Economic Performance and Emission Reduction of Supply Chains in Different Power Structures: Perspective of Sustainable Investment

Abstract

:1. Introduction

2. Literature Review

3. Modelling Framework

4. Analysis of Different Power Structures

5. Comparison

5.1. Analytical Comparison of the Decisions and Performance

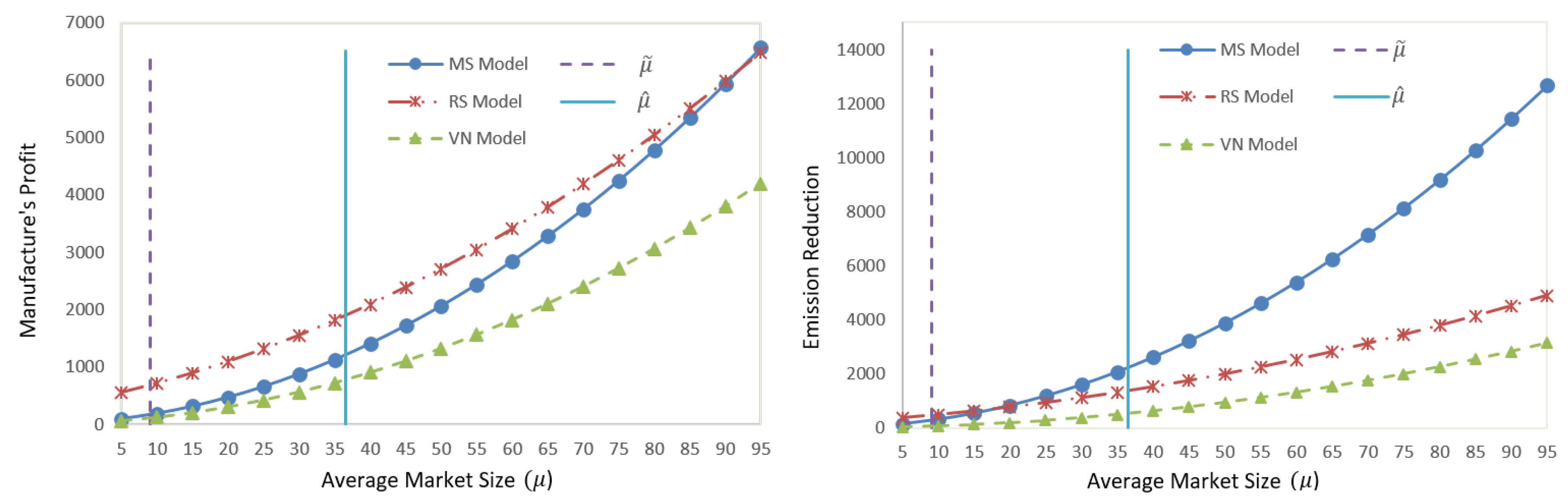

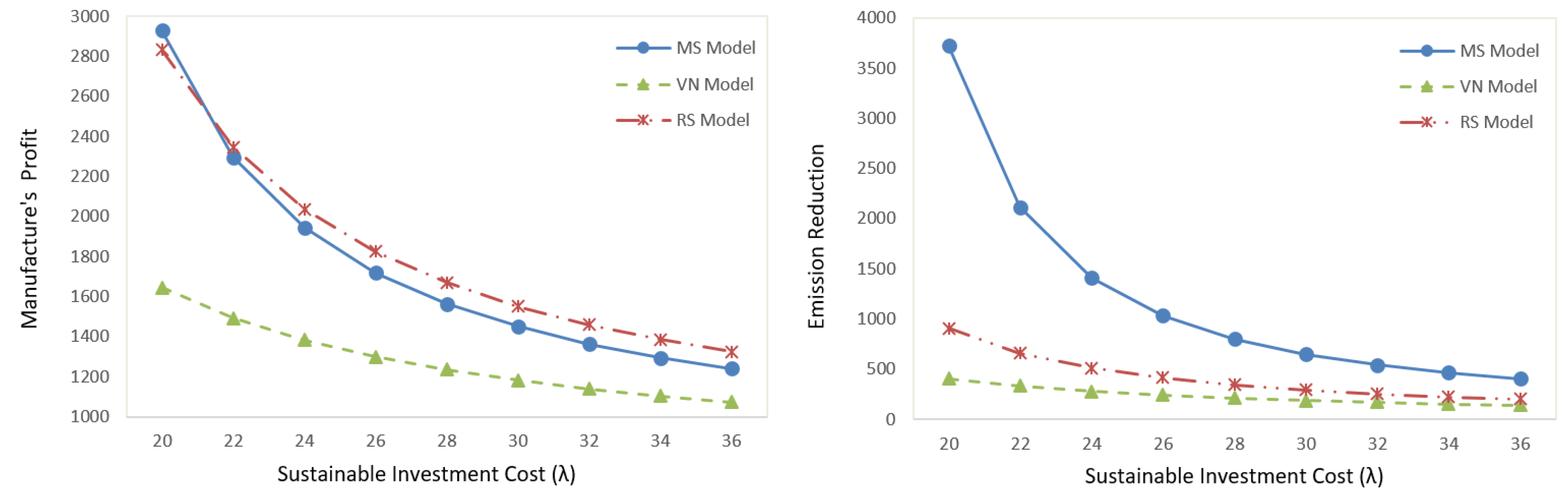

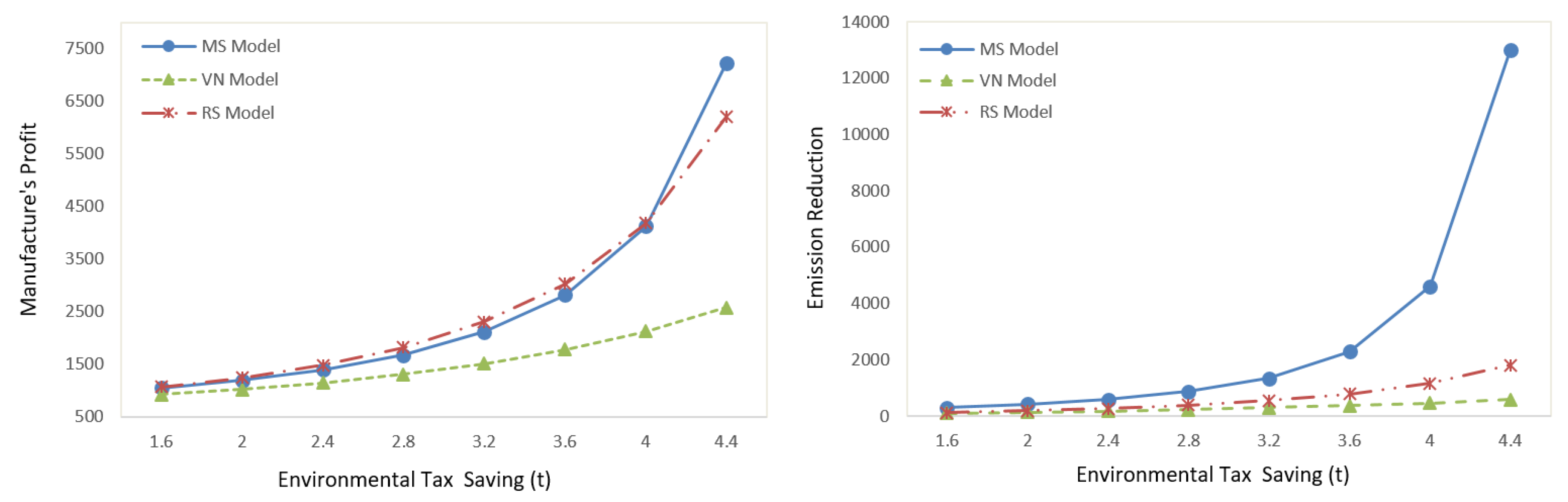

5.2. Numerical Studies

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

References

- Krass, D.; Nedorezov, T.; Ovchinnikov, A. Environmental taxes and the choice of green technology. Prod. Oper. Manag. 2013, 22, 1035–1055. [Google Scholar] [CrossRef]

- Atasu, A.; Özdemir, Ö.; Van Wassenhove, L.N. Stakeholder perspectives under EWaste Take-Back legislation. Prod. Oper. Manag. 2013, 22, 382–396. [Google Scholar] [CrossRef]

- Drake, D.F.; Kleindorfer, P.R.; Van Wassenhove, L.N. Technology choice and capacity portfolios under emissions regulation. Prod. Oper. Manag. 2015, 25, 1006–1025. [Google Scholar] [CrossRef]

- Shi, X.; Qian, Y.; Dong, C. Economic and environmental performance of fashion supply chain: The Joint effect of power structure and sustainable investment. Sustainability 2017, 9, 961. [Google Scholar] [CrossRef]

- Shen, B. Sustainable fashion supply chain: Lessons from H&M. Sustainability 2014, 6, 6236–6249. [Google Scholar] [CrossRef]

- Dong, C.; Shen, B.; Chow, P.S.; Yang, L.; Ng, C.T. Sustainability investment under cap-and-trade regulation. Ann. Oper. Res. 2016, 240, 509–531. [Google Scholar] [CrossRef]

- Apple Environmental Responsibility Report 2017. Available online: https://images.apple.com/environment/pdf/Apple_Environmental_Responsibility_Report_2017.pdf (accessed on 20 April 2017).

- Marks&Spencer Plan A Report 2016. Available online: http://planareport.marksandspencer.com/M&S_PlanA_Report_2016.pdf (accessed on 15 June 2016).

- Chen, X.; Wang, X.; Chan, H. Manufacturer and retailer coordination for environmental and economic competitiveness: A power perspective. Transp. Res. Part E Logist. Transp. Rev. 2017, 97, 268–281. [Google Scholar] [CrossRef]

- Cheng, Y.; Kuang, Y.; Shi, X.; Dong, C. Sustainable investment in a supply chain in the big data era: An information updating approach. Sustainability 2018, 10, 403. [Google Scholar] [CrossRef]

- Choi, T.M. Local sourcing and fashion quick response system: The impacts of carbon footprint tax. Transp. Res. Part E Logist. Transp. Rev. 2013, 55, 43–54. [Google Scholar] [CrossRef]

- Rosič, H.; Jammernegg, W. The economic and environmental performance of dual sourcing: A newsvendor approach. Int. J. Prod. Econ. 2013, 143, 109–119. [Google Scholar] [Green Version]

- Niu, B.; Chen, L.; Zhang, J. Punishing or subsidizing? Regulation analysis of sustainable fashion procurement strategies. Transp. Res. Part E Logist. Transp. Rev. 2017, 107, 81–96. [Google Scholar] [CrossRef]

- Shen, B.; Li, Q. Impacts of returning unsold products in retail outsourcing fashion supply chain: A sustainability analysis. Sustainability 2015, 7, 1172–1185. [Google Scholar] [CrossRef]

- Guo, Z.; Liu, H.; Zhang, D.; Yang, J. Green supplier evaluation and selection in apparel manufacturing using a fuzzy multi-criteria decision-making approach. Sustainability 2017, 9, 650. [Google Scholar] [CrossRef]

- He, Z.; Chen, P.; Liu, H.; Guo, Z. Performance measurement system and strategies for developing low-carbon logistics: A case study in China. J. Clean. Prod. 2017, 156, 395–405. [Google Scholar] [CrossRef]

- Benjaafar, S.; Li, Y.; Daskin, M. Carbon footprint and the management of supply chains: Insights from simple models. IEEE Trans. Autom. Sci. Eng. 2013, 10, 99–116. [Google Scholar] [CrossRef]

- Toptal, A.; Özlü, H.; Konur, D. Joint decisions on inventory replenishment and emission reduction investment under different emission regulations. Int. J. Prod. Res. 2014, 52, 243–269. [Google Scholar] [CrossRef] [Green Version]

- Yalabik, B.; Fairchild, R.J. Customer, regulatory, and competitive pressure as drivers of environmental innovation. Int. J. Prod. Econ. 2011, 131, 519–527. [Google Scholar] [CrossRef]

- Liu, Z.L.; Anderson, T.D.; Cruz, J.M. Consumer environmental awareness and competition in two-stage supply chains. Eur. J. Oper. Res. 2012, 218, 602–613. [Google Scholar] [CrossRef]

- Jaber, M.Y.; Glock, C.H.; El Saadany, A.M. Supply chain coordination with emissions reduction incentives. Int. J. Prod. Res. 2013, 51, 69–82. [Google Scholar] [CrossRef]

- Zhang, L.; Wang, J.; You, J. Consumer environmental awareness and channel coordination with two substitutable products. Eur. J. Oper. Res. 2015, 241, 63–73. [Google Scholar] [CrossRef]

- Du, S.; Zhu, J.; Jiao, H.; Ye, W. Game-theoretical analysis for supply chain with consumer preference to low carbon. Int. J. Prod. Res. 2015, 53, 3753–3768. [Google Scholar] [CrossRef]

- Li, Q.; Shen, B. Sustainable design operations in the supply chain: Non-profit manufacturer vs. for-profit manufacturer. Sustainability 2016, 8, 639. [Google Scholar] [CrossRef]

- Anupindi, R.; Bassok, Y. Centralization of stocks: Retailers vs. manufacturer. Manag. Sci. 1999, 45, 178–191. [Google Scholar] [CrossRef]

- Iyer, G.; Villas-Boas, J.M. A bargaining theory of distribution channels. J. Mark. Res. 2003, 40, 80–100. [Google Scholar] [CrossRef]

- Dukes, A.J.; Geylani, T.; Srinivasan, K. Strategic assortment reduction by a dominant retailer. Mark. Sci. 2009, 28, 309–319. [Google Scholar] [CrossRef]

- Choi, S.C. Price competition in a channel structure with a common retailer. Mark. Sci. 1991, 10, 271–296. [Google Scholar] [CrossRef]

- Ertek, G.; Griffin, P.M. Supplier-and buyer-driven channels in a two-stage supply chain. IIE Trans. 2002, 34, 691–700. [Google Scholar] [CrossRef]

- Chen, X.; Wang, X. Free or bundled: Channel selection decisions under different power structures. Omega 2015, 53, 11–20. [Google Scholar] [CrossRef]

- Luo, Z.; Chen, X.; Chen, J.; Wang, X. Optimal pricing policies for differentiated brands under different supply chain power structures. Eur. J. Oper. Res. 2017, 259, 437–451. [Google Scholar] [CrossRef]

- Shi, R.; Zhang, J.; Ru, J. Impacts of power structure on supply chains with uncertain demand. Prod. Oper. Manag. 2013, 22, 1232–1249. [Google Scholar] [CrossRef]

- Shen, B.; Choi, T.M.; Chan, H.L. Selling green first or not? A Bayesian analysis with service levels and environmental impact considerations in the Big Data Era. Technol. Forecast. Soc. Chang. 2017. [Google Scholar] [CrossRef]

- Chan, H.L.; Shen, B.; Cai, Y. Quick response strategy with cleaner technology in a supply chain: Coordination and win-win situation analysis. Int. J. Prod. Res. 2017, 1–12. [Google Scholar] [CrossRef]

- Iyer, A.V.; Bergen, M.E. Quick response in manufacturer-retailer channels. Manag. Sci. 1997, 43, 559–570. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Papers | Carbon Emission | Sustainable Investment Decision | Consumer Environmental Awareness | Power Structure | Stochastic Demand |

|---|---|---|---|---|---|

| Choi [11], Shen and Li [14], Shen et al. [33] | √ | √ | |||

| Chan et al. [34] | √ | √ | √ | ||

| Li and Shen [24], Du et al. [23] | √ | √ | √ | ||

| Zhang et al. [22] | √ | √ | √ | ||

| Cheng et al. [10], Dong et al. [6] | √ | √ | √ | √ | |

| Choi [28], Ertek and Griffin [29], Chen and Wang [30] | √ | ||||

| Shi et al. [32] | √ | √ | |||

| Chen et al. [9], Shi et al. [4] | √ | √ | √ | √ | |

| This paper | √ | √ | √ | √ | √ |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shi, X.; Zhang, X.; Dong, C.; Wen, S. Economic Performance and Emission Reduction of Supply Chains in Different Power Structures: Perspective of Sustainable Investment. Energies 2018, 11, 983. https://0-doi-org.brum.beds.ac.uk/10.3390/en11040983

Shi X, Zhang X, Dong C, Wen S. Economic Performance and Emission Reduction of Supply Chains in Different Power Structures: Perspective of Sustainable Investment. Energies. 2018; 11(4):983. https://0-doi-org.brum.beds.ac.uk/10.3390/en11040983

Chicago/Turabian StyleShi, Xiutian, Xiaoli Zhang, Ciwei Dong, and Subin Wen. 2018. "Economic Performance and Emission Reduction of Supply Chains in Different Power Structures: Perspective of Sustainable Investment" Energies 11, no. 4: 983. https://0-doi-org.brum.beds.ac.uk/10.3390/en11040983