Roadmap to Neutrality—What Foundational Questions Need Answering to Determine One’s Ideal Decarbonisation Strategy

EEP—Institute for Energy Efficiency in Production, University of Stuttgart, 70569 Stuttgart, Germany

Energies 2022, 15(9), 3126; https://0-doi-org.brum.beds.ac.uk/10.3390/en15093126

Submission received: 8 February 2022

/

Revised: 19 April 2022

/

Accepted: 22 April 2022

/

Published: 25 April 2022

(This article belongs to the Special Issue BIWAES 2021—Biennial International Workshop Advances in Energy Studies "Empowering Communities, Beyond Energy Scarcity")

Abstract

:Considering increasingly ambitious pledges by countries and various forms of pressure from current international constellations, society, investors, and clients further up the supply chain, the question for companies is not so much whether to take decarbonisation action, but what action and by when. However, determining an ideal mix of measures to apply ‘decarbonisation efficiency’ requires more than knowledge of technically feasible measures and how to combine them to achieve the most economic outcome: In this paper, working in a ‘backcasting’ manner, the author describes seven aspects which heavily influence the composition of an ‘ideal mix’ that executive leadership needs to take a (strategic) position on. Contrary to previous studies, these aspects consider underlying motivations and span across (socio-)economic, technical, regulatory, strategic, corporate culture, and environmental factors and further underline the necessity of clarity of definitions. How these decisions influence the determination of the decarbonisation-efficient ideal mix of measures is further explored by providing concrete examples. Insights into the choices taken by German manufacturers regarding several of these aspects stem from about 850 responses to the ‘Energy Efficiency Index of German Industry’. Knowledge of the status quo, and clarity in definitions, objectives, time frames, and scope are key.

1. Introduction

1.1. Background

Ahead of the United Nations’ Climate Conference COP26 in Glasgow, a vast array of severe weather incidences across the globe—floods, storms, droughts, increase in temperature, melting ice shelves, etc. [1], underlined the warnings presented by various bodies [2,3,4,5]. The latter stress that significant action is required by policymakers to still be able to limit global warming to less than 2 °C, ideally 1.5 °C, above pre-industrial levels, as agreed in the Paris Climate Agreement [6].

The Intergovernmental Panel on Climate Change (IPCC), the International Energy Agency (IEA), the German Energy Agency, and many other bodies have published reports, roadmaps, and scenarios [4,7,8] on actions necessary to meet the set target. The pace of environmental change suggests that actions should be taken sooner rather than later to keep the required action trajectory manageable and maintain the ability to meet the target. Nonetheless, unforeseen situations, such as the conflict between Russia and the Ukraine and the linkages to energy-dependency, can further increase the urgency of decarbonisation and switching to renewables [9]. In fact, events of an imminent magnitude can trigger stakeholders to societally endorsed changes of policy and concerted action in a time of crisis. For example, this was the case with the COVID-19 pandemic and also with the nuclear reactor catastrophe in Fukushima, which led Germany to move away from nuclear energy and announce the Energiewende [10].

Ahead of COP26, an increasing number of countries have reacted by declaring their ambitions for net-zero emissions in line with the requirement to submit updated intended nationally determined contributions (INDCs) to the United Nations Framework Convention on Climate Change. According to the Climate Action Tracker [11], “over 140 countries had announced or are considering net-zero targets, covering 90% of global emissions”. Net-zero means that emissions remaining after reduction efforts are balanced out through offsetting (i.e., via carbon sinks or compensatory projects) [12]. While many countries pledge to reach net-zero emissions by 2050, some aim at reaching this goal earlier (e.g., Germany 2045), some later (e.g., China 2060). Moreover, whereas some countries target carbon neutrality, others target climate neutrality (e.g., European Union 2050) [13]. Carbon neutral only refers to carbon-dioxide emissions (CO2), whilst climate neutral includes other emissions such as methane, etc. How countries aim to achieve these goals, however, remains vastly vague.

As setting a target never automatically leads to its achievement or even further actions, it is crucial to equip policymakers with the insights needed (on how) to achieve net-zero in actuality and effectively. Looking at the demands faced by governments to fight and prioritize climate change, it may seem like it is up to the governments alone to mitigate climate change. However, by direct action, governments only account for the emissions of their immediate actions and on their premises. Conversely, they have indirect influence on the emissions of their entire economy through regulatory measures and policies. These may include bans, minimum requirements, mandatory actions, the provision of infrastructure, incentives, and subsidies.

Typically, most emissions are caused by energy generation and key economic sectors, such as transport, industry, housing, and agriculture [14,15]. Therefore, achieving climate change targets essentially comes down to getting these sectors to reduce their emissions, usually with the aforementioned set of policy measures.

Specifically, the challenge is to identify which set of measures is effective and economic to decarbonise which part of the economy. Instructive measures have proven impactful in the past (i.e., minimum standards, phasing-out of incandescent light bulbs, etc.) [16,17]. Nonetheless, given that achieving net-zero requires emissions to be cut or removed across the board, it is necessary that individual and intrinsic actions are as broad as possible. Hence, it is essential to find effective means to trigger such intrinsic wish in stakeholders to reduce emissions, in other words, convincing them to ‘buy-in’. This way, rather than avoiding regulations and trying to find loopholes, stakeholders proactively look for means with which they can succeed in meeting their self-set targets.

Two key challenges arise: Firstly, one has to identify means that successfully trigger the (intrinsic) decision to decarbonise and, secondly, to provide those who have taken this decision (or are at least contemplating to) with the means to decarbonise effectively.

As stakeholders are principally aware of their own operations, they have a good chance finding ways to reduce their emission footprint. The cumulative proactive efforts of stakeholders then allow governments to shift attention from the spot-policing of compliance (with instructed policies) to ensuring a suitable environment for stakeholders to be able to decarbonise (i.e., planning capacities, generation and transmission infrastructure, support mechanisms). Furthermore, potential gaps in stakeholder ambitions to meet the countries’ goals can then be addressed.

1.2. Industrial Sector of High Relevance for Achieving Net-Zero—But How to Get Started?

One of the most relevant groups in the energy transition is the industrial sector. Not only does it account for a large proportion of most countries’ energy consumption, but also for associated energy- and process-related emissions [18,19,20,21,22]. Furthermore, this sector determines the shape, performance, and durability, as well as the energy and resource consumption of goods during production and service life, but also their repairability, recyclability, and how and where the required raw materials are sourced. Hence, the industrial sector influences all other sectors by controlling product and machinery characteristics as well as their modes of operation (e.g., power stations, turbines, transmission infrastructure equipment, vehicles, materials for new buildings and retrofits, machinery, electronics, clothing, or furniture). These decisions largely determine the embedded emissions of all produce, a factor which is rapidly gaining in importance. This is further underlined by both the ‘Sustainable Product Initiative’, which is developed by the European Commission at present, including “requirements on mandatory sustainability labelling and disclosure of information to consumers on products along value chains” [23], and a ‘Resource Passport’ for buildings that the German government plans to introduce, along with reshaping its support programmes from purely considering energy-related characteristics to the whole lifecycle footprint [24].

Therefore, decarbonisation in manufacturing can be considered a critical enabler to the question of how to achieve carbon or climate neutrality on a country-wide level and beyond. A growing number of studies thus explore pathways for deep decarbonisation, particularly of energy-intensive industries. According to Nurdiawati et al. [25] (p. 2), many of these studies “focused much on the technological pathways and less on the supportive enabling reforms that would facilitate their uptake”. Bauer et al. [26] explore pathways for decarbonising four emission-intensive sectors, even moving beyond direct emissions to also considering value-chain and end-consumers emissions. Bataille et al. [27] (p. 1) present an “integrated [policy] strategy for a managed transition” in energy intensive industries, also including technology options, and Rissman et al. [28] review policy options, sociological, technological, and practical solutions in detail.

These studies address decarbonisation of industry from either a policy, a supply-side, or technology perspective—often with a focus on energy intensive industries—but are short of giving corporate stakeholders (irrespective of their company’s energy intensity) concrete advice on how to get started from an individual company’s perspective. Similarly, studies such as the one by Johnson et al. [29] analyse and compare national roadmaps for decarbonising the heavy industry on a global scale, alongside factors such as ambition, financial effort, and mitigation measures. Nevertheless, this approach again leaves a gap when it comes to company-tailored advice.

Consultancies and advisories fill this gap insufficiently. While they generally indicate which steps have to be taken by a stakeholder to shape a decarbonisation roadmap from a company perspective [30,31,32], they either do not go into sufficient detail, or do not address the prerequisite, qualifying steps, notably those of strategic decision making. These, such as the motivation leading to the decision to decarbonise, however, often have serious implications on the shape of an ‘ideal’ decarbonisation strategy and how it can be implemented effectively.

An effective way to develop decarbonisation roadmaps could involve applying approaches from the backcasting framework literature. This concept, established by Robinson [33], refers to a strategy where stakeholders/policymakers set up a target (energy consumption/emissions) and work backwards from this target to reach it in the future. This framework is widely applied in designing emission-reduction pathways. In this context, a new strand of the scenario literature includes a focus on low-carbon scenario road mapping. As part of this new literature, Hughes and Strachan find “that low carbon scenarios tend to focus either on qualitative, social trend-based approaches to developing futures, or on purely technological, engineering-based views of an energy system” [34] (p. 46). In particular, technologically focused studies, such as Bataille et al. [35] and Manders et al. [36], often operate within a ‘backcasting’ framework explained by Holmberg and Robèrt [37]. However, they argue that road mapping the future is always, to some extent, hampered by uncertainty and that therefore the system level, as well as the actor and the technology level, must be considered. Thus, one may argue, that due to the uncertainty and inaccuracy of existing studies and roadmaps, they remain low in their ability to give concrete advice.

Having said that, studies that not only focus on either technology, individual, social, or system level are still rare. Similarly, there is a lack of studies that take into account the whole industrial/manufacturing sector instead of only focusing on its energy-intensive parts. Closing this gap, and thus contributing to effective decarbonisation roadmaps, is the aim of this article.

1.3. The Issue: Enabling Corporate Stakeholders to Decarbonise Effectively

The present article addresses this gap by answering the following research question: What foundational questions matter and need answering to provide practical guidance to corporate stakeholders on how to shape an effective and tailored decarbonisation strategy?

Derived from professional practice and applying a mix-methods approach based on data gathered via the Energy Efficiency Index of German Industry (EEI) [38], this work addresses underlying motivations and spans across (socio-)economic, technical, regulatory, strategic, corporate culture, and environmental factors. It further underlines the necessity of a mutual understanding, clarity, and communication of definitions and targets.

Plenty of companies have already made pledges related to emission reductions. However, these companies constitute only a small proportion of the global manufacturing industry, even though they might be big in size individually. Nonetheless, to achieve net-zero on a societal level, it is not sufficient to address the largest emitters only, but to find ways to reach at best all emitters. Specifically, it is crucial to get their ‘buy-in’, irrespective of their emission intensity or size, and empower them (and the communities they are embedded in) to take action.

Tackling these challenges, this work aims at aiding executive leadership, as well as other company functions relevant to the transition, in shaping their pathway to net-zero effectively. It further provides insights to policy makers, service providers, financiers, and the general public on (often not obvious) obstacles, needs for support, and infrastructure, as well as interdependencies along the process. Several of the general principles may also apply and, therefore, prove to be helpful to other sectors, state actors, communities, or individuals.

The motivation for this article partly arose out of a meeting with a company invested in advancing energy efficiency, but which had not yet seen the point in decarbonisation. Following an explanation of why it is in their best interest to take decarbonisation seriously (by highlighting a series of external pressure points), the manager expressed the belief that immediate action was necessary. To brief the company’s CEO, the manager then enquired what aspects the executive leadership of a manufacturing company needs to consider to shape an effective and economic strategy. Although the analysis may generally be broadly applicable to many stakeholder-types, the author focuses on (predominantly manufacturing) companies that have taken the decision to decarbonise or contemplate whether to do so.

Following a backcasting approach, this article provides an overview of seven foundational questions that need answering to enable a general understanding, as well as to provide practical guidance on how to shape an effective and tailored decarbonisation strategy. The results demonstrate that clarity in definitions, objectives, timeframes, and scope, as well as a thorough understanding of the status quo and the technically feasible options, are key. In light of changing emission and energy prices, as well as the goal of ensuring resilience against external shocks, digital solutions, and an adjusted approach to economic viability calculations are needed to help with keeping such a strategy ideal.

2. Methods and Materials

As discussed earlier, previous studies about decarbonisation road mapping tend to focus either on the system (national roadmaps) or on the individual level (specific sectors). Furthermore, they tend to concentrate either on policy or technological factors. This article digs a bit deeper by taking most of these factors into consideration and combining them, thus eventually requiring a combination of qualitative and quantitative elements.

The associated methodology applied by the author is a backcasting method, as described by Robinson [33] (p. 339), that is adjusted for the context of company decision-makers and the goal of decarbonisation. The resulting seven individual steps take inspiration from the six steps originally proposed by Robinson but differ in their shape and nature. ‘Backcasting’ in this context means working backwards from the desired outcome to the ingredients that need to be obtained or taken into account to reach that future. It is thus an explicitly normative approach [33] (p. 337).

In an iterative process, starting in May 2019, the author analysed manufacturing companies’ stand towards decarbonisation with a particular focus on local decarbonisation efforts, notably around energy efficiency.

The qualitative element of the analysis of companies’ actions, ambitions, and intentions is based on primary sources. Direct conversations with companies allow for a first-hand understanding of their viewpoints and needs. The businesses consulted were manufacturing companies that are either clients in energy efficiency or decarbonisation projects, participate in the Energy Efficiency Index of German Industry (EEI), seek guidance on the topic or partook in events concerning industrial decarbonisation. In addition, business press, newspaper articles, press releases, and pledges from companies, as well as feedback received in context of public speeches and outcomes from expert discussions have been taken into account. These kinds of observations promise to shed light on aspects concerning willingness and efforts to decarbonise.

Afterwards, these observations were tested quantitatively within the framework of the Energy Efficiency Index of German Industry (EEI) to confirm the anecdotal evidence and assess the actual progress of decarbonisation. Introduced in 2013, EEI surveys German manufacturing companies of all sizes, energy intensities, and across 27 sub-sectors twice a year. It aims at gaining an understanding of companies’ stands, expectations, plans, opinions, experiences towards energy efficiency, and increasingly also decarbonisation. EEI data is gathered applying a mixed-methods approach combining online (ca. 10%) and telephone surveys (ca. 90%) [38].

An iterative process was applied to deepen the understanding of interdependencies and elements that are the foundational ingredients that enable—or hold back—decarbonisation. Whenever the EEI uncovered a relevant finding, the next data collection, after pre-testing, was utilised to drill deeper. In total, evidence from five data collections is considered in the context of this article (cf. Table 1).

To provide a general overview, a series of EEI questions of the past five data collections were identified to illustrate selected aspects: (a) whether companies plan to decarbonise, and (b) if so, by when. What level of ambition they have for (c) 2025 and (d) for 2030 and (e) optimising for which dimension(s). Based on (f), what motivation they do so, and (g) what weight different determinants have in deciding for decarbonisation measures. Beside the area of observation (h), EEI explores the increasing relevance of product carbon footprints (i). The awareness of companies’ emission footprint (j), along with knowledge about energy consumption and type (k, l) and energy saving potentials (m), are explored to assess companies’ knowledge of their status quo [39,40,41,42,43].

3. Results

Before making a decision, one often considers the implications and repercussions of that decision. Nevertheless, even after a thorough consideration it is not unlikely that an aspect that significantly impacts the overall ambition is overlooked—unless one has succeeded in a very similar or identical undertaking before. Decarbonising one’s business is to some extent like building a house for the first time. After completion, one has learnt much about what to do better or differently the next time. Nonetheless, in many instances one only builds one house (if any). Roughly the same applies in the case of decarbonisation: once it is achieved—however (in-)efficiently—there is rarely a situation where one does it again from scratch (unless a company has multiple sites and started with a pilot one or offers the experience as a service to others). Again, similar to one’s house, there remains the prospect of continuous optimisation. While some improvements might be incremental, other interventions would require significant interference if at all possible (for example switching from a radiator-based heating system to underfloor heating to allow the installed heat pump to serve the home with heat more efficiently [44]). Setting a clear target to be reached in the future and being aware of multidimensional factors, which might influence how it is reached, is the ultimate goal for a successful decarbonisation strategy.

Therefore, it is of high relevance—to stakeholders of any sector—to find answers to seven foundational questions, ideally before, but at least simultaneously to taking action. Only the response to these questions allows one to determine one’s ideal decarbonisation strategy, or to make an informed decision whether to go ahead and act, or even to openly pledge to take action.

- (1)

- Terminology;

- (2)

- Optimisation variable;

- (3)

- Level of ambition;

- (4)

- Area of observation;

- (5)

- Motivation and needs;

- (6)

- Priorities;

- (7)

- Status quo.

Based on the responses to these, it is then possible to derive (a) general, and (b) specific routes of action to determine a decarbonisation strategy suiting one’s situation, goals, and opportunities. Making use of (c) digitalisation and (d) a modified form of economic viability calculations allows one to find one’s ideal roadmap to neutrality and to adjust it dynamically to changing environments.

Why these seven, one could argue. Essentially, every one of them is guided by the notion of what could go wrong (or has gone wrong elsewhere), what could reduce the efficiency and/or effectiveness of a decarbonisation strategy, and how this can be avoided.

As mentioned when discussing the backcasting framework and also as explained by Rissmann et al., “the best practice in designing efficient industrial operations is to analyse the entire process by working “backwards” from the desired application to the energy consuming-equipment” [28] (p. 16). Transposed to the context of this article, the “desired application” reflects the desired outcome.

In this context, however, the outcome needs to be further specified as decarbonisation can be understood differently, achieved differently, and should be pursued differently, if it is to address different motivations or to consider different priorities. Therefore, as Rissman et al. stated referring to increasing efficiency of industrial systems and processes, “design should be an integrative process that accounts for how each part of the system affects other parts.” [28] (p. 16).

In this article, “design” refers to the preliminary steps (i.e., strategic considerations) that need to be taken, typically by executive leadership, to allow them, and subsequently their company to shape and pursue an effective and efficient roadmap to neutrality.

Other than the practical “design layers” that describe step by step the “how” of increasing efficiency [28] (p. 16) [45], the seven foundational questions address the “what”, “where”, “by when”, and “why”, as well as the “how”. Nevertheless, they apply on a more strategic than a specifically practical level.

The following sections will provide a more detailed explanation of the seven dimensions (Section 3.1, Section 3.2, Section 3.3, Section 3.4, Section 3.5, Section 3.6 and Section 3.7), followed by an overview of how they guide implementation in general and more individually (Section 3.8 and Section 3.9), as well as steps to make and keep a strategy ideal (Section 3.10 and Section 3.11).

3.1. Terminology

The foundation of an effective decarbonisation strategy, as of any other work in any other area, is to establish mutual understanding and clarity across all stakeholders involved regarding the terms used and how they are understood. Otherwise, misunderstandings or misperceptions will lead to either unnecessary action being taken or, worse, essential actions being overlooked.

Buettner [46] points out that a key reason for the frequent mixed-up between carbon- and climate neutrality is that, while CO2-equivalents (CO2-eq.) are the ‘currency’ to measure greenhouse gas (GHG) emissions adversely affecting our climate, the suffix “-eq” (standing for equivalents) gets easily lost on the way. This is particularly the case in oral or simplified conversation and correspondence.

Apart from this, it is further possible that the difference between carbon neutrality, climate neutrality, and environmental neutrality itself is not clear. However, this unclarity has fortunately been decreasing over the past three years. In short, climate neutrality exceeds the ambition of carbon neutrality by also addressing methane and all other gases that have a warming potential for the atmosphere (GHGs), such as nitrous oxide and hydrofluorocarbons. Environmental neutrality reaches even further and addresses all other gases and substances that have a negative impact on the environment (such as particulate matter and sulphur dioxide, cf. Figure 1) [46].

This frequent lack in clarity regarding definitions can also be observed beyond private sector stakeholders, in the public sector, in politics, public discussion and in media, for instance when reporting on targets: The German business paper Handelsblatt and the New York times diverge over the target set by Japan in late 2020. According to Handelsblatt [48], Japan is aiming for climate neutrality, while the New York Times [49] reports carbon neutrality to be the target. Without the means to retrieve the information from the original source in the language of origin, one will not know which neutrality is being targeted by Japan.

Therefore, establishing clarity of the target dimension and how it is being defined is crucial [46] for all stakeholders involved in the process (i.e., within a company), thus making it the first success criterion to any kind of net-zero pledge.

3.2. Optimisation Variable

Even if the terminology is commonly understood, a strategy can only be effective if it serves achieving a clearly defined objective, in this instance one or multiple target dimensions that serve as variable(s) that are optimised for [50]. In context of emission reduction optimisation, common variables are (not exhaustive):

- (a)

- Reduction of energy consumption (reduces emissions);

- (b)

- CO2-neutrality (usually includes reduction of a);

- (c)

- Climate neutrality (includes a and b and is policy goal of, e.g., EU and Germany);

- (d)

- Environmental neutrality (includes a, b and c).

For stakeholders in general, but also for a company in particular, it makes sense to pursue pragmatic pathways to effectively achieve what is needed. However, it is also relevant to observe the legislator’s target setting, notably its target dimension. If climate neutrality is the country’s target, policies are very likely tailored to serve this goal and companies are well-advised to take this into consideration rather than looking only at a subset of this dimension (e.g., carbon neutrality).

Even though the optimisation variables a–d are not mutually exclusive, the Energy Efficiency Index of German Industry (EEI) observed in its second data collection 2020 [41] that the 834 participating manufacturers on average optimise their companies towards two target dimensions. This suggests that within a further reaching optimisation variable, they also aim at optimising for (at least) one of its components in particular:

Most companies (58%) optimise towards a reduction of energy demand, second most (53%) for the reduction of CO2-emissions. The fact that just over a third of companies indicate they want to optimise for GHG reductions (36%) or overall environmental impacts (36%) leads to the surmise that GHG reductions or, in other words, the means to reach climate neutrality remain abstract in the industrial context. This stands in opposition to the fact that climate neutrality has been the known target of both Germany and the European Union (EU) at the time of the data collection (cf. Figure 2) [41].

Addressing the potential issue of climate neutrality being rather complex due to some of its hard to identify and quantify sub-components (e.g., nitrous oxide and hydrofluorocarbon.), the United Nations Economic Commission for Europe’s Task Force on Carbon Neutrality is pursuing an in-between target dimension: Carbon neutrality plus methane reduction (and hydrogen) in its carbon neutrality project [51] (para 17) [52]. An agreement to reduce global methane emissions in context of COP26, counting more than 100 countries to date [53], indicates the notion of ‘carbon neutrality +’ to be tangible for those that find it difficult to commit to the further reaching climate neutrality goal.

After awareness of terminologies, determining the optimisation variable(s) as target dimensions and overarching goals that stakeholders are aiming to work and orient their forthcoming actions towards is thus the second success criterion on the path to net-zero.

3.3. Level of Ambition

The choice of target dimension (e.g., carbon or climate neutrality) only provides a limited indication of the level of ambition, as it remains unclear by when it is to be achieved. Very timely target years usually suggest a high level of ambition, whereas far into the future targets indicate either a very cautious regime, limited means to reach the goal earlier or simply lacking ambition. The German energy provider RWE plans to become climate neutral two years after the scheduled German coal phase-out—in 2040 [54]. Very timely target years, however, often significantly depend upon compensatory measures rather than actual emission reductions [55].

Clarity on the level of ambition is only achieved when it is also determined (a) by when the goal should be achieved and (b) what percentage reduction of the target dimension this is set to be. The latter is of high relevance, as there are scenarios in which a 100% reduction either cannot be achieved or simply is not the goal. This is the case if the target dimension is energy consumption, or if proportions of the energy- or process-related emissions cannot be avoided through reduction, substitution, or other alike means. In such cases, it could be attempted to balance remaining emissions through offsets (e.g., compensation) to manage a ‘net-zero’ instead of the ‘actual zero’ state in respect to their target dimension. Nevertheless, several stakeholders the author works with object to compensatory projects by principle and exclude these from their feasible set of decarbonisation measures, thus excluding themselves from the option of reaching ‘net’-zero.

Beyond defining an ambition in terms of the finish line, it makes sense to also consider interim milestones to ensure the target can be met and potentially unpopular interventions are not being postponed to the future. Moreover, interim milestones ensure that the trajectory required to achieve the target is the same as the actual trajectory and adjustments are made if necessary. While there is no requirement to determine interim goals for companies, it is logical to do so in terms of year and level of achievement by then.

Many countries have set milestones for (at least) 2030 [56] (p. 41). As thorough assessments by these countries into the state of play are to be expected, it makes sense for stakeholders operating in these countries to define a milestone that ideally is already following the country’s target for the respective year(s), too. The cases of Germany and the Netherlands being successfully sued at their constitutional courts over insufficient short- to medium-term action towards their 2030 targets underlines that additional interim milestones and, if necessary additional actions could be of relevance [57,58]. This is also why the outcome of the Glasgow Climate Conference COP26 encourages revisiting the current level of action, status, and subsequent tightening of pledges in shorter cycles than originally agreed upon in the Paris Climate Agreement (Art. 4 (9)) [6,59]. The current crisis, which has led to a desire in many European countries to quickly reduce dependence on fossil fuel imports, adds an additional and concrete urgency [9].

Nonetheless, countries can only succeed in meeting their (climate) goals, if they get the individual emitters, notably across building, transport, and industrial sectors, to reduce their (energy- and process-related) emissions.

Looking at the ambitions of German manufacturing, 59% of the 852 companies participating in the EEI in autumn 2019, ahead of the COVID-19 pandemic, indicated they plan to achieve net-zero. Of these 488, two thirds aim to have met this goal already before or by 2025 (cf. Figure 3). Peaking numbers in 2025, 2030, 2035, 2040, and 2045 (highlighted in yellow) suggest that semi-decades are chosen by many companies as their target years or at least milestones. The data further suggests that a vast majority of companies participating in the EEI prefer taking substantial immediate or at least short-term action [39].

Taking the likely impact of the COVID-19 pandemic into consideration and addressing the apparently important milestone year 2025, the first iteration of EEI in 2020 found that the 611 participating companies on average, and based on 2019 figures, aim (on average) at reducing their GHG emissions by 22.1% by then [40]. Asking for their 2030 ambitions at the time when the enhanced target of the European Commission for 2030 was being discussed (autumn 2020), 415 companies participating in the second data collection of EEI in 2020 expressed to aim (on average) for a 26.4% GHG reduction (based on 2019) [41]. This data confirms that (at least participating) companies consider substantial short-term action, accounting for more than 80% of what is planned for the whole decade, to happen within its first half. The arising curve of ambition appears to follow a path similar to limited growth functions, whereas policy action is often perceived to follow the opposite path of an exponential growth curve slowly growing towards 2030 and then taking up pace. The action gap arising from this/from what stakeholders need to enable them to meet their goals, and the current impact of policy, is explored further by Buettner et al. [60].

The level of ambition—the combination of target dimension, percentage-goal, and due date—can either be ‘simply’ determined by stakeholders, or be set once ‘all cards are on deck’, meaning all relevant (limiting) factors and potentials, feasible measures, as well as their costs are known. Irrespective of when exactly this decision is taken, setting and announcing a level of ambition is the third success criterion on the path to net-zero.

3.4. Area of Observation

In the context of target setting, the area of observation, or the ‘system barrier’ is not always clear and obvious. Like the necessity to establish clarity of definitions, it is necessary to define to what the set target dimension and level of ambition refer.

This leads to three questions that need to be considered by stakeholders.

(1) Does the target apply to one site, multiple sites, or all sites of the stakeholder, or only to those in countries where some form of CO2-levy is operational or considered. Does it only apply to sites in selected countries, e.g., Germany? Intuitively, it would be understandable if stakeholders prioritise those sites where there is an elevated levy-induced ‘incentive’ to take action, respectively those where the enabling environment makes it easier to succeed when taking action. From the author’s practical experience, companies often initially focus on one site, or sites within their home country and then, when actions prove to be successful, they gradually expand beyond both geographically and in terms of efforts taken on the initial site.

(2) Are we referring to emissions and energy use in relation to this site/these sites only and, if so, including or excluding the corporate vehicle fleet (Scope 1 + 2). Or does the ambition go beyond the direct and indirect emissions that are under quasi-direct control of the stakeholder? Such Scope 3 emissions arise indirectly from one’s action but are often outwit direct control, and include business travel, the workforce’s commute and additional emissions arising along up- and downstream supply chains (cf. Figure 4) [61].

To the author’s experience, most companies initially only address their energy-related emissions (Scope 2), as well as emissions directly arising from their work (Scope 1), due to the complexities of addressing Scope 3 emissions. Complexities arise predominantly out of potential double counting: Scope 1 emissions of one company might be Scope 3 emissions of another company [61,62]. Currently under investigation by EEI in its second data collection 2021, the interim analysis suggests that 77% of the 848 (846, 843) companies responding to this question strive to address Scope 1 emissions or have done so successfully already, 78% target Scope 2 and 75% Scope 3 emissions (cf. Figure 5). Further analysis of the new data will allow an examination of whether companies on average only address Scope 3 after a head start on Scope 1 and 2. The interim analysis suggests so: the progress is furthest in respect to Scope 2, followed by Scope 1 and with a substantial gap in Scope 3, which is understandable, as Scope 2 is ‘easiest’ to achieve by optimising energy supply contracts [43].

(3) Approaching emissions from a different, a product angle: are only those emissions considered up to the point when (a) a product leaves the premises or arrives at the customer/the shop? Or is the additional emission footprint of the product (b) arising during its useful life, or (c) even until it is fully disassembled and recycled of relevance, too? Particularly in the automotive industry (b), this is of high relevance to meet the European Union’s requirement on new vehicles to not exceed 95 g of CO2-eq per km on fleet average to avoid being fined 95 Euros per gram and vehicle exceeding the average [63]. Considering the large footprint carried by the manufacture of lithium-ion batteries, but also steel, aluminium etc., manufacturers such as Volkswagen work to sell their electric vehicles with a net-zero footprint at the point of handover [64]. A significant undertaking, as many end products’ Scope 3 emissions make up more than 75°% of the overall “Product Carbon Footprint” (PCF)—82% in the automotive industry [65] (p. 9).

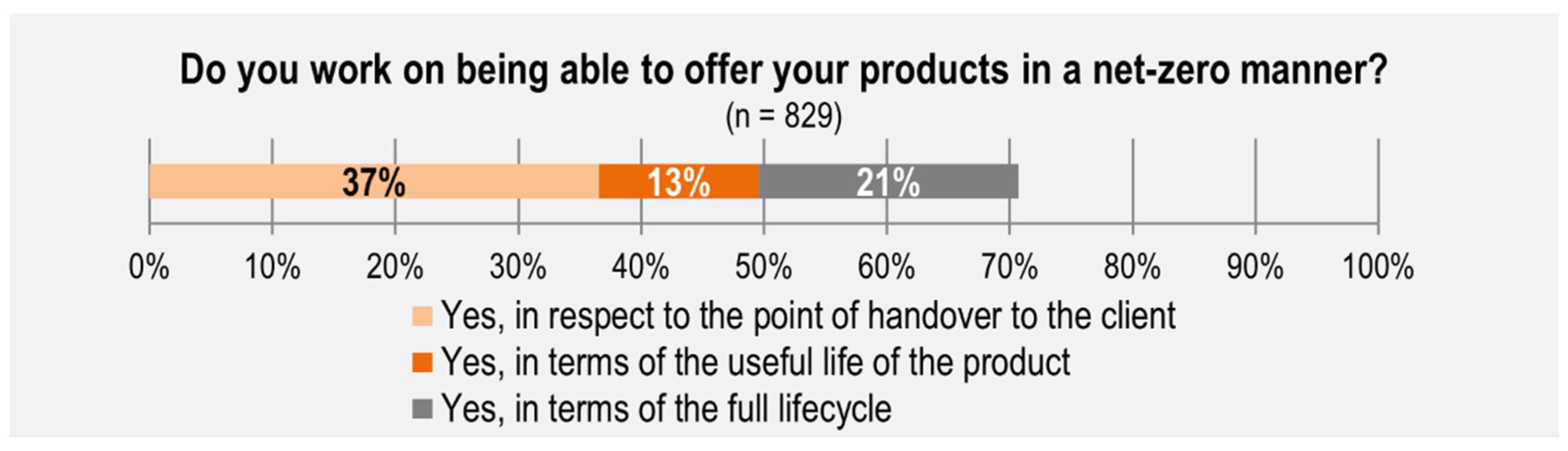

The automotive industry is not the only sector where PCFs are increasingly found. The chemical giant BASF announced the assessment of the carbon footprint of all its products, as well [66]. Interim analysis of the EEI’s second data collection in 2021 suggest that 37% of 829 companies responding to this question consider the PCF until the point of handover, 13% until the end of useful life, and 21% until the product is fully recycled/disposed of. However, 29% do not consider their products’ PCF at all at this point. In total, almost 71% of companies work to offer products with a ‘net-zero’ footprint in one form or another, at least in respect to the point of handover (cf. Figure 6) [43], which is a good move in context of the EU’s sustainable product legislative initiative mentioned earlier [23].

As the bandwidth and efforts required largely differ depending on what system barriers are being set, defining the area of observation, the spatial, as well as the scope of reduction, constitutes the fourth success criterion to reach net-zero.

3.5. Motivation and Needs

Beyond the somewhat technical questions of what, by when, and how far, it is of critical relevance to explore why decarbonisation is sought. What is the underlying motivation of the executive leadership and the stakeholder for pursuing net-zero? Motivation plays a large role in determining one’s ideal strategy and mix of measures, as elements that are of high internal (e.g., corporate culture) or external (e.g., legislation) relevance may be emphasised over a purely technical composition of measures. The motivation also determines how the topic of decarbonisation is embedded in the stakeholder’s overall strategy.

- Common motivators include (not exhaustive) [67]:

- Requirements of the upstream supply-chain;

- Requirements of investors/shareholders;

- Image improvement: display leadership and innovativeness;

- Image improvement: attracting and retaining skilled personnel;

- Pursuing societal responsibility and corporate culture;

- Meeting societal expectations;

- Demands from policymakers and meeting legal requirements;

- Long-term economic advantages, including building up competency;

- Risk reduction regarding external shocks, such as energy price and acquisition and emission costs;

- Ensuring security of supply arising from (micro-) outages.

As Buettner and König [67] outline analysing these motivators, there is an increasing pressure to take action, triggered by both, but not only, investors and up-stream supply-chains. The latter has just been confirmed by EEI [43]: around a third of 836 participating companies are facing emission-related contractual demands from their upstream supply-chain. Image is not only of relevance to remain able to sell one’s products but also to attract and retain scarce skilled personnel. The steeply increasing price of (a) CO2 within the European Emission trading system (EU ETS, currently at 96 EUR/tCO2-eq, [68]), (b) electricity, and (c) gas are an increasing cause of concern among stakeholders [69,70,71,72], even more so since Ukraine was attacked.

As decarbonisation measures that best address the various motivators can differ widely, getting a clear picture of the main motivator(s) for the decision to act constitutes the fifth success criterion on the path to net-zero.

3.6. Priorities

While answering the question of why, when, and what is the essential foundation of determining a roadmap to neutrality, the latter can only succeed if further decision criteria are being determined. These criteria are needed to rank and filter feasible measures simultaneously or after scoring how well these measures address the key motivators. Decision criteria include (not exhaustive) [73]:

- Level of investment;

- Investment cost per tonne of CO2-eq. avoided;

- Emission cost savings (absolute or relative to invest);

- Image effect through visible measures;

- Expected increase in productivity

- Technical aspects and risks (complexity and difficulty level);

- Disruption of operations (cross-cutting-, support processes or core processes);

- Implementation competence (experience with type of measure or access to personnel with necessary skills);

- Impact on company valuation

- Payback time (including emission-related opportunity costs of inaction);

- Availability of required material and equipment (supply bottlenecks).

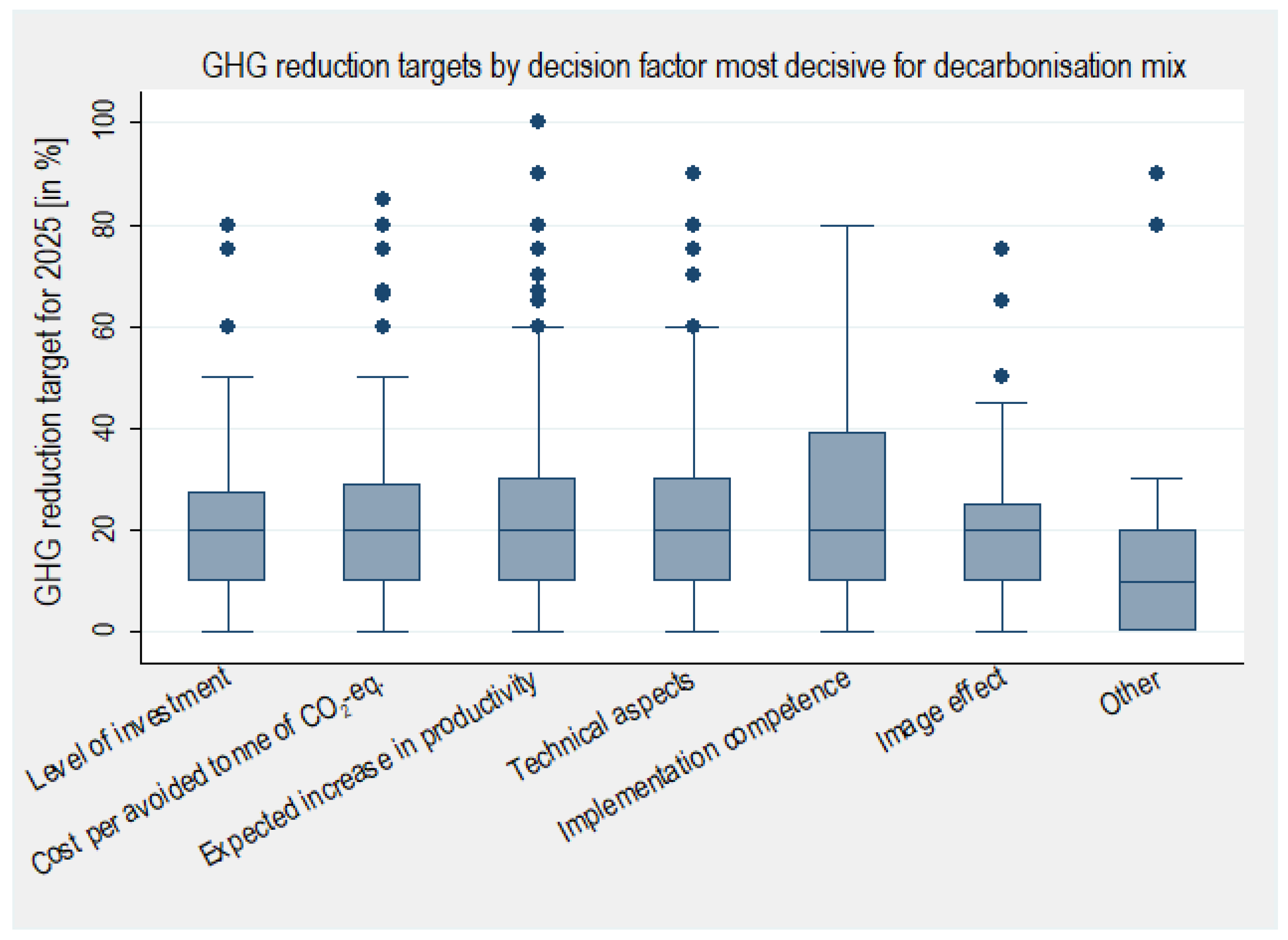

Analysing data of the EEI [40], Buettner and König found that economic factors such as absolute and relative level of investment have the highest priority as decision criterion [73]. Given that, they also found that technical aspects are the third most frequently mentioned primary decision criterion, having asked 787 companies. They further identified that the aggregate findings diverge significantly when assessing the top three decision factors from a company size, energy intensity, or sub-sectorial perspective. In context of the GHG reduction target, looking at the primary decision factor only, implementation competence stands out (cf. Figure 7). Either companies setting a particularly ambitious GHG reduction target (understandably) look particularly at their implementation competence when deciding which action(s) to pursue or, companies that have (access to) implementation competence (are able) to set more ambitious targets. At least, these two readings appear to play a role for the upper two quartiles of companies illustrated in Figure 7, indicating ‘implementation competence’ to be their primary decision criterion when selecting of individual measures, as the median GHG reduction target is at the same level as for the other primary decision criteria [40].

As the criteria according to which measures are vetted for feasibility and ranked have a significant impact on how the set of individual measures of a decarbonisation roadmap will look like, deciding upon the top three determinants or their ranking order is the sixth success criterion on the way to net-zero.

3.7. Status Quo

While the first six success criteria are largely a strategic and economic decision to be taken by the stakeholder, they are still insufficient to derive a successful decarbonisation strategy. Determining one’s ideal decarbonisation strategy and subsequently a concrete set of measures is dependent on knowing about where one stands right now-the status quo. As simple as determining the status quo sounds, it requires a thorough assessment across various dimensions:

- (a)

- What has already been done? How is the state of the sites, machinery, and equipment? Are there any obvious low hanging fruits?

- (b)

- What intervention is approaching anyway? This can be replacement investments, a restructuring of the production line, process, or product range.

- (c)

- How ‘safe’ is the site in its existence? This is of relevance if investing into high efficiency technologies that are pricey to acquire but promise large relative energy and emission savings. If the (non-environmental) sustainability of the business model or production technology is questionable it might, however, not make sense to invest large sums at that site.

- (d)

- What is the current energy consumption per type of fuel and site, and what are the energy and process-related emissions in respect to the target dimension and area of observation? Based on this information, stakeholders will know where they are starting from and potentially also where interventions might promise the biggest impact per effort taken.

- (e)

- What are the local conditions?

- o

- Are there undeveloped areas or available roof spaces? For instance, for on-site generation of renewable energy, energy storage, or heat recovery systems.

- o

- How are the climatic conditions? This includes temperature range (e.g., for air/air heat pumps or air conditioning needs and level of insulation), solar radiation (to harness solar energy), wind and air corridors (to apply micro wind generation or use passive ventilation), adjacent waters (for micro-hydro or air/water heat pumps), geology (regarding earthquake risk and for geothermal energy including air/ground heat pumps) and environmental protection zones (e.g., limited development due to protected species or drinking water protection areas).

- o

- How is the surrounding infrastructure? Is there access to overland power lines, proximity to wind farms, solar parks, or hydro power stations? Are there nearby plots of land that would be suitable for these technologies (for off-premises self-generation)?

- o

- Who is in the neighbourhood? This is primarily the proximity to entities with whom a symbiotic relationship could be built, typically a sender or recipient of secondary energy or secondary raw materials either on the stakeholders’ site (i.e., pre-heating of processes), the industrial estate or in the borough (i.e., feeding waste heat into district heating grid, as Aurubis does for Hamburg’s Hafencity [74]). Here, it also plays a role how ambitious the local authority is, as well as the state, region, and country the site is located in and further, whether there are support- and co-funding schemes or other support-mechanisms in place to benefit from or to reduce the overall investments.

According to EEI, about half of participating companies have not been aware of their energy- or process-related emission footprint at the time of participation (cf. Figure 8) [41].

Apart from lighting, the majority of companies were also not aware of their percentage energy saving potentials of the cross-cutting technologies they use (cf. Figure 9) [42].

More than four out of ten companies were unaware of what proportion of their energy is used for heating and cooling (cf. Figure 10). The latter are, in contrast to electricity, rather immobile, harder to electrify, and difficult to decarbonise, but they offer great potentials for waste energy utilisation, which 22% of participating companies do not harness at all (cf. Figure 11) [42].

Acquiring a fair understanding of the status quo, the foundation the road to neutrality is built on, is the starting point of all further steps and hence the seventh success criterion.

With the answers to these seven foundational questions, spanning across economic, technical, strategic, principled, and geo-spatial dimensions, it is then feasible for stakeholders to derive both general (Section 3.8) and specific ways (Section 3.9) forward.

3.8. General

Building on the answers to the seven foundational questions, it is now necessary to determine the proportion to which the goal is to be achieved through measures that can be implemented locally and measures that are to be implemented externally or by others.

- As described by Buettner et al. [38], internal measures can include:

- Reduction of energy consumption (and of the connected load) through energy efficiency measures, including utilising waste energy and passive resources such as passive ventilation or solar gains.

- Reduction of process-related or process-induced emissions, for instance by substituting (metallurgical) coke with green hydrogen in steel production, by identifying alternative chemical transformation pathways that are less emission intensive but lead to an equivalent outcome, or by developing more resource efficient processes and products that require a smaller proportion of emission intensive ingredients (e.g., cement clinker in the cement industry).

- Self-generation of renewable energies and their storage, such as solar-, wind-, hydro- or geothermal energy, including means of flexibilising the energy demand.

- External measures are all other measures, such as:

- Acquisition of renewable energy (e.g., electricity, hydrogen, biomass, biogas, district heating).

- Procurement of (intermediate) products, raw materials, services, and mobility that have a net-zero emission footprint—either directly acquired on the market or via requirements set for suppliers.

- Offsetting emissions through projects (e.g., afforestation or efficiency-replacement programs through one’s own products—comparable to a self-initiated scrappage scheme).

- Offsetting through purchase of certificates.

- Acceptance of the payment of emission charges (in this case ‘net-zero’ is out of reach in most scenarios).

Carbon capture and storage or utilisation (CCU/CCS/CCUS) is an additional measure, but it does not avoid the emergence of emissions, it only prevents them from being emitted into the atmosphere. While emissions are captured locally (internal measure), their further treatment can take place locally as well as elsewhere (external measure) [47]. A vast range of studies (such as Cresko et al. [45] and Rissmann et al. [28]) provide further and concrete detail on internal and external measures.

To determine the sequence of measures and the split between local and external measures, both the prioritisation procedures and the scoping outcomes are instrumental as the potential effect of individual measures, investment cost, complexity, payback time, and other key performance indicators will differ and need to be weighted.

It needs to be stated that the split will change over time and with progressing implementation. Bosch, for instance, announced in May 2019 that it would reach carbon neutrality by 2020 [55]. This was only feasible by launching activities in all areas. As local measures could not all be implemented within such a short period, the coverage gap was addressed through offsetting via climate protection projects and the acquisition of green energy. With the progressing implementation of local measures, these external measures can be melted down to a degree until the optimal constellation for net-zero carbon emission is reached. In the meantime, Bosch has changed to the political target dimension of the European Union, climate neutrality, and clarified that succeeding in their original area of observation (Scope 1 + 2), they are now working on Scope 3 [75].

Unless addressed when responding to the seven foundational questions, it is essential to make the decision of whether the tool of compensation through projects or certificates is within one’s toolkit. Offsetting does allow reaching net-zero in an expedited manner at the additional cost of the certificates/for the projects—literally buying time until emission saving measures implemented locally take an effect. Accepting emission costs until these can be avoided ‘naturally’ is the alternative. In the author’s experience, several companies rule out compensation as an instrument of their decarbonisation toolkit, as they consider it cheating, since it does not help them reach actual zero emissions. Furthermore, they may wish to avoid the repercussions if such projects are found to be dubious or faulty, or simply want to work towards zero ‘naturally’ [76,77,78].

3.9. Specific

Beyond the general types of measures described in the previous sub-chapter, there are further interventions, very specific to the situation of a stakeholder and their status quo, that present an opportunity to take a technology leap on the way to shape a net-zero business model. This is to replace existing machinery and equipment with innovative cutting-edge ones that also allow for capitalisation on the opportunities presented by automation, digitalisation, and machine learning. This can, for instance, be control systems that adjust the source of energy, storage, and a range of energy flexibility means by the current availability and price of clean energy, including virtual storage [79]. Another example is factory operation systems that report machine data to a central dashboard in a plug-n-play manner. Similar to the interoperability of “Internet of Things” (IoT) devices in more recent smart home systems or computer operating systems, they adjust to different form factors via drivers built around a core operating system [80]. Other studies also highlight the growing importance of digitalisation in other areas of sustainable business performance, such as cloud-manufacturing, recyclability, and circular economy [81].

3.10. Economic Viability

Buettner and Wang [47] point out that in the context of decarbonisation it is necessary to reconsider traditional economic viability calculations to assess the economic performance of technically feasible measures. The traditional model does neither account for increasing energy costs, nor for the increasing costs of inaction in the format of emission pricing (the price within the EU Emission Trading System (EU ETS), for instance, has risen by over 50% between 1 November 2021 and 1 February 2022 [68]). Further, a short payback time is often a key decision criterion due to various reasons, including business cycles, useful life of machinery, etc. However, in the context of decarbonisation, it makes sense to look for the best constellation for the respective milestone or target year.

To apply this, all types of measures remaining up to this point are to be assessed based on their economic merits, including emission costs avoided, and then weighted and scored as defined by the stakeholder. Simplified, the resulting ranking order constitutes the ideal configuration at that very point of time. ‘Simplified’, as some measures might depend on each other, are not compatible or only unleash their highest efficiency if applied in a bundle.

3.11. Dynamic Adjustment to Changing Environments

As energy prices and emission costs change over time, the ideal configuration changes over time, as well. To keep one’s optimal decarbonisation strategy up to date with energy and emission price developments, it is advisable to make the ranking table of measures described in Section 3.10 dynamically respond to such changes. This is of particular relevance, as these cost-changes can have a significant impact on the ranking order of potential measures in a multiple year timeframe. As described by Buettner and Wang [47], building on energy and emission cost schedules and forecasts, it is then feasible to optimise the mix of measures based on specific milestone or target years, or a combination of these, respectively.

Combining all of the factors discussed in this chapter result in a focus-, situation-, priority- and specificity-driven approach, which is a very individual puzzle that changes its configuration over time.

4. Conclusions and Discussion

Within this article, the author illustrated how the methods applied lead to an understanding of how everything is connected. Using the backcasting method, he provides a step-by-step overview of seven foundational aspects that require attention, thereby helping decision makers in shaping a successful and effective decarbonisation strategy.

Even though the general approach towards what needs to be done may be similar to approaches applied by others, this roadmap to neutrality differs by (a) taking the perspective of an executive decision maker on the demand-side and (b) going a level deeper, where most other approaches indicate what needs to be done, either in general from a system or country level [28,29], or on a micro level (i.e., technical optimisation options and procedures) [25,26,45]. In addition, where existing approaches outline technical roadmaps [45] or indicate what must be done but not always how [30,31,32,84] and stop short of putting it into context, the approach presented explains the underlying strategic aspects that need to be considered beforehand. Firstly, such considerations raise awareness of the implications of decisions (to be) made and, secondly, ensure the ability to take decarbonisation actions in the best manner and interest of the company. Finally, this approach differs in its methodology by combining qualitative and quantitative data, which (a) allows one to validate learnings from individual cases on a much wider basis, and (b) to interpret broad quantitative findings in context, as sometimes multiple readings appear plausible.

Determining one’s ideal decarbonisation strategy, associated decarbonisation roadmap and range of concrete measures essentially comes down to considering one’s situation, priorities and motivations, and focus. With these points—addressed by the seven success criteria—one’s specific puzzle of measures falls into place.

As shown in the step-by-step approach, clarity regarding the terminology of the target dimension (e.g., carbon vs. climate neutrality; Section 3.1) and the optimisation variables, inferable from this target dimension (Section 3.2), are the first two steps. This is important, as a target can only be set and achieved effectively if it is clearly defined, and ideally is also in line with general country- and regional-level goals. Given this, the level of ambition (Section 3.3) needs to be clarified, as it goes beyond the previously mentioned dimensions, including time-targets and reduction goals. Here, it may also make sense to establish interim milestones to assess progress in smaller steps. Next, stakeholders should define the area of observation and the system barriers (Section 3.4), as well as the scope of emission reductions. This includes the chosen sites the company intends to decarbonise (spatial) and the scopes of emission—scope 1, 2, and 3—that are supposed to be reduced. Besides these rather technical decisions, the identification of one’s intrinsic motivation to decarbonise can also be crucial (Section 3.5). Such motivators can reach from purely economic rationales and legal requirements to reputational issues and social responsibility. Being clear about their motivations, stakeholders also need to formulate their priorities, which serve as criteria for the implementation of measures (Section 3.6). Data from EEI shows that, on average, companies rank investment level highest and that the ranking largely depends on company size and energy-intensity level. Finally, yet importantly, it is essential that companies know their starting point—their status quo (Section 3.7). Only those who are aware of their fundamentals can hope to effectively build on them. This includes current levels of energy consumption and emissions but also many other factors, such as surrounding infrastructure and climatic conditions.

After one has fulfilled all of the abovementioned points, further decisions on whether to take external (e.g., acquisition of renewable energy) or internal (e.g., reduction of energy consumption) measures to reach the target need to be made (Section 3.8). Deciding on whether to count on compensation measures or not is part of this process. More specific decisions on which measures to take depend on the individual situation of a company (Section 3.9).

Nevertheless, it remains to be underlined that the road to net-zero does not end with meeting the (milestone-)targets set within time. Like reaching one’s ideal weight, it is one challenge to reach it, and another one to keep it. The ideal mixture of measures to maintain it is likely to change with time, situation, and environment.

An adjusted form of economic viability assessment (Section 3.10), as well as a continuous adjustment to current prices, availabilities, changing environments and policies (Section 3.11) will ease the challenge of keeping the decarbonisation strategy and associated mix of measures ideal over time.

Data of the Energy Efficiency Index of German Industry illustrated that a significant proportion of manufacturers participating in the survey are already on a good path. However, the remaining companies need to be picked up, and much work remains to be done across all areas looked at to successfully transition to a net-zero economy and to keep it net-zero.

Even though most of the evidence was gathered from German manufacturers and reflects the situation in Germany, it can be argued that the seven foundational questions are likely to remain valid irrespective of geography or culture. In contrast, the answers to the seven questions are likely to be different depending on those factors. Therefore, the currently ongoing data collection via the Energy Efficiency Barometer of Industry and the exchange with bodies, stakeholders, and companies in other geographies is of particular interest. Whether the seven questions can be also applied to areas outside the industry remains to be assessed by further analysis.

Funding

The article processing charge was funded by the Deutsche Forschungsgemeinschaft (DFG) in the funding programme Open Access Publishing.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

The data presented in this study are available on request from the corresponding author. The data are not publicly available due to privacy issues.

Acknowledgments

The underlying research in the form of the Energy Efficiency Index of German Industry (EEI, #EEIndex) would not have been possible without the continuous support of the Karl-Schlecht-Foundation and the Heinz und Heide Dürr Foundation, as well as the companies participating and the network of partners of the EEI, including those reviewing and supporting in progress of developing this paper and the EEI data collection process, notably Samuel Wörz, Frederick Vierhub-Lorenz, Marina Gilles, Anabel Reichle, Ole Pfister, and Werner König, the decarbonisation team and the team of student researchers. In Germany, evidence is usually collected each April/May and October/November (www.eep.uni-stuttgart.de/eei; accessed on 21 April 2022); the #EEBarometer runs all year round in nine further languages across 88 countries (www.eep.uni-stuttgart.de/eeei; accessed on 21 April 2022). The summarised results and recordings of briefings on the results can also be found there. All conclusions, errors, or oversights are solely the responsibility of the author.

Conflicts of Interest

The author declares no conflict of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript; or in the decision to publish the results.

References

- McClean, D. Earth Day: 2020 Saw a Major Rise in Floods and Storms. UNDRR. 2021. Available online: https://www.undrr.org/news/earth-day-2020-saw-major-rise-floods-and-storms (accessed on 29 December 2021).

- Renouf, J.S. Making sense of climate change—The lived experience of experts. Clim. Chang. 2021, 164, 14. [Google Scholar] [CrossRef]

- Ripple, W.J.; Wolf, C.; Galetti, M.; Newsome, T.M.; Green, T.L.; Alamgir, M.; Crist, E.; Mahmoud, M.I.; Laurance, W.F. The Role of Scientists’ Warning in Shifting Policy from Growth to Conservation Economy. BioScience 2018, 68, 239–240. [Google Scholar] [CrossRef] [Green Version]

- Masson-Delmotte, V.; Zhai, P.; Pörtner, H.O.; Roberts, D.; Skea, J.; Shukla, P.R.; Pirani, A.; Moufouma-Okia, W.; Péan, C.; Pidcock, R.; et al. An IPCC Special Report on the Impacts of Global Warmin of 1.5 °C above Pre-Industrial Levels and Related Global Greenhouse Gas Emission Pathways, in the Context of Strengthening the Global Response to the Threat of Climate Change, Sustainable Development, and Efforts to Eradicate Proverty. IPCC. 2019. Available online: https://www.ipcc.ch/site/assets/uploads/sites/2/2019/06/SR15_Full_Report_High_Res.pdf (accessed on 31 January 2022).

- Masson-Delmote, V.; Zhai, P.; Piani, A.; Connors, S.L.; Péan, C.; Berger, S.; Caud, N.; Chen, Y.; Goldfarb, L.; Gomis, M.I.; et al. Climate Change 2021—The Physical Science Basis—Summary for Policymaker. IPCC. 2021. Available online: https://www.ipcc.ch/report/ar6/wg1/downloads/report/IPCC_AR6_WGI_SPM_final.pdf (accessed on 31 January 2022).

- United Nations. Paris Agreement. 2015. Available online: https://unfccc.int/sites/default/files/english_paris_agreement.pdf (accessed on 28 December 2021).

- IEA. World Energy Outlook 2021. 2021. Available online: https://iea.blob.core.windows.net/assets/4ed140c1-c3f3-4fd9-acae-789a4e14a23c/WorldEnergyOutlook2021.pdf (accessed on 28 December 2021).

- Jugel, C.; Albicker, M.; Bamberg, C.; Battaglia, M.; Brunken, E.; Bründlinger, T.; Dorfinger, P.; Döring, A.; Friese, J.; Gründing, D.; et al. dena-Leitstudie Aufbruch Klimaneutralität. Deutsche Energie-Agentur GmbH. 2021. Available online: https://www.dena.de/fileadmin/dena/Publikationen/PDFs/2021/Abschlussbericht_dena-Leitstudie_Aufbruch_Klimaneutralitaet.pdf (accessed on 28 December 2021).

- The Economist. How to Escape the Bear Market: Europe Reconsiders Its Energy Future. 2022. Available online: https://www.economist.com/business/2022/03/05/europe-reconsiders-its-energy-future (accessed on 23 March 2022).

- Fairley, P. Germany Folds. IEEE Spectr. 2011, 48, 47. [Google Scholar] [CrossRef]

- Climate Action Tracker. CAT Net Zero Target Evaluations. 2021. Available online: https://climateactiontracker.org/global/cat-net-zero-target-evaluations/ (accessed on 31 December 2021).

- Net Zero Climate. What Is Net Zero? Available online: https://netzeroclimate.org/what-is-net-zero/ (accessed on 31 December 2021).

- Net Zero Tracker. Net Zero Tracker Beta. 2021. Available online: https://zerotracker.net/ (accessed on 31 December 2021).

- Lamb, W.F.; Wiedmann, T.; Pongratz, J.; Andrew, R.; Crippa, M.; Olivier, J.G.J.; Wiedenhofer, D.; Mattioli, G.; Khourdajie, A.A.; House, J.; et al. A review of trends and drivers of greenhouse gas emissions by sector from 1990 to 2018. Environ. Res. Lett. 2021, 16, 073005. [Google Scholar] [CrossRef]

- IEA. Global Energy Review: CO2 Emissions in 2020. 2021. Available online: https://www.iea.org/articles/global-energy-review-co2-emissions-in-2020 (accessed on 28 December 2021).

- Kim, Y.J.; Brown, M. Impact of domestic energy-efficiency policies on foreign innovation: The case of lighting technologies. Energy Policy 2019, 128, 539–552. [Google Scholar] [CrossRef] [Green Version]

- Houde, S.; Spurlock, C.A. Minimum Energy Efficiency Standards for Appliances. Old and New Economic Rationales. Econ. Energy Environ. Policy 2016, 5, 65–84. Available online: https://0-www-jstor-org.brum.beds.ac.uk/stable/26189506 (accessed on 28 December 2021). [CrossRef]

- Umweltbundesamt. Energieverbrauch 2020 nach Sektoren und Energieträgern. 2021. Available online: https://www.umweltbundesamt.de/bild/endenergieverbrauch-2020-nach-sektoren (accessed on 10 December 2021).

- Umweltbundesamt. Energiebedingte Treibhausgas-Emissionen 1990–2019. 2021. Available online: https://www.umweltbundesamt.de/sites/default/files/styles/800w400h/public/medien/384/bilder/2_abb_energiebed-thg-emi_2021-06-02.png (accessed on 10 December 2021).

- Umweltbundesamt. Entwicklung der Treibhausgasemissionen in Deutschland 2010–2019. 2021. Available online: https://www.umweltbundesamt.de/sites/default/files/medien/421/bilder/1_entwicklung_der_treibhausgasemissionen_in_deutschland_0.jpg (accessed on 10 December 2021).

- IEA. Global CO2 Emissions by Sector, 2019. 2021. Available online: https://www.iea.org/data-and-statistics/charts/global-co2-emissions-by-sector-2019 (accessed on 31 January 2022).

- IEA. Key World Energy Statistics 2021. 2021. Available online: https://www.iea.org/reports/key-world-energy-statistics-2021 (accessed on 31 January 2022).

- European Commission. Sustainable Product Policy & Ecodesign. Available online: https://ec.europa.eu/growth/industry/sustainability/sustainable-product-policy-ecodesign_en (accessed on 30 March 2022).

- Herz, C. Neuer Ressourcenpass für Gebäude: Was jetzt auf Mieter und Eigentümer Zukommt. Handelsblatt. 2022. Available online: https://www.handelsblatt.com/finanzen/immobilien/immobilien-neuer-ressourcenpass-fuer-gebaeude-was-jetzt-auf-mieter-und-eigentuemer-zukommt/28051264.html (accessed on 27 March 2022).

- Nurdiawati, A.; Urban, F. Towards Deep Decarbonisation of Energy-Intensive Industries: A Review of Current Status, Technologies and Policies. Energies 2021, 14, 2408. [Google Scholar] [CrossRef]

- Bauer, F.; Hansen, T.; Nilsson, L.J. Assessing the feasibility of archetypal transition pathways towards carbon neutrality—A comparative analysis of European industries. Resour. Conserv. Recycl. 2022, 177, 106015. [Google Scholar] [CrossRef]

- Bataille, C.; Åhman, M.; Neuhoff, K.; Nilsson, L.J.; Fischedick, M.; Lechtenböhmer, S.; Solano-Rodriquez, B.; Denis-Ryan, A.; Stiebert, S.; Waisman, H.; et al. A review of technology and policy deep decarbonization pathway options for making energy-intensive industry production consistent with the Paris Agreement. J. Clean. Prod. 2018, 187, 960–973. [Google Scholar] [CrossRef] [Green Version]

- Rissman, J.; Bataille, C.; Masanet, E.; Aden, N.; Morrow, W.R.; Zhou, N.; Elliott, N.; Dell, R.; Heeren, N.; Huckestein, B.; et al. Technologies and policies to decarbonize global industry: Review and assessment of mitigation drivers through 2070. Appl. Energy 2020, 266, 114848. [Google Scholar] [CrossRef]

- Johnson, O.W.; Mete, G.; Sanchez, F.; Shawoo, Z.; Talebian, S. Towards Climate-Neutral Heavy Industry: An Analysis of Industry Transition Roadmaps. Appl. Sci. 2021, 11, 5375. [Google Scholar] [CrossRef]

- South Pole. Become Climate Neutral. 2021. Available online: https://www.southpole.com/sustainability-solutions/become-climate-neutral (accessed on 31 December 2021).

- Climate Neutral. How It Works. 2021. Available online: https://www.climateneutral.org/how-it-works (accessed on 31 December 2021).

- Fashion Cloud. So Wird Dein Unternehmen Klimaneutral. 2021. Available online: https://fashion.cloud/de/so-wird-dein-unternehmen-klimaneutral/ (accessed on 31 December 2021).

- Robinson, J.B. Energy backcasting A proposed method of policy analysis. Energy Policy 1982, 10, 337–344. [Google Scholar] [CrossRef]

- Hughes, N.; Strachan, N.; Gross, R. The structure of uncertainty in future low carbon pathways. Energy Policy 2013, 52, 45–54. [Google Scholar] [CrossRef]

- Bataille, C.; Waisman, H.; Colombier, M.; Segafredo, L.; Williams, J. The Deep Decarbonization Pathways Project (DDPP): Insights and emerging issues. Clim. Policy 2016, 16, 1–6. [Google Scholar] [CrossRef] [Green Version]

- Mander, S.L.; Bows, A.; Anderson, K.L.; Shackley, S.; Agnolucci, P.; Ekins, P. The Tyndall decarbonisation scenarios—Part I: Development of a backcasting methodology with stakeholder participation. Energy Policy 2008, 36, 3754–3763. [Google Scholar] [CrossRef] [Green Version]

- Holmberg, J.; Robèrt, K.-H. Backcasting—A framework for for strategic planning. Int. J. Sustain. Dev. World Ecol. 2000, 7, 291–308. [Google Scholar] [CrossRef]

- Buettner, S.M.; Schneider, C.; König, W.; Mac Nulty, H.; Piccolroaz, C.; Sauer, A. How do German manufacturers react to the increasing societal pressure for decarbonisation? Appl. Sci. 2022, 12, 543. [Google Scholar] [CrossRef]

- EEP. Der Energieeffizienz-Index der Deutschen Industrie. Umfrageergebnisse 2. Halbjahr 2019; Institut für Energieeffizienz in der Produktion, Universität Stuttgart: Stuttgart, Germany, 2019; Available online: https://www.eep.uni-stuttgart.de/eei/archiv-aeltere-erhebungen/ (accessed on 21 April 2022).

- EEP. Der Energieeffizienz-Index der Deutschen Industrie. Umfrageergebnisse 1. Halbjahr 2020; Institut für Energieeffizienz in der Produktion, Universität Stuttgart: Stuttgart, Germany, 2020; Available online: https://www.eep.uni-stuttgart.de/eei/archiv-aeltere-erhebungen/ (accessed on 21 April 2022).

- EEP. Der Energieeffizienz-Index der Deutschen Industrie. Umfrageergebnisse 2. Halbjahr 2020; Institut für Energieeffizienz in der Produktion, Universität Stuttgart: Stuttgart, Germany, 2020; Available online: https://www.eep.uni-stuttgart.de/eei/archiv-aeltere-erhebungen/ (accessed on 21 April 2022).

- EEP. Der Energieeffizienz-Index der Deutschen Industrie. Umfrageergebnisse 1. Halbjahr 2021; Institut für Energieeffizienz in der Produktion, Universität Stuttgart: Stuttgart, Germany, 2021; Available online: https://www.eep.uni-stuttgart.de/eei/archiv-aeltere-erhebungen/ (accessed on 21 April 2022).

- EEP. Der Energieeffizienz-Index der Deutschen Industrie. Umfrageergebnisse 2. Halbjahr 2021; Institut für Energieeffizienz in der Produktion, Universität Stuttgart: Stuttgart, Germany, 2022; Available online: https://www.eep.uni-stuttgart.de/eei/archiv-aeltere-erhebungen/ (accessed on 21 April 2022).

- Weber, R. Wärmepumpen als Klimaretter? 2021. Available online: https://www.daserste.de/information/wirtschaft-boerse/plusminus/sendung/waermepumpe-bewertung-100.html (accessed on 30 December 2021).

- Cresko, J.; Shenoy, D.; Liddell, H.P.; Sabouni, R. Chapter 6: Innovating Clean Energy Technologies in Advanced Manufacturing September 2015. Quadrennial Technology Review 2015; U.S. Department of Energy: Washington, DC, USA, 2015; pp. 180–225. Available online: https://www.energy.gov/sites/prod/files/2017/03/f34/qtr-2015-chapter6.pdf (accessed on 21 April 2022).

- Buettner, S.M. Framing the Ambition of Carbon Neutrality, UNECE Task Force on Industrial Energy Efficiency. In Group of Experts on Energy Efficiency; GEEE-7/2020/INF.2; United Nations Economic Commission for Europe: Geneva, Switzerland, 2020; Available online: https://www.unece.org/fileadmin/DAM/energy/se/pdfs/geee/geee7_Sept2020/GEEE-7.2020.INF.2_final_v.2.pdf (accessed on 8 February 2022).

- Buettner, S.M.; Wang, D. A Pathway to Reducing Greenhouse Gas Footprint in Manufacturing: Determinants for an Economic Assessment of Industrial Decarbonisation Measures. EEP—Institute for Energy Efficiency in Production, University of Stuttgart, Stuttgart, Germany. 2022; unpublished. [Google Scholar]

- DPA. Japans neuer Ministerpräsident peilt Klimaneutralität bis 2050 an. Handelsblatt. 2020. Available online: https://www.handelsblatt.com/politik/international/energiewende-japans-neuer-ministerpraesident-peilt-klimaneutralitaet-bis-2050-an/26307902.html (accessed on 30 December 2021).

- Dooley, B.; Inoue, M.; Hida, H. Japan’s New Leader Sets Ambitious Goal of Carbon Neutrality by 2050. The New York Times, 2020. Available online: https://www.nytimes.com/2020/10/26/business/japan-carbon-neutral.html(accessed on 30 December 2021).

- Watkins, M.D. Demystifying Strategy: The What, Who, How, and Why. Harvard Business Review. 2007. Available online: https://hbr.org/2007/09/demystifying-strategy-the-what#:~:text=A%20good%20strategy%20provides%20a,prioritize)%20to%20achieve%20desired%20goals (accessed on 4 February 2022).

- Group of Experts on Cleaner Electricity Systems. Framework for Attaining Carbon Neutrality in the United Nations Economic Commission for Europe (ECE) Region by 2050. ECE/ENERGY/GE.5/2020/8 Rev.1. United Nations Economic and Social Council, 2020. Available online: https://unece.org/fileadmin/DAM/energy/se/pdfs/CES/ge16_2020/ECE_ENERGY_GE.5_2020_8_rev1.pdf (accessed on 7 February 2022).

- G2G. G2G Talk: An Interview with Olga Algayerova. How Is the UN Economic Commission for Europe (UNECE) Working with Countries to Attain Carbon Neutrality in the ECE Region? 2021. Available online: https://www.c2g2.net/c2gtalk-olga-algayerova/ (accessed on 31 December 2021).