence from the Canadian workplace and employee survey. ILR Rev. 2017, 70, 1219–1253. [Google Scholar] [CrossRef]

- Allison, P.D. Structural equation models with fixed effects. In Fixed Effects Regression Models; SAGE Publications: Thousand Oaks, CA, USA, 2009. [Google Scholar]

- Helgadottir, D. The Interaction between Directive 2015/2366 (EU) on Payment Services and Regulation (EU) 2016/679 on General Data Protection concerning Third Party Players. Trinity CL Rev. 2020, 23, 199. [Google Scholar] [CrossRef]

- MacKenzie, S.B.; Podsakoff, P.M.; Podsakoff, N.P. Construct measurement and validation procedures in MIS and behavioral research: Integrating new and existing techniques. MIS Q. 2011, 35, 293–334. [Google Scholar] [CrossRef]

- Federation, E.B. Banking in Europe: EBF Facts & Figures 2019. 2019. Available online: https://www.ebf.eu/ebf-media-centre/banking-in-europe-ebf-publishes-2019-facts-figures/ (accessed on 25 September 2021).

- Hair, J.F.; Anderson, R.E.; Babin, B.J.; Black, W.C. Multivariate Data Analysis: A Global Perspective; Pearson Education: Upper Saddle River, NJ, USA, 2010; Volume 7. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Raykov, T. Estimation of composite reliability for congeneric measures. Appl. Psychol. Meas. 1997, 21, 173–184. [Google Scholar] [CrossRef]

- Zhao, X.; Lynch, J.G., Jr.; Chen, Q. Reconsidering Baron and Kenny: Myths and truths about mediation analysis. J. Consum. Res. 2010, 37, 197–206. [Google Scholar] [CrossRef]

- Sampaio, C.H.; Ladeira, W.J.; Santini, F.D.O. Apps for mobile banking and customer satisfaction: A cross-cultural study. Int. J. Bank Mark. 2017, 35, 1133–1153. [Google Scholar] [CrossRef]

- Hernandez-Ortega, B. The role of post-use trust in the acceptance of a technology: Drivers and consequences. Technovation 2011, 31, 523–538. [Google Scholar] [CrossRef]

- Senyo, P.K.; Osabutey, E.L. Unearthing antecedents to financial inclusion through FinTech innovations. Technovation 2020, 98, 102155. [Google Scholar] [CrossRef]

| Constructs | Items | Std. Rwg |

|---|---|---|

| Perceived Risk (2nd order factor based on Feathermann and Pavlou, 2003) | Psychological Risk | 0.753 |

| PsyRisk1 | 0.828 | |

| PsyRisk2 | 0.911 | |

| Financial Risk | 0.825 | |

| FinRisk1 | 0.853 | |

| FinRisk2 | 0.748 | |

| Privacy Risk | 0.730 | |

| PrivRisk1 | 0.794 | |

| PrivRisk2 | 0.800 | |

| PrivRisk3 | 0.771 | |

| PrivRisk4 | 0.814 | |

| Time Risk | 0.885 | |

| TimeRisk1 | 0.781 | |

| TimeRisk2 | 0.804 | |

| TimeRisk3 | 0.756 | |

| TimeRisk4 | 0.796 | |

| Performance Risk | 0.916 | |

| PerRisk1 | 0.673 | |

| PerRisk2 | 0.731 | |

| PerRisk3 | 0.847 | |

| PerRisk4 | 0.816 | |

| Social Risk | 0.690 | |

| SoRisk1 | 0.963 | |

| SoRisk2 | 0.877 | |

| Overall Risk | 0.808 | |

| ORisk1 | 0.865 | |

| ORisk2 | 0.851 | |

| ORisk3 | 0.854 | |

| ORisk4 | 0.850 | |

| Performance Expectancy (4 items based on Venkatesh et al., 2003) | PE1 | 0.777 |

| PE2 | 0.791 | |

| PE3 | 0.896 | |

| PE4 | 0.860 | |

| Effort Expectancy (4 items based on Venkatesh et al., 2003) | EE1 | 0.661 |

| EE2 | 0.796 | |

| EE3 | 0.755 | |

| EE4 | 0.704 | |

| Social Influence (5 items based on Venkatesh et al., 2003) | SI1 | 0.783 |

| SI2 | 0.788 | |

| SI3 | 0.881 | |

| SI4 | 0.893 | |

| SI5 | 0.856 | |

| Facilitating conditions (2 items based on Venkatesh et al., 2003) | FC1 | 0.784 |

| FC2 | 0.742 | |

| Intention to Adopt (2 items based on Venkatesh et al., 2003) | INT1 | 0.942 |

| INT2 | 0.910 |

| Constructs | CR | AVE | PE | INT | EE | FC | SI | PR |

|---|---|---|---|---|---|---|---|---|

| Performance Expectancy (PE) | 0.900 | 0.693 | 0.833 | |||||

| Intention (INT) | 0.923 | 0.857 | 0.622 ** | 0.926 | ||||

| Effort Expectancy (EE) | 0.820 | 0.534 | 0.612 ** | 0.427 ** | 0.731 | |||

| Facilitating Conditions (FC) | 0.736 | 0.583 | 0.380 ** | 0.482 ** | 0.777 ** | 0.764 | ||

| Social Influence (SI) | 0.924 | 0.708 | 0.713 ** | 0.487 ** | 0.298 ** | 0.223 ** | 0.841 | |

| Perceived Risk (PR) | 0.927 | 0.647 | 0.009 | −0.206 ** | −0.287 ** | −0.193 ** | 0.385 ** | 0.805 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rosati, P.; Fox, G.; Cummins, M.; Lynn, T. Perceived Risk as a Determinant of Propensity to Adopt Account Information Services under the EU Payment Services Directive 2. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 493-506. https://0-doi-org.brum.beds.ac.uk/10.3390/jtaer17020026

Rosati P, Fox G, Cummins M, Lynn T. Perceived Risk as a Determinant of Propensity to Adopt Account Information Services under the EU Payment Services Directive 2. Journal of Theoretical and Applied Electronic Commerce Research. 2022; 17(2):493-506. https://0-doi-org.brum.beds.ac.uk/10.3390/jtaer17020026

Chicago/Turabian StyleRosati, Pierangelo, Grace Fox, Mark Cummins, and Theo Lynn. 2022. "Perceived Risk as a Determinant of Propensity to Adopt Account Information Services under the EU Payment Services Directive 2" Journal of Theoretical and Applied Electronic Commerce Research 17, no. 2: 493-506. https://0-doi-org.brum.beds.ac.uk/10.3390/jtaer17020026