Cost-Free LTC Model Incorporated into Private Pension Schemes

Abstract

:1. Introduction

2. Literature Review

- Provision of services in kind (Netherlands and Sweden).

- Financial benefits for comprehensive coverage plans (France).

- Cash benefits for dependent care (Austria, Germany and Italy).

3. Methodology

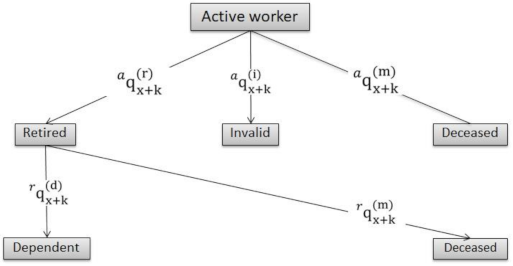

3.1. The Model

3.2. The Factor

4. An Application to Spain Results

- (a)

- Level I: Moderate dependency. The individual needs help to perform several basic daily activities at least once a day or has intermittent or limited support needs for personal autonomy.

- (b)

- Level II: Severe dependency. Assistance is needed to perform several basic daily activities with a frequency of two or three times a day, but does not require permanent assistance.

- (c)

- Level III: Severe dependency. Assistance is needed to perform several basic daily activities several times a day. Due to total loss of physical, mental, intellectual or sensory autonomy, the individual needs extensive support for personal autonomy.

- (i)

- Basic: Essential coverage is provided and financed by the Spanish General Administration.

- (ii)

- Complementary: the coverage is provided by agreements between the Spanish General Administration and the Autonomous Communities.

- (iii)

- Improvement Level: the private sector has a role in this area.

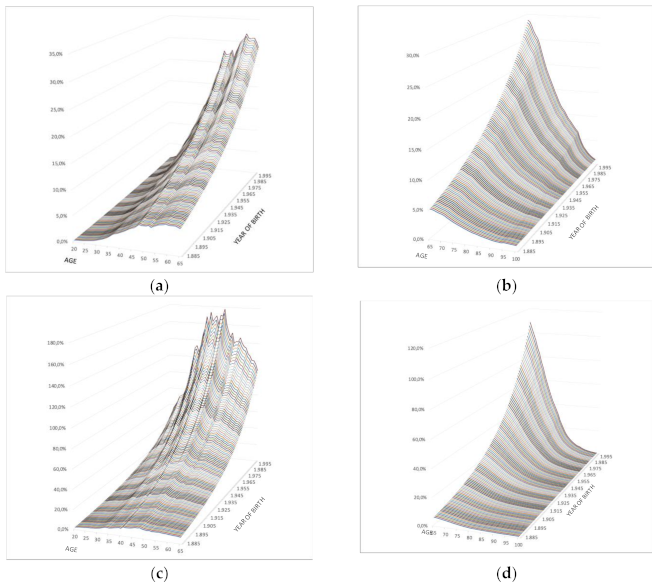

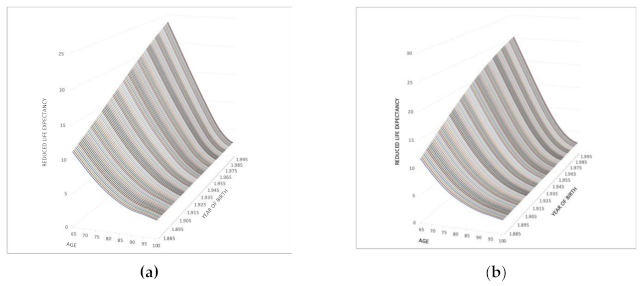

4.1. Severe and Highly Dependent Mortality

- The greatest increase in the dependent population mortality over the independent population is found at ages close to retirement, both for men and women, with more pronounced values in more recent generations.

- During the retirement period, the excess mortality of severely and highly dependent people is reduced to almost zero differentials. This implies that the mortality of a self-employed person is similar to that of a severely dependent person at the end of life.

- The older generations show lower increases in mortality in dependency than the younger generations, so the effect of severe and high dependency will be significantly greater in the younger generations.

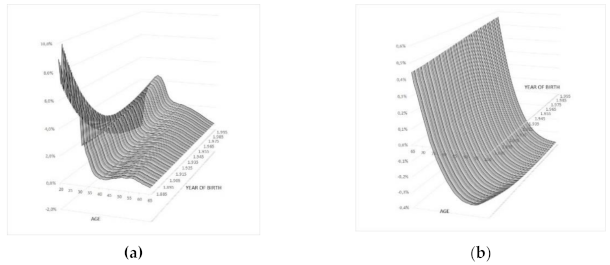

4.2. Corrective Factor for Severe or High Dependence

5. Discussion

- The increase may be intended to reimburse some of the LTC expenditure rather than being paid directly to a beneficiary.

- If there were a surplus, it would increase the initial pension.

- Accuracy and sufficient data on newly dependent people produced at each age, by degree of dependency, age and sex. Actuarial science requires a great deal of data from which to obtain significant probabilities. This would allow for the automatic incorporation of the transition probability of becoming a dependent. Thus, the application of the conversion factor would automatically adapt the expenditure to the life expectancy as a dependent resulting in a zero cost.

- Knowing the probability of a previous transition, a pension could also be designed that is totally independent and additional to the retirement pension; obviously, this would increase the final cost but would provide an opportunity to be financed progressively in the period of activity. Finding the optimum coverage would also come from determining and standardising the average cost at each age of the LTCs.

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Holzmann, R.; Hinz, R. Old-Age Income Support in the 21st Century. In Old-Age Income Support in the 21st Century; The World Bank: Washington, DC, USA, 2005; p. 229. [Google Scholar]

- Organization for Economic Cooperation and Development (OECD). Help Wanted?—Providing and Paying for Long-Term Care; OECD Press: Paris, France, 2011. [Google Scholar]

- Boyer, M.; De Donder, P.; Fluet, C.; Leroux, M.L.; Michaud, P.C. A Canadian Parlor Room–Type Approach to the Long-Term-Care Insurance Puzzle. Can. Pub. Pol. 2019, 45, 262–282. [Google Scholar] [CrossRef]

- Grignon, M.; Bernier, N. Financing Long-Term Care in Canada; Institute for Research on Public Policy Study: Montreal, Canada, 2012; p. 33. [Google Scholar]

- Konetzka, R.T.; He, D.; Dong, J.; Nyman, J.A. Moral hazard and long-term care insurance. Geneva Pap. Risk Insur. Issues Pr. 2019, 44, 231–251. [Google Scholar] [CrossRef]

- Brown, J.R.; Finkelstein, A. The Private Market for Long-Term Care Insurance in the United States: A Review of the Evidence. J. Risk Ins. 2009, 76, 5–29. [Google Scholar] [CrossRef]

- Campbell, J.C.; Ikegami, N.; Kwon, S. Policy learning and cross-national diffusion in social long-term care insurance: Germany, Japan, and the Republic of Korea. Int. Soc. Sec. Rev. Geneva 2009, 62, 63–80. [Google Scholar] [CrossRef] [Green Version]

- Colombo, F.; Llena-Nozal, A.; Mercier, J.A.; Tadens, F. Help Wanted? Providing and Paying for Long-Term Care; OECD Health Policy Studies: Paris, France, 2011; 324p. [Google Scholar]

- De La Peña, J.I. Más allá del seguro de dependencia: El seguro de residencia. Actual. Financ. 2000, 10, 37–54. [Google Scholar]

- Wiener, J.M.; Tilly, J.; Cuéllar, A.E. Consumer-Directed Home Care in the Netherlands, England and Germany; Public Policy Institute: Washington, DC, USA, 2003; p. 79. [Google Scholar]

- Zweifel, P.; Felder, S.; Werblow, A. Population ageing and health care expenditure: New evidence for the “red herring”. Geneva Pap. Risk Insur. Issues Pract 2004, 29, 652–666. [Google Scholar] [CrossRef]

- Bonsang, E. How do middle-aged children allocate time and money transfers to their older parents in Europe? Empirica 2007, 34, 171–188. [Google Scholar] [CrossRef]

- Bonsang, E. Does informal care from children to their elderly parents substitute for formal care in Europe? J. Health Econ. 2009, 28, 143–154. [Google Scholar] [CrossRef]

- Charles, K.K.; Sevak, P. Can family caregiving substitute for nursing home care? J. Health Econ. 2005, 24, 1174–1190. [Google Scholar] [CrossRef]

- Pinquart, M.; Sörensen, S. Older Adults’ Preferences for Informal, Formal, and Mixed Support for Future Care Needs: A Comparison of Germany and the United States. Int. J. Aging Hum. Dev. 2002, 54, 291–314. [Google Scholar] [CrossRef]

- Van Houtven, C.H.; Norton, E.C. Informal care and health care use of older adults. J. Health Econ. 2004, 23, 1159–1180. [Google Scholar] [CrossRef]

- Courbage, C.; Costa-Font, J. On Health, Ageing and Insurance. Geneva Pap. Risk Insur.-Issues Pract 2006, 31, 551–556. [Google Scholar] [CrossRef]

- Organization for Economic Cooperation and Development (OECD). Long-Term Care for Older People (2001–2004); The OECD Health Project; OECD Press: Paris, France, 2005. [Google Scholar]

- Organization for Economic Cooperation and Development (OECD). Ageing and Employment Policies: Live Longer, Work Longer; OECD Press: Paris, France, 2006. [Google Scholar]

- Swartz, K. Searching for a Balance of Responsibilities: OECD Countries’ Changing Elderly Assistance Policies. Annu. Rev. Public Health 2013, 34, 397–412. [Google Scholar] [CrossRef]

- Barr, N. Long-term Care: A Suitable Case for Social Insurance. Soc. Policy Adm. 2010, 44, 359–374. [Google Scholar] [CrossRef] [Green Version]

- Colombo, F.; Mercier, J. Help Wanted? Fair and Sustainable Financing of Long-term Care Services. Appl. Econ. Perspect. Policy 2012, 34, 316–332. [Google Scholar] [CrossRef]

- Forder, J.; Fernández, J.L. What Works Abroad? Evaluating the Funding of Long-Term Care: International Perspectives. Report Com-missioned by Bupa Care Services. Personal Social Services Research Unit Discussion Paper 2794; PSSRU: Canterbury, UK, 2011; 46p. [Google Scholar]

- Comas-Herrera, A.; Guillen, M. How Much Risk is Mitigated by LTC Insurance? A Case Study of the Public System in Spain. SSRN Electron. J. 2011, 37, 712–724. [Google Scholar] [CrossRef] [Green Version]

- Miyazawa, K.; Moudoukoutas, P.; Yagi, T. Is Public Long-Term Care Insurance Necessary? J. Risk Insur. 2000, 67, 249. [Google Scholar] [CrossRef]

- Zuchandke, A.; Reddemann, S.; Krummaker, S.; Von Der Schulenburg, J.-M.G. Impact of the Introduction of the Social Long-Term Care Insurance in Germany on Financial Security Assessment in Case of Long-Term Care Need. Geneva Pap. Risk Insur. Issues Pr. 2010, 35, 626–643. [Google Scholar] [CrossRef] [Green Version]

- International Actuarial Association (IAA). Pension Fund Environmental, Social and Governance Risk Disclosures: Developing Global Practice; International Actuarial Association: Ottawa, Canada, 2020; p. 24. [Google Scholar]

- Costa-Font, J.; Courbage, C.; Zweifel, P. Policy Dilemmas in Financing Long-term Care in Europe. Glob. Policy 2016, 8, 38–45. [Google Scholar] [CrossRef] [Green Version]

- Kenny, T.; Barnfield, J.; Daly, L.; Dunn, A.; Passey, D.; Rickayzen, B.; Teow, A. The future of social care funding: Who pays? Br. Actuar. J. 2016, 22, 10–44. [Google Scholar] [CrossRef] [Green Version]

- Hurd, M.D.; Michaud, P.-C.; Rohwedder, S.; Wise, D.A. The Lifetime Risk of Nursing Home Use. In Discoveries in the Economics of Aging; University of Chicago Press: Chicago, IL, USA, 2015; pp. 81–114. [Google Scholar]

- Okma, K.; Gusmano, M.K. Aging, Pensions and Long-term Care: What, Why, Who, How? Comment on “Financing Longterm Care: Lessons from Japan”. Int. J. Health Policy Manag. 2019, 9, 218–221. [Google Scholar] [CrossRef]

- Lusardi, A.; Michaud, P.C.; Mitchell, O.S. Optimal Financial Knowledge and Wealth Inequality. J. Political Econ. 2017, 125, 431–477. [Google Scholar] [CrossRef] [Green Version]

- Herranz, P.; Guerrero, F.M.; Segovia, M.M. Long-term care insurance actuarial model. Rev. Mét. Cuant. Econ. Empr. 2008, 6, 42–73. [Google Scholar]

- Calmus, D. The Long-Term Care Funding Crisis; Center for Policy Innovation: Washington, DC, USA, 2013; p. 15. [Google Scholar]

- Chen, Y.-P. Funding Long-term Care in the United States: The Role of Private Insurance. Geneva Pap. Risk Insur. Issues Pr. 2001, 26, 656–666. [Google Scholar] [CrossRef]

- De La Peña, J.I. El impacto del envejecimiento de la población en el seguro de salud y de dependencia. Pap. Poblac. 2003, 35, 47–72. [Google Scholar]

- Da Roit, B.; Le Bihan, B.; Österle, A. Long-term care policies in Italy, Austria and France: Variations in cash-for-care schemes. Soc. Policy Admin 2007, 41, 653–671. [Google Scholar] [CrossRef]

- Da Roit, B.; Le Bihan, B. Similar and Yet So Different: Cash-for-Care in Six European Countries’ Long-Term Care Policies. Milbank Q. 2010, 88, 286–309. [Google Scholar] [CrossRef] [Green Version]

- Damiani, G.; Farelli, V.; Anselmi, A.; Sicuro, L.; Solipaca, A.; Burgio, A.; Iezzi, D.F.; Ricciardi, G. Patterns of Long Term Care in 29 European countries: Evidence from an exploratory study. BMC Health Serv. Res. 2011, 11, 316. [Google Scholar] [CrossRef]

- Robine, J.M.; Michel, J.P.; Hermann, F.R. Who will care for the oldest people? BMJ 2007, 334, 570–571. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Tennyson, S.; Yang, H.K. The role of life experience in long-term care insurance decisions. J. Econ. Psychol. 2014, 42, 175–188. [Google Scholar] [CrossRef]

- Brown, J.R.; Finkelstein, A. Insuring Long-Term Care in the United States. J. Econ. Perspect. 2011, 25, 119–142. [Google Scholar] [CrossRef] [Green Version]

- Cremer, H.; De Donder, P.; Pestieau, P. Providing Sustainable Long-Term Care: A Looming Challenge; Technical Report 3; Toulouse School of Economics: Toulouse, France, 2009. [Google Scholar]

- De Donder, P.; Leroux, M.L. The political economy of (in)formal long term care transfers. CEDIA Work. Pap. 2015. [Google Scholar]

- Moran, M.; Glendinning, C.; Wilberforce, M.; Stevens, M.; Netten, A.; Jones, K.; Manthorpe, J.; Knapp, M.; Fernández, J.L.; Challis, D.; et al. Older people’s experiences of cash-for-care schemes: Evidence from the English Individual Budget pilot projects. Ageing Soc. 2013, 33, 826–851. [Google Scholar] [CrossRef] [Green Version]

- Arksey, H.; Kemp, P.A. Dimensions of Choice: A Narrative Review of Cash-for-Care Schemes; Working Paper No. DHP 2250; Social Policy Research Unit, University of York: York, UK, 2008; p. 25. [Google Scholar]

- Warshawsky, M.J. Retirement Income: Risks and Strategies; MIT Press: Cambridge, MA, USA, 2012; 280p. [Google Scholar]

- Brown, J.R.; Warshawsky, M. The life care annuity: A new empirical examination of an insurance innovation that addresses problems in the markets for life annuities and long-term care insurance. J. Risk Ins. 2013, 80, 677–703. [Google Scholar] [CrossRef]

- Murtaugh, C.M.; Spillman, B.C.; Warshawsky, M.J. In Sickness and in Health: An Annuity Approach to Financing Long-Term Care and Retirement Income. J. Risk Insur. 2001, 68, 225. [Google Scholar] [CrossRef] [Green Version]

- Warshawsky, M.J. The Life Care Annuity—A Proposal for an Insurance Product Innovation to Simultaneously Improve Financing and Benefit Provision for Long-Term Care and to Insure the Risk of Outliving Assets in Retirement; Working Paper No 2; Georgetown University Health Policy Institute: Washington, DC, USA, 2007; 30p. [Google Scholar]

- Zhou-Richter, T.; Gründl, H. Life Care Annuities—Trick or Treat for Insurance Companies? SSRN Electron. J. 2011. [Google Scholar] [CrossRef]

- Pitacco, E. Longevity Risk in Living Benefits; Working Paper 23/02; Center for Research on Pensions and Welfare Policies: Turin, Italy, 2002; 37p. [Google Scholar]

- Davidoff, T. Housing, health, and annuities. J. Risk Ins. 2009, 76, 31–52. [Google Scholar] [CrossRef]

- Spillman, B.C.; Murtaugh, C.M.; Warshawsky, M.J. Policy implications of an annuity approach to integrating long-term care financing and retirement income. J. Aging Health 2003, 15, 45–73. [Google Scholar] [CrossRef] [PubMed]

- Haberman, S.; Pitacco, E. Actuarial Models for Disability Insurance; CRC Press: London, UK, 2018; p. 280. [Google Scholar]

- Pitacco, E. Biometric Risk Transfers in Life Annuities and Pension Products: A Survey; Working Paper 2013/25; Center for Research on Pensions and Welfare Policies: Turin, Italy, 2013; 34p. [Google Scholar]

- Yakoboski, P.J. Understanding the motivations of long-term care insurance owners: The importance of retirement planning. Benefits Q. 2002, 18, 16–21. [Google Scholar] [PubMed]

- Webb, D.C. Asymmetric Information, Long-Term Care Insurance, and Annuities: The Case for Bundled Contracts. J. Risk Insur. 2009, 76, 53–85. [Google Scholar] [CrossRef]

- Bommier, A.; Lee, R.D. Overlapping generations models with realistic demography. J. Popul. Econ. 2003, 16, 135–160. [Google Scholar]

- Finkelstein, A.; Poterba, J. Adverse Selection in Insurance Markets: Policyholder Evidence from the U.K. Annuity Market. J. Politi. Econ. 2004, 112, 183–208. [Google Scholar] [CrossRef] [Green Version]

- Finkelstein, A.; McGarry, K. Multiple Dimensions of Private Information: Evidence from the Long-Term Care Insurance Market. Am. Econ. Rev. 2006, 96, 938–958. [Google Scholar] [CrossRef]

- Crimmins, E.M.; Beltrán-Sánchez, H. Mortality and Morbidity Trends: Is There Compression of Morbidity? J. Gerontol. Ser. B 2010, 66, 75–86. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Yang, Z.; Norton, E.C.; Stearns, S.C. Longevity and Health Care Expenditures: The Real Reasons Older People Spend More. J. Gerontol. Ser. B 2003, 58, S2–S10. [Google Scholar] [CrossRef]

- Spillman, B.C.; Lubitz, J. The Effect of Longevity on Spending for Acute and Long-Term Care. N. Engl. J. Med. 2000, 342, 1409–1415. [Google Scholar] [CrossRef]

- Spillman, B.C.; Lubitz, J. New Estimates of Lifetime Nursing Home Use: Have Patterns of Use Changed? Med. Care 2002, 40, 965–975. [Google Scholar] [CrossRef]

- Manton, K.G.; Gu, X.; Lamb, V.L. Long-Term Trends in Life Expectancy and Active Life Expectancy in the United States. Popul. Dev. Rev. 2006, 32, 81–105. [Google Scholar] [CrossRef]

- Zhou-Richter, T.; Browne, M.J.; Gründl, H. Don´t They Care? Or, Are They Just Unaware? Risk Perception and the Demand for Long-Term Care Insurance. J. Risk Ins. 2010, 77, 715–747. [Google Scholar] [CrossRef]

- Boyer, M.M.; Glenzer, F. Pensions, annuities, and long-term care insurance: On the impact of risk screening. Geneva Risk Insur. Rev. 2020, 1–42. [Google Scholar] [CrossRef]

- Fernández-Ramos, M.C.; De La Peña, J.I. Influencia de la cobertura de dependencia en los planes de pensiones. An. Asepuma 2015, 23, 403. [Google Scholar]

- De La Peña, J.I.; Fernández-Ramos, M.C.; Peña-Miguel, N. Long Term care pension benefits coverage via conversion factor based on different mortality rates: More money as age goes on. Interciencia 2018, 43, 9–16. [Google Scholar]

- De La Peña, J.I. Planes de Previsión Social; Pirámide: Madrid, Spain, 2000; 784p. [Google Scholar]

- De la Peña, J.I.; Fernández-Ramos, M.C.; Herrera, A.T.; Peña-Miguel, N. Measures of actuarial balance in Spanish social security: Back to the past. An Inst. Actuar. Esp. 2017, 23, 129–143. [Google Scholar]

- Meneu, R.; Devesa, J.E.; Devesa, M.; Nagore, A.; Domínguez, I.; Encinas, B. The sustainability factor: Alternative designs with an actuarial and financial valuation of its effects over the parameters of the system. Econ. Esp. Prot. Soc. 2013, 4, 63–96. [Google Scholar]

- Barr, N. Pensions: Overview of the Issues. Oxf. Rev. Econ. Policy 2006, 22, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Finkelstein, A.; Poterba, J.; Rothschild, C. Redistribution by Insurance Market Regulation: Analyzing a Ban on Gender-Based Retirement Annuities. J. Financ. Econ. 2009, 91, 38–58. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Rothschild, C. Non exclusivity, Linear Pricing, and Annuity Market Screening. J. Risk Ins. 2015, 82, 1–32. [Google Scholar] [CrossRef]

- Villeneuve, B. Mandatory Pensions and the Intensity of Adverse Selection in Life Insurance Markets. J. Risk Insur. 2003, 70, 527–548. [Google Scholar] [CrossRef]

- Fernández-Ramos, M.C. Soluciones Pragmáticas en el Campo Privado para la Cobertura de la Dependencia en España. Ph.D. Thesis, Universidad del País Vasco, Bilbao, Spain, 14 July 2015; 336p. [Google Scholar]

- De la Peña, J.I.; Fernández-Ramos, M.C.; Herrera, A.T.; Iturricastillo, I.; Peña-Miguel, N. Dependence benefit into a pension plan upon specific mortality table. Econ. Esp. Prot. Soc. 2017, 9, 61–94. [Google Scholar]

- Ainslie, R. Annuity and Insurance Products for Impaired Lives; The Staple Inn Actuarial Society: London, UK, 2000. [Google Scholar]

- Rickayzen, B.D. An Analysis of Disability—Linked Annuities; Actuarial Research 180; Cass Business School: London, UK, 2007; 52p. [Google Scholar]

- Ellingsen, T.M. Mortality among disability pensioners. In Proceedings of the International Congress of Actuaries, Cape Town, South Africa, 8–12 March 2010. [Google Scholar]

- Sánchez, E.; López, J.M.; de Paz, S. La corrección de los tantos de mortalidad de los dependientes: Una aplicación al caso español. An Inst. Actuar Esp. 2008, 13, 135–151. [Google Scholar]

- Macdonald, A.; Pritchard, D. Genetics, Alzheimer’s and long-term care insurance. N. Am. Actuar. J. 2001, 5, 54–78. [Google Scholar] [CrossRef]

- Rickayzen, B.D.; Walsh, D.E.P. A Multi-State Model of Disability for the United Kingdom: Implications for Future Need for Long-Term Care for the Elderly. Br. Actuar. J. 2002, 8, 341–393. [Google Scholar] [CrossRef]

- Leung, E. Projecting the Needs and Costs of Long-Term Care in Australia; Research Paper 110; Centre for Actuarial Studies, University of Melbourne: Melbourne, Australia, 2003; 34p. [Google Scholar]

- Fernández-Ramos, M.C.; De La Peña, J.I. Legislative development of protection for dependence. Opportunities for the private sector: The case of the Castilla and Leon region, Spain. Rev. Estud. Reg. 2013, 97, 113–136. [Google Scholar]

- Ley 17/2012, de 27 de Diciembre, de Presupuestos Generales del Estado para el año 2013 [Law 17/2012, of 27 December, on the General State Budget for 2013] BOE 312. Available online: https://www.boe.es/boe/dias/2012/12/28/pdfs/BOE-A-2012-15651.pdf (accessed on 2 January 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Approximate Funds 2019 (USD Billion) | Structure |

|---|---|---|

| Australia | 2077 | Multi-employer funds, independent trustees and retail funds. |

| Canada | 1924 | Employer-sponsored, also industry and retail funds. |

| France | 155 | Unfunded industry-wide plans, employer-sponsored and insured retail funds. |

| Germany | 502 | Employer-sponsored also insured and unfunded. |

| Ireland | 184 | Employer-sponsored. |

| Italy | 210 | Employer-sponsored. |

| Japan | 1400 | (Excludes Japanese government pension fund.) Employer-sponsored, also retail funds. |

| Netherlands | 1690 | Employer- or multi-employer-sponsored. |

| Poland | 48 | Employer-sponsored. |

| South Africa | 231 | Employer- or multi-employer-sponsored. |

| Spain | 43 | Employer- or multi-employer-sponsored, also insured retail funds. |

| Switzerland | 1047 | Employer- or multi-employer-sponsored. |

| UK | 3451 | Employer-sponsored, multi-employer funds for minimum defined contribution benefits, also retail funds. |

| USA | 29,196 | Employer- or multi-employer-sponsored, also retail funds. |

| Total | 42,158 |

| Factors | Men | Women |

|---|---|---|

| 0.245 | 0.165 | |

| 1.135 | 1.09 | |

| 62.50 | 58.61 | |

| 0.1142 | 0.0962 |

| Age | ||||||||

|---|---|---|---|---|---|---|---|---|

| 20 | 0.009005 | 0.010674 | 85.4 | 92.5 | 0.009095 | 0.011724 | 54.3 | 48.6 |

| 25 | 0.000317 | 0.000285 | 81.4 | 88.7 | 0.000486 | 0.001895 | 49.9 | 44.5 |

| 30 | 0.000221 | 0.000162 | 76.5 | 83.8 | 0.000539 | 0.002627 | 45.0 | 39.9 |

| 35 | 0.000453 | 0.000202 | 71.6 | 78.9 | 0.001050 | 0.003963 | 40.2 | 35.5 |

| 40 | 0.001134 | 0.000280 | 66.8 | 74.0 | 0.002256 | 0.005997 | 35.4 | 31.3 |

| 45 | 0.001261 | 0.000275 | 62.2 | 69.1 | 0.003365 | 0.008909 | 30.9 | 27.3 |

| 50 | 0.001265 | 0.000325 | 57.6 | 64.2 | 0.005198 | 0.013246 | 26.4 | 23.5 |

| 55 | 0.001134 | 0.000340 | 52.9 | 59.3 | 0.008439 | 0.019416 | 22.2 | 20.2 |

| 60 | 0.001270 | 0.000395 | 48.2 | 54.4 | 0.014677 | 0.028025 | 18.2 | 17.2 |

| 65 | 0.001650 | 0.000518 | 43.5 | 49.5 | 0.025737 | 0.039513 | 14.6 | 14.6 |

| 70 | 0.002431 | 0.000740 | 38.9 | 44.6 | 0.054135 | 0.060454 | 11.6 | 12.5 |

| 75 | 0.003742 | 0.001048 | 34.4 | 39.8 | 0.085696 | 0.077951 | 9.1 | 10.8 |

| 80 | 0.005241 | 0.001447 | 30.1 | 35.0 | 0.124647 | 0.096128 | 7.3 | 9.4 |

| 85 | 0.007708 | 0.002037 | 25.9 | 30.2 | 0.165352 | 0.113471 | 6.1 | 8.4 |

| 90 | 0.010964 | 0.003079 | 21.9 | 25.6 | 0.201444 | 0.129209 | 5.3 | 7.6 |

| 95 | 0.017031 | 0.005315 | 18.2 | 21.0 | 0.231195 | 0.143675 | 4.7 | 7.0 |

| 100 | 0.025290 | 0.009638 | 14.7 | 16.6 | 0.255807 | 0.158651 | 4.4 | 6.3 |

| Age | |||||||

|---|---|---|---|---|---|---|---|

| 20 | 1.57 | 1.90 | 0.01% | 0.10% | 0.2891% | 31.1 | 43.9 |

| 25 | 1.63 | 1.99 | 0.53% | 5.64% | 2.9023% | 31.5 | 44.2 |

| 30 | 1.70 | 2.10 | 1.43% | 15.17% | 3.8768% | 31.5 | 43.9 |

| 35 | 1.78 | 2.22 | 1.32% | 18.58% | 2.7743% | 31.4 | 43.4 |

| 40 | 1.89 | 2.37 | 0.99% | 20.39% | 1.6587% | 31.4 | 42.7 |

| 45 | 2.02 | 2.53 | 1.67% | 31.43% | 1.6474% | 31.3 | 41.8 |

| 50 | 2.18 | 2.73 | 3.11% | 39.76% | 1.5481% | 31.2 | 40.6 |

| 55 | 2.39 | 2.94 | 6.44% | 56.13% | 1.3008% | 30.8 | 39.1 |

| 60 | 2.65 | 3.17 | 10.55% | 70.01% | 0.9094% | 30.0 | 37.2 |

| 65 | 2.98 | 3.39 | 14.60% | 75.35% | 0.5352% | 28.9 | 34.9 |

| 70 | 3.37 | 3.58 | 21.27% | 80.70% | 0.1167% | 27.3 | 32.1 |

| 75 | 3.77 | 3.69 | 21.90% | 73.42% | −0.0904% | 25.3 | 29.0 |

| 80 | 4.10 | 3.71 | 22.78% | 65.42% | −0.2288% | 22.7 | 25.5 |

| 85 | 4.25 | 3.59 | 20.45% | 54.70% | −0.3138% | 19.8 | 21.8 |

| 90 | 4.15 | 3.35 | 17.37% | 40.96% | −0.3586% | 16.6 | 17.9 |

| 95 | 3.83 | 3.02 | 12.57% | 26.03% | −0.3786% | 13.4 | 14.0 |

| 100 | 3.37 | 2.63 | 9.12% | 15.46% | −0.3798% | 10.4 | 10.3 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

De La Peña, J.I.; Fernández-Ramos, M.C.; Garayeta, A. Cost-Free LTC Model Incorporated into Private Pension Schemes. Int. J. Environ. Res. Public Health 2021, 18, 2268. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph18052268

De La Peña JI, Fernández-Ramos MC, Garayeta A. Cost-Free LTC Model Incorporated into Private Pension Schemes. International Journal of Environmental Research and Public Health. 2021; 18(5):2268. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph18052268

Chicago/Turabian StyleDe La Peña, J. Iñaki, M. Cristina Fernández-Ramos, and Asier Garayeta. 2021. "Cost-Free LTC Model Incorporated into Private Pension Schemes" International Journal of Environmental Research and Public Health 18, no. 5: 2268. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph18052268