Effects of the 2008 Financial Crisis and COVID-19 Pandemic on the Dynamic Relationship between the Chinese and International Fossil Fuel Markets

Abstract

:1. Introduction

2. Previous Research

3. Materials and Methods

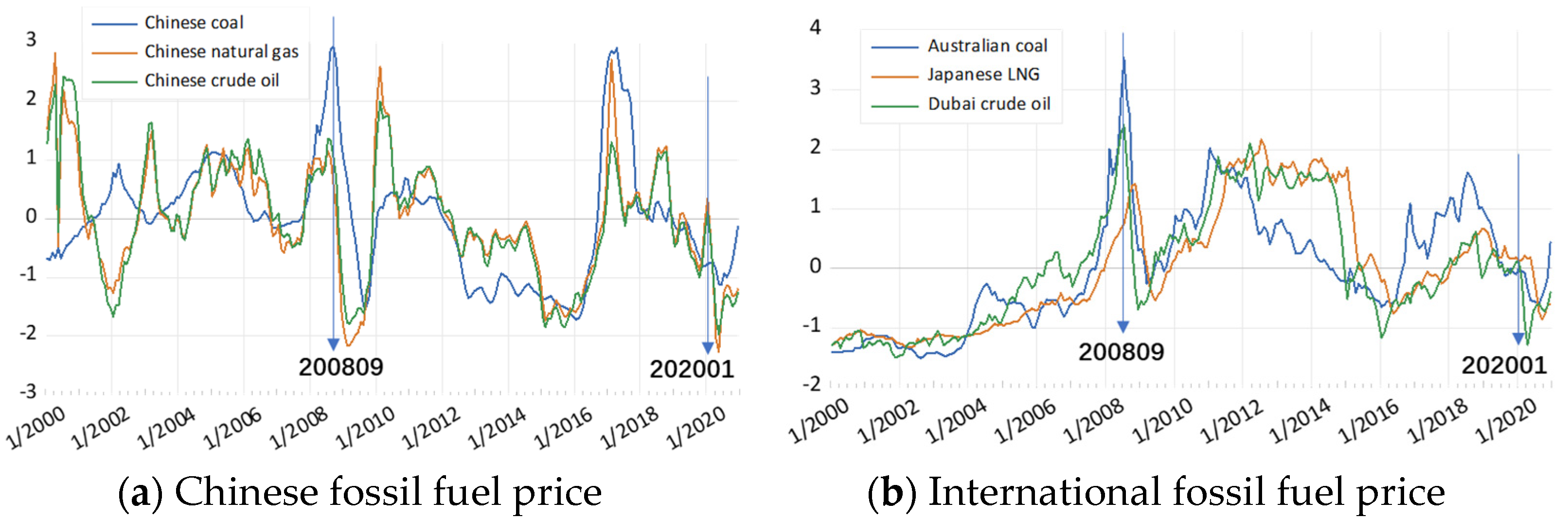

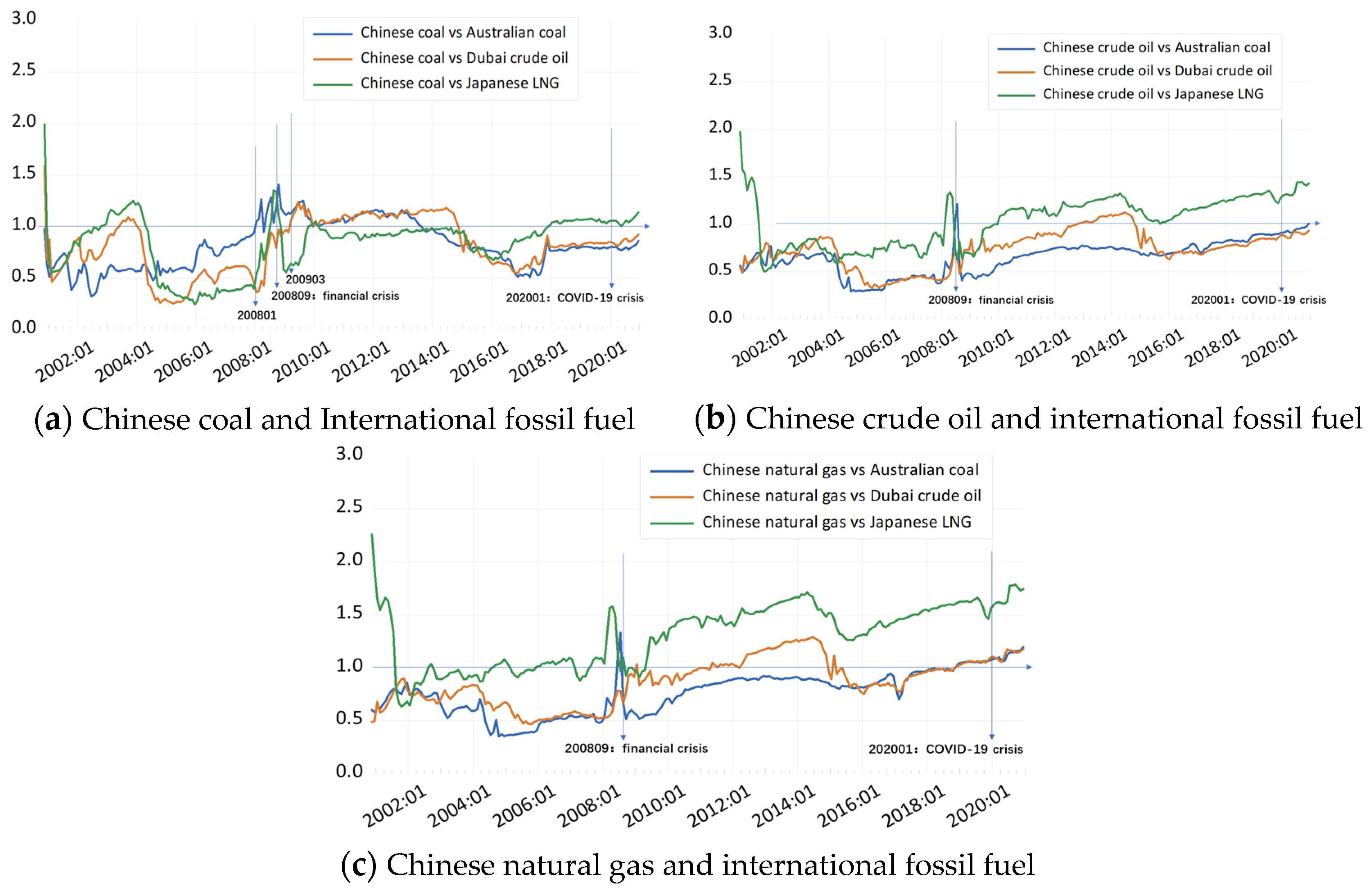

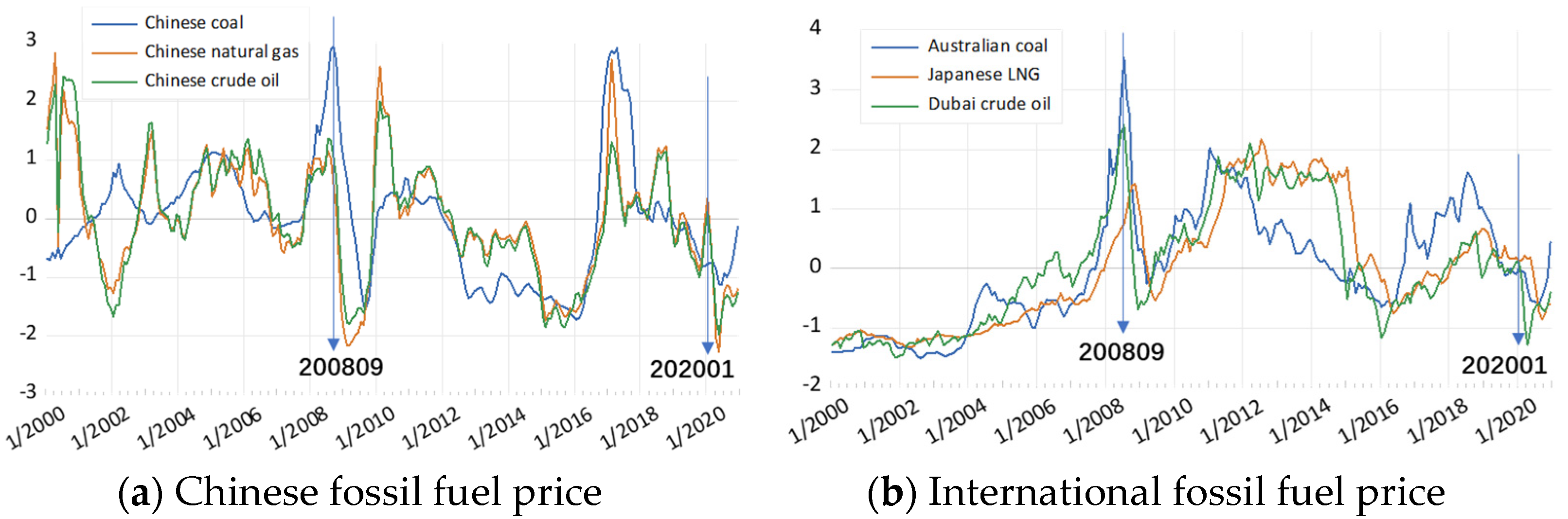

4. Results

4.1. Recursive Cointegration

4.2. Johansen Cointegration

4.3. Results of the Impact of Both Crises on the Chinese and International Fossil Fuel Market

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Adrian, Tobias, and Hyun Song Shin. 2010. The Changing Nature of Financial Intermediation and the Financial Crisis of 2007–2009. Federal Reserve Bank of New York Staff Reports 439: 1–34. [Google Scholar] [CrossRef] [Green Version]

- Akhtaruzzaman, Md, Sabri Boubaker, Mardy Chian, and Angel Zhong. 2020. COVID-19 and oil price risk exposure. Finance Research Letters 5: 2–7. [Google Scholar] [CrossRef]

- Aruga, Kentaka, and Sudha Kannan. 2020. Effects the 2008 financial crisis on the linkages among the oil, gold, and platinum markets. Cogent Economics & Finance 8: 1807684. [Google Scholar]

- Aruga, Kentaka, Md. Monirul Islam, and Arifa Jannat. 2020. Effects of COVID-19 on Indian Energy Consumption. Sustainability 12: 5616. [Google Scholar] [CrossRef]

- Bahmanyar, Alireza, Abouzar Estebsari, and Damien Ernst. 2020. The impact of different COVID-19 containment measures on electricity consumption in Europe. Energy Research & Social Science 68: 2–4. [Google Scholar]

- Bouri, Elie, Brian Lucey, Tareq Saeed, and Xuan Vinh Vo. 2021a. The realized volatility of commodity futures: Interconnectedness and determinants. International Review of Economics and Finance 73: 139–51. [Google Scholar] [CrossRef]

- Bouri, Elie, Xiaojie Lei, Naji Jalkh, Yahua Xu, and Hongwei Zhang. 2021b. Spillovers in higher moments and jumps across US stock and strategic commodity markets. Resources Policy 72: 102060. [Google Scholar] [CrossRef]

- CEINET Statistics Database. 2021. Available online: https://db.cei.cn/ (accessed on 12 January 2021).

- Chan, Hing Lin, and Kai-Yin Woo. 2016. An investigation into the dynamic relationship between international and China’s crude oil prices. Applied Economics 48: 2215–24. [Google Scholar] [CrossRef]

- Chang, Chia-Lin, Michael Mcaleer, and Yu-Ann Wang. 2020. Herding behavior in energy stock market during the Global Financial Crisis, SARS, and ongoing COVID-19. Renewable and Sustainable Energy Reviews 134: 1–15. [Google Scholar] [CrossRef]

- Energy. 2020. The impact of COVID-19 on Asian oil demand. Available online: https://www.energydigital.com/oil-and-gas/impact-covid-19-asian-oil-demand (accessed on 21 December 2020).

- Fama, Eugene F. 1991. Efficient capital markets: II. The Journal of Finance 46: 1575–617. [Google Scholar] [CrossRef]

- Hansen, Henrik, and Soren Johansen. 1993. Recursive Estimation in Cointegrated VAR Models. Unpublished Manuscript. Copenhagen: University of Copenhagen, pp. 1–20. ISSN 0902-6452. [Google Scholar]

- Hauser, Philipp, Carl-Philipp Anke, Julia B. Gutiérrez-López, Dominik Möst, Hendrik Scharf, David Schönheit, and Steffi Misconel. 2020. The Impact of the COVID-19 Crisis Energy Prices in Comparison to the 2008 Financial Crisis. IAEE Energy Forum Covid-19 Special Issue: 100–5. [Google Scholar]

- Höhler, Julia, and Alfons O. Lansink. 2021. Measuring the impact of COVID-19 on stock prices and profits in the food supply chain. Agribusiness 37: 171–86. [Google Scholar] [CrossRef] [PubMed]

- Hu, Haiqing, Wei Wei, and Chun-Ping Chang. 2020. The relationship between shale gas production and natural gas prices: An environmental investigation using structural breaks. Science of the Total Environment 713: 136545. [Google Scholar] [CrossRef] [PubMed]

- International Energy Agency (IEA). 2020. Global Energy Review 2020. Available online: https://www.iea.org/reports/global-energy-review-2020 (accessed on 20 December 2020).

- Jackson, James K., Martin A. Weiss, Andres B. Schwarzenberg, Revecca M. Nelson, Karen M. Sutter, and Michael D. Sutherland. 2021. Global Economic Effects of COVID-19. Congressional Research Service R 46270: 2–22. [Google Scholar]

- Jiang, Peng, Yee Van Fan, and Jiří Jaromír Klemeš. 2021. Impacts of COVID-19 on energy demand and consumption: Challenges, lessons and emerging opportunities. Applied Energy 285: 116441. [Google Scholar] [CrossRef]

- Johansen, Soren, and Katarina Juselius. 1990. Maximum likelihood estimation and inference on cointegration: With applications to the demand for money. Oxford Bulletin of Economics and Statistics 52: 169–210. [Google Scholar] [CrossRef]

- Li, Jianglong, Chunping Xie, and Houyin Long. 2019. The roles of inter-fuel substitution and inter-market contagion in driving energy prices: Evidences from China’s coal market. Energy Economics 84: 104525. [Google Scholar] [CrossRef]

- Lin, Boqiang, and Xiaoling Ouyang. 2014. A revisit of fossil-fuel subsidies in China: Challenges and opportunities for energy price reform. Energy Conversion and Management 82: 124–34. [Google Scholar] [CrossRef]

- Mollick, André V., and Tibebe A. Assefa. 2013. U.S. stock returns and oil prices: The tale from daily data and the 2008–2009 financial crisis. Energy Economics 36: 1–18. [Google Scholar] [CrossRef]

- Norouzi, Nima, Gerardo Zarazua de Rubens, Saeed Choupanpiesheh, and Peter Enevoldsen. 2020. When pandemics impact economies and climate change: Exploring the impacts of COVID-19 on oil and electricity demand in China. Energy Research & Social Science 68: 2–14. [Google Scholar]

- Nyga-Lukaszewska, Honorata, and Kentaka Aruga. 2020. Energy Prices and COVID-Immunity: The Case of Crude oil and Natural Gas Prices in the US and Japan. Energies 13: 6300. [Google Scholar] [CrossRef]

- Shahzad, Syed Jawad Hussain, Muhammad Abubakr Naeem, Zhe Peng, and Elie Bouri. 2021. Asymmetric volatility spillover among Chinese sectors during COVID-19. International Review of Financial Analysis 75: 101754. [Google Scholar] [CrossRef]

- SIPA. 2020. COVID-19 Pandemic’s Impacts on China’s Energy Sector: A Preliminary Analysis. Available online: https://www.energypolicy.columbia.edu/research/commentary/covid-19-pandemic-s-impacts-china-s-energy-sector-preliminary-analysis (accessed on 25 December 2020).

- Spatt, Chester S. 2020. A Tale of Two Crises: The 2008 Mortgage Meltdown and the 2020 COVID-19 Crisis. Review of Asset Pricing Studies 10: 760–90. [Google Scholar] [CrossRef]

- Tang, Chaofeng, and Kentaka Aruga. 2020. A study on the Pass-Through Rate of the Exchange Rate on the Liquid Natural Gas (LNG) Import Price in China. International Journal of Financial Studies 8: 70. [Google Scholar] [CrossRef]

- Turak, Natasha. 2020. Oil Nose-Dives as Saudi Arabia and Russia Set Off ‘Scorched Earth’ Price War. Available online: https://www.cnbc.com/2020/03/08/opec-deal-collapse-sparks-price-war-20-oil-in-2020-is-coming.html (accessed on 28 April 2021).

- World Bank. 2021. Latest Commodity Prices Published (Monthly Prices). Available online: https://www.worldbank.org/en/research/commodity-markets (accessed on 8 February 2021).

- World Health Organization (WHO). 2020. Novel Coronavirus (2019-nCoV) Situation Report-1. Available online: https://www.who.int/docs/default-source/coronaviruse/situation-reports/20200121-sitrep-1-2019-ncov.pdf (accessed on 8 December 2020).

- Wu, Jing, Michelle Gamber, and Wenjie Sun. 2020. Does Wuhan Need to be in lockdown during the Chinese Lunar New Year? International Journal of Environmental Research and Public Health 17: 1002. [Google Scholar] [CrossRef] [Green Version]

- Yuan, Chaoqing, Sifeng Liu, and Junlong Wu. 2010a. The relationship among energy prices and energy consumption in China. Energy Policy 38: 197–207. [Google Scholar] [CrossRef]

- Yuan, Chaoqing, Sifeng Liu, and Naiming Xie. 2010b. The impact on Chinese economic growth and energy consumption of the Global Financial Crisis: An input-output analysis. Energy 35: 1805–12. [Google Scholar] [CrossRef]

- Zhang, Yanfang, Rui Nie, Ruyi Shi, and Ming Zhang. 2018. Measuring the capacity utilization of the coal sector and its decoupling with economic growth in China’s supply-side reform. Resources, Conservation and Recycling 129: 314–325. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variables | Level Data (t-Value) | First Difference Data | ||||

|---|---|---|---|---|---|---|

| ADF | PP | KPSS | ADF | PP | KPSS | |

| Australian coal | −2.46 | −2.41 | 0.85 * | −11.5 * | −11.59 * | 0.05 |

| Japanese LNG | −1.81 | −1.73 | 0.92 * | −7.45 * | −9.44 * | 0.19 |

| Dubai Crude-oil | −2.55 | −1.97 | 0.67 * | −9.67 * | −8.92 * | 0.18 |

| China coal | −2.60 | −3.10 | 0.38 * | −4.55 * | −6.90 * | 0.03 |

| Chinese natural gas | −3.27 | −4.12 | 0.37 * | −7.45 * | −13.4 * | 0.02 |

| Chinese crude oil | −2.88 | −3.75 | 0.43 * | −12.89 * | −12.88 * | 0.02 |

| Relationship between Variate | Lag | Lowest SC |

|---|---|---|

| Chinese coal vs. Australian coal | 2 | −1.35 * |

| Chinese coal vs. Dubai crude oil | 2 | −1.62 * |

| Chinese coal vs. Japanese LNG | 2 | −2.38 * |

| Chinese crude oil vs. Australian coal | 2 | −0.41 * |

| Chinese crude oil vs. Dubai crude oil | 2 | −1.04 * |

| Chinese crude oil vs. Japanese LNG | 4 | −1.60 * |

| Chinese natural gas vs. Australian coal | 2 | −0.02 * |

| Chinese natural gas vs. Dubai crude oil | 2 | −0.69 * |

| Chinese natural gas vs. Japanese LNG | 4 | −1.28 * |

| Between Different Market | Rank Number | Trace Statistic | 0.05 Critical Value | Max-Eigenvalue Statistic | 0.05 Critical Value |

|---|---|---|---|---|---|

| Chinese coal vs. Australian coal | None * | 25.95 * | 15.49 | 21.45 * | 14.26 |

| At most 1 * | 4.5 * | 3.84 | 4.5 * | 3.84 | |

| Chinese coal vs. Dubai crude oil | None * | 27.65 * | 15.49 | 23.19 * | 14.26 |

| At most 1 * | 4.45 * | 3.84 | 4.45 * | 3.84 | |

| Chinese coal vs. Japanese LNG | None * | 38.54 * | 15.49 | 35.84 * | 14.26 |

| At most 1 | 2.69 | 3.84 | 2.69 | 3.84 | |

| Chinese crude oil vs. Australian coal | None * | 23.16 * | 15.49 | 18.81 * | 15.49 |

| At most 1* | 4.34 * | 3.84 | 4.34 * | 3.84 | |

| Chinese crude oil vs. Dubai crude oil | None * | 23.64 * | 15.49 | 21.45 * | 15.49 |

| At most 1 * | 4.5 * | 3.84 | 4.5 * | 3.84 | |

| Chinese crude oil vs. Japanese LNG | None * | 39.54 * | 15.49 | 35.65 * | 15.49 |

| At most 1* | 3.89 * | 3.84 | 3.89 * | 3.84 | |

| Chinese natural gas vs. Australian coal | None * | 28.59 * | 15.49 | 23.55 * | 15.49 |

| At most 1 * | 5.04 * | 3.84 | 5.04 * | 3.84 | |

| Chinese natural gas vs. Dubai crude oil | None * | 26.18 * | 15.49 | 22.68 * | 15.49 |

| At most 1 | 3.49 | 3.84 | 3.49 | 3.84 | |

| Chinese natural gas vs. Japanese LNG | None * | 45.01 * | 15.49 | 40.81 * | 15.49 |

| At most 1 | 4.20 | 3.84 | 4.20 | 3.84 |

| Chinese and International Fossil Fuel | Used Model | Independent Variables | Dummy Variate | Coefficient | t-Value |

|---|---|---|---|---|---|

| Chinese coal vs. Australian coal | VAR | China coal | dummy1 | −0.129 * | −2.994 * |

| dummy2 | 0.036 | 0.920 | |||

| Australian coal | dummy1 | −0.160 * | −2.549 * | ||

| dummy2 | 0.043 | 0.742 | |||

| Chinese coal vs. Dubai crude oil | VAR | China coal | dummy1 | −0.147 * | 3.203 * |

| dummy2 | 0.048 | 1.131 | |||

| Dubai crude oil | dummy1 | −0.067 | −1.291 | ||

| dummy2 | −0.020 | −0.414 | |||

| Chinese coal vs. Japanese LNG | VAR | China coal | dummy1 | −0.181 * | −3.890 * |

| dummy2 | 0.037 | 0.841 | |||

| Japanese LNG | dummy1 | −0.037 | −1.103 | ||

| dummy2 | 0.033 | −1.029 | |||

| Chinese crude oil vs. Australian coal | VAR | Chinese crude oil | dummy1 | −0.097 | −0.925 |

| dummy2 | −0.071 | −0.723 | |||

| Australian coal | dummy1 | −0.145 * | −2.320 * | ||

| dummy2 | 0.050 | 0.852 | |||

| Chinese crude oil vs. Dubai crude oil | VAR | Chinese crude oil | dummy1 | −0.066 | −0.699 |

| dummy2 | −0.036 | −0.392 | |||

| Dubai crude oil | dummy1 | −0.051 | −1.014 | ||

| dummy2 | −0.023 | −0.475 | |||

| Chinese crude oil vs. Japanese LNG | VAR | Chinese crude oil | dummy1 | −0.208 * | −2.252 * |

| dummy2 | −0.081 | −0.899 | |||

| Japanese LNG | dummy1 | −0.048 | −1.573 | ||

| dummy2 | −0.044 | −1.451 | |||

| Chinese natural gas vs. Australian coal | VAR | Chinese natural gas | dummy1 | −0.263 * | −2.194 * |

| dummy2 | −0.241 * | −2.138 * | |||

| Australian coal | dummy1 | −0.162 * | −2.536 * | ||

| dummy2 | 0.033 | 0.553 | |||

| Chinese natural gas vs. Dubai crude oil | VECM | Chinese natural gas | dummy1 | −0.186 | −1.675 |

| dummy2 | −0.193 | −1.781 | |||

| Dubai crude oil | dummy1 | −0.082 | −1.552 | ||

| dummy2 | −0.058 | −1.123 | |||

| Chinese natural gas vs. Japanese LNG | VECM | Chinese natural gas | dummy1 | −0.304 * | −3.005 * |

| dummy2 | −0.242 * | −2.421 * | |||

| Japanese LNG | dummy1 | −0.048 | −1.523 | ||

| dummy2 | −0.039 | −1.243 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tang, C.; Aruga, K. Effects of the 2008 Financial Crisis and COVID-19 Pandemic on the Dynamic Relationship between the Chinese and International Fossil Fuel Markets. J. Risk Financial Manag. 2021, 14, 207. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050207

Tang C, Aruga K. Effects of the 2008 Financial Crisis and COVID-19 Pandemic on the Dynamic Relationship between the Chinese and International Fossil Fuel Markets. Journal of Risk and Financial Management. 2021; 14(5):207. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050207

Chicago/Turabian StyleTang, Chaofeng, and Kentaka Aruga. 2021. "Effects of the 2008 Financial Crisis and COVID-19 Pandemic on the Dynamic Relationship between the Chinese and International Fossil Fuel Markets" Journal of Risk and Financial Management 14, no. 5: 207. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm14050207