The environmental performance for new high-tech zone projects and the associated influencing factors were developed as a general form of the regression model based on the preliminary research hypothesis. The general form was expressed as:

where Y is the environmental performance value of the dependent variable calculated by DEA,

is the regression coefficient for the model,

X1–

X8 are the independent variables (eight internal and external influencing factors), and

is a constant term.

4.4.1. Descriptive Statistical Analysis

The descriptive statistics in

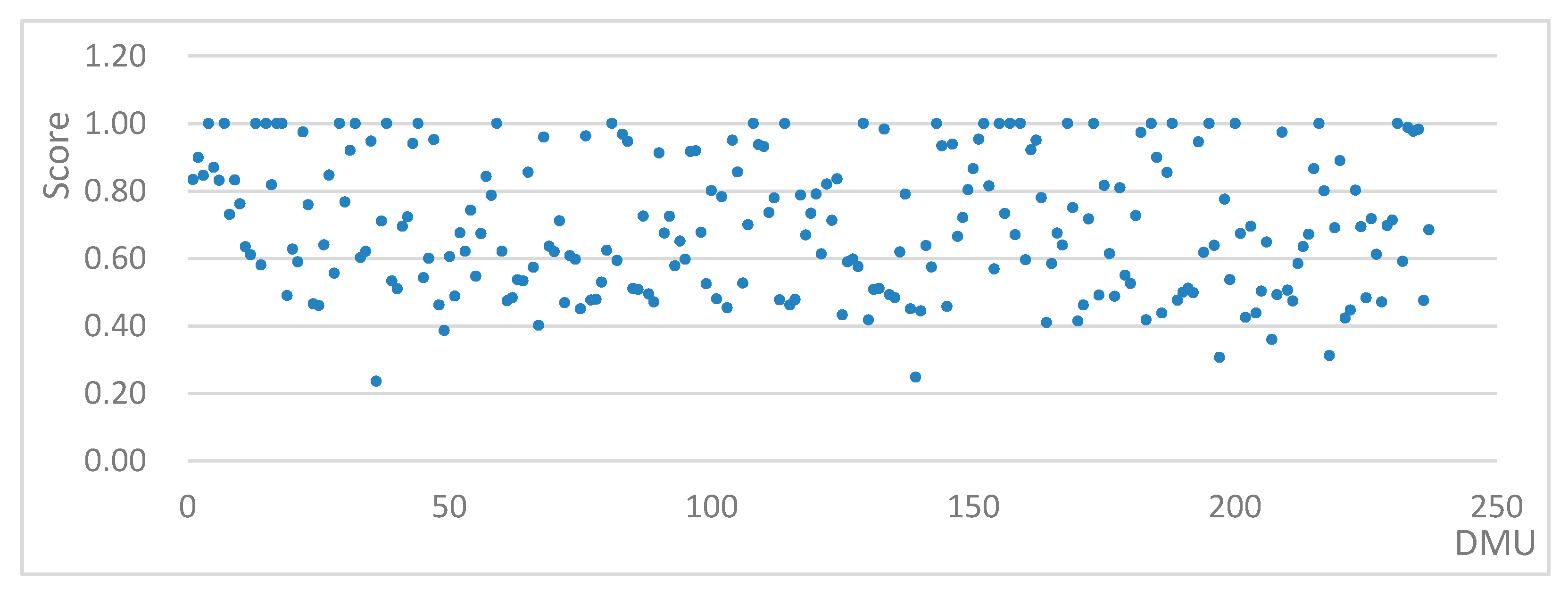

Table 5 indicate that the mean value for the Y environmental performance was 0.6976; that is, 69.76% of environmental resource inputs contributed to the environmental output, but 30.24% of the environmental resources investment was wasted in the implementation process, which means that the environmental performance level of the new project had a large improvement space. The standard deviation for the environmental performance was 0.1985, which was less than 0.2, which indicated that the environmental performance was concentrated around the mean. The minimum environmental performance value was 23.7%, and the maximum was 100%, which meant that the overall environmental performance evaluation results were different for different projects, that there were significant environmental performance differences in the new projects, and that the environmental performances across the enterprises were uneven.

The mean enterprise nature data group indicator indicated that there were more non-listed enterprises than listed enterprises in the research sample. The ROE average was 0.1598, the maximum was 2.68, and the minimum was −1.25. The mean value was low, and the maximum value and the minimum value had positive and negative values, indicating that the new project owner had a win or loss in their current business. The asset-liability ratio, which reflected the long-term solvency, was generally low, but the financial status was relatively healthy, with an average of 0.487 and a standard deviation of 0.256, which indicated that the asset-liability ratio was concentrated around the mean. The enterprise scale also adopted dummy variables, which were counted based on the registered capital scale of the project; that is, a minimum value of 1, a maximum value of 6, and an average value of 3.18; therefore, the enterprise size distribution was considered reasonable. The four variables for environmental management: implementation frequency, project duration, social petitions, and government audits, were extracted from actual statistics. In the sample, the enterprises that had environmental management system certifications, environmental protection departments, and new energy conservation and emissions reduction technologies were counted as the environmental management behavior implementation frequencies; the maximum environmental management behavior implementation frequency was 37, the minimum value was 3, and the average was 19.36; therefore, environmental management for the new project fixed assets investment was considered good. The project duration was based on a monthly construction period, with the maximum being 83, the minimum being 2, the mean being 28.05, and the standard deviation was 13.24, which indicated that the sample data in this group were relatively dispersed, which was consistent with the actual situation because new project scales, technical implementation difficulties, and therefore construction periods varied considerably. The number of social petitions was taken as the number of complaints from residents in surrounding communities during new project construction, for which the maximum was eight, the minimum was zero, and the mean was 2.56. The number of government audits was the number of times an enterprise was audited by the environmental department, for which the maximum was 5, the minimum was 1, and the mean was 3.31. All indicators in the above data sets reflected the actual new project situation for enterprises currently participating in energy conservation assessments and reviews.

4.4.2. Statistical Tests and Regression Analyses

In this paper, SPSS Statistics for Windows, version 19.0 ( SPSS Inc. Chicago, IL, USA) was used to calculate the Pearson’s correlation coefficient to test the correlations between the explanatory variables.

The correlation matrix in

Table 6 shows the strength and direction of each independent variable and dependent variable, as well as the correlations between the independent variables. As can be seen, all eight independent variables were correlated with Y, most indicators passed the 1% (bilateral) and 5% (bilateral) significance tests, and the eight selected independent variables were found to better explain the dependent variables. The correlation between X

4 (Enterprise scale) and X

6 (Project duration) was 0.459 at a 0.01 significance level; therefore, as the absolute correlation value was greater than 0.4, there was a moderate or low degree of correlation, indicating possible multicollinearity between the two indicators. Therefore, the multicollinearity in the multiple regression analysis was tested with Tolerance and VIF (variance inflation factor). As outlined in the fourth edition of modern psychology and educational statistics, the multiple regression method, which can be divided into a forced entry method and forced elimination method, should include all predictive variables in the regression equation when estimating the dependent variables. As the forced entry method includes all predictors with explanatory power for the dependent variables in the regression equation and then calculates the regression coefficients of all the variables without considering the relationships between the predictors at a certain significance level, the forced entry method was adopted in this paper, and therefore, there was only one regression model. As can be seen from the results for the relevant indicators in the fitting model in

Table 7, the R square was 0.401, the Adjust R square was 0.349, and the goodness of fit was 0.349, which is considered a good result in social science and management economics. The results indicated that the eight independent variables in the regression model explained 34.9% of the degree of variation in the dependent variables.

Table 8 shows the variance analysis test results for the fitted regression model. The F-value for the significance test of variance was 187.677, and the P-value for the significance test was 0.000, which was less than the significance level of 0.05, indicating that the overall explanatory variance of the regression model reached the significance level. The F-value test also passed the significance test. The regression equation was found to have a good goodness of fit, and therefore, the regression equation reflected the research phenomenon well. However, as the statistical significance of the model did not mean that all model variables had statistical significance, it was necessary to further test each independent variable to determine which regression coefficients were significant.

Therefore, a collinearity diagnosis was conducted on the multiple linear regression analysis, the results for which are shown in

Table 9, which shows the regression coefficients in a coefficient summary table, the t-values, the significance probability values for the corresponding significance test, the tolerance, and the VIF for the collinearity statistics. The smaller the tolerance, the higher the accuracy of the prediction by the other independent variables, and the more serious the multicollinearity, and when the tolerance is less than 0.1, severe multicollinearity exists. The VIF (variance inflation factor) is the reciprocal of tolerance; that is, the larger the VIF, the more serious the multicollinearity; therefore, the VIF should not be greater than five in general.

As can be seen from

Table 9, the tolerance values for the eight independent variables were all greater than 0.1, and the VIF values were all below 4.000, with none being greater than the evaluation index value 10, which indicated that there were no obvious multicollinearity problems between the independent variables in the regression equation.

4.4.3. Discussion

From

Table 9, standardized regression coefficients were adopted for the standardized regression model, as follows:

from which the following was observed.

(1) As the enterprise nature coefficient was 0.122, the symbol was positive, the t-test was 2.899, and the probability P was 0.027, it passed the 5% significance level test, which indicated that there was a significant positive correlation between environmental performance and enterprise nature; therefore, Hypothesis 1 was valid; that is, there is a positive correlation between the enterprise nature and the new project environmental performance.

(2) The ROE coefficient was 0.133, the symbol was positive, the t-test was 3.625, and the probability P was 0.032; therefore, the ROE passed the 5% significance test, which indicated that the environmental performance was positively correlated with ROE and Hypothesis 2 was valid; that is, there is a positive correlation between profitability and new project environmental performance.

(3) The asset-liability ratio coefficient was 0.012, the symbol was negative, the t-test was −2.015, and the probability P was 0.007, which passed the 1% significance test, indicating that environmental performance had a significant negative correlation with the asset-liability ratio and Hypothesis 3 was valid; that is, there is a negative correlation between the financial status of the project and the environmental performance of the new project.

(4) The enterprise scale coefficient was 0.034, the symbol was negative, the t-test was −1.148, and the probability P was 0.252; therefore, the significance test was not passed, which may have been due to the principle of managing diminishing returns and the limited enterprise scales. As the enterprise scale expands, transaction costs increase. At the same time, the management capacity was limited, and management efficiency too large, resulting in an efficiency decrease; therefore, Hypothesis 4 was not valid; that is, there is not a positive correlation between the project enterprise scale and new project environmental performance.

(5) The environmental management behavior implementation frequency coefficient was 0.381, the symbol was positive, the t-test was 8.397, and the probability P was 0.000, which passed the 1% significance test, which indicated that there was a significant positive correlation between the environmental performance and the environmental management behavior implementation frequency; therefore, Hypothesis 5 was valid; that is, there is a positive correlation between the environmental management behavior implementation frequency and the environmental performance of new projects.

(6) The project duration coefficient was 0.059, the symbol was negative, the t-test was 3.506, and the probability P was 0.712; therefore, the significance test was not passed, which may have been related to social inertia. Because of the economic externalities associated with environmental problems, perfunctory behavior or free-riding is common. Therefore, the longer the project duration, the more obvious the perfunctory free-riding behavior, and the lower the environmental performance; therefore, Hypothesis 6 was not valid: that is, there is not a positive correlation between the project period and the environmental performance of the new project.

(7) The social petition coefficient was 0.279, the symbol was negative, the t-test was −7.449, and the probability P was 0.000, which passed the 1% significance test, and indicated that the environmental performance level had a significant negative correlation with the number of social petitions; therefore, Hypothesis 7 should be corrected to the following; there is a negative correlation between the society petition frequency and the environmental performance of new projects. The reason for this could be that the amount of pollution discharged by new projects participating in energy conservation evaluation assessment and reviews does not normally reach the evaluation standard, which can significantly impact the surrounding communities; therefore, there would be an increase in opposition and complaints.

(8) The government audit number coefficient was 0.340, the symbol was positive, the t-test was 8.010, and the probability P was 0.000, which passed the 1% significance test, and indicated that the environmental performance had a significant positive correlation with the number of government audits; therefore, Hypothesis 8 was valid: that is, there is a positive correlation between government supervision behavior and the environmental performance of new projects. The verification of this hypothesis indicated that, to a certain extent, external pressure (mainly from the management committee of the high-tech zone and local governments at various levels) could prompt enterprises to strengthen their environmental management behavior and improve their environmental performance. Therefore, high-tech development zone administrative committees need to supervise the environmental management of enterprises and carry out energy conservation evaluation assessments and reviews.

{kind=link}

{kind=link}