1. Introduction

The business environment has become dynamic and has experienced a rapid shift due to the introduction of new technologies and innovations, together with increased demand from customers. With this advancement of information and communication technology (ICT) and the advent of 3G and 4G services by telecom companies, mobile technology has become an integral part of our everyday human life. Mobile services have been introduced into various areas like banking, commerce, government, and healthcare [

1,

2,

3]. From this perspective, a bibliometric analysis recently performed by Hew [

4] showed increased interest in the scientific world in mobile technology, and suggested avenues for the future research of mobile technologies. As businesses become complex with changing conditions and unpredictable economic climates, innovation is inevitable if a businesses is to remain competitive. In 2019, the number of mobile phone users is forecast to reach 4.68 billion, and that figure is expected to increase significantly every year thereafter [

5]. The high level of penetration of smartphones worldwide offers significant growth opportunities for increasing mobile financial services (MFS) usage and motivating financial institutions and telecommunication service providers by providing new mobile applications to increase and satisfy customers bases [

6,

7,

8].

The widespread adoption of mobile phones, particularly in developing countries, has brought about the rise of mobile money services considered as one type of MFS. Mobile money (m-money) is a crucial recent technological innovations in mobile communication technology. The introduction of mobile money has brought new challenges and opportunities for businesses and individuals. Riquelme and Rios [

9] stressed that as technology changes, both financial companies and consumers are embracing the advantages of the efficiency which comes along with it. Mobile users see mobile money services as an added value offered to them for carrying various banking as well as non-banking activities in real-time in a highly competitive world [

6,

10]. Mobile money, regarded as an innovative and effective means to achieve financial inclusion, is expected to provide financial services to two billion unbanked adults [

11] in emerging economies that lack access to affordable financial services [

5]. The unbanked are defined as adults who are not bank account holders or do not have access to a financial institution.

For the last ten years, access to financial services by unbanked individuals has been expanding partly because of the rapid growth in the adoption of mobile money services [

11]. Mobile money bridges the gap between the cash and digital economies, enabling those without access to banks to load cash in a mobile wallet and transact digitally using money transfers, deposits, withdrawals of money, and paying bills, to mention a few, through a mobile phone network. In developing countries, these services have been highly successful, led by the example of the world’s leading mobile money service, M-Pesa, which was launched in Kenya in 2007 and operates today in 8 countries. Mobile money services have had a tremendous positive impact on people’s lives, and have contributed to increasing financial inclusion and economic growth, absorbing financial shocks, and reducing poverty [

12,

13].

In this paper, the adoption and usage of mobile money are examined in one of the emerging economies of the sub-Saharan West Africa countries, Togo, which has a population of more than 7.5 million people [

14]. The adoption of products and customer engagement are the main indicators of the sustainability of the designated products (i.e., mobile money services), such that the number of active accounts is employed to comprehend how customers are accepting the services [

15]. A service such as mobile money can be availed without internet connectivity by employing basic mobile phones, and it is viewed as convenient and safe. Based on the mobile money report published in 2018, Togo has made significant improvements from 2014 to 2017, since the services were launched in 2013 in the country. Under the sub-Saharan Africa category and over the period, the country obtained the best financial inclusion rate ahead of countries such as Côte d’Ivoire, Madagascar, Chad and Mali [

16]. Noticeably, various companies in Togo have attempted to encourage their customers to use mobile money for their financial transactions. Recently, the national social security fund (i.e., la Caisse Nationale de Sécurité Sociale: CNSS) has admonished various employers to pay their social security contributions via Flooz and T-Money [

17]. There are presently two major mobile telecommunication companies (Moov and Togocel) which provide mobile money service in Togo: Flooz and T-Money respectively.

Despite the inherent benefits of such services, the mobile money adoption rate in Togo has remained somehow low, a phenomenon which requires further investigation. Nearly 67% of the Togolese population was subscribed to mobile telephony in 2015, and the number of mobile internet users doubled between 2014 and 2015. However, less than 15% of consumers have bank accounts in Togo [

18,

19]; in addition, mobile banking acceptance rates are lower than expected, i.e., 1% [

20]. It is then rational to merely presume that mobile money should provide significant input to nurture the rate of mobile financial services usages. In reality, this is far from being reality. Although most financial institutions, together with the government of Togo, offer subsidies to farmers through e-wallet technology to support a digitization project of the agriculture transformation agenda [

21], the sustained usage of the designated technology has not been embraced on an adequately large scale.

Regarding their environment, based on a World Bank survey on mobile money financial inclusion (2018), mobile phone subscribers currently represent almost 80% of phone users, while the penetration rate of m- money accounted only for almost 45% in Togo, ranking behind its neighbor country Ghana (60%) [

16]. Therefore, the rate of mobile money acceptance in the West Africa nation also differs. These phenomena create a challenge both for established players and for new participants like Fintech startups. Whereas mobile money has stimulated financial inclusion to lots of unbanked Ghanaians, Togo lags behind in its mobile money acceptance rate. Early studies have investigated consumer adoption of mobile money services in Africa (including Togo) [

22,

23,

24]. However, limited studies have probed the factors that contribute to the continued usage of mobile-based money technology and services within the underbanked and unbanked user segment and beyond.

Moreover, mobile money services are yet to focus on traditional offers such as money transfers, bill payments, and airtime top-ups and are not tailored enough to the demands of the low-income population [

25]. There is still a large group of customers who are reluctant to espouse such services due to uncertainty and technology anxiety issues about mobile financial services in general [

26,

27]. Nevertheless, such services have been well accepted in similar emerging economies, including the Philippines and Kenya. In recent work, for instance, Suri et al. [

28] stressed that the mobile money service M-Pesa lifted 2% of Kenyan households out of poverty. The literature on the espousal of mobile-based money in Togo is very scant [

23], and no research has been found in Togo regarding the mobile money adoption using the TAM model, although this model has had extensive relevance in explaining consumers’ responses to IT use and adoption [

29]. There are still important challenges delaying their disposition if digital finance is to reach its full potential in Togo. Customers are not adequately empowered to be active players in the ecosystem. All these reports led the authors to choose Togo as a good experiment field for assessing the determinants of mobile-based money services adoption and sustainable development from the developing country context.

Since it is unclear how Togolese mobile money users perceive technology usage, the motivation behind this research is to assess and predict key antecedents influencing behavioral users’ attitudes towards adopting mobile money services. This study attempts to bridge the gap in the existing literature by analyzing the perceptions that users have towards this technology while presenting a strategic framework for policymakers and practitioners to use the inherent advantages offered by mobile money. This research differs from past studies in three ways:

First, it aims to explore the attributes that warrant the adoption and sustainability of mobile money services among both potential and actual users. Therefore, the result provides a practical analysis, so that providers could understand customer behavioral intentions regarding the provided services, which, in turn, help in taking effective decisions.

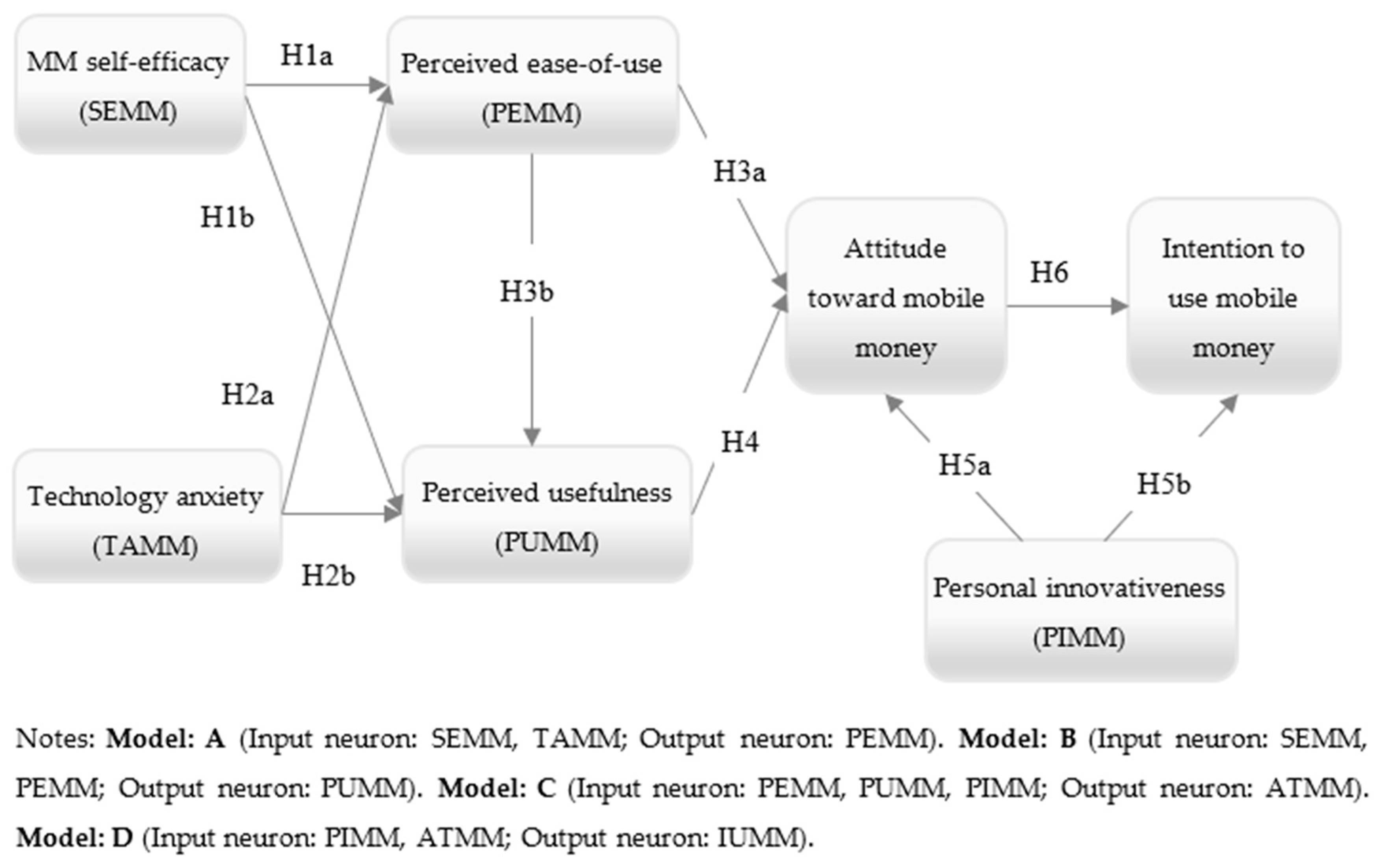

Second, the study empirically creates a framework to test the applicability of the TAM to mobile money transfer context, as it is a useful research model to explain the internal and external motivation in initiating technology adoption [

30]. TAM has been utilized successfully in assessing the antecedents that drive the adoption of several technologies. The projected model has similarities to earlier extended TAMs used in the developed countries, i.e., acceptance of self-service technology (SST) by French consumers [

31] and assessing the adoption of mobile payment through US consumers [

29]. We utilize the TAM from the perspective of developing countries and incorporate into the model mobile money self-efficacy, new technology anxiety, and personal innovativeness of IT. The effect of these constructs on the core TAM variables (perceived ease-of-use and perceived usefulness) is examined, as they are likely to impact the perceived ease-of-use and perceived usefulness on mobile money attitude and mobile money use intention.

Finally, this study aims to use an innovative research methodology presented in a two-stage approach. In the first stage, a structural equation model (SEM) is adopted to understand the significant influence of antecedents on mobile money services acceptance. The second stage used an artificial neural network (ANN) model to identify the importance of the antecedents. Therefore, this study develops a more inclusive and predictive model that can overcome the basic drawback of the prevailing model and offer a predictive analysis of the user perceptions of mobile money adoption in developing economies.

This research makes several contributions regarding an evolving market and technology to researchers, the literature on innovation systems and financial inclusion for developing countries, financial institutions, users and government by exploring and discussing direct implications for m- money role players.

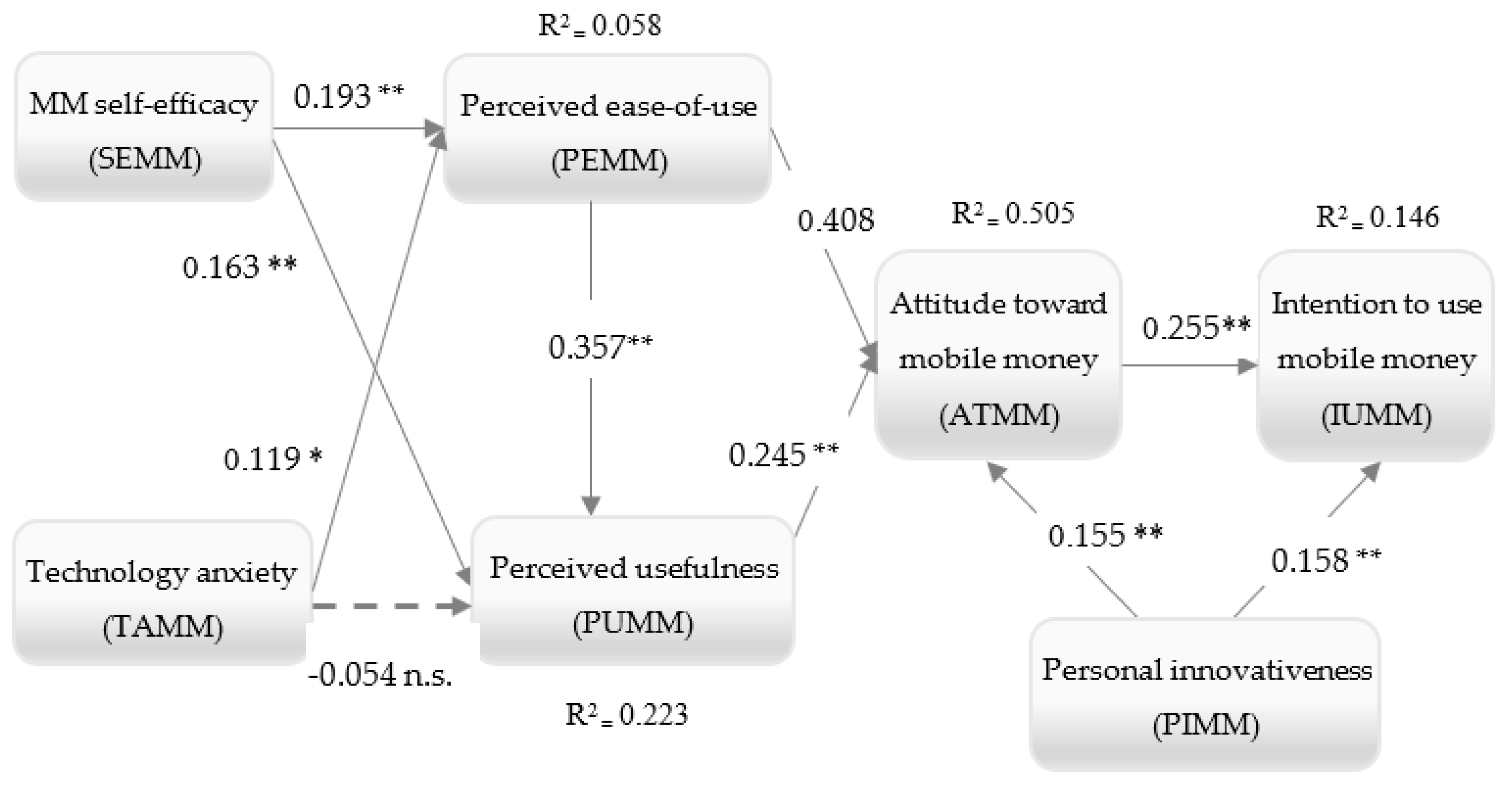

Primarily, we offer nuanced empirical outcomes on the fundamental factors that drive the success or failure of mobile money innovations by extending the traditional TAM. Given the result of the integrated methodology and the variables of TAM, the perception of ease-of-use is revealed to be the most important predictor, followed by the perceived usefulness in mobile-based money regarding the attitude constructs. It is important therefore that mobile money transfer providers consider how to make the use of the services easily, as well as emphasize on building the user-centric apps to create the awareness of usefulness. This study sheds further light upon the attitude of the Togolese consumer regarding mobile data services in general, and the usage of mobile-based phones for financial services specifically. Considering the extended variables associated with TAM, personal innovativeness acts as an enabler of user behavior, and company providers require to stimulate this aspect to facilitate the usage of mobile money services. Therefore, these implications could lead to an increase in financial transactions conducted on mobile devices. The contributions go along way towards extending the understanding of TAM to recently emerging contexts such as the mobile-based money in Togo.

Moreover, this research provides a robust tool combining SEM and ANN in order to predict the determinants that are more prone to the adoption and sustainability of mobile-based money services. Unlike earlier researches that studied consumer behaviors using a single approach (e.g., SEM), our study applied an SEM-artificial neural network technique to explain consumer behaviors regarding m-money. The SEM–ANN methodology shows to be a powerful technique, as it examines and provides the “what” and the “why” factors that have affected or will affect in the future. The result shows that SEM and ANN analyses complemented each other in shedding light on the complex process associated with the various influential factors to the development of mobile money innovations. Our SEM analysis contributes to the understanding of the relationships between various factors. One of the most substantial attributes of ANNs remains to be adjusted to periodic variations and detecting patterns in intricate natural nonlinear schemes. Therefore, the results of this study prove ANN to better predict than the usage of the SEM technique regarding the adoption of m-money. Correspondingly, this research can grasp the advantages of both methods (multi-analytic method: SEM-ANN) and assess complex linear and non-linear associations along with ranking the relative importance of the predictors.

Having established the justification and purpose of this study, the remainder of the paper is organized as follows: We present the contextual setting viewed as literature review while covering hypotheses development and research model presentation. Then, we present the research methodology, including the background of SEM-ANN analysis. In the final section, the findings, conclusion and implications, limitation, and future research regarding mobile-based money services adoption and sustainability are discussed.

5. Artificial Neural Networks (ANNs) and Sensitivity Analysis

Many statistical techniques are parametric, necessitating a great statistic background, whereas artificial neural networks (ANNs) are non-parametric models [

147]. ANNs are the most effective models among intelligent methods [

148]. ANNs techniques refer to a massively parallel distributed processor comprise of simple processing units, which have a neural tendency for storing experimental knowledge and making it available for use [

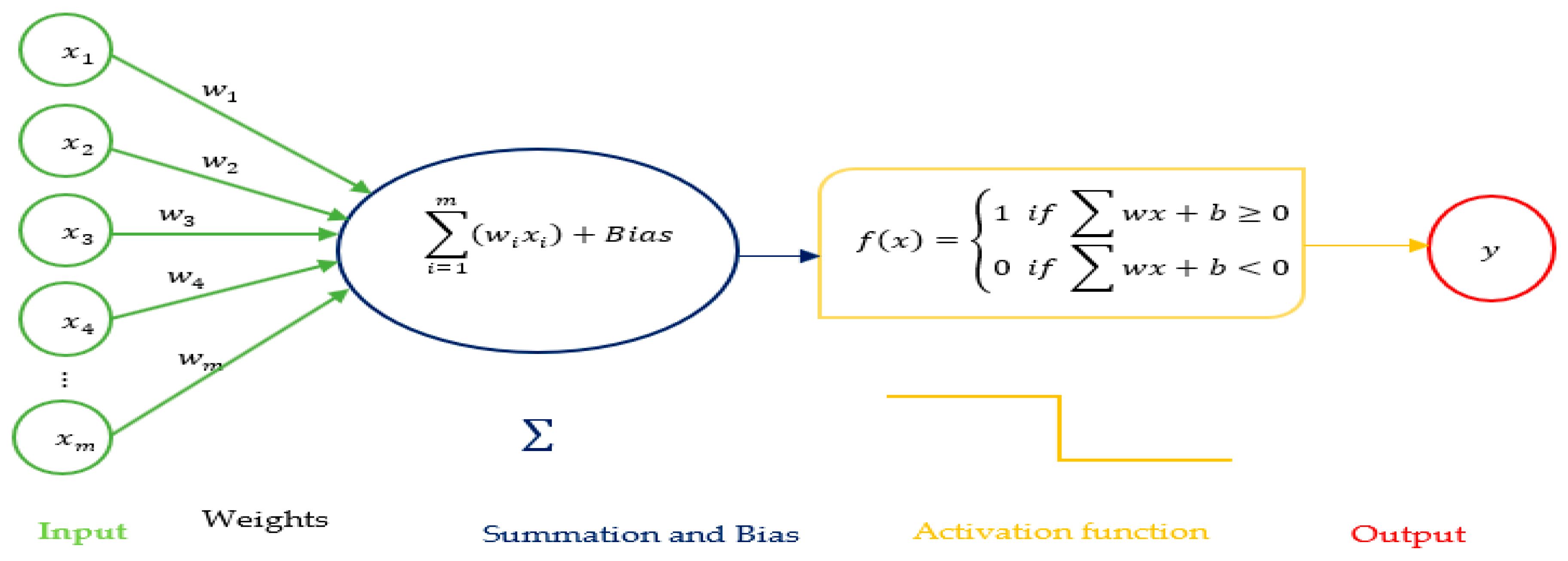

149]. They are very comparable to the biological neural networks in the human brain, in the sense that knowledge is collected through learning or training process and stored by “interneuron connection strengths recognized as synaptic weights”. They use a massive interconnection of simple computing units termed as neurons or nodes in input, hidden, and output layers with connection strengths called synaptic weights that are adjusted via an iterative process [

118]. The interconnection pattern between these neurons in ANN represent the network architecture. Each input has a connected weighted

(w), which is attributed based on its relative importance to other inputs. The node uses a function

f defined as a weighted sum of its inputs based on the following formula:

where

w1 and

w2 are weighted,

x1 and

x2 are input,

b representing the bias and

Y the output.

Figure 3 represents the general network architecture for a single layer perceptron.

One of the particularities of ANN is to deal equally with a linear and non-linear relationship with requiring any distribution assumptions such as normality, linearity, or homoscedasticity as compared to SEM [

118]. Hence, the function

f is non-linear, which is a so-called activation function.

Selecting a proper activation function remains an important consideration because it can affect how the input data should be set up, as well as how the output format would be generated.

There are three commonly used activation functions, i.e., sigmoid, hyperbolic tangent (Tanh), and rectified linear unit (ReLU) as presented in the formula below. The Sigmoid function is an activation function having an output bound between [0, 1]; while Tanh function has an output range of [−1, 1]. Relu function refers to the type of activation function returning the max (0, x). Although the output layer can have any activation functions, Sigmoid is the widely used activation function for the output layer in the information technology context [

113]. The Sigmoid function and its combinations generally work better in the context of classifiers and sometimes prefer when the researcher expects an output or intermediate layer of the net to represent the probability of an event. Based on the output value range of sigmoid, the normalizing output of each neuron can be assessed as well.

A feedforward backpropagation (FFBP) neural network is an ANN which employs a supervised learning procedure with a feed-forward algorithm for prediction. It is viewed as advanced multiple regression analysis (MRA) or SEM able to deal with complex and non-linear relationships.

In this study, the extensive neural network model—multilayer perceptron (MLP) with the FFBP training algorithm—was applied [

10,

150] in SPSS 21 using the sigmoid activation function for hidden and output layers [

112,

151]. This sigmoid function will be converging to one for large positive numbers and 0.5 for zero and very close to zero for large negative numbers. Therefore, it allows transitions to be calculated between the low and high output of the neuron. The output is subject to the activation and which in turn rely on the input values and their corresponding weights. The number of neurons in the input layer is equivalent to the number of predictor constructs. Similarly, the number of neurons in the output layer is equal to the number of dependent variables, i.e., predicted constructs, and the problem scheme determines all.

Over-fitting is a major issue in the predictive modeling approach. To avoid over-fitting, a ten-fold cross-validation technique was performed, with 90% of the sample used for training and the remaining 10% of the hold-out data for testing purpose [

112,

151]. The determination of hidden nodes is regarded in the literature as one of the greatest challenges. Wang and Elhag [

152] suggested a range of 1 to 10 hidden nodes in the neural network model. The number of hidden units was engendered automatically, and the root-mean-square-error (RMSE) values were computed together with the normalized importance in the sensitivity analysis.

The accuracy of the network models is assessed by RMSE [

10,

150], which is computed as the difference between actual and predicted values of the dependent constructs, i.e., consumers intention to use mobile-based money services. The summary of RMSE values for all four ANN models is provided in

Table 8. The RMSE values achieved through all four neural network models, both for training and testing data points, are very small. Hence, the results generated are relatively accurate [

112,

113]. The number of non-zero synaptic weights linked to the relevant hidden units is used to validate the relevance of the variables (See

Table 9). Hence, all factors are found to be relevant in predicting the dependent variable. The normalized or relative importance values were computed as the ratio of the relative importance of each variable with its largest importance and expressed in percentage form [

112]. Only significant linear factors obtained via the SEM technique were regarded as the input units of the ANN models. From

Table 10, the sensitivity analysis performance was then computed by averaging the importance of the input variables in predicting the output for the ten networks [

10]. Therefore, the relative strengths of the causal relationships were assessed grounded on the normalized importance from the sensitivity analysis [

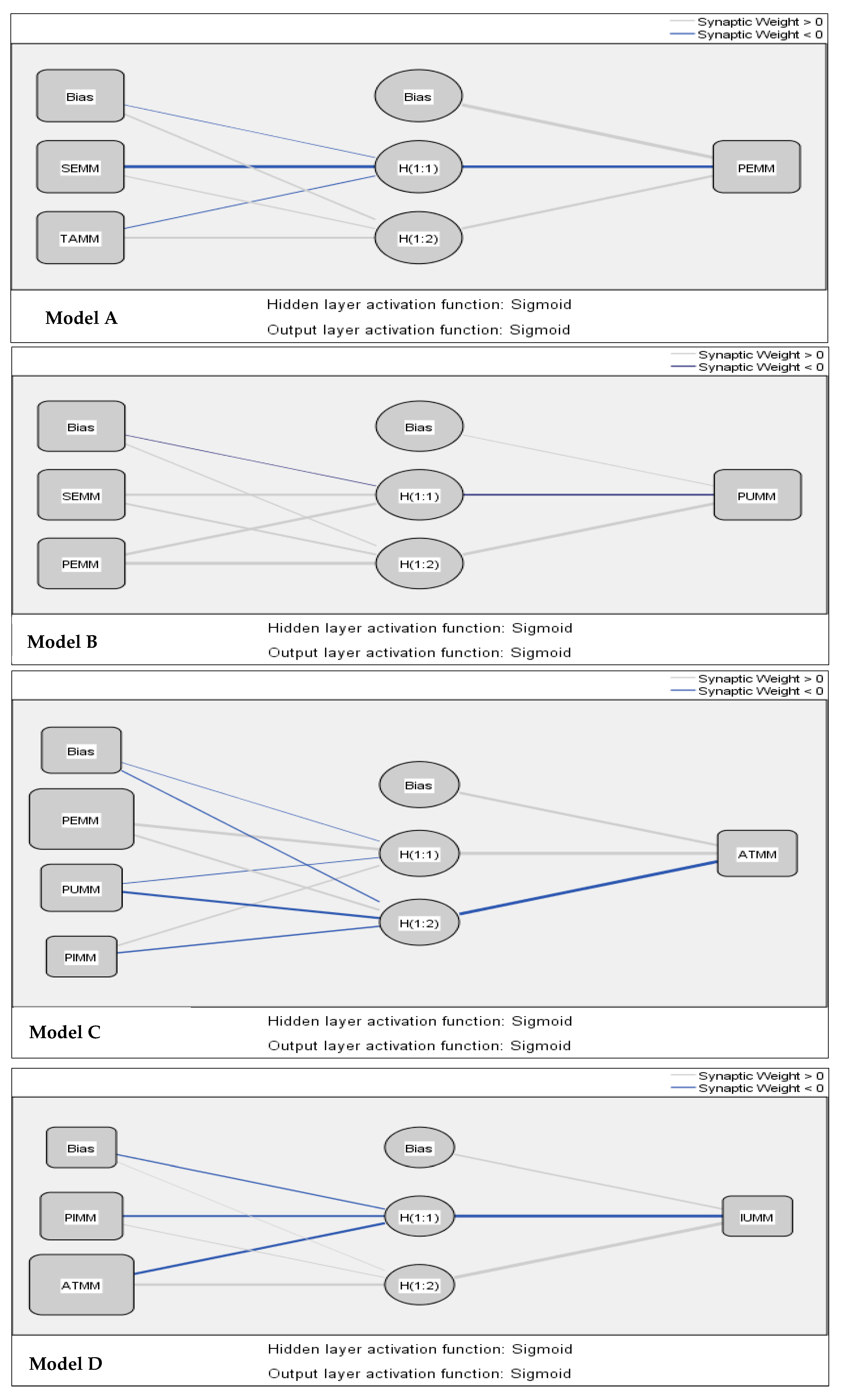

92]. SEMM was found to be the key determinant in predicting PEMM followed by TAMM in model A. In model B, PEMM is the most prominent predictor for PUMM, followed by SEMM. For model C, the order of importance towards ATMM in descending order is PEMM, followed by PUMM and PIMM. Last but not least, ATMM constituted the most effective in term of predicting IUMM, followed by PIMM.

Remarkably, the ANN models (See

Figure 4) are able to learn both complex linear and nonlinear relationships among decision variables, as compared to structural models, which detect linear relations only [

113].

7. Conclusions and Implications

Mobile money transfers are among the latest innovative financial applications of mobile technologies. Due to the lower acceptance of mobile money in Togo, this research grasped the importance of understanding and assessing key determinants affecting mobile money acceptance. Therefore, the research aimed to study beliefs and behavioral variables that impact the acceptance and sustainability of mobile money application from the developing country perspective, as well as offering conclusions beyond mere descriptive analysis.

To reach this objective, the traditional TAM model has been used, to which relevant constructs were added in the adoption of an innovation such as self-efficacy, new technology anxiety, personal innovativeness allied with the proposed methodological application. A survey was conducted among the users and potential users of mobile-based money services for the analysis of the proposed theoretical model. The proposed model employed a two-stage SEM-ANN approach—SEM for testing possible relationships and ANN for predicting the determinants of mobile money. The predictive analytical approach of the neural network was employed to assess the data, and the outputs from the data were utilized to compare with the ones from structural equation modeling analysis. Such an integrated methodology provides a rigorous and comprehensive reference for future research work in the area of mobile money transfer from the developing countries perspectives. Togolese mobile financial service providers may develop appropriate business policies and strategies for mobile money transfer system, which enhance the overall business performance.

Moreover, this research reveals the relevance of the two-stage approach integrating SEM and ANN techniques to enhance the assessment of technology adoption models for decisions makers. By comparing the results of the SEM and the ANN analyses, the major difference lies in the strength of the effect of the two constructs relating to innate personal ability and personality trait. The ANN analysis increases the relative importance of self-efficacy in ease-of using mobile money transfer. Similarly, the relative importance of personal innovativeness has been improved regarding its effect both on users’ attitude and intention to use mobile money with ANN analysis. The results reveal that ANNs are better than SEM at learning, predicting, and clarifying various factors influencing mobile money adoption. However, SEM supports the causal analysis (the reliability and validity of the measurements and path analysis) which found limited in ANN application. Therefore, a multi-analysis technique such as the integrated approach (SEM-ANN) contributes more to sharpen the understanding of the effect of model variables than using a sole technique.

From a different angle, the outcomes of this research have immense practical and managerial implications. This study can provide useful insights to the decision makers of telecommunication service providers, mobile money app developers, and mobile money service providers to enhance and maintain their customer base. First, the government of several emerging economies has been making efforts to achieve greater financial inclusion by using technology [

21]. Recently, African Development Bank (AfDB) in collaboration with the government of Togo offer subsidies to farmers through e-wallets provided by mobile network operators Moov and Togocel in patronizing the digitization project of the agriculture transformation agenda [

21]. Grounded on the World Bank/AfDB report, the mobile financial services (MFS) have a significant positive influence on the macroeconomic development of some West African Nations and even the percentage of effect could reach a double-digit. Based on the proportion of GDP, among the largest beneficiaries, are Togo (10.7%) and Cape Verde (9.4%) [

164]. Asif et al. [

165] reported the significant benefits of mobile money on a firm investment in three East Africa economies and encouraged the use of such services in other developing countries.

Given the importance of financial inclusion and sustainable development, mobile money transfer services might go a long way in solving the concerns of the non-existent banking network. Banks have been reluctant to open branches in far-reaching zones because of security and viability issues. Thus, services such as mobile money transfers can effectively fill that need, and can be an effective instrument with which to achieve greater financial inclusion [

166]. This study reveals that perceived usefulness of the mobile money services impacts the consumer’s attitude regarding the decision to adopt this technology, including its ease of operations. The developers of mobile money apps require to focus on the development of the user-centric apps to create the awareness of usefulness together with ease in operations of users in their view. Then, in turn, should lead to an increase in financial transactions conducted on mobile devices. It is important to stress the influential role of personal innovativeness on the users’ attitude and intention to use mobile money. For the scholars’ conceptualization of personal innovativeness, a person is described as being innovative if he or she is early to adopt an innovation [

98,

167]. Therefore, personal innovativeness acts as an enabler of user behavior, and company providers need to stimulate this factor to facilitate the usage of mobile money services. This signpost that for the usage of such services, users are seeking not only basic functionality, but also innovations. Service providers may ponder directing some of their advertising campaigns to the segment of more innovative uses. As per the suggestion of Moore [

168], innovators offer companies with great feedback early in the design cycle and start building a supporter who will impact buyers. Since it is now possible to gather big data on consumer behavior and habits through mobile phone sensors, an artificial intelligence approach could be utilized to profile each consumer and offer personalized service that the customer would find innovative and useful. For Midgley and Dowling [

87], innovators regarded as early adopters are more likely to be opinion leaders and the messages these innovators addressing to others stimulate the interpersonal predisposed adoption process of light users or non-users. This will have a positive impact on the mobile-based money adoption rate.

{kind=link}

{kind=link}

{kind=link}

{kind=link}