Alliance Portfolio Management and Sustainability of Entrepreneurial Firms

1

Business School, China Research Institute of Enterprise Governed by Law, Southwest University of Political Science & Law, Chongqing 401120, China

2

School of Economics and Business Administration, Chongqing University, Chongqing 400030, China

*

Author to whom correspondence should be addressed.

Sustainability 2018, 10(10), 3815; https://0-doi-org.brum.beds.ac.uk/10.3390/su10103815

Submission received: 25 September 2018

/

Revised: 14 October 2018

/

Accepted: 16 October 2018

/

Published: 22 October 2018

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:The aim of the present work is to testify whether the alliance portfolio management capability has an impact on entrepreneurial firms’ sustainability. A moderating mediation model has been applied to a sample consisting of 101 entrepreneurial firms listed in New OTC Market (Over the Counter Market) in China. Based on the research design, second-hand data and first-hand data were used. The findings reveal that the two dimensions of the alliance portfolio management capability, i.e., partnering proactiveness and relational governance, can trigger a higher value of the alliance portfolio and result in the sustainable growth of entrepreneurial firms. What is more, when the board of directors has centralized power, the alliance portfolio management capability will increase the value of the alliance portfolio and improve the sustainability of entrepreneurial firms. Unlike the previous literature, this study discovers the internal mechanism between the alliance portfolio management capability and firms’ sustainability in the context of entrepreneurship. The theoretical condition of this relationship is provided from the perspective of the board of directors.

1. Introduction

Sustainability has different meanings to established firms and entrepreneurial firms. As far as entrepreneurial firms are concerned, given the high risk and uncertainty in the early stage, sustainability means they can survive and then grow sustainably. According to the research on strategy and organizations, it is acknowledged that entrepreneurial firms have higher failure rates than established firms [1]. Due to the liability of newness [2], entrepreneurial firms are short of stable relations with suppliers and customers, as well as sufficient resources [3]. In our research sample, of the firms in the Internet and Information industry in New OTC Market (Over the Counter Market) in China, a quarter had negative profit and 3 firms even withdrew from the market 3 years after their IPO. However, among the 2/5 of firms that had a negative profit before IPO, half of them have gained a positive profit now, within 1 to 5 years. The reason why entrepreneurial firms vary in their pace to survive may be attributed to their access to external resources and the management ability.

Strategic alliances are a valuable tool for entrepreneurial firms, especially benefitting their sustainability. In many cases, entrepreneurial firms have to build on the resources and knowledge from strategic alliances in order to complement their internal insufficient R&D efforts [4], obtain a reputation for themselves [5], and increase the capabilities of learning [6] due to resources and legitimacy liability [7]. Entrepreneurial firms may have a motivation to establish strategic alliances and manage the critical alliance relationships so as to maintain sustainable growth, which are benefits from the complementary resources provided by alliance partners.

Prior research on strategic alliances has focused on dyadic ties from an atomistic perspective [8]. However, entrepreneurial firms are often involved in multiple alliances simultaneously with different partners, establishing an alliance portfolio [9] since they have a diversified resource demand. It has been pointed out that an alliance portfolio is an interesting unit of analysis which leads to new and critical issues [10,11]. The existing literature on alliance portfolios argues that alliances provide firms with different and complementary resources, particularly when the firms are young [12]. Therefore, establishing and managing an alliance portfolio at the founding stage is beneficial for entrepreneurial firms to overcome the liability of newness and gain sustainability. Further, there have been more studies focusing on the structure of the alliance portfolio. However, research on the management of the alliance portfolio is limited [11]. In practice, entrepreneurial firms should develop the ability to manage multiple alliances simultaneously in order to leverage and mobilize resources from different accesses [13]. Accordingly, the capability of the management of the alliance portfolio is defined as the capability to establish, coordinate, and govern the portfolio as a whole [14]. Moreover, the effect of the alliance portfolio management capability on sustainability may be influenced by the board of directors [15]. Strategy management scholars argued that the board of directors needs to be involved in strategic decision-making and in the strategic management process [16]. The extent of their involvement may influence the performance of certain strategic actions [17]. Consequently, the board of directors might be helpful to explain the disparity in the relationship between the alliance portfolio management capability and the firms’ sustainability.

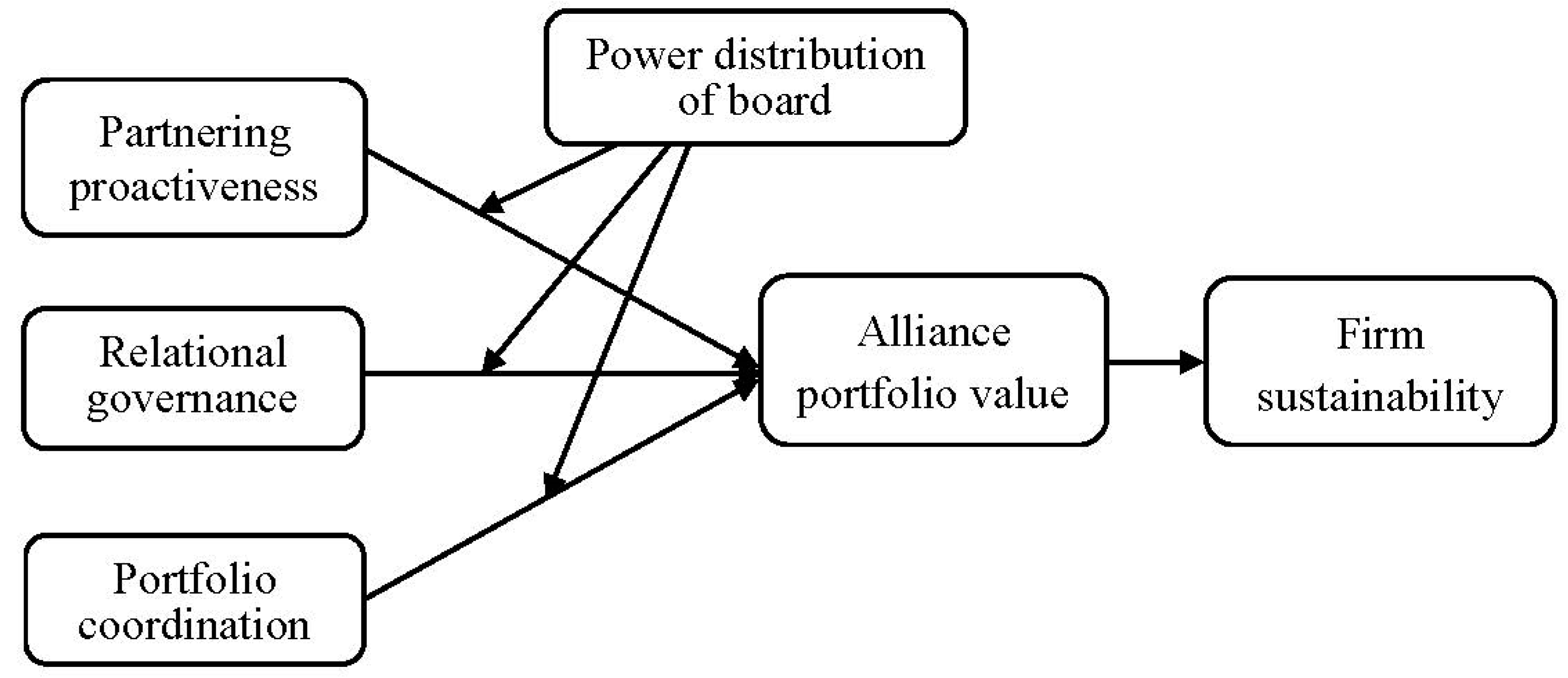

In sum, we ask “how does the alliance portfolio management capability shape the sustainability of entrepreneurial firms under the conditions of power distribution within the board of directors?” We developed the dimensions of the alliance portfolio management capability according to a recent study on partnering proactiveness, portfolio coordination, and relational governance [15], and explored their impact on the sustainability of entrepreneurial firms. We found that both partnering proactiveness and relational governance have a positive impact on the sustainability of entrepreneurial firms, and the effect is fully mediated by the value of the alliance portfolio. What is more, the power distribution within the board of directors moderates the above mediation effect. The analysis reveals that partnering proactiveness and relational governance improve the value of the alliance portfolio and the sustainability of the entrepreneurial firms when the board has central power, but there is a weak improvement when the board has decentralized power.

This work makes the following contributions. Firstly, this study analyzed the antecedents of entrepreneurial firms’ sustainability from the perspective of the alliance portfolio management capability, focusing on the management of the alliance portfolio instead of its structure. Secondly, this study reveals the internal mechanism between the alliance portfolio management capability and firm sustainability by identifying the mediation effect of the alliance portfolio value. Prior research focused on the direct effect of the alliance portfolio management capability and financial outcomes [14,18]. In contrast, this study figured out multiple functions of the alliance portfolio management capability, with the portfolio-level value generating direct effect and firm-level performance yielding an indirect effect. Thirdly, we find the moderation effect of the power distribution of the board in the mediation effect. Despite the extensive research on the board of directors, little is known about the influence of the board in new ventures and entrepreneurial firms, or the linkage to the alliance portfolio. This study enriches the research on the alliance portfolio from the perspective of the corporate government [11,19].

2. Theoretical Background

2.1. Sustainability Development

It is acknowledged that entrepreneurial firms have a higher possibility of failure than established firms because of the liability of newness [3]. Stinchcombe argued that entrepreneurial firms are short of resources, having not established stable and effective relationships with suppliers and customers. Due to these characteristics, sustainability means something different to entrepreneurial firms compared to established firms. As far as established firms are concerned, sustainability focuses on sustainable growth, which refers to a larger market share and sustainable competitive advantages in order to grow stronger. In contrast, sustainability means sustainable survival for entrepreneurial firms in the early stage, which refers to a stable growth of sales or profits to guarantee their survival.

The survival rate of entrepreneurial firms is very low. A number of research articles have focused on the survival of new ventures and entrepreneurial firms, such as new venture formation or new venture performance [20,21]. However, new venture formation is normally measured by firm registration or by sales or profits [22], which cannot show the firm’s sustainable survival or growth in the beginning. Further, prior research has discovered the antecedents of entrepreneurial firms’ performance in terms of human capital [23,24] and the social capital of entrepreneurs [25,26], entrepreneurial behaviors [27,28], etc. Since strategic alliances are an important tool for cooperation and resources acquisition, alliances might provide a unique lens for a better explanation of entrepreneurial firms’ sustainability, which guarantees a stable relationship and legitimacy. Nevertheless, little is known about the impact of alliances on entrepreneurial firms’ sustainability. Compared with the independent role of a single alliance, an alliance portfolio is more conducive to explain the logic of the sustainable survival and growth of entrepreneurial firms because it is more likely to capture the cross-alliance interdependencies, which are the way of mobilizing diversified resources and obtaining a sustainable competitive advantage. Therefore, alliance portfolios might provide additional theoretical explanations for an entrepreneurial firm’s sustainability.

2.2. The Alliance Portfolio Management Capability

It is prevalent that firms engage in multiple strategic alliances with different partners simultaneously, which formed alliance portfolios. The phenomenon of alliance portfolios has been paid more attention to by researchers from different fields, such as the strategy [13], entrepreneurship [29], and network fields [6]. From network theory, an alliance portfolio is defined as an egocentric alliance network of the focal firm [6]. From the additive perspective, an alliance portfolio is defined as an aggregation of all the strategic alliances of focal firms [10,16]. Taking the portfolio as the analysis unit, research into alliance portfolios focuses on the cross-alliance interaction and interdependencies between the partners and alliances as its core issue.

Based on the prior research on alliance portfolios, a holistic approach is needed to better understand the coherent portfolio comprising of multiple individual alliances [11,30]. By adopting this approach, firms can access diversified resources and enjoy additional benefits stemming from the management of the portfolio. Accordingly, researchers attached great importance to it and valuable conclusions have been made on alliance portfolio management. Research on alliance portfolio management focuses on two main topics, which are (a) the emergence of the alliance portfolio management capability and (b) the strategic tools applied to manage alliance portfolio.

Since the latter topic is more concerned about the pragmatic value, the former topic on the management of alliance portfolios is an important stream in the alliance portfolio research. Compared to the alliance capability that focuses on how firms build a single alliance capability, the alliance portfolio management capability includes the capability to form alliance portfolio strategies, develop alliance portfolio management systems, govern multiple partners and their relationships, and coordinate the portfolio [14,16]. The way that the alliance portfolio management capability affects firm performance is associated with alliance experience [31], alliance-related knowledge [32], as well as the integration of these elements in the portfolio [18]. Although previous research has provided an understanding of single alliance capability, studies on the alliance portfolio management capability are limited and have drawn attention recently.

The alliance portfolio management capability is defined as the ability of firms to master sustainable competitive advantages through partner selection, alliance construction, governance mechanisms, and alliance portfolio coordination and configuration [33]. In other words, it is the ability to effectively managing multiple individual alliances simultaneously and to match them with its strategic objectives [34]. The most influential research on the alliance portfolio management capability is by Sarkar et al. [14], which suggested that the alliance portfolio management capability consists of three dimensions: partnering proactiveness, relational governance, and portfolio coordination.

Partnering proactiveness refers to the ability to identify partners who have complementary resources and to establish a cooperative alliance with them. Castro et al. [35] argued that the accurate choice of partners is the first step to successful alliance cooperation. The choice of alliance partners should be comprehensively considered in terms of strategic objectives, complementary resources, and cultural differences. Actively selecting partners with a good reputation and complementary resources is a favorable guarantee for the smooth development of cooperative activities.

Relational governance emphasizes mutual trust and knowledge sharing through contractual governance and relational governance. Hoetker and Molewigt [36] argued that contract governance has two main roles in strategic alliances: one is the control role based on transaction cost theory, and the other is the mediating role based on organizational theory. The controlling role can reduce the risk of the core knowledge and capability being stolen in alliance cooperation, making it easier to acquire and absorb a partner’s resources and knowledge. The mediating role can reduce the conflicts in cooperation, and promote resource and knowledge exchange among alliance partners. Relational governance is indispensable in alliance cooperation. De Vries et al. [37] found that good relationship quality and cooperation experience can enhance the relationship strength between partners and that the relationship strength positively affects the development of exploitative and exploratory cooperation.

Portfolio coordination focuses on the integration and management of resources and knowledge within the alliance portfolio, and the overall regulation of the number and scope of alliance partners [35]. Firstly, the resources brought by alliances are mostly disordered, which can only show their value through coordinating activities [15]. Firms can meet different needs of resources for exploitative and exploratory cooperation through resource coordination and integration. Secondly, when the external technological environment changes, firms can expand the scope of the alliance portfolio by attracting more partners with excellent innovation abilities and develop new technologies through active exploratory cooperation. When the external market environment changes, firms can choose partners with a strong market ability to maintain or improve their market share.

2.3. Board of Directors

The extant research on corporate governance has focused on two functions of the board of directors, that is, the control function and the service function. Based on the agency theory, the board of directors plays a controlling and monitoring role in strategic decision-making in order to deal with multiple agency problems [38]. Based on the stewardship theory, the controlling role of board members is challenged by the idea that there is no collision between the board members and managers [15]. Board members should be actively involved in strategic decision-making so as to realize the service function. Whether the decision-making process is scientific and effective will undoubtedly have a decisive impact on the firms’ market competitiveness and sustainability development.

The function of the board of directors depends on its power distribution. Power reflects the ability of board members to achieve the desired results through formal or informal means [39]. Powerful board members, normally the ones who have more shares, may have a high status and authority in decision-making. Further, power distribution determines whether the board is centralized or decentralized, which influences the speed of the decision-making. From the perspective of the alliance portfolio management capability, the power distribution of the board of directors determines the extent to which the capability may function. Recent research recommended that the board of directors might provide additional explanations for alliance portfolio management [15].

The power distribution of the board might influence the sustainability of firms. Agency theory holds that the board with a high power concentration can effectively reduce the short-term profit pressure and increase the long-term R&D investment of firms [40]. Controlling directors will pay attention to the long-term strategic development because of their long-term holdings and initiate breakthrough innovations that can bring new markets and a strong competitiveness to the firms [41]. In the case of low power concentrations, the “free rider” and “foot vote” phenomena are common among minority directors, which leads to the weak supervision of directors over managers, asymmetric information, and “risk aversion” choices by managers [42], resulting in the lack of long-term development considerations, which is not conducive to a firm’s sustainability development.

3. Hypothesis

3.1. Mediation of the Alliance Portfolio Value in the Relationship of the Alliance Portfolio Management Capability and Sustainability

Prior research has argued that the alliance portfolio management capability is associated with portfolio-level outcomes and firm-level performance. It is acknowledged that firms can finish the complex task of alliance portfolio management [43], maximize alliance success [44], and obtain cooperative benefits and competitive advantages [32] through their alliance portfolio management capability. However, the relationship between the alliance portfolio management capability and performance has been discussed on the portfolio level and the firm level separately, with little consideration on the combined effect of the different levels of performance, nor of the internal mechanism of the relationship between capability and firm-level performance. We believe that firms with a high capability of managing an alliance portfolio may acquire a better alliance portfolio value, and then a firm-level sustainability.

Alliance portfolio value refers to the overall alliance capital and success that is more than the sum of the individual alliance performances [9]. The value of the alliance portfolio is linked to a firm’s dedicated capability to manage the whole alliance portfolio. From network theory and the system view, the dedicated alliance portfolio capability is an effective system for firms to coordinate multiple alliances across the boundary of alliances and monitor the strategic objectives and operational tasks. Following the recent research on the concept and framework of alliance portfolio management capability [14,15], we divide it into three dimensions: partnering proactiveness, relational governance, and portfolio coordination.

3.1.1. Partnering Proactiveness

Partnering proactiveness is defined as the capability of a firm to identify new opportunities for alliances and to respond to them [14]. The new opportunities include new projects that can bring value to a firm’s existing business and new partners with a high status and valuable and rare resources. Firms proactively exploring and exploiting new alliance opportunities are more likely to obtain competitive advantages compared to those that are inactive in partner pursuits [45]. Through providing “helpful partners”, partnering proactiveness makes entrepreneurial firms perform better in opportunity exploitation for two reasons. Firstly, entrepreneurial firms which actively seeking and selecting partners may know more about the partners such as their implicit knowledge and alliance intention, decreasing the risk of asymmetric information [46]. Secondly, a scarcity of potential high-quality alliance partners will be created by the proactive activity of entrepreneurial firms. In particular, when the “partner market” is an uncompetitive or rare market, partnering proactiveness may exaggerate the preemptive partner advantage [47], resulting in a first-mover advantage in alliance portfolio formation.

Being active in partnering activities is quite important for entrepreneurial firms in the context of high uncertainty. On the one hand, due to the limited time value of new opportunities, entrepreneurial firms should act on the opportunity as soon as possible [48]. Entrepreneurial firms which are resource-constrained and lack legitimacy cannot respond to new opportunities quickly with a high velocity. From an RBV (Resource Based View), valuable and rare resources of the partner are critical to trigger a sustainable advantage [49], which enables entrepreneurial firms to act on new opportunities in time and survive sustainably. On the other hand, through active partner selection, entrepreneurial firms can achieve a first-mover advantage on the partner-side, which guarantees high-status partner relationships and compatible resources. Meanwhile, a weakened risk of asymmetric information can improve the high-quality communication between entrepreneurial firms and their partners. Excellent partners and better communication with them will bring a better portfolio value and firm sustainability. Consequently, we hypothesize the following:

Hypothesis 1a (H1a).

The relationship between partnering proactiveness and firm sustainability is fully mediated by alliance portfolio performance.

3.1.2. Relational Governance

Relational governance refers to the relation-oriented commitment that a firm would like to make, which may lead to trustful and resilient relations [50]. Being cooperative in nature, the aim of relational governance is to bind together and lock in partners through informal interactions and relation-specific investments [51]. With the same interests in relationships, the capability of relational governance facilitates the establishment of strong ties between the focal firms and partners, and develops self-enforcing safeguards as the basis of alliance execution.

Relational governance is a solution to opportunism, which is the main risk that entrepreneurial firms often encounter when they initiate alliances. Given the liability of legitimacy, entrepreneurial firms do not have a high status or reputation in the market, which may induce opportunistic behavior from the partners [52]. The threat of opportunistic behavior in alliance portfolios can be minimized by relational governance [53]. Based on transaction cost theory, relational governance can develop trust, a high-quality information flow, and a joint-problem solution [54]. These factors may dispel opportunistic behavior and improve the cooperation among partners. Further, through relation-specific investment, relational governance also lowers the cost of contracting and monitoring [55], and increases the efficiency of alliance execution. It encourages partners to focus on resources and knowledge exchange which are fundamental for the value of the alliance portfolio. In sum, the capability of managing relations with partners will decrease the governance cost and facilitate partners to engage in cooperation. This will lead to an efficient alliance process and a high-quality alliance execution, which is associated with the sustainable performance of entrepreneurial firms. Consequently, we hypothesize the following:

Hypothesis 1b (H1b).

The relationship between relational governance and firm sustainability is fully mediated by alliance portfolio performance.

3.1.3. Portfolio Coordination

Different from partnering proactiveness and relational governance that are the fundamental capabilities of architecture construction (i.e., the partner structure and relations structure), portfolio coordination points to portfolio enhancing based on a certain structure [14]. Taking a holistic approach, portfolio coordination focuses on managing the synergy of multiple alliance activities and the mobilization of different resources from different partners [10]. Ozcan and Eisenhardt [9] argued that “Portfolios… have aggregate properties [synergies] that affect performance, but not meaningful for single ties”. Therefore, portfolio coordination is the capability of comprising complementary strategy, activity interaction, knowledge flow, etc., from the perspective of the portfolio instead of an atomistic dyad.

Portfolio coordination improves the interdependency effect, which is the core of an alliance portfolio. The extent of coordination across different alliances determines whether synergies can be stimulated and whether conflicts can be minimized. Synergies in portfolio comprise of the economy of scale and scope, knowledge flow, and resources complementarities [56,57]. Conflicts in portfolios include redundancies originating from resources similarities or overlapping competition between partners [58,59]. A high level of synergy and a low level of conflict makes the value created by the alliance portfolio greater than the sum of individual alliances, which is associated with the performance of firms.

Portfolio coordination can help entrepreneurial firms achieve high alliance portfolio value and improve their sustainability in survival and growth. For entrepreneurial firms, entrepreneurial activities or projects in the early stage are usually complex tasks because of their constrained resources. Thus, they need to mobilize a series of special organizations into a collective entity and create synergies across organizations [6]. Accordingly, inter-alliance coordination is necessary for entrepreneurial firms to manage a complex task in order to create synergistic value by coordinating alliance activities and knowledge flows in the portfolio. From synergy theory, a high level of synergy can motivate concerted actions between focal firms and their partners [57], which are helpful for dyadic cooperation and problem solving. Further, resource complementarities among multiple alliances will emerge through the focal firm’s coordinating activity, which ensures an abundant and differentiated resource pool as the basis for the alliance portfolio value [59]. In short, portfolio coordination enables entrepreneurial firms to maintain a high alliance portfolio level performance through synergy, which leads to firm sustainability. Consequently, we hypothesize the following:

Hypothesis 1c (H1c).

The relationship between portfolio coordination and firm sustainability is fully mediated by alliance portfolio performance.

3.2. The Moderation of the Power Distribution of the Board in the Mediation Effect

It has been established that network relationships originate from other relationships such as the board of directors in organizations [17]. From the perspective of “network pluralism” or “relational pluralism”, the relationship at the board level may influence inter-organizational relationship [60]. For example, Beckman et al. [17] argued that the social network of board members shapes the diversity of the alliance portfolio. Collins [61] found that TMT’s external social connection is related to the alliance portfolio diversity. However, these research articles focused on the structure of the network, such as the scale of the board or the diversity of the portfolio, with little attention on the content dimension such as the power distribution or on the capability of network management. We believe that the power distribution of the board of directors has a moderating effect on the relationship between the alliance portfolio management capability and sustainability.

Prior research pointed out that corporate governance should be applied in alliance portfolio management [19]. As a kind of strategic decision, alliance portfolio management should be discussed and approved by the board of directors given their service function based on steward theory [62]. From stewardship theory, the role of the board is not only to bring external information and potential connections and being conduits to divergent resources, but also to involve themselves in strategic management [63], such as fostering the capability of alliance managements. Rather than focus on the external social network of the board, we emphasize that how the power distribution of the board may influence the effect of the alliance portfolio management capability on the portfolio value and firm sustainability.

According to the power distribution of the board, we divided the board of directors into two types, that is, a centralized and decentralized board, according to the share that the board members have. The centralized board refers to the type of board in which the power is centralized with a certain board member, normally the chair of the board. The decentralized board refers to the type of board in which the power is shared among the board in a more equal manner. Based on the team theory, the power distribution in a team has a great impact on the operational efficiency of the team [64]. In the decentralization condition, a team has an ambiguous authority, leading to conflicts which may damage the team efficiency [65,66]. Thus, it is difficult to make strategic decisions quickly in a decentralized board, which results in complicated procedures and even chaos in decision making. Nevertheless, in a centralized board, the member who has the central power is more likely to influence others and enable the whole board to achieve common objectives and synergetic actions.

The power distribution of the board of directors may influence the function of the alliance portfolio management capability. Firstly, as far as a centralized board is concerned, a fast alliance portfolio decision is easy to make, which enhances the time value of the alliance opportunity that partnering proactiveness contains. New alliance opportunity seeking is sped up by a centralized board due to its fast decision-making process, which leads to better alliance portfolio value and firm sustainability. Further, relational governance and coordination can be implemented better in a centralized board since the board can input more managerial attention and resources into the alliance portfolio. Synergistic effects and board efficiency are more likely to emerge in a board under the control of a central chair, supporting relational governance and coordination in alliance management.

Secondly, a decentralized board may weaken the impact of the alliance portfolio management capability on the portfolio value and the firm’s sustainability. In a decentralized board, every board member would like to be involved in strategic decisions. Although this will enable the firm to enjoy the information and knowledge benefits from different board members, it slows down the decision-making that is important for entrepreneurial firms, especially in proactive partnering. Moreover, a decentralized board may separate the managerial attention and critical resources on relation-specific investment as well as on portfolio coordination activities. Accordingly, when the board is decentralized, partnering proactiveness may not help the entrepreneurial firm to explore new alliance opportunities as soon as possible and the weakened governance and coordination would not be able to enable the firm to improve its alliance relationships and cross-alliance synergies, which would damage the value of the alliance portfolio. Consequently, we hypothesize the following:

Hypothesis 2a (H2a).

The mediating relationship between partnering proactiveness, alliance portfolio value, and firm sustainability is moderated by the power distribution of the board. A centralized board may strengthen the mediating effect and a decentralized board may weaken the mediating effect.

Hypothesis 2b (H2b).

The mediating relationship between relational governance, alliance portfolio value, and firm sustainability is moderated by the power distribution of the board. A centralized board may strengthen the mediating effect and a decentralized board may weaken the mediating effect.

Hypothesis 2c (H2c).

The mediating relationship between portfolio coordination, alliance portfolio value, and firm sustainability is moderated by the power distribution of the board. A centralized board may strengthen the mediating effect and a decentralized board may weaken the mediating effect.

The theoretical framework is shown in Figure 1.

4. Methodology

4.1. Data and Sample

The data were collected as part of an ongoing construction of a dataset named CPSED II (Chinese Panel Study of Entrepreneurial Development), which targeted the New OTC Market as research samples consisted of archive and survey data. The dataset focused on the Software and Information Technology (code: I64) and Internet (code: I65) industries, as well as the traditional manufacturing (code: C) industry. These codes are from the “Guidelines for the Industry Classification of Listed Companies” published by the China Securities Regulatory Commission. According to the firm list published on the Web of National Equities Exchange and Quotations (www.neeq.com.cn), there were 1115 firms from the industry of I64 and I65, and 5592 firms from the manufacturing industry on the New OTC Market from 1 January 2013 to 31 March 2016.

Since the dataset on the manufacturing industry is in the process of a data check, we used the dataset on I64 and I65 as our sample. In the part of archive data, we selected 10 firms randomly to pretest the coding questionnaire and the other 1105 firms were entered into a formal coding process. Due to insufficient information of the prospectus and the mistakes in the coding process, 136 samples were eliminated. Thus, the dataset in I64 and I65 contained 969 firms. The source of the data included prospectuses for equity transfers, annual reports, and other announcements such as alliances. A total of 969 prospectuses and 1897 annual reports were coded in the dataset. By taking 10 indexes of the firms’ demographic characteristics as the standard to compare the samples in our dataset and those which were eliminated, there were no differences among these characteristics, suggesting that the variance of the total samples did not exist because of the sample elimination.

In the part of survey data from I64 and I65, we conducted a framework combing “offline contact” and “online questionnaire”, including 4 procedures, i.e., (1) mailing an invitation letter; (2) phone contact; (3) sending a questionnaire link; (4) filling out the questionnaires online. Given the difficulties in the CEO investigations, offline contact was very important in our survey, which improved the quality of our survey data. We conducted a pre-test of the questionnaire that included 11 interviewees on each survey question and, according to the response, we improved the design of the questionnaire in a follow-up formal survey. Then the survey team sent out 865 questionnaires from 8 November 2017 to 31 January 2018, after offline contact through phone calls. We successfully contacted 293 CEOs (including assistant general managers and secretaries of the board of directors (33.9%)). A total of 136 CEOs were willing to accept the investigation (46.4%) and 157 general managers refused (53.6%). Finally, the number of effective questionnaires was 101, achieving a response rate of 74.3%.

In addition to the coded data, we also adopted a public secondary dataset, including the corporate governance and performance dataset in China’s Stock Market and Accounting Research (CSMAR) database (http://www.gtarsc.com), which was regarded as one of the most reliable sources of information about listed Chinese firms. The CSMAR database provided the financial information on the Chinese stock market including the New OTC Market.

4.2. Measurement

4.2.1. Dependent Variable

A firm’s sustainability (FS) was the dependent variable in this study. It referred to the long-term profitability and sustaining competitiveness of a firm. There were different methods to measure it, among which, the Sustainable Growth Model of Van Horne and Higgins are widely used [67,68]. We followed Van et al. [69] by using the growth of profit and sales as indicators to measure a firm’s sustainability, which emphasized the dimension of sustainability on economic performance. Thus, the positive and higher growth of profit and sales indicated the increased sustainability of an entrepreneurial firm. The data on sustainability was collected from the CSMAR database on December 2017 (according to the annual reports).

4.2.2. Independent Variables

The alliance portfolio management capability included three dimensions—partnering proactiveness (PP), relational governance (RG), and portfolio coordination (PC)—which were measured by a multiple-items survey. The survey items were adapted from previous research on the alliance portfolio management capability [36]. The items are provided in Appendix A. We conducted an Exploratory Factor Analysis (EFA) on the survey items, see Table 1. The items for partnering proactiveness (items 1–5, α = 0.909), relational governance (items 6–10, α = 0.841), and portfolio coordination (items 11–15, α = 0.811) loaded on the relevant constructs instead of other factors in the measurement model, provided good reliability. We also conducted a Confirmative Factor Analysis (CFA) on this measurement. The CFA indicated a good fit for the measurement of the three dimensions; see Table 1. The data on the alliance portfolio management capability was from the survey on August 2017, which was ahead of the time that we measured the dependent variable.

4.2.3. Mediating Variable

We measured the alliance portfolio value (APV) using a four-item scale based on Schilke et al. [70]. The EFA and CFA showed that all four of the items for the alliance portfolio value of the focal firm were loaded on the same factor (items 16–18, α = 0.896). The data on the alliance portfolio value was from the survey. The items are provided in Appendix A.

4.2.4. Moderating Variable

We set the power distribution of the board of directors (PDB) as the moderator. We constructed the measurement of the power distribution of the board based on Finkelstein’s structural power model [71], which was calculated by the difference between the maximum and the minimum share of the board of directors. We first coded the share of each director in the board and calculated the difference of the maximum value and the minimum value. Accordingly, to the mean of the share difference in each board, we coded 1 when the difference was higher than the mean and coded 0 when the difference was lower than the mean. The greater the difference, the more concentrated and the more powerful the board was. The data on the power distribution of the board were from the archive data. The former archive data were collected by the end of 2016. We coded the characteristics of the board, including the power distribution by the end of 2016 and 2017, according to the annual reports as a supplement of the dataset. After the changes on the board from 2013 to 2017, the data showed the final power distribution of the board on 2017.

4.2.5. Control Variables

We applied five control variables in this study. Three of them are similar to Castro et al. [15]. The first two control variables were associated with firm size, which was measured by the total capital (TC) and the number of employees (EM). There were two reasons for selecting the firm size as a control variable. On the one hand, large firms might possess more resources to establish, maintain, and manage an alliance portfolio compared to small entrepreneurial firms, which leads to a high alliance portfolio value. On the other hand, large firms had a better market position and competitive advantages to ensure their sustainable growth. Considering this measurement, different size measurements capture different aspects of the firm size, which shows different implications in performance. The total capital measures the resources of a firm and the number of employees focuses on the human resources that can be invested in the business process [72].

We controlled the firm age (AG) in this study, which was measured by the time scope from the year the firm started to 2017. Firms that had started a relatively long time agi may have had more experience in alliance portfolio management, resulting in a higher alliance portfolio value. Furthermore, older firms might enjoy a better position and reputation in the market, which would improve the possibility of their sustainable survival.

From the perspective of the board, we controlled two variables associated with the attributes of the board. The first is the Board Size (BS), measured by the number of board members. A higher number of board members might bring more resources to the firm and result in a better alliance portfolio performance, as well as better financial outcomes. The second is the diversity (DI) of knowledge in the board. This was measured by the difference of the majors that the directors had completed during their college year. We applied the Blau index to calculate the diversity of the majors in the board. A more knowledge-diversified board might bring different knowledge and information to the alliance portfolio, which would inspire new and effective ideas in the alliance management. Previous research suggested that the human capital of the boards, including managerial experience, could be important [73,74]. Therefore, we followed Beckman et al. [17] in measuring the human capital of the board as a control variable.

Table 2 is the measurements of the variables.

4.3. Common Method Bias

In order to minimize the effect of common method bias, we combined first-hand data and second-hand data in our design. The independent variables and mediating variable used first-hand data from our survey. The dependent variable used second-hand data from the CSMAR database in China as well as from our archive dataset. Consequently, there were no common method biases in this study.

5. Data Analysis and Findings

We applied the data analytical approach and PROCESS macro developed by Preacher and Hayes [75] to estimate the mediation model (H1a–H1c) and moderating mediation model (H2a–H2c). The SPSS syntax contained in the PROCESS macro provided an alternative bootstrap test of the mediation effect, which is more rigorous and powerful than Sobel’s test [75]. The confidence interval for mediators for 5000 resamples is 95%.

5.1. Descriptive Statistics

The descriptive statistics are given in Table 3. According to the geographic distribution, our samples covered different regions in China.

A total of 43.6% of the sample was from the area around Beijing, including the Tianjin and Hebei provinces, 20% was from the Yangtze River Delta, and 18% was from the Pearl River Delta. All of these areas are developed regions in China. The lowest portion of the sample was from the northeast area (3%), which represented the developing region of China. As far as the age of the firms gp, 47% of the sample firms were under 8 years. According to the time of IPO, 75.2% of sample firms were 3 years and less in the New OTC Market, 23.8% of the firms were more than 4 years, but less than 6 years old. This showed that our sample was young according to their IPO time. They were particularly more entrepreneurial in the New OTC Market, which was a new attempt with different requirements from the Main Board in the Chinese stock market. Due to the scale of the board of directors, 79.3% of the sample had a small board; and only 13.9% had a relatively big board of more than 7 members. In addition, firm size in terms of the total capital and the number of employees indicated that our sample of entrepreneurial firms had a small board of directors.

The correlation statistics are provided in Table 4. They suggested the significant correlations between the independent variables and the dependent variables, with no multi-collinearity problems.

5.2. Findings

Table 5 shows the results of the tests of the mediation effects. When the alliance portfolio value was introduced as a mediator, partnering proactiveness (beta = 0.0073, LLCI: −0.0496, ULCI: 0.0642) and relational governance (beta = 0.0051, LLCI: −0.0582, ULCI: 0.0685) no longer had a significant direct effect on the firms’ sustainability. Here, beta refers to a regressive coefficient. LLCI refers to a lower level of the confidence interval and ULCI refers to an upper level of the confidence interval. If the confidence interval (LLCI, ULCI) includes 0, it shows the coefficient as not significant; if the confidence interval excludes 0, the coefficient is significant [76]. However, there was an indirect effect between these two dimensions and the firms’ sustainability (partnering proactiveness: beta = 0.0412, LLCI: 0.0112, ULCI: 0.1031; relational governance: beta = 0.0383, LLCI: 0.0135, ULCI: 0.0916). Based on the definition of the mediation effect, the independent variable (X) affects the dependent variable (Y) through the mediator (M). A full mediation effect means that the direct effect from X to Y no longer exists when M is introduced [77]. This means that the relationship between partnering proactiveness, relational governance, and the firms’ sustainability was fully mediated by the alliance portfolio value. Thus, H1a and H1b were supported.

In contrast, the portfolio coordination no longer had a significant direct effect on the firms’ sustainability (beta = 0.0546, LLCI: −0.0061, ULCI: 0.1153) when the alliance portfolio value was introduced as a mediator. There was no significant indirect effect in this relationship either (beta = 0.0301, LLCI: −0.0022, ULCI: 0.0879). Thus, the alliance portfolio value did not play a mediating role in the relationship between the portfolio coordination and firms’ sustainability. Consequently, H1c was not supported.

Table 6 shows the moderating mediation effects. Based on the contingency theory, the moderation and mediation effects are integrated when the path contains a mediation model that is theorized to vary due to the different level of the moderator [78]. When the power distribution of the board was introduced as a moderator, partnering proactiveness (beta = 0.0073, LLCI: −0.0496, ULCI: 0.0642) and relational governance (beta = 0.0051, LLCI: −0.0582, ULCI: 0.0685) no longer had a significant direct effect on the firms’ sustainability. However, at different levels of the board’s power distribution, the mediating effect of partnering proactiveness (beta = 0.0082, LLCI: 0.0175, ULCI: 0.0512) and relational governance (beta = 0.0259, LLCI: 0.0000, ULCI: 0.0906) on the alliance portfolio value and the firms’ sustainability began to exist. This means that when the power distribution of the board took a different value, the above mediating effects both began existed. Further, the mediation effect was larger when the board of directors had a centralized power compared to a decentralized power. In sum, under the moderation of the power distribution of the board, the impact of partnering proactiveness and the relational governance on the firms’ sustainability was fully mediated by the alliance portfolio value. Accordingly, H2a and H2b were supported.

In contrast, when the power distribution of the board took on a different value, the portfolio coordination no longer had a significant direct effect on the firms’ sustainability (beta = 0.0546, LLCI: −0.0061, ULCI: 0.1153), neither was there a mediation effect on the firms’ sustainability (beta = 0.0008, LLCI: −0.0314, ULCI: 0.0155). Consequently, H2c was not supported.

5.3. Sensitivity Analysis

We conducted a sensitivity analysis using the growth of sales as the measurement of sustainability. Using the independent variables of this study, we found the same results. When the power distribution of the board was introduced as a moderator, the partnering proactiveness (beta = 0.3833, LLCI: −0.6214, ULCI: 0.1453) and relational governance (beta = 0.5754, LLCI: −0.3230, ULCI: 0.4737) no longer had a significant direct effect on the firms’ sustainability. However, at different values of the board’s power distribution, the mediating effect of partnering proactiveness (beta = 0.1592, LLCI: 0.1743, ULCI: 0.8575) and relational governance (beta = 0.3389, LLCI: 0.0807, ULCI: 0.1425) on the alliance portfolio value and the firms’ sustainability both existed. This means that under the moderation of the power distribution of the board, the impact of partnering proactiveness and relational governance on the firms’ sustainability was fully mediated by the alliance portfolio value. Accordingly, H2a and H2b were supported. In contrast, when the power distribution of the board took on a different value, portfolio coordination no longer had a significant direct effect on the firms’ sustainability (beta = 0.3980, LLCI: −0.4802, ULCI: 0.2761), neither did the mediation effect on the firms’ sustainability (beta = 0.0229, LLCI: −0.3270, ULCI: 0.9770). Consequently, H2c was not supported. Additionally, the robustness of our results was confirmed (the respective tables are available upon request).

5.4. Endogeneity Analysis

We considered the endogeneity issue in two ways. From the theoretical point of view, based on the Dynamic Capability Theory, the capability is triggered by cognitive elements such as knowledge or mindset, and by behavioral elements such as learning [79]. In this sense, the alliance portfolio management capability might originate from organizational knowledge or experience focusing on alliance portfolio management, which has been proven in prior research. Meanwhile, the sustainable performance of firms does not inevitably lead to more knowledge or better behavior in alliance portfolio management. Consequently, there is no strong causality between sustainability and the alliance portfolio management capability.

From the statistic perspective, we conducted an endogeneity analysis using the models containing lagged dependent variables based on the work by Li [80]. This model was introduced to test whether the alliance portfolio management capability had an effect on the firms’ future sustainability. Since the firms’ sustainability had the characteristics of a time series, we introduced the firms’ sustainability in the following year (August 2018, according to the semiannual report). We found the same results, which meant that there was no serious endogeneity problem. When the alliance portfolio value was introduced as a mediator and the power distribution of the board was introduced as a moderator, partnering proactiveness (beta = 0.0143, LLCI: −0.0140, ULCI: 0.0425) and relational governance (beta = 0.0051, LLCI: −0.0270, ULCI: 0.0372) no longer had a significant direct effect on the firms’ sustainability. However, at different board power distribution values, the mediating effect of partnering proactiveness (beta = 0.0009, LLCI: 0.0029, ULCI: 0.0141) and relational governance (beta = 0.0048, LLCI: 0.0009, ULCI: 0.0262) on the alliance portfolio value and the firms’ sustainability still existed. This meant that under the moderation of the power distribution of the board, the impact of partnering proactiveness and relational governance was fully mediated by the alliance portfolio value.

6. Conclusions and Discussion

6.1. Conclusions

This work has examined the impact of the alliance portfolio management capability on the alliance portfolio value and the firms’ sustainability under the condition of the power distribution of the board of directors.

Our study provided evidence that entrepreneurial firms should manage their alliance portfolio well in order to grow sustainably. The capability of alliance portfolio management was recognized as a significant organizational ability for managing multiple alliances. We conceptualize the alliance portfolio management capability into three dimensions: partnering proactiveness, relational governance, and portfolio coordination [14,15]. We found that partnering proactiveness and relational governance have a significant positive impact on the firms’ sustainability and that it was fully mediated by the alliance portfolio value. This study is in line with our prior study, which revealed the positive role of the alliance portfolio management capability on performance at the portfolio level [18]. What is more, this study discovered the mediating function of the portfolio value in the relationship between the portfolio management capability and the firms’ sustainability.

This study also revealed the moderation effect of the board of directors in terms of its power distribution. Linking the board of directors with alliance portfolio management is in accordance with the research trend to order to analyze the alliance portfolio management from the perspective of the corporate government [11]. We found that the power distribution of the board moderates the impact of partnering proactiveness and relational governance on the portfolio value and the firms’ sustainability. This shows that a centralized board can improve the role of proactiveness and governance in the alliance portfolio in terms of the focused attention and managerial resources input into the alliance portfolio management process. A decentralized board might hinder the decision efficiency of proactiveness and governance, which results in a worse portfolio performance and firms’ sustainability in the context of entrepreneurship, where the time for opportunity exploitation is limited. Accordingly, the corporate governance structure provides a better explanation for the role of the alliance portfolio management capability.

We have not found the mediation of the alliance portfolio value in the relationship between the portfolio coordination and the firms’ sustainability. The main reason for this comes from the context of entrepreneurship. Different from established firms, it is hard for entrepreneurial firms to cultivate coordination capability across multiple alliances due to their insufficient resources. Compared to the other two dimensions of capability that focus more on alliance partner seeking and related investment in the alliance level, portfolio coordination focuses on the cross-alliance management that needs the commitment of more managerial resources and increases the management cost. Accordingly, a high cost of coordination may decrease the entrepreneurial firms’ performance on the alliance portfolio value acquisition and sustainability development.

Within the context of practical implications, this study contributes to the reflection of alliance portfolio management. In general, our conclusions of the positive impact of the alliance portfolio management capability on sustainability through the value improvement of the alliance portfolio enables entrepreneurial firms to make more investments through alliance portfolio management. For owners in entrepreneurial firms, in order to survive or grow sustainably in the early stage, they should be actively involved in alliance portfolio management. In particular, they should be actively participating in partner seeking and relational governance in order to manage the alliance portfolio as a whole and to minimize the coordination cost. As for the board of directors, a centralized power distribution would be better for entrepreneurial firms in the early stage in order to realize the value of the alliance portfolio management capability. In practice, the chairman of the board needs to hold more power and use said power to improve the capability building in the alliance portfolio management. The result is in compliance with the suggestions of Hoffman [16] and Castro et al. [15], that the board of directors should be involved in the alliance portfolio management.

6.2. Discussion

The conclusion of managing multiple alliances simultaneously based on the alliance capability contributes to the strategic alliance research in three ways. Firstly, in contrast to prior research focusing on dyadic alliances from the atomistic perspective, we analyzed the alliance capability from the portfolio perspective, which is the accumulation of multiple alliances. The difference between a single alliance and an alliance portfolio is the interdependencies among the multiple alliances, which make the management of the alliance portfolio more difficult and costly. As recent research transformed the atomistic unit into a portfolio unit, meanwhile, firms have made efforts to manage the cross-boundary alliances in practice. The capability to manage the portfolio of diversified partnerships assumes higher relevance in explaining the variance of the alliance portfolio outcomes and the firm’s performance. Accordingly, our study investigated the capability of managing cross-boundary alliances, which highlights the strategic importance of leveraging multiple partners’ resources and governing a portfolio of relationships.

Secondly, compared to the existing alliance portfolio literature that focused on the emergence and configuration of the alliance portfolio, we made contributions to alliance portfolio management. The previous research has made more progress on the structure of the alliance portfolio and their impact on performance. Little is known about how to manage such a portfolio with a complicated structure. Some studies pointed to the firms’ alliancing routines, behavior, and process. Our understanding of what underlies alliance portfolio management is capability, in accordance with the research of Sarkar et al. [14]. Based on this, we make a contribution by investigating how alliance portfolio management capability strengthens the value of the alliance portfolio, which, in turn, helps entrepreneurial firms to grow sustainably.

Thirdly, this study provides an in-depth understanding of the effect of the alliance portfolio management capability in entrepreneurial firms. Although research on the alliance portfolio management capability is growing recently, little is known in the context of entrepreneurship. Facing great uncertainty with regards to survival and early growth, entrepreneurial firms have a great demand for resources in order to support growth. Since our study moves towards, for a better understanding of alliance portfolios, in terms of the network as resource repositories, it is necessary for entrepreneurial firms to understand the importance of alliance portfolio management as a valuable tool for acquiring resources. Just like Pettigrew et al. [80] argued, engaging in networks and fostering the capability to manage that “are now seen to be key additional factors in explaining…‘why do firms differ in their profitability’”.

Our study also provides a great understanding of the role of the board in entrepreneurial firms. From the perspective of the service function, the board of directors may be involved in strategic decision-making such as determining how to manage the strategic alliances. A centralized board controlled by a chairman can improve the effect of the alliance portfolio management capability since a centralized board leads to a fast decision. Moreover, in contrast to the literature on corporate governance that focuses on demographics and the structure of the board, we investigated the power distribution of the board, which shows the real function of the board.

Although our dataset is from China, our conclusions can be applied in other countries, especially developing countries. In a transition economy such as China, entrepreneurial firms face more challenges due to the weak market structure, the absence of support from formal institutions, and the coexistence of resource allocation by market forces and government agencies [81]. An incomplete market transition leads to difficulties in purchasing resources directly from the market and to ambiguous information of where and how to acquire resources for growth. In this sense, strategic alliances provide a valuable and practical way for entrepreneurial firms to acquire critical resources. Moreover, entrepreneurial firms need to foster the alliance portfolio management capability to select, leverage, and mobilize diversified resources from different partners.

6.3. Limitations

Despite the advantages of a research design that combined both first-hand data and second-hand data on entrepreneurial firms, there are several limitations.

Firstly, our sample is from the Information Technology and Internet industry, which may have a bias in certain industries. Although a single industry study has benefits on theory generation in the context of a single set of technical conditions, it brings some open questions for future research. For example, what are the dimensions of the alliance portfolio management capability or how is the effect of the capability on the firms’ sustainability in other industries, such as the traditional manufacturing industry, in which alliances are more prevalent and complicated. It is important to understand the structure of an industry to analyze the structure of the alliance portfolio and the portfolio management capability. Hence, it is recommended that future efforts should be made to expand the sample size across industries in order to test the present model in different contexts.

Secondly, the role of geographic factors has not been tested in this study. Our data is from China, a big country with lots of regions that are developing differently. A total of 43.6% of entrepreneurial firms studied in this work were founded in the region around Beijing. As they are located in the capital of China, they have abundant political resources that help them to establish political connections which are valuable for alliance portfolio formations. 38% of entrepreneurial firms in this work are from more developed areas along the coast, where clusters of venture capitalists, suppliers, and other service entities exist. These different regional conditions foster different alliance portfolios and different alliance portfolio management capabilities for firms. Accordingly, there is a question of whether a region-specific path dependency exists in the context of alliance portfolio management. Future efforts should be made to analyze the impact of geographic characteristics on alliance portfolio management.

Author Contributions

W.H. developed the research model, analyzed the data and wrote this paper; Y.D. designed the questionnaire, reviewed and edited this paper; F.-W.C. contributed to data collection and literature review.

Funding

This research was funded by the National Natural Science Foundation of China, grant number (71002007; 71772019; 71732004; 71532005).

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

{kind=link}

Table A1.

The items of dependent variable and independent variables.

| Construct | Indicators | Sources |

|---|---|---|

| Partnering proactiveness | We actively monitor our environment to identify collaboration or alliance opportunities. | Adapted from Sarker et al. 2009; Castro, etc. 2015 |

| We routinely gather information about potential partners from diverse forums. | ||

| We are alert to market developments that create potential alliance opportunities. | ||

| We strive to preempt our competition by entering into alliances with the key firms before they can. | ||

| We often take the initiative in approaching firms with alliance proposals. | ||

| Relational governance | Staying together during adversities/challenges is very important in our relationships. | Adapted from Sarker et al. 2009; Castro, etc. 2015 |

| We endeavor to build relationships based on mutual trust and commitment. | ||

| We strive to be flexible and accommodate partners when problems/needs arise.When disagreements arise in our alliances, we usually reassess facts to try and reach a mutually satisfactory compromise.Information exchange with partners takes place frequently and informally, and not only according to prespecified agreements. | ||

| Portfolio coordination | We consider our alliances as a portfolio that requires overall coordination, and not as independent, one-off arrangements. | Adapted from Sarker et al. 2009; Castro, etc. 2015 |

| Our activities across different alliances are well coordinated. | ||

| We systematically coordinate our strategies across different alliances. | ||

| We have processes to systematically transfer knowledge across alliance partners. | ||

| Managers from different departments meet periodically to examine how we can create synergies across our alliances. | ||

| Alliance portfolio value | Overall we are satisfied with the performance of our alliances. Generally our alliances satisfy our initial objectives. | Adapted from Schilke et al. 2010 |

| We are satisfied with the knowledge accumulated from participating in alliances. | ||

| Our alliances have been profitable investments. |

References

- Brüderl, J.; Preisendörfer, P.; Ziegler, R. Survival Chances of Newly Founded Business Organizations. Am. Sociol. Rev. 1992, 57, 227–242. [Google Scholar] [CrossRef]

- Stinchcombe, A.L. Social Structure and Organization. In Handbook of Organization; March, J.G., Ed.; Rand McNally: Chicago, IL, USA, 1965; Volume 7, pp. 142–193. [Google Scholar]

- Chen, F.W.; Fu, L.W.; Wang, K. The Influence of Entrepreneurship and Social Networks on Economic Growth—From a Sustainable Innovation Perspective. Sustainability 2018, 10, 2510. [Google Scholar] [CrossRef]

- Li, D. Multilateral R&D Alliances by New Ventures. J. Bus. Ventur. 2013, 28, 241–260. [Google Scholar]

- Jiang, R.J.; Tao, Q.T.; Santoro, M.D. Alliance Portfolio Diversity and Firm Performance. Strat. Manag. J. 2010, 31, 1136–1144. [Google Scholar] [CrossRef]

- Anand, B.N.; Khanna, T. Do Firms Learn to Create Value? The Case of Alliances. Strat. Manag. J. 2000, 21, 295–315. [Google Scholar] [CrossRef]

- Baum, J.A.; Calabrese, T.; Silverman, B.S. Don’t Go It Alone: Alliance Network Composition and Startups’ Performance in Canadian Biotechnology. Strat. Manag. J. 2000, 21, 267–294. [Google Scholar] [CrossRef]

- Schreiner, M.; Kale, P.; Corsten, D. What Really is Alliance Management Capability and How does It Impact Alliance Outcomes and Success? Strat. Manag. J. 2009, 30, 1395–1419. [Google Scholar] [CrossRef]

- Ozcan, P.; Eisenhardt, K.M. Origin of Alliance Portfolios: Entrepreneurs, Network Strategies, and Firm Performance. Acad. Manag. J. 2009, 52, 246–279. [Google Scholar] [CrossRef]

- Lavie, D. Alliance Portfolios and Firm Performance: A Study of Value Creation and Appropriation in the US Software Industry. Strat. Manag. J. 2007, 28, 1187–1212. [Google Scholar] [CrossRef]

- Wassmer, U. Alliance Portfolios: A Review and Research Agenda. J. Manag. 2010, 36, 141–171. [Google Scholar] [CrossRef]

- Steensma, H.K.; Marino, L.K.; Weaver, K.M.; Dickson, P.H. The Influence of National Culture on the Formation of Technology Alliances by Entrepreneurial Firms. Acad. Manag. J. 2000, 43, 951–973. [Google Scholar]

- Wassmer, U.; Dussauge, P. Network Resource Stocks and Flows: How Do Alliance Portfolios Affect the Value of New Alliance Formations? Strat. Manag. J. 2012, 33, 871–883. [Google Scholar] [CrossRef]

- Sarkar, M.B.; Aulakh, P.S.; Madhok, A. Process Capabilities and Value Generation in Alliance Portfolios. Organ. Sci. 2009, 20, 583–600. [Google Scholar] [CrossRef]

- Castro, I.; Galán, J.L.; Casanueva, C. Management of Alliance Portfolios and the Role of the Board of Directors. J. Bus. Econ. Manag. 2016, 17, 215–233. [Google Scholar] [CrossRef]

- Hoffmann, W.H. How to Manage a Portfolio of Alliances. Long Range Plan. 2005, 38, 121–143. [Google Scholar] [CrossRef]

- Beckman, C.M.; Schoonhoven, C.B.; Rottner, R.M.; Kim, S.-J. Relational Pluralism in De Novo Organizations: Boards of Directors as Bridges or Barriers to Diverse Alliance Portfolios? Acad. Manag. J. 2014, 57, 460–483. [Google Scholar] [CrossRef]

- Heimeriks, K.H.; Duysters, G. Alliance Capability as a Mediator between Experience and Alliance Performance: An Empirical Investigation into the Alliance Capability Development Process. J. Manag. Stud. 2007, 44, 25–49. [Google Scholar] [CrossRef]

- Reuer, J.J.; Ragozzino, R. Agency Hazards and Alliance Portfolios. Strat. Manag. J. 2006, 27, 27–43. [Google Scholar] [CrossRef]

- Reynolds, P.; Miller, B. New Firm Gestation: Conception, Birth, and Implications for Research. J. Bus. Ventur. 1992, 7, 405–417. [Google Scholar] [CrossRef]

- Shane, S.; Cable, D. Network Ties, Reputation, and the Financing of New Ventures. Manag. Sci. 2002, 48, 364–381. [Google Scholar] [CrossRef] [Green Version]

- Davidsson, P.; Gordon, S.R. Panel Studies of New Venture Creation: A Methods-focused Review and Suggestions for Future Research. Small Bus. Econ. 2012, 39, 853–876. [Google Scholar] [CrossRef] [Green Version]

- Carter, N.M.; Williams, M.; Reynolds, P.D. Discontinuance among New Firms in Retail: The Influence of Initial Resources, Strategy, and Gender. J. Bus. Ventur. 1997, 12, 125–145. [Google Scholar] [CrossRef]

- Dimov, D. Nascent Entrepreneurs and Venture Emergence: Opportunity Confidence, Human Capital, and Early Planning. J. Manag. Stud. 2010, 47, 1123–1153. [Google Scholar] [CrossRef]

- Liao, J.; Welsch, H. Roles of Social Capital in Venture Creation: Key Dimensions and Research Implications. J. Small Bus. Manag. 2005, 43, 345–362. [Google Scholar] [CrossRef]

- Guo, C.; Miller, J.K. Guanxi Dynamics and Entrepreneurial Firm Creation and Development in China. Manag. Organ. Rev. 2010, 6, 267–291. [Google Scholar] [CrossRef]

- Lichtenstein, B.B.; Carter, N.M.; Dooley, K.J. Gartner, W.B. Complexity Dynamics of Nascent Entrepreneurship. J. Bus. Ventur. 2007, 22, 236–261. [Google Scholar] [CrossRef]

- Lu, J.; Tao, Z. Determinants of Entrepreneurial Activities in China. J. Bus. Ventur. 2010, 25, 261–273. [Google Scholar] [CrossRef] [Green Version]

- Marino, L.; Strandholm, K.; Steensma, H.K.; Weaver, K.M. The Moderating Effect of National Culture on the Relationship between Entrepreneurial Orientation and Strategic Alliance Portfolio Extensiveness. Entrep. Theory Pract. 2002, 26, 145–160. [Google Scholar] [CrossRef]

- Kale, P.; Singh, H. Managing Strategic Alliances: What Do We Know Now, and Where Do We Go from Here? Acad. Manag. Perspect. 2009, 45–62. [Google Scholar] [CrossRef]

- Hoang, H.; Rothaermel, F.T. The Effect of General and Partner-specific Alliance Experience on Joint R&D Project Performance. Acad. Manag. J. 2005, 48, 332–345. [Google Scholar]

- Kale, P.; Dyer, J.H.; Singh, H. Alliance Capability, Stock Market Response, and Long-term Alliance Success: The Role of the Alliance Function. Strat. Manag. J. 2002, 23, 747–767. [Google Scholar] [CrossRef]

- Lichtenthaler, U. Determinants of Absorptive Capacity: The Value of Technology and Market Orientation for External Knowledge Acquisition. J. Bus. Ind. Mark. 2016, 31, 600–610. [Google Scholar] [CrossRef]

- Haider, S.; Mariotti, F. The Orchestration of Alliance Portfolios: The Role of Alliance Portfolio Capability. Scand. J. Manag. 2016, 32, 127–141. [Google Scholar] [CrossRef]

- Castro, I.; Roldán, J.L. Alliance Portfolio Management: Dimensions and Performance. European Manag. Rev. 2015, 12, 63–81. [Google Scholar] [CrossRef]

- Hoetker, G.; Mellewigt, T. Choice and Performance of Governance Mechanisms: Matching Alliance Governance to Asset Type. Strat. Manag. J. 2009, 30, 1025–1044. [Google Scholar] [CrossRef]

- De Vries, J.; Schepers, J.; Van Weele, A.; Van der Valk, W. When Do They Care to Share? How Manufacturers Make Contracted Service Partners Share Knowledge. Ind. Mark. Manag. 2014, 43, 1225–1235. [Google Scholar] [CrossRef]

- Tihanyi, L.; Ellstrand, A.E. The Involvement of Board of Directors and Institutional Investors in Investing in Transition Economies: An Agency Theory Approach. J. Int. Manag. 1998, 4, 337–351. [Google Scholar] [CrossRef]

- Salancik, G.R.; Pfeffer, J. Who Gets Power and How They Hold on to it: A Strategic- contingency Model of Power. Organ. Dyn. 1977, 5, 3–21. [Google Scholar] [CrossRef]

- Baysinger, B.D.; Kosnik, R.D.; Turk, T.A. Effects of Board and Ownership Structure on Corporate R&D Strategy. Acad. Manag. J. 1991, 34, 205–214. [Google Scholar]

- Xue, Y. Make or Buy New Technology: The Role of CEO Compensation Contract in a Firm’s Route to Innovation. Rev. Account. Stud. 2007, 12, 659–690. [Google Scholar] [CrossRef]

- Su, Y.; Xu, D.; Phan, P.H. Principal-Principal Conflict in the Governance of the Chinese Public Corporation. Manag. Organ. Rev. 2008, 4, 17–38. [Google Scholar] [CrossRef]

- Kogut, B. The Stability of Joint Ventures: Reciprocity and Competitive Rivalry. J. Ind. Econ. 1989, 38, 183–198. [Google Scholar] [CrossRef]

- Simonin, B.L. The Importance of Collaborative Know-how: An Empirical Test of the Learning Organization. Acad. Manag. J. 1997, 40, 1150–1174. [Google Scholar]

- Newbert, S.L.; Tornikoski, E.T. Supporter Networks and Network Growth: A Contingency Model of Organizational Emergence. Small Bus. Econ. 2012, 39, 141–159. [Google Scholar] [CrossRef]

- Phillips, N.; Tracey, P.; Karra, N. Building Entrepreneurial Tie Portfolios through Strategic Homophily: The Role of Narrative Identity Work in Venture Creation and Early Growth. J. Bus. Ventur. 2013, 28, 134–150. [Google Scholar] [CrossRef]

- Sarkar, M.B.; Echambadi, R.; Cavusgil, S.T.; Aulakh, P.S. The Influence of Complementarity, Compatibility, and Relationship Capital on Alliance Performance. J. Acad. Mark. Sci. 2001, 29, 358–373. [Google Scholar] [CrossRef]

- Davidsson, P. Entrepreneurial Opportunities and the Entrepreneurship Nexus: A Re-conceptualization. J. Bus. Ventur. 2015, 30, 674–695. [Google Scholar] [CrossRef]

- Barney, J.B.; Zhang, S. The Future of Chinese Management Research: A Theory of Chinese Management Versus a Chinese Theory of Management. Manag. Organ. Rev. 2009, 5, 15–28. [Google Scholar] [CrossRef]

- Dyer, J.H.; Singh, H. The Relational View: Cooperative Strategy and Sources of Interorganizational Competitive Advantage. Acad. Manag. Rev. 1998, 23, 660–679. [Google Scholar] [CrossRef]

- Riordan, M.H.; Williamson, O.E. Asset Specificity and Economic Organization. Int. J. Ind. Organ. 1985, 3, 365–378. [Google Scholar] [CrossRef]

- Navis, C.; Glynn, M.A. How New Market Categories Emerge: Temporal Dynamics of Legitimacy, Identity, and Entrepreneurship in Satellite Radio, 1990–2005. Adm. Sci. Q. 2010, 55, 439–471. [Google Scholar] [CrossRef]

- Poppo, L.; Zenger, T. Do Formal Contracts and Relational Governance Function as Substitutes or Complements? Strat. Manag. J. 2002, 23, 707–725. [Google Scholar] [CrossRef]

- Uzzi, B. The Sources and Consequences of Embeddedness for the Economic Performance of Organizations: The Network Effect. Am. Sociol. Rev. 1996, 61, 674–698. [Google Scholar] [CrossRef]

- Williamson, O.E. The Theory of the Firm as Governance Structure: From Choice to Contract. J. Econ. Perspect. 2002, 16, 171–195. [Google Scholar] [CrossRef] [Green Version]

- Powell, W.W.; Koput, K.W.; Smith-Doerr, L. Interorganizational Collaboration and the Locus of Innovation: Networks of Learning in Biotechnology. Adm. Sci. Q. 1996, 41, 116–145. [Google Scholar] [CrossRef]

- Parise, S.; Casher, A. Alliance Portfolios: Designing and Managing Your Network of Business-partner Relationships. Acad. Manag. Perspect. 2003, 17, 25–39. [Google Scholar] [CrossRef]

- Gimeno, J. Competition Within and Between Networks: The Contingent Effect of Competitive Embeddedness on Alliance Formation. Acad. Manag. J. 2004, 47, 820–842. [Google Scholar]

- Vassolo, R.S.; Anand, J.; Folta, T.B. Non-additivity in Portfolios of Exploration Activities: A Real Options-based Analysis of Equity Alliances in Biotechnology. Strat. Manag. J. 2004, 25, 1045–1061. [Google Scholar] [CrossRef]

- Carpenter, M.A.; Westphal, J.D. The Strategic Context of External Network Ties: Examining the Impact of Director Appointments on Board Involvement in Strategic Decision Making. Acad. Manag. J. 2001, 44, 639–660. [Google Scholar] [Green Version]

- Collins, J.D. Social Capital as a Conduit for Alliance Portfolio Diversity. J. Manag. Issues 2013, 25, 62–78. [Google Scholar]

- Hillman, A.J.; Dalziel, T. Boards of Directors and Firm Performance: Integrating Agency and Resource Dependence Perspectives. Acad. Manag. Rev. 2003, 28, 383–396. [Google Scholar] [CrossRef] [Green Version]

- Garg, S. Venture Boards: Distinctive Monitoring and Implications for Firm Performance. Acad. Manag. Rev. 2013, 38, 90–108. [Google Scholar] [CrossRef]

- Halevy, N.Y.; Chou, E.D.; Galinsky, A. A Functional Model of Hierarchy: Why, How, and When Vertical Differentiation Enhances Group Performance. Organ. Psychol. Rev. 2011, 1, 32–52. [Google Scholar] [CrossRef]

- Finkelstein, S.; Mooney, A.C. Not the Usual Suspects: How to Use Board Process to Make Boards Better. Acad. Manag. Perspect. 2003, 17, 101–113. [Google Scholar] [CrossRef]

- Christie, A.M.; Barling, J. Beyond Status: Relating Status Inequality to Performance and Health in Teams. J. Appl. Psychol. 2010, 95, 920–934. [Google Scholar] [CrossRef] [PubMed]

- Higgins, R.C. How Much Growth can a Firm Afford? Financ. Manag. 1977, 6, 7–16. [Google Scholar] [CrossRef]

- Van Horne, J.C. Sustainable Growth Modeling. J. Corp. Financ. 1988, 1, 19–24. [Google Scholar]

- Van Horne, J.C.; Frayret, J.; Poulin, D. Creating Value with Innovation: From Center of Expertise to the Forest Products Industry. For. Policy Econ. 2006, 8, 751–761. [Google Scholar] [CrossRef]

- Schilke, O.; Goerzen, A. Alliance Management Capability: An Investigation of the Construct and its Measurement. J. Manag. 2010, 36, 1192–1219. [Google Scholar] [CrossRef]

- Finkelstein, S. Power in Top Management Teams: Dimensions, Measurement, and Validation. Acad. Manag. J. 1992, 35, 505–538. [Google Scholar]