Developing an Impact-Focused Typology of Socially Responsible Fund Providers

Ingolstadt School of Management, Professorship for Christian Social Ethics and Social Policy, Catholic University Eichstätt-Ingolstadt, Auf der Schanz 49, 85049 Ingolstadt, Germany

*

Author to whom correspondence should be addressed.

†

Joel Diener is a PhD candidate at the Professorship for Christian Social Ethics and Social Policy at the Catholic University of Eichstätt-Ingolstadt.

J. Risk Financial Manag. 2022, 15(7), 298; https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15070298

Submission received: 18 May 2022

/

Revised: 24 June 2022

/

Accepted: 27 June 2022

/

Published: 5 July 2022

(This article belongs to the Special Issue Green Marketing, Green Finance and Sustainable Development)

Abstract

:The concept of investor impact of socially responsible investments is relatively new. Our article expands knowledge in this field by analyzing how investor impact is implemented in the ethical investment policies of 45 providers of publicly traded, socially responsible funds. Based on a typological content analysis, we first develop an impact-focused category system, which in the second step is used to distinguish three types of fund providers: ESG hermits, ESG ambassadors and ESG evangelists. Our results suggest that socially responsible fund providers with a stronger impact orientation, such as ESG evangelists, also employ strategies that are more likely to achieve investor impact. In contrast, fund providers with a weaker impact orientation, such as ESG hermits, focus more on purity aspects and therefore tend to utilize strategies that defend the purity claim but also show a weaker investor impact.

1. Introduction

During the past two decades, socially responsible investing (SRI) has become a multi-billion-dollar industry. For example, the United Nations Principles for Responsible Investment (UN PRI), the leading proponent of responsible investment, has grown from 63 signatories with over $6.5 trillion of assets under management (AUM) in 2006 to over 4000 signatories with over $120 trillion of AUM in 2021 (UN PRI 2021).

Considering global challenges such as combating climate change and achieving the UN Sustainable Development Goals (SDGs), investors are increasingly demanding that their investments contribute to a “better world” (Wins and Zwergel 2016; Bauer et al. 2019; Barber et al. 2021). An impact view is also salient in the sector’s self-representation, with the UN PRI recently adding a change-oriented perspective to its assessment of signatories (UN PRI 2020) and at the regulatory level with the EU Sustainable Finance Taxonomy (European Parliament 2020). Individual success stories, such as sustainability-focused hedge fund Engine No.1, which won three seats on Exxon Oil’s board to accelerate the company’s transition to sustainability (Hiller and Herbst-Bayliss 2021), are fueling this evolution.

However, to develop investment solutions and policies that accelerate the transformation process of the economy, it is necessary to understand those parameters that determine the non-financial impact of the SRI sector (Schwirplies and Ziegler 2016). In this context, it is important to differentiate between the impact of a company and the impact of an investment product on the behavior of this company (Kölbel et al. 2020). The latter, which Kölbel et al. (2020) call “investor impact”, is what interests us in this article. Although there is extensive literature on SRI, and although the first academic studies (e.g., Landier and Lovo 2020; Clementino and Perkins 2020; Pástor et al. 2021; Hoepner et al. 2022) and some practitioner reports (GSIA 2020; Eurosif 2018) have begun to explore the concept of investor impact, many questions have yet to be answered.

To narrow the research gap and to bring more methodological clarity to the academic discussion, we analyze in our exploratory study how investor impact is implemented in the ethical investment policies of socially responsible fund providers. Based on a typological content analysis following Kuckartz (2016), we first construct an impact-focused category system with twelve clearly distinguishable criteria. Five criteria are newly developed indicators that can be used to separate those fund providers that credibly strive for sustainability improvements from those that merely pretend to be impact-focused. We call these criteria “impact orientation indicators” (IOI). The other seven criteria describe the strategies that the SRI fund providers apply to influence the sustainability development of their portfolio companies. We label these criteria “investor impact strategies” (IIS) and briefly address the effectiveness of IIS in influencing corporate behavior. In the second step, based on these twelve criteria, a typology of fund providers is created. Here, three types are distinguished: ESG hermits, ESG ambassadors and ESG evangelists. ESG hermits are characterized by a strong emphasis on purity and a rather weak impact orientation. They therefore tend to utilize IIS that defend the purity claim but also show a weaker investor impact, for example, exclusion or divestment. In contrast, ESG ambassadors emphasize that they contribute to positive change in portfolio companies. Their impact orientation is much stronger. Although ESG ambassadors also rely on exclusion and divestment, they additionally apply positive approaches to increase their impact. The last group, the ESG evangelists, has the strongest impact orientation. In addition to ESG ambassadors’ tools, ESG evangelists amplify their impact through various forms of shareholder engagement, either individually or in collaboration.

Our research contribution is as follows. We are the first to provide an impact-focused typology of socially responsible investment companies. By focusing on investor impact, we set a clear counterpoint to those researchers and practitioners who classify SRI funds either by their screening intensity (e.g., Renneboog et al. 2008; Lee et al. 2010 or Pérez-Gladish et al. 2012) or by their financial impact (e.g., Friede et al. 2015). In this sense, our pioneering work adds a new assessment dimension to both the research and practice of SRI. Second, we structure the literature in this area to enable further studies in the emerging research field of the investor impact of SRI funds. We identify many interesting avenues for future research, such as the effectiveness of different IIS, measuring investor impact or benchmarking performance based on a fund provider’s impact orientation. Finally, our findings should encourage investors, for whom investor impact is more than just empty words, to take some time to investigate the ethical investment policies of their investment options.

2. Conceptual Foundation

In recent years, there is a growing awareness for global challenges such as biodiversity loss (WWF et al. 2016), overconsumption of natural resources (Moore et al. 2012) and especially climate change. For example, in 2015, the UN Sustainable Development Goals were launched, which outline sustainability goals for all United Nations (UN) members. That same year, 195 countries pledged in the Paris Climate Agreement to limit global warming to below two degrees Celsius to combat climate change. This development has had a lasting and significant impact on the understanding of SRI; whereas in the early years, purity considerations and the protection of one’s own conscience were paramount, the focus has now shifted to SRI’s contribution to social and environmental development.

At the regulatory level, this is reflected, for example, in the EU Action Plan for a Greener and Cleaner Economy. There, sustainable investments are now identified as an important tool for fulfilling the Paris Agreement (European Commission 2018). In other jurisdictions, pension funds, asset managers and other institutional investors are mandated to disclose how they take environmental, social and governance (ESG) considerations into account in their investment decisions (OECD 2017). An increasing emphasis on impact can also be observed in the sector’s self-representation. For example, the UN PRI, the largest SRI advocacy group with more than 2000 signatories, recently added a change-oriented perspective to its signatory assessment (UN PRI 2020). In addition, asset managers and owners in the EU lately demanded that rating agencies focus more on a company’s actual sustainability performance and the impact of its products, and less on data disclosure or company policies (European Commission 2021). Finally, the 2020 UK Stewardship code emphasizes the importance to create sustainable benefits for the economy, the environment and society (FRC 2020). Lastly, investors are also paying more attention to the impact of their investments on sustainable development when selecting their investment service providers. Research here is conducted by Sandberg and Nilsson (2011) as well as Wins and Zwergel (2016). Both studies found that the majority of SRI investors want fund management to increase the sustainability performance of portfolio companies, with 90% of investors in Sweden (Sandberg and Nilsson 2011) and 86.4% of investors in Germany (Wins and Zwergel 2016) demanding this. In a recent study, Barber et al. (2021) found that investors are even willing to pay more for investments that have a positive impact. Furthermore, Bauer et al. (2019) showed that when investors have a say in a fund’s investment policy, they prefer activities that promote sustainable development. In summary, regulators as well as leading SRI institutions and investors all increasingly focus on influencing corporate behavior.

However, to develop investment solutions and policies that accelerate the sustainability transformation of the economy, it is necessary to understand the parameters that determine the non-financial impact of the SRI sector (Schwirplies and Ziegler 2016).

Here, it is important to not confuse the impact of a company1 with the impact of an investment product on that company. Whereas the former has a direct influence on the sustainability development through its business activities, the latter does not. The impact of an investment product, or “investor impact”, is rather indirect, as shareholders can influence the management decisions of their portfolio companies (Brest and Born 2013; Brest et al. 2018).

First studies are starting to explore the concept of investor impact. For example, the theoretical studies of Landier and Lovo (2020) and Pástor et al. (2021) explore whether an investor can generate positive impacts. Landier and Lovo (2020) design an equilibrium model of a productive economy with negative externality effects. They show that in such a model, an ESG fund can influence the behavior of portfolio companies. With a similar method, Pástor et al. (2021) show that socially responsible investing generates a positive impact: First, it makes firms greener, and second, it increases the overall real investment activities of green firms while simultaneously decreasing the investment activities of brown firms. In their analyses, however, neither study distinguishes which strategies account for this effect.

IIS have also been the subject of some recent empirical studies. For example, Slager and Chapple (2015) and Clementino and Perkins (2020) analyzed the effects of exclusion threats on corporate behavior. Whereas Slager and Chapple (2015) found that firms at risk of being excluded more often improved their sustainability performance, Clementino and Perkins (2020) observed that pressure from investors can lead to a hostile organizational response. They note that such a reaction is more likely when management sees no business benefit in responding to investor demands. Baker et al. (2018) and Zerbib (2019) examined how positive selection affects corporate debt prices. Whereas Zerbib (2019) found a negative yield premium of 0.02% on average, Baker et al. (2018) reported a negative yield premium of 0.06%. Gifford (2010) as well as Dimson et al. (2015) studied the effects of shareholder dialogue. With a case study approach, Gifford (2010) showed that a high share of capital and management open to external input increased the prospects of success. Dimson et al. (2015) investigated the effects of engaging in long-term dialogue with senior management and found that in 18% of cases, changes were implemented in line with investors’ demands. Further, Hoepner et al. (2022), Barko et al. (2017) and Dyck et al. (2019) explored the role of shareholder resolutions in improving corporate sustainability. Hoepner et al. (2022) found that the proposal led to sustainability improvements in 31% of cases. They also observed that ESG engagement reduced the company’s risk exposure and was therefore financially beneficial. Dyck et al. (2019) and Barko et al. (2017) examined how shareholder proposals affected the ESG ratings of the targeted companies. They found that ratings improved, which is an indicator of successful engagement. However, although fund providers typically combine IIS, all studies conducted an isolated assessment and neglected the effects of the interplay of strategies.

The GSIA (2020) or Eurosif (2018) practitioner reports analyze which IIS are applied. They distinguish very broadly between exclusion (i.e., both negative and norm-based screening), positive approaches (i.e., both positive and best-in-class investing) and shareholder engagement strategies. Further, the reports note that IIS may be applied in combination, but do not specify which IIS occur together and whether there may be specific patterns here. Another research topic that arises in the context of investor impact is the credibility of impact claims. Both Heeb et al. (2021) and Busch et al. (2021) warn against products that claim a sustainability effect but at best make investors feel good. However, research has not yet addressed the issue of developing indicators to distinguish providers of such products from those that credibly strive for sustainability improvements. Overall, the concept of investor impact remains largely unexplored to date (Kölbel et al. 2020).

We take the growing awareness for investor impact on the one hand and the lack of academic research on investor impact on the other hand as a starting point for this exploratory study. We will focus on how investor impact is implemented in the ethical investment policies of socially responsible fund providers. For a sample of SRI fund providers, we analyze what strategies are applied to influence the sustainability development of their portfolio companies and examine whether there are indicators to separate those fund providers that credibly strive for sustainability improvements from those that merely pretend to be impact-focused. Based on these results, we then explore if there are different types of fund providers. In the next chapter, we will explain in more detail how we proceeded, and also describe the five IOIs and the seven IISs.

3. Data and Method

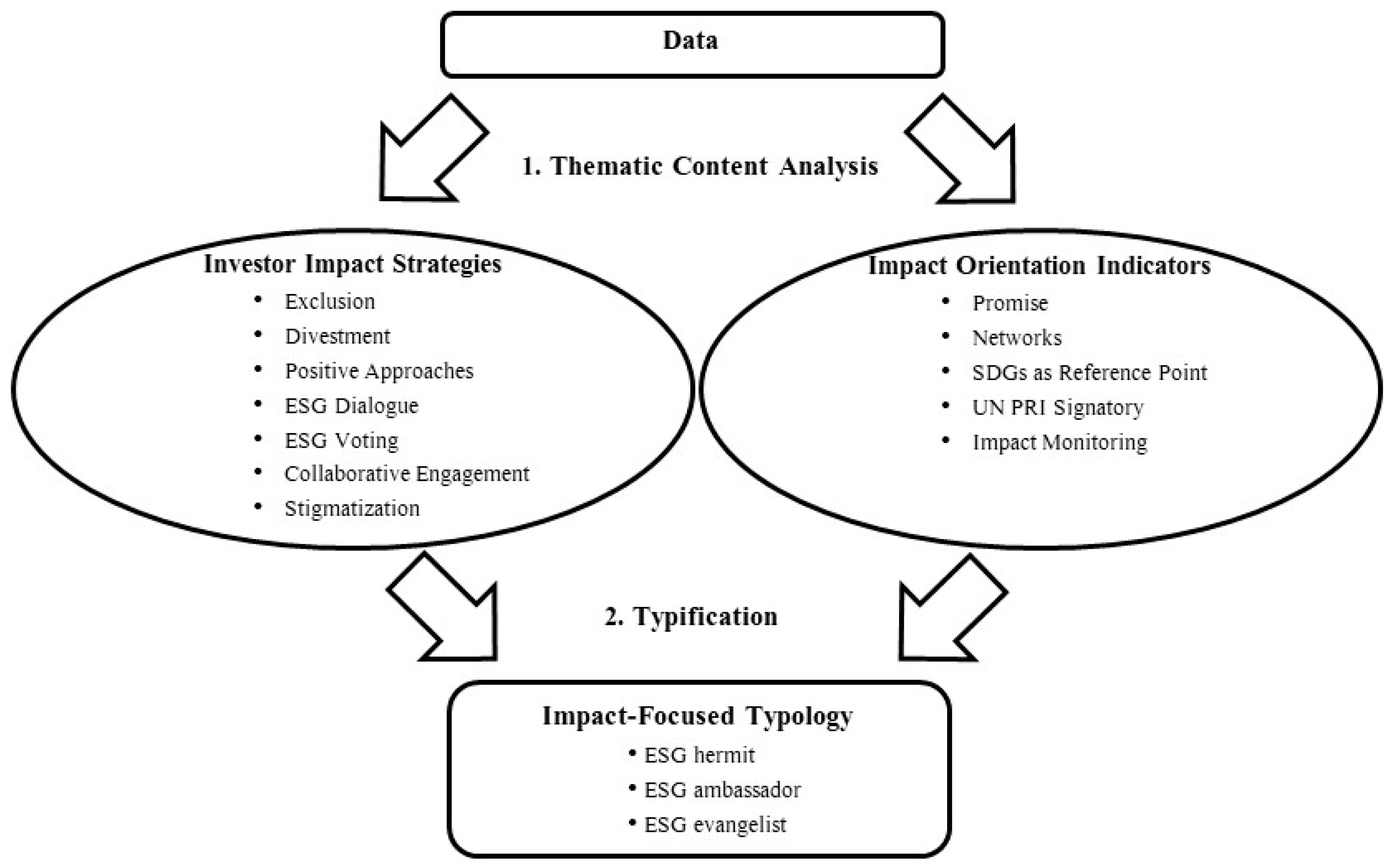

To analyze how investor impact is implemented in the ethical investment policies of providers of publicly traded SRI funds, we screened over 400 documents with approximately 8500 pages from 45 different providers from the USA, Germany, Austria, Switzerland, France, Spain, and the United Kingdom. To portray the market-oriented self-representation, we considered only publicly available information material. We also chose to analyze the full sample to be able to make general statements about our sample of SRI fund providers. Methodologically, we followed Kuckartz’s (2016) typological content analysis. The method is particularly suitable for exploratory studies, as it allows for an open but systematic and rule-based investigation of both explicit and implicit communication (Kuckartz 2022).

The following Figure 1 outlines how we proceeded here:

3.1. Thematic Content Analysis

As a first step, we conducted a thematic content analysis and examined the 45 cases using MAXQDA 2020 (VERBI Software 2020), a data analysis software. Initially, we structured the material along our research question and based on our conceptual foundation. Following an exploratory-inductive approach, we coded each segment of the material that contained information about ethical investment strategy. We then defined top categories and assigned each segment to a category. Next, we functionally reduced the categories that shared many common attributes, arriving at 56 clearly distinguishable categories. These categories were then discussed, and the material was recoded several times by two researchers to identify those criteria that best determined the underlying impact perspective of a provider of socially responsible funds.

During this process, impact implementation was found to occur along two dimensions: IOI and IIS. Some of the IIS were already the subject of scientific analysis by other researchers, but the IOI were mostly newly developed during the thematic content analysis. At the end, we selected the most relevant categories for each dimension from our category pool based on theory. In the next two sections, we will briefly describe them.

3.1.1. Description of the Impact Orientation Indicators

The first IOI is the promise that the respective fund providers make in their marketing material. What do they want to be associated with? What image is transported to the customers? How do they try to differentiate from their competitors? Broadly speaking, an emphasis on purity and the protection of investors’ conscience contrasts with an emphasis on investor impact. Of course, these two extremes are not necessary mutually exclusive. Rather, they indicate the spectrum of different promises that exists. Although these self-statements must be taken with caution, they may serve as a complementary indicator to evaluate the impact orientation of a fund provider.

Our second IOI would be the membership in networks. This can be networks that promote global sustainability improvements or networks that additionally have a common normative foundation as another unifying dimension. Examples for the former would be the Carbon Disclosure Project (CDP) or the European Sustainable Investment Forum (Eurosif), and for the latter, the Interfaith Center on Corporate Responsibility (ICCR). The networks have multiple roles to play for their members: influencing public policy, exchanging information and best practice and promoting a greater awareness for socially responsible investing in society at large or coordinating shareholder engagement (Goodman et al. 2014). Additionally, those networks are instrumental for establishing social norms (Cialdini and Trost 1998) and the intra-group dynamics might lead to increased sustainability efforts of the members. Research on charitable giving has shown that it is easier to convince potential donors if they find others to give too (DellaVigna et al. 2012; Shang and Croson 2009). Overall, membership in networks (even more leading or starting one) signals that a contribution towards sustainability transition is abecedarian for the fund provider.

Our third IOI is taking the SDGs as a reference point. They were launched by the United Nations in 2015 in response to global challenges such as climate change, overconsumption of natural resources, poverty or undernourishment. This sustainability agenda covers 17 targets for all member states of the United Nations and may therefore serve as a global action framework to reach the most urgent sustainability goals (UN 2015). It is in fact well recognized that the SDGs cannot be reached by the public sector alone. Rather, a joint effort with the private sector is needed with the latter having to close a funding gap of 80% of the total costs of 75 trillion US-Dollar (PRI 2017). Consequently, an investor who incorporates the SDGs into its ethical investment policy and aims to allocate capital towards achieving the SDGs should also possess a strong impact orientation.

Our fourth IOI is being a signatory of the UN PRI. This is because UN PRI members explicitly self-commit to follow an active, change-orientated investment policy. Principle two, for example, declares: “We will be active owners and incorporate ESG issues into our ownership policies and practices” (UN PRI 2018, p. 5). The UN PRI are committed to understanding the impact of ESG factors on investments. With their annual assessment reports, the UN PRI actively supports the signatories to improve their socially responsible investment practices. Further, the PRI clearinghouse provides the largest platform for shareholder engagement. Being a UN PRI signatory therefore clearly signals a strong impact orientation.

The fifth IOI is the existence or absence of impact monitoring. As Dillenburg et al. (2003) rightly note, only “what gets measured gets managed”. Consequently, if an investor aims to achieve impact and increase its impact effectivity, a structured and timely impact monitoring is inevitable. Impact can be measured in quantitative or qualitative terms. An example for the former would be a reduction of CO2-emissions and for the latter a commitment to address child labor in the value chain. There are currently numerous initiatives aimed at harmonizing corporate reporting on ESG issues. For example, the International Organization of Securities Commissions has expressed its ambition to accelerate the standardization of sustainability metrics. The International Federation of Accountants has advocated the establishment of an International Sustainability Standards Board, and the World Economic Forum (WEF) has launched an initiative to define common metrics for sustainable value creation (WEF 2020). Among others, three main reasons for impact monitoring must be mentioned. First, it allows the fund provider to focus its limited resources on the relevant areas and portfolio companies. Second, it enables the fund provider to change the IIS, for examples involving other stakeholders or collaborating with other investors, if the intended outcome is not achieved. Third, the documentation of their activities is used for reporting to their clients. Such an investor impact report may contain case studies of successful engagements or an overview of the carbon footprint of the different portfolio companies. Proper impact monitoring is therefore another IOI; or expressed the other way around: An investor claiming to be impact-focused but lacking impact monitoring is, at best, unprepared.

3.1.2. Description of the Investor Impact Strategies

There are two principal mechanisms for fund providers to affect corporate sustainable development: financial influence and investor advocacy influence (Waygood 2011). The first mechanism refers to the investor impact on the company’s capital costs through buying or selling equity and debt instruments: As firms can raise less (more) capital if the capital costs increase (decrease), this constrains (extends) its business activities. IIS that apply the first mechanism are exclusion, divestment and positive approaches. The second mechanism refers to any IIS in which investors use their ownership rights to influence management. IIS that apply the second mechanism are ESG dialogue, ESG voting and shareholder proposals as well as collaborative engagement. Additionally, with stigmatization, we identified an IIS that applies both mechanisms. Here, investors are either deterred, which affects the cost of capital, or they are urged to use their share ownership to influence the management of the company.

The first IIS, exclusion or negative screening is the practice of eliminating any company from the investment universe whose products or business practices are considered “unethical”. Exclusion can be implemented in several ways. Some investors shun only certain business practices, whereas others even exclude entire industries. Some investors extend the exclusions to a company’s subsidiaries, whereas others also consider suppliers or even financial institutions. Often, the decision to exclude is based on exceeding a specific threshold, either in terms of revenue shares or absolute revenue amounts. Empirical findings on the effectiveness of exclusion are inconclusive. For example, whereas Derwall et al. (2011) and Slager and Chapple (2015) find that exclusion affects corporate behavior, Richardson (2009) and Häßler and Markmiller (2013) state that exclusion does not have a significant impact on managerial attitudes. In fact, Clementino and Perkins (2020) discover that in some cases institutional pressure actually causes firms to respond adversely.

Divestment is also a common IIS, either as an immediate response to negative developments or as a last resort in an engagement process. This is an aggressive form of exclusion because, in addition to excluding a company’s shares from future purchases, the portfolio is also cleansed of existing positions (Dawkins 2018). Triggers for divestment might be a worsening of the ESG rating, the involvement into a controversy or that a problematic aspect has been overlooked in the initial screening process. Luo and Balvers (2017) show in a theoretical model, that the market requires a firm with a controversial business to pay a premium for the systematic investor boycott risk. Furthermore, Dawkins (2018) argues from both a theoretical and ethical perspective, that divestment, especially when combined with shareholder engagement, is a very effective tool for improving sustainability. Empirical evidence, however, does not support these theoretical considerations. For example, Teoh et al. (1999) found no effects of the divest South Africa movement on the financial situation of targeted companies. Another divestment campaign, the Sudan Accountability and Divestment Act (SADA) in 2007, also had no effect on the share prices of the companies concerned. (GAO 2010).

In contrast to the rather confrontational IISs of exclusion and divestment, positive approaches reward particularly exemplary companies. This approach goes beyond a pure “do-no-harm” approach, i.e., it not only excludes the most questionable companies, but also invests specifically in securities that make a positive contribution to sustainable development. They can have the form of either best-in-class or positive screening. The aim is to increase share prices and reduce financing costs to encourage and assist socially responsible behavior, which is the inverse of exclusion strategies. Empirical studies of Slager and Chapple (2015) and Clementino and Perkins (2020) show the success for equities, whereas Baker et al. (2018) and Zerbib (2019) show it for corporate debt. Further, there is evidence from Dimson et al. (2015) that this strategy should also be financially rewarding.

The next IIS, ESG dialogue, comprises all activities in which investors enter into a direct exchange with company management on ESG issues. Reasons might be a sudden drop in the ESG rating or an effort of the investor to encourage the company to achieve more ambitious sustainability goals. The ESG dialogue can be conducted in various forms: in private by letter or e-mail-writing, telephone calls, on-site visits with one-on-one meetings or in public by asking critical questions at annual general meetings or sending open letters. In addition, some investors enter into dialogue even before they have bought into the stock, either if an ESG rating is missing or if there are business practices worthy of discussion. Gifford (2010) and Dimson et al. (2015) both examine the impact of ESG dialogue and classify it as a useful tool to affect corporate change.

A more formal way of influencing the firms’ management is to submit shareholder proposals and to exercise voting rights, with the latter being the most widely used form of Shareholder Engagement (Louche 2015). There are certain service providers such as Institutional Shareholder Services (ISS) that offer operational support and also provide voting recommendations. In the context of SRI, it is important to differentiate between the general proxy voting on behalf of the clients of the fund provider and an explicit ESG voting strategy that systematically incorporate ESG aspects. For ESG voting against management to be successful, a sufficient large share of ownership is necessary. However, even if voting is not successful, a sufficient large share of opposition might still lead to changes in the company’s business activities. Therefore, some companies have started to pool their voting rights on ESG issues with other like-minded investors. Hoepner et al. (2022), Barko et al. (2017) and Dyck et al. (2019) study the effects of shareholder proposals and all find this tool to be effective in improving corporate sustainability performance.

In the next IIS, collaborative engagement, investors form coalitions and pool their influence, for example, for fighting climate change or improving human rights (Dyck et al. 2019; Chen et al. 2020). This can be done via engagement platforms such as the PRI clearinghouse or via direct engagement partnerships between investors with similar ESG policies. A prominent case of successful coordination are the three seats on Exxon Oil’s board for sustainability-focused hedge fund Engine No.1 to accelerate the shift towards greater sustainability (Hiller and Herbst-Bayliss 2021). According to Dimson et al. (2013) and Dimson et al. (2018), this form of engagement is highly effective, as it leverages the shareholders’ influence without increasing the risk of being under diversified in an asset.

The final mechanism we found in our data is stigmatization. Here, investors malign the company’s image to, on the one hand, deter other investors and influence the cost of capital and, on the other hand, generate public pressure, e.g., through media campaigns. This IIS can be used either in isolation or as part of an engagement strategy. Involving other investors and other stakeholders is the aim. The consequences of such a campaign can be that companies have problems finding new employees (Kölbel et al. 2020) or that banks stop financing certain activities (Sorkin 2015). Research in the context of SRI is very thin, however, adjacent areas give at least some indirect evidence. King and Soule (2007) document that social movements could influence the stock prices of a targeted company. However, they did not investigate how those affects actually lead to changes within the targeted corporations. Indirect, anecdotal evidence for stigmatization to be successful comes from Markman et al. (2016). The authors document that the nongovernmental organization (NGO) People for the Ethical Treatment (PETA) succeeded in conducting a media campaign to end the practice of sheep mulesing. The campaign not only impacted the targeted apparel retailers, but also disrupted the entire apparel industry and even spilled over into adjacent industries. Waldron et al. (2014) find both successful public campaigns, e.g., from the Rainforest Action Network (RAN) and unsuccessful ones, e.g., from Greenpeace. In a later study, Waldron et al. (2019) find Oxfam and GLAAD to be successful, whereas the campaigns of Friends of the Earth and PETA failed. However, it stands to reason in how far the toolbox of an SRI investors is comparable to the options of NGOs.

3.2. Typification

The result of the thematic content analysis is an impact-focused category system with twelve criteria, five IOIs and seven IISs, to evaluate the ethical investment policies. To confirm the validity of our category system, we had two independent research assistants each code a random sample of approximately 10% of the coded segments. We prioritize greater external objectivity, so neither were involved in the design of the category system (Kolbe and Burnett 1991). As a statistical measure for the reliability of agreement, we choose Fleiss’ Kappa and obtained a value of 0.704, which according to Landis and Koch (1977), represents a substantial agreement and suggests a high confidence in the category system. Following Campbell et al. (2013), we then discussed the results to eliminate weaknesses in the category system.

Based on this impact-focused category system, we develop a typology of socially responsible fund providers. For that typology to reflect the observed reality most accurately, we decided to inductively create polythetic types through pragmatic reduction (Bailey 1972). Following the typification approach of Kuckartz (2016), we first used the category system to create case summaries for every socially responsible fund provider. In the second step, we ranked, sorted and grouped the case summaries according to their similarity. In the third step, we decided how many groups would be appropriate. In an iterative process, we repeated these steps several times, discussing ambiguous cases and then assigning them to a type until we had groups that were clearly distinguishable and internally consistent. In the final step, we creatively formulated type descriptions that should reflect the characteristics of each type as accurately as possible.

4. Results

In this section, we will provide a detailed description of the profiles of every type of fund provider. For that purpose, we constructed model cases as described by Kuckartz (2022). It must be noted that only the joint use of the IOIs allows for a sound assessment of the investor impact orientation. Overall, we classified around 25% of our sample as ESG hermits, another 25% as ESG ambassadors and around 50% as ESG evangelists. Table 1 provides an overview of the main differences and similarities between those three types:

4.1. ESG Hermit

ESG hermits are primarily concerned with staying away from any business activities that are “unethical” by their own definition. Actively influencing portfolio companies is therefore negligible for this type. The investment solutions are aimed at customers who want to be active in the financial markets, but for whom a “clear conscience” is important above all.

“Investors no longer need to choose between sacrificing the opportunity for strong risk adjusted returns or their integrity.”(fund provider from the USA)

ESG hermits are not part of any network and do not take the SDGs as a reference point for their ethical investment policies. Further, they have not signed up to the UN PRI and thus shy away from a critical review or even an external audit of their investment practices. This may indicate that ESG hermits are highly convinced of their ideas, strategies and ethical judgments and prefer not to be influenced. Consistent with the negligible importance of investor impact, they have no tools to track the success of their activities. Instead, ESG hermits continuously monitor the conformity of their portfolio companies to their definition of an “ethical” business. For this purpose, they use professional third-party screening providers such as MSCI ESG Research or ISS ESG, but do not rely on these external sources only. Instead, ESG hermits also use their own internal research tools to check whether the accusations are substantiated, for example, in the case of a scandal. The explanation for this costly dual control is that the protection of their own reputation is paramount for survival.

“Our staff reassess the company to verify or refute the accusation. We can’t go on what someone else has said.”(fund provider from the USA)

Overall, it must be noticed that the impact orientation of ESG hermits is rather weak, as their primary goal is to protect clients’ consciences. Consequently, they apply the more confrontational IISs of exclusion, divestment and stigmatization, which tend to be less effective in generating investor impact.

The way ESG hermits approach exclusion is very purity-focused. For example, they criticize the use of “ethical thresholds”—an approach in which an investment in a stock is acceptable until a pre-determined percentage of revenue is generated by “unethical” practices. In their view, this is an unacceptable ethical compromise, which is why they tout their own zero-tolerance policy as a better alternative.

“We will not invest a single penny into any company that violates our filters.”(fund provider from the USA)

Additionally, they claim to screen more comprehensively than others and therefore to consider not only the companies themselves, but also their suppliers and subsidiaries.

If it is found that a company is less ethical than previously assumed, it will be divested. No attempt is made to enter into dialogue, nor are other options taken to resolve the matter. This behavior can be explained by concerns that scandals may be indirectly associated with the ESG hermit, which would damage its reputation (Husson-Traore and Meller 2013) and negatively impact future business prospects. There might be differences in the pace of divestment, however. Whereas some ESG hermits sell the stock immediately after a critical event, others have a certain “grace period” to balance financial and ethical effects.

Some ESG hermits express their opposition to certain corporate practices very clearly by practicing stigmatization. However, instead of being embedded in an engagement strategy, this approach remains purely confrontational. The accusations are directed either at companies that have lost favor with the ESG hermit because of their controversial behavior and have been divested, or at companies that are “evil” and therefore will never be considered. Whereas in the first case the accusation is intended to legitimize the decision to sell (even if this would mean foregoing profits), in the second case the aim is to involve other investors as well as relevant stakeholders to force the companies to alter their “immoral” behavior. As a side effect, public attention also serves as inexpensive marketing to attract new customers who also disagree with the behavior of the targeted companies. An example here would be a fund provider from the USA that publishes a so called “hall of shame”.

Comparable to a hermit in the desert, fund providers of this type try to remain as pure as possible and therefore avoid any contact with “unethical” people, companies or ideas.

4.2. ESG Ambassador

ESG ambassadors see themselves as having a customer mandate that is much broader than just the mandate to maintain a “clear conscience”. Therefore, in contrast to ESG hermits, ESG ambassadors follow a more change-oriented logic and claim that investing with them will positively impact the environment and society. One fund provider even changed the name of its fund into “global impact fund” to further emphasize its impact orientation. The investment products are consequently targeted at customers who want to achieve a positive impact.

“Investments designed for performance and a better world.”(fund provider from the USA)

ESG ambassadors also strive to exert influence via sustainability networks such as national sustainable investment forums or initiatives such as the carbon disclosure project. Such heterogeneous networks provide ESG ambassadors with valuable contacts and serve primarily to share information and best practices. The impact orientation can also be seen when looking at the way ESG ambassadors select their portfolio companies. Here, the SDGs serve as a reference point to either exclude companies that hinder the achievement of the SDGs or to include companies that contribute to their achievement. An example would be a company that makes affordable medicines available (SDG 3) or that provides telecommunications infrastructure in emerging and developing countries, enabling access to information and education (SDG 4 and SDG 9). Further, ESG ambassadors are signatories of the UN PRI. That way they commit to a change-orientated investment policy but are also exposed to an external impact audit of their investment practices. However, the success of the ESG ambassadors’ IISs is not tracked by any form of impact monitoring. This, of course, casts doubt on the claim that they strive to positively impact environment and society. Despite this shortcoming, the overall impact orientation must be classified as medium to strong compared to the ESG hermits.

The stronger impact orientation of the ESG ambassadors is also reflected in the applied IISs. For example, ESG ambassadors also practice exclusion, but instead of “purity”, the aim is to avoid negative impacts. In addition, the portfolio companies’ efforts to mitigate these negative impacts are included in the evaluation.

“It is taken into account whether companies counteract the negative effects, compensate for them or prevent them completely.”(fund provider from Germany)

However, when ratings deteriorate, ESG ambassadors follow the same divestment strategy as ESG hermits.

Along with these confrontational IISs, ESG ambassadors apply rather cooperative IISs. With positive approaches such as best-in-class or positive screening, they foster companies that meet superior ESG standards. The awareness that a pure do-not-harm approach falls far too short is the motivation to implement this IIS.

“From the outset, they wanted to go beyond a pure do-no-harm approach, i.e. not only exclude the most questionable companies and countries, but also invest specifically in securities that make a positive contribution to sustainable development.”(fund provider from Germany)

Engagement activities such as ESG dialogue or ESG voting and shareholder proposals, however, are not part of the ESG ambassador’s toolbox. Given that these IISs are arguably more effective in achieving investor impact, we perceive a gap between theoretical impact orientation and practical implementation. Whether this is an indication that ESG ambassadors are practicing “impact washing” (Busch et al. 2021) or a result of being unaware of differences in the effectiveness of the IISs could be an interesting research question for future studies. Another difference is that ESG ambassadors, unlike ESG hermits, do not use stigmatization to impose their agenda upon portfolio companies.

This type of fund provider has a clear idea of how its portfolio companies should operate and which activities and industries to avoid. However, instead of pushing companies to make sustainable transformations, ESG ambassadors offer support in exchange for sustainability improvements. Companies are free to accept the offer, but if they reject it or even change for the worse, their shares are sold without any prior engagement activities. The allegorical equivalent for this type of fund provider would therefore be a polite ambassador.

4.3. ESG Evangelist

Similar to ESG ambassadors, ESG evangelists are primarily concerned with positively impacting the environment and society. The investment products are consequently targeted at customers for whom a positive impact is important above all.

“The Bank’s active ownership approach is to support long-term, sustainable development. As an active owner, we incorporate environmental, social and governance (ESG) issues into our investment ownership policies and practices and seek to reduce the negative impact on society and the environment and to promote sustainable growth.”(fund provider from Switzerland)

ESG evangelists are active in two different types of networks. Sustainability networks are used to influence public policy, to exchange information or to promote a greater awareness for socially responsible investing. Additionally, they are part of normative networks. Since the value basis here is very similar, those networks are often used to coordinate engagement activities.

ESG evangelists possess a clear understanding of contemporary challenges, consequently taking the SDGs as a reference point for the investment selection. Moreover, they are signatories of the UN PRI and also take part in external audits of their business practices. This type of fund provider also makes use of the PRI clearinghouse, which coordinates engagement activities. To ensure that limited financial and human resources are allocated in the most efficient way, ESG evangelists employ impact monitoring. They therefore show the strongest impact orientation of all three types.

In terms of IISs, ESG evangelists take a flexible approach, and select from the bouquet of measures those that are best suited to the situation at hand. They use screening, negative and positive, but instead of dividing the investment universe into good and bad companies, they employ a differentiated approach guided by an impact logic.

“In a few cases, exceptions are made for companies with which we are engaged in productive shareholder dialogue or that are making notable progress on areas that concern us.”(fund provider from the USA)

Although protecting their credibility is also important to ESG evangelists, they do not directly divest if their investment screens are violated. Instead, in case of a breach, they prefer to first initiate an engagement process. However, if the case cannot be resolved to their satisfaction, divestment is explicitly earmarked as the last option. This decision to additionally apply shareholder engagement is justified by the goal to achieve investor impact and the use of shareholder engagement thus becomes a question of credibility:

“It is only through engagement that the vision of an often postulated “double return” is credibly pursued.”(fund provider from Austria)

ESG evangelists actively participate in ESG dialogues, for example, by writing letters or meeting with senior executives. Further, they have an explicit ESG voting policy to support shareholder proposals that address sustainability issues, but also regularly submit their own proposals. ESG evangelists often do not carry out these activities alone. Instead, they partner with other like-minded investors. Such collaborative engagement is beneficial because influence can be increased without having to increase the portfolio weighting of a company in the portfolio. The PRI clearinghouse plays an important role in coordinating collaborative engagements, but ESG evangelists have also established their own direct engagement partnerships with like-minded investors. Some even launched their own engagement networks, for example, the “Shareholders for Change” initiative. Although stigmatization is also part of the toolbox, it is very rarely utilized. The clear preference is to reach a settlement without public involvement, as such escalation damages long-term partnerships and the relationship of trust. Stigmatization would only become an option if several attempts and different forms of private shareholder engagement failed to solve the problems at hand.

“This means that, unless otherwise agreed, the content of the majority of our meetings is kept confidential between the company and us as an investor. However, we recognise the importance of the media as a tool for delivering change and are not afraid to comment on poor practice (as a method of escalating our engagement) or to engage with the press to raise the profile of important issues and initiatives.”(fund provider from the United Kingdom)

In conclusion, the mission of this type is nothing less than to change the world through its investments. ESG evangelists do not shy away from using confrontational IISs but apply them only very selectively. Their preferred IISs are various forms of engagement. The idea here is to convince portfolio companies to follow the proposed changes and ultimately enthrall them for sustainability improvements. We therefore name this type the ESG evangelist.

5. Discussion and Future Research

The concept of investor impact remains relatively unexplored to date (Kölbel et al. 2020). Our article intends to expand the knowledge in this field by analyzing how investor impact is implemented in the ethical investment policies of socially responsible fund providers. In the first step of our exploratory study, we identify seven IISs and five IOIs and also briefly address the effectiveness of the different IISs in influencing corporate behavior. In a second step, we built on this to create a tripartite typology. Our results suggest that socially responsible fund providers with a stronger impact orientation, such as ESG evangelists, also employ strategies that are more likely to achieve investor impact. In contrast, fund providers with a weaker impact orientation, such as ESG hermits, focus more on purity aspects and therefore tend to utilize strategies that defend the purity claim but also show a weaker investor impact.

We assume that the strong practical differences among socially responsible fund providers are connected to a general moral orientation that is deeply rooted within these organizations. Peifer (2011) distinguishes two opposing poles here. At one extreme, there are those who screen out unethical companies as a preferred means for morally sound investing. This aligns with Max Weber’s historical description of value-rational action, in which “the value for its own sake... regardless of its prospects of success” (Weber [1922] 1978, pp. 24–25) is pursued. At the other extreme are those for whom the preferred means of obtaining a moral portfolio is to own shares in “unethical” companies and then practice shareholder engagement. This corresponds to Weber’s instrumental orientation, in which “the end, the means, and the secondary results are rationally considered” (Weber [1922] 1978, p. 26).

Of course, these two types are not necessary mutually exclusive. Rather, they indicate the spectrum of different impact orientations that exists. Consequently, in our study, we do not find these two Weberian types in pure form. Rather, we observed socially responsible fund providers practicing negative screening only and others that added qualitative screening or shareholder engagement to it.

Recently, the “Theory of Change” has become an important analytical tool in the field of sustainability in general and sustainable investment in particular2. It points “to the construction of a model that specifies the underlying logic, assumptions, influences, causal linkages and expected outcomes of a development program or project. … this model can be tested against the actual process experiences and results attained, by the intervention” (Wendt 2021, p. 4). It is important to emphasize, however, that our types do not claim to already represent such a thoroughly reflected concept. Rather, they are an interim observation that can hopefully be complemented with other evidence to form a fully-fledged ToC explanation that may ultimately serve as a platform for a collective learning process of the various stakeholders.

We also discovered some interesting phenomena with our explorative study, for which a deeper analysis would go beyond the scope of this article. However, we wanted to briefly mention those findings. First, we found that ESG hermits are the least transparent, i.e., they disclose next to no information about their IISs or screens, whereas ESG evangelists are very transparent. An explanation could be that many of the type three fund providers primarily target retail investors and a lack of information discourages those to invest (Gutsche and Zwergel 2016). An alternative explanation would be that they use other distribution channels, e.g., direct sales partner and therefore less efforts are made to make information accessible on the internet. Second, we noticed opposing views towards the use of derivatives and short selling among all three types. Whereas of every type of fund providers some perceive them as evil and unethical, others explicitly use them to short the stocks of those companies that are involved in immoral businesses. Third, despite large difference in the impact orientation, all three types of fund providers practice exclusion. The explanation might be a historical one, as exclusion had played a central role from the very beginning of the SRI history. For example, the Quaker movement avoided doing business with anyone involved in slavery (Kinder and Domini 1997) and the divestment campaign of the 1980 and 1990 fought against the South African apartheid regime (Robinson 2002). Pragmatic reasons may play a role as well: exclusion does simply require less effort than consistently engaging with portfolio companies (Berry and Junkus 2013).

Our results open up many interesting research avenues. A first aspect would be to assess in more detail the effectiveness of the different IISs. In particular, the effects of strategies that aim to influence the cost of capital must be empirically assessed and quantified. For example, studies by Zerbib (2019) and Baker et al. (2018) for the green bond market suggest that these bonds trade at a negative yield premium, whereas Tang and Zhang (2018) find no such evidence. The start of quantitative tapering in the U.S. and the ECB’s planned interest rate hikes could reinforce these effects. Moreover, it might be useful to assess whether and how long divestment campaigns affect stock prices and, more importantly, how much ownership is required here. With the extensive and coordinated divestment efforts against the highly capitalized fossil fuel industry, there would be a perfect example to evaluate this issue. It might also be very interesting to see how the combination of IISs affects the success rate. Dawkins (2018), for example, makes the case that combining engagement strategies with the threat of divestment increases the effectiveness.

There is also a need to develop reliable tools to measure investor impact. For the impact of investments in non-listed firms and specific projects, there are already some metrics standards such as GIIN, IRIS or GIIRS. Those allow investors to quantify or at least qualify their impact. A similar development is necessary for the listed market. Another interesting research topic would be to analyze the financial performance of the products of our three types. Previous research has shown that SRI and non-SRI funds deliver similar returns (see, e.g., Friede et al. 2015). However, the results might be different if we were to compare SRI funds based on our three types of fund providers, as there is evidence that engagement can lead to better performance (Dimson et al. 2015; Busch et al. 2016). The observed equal performance of SRI and non-SRI funds might mask potential performance differences between the products of our three types of fund providers.

In studies examining investors’ expectations of the sustainability impacts of their investment providers, it may be useful to also consider the investment horizon in the study design, as especially retail investors often have a much shorter investment horizon than the time frame required to successfully address structural global problems such as climate change. Another question that could be explored in further studies is how differences in the financial weight of SRI funds affect their ethical investment policies. Whereas it could be argued that smaller funds need to be more innovative to secure market share, larger funds have more resources and more influence.

Furthermore, there are currently many initiatives aimed at establishing common metrics for sustainable value creation, e.g., by the International Organization of Securities Commissions or the World Economic Forum (WEF 2020). All these efforts will make it easier for investors to track the success of their activities. It will therefore be interesting to see whether these developments have an impact on the spread of impact measurement, making it a fundamental part of the ethical investment policy of fund providers. Finally, since this article focused on providers of publicly traded socially responsible funds, it would be interesting to conduct a similar analysis for providers of privately traded funds to enable a comparison of the results.

Due to the sample size and exploratory nature, the results of this study represent only preliminary ideas that need to be confirmed by more and larger samples. However, the ideas we have developed may be worth considering by policy actors, fund providers and investors. Regulators such as the EU Commission might want to start taking into account the impact that an investment generates, not just follow the purity claims that ESG hermits carry before them like a monstrance. The EU taxonomy, which currently leaves out the transformation aspects (Diener and Habisch 2021) and rates companies only according to the status quo, is therefore going in the wrong direction, in our opinion. Our findings may also encourage fund providers who want to make a difference to reconsider their exclusion or best-in-class strategy and turn to methods that are empirically proven to deliver investor impact. Finally, and most importantly, our results should encourage ethical investors, for whom investor impact is more than just empty words, to be pickier when selecting their investment solutions, as customers’ choices determine the success or failure of a product. Worryingly, recent findings by Heeb et al. (2021) show that investors are generally willing to pay more for sustainable investments, but not necessarily for more impact.

In the end, purity and investor impact are opposing concepts. As long as investors, both private and institutional, demand purity-oriented products, they will almost certainly get them. The negative side effect of this demand is that unsustainable assets are transferred into private funds (The Economist 2022) or sold into jurisdictions with, for example, lower environmental standards. In this way, pure portfolios are created, but they have no real impact on sustainability, and one could even argue that this approach worsens the situation. That way, the hope that SRI will make an effective contribution to overcoming contemporary sustainability challenges will remain an illusion for the foreseeable future. It will be interesting to see which concept will prevail.

Author Contributions

Conceptualization, J.D. and A.H.; methodology, J.D.; software, J.D.; validation, J.D. and A.H.; formal analysis, J.D.; investigation, J.D.; resources J.D.; data curation, J.D.; writing—original draft preparation, J.D.; writing—review and editing, J.D. and A.H.; visualization, J.D.; supervision, A.H.; project administration, J.D.; funding acquisition, J.D. and A.H. All authors have read and agreed to the published version of the manuscript.

Funding

This work was supported by the German Research Foundation (DFG) within the funding programme Open Access Publishing. Joel Diener wishes to express his deepest gratitude to “Stiftung der Deutschen Wirtschaft” for the PhD scholarship he received.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Acknowledgments

We would like to acknowledge two anonymous reviewers for their views and comments.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses or interpretation of data; in the writing of the manuscript, or in the decision to publish the results.

| 1 | There is an ongoing discussion about the ambiguity associated with rating a firm’s impact; see for example Li and Polychronopoulos (2020) or Fish et al. (2019). |

| 2 |

References

- Bailey, Kenneth D. 1972. Polythetic Reduction of Monothetic Property Space. Sociological Methodology 4: 83–111. [Google Scholar] [CrossRef]

- Baker, Malcolm P., Daniel B. Bergstresser, George Serafeim, and Jeffrey A. Wurgler. 2018. Financing the Response to Climate Change: The Pricing and Ownership of U.S. Green Bonds (Working Paper No. 2514). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Barber, Brad M., Adair Morse, and Ayako Yasuda. 2021. Impact investing. Journal of Financial Economics 139: 162–85. [Google Scholar] [CrossRef]

- Barko, Tamas, Martijn Cremers, and Luc Renneboog. 2017. Shareholder Engagement on Environmental, Social, and Governance Performance. Journal of Business Ethics forthcoming forthcoming. [Google Scholar] [CrossRef]

- Bauer, Rob, Ruof Tobias, and Smeets Paul. 2019. Get Real! Individuals Prefer More Sustainable Investments. Working Paper; SSRN. Available online: https://papers.ssrn.com/abstract=3287430 (accessed on 5 March 2022).

- Berry, Thomas C., and Joan C. Junkus. 2013. Socially Responsible Investing: An Investor Perspective. Journal of Business Ethics 112: 707–20. [Google Scholar] [CrossRef]

- Brest, Paul, and Kelly Born. 2013. Unpacking the impact in impact investing. Stanford Social Innovation Review 11: 22–31. [Google Scholar]

- Brest, Paul, Ronald J. Gilson, and Mark A. Wolfson. 2018. How Investors Can (and Can’t) Create Social Value. Amsterdam: Elsevier. [Google Scholar] [CrossRef]

- Busch, Timo, Bauer Rob, and Orlitzky Marc. 2016. Sustainable Development and Financial Markets: Old Paths and New Avenues. Business & Society 55: 303–29. [Google Scholar] [CrossRef]

- Busch, Timo, Bruce-Clark Peter, Derwall Jeroen, Eccles Robert, Hebb Tessa, Hoepner Andreas, Klein Christian, Krueger Philipp, Paetzold Falko, Scholtens Bert, and et al. 2021. Impact investments: A call for (re)orientation. SN Business and Economics 1: 33. [Google Scholar] [CrossRef]

- Campbell, John L., Quincy Charles, Osserman Jordan, and Pedersen Ove K. 2013. Coding in-depth semistructured interviews: Problems of unitization and intercoder reliability and agreement. Sociological Methods & Research 42: 294–320. [Google Scholar] [CrossRef]

- Chen, Tao, Dong Hui, and Lin Chen. 2020. Institutional shareholders and corporate social responsibility. Journal of Financial Economics 135: 483–504. [Google Scholar] [CrossRef]

- Cialdini, Robert B., and Melanie R. Trost. 1998. Social influence: Social norms, conformity and compliance. In The Handbook of Social Psychology, 4th ed. Edited by Daniel T. Gilbert, Susan T. Fiske and Gardner Lindzey. New York City: McGraw-Hill, pp. 151–92. [Google Scholar]

- Clementino, Ester, and Richard Perkins. 2020. How do companies respond to environmental, social and governance (ESG) ratings? Evidence from Italy. Journal of Business Ethics 171: 379–97. [Google Scholar] [CrossRef]

- Dawkins, Cedric E. 2018. Elevating the role of divestment in socially responsible investing. Journal of Business Ethics 153: 465–78. [Google Scholar] [CrossRef]

- DellaVigna, Stefano, John A. List, and Ulrike Malmendier. 2012. Testing for altruism and social pressure in charitable giving. Quarterly Journal of Economics 127: 1–56. [Google Scholar] [CrossRef] [PubMed]

- Derwall, Jeroen, Koedijk Kees, and Ter Horst Jenke. 2011. A tale of values-driven and profit-seeking social investors. Journal of Banking and Finance 35: 2137–47. [Google Scholar] [CrossRef]

- Diener, Joel, and André Habisch. 2021. A plea for a stronger role of non-financial impact in the socially responsible investment discourse. Corporate Governance 21: 294–306. [Google Scholar] [CrossRef]

- Dillenburg, Stephen J., Greene Timothy, and Erekson Homer. 2003. Approaching socially responsible investment with a comprehensive ratings scheme: Total social impact. Journal of Business Ethics 43: 167–77. [Google Scholar] [CrossRef]

- Dimson, Elroy, Karakaş Oğuzhan, and Li Xi. 2015. Active ownership. Review of Financial Studies 28: 3225–326. [Google Scholar] [CrossRef]

- Dimson, Elroy, Karakaş Oğuzhan, and Li Xi. 2018. Coordinated Engagements. Available online: https://papers.ssrn.com/abstract=3209072 (accessed on 17 April 2022).

- Dimson, Elroy, Kreutzer Idar, Lake Rob, Sjo Hege, and Starks Laura. 2013. Responsible Investment and the Norwegian Government Pension Fund Global. Oslo: Norwegian Ministry of Finance. [Google Scholar]

- Dyck, Alexander, Lins Karl, Roth Lukas, and Hannes F. Wagner. 2019. Do institutional investors drive corporate social resposnbility? International evidence. Journal of Financial Economics 131: 693–714. [Google Scholar] [CrossRef]

- European Commission. 2018. Action Plan: Financing Sustainable Growth. COM/2018/097 final. Brussels: European Commission. [Google Scholar]

- European Commission. 2021. Study on Sustainability-Related Ratings, Data and Research: Executive Summary. Directorate-General for Financial Stability, Financial Services and Capital Markets Union, Publications Office. Available online: https://data.europa.eu/doi/10.2874/52845 (accessed on 7 December 2021).

- European Parliament. 2020. Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the Establishment of a Framework to Facilitate Sustainable Investment, and Amending Regulation (EU) 2019/2088. Brussels: Official Journal of the European Union L 198/13. [Google Scholar]

- Eurosif. 2018. European SRI Study 2018. Brussels: European Sustainable Investment Forum. [Google Scholar]

- Fish, Alexander, Dong Hyun Kim, and Shankar Venkatraman. 2019. The ESG Sacrifice. Working Paper. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3488475 (accessed on 12 April 2022).

- Friede, Gunnar, Busch Timo, and Bassen Alexander. 2015. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. Journal of Sustainable Finance and Investment 5: 10–233. [Google Scholar] [CrossRef]

- GAO. 2010. United States Government Accountability Office: Testimony Before the Subcommittee on International Monetary Policy and Trade on Sudan Divestment. Available online: https://www.gao.gov/assets/gao-11-245t.pdf (accessed on 2 February 2022).

- Gifford, E. James M. 2010. Effective Shareholder Engagement: The Factors that Contribute to Shareholder Salience. Journal of Business Ethics 92: 79–97. [Google Scholar] [CrossRef]

- Global Sustainable Investment Alliance (GSIA). 2020. GLOBAL SUSTAINABLE INVESTMENT REVIEW 2020. Available online: http://www.gsi-alliance.org/wp-content/uploads/2021/08/GSIR-20201.pdf (accessed on 20 November 2021).

- Goodman, Jennifer, Louche Céline, Katinka C. van Cranenburgh, and Daniel Arenas. 2014. Social Shareholder Engagement: The Dynamics of Voice and Exit. Journal of Business Ethics 125: 193–210. [Google Scholar] [CrossRef]

- Gutsche, Gunnar, and Bernhard Zwergel. 2016. Information barriers and SRI market participation–Can sustainability and transparency labels help? In MAGKS Discussion Paper No. 24. Marburg: School of Business and Economics, Philipps-University Marburg. [Google Scholar]

- Häßler, Rolf D., and Ines Markmiller. 2013. Der Einfluss nachhaltiger Kapitalanlagen auf Unternehmen. München: Oekom Research. [Google Scholar]

- Heeb, Florian, Kölbel Julian, Paetzold Falko, and Zeisberger Stefan. 2021. Do Investors Care About Impact? Available online: https://ssrn.com/abstract=3765659 (accessed on 22 January 2022).

- Hiller, Jennifer, and Svea Herbst-Bayliss. 2021. Engine No. 1 Extends Gains with a Third Seat on Exxon Board. London: Reuters. [Google Scholar]

- Hoepner, Andreas, Laura T. Starks, Sautner Zacharias, Zhou Xiao, and Oikonomou Ioannis. 2022. ESG Shareholder Engagement and Downside Risk. AFA 2018 paper, European Corporate Governance Institute–Finance Working Paper No. 671/2020. Brussels: European Corporate Governance Institute. [Google Scholar]

- Husson-Traore, Anne-Catherine, and Sarah Meller. 2013. Controversial Companies: Do Investor Blacklist Make A Difference? Paris: Novethic. [Google Scholar]

- Kinder, Peter D., and Amy L. Domini. 1997. Social Screening: Paradigms Old and New. The Journal of Investing 6: 12–19. [Google Scholar] [CrossRef]

- King, Brayden G., and Sarah A. Soule. 2007. Social movements as extra-institutional entrepreneurs: The effect of protests on stock price returns. Administrative Science Quarterly 52: 413–42. [Google Scholar] [CrossRef]

- Kolbe, Richard H., and Melissa S. Burnett. 1991. Content-analysis research: An examination of applications with directives for improving research reliability and objectivity. Journal of Consumer Research 18: 243–50. [Google Scholar] [CrossRef]

- Kölbel, Julian F., Heeb Florian, Paetzold Falko, and Busch Timo. 2020. Can Sustainable Investing Save the World? Reviewing the Mechanisms of Investor Impact. Organization and Environment 33: 554–74. [Google Scholar] [CrossRef]

- Kuckartz, Udo. 2016. Qualitative Inhaltsanalyse. In Methoden, Praxis, Computerunterstützung. 3., überarbeitete Auflage. Weinheim: Beltz Juventa. [Google Scholar]

- Kuckartz, Udo. 2022. Qualitative Inhaltsanalyse. In Methoden, Praxis, Computerunterstützung. 5., überarbeitete Auflage. Weinheim: Beltz Juventa. [Google Scholar]

- Landier, Augustin, and Stefano Lovo. 2020. ESG Investing: How to Optimize Impact? In HEC Paris Research Paper No. FIN-2020-1363. Available online: http://0-dx-doi-org.brum.beds.ac.uk/10.2139/ssrn.3508938 (accessed on 28 March 2022).

- Landis, J. Richard, and Gary G. Koch. 1977. The measurement of observer agreement for categorical data. Biometrics 33: 159–74. [Google Scholar] [CrossRef] [PubMed]

- Lee, Darren D., Jacquelyn E. Humphrey, Karen L. Benson, and Jason Y. K. Ahn. 2010. Socially responsible investment fund performance the impact of screening intensity. Accounting and Finance 50: 351–70. [Google Scholar] [CrossRef]

- Li, Feifei, and Ari Polychronopoulos. 2020. What a Difference an ESG Ratings Provider Makes. Newport Beach: Research Affiliates Publication. [Google Scholar]

- Louche, Céline. 2015. CSR and Shareholders. In Corporate Social Responsibility, 1st ed. Edited by Esben Rahbek and Gjedrum Pedersen. London: Sage Publishing, pp. 205–39. [Google Scholar]

- Luo, Arthur H., and Ronald J. Balvers. 2017. Social screens and systematic investor boycott risk. Journal of Financial and Quantitative Analysis 52: 365–99. [Google Scholar] [CrossRef]

- Markman, Gideon D., Theodore L. Waldron, and Andreas Panagopoulos. 2016. Organizational hostility: Why and how nonmarket players compete with firms. Academy of Management Perspectives 30: 74–92. [Google Scholar] [CrossRef]

- Moore, David, Cranston Gemma, Reed Anders, and Galli Alessandro. 2012. Projecting future human demand on the Earth’s regenerative capacity. Ecological Indicators 16: 3–10. [Google Scholar] [CrossRef]

- OECD. 2017. Investment Governance and the Integration of Environmental, Social and Governance Factors. Available online: https://www.oecd.org/finance/Investment-Governance-Integration-ESG-Factors.pdf (accessed on 3 March 2022).

- Pástor, Lubos, Robert F. Stambaugh, and Lucian A. Taylor. 2021. Sustainable investing in equilibrium. Journal of Financial Economics 142: 550–71. [Google Scholar] [CrossRef]

- Peifer, Jared L. 2011. Morality in the financial market? A look at religiously affiliated mutual funds in the USA. Socio-Economic Review 9: 235–59. [Google Scholar] [CrossRef]

- Pérez-Gladish, Blanca, Paz Méndez, and Bouchra M’Zali. 2012. A decision support tool for environmentally conscious investors. Journal of Financial Decision Making 7. [Google Scholar]

- Principles of Responsible Investment (PRI). 2017. Aligning Responsible Investment with the UN Sustainable Development Goals. Available online: https://www.commoninterests.com/wp-content/uploads/2017/07/Aligning-investment-with-the-SDGs.pdf (accessed on 2 September 2021).

- Renneboog, Luc, Ter Horst Jenke, and Zhang Chendi. 2008. Socially responsible investments: Institutional aspects, performance, and investor behavior. Journal of Banking and Finance 32: 1723–42. [Google Scholar] [CrossRef]

- Richardson, Benjamin J. 2009. Climate Finance and its Governance: Moving to a Low Carbon Economy through Socially Responsible Financing? International and Comparative Law Quarterly 58: 597–626. [Google Scholar] [CrossRef]

- Robinson, Lynn D. 2002. Doing Good and Doing Well: Shareholder Activism, Responsible Investment, and Mainline Protestantism. In The Quiet Hand of God: Faith-Based Activism and the Public Role of Mainline Protestantism. Edited by Robert Wuthnow and John H. Evans. Berkeley: University of California Press. [Google Scholar]

- Sandberg, Joakim, and Jonas Nilsson. 2011. Conflicting intuitions about ethical investment: A survey among Individual investors. In Sustainable Investment and Corporate Governance Working Papers. Sustainable Investment Research Platform, SIRP WP 10–16. Sustainable Investment Research Platform. [Google Scholar]

- Schwirplies, Claudia, and Andreas Ziegler. 2016. Offset carbon emissions or pay a price premium for avoiding them? A cross-country analysis of motives for climate protection activities. Applied Economics 48: 746–58. [Google Scholar] [CrossRef]

- Shang, Jen, and Rachel Croson. 2009. A field experiment in charitable contribution: The impact of social information on the voluntary provision of public goods. Economic Journal 119: 1422–39. [Google Scholar] [CrossRef]

- Slager, Rieneke, and Wendy Chapple. 2015. Carrot and stick? The role of financial market intermediaries in corporate social performance. Business and Society 55: 398–426. [Google Scholar] [CrossRef]

- Sorkin, Andrew R. 2015. A new tack in the war on mining mountains. The New York Times, March 9. [Google Scholar]

- Tang, Dragon Yongjun, and Yupu Zhang. 2018. Do Shareholders Benefit from Green Bonds? Working Paper. Available online: https://ssrn.com/abstract=3259555 (accessed on 27 May 2022).

- Teoh, Siew, Welch Ivo, and C. Paul Wazzan. 1999. The effect of socially activist investment policies on the financial markets: Evidence from the South African boycott. Journal of Business 72: 35–89. [Google Scholar] [CrossRef]

- The Economist. 2022. The Truth about Dirty Assets. Available online: https://www.economist.com/leaders/2022/02/12/the-truth-about-dirty-assets (accessed on 21 June 2022).

- The Financial Reporting Council (FRC). 2020. The UK Stewardship Code. Review of Early Reporting. Available online: https://www.frc.org.uk/getattachment/975354b4-6056-43e7-aa1f-c76693e1c686/The-UK-Stewardship-Code-Review-of-Early-Reporting.pdf (accessed on 5 April 2022).

- UN Principles for Responsible Investment (UN PRI). 2018. PRI Brochure. UNEP Finance Initiative and UN Global Compact. Available online: https://www.unpri.org/pri/about-the-pri (accessed on 15 July 2019).

- UN Principles for Responsible Investment (UN PRI). 2020. PRI REPORTING FRAMEWORK Overview and Structure. UNEP Finance Initiative and UN Global Compact. Available online: https://dwtyzx6upklss.cloudfront.net/Uploads/w/h/f/overview_and_guidance_reporting_framework_structure3_584160.pdf (accessed on 21 August 2021).

- UN Principles for Responsible Investment (UN PRI). 2021. PRI Brochure. UNEP Finance Initiative and UN Global Compact. Available online: https://www.unpri.org/download?ac=10948 (accessed on 22 August 2021).

- United Nations General Assembly. 2015. Transforming our World: The 2030 Agenda for Sustainable Development, A/RES/70/1. New York: UN General Assembly. [Google Scholar]

- VERBI Software. 2020. MAXQDA 2022 [Computer Software]; Berlin: VERBI Software. Available online: maxqda.com (accessed on 5 August 2020).

- Waldron, Theodore L., Chad Navis, and Fisher Greg. 2014. Explaining differences in firms’ responses to activism. Academy of Management Review 38: 397–417. [Google Scholar] [CrossRef]

- Waldron, Theodore L., Chad Navis, Olivia Aronson, Jeffrey G. York, and Desiree F. Pacheco. 2019. Values-Based Rivalry: A Theoretical Framework of Rivalry Between Activists and Firms. Academy of Management Review 44: 800–18. [Google Scholar] [CrossRef]

- Waygood, Steve. 2011. How do the capital markets undermine sustainable development? What can be done to correct this? Journal of Sustainable Finance & Investment 1: 81–87. [Google Scholar] [CrossRef]

- Weber, Max. 1978. Economy and Society: An Outline of Interpretive Sociology. Berkeley and Los Angeles: University of California Press. First published 1922. [Google Scholar]

- WEF. 2020. Measuring Stakeholder Capitalism: Towards Common Metrics and Consistent Reporting of Sustainable Value Creation. White Paper. Geneva: WEF. [Google Scholar]

- Wendt, Karen. 2021. Theory of Change: Defining the Research Agenda. In Theories of Change: Change Leadership Tools, Models and Applications for Investing in Sustainable Development. Edited by Karen Wendt. Cham: Springer International Publishing, pp. 383–89. [Google Scholar] [CrossRef]

- Wins, Anett, and Bernhard Zwergel. 2016. Comparing those who do, might and will not invest in sustainable funds: A survey among German retail fund investors. Business Research 9: 51–99. [Google Scholar] [CrossRef]

- WWF, Zoological Society of London, and Global Footprint Network. 2016. Living Planet Report 2016: Risk and Resilience in a New Era. London: World Wide Fund for Nature. [Google Scholar]

- Zerbib, Olivier David. 2019. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. Journal of Banking and Finance 98: 39–60. [Google Scholar] [CrossRef]

Figure 1.

Methodical approach.

{kind=link}

Table 1.

Contrasting the three main types of fund providers.

| ESG Hermits | ESG Ambassadors | ESG Evangelists | |

|---|---|---|---|

| 1. Indicators for Impact Orientation | |||

| Promise | purity | investor impact | investor impact |

| Networks | None | Sustainability networks | Sustainability networks |

| + normative networks | |||

| SDGs as Reference Point | No | Yes | Yes |

| UN PRI Signatory | No | Yes | Yes |

| Impact Monitoring | None | None | yes |

| 2. Investor Impact Strategies | |||

| Exclusion | yes | yes | yes |

| Divestment | divestment as first | divestment as first | first engage, then divest |

| option in controversies | option in controversies | in controversies | |

| Positive Approaches | no | yes | yes |

| ESG Dialogue | no | no | yes |

| ESG Voting and Shareholder Proposals | no | no | yes |

| Collaborative Engagement | no | no | yes |

| Stigmatization | If used, only to confront | None | If used as last step of escalation in |

| and pressure | engagement strategy |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Diener, J.; Habisch, A. Developing an Impact-Focused Typology of Socially Responsible Fund Providers. J. Risk Financial Manag. 2022, 15, 298. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15070298

AMA Style