Determinants of COVID-19 Impact on the Private Sector: A Multi-Country Analysis Based on Survey Data

Faculty of Management and Economics, Gdańsk University of Technology, 80-233 Gdańsk, Poland

*

Author to whom correspondence should be addressed.

Energies 2021, 14(14), 4155; https://0-doi-org.brum.beds.ac.uk/10.3390/en14144155

Submission received: 8 June 2021

/

Revised: 30 June 2021

/

Accepted: 7 July 2021

/

Published: 9 July 2021

(This article belongs to the Special Issue Challenge and Research Trends of Forecasting Financial Energy)

Abstract

:Our paper aims to investigate the impact of COVID-19 on private sector companies in terms of sales, production, finance and employment. We check whether the country and industry in which companies operate, government financial support and loan access matter to the behaviour and performances of companies during the pandemic. We use a microdata set from a worldwide survey of more than 15,729 companies conducted between April and September 2020 by the World Bank. Logistic regression is used to assess which factors increase the likelihood of businesses suffering due to the COVID-19 pandemic. Our results show that COVID-19 negatively impacts the performance of companies in almost all countries analysed, but a stronger effect is observed among firms from developing countries. The pandemic is more harmful to firms providing services than those representing the manufacturing sector. Due to the pandemic, firms suffer mainly in sales and liquidity decrease rather than employment reduction. The increase in the number of temporary workers is an important factor that significantly reduces the probability of sales, exports or supply decline. The analysis results indicate policy tools supporting enterprises during the pandemic, such as increasing the flexibility of the labour market or directing aid to developing countries.

1. Introduction

The coronavirus pandemic has spread to nearly every country on the planet. As policymakers struggle with new lockdown policies to combat the virus’s spread, national economies pay the cost. According to the International Monetary Fund (IMF) [1], the global economy contracted by 4.4% in 2020. The volume of international trade in goods dropped by 16% between April and June 2020 compared to the same period in 2019 [2]. The COVID-19 crisis has also had a significant impact on the labour market—overall, an unprecedented global loss of 114 million jobs was observed in 2020 compared to 2019, highest in the both North and South America and lowest in Europe and Central Asia, where job retention programmes have supported reductions in working hours [3]. Apart from statistics, in economic literature, we can find several new studies related to the impact of the COVID-19 pandemic on economic activities. They focus mainly on the macroeconomic effects of pandemics, i.e., a high correlation between the level of restriction and economic downturn [4,5,6,7,8,9]. The pandemic has also affected investments and consumption patterns [10,11,12,13].

Our paper aims to examine the impact of COVID-19 on private sector firms, and it is in line with quickly expanding studies on COVID-19 implications at the micro-level. Previous papers are mainly related to the implications of COVID-19 on management and marketing activities [14]. They analyse how the COVID-19 pandemic influence human resources management [15], research and development activities [16], corporate social responsibility (CSR systems [17], consumer behaviours [18], manager behaviours [19] and even gender equality in pandemic situations [15]. The researchers in this area have worked rapidly to find alternative solutions and facilitate the transformation of companies to adapt to the new scenario and ensure their survival. The results of these works are guidelines for managers, especially indications of how to find uncertainty in businesses and develop strategies [20], tools for creating new marketing strategies [21,22], new strategies for organisations [17], practical advice on financial management [23] and guidelines on marketing innovation strategies of firms under crisis [22]. In addition, some of the papers show how to implement the interventions in public laws and policy, and national and local regulations [24].

Far fewer analyses relate to the impact of the COVID-19 pandemic on the economic activities of companies. The majority of studies focus on the three aspects. First, they try to identify channels through which firms adjust to the economic disruption caused by COVID-19 and try to overcome the pandemic [25]. The firms struggle with broken supply chains, discontinuity of services (both public and commercial), availability of staff, transport and logistics [26]. This is not just the result of the disease but also of how people or businesses respond to the circumstances. These analyses show that firms try to overcome the crises mainly by accelerating their adoption of digital, automation and other technologies [27,28] and shifting business activities to remote/hybrid work [29].

The second group of papers concentrates on the firm’s expectations, i.e., how long did businesses expect the crisis to last and how do expectations affect their decisions. Research shows that a company’s market condition before the pandemic determines its expectations regarding the pandemic duration. Weak companies are more affected; they expect further difficulties and are the first to limit employment and investments [30]. On the other hand, the higher liquidity firm has and the more prominent the firm is, the greater the belief in the ability to survive the crisis [25]. Additionally, Ref. [31] finds that despite international firms being more exposed to the COVID-19 pandemic, they have more resilient actions and better expectations for future domestic firms due to their global connectedness.

The last group of analyses relates to the implication of demand and supply shocks caused by COVID-19 on enterprises’ operational and financial activity. According to [32], companies worldwide have been or still are forced to suspend some of their operations, partly due to temporary job closures ordered by some governments and partly due to supply chain disruptions. In some cases, changing demand patterns have forced companies to relocate or realign their production processes. In other cases, companies have had to find entirely new ways to operate in a challenging and uncertain environment. Severe effects of the COVID-19 pandemic have been documented in various countries in the form of lost sales, business closures, mass layoffs and liquidity shortages (for US firms: [25,33,34]; for firms from high and middle-income countries [35]; for selected European companies: [36]; for firms from developing countries [37]; for firms from selected Asian countries: [38,39,40,41]). However, few studies analyse the determinants of the impact of the COVID-19 pandemic on the economic activity of firms.

In this regard, our article fills the research gap by identifying determinants of the COVID-19 pandemic in enterprises. Few previous studies indicate firm size as a significant factor that determines the pandemic effects on the economic activities of firms. Despite large companies and small and medium-sized enterprises (SMEs) affected by the pandemic, all studies show that the impact on SMEs is much more significant [25,42]. Among SMEs, according to [38], faster-growing firms experience the demand shock somewhat less severely but are more affected by international trade disruptions, supply and financial shocks. Additionally, Ref. [39] find that better skills protect against the effects of a pandemic, i.e., employees with medium to high professional qualifications are less affected by the crisis. The weakness of the above analyses is that they are often based on data from one country and a limited set of determinants (size, employee skills, susceptibility to supply shocks). Our paper analyses whether the country and industry in which firms operate, government financial support and access to credit impact their behaviour and performance during the pandemic. We use a microdata set from a global survey of more than 15,720 firms conducted by the World Bank in 37 countries. In our work, we wanted to investigate the following research hypotheses:

Hypothesis 1 (H1).

Financial aid granted by commercial banks will most strongly reduce the probability of the company’s performance drop.

Hypothesis 2 (H2).

Increasing online business activity reduces the likelihood of a decline in sales more than increasing remote working.

Hypothesis 3 (H3).

Declines in supply were the most difficult to cover with financial aid or changes in the work organisation.

Hypothesis 4 (H4).

Regardless of the sector and the measure of economic activity, companies in developing countries were more exposed to losses.

To summarise, our contribution to the empirical literature is that we, based on a large sample of firms worldwide, provide insight into the economic impact of the COVID-19 on the private sector. The results illuminate the strong economic impact of COVID-19 on private firms in the first weeks following the onset of COVID-19-related disruptions. We concentrate on the identification of factors, which determine the strength of this influence. The paper is organised as follows. The subsequent section outlines the description of the survey and the dataset. Section 2 introduces the empirical part of the paper by presenting the methodology used to measure the impact of COVID-19 on the activities of firms. The following section offers the results of our analysis, and the last one presents our conclusions.

Description of the Survey and the Data Set

The World Bank has developed a short company survey instrument, called Follow-up COVID-19, to measure the impact of the COVID-19 pandemic on the private sector. This survey is part of the Enterprise Survey (ES.), a flagship firm-level survey of a representative sample of an economy’s private sector that the World Bank has conducted since the 1990s [43]. The Enterprise Survey is aimed at companies with five or more employees and answered by business owners and top managers. It covers a wide range of business environment issues, such as performance, finance, competition and corruption. The ES concerns manufacturing firms (with ISIC (International Standard Industrial Classification of All Economic Activities) codes 15–37, 45, 50–52, 55, 60–64 and 72) and services companies from construction, retail, wholesale, hotel, restaurant, transport, storage, communications and IT sectors. The Enterprise Survey is carried out in 42 countries, but the number of interviews depends on the economy’s size, i.e., from 150 in small countries to 1200–1800 in large economies.

After the COVID-19 outbreak, follow-up surveys on the impact of COVID-19 under the ES methodology were conducted. The World Bank has two rounds of follow-up surveys. Our research is based on data obtained during the first completed round, between April and September 2020. The topics covered include changes in sales, demand for products or services, supply of inputs, workforce, cashflow availability and government supports. The survey was conducted using mainly computer-assisted telephone interviewing (CATI), i.e., a telephone surveying technique in which the interviewer follows a script provided by a software application. Telephone interviews are supported by email for self-administration if needed. The exceptions are three African countries (face-to-face interviews) and Russia, where an online survey was applied.

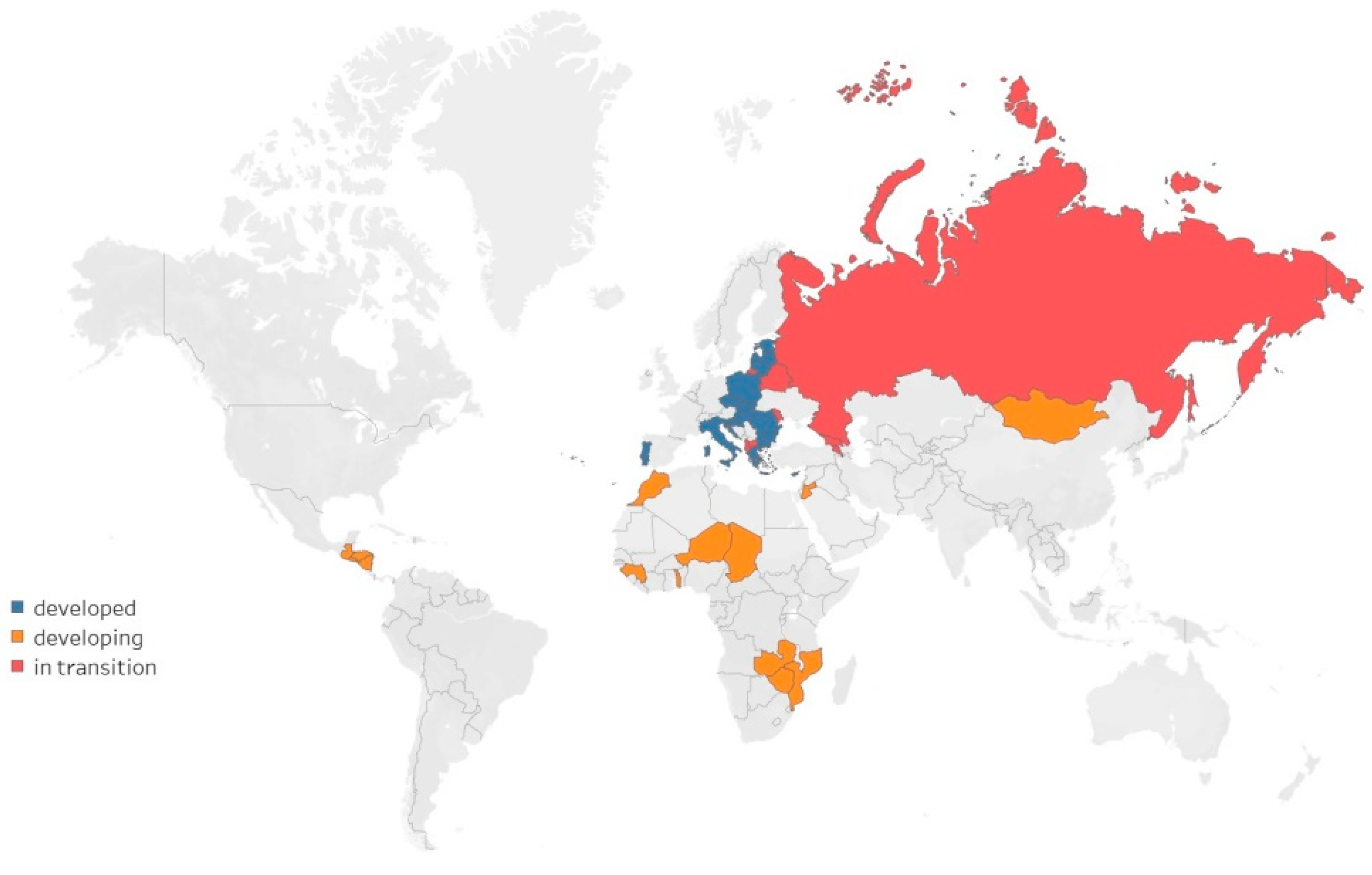

The sample covers micro, small, medium and large enterprises from 37 countries, including companies from Europe (62.7%), Asia (10.2%), Africa (21%) and Central America (6.2%) (Figure 1). Almost half (45.5%) are from the European Union countries, and nearly the same percentage (45.2%) are from developed countries. Firms from developing countries and transition economies represent 32.8 % and 22%, respectively.

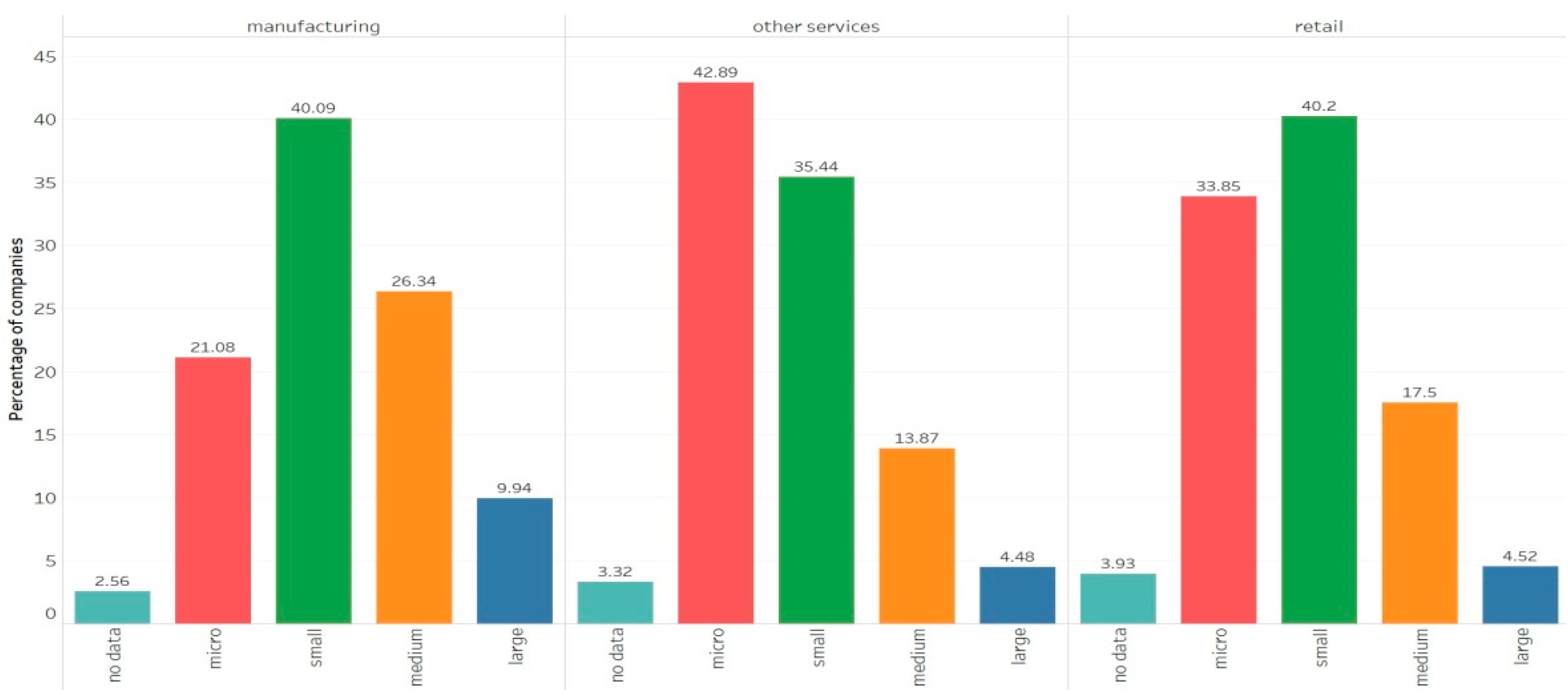

A representative sample of the private sector excluding agriculture and extractive industries covers companies dealing in manufacturing (49.4%), retail (19.6%) and other services (31%). Small and medium-sized firms account for 60% of the sample in the manufacturing sector and almost 88% in retail (Figure 2). The largest share of large companies can be observed in manufacturing (10%).

2. Research Methodology

The analysis covers survey data obtained from the World Bank’s Enterprise Surveys—COVID-19 Survey, Round 1 from 2020 [43]. The research sample includes 15,720 companies from 37 countries. However, it should be noted that not all respondents answered every question; hence, the number of observations at individual stages of the analysis may differ.

Logistic regression was used to assess which factors increase the likelihood of companies suffering due to the COVID-19 pandemic. It is an excellent tool for modelling binary dependent variables [44]. In our case, it was the fact that there was a decrease in sales, exports, demand, supply or liquidity. Therefore, we wanted to find factors that increase the probability that a given dependent variable would take the value of 1:

The following formula expresses this probability:

where , the probability the dependent variable , equals 1, represent the regression coefficient and represent the independent variables.

The positive sign of the parameter indicates that the increase in the variable increases the probability of taking the value of 1, while the negative sign of the parameter decreases this likelihood. Models were estimated using the MLM—maximum likelihood method [45]. In order to determine the strength and direction of the impact of the variables, odds ratios were determined:

The is the fold change in the odds ratio; if , the increase in the odds ratio (3) can be observed, and for , we can observe the decrease in the odds ratio. The set of variables used in the analysis is presented in Table 1.

The quality of the model was assessed using McFadden’s pseudo-R2, the log-likelihood for the entire model and the likelihood ratio test [46].

3. Results

In the first step of the analysis, the descriptive characteristics of the analysed entities were established, mainly in terms of the sector in which they operate. We assumed that services and manufacturing were not equally affected by the effects of the pandemic, as the restrictions introduced in these sectors were different.

Table 2 shows the percentage distribution of constantly operating companies and temporarily or permanently closed ones, depending on the type of business. When analysing the data contained in Table 2, it can be seen that the percentage of permanently closed companies was similar in each sector. Nevertheless, other services are evidently disadvantaged, as the ratio of companies closed temporarily was almost twice as high as in the case of manufacturing or retail.

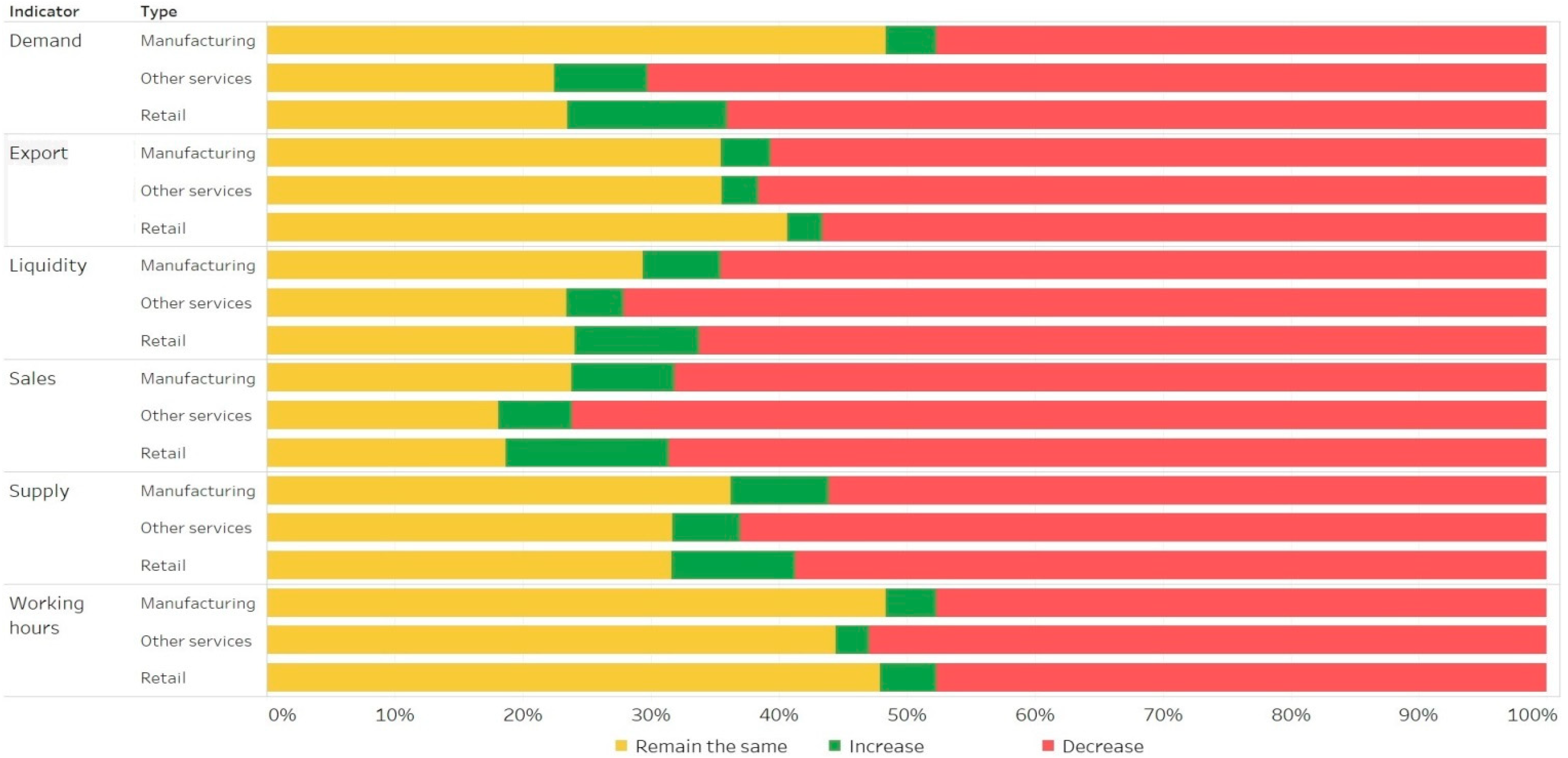

Figure 3 suggests that the type of business activity influences individual elements of the company’s operations. In each case, the yellow colour means that the variable is at the same level as in the corresponding month of 2019; green means an increase and red a decrease. In Figure 3, in all aspects, the red dominates, so all aspects of business activities have been adversely affected by the pandemic. In many manufacturing companies, supply and demand have not changed. Retail turned out to be the sector in which the highest percentage of companies recorded an increase in sales and demand. At the same time, it shows the most significant decrease in sales, demand and financial liquidity in other services sectors. The graphical analysis suggests a certain relationship between the type of business activity and performance during the pandemic. This finding was further confirmed by the chi-square test of independence, which showed for each of the six analysed aspects that achievements in a given field are associated with the type of economic activity.

The preliminary analysis showed that many aspects of enterprises’ activity shrank compared to the corresponding month of 2019. By analysing the basic descriptive statistics, we wanted to know the depth of these declines. Quantitative data from the World Bank survey [43] concerned only the sales volume and the number of laid-off employees. Table 3 presents basic descriptive statistics for these factors. When analysing the data on the decline in sales volume, it can be seen that it was significant. In manufacturing, half of the firms recorded a decline of 40% or higher, and the majority indicated a decrease of 30%. In retail, the median was also 40%, but in this case, most companies reported that sales fell by half; most companies from the other services sector revealed a similar decrease in sales. There is quite a strong differentiation and right-handed asymmetry in all sectors, which means that most companies recorded declines below the average, which was the highest for other services—52%. There are also significant differences in the case of 10% of companies affected by the highest sales drops. They amounted to at least 80% in manufacturing, but the decrease reached 100% in other services. Interestingly, looking at the data on the number of laid-off employees, the median and mode were 0 in each case; taking into account the positive skewness sign, it can be concluded that most companies did not reduce the number of employed staff, and those that did so reduced employment on average by 3.3 (retail) to 5.3 (manufacturing) workers. However, attention should be paid to the enormous values of the coefficient of variation and the range between the maximum and minimum values. At least one company in the manufacturing and retail sectors dismissed 600 people, while many companies issued no lay-offs. Thus, not only the industry itself but also other factors forced the reduction of staff.

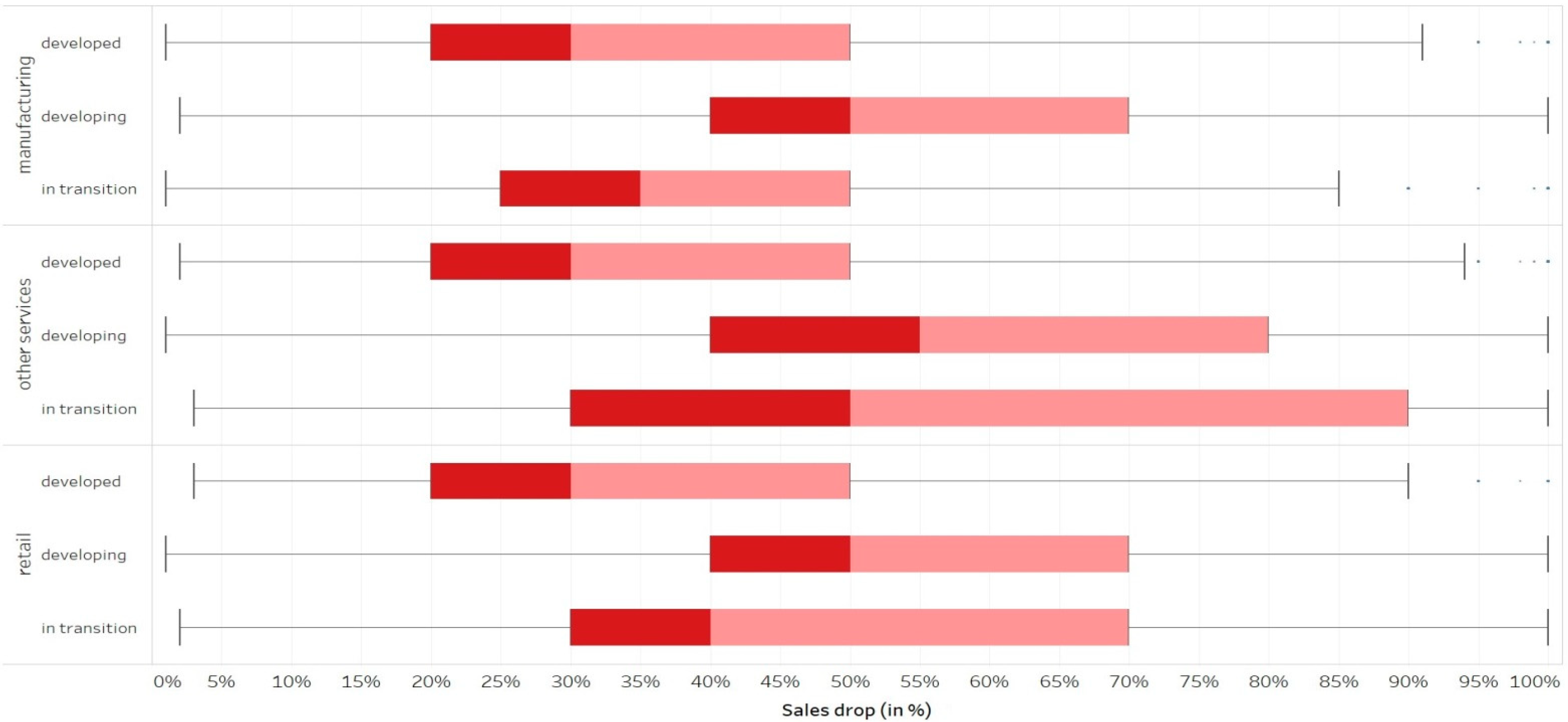

Because all sectors were most severely affected by sales declines, we decided to show the scale of the problem in more detail. Figure 4 (box plot—dark red represents values between first quartile and the median, light red represents those between the median and third quartile) shows the declared decrease in sales in analysed sectors, taking into account the region as well. Not only were most companies from the other services sector affected by sales declines (Figure 3), but also the volume of this decline was the most severe in this sector (Figure 4), mainly if the business was run in a transition (median 40%, mode 100% sales drop) or developing country (median 55%, mode 50% sales drop). The manufacturing sector in developed countries (mode and median 30%) experienced the relatively mildest decline. However, it should be borne in mind that the analysed set of enterprises is characterised by high differentiation (long boxes) and the presence of extreme values (lower and upper whiskers). In each sector/region combination, some companies declared a 100% sales decline, but in some, it was practically unnoticed (1–2%). It most likely results from the industry in which the company operates and the degree of flexibility of operations.

The models presented in Table 4 have satisfactory properties, both in terms of predictive properties and the model’s fit to empirical data. In the sales decline (SalesD) case, seven diagnostic variables turned out to be statistically significant. The estimated parameters showed a negative value for three of them, which indicates that the sales drop is less likely to occur as the predictor takes the value of 1. In this case, the odds of recording a decline in sales decreased if it was a manufacturing company (Man), which increased the number of temporary employees (TW), and if its headquarters were in a developed country (Developed). At the same time, the remaining variables indicate characteristics that increase the chance of recording a drop in sales (a positive coefficient value and odds ratio above 1). Such factors turned out to be EF, DP, Support and Developing. This means that companies that received any form of government support had a better chance of observing a drop in sales. However, it should be considered whether this phenomenon is not due to the fact that the government aid (at least in Poland) was directed to a greater extent to entrepreneurs who were able to document an actual drop in sales and revenues compared to the periods before the pandemic. Moreover, the factors increasing the chances of recording a decline in sales included two forms of primary aid: equity finance and delaying payments to suppliers and employees. Doing business in developing countries was also a factor increasing the chance of recording a drop in sales.

In the case of another dependent variable—a decrease in exports (ExportD)—in the estimated model, 6 out of 14 proposed diagnostic variables turned out to be statistically significant. However, it should be borne in mind that in this case, the number of observations was almost two times lower, as not all of the analysed companies conducted export activities. The variable Man turned out to be among the factors reducing the odds of recording a decline in exports, so again companies from the broadly understood services sector fared worse than manufacturing companies. TW (an increase in the number of temporary workers) reduced the chance of recording a decline in exports, as in the case of sales. Moreover, the LCB variable also turned out to be statistically significant. Hence, companies whose primary source of aid were loans offered by commercial banks had less chance of reducing exports. Factors increasing this chance turned out to be running a business in developed and developing countries, which means that they fared worse than companies operating in countries belonging to the “in transition” group. In addition, surprisingly, the variable DA, i.e., starting or intensifying online deliveries, was a factor increasing the odds of export reduction.

Another of the estimated models concerned the decline in demand. The number of observations for this model was similar to the number of observations for the sales (SalesD) and supply (SupplyD) model. Among the factors limiting the decline in demand, there was only one. It was a geographical factor, i.e., running a business in a developed country. The remaining five diagnostic variables indicate factors that increase the odds of reduced demand, including operating in a developing country, receiving any form of government support, having the basic form of aid as equity finance (EF), delaying payments (DP) and grants from the government (GG).

The last estimated model (SupplyD) was the one with the lowest number of significant factors. It is also the model with the poorest properties. Many variables coincide with those indicated in previous cases, so the factor that increased the risk of a decrease in supply was operating in a developing country. On the other hand, the odds of such a decrease were reduced by an increased share of temporary workers, running a business in a developed country and an increased share of remote work (RW).

In order to make the analysis more detailed, the more detailed models were estimated. They show the extent to which the individual types of financial support and the activities undertaken by enterprises impacted the decreases observed in particular areas of business operations. Table 5 shows the impact of various factors on the decline in sales. The three presented models relate to manufacturing, services and retail, respectively. It turns out that in the case of manufacturing companies, obtaining a loan from a commercial bank, equity finance or delaying payments increased the likelihood of a decrease in sales. The mitigating factor was the introduction of temporary work. As in the case of the models presented in Table 4, in these more detailed models, business residence turned out to be of crucial importance. Thus, operating in a developed country reduced the chance of seeing a drop in sales, while operating in a developing or “in transition” country increased the likelihood of seeing a decline in sales. Similar trends are also observed in the case of services and trade. In the latter case, the intensification of online deliveries also turned out to reduce the decline in sales.

Table 6 shows the factors influencing the chances of reducing exports. The residence of business was again of key importance; regardless of whether we are talking about manufacturing, trading or service enterprises, operating in “in transition” countries was a factor reducing export losses, while doing business in developed or developing countries increased these odds significantly. In the context of exports, the introduction of temporary work helped to reduce the chances of a decline only in the case of industry; in other sectors, this factor turned out to be statistically insignificant. The deferral of payments in manufacturing companies was also a factor in reducing the odds of export losses, while in the case of services, the intensification of online activity turned out to be a protective umbrella.

As Figure 3 shows, the decline in demand was one of the two most typical adverse effects of the COVID-19 pandemic. Table 7 presents which factors contributed to the decrease in the probability of a reduction in demand in various types of enterprises. Not surprisingly, running a business was important again, but this time running a business in a developed country was a factor reducing the chances of recording a drop in demand. The same was observed in the case of the intensification of temporary work and in production companies’ case, also of remote work. As in the case of Table 4, here we can see that receiving support was associated with a greater chance of recording a decline in demand. This should be explained in the same way, i.e., directing aid to units suffering losses due to the pandemic; however, other factors proved to be statically significant in different sectors. In the case of services, it was equity finance, and in the case of manufacturing, EF and additionally a payment delay. In the case of service companies, the factors reducing losses in demand turned out to be the intensification of online activities and online delivery, and obtaining support from commercial banks.

The data on the decline in supply are presented last (Table 8). This element turned out to be relatively insensitive to financial support and organisational changes in companies from the retail sector. However, many factors were statistically significant in the case of services. The severity of the supply drops was diversified by the intensification of temporary work apart from the aforementioned element—the level of development of the country’s economy. Additionally, in the case of service companies, the chances of reducing the decline in supply were caused by the introduction of remote work and deferred payments.

4. Conclusions

Our paper aims to examine the impact of COVID-19 on private sector firms in terms of sales, production, finance and employment. We determined whether the country and industry in which firms operate, government financial support and access to credit impact its behaviour and performance during the pandemic. It is crucial to keep in mind that the World Bank survey was conducted immediately after the first lockdown. Many companies did not react immediately to the pandemic and considered it a short-term phenomenon, which had a more significant impact on their behaviour. It is necessary for the authors to compare the results from this survey with the future survey conducted by the World Bank in 2021 (these data are inaccessible at the present moment).

Our results show that a country’s development stage strongly influences the probability of changes in trading activities such as sales, exports, demand and supply. Our research confirms that the global COVID-19 pandemic negatively impacts firms in developing economies to a greater extent than those in developed countries (confirming the fourth hypothesis). Firms in developing countries are hit hardest because they have “fewer resources or channels” to protect themselves against this economic crisis, i.e., lower labour productivity, lower capital intensity and a lower degree of digitisation in production processes [47]. Our research indicates the need for organisations such as the World Bank or IMF to provide financial support to developing countries to respond to the health and economic impacts of COVID-19.

The analysis also provides evidence on the role of the sector in which a firm operates in the decline of economic activity due to the COVID-19 pandemic. It is less probable that firms in the manufacturing sector will be affected by decreased sales and exports than those in the services sector. It is probably related to the higher level of automation in many manufacturing processes than services. On the other hand, companies providing services are more dependent on human contact and interaction and thus may suffer more significant losses from a crisis of this nature. Moreover, more detailed analyses (Table 5, Table 6, Table 7 and Table 8) showed that different forms of aid and changes in enterprises’ operating activities affect differently depending on the sector and measure of performance. Among the various discussed forms of coping with the lack of liquidity, the most statistically significant was deferment of payments. However, it occurred in both a positive and negative context. Therefore, one should be aware that this tactic works like a double-edged sword. On the one hand, it allowed entrepreneurs to postpone selected payments but thus contributed to the deterioration of liquidity in other companies, hence, for example, different directions of impact in production and service companies. Therefore, hypothesis 1, assuming that commercial banks’ support will be of key importance for reducing the harmful effects of the pandemic, has not been confirmed.

The second hypothesis assumed that the intensification of online activities would significantly affect the reduction of performance drops and certainly better than remote work. This turned out to be valid only in the case of service companies. Remote work was irrelevant to retail. The intensification of online activity increased the chances of a decline in demand (most likely, the sales level was maintained throughout the entire network, but certain sales points were experiencing declines). Based on the results of our analysis, we point to an essential factor that significantly reduces the probability of the decline of sales, exports or supply—the increase in the number of temporary workers. During the COVID-19 pandemic, market conditions change almost daily, and companies struggle to keep up. Thus, while the short-term use of temporary workers helped many companies during the pandemic, it will probably be an effective tool for work management in post-COVID-19 reality, as well. Our results indirectly support the thesis with a greater emphasis on the flexibility of labour markets in countries affected by the pandemic as an economic policy tool supporting recovery from the crisis.

Our research also shows that financial aid from commercial banks and/or the government does not reduce the probability of declining sales or supply (confirming the third hypothesis). The positive impact of this support was visible only in terms of exports. These undetectable effects of financial aid could be related to too little time elapsed since the first lockdown or low interest rates (excess liquidity of the banking system), observed in many developed countries.

Our results contribute to the rapidly emerging literature examining the direct impact of the pandemic on firms’ ability to operate and allow us to formulate some policy implications. We believe that the success of the recovery pace depends critically on the policy actions taken during the crisis. If policies ensure that workers do not become unemployed, firms do not go bankrupt and trade networks are preserved, the recovery will be faster and smoother. Our results underscore the fragility of businesses in sales and liquidity areas, especially in the short time after the pandemic began. Our results suggest that many of these firms had little cash on hand at the onset of the pandemic, meaning that they either had to drastically cut spending, take on additional debt or file for bankruptcy. It highlights how the immediacy of new financial resources can affect medium-term performance. This is a major recommendation for developed economies to ensure quick access to financial support, especially for small and medium firms.

Governments in developed countries can easily finance an extraordinary increase in spending even as their revenues fall. Countries with limited or no fiscal space face difficult choices and need the support of the international community. This is a case of many low-income and emerging economies facing capital flight—the challenge is even greater. This is why we recommend international institutions (e.g., the International Monetary Fund) to create a new financial support programme and help low-income countries create the right economic conditions for recovery at home.

We are aware that our research has some limitations. Some of them are related to the data. The surveys are mainly conducted in the World Bank client countries, and therefore, most of the high-income countries are not covered by the surveys (USA, Canada, Western European countries or Japan). This is why the comparison of the COVID-19 impact on private firms’ activities in developed and developing countries does not give a complete picture. Additionally, our research does not allow us to assess the impact of the COVID-19 pandemic on firms in more specific sectors. According to [48], the analysed impact depends strongly on the sector, particularly on the sectoral share of jobs that can still be performed under closure. However, the most significant limitation of our research is the inability to show the change in companies’ activities over time. Many things happened in the course of the year. In late spring 2020, many countries began to lift some restrictions after the first signs of recovery. However, in late autumn 2020, the second COVID-19 wave began, and restrictive measures were again introduced. In addition, some countries were affected by the third wave of the coronavirus, which came in the spring of 2021. Therefore, in future research, when the second survey will be accessible, we plan to examine what difference a year made in the impact of the pandemic COVID-19 on firms’ activities.

Further analysis is needed. The authors intend to extend research on the factors that determine the pandemic’s impact on various aspects of business activities. We plan to develop a predictive model using an innovative methodology, i.e., the fuzzy logic theory. It is a tool widely used in mechanical, robotic and industrial engineering for modelling imprecise, uncertain and ambiguous phenomena. The situation of many companies in the COVID-19 pandemic is influenced by many factors that often cannot be defined precisely. Hence, the fuzzy logic approach will increase the predictive power of planned analysis.

Author Contributions

Conceptualisation, both authors; literature review, M.O.; methodology, M.E.K.-C. software, M.E.K.-C.; formal analysis, M.E.K.-C.; investigation, both authors; resources, M.E.K.-C.; data curation, M.E.K.-C.; writing—original draft preparation, both authors, writing—review and editing, both authors; visualisation, M.E.K.-C. Both authors have read and agreed to the published version of the manuscript.

Funding

There was no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data used in the study were taken from http://www.enterprisesurveys.org (accessed on 7 April 2021).

Acknowledgments

We thank the Enterprise Analysis Unit of the Development Economics Global Indicators Department of the World Bank Group for making the data available.

Conflicts of Interest

The authors declare no conflict of interest.

References

- IMF. World Economic Outlook. 2021. Available online: https://www.imf.org/en/Publications/WEO/Issues/2021/03/23/world-economic-outlook-april-2021 (accessed on 2 April 2021).

- UNCTAD. Gender and Unemployment: Lessons from the COVID-19 Pandemic. 2021. Available online: https://unctad.org/news/gender-and-unemployment-lessons-covid-19-pandemic (accessed on 3 April 2021).

- ILO. ILO Monitor: COVID-19 and the World of Work. Updated Estimates and Analysis, 7th ed.; International Labour Organization, 2020; pp. 1–11. Available online: https://www.ilo.org/wcmsp5/groups/public/@dgreports/@dcomm/documents/briefingnote/wcms_767028.pdf (accessed on 30 March 2021).

- Arias-Calluari, K.; Alonso-Marroquin, F.; Najafi, M.N.; Harré, M. Methods for forecasting the effect of exogenous risks on stock markets. Phys. A Stat. Mech. Its Appl. 2020, 568, 125587. [Google Scholar] [CrossRef]

- Cai, D.; Hayakawa, K. Heterogeneous Impacts of COVID-19 on Trade: Evidence from China’ s Province-level Data. IDE Disscusion Pap. 2020, 803, 1–29. [Google Scholar]

- Friedt, F.; Zhang, K. The Triple Effect of Covid-19 on Chinese Exports: First Evidence of the Export Supply, Import Demand & GVC Contagion Effects. Covid Econ. 2020, 53, 72–109. [Google Scholar]

- Ludvigson, S.C.; Ma, S.; Ng, S. COVID-19 and The Macroeconomic Effects of Costly Disasters. Natl. Bur. Econ. Res. 2020, 1–24. Available online: https://www.nber.org/system/files/working_papers/w26987/w26987.pdf (accessed on 3 April 2021).

- Pardal, P.; Dias, R.; Šuleř, P.; Teixeira, N.; Krulický, T. Integration in Central European capital markets in the context of the global COVID-19 pandemic. Equilibrium. Q. J. Econ. Econ. Policy 2020, 15, 627–650. [Google Scholar] [CrossRef]

- Zinecker, M.; Doubravský, K.; Balcerzak, A.P.; Pietrzak, M.B.; Dohnal, M. The Covid-19 disease and policy response to mitigate the economic impact in the EU. Technol. Econ. Dev. Econ. 2021, 27, 742–762. [Google Scholar] [CrossRef]

- Wren-Lewis, S. The economic effects of a pandemic. In Economics in the Time of COVID-19; Baldwin, R., Weder di Mauro, B., Eds.; CEPR Press: London, UK, 2020; pp. 105–109. [Google Scholar]

- Barrero, J.M.; Bloom, N.; Davis, S.J. COVID-19 is also a reallocation shock. Brook. Pap. Econ. Act. 2020, 329–383. [Google Scholar] [CrossRef]

- Barua, S. Understanding Coronanomics: The Economic Implications of the Coronavirus (COVID-19) Pandemic. SSRN Electron. J. 2020, 1–44. Available online: https://ssrn.com/abstract=3566477 (accessed on 5 April 2021). [CrossRef]

- Coibion, O.; Gorodnichenko, Y.; Weber, M. The Cost of the COVID-19 Crisis: Lockdowns, Macroeconomic Expectations, and Consumer Spending. NBER Woking Pap. 2020, 27141, 1–51. [Google Scholar] [CrossRef]

- Carracedo, P.; Puertas Medina, R.; Luisa Martí Selva, M. Research lines on the impact of the COVID-19 pandemic on business. A text mining analysis. J. Bus. Res. 2020, 132, 586–593. [Google Scholar] [CrossRef]

- Carnevale, J.B.; Hatak, I. Employee adjustment and well-being in the era of COVID-19: Implications for human resource management. J. Bus. Res. 2020, 116, 183–187. [Google Scholar] [CrossRef]

- Donthu, N.; Gustafsson, A. Effect of COVID-10 on business and research. J. Bus. Res. 2020, 117, 284–289. [Google Scholar] [CrossRef]

- He, H.; Harris, L. The impact of Covid-19 pandemic on corporate social responsibility and marketing philosophy. J. Bus. Res. 2020, 116, 176–182. [Google Scholar] [CrossRef]

- Sheth, J. Impact of Covid-19 on consumer behavior: Will the old habits return or die? J. Bus. Res. 2020, 117, 280–283. [Google Scholar] [CrossRef]

- Pantano, E.; Pizzi, G.; Scarpi, D.; Dennis, C. Competing during a pandemic? Retailers’ ups and downs during the COVID-19 outbreak. J. Bus. Res. 2020, 116, 209–213. [Google Scholar] [CrossRef] [PubMed]

- Sharma, P.; Leung, T.Y.; Kingshott, R.P.J.; Davcik, N.S.; Cardinali, S. Managing uncertainty during a global pandemic: An international business perspective. J. Bus. Res. 2020, 116, 188–192. [Google Scholar] [CrossRef] [PubMed]

- Kirk, C.P.; Rifkin, L.S. I’ll trade you diamonds for toilet paper: Consumer reacting, coping and adapting behaviors in the COVID-19 pandemic. J. Bus. Mark. Manag. 2020, 117, 124–131. [Google Scholar] [CrossRef] [PubMed]

- Wang, Y.; Hong, A.; Li, X.; Gao, J. Marketing innovations during a global crisis: A study of China firms’ response to COVID-19. J. Bus. Res. 2020, 116, 214–220. [Google Scholar] [CrossRef]

- Eggers, F. Masters of disasters? Challenges and opportunities for SMEs in times of crisis. J. Bus. Res. 2020, 116, 199–208. [Google Scholar] [CrossRef]

- Woodside, A. Interventions as experiments: Connecting the dots in forecasting and overcoming pandemics, global warming, corruption, civil rights violations, misogyny, income inequality, and guns. J. Bus. Res. 2020, 117, 212–218. [Google Scholar] [CrossRef]

- Bartik, A.W.; Bertrand, M.; Cullen, Z.; Glaeser, E.L.; Luca, M.; Stanton, C. The impact of COVID-19 on small business outcomes and expectations. Proc. Natl. Acad. Sci. USA 2020, 117, 17656–17666. [Google Scholar] [CrossRef]

- Deloitte Managing supply chain risk and disruption COVID-19. Deloitte 2020, 1–15. Available online: https://www2.deloitte.com/global/en/pages/risk/cyber-strategic-risk/articles/covid-19-managing-supply-chain-risk-and-disruption.html (accessed on 27 April 2021).

- de Villiers, R. Accelerated Technology Adoption by Consumers During the COVID-19 Pandemic. J. Text. Sci. Fash. Technol. 2020, 6, 1–6. [Google Scholar] [CrossRef]

- Rinker, M.; Khare, C.; Padhye, S.; Fayman, K. Industry 4.0 Digital Transformation Conference—Has the Pandemic Accelerated Digital Transformation? J. Adv. Manuf. Process. 2020, 3. [Google Scholar] [CrossRef]

- Phillips, S. Working through the pandemic: Accelerating the transition to remote working. Bus. Inf. Rev. 2020, 37, 129–134. [Google Scholar] [CrossRef]

- Buchheim, L.; Dovern, J.; Krolage, C.; Link, S. Firm-level Expectations and Behavior in Response to the COVID-19 Crisis. IZA Discuss. Pap. 2020, 8304, 1–27. [Google Scholar]

- Borino, F.; Carlson, E.; Rollo, V.; Solleder, O. International firms and COVID-19: Evidence from a global survey. Covid Econ. Vetted Real-Time Pap. 2021, 30–59. [Google Scholar]

- Webster, A.; Khorana, S.; Pastore, F. The Labour Market Impact of COVID-19: Early Evidence for a Sample of Enterprises from Southern Europe. IZA Disscus. Pap. 2021, 14269, 1–37. [Google Scholar]

- Fairlie, R.W. The Impact of Covid-19 on Small Business Owners: The First Three Months After Social-Distancing Restrictions. NBER Work. Pap. 2020, 27462, 1–30. [Google Scholar]

- Humphries, J.E.; Neilson, C.; Ulyssea, G.; Haven, N.; Humphries, J.E.; Neilson, C. The evolving impacts of COVID-19 on small businesses since the CARES Act. Cowles Found. Discuss. Pap. 2020, 2230, 1–27. [Google Scholar] [CrossRef]

- Bosio, E.; Djankov, S.; Jolevski, F.; Ramalho, R. Survival of Firms during Economic Crisis. SSRN Electron. J. 2020, 9239. [Google Scholar] [CrossRef]

- Carletti, E.; Oliviero, T.; Pagano, M.; Pelizzon, L.; Subrahmanyam, M.G. The COVID-19 shock and equity shortfall: Firm-level evidence from Italy. Rev. Corp. Financ. Stud. 2020, 9, 534–568. [Google Scholar] [CrossRef]

- Apedo-Amah, M.C.; Avdiu, B.; Cirera, X.; Cruz, M.; Davies, E.; Grover, A.; Iacovone, L.; Kilinc, U.; Medvedev, D.; Maduko, F.O.; et al. Unmasking the Impact of COVID-19 on Businesses: Firm Level Evidence from across the World. 2020. Available online: https://elibrary.worldbank.org/doi/abs/10.1596/1813-9450-9434 (accessed on 30 May 2021).

- Adian, I.; Doumbia, D.; Gregory, N.; Ragoussis, A.; Reddy, A.; Timmis, J. Small and Medium Enterprises in the Pandemic: Impact, Responses and the Role of Development Finance. World Bank Policy Res. Pap. 2020, 9414, 1–35. [Google Scholar]

- Beglaryan, M.; Shakhmuradyan, G. The impact of COVID-19 on small and medium-sized enterprises in Armenia: Evidence from a labor force survey. Small Bus. Int. Rev. 2020, 4, 1–11. [Google Scholar] [CrossRef]

- Dai, R.; Feng, H.; Hu, J.; Jin, Q.; Li, H.; Wang, R.; Wang, R.; Xu, L. The Impact of COVID-19 and Medium-sized Enterprises: Evidence from Two-wave Phone. Cent. Glob. Dev. Work. Pap. 2020, 549, 1–27. [Google Scholar]

- Shinozaki, S.; Rao, L.N. COVID-19 Impact on Micro, Small, and Medium-Sized Enterprises under the Lockdown: Evidence from a Rapid Survey in the Philippines. ADB Econ. Work. Pap. Ser. 2021, 1216, 1–39. [Google Scholar]

- Balla-Elliott, D.; Cullen, Z.B.; Glaeser, E.L.; Stanton, C.T. Business Re-Opening During the COVID-19 Pandemic. Harv. Bus. Sch. Entrep. Manag. Work. Pap. 2020, 27362, 20–132. [Google Scholar] [CrossRef]

- Enterprise Surveys, The World Bank. Available online: http://www.enterprisesurveys.org (accessed on 7 April 2021).

- Amemiya, T. Qualitative response models: A survey. J. Econ. Lit. 1981, 19, 1483–1536. [Google Scholar]

- Diop, A.; Diop, A.; Dupuy, J.F. Maximum likelihood estimation in the logistic regression model with a cure fraction. Electron. J. Stat. 2011, 5, 460–483. [Google Scholar] [CrossRef]

- Gourieroux, C. Econometrics of Qualitative Dependent Variables; Cambridge University Press: Cambrige, UK, 2000. [Google Scholar] [CrossRef]

- Dieppe, A.; Francis, N.; Kawamoto, A.; Celik, S.K.; Kindberg-Hanlon, G.; Matsuoka, H.; Okawa, Y.; Okou, C. Global Productivity: Trends, Drivers, and Policies; World Bank Group-International Bank for Reconstruction and Development: Washington DC, USA, 2020. [Google Scholar]

- Dingel, J.I.; Neiman, B. How many jobs can be done at home? J. Public Econ. 2020, 189. [Google Scholar] [CrossRef]

Figure 1.

List of countries in the sample.

Figure 2.

The sample in the term of firm size.

Figure 3.

Performance of companies in various aspects depending on the sector.

Figure 4.

Distribution of the decline in sales by sector and region–dark red represents values between first quartile and Table 4.

Figure 4.

Distribution of the decline in sales by sector and region–dark red represents values between first quartile and Table 4.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Variables used in the study.

| Variable | Description |

|---|---|

| Man | 1 if it is a manufacturing company, 0 otherwise |

| Retail | 1 if it is a retail company, 0 otherwise |

| Service | 1 if it is an “other services” company, 0 otherwise |

| SalesD | 1 if the sales decreased (comparing to the same month in 2019), 0 otherwise* |

| ExportD | 1 if the exports decreased (comparing to the same month in 2019), 0 otherwise* |

| DemandD | 1 if the demand decreased (comparing to the same month in 2019), 0 otherwise |

| SupplyD | 1 if the supply decreased (comparing to the same month in 2019), 0 otherwise* |

| CFD | 1 if the cash flow decreased (comparing to the same month in 2019), 0 otherwise* |

| LCB | 1 if the primary aid source was a loan from a commercial bank, 0 otherwise |

| LNB | 1 if the primary aid source was a loan from a non-banking financial institution, 0 otherwise |

| EF | 1 if the primary aid source was equity finance, 0 otherwise |

| DP | 1 if the primary aid source was delaying payments to suppliers or workers, 0 otherwise |

| GG | 1 if the primary aid source was a government grant, 0 otherwise |

| OBA | 1 if the company started or increased business activity online, 0 otherwise |

| DA | 1 if the company started or increased delivery online, 0 otherwise |

| RW | 1 if the company started or increased remote work, 0 otherwise |

| TW | 1 if the company increased the number of temporary workers, 0 otherwise |

| Developed | 1 if a developed country, 0 otherwise |

| Developing | 1 if a developing country, 0 otherwise |

Source: Authors’ investigation. * Constant included but not reported. p-values are given in parentheses.

Table 2.

Percentage of companies that remained open or were temporarily or permanently closed.

| Sector | Remained Open | Temporarily Closed | Permanently Closed |

|---|---|---|---|

| Manufacturing | 90.2% | 5.9% | 4.0% |

| Retail | 89.6% | 6.4% | 4.0% |

| Other services | 84.1% | 10.7% | 5.2% |

Source: Authors’ investigation based on the World Bank’s Enterprise Surveys—COVID-19 Survey. Produced based on data taken from [43], World Bank, 2021. The World Bank approved the access to the World Bank Enterprise Survey Portal.

Table 3.

Percentage of companies that remained open or were temporarily or permanently closed.

| Mean | Median | Mode | Coefficient of Variation | Skewness | Min. | Max. | 90th Percentile | |

|---|---|---|---|---|---|---|---|---|

| Decrease in Sales (in Percentage Points) | ||||||||

| Manufacturing | 43.05 | 40 | 30 | 57.51 | 0.69 | 1 | 100 | 80 |

| Retail | 46.83 | 40 | 50 | 55.98 | 0.45 | 1 | 100 | 90 |

| Other services | 52.16 | 50 | 50 | 53.96 | 0.29 | 1 | 100 | 100 |

| Number of laid-off workers | ||||||||

| Manufacturing | 5.33 | 0 | 0 | 478.60 | 14.01 | 0 | 600 | 10 |

| Retail | 3.30 | 0 | 0 | 677.43 | 21.12 | 0 | 600 | 6 |

| Other services | 4.06 | 0 | 0 | 363.83 | 7.94 | 0 | 250 | 10 |

Source: Authors’ investigation based on the World Bank’s Enterprise Surveys—COVID-19 Survey Produced based on data taken from [43], World Bank, 2021. The World Bank approved the access to the World Bank Enterprise Survey Portal.

Table 4.

Logit binary model’s estimation results *.

| Variable | SalesD | ExportD | DemandD | SupplyD | ||||

|---|---|---|---|---|---|---|---|---|

| Coef. | Odds Ratio | Coef. | Odds Ratio | Coef. | Odds Ratio | Coef. | Odds Ratio | |

| Man | −0.022 (0.017) | 0.8057 | −0.934 (0.005) | 0.393 | −0.074 (0.308) | 0.928 | 0.060 (0.318) | 1.062 |

| Retail | −0.074 (0.531) | 0.9281 | −0.461 (0.333) | 0.630 | 0.057 (0.558) | 1.059 | 0.081 (0.301) | 1.084 |

| LCB | 0.132 (0.260) | 1.1409 | −0.680 (0.049) | 0.506 | 0.042 (0.666) | 1.043 | −0.021 (0.797) | 0.978 |

| LNB | 0.452 (0.662) | 1.5719 | ** | −0.189 (0.766) | 0.828 | −0.357 (0.522) | 0.699 | |

| EF | 0.447 (0.0000) | 1.5643 | −0.064 (0.859) | 0.937 | 0.316 (0.0003) | 1.375 | 0.052 (0.473) | 1.054 |

| DP | 0.462 (0.0009) | 1.5878 | −0.488 (0.219) | 0.613 | 0.351 (0.0017) | 1.421 | 0.009 (0.913) | 1.010 |

| GG | 0.235 (0.146) | 1.2644 | −0.382 (0.442) | 0.682 | 0.230 (0.099) | 1.258 | 0.171 (0.136) | 1.187 |

| OBA | −0.029 (0.783) | 0.9714 | −0.106 (0.714) | 0.899 | 0.132 (0.132) | 1.141 | 0.096 (0.188) | 1.101 |

| DA | −0.045 (0.667) | 0.9554 | 0.595 (0.086) | 1.813 | −0.140 (0.104) | 0.869 | 0.060 (0.411) | 1.062 |

| RW | −0.034 (0.691) | 0.9658 | −0.364 (0.135) | 0.694 | −0.104 (0.147) | 0.901 | −0.130 (0.029) | 0.877 |

| TW | −1.177 (0.0000) | 0.3080 | −1.747 (0.0000) | 0.174 | 1.068 (0.0000) | 0.344 | −0.861 (0.0000) | 0.422 |

| Support | 0.224 (0.018) | 1.2514 | −0.219 (0.430) | 0.803 | 0.240 (0.003) | 1.271 | 0.096 (0.134) | 1.101 |

| Developed | −0.599 (0.0000) | 0.5493 | 1.924 (0.0000) | 6.847 | −0.424 (0.0000) | 0.654 | −0.504 (0.0000) | 0.603 |

| Developing | 0.476 (0.0003) | 1.6097 | 1.772 (0.0000) | 5.885 | 0.360 (0.0000) | 1.433 | 0.711 (0.0000) | 2.036 |

| Obs. No. | 8735 | 4033 | 8520 | 8668 | ||||

| R2 | 0.093 | 0.105 | 0.081 | 0.043 | ||||

| cCor. pred. | 91.4% | 98% | 86.4% | 77.7% | ||||

| LR test | 172.597 (0.0000) | 82.178 (0.0000) | 147.613 (0.0000) | 400.9 (0.0000) | ||||

* Constant included but not reported. p-values are given in parentheses. ** Dropped Prob(ExportD = 1|LNB = 1) = 1. Variable service and CFD were not included in the model due to the collinearity. Source: Authors’ investigation based on the World Bank’s Enterprise Surveys—COVID-19 Survey Produced based on data taken from [43], World Bank, 2021. The World Bank approved the access to the World Bank Enterprise Survey Portal.

Table 5.

Logit binary model’s estimation results *—sales decrease.

| Variable | Manufacturing | Services | Retail | |||

|---|---|---|---|---|---|---|

| Coef. | Odds Ratio | Coef. | Odds Ratio | Coef. | Odds Ratio | |

| LCB | 0.303 (0.063) | 1.354 | 0.061 (0.776) | 1.063 | −0.248 (0.365) | 0.780 |

| LNB | −0.348 (0.745) | 0.705 | ** | ** | ||

| EF | 0.429 (0.025) | 1.535 | 0.645 (0.002) | 1.906 | 0.198 (0.454) | 1.219 |

| DP | 0.539 (0.005) | 1.715 | 0.321 (0.218) | 1.379 | 0.408 (0.204) | 1.504 |

| GG | 0.156 (0.462) | 1.168 | 0.218 (0.491) | 1.244 | 0.468 (0.265) | 1.597 |

| OBA | 0.101 (0.496) | 1.106 | −0.214 (0.268) | 0.807 | 0.012 (0.961) | 1.012 |

| DA | 0.228 (0.142) | 1.256 | −0.158 (0.412) | 0.854 | −0.597 (0.011) | 0.550 |

| RW | −0.0413 (0.723) | 0.959 | −0.177 (0.287) | 0.838 | 0.233 (0.303) | 1.262 |

| TW | −0.836 (0.003) | 0.433 | −1.655 (0.000) | 0.191 | −1.400 (0.001) | 0.246 |

| Support | 0.086 (0.493) | 1.090 | 0.637 (0.001) | 1.891 | 0.099 (0.663) | 1.104 |

| Developed | −0.403 (0.007) | 0.667 | −1.068 (0.000) | 0.344 | −0.425 (0.111) | 0.653 |

| Developing | 0.454 (0.005) | 1.575 | 0.476 (0.032) | 1.610 | 0.517 (0.050) | 1.677 |

| Obs. No. | 4295 | 2820 | 1620 | |||

| R2 | 0.024 | 0.062 | 0.041 | |||

| Cor. pred. | 90.2% | 92.8% | 92.1% | |||

| LR test | 66.535 (0.0000) | 91.55 (0.0000) | 36.948 (0.0001) | |||

* Constant included but not reported. p-values are given in parentheses. ** Dropped Prob(Y = 1|X = 1) = 1. Variable CFD was not included in the model due to the collinearity. Source: Authors’ investigation based on the World Bank’s Enterprise Surveys—COVID-19 Survey. Produced based on data taken from [43], World Bank, 2021. The World Bank approved the access to the World Bank Enterprise Survey Portal.

Table 6.

Logit binary model’s estimation results *—export decrease.

| Variable | Manufacturing | Services | Retail | |||

|---|---|---|---|---|---|---|

| Coef. | Odds Ratio | Coef. | Odds Ratio | Coef. | Odds Ratio | |

| LCB | −0.847 (0.0371) | 0.428 | 0.088 (0.923) | 1.0925 | −1.568 (0.248) | 0.208 |

| LNB | ** | ** | ** | |||

| EF | −0.090 (0.834) | 0.913 | −0.272 (0.721) | 0.762 | 0.183 (0.896) | 1.201 |

| DP | −0.782 (0.087) | 0.457 | 0.308 (0.790) | 1.360 | 0.240 (0.882) | 1.272 |

| GG | −0.717 (0.203) | 0.488 | ** | −0.380 (0.824) | 0.683 | |

| OBA | 0.303 (0.407) | 1.354 | −1.507 (0.036) | 0.222 | −0.491 (0.620) | 0.611 |

| DA | 0.784 (0.078) | 2.191 | 1.064 (0.219) | 2.899 | −0.378 (0.677) | 0.684 |

| RW | −0.300 (0.2831) | 0.740 | −0.183 (0.791) | 0.832 | −1.154 (0.236) | 0.315 |

| TW | −1.690 (0.0009) | 0.184 | −1.602 (0.157) | 0.201 | −1.337 (0.298) | 0.262 |

| Support | −0.011 (0.973) | 0.988 | −0.149 (0.843) | 0.861 | −1.908 (0.064) | 0.148 |

| Developed | 1.713 (0.0000) | 5.548 | 2.815 (0.002) | 16.702 | 3.965 (0.001) | 52.756 |

| Developing | 1.595 (0.0000) | 4.930 | 2.132 (0.004) | 8.440 | 3.045 (0.015) | 21.022 |

| Obs. No. | 2340 | 1078 | 615 | |||

| R2 | 0.081 | 0.173 | 0.317 | |||

| Cor. pred. | 97.4% | 99.0% | 98.7% | |||

| LR test | 45.528 (0.0000) | 21.178 (0.0199) | 27.061 (0.0045) | |||

* Constant included but not reported. p-values are given in parentheses. ** Dropped Prob(Y = 1|X = 1) = 1. Variable CFD was not included in the model due to the collinearity. Source: Authors’ investigation based on the World Bank’s Enterprise Surveys—COVID-19 Survey. Produced based on data taken from [43], World Bank, 2021. The World Bank approved the access to the World Bank Enterprise Survey Portal.

Table 7.

Logit binary model’s estimation results *—demand decrease.

| Variable | Manufacturing | Services | Retail | |||

|---|---|---|---|---|---|---|

| Coef. | Odds Ratio | Coef. | Odds Ratio | Coef. | Odds Ratio | |

| LCB | 0.017 (0.229) | 1.185 | 0.086 (0.621) | 1.09 | −0.450 (0.051) | 0.6376 |

| LNB | −0.522 (0.564) | 0.5931 | −0.370 (0.734) | 0.691 | ** | |

| EF | 0.341 (0.005) | 1.4069 | 0.425 (0.008) | 1.530 | 0.023 (0.915) | 1.023 |

| DP | 0.523 (0.001) | 1.688 | 0.008 (0.967) | 1.008 | 0.408 (0.139) | 1.504 |

| GG | 0.110 (0.553) | 1.1164 | 0.422 (0.116) | 1.525 | 0.246 (0.484) | 1.279 |

| OBA | 0.220 (0.079) | 1.2465 | −0.111 (0.465) | 0.894 | 0.359 (0.092) | 1.432 |

| DA | 0.043 (0.730) | 1.0444 | −0.171 (0.257) | 0.842 | −0.621 (0.002) | 0.537 |

| RW | −0.170 (0.081) | 0.8434 | −0.115 (0.384) | 0.891 | 0.144 (0.441) | 1.155 |

| TW | −1.229 (0.0000) | 0.2925 | −0.744 (0.028) | 0.475 | −1.094 (0.009) | 0.334 |

| Support | 0.192 (0.079) | 1.2117 | 0.278 (0.059) | 1.320 | 0.304 (0.122) | 1.355 |

| Developed | −0.292 (0.020) | 0.7465 | −0.623 (0.0003) | 0.536 | −0.426 (0.061) | 0.652 |

| Developing | 0.336 (0.0113) | 1.3969 | 0.388 (0.017) | 1.474 | 0.358 (0.103) | 1.430 |

| Obs. No. | 4223 | 2716 | 1581 | |||

| R2 | 0.029 | 0.026 | 0.038 | |||

| Cor. pred. | 85.3% | 87.3% | 87.8% | |||

| LR test | 77.395 (0.0000) | 54.195 (0.0000) | 41.887 (0.0000) | |||

* Constant included but not reported. p-values are given in parentheses. ** Dropped Prob(Y = 1|X = 1) = 1. Variable CFD were not included in the model due to the collinearity. Source: Authors’ investigation based on the World Bank’s Enterprise Surveys—COVID-19 Survey. Produced based on data taken from [43], World Bank, 2021. The World Bank approved the access to the World Bank Enterprise Survey Portal.

Table 8.

Logit binary model’s estimation results *—supply decrease.

| Variable | Manufacturing | Services | Retail | |||

|---|---|---|---|---|---|---|

| Coef. | Odds Ratio | Coef. | Odds Ratio | Coef. | Odds Ratio | |

| LCB | 0.083 (0.483) | 1.087 | −0.067 (0.651) | 0.935 | −0.217 (0.278) | 0.804 |

| LNB | −0.475 (0.560) | 0.621 | −0.234 (0.829) | 0.790 | −0.419 (0.705) | 0.657 |

| EF | 0.089 (0.385) | 1.093 | 0.079 (0.545) | 1.082 | −0.071 (0.691) | 0.930 |

| DP | 0.312 (0.021) | 1.366 | −0.326 (0.0387) | 0.721 | −0.148 (0.459) | 0.861 |

| GG | 0.070 (0.654) | 1.072 | 0.239 (0.273) | 1.269 | 0.397 (0.160) | 1.488 |

| OBA | 0.281 (0.009) | 1.325 | −0.134 (0.294) | 0.874 | 0.045 (0.787) | 1.046 |

| DA | 0.020 (0.848) | 1.020 | 0.261 (0.047) | 1.299 | −0.194 (0.245) | 0.823 |

| RW | −0.099 (0.230) | 0.905 | −0.198 (0.067) | 0.820 | −0.076 (0.607) | 0.926 |

| TW | −0.871 (0.0001) | 0.418 | −0.748 (0.012) | 0.473 | −0.967 (0.012) | 0.380 |

| Support | 0.062 (0.479) | 1.064 | 0.138 (0.242) | 1.148 | 0.150 (0.335) | 1.162 |

| Developed | −0.570 (0.0000) | 0.565 | −0.379 (0.005) | 0.684 | −0.509 (0.005) | 0.600 |

| Developing | 0.525 (0.0000) | 1.691 | 0.957 (0.0000) | 2.606 | 0.734 (0.0000) | 2.085 |

| Obs. No. | 4279 | 2772 | 1617 | |||

| R2 | 0.041 | 0.056 | 0.046 | |||

| Cor. pred. | 76.5% | 78.4% | 79.4% | |||

| LR test | 194.54 (0.0000) | 164.83 (0.0000) | 76.561 (0.0000) | |||

* Constant included but not reported. p-values are given in parentheses. Variable CFD was not included in the model due to the collinearity. Source: Authors’ investigation based on the World Bank’s Enterprise Surveys—COVID-19 Survey. Produced based on data taken from [43], World Bank, 2021. The World Bank approved the access to the World Bank Enterprise Survey Portal.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Olczyk, M.; Kuc-Czarnecka, M.E. Determinants of COVID-19 Impact on the Private Sector: A Multi-Country Analysis Based on Survey Data. Energies 2021, 14, 4155. https://0-doi-org.brum.beds.ac.uk/10.3390/en14144155

AMA Style

Olczyk M, Kuc-Czarnecka ME. Determinants of COVID-19 Impact on the Private Sector: A Multi-Country Analysis Based on Survey Data. Energies. 2021; 14(14):4155. https://0-doi-org.brum.beds.ac.uk/10.3390/en14144155

Chicago/Turabian StyleOlczyk, Magdalena, and Marta Ewa Kuc-Czarnecka. 2021. "Determinants of COVID-19 Impact on the Private Sector: A Multi-Country Analysis Based on Survey Data" Energies 14, no. 14: 4155. https://0-doi-org.brum.beds.ac.uk/10.3390/en14144155

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.