An Overview of Promising Alternative Fuels for Road, Rail, Air, and Inland Waterway Transport in Germany

, ,

, ,  , , , ,

, , , ,

Abstract

:

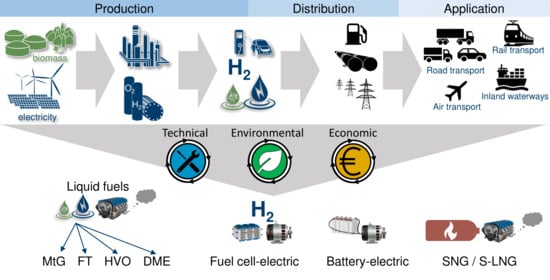

1. Introduction

2. Materials and Methods

2.1. Technology Readiness Level

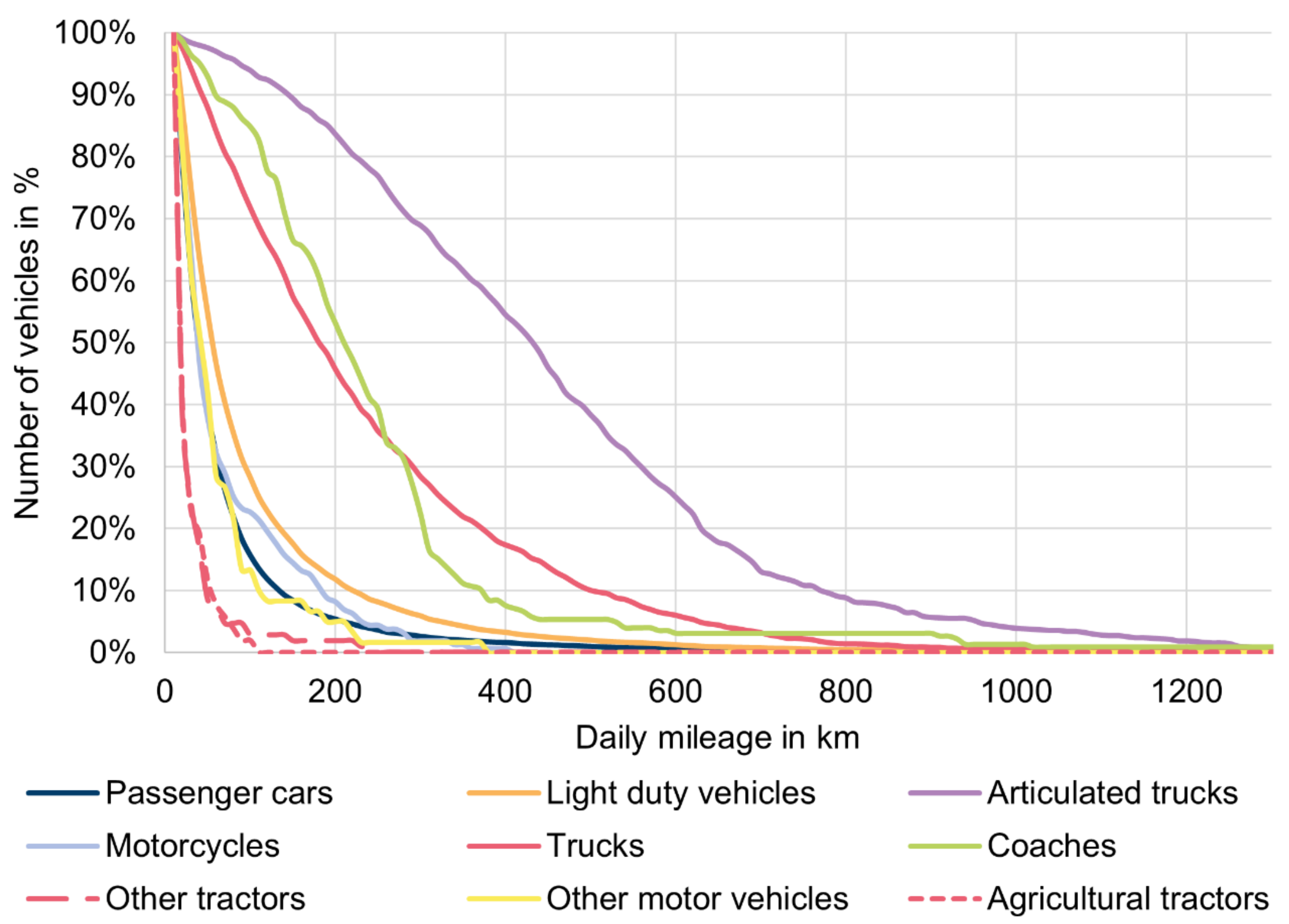

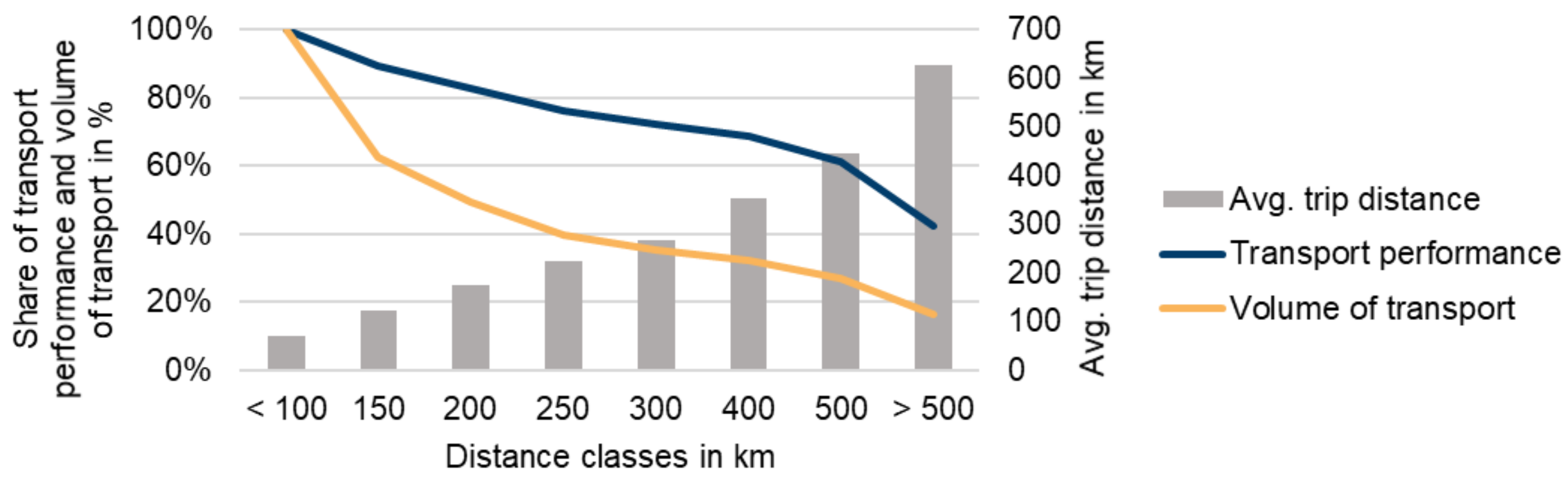

2.2. Identification of Required Mission Ranges for Different Means of Transport

3. Potential, Technical Maturity, and Costs of Alternative Fuel Production

3.1. Potential of Biomass-Based Alternative Fuels

3.2. TRL of Fuel Production Pathways

3.3. Costs

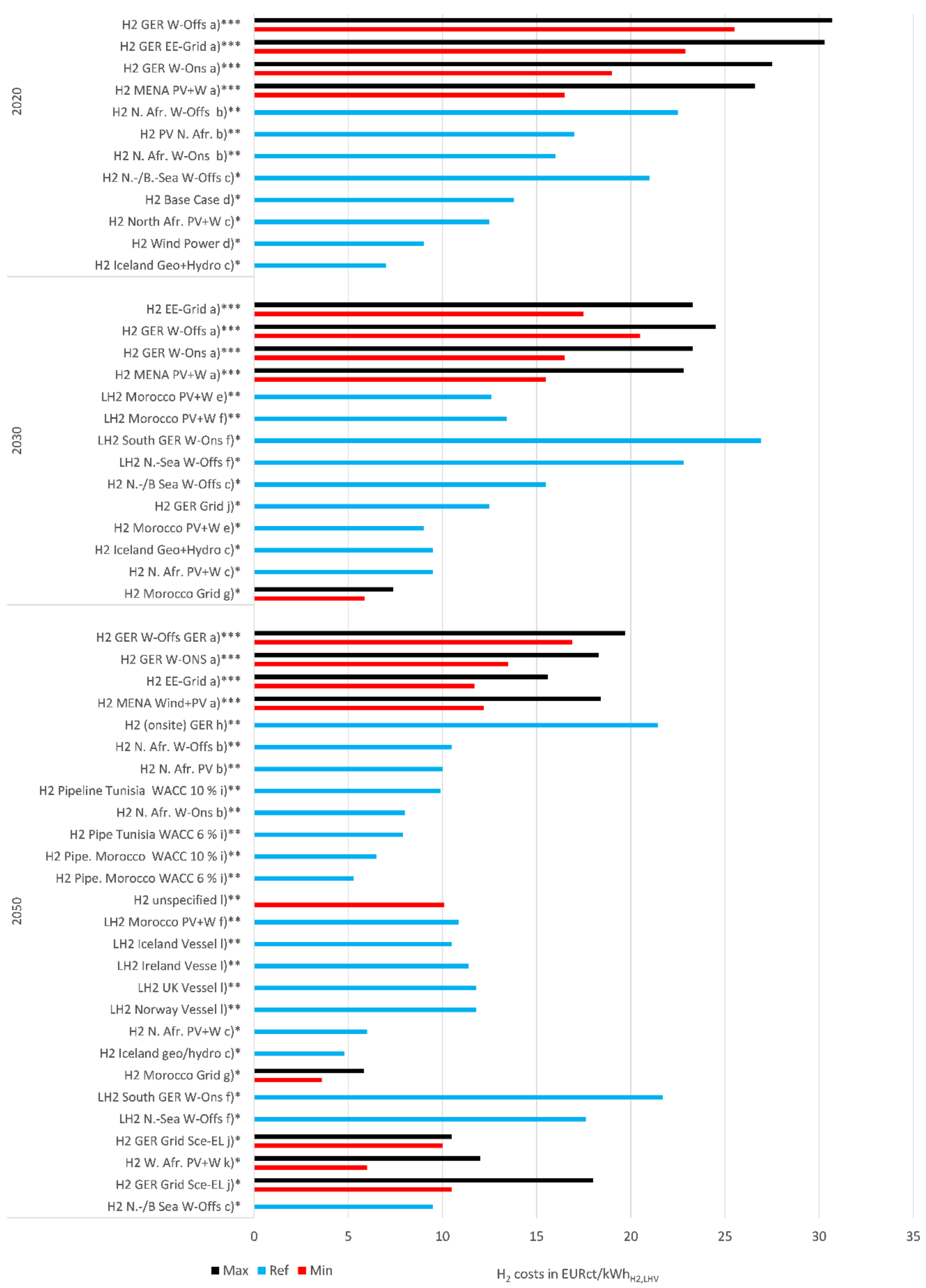

3.3.1. Import Costs of Energy Carriers

3.3.2. Review of Total Costs

Future Cost Ranges of Hydrogen from Renewable Sources

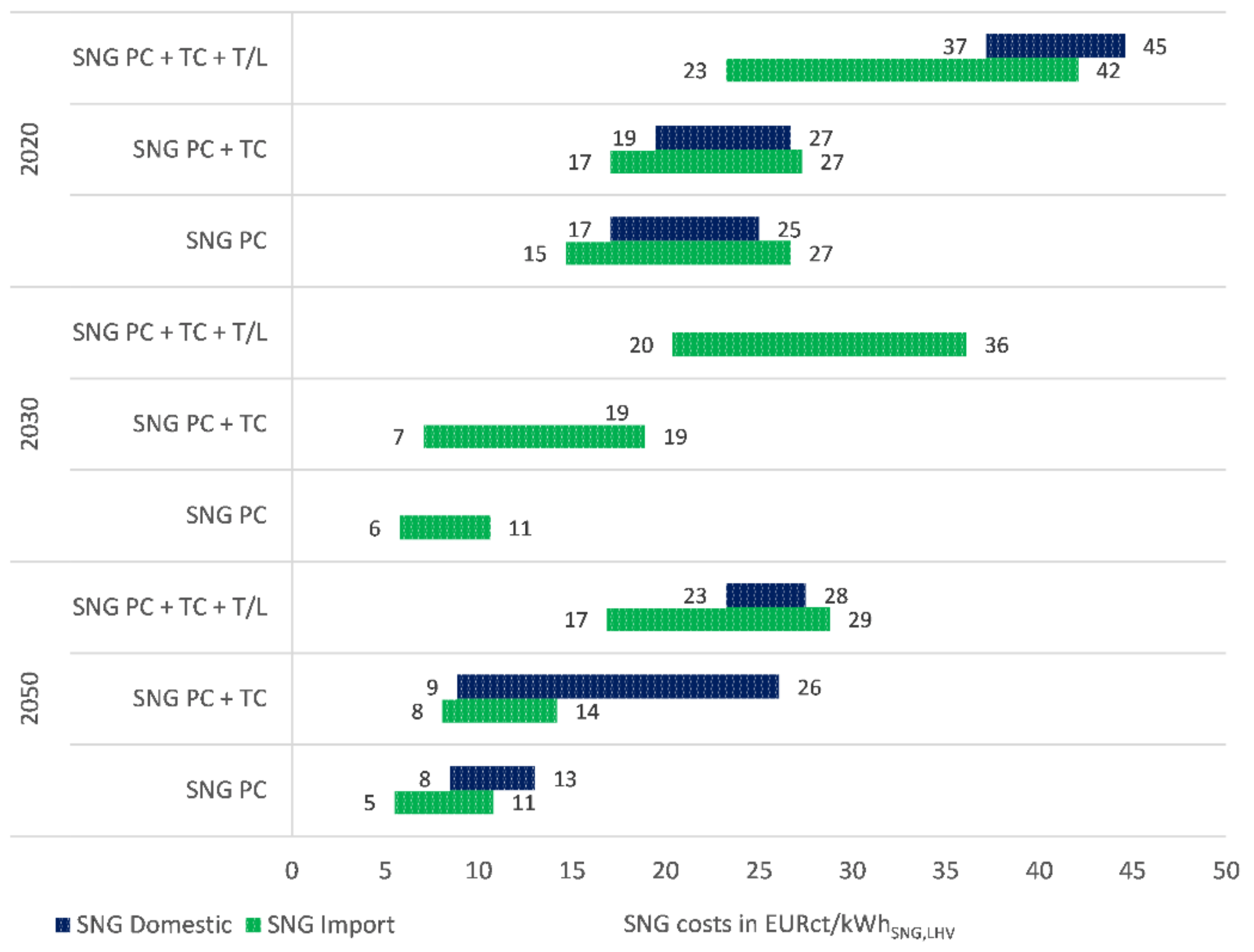

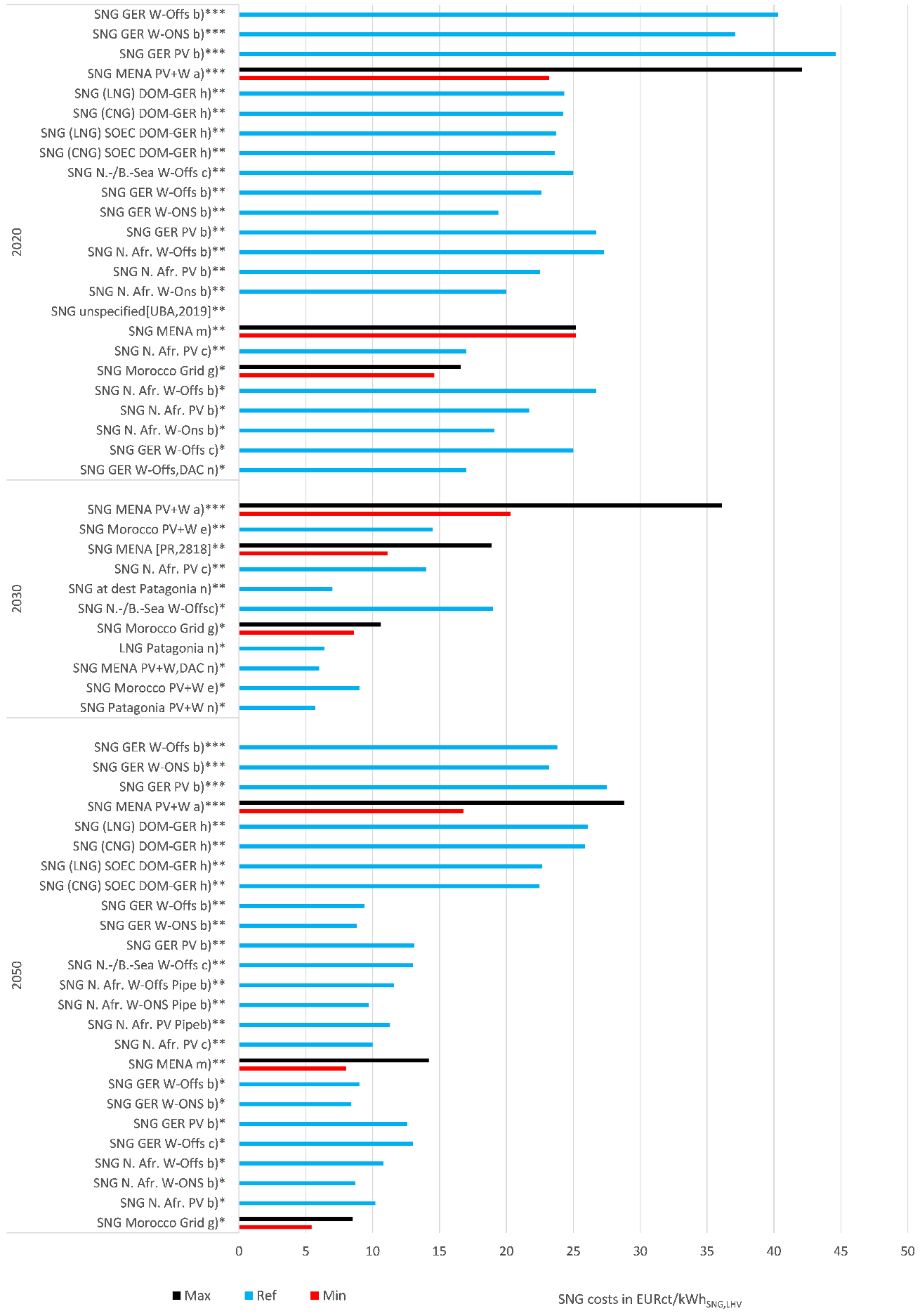

Future Cost Ranges of SNG from Renewable Sources

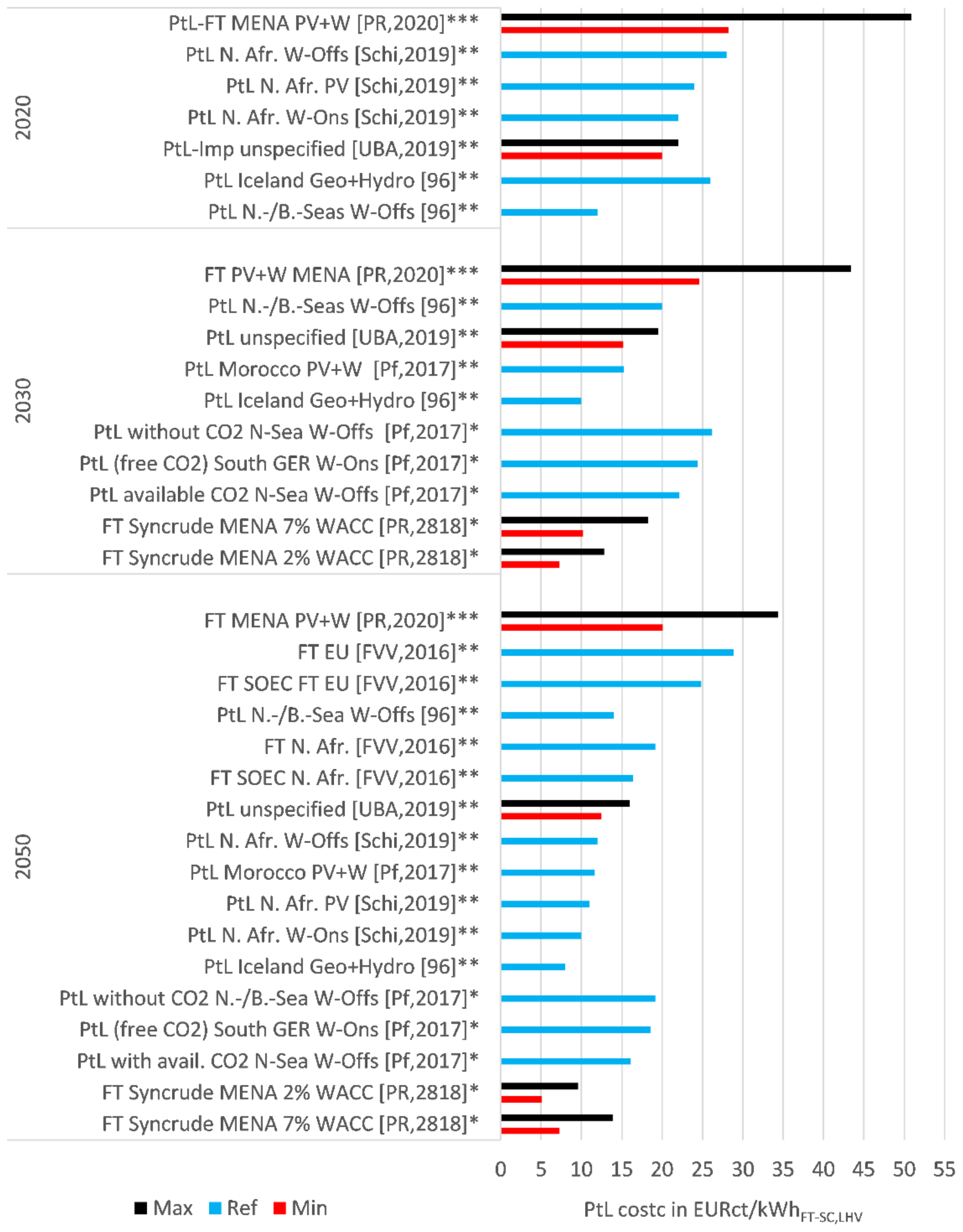

Future Cost Ranges of PtL-Fuels from Renewable Sources

3.4. Interim Conclusion

4. Assessment of Alternative Fuel Utilization

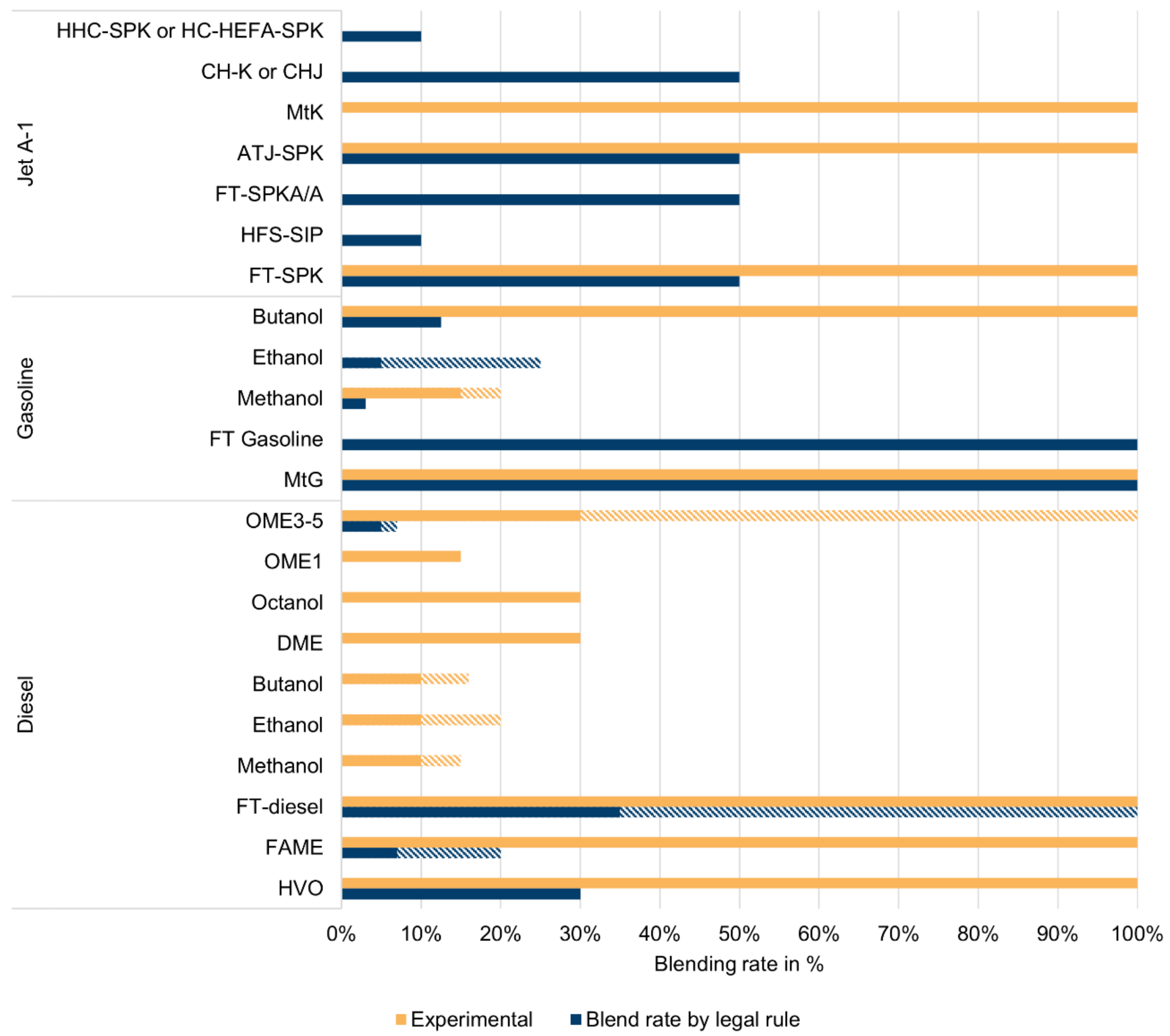

4.1. Drop-In Possibility of Alternative Fuels

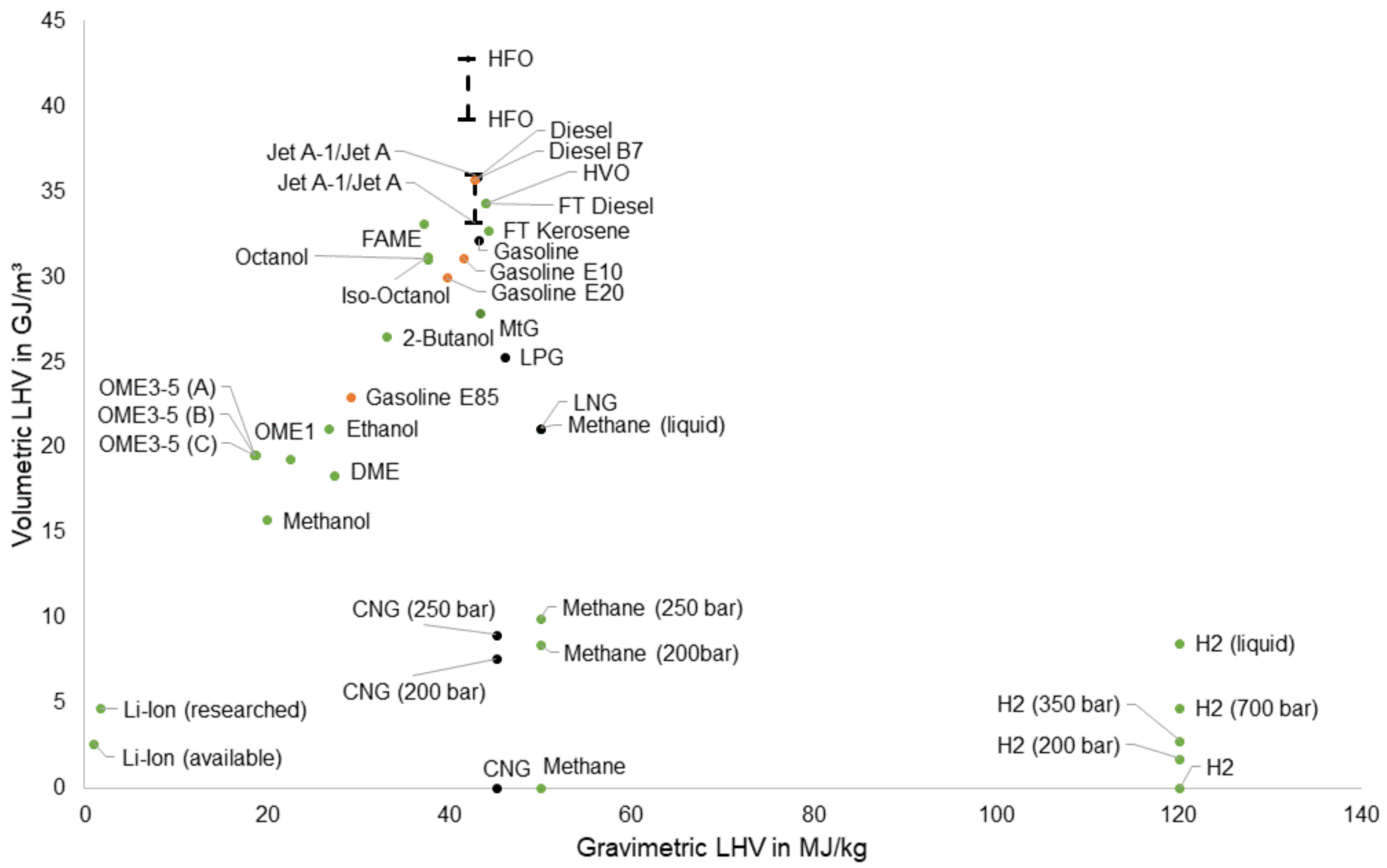

4.2. Heating Value of Alternative Fuels

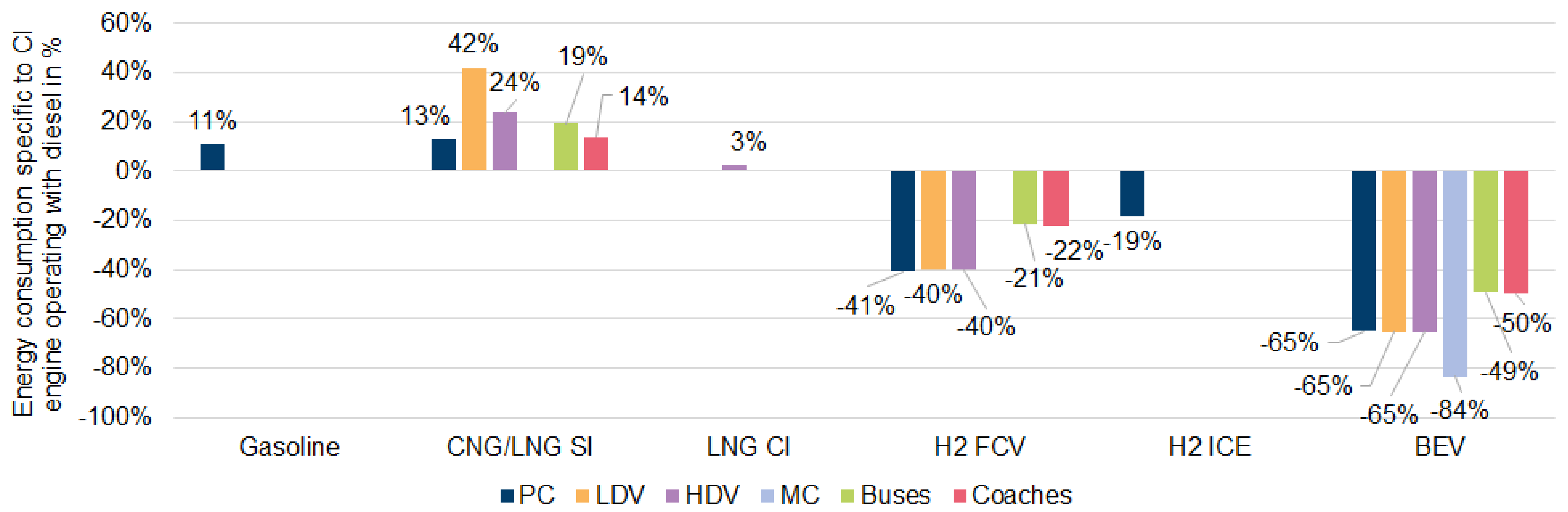

4.3. Drivetrain Efficiencies

4.3.1. Road Transport

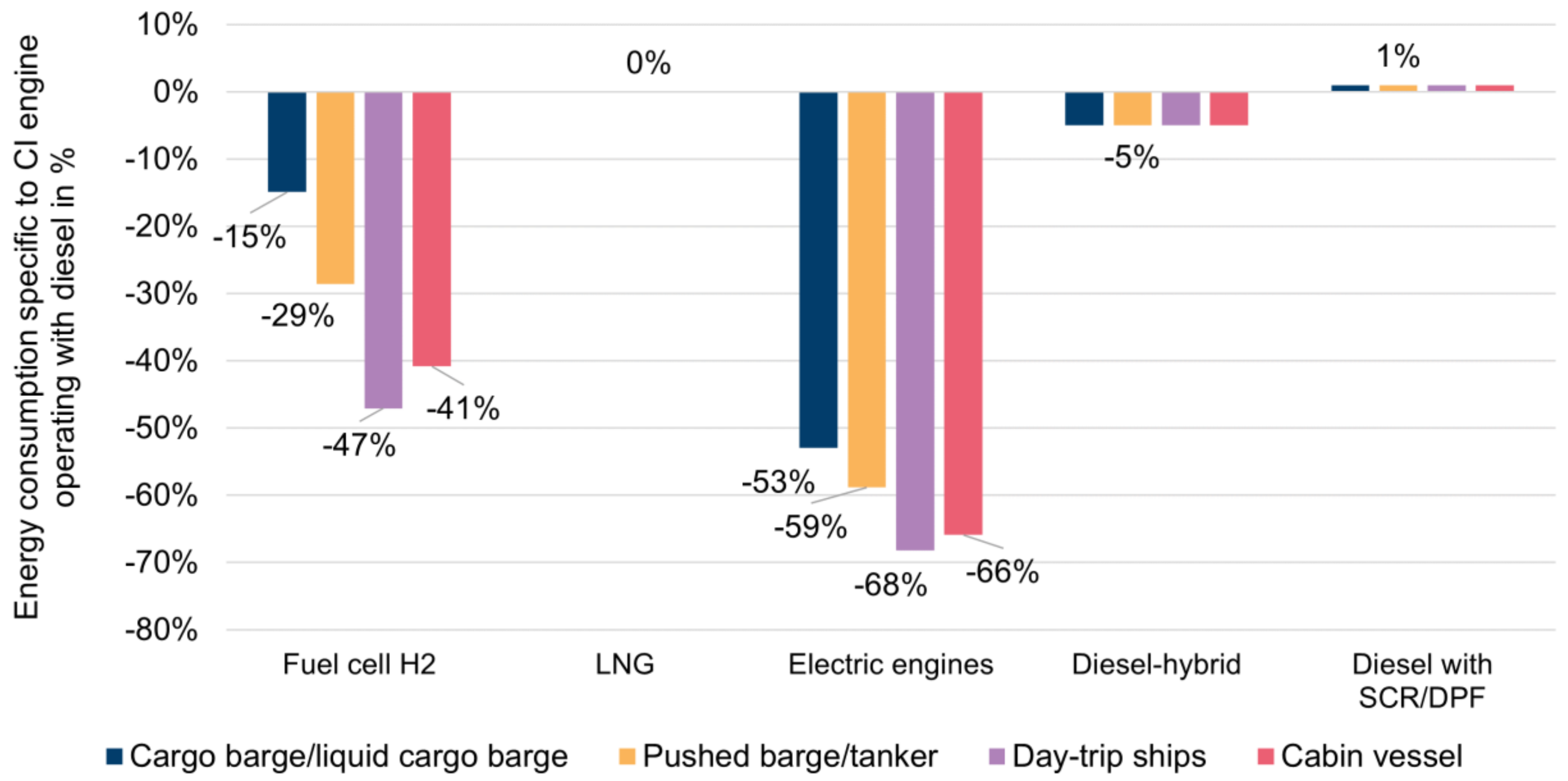

4.3.2. Inland Waterway Transport

4.3.3. Rail Transport

4.3.4. Air Transport

4.4. Interim Conclusion

5. Environmental Impacts of Promising Alternative Fuels

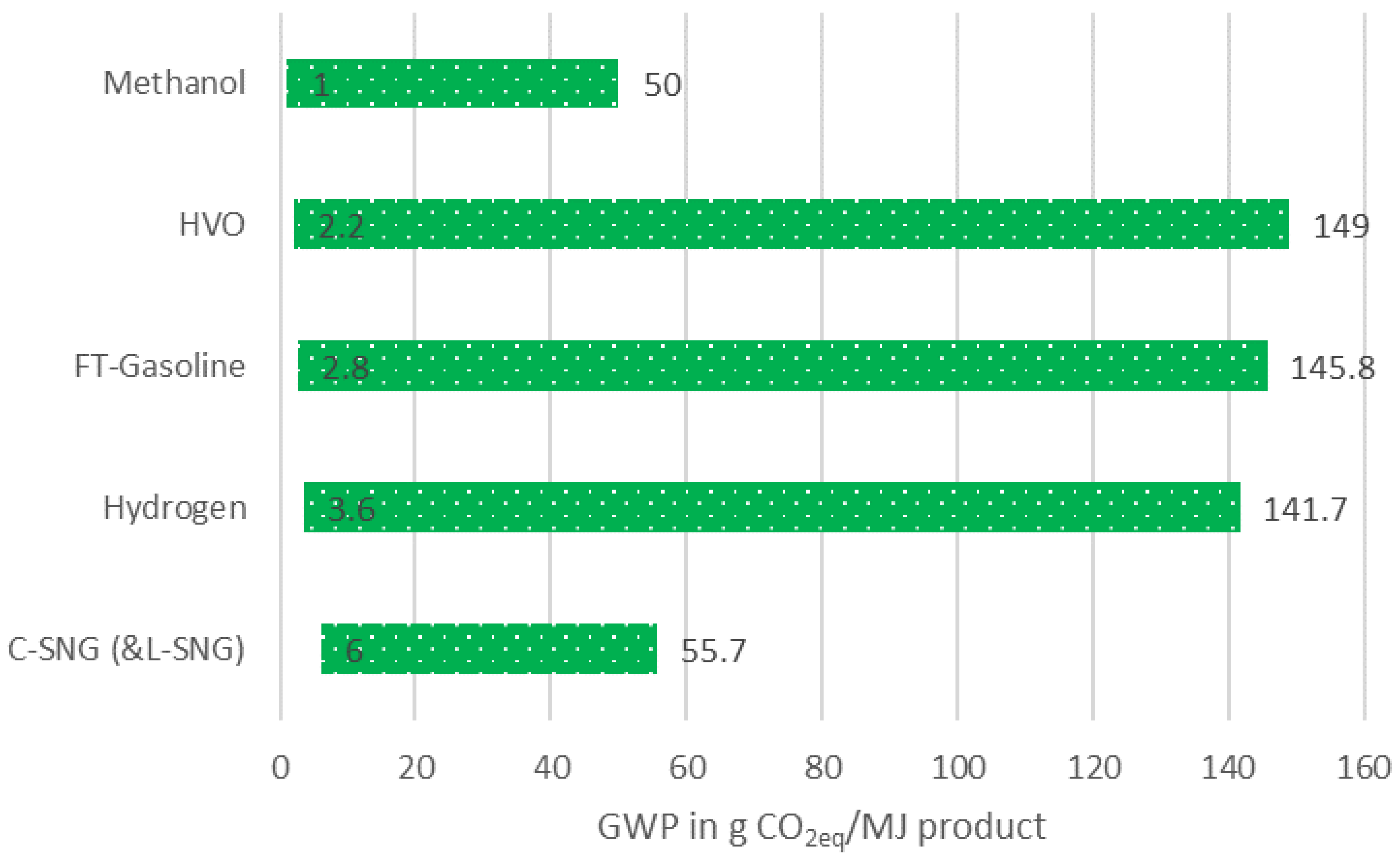

5.1. Hydrogen

5.2. C-SNG/L-SNG

5.3. HVO

5.4. Methanol

5.5. DME

5.6. MtG

5.7. FT Diesel and Kerosene

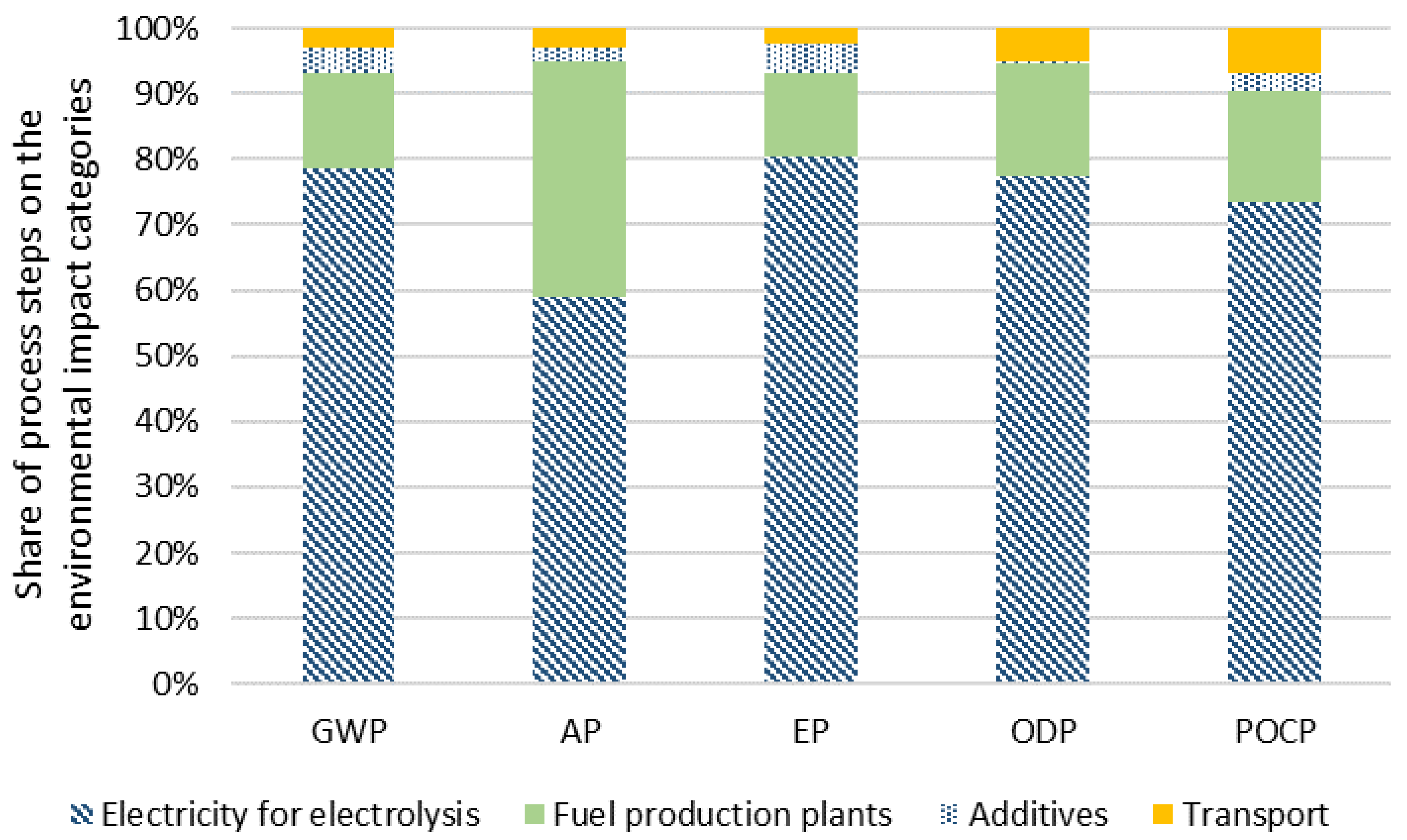

5.8. Contribution Analysis for Several Alternative Fuels

5.9. Interim Conclusion

6. Discussion

6.1. Cost

6.2. Road Transport

6.3. Inland Waterway Transport

6.4. Rail Transport

6.5. Air Transport

6.6. Environmental Impacts of Promising Alternative Fuels

7. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

| Fuel | Process | Production TRL |

|---|---|---|

| Hydrogen | Upgraded biogas from municipal organic waste, wet manure, sewage sludge, maize, or double cropping | TRL 9 [5] |

| Gasification of farmed wood | TRL 8 [5] | |

| Renewable electricity via alkaline electrolysis | TRL 9 [5] | |

| Renewable electricity via polymer electrolyte membrane electrolysis | TRL 9 [57] | |

| Renewable electricity via solid oxide electrolysis cell | TRL 6–7 [57] | |

| HVO | Conventional (biomass) | TRL 9 [5,76] |

| FAME | Conventional (biomass) | TRL 9 [5,76] |

| Syndiesel | BtL, lignocellulose pyrolysis-based | TRL 6 [5,76] |

| lignocellulose gasification | TRL 8 [5] | |

| lignocellulose hydrothermal liquefaction (HTL) and upgrading | TRL 4 [5] | |

| FT diesel from CO2 and H2 | TRL 6 [4] | |

| Diesel via methanol from CO2 and H2 | TRL 9 [5] | |

| Synthetic gasoline | lignocellulose pyrolysis-based | TRL 6 [5] |

| MtG | TRL 9 [4] | |

| Methanol | Lignocellulose | TRL 8 [5] |

| From CO2 and H2 | TRL 9 [4,5] | |

| Ethanol | Conventional (biomass) | TRL 9 [5,76] |

| Lignocellulose | TRL 7 [76], TRL 8 [5] | |

| From CO2 and H2 | TRL 4 [4] | |

| Butanol(1/2) | Conventional (biomass) | TRL 7 [5] |

| From CO2 and H2 | TRL 4 [4] | |

| DME | Lignocellulose | TRL 8 [5] |

| From CO2 and H2 | TRL 9 [4,5] | |

| OME1 | Lignocellulose | TRL 5 [5] |

| From CO2 and H2 | TRL 5 [4] | |

| OME3-5 | Lignocellulose | TRL 5 [5] |

| From CO2 and H2 | TRL 4–5 [4,79] | |

| Iso-octanol | From CO2 and H2 | TRL 4 [4] |

| Octanol | TRL 1 [78] | |

| From lignocellulose | TRL 3 based on Leitner et al. [77] | |

| CNG/CBM/SNG | Biomethane/biogas from residues (e.g., biowaste, manure, stillage) | TRL 9 [5,76] |

| Biomethane/synthetic natural gas (SNG) from lignocelluloses (e.g., wood and straw) | TRL 7 [76], TRL 8 [5] | |

| From CO2 and H2 | TRL 9 based on [5], Deutsche Energie-Agentur [80] | |

| SLNG/LBM | Upgraded biogas to LBM from municipal waste, wet manure, sewage sludge, maize, double cropping | TRL 9 [5] |

| SNLG from gasification of lignocelluloses (e.g., waste wood and wood chips) | TRL 8 [5] | |

| SLNG from CO2 and H2 | TRL 9 [5] | |

| Synthetic jet fuel | FT-SPK from CO2 and H2 | TRL 6 [4] |

| FT-SPK from biomass via gasification | TRL 9; Fulcrum [67] and Red Rock [68] have plants under construction with 30 kt/year and 45 kt/year | |

| Jet fuel from MtK process | TRL 4 based on based on Tabak et al. [63] and Tabak and Yurchak [64] | |

| HEFA-SPK from bio-oils, animal fat, and recycled oils | TRL 9; commercial process by World Energy Paramount (former AltAir Paramounts LLC) [60] and Neste Oyj [69] | |

| HFS-SIP from the microbial conversion of sugars into hydrocarbons | TRL 9, commercial process by Amyris in Brazil [60] | |

| ATJ-SPK from agricultural waste products (stover, grasses, forestry slash, and crop straws) | TRL 9; Pilot plant by LanzaTech [70]; commercial plant by Ekobenz with 22.5 kt/year [71]. Commercial-scale plants planned by LanzaTech [72] and SWEDISH BIOFUELS AB [73] | |

| CHJ from triglyceride-based feedstocks (plant oils, waste oils, algal oils, soybean oil, jatropha oil, camelina oil, carinata oil, and tung oil) | TRL 6–7; demonstration plant of ARA and euglena [74] | |

| HHC-SPK from biologically-derived hydrocarbons such as algae | TRL 4; laboratory scale by IHI [75] |

| Authors | Year | Content/Investigated Regions | Identified Costs | Meta-Study |

|---|---|---|---|---|

| Merten et al. [83] | 2020 | Germany: imported vs. locally produced hydrogen | Generation Transport | yes |

| Kreidelmeyer et al. [92] | 2020 | Fuel: H2, methane, methanol, FT-syncrude | Generation Transport Taxes/Levies | no |

| Import region: MENA Assessed | ||||

| Costs: production, transport, and distribution | ||||

| Robinius et al. [34] | 2020 | Import costs of (synfuels, SNG, and H2) are determined through optimized technology decision-making, electricity imported from countries neighboring Germany | Generation Transport | no |

| Gerhardt et al. [106] | 2020 | Import costs from Morocco and Tunisia, energy costs, demineralization, liquefaction, and transport | Generation Transport | no |

| Christoph Hank et al. | 2020 | Import costs from Morocco for LH2, LOHC, liquefied methane, methanol, and ammonia | Generation Transport | |

| Mottschall et al. [107] | 2019 | Difference between H2, CH4, and PtL import costs | Generation Transport | yes |

| No own calculation | ||||

| Schindler [89] | 2019 | Cost analyses of end user costs of in-Germany-produced and imported H2, SNG, and PtL Fuels for 2020 and 2050 | Generation Transport Taxes/Levies | no |

| Primary source is unknown | ||||

| Eichhammer et al. [90] | 2019 | Generation costs of hydrogen and derived products from Morocco 2015, 2030, and 2050 | Generation | no |

| Michalski et al. [105] | 2019 | H2 generation costs in Germany, with electricity imported from neighboring countries | Generation | no |

| Jensterle et al. [104] | 2019 | Country-specific suitability of energy carrier export due to various soft factors | Generation Transport | no |

| Schemme et al. [4] | 2019 | Techno-economic aspects of specific synfuels: H2, methanol, ethanol, DME, OME, MtG, FT, and butanol | Generation | no |

| Terlouw et al. [111] | 2019 | Energy system modeling for 2050, determining favorable RE locations for energy carrier production, hydrogen transport technologies’ TRLs, and costs | Generation Transport | no |

| Perner et al. [110] | 2018 | Future costs of fossil fuels | ||

| PtL from North and Baltic Sea/North Africa/Iceland and Germany | ||||

| Level: Transport + conversion losses + electricity costs | ||||

| without taxes and levies | ||||

| Kramer et al. [109] | 2018 | Min/max scenario for 2030 differed for all common alternative fuels | Generation Neglecting of transport costs | no |

| Hobohm et al. [112] | 2018 | Calculation of energy carrier demand of different sectors and end user prices | Generation transport taxes/levies | no |

| Pfennig et al. [6] | 2017 | 2030/2050 generation costs of generalized PtL fuels from the North Sea and Morocco | Generation transport | no |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Appendix B

Environmental Impacts of CNG/LNG

References

- Intergovernmental Panel on Climate Change. Climate Change 2013: The Physical Science Basis. Contribution of Working Group I to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Stocker, T.F., Qin, D., Plattner, G.-K., Tignor, M., Allen, S.K., Boschung, J., Nauels, A., Xia, Y., Bex, V., Midgley, P.M., Eds.; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2013; p. 1535. [Google Scholar]

- United Nations. Paris Agreement. In Proceedings of the UN Climate Change Conference (COP21), Paris, France, 30 November–12 December 2015. [Google Scholar]

- Welke, M.; Beck, M. Klimaschutz in Zahlen, Fakten, Trends und Impulse Deutscher Klimapolitik Ausgabe 2020; Bundesministerium für Umwelt, Naturschutz und nukleare Sicherheit: Berlin, Germany, 2020.

- Schemme, S.; Breuer, J.L.; Köller, M.; Meschede, S.; Walman, F.; Samsun, R.C.; Peters, R.; Stolten, D. H2-based synthetic fuels: A techno-economic comparison of alcohol, ether and hydrocarbon production. Int. J. Hydrog. Energy 2020, 45, 5395–5414. [Google Scholar] [CrossRef]

- Prussi, M.; Yugo, M.; Prada, L.D.; Padella, M.; Edwards, R. JEC Well-To-Wheels Report v5; Publications Office of the European Union: Luxembourg, 2020.

- Pfennig, M.; Gerhardt, N.; Pape, C.; Böttger, D. Mittel-und Langfristige Potenziale von PtL-und H2-Importen aus Internationalen EE-Vorzugsregionen; Fraunhofer-Institut für Windenergie und Energiesystemtechnik: Kassel, Germany, 2017. [Google Scholar]

- Schorn, F.; Breuer, J.L.; Samsun, R.C.; Schnorbus, T.; Heuser, B.; Peters, R.; Stolten, D. Methanol as a renewable energy carrier: An assessment of production and transportation costs for selected global locations. Adv. Appl. Energy 2021, 3, 100050. [Google Scholar] [CrossRef]

- Bracker, J.; Timpe, C. An Outline of Sustainability Criteria for Synthetic Fuels Used in Transport; Öko-Institut e.V.: Freiburg, Germany, 2017. [Google Scholar]

- Liebich, A.; Fröhlich, T.; Münter, D.; Fehrenbach, H.; Giegrich, J.; Köppen, S.; Dünnebeil, F.; Knörr, W.; Biemann, K.; Simon, S.; et al. Detailed Analyses of the System Comparison of Storable Energy Carriers from Renewable Energies—Final Report; Federal Environment Agency: Dessau-Roßlau, Germany, 2021. Available online: https://inis.iaea.org/search/search.aspx?orig_q=reportnumber:%22UBA-FB--000263/ANH%22 (accessed on 9 December 2021).

- Liebich, A.; Fröhlich, T.; Münter, D.; Fehrenbach, H.; Giegrich, J.; Köppen, S.; Dünnebeil, F.; Knörr, W.; Biemann, K.; Simon, S.; et al. Detailed Analyses of the System Comparison of Storable Energy Carriers from Renewable Energies—Annex; Federal Environment Agency: Dessau-Roßlau, Germany, 2021. Available online: https://www.researchgate.net/publication/350121764_Full_text_SYSEET_Detailed_analyses_of_the_system_comparison_of_storable_energy_carriers_from_renewable_energies_Annex (accessed on 9 December 2021).

- Ziolkowska, J.R. Chapter 1—Biofuels technologies: An overview of feedstocks, processes, and technologies. In Biofuels for a More Sustainable Future; Elsevier: Amsterdam, The Netherlands, 2020; pp. 1–19. [Google Scholar] [CrossRef]

- Peters, R.; Decker, M.; Eggemann, L.; Schemme, S.; Schorn, F.; Breuer, J.L.; Weiske, S.; Pasel, J.; Samsun, R.C.; Stolten, D. Thermodynamic and ecological preselection of synthetic fuel intermediates from biogas at farm sites. Energy Sustain. Soc. 2020, 10, 4. [Google Scholar] [CrossRef]

- Peters, R.; Baltruweit, M.; Grube, T.; Samsun, R.C.; Stolten, D. A techno economic analysis of the power to gas route. J. CO2 Util. 2019, 34, 616–634. [Google Scholar] [CrossRef]

- Bruchof, D. Energiewirtschaftliche Verkehrsstrategie—Möglichkeiten und Grenzen Alternativer Kraftstoffe und Antriebe in Deutschland und der EU-27. Ph.D. Thesis, Universität Stuttgart, Stuttgart, Germany, 2012. [Google Scholar]

- Mankins, J.C. Technology Readiness Levels: A White Paper; NASA, Office of Space Access and Technology, Advanced Concepts Office: Washington, DC, USA, 1995.

- Assistant Secretary of Defense for Research and Engineering. Technology Readiness Assessment (TRA) Guidance; Department of Defense: Washington, DC, USA, 2011.

- European Space Agency. Technology Readiness Level (TRL). Available online: http://sci.esa.int/sci-ft/50124-technology-readiness-level/ (accessed on 29 July 2019).

- European Commission. Horizon 2020—Work Programme 2016–2017. In 20. General Annexes; European Commission: Brussels, Belgium, 2017; p. 29. [Google Scholar]

- ISO 16290:2013; Space Systems—Definition of the Technology Readiness Levels (TRLs) and Their Criteria of Assessment. International Organization for Standardization: Geneva, Switzerland, 2013.

- Rose, A.D.; Buna, M.; Strazza, C.; Olivieri, N.; Stevens, T.; Peeters, L.; Tawil-Jamault, D. Technology Readiness Level Guidance Principles for Renewable Energy Technologies—Final Report; European Commission: Brussels, Belgium, 2017. [Google Scholar]

- Australian Renewable Energy Agency. Commercial Readiness Index for Renewable Energy Sector. Available online: https://arena.gov.au/assets/2014/02/Commercial-Readiness-Index.pdf (accessed on 18 March 2021).

- Wermuth, M.; Neef, C.; Wirth, R.; Hanitz, I.; Löhner, H.; Hautzinger, H.; Stock, W.; Pfeiffer, M.; Fuchs, M.; Lenz, B.; et al. Kraftfahrzeugverkehr in Deutschland 2010; Bundesministerium für Verkehr, Bau und Stadtentwicklung: Braunschweig, Germany, 2012.

- Nobis, C.; Kuhnimhof, T. Mobilität in Deutschland—MiD Ergebnisbericht, Studie von Infas, DLR, IVT und Infas 360 im Auftrag des Bundesministers für Verkehr und Digitale Infrastruktur; Infas Institut für Angewandte Sozialwissenschaft GmbH: Bonn/Berlin, Germany, 2018. [Google Scholar]

- Radke, S. Verkehr in Zahlen 2019/2020; Bundesministerium für Verkehr und digitale Infrastruktur: Flensburg, Germany, 2019.

- Tesla, Inc. WLTP Reichweite Tesla Model S. Available online: https://www.tesla.com/de_de/models (accessed on 14 May 2020).

- Breuer, J.L.; Can Samsun, R.; Peters, R.; Stolten, D. Road traffic volume map 2014 for North Rhine-Westphalia, Germany. Harv. Dataverse 2019. [Google Scholar] [CrossRef]

- Breuer, J.L.; Samsun, R.C.; Peters, R.; Stolten, D. The impact of diesel vehicles on NOx and PM10 emissions from road transport in urban morphological zones: A case study in North Rhine-Westphalia, Germany. Sci. Total Environ. 2020, 727, 138583. [Google Scholar] [CrossRef] [PubMed]

- McKinsey & Company. Hydrogen-Powered Aviation a Fact-Based Study of Hydrogen Technology, Economics, and Climate Impact by 2050; Publications Office of the European Union: Luxembourg, 2020.

- Bundesnetzagentur für Elektrizität, Gas, Telekommunikation, Post und Eisenbahnen; Marktuntersuchung Eisenbahnen: Bonn, Germany, 2019.

- Deutsche Bahn Netze. Infrastrukturregister: Grundsätze Stand Juni 2019, Version 4. Available online: https://fahrweg.dbnetze.com/fahrweg-de/kunden/nutzungsbedingungen/infrastrukturregister/grundsaetze-1369462 (accessed on 5 August 2019).

- Statistisches Bundesamt. Güterverkehrsstatistik der Binnenschifffahrt 2016; Statistisches Bundesamt: Wiesbaden, Germany, 2017.

- Helgeson, B.; Peter, J. The role of electricity in decarbonizing European road transport—Development and assessment of an integrated multi-sectoral model. Appl. Energy 2020, 262, 114365. [Google Scholar] [CrossRef] [Green Version]

- Köhler, J.; Kirsch, D.; Klukas, A.; Timmerberg, S.; Kaltschmitt, M. Teilstudie “Studie über die Marktreife von Erdgasmotoren in der Binnen-und Seeschifffahrt”; Wissenschaftliche Beratung des BMVI zur Mobilitäts-und Kraftstoffstrategie: Karlsruhe, Germany, 2018.

- Robinius, M.; Markewitz, P.; Lopion, P.; Kullmann, F.; Heuser, P.-M.; Syranidis, K.; Cerniauskas, S.; Schöb, T.; Reuß, M.; Ryberg, S.; et al. Wege Für Die Energiewende Kosteneffiziente und klimagerechte Transformationsstrategien für das deutsche Energiesystem bis zum Jahr 2050. Energy Environ. 2020, 499, 1–141. [Google Scholar]

- Van Wijk, A.; van der Roest, E.; Boere, J. Solar Power to the People; IOS Press BV: Amsterdam, The Netherlands, 2017. [Google Scholar]

- Hydrogen Council. Path to Hydrogen Competitiveness a Cost Perspective; Hydrogen Council: Brussels, Belgium, 2020.

- Hydrogen Council, McKinsey & Company. Hydrogen Insights a Perspective on Hydrogen Investment, Market Development and Cost Competitiveness; Hydrogen Council: Brussels, Belgium, 2021.

- Transport & Environment. RED II and Advanced Biofuels, Recommendations about Annex IX of the Renewable Energy Directive and Its Implementation at National Level; Transport & Environment: Brussels, Belgium, 2020.

- European Union. Directive (EU) 2018/2001 of the European Parliament and of the Council of 11 December 2018 on the Promotion of the Use of Energy from Renewable Sources (Recast); European Union: Brussels, Belgium, 2018. [Google Scholar]

- Gemeinsame Forschungsstelle, Institut für Energie und Verkehr; Hamje, H.; Hass, H.; Lonza, L.; Maas, H.; Reid, A.; Rose, K.D.; Venderbosch, T. EU Renewable Energy Targets in 2020: Revised Analysis of Scenarios for Transport Fuels; Publications Office: Brussels, Belgium, 2014.

- European Commission. Report from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions on the Status of Production Expansion of Relevant Food and Feed Crops Worldwide; European Commission: Brussels, Belgium, 2019. [Google Scholar]

- European Commission. Commission Delegated Regulation (EU) 2019/807 of 13 March 2019 Supplementing Directive (EU) 2018/2001 of the European Parliament and of the Council as Regards the Determination of High Indirect Land-Use Change-Risk Feedstock for Which a Significant Expansion of the Production Area into Land with High Carbon Stock Is Observed and the Certification of Low Indirect Land-Use Change-Risk Biofuels, Bioliquids and Biomass Fuels; European Union: Brussels, Belgium, 2019. [Google Scholar]

- Mineralöl Wirtschafts Verband e.V. Jahresbericht 2018, Vision 2050, Flüssige Kraftstoffe bewegen Deutschland auch 2050. Available online: https://www.mwv.de/wp-content/uploads/2016/06/180830_MWV_Jahresbericht-2018_RZ_Web_es_small.pdf (accessed on 20 February 2020).

- Arbeitsgruppe Erneuerbare Energien-Statistik. Erneuerbare Energien in Deutschland Daten zur Entwicklung im Jahr 2019; Umweltbundesamt: Dessau-Roßlau, Germany, 2020.

- Referat 221—Grundsatzangelegenheiten der Gruppe 22, Anerkennungs- und Akkreditierungsfragen, nachhaltige Biomasse. Evaluations-und Erfahrungsbericht für das Jahr 2017—Biomassestrom-Nachhaltigkeitsverordnung—Biokraftstoff-Nachhaltigkeitsverordnung; Bundesanstalt für Landwirtschaft und Ernährung: Bonn, Germany, 2018.

- Fehrenbach, H. Einsatz von Biokraftstoffen im Verkehrssektor bis 2030; IFEU—Institut für Energie-und Umweltforschung GmbH: Heidelberg, Germany, 2019.

- Billig, E.; Decker, M.; Benzinger, W.; Ketelsen, F.; Pfeifer, P.; Peters, R.; Stolten, D.; Thrän, D. Non-fossil CO2 recycling—The technical potential for the present and future utilization for fuels in Germany. J. CO2 Util. 2019, 30, 130–141. [Google Scholar] [CrossRef]

- Brosowski, A.; Thrän, D.; Mantau, U.; Mahro, B.; Erdmann, G.; Adler, P.; Stinner, W.; Reinhold, G.; Hering, T.; Blanke, C. A review of biomass potential and current utilisation—Status quo for 93 biogenic wastes and residues in Germany. Biomass Bioenergy 2016, 95, 257–272. [Google Scholar] [CrossRef] [Green Version]

- DBFZ Deutsches Biomasseforschungszentrum gemeinnützige GmbH; Brosowski, A.; Adler, P.; Erdmann, G.; Stinner, W.; Thrän, D.; Mantau, U.; Blanke, C.; Mahro, B.; Hering, T.; et al. Biomassepotentiale von Rest-und Abfallstoffen; Fachagentur Nachwachsende Rohstoffe e. V. (FNR): Gülzow-Prüzen, Germany, 2015. [Google Scholar]

- Fehrenbach, H.; Giegrich, J.; Köppen, S. BioRest: Verfügbarkeit und Nutzungsoptionen Biogener Abfall-und Reststoffe im Energiesystem (Strom-, Wärme-und Verkehrssektor); Umweltbundesamt TEXTE: Berlin, Germany, 2019.

- Johansson, S. Limits to biofuels. EPJ Web Conf. 2013, 54, 01014. [Google Scholar] [CrossRef] [Green Version]

- De Castro, C.; Carpintero, Ó.; Frechoso, F.; Mediavilla, M.; de Miguel, L.J. A top-down approach to assess physical and ecological limits of biofuels. Energy 2014, 64, 506–512. [Google Scholar] [CrossRef]

- Soler, A.; Yugo, M. Role of E-Fuels in the European Transport System—Literature Review; No. 14/19; Concawe: Brussels, Belgium, 2020. [Google Scholar]

- Kasten, P.; Heinemann, C. Kein Selbstläufer: Klimaschutz und Nachhaltigkeit durch PtX.; Öko-Institut e.V.: Berlin, Germany, 2019. [Google Scholar]

- International Energy Agency. Technology Roadmap Biofuels for Transport. Available online: https://webstore.iea.org/download/direct/632?fileName=Biofuels_Roadmap_WEB.pdf (accessed on 18 March 2021).

- Eurostat Statistics Explained. Land Cover Statistics. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Land_cover_statistics#Land_cover_in_the_EU (accessed on 25 November 2020).

- Zelt, O.; Kobiela, G.; Ortiz, W.; Scholz, A.; Monnerie, N.; Rosenstiel, A.; Viebahn, P. Multikriterielle Bewertung von Bereitstellungstechnologien Synthetischer Kraftstoffe; Wuppertal Institut für Klima, Umwelt, Energie gGmbH: Wuppertal, Germany, 2021. [Google Scholar]

- ASTM D7566-20b; Standard Specification for Aviation Turbine Fuel Containing Synthesized Hydrocarbons. ASTM International: West Conshohocken, PA, USA, 2020.

- Wormslev, E.C.; Broberg, M.K. Nordic Perspectives on the Use of Advanced Sustainable Jet Fuel for Aviation—Update 2019; Nordic Energy Research: Kopenhagen, Denmark, 2020. [Google Scholar]

- ICAO Secretariat. Estimated Prices of Aviation Alternative Fuels. In Proceedings of the Conference on Aviation and Alternative Fuels, Mexico City, Mexico, 11 October 2017. [Google Scholar]

- Sustainable Aviation. Sustainable Aviation Fuels Road-Map. Available online: https://www.sustainableaviation.co.uk/wp-content/uploads/2020/02/SustainableAviation_FuelReport_20200231.pdf (accessed on 26 March 2020).

- Schmidt, P.; Batteiger, V.; Roth, A.; Weindorf, W.; Raksha, T. Power-to-Liquids as Renewable Fuel Option for Aviation: A Review. Chem. Ing. Tech. 2018, 90, 127–140. [Google Scholar] [CrossRef]

- Tabak, S.A.; Avidan, A.A.; Krambeck, F.J. Production of Synthetic Gasoline and Diesel Fuel from Non-Petroleum Resources; Mobil Research and Development Corp., Research Dept., Paulsboro Lab.: Paulsboro, NJ, USA, 1986; pp. 293–299. [Google Scholar]

- Tabak, S.A.; Yurchak, S. Conversion of methanol over ZSM-5 to fuels and chemicals. Catal. Today 1990, 6, 307–327. [Google Scholar] [CrossRef]

- Ruokonen, J.; Nieminen, H.; Dahiru, A.R.; Laari, A.; Koiranen, T.; Laaksonen, P.; Vuokila, A.; Huuhtanen, M. Modelling and Cost Estimation for Conversion of Green Methanol to Renewable Liquid Transport Fuels via Olefin Oligomerisation. Processes 2021, 9, 1046. [Google Scholar] [CrossRef]

- Zech, K.; Naumann, K.; Müller-Langer, F.; Schmidt, P.; Weindorf, W.; Altmann, M.; Michalski, J.; Niklaß, M.; Meyer, H.; Lischke, A.; et al. Biokerosin und EE-Kerosin für Die Luftfahrt der Zukunft—von der Theorie zu Pilotvorhaben; Federal Ministry for Digital and Transport: Leipzig, Germany; Munich, Germany; Berlin/Heidelberg, Germany, 2011.

- Fulcrum. Sierra BioFuels Plant. Available online: http://fulcrum-bioenergy.com/facilities/ (accessed on 3 December 2020).

- Red Rock Biofuels. Red Rock Biofuels—Lakeview Plant. Available online: https://www.redrockbio.com/lakeview-site/ (accessed on 3 December 2020).

- Neste Oyj. What Is Neste MY Sustainable Aviation Fuel? Available online: https://www.neste.com/products/all-products/aviation/key-benefits (accessed on 3 December 2020).

- BETO-Funded Technology Produces Jet Fuel for Virgin Atlantic. Available online: https://www.energy.gov/eere/bioenergy/articles/beto-funded-technology-produces-jet-fuel-virgin-atlantic (accessed on 3 December 2020).

- Ekobenz. Innovative Production of Synthetic Fuels. Available online: http://ekobenz.com/production-plant (accessed on 3 December 2020).

- Stark, A. Lanzatech Wins Bid for World’s First Large Scale ATJ Facility. Available online: www.process-worldwide.com (accessed on 21 December 2021).

- European Comission. Production of Fully Synthetic Paraffinic Jet Fuel from Wood and Other Biomass. Available online: https://cordis.europa.eu/project/id/612763 (accessed on 3 December 2020).

- Euglena Co. Ltd. ASTM D7566 Revised to Add a New Standard for Jet Fuel Produced through the BIC Process, the Technology Employed in Euglena Co’s Demo Plant. Available online: https://www.euglena.jp/pdf/n20200131.pdf (accessed on 21 December 2021).

- IHI. Bio-jet Fuel Manufactured from Microalgae Receives ASTM International Standard Certification-Contributing to the Reduction of CO2 Emissions from Aircraft. Available online: https://www.ihi.co.jp/en/all_news/2020/other/1196667_2042.html (accessed on 21 December 2021).

- Müller-Langer, F.; Majer, S.; O’Keeffe, S. Benchmarking biofuels—A comparison of technical, economic and environmental indicators. Energy Sustain. Soc. 2014, 4, 20. [Google Scholar] [CrossRef] [Green Version]

- Leitner, W.; Klankermayer, J.; Pischinger, S.; Pitsch, H.; Kohse-Hoinghaus, K. Advanced Biofuels and Beyond: Chemistry Solutions for Propulsion and Production. Angew. Chem. Int. Ed. 2017, 56, 5412–5452. [Google Scholar] [CrossRef] [PubMed]

- Schemme, S.; Breuer, J.L.; Samsun, R.C.; Peters, R.; Stolten, D. Promising catalytic synthesis pathways towards higher alcohols as suitable transport fuels based on H2 and CO2. J. CO2 Util. 2018, 27, 223–237. [Google Scholar] [CrossRef]

- Schemme, S.; Meschede, S.; Köller, M.; Samsun, R.C.; Peters, R.; Stolten, D. Property Data Estimation for Hemiformals, Methylene Glycols and Polyoxymethylene Dimethyl Ethers and Process Optimization in Formaldehyde Synthesis. Energies 2020, 13, 3401. [Google Scholar] [CrossRef]

- Deutsche Energie-Agentur. Audi E-Gas Projekt. Available online: https://www.powertogas.info/projektkarte/audi-e-gas-projekt/ (accessed on 10 January 2020).

- BMWi, Federal Ministry for Economic Affairs and Climate Action. The National Hydrogen Strategy; BMWi: Berlin, Germany, 2020.

- Bründlinger, T.; König, J.E.; Frank, O.; Gründig, D.; Jugel, C.; Kraft, P.; Krieger, O.; Mischinger, S.; Prein, D.P.; Seidl, H.; et al. Dena-Leitstudie Integrierte Energiewende; Deutsche Energie-Agentur: Berlin, Germany, 2018. [Google Scholar]

- Merten, F.; Scholz, A.; Krüger, C.; Heck, S.; Girard, Y.; Mecke, M.; Goerge, M. Bewertung der Vor-und Nachteile von Wasserstoffimporten im Vergleich zur Heimischen Erzeugung; Wuppertal Institut, DIW Econ: Wuppertal, Germany, 2020. [Google Scholar]

- Dena, German Energy Agency. Zwischenbericht, dena-Leitstudie Aufbruch Klimaneutralität, Ein Blick in die Werkstatt: Erste Erkenntnisse und Ableitungen Zentraler Handlungsfelder; Deutsche Energie-Agentur GmbH: Berlin, Germany, 2021. [Google Scholar]

- Perner, J.; Unteutsch, M.; Lövenich, A. The Future Cost of Electricity-Based Synthetic Fuels; Agora Energiewende, Frontier Economics: Berlin, Germany, 2018. [Google Scholar]

- Fasihi, M.; Breyer, C. Baseload electricity and hydrogen supply based on hybrid PV-wind power plants. J. Clean. Prod. 2020, 243, 118466. [Google Scholar] [CrossRef]

- Hank, C.; Sternberg, A.; Köppel, N.; Holst, M.; Smolinka, T.; Schaadt, A.; Hebling, C.; Henning, H.-M. Energy efficiency and economic assessment of imported energy carriers based on renewable electricity. Sustain. Energy Fuels 2020, 4, 2256–2273. [Google Scholar] [CrossRef]

- Ishmam, S.; Winkler, C.; Sanchez, P.-E.; Ojieabu, N.; Heinrichs, H.; Agbo, S.; Kuckertz, P.; Khuat, H.; Patil, S.; Kotzur, L.; et al. H2ATLAS-AFRICA. Available online: https://africa.h2atlas.de/ (accessed on 21 December 2021).

- Schindler, J. Gestehungskosten von PtX-Produkten im Vergleich Zwischen Deutschland und Nordafrika; EnergieAgentur.NRW: Wuppertal, Germany, 2019. [Google Scholar]

- Eichhammer, W.; Oberle, S.; Händel, M.; Boie, I.; Gnann, T.; Wietschel, M.; Lux, B. Study on the Opportunities of “Power-to-X” in Morocco; Fraunhofer Institute for Systems and Innovation Research: Karlsruhe, Germany, 2019. [Google Scholar]

- IEA, International Energy Agency. The Future of Hydrogen Seizing Today’s Opportunities. Available online: https://iea.blob.core.windows.net/assets/9e3a3493-b9a6-4b7d-b499-7ca48e357561/The_Future_of_Hydrogen.pdf (accessed on 9 November 2021).

- Kreidelmeyer, S.; Dambeck, H.; Kirchner, A.; Wünsch, M. Kosten und Transformationspfade für Strombasierte Energieträger; Prognos AG: Basel, Switzerland, 2020. [Google Scholar]

- IEA, International Energy Agency. IEA G20 Hydrogen Report: Assumptions. Available online: https://iea.blob.core.windows.net/assets/29b027e5-fefc-47df-aed0-456b1bb38844/IEA-The-Future-of-Hydrogen-Assumptions-Annex_CORR.pdf (accessed on 21 December 2021).

- Robinius, M. Strom- und Gasmarktdesign zur Versorgung des Deutschen Straßenverkehrs mit Wasserstoff; Forschungszentrum Jülich: Jülich, Germany, 2016; Volume 300. [Google Scholar]

- Kawasaki. Liquefied Hydrogen Carrier with World’s Highest Carrying Capacity—AiP Obtained from ClassNK. Available online: https://global.kawasaki.com/en/corp/newsroom/news/detail/?f=20210506_9983 (accessed on 15 December 2021).

- Fraunhofer IEE. PtX-Atlas. Available online: https://maps.iee.fraunhofer.de/ptx-atlas/ (accessed on 20 December 2021).

- Huss, A.; Maas, H.; Hass, H. Well-to-Wheels Analysis of Future Automotive Fuels and Powertrains in the European Context TANK-TO-WHEELS (TTW) Report Version 4; Publications Office of the European Union: Luxembourg, 2013.

- Robinius, M.; Linßen, J.; Grube, T.; Reuß, M.; Stenzel, P.; Syranidis, K.; Kuckertz, P.; Stolten, D. Comparative Analysis of Infrastructures: Hydrogen Fueling and Electric Charging of Vehicles. Schr. Des Forsch. Jülich Reihe Energ. Umw. Energy Environ. 2018, 408, 108. [Google Scholar]

- Union zur Förderung von Oel-und Proteinpflanzen e.V. UFOP Report on Global Market Supply 2020/2021. Available online: https://www.ufop.de/files/7216/1649/5848/UFOP_SupplyReport_2020-2021__120321.pdf (accessed on 2 December 2021).

- Völler, K.; Reinholz, T. Branchenbarometer Biomethan 2019; Deutsche Energie-Agentur GmbH: Berlin, Germany, 2019. [Google Scholar]

- Bundesministerium für Wirtschaft und Energie. Gesamtausgabe der Energiedaten—Datensammlung des BMWi. Available online: https://www.bmwi.de/Redaktion/DE/Binaer/Energiedaten/energiedaten-gesamt-xls.html (accessed on 18 February 2021).

- Detz, R.J.; Reek, J.N.H.; van der Zwaan, B.C.C. The future of solar fuels: When could they become competitive? Energy Environ. Sci. 2018, 11, 1653–1669. [Google Scholar] [CrossRef]

- Union zur Förderung von Oel-und Proteinpflanzen e.V. UFOP Report on Global Market Supply 2018/2019. Available online: https://www.ufop.de/files/4815/4695/8891/WEB_UFOP_Report_on_Global_Market_Supply_18-19.pdf (accessed on 18 February 2021).

- Jensterle, M.; Narita, J.; Piria, R.; Schröder, J.; Steinbacher, K.; Wahabzada, F.; Zeller, T.; Crone, K.; Löchle, S. Grüner Wasserstoff: Internationale Kooperations-Potenziale für Deutschland Kurzanalyse zu Ausgewählten Aspekten Potenzieller Nicht-EU-Partnerländer; Deutsche Energie-Agentur, Deutsche Gesellschaft für Internationale Zusammenarbeit, NAVIGANT, Adelphi: Berlin, Germany, 2019. [Google Scholar]

- Michalski, J.; Altmann, M.; Bünger, U.; Weindorf, W. Wasserstoffstudie Nordrhein-Westfalen; Ministerium für Wirtschaft, Innovation, Digitalisierung und Energie des Landes Nordrhein-Westfalen: Düsseldorf, Germany, 2019.

- Gerhardt, N.; Bard, J.; Schmitz, R.; Beil, M.; Pfennig, M.; Kneiske, T. Wasserstoff im Zukünftigen Energiesystem: Fokus Gebäudewärme; Fraunhofer-Institut für Energiewirtschaft und Energiesystemtechnik: Kassel, Germany, 2020. [Google Scholar]

- Mottschall, M.; Kasten, P.; Kühnel, S.; Minnich, L. Sensitivitäten zur Bewertung der Kosten verschiedener Energieversorgungs-Optionen des Verkehrs bis zum Jahr 2050; TEXTE 114/2019; Umweltbundesamt, Öko-Institut: Dessau-Roßlau, Germany, 2019.

- Schmidt, P.R.; Zittel, W.; Weindorf, W.; Raksha, T. Renewables in Transport 2050; Forschungsvereinigung Verbrennungskraftmaschinen e.V.: Frankfurt am Main, Germany, 2016. [Google Scholar]

- Kramer, U.; Ortloff, F.; Stollenwerk, S.; Thee, R. Defossilisierung des Transportsektors; Forschungsvereinigung Verbrennungskraftmaschinen e.V.: Frankfurt am Main, Germany, 2018. [Google Scholar]

- Perner, J.; Unteutsch, M.; Lövenich, A. Die Zukünftigen Kosten Strombasierter Synthetischer Brennstoffe; Agora Verkehrswende, Agora Energiewende, Frontier Economics: Berlin, Germany, 2018. [Google Scholar]

- Terlouw, W.; Peters, D.; Tilburg, J.v.; Schimmel, M.; Berg, T.; Cihlar, J.; Mir, G.U.R.; Spöttle, M.; Staats, M.; Lejaretta, A.V.; et al. Gas for Climate. The Optimal Role for Gas in a Net-Zero Emissions Energy System; Navigant Netherlands B.V.: Utrecht, The Netherlands, 2019. [Google Scholar]

- Hobohm, J.; der Maur, A.A.; Dambeck, H.; Kemmler, A.; Koziel, S.; Kreidelmeyer, S.; Piégsa, A.; Wendring, P.; Meyer, B.; Apfelbacher, A.; et al. Status und Perspektiven Flüssiger Energieträger in der Energiewende; Fraunhofer Institut für Umwelt-, Sicherheits-und Energietechnik: Oberhausen, Germany; Deutsches Biomasseforschungszentrum gemeinnützige GmbH: Leipzig, Germany, 2018. [Google Scholar]

- Fasihi, M.; Breyer, C. Synthetic Fuels and Chemicals: Options and Systemic Impact. In Proceedings of the Strommarkttreffen, Berlin, Germany, 29 June 2018. [Google Scholar]

- DIN EN 590; Automotive Fuels—Diesel—Requirements and Test Methods. Deutsches Institut für Normung e.V.: Berlin, Germany, 2014.

- DIN EN 228; Automotive Fuels—Unleaded Petrol—Requirements and Test Methods. Deutsches Institut für Normung e.V.: Berlin, Germany, 2017.

- Schripp, T.; Herrmann, F.; Oßwald, P.; Köhler, M.; Zschocke, A.; Weigelt, D.; Mroch, M.; Werner-Spatz, C. Particle emissions of two unblended alternative jet fuels in a full scale jet engine. Fuel 2019, 256, 115903. [Google Scholar] [CrossRef]

- Sasol AG. Sasol Takes to the Skies with the World’s First Fully Synthetic Jet Fuel. Available online: https://www.sasol.com/media-centre/media-releases/sasol-takes-skies-world-s-first-fully-synthetic-jet-fuel (accessed on 21 December 2021).

- International Air Transport Association. IATA Guidance Material for Sustainable Aviation Fuel Management; International Air Transport Association: Montreal, QC, Canada; Geneva, Switzerland, 2012. [Google Scholar]

- Zech, K.; Naumann, K.; Müller-Langer, F.; Schmidt, P.; Weindorf, W.; Mátra, Z. Drop-In-Kraftstoffe für die Luftfahrt. Studie im Rahmen des Auftrags» Wissenschaftliche Begleitung, Unterstützung und Beratung des BMVI in den Bereichen Verkehr und Mobilität mit besonderem Fokus auf Kraftstoffe und Antriebstechnologien sowie Energie und Klima für das Bundesministerium für Verkehr und digitale Infrastruktur (BMVI); Deutsches Zentrum Für Luft-Und Raumfahrt e. V.(DLR): Berlin, Germany, 2014. [Google Scholar]

- Bauen, A.; Gomez, I.; OudeNijeweme, D.; Paraschiv, M. Alternative Fuels—Expert Group Report; European Commission: Brussels, Belgium, 2017. [Google Scholar]

- ASTM D4806-13a; Standard Specification for Denatured Fuel Ethanol for Blending with Gasolines for Use as Automotive Spark-Ignition Engine Fuel. ASTM International: West Conshohocken, PA, USA, 2013. [CrossRef]

- ASTM D7862-13; Standard Specification for Butanol for Blending with Gasoline for Use as Automotive Spark-Ignition Engine Fuel. ASTM International: West Conshohocken, PA, USA, 2013.

- Institut für nachhaltige Wirtschaft und Logistik. Potenzialanalyse Methanol als Emissionsneutraler Energieträger für Schifffahrt und Energiewirtschaft; Maritimes Cluster Norddeutschland e. V.: Elsfleth, Germany, 2018. [Google Scholar]

- Wei, H.; Feng, D.; Pan, J.; Shao, A.; Pan, M. Knock characteristics of SI engine fueled with n-butanol in combination with different EGR rate. Energy 2017, 118, 190–196. [Google Scholar] [CrossRef]

- ASTM D975-20c; Standard Specification for Diesel Fuel. ASTM International: West Conshohocken, PA, USA, 2020. [CrossRef]

- DIN EN 15940; Automotive Fuels—Paraffinic Diesel Fuel from Synthesis or Hydrotreatment—Requirements and Test Methods. Deutsches Institut für Normung e.V.: Berlin, Germany, 2019. [CrossRef]

- DIN EN 16709; Automotive Fuels—High FAME Diesel Fuel (B20 and B30)—Requirements and Test Methods. Deutsches Institut für Normung e.V.: Berlin, Germany, 2019.

- DIN EN 14214; Liquid Petroleum Products—Fatty Acid Methyl Esters (Fame) for Use in Diesel Engines and Heating Applications—Requirements and Test Methods. Deutsches Institut für Normung e.V.: Berlin, Germany, 2019.

- Bohl, T.; Smallbone, A.; Tian, G.; Roskilly, A.P. Particulate number and NO trade-off comparisons between HVO and mineral diesel in HD applications. Fuel 2018, 215, 90–101. [Google Scholar] [CrossRef] [Green Version]

- Kuronen, M.; Mikkonen, S.; Aakko, P.; Murtonen, T. Hydrotreated Vegetable Oil as Fuel for Heavy Duty Diesel Engines. SAE Tech. Pap. 2007, 2007-01-4031. [Google Scholar] [CrossRef]

- Sayin, C.; Ozsezen, A.N.; Canakci, M. The influence of operating parameters on the performance and emissions of a DI diesel engine using methanol-blended-diesel fuel. Fuel 2010, 89, 1407–1414. [Google Scholar] [CrossRef]

- Sayin, C. Engine performance and exhaust gas emissions of methanol and ethanol–diesel blends. Fuel 2010, 89, 3410–3415. [Google Scholar] [CrossRef]

- Damyanov, A. Alcoholic Fuels in Diesel Engines. Methanol, Ethanol and Butanol. In Zukünftige Kraftstoffe. ATZ/MTZ-Fachbuch; Maus, W., Ed.; Springer: Berlin/Heidelberg, Germany, 2019. [Google Scholar] [CrossRef]

- Rajesh Kumar, B.; Saravanan, S.; Rana, D.; Anish, V.; Nagendran, A. Effect of a sustainable biofuel—n-octanol—On the combustion, performance and emissions of a DI diesel engine under naturally aspirated and exhaust gas recirculation (EGR) modes. Energy Convers. Manag. 2016, 118, 275–286. [Google Scholar] [CrossRef]

- Continental. Klimaneutral Fahren: Continental Testet Erfolgreich Synthetischen Diesel-Ersatzkraftstoff OME. Available online: https://www.continental.com/de/presse/pressemitteilungen/2017-08-01-klimaneutral-fahren-92062 (accessed on 21 December 2021).

- Beidl, C.; Münz, M.; Mokros, A. Synthetische Kraftstoffe. In Zukünftige Kraftstoffe. ATZ/MTZ-Fachbuch; Maus, W., Ed.; Springer Vieweg: Berlin/Heidelberg, Germany, 2019; pp. 814–849. [Google Scholar] [CrossRef]

- Hemighaus, R.; Boval, T.; Bacha, J.; Barnes, F.; Franklin, M.; Gibbs, L.; Hogue, N.; Jones, J.; Lesnini, D.; Lind, J.; et al. Aviation Fuels Technical Review. Available online: https://skybrary.aero/bookshelf/books/2478.pdf (accessed on 28 June 2021).

- ASTM D7467-20a; Standard Specification for Diesel Fuel Oil, Biodiesel Blend (B6 to B20). ASTM International: West Conshohocken, PA, USA, 2020. [CrossRef]

- DIN EN 16734; Automotive Fuels—Automotive B10 Diesel Fuel—Requirements and Test Methods. Deutsches Institut für Normung e.V.: Berlin, Germany, 2016.

- Mignard, D.; Pritchard, C. On the use of electrolytic hydrogen from variable renewable energies for the enhanced conversion of biomass to fuels. Chem. Eng. Res. Des. 2008, 86, 473–487. [Google Scholar] [CrossRef]

- Eichlseder, H.; Klell, M. Speicherung und Transport. In Wasserstoff in der Fahrzeugtechnik: Erzeugung, Speicherung, Anwendung; Vieweg+Teubner: Wiesbaden, Germany, 2010; pp. 95–150. [Google Scholar]

- Aspen Plus® V10 [Computer software]; Aspen Technology Inc.: Delaware, DE, USA, 2017.

- ExxonMobil. ExxonMobil Jet Fuel. Available online: https://www.exxonmobil.com/en-FI/Commercial-Fuel/pds/GL-XX-JetFuel-Series (accessed on 26 May 2020).

- Hahne, E. Technische Thermodynamik; Springer: Oldenbourg, Germany, 2011. [Google Scholar]

- National Institute of Standards and Technology. NIST Standard Reference Simulation Website; NIST Standard Reference Database Number: Gaithersburg, MD, USA, 2019; Volume 173. [Google Scholar]

- Kim, S.; Thiessen, P.A.; Bolton, E.E.; Chen, J.; Fu, G.; Gindulyte, A.; Han, L.; He, J.; He, S.; Shoemaker, B.A.; et al. PubChem Substance and Compound databases. Nucleic Acids Res. 2016, 44, D1202–D1213. [Google Scholar] [CrossRef] [PubMed]

- Liu, H.; Wang, Z.; Wang, J.; He, X.; Zheng, Y.; Tang, Q.; Wang, J. Performance, combustion and emission characteristics of a diesel engine fueled with polyoxymethylene dimethyl ethers (PODE3-4)/diesel blends. Energy 2015, 88, 793–800. [Google Scholar] [CrossRef]

- Ulvestad, A. A brief Review of Current Lithium Ion Battery Technology and Potential Solid State Battery Technologies. arXiv 2018, arXiv:1803.04317. [Google Scholar]

- Institut für Arbeitsschutz der Deutschen Gesetzlichen Unfallversicherung. GESTIS-Stoffdatenbank Methan. Available online: http://gestis.itrust.de/nxt/gateway.dll/gestis_de/000000.xml?f=templates$fn=default.htm$vid=gestisdeu:sdbdeu$3.0 (accessed on 26 May 2020).

- BP P.L.C. Safety data sheet Residual Fuel Oil (Flashpoint > 100 °C)—Blended. Available online: https://www.bp.com/content/dam/bp/business-sites/en/global/bp-global-energy-trading/documents/what-we-do/marine/ara/belguim-rma-rmk-terminal-high-flash.pdf (accessed on 18 February 2021).

- Ernst, C.-S. Energetische, Ökologische und Ökonomische Lebenszyklusanalyseelektrifizierter Antriebsstrangkonzepte. Ph.D. Thesis, RWTH Aachen University, Aachen, Germany, 2015. [Google Scholar]

- Bräunling, W.J.G. Reale Triebwerkskreisprozesse. In Flugzeugtriebwerke: Grundlagen, Aero-Thermodynamik, Ideale und Reale Kreisprozesse, Thermische Turbomaschinen, Komponenten, Emissionen und Systeme; Springer: Berlin/Heidelberg, Germany, 2009; pp. 1141–1251. [Google Scholar]

- Van Basshuysen, R.; Schäfer, F. (Eds.) Handbuch Verbrennungsmotor: Grundlagen, Komponenten, Systeme, Perspektiven. 8. Überarbeitete Auflage ed.; Springer Vieweg: Wiesbaden, Germany, 2017; p. 1841. [Google Scholar]

- Füßel, A. Vergleich der aktuellen BEV-und ICE-Technologie. In Technische Potenzialanalyse der Elektromobilität; Springer Vieweg: Wiesbaden, Germany, 2017; pp. 15–33. [Google Scholar]

- Zerta, M.; Schmidt, P.; Weindorf, W.; Bünger, U.; Langfeldt, L.; Scholz, B.; Giebel, L.-V.; Klemm, P.; Sattler, G. SHIPFUEL–Strombasierte Kraftstoffe für Brennstoffzellen in der Binnenschifffahrt–Hintergrundbericht; Studie im Auftrag der Nationalen Organisation Wasserstoff-und Brennstoffzellentechnologie (NOW) für das Bundesministerium für Verkehr und Digitale Infrastruktur (BMVI); Nationale Organisation Wasserstoff- und Brennstoffzellentechnologie: München, Germany; Berlin/Hamburg; Germany, 2019. [Google Scholar]

- United States Department of Energy. Determining Electric Motor Load and Efficiency; EERE Publication and Product Library: Washington, DC, USA, 1997.

- Breeze, P. The Proton Exchange Membrane Fuel Cell. In Fuel Cells; Elsevier: Amsterdam, The Netherlands, 2017; pp. 33–43. [Google Scholar]

- Ahluwalia, R.K.; Wang, X. Direct hydrogen fuel cell systems for hybrid vehicles. J. Power Sources 2005, 139, 152–164. [Google Scholar] [CrossRef]

- INFRAS. Handbuch für Emissionsfaktoren des Straßenverkehrs (HBEFA). Available online: https://www.hbefa.net/d/ (accessed on 25 January 2021).

- Bünger, U.; Landinger, H.; Weindorf, W.; Wurster, R.; Zerhusen, J.; Zittel, W. Vergleich von CNG und LNG zum Einsatz in LKW im Fernverkehr, Eine Expertise für die Open Grid Europe GmbH | Abschlussbericht; Ludwig-Bölkow-Systemtechnik GmbH: Ottobrunn, Germany, 2016. [Google Scholar]

- Weiss, M.; Cloos, K.C.; Helmers, E. Energy efficiency trade-offs in small to large electric vehicles. Environ. Sci. Eur. 2020, 32, 46. [Google Scholar] [CrossRef] [Green Version]

- Otten, M.; ’T Hoen, M.; den Boer, E. STREAM Freight Transport 2016: Emissions of Freight Transport Modes; CE Delft: Delft, The Netherlands, 2017. [Google Scholar]

- CE Cideon Engineering GmbH Co. KG. Produktblatt Hybrid Lokomotive. Available online: https://www.cideon-engineering.com/de/wp-content/uploads/sites/2/2019/02/CE_Produktblatt_HybidLokomotive.pdf (accessed on 18 February 2021).

- Bombardier. World Premiere: Bombardier Transportation Presents a New Battery-Operated Train and Sets Standards for Sustainable Mobility. Available online: https://rail.bombardier.com/en/about-us/worldwide-presence/germany/de.html/bombardier/news/2018/bt-20180912-world-premiere--bombardier-transportation-presents-a/de (accessed on 21 December 2021).

- Vlexx GmbH. Bombardier TALENT 3 Datenblatt. Available online: https://www.vlexx.de/media/vlexx/downloads/ens/Datenblatt_TALENT-3_lr.pdf (accessed on 15 October 2021).

- Betz, P. Neue Diesel-Hybrid-Technik von Voith Turbo für Schienenfahrzeuge. Available online: https://www.openpr.de/news/194991/Neue-Diesel-Hybrid-Technik-von-Voith-Turbo-fuer-Schienenfahrzeuge.html (accessed on 21 December 2021).

- Alstom. World Premiere: Alstom’s Hydrogen Trains Enter Passenger Service in Lower Saxony. Available online: https://www.alstom.com/press-releases-news/2018/9/world-premiere-alstoms-hydrogen-trains-enter-passenger-service-lower (accessed on 21 December 2021).

- Plank-Wiedenbeck, U.; Jentsch, M.; Lademann, F.; Büttner, S.; Meyer, N.; Ivanov, A. Schlussbericht Machbarkeitsstudie Pilotprojekt Einsatz von H2BZ-Triebwagen in Thüringen; Freistaat Thüringen Ministerium für Umwelt, Energie und Naturschutz: Weimar, Germany, 2019.

- Deutsche Bahn AG. Grundlagenbericht UmweltMobilCheck, Stand 01.04.2016. Available online: https://www.deutschebahn.com/resource/blob/265408/a54aed9e6a0513294c3b9607986fb38f/umc__grundlagenbericht__2016-data.pdf (accessed on 22 June 2019).

- Roland Berger. Hydrogen—A Future Fuel for Aviation? Available online: https://www.rolandberger.com/publications/publication_pdf/roland_berger_hydrogen_the_future_fuel_for_aviation.pdf (accessed on 21 December 2021).

- Seeckt, K.; Scholz, D. Jet versus Prop, Hyrogen versus Kerosene for a Regional Freighter Aircraft. In Proceedings of the Deutscher Luft- und Raumfahrtkongress. 2009. Available online: https://www.fzt.haw-hamburg.de/pers/Scholz/GF/GF_Paper_DLRK_09-09-08.pdf (accessed on 21 December 2021).

- Umweltbundesamt. Jährliche Treibhausgas-Emissionen in Deutschland/Annual Greenhouse Gas Emissions in Germany—Nationales Treibhausgasinventar 2021, 12/2020; Umweltbundesamt: Dessau-Roßlau, Germany, 2021.

- Meyer, K.; Helms, H.; Fehrenbach, H.; Biemann, K.; Kämper, C.; Lambrecht, U.; Jöhrens, J. Klimabilanz von Strombasierten Antrieben und Kraftstoffen; Agora Verkehrswende: Berlin, Germany, 2019; p. 56. [Google Scholar]

- Naumann, K.; Schröder, J.; Oehmichen, K.; Etzold, H.; Müller-Langer, F.; Remmele, E.; Thuneke, K.; Raksha, T.; Schmidt, P. Monitoring Biokraftstoffsektor; Deutsches Biomasseforschugnszentrum gemeinnützige GmbH: Leipzig, Germany, 2019. [Google Scholar]

- ISO 14040; Environmental Management—Life Cycle Assessment—Principles and Framework. International Organization for Standardization (ISO): Geneva, Switzerland, 2006.

- ISO 14044; Environmental Management—Life Cycle Assessment—Requirements and Guidelines. International Organization for Standardization (ISO): Geneva, Switzerland, 2006.

- Moro, A.; Helmers, E. A new hybrid method for reducing the gap between WTW and LCA in the carbon footprint assessment of electric vehicles. Int. J. Life Cycle Assess. 2017, 22, 4–14. [Google Scholar] [CrossRef] [Green Version]

- Koj, J.C.; Wulf, C.; Zapp, P. Environmental impacts of power-to-X systems—A review of technological and methodological choices in Life Cycle Assessments. Renew. Sustain. Energy Rev. 2019, 112, 865–879. [Google Scholar] [CrossRef]

- Zhang, X.; Bauer, C.; Mutel, C.L.; Volkart, K. Life Cycle Assessment of Power-to-Gas: Approaches, system variations and their environmental implications. Appl. Energy 2017, 190, 326–338. [Google Scholar] [CrossRef]

- Walker, S.B.; Fowler, M.; Ahmadi, L. Comparative life cycle assessment of power-to-gas generation of hydrogen with a dynamic emissions factor for fuel cell vehicles. J. Energy Storage 2015, 4, 62–73. [Google Scholar] [CrossRef]

- Koj, J.C.; Wulf, C.; Linssen, J.; Schreiber, A.; Zapp, P. Utilisation of excess electricity in different Power-to-Transport chains and their environmental assessment. Transp. Res. Part D Transp. Environ. 2018, 64, 23–35. [Google Scholar] [CrossRef]

- Kigle, S.; Pichlmaier, S.; Huber, J.; Regett, A. Ökobilanz strombasierter synthetischer Kraftstoffe: Worauf es ankommt. EW 2019, 2019, 18–23. [Google Scholar]

- Wettstein, S.; Itten, R.; Stucki, M. Life Cycle Assessment of Renewable Methane for Transport and Mobility; Swiss National Science Foundation: Zürich, Switzerland, 2018; pp. 1–35. [Google Scholar]

- Rinawati, D.I.; Keeley, A.R.; Takeda, S.; Managi, S. A systematic review of life cycle assessment of hydrogen for road transport use. Prog. Energy 2021, 4, 012001. [Google Scholar] [CrossRef]

- Wulf, C.; Kaltschmitt, M. Hydrogen Supply Chains for Mobility—Environmental and Economic Assessment. Sustainability 2018, 10, 1699. [Google Scholar] [CrossRef] [Green Version]

- Koj, J.C.; Wulf, C.; Schreiber, A.; Zapp, P. Site-dependent environmental impacts of industrial hydrogen production by alkalinewater electrolysis. Energies 2017, 10, 860. [Google Scholar] [CrossRef] [Green Version]

- Bareiß, K.; de la Rua, C.; Möckl, M.; Hamacher, T. Life cycle assessment of hydrogen from proton exchange membrane water electrolysis in future energy systems. Appl. Energy 2019, 237, 862–872. [Google Scholar] [CrossRef]

- Kanz, O.; Bittkau, K.; Ding, K.; Rau, U.; Reinders, A. Review and Harmonization of the Life-Cycle Global Warming Impact of PV-Powered Hydrogen Production by Electrolysis. Front. Electron. 2021, 2, 711103. [Google Scholar] [CrossRef]

- Bongartz, D.; Doré, L.; Eichler, K.; Grube, T.; Heuser, B.; Hombach, L.E.; Robinius, M.; Pischinger, S.; Stolten, D.; Walther, G.; et al. Comparison of light-duty transportation fuels produced from renewable hydrogen and green carbon dioxide. Appl. Energy 2018, 231, 757–767. [Google Scholar] [CrossRef]

- Reiter, G.; Lindorfer, J. Global warming potential of hydrogen and methane production from renewable electricity via power-to-gas technology. Int. J. Life Cycle Assess. 2015, 20, 477–489. [Google Scholar] [CrossRef]

- Uusitalo, V.; Väisänen, S.; Inkeri, E.; Soukka, R. Potential for greenhouse gas emission reductions using surplus electricity in hydrogen, methane and methanol production via electrolysis. Energy Convers. Manag. 2017, 134, 125–134. [Google Scholar] [CrossRef]

- Prussi, M.; Yugo, M.; De Prada, L.; Padella, M.; Edwards, R.; Lonza, L. JEC Well-to-Tank report v5—Well-to-Wheels Analysis of Future Automotive Fuels and Powertrains in the European Context; Publications Office of the European Union: Luxembourg, 2020.

- Fachagentur Nachwachsende Rohstoffe e.V. Biokraftstoffe; Biokraftstoffe: Gülzow-Prüzen, Germany, 2014. [Google Scholar]

- Arvidsson, R.; Persson, S.; Fröling, M.; Svanström, M. Life cycle assessment of hydrotreated vegetable oil from rape, oil palm and Jatropha. J. Clean. Prod. 2011, 19, 129–137. [Google Scholar] [CrossRef]

- Bierkandt, T.; Severin, M.; Ehrenberger, S.; Köhler, M. Klimaneutrale Synthetische Kraftstoffe im Verkehr—Potenziale und Handlungsempfehlungen; DLR: Stuttgart, Germany, 2018. [Google Scholar]

- Biernacki, P.; Röther, T.; Paul, W.; Werner, P.; Steinigeweg, S. Environmental impact of the excess electricity conversion into methanol. J. Clean. Prod. 2018, 191, 87–98. [Google Scholar] [CrossRef]

- Deutz, S.; Bongartz, D.; Heuser, B.; Kätelhön, A.; Schulze Langenhorst, L.; Omari, A.; Walters, M.; Klankermayer, J.; Leitner, W.; Mitsos, A.; et al. Cleaner production of cleaner fuels: Wind-to-wheel—environmental assessment of CO2-based oxymethylene ether as a drop-in fuel. Energy Environ. Sci. 2018, 11, 331–343. [Google Scholar] [CrossRef] [Green Version]

- Hoppe, W.; Bringezu, S. Vergleichende Ökobilanz der CO2-basierten und konventionellen Methan- und Methanolproduktion. Uwf Umw. 2016, 24, 43–47. [Google Scholar] [CrossRef]

- Hoppe, W.; Thonemann, N.; Bringezu, S. Life Cycle Assessment of Carbon Dioxide-Based Production of methane and Methanol and Derived Polymers. J. Ind. Ecol. 2017, 22, 327–340. [Google Scholar] [CrossRef]

- Schmidt, P.; Weindorf, W. Power-to-Liquids: Potentials and Perspectives for the Future Supply of Renewable Aviation Fuel; German Environment Agency: Dessau-Roßlau, Germany, 2016.

- Spielmann, M.; Ruiz, S.; Zah, R. Analyse der Umwelt-Hotspots von Strombasierten Treibstoffen; BAFU: Zürich, Switzerlands, 2015; pp. 1–68.

- Sternberg, A.; Bardow, A. Power-to-What?—Environmental assessment of energy storage systems. Energy Environ. Sci. 2015, 8, 389–400. [Google Scholar]

- Sternberg, A.; Teichgräber, H.; Voll, P.; Bardow, A. CO2 vs. Biomass: Identification of Environmentally Beneficial Processes for Platform Chemicals from Renewable Carbon Sources. Comput. Aided Chem. Eng. 2015, 37, 1361–1366. [Google Scholar]

- Fernández-Dacosta, C.; Shen, L.; Schakel, W.; Ramirez, A.; Kramer, G.J. Potential and challenges of low-carbon energy options: Comparative assessment of alternative fuels for the transport sector. Appl. Energy 2019, 236, 590–606. [Google Scholar] [CrossRef]

- Matzen, M.; Demirel, Y. Methanol and dimethyl ether from renewable hydrogen and carbon dioxide: Alternative fuels production and life-cycle assessment. J. Clean. Prod. 2016, 139, 1068–1077. [Google Scholar] [CrossRef] [Green Version]

- Wagner, U.; Eckl, R.; Tzscheutschler, P. Energetic life cycle assessment of fuel cell powertrain systems and alternative fuels in Germany. Energy 2006, 31, 3062–3075. [Google Scholar] [CrossRef]

- Troy, S.; Zapp, P.; Kuckshinrichs, W.; Weiske, S.; Peters, R.; Moser, P.; Stahl, K. Life Cycle Assessment for full chain CCU demonstration in the ALIGN-CCUS project—dimethyl ether and polyoxymethylen dimethyl ethers production from CO2 and its usages in the mobility and electricity sectors. In Proceedings of the 15th International Conference on Greenhouse Gas Control Technologies, GHGT-15, Abu Dhabi, United Arab Emirates, 15–18 March 2021. [Google Scholar]

- Hurtig, O.; Yearwood, J. Deliverable 4.3: Economic and Environmental Impacts of Most Promising CCU Pathways; Trinomics, Dechema: 2018. Available online: http://carbonnext.eu/Deliverables/_/D4.3%20Economic%20and%20environmental%20impacts%20of%20most%20promising%20CCU%20pathways.pdf (accessed on 21 December 2021).

- Hombach, L.E.; Doré, L.; Heidgen, K.; Maas, H.; Wallington, T.J.; Walther, G. Economic and environmental assessment of current (2015) and future (2030) use of E-fuels in light-duty vehicles in Germany. J. Clean. Prod. 2019, 207, 153–162. [Google Scholar] [CrossRef]

- Alhyari, M.M.; Al-Salaymeh, A.; Irshidat, M.; Kaltschmitt, M.; Neuling, U. The Impact of Energy Source on the Life-Cycle Assessment of Power-to-Liquid Fuels. J. Ecol. Eng. 2019, 20, 239–244. [Google Scholar] [CrossRef]

- Volvo. LKW MIT LNG-ANTRIEB. Available online: https://www.volvotrucks.de/de-de/trucks/alternative-antriebe/lng-lkw.html (accessed on 19 December 2020).

- Scania. Praxisinfos zu Gas-Lkw. Available online: https://www.scania.com/de/de/home/products-and-services/articles/vorteile-erdgas-lkw.html (accessed on 19 December 2020).

- Stojcevski, T. METHANOL—As Engine Fuel, Status Stena Germanica and Market Overview. Available online: https://www.zerovisiontool.com/sites/www.zerovisiontool.com/files/attachments/pilo (accessed on 19 August 2019).

- Zhai, K. A Brief Review of China’s Methnaol Vehicle Pilot and Policy; Methanol Institute: Beijing, China, 2019. [Google Scholar]

- AUTO-CHE.COM. Methanol/Diesel Dual Fuel Dump Truck. Available online: http://auto-che.com/t/methanol-diesel-dump-truck.html (accessed on 21 August 2019).

- Wietschel, M.; Gnann, T.; Kühn, A.; Plötz, P.; Moll, C.; Speth, D.; Buch, J.; Boßmann, T.; Stütz, S.; Schellert, M.; et al. Machbarkeitsstudie zur Ermittlung der Potentiale des Hybrid-Oberleitungs-Lkw; Fraunhofer Institut für System und Innovationsforschung (ISI): Karlsruhe, Germany, 2017. [Google Scholar]

- Breuer, J.L.; Samsun, R.C.; Stolten, D.; Peters, R. How to reduce the greenhouse gas emissions and air pollution caused by light and heavy duty vehicles with battery-electric, fuel cell-electric and catenary trucks. Environ. Int. 2021, 152, 106474. [Google Scholar] [CrossRef] [PubMed]

- Peters, R.; Breuer, J.L.; Decker, M.; Grube, T.; Robinius, M.; Samsun, R.C.; Stolten, D. Future Power Train Solutions for Long-Haul Trucks. Sustainability 2021, 13, 2225. [Google Scholar] [CrossRef]

- European Union. Regulation (EU) 2016/1628 of the European Parliament and of the Council of 14 September 2016 on Requirements Relating to Gaseous and Particulate Pollutant Emission Limits and Type-Approval for Internal Combustion Engines for Non-Road Mobile Machinery, Amending Regulations (EU) No 1024/2012 and (EU) No 167/2013, and Amending and Repealing Directive 97/68/EC; European Union: Brussels, Belgium, 2016. [Google Scholar]

- Quispel, M. Reducing Air Pollutant Emissions of Inland Waterway Transport in Europe. Available online: https://www.ccr-zkr.org/files/documents/workshops/wrshp081013/1_MQuispel_en.pdf (accessed on 16 February 2021).

- Dahlke, F. Binnenschifffahrt—Innovative Antriebskonzepte. In Proceedings of the Jahrestagung Mobilität 2019, Düsseldorf, Germany, 27 June 2019. [Google Scholar]

- Zero Emission Services B.V. Schlüsselakteure Entwickeln ein Emissionsloses Antriebssystem für die Binnenschifffahrt. Available online: https://zeroemissionservices.nl/de/schlusselakteure-entwickeln-ein-emissionsloses-antriebssystem-fur-die-binnenschifffahrt/ (accessed on 21 December 2021).

- Kasten, P.; Mottschall, M.; Köppel, W.; Degünther, C.; Schmied, M.; Wüthrich, P. Erarbeitung einer Fachlichen Strategie zur Energieversorgung des Verkehrs bis zum Jahr 2050. TEXTE 2016, 72/2016. Available online: https://www.umweltbundesamt.de/sites/default/files/medien/377/publikationen/2016-11-10_endbericht_energieversorgung_des_verkehrs_2050_final.pdf (accessed on 19 December 2020).

- DNV GL. Highlight Projects in the LNG as Fuel History. Available online: https://brandcentral.dnvgl.com/download/DownloadGateway.dll?h=BE1B38BB718539CC0AB58A5FF2EA7A8335EF9A5BC87A42E8FE938B52042522100D70F7679F884F56637AC7C6F561AD0F (accessed on 7 April 2021).

- Rolls-Royce. Rolls-Royce and Robert Allan Present the World’s First LNG-Powered Shallow-Water Push Boat. Available online: https://www.rolls-royce.com/media/press-releases/2019/06-12-2019-rr (accessed on 21 December 2021).

- Bundesministerium für Verkehr, Bau und Stadtentwicklung. Die Mobilitäts-und Kraftstoffstrategie der Bundesregierung (MKS); Bundesministerium für Verkehr, Bau und Stadtentwicklung: Berlin, Germany, 2013.

- Kopyscinski, J.; Schildhauer, T.; Biollaz, S. Production of synthetic natural gas (SNG) from coal and dry biomass–A technology review from 1950 to 2009. Fuel 2010, 89, 1763–1783. [Google Scholar] [CrossRef]

- Generaldirektion Wasserstraßen und Schifffahrt. Veränderungen des Schiffsbestandes der Deutschen Binnenflotte im Jahr 2017—Zentrale Binnenschiffsbestandsdatei. Available online: https://www.gdws.wsv.bund.de/SharedDocs/Downloads/DE/Binnenschiffsbestandsdatei/2017.pdf?__blob=publicationFile&v=3 (accessed on 20 February 2021).

- MariGreen project. Perspectives for the Use of Hydrogen as Fuelin Inland Shipping; Institute for Combustion Engines VKA: Leer, Germany; Mariko GmbH: Aachen, Germany; FME: Groningen, The Netherlands, 2018. [Google Scholar]

- RH2INE Awarded Co-Funding of the EU Connecting Europe Facility! Available online: https://www.rh2ine.eu/latest-news/253/ (accessed on 12 December 2020).

- Thomson, R. Hydrogen Has Emerged as a Key Contender in the Battle to Secure a Sustainable Future for Aviation. Available online: https://www.rolandberger.com/en/Publications/Hydrogen-A-future-fuel-of-aviation.html (accessed on 20 August 2020).

- Schmied, M.; Wüthrich, P.; Zah, R.; Friedl, C. Postfossile Energieversorgungsoptionen für einen Treibhausgasneutralen Verkehr im Jahr 2050: Eine Verkehrsträgerübergreifende Bewertung. TEXTE 2015, 30/2015. Available online: https://www.umweltbundesamt.de/publikationen/postfossile-energieversorgungsoptionen-fuer-einen (accessed on 6 July 2020).

- International Civil Aviation Organization. Electric and Hybrid Aircraft Platform for Innovation (E-HAPI). Available online: https://www.icao.int/environmental-protection/Pages/electric-aircraft.aspx (accessed on 6 July 2020).

- Roland Berger. Aircraft Electrical Propulsion—The Next Chapter of Aviation? 2017. Available online: http://docplayer.net/59715725-Aircraft-electrical-propulsion-the-next-chapter-of-aviation.html (accessed on 6 July 2020).

- Eviation Aircraft. ALICE Specification. Available online: https://www.eviation.co/aircraft/#4 (accessed on 22 September 2020).

- ICAO Secretariat. Electric, Hybrid, and Hydrogen Aircraft—State of Play. In ICAO Environmental Report 2019; ICAO: Montreal, QC, Canada, 2019; pp. 124–130. [Google Scholar]

- Deutsches Zentrum für Luft-und Raumfahrt. HY4 Emissionsfreie Passagierflugzeuge. Available online: https://www.dlr.de/content/de/downloads/2015/dlr-flyer-hy4_1892.pdf?__blob=publicationFile&v=16 (accessed on 18 February 2021).

- AIRBUS. This Chase Aircraft Is Tracking 100% SAF’s Emissions Performance. Available online: https://www.airbus.com/en/newsroom/stories/2021-11-this-chase-aircraft-is-tracking-100-safs-emissions-performance (accessed on 21 December 2021).

- Naumann, K.; Müller-Langer, F.; Meisel, K.; Majer, S.; Schröder, J.; Schmieder, U. Further Development of the German Greenhouse Gas Reduction Quota, Background Paper; Deutsches Biomasseforschungszentrum gemeinnützige GmbH: Leipzig, Germany, 2021. [Google Scholar]

- Heidt, C.; Lambrecht, U.; Hardinghaus, M.; Knitschky, G.; Schmidt, P.; Weindorf, W.; Naumann, K.; Majer, S.; Müller-Langer, F.; Seiffert, M. CNG und LPG—Potenziale dieser Energieträger auf dem Weg zu einer Nachhaltigeren Energiever-Sorgung des Straßenverkehrs; DLR: Ottobrunn, Germany; Leipzig, Germany; Berlin/Heidelberg, Germany, 2013. [Google Scholar]

- Wachsmuth, J.; Oberle, S.; Zubair, A.; Köppel, W. Wie klimafreundlich ist LNG?—Kurzstudie zur Bewertung der Vorkettenemissionen bei Nutzung von Verflüssigtem Erdgas (LNG); CLIMATE CHANGE 21/2019; Umweltbundesamt: Dessau-Roßlau, Germany, 2019.

| TRL | Definition |

|---|---|

| 1 | Identification of new concept, applications, and barriers |

| 2 | Definition of application, consideration of interfaces, and commercial offer |

| 3 | Proof of concept prototype ready: concept is laboratory tested |

| 4 | Integrated small-scale prototype with auxiliary systems laboratory validated |

| 5 | Large-scale prototype completed with auxiliaries, refined commercial assessment |

| 6 | Technology pilot demonstrated in relevant environment, manufacturing strategy defined |

| 7 | Pilot demonstrated in operational environment, manufacturing approach demonstrated |

| 8 | Technology in its final form, low-rate production |

| 9 | System fully operational and ready for commercialization |

| Source | Fuel | Cost in EUR/LDE | Cost in EURct/kWh | Reference |

|---|---|---|---|---|

| Renewable electricity | Hydrogen | 1.38 | 13.85 | [98] |

| Methanol | 1.89 a | 18.97 a | [4] | |

| Ethanol | 2.22 a | 22.29 a | [4] | |

| Butanol | 2.53–2.60 a | 25.40–26.10 a | [4] | |

| Octanol | 2.85 a | 28.61 a | [4] | |

| Dimethyl ether | 1.85 a | 18.57 a | [4] | |

| Oxymethylene ether1 | 2.64 a | 26.40 a | [4] | |

| Oxymethylene ether3–5 | 3.46–3.96 a | 34.74–39.76 a | [4] | |

| Methanol-to-Gasoline | 1.88 a | 18.87 a | [4] | |

| Fischer–Tropsch-Diesel/Gasolines/Kerosene | 2.30 a | 23.09 a | [4] | |

| SNG | 2.25 b | 22.59 b | [13] | |

| Biomass | FAME | 0.88 | 8.85 | [99] |

| HVO | 0.73 | 7.34 | [99] | |

| Bioethanol | 1.12 | 11.28 | [99] | |

| Biomethane | 0.69–0.72 | 6.90–7.20 | [100] | |

| Electricity | 0.60 c–3.01 d | 60 c–30.19 d | [98,101] |

| Abbreviation | Sustainable Aviation Fuel |

|---|---|

| FT-SPK | Fischer–Tropsch hydroprocessed synthesized paraffinic kerosene |

| HEFA-SPK | Synthesized paraffinic kerosene from hydroprocessed esters and fatty acids |

| HFS-SIP | Synthesized iso-paraffins from hydroprocessed fermented sugars |

| FT-SPKA/A | Synthesized kerosene with aromatics derived by the alkylation of light aromatics from non-petroleum sources |

| ATJ-SPK | Alcohol-to-Jet synthetic paraffinic kerosene |

| CH-SK, or CHJ | Catalytic hydrothermolysis synthesized kerosene |

| HHC-SPK or HC-HEFA-SPK | Hydroprocessed hydrocarbons, esters, and fatty acid synthetic paraffinic kerosene |

| Drivetrain | Fuel | Field of Application | Max. Efficiency |

|---|---|---|---|

| Otto engine | Gasoline | Motorcycle | 31% [153] |

| Passenger cars, commercial vehicles | 36% [109,153] | ||

| Gasoline 2 stroke | Small engines | 24% [153] | |

| LPG | Commercial vehicles | 36.5% [109] | |

| CNG | Commercial vehicles | 37% [109] | |

| Diesel engine | Diesel | Passenger cars | 43% [153] |

| Diesel | Commercial vehicles, trucks | 42–45% [109,153] | |

| LNG | Commercial vehicles | 42% [109] | |

| FT diesel, HVO, OME3–5, DME | Commercial vehicles | 42% [109] | |

| Large diesel engine with high RPM | Diesel | Shipping | 44% [153] |

| Diesel engines with medium RPM | Diesel | Shipping | 45% [153] |

| Cross-head engines | HFO 2 stroke | Shipping | 54% [153] |

| Turbines | Jet fuel | Air transport | 50% [152] |

| Battery–electric | Electric energy | - | 81–95% [109,151] |

| Fuel cell–electric | H2 | - | 49–62% a |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Breuer, J.L.; Scholten, J.; Koj, J.C.; Schorn, F.; Fiebrandt, M.; Samsun, R.C.; Albus, R.; Görner, K.; Stolten, D.; Peters, R. An Overview of Promising Alternative Fuels for Road, Rail, Air, and Inland Waterway Transport in Germany. Energies 2022, 15, 1443. https://0-doi-org.brum.beds.ac.uk/10.3390/en15041443

Breuer JL, Scholten J, Koj JC, Schorn F, Fiebrandt M, Samsun RC, Albus R, Görner K, Stolten D, Peters R. An Overview of Promising Alternative Fuels for Road, Rail, Air, and Inland Waterway Transport in Germany. Energies. 2022; 15(4):1443. https://0-doi-org.brum.beds.ac.uk/10.3390/en15041443

Chicago/Turabian StyleBreuer, Janos Lucian, Juri Scholten, Jan Christian Koj, Felix Schorn, Marc Fiebrandt, Remzi Can Samsun, Rolf Albus, Klaus Görner, Detlef Stolten, and Ralf Peters. 2022. "An Overview of Promising Alternative Fuels for Road, Rail, Air, and Inland Waterway Transport in Germany" Energies 15, no. 4: 1443. https://0-doi-org.brum.beds.ac.uk/10.3390/en15041443