The Impact of Organizational Culture on the Effectiveness of Corporate Governance to Control Earnings Management

, , and

, , and

Abstract

:1. Introduction

2. Literature Review

3. Sample

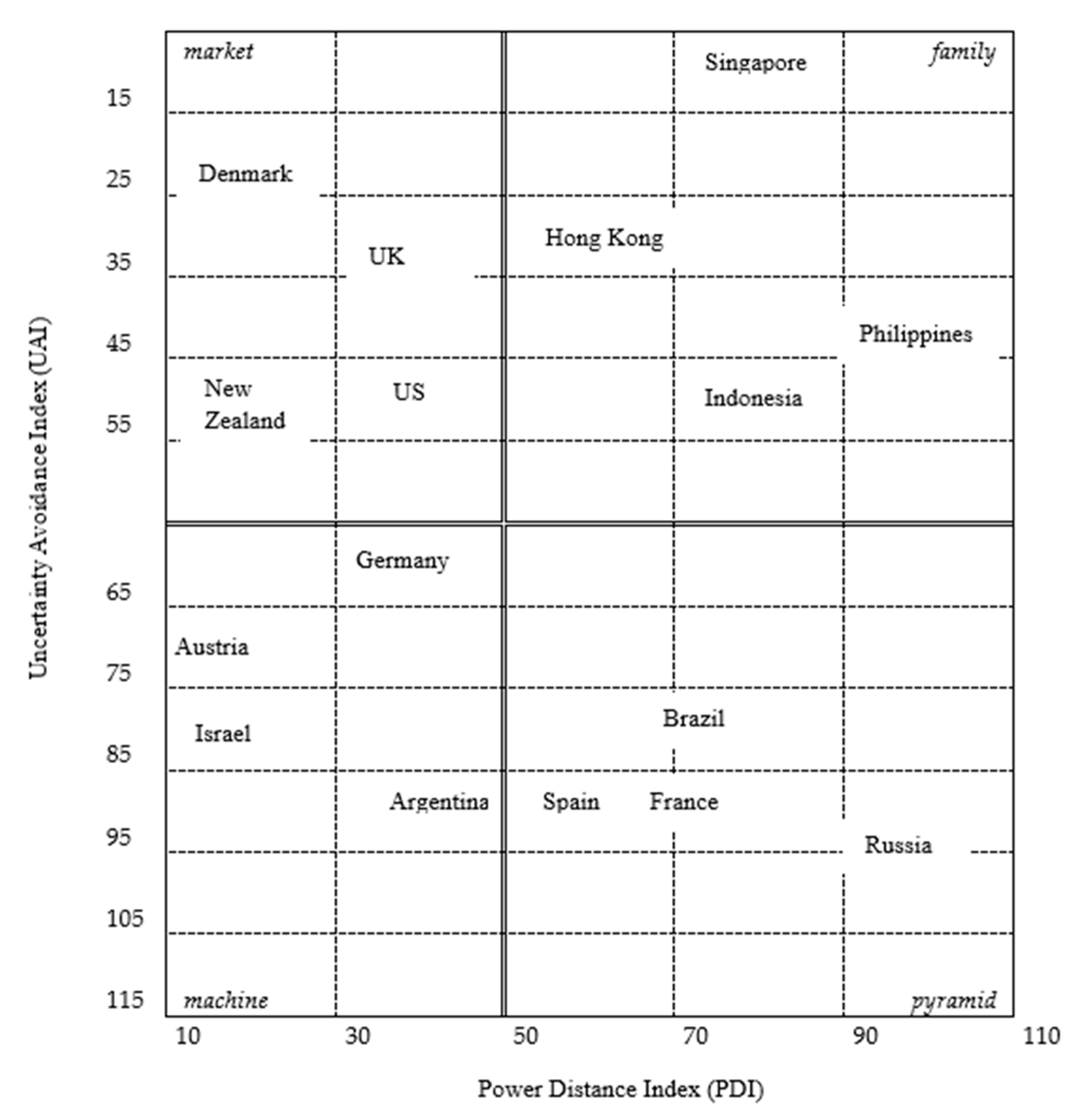

Power Distance Index (PDI)

4. Methods

5. Results and Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Country | N | Minimum | Maximum | Mean | St. Deviation |

|---|---|---|---|---|---|

| Argentina | |||||

| LIQ | 62 | 0.036108 | 3.241274 | 1.329583 | 0.594736 |

| DEBT | 58 | 0.024524 | 5.577501 | 1.678241 | 1.236976 |

| ROI | 54 | −0.172610 | 0.183759 | 0.048006 | 0.081617 |

| ASSET | 65 | 112.30 | 26,182,778.70 | 1,428,041.43 | 3,887,832.84 |

| Austria | |||||

| LIQ | 41 | 0.487176 | 3.673633 | 1.481904 | 0.735024 |

| DEBT | 48 | 0.000238 | 4.121267 | 1.398500 | 0.874428 |

| ROI | 49 | −0.097866 | 0.108038 | 0.040424 | 0.040772 |

| ASSET | 51 | 6024.03 | 41,436,809.20 | 3,284,541.74 | 6,657,676.78 |

| Brazil | |||||

| LIQ | 223 | 0.000210 | 3.941638 | 1.525006 | 0.859427 |

| DEBT | 196 | 0.053363 | 5.636541 | 1.644527 | 1.344929 |

| ROI | 236 | −0.169274 | 0.198038 | 0.037024 | 0.078451 |

| ASSET | 247 | 108.47 | 46,619,535.46 | 2,978,728.14 | 5,964,100.76 |

| Denmark | |||||

| LIQ | 87 | 0.000000 | 4.000000 | 1.449812 | 0.858622 |

| DEBT | 103 | 0.007510 | 4.246780 | 1.048369 | 0.821086 |

| ROI | 91 | −0.165393 | 0.197515 | 0.051404 | 0.073359 |

| ASSET | 111 | 469.20 | 56,275,133.78 | 2,552,901.94 | 8,325,196.84 |

| France | |||||

| LIQ | 521 | 0.000000 | 4.146832 | 1.610837 | 0.785762 |

| DEBT | 540 | 0.000000 | 5.404494 | 1.524987 | 1.170935 |

| ROI | 504 | −0.185563 | 0.192030 | 0.027095 | 0.068797 |

| ASSET | 582 | 299.89 | 69,724,453.60 | 3,434,927.76 | 9,734,571.06 |

| Germany | |||||

| LIQ | 374 | 0.000000 | 4.465187 | 1.759668 | 0.917197 |

| DEBT | 416 | 0.019328 | 5.423699 | 1.353105 | 1.029270 |

| ROI | 403 | −0.163560 | 0.199635 | 0.036817 | 0.065535 |

| ASSET | 441 | 338.01 | 74,429,143.40 | 3,681,025.27 | 10,298,925.20 |

| Hong Kong | |||||

| LIQ | 1614 | 0.000000 | 4.865038 | 1.815782 | 1.025857 |

| DEBT | 1770 | 0.004604 | 5.029085 | 1.003740 | 0.986760 |

| ROI | 1737 | −0.196923 | 0.199044 | 0.025673 | 0.076096 |

| ASSET | 1926 | 215.30 | 80,779,548.73 | 1,982,741.39 | 6,390,365.37 |

| Indonesia | |||||

| LIQ | 440 | 0.000160 | 4.559739 | 1.555239 | 1.011302 |

| DEBT | 475 | 0.002521 | 5.305388 | 1.118221 | 1.008536 |

| ROI | 485 | −0.146024 | 0.181770 | 0.045313 | 0.060192 |

| ASSET | 520 | 119.24 | 23,678,859.53 | 636,240.21 | 1,662,465.92 |

| Israel | |||||

| LIQ | 240 | 0.000000 | 4.638840 | 1.682505 | 0.948095 |

| DEBT | 302 | 0.000571 | 6.753144 | 1.655376 | 1.404634 |

| ROI | 75 | −0.148082 | 0.199649 | 0.056216 | 0.084741 |

| ASSET | 229 | 117.99 | 10,253,377.93 | 286,447.73 | 1,092,101.74 |

| New Zealand | |||||

| LIQ | 86 | 0.017737 | 4.578288 | 1.445028 | 0.925851 |

| DEBT | 98 | 0.014684 | 3.819961 | 0.884742 | 0.698235 |

| ROI | 85 | −0.148597 | 0.163685 | 0.048834 | 0.065393 |

| ASSET | 104 | 262.71 | 11,712,560.80 | 915,036.52 | 1,710,211.67 |

| Philippines | |||||

| LIQ | 171 | 0.000000 | 4.682074 | 1.631291 | 1.097005 |

| DEBT | 189 | 0.000336 | 4.051145 | 0.970963 | 0.889239 |

| ROI | 205 | −0.133340 | 0.194492 | 0.030717 | 0.060335 |

| ASSET | 213 | 119.56 | 33,743,409.52 | 1,648,782.37 | 4,408,567.40 |

| Russia | |||||

| LIQ | 145 | 0.082849 | 3.771505 | 1.234947 | 0.707970 |

| DEBT | 119 | 0.000962 | 6.191603 | 1.551234 | 1.532212 |

| ROI | 144 | −0.159495 | 0.196888 | 0.047040 | 0.075180 |

| ASSET | 166 | 1608.53 | 73,544,712.37 | 3,122,642.63 | 8,120,882.68 |

| Singapore | |||||

| LIQ | 350 | 0.000000 | 4.869171 | 1.829030 | 1.127291 |

| DEBT | 386 | 0.008375 | 3.930476 | 0.933673 | 0.792831 |

| ROI | 383 | −0.160139 | 0.195037 | 0.021914 | 0.056903 |

| ASSET | 422 | 159.07 | 76,795,732.47 | 1,913,751.25 | 6,510,460.00 |

| Spain | |||||

| LIQ | 123 | 0.405191 | 3.631303 | 1.443715 | 0.765132 |

| DEBT | 152 | 0.014358 | 6.093629 | 1.640159 | 1.423719 |

| ROI | 164 | −0.172317 | 0.176933 | 0.023693 | 0.061967 |

| ASSET | 178 | 2880.96 | 65,112,860.20 | 3,196,049.10 | 8,204,187.49 |

| United Kingdom | |||||

| LIQ | 913 | 0.000000 | 4.679141 | 1.606375 | 0.989184 |

| DEBT | 993 | 0.001134 | 4.909624 | 0.942690 | 0.971165 |

| ROI | 874 | −0.198843 | 0.197871 | 0.035317 | 0.086542 |

| ASSET | 1090 | 125.04 | 74,941,262.40 | 1,800,685.761,800,685.76 | 6,711,569.39 |

| United States | |||||

| LIQ | 1176 | 0.000000 | 4.562160 | 1.677097 | 0.882393 |

| DEBT | 1221 | 0.000000 | 6.159712 | 1.688828 | 1.272706 |

| ROI | 1294 | −0.120842 | 0.196867 | 0.063278 | 0.057070 |

| ASSET | 1399 | 110.00 | 80,549,000.00 | 7,536,909.64 | 12,180,106.81 |

| Total Sample | |||||

| LIQ | 6566 | 0.000000 | 4.869171 | 1.669884 | 0.960132 |

| DEBT | 7066 | 0.000000 | 6.753144 | 1.252692 | 1.137450 |

| ROI | 6783 | −0.198843 | 0.199649 | 0.038260 | 0.071556 |

| ASSET | 7744 | 108.47 | 80,779,548.73 | 3,094,962.64 | 8,365,296.53 |

| 1 | The range of values for PDI in Hofstede et al. (2010) are between 10 and 110 and for UAI the values are between 5 and 115. |

| 2 | Data are extracted from Eikon database by Thomson Reuters. |

| 3 | The concepts of discretionary and non-discretionary accruals are explained by Dechow et al. (2010), Francis et al. (2004) and Kothari et al. (2005), among others. |

| 4 | Different models have been used in the literature to estimate non-discretionary accruals. A comprehensive overview of these models is presented by Callao et al. (2014). |

| 5 | For this regression, data were extracted from Eikon. |

| 6 | We take the value 63 as a reference based on Hofstede et al. (2010). |

| 7 | We take the value 50 as a reference based on Hofstede et al. (2010). |

| 8 | Shi et al. (2022), although in relation to CSR, show the influence of UAI on the negative relationship between CSR and earnings management. This negative association is higher in high uncertainty avoidance cultures. |

References

- Ball, Ray, and Lakshmanan Shivakumar. 2005. Earnings quality in UK private firms: Comparative loss recognition timeliness. Journal of Accounting and Economics 39: 83–128. [Google Scholar] [CrossRef]

- Barton, Jan, and Paul J. Simko. 2002. The balance sheet as an earnings management constraint. The Accounting Review 77: 1–27. [Google Scholar] [CrossRef]

- Bonetti, Pietro, Michel L. Magnan, and Antonio Perbonetti. 2016. The Influence of Country- and Firm-Level Governance on Financial Reporting Quality: Revisiting the Evidence. Journal of Business Finance & Accounting 43: 1059–94. [Google Scholar]

- Breuer, Wolfgang, and Astrid J. Salzmann. 2012. National culture and corporate governance. In Corporate Governance. Berlin and Heidelberg: Springer, pp. 369–97. [Google Scholar]

- Burgstahler, David, and Ilia Dichev. 1997. Earnings Management to Avoid Earnings Decreases and Losses. Journal of Accounting and Economics 24: 99–126. [Google Scholar] [CrossRef]

- Callao, Susana, José I. Jarne, and David Wroblewski. 2014. The development of earnings management research. Review of literature from three different perspectives. Theoretical Journal of Accounting 79: 135–77. [Google Scholar] [CrossRef]

- Cameran, Mara, Peiwei Lyu, and Pietro Perotti. 2022. The Consequences of Audit Partner Narcissism: Evidence from the UK Market. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4109142 (accessed on 1 May 2022).

- Charitou, Melita, Petros Lois, and Halim B. Santoso. 2012. The Relationship Between Working Capital Management and Firms Profitability: An Empirical Investigation for an Emerging Asian Country. International Business and Economics Research Journal 11: 839–47. [Google Scholar] [CrossRef]

- Chen, Chu, Giorgio Gotti, Tony Kang, and Michael C. Wolfe. 2018. Corporate Codes of Ethics, Culture, and Earnings Discretion: International Evidence. Journal of Business Ethics 151: 141–63. [Google Scholar] [CrossRef]

- Chih, Hsiang-Lin, Chung-Hua Shen, and Feng-Ching Kang. 2007. Corporate Social Responsibility, Investor Protection, and Earnings Management: Some International Evidence. Journal of Business Ethics 79: 179–98. [Google Scholar] [CrossRef]

- Choi, Daeheon, Chune Y. Chung, Young-Eun Kim, Y. J. Kim, and Paul M. S. Choi. 2020. Sustainable Corporate Ownership Structures and Earnings Management in the Vietnamese Stock Market. Sustainability 12: 6089. [Google Scholar] [CrossRef]

- Cornett, Marcia M., Jamie J. McNutt, and Hassan Tehranian. 2009. Corporate governance and earnings management at large US bank holding companies. Journal of Corporate Finance 15: 412–30. [Google Scholar] [CrossRef]

- Dechow, Patricia, and Richard Sloan. 1991. Executive incentives and the horizon problem: An empirical investigation. Journal of Accounting and Economics 14: 51–89. [Google Scholar] [CrossRef]

- Dechow, Patricia, Weili Ge, and Catherine Schrand. 2010. Understanding earnings quality: A review of the proxies, their determinants and their consequences. Journal of Accounting and Economics 50: 344–401. [Google Scholar] [CrossRef]

- Defond, Mark, and James Jiambalvo. 1994. Debt covenant violation and manipulation of accruals. Journal of Accounting and Economics 17: 145–76. [Google Scholar] [CrossRef]

- Desender, Kurt, Christian Castro, and Sergio De León. 2011. Earnings Management and Cultural Values. American Journal of Economics and Sociology 70: 639–70. Available online: http://0-www-jstor-org.brum.beds.ac.uk/stable/41329204 (accessed on 28 August 2020). [CrossRef]

- Doupnik, Timothy S. 2008. Influence of Culture on Earnings Management: A Note. Abacus 44: 317–40. [Google Scholar] [CrossRef]

- Duong, Hong K., Helen Kang, and Stephen B. Salter. 2016. Culture and corporate governance. Journal of International Accounting Research 15: 67–96. [Google Scholar] [CrossRef]

- Elias, Rafik. 2004. The impact of corporate ethical values on perceptions of earnings management. Managerial Auditing Journal 19: 84–98. [Google Scholar] [CrossRef]

- Francis, Jennifer, Ryan LaFond, Per M. Olsson, and Katherine Schipper. 2004. Costs of Equity and Earnings Attributes. The Accounting Review 79: 967–1010. [Google Scholar] [CrossRef]

- García Osma, Beatriz, and Belén Gill de Albornoz Nouger. 2005. El Gobierno Corporativo y las Prácticas de Earnings Management: Evidencia Empírica en España. Valencia: Instituto Valenciano de Investigaciones Económicas, vol. 11, pp. 1–46. [Google Scholar]

- García Osma, Beatriz, Belén Gill de Albornoz Nouger, and Ana Gisbert Clemente. 2005. La investigación sobre earnings managements. Spanish Journal of Finance and Accounting 34: 1001–33. [Google Scholar]

- Geiger, Marshall, and Joyce van der Laan Smith. 2010. The Effect of Institutional and Cultural Factors on the Perceptions of Earnings Management. Journal of International Accounting Research 9: 21–43. [Google Scholar] [CrossRef]

- Geiger, Marshall, Brendan O’Connell, Paul Clikeman, Elena Ochoa, Kristen Witkowski, and Ilias Basioudis. 2006. Perceptions of earnings management: The effects of national cultura. Advances in International Accounting 19: 175–99. [Google Scholar] [CrossRef]

- Gray, S. J. 1988. Towards a theory of cultural influence on the development of accounting systems internationally. Abacus 24: 1–15. [Google Scholar] [CrossRef]

- Guan, Liming, Hamid Pourjalali, Partha Sengupta, and Jenny Teruya. 2005. Effect of cultural environment on earnings manipulation: A five Asia—Pacific country analysis. Multinational Business Review 13: 23–41. [Google Scholar] [CrossRef]

- Han, Sam, Tony Kang, Stephen Salter, and Yong Keun Yoo. 2010. A cross-country study on the effects of national culture on earnings management. Journal of International Business Studies 41: 123–41. [Google Scholar] [CrossRef]

- Hassan, M. Kabir, and Md. Sydul Karim. 2022. Corporate Culture and Inventory Behavior (May 15). Available online: https://ssrn.com/abstract=4110229 (accessed on 28 August 2020). [CrossRef]

- Healy, Paul, and James M. Wahlen. 1999. A Review of the Earnings Management Literature and its Implications for Standard Setting. Accounting Horizons 13: 365–83. [Google Scholar] [CrossRef]

- Hofstede, Geert. 1980. Culture’s Consequences: International Differences in Work-Related Values. Beverly Hills: Sage. [Google Scholar]

- Hofstede, Geert, Gert J. Hofstede, and Michael Minkov. 2010. Cultures and Organizations: Software of the Mind Intercultural Cooperation and Its Importance for Survival. New York: McGraw Hill. [Google Scholar]

- Holthausen, Robert, David F. Larcker, and Richard G. Sloan. 1995. Annual bonus schemes and the manipulation of earnings. Journal of Accounting and Economics 19: 29–74. [Google Scholar] [CrossRef]

- Iatridis, George, and George Kadorinis. 2009. Earnings management and firm financial motives: A financial investigation of UK listed firms. International Review of Financial Analysis 4: 164–73. [Google Scholar] [CrossRef]

- Jaggi, Bikki, and Judy Tsui. 2007. Insider trading, earnings management and corporate governance: Empirical evidence based on Hong Kong firms. Journal of International Financial Management and Accounting 18: 192–222. [Google Scholar] [CrossRef]

- Jaggi, Bikki, and Picheng Lee. 2002. Earnings management in response to debt covenant violations and debt restructuring. Journal of Accounting, Auditing and Finance 17: 295–324. [Google Scholar] [CrossRef]

- Kanagaretnam, Kiridaran, Chee Y. Lim, and Gerald Lobo. 2011. Effects of national culture on earnings quality of Banks. Journal of International Business Studies 42: 853–74. [Google Scholar] [CrossRef]

- Kasznik, Ron. 1999. On the association between voluntary disclosure and earnings management. Journal of Accounting Research 37: 57–81. [Google Scholar] [CrossRef]

- Katmon, Nooraisah, and Omar Al Farooque. 2017. Exploring the Impact of Internal Corporate Governance on the Relation between Disclosure Quality and Earnings Management in the UK Listed Companies. Journal of Business Ethics 142: 345–67. [Google Scholar] [CrossRef]

- Khuong, Nguyen V., Le H. T. Anh, and Nguyen T. H. Van. 2022. Firm life cycle and earnings management: The moderating role of state ownership. Cogent Economics & Finance 10: 2085260. [Google Scholar] [CrossRef]

- Kim, Yangseon, Caixing Liu, and S. Ghon Rhee. 2003. The Relation of Earnings Management to Firm Size. Working Paper. Honolulu: University of Hawaii, pp. 1–31. [Google Scholar]

- Kjærland, Frode, Ane T. Haugdal, Anna Søndergaard, and Anne Vågslid. 2020. Corporate Governance and Earnings Management in a Nordic Perspective: Evidence from the Oslo Stock Exchange. Journal of Risk and Financial Management 13: 256. [Google Scholar] [CrossRef]

- Klein, April. 2002. Audit committee, board of director characteristics and earnings management. Journal of Accounting and Economics 33: 375–400. [Google Scholar] [CrossRef]

- Kneiding, Christoph, and Alexander S. Kritikos. 2007. Microfinance in Eastern and Western Europe: A Comparative Analysis. GfA Discussion Paper No. 09/2007. Berlin: Gesellschaft fur Arbeitsmarktaktivierung, pp. 1–18. [Google Scholar]

- Kothari, S.P., Andrew J. Leone, and Charles E. Wasley. 2005. Performance matched discretionary accrual measures. Journal of Accounting and Economics 39: 163–97. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florencio Lopez-de-Silanes, and Andrei Shleifer. 1999. Corporate ownership around the world. The Journal of Finance 54: 471–517. [Google Scholar] [CrossRef]

- Larcker, David F., and Scott A. Richardson. 2004. Fees paid to audit firms, accrual choices, and corporate governance. Journal of Accounting Research 42: 625–58. [Google Scholar] [CrossRef]

- Li, Jiatao, and J. Richard Harrison. 2008. Corporate governance and national culture: A multi-country study. Corporate Governance 8: 607–21. [Google Scholar] [CrossRef]

- Li, Kai, Feng Mai, Rui Shen, and Xinyan Yan. 2020. Measuring Corporate Culture Using Machine Learning. Review of Financial Studies 34: 3265–315. [Google Scholar] [CrossRef]

- Licht, Amir, Chanan Goldschmidt, and Shalom H. Schwartz. 2005. Culture, law, and corporate governance. International Review of Law and Economics 25: 229–55. [Google Scholar] [CrossRef]

- Llukani, Teuta. 2013. Earnings management and firm size: An empirical analyze in Albanian market. European Scientific Journal 9: 135–43. [Google Scholar]

- McNichols, Maureen F. 2000. Research design issues in earnings management studies. Journal of Accounting and Public Policy 19: 313–45. [Google Scholar] [CrossRef]

- Monterrey Majoral, Juan. 2004. Información contable y gobierno corporativo. Revista de Contabilidad 7: 89–122. [Google Scholar]

- Nia, Nia M., Nila F. Nuzula, and Caci R. Damayanti. 2022. Corporate governance and socially responsible on accounting conservatism and earnings management in indonesia’s soe enterprises. Profit: Jurnal Administrasi Bisnis 16: 216–29. [Google Scholar]

- Riahinejad, Mohaddeseh, and Afsaneh Tavangar. 2022. The Effect of Organizational Culture on the Relationship between Earnings Management and the Readability of Financial Statements. The Financial Accounting and Auditing Researches 13: 87–114. Available online: https://www.sid.ir/en/journal/ViewPaper.aspx?id=896009 (accessed on 28 August 2020).

- Rosner, Rebecca L. 2003. Earnings manipulation in failing firms. Contemporary Accounting Research 2: 361–408. [Google Scholar] [CrossRef]

- Shan, Yuan G. 2015. Value relevance, earnings management and corporate governance in China. Emerging Markets Review 23: 186–207. [Google Scholar] [CrossRef]

- Shen, Chung-Hua, and Hsiang-Lin Chih. 2005. Investor protection, prospect theory, and earnings management: An international comparison of the banking industry. Journal of Banking and Finance 29: 2675–97. [Google Scholar] [CrossRef]

- Shen, Chung-Hua, and Hsiang-Lin Chih. 2007. Earnings management and corporate governance in Asia’s emerging markets. Corporate Governance: An International Review 15: 999–1021. [Google Scholar] [CrossRef]

- Shi, Hao, Haijian Liu, and Yixue Wu. 2022. Are socially responsible firms responsible to accounting? A meta-analysis of the relationship between corporate social responsibility and earnings management. Journal of Financial Reporting and Accounting. ahead-of-print. [Google Scholar] [CrossRef]

- Shleifer, Andrei, and Robert W. Vishny. 1997. A survey of corporate governance. The Journal of Finance 52: 737–83. [Google Scholar] [CrossRef]

- Swastika, Dwi L.T. 2013. Corporate Governance, Firm Size, and Earnings management: Evidente in Indonesia stock exchange. Journal of Business and Management 10: 77–82. [Google Scholar]

- Sweeney, Amy P. 1994. Debt covenant violations and managers’ accounting responses. Journal of Accounting and Economics 17: 281–308. [Google Scholar] [CrossRef]

- Teoh, Siew H., Ivo Welch, and T.J. Wong. 1998. Earnings management and the underperformance of seasoned equity offerings. Journal of Financial Economics 50: 63–99. [Google Scholar] [CrossRef]

- Xie, Biao, Wallace N. Davidson III, and Peter J. DaDalt. 2003. Earnings management and corporate governance: The role of the board and the audit committee. Journal of Corporate Finance 9: 295–316. [Google Scholar] [CrossRef]

- Zhang, Xu, Xing Liang, and Hongyan Sun. 2013. Individualism–Collectivism, Private Benefits of Control, and Earnings Management: A Cross-Culture Comparison. Journal of Business Ethics 114: 655–64. [Google Scholar] [CrossRef]

| Countries in the Study by Organizational Model Hofstede et al. (2010) | Firms in the Sample | Observations 2009–2018 |

|---|---|---|

| PYRAMID | 1273 | 12,730 |

| Brazil | 252 | 2520 |

| France | 648 | 6480 |

| Russia | 181 | 1810 |

| Spain | 192 | 1920 |

| MACHINE | 946 | 9460 |

| Argentina | 67 | 670 |

| Austria | 54 | 540 |

| Germany | 493 | 4930 |

| Israel | 332 | 3320 |

| MARKET | 2759 | 27,590 |

| Denmark | 113 | 1130 |

| New Zealand | 105 | 1050 |

| United Kingdom | 1114 | 11,140 |

| United States | 1427 | 14,270 |

| FAMILY | 3184 | 31,840 |

| Hong Kong | 1979 | 19,790 |

| Indonesia | 528 | 5280 |

| Philippines | 221 | 2210 |

| Singapore | 456 | 4560 |

| UAI | PDI | dicUAI | dicPDI | |

|---|---|---|---|---|

| PYRAMID | ||||

| Brazil | 76 | 69 | 0 | 1 |

| France | 86 | 68 | 0 | 1 |

| Russia | 95 | 93 | 0 | 1 |

| Spain | 86 | 57 | 0 | 1 |

| MACHINE | ||||

| Argentina | 86 | 49 | 0 | 0 |

| Austria | 70 | 11 | 0 | 0 |

| Germany | 65 | 35 | 0 | 0 |

| Israel | 81 | 13 | 0 | 0 |

| MARKET | ||||

| Denmark | 23 | 18 | 1 | 0 |

| New Zealand | 49 | 22 | 1 | 0 |

| United Kingdom | 35 | 35 | 1 | 0 |

| United States | 46 | 40 | 1 | 0 |

| FAMILY | ||||

| Hong Kong | 29 | 68 | 1 | 1 |

| Indonesia | 48 | 78 | 1 | 1 |

| Philippines | 44 | 94 | 1 | 1 |

| Singapore | 8 | 74 | 1 | 1 |

| N | Minimum | Maximum | Mean | St Deviation | |

|---|---|---|---|---|---|

| absDA | 64,822 | 0.000001 | 0.457500 | 0.081276 | 0.077274 |

| logCGVS | 15,125 | 0.033424 | 1.991580 | 1.708211 | 0.313714 |

| logUAI | 81,620 | 0.903090 | 1.977724 | 1.616580 | 0.242846 |

| logPDI | 81,620 | 1.041393 | 1.973128 | 1.696623 | 0.203969 |

| UAIxlogCGVS | 15,125 | 0.000000 | 1.991580 | 1.406885 | 0.744396 |

| PDIxlogCGVS | 15,125 | 0.000000 | 1.990516 | 0.423751 | 0.707890 |

| LIQ | 58,777 | 0.000000 | 4.973490 | 1.668410 | 0.943571 |

| DEBT | 63,065 | 0.000000 | 7.050347 | 1.274744 | 1.138188 |

| ROI | 61,584 | −0.199967 | 0.199969 | 0.041727 | 0.070775 |

| SIZE | 70,730 | 2.304473 | 8.634152 | 5.475125 | 1.048062 |

| logGDP | 81,620 | 3.260435 | 4.810111 | 4.497539 | 0.357641 |

| N: 81,620 |

| absDA | logCGVS | logUAI | logPDI | LIQ | DEBT | ROI | SIZE | logGDP | |

|---|---|---|---|---|---|---|---|---|---|

| absDA | 1 | −0.293 ** | −0.314 ** | −0.210 ** | 0.014 ** | 0.133 ** | −0.152 ** | 0.016 ** | −0.012 ** |

| logCGVS | 1 | −0.128 ** | −0.266 ** | −0.035 ** | 0.094 ** | 0.076 ** | −0.166 ** | 0.433 ** | |

| logUAI | 1 | −0.232 ** | −0.092 ** | 0.186 ** | 0.037 ** | 0.038 ** | −0.244 ** | ||

| logPDI | 1 | 0.009 * | −0.089 ** | −0.053 ** | 0.309 ** | −0.415 ** | |||

| LIQ | 1 | −0.410 ** | 0.082 ** | −0.082 ** | 0.082 ** | ||||

| DEBT | 1 | 0.061 ** | 0.173 ** | 0.022 ** | |||||

| ROI | 1 | 0.196 ** | −0.009 * | ||||||

| SIZE | 1 | −0.498 ** | |||||||

| logGDP | 1 |

| B | Standard Error | t | Sig. | |

|---|---|---|---|---|

| logCGVS | −0.069 | 0.002 | −31.138 | 0.000 |

| logUAI | −0.033 | 0.004 | −8.493 | 0.000 |

| logPDI | −0.057 | 0.005 | −10.478 | 0.000 |

| dicUAIx logCGVS | 0.021 | 0.001 | 17.033 | 0.000 |

| dicPDIx logCGVS | 0.042 | 0.001 | 30.855 | 0.000 |

| LIQ | 0.000 | 0.001 | −0.665 | 0.506 |

| DEBT | 0.003 | 0.000 | 8.373 | 0.000 |

| ROI | −0.119 | 0.008 | −14.133 | 0.000 |

| SIZE | 0.001 | 0.001 | 1.126 | 0.260 |

| logGDP | 0.015 | 0.002 | 6.720 | 0.000 |

| Constant | 0.206 | 0.016 | 13.183 | 0.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jarne-Jarne, J.I.; Callao-Gastón, S.; Marco-Fondevila, M.; Llena-Macarulla, F. The Impact of Organizational Culture on the Effectiveness of Corporate Governance to Control Earnings Management. J. Risk Financial Manag. 2022, 15, 379. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15090379

Jarne-Jarne JI, Callao-Gastón S, Marco-Fondevila M, Llena-Macarulla F. The Impact of Organizational Culture on the Effectiveness of Corporate Governance to Control Earnings Management. Journal of Risk and Financial Management. 2022; 15(9):379. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15090379

Chicago/Turabian StyleJarne-Jarne, José Ignacio, Susana Callao-Gastón, Miguel Marco-Fondevila, and Fernando Llena-Macarulla. 2022. "The Impact of Organizational Culture on the Effectiveness of Corporate Governance to Control Earnings Management" Journal of Risk and Financial Management 15, no. 9: 379. https://0-doi-org.brum.beds.ac.uk/10.3390/jrfm15090379