Evaluation of Benefits and Health Co-Benefits of GHG Reduction for Taiwan’s Industrial Sector under a Carbon Charge in 2023–2030

Abstract

:1. Introduction

2. Methodology

2.1. The Need to Account for the Health Co-Benefits of GHG Emission Reductions

2.2. Methodology Outline for the Monetary Benefits from GHG Reductions and Monetary Health Co-Benefits from Air Pollution Reduction

2.3. Model Construction for the Emission Reductions of GHGs and Air Pollutants

2.4. Monetary Aspects of Emission Reductions of GHGs and of Air Pollution

2.4.1. Evaluating the Monetary Benefits of GHG Reduction

2.4.2. Evaluation of the Monetary Health Co-Benefits of Air Pollution Reductions

The Relationship between Emissions of Air Pollution and Their Concentrations

Estimations for Contracting Certain Diseases and Emission Concentrations

Monetize the Damage from Contracting a Particular Health Incidence

3. Scenario Assumptions and Simulation Results

3.1. Principle of Carbon Charge and Emission Allocations among Manufacturers in the Industrial Sector in Taiwan

3.2. Scenarios Designed for Benefit Simulations of Emission Reductions

3.2.1. Results for Scenario 1: The Carbon Charge on Scope 1 and Scope 2 Emissions for 25 Manufacturers in the Industrial Sector

3.2.2. Results for Scenario 2: The Carbon Charge on Scope 1 Emissions for 25 Manufacturers in the Industrial Sector

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- United Nations Climate Change. Climate Action and Support Trends: Based on National Reports Submitted to the UNFCCC Secretariat under the Current Reporting Framework; United Nations Climate Change Secretariat: Bonn, Germany, 2019; Available online: https://unfccc.int/sites/default/files/resource/Climate_Action_Support_Trends_2019.pdf (accessed on 30 May 2022).

- Ecochain. Measuring Sustainability: Scope 1, 2 and 3 Emissions: Overview to Direct and Indirect Emissions; Ecochain: Amsterdam, The Netherlands, 2020; Available online: https://ecochain.com/knowledge/scope-1-2-and-3-emissions-overview-to-direct-and-indirect-emissions/ (accessed on 24 April 2022).

- Bureau of Energy, Ministry of Economic Affairs. Statistics and Analyses of Carbon Dioxin of Fuel Combustion in 2020; Bureau of Economic Affair: Taipei, Taiwan, 2021. Available online: https://www.moeaboe.gov.tw/ECW/populace/content/SubMenu.aspx?menu_id=114&sub_menu_id=5576 (accessed on 25 May 2022).

- Law Library of Congress and Global Legal Research Directorate. Net Zero Emissions Legislation around the World; Library of Congress: Washington, DC, USA, 2021. Available online: https://tile.loc.gov/storage-services/service/ll/llglrd/2021687417/2021687417.pdf (accessed on 22 May 2022).

- Environmental Protection Administration. Amendment of Greenhouse Gas Reduction and Management Act to Climate Change Response Act; Environmental Protection Administration: Taipei, Taiwan, 2022. Available online: https://enews.epa.gov.tw/DisplayFile.aspx?FileID=957815CAA7D45909 (accessed on 20 June 2022).

- Ionescu, L. Climate policies, carbon pricing, and pollution tax: Do carbon taxes really lead to a reduction in emissions? Geopolit. Hist. Int. Relat. 2019, 11, 92–97. [Google Scholar]

- Wang, M.; Li, Y.; Li, M.; Shi, W.; Quan, S. Will carbon tax affect the strategy and performance of low-carbon technology sharing between enterprises? J. Clean. Prod. 2019, 210, 724–737. [Google Scholar] [CrossRef]

- Zhang, K.; Xue, M.-M.; Feng, K.; Liang, Q.-M. The economic effects of carbon tax on China’s provinces. J. Policy Model. 2019, 41, 784–802. [Google Scholar] [CrossRef]

- Intergovernmental Panel on Climate Change. Summary for Policymakers, Climate Change 2001: Mitigation, 2001; Intergovernmental Panel on Climate Change: Geneva, Switzerland, 2001; Available online: https://www.ipcc.ch/site/assets/uploads/2018/03/WGIII_TAR_full_report.pdf (accessed on 10 May 2022).

- Intergovernmental Panel on Climate Change. Annex I: Glossary. In Climate Change and Land: An IPCC Special Report on Climate Change, Desertification, Land Degradation, Sustainable Land Management, Food Security, and Greenhouse Gas Fluxes in Terrestrial Ecosystems; Shukla, P.R., Skea, J., Calvo Buendia, E., Masson-Delmotte, V., Pörtner, H.-O., Roberts, D.C., Zhai, P., Slade, R., Connors, S., van Diemen, R., Eds.; Intergovernmental Panel on Climate Change: Geneva, Switzerland, 2019; pp. 803–829. Available online: https://www.ipcc.ch/site/assets/uploads/sites/4/2019/11/11_Annex-I-Glossary.pdf (accessed on 27 May 2022).

- Wu, P.-I. Review of carbon taxation for Taiwan: Co-benefits led by the perceptible air pollution reduction. Taiwan Int. Stud. Q. 2020, 16, 1–78. [Google Scholar]

- Mayrhofer, J.P.; Gupta, J. The science and politics of co-benefits in climate policy. Environ. Sci. Policy. 2016, 57, 22–30. [Google Scholar] [CrossRef]

- Gao, J.; Kovats, S.; Vardoulakis, S.; Wilkinson, P.; Woodward, A.; Li, J.; Gu, S.; Liu, X.; Wu, H.; Wang, J.; et al. Public health co-benefits of greenhouse gas emissions reduction: A systematic review. Sci. Total Environ. 2018, 627, 388–407. [Google Scholar] [CrossRef]

- Karlsson, M.; Alfredsson, E.; Westling, N. Climate policy co-benefits: A review. Clim. Policy 2020, 20, 773–778. [Google Scholar] [CrossRef] [Green Version]

- Yang, X.; Teng, F.; Wang, G. Incorporating environmental co-benefits into climate policies: A regional study of the cement industry in China. Appl. Energy 2013, 112, 1446–1453. [Google Scholar] [CrossRef]

- Burtraw, D.; Krupnick, A.; Palmer, K.; Paul, A.; Toman, M.; Bloyd, C. Ancillary benefits of reduced air pollution in the US from moderate greenhouse gas mitigation policies in the electricity sector. J. Environ. Econ. Manag. 2003, 45, 650–673. [Google Scholar] [CrossRef]

- Farzaneh, H.; Dashti, M.; Zusman, E.; Lee, S.; Dagvadorj, D.; Nie, Z. Assessing the environmental-health-economic co-benefits from solar electricity and thermal heating in Ulaanbaatar, Mongolia. Int. J. Environ. Res. Public Health 2022, 19, 6931. [Google Scholar] [CrossRef]

- Levy, J.I.; Woo, M.K.; Penn, S.L.; Omary, M.; Tambouret, Y.; Kim, C.S.; Arunachalam, S. Carbon reductions and health co-benefits from US residential energy efficiency measures. Environ. Res. Lett. 2016, 11, 034017. [Google Scholar] [CrossRef]

- Balbus, J.M.; Greenblatt, J.B.; Chari, R.; Millstein, D.; Ebi, K.L. A wedge-based approach to estimating health co-benefits of climate change mitigation activities in the United States. Clim. Change 2014, 127, 199–210. [Google Scholar] [CrossRef]

- Liou, J.; Wu, P. Monetary health co-benefits and GHG emissions reduction benefits: Contribution from private on-the-road transport. Int. J. Environ. Res. Public Health. 2021, 18, 5537. [Google Scholar] [CrossRef] [PubMed]

- Joh, S.; Nam, Y.-M.; Shim, S.G.; Sung, J.; Shin, Y. Empirical study of environmental ancillary benefits due to greenhouse gas mitigation in Korea. Int. J. Sustain. Dev. 2003, 6, 311–327. [Google Scholar] [CrossRef]

- Crawford-Brown, D.; Barker, T.; Anger, A.; Dessens, O. Ozone and PM related health co-benefits of climate change policies in Mexico. Environ. Sci. Policy 2012, 17, 33–40. [Google Scholar] [CrossRef]

- Thompson, T.M.; Rausch, S.; Saari, R.K.; Selin, N.E. Air quality co-benefits of subnational carbon policies. J. Air Waste Manag. Assoc. 2016, 66, 988–1002. [Google Scholar] [CrossRef] [Green Version]

- Wang, T.; Jiang, Z.; Zhao, B.; Gu, Y.; Liou, K.; Kalandiyur, N.; Zhang, D.; Zhu, Y. Health co-benefits of achieving sustainable net-zero greenhouse gas emissions in California. Nat. Sustain. 2020, 3, 597–605. [Google Scholar] [CrossRef]

- Krook Riekkola, A.; Ahlgren, E.O.; Söderholm, P. Ancillary benefits of climate policy in a small open economy: The case of Sweden. Energy Policy 2011, 39, 4985–4998. [Google Scholar] [CrossRef]

- Vennemo, H.; Aunan, K.; Jinghua, F.; Holtedahl, P.; Tao, H.; Seip, H.M. Domestic environmental benefits of China’s energy related CDM potential. Clim. Change 2006, 75, 215–239. [Google Scholar] [CrossRef]

- Ščasný, M.; Massetti, E.; Melichar, J.; Carrara, S. Quantifying the ancillary benefits of the representative concentration pathways on air quality in Europe. Environ. Res. Econ. 2015, 62, 383–415. [Google Scholar] [CrossRef] [Green Version]

- Van Vuuren, D.P.; Cofala, J.; Eerens, H.E.; Oostenrijk, R.; Heyes, C.; Klimont, Z.; den Elzen, M.G.J.; Amann, M. Exploring the ancillary benefits of the Kyoto Protocol for air pollution in Europe. Energy Policy 2006, 34, 444–460. [Google Scholar] [CrossRef] [Green Version]

- West, J.J.; Smith, S.J.; Silva, R.A.; Naik, V.; Zhang, Y.; Adelman, Z.; Fry, M.M.; Anenberg, S.; Horowitz, L.W.; Lamarque, J.-F. Co-benefits of mitigating global greenhouse gas emissions for future air quality and human health. Nat. Clim. Change 2013, 3, 885–889. [Google Scholar] [CrossRef] [PubMed]

- Banacloche, S.; Lechon, Y.; Rodríguez-Martínez, A. Carbon capture penetration in Mexico’s 2050 horizon: A sustainability assessment of Mexican CCS policy. Int. J. Greenh. Gas Cont. 2022, 115, 103603. [Google Scholar] [CrossRef]

- Gómez-Sanabria, A.; Kiesewetter, G.; Klimont, Z.; Schoepp, W.; Haberl, H. Potential for future reductions of global GHG and air pollutants from circular waste management systems. Nat. Commun. 2022, 13, 106. [Google Scholar] [CrossRef] [PubMed]

- Monjardino, J.; Dias, L.; Fortes, P.; Tente, H.; Ferreira, F.; Seixas, J. Carbon neutrality pathways effects on air pollutant emis sions: The Portuguese case. Atmosphere 2021, 12, 324. [Google Scholar] [CrossRef]

- Zhu, S.; Kinnon, M.M.; Soukup, J.; Paradise, A.; Dabdub, D.; Samuelsen, S. Assessment of the greenhouse gas, Episodic air quality and public health benefits of fuel cell electrification of a major port complex. Atmos. Environ. 2022, 275, 118996. [Google Scholar] [CrossRef]

- Salimifard, P.; Buonocore, J.J.; Konschnik, K.; Azimi, P.; Vanry, M.; Cedeno Laurent, J.G.; Hernández, D.; Allen, J.G. Climate policy impacts on building energy use, emissions, and health: New York City local law 97. Energy 2021, 238, 121879. [Google Scholar] [CrossRef]

- Zhu, S.; Mac Kinnon, M.; Carlos-Carlos, A.; Davis, S.J.; Samuelsen, S. Decarbonization will lead to more equitable air quality in California. Nat. Commun. 2022, 13, 5738. [Google Scholar] [CrossRef]

- Cleghorn, C.; Mulder, I.; Macmillan, A.; Mizdrak, A.; Drew, J.; Nghiem, N.; Blakely, T.; Ni Mhurchu, C. Can a greenhouse gas emissions tax on food also be healthy and equitable? A systemised review and modelling study from Aotearoa New Zealand. Int. J. Environ. Res. Public Health 2022, 19, 4421. [Google Scholar] [CrossRef]

- Chatterjee, S.; Rafa, N.; Nandy, A. Welfare, development, and cost-efficiency: A global synthesis on incentivizing energy efficiency measures through co-benefits. Energy Res. Soc. Sci. 2022, 89, 102666. [Google Scholar] [CrossRef]

- Environmental Protection Administration. The Targets for Greenhouse Gases Control for the First Period; Environmental Protection Administration: Taipei, Taiwan, 2018. Available online: https://ghgrule.epa.gov.tw/admin/resource/files/%E7%AC%AC%E4%B8%80%E6%9C%9F%E6%BA%AB%E5%AE%A4%E6%B0%A3%E9%AB%94%E9%9A%8E%E6%AE%B5%E7%9B%AE%E6%A8%99.pdf (accessed on 20 June 2022).

- Environmental Protection Administration. The Targets for Greenhouse Gases Control for the Second Period; Environmental Protection Administration: Taipei, Taiwan, 2021. Available online: https://ghgrule.epa.gov.tw/admin/resource/files/%E7%AC%AC%E4%BA%8C%E6%9C%9F%E6%BA%AB%E5%AE%A4%E6%B0%A3%E9%AB%94%E9%9A%8E%E6%AE%B5%E7%9B%AE%E6%A8%99.pdf (accessed on 20 June 2022).

- Parry, I.; Veung, C. How much carbon pricing in countries’ own interests? The critical role of co-benefits. Clim. Change Econ. 2015, 6, 1550019. [Google Scholar] [CrossRef] [Green Version]

- Carnegie Mellon University. EIO-LCA: Free, Fast, Easy Life Cycle Assessment. 2018. Available online: http://www.eiolca.net/ (accessed on 5 June 2022).

- Reimann, K.; Finkbeiner, M.; Horvath, A.; Matsuno, Y. Evaluation of Environmental Life Cycle Approaches for Policy and Decision Making Support in Micro and Macro Level Applications; European Commission Joint Research Centre Institute for Environment and Sustainability: Ispra, Italy, 2010; Available online: http://www.avnir.org/documentation/e_book/Evaluation-environmental-life-cycle-approaches-micro-macro-level-applications.pdf (accessed on 2 May 2022).

- United States Environmental Protection Agency, Office of Air Protection Radiation, Office of Air Quality Planning and Standards. Technical Support Document Estimating the Benefit per Ton of Reducing PM2.5 Precursors from 17 Sectors; United States Environmental Protection Agency: Washington, DC, USA, 2018. Available online: https://www.epa.gov/sites/default/files/2018-02/documents/sourceapportionmentbpttsd_2018.pdf (accessed on 10 May 2022).

- Bjorn, A.; Declercq-Lopez, L.; Spatari, S.; MacLean, H.L. Decision support for sustainable development using a Canadian economic input–output life cycle assessment model. Can. J. Civil. Eng. 2005, 32, 16–29. [Google Scholar] [CrossRef]

- Ghani, N.A.; Egilmez, G.; Kucukvar, M.; Bhutta, M.K.S. From green buildings to green supply chains an integrated input-output life cycle assessment and optimization framework for carbon footprint reduction policy making. Manag. Environ. Qual. 2017, 28, 532–548. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Q.; Li, T.; Liu, Z.; Zhang, H.; Ren, K. Life cycle assessment of an engine with input-output based hybrid analysis method. J. Clean. Prod. 2014, 78, 131–138. [Google Scholar] [CrossRef]

- Meglin, R.; Kytzia, S.; Habert, G. Regional circular economy of building materials: Environmental and economic assessment combining material flow analysis, input-output analyses, and life cycle assessment. J. Ind. Ecol. 2022, 26, 562–576. [Google Scholar] [CrossRef]

- Nishioka, Y.; Levy, J.; Norris, G.A.; Bennett, D.; Spengler, J. A risk-based approach to health impact assessment for input-output analysis, Part 1: Methodology (7 pp). Int. J. Life Cycle Assess. 2005, 10, 193–199. [Google Scholar] [CrossRef]

- Norman, J.; Charpentier, A.D.; MacLean, H.L. Economic input−output life-cycle assessment of trade between Canada and the United States. Environ. Sci. Technol. 2007, 41, 1523–1532. [Google Scholar] [CrossRef] [Green Version]

- Pranav, S.; Lahoti, M.; Shan, X.; Yang, E.-H.; Muthukumar, G. Economic input-output LCA of precast corundum-blended ECC overlay pavement. Resour. Conserv. Recycl. 2022, 184, 106385. [Google Scholar] [CrossRef]

- Shi, X.; Mukhopadhyay, A.; Zollinger, D.; Grasley, Z. Economic Input-output life cycle assessment of concrete pavement containing recycled concrete aggregate. J. Clean. Prod. 2019, 225, 414–425. [Google Scholar] [CrossRef]

- Yoshikawa, N.; Matsuda, T.; Amano, K. Life cycle environmental and economic impact of a food waste recycling-farming system: A case study of organic vegetable farming in Japan. Inter. J. Life Cycle Assess. 2021, 26, 963–976. [Google Scholar] [CrossRef]

- Llop, M. Economic impact of alternative water policy scenarios in the Spanish production system: An input-output analysis. Ecol. Econ. 2008, 68, 288–294. [Google Scholar] [CrossRef]

- Gemechu, E.D.; Butnar, I.; Llop, M.; Castells, F. Economic and environmental effects of CO2 taxation: An input-output analysis for Spain. J. Environ. Plan. Man. 2014, 57, 751–768. [Google Scholar] [CrossRef]

- Directorate General of Budget, Accounting and Statistics. Annual IO Tables; National Statistics: Taipei, Taiwan, 2019. Available online: https://eng.stat.gov.tw/ct.asp?xItem=29540&ctNode=1650&mp=5 (accessed on 10 July 2022).

- Environmental Protection Administration. Republic of China National Greenhouse Gas Inventory Report; Environmental Protection Administration: Taipei, Taiwan, 2022; Available online: https://unfccc.saveoursky.org.tw/nir/2021nir/uploads/00_abstract_en.pdf (accessed on 27 May 2022).

- Directorate General of Budget, Accounting and Statistics. Green GDP Reports; National Statistics: Taipei, Taiwan, 2021. Available online: https://ebook.dgbas.gov.tw/public/Data/212372827CA7FAUC2.pdf (accessed on 27 May 2022).

- Environmental Protection Administration. Taiwan Emission Data Systemt; Environmental Protection Administration: Taipei, Taiwan, 2022. Available online: https://air.epa.gov.tw/EnvTopics/AirQuality_6.aspx (accessed on 26 May 2022).

- Bureau of Energy, Ministry of Economic Affairs. Taiwan Energy Statistics Year Book; Bureau of Energy, Ministry of Economic Affairs: Taipei, Taiwan, 2022; Available online: https://www.esist.org.tw/publication/page01_detail?Id=30427c7ed1a1 (accessed on 27 May 2022).

- Directorate General of Budget, Accounting and Statistics. Standard Industrial Classification System of the Republic of China (Rev.9, 2011); National Statistics: Taipei, Taiwan, 2011. Available online: https://www.dgbas.gov.tw/public/Attachment/17514272871.xls (accessed on 24 May 2022).

- Environmental Defense Fund. The True Cost of Carbon Pollution: How the Social Cost of Carbon Improves Policies to Address Climate Change; Environmental Defense Fund: Washington, DC, USA, 2022; Available online: https://www.edf.org/true-cost-carbon-pollution (accessed on 25 May 2022).

- Greenstone, M.; Kopits, E.; Wolverton, A. Developing a social cost of carbon for US regulatory analysis: A methodology and interpretation. Rev. Environ. Econ. Policy 2013, 7, 23–46. [Google Scholar] [CrossRef] [Green Version]

- Pizer, W.; Adler, M.; Aldy, J.; Anthoff, D.; Cropper, M.; Gillingham, K.; Greenstone, M.; Murray, B.; Newell, R.; Richels, R.; et al. Using and improving the social cost of carbon. Science 2014, 346, 1189–1190. [Google Scholar] [CrossRef] [PubMed]

- Kotchen, M.J. Which social cost of carbon? A theoretical perspective. J. Assoc. Environ. Res. Econ. 2018, 5, 673–694. [Google Scholar]

- Interagency Working Group on Social Cost of Carbon, United States Government. Technical Support Document: Social Cost of Carbon for Regulatory Impact Analysis—Under Executive Order 12866; United States Environmental Protection Agency: Washington, DC, USA, 2010. Available online: https://www.epa.gov/sites/production/files/2016-12/documents/scc_tsd_2010.pdf (accessed on 24 May 2022).

- Interagency Working Group on Social Cost of Greenhouse Gases, United States Government. Technical Support Document: Technical Update of the Social Cost of Carbon for Regulatory Impact Analysis—Under Executive order 12866; United States Environmental Protection Agency: Washington, DC, USA, 2016. Available online: https://19january2017snapshot.epa.gov/sites/production/files/2016-12/documents/sc_CO2_tsd_august_2016.pdf (accessed on 10 May 2022).

- Interagency Working Group on Social Cost of Greenhouse Gases, United States Government. Technical Support Document: Social Cost of Carbon, Methane, and Nitrous Oxide Interim Estimates under Executive Order 13990; United States Environmental Protection Agency: Washington, DC, USA, 2021. Available online: https://www.whitehouse.gov/wp-content/uploads/2021/02/TechnicalSupportDocument_SocialCostofCarbonMethaneNitrousOxide.pdf (accessed on 10 May 2022).

- Nordhaus, W.D.; Cowles Foundation for Research in Economics at Yale University. In The “DICE” Model: Background and Structure of a Dynamic Integrated Climate-Economy Model of Global Warming. No 1009, Cowles Foundation Discussion Papers. 1992. Available online: https://cowles.yale.edu/sites/default/files/files/pub/d10/d1009.pdf (accessed on 4 June 2022).

- Hope, C.; Anderson, J.; Wenman, P. Policy analysis of the greenhouse effect: An application of the PAGE model. Energy Policy 1993, 21, 327–338. [Google Scholar] [CrossRef]

- Tol, R.S.J. On the optimal control of carbon dioxide emissions: An application of FUND. Environ. Model. Assess. 1997, 2, 151–163. [Google Scholar] [CrossRef]

- Gayer, T.; Viscusi, W.K. Determining the proper scope of climate change policy benefits in U.S. regulatory analyses: Domestic versus global approaches. Rev. Environ. Econ. Policy 2016, 10, 245–263. [Google Scholar] [CrossRef]

- Moyer, E.J.; Woolley, M.D.; Matteson, N.J.; Glotter, M.J.; Weisbach, D.A. Climate impacts on economic growth as drivers of uncertainty in the social cost of carbon. J. Legal Stud. 2014, 43, 401–425. [Google Scholar] [CrossRef] [Green Version]

- Pindillia, E.; Sleeterb, R.; Hogan, D. Estimating the societal benefits of carbon dioxide sequestration through peatland restoration. Ecol. Econ. 2018, 154, 145–155. [Google Scholar] [CrossRef]

- Chang, K.-H.; Lin, C.-H.; Lin, W.-Y.; Lin, P.-H.; Lai, H.-C.; Chen, L.-Y.; Chen, J.-H.; Liu, T.-H. Establish Domestic AERMOD Model and Air Quality Model Validation System; Environmental Protection Administration: Taipei, Taiwan, 2019; Available online: https://drive.google.com/file/d/1Iii43gM1Noe-0BYtgmix4FyotIy0f6VJ/view (accessed on 10 May 2022).

- Liou, J.L. Effect of income heterogeneity on valuation of mortality risk in Taiwan: An application of unconditional quantile regression method. Int. J. Environ. Res. Public Health 2019, 16, 1620. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Krewski, D.; Jerrett, M.; Burnett, R.T.; Ma, R.; Hughes, E.; Shi, Y.; Turner, M.C.; Pope III, C.A.; Thurston, G.; Calle, E.E.; et al. Extended follow-up and spatial analysis of the American cancer society study linking particulate air pollution and mortality. Res. Rep. Health Eff. Inst. 2009, 149, 5–114. [Google Scholar]

- Lepeule, J.; Laden, F.; Dockery, D.; Schwartz, J. Chronic exposure to fine particles and mortality: An extended follow-up of the Harvard six cities study from 1974 to 2009. Environ. Health Persp. 2012, 120, 965–970. [Google Scholar] [CrossRef] [PubMed]

- National Development Council. Population Projections for the Taiwan: 2020~2070; National Development Council: Taipei, Taiwan, 2021. Available online: https://pop-proj.ndc.gov.tw/dataSearch.aspx?r=2&uid=2104&pid=59 (accessed on 10 July 2022).

- Directorate General of Budget, Accounting and Statistics. Salary and Productivity Survey Database; National Statistics: Taipei, Taiwan, 2020. Available online: https://earnings.dgbas.gov.tw/query_payroll_C.aspx?mp=4 (accessed on 25 May 2022).

- Directorate General of Budget, Accounting and Statistics. Price Index Database; National Statistics: Taipei, Taiwan, 2020. Available online: http://statdb.dgbas.gov.tw/pxweb/Dialog/price.asp?mp=4 (accessed on 30 May 2022).

- Customs Administration, Ministry of Finance. Statistics Database Query: Trade Statistics; Customs Administration, Ministry of Finance: Taipei, Taiwan, 2022. Available online: https://portal.sw.nat.gov.tw/APGA/GA35E (accessed on 10 June 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Year | Discount Rate | ||

|---|---|---|---|

| Average SCC under a 5% Discount Rate | Average SCC under a 3% Discount Rate | Average SCC under a 2.5% Discount Rate | |

| 2020 | 14 | 51 | 76 |

| 2025 | 17 | 56 | 83 |

| 2030 | 19 | 62 | 89 |

| 2035 | 22 | 67 | 96 |

| 2040 | 25 | 73 | 103 |

| 2045 | 28 | 79 | 110 |

| 2050 | 32 | 85 | 116 |

| Pollutant | Point Source | Line Source 2 | Area Source |

|---|---|---|---|

| PM2.5 | 0.00009866 | 0.00013522 | 0.00007858 |

| SOx | 0.00001413 | -- | 0.00002752 |

| NOx | 0.00000500 | 0.00000629 | 0.00004108 |

| Year | Projected Population (Persons) |

|---|---|

| 2023 | 23,487,421 |

| 2024 | 23,471,823 |

| 2025 | 23,436,816 |

| 2026 | 23,402,062 |

| 2027 | 23,360,315 |

| 2028 | 23,313,038 |

| 2029 | 23,260,030 |

| 2030 | 23,201,540 |

| Parameter | Value | Definition |

|---|---|---|

| 11.93 | The VSL computed in the study by [75] in 2019; unit: million US$ | |

| 0.2476 | The earnings elasticity estimated for monthly earnings between US$ 1333.3 and US$ 1600.01 | |

| 1333.3 | Average monthly earnings in US$ in 2014 | |

| 1600.01 | Average monthly earnings in US$ in 2020 | |

| 98.93 | The consumer price indices d for 2014 and 2020, with A base year of 2015; i.e., | |

| 102.55 |

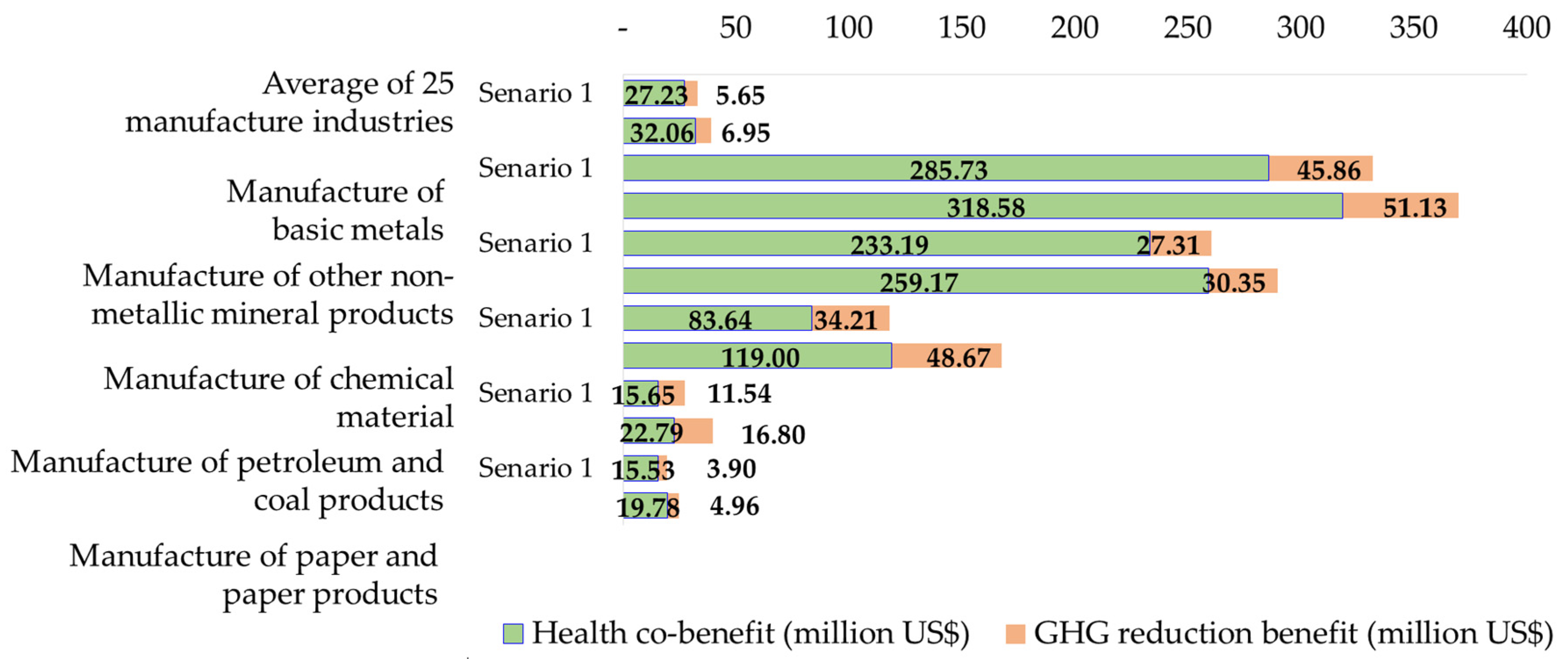

| Manufacturer | Health Co-Benefits (Million US$) | Share of Health Co-Benefit of Each Manufacturer (%) | GHGs Reduction Benefits (Million US$) | Share of GHG Reduction Benefits of Each Manufacturer (%) | Total Benefits (Million US$) | Share of Total Benefits of Each Manufacturer (%) |

|---|---|---|---|---|---|---|

| Manufacturers of Basic Metals | 285.73 | 41.98 | 45.86 | 32.48 | 331.59 | 40.34 |

| Manufacturers of Other Non-metallic Mineral Products | 233.19 | 34.26 | 27.31 | 19.34 | 260.50 | 31.69 |

| Manufacturers of Chemical Materials | 83.64 | 12.29 | 34.21 | 24.23 | 117.85 | 14.34 |

| Manufacturers of Petroleum and Coal Products | 15.65 | 2.30 | 11.54 | 8.17 | 27.18 | 3.31 |

| Manufacturers of Paper and Paper Products | 15.53 | 2.28 | 3.90 | 2.76 | 19.43 | 2.36 |

| Manufacturers of Chemical Products | 13.56 | 1.99 | 1.56 | 1.10 | 15.11 | 1.84 |

| Manufacturers of Electronic Parts and Components | 3.16 | 0.46 | 8.06 | 5.71 | 11.22 | 1.37 |

| Manufacturers of Textiles | 8.47 | 1.24 | 2.13 | 1.51 | 10.60 | 1.29 |

| Manufacturers of Fabricated Metal Products | 7.20 | 1.06 | 2.84 | 2.01 | 10.05 | 1.22 |

| Manufacture of Plastics Products | 4.31 | 0.63 | 1.51 | 1.07 | 5.82 | 0.71 |

| Manufacturers of Food Products | 4.39 | 0.65 | 0.43 | 0.30 | 4.82 | 0.59 |

| Other Manufacturing | 1.89 | 0.28 | 0.50 | 0.35 | 2.39 | 0.29 |

| Manufacturers of Rubber Products | 1.44 | 0.21 | 0.38 | 0.27 | 1.82 | 0.22 |

| Manufacturers of Electrical Equipment | 0.83 | 0.12 | 0.14 | 0.10 | 0.97 | 0.12 |

| Manufacturers of Wood and of Products of Wood and Bamboo | 0.74 | 0.11 | 0.07 | 0.05 | 0.81 | 0.10 |

| Printing and Reproduction of Recorded Media | 0.25 | 0.04 | 0.19 | 0.13 | 0.44 | 0.05 |

| Manufacturers of Machinery and Equipment | 0.24 | 0.03 | 0.18 | 0.13 | 0.42 | 0.05 |

| Manufacturers of Motor Vehicles and Parts | 0.19 | 0.03 | 0.16 | 0.11 | 0.35 | 0.04 |

| Manufacturers of Other Transport Equipment and Parts | 0.09 | 0.01 | 0.06 | 0.04 | 0.15 | 0.02 |

| Manufacturers of Computers, Electronic and Optical Products | 0.01 | 0.00 | 0.09 | 0.07 | 0.10 | 0.01 |

| Manufacturers of Pharmaceuticals and Medicinal Chemical Products | 0.06 | 0.01 | 0.03 | 0.02 | 0.08 | 0.01 |

| Manufacturers of Leather, Fur and Related Products | 0.07 | 0.01 | 0.01 | 0.01 | 0.08 | 0.01 |

| Manufacturers of Beverages and Tobacco | 0.04 | 0.01 | 0.01 | 0.01 | 0.05 | 0.01 |

| Manufacturers of Furniture | 0.03 | 0.00 | 0.01 | 0.01 | 0.05 | 0.01 |

| Manufacturers of Wearing Apparel and Clothing Accessories | 0.00 | 0.00 | 0.01 | 0.01 | 0.01 | 0.00 |

| Total benefits of 25 manufacturers | 680.71 | 100.00 | 141.19 | 100.00 | 821.90 | 100.00 |

| Average for 25 manufacturers | 27.23 | 82.82 | 5.65 | 17.18 | 32.88 | 100.00 |

| Manufacturer category | Health Co-Benefits (Million US$) | Share of Health Co-Benefit of Each Manufacturer (%) | GHG Reduction Benefits (Million US$) | Share of GHG Reduction Benefits of Each Manufacturer (%) | Total Benefits (Million US$) | Share of Total Benefits of Each Manufacturer (%) |

|---|---|---|---|---|---|---|

| Manufacturers of Basic Metals | 318.58 | 39.75 | 51.13 | 29.44 | 369.71 | 37.91 |

| Manufacturers of Other Non-metallic Mineral Products | 259.17 | 32.34 | 30.35 | 17.47 | 289.52 | 29.69 |

| Manufacturers of Chemical Materials | 119.00 | 14.85 | 48.67 | 28.02 | 167.68 | 17.20 |

| Manufacturers of Petroleum and Coal Products | 22.79 | 2.84 | 16.80 | 9.67 | 39.60 | 4.06 |

| Manufacturers of Paper and Paper Products | 19.78 | 2.47 | 4.96 | 2.86 | 24.75 | 2.54 |

| Manufacturers of Chemical Products | 16.26 | 2.03 | 1.87 | 1.07 | 18.12 | 1.86 |

| Manufacturers of Textiles | 12.20 | 1.52 | 3.06 | 1.76 | 15.26 | 1.56 |

| Manufacturers of Fabricated Metal Products | 8.73 | 1.09 | 3.45 | 1.98 | 12.18 | 1.25 |

| Manufacturers of Electronic Parts and Components | 3.16 | 0.39 | 8.05 | 4.63 | 11.21 | 1.15 |

| Manufacturers of Food Products | 7.70 | 0.96 | 0.75 | 0.43 | 8.46 | 0.87 |

| Manufacturers of Plastics Products | 5.67 | 0.71 | 2.00 | 1.15 | 7.67 | 0.79 |

| Other Manufacturing | 3.06 | 0.38 | 0.81 | 0.47 | 3.87 | 0.40 |

| Manufacturers of Rubber Products | 1.88 | 0.23 | 0.50 | 0.29 | 2.38 | 0.24 |

| Manufacturers of Electrical Equipment | 1.10 | 0.14 | 0.18 | 0.10 | 1.28 | 0.13 |

| Manufacturers of Wood and of Products of Wood and Bamboo | 1.00 | 0.12 | 0.10 | 0.06 | 1.09 | 0.11 |

| Printing and Reproduction of Recorded Media | 0.36 | 0.04 | 0.27 | 0.15 | 0.62 | 0.06 |

| Manufacturers of Machinery and Equipment | 0.29 | 0.04 | 0.22 | 0.13 | 0.52 | 0.05 |

| Manufacturers of Motor Vehicles and Parts | 0.26 | 0.03 | 0.21 | 0.12 | 0.48 | 0.05 |

| Manufacturers of Other Transport Equipment and Parts | 0.12 | 0.01 | 0.08 | 0.05 | 0.20 | 0.02 |

| Manufacturers of Pharmaceuticals and Medicinal Chemical Products | 0.09 | 0.01 | 0.04 | 0.02 | 0.13 | 0.01 |

| Manufacturers of Computers, Electronic and Optical Products | 0.01 | 0.00 | 0.12 | 0.07 | 0.13 | 0.01 |

| Manufacturers of Leather, Fur and Related Products | 0.10 | 0.01 | 0.02 | 0.01 | 0.12 | 0.01 |

| Manufacturers of Beverages and Tobacco | 0.08 | 0.01 | 0.02 | 0.01 | 0.10 | 0.01 |

| Manufacturers of Furniture | 0.04 | 0.01 | 0.02 | 0.01 | 0.06 | 0.01 |

| Manufacturers of Wearing Apparel and Clothing Accessories | 0.00 | 0.00 | 0.02 | 0.01 | 0.02 | 0.00 |

| Total benefits of 25 manufacturers | 801.43 | 100.00 | 173.71 | 100.00 | 975.14 | 100.00 |

| Average for 25 manufacturers | 32.06 | 82.19 | 6.95 | 17.81 | 39.01 | 100.00 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, P.-I.; Liou, J.-L.; Huang, T.-K. Evaluation of Benefits and Health Co-Benefits of GHG Reduction for Taiwan’s Industrial Sector under a Carbon Charge in 2023–2030. Int. J. Environ. Res. Public Health 2022, 19, 15385. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph192215385

Wu P-I, Liou J-L, Huang T-K. Evaluation of Benefits and Health Co-Benefits of GHG Reduction for Taiwan’s Industrial Sector under a Carbon Charge in 2023–2030. International Journal of Environmental Research and Public Health. 2022; 19(22):15385. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph192215385

Chicago/Turabian StyleWu, Pei-Ing, Je-Liang Liou, and Ta-Ken Huang. 2022. "Evaluation of Benefits and Health Co-Benefits of GHG Reduction for Taiwan’s Industrial Sector under a Carbon Charge in 2023–2030" International Journal of Environmental Research and Public Health 19, no. 22: 15385. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph192215385