Precision Measurement of the Return Distribution Property of the Chinese Stock Market Index

1

School of Information, Xi’an University of Finance and Economics, Xi’an 710100, China

2

School of Management, Xi’an Polytechnic University, Xi’an 710048, China

*

Author to whom correspondence should be addressed.

†

These authors contributed equally to this work.

Entropy 2023, 25(1), 36; https://0-doi-org.brum.beds.ac.uk/10.3390/e25010036

Submission received: 20 November 2022

/

Revised: 18 December 2022

/

Accepted: 19 December 2022

/

Published: 24 December 2022

(This article belongs to the Special Issue Explaining Economic and Social Science Phenomena through Physical Models)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:In econophysics, the analysis of the return distribution of a financial asset using statistical physics methods is a long-standing and important issue. This paper systematically conducts an analysis of composite index 1 min datasets over a 17-year period (2005–2021) for both the Shanghai and Shenzhen stock exchanges. To reveal the differences between Chinese and mature stock markets, we precisely measure the property of the return distribution of the composite index over the time scale , which ranges from 1 min to almost 4000 min. The main findings are as follows: (1) The return distribution presents a leptokurtic, fat-tailed, and almost symmetrical shape that is similar to that of mature markets. (2) The central part of the return distribution is described by the symmetrical Lévy -stable process, with a stability parameter comparable with a value of about 1.4, which was extracted for the U.S. stock market. (3) The return distribution can be described well by Student’s t-distribution within a wider return range than the Lévy -stable distribution. (4) Distinctively, the stability parameter shows a potential change when increases, and thus a crossover region at 15 60 min is observed. This is different from the finding in the U.S. stock market that a single value of about 1.4 holds over 1 1000 min. (5) The tail distribution of returns at small decays as an asymptotic power law with an exponent of about 3, which is a widely observed value in mature markets. However, it decays exponentially when 240 min, which is not observed in mature markets. (6) Return distributions gradually converge to a normal distribution as increases. This observation is different from the finding of a critical 4 days in the U.S. stock market.

1. Introduction

Econophysics is an emerging interdisciplinary field. It investigates economic and financial problems through the models, methods, and concepts adopted in physics, especially statistical physics [1,2,3,4,5]. Among the most important and remarkably interesting studies in the econophysics field, the price fluctuation of assets in the financial market has been intensively investigated in both empirical and theoretical ways since 1900 [6,7,8,9,10,11,12,13,14,15,16,17,18,19,20,21,22,23,24,25].

The stock market is a complex financial system in which the traders, assets, and many unforeseen external factors interact with each other non-linearly; thus, it is extremely hard to write down a dynamical equation among these elements. Fortunately, the price fluctuations of individual stocks and market indices provide us with a powerful tool to understand its dynamics [2,6]. Fluctuations are often quantified by a logarithmic return over a time scale of that can be mathematically defined as follows:

where denotes the time series of a company stock price or market index. The return is of a great key role in asset pricing and is at the core of financial risks through multifractal analysis [6,7,8,16].

In the late 20th century, huge amounts of data from the stock market are available for scholars due to the rapid development of computer technology [2,6]. This development allows physicists to analyze precisely the properties of the return of a financial asset using the methodology developed for statistical physics. In 1995, a paper published in Nature analyzed the return distribution of the Standard & Poor’s 500 (S&P 500) index over the 6-year period (1984–1989) [26]. This work found that the central region of the return distribution can be well described by a truncated Lévy stable symmetrical distribution [27] with an index of 1.4 (comparable with 1.5 for the income distribution [3] and 1.7 for the distribution of the fluctuation of cotton price [13]). More importantly, this study observed the scaling behavior of the probability density over three orders of magnitude of . Four years later, the same team conducted more detailed studies on the stock indices [28] and individual company stocks [29,30] in the U.S. market. These new works found a universal asymptotic inverse cubic power-law in the return distribution tails for both the S&P 500 index and individual company stocks (the power-law has been observed in many natural and social complex systems [31]). They also observed a critical point of below which the tail distributions retain a similar power-law, and gradually converge to Gaussian distribution otherwise ( 4 days and 16 days for market index and individual company stocks, respectively) [28,30,32]. Further studies illustrated similar scaling behavior in other mature stock markets such as in England, France, Germany, Mexico, and Japan [28,30,33,34,35,36,37].

Although mature stock markets seem to show a universality of power-law scaling behavior, many exceptions exist in other stock markets. Studies on the stocks traded in the Australian Stock Exchange and the daily WIG index of the Warsaw Stock Exchange showed that tail distributions follow the power law, with the exponent being significantly different from 3 [38,39,40]. As for the Indian stock market, a study on the daily returns of the 49 largest stocks indicated [41] that the tail distributions decay exponentially as . However, new studies in 2007 and 2008 [42,43] found that the distributions of fluctuations of the individual stock prices, the Nifty index, and the Sensex index follow the asymptotic power law with exponent 3. For the Hong Kong stock market, research has also been conducted and delivered different results from research based on the U.S. stock market [44,45]. These non-unified results make it difficult to understand the dynamic property of the stock market. It seems to be dependent on the degree of development of a specific financial market [46].

The Chinese Mainland stock market, the largest emerging financial market in the world, has different trading rules and government regulations compared with other developed financial markets, such as T + 1 trading, intraday price limits, and IPO policy [47]. These differences may result in different interactions among traders, assets, and external factors in the Chinese stock market. Thus, it is of great importance to understand the dynamic properties of the Chinese stock market via return distributions. However, the previous analyses on the return distribution for the Chinese stock market were conducted about 10 years ago and did not obtain conclusive results because of the limitation of data statistics. In 2005, scholars analyzed the data of 104 individual stocks listed on the Shanghai Stock Exchange (SSE) and Shenzhen Stock Exchange (SZSE) and found the tail distributions of daily stock price returns follow the power law, with the exponent being significantly different from that in the U.S. stock market [48]. They also stated that the distributions of returns are asymmetrical, but almost symmetrical distributions were observed in the U.S. stock market [48]. A similar analysis of the SSE Composite Index (SSECI) and the SZSE Component Index in 2007 observed asymmetrical return distribution with a power-law exponent of less than 3 over 1 60 min [49]. In contrast, a more detailed analysis of the 1 min data and 1-day data of the SSECI in 2008 showed [50] that the power-law exponent is systematically larger than 3. Subsequently, a study on the tick-by-tick data from 23 individual stocks listed in SZSE argued that return distribution can be well fitted with the Student’s t-distribution [51,52], which is different from the truncated Lévy stable process model [26,27]. In 2010, a study of the SSE 50 index and SZSE 100 index revealed [53] that tail distributions obey the power-law when 1 week and follow exponential decay otherwise.

In the past 20 years, more high-frequency data on the Chinese stock market have been accumulated for analysis. These data provide us with a good opportunity to precisely measure the properties of return distributions. To shed light on the understanding of the dynamical property of the Chinese stock market and help clarify the confusion stated above, this paper analyzes 1 min datasets recorded for the SSECI and the SZSE Composite Index (SZSECI) over the 17-year period (4 January 2005 to 31 December 2021), using the methods and concepts adopted in statistical physics.

2. Datasets

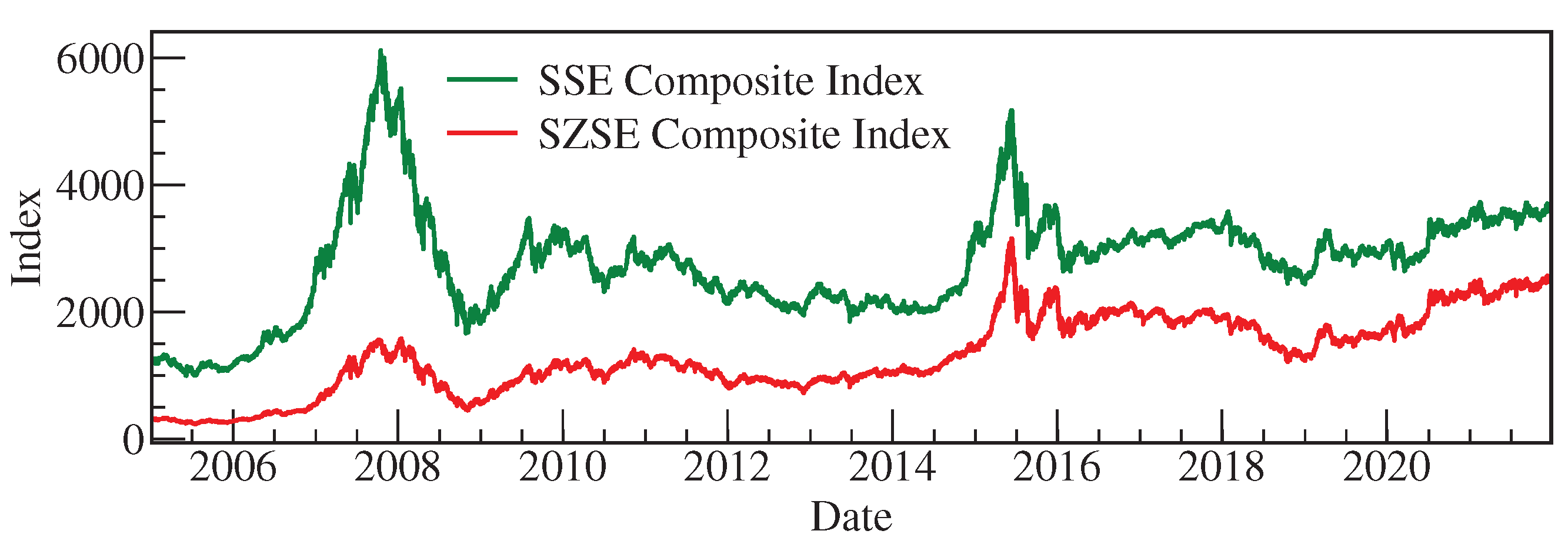

This paper analyzes 1 min datasets over the 17-year period (4 January 2005 to 31 December 2021) for both the SSECI and the SZSECI, as shown in Figure 1. The SSE and SZSE, the only two stock exchanges in Mainland China, were established in late 1990. The SSECI comprises all stocks of A-shares and B-shares listed and traded on the SSE. Similarly, the SZSECI consists of all stocks listed and traded on SZSE. Both indices aim to reflect the overall Chinese stock market performance and are calculated by the capitalization-weighted method. Both exchanges trade during 9:30–11:30 and 13:00–15:00 of a trading day and are closed on the weekend and national holidays. When we construct a time series , we first skip the non-trading days and the period of 11:30–13:00 on trading days, and then connect from 9:00 to 15:00 of the previous trading day. The time series of indices with other time scales are constructed using the 1 min datasets (991,680 records for each index).

3. Results and Discussion

To provide an overview of the statistical property of returns, Figure 2 shows the probability density functions (PDFs) of returns of over 1 3840 min for both the SSECI and the SZSECI. It is evident from Figure 2 that the PDFs of both indices have a similar shape. To study the shape quantitatively, we examine the skewness and kurtosis and the corresponding statistical significance tests [54,55]. These examinations show that our data present slightly negative skewness with statistical significance, but its most central parts are symmetrical. These examinations also show that Fisher’s kurtosis is larger than 0, with very high statistical significance. Additionally, as can be seen in this figure, these distributions are leptokurtic, fat-tailed, and almost symmetrical.

Previous works have illustrated that the central parts of the return PDFs shown in Figure 2 can be well described by the Lévy -stable process [6,26,27,49,50]. The symmetrical Lévy -stable PDF is mathematically written as

where refers to PDF, is the return defined by Equation (1), denotes time scale (in Equations (2)–(5), to make dimensionless, we let equal the time scale divided by 1 min), (, stability parameter, also known as index) is a key parameter for Lévy -stable distribution, and is the scale parameter. In Equation (2), is the characteristic function. According to Equation (2), the PDF of 0 is

where denotes the Gamma function.

Next, we use the approach proposed by Ref. [26] to extract the stability parameter from the data shown in Figure 2. According to Equation (3), the parameter equals the negative of the reciprocal of the slope shown in Figure 3. The values are as follows: 1.34 ± 0.03 (SSECI) and 1.13 ± 0.04 (SZSECI) over 1 15 min, and 1.49 ± 0.03 (SSECI) and 1.57 ± 0.02 (SZSECI) over 60 3840 min. Such values of extracted from our data are consistent with 0 2 and comparable with 1.40 ± 0.05 which is extracted from the U.S. stock market [26]. A potential crossover region at 15 60 min for these two indices is observed. This potential crossover region is not observed in the U.S. stock market in which a single fitting holds over 1 1000 min [26], and also in the previous similar studies regarding the Chinese Stock market [49,50]. We skip the first few minutes to an hour for each trading day to see whether this crossover region disappears, but it exists. The overnight return also cannot contribute to this phenomenon since the data points with 60 min do not include the overnight effect. By removing the data affected by extreme events, such as the global financial crisis of 2007–2008, the 2015–2016 Chinese stock market turbulence, and the COVID-19 global pandemic [56,57], we observe that those extreme events have no contribution to this crossover region. Therefore, this potential crossover region may indicate an underlying dynamical behavior of the Chinese stock market that differs from the U.S. stock market.

The symmetrical Lévy -stable distribution shown in Equation (2) will collapse on the 1 distribution under the transformations below.

where denotes rescaled return, and and are defined by Equations (1) and (2), respectively.

Figure 4 shows the rescaled PDFs of returns with the stability parameter extracted from Figure 3. An obvious collapse of distributions with a large is observed here. However, only central parts of distributions with a larger overlap with the 1 min data. The red curves are the symmetrical Lévy -stable distributions with the parameters obtained in Figure 3. Note that these red curves are not simple fits to data. Their scale factors are obtained using Equation (3) and the experimental for 15 min or the extrapolation of using the straight-line fits for 60 min in Figure 3. The symmetrical Lévy -stable distributions with the parameters extracted from Figure 3 show good agreement with data in the central parts. From the two aspects discussed above, we could conclude that the symmetrical Lévy -stable process describes a part of the dynamical properties of the Chinese stock market. In Figure 4, the tail distributions of data are larger than the Gaussian distribution and smaller than the Lévy -stable distribution. Thus, we tried using the Student’s t-distribution to fit data, as demonstrated by the solid black curves shown in panels a and b which have sufficient data. The fit results show that the Student’s t-distribution can describe the data at a wider range than the Lévy -stable distribution well, which could be explained by the so-called non-extensive statistical framework [58,59].

Given the discussion above, it is essential to obtain a detailed study of the tail distribution. To compare tails with different , we introduce the normalized return

where is the average of returns over the entire time T, and V is the volatility of the time series.

Figure 5 shows the PDF and the complementary cumulative distribution function (CCDF) of the = 1 min tail of normalized returns in a log–log style. The PDF of the tail follows a power-law decay in the form of , as shown in panels a and b. Naturally, the CCDF follows the form of , as shown in panels c and d. Similar behavior for both positive and negative tails is observed obviously. We use a straight-line fit to extract the exponent , as shown by the dashed black lines. The exponents extracted from PDF are consistent with those from CCDF within acceptable errors. For the SSECI positive tail, the average (weighted by the reciprocal of squared errors) of exponents extracted from fits to PDF and CCDF is 3.07 ± 0.05. For the SZSECI positive tail, that value is 3.14 ± 0.04. The values of the SSECI and the SZSECI are in agreement with each other within errors, and well as outside the Lévy -stable process.

Figure 6 compares the CCDF of the normalized returns with 1 3840 min for positive and negative tails. Here, the theoretical values of standard normal distribution and Student’s t-distribution are also drawn for comparison. It can be seen from Figure 6 that these tails with small time scales follow an asymptotic power-law decay, but the tails gradually deviate from the power-law when becomes longer. For the case of short , the tail distributions are fitted by the power law and the Student’s t-distribution; thus, the exponents are extracted. The exponents extracted from these two functions are close to the value of 3 which is frequently observed in mature stock markets. Such values ensure a finite variance of returns. This is important for option pricing and risk management.

From Figure 6, we find that the tail distributions with a large deviate from the asymptotic power law. However, we cannot obtain more details on the tails with a large since they are suppressed to the central region by normalization. Here, we investigate the return tails in a log-linear style, as shown in Figure 7. Both positive and negative tails show exponential decay in the form of when 240 min. The exponential decay also ensures a finite variance of returns. From Figure 6 and Figure 7, we can conclude that the tails decay for the asymptotic power-law at a small value of , and exponentially decay at large values, which is not observed in mature stock markets.

We also verified the convergence behavior of return distribution by comparing the moments between the normalized return data and the standard normal distribution, as shown in Figure 8. The result indicates that the data gradually converge to the standard normal distribution starting from 1 min. To quantify this convergence behavior, we introduce a measure of the moment difference between the normalized return data and the standard normal distribution, as shown in Equation (7).

where and denote the moments of the normalized return data with a and the standard normal distribution, respectively; n is the number of data points shown in Figure 8. The measure of D can also serve as the distance between two curves. Therefore, we define speed using Equation (8) to measure the speed of this convergence between a moment curve i and another moment curve , as shown in Figure 8.

Figure 9 shows the measured distance between the normalized return data and the standard normal distribution and the speed of the convergence of data. This figure demonstrates quantitatively that the convergence starts at 1 min, and the speed at a small is much faster than others. This convergence behavior is different from the early studies in the U.S. [28] and the Chinese stock markets [50], in which convergence to the standard normal distribution occurs only when 4 days [28,50].

4. Conclusions

Because the previous studies on the return distribution of the Chinese stock market are dramatically limited by statistics, this paper systematically and precisely investigates the property of the return distributions of both the SSECI and the SZSECI in the Chinese stock market. We used 1 min high statistics datasets over a 17-year period (4 January 2005 to 31 December 2021) to construct return distributions with time intervals ranging from 1 min to almost 4000 min. The results illustrate that the properties of the return distributions for both the SSECI and the SZSECI are similar. The main findings are as follows: (1) The return distributions present a leptokurtic, fat-tailed, and almost symmetrical shape that is similar to that of mature stock markets. (2) The central parts of the return distributions can be described by the symmetrical Lévy -stable process. The key parameters characterizing this process are extracted from our data. They are 1.34 ± 0.03 (SSECI) and 1.13 ± 0.04 (SZSECI) over 1 15 min and 1.49 ± 0.03 (SSECI) and 1.57 ± 0.02 (SZSECI) over 60 3840 min. Such values are comparable with the value of extracted from the U.S. stock market [26] and within the Lévy -stable process range of . (3) Return distributions can be described well by Student’s t-distribution within a wider return range than the Lévy -stable distribution. (4) A potential crossover region at 15 60 min was discovered. Such a crossover region is not observed in the U.S. stock market, where a single value of holds over 1 1000 min [26]. (5) To obtain a better understanding of tail distribution, this paper checks the PDF and CCDF of tails in detail. For small , the tail shows scaling behavior and follows an asymptotic power-law decay with an exponent of about 3, which is a value widely observed in mature stock markets. However, the tail decays exponentially when 240 min, which is not observed in mature stock markets. (6) Finally, it is observed that return distributions gradually converge to a normal distribution as increases. Such convergence behavior is different from previous studies in the U.S [28] and Chinese stock markets [50], which state that convergence only occurs when 4 days.

Stock markets are inhomogeneous and time-varying. A multifractal analysis via the return distribution and analysis of volatility surfaces in stock markets across the world should be conducted using the latest high-frequency datasets that have been collected over the same time period. By comparing the empirical results from different stock markets and constructing theoretical models, one can learn the underlying dynamics of stock markets [60], such as the impacts of investor risk attitude, trading rules, and government regulations in different countries.

Author Contributions

P.L. and Y.Z. made important contributions to this publication in the acquisition of data and data analysis. P.L. wrote the manuscript. All authors reviewed and approved the submitted manuscript.

Funding

This work was supported by the Humanities and Social Sciences Youth Foundation of the Chinese Ministry of Education (Contract No. 22YJCZH107) and the Scientific Research Support Program of Xi’an University of Finance and Economics (Contract No. 22FCZD03).

Data Availability Statement

The data presented in this study are available on reasonable request from the corresponding author.

Acknowledgments

The authors would like to thank the anonymous referees and editors for their helpful comments which improve the quality of this paper.

Conflicts of Interest

The authors declare no competing interest.

References

- The Nobel Foundation. Jan Tinbergen Facts. 2022. Available online: https://www.nobelprize.org/prizes/economic-sciences/1969/tinbergen/facts/ (accessed on 18 December 2022).

- Kutner, R.; Ausloos, M.; Grech, D.; Matteo, T.D.; Schinckus, C.; Stanley, H.E. Econophysics and sociophysics: Their milestones & challenges. Physica A 2019, 516, 240–253. [Google Scholar]

- Ribeiro, M.B. Income Distribution Dynamics of Economic Systems: An Econophysical Approach; Cambridge University Press: Cambridge, UK, 2020. [Google Scholar]

- Andersen, J.V.; Nowak, A. Symmetry and financial markets. EPL 2022, 139, 22001. [Google Scholar] [CrossRef]

- Smolyak, A.; Havlin, S. Three decades in econophysics—From microscopic modeling to macroscopic complexity and back. Entropy 2022, 24, 271. [Google Scholar] [CrossRef] [PubMed]

- Mantegna, R.N.; Stanley, H.E. An Introduction to Econophysics: Correlations and Complexity in Finance; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- Bouchaud, J.-P.; Potters, M. Theory of Financial Risks: From Statistical Physics to Risk Management; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- Malevergne, Y.; Sornette, D. Extreme Financial Risks: From Dependence to Risk Management; Springer: Berlin/Heidelberg, Germany, 2006. [Google Scholar]

- Bachelier, L. Théorie de la Spéculation. Ph.D. Thesis, University of Paris, Paris, France, 1900. [Google Scholar]

- Fama, E.F. Efficient capital markets: A review of theory and empirical work. J. Finance 1970, 25, 383–417. [Google Scholar] [CrossRef]

- Mandelbrot, B. The Pareto-Lévy law and the distribution of income. Int. Econ. Rev. 1960, 1, 79–106. [Google Scholar] [CrossRef] [Green Version]

- Mandelbrot, B. New methods in statistical economics. J. Polit. Econ. 1963, 71, 421–440. [Google Scholar] [CrossRef]

- Mandelbrot, B. The variation of certain speculative prices. J. Bus. 1963, 36, 394–419. [Google Scholar] [CrossRef]

- Mandelbrot, B. The variation of some other speculative prices. J. Bus. 1967, 40, 393–413. [Google Scholar] [CrossRef]

- Akgiray, V.; Booth, G.G. The stable-law model of stock returns. J. Bus. Econ. Stat. 1988, 6, 51–57. [Google Scholar] [CrossRef]

- Jiang, Z.-Q.; Xie, W.-J.; Zhou, W.-X.; Sornette, D. Multifractal analysis of financial markets: A review. Rep. Prog. Phys. 2019, 82, 125901. [Google Scholar] [CrossRef] [Green Version]

- Merton, R.C. Option pricing when underlying stock returns are discontinuous. J. Finance Econ. 1976, 3, 125–144. [Google Scholar] [CrossRef]

- Madan, D.B.; Carr, P.P.; Chang, E.C. The variance gamma process and option pricing. Rev. Finance 1998, 2, 79–105. [Google Scholar] [CrossRef] [Green Version]

- Kou, S.G. A jump-diffusion model for option pricing. Manag. Sci. 2002, 48, 955–1101. [Google Scholar] [CrossRef] [Green Version]

- Bouskraoui, M.; Arbai, A. Pricing option CGMY model. IOSR-JM 2017, 13, 5–11. [Google Scholar] [CrossRef]

- Schoutens, W. Meixner Processes in Finance; Eurandom: Eindhoven, The Netherlands, 2001. [Google Scholar]

- Heston, S.L. A closed-form solution for options with stochastic volatility wth applications to bond and currency options. Rev. Finance Stud. 2015, 6, 327–343. [Google Scholar] [CrossRef] [Green Version]

- Dupire, B. Pricing with a smile. Risk 1994, 7, 18–20. [Google Scholar]

- Chourdakis, K. Lévy processes driven by stochastic volatility. Asia-Pac. Financ. Mark. 2005, 12, 333–352. [Google Scholar] [CrossRef]

- Bayer, C.; Friz, P.; Gatheral, J. Pricing under rough volatility. Quant. Finance 2016, 16, 887–904. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Stanley, H.E. Scaling behaviour in the dynamics of an economic index. Nature 1995, 376, 46–49. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Stanley, H.E. Stochastic process with ultraslow convergence to a gaussian: The truncated Lévy flight. Phys. Rev. Lett. 1994, 73, 2946–2949. [Google Scholar] [CrossRef]

- Gopikrishnan, P.; Plerou, V.; Amaral, L.A.N.; Meyer, M.; Stanley, H.E. Scaling of the distribution of fluctuations of financial market indices. Phys. Rev. E 1999, 60, 5305–5316. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Gopikrishnan, P.; Meyer, M.; Amaral, L.A.N.; Stanley, H.E. Inverse cubic law for the distribution of stock price variations. Eur. Phys. J. B 1998, 3, 139–140. [Google Scholar] [CrossRef]

- Plerou, V.; Gopikrishnan, P.; Amaral, L.A.N.; Meyer, M.; Stanley, H.E. Scaling of the distribution of price fluctuations of individual companies. Phys. Rev. E 1999, 60, 6519–6529. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Laherrère, J.; Sornette, D. Stretched exponential distributions in nature and economy: “Fat tails” with characteristic scales. Eur. Phys. J. B 1998, 2, 525–539. [Google Scholar] [CrossRef] [Green Version]

- Gabaix, X.; Gopikrishnan, P.; Plerou, V.; Stanley, H.E. A theory of power-law distributions in financial market fluctuations. Nature 2003, 423, 267–270. [Google Scholar] [CrossRef]

- Plerou, V.; Stanley, H.E. Stock return distributions: Tests of scaling and universality from three distinct stock markets. Phys. Rev. E 2008, 77, 037101. [Google Scholar] [CrossRef] [Green Version]

- Stanley, H.E.; Plerou, V.; Gabaix, X. A statistical physics view of financial fluctuations: Evidence for scaling and universality. Physica A 2008, 387, 3967–3981. [Google Scholar] [CrossRef]

- Lux, T. The stable paretian hypothesis and the frequency of large returns: An examination of major German stocks. Appl. Finance Econ. 1996, 6, 463–475. [Google Scholar] [CrossRef]

- Coronel-Brizio, H.F.; Hernández-Montoya, A.R. On fitting the Pareto-Levy distribution to stock market index data: Selecting a suitable cutoff value. Physica A 2005, 354, 437–449. [Google Scholar] [CrossRef] [Green Version]

- Alfonso, L.; Mansilla, R.; Terrero-Escalante, C.A. On the scaling of the distribution of daily price fluctuations in the Mexican financial market index. Physica A 2012, 391, 2990–2996. [Google Scholar] [CrossRef] [Green Version]

- Storer, R.; Gunner, S.M. Statistical properties of the Australian “all ordinaries” index. Int. J. Mod. Phys. C 2002, 13, 893–897. [Google Scholar] [CrossRef]

- Bertram, W.K. An empirical investigation of Australian Stock Exchange data. Physica A 2004, 341, 533–546. [Google Scholar] [CrossRef]

- Makowiec, D.; Gnaciński, P. Fluctuations of WIG—The index of Warsaw stock exchange preliminary studies. Acta Phys. Pol. B 2001, 32, 1487–1500. [Google Scholar]

- Matia, K.; Pal, M.; Salunkay, H.; Stanley, H.E. Scale-dependent price fluctuations for the Indian stock market. EPL 2004, 66, 909–914. [Google Scholar] [CrossRef] [Green Version]

- Pan, R.K.; Sinha, S. Inverse-cubic law of index fluctuation distribution in Indian markets. Physica A 2008, 387, 2055–2065. [Google Scholar] [CrossRef] [Green Version]

- Pan, R.K.; Sinha, S. Self-organization of price fluctuation distribution in evolving markets. EPL 2007, 77, 58004. [Google Scholar] [CrossRef] [Green Version]

- Huang, Z.-F. The first 20 min in the Hong Kong stock market. Physica A 2000, 287, 405–411. [Google Scholar] [CrossRef] [Green Version]

- Wang, B.H.; Hui, P.M. The distribution and scaling of fluctuations for Hang Seng index in Hong Kong stock market. Eur. Phys. J. B 2001, 20, 573–579. [Google Scholar] [CrossRef]

- Matteo, T.D.; Aste, T.; Dacorogna, M.M. Scaling behaviors in differently developed markets. Physica A 2003, 324, 183–188. [Google Scholar] [CrossRef]

- Wan, Y.-L.; Xie, W.-J.; Gu, G.-F.; Jiang, Z.-Q.; Chen, W.; Xiong, X.; Zhang, W.; Zhou, W.-X. Statistical properties and pre-hit dynamics of price limit hits in the Chinese stock markets. PLoS ONE 2015, 10, e0120312. [Google Scholar] [CrossRef]

- Yan, C.; Zhang, J.W.; Zhang, Y.; Tang, Y.N. Power-law properties of Chinese stock market. Physica A 2005, 353, 425–432. [Google Scholar] [CrossRef]

- Dou, G.X.; Ning, X.X. Statistical properties of probability distributions of returns in Chinese stock markets. Chin. J. Manag. Sci. 2007, 15, 16–22. [Google Scholar]

- Chen, S.; Yang, H.L.; Li, S.F. Multiscale power-law properties and criticality of Chinese stock market. Chin. J. Manag. Sci. 2008, 16, 8–15. [Google Scholar]

- Gu, G.-F.; Chen, W.; Zhou, W.-X. Empirical distributions of Chinese stock returns at different microscopic timescales. Physica A 2008, 387, 495–502. [Google Scholar] [CrossRef] [Green Version]

- Mu, G.-H.; Zhou, W.-X. Tests of nonuniversality of the stock return distributions in an emerging market. Phys. Rev. E 2010, 82, 066103. [Google Scholar] [CrossRef]

- Bai, M.-Y.; Zhu, H.-B. Power law and multiscaling properties of the Chinese stock market. Physica A 2010, 389, 1883–1890. [Google Scholar] [CrossRef]

- D’Agostino, R.B.; Belanger, A.; D’Agostino, R.B., Jr. A suggestion for using powerful and informative tests of normality. Am. Stat. 1990, 44, 316–321. [Google Scholar]

- Anscombe, F.J.; Glynn, W.J. Distribution of the kurtosis statistic b2 for normal samples. Biometrika 1983, 70, 227–234. [Google Scholar] [CrossRef]

- Liu, P.; Zheng, Y. Temporal and spatial evolution of the distribution related to the number of COVID-19 pandemic. Physica A 2022, 603, 127837. [Google Scholar] [CrossRef]

- Liu, P.; Zheng, Y. Distribution law of the COVID-19 number through different temporal stages and geographic scales. arXiv 2022, arXiv:2208.06435. [Google Scholar]

- Queirós, S.M.D. on non-Gaussianity and dependence in financial time series: A nonextensive approach. Quant. Finance 2005, 5, 475–487. [Google Scholar] [CrossRef]

- Queirós, S.M.D.; Moyano, L.G.; Souza, J.D.; Tsallis, C. A nonextensive approach to the dynamics of financial observables. Eur. Phys. J. B 2007, 55, 161–167. [Google Scholar] [CrossRef]

- Granha, M.F.B.; Vilela, A.L.M.; Wang, C.; Nelson, K.P.; Stanley, H.E. Opinion dynamics in financial markets via random networks. Proc. Natl. Acad. Sci. USA 2022, 119, e2201573119. [Google Scholar] [CrossRef] [PubMed]

Figure 1.

The time series of the SSECI and the SZSECI. The 1 min datasets over the 17-year period (4 January 2005 to 31 December 2021) analyzed in this paper are shown. The higher one and lower one represent the SSECI and the SZSECI, respectively.

Figure 1.

The time series of the SSECI and the SZSECI. The 1 min datasets over the 17-year period (4 January 2005 to 31 December 2021) analyzed in this paper are shown. The higher one and lower one represent the SSECI and the SZSECI, respectively.

Figure 2.

Probability density of returns over time intervals ranging from 1 min to 3840 min. Return is defined as , where refers to the time series of the SSECI (panel a) or the SZSECI (panel b). Different markers represent data of returns with different time intervals . These two panels share a common legend. It is evident that these distributions expand as increases.

Figure 2.

Probability density of returns over time intervals ranging from 1 min to 3840 min. Return is defined as , where refers to the time series of the SSECI (panel a) or the SZSECI (panel b). Different markers represent data of returns with different time intervals . These two panels share a common legend. It is evident that these distributions expand as increases.

Figure 3.

Probability density of the return as a function of the time interval . The black stars are the data points. The red and blue lines are straight-line fits to the data points over 1 15 and 60 3840, respectively. The fit results of slopes for red and blue lines are also shown. Similar scaling behavior is observed for both the SSECI (panel a) and the SZSECI (panel b). From this figure, the key parameter characterizing the Lévy -stable process is extracted (see main text for details). A potential crossover region at 15 60 is observed here.

Figure 3.

Probability density of the return as a function of the time interval . The black stars are the data points. The red and blue lines are straight-line fits to the data points over 1 15 and 60 3840, respectively. The fit results of slopes for red and blue lines are also shown. Similar scaling behavior is observed for both the SSECI (panel a) and the SZSECI (panel b). From this figure, the key parameter characterizing the Lévy -stable process is extracted (see main text for details). A potential crossover region at 15 60 is observed here.

Figure 4.

The comparison of rescaled PDFs of returns with theoretical models. (Panels a,c) reflect the SSECI, and (panels b,d) represent the SZSECI. The colored markers are data points with different time scales. The dashed black curves are Gaussian distributions with a mean of 0 and a standard deviation of 1 min data. The solid black curves are Student’s t-distribution fits 1 min data. The solid red curves are symmetrical Lévy -stable distributions with the observed parameters, as shown by the red text (see main text for details). The top two panels and the bottom two panels share a common legend, respectively.

Figure 4.

The comparison of rescaled PDFs of returns with theoretical models. (Panels a,c) reflect the SSECI, and (panels b,d) represent the SZSECI. The colored markers are data points with different time scales. The dashed black curves are Gaussian distributions with a mean of 0 and a standard deviation of 1 min data. The solid black curves are Student’s t-distribution fits 1 min data. The solid red curves are symmetrical Lévy -stable distributions with the observed parameters, as shown by the red text (see main text for details). The top two panels and the bottom two panels share a common legend, respectively.

Figure 5.

PDF and CCDF of the normalized return tails with a time scale of 1 min. (Panels a,c) reflect the SSECI, and (panels b,d) represent the SZSECI. The red full circles and blue empty circles represent positive and negative tails, respectively. Dashed black straight lines are straight-line fits to data. Fit results of power-law exponents are shown. It is evident that the positive and negative tails show very similar behavior and follow a similar asymptotic power-law decay.

Figure 5.

PDF and CCDF of the normalized return tails with a time scale of 1 min. (Panels a,c) reflect the SSECI, and (panels b,d) represent the SZSECI. The red full circles and blue empty circles represent positive and negative tails, respectively. Dashed black straight lines are straight-line fits to data. Fit results of power-law exponents are shown. It is evident that the positive and negative tails show very similar behavior and follow a similar asymptotic power-law decay.

Figure 6.

CCDF of the normalized return tails with different time scales in log–log plot. (Panels a,b) represent the SSECI and the SZSECI, respectively. These two panels share a common legend. The colored solid markers denote positive tails, and the corresponding open markers represent negative tails. The solid and dashed black curves represent the standard normal distribution and the Student’s t-distribution (with a degree of freedom of 3.14 and a standard deviation of 1), respectively. Scaling behavior in tail distributions is observed here, and the tails with small follow an asymptotic power law decay.

Figure 6.

CCDF of the normalized return tails with different time scales in log–log plot. (Panels a,b) represent the SSECI and the SZSECI, respectively. These two panels share a common legend. The colored solid markers denote positive tails, and the corresponding open markers represent negative tails. The solid and dashed black curves represent the standard normal distribution and the Student’s t-distribution (with a degree of freedom of 3.14 and a standard deviation of 1), respectively. Scaling behavior in tail distributions is observed here, and the tails with small follow an asymptotic power law decay.

Figure 7.

CCDF of return tails with different time scales in log–linear plot. (Panels a,b) reflect the SSECI and the SZSECI, respectively. Colored markers are for positive tails. Solid straight lines are exponential fits to data, and the values of with its fitting errors are also presented here. These two panels share a common legend. To keep the figure from looking cluttered, the negative tails are not shown here; they feature similar results to positive tails.

Figure 7.

CCDF of return tails with different time scales in log–linear plot. (Panels a,b) reflect the SSECI and the SZSECI, respectively. Colored markers are for positive tails. Solid straight lines are exponential fits to data, and the values of with its fitting errors are also presented here. These two panels share a common legend. To keep the figure from looking cluttered, the negative tails are not shown here; they feature similar results to positive tails.

Figure 8.

Comparison of moments between the normalized return data and the standard normal distribution for the SSECI (panel a) and the SZSECI (panel b). The colored curves denote the data, and the solid black curves refer to the moments of standard normal distribution. These two panels share a common legend. It is evident that the data gradually converge to the standard normal distribution as increases.

Figure 8.

Comparison of moments between the normalized return data and the standard normal distribution for the SSECI (panel a) and the SZSECI (panel b). The colored curves denote the data, and the solid black curves refer to the moments of standard normal distribution. These two panels share a common legend. It is evident that the data gradually converge to the standard normal distribution as increases.

Figure 9.

The moment distance between the normalized return data and the standard normal distribution (panel a) and the speed of convergence of data (panel b). is the time scale divided by 1 min. The circle and star points represent the data of SSECI and SZSECI, respectively.

Figure 9.

The moment distance between the normalized return data and the standard normal distribution (panel a) and the speed of convergence of data (panel b). is the time scale divided by 1 min. The circle and star points represent the data of SSECI and SZSECI, respectively.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Liu, P.; Zheng, Y. Precision Measurement of the Return Distribution Property of the Chinese Stock Market Index. Entropy 2023, 25, 36. https://0-doi-org.brum.beds.ac.uk/10.3390/e25010036

AMA Style

Liu P, Zheng Y. Precision Measurement of the Return Distribution Property of the Chinese Stock Market Index. Entropy. 2023; 25(1):36. https://0-doi-org.brum.beds.ac.uk/10.3390/e25010036

Chicago/Turabian StyleLiu, Peng, and Yanyan Zheng. 2023. "Precision Measurement of the Return Distribution Property of the Chinese Stock Market Index" Entropy 25, no. 1: 36. https://0-doi-org.brum.beds.ac.uk/10.3390/e25010036

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.