Effectiveness and Benefits of the Eco-Management and Audit Scheme: Evidence from Polish Organisations

Institute of Management, Poznań University of Economics and Business, Al. Niepodległości 10, 61-875 Poznań, Poland

*

Author to whom correspondence should be addressed.

Energies 2022, 15(2), 434; https://0-doi-org.brum.beds.ac.uk/10.3390/en15020434

Submission received: 1 December 2021

/

Revised: 16 December 2021

/

Accepted: 1 January 2022

/

Published: 7 January 2022

(This article belongs to the Special Issue Process and System Approach to Achieve Energy Efficiency)

Abstract

:Climate change and environmental pollution are considered to be among the main challenges faced by the modern world. The growth of environmental awareness and the adoption of a pro-environmental approach are considered to be the key megatrends with the greatest impact on the global economy in the upcoming years. According to Eurobarometer, EU citizens are particularly aware of the importance of protecting the environment. Although the negative environmental impact of European industry has improved over the past decades, EU citizens believe that there is further scope in terms of helping companies transition towards adopting more sustainable models. One of the factors contributing to the reduction in negative environmental impact is the participation of enterprises in voluntary programs such as the Environmental Management System (EMS), according to ISO 14001, or the Eco-management and Audit Scheme (EMAS). The whole population of Polish companies registered under the EMAS was included in the study and although the sample size was small, it was a full study, and for that reason allows for the generalisation and conclusion regarding the whole population of EMAS-registered companies in Poland. The results of the study conducted on EMAS-registered organisations in Poland in 2015 suggest that the average effectiveness of the EMAS observed between 2007 and 2014 was 66.4%. The aim of this study was to review the changes in EMAS effectiveness and benefits obtained by participating organisations after five years. The results indicate that the average effectiveness during the period of 2015–2020 increased to 79.1%; nevertheless, registered organisations recognise fewer benefits for participation in the scheme. The study has shown that as EMAS matures in organisations, it becomes more effective. It influences a lot of factors, such as environmental awareness and management commitment, the use of SRDs (including BEMPs), environmental performance indicators for specific sectors, the criteria for the excellence of assessing the level of environmental performance, and the skilful use of indicators in organisations.

1. Introduction

A total of 3838 organisations, including 65 organisations in Poland [1], are registered under the EU Eco-management and Audit Scheme (EMAS) (May 2021); in this context, Poland ranks 6th globally. The countries with more registrations than Poland are Germany (1131), Italy (1010), Spain (962), Austria (262), and Cyprus (67) [1]. The trend of EMAS registration has been decreasing since its peak in 2010 (4615 organisations). The negative trend may be attributed to a lack of resources for environmental investment [2,3] and the short-term orientation of many organisations, considering that environmental investments generally have a long-term return [4]. Many organisations registered under the EMAS scheme do not renew their registrations, because, among other reasons, they do not achieve the expected benefits in relation to the expenditures and outlays, they have problems updating the environmental statement, they do not receive regulatory concessions such as tax reliefs and, in general, they are disappointed by the lack of incentives from the member states and public administration [2,5,6]. Moreover, developed by the International Organisation for Standardisation (ISO), the environmental management system based on ISO 14001 is over 100 times more popular than EMAS, with 396,242 valid ISO 14001 certificates issued worldwide, including 92,828 in Europe and 3766 in Poland [7]. However, the EMAS requirements are higher than the requirements of the ISO 14001 standard. The organisation should demonstrate continuous compliance with legislation regarding environmental protection, publish a validated environmental statement on an annual basis and undergo verification and registration. It is more costly, both in time and money used.

This study aims to evaluate whether the effectiveness of EMAS in Polish organisations has changed in the last five years along with the range of benefits and incentives for registered organisations. EMAS, as an environmental management tool, shall contribute to the transition of a linear economy to a circular economy (CE) [8] on a micro-scale (organisational scale) and consequently towards sustainable development. Therefore, it is important to continually monitor its effectiveness. The European Commission builds EMAS as a brand based on key attributes such as ‘performance’, ‘credibility’, and ‘transparency’. It promotes the factors behind the implementation of EMAS, which include the improvement of environmental performance and resource efficiency, climate protection, corporate social responsibility, the achievement of legal compliance, improvement in supply chain management, green procurement, improvement in the image of the organisation through credible information (transparent and validated reporting), an increase in the engagement of employees, and an influence on the stakeholder’s involvement [9]. EMAS also encourages the development of financial incentives, such that organisations, particularly micro and small and medium enterprises (SMEs), may join the scheme [10].

2. Description of EMAS

The EMAS legislation has been updated three times since its original introduction in 1993 (EWG No 1836/93) [11]. The second revision was released in 2001 (EC 761/2001), and the third revision in 2009 (EC 1221/2009). The fourth revision of the EMAS, published in 2017 (EC 2017/1505) was aimed at introducing amendments to annexes to include the changes associated with the revision of the ISO 14001:2015 (Annex I Environmental Review, Annex II EMS Requirements and additional Issues to be addressed by organisations implementing EMAS and Annex III Initial Environmental Audit). Annex IV of the EMAS regulation was amended in 2018 (EC 2018/2026). The latest revision includes a modification of the requirements for environmental reporting (EMAS core indicators) and the language of environmental statements, new opportunities to report on environmental performance, and the use of EMAS environmental statements for other reporting obligations [12]. The European Commission also publishes Sectoral Reference Documents (SRDs) on the best environmental management practices (BEMP), environmental performance indicators, and benchmarks of excellence. Such documents provide guidance and inspiration to organisations in specific sectors and industries for improving environmental performance, which may stimulate them to implement continual improvement actions. Official SRDs are published for eight sectors (retail trade, tourism, food and beverage manufacturing, car manufacturing, electrical and electronic equipment manufacturing, public administration, agriculture, and waste management). Publications considering more sectors are in progress (construction, telecommunications, and the manufacture of fabricated metal products). SRDs and BEMPs must be taken into account by organisations when applying for EMAS registration and those already registered in the EMAS. SRDs are available in all official languages of the EU and can be used by any organisation, irrespective of whether they are registered in the EMAS.

EMAS-registered organisations are obliged to communicate their environmental aspects and objectives, environmental performance indicators, and other relevant environmental information publicly available and validated by an accredited verifier annual statement. Measuring environmental performance is a crucial aspect of EMAS. The analysis of relevant indicators enables organisations to avail measurable information concerning their environmental performance and the effectiveness of their environmental activities. Studies on EMAS oriented towards effectiveness analysis and environmental performance have been conducted by Erkko et al. [13], Pedersen [14], Iraldo et al. [15,16], Daddi et al. [17], Mazzi et al. [18], Matuszak-Flejszman et al. [19], Janik and Szafraniec [20], and Heras-Saizarbitoria et al. [21].

EMAS Core performance indicators focus on six areas: energy, material, water, waste, land use concerning biodiversity, and emissions. Although Annex IV of the EMAS regulations (Environmental Reporting) has been recently updated, the core EMAS indicators are focused on operational performance rather than the consideration of a mixture of different types of indicators (OPI–Operational Performance Indicator, MPI–Management Performance Indicator, ECI–Environmental Condition Indicator) as defined by ISO 14031 (2013). Moreover, the core EMAS indicators cover only organisational direct environmental aspects. EMAS requires the registered organisations to manage and improve direct and indirect environmental aspects; thus, it would be reasonable to include indicators related to indirect aspects, as well. The current definition of core EMAS indicators is inadequate for organisations, as the direct aspects are not considered to be significant [19]. Annex IV, covering reporting based on environmental performance indicators, has been improved in a few areas:

- –

- The opportunity for organisations to report qualitative information when quantitative data are not available;

- –

- Clarification regarding the fact that reporting shall cover at least three years of activity;

- –

- The removal of the word ‘efficiency’ from the energy and material indicator title;

- –

- Change of ‘Biodiversity indicator’ into ‘Land use regarding biodiversity’;

- –

- The clarification of calculation methods;

- –

- The addition of acceptable measurement units in each area;

- –

- In the context of energy, the differentiation between ‘total renewable energy consumption’ and ‘total renewable energy generation’;

- –

- Regarding material, clarification that when different types of materials are used, the annual mass-flow should be reported separately, as appropriate;

- –

- The clarification of the indicator in the context of land use;

- –

- Regarding emissions, reference encouraging organisations to report their greenhouse gas emissions according to an established methodology (e.g., Greenhouse Gas Protocol);

- –

- The clarification of the requirements enabling the comparability of reported indicators over time;

- –

- The additional requirement to monitor significant direct and indirect environmental impacts related to core business activities that are not covered by the core indicators.

The EMAS intends to be one of the main EU instruments that support and accelerate the transition from a linear economy to a CE on a micro-scale (organisational level). EMS and eco-design have been recognised as tools with the highest level of integration with a CE [22]. CE practices and the performance of EMAS-registered organisations have been assessed for SMEs in Spain [23] and Poland [20]. It was concluded that EMAS organisations use various indicators related to the main elements of a CE. However, their method of quantifying CE practices is not uniform. Most CE indicators focus on the preservation of materials via strategies such as recycling [24], but there is no common standard for measuring circularity at the micro-level [25]. CE assessment has a low level of maturity, and the level of implementation of CE approaches by organisations is limited [26].

3. Materials and Methods

The study has been carried out in two phases: (1) a study conducted in 2015 covering a research period of 2007–2014, (2) a study conducted in 2021 covering a research period of 2015–2020. The detailed results of the first phase have been published in Matuszak-Flejszman et. al. [19]. This paper contains results and discussion based on the results of the second phase of the study along with a comparative analysis between phase one and phase two. This paper aims to review and evaluate the (a) changes in the effectiveness of the EMAS in Polish organisations and (b) changes in the benefits and incentives among EMAS-registered organisations after five years. The phase two study tests two research hypotheses:

Hypotheses 1 (H1).

The effectiveness of the EMAS during the period of 2015 to 2020 is higher than that during the period of 2008 to 2014.

Hypotheses 2 (H2).

The benefits derived from EMAS registration are perceived to be higher in 2020 when compared to 2015.

The first hypothesis is based on the theory of ‘the law of efficiency fall down’. Implementing a new management system is an organisational change. Studies focused on changes in management indicate that companies may face a temporary reduction in effectiveness after change implementation owing to ‘the law of efficiency fall down’ and the learning curve [27].

The second hypothesis suggests that organisations that continue to be registered in the EMAS shall notice more benefits and incentives over time.

The study was conducted on EMAS-registered organisations in Poland. The same research tool was used during phase one in 2015 and during phase two in 2021. The data was collected using the combination of two methods and sources: (1) primary sources—a survey questionnaire and (2) secondary sources—the review of data in environmental statements. The study covered the whole population of EMAS-registered organisations in Poland, as detailed in Table 1.

The survey questionnaire was based on CAWI (Computer Assisted Web Interview). CAWI questionnaires appear in the browser as a webpage that respondents can reach in various ways. The computerised environment makes it possible to filter and implement logical relationships taking place in the background so that only questions to be answered appear on the screen. The responses to the questionnaire are immediately sent to the main server, thanks to which the data collection and results can be tracked continuously. The advantages of CAWI compared to traditional paper questionnaires are lower costs, shorter time of data collection and processing, and no geographic restrictions. The questionnaire contained 18 questions. The link to the questionnaire was sent directly to organisations’ environmental representatives to ensure the reliability of the collected data. E-mail addresses in companies often consist of name and surname (which, according to GDPR, is classified as personal data). These data came from publicly available sources and are not sensitive (they do not concern health, genetic information, intimate life, political views, ethnicity, beliefs, and religious beliefs). At the time of the second phase of the study, there were 65 organisations registered in the Polish EMAS register, and 61.5% responded to the questionnaire (Table 1).

Secondary sources contained data published by all registered organisations, publically available through the EMAS register managed by the General Directorate for Environmental Protection website. We analysed data related to the description of environmental objectives and targets and data on the environmental performance of all organisations registered in the EMAS register during the study (Table 1).

The study did not involve methods of continuous tracking or the observation of participants. Participants were involved only in completing survey questionnaires (anonymous responses analysed collectively without the identification of individual respondents). The industry with the maximum number of registered organisations in Poland operates in four main sectors: (1) public administration, (2) waste management, (3) electricity production and supply, and (4) water supply and wastewater management.

4. Results and Discussion

4.1. EMAS Effectiveness Based on Objectives

The environmental statements of the organisations include a description of the objectives and targets related to significant environmental aspects and impacts. The study focused on assessing the effectiveness of the EMAS based on the number of environmental objectives set by organisations and the number of achieved environmental objectives in each reporting year (expressed as a percentage). The total number of measurements is provided in Table 2. The number of measurements in a particular calendar year equals the number of organisations registered in the EMAS. In total, 544 environmental statements were analysed during the study, including 187 during the first phase and 357 during the second phase.

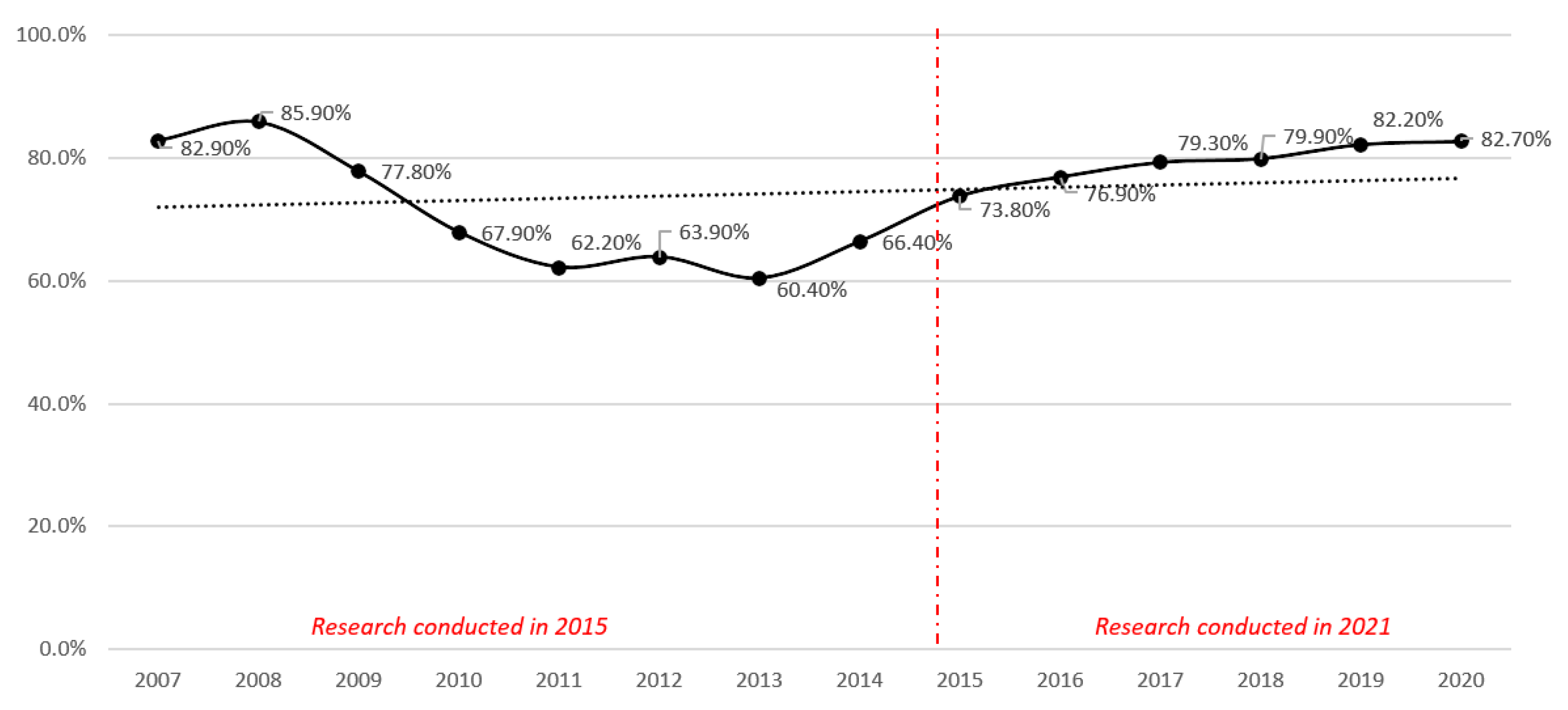

The results show that the average effectiveness increased from 66.4% between 2007 and 2014 to 79.1% between 2015 and 2020 (Figure 1). The analysis indicates that the greatest effectiveness was achieved in 2008 when only 11 organisations were registered in EMAS. From 2007 to 2014, the effectiveness varied substantially (9.9% standard deviation). In the subsequent years, the effectiveness of achieving environmental objectives dropped; however, in 2014, it started to increase again. Finally, the effectiveness has stabilised (3.4% standard deviation) since 2015. These results partly positively verify H1 (the effectiveness of EMAS in the 2015 to 2020 period was higher than that in the 2008 to 2014 period). The average effectiveness is higher. However, the individual effectiveness is not, because the most effective year was 2008. This may be related to economic cycles and the response to the economic crisis of 2008, which may have resulted in lower environmental efficiency by 2013. During the economic growth and boom phase, businesses tend to increase their investments. This may also apply to environmental investments, which consequently leads to the increased effectiveness of achieving environmental objectives. The investments made in a certain period of time usually give a return in the later periods. It should also be emphasised that in the initial years after the implementation of EMAS, the environmental effects resulting from the organisation’s activities are more visible, which also translated into the greater efficiency of the EMAS until 2008. In addition, they show that the maturity of the EMAS system positively influences its effectiveness. They also indicate that the requirements related to the application of BEMPs contained in the SRDs may significantly contribute to an increase in effectiveness. Out of the total number of organisations registered in the Polish EMAS, 30% are operating in the public administration sector and 24% are in the waste management sector [28]. The SRD for public administration and waste management were introduced in 2019 and 2020, respectively. Future research may focus on evaluating whether the use of SRDs affects the effectiveness of the EMAS scheme and comparing the effectiveness of organisations in a particular sector before and after the implementation of SRD. Figure 1 shows that the trend in the effectiveness of environmental objective implementation is stable (trend line indicated by the black dotted line).

Although transparency is one of the key EMAS principles, the information regarding the non-achievement of environmental goals is not required to be disclosed in environmental statements. During the study, 36.9% of organisations did not report their reasons for not achieving their objectives in their environmental statements (compared to 32.1% in the 2015 study). Based on the information collected from organisations over time, the major reasons for the non-achievement of objectives have been selecting too short a timeframe, changing priorities and strategies, and setting too-ambitious objectives.

As shown in Figure 2, fewer objectives were set for energy, water, and waste management; more objectives were set for materials, emissions, biodiversity, and other areas; and a major difference was observed in the objectives related to emissions between 2015 and 2020. This proves that issues related to climate change and the carbon footprint have gained importance in the last few years. Climate action is one of the Sustainable Development Goals (SDGs) set by the United Nations [29].

Environmental objectives fixed in other areas (mainly by public administration authorities) were related to indirect environmental aspects (such as ensuring the effective and stable protection of nature reserves, preserving naturally valuable areas, protecting fauna and flora through effective decisions, providing environmental education to society, and ensuring the environmental awareness of employees).

4.2. EMAS Effectiveness Based on Performance Indicators

In general, the EMAS requires the monitoring of core environmental performance indicators. Organisations may not report all core indicators when one or more of them are not relevant to significant direct environmental aspects. In such cases, organisations need to provide reasons explaining why they have decided not to monitor a particular indicator. An analysis of the data obtained for the current study showed that about one-third of organisations do not monitor some core indicators (Figure 3). The most common reason is that core indicators are defined only for direct environmental aspects. For organisations where direct environmental aspects are not considered significant (such as public administration), core indicators are inadequate and do not show the size of the environmental impact.

The current study found a major difference in energy, water, and waste. Similar areas were indicated for not setting up environmental objectives. The difference may be that there were only four public administration organisations registered in EMAS in 2015, and, by 2020, an additional 16 public administration organisations (Regional Directorates for Environmental Protection) had been registered. In the Polish case, many public administrations rent office space and pay a flat rate for energy, water consumption, and waste disposal. This often means that it is technically impossible to measure utility usage owing to a lack of separate infrastructure to monitor actual consumption. In these cases, public authorities pay a flat rate for energy, water consumption, and waste disposal. Organisations that lease their premises do not often measure the indicator related to land use concerning biodiversity. The reason is that they cannot influence the indicator, as the areas are managed by property managers who decide on land usage.

It was observed that more organisations monitored other environmental indicators in 2021 compared to 2015. As presented in Figure 4, the other indicators were related to operational activities (OPI), managerial activities (MPI), and environmental conditions (ECI).

The most significant difference was in the MPI monitoring, which indicated that the gravity of the environmental management system is gradually moving from the operational level to the strategic level. In the beginning, most environmental management systems were implemented and managed only at the operational level and were rarely related to strategic planning [30]. Consequently, environmental objectives were often unsuccessful and ineffective. Currently, owing to increased societal expectations on organisations’ environmental and social responsibility, more organisations are treating environmental issues as a new area of interest to stand out strategically [31]. Research shows that as organisations’ strategic commitment to environmental issues becomes more evident, environmental management positively impacts competitive advantage and organisational culture and strengthens business strategy [32]. Building effective management systems requires the integration of environmental objectives into organisational strategy [33]. Therefore, this evident transition from the operational to the strategic level may have been one factor that has contributed to increasing EMAS effectiveness over the last few years. Increasing awareness of the importance of protecting the environment may have contributed to the conjuncture in which environmental issues have become a strategic necessity rather than just a strategic advantage.

For organisations that monitor EMAS core indicators, the current study examined the trend of each indicator (increasing, decreasing, or stable). The weighted index was calculated to determine if the overall change was positive or negative. The results are presented in Table 3.

The results showed that organisations achieved positive change in each environmental indicator area, except emissions. The data confirmed the growing importance of environmental issues in organisations and the positive impact of the SDGs on organisations’ environmental activities. The most significant positive difference in indicators was seen in the energy performance area, though this may have been caused by the fact that energy management and efficiency have gained importance in the institutional policies of most developed countries [34]. Conversely, this may be related to the growing interest of organisations in implementing the Energy Management System according to ISO 50,001 [35]. The results of an ISO Survey have indicated that, in 2015, there were 11,985 certified organisations worldwide (including 74 in Poland), and in 2020, there were 19,731 valid certificates (including 178 in Poland) [7]. The ISO 50,001 standard seems to be very helpful and necessary for enabling organisations to follow a systematic approach in achieving continual improvement in energy performance, including energy efficiency, energy security, energy use, and consumption. More and more organisations are using renewable energy sources, such as photovoltaic panels or wind energy, and are paying attention to the energy efficiency of machines and devices when buying new infrastructure. In addition, a recent trend of replacing lighting with LEDs may have also contributed to these results. Previous researchers have said that an energy management system based on ISO 50,001 is an important tool for supporting efficient energy use in any organisation and implementing CE principles [36].

4.3. Benefits and Incentives

The benefits were evaluated based on the results of the survey questionnaire (primary data) in four areas: (1) business management and marketing, (2) economic and financial, (3) social, (4) ecological and environmental. The five-point scale was used, where 1 indicated no benefits and 5 indicated great benefits. As shown in Figure 5, in each area, the benefits in 2020 were assessed as lower than in 2015. Based on this evidence, the second hypothesis, H2: Benefits of EMAS registration were perceived higher in 2020 compared to 2015, was verified negatively.

In the first group, the highest decrease was observed in investors’ interest and competitiveness. As presented in Table 4, the highest increase was observed in achieving legal compliance. This may confirm that organisations’ environmental issues have become a necessity rather than a factor for improving competitiveness.

In the second group, all factors were assessed as lower and lowest on average. Economic or financial benefits were gained almost exclusively by managing direct environmental aspects (through rational management of raw materials) and not through any financial incentives from policymakers, government, or other institutions. The dedailed results have been presented in Table 5. This confirms that a lack of incentives may negatively impact the implementation and maintenance of the EMAS in organisations. Similar conclusions have been made in studies conducted in other countries [3,37,38].

The factors in the third group were ranked highest on average. As presented in Table 6, the highest increase was observed in employee engagement, the highest decrease was observed in the reduction in the number of breakdowns and accidents and response to failures. The increase in the area of employee engagement is related to the increasing environmental awareness of employees, and, thus, greater involvement in activities aimed at minimising the negative impact on the environment. In contrast, the number of breakdowns and accidents are, by definition, emergencies, thus, the EMAS may or may not directly impact these issues.

In the fourth group, improvements were observed in consumption reduction (including fuels, electricity, or water). As shown in Table 7, the highest decrease was observed in the removal of harmful substances from technology. This may be related to more stringent legal requirements, environmental awareness in society, and the environmental strategies of organisations. Research has shown that in Italy and Germany, in particular, the EMAS is positively correlated with the number of patents, including green patents for eco-innovations [39].

The difference in the perception of EMAS benefits between 2015 and 2020 may be related to the fact that it is easier for organisations to achieve environmental effects in the initial phase of system operation. The benefits are usually more visible at an early stage of EMAS functioning when even implementing minor improvements can result in relatively large effects, thus making the benefits visible and tangible. Further, the functioning of the management system and the introduction of improvements are associated with the lowering of the effectiveness of environmental activities. In this case, to achieve the same effects (reducing electricity consumption by 10%, for instance), more resources (such as human, financial, and time) have to be involved. In the initial stage of the management system’s functioning, market pressure and customer requirements are visible, as these are among the most important incentives for implementing an environmental management system in the organisation. Moreover, some improvements implemented once are often sufficient and do not need to be implemented again; for example, the removal of harmful substances from technology and products can be implemented once and become a new benchmark for an organisation.

Organisations implementing the EMAS expect more benefits from regulators, public administration, and other authorities, such as non-governmental organisations (NGOs). During the current study, most respondents (82.5%) indicated they expected more transparent and simplified legal rules. This included the expectation of reliable consultations while establishing new legal regulations, taking into account EMAS-registered organisations’ comments and remarks during the creation of legal acts, and avoiding the duplication of legal acts.

Meanwhile, 77.5% of respondents expected the provision of privileges to EMAS-registered organisations or the extension of the incentives catalogue, for example, a reduction in the frequency and scope of external inspections and controls from environmental authorities, a reduction in environmental charges, tax reliefs, priority handling of cases in governmental offices, an easy and fast route for obtaining environmental decisions and permits, or preferential access to public procurement.

A total of 52.5% of respondents expected additional promotional activities, including the promotion of the EMAS and registered organisations, the continuous education of society through mass media, joint and systematic training with regulatory authorities, public administration, competent bodies and environmental verifiers, and joint participation in ecological projects.

As many as 47.5% of respondents sought the unification of environmental reporting. Under legal requirements, environmental reporting is mainly related to the financial instrument of environmental protection (such as fees for economic use of the environment). The environmental reporting system in Poland is complex. Organisations have to report different aspects to different authorities, obey different deadlines for submission, and different procedures. In addition to the environmental reporting required by legal regulations, EMAS-registered organisations are required to report the effects of their activities in their environmental statements. Thus, though registered companies expect benefits, they face a high administrative burden.

5. Conclusions

It is difficult to unequivocally attest that as EMAS matures in organisations, it becomes more effective, because, in addition to internal factors, the effectiveness of the EMAS can be affected by many external factors, e.g., crisis situations, legislative requirements, or environmental conditions. Moreover, many internal factors can directly or indirectly affect the effectiveness of EMAS. One important factor is environmental awareness and management commitment. Studies have already shown that the importance of the EMAS is gradually shifting from the operational level to the strategic level with its maturity. Environmental awareness is a very important factor influencing the effectiveness of the EMAS. Employees with appropriate environmental knowledge act effectively in the capable supervision of significant environmental aspects and maintain the appropriate attitude to protect the environment not only in normal but also in special and emergency situations. As a result, it also has a large impact on building the environmental awareness of subcontractors and suppliers. The increase in pro-ecological awareness may contribute to a situation in which adopting pro-environmental behaviour will be a necessity rather than a recommendation. Management commitment is also a very important factor influencing the effectiveness of the EMAS, as management should be focused on the systematic achievement of the environmental performance of the organisation and ensure an open dialogue with stakeholders. This is directly responsible for the effectiveness of the EMAS, as has been confirmed by research results.

An important factor influencing the effectiveness of the EMAS is the use of SRDs, including BEMPs, environmental performance indicators for specific sectors, and the criteria for the excellence of assessing the level of environmental performance. Applying these practices will provide the most effective way of implementing and maintaining the EMAS; accordingly, under given economic and technical conditions, the best environmental performance can be achieved. Therefore, further research shall be focused on assessing whether the application of SRDs affects the effectiveness and efficiency of the organisation’s environmental activities in analysing the impact of these organisations in individual industries before and after the implementation of SRDs.

Environmental performance evaluation plays an essential role in assessing the effectiveness of the EMAS. The skilful use of indicators in organisations is another challenge. It will have a considerable impact on assessing and ensuring the effectiveness of the EMAS. It has been mentioned that the core EMAS indicators are still purely focused on operational performance, rather than incorporating a mixture of different types of indicators (OPI, MPI, ECI). Moreover, the core indicators cover only direct environmental aspects; it would be reasonable to include indirect performance indicators as well.

Author Contributions

Conceptualisation, A.M.-F. and B.P.; methodology, A.M.-F.; validation, A.M.-F.; formal analysis, B.P.; investigation, B.P.; resources, A.M.-F.; data curation, B.P.; writing—original draft preparation, B.P.; writing—review and editing, A.M.-F.; visualisation, B.P.; supervision, A.M.-F. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the corresponding author.

Acknowledgments

We would like to thank the reviewers for their time spent on reviewing our manuscript and their valuable comments which helped to enhance the quality of the publication. We would also like to thank those providing language services and proofreading for the article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Register EMAS. 2021. Available online: http://www.ec.europa.eu (accessed on 10 May 2021).

- Merli, R.; Lucchetti, M.C.; Preziosi, M.; Arcese, G. Causes of Eco-Management and Audit Scheme (EMAS) stagnation and enabling measures to stimulate new registrations: Characterization of public administrations and private-owned organizations. J. Clean. Prod. 2018, 190, 137–148. [Google Scholar] [CrossRef]

- Merli, R.; Preziosi, M. The EMAS impasse: Factors influencing Italian organizations to withdraw or renew the registration. J. Clean. Prod. 2018, 172, 4532–4543. [Google Scholar] [CrossRef]

- Heras-Saizarbitoria, I.; Boiral, O.; Arana, G. Renewing environmental certification in times of crisis. J. Clean. Prod. 2016, 115, 214–223. [Google Scholar] [CrossRef]

- Preziozi, M.; Merli, R.; D’Amico, M. Why Companies Do Not Renew Their EMAS Registration? An Exploratory Research. Sustainability 2016, 8, 191. [Google Scholar] [CrossRef] [Green Version]

- Szyszka, B.; Matuszak-Flejszman, A. EMAS: Unfulfilled expectations and challenges associated with the planned publication of the new ISO 14001:2015. In Sustainable Development; Brebbia, C.A., Ed.; Wessex Institute of Technology: Southampton, UK, 2015; pp. 313–323. [Google Scholar] [CrossRef] [Green Version]

- International Organization for Standardization. Survey. 2020. Available online: https://www.iso.org/the-iso-survey.html (accessed on 10 May 2021).

- European Commission. Moving Towards a Circular Economy with EMAS. Beat Practices to Implement Circular Economy Strategies (With Case Study Examples); Publications Office of the European Union: Luxembourg, 2017. [Google Scholar]

- European Commission. 3 Good Reasons for EMAS 3x; Publications Office of the European Union: Luxembourg, 2012. [Google Scholar]

- European Commission. EMAS Promotion and Policy Support in the Member States. Compendium; Publications Office of the European Union: Luxembourg, 2015. [Google Scholar]

- European Commission. Regulation (EC) No. 1221/2009 of the European Parliament and of the Council of 25 November 2009 on the Voluntary Participation by Organizations in a Community Eco-Management and Audit Scheme (EMAS), Repealing Regulation (EC) 761/2001 and Commission Decisions 2001/681/EC and 2006/193/EC; The Stationery Office Ltd.: London, UK, 2009. [Google Scholar]

- European Commission. Commission Regulation (EU) 2018/2026 of 19 December 2018 Amending Annex IV to Regulation (EC) No 1221/2009 of the European Parliament and of the Council on the Voluntary Participation by Organisations in a Community Eco-Management and Audit Scheme (EMAS); The Stationery Office Ltd.: London, UK, 2018. [Google Scholar]

- Erkko, S.; Melanen, M.; Mickwitz, P. Eco-efficiency in the Finnish EMAS reports—A buzz word? J. Clean. Prod. 2005, 13, 799–813. [Google Scholar] [CrossRef]

- Pedersen, E.R. Perceptions of performance: How European Organizations Experience EMAS Registration. Corp. Soc. Responsib. Environ. Manag. 2007, 14, 61–73. [Google Scholar] [CrossRef]

- Iraldo, F.; Testa, F.; Daddi, T. The effectiveness of EMAS as a management tool: A key role for the internalization of environmental practices. Organ. Environ. 2018, 31, 48–69. [Google Scholar]

- Iraldo, F.; Testa, F.; Frey, M. Is an environmental management system able to influence environmental and competitive performance? The case of the eco-management and audit scheme (EMAS) in the European Union. J. Clean. Prod. 2009, 17, 1444–1452. [Google Scholar] [CrossRef]

- Daddi, T.; Magistrelli, M.; Frey, M.; Iraldo, F. Do environmental management systems improve environmental performance? Empirical evidence from Italian companies. Environ. Dev. Sustain. 2011, 13, 845–862. [Google Scholar] [CrossRef]

- Mazzi, A.; Mason, C.; Mason, M.; Scipioni, A. Is it possible to compare environmental performance indicators reported by public administrations? Results from an Italian survey. Ecol. Indic. 2012, 23, 653–659. [Google Scholar] [CrossRef]

- Matuszak-Flejszman, A.; Szyszka, B.; Jóhannsdóttir, L. Effectiveness of EMAS: A case study of Polish organisations registered under EMAS. Environ. Imp. Assess. Rev. 2019, 74, 86–94. [Google Scholar] [CrossRef]

- Janik, A.; Szafraniec, M. Circular Economy Performance of EMAS Organizations in Poland based on an Analysis of Environmental Statements. Multidiscip. Asp. Prod. Eng. 2019, 2, 536–547. [Google Scholar] [CrossRef] [Green Version]

- Heras-Saizarbitoria, I.; Boiral, O.; García, M.; Allur, E. Environmental best practice and performance benchmarks among EMAS-certified organizations: An empirical study. Environ. Impact Assess. Rev. 2020, 80, 106315. [Google Scholar] [CrossRef]

- Marrucci, L.; Daddi, T.; Iraldo, F. The integration of circular economy with sustainable consumption and production tools: Systematic review and future research agenda. J. Clean. Prod. 2019, 240, 118268. [Google Scholar] [CrossRef]

- Barón, A.; de Castro, R.; Giménez, G. Circular economy practices among industrial EMAS-registered SMEs in Spain. Sustainability 2020, 12, 9011. [Google Scholar] [CrossRef]

- Moraga, G.; Huysveld, S.; Mathieux, F.; Blengini, G.A.; Alaerts, L.; Van Acker, K.; de Meester, S.; Dewulf, J. Circular economy indicators: What do they measure? Resour. Conserv. Recycl. 2019, 146, 452–461. [Google Scholar] [CrossRef]

- Kristensen, H.S.; Mosgaard, M.A. A review of micro level indicators for a circular economy—Moving away from the three dimensions of sustainability? J. Clean. Prod. 2020, 243, 118531. [Google Scholar] [CrossRef]

- Roos Lindgreen, E.R.; Salomone, R.; Reyes, T. A critical review of academic approaches, methods and tools to assess circular economy at the micro level. Sustainability 2020, 12, 4973. [Google Scholar] [CrossRef]

- Czerska, M.; Rutka, R. Wykorzystanie ‘prawa dołka’ w kierowaniu zmianą. In Zarządzanie i Finanse; Wydział Zarządzania—Uniwersytet Gdański: Sopot, Poland, 2013; Volume 4, pp. 47–60. [Google Scholar]

- Matuszak-Flejszman, A.; Błaszczyk, A. Najlepsze praktyki zarządzania środowiskowego stosowane w ramach EMAS, Nauki o zarządzaniu i jakości wobec wyzwań zrównoważonego rozwoju. In Towaroznawstwo w Badaniach i Praktyce; Salerno-Kochan, R., Ed.; Sieć Badawcza Łukasiewicz—Instytut Technologii Eksploatacji: Radom, Poland, 2019. [Google Scholar]

- UN General Assembly. Transforming Our World: The 2030 Agenda for Sustainable Development, 21 October 2015, A/RES/70/1. Available online: https://www.refworld.org/docid/57b6e3e44.html (accessed on 25 October 2021).

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The Sustainability Balanced Scorecard—Linking sustainability management to business strategy. Bus. Strategy Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Hamdoun, M.; Zouaoui, M. Impact of environmental management on competitive advantage of Tunisian companies: The mediator role of organizational culture. Int. Rev. Manag. Mark. 2017, 7, 76–82. [Google Scholar]

- Ruokonen, E.; Temmes, A. The approaches of strategic environmental management used by mining companies in Finland. J. Clean. Prod. 2019, 210, 466–476. [Google Scholar] [CrossRef]

- Del Brio, J.A.; Fernandez, E.; Janquera, B.; Vazques, C.J. Motivations for Adopting the ISO 14001 Standard: A Study of Spanish Industrial Companies. Environ. Qual. Manag. 2001, 10, 13–28. [Google Scholar] [CrossRef]

- Laskurain, I.; Ibarloza, A.; Larrea, A.; Allur, E. Contribution to energy management of the main standards for environmental management systems: The case of ISO 14001 and EMAS. Energies 2017, 10, 1758. [Google Scholar] [CrossRef] [Green Version]

- International Organization for Standardization. ISO 50001:2018. Energy Management Systems—Requirements with Guidance for Use; ISO: Geneva, Switzerland, 2018. [Google Scholar]

- Wysokińska-Senkus, A. The role of the energy management system in the implementation of the principles of the circular economy. Intercathedra 2017, 33, 78–85. [Google Scholar]

- Murmura, F.; Liberatore, L.; Bravi, L.; Casolani, N. Evaluation of Italian companies’ perception about ISO 14001 and Eco Management and Audit Scheme III: Motivations, Benefits and Barriers. J. Clean. Prod. 2017, 174, 691–700. [Google Scholar] [CrossRef]

- Myszczyszyn, J. Eco-management and audit scheme (EMAS) as an important element of the sustainable development policy on the example of public sector organizations. Environ. Prot. Nat. Resour. 2017, 28, 20–24. [Google Scholar] [CrossRef] [Green Version]

- Montobbio, F.; Solito, I. Does the eco-management and audit scheme foster innovation in European firms? Bus. Strategy Environ. 2018, 27, 82–99. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Effectiveness of achieving environmental objectives in each calendar year.

Figure 2.

Organisations that set objectives in particular areas. Source: Reprinted from [19].

Figure 2.

Organisations that set objectives in particular areas. Source: Reprinted from [19].

Figure 3.

Organisations that monitor core indicators. Source: Reprinted from [19].

Figure 3.

Organisations that monitor core indicators. Source: Reprinted from [19].

Figure 4.

Organisations that monitor other indicators.

Figure 5.

Differences in EMAS benefits assessed by registered organisations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Changes in the number of EMAS-registered organisations in Poland (population) and the research sample.

Table 1.

Changes in the number of EMAS-registered organisations in Poland (population) and the research sample.

| Phase 1 Research 2015 (Period 2007–2014) | Phase 2 Research 2021 (Period 2015–2020) | |

|---|---|---|

| Primary sources | N = 39 n = 26 return 66.7% | N = 65 n = 40 return 61.5% |

| Secondary sources | N = 59 n = 59 analysed percentage 100% | N = 65 n = 65 analysed percentage 100% |

Table 2.

Total number of measurements (in calendar years).

| Year | Number of Samples (n) | ||

|---|---|---|---|

| 1. | Research 2015 | 2007 | 6 |

| 2. | 2008 | 11 | |

| 3. | 2009 | 13 | |

| 4. | 2010 | 17 | |

| 5. | 2011 | 24 | |

| 6. | 2012 | 33 | |

| 7. | 2013 | 40 | |

| 8. | 2014 | 43 | |

| - | SUM | 187 | |

| 1. | Research 2021 | 2015 | 52 |

| 2. | 2016 | 56 | |

| 3. | 2017 | 59 | |

| 4. | 2018 | 62 | |

| 5. | 2019 | 63 | |

| 6. | 2020 | 65 | |

| - | SUM | 357 |

Table 3.

Changes in environmental performance indicators.

| Area | Decrease | Stable | Increase | Weighted Index (Decrease w = 2, Stable w = 1, Increase w = 0) | |

|---|---|---|---|---|---|

| 1. | Water (2015 study) | 44.2% | 39.5% | 16.3% | 1.28 |

| Water (2021 study) | 53.8% | 38.5% | 7.7% | 1.46 | |

| delta | 9.6% | −1.0% | −8.6% | 0.18 | |

| 2. | Energy (2015 study) | 30.4% | 28.3% | 41.3% | 0.89 |

| Energy (2021 study) | 71.4% | 21.4% | 7.1% | 1.64 | |

| delta | 41.0% | −6.9% | −34.2% | 0.75 | |

| 3. | Materials (2015 study) | 35.7% | 40.5% | 23.8% | 1.12 |

| Materials (2021 study) | 30.8% | 69.9% | 0.0% | 1.32 | |

| delta | −4.9% | 29.4 | −23.8% | 0.20 | |

| 4. | Waste (2015 study) | 57.6% | 17.4% | 25.0% | 1.33 |

| Waste (2021 study) | 41.2% | 58.8% | 0.0% | 1.41 | |

| delta | −16.2% | 41.4% | −25.0% | 0.09 | |

| 5. | Emissions (2015 study) | 55.2% | 39.5% | 5.3% | 1.50 |

| Emissions (2021 study) | 47.1% | 41.2% | 11.8% | 1.35 | |

| delta | −8.1% | 1.7% | 6.5% | −0.15 |

Table 4.

Business management and marketing benefits of the EMAS.

| Benefit Description | 2015 | 2021 | Delta |

|---|---|---|---|

| Brand, reputation, credibility | 3.54 | 3.40 | −0.14 |

| Investors’ interest | 2.25 | 1.40 | −0.85 |

| Competitiveness | 2.33 | 1.55 | −0.78 |

| New customers | 1.96 | 1.45 | −0.51 |

| Opportunities to enter new markets | 2.08 | 1.35 | −0.73 |

| Legal compliance | 3.46 | 4.10 | 0.64 |

| Number of inspections | 1.71 | 1.65 | −0.06 |

| Internal or external communication | 3.17 | 3.30 | 0.13 |

| Cooperation with suppliers and subcontractors | 2.50 | 2.55 | 0.05 |

| Contact with media | 2.67 | 2.60 | −0.07 |

| AVERAGE | 2.57 | 2.33 | −0.24 |

Table 5.

Economic and financial benefits of the EMAS.

| Benefit Description | 2015 | 2021 | Delta |

|---|---|---|---|

| Cost reduction through rational management of raw materials and resources | 2.58 | 2.50 | −0.08 |

| Reduction in fees for the economic use of the environment | 1.92 | 1.80 | −0.12 |

| Opportunities to use bank loans | 1.88 | 1.55 | −0.33 |

| Obtain funds or subsidies for pro-ecological activities | 2.00 | 1.70 | −0.30 |

| Insurance rates | 1.50 | 1.45 | −0.05 |

| Tax relief | 1.46 | 1.20 | −0.26 |

| Penalties for exceeding legal requirements | 2.08 | 1.50 | −0.58 |

| AVERAGE | 1.92 | 1.67 | −0.25 |

Table 6.

Social benefits of the EMAS.

| Benefit Description | 2015 | 2021 | Delta |

|---|---|---|---|

| Employees’ awareness | 3.83 | 4.00 | 0.17 |

| Employees’ engagement | 3.42 | 3.80 | 0.38 |

| Relations with local community | 3.46 | 3.20 | −0.26 |

| Open dialogue with society | 3.25 | 3.35 | 0.10 |

| Relations with local authorities | 3.21 | 2.90 | −0.31 |

| Number of accidents | 3.08 | 2.25 | −0.83 |

| Response to failure | 3.33 | 2.55 | −0.78 |

| Suppliers’ pro-environmental awareness | 3.42 | 3.10 | −0.32 |

| AVERAGE | 3.37 | 3.14 | −0.23 |

Table 7.

Ecological and environmental benefits of EMAS.

| Benefit Description | 2015 | 2021 | Delta |

|---|---|---|---|

| Consumption of raw materials | 2.79 | 2.80 | 0.01 |

| Water consumption | 3.08 | 3.10 | 0.02 |

| Electricity consumption | 2.88 | 3.00 | 0.12 |

| Fuel consumption | 2.63 | 2.95 | 0.32 |

| Waste reduction | 3.00 | 2.90 | −0.10 |

| Waste management (recycling) | 3.00 | 2.80 | −0.20 |

| Amount of packaging | 2.58 | 2.40 | −0.18 |

| Wastewater | 2.71 | 2.15 | −0.56 |

| Vibration | 1.71 | 1.25 | −0.46 |

| Dust | 2.25 | 1.75 | −0.50 |

| Noise | 2.25 | 1.70 | −0.55 |

| Radiation | 1.75 | 1.20 | −0.55 |

| Air emissions | 2.79 | 2.60 | −0.19 |

| Removal of harmful substances from technology | 2.21 | 1.45 | −0.76 |

| Removal of harmful substances from products | 1.83 | 1.70 | −0.13 |

| AVERAGE | 2.49 | 2.25 | −0.24 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Matuszak-Flejszman, A.; Paliwoda, B. Effectiveness and Benefits of the Eco-Management and Audit Scheme: Evidence from Polish Organisations. Energies 2022, 15, 434. https://0-doi-org.brum.beds.ac.uk/10.3390/en15020434

AMA Style

Matuszak-Flejszman A, Paliwoda B. Effectiveness and Benefits of the Eco-Management and Audit Scheme: Evidence from Polish Organisations. Energies. 2022; 15(2):434. https://0-doi-org.brum.beds.ac.uk/10.3390/en15020434

Chicago/Turabian StyleMatuszak-Flejszman, Alina, and Beata Paliwoda. 2022. "Effectiveness and Benefits of the Eco-Management and Audit Scheme: Evidence from Polish Organisations" Energies 15, no. 2: 434. https://0-doi-org.brum.beds.ac.uk/10.3390/en15020434

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.