1. Introduction

Recent research in developing countries has extensively focused on corporate social responsibility (CSR), corporate environmental responsibility (CER) and corporate carbon (CC) disclosures within the broad range of sustainability management disclosures (SMD) [

1,

2,

3,

4,

5,

6,

7]. Furthermore, the number of studies continues to grow, in the context of both developed and developing countries [

8,

9,

10,

11,

12,

13,

14,

15,

16]. However, the SMD studies conducted in developing countries have not paid significant attention to the issue of corporate corruption and bribery [

17,

18,

19], and no such study has been undertaken in the Bangladeshi context. As corruption is a global problem that compromises governance, transparency and accountability, it is treated as a cancerous presence within society [

20]. Moreover, the existing literature also reports that developing countries are highly affected by corruption, because it affects both economic growth and financial stability [

20,

21,

22,

23,

24,

25,

26]. This raises the question of why researchers covering developing countries have neglected the issue of corporate corruption. The question is especially significant in the context of Bangladesh, because the country has a poor track record regarding corruption, based on Transparency International’s (TI) Corruption Perception Index (CPI). CPI reported that the country received the highest corruption score (high score means higher corruption and vice-versa) on this system between 2001−2005, whereas in 2018, it ranked 143rd out of 180 countries. Therefore, we would like to draw attention to this issue through a corporate corruption study, which we believe will benefit researchers and policy makers within the country.

TI defines corruption as “the abuse of entrusted power for private gain”, while bribery refers to a “facilitating payment”. Corruption or bribery can be used to expedite work, create political connections for receiving formal and informal benefits (e.g., tax benefits, licensing, subsidies) and generate monopolistic market positions [

19]. Corruption decreases the competitive advantage and opportunities of developing countries due to the limited resources and capabilities these nations have in comparison to more developed countries [

18,

19,

27]. In order to curb corruption, many national and international institutions have developed, and continue to develop, different sets of standards, rules, regulations, codes of conduct, corporate governance policies and whistle blowing policies (e.g., World Bank initiatives, organization for economic cooperation and development (OECD), bribery guidelines, united nations global compact (UNGC) anti-corruption guidelines, global reporting initiative (GRI) sustainability framework, ISO 26000 guidelines, AA 1000 standard and SA 8000 standard). The final goal of these rules, regulations and standards is greater control of corruption and enhanced corporate transparency and accountability through the disclosure of relevant information.

Board experts are crucial to sound corporate governance. The presence of external experts on the board mitigates potential conflicts while enabling the firm to benefit from experience-based advice and suggestions, which convey positive signals to the market. As independent and resourceful experts, these external board members monitor corporate activities closely and support the strategic decision-making of the corporation. Existing literature has reported that expert directors are usually responsible for preparing, monitoring and communicating corporate strategies and policies regarding CSR, CER, corporate transparency and accountability, corporate financial integrity and stability and the corporate financial inclusion of stakeholders [

3,

15,

28]. Hillman et al. [

29] and Hillman and Dalziel [

30] suggest that a board has to perform two functions, namely (1) monitoring the corporate management structure and (2) supporting the diverse range of stakeholders via accessing information. According to Hillman et al. [

29], Hillman and Dalziel [

30] and de Villiers et al. [

15], expert board members not only reduce information asymmetry, but also demand management explanations regarding any strategic or misguided initiatives, while also criticizing unethical and undocumented activities. Therefore, having qualified and professional experts on the board helps to accelerate corporate transparency and accountability through the disclosure mechanism. Malagueño et al. [

27] empirically tested the cross country benefits of both accounting and auditing standards and having an expert presence on the board, concluding that establishing an improved accounting and auditing mechanism significantly reduces corruption. Al-Shaer and Zaman [

9] also found that having accounting experts on the board increases the credibility of the information disclosure process. Moreover, Agrawal and Knoeber [

31] have shown that external resources on the board (e.g., politicians and lawyers) increase a corporation’s lobbying and negotiation power, in addition to decreasing political costs because of such members’ skills, knowledge, networks and reputation. Ferguson [

32] claims that lawyers play a critical role in controlling corruption within a corporation, by explaining the legal repercussions of any corporate action and thus, serving as a “gatekeeper”. In addition, they suggest that lawyers are treated as “facilitators” in order to refrain from corruption, rather than as “advisors” who assist in violating the law. The existing literature on corporate governance and international business demonstrates mixed reactions regarding the relationships among a firm’s political connections and corruption, growth and investment, as well as a firm’s values and accounting performance [

33,

34,

35,

36,

37,

38,

39,

40,

41,

42,

43].

In light of the above discussion and evidence, we believe that board expertise can increase corporate transparency and promote corporate corruption disclosure (CCD). Moreover, our discussion is particularly relevant when considering that the study is in relation to Bangladesh, a developing economy that is currently facing severe allegations regarding corruption. Thus far, only Azim and Kluvers [

44] have offered a descriptive study on micro-credit banks’ (Grameen banks) corruption-prevention mechanisms, while Uddin et al. [

6] offer an assessment of political CSR, and Muttakin et al. [

4] study the political connections and CSR disclosure in the Bangladeshi context. The dearth of corporate-level studies on this most critical issue makes us question how external experts (from accounting, law and politics) in the country are promoting corporate corruption disclosure at the business management level. Based on this research question, the study aims to investigate how Bangladeshi firms add expert board members in order to mitigate agency conflict, information asymmetry and the pressures posed by a diverse range of stakeholders. In order to find empirical evidence, we consider listed financial firms between 2012−2016. Our reasons for selecting financial-sector firms are: 1) they are the most regulated and visible sector, 2) they have higher economic importance, 3) they have been implicated in recent corruption scandals (capital as well as money markets) and 4) this sector has higher levels of political and government intervention.

1.1. Theoretical Background and Hypotheses

Previous studies have conducted extensive research regarding board characteristics and disclosure, dealing with the agency [

45] and resource dependence [

46] theories, which are most appropriate when describing the motivations and determinants of information disclosure. Chang et al. [

47] and Walls et al. [

48] have described how agency theory and resource dependence theory (RDT) are most prominent in the study of disclosure and corporate governance. Moreover, de Villiers et al. [

15] have stated that a theoretical understanding of the agency and resource dependence theories offers the best solution for determining the capability of a board’s monitoring process. It is also worth mentioning that stakeholder theory and legitimacy theory are also highly useful in the context of disclosure and corporate governance.

Agency theory describes the relationship between agents and principals [

45]. This ownership separation may create conflict between the two parties, with managers’ self-interest giving rise to informal and illegal activities. Short-term opportunistic managers are likely to be involved in unlawful and corrupt behavior that may damage a firm’s reputation and governance ability [

49,

50]. Therefore, external directors are required to monitor the activities of insiders and to communicate with stakeholders. It is also evident that agency theory reduces information asymmetries in general, while corruption disclosure helps reduce the information gap between managers and investors [

10].

Resource dependence theory describes how access to resources depends on a director’s access to a firm’s flow of information and resources, which can then be utilized [

30,

46,

51]. According to this perspective, a resourceful person serves the board as a strategic policy maker on a particular issue. Existing studies have divided these resources into “human capital” (advice, experience, expertise, knowledge and reputation) and “relational capital” (network, channel) [

9]. Furthermore, Hillman et al. [

52] have classified such directors as “business experts”, “support specialists” and “community influential”, positions which have also been supported by other researchers [

15,

51]. Prior literature also suggests resourceful persons are generally prominent and reputed in their areas, and that they therefore do not compromise on any unethical and undocumented activities [

46]. Based on the previous experiences and connections the expert directors help to incorporate different types of policies and regulations to tackle corruption, bribery, undocumented transactions and unethical behavior in business management. It is also considered that outside directors are the representative of the general stakeholders, therefore the presence of resourceful person reduces the information asymmetry problem. Both legal experts and accountants on the board are associated with strong anti-corruption and transparent accounting mechanisms within the organization. De Villiers et al. [

15] state that a resourceful director positively enhances strategy and programs relating to the improved informational performance of a firm. Moreover, the diverse experiences, strengths and backgrounds of directors are also considered ‘useful and valuable’ resources for the organization. Board diversity promotes stakeholder management and reduces information asymmetry because external directors function as a watchdog. For example, audit committees, CSR committees and money laundering committees are constituted by such resourceful persons, who reinforce not only internal strength, but also external assurances [

9,

15,

49]. RDT also considers a broad range of efficiency negotiators, as they have a strong network domestically and globally. Kassinis and Vafeas [

28] argues that a strong negotiator with the government helps firms to minimize taxes and tariffs, as well as to expand business in the foreign market. For example, political experts’ sound relationship with the national government may enhance foreign market business negotiation (e.g., international bidding and tender) as well as trust and confidence. Therefore, a resource-rich director, for example a lawyer or an accounting expert, provides resource-based opinions and suggests how to improve the anti-corruption, accountability and transparency processes of the corporation.

Finally, stakeholder theory [

53] focuses on multiple stakeholder engagement. This is in contrast to legitimacy theory [

54], which prioritizes the generalized perceptions of business and society. Good corporate governance ensures a stakeholder’s long-term benefits and responsibilities, while a well-governed board is accountable to its diverse range of stakeholders [

10,

55]. It is also evident that disclosure performance is considered the most effective tool for reducing information asymmetry, because it helps eliminate legitimacy threats among businesses, stakeholders and society. The media also plays an active role in circulating different forms of information to the multiple stakeholders within a firm through different channels (traditional, social and online). Resource-based external directors seek to identify the interests of these stakeholders, while supporting strong monitoring processes that may increase the quality of decision-making, encourage corruption disclosure and reduce the risk of corruption [

49]. Moreover, anti-corruption disclosures increase the strategic legitimacy of the corporation as a result of their disclosures and initiatives. Additionally, the presence of external experts on the board sends a strong and confident signal to both the stakeholders and wider society, which will also help to mitigate any legitimacy threats [

56].

1.2. Hypotheses

1.2.1. Accounting Experts and CCD

The role of accounting experts on the board is to oversee the accounting systems, ensure transparency regarding financial reporting and the accountability of financial statements and prevent internal control by the firm [

28]. As an expert on accounting and auditing, an accountant on the board helps to monitor the management’s capacity and capability regarding financial decisions, while also providing experience-based opinions regarding the firm’s financial statements [

57]. Moreover, accounting experts play the role of an arbitrator between internal and external auditors, reducing the number of agency conflicts within the firm [

58]. The presence of accounting experts on the board has also received regulatory and institutional attention around the world. For example, the US Securities and Exchange Commission mandatorily requires accounting and financial expertise in corporate governance. Furthermore, the US Sarbanes Oxley Act of 2002 mandates having at least one financial expert on the board, while the UK corporate governance code of conduct, the Australian corporate governance principles, the Singapore code of corporate governance and the updated corporate governance rules of India also require the inclusion of financial and technical experts on the board [

59]. In this context, the Bangladesh Securities and Exchange Commission also requires the presence of financial and technical experts on the board. Kusnadi et al. [

59] have shown that having accounting experts on the board positively and significantly promotes the quality of financial reporting by Singaporean firms; they further verified these results by considering both accounting and financial experts and reported the same results, remarking that accounting experts function as a watchdog over the financial reporting system of the company. DeZoort and Harrison [

60] have conducted a detailed study on the role of fraud detection and accountant accountability of US auditors, reporting a positive and significant relationship. In addition, they also reported that accountable accountants worked more actively against corruption and fraud than anonymous auditors. The most recent study by Al-Shaer and Zaman [

9] found that accounting experts promote CSR (anti-corruption initiatives are also a major part of CSR) disclosures relating to UK firms due to their experience, background and reputation. Malagueño et al. [

27] used a cross-country study to document how higher standards of accounting and audit reporting decreases perceived levels of corruption. Moreover, Saha and Roy [

61] have described how accounting experts face significant threats in the appointment and regulatory compliance of three global companies, which increases corporate corruption levels and the number of scandals. No prior study has documented the role of an accounting expert in terms of the corruption disclosure of Bangladeshi firms, which leads us to state the following hypothesis:

Hypothesis (H1): The Presence of Accounting Experts on the Board Positively Promotes CCD.

1.2.2. Legal Experts and CCD

Having legal experts (LEGE) on the board enables firms to receive sufficient advice, suggestions, recommendations and guidelines regarding monetary and non-monetary contracts with third parties, how to deal with legal issues within the organization and how to manage corruption allegations. Lawyers are considered highly competent, professional people whose legal background enables them to effectively deal with sensitive political and social information, such as corruption, CSR and environmental performance [

15,

62]. The role of these lawyers is to support their firms or clients by formulating and exercising due diligence mechanisms regarding corruption control and prevention. Defining the legal expert’s role in controlling corruption, Ferguson [

32] wrote: “…lawyers are ‘transaction facilitators’ and are expected to construct transactions in a way that complies with the relevant laws, including laws prohibiting the offering or paying of bribes. In addition to providing legal advice, lawyers educate their clients on the law and on how to comply with the law while achieving business objectives. Lawyers may act as internal or external investigators…. Lawyers may act as compliance officers or ethics officers by creating, enforcing and reviewing their client’s compliance program. Lawyers may act as assurance practitioners and conduct an assurance engagement…. Finally, some lawyers may be in the position of a gatekeeper…” (771:2017). Therefore, the presence of a legal expert on the board mitigates agency problems, while also sending a quality signal to investors. Lawyers’ expertise acts as a reputational intermediary for the firms, which is why they were described by Ferguson [

32] as corporate gatekeepers (775:2017). De Villiers et al. [

15] found that having legal experts on the board also significantly promoted the environmental performance of US corporations by virtue of their active professional experience. Furthermore, they stated that the active participation of a board expert increased access to human capital and social networks. According to McKendall et al. [

63], when dealing with different laws and compliance levels, such as money laundering, anti-corruption, financial integrity and environmental and climate change laws, firms need to understand every relevant aspect due to investment and financial decisions. Legal experts, therefore, provide the requisite legal explanations and advice to the board [

28]. A recent report on the lawyer’s role in the fight against corruption vividly stated that a lawyer’s professionalism can help enhance the anti-corruption movement around the world [

64]. Lee [

65] also investigated bankrupt accountants and lawyers in Scotland during the period 1855−1904, documenting how professional misconduct and criminal activities led to financial misappropriation. To the best of our knowledge, there have not been any studies concerning the role of lawyers on the board and corruption in the context of Bangladesh or at a global level. However, based on our theoretical proposition and the existing literature on corporate disclosures, we believe that the presence of legal experts on the board mitigates information asymmetry among corporations, society and stakeholders. Moreover, having a legal expert on the board also enhances a board’s legal decision-making power regarding finance and the environment. Additionally, having these lawyers increases anti-corruption initiatives by establishing both due diligence processes and professional obligations. Therefore, we propose the following hypothesis:

Hypothesis (H2): The Presence of Legal Experts on the Board Positively Promotes CCD.

1.2.3. Political Directors and CCD

Having political directors on the board enables a firm to have political relations with the government [

31,

32,

33,

34,

35,

36,

37]. According to these authors, there are two types of resource-based external directors: business groups (senior managers, business consultants, investors) and non-business groups (bureaucrats, academicians, lawyers, politicians). Non-business group political directors provide support to management in relation to government purchases, business policies, lobbying, financial policies and environmental regulation [

15,

31]. It is also evident that larger firms require greater levels of political visibility due to the impact of foreign trade policies, equal employment rules, environmental policies and regulatory policies regarding food and drugs [

31,

66]. For example, US manufacturing and energy firms frequently use lobbyists for establishing political connections. They also help promulgate specific regulations for corruption control and rising levels of accountability. Moreover, in the context of international trade, political directors enhance a firm’s global network of connections and share their global experience with management. Furthermore, political directors are also aware of corruption issues, as well as the money-laundering policies and initiatives undertaken by the government, thus deterring the firm’s management from engaging in corruption and encouraging them to launch anti-corruption programs and mechanisms. Joseph et al. [

23] conducted a comparative study between the anti-corruption disclosure practices of Malaysian and Indonesian firms, finding that Indonesian firms’ corruption disclosure practices are higher than those of Malaysian firms. They concluded that higher board level responsibilities, along with codes of conduct, whistle-blowing and accounting standards are the main elements that differentiate corruption disclosure practices between the two countries. Lombardi et al.’s [

67] most recent study documented how a specialized board actively prepares and executes plans in order to prevent corruption within an Italian company, thereby promoting sustainable corporate governance. Cheng et al. [

36] have empirically proven that political management significantly increases information disclosure, in order to maintain a strong relationship with government. Due to their familiarity with governments and their strong networking capabilities, boards with high political connections are concerned with reputation and social status, therefore encouraging higher transparency and accountability levels regarding corruption. Consequently, higher political connections create increased awareness of corruption and lead to the implementation of improved disclosure processes [

7]. Boubakri et al. [

37], Claessens et al. [

39], Fan et al. [

68], Adhikari et al. [

41], Faccio et al. [

42] and Khwaja and Mian [

43] have reported that high levels of political connections are associated with higher benefits and opportunities for both the firms and their shareholders (e.g., access to bank loans and government finance; lax taxes and regulatory burdens; awards of government contracts; and protection from bankruptcy). Conversely, Hung et al. [

21] found that high levels of political connection decreased voluntary disclosure in terms of inefficient capital markets, weaker litigation risks and improper product markets. Additionally, they stated that the upper levels of political management suppressed information due to political cronyism and corruption. Until now, we have not documented the relationship between political directors and the corporate corruption disclosure of Bangladeshi firms. Therefore, based on the mixed results of previous studies, we set the following hypothesis:

Hypothesis (H3): The Presence of Political Directors on The Board Positively Promotes CCD.

1.2.4. The Influence of Interaction Effects between Political Directors and Legal Experts on CCD

The existing literature has vividly explained and investigated how political board members reduce disclosure levels; the situation is more severe when there is high level of corruption [

4,

38,

69,

70]. The increased political connections of the board also reduce the legitimacy of the management due to political cronyism. Moreover, when a country and its economy are highly corrupt, it is difficult for the board to fight corruption because of its own political management. Politicians on the board of a company in a country that has a looser grip on corruption, are more motivated by the political benefits of their role than inclusive development of the stakeholders. Uddin et al. [

6] have shown how, in a highly corrupt country, political management is sought for two main reasons: implementing the ruling political party’s agenda and personal benefits derived by powerful managers. Moreover, Muttakin et al. [

4] have posited that, in a weak institution, family-led politics, the absence of the rule of law and highly corrupt national political management eschew disclosure practices due to limited stakeholder pressure and social legitimacy. Carretta et al. [

66] state that the political directors who hold executive positions have also had a negative impact on the banking performance of Italian firms. The existing literature explains how developing countries with less control over the corruption of their political management structures, have failed to demonstrate corporate transparency and accountability, which is likely to result in reduced performance, productivity and investment [

4,

21,

38,

43,

69,

70]. Prior studies have also found that the presence of political experts intensifies the corruption that is exerted on earnings forecasts [

38]. Therefore, in countries with less control over corruption, political experts like to maintain control over the board in an attempt to undermine the role of other experts. Moreover, from the perspective of a developed country, Fernández-Gago et al. [

10] have found that there is a negative relationship between an independent director and his or her political connections in the CSR disclosure of Spanish corporations, while Shi et al. [

71] have shown how high-level, politically-connected independent directors have destroyed the value of Chinese firms. According to the arguments of Shi et al. [

71], Muttakin et al. [

4], Chen [

26] and Chen et al. [

38] we believe that in Bangladesh, which has a looser control over corruption and the rule of law, the political connection of firms has drastically reduced the role of legal experts. As a result, we propose the following hypothesis:

Hypothesis (H4): The Presence of Political Directors on the Board Negatively Moderates the Role of Legal Directors in Promoting CCD.

1.2.5. Corporate Media Visibility and CCD

The media is considered to be a mirror of society, wielding a great deal of influence on business management, political government and public opinion within a country. Strong media coverage mitigates information asymmetry between businesses and the public. According to both stakeholder and legitimacy theory, the media is one of the most influential mechanisms for discovering and addressing social irregularities, as well as strengthening accountability. Corporate media visibility refers to news reports or press coverage of a particular organization in different forms (e.g., traditional, electronic and social media) [

16,

72,

73]. As an important stakeholder, corporations seek to maintain a positive relationship with the media by providing different sets of information regarding anti-corruption, anti-bribery, financial integrity and diverse CSR initiatives in order to improve the transparency and accountability of their businesses, as well as to provide sustainable corporate governance practices. Blanc et al. [

18] have found that media exposure has a positive effect on the anti-corruption disclosure of leading global firms, while the power of media exposure is relatively high in places where there are greater levels of press freedom. Islam et al. [

19] have shown that two Chinese mobile companies produced more anti-bribe disclosures following international concern, which led to global stakeholder pressure to restore their reputations. Islam et al. [

17] argue that pressure from both the media and NGOs has had a positive influence on the corporate anti-bribery disclosures of two European corporations in order to maintain their legitimacy. Furthermore, they also describe how networked governance plays a crucial role within corporate transparency and accountability. Additionally, positive corporate media coverage reduces corporate risk and minimizes social threats [

72]. Das et al. [

74] have described how Bangladeshi media are concerned about social and environmental issues regarding corruption and government irregularities regarding corporation and this argument is supported by Islam and Islam [

75]. We believe that the Bangladeshi media explicitly and implicitly reports on corporate corruption, which escalates corporate corruption disclosure levels. Therefore, we propose the following hypothesis:

Hypothesis (H5): Corporate media visibility positively promotes corporate corruption disclosure.

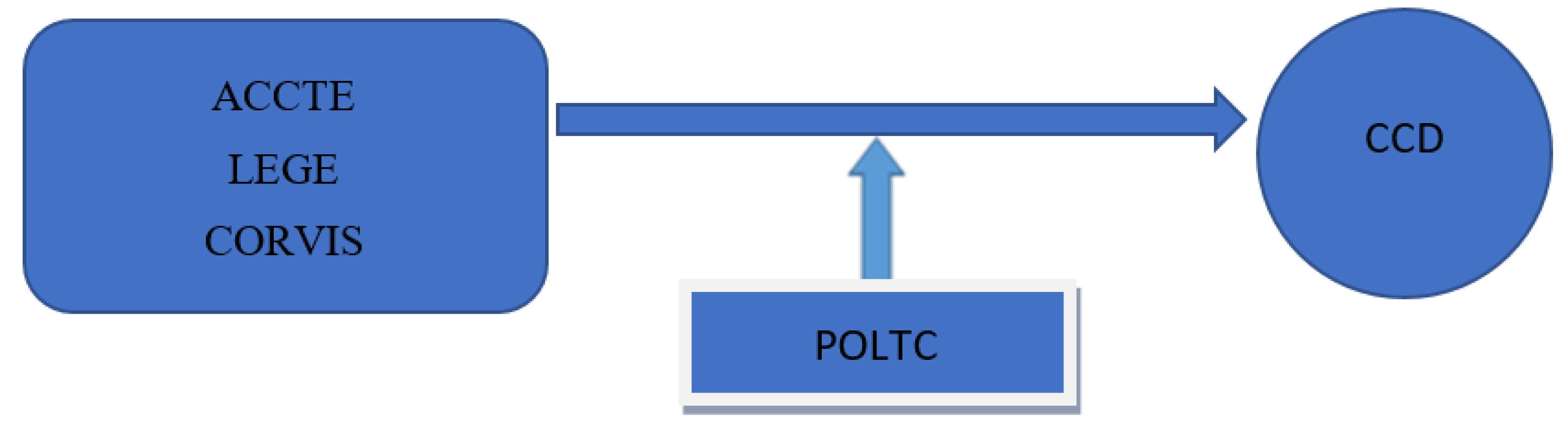

From the above theoretical and literature discussion, we draw on the following conceptual model (

Figure 1).

3. Result and Discussion

Table 3 shows the descriptive statistical results of the study. Mean CCD has a log value of 6.43, while the average Keywords position is 756, which is comparatively high, as compared with the study of Lopatta et al. [

49]. The ratio of ACCTE shows that most of the boards have at least one expert, whereas the maximum number is 5. The mean participation of ACCTE on the board is 60%, which means that 32 firms have active ACCTE. The average presence of LEGE on the board is 26%, which indicates that only 14 firms have LEGE. On the other hand, 51% of the firms had a politically engaged board member, demonstrating the higher political connections of Bangladeshi financial firms. The high political connection ratio is consistent with the study of Wang et al. [

33], which found that 59% of Chinese firms are politically connected. The mean number of media articles published by the sample firms is 6.09, while the highest number is 53. Media article results indicate lower levels of corporate visibility compared with the European multinational corporation study of Islam et al. [

17].

Table 4 presents the correlation matrix between the dependent and independent variables of the study. CCD is positively and significantly correlated with POLTC, CORVIS, SIZE, LEV and AGE, while ACCTE and LEGE has no significant association. We report that the maximum correlation is between CORVIS and SIZE (0.710). However, we do not document any fair value exceeding the critical value of 0.80, which indicates no multicollinearity problems in the study [

93]. Furthermore, we checked the variance inflation factors (VIF) and found a maximum VIF not exceeding the threshold level of 4, which confirms no limitation from multicollinearity issues [

94].

Table 5 reports the OLS regression results of the study. As stated earlier, our dependent variable is CCD, which is regressed on several explanatory variables to reveal board experts’ motivation behind corruption disclosure. The findings show that the explanatory power of the study is 42%, which is very high compared to the recent anti-corruption studies conducted by Wang et al. [

33], Cao et al. [

34], Hung et al. [

21] Lopatta et al. [

49] and Chen et al. [

38].

The regression analysis finds that ACCTE on the board has a positive and significant influence on CCD (

). The result shows that having more accounting experts within the management environment is a strong instrument for anti-corruption compliance and procedures that are likely to increase transparency, accountability and disclosure. According to RDT, accounting experts who are on the board play a number of roles, such as leading experts to pressurize management into preventing fraud, corruption and informal transactions. Moreover, ACCTE are also highly professional individuals who possess sound knowledge and experience regarding accounting and auditing, which ultimately increases the soundness and accountability of the firm’s financial statements. Our results are consistent with the study of DeZoort and Harrison [

60] who argue that accounting experts significantly increase fraud detection responsibility and act as a strong mechanism in controlling corruption. Kusnadi et al. [

59] investigated ACCTE and the financial reporting quality (FRQ) of US firms, finding that ACCTE were positively and significantly associated with FRQ due to their strong professional knowledge and positive role modeling signals. Moreover, Al-Shaer and Zaman [

9] and Zhuang et al. [

95] have reported that ACCTE and the presence of professional individuals on the board profoundly increases the credibility of sustainability disclosure. The findings also show that external expert directors reduce agency conflict by disclosing authentic CCD. Therefore, our H1 is both accepted and in the line with RDT and we can say that ACCTE have the credibility to curb corruption and enhance the transparency of financial firms in Bangladesh.

Our next hypothesis concerns LEGE, where we found a positive and significant relationship with CCD (

). The result shows that having more LEGE on the board promotes higher CCD. According to the RDT, the presence of LEGE on the board acts as a watchdog on behalf of stakeholders, persuading management to promulgate, clarify and execute an anti-corruptive organizational atmosphere. As resourceful and experienced individuals on national and international legal matters, rules and standards, lawyers have an insight into the management of different financial and technological laws in order to prevent corruption, bribes and unethical activities. Moreover, LEGE work as consultants on the board to mitigate the conflicts between agents and principals. Our empirical finding is supported by the study of de Villiers et al. [

15], which documents how LEGE on the board of US firms monitor, understand and pursue environmental issues that strengthen the capabilities of corporate management. Agrawal and Knoeber [

31] have also investigated how having lawyers on the board helps to mitigate greater potential costs for the firms. Additionally, Ferguson [

32] treats lawyers as ‘transaction facilitators’ in helping to curb corruption and anti-corruption issues regarding business management. Our findings support H2 and we can, therefore, say that, regarding the proposition of RDT and agency theory, having LEGE on the board highly influences CCD and may increase the credibility, trustworthiness and accountability of Bangladeshi financial firms to their stakeholders.

Our next hypothesis concerns having POLTC on the board. Prior research has suggested a mixed result regarding the relationship between POLTC and CCD. We hypothesized that there would be a positive and significant association between POLTC and CCD. The result shows POLTC is positively and significantly associated with CCD (

). The empirical result indicates that POLTC board members share their expertise and experience regarding the control of corruption and bribery and can enhance CCD in order to show better organizational transparency and accountability. Moreover, CCD is likely to work as a tool for increasing corporate transparency and reducing the legitimacy gap among the stakeholders. Disclosing corruption, bribery and ethical information improves better quality governance that forces politicians to be more accountable. CCD is a strategic approach of the corporation that indicates management capability to mitigate corruptions, bribes and unethical transactions. Additionally, POLTC have strong relationships with the government and know the best practices regarding the law and rules relating to financial stability, which may provide management with strong assistance in fighting corruption and financial crimes. Our findings are supported by those of prior studies of Zhuang et al. [

95], Cheng et al. [

36], Gu et al. 2013 [

7] and Claessens et al. [

39]. Agrawal and Knoeber [

31] report that having POLTC on the board enhances negotiating and lobbying power with the government, while also reducing the explicit costs and trade barriers of the firm. Cheng et al. [

36] and Zhuang et al. [

95] have investigated Chinese listed firms’ political connections, finding that political engagement enhances information disclosure in order to show the transparency and accountability of the management.

Furthermore, the most recent study of Hu, Karim, Lin and Tan [

96] empirically tested the role of politically connected independent director on the board regarding investors’ perceptions. They documented the mixed results that the politically connected independent director brings political benefits such as debt financing access, government subsidies, market power and bailout by the government (also treated as the firm’s resources) while they reduce minority shareholders interest and weaken financial stability of non-politically connected firms through financial and regulatory constraints. More interestingly, they concluded that minority shareholders of non-political firms think that politically connected independent directors are “value-added to corporate governance” and “valuable firm assets” even though they expropriated their interests. In addition, DeBoskey, Luo, and Wang [

97] investigated the disclosure transparency of S&P 500 firms and reported that an independent political contribution committee can enhance the transparency and oblige the politicians to be more responsible, transparent and accountable. Thus, the results support H3 that the presence of POLTC on the management is not harmful to a firm, as they have strong negotiating skills and strong affiliations with the governments’ anti-corruption campaigns and initiatives.

Our next variable is an interaction between POLTC and LEGE. A moderator is considered a third variable (Z) that changes the association between a predictor variable (X) and an outcome variable (Y) [

98]. According to the prior literature in statistics, the moderating effects can be positive, negative, ordinal and disordinal [

98]. Moreover, a moderator may increase, decrease, or directionally change the relationship between the predictor and an outcome [

98,

99]. We tested the moderating role of POLTC on the relationship between LEGE and CCD. The findings show a negative and significant interaction variable (POLTC*LEGE) (

), supporting H4. The result indicates that although LEGE positively promotes CCD when it is considered as a stand-alone variable (H2), its positive role is compromised by the existence of political board members. In other words, having higher numbers of POLTC on the board reduces the positive role of LEGE control of corporate management because of a politically connected individual’s power and personal benefits and their party’s political agenda development [

6]. This result is more evident regarding developing countries with less control over corruption [

4,

6]. More politically connected firms face reduced external pressures, resulting in reluctance regarding the role of other stakeholders and experts in disclosure policy [

4]. The finding indicates that LEGE indirectly fail to promote CCD due to the greater influence of POLTC. In the RDT, this is understandable because a resourceful individual can direct the board both directly and indirectly. The study finds that, on average, 51% of firms have political directors, indicating higher political connections while LEGE, at only 26%, is comparatively very low. Moreover, higher political connections result is consistent with recent studies of Wang et al. [

33], Cao et al. [

34], Xu and Yano [

35]. Mottakin et al. [

4] empirically found that having higher political connections caused Bangladeshi manufacturing firms to sharply eschew from CSR disclosure because of their higher levels of corruption, low corporate governance, low external pressure and the lack of rule of law in the country. Furthermore, Uddin et al. [

6] have documented how Bangladeshi financial firms are highly controlled and managed by political individuals because of the agenda of their political parties and by demonstrating personal power. Our result is supported by the recent studies conducted by Fernández-Gago et al. [

10] and Shi et al. [

71], while the findings also report that having POLTC on the board indirectly and negatively motivate independent directors to promote CSR disclosure. Moreover, our findings are consistent with the most recent corruption and political connection studies of Hung et al. [

21], Wang et al. [

33], Cao et al. [

34], Xu and Yano [

35] and Chen et al. [

38]. These authors found evidence that highly political connected firms were unaware of voluntary disclosure that decreases growth, analyst forecasting accuracy, equity, innovation and internal control, each of which ultimately diminishes the role of LEGE. Therefore, we like to believe that the higher political management of Bangladeshi financial firms reduces the indirect role of LEGE to an extreme degree and untimely discourages CCD. The result explains that the presence of POLTC and LEGE on the same board weakens the expertise role of LEGE by the superior dominance of POLTC. From developing economy perspective, it is widely considered that political connection has a negative impact on corruption and firm value. The negative relationship shows the rent-seeking behaviors of the political directors through the institutional lens. This assumption may be suitable in the context of Bangladesh where institutional weakness and politicization dominates every sector of the country [

4,

6,

100]. Prior research, however, has documented the mixed empirical results indicating the negative role of a politician can be controlled by the effective governance and stakeholder engagement.

Our final hypothesis is CORVIS. We found a positive and significant association between CORVIS and CCD (

). The result shows the media plays an influential role in encouraging CCD. According to stakeholder theory, the media is the most prominent stakeholder that publishes news of the firm regarding corruption, bribes and any other irregularities. Therefore, in order to mitigate stakeholder pressure, firms like to disclose increasingly more CCD so as to show transparency and accountability. As a social watchdog, higher media visibility demonstrates corporation concerns over reputation and social legitimacy, which ultimately shows a firm’s commitment to fighting corruption. Our finding supports H5 and is consistent with the prior studies of Islam et al. [

17], Blanc et al. [

18] and Islam et al. [

19]. Islam et al. [

17], who have also investigated the relationship between bribery disclosure and the media visibility of two European mobile corporations, finding a positive and significant association. Higher media coverage highlights strong network governance of the given corporation, while also reducing external pressure. This finding is also supported by Zhou et al. [

72] and Blanc et al. [

18]. The result leads us to believe that the Bangladeshi media is playing an active role in the fight against corruption.

In the study we used several control variables. We found that SIZE is positively and significantly associated with CCD (

), while AGE is negatively and significantly associated with CCD (

). These results are supported by the previous studies of Hung et al. [

21], Cheng et al. [

36] and Xu and Yano [

35]. We also report an insignificant relationship between ROA and LEV with CCD, which is supported by Lopatta et al. [

49]. The Year dummy variable shows that, across the five years, only in 2016 is there a significant influence on CCD (

), the possible reason may be increasing pressure from the different stakeholders and regulators than prior years. The result supports the recent findings of Masud et al. [

5] and Masud et al. [

2], showing that stakeholders (media, NGO, civil society and environmental activist group) are more active and concerned with these issues (environmental pollution, corruption, bribery) than in the previous year and that the need to disclose CSR information is growing.

Alternative Measurement and Robustness Test

The study used several alternative measurement techniques based on the independent variables in order to test the robustness and trustworthiness of the research (see

Table 6). We considered alternative measurement techniques of the explanatory variables of ACCTE and LEGE, following Kusnadi et al. [

59]. We calculated ACCTE and LEGE as a total number, instead of ratio and dummy respectively and produced the same results. Therefore, the alternative test results show that the presence of corporate board experts is one of the key determinants of CCD in Bangladesh, while higher levels of political connection within the corporate management structure indirectly reduces the influence of a resourceful individual in terms of controlling corruption and bribes. The robustness result of the moderating variable reveals the exact significant results of the main study, strongly suggesting the limitations of high political connections regarding Bangladeshi financial sector firms.

4. Conclusions

Corruption is an important problem in developing countries and this is also true of Bangladesh. Like many other sectors, the Bangladeshi financial sector faces a number of challenges such as the threat of bankruptcy, illegal money transfers, money laundering, terrorism financing and a lack of corporate governance. Corruption disclosure is considered an effective and efficient market and policy mechanism for controlling corruption and enhancing transparency and accountability. CCD sends confident, positive signals to the market and is therefore welcome by stakeholders. Higher CCD practices depend on the proportion of external experts in the board and the quality of corporate management. Having resourceful individuals on the board not only influences decisions regarding corporate governance, but also sends a strong signal to the diverse stakeholders, due to the experts’ reputation, experience, education and visibility. The presence of such experts leads to higher levels of transparency and accountability, which reinforces CCD and ultimately mitigates agency conflict between the management and stakeholders and the associated costs. In terms of the burning issue of corruption, there is no existing research documenting these issues in Bangladesh, which makes this study both timely and meaningful. To the best of our knowledge, this is the first empirical study on CCD that combines the board expert variables (ACCTE, LEGE), corporate political connections (POLTC) and corporate media attention, from the perspective of a developing country. In order to provide sound empirical findings, the study considers financial-sector firms between 2012−2016, using multiple regression statistical techniques.

The study finds that resourceful board directors are highly influential and dependable in terms of disclosing information regarding corruption and bribes. We have documented how firms that have added at least one resource-based director on their board have more CCD compared to those that lack a resource-based director. This indicates that board members from the fields of accounting, law, or politics help to ensure greater levels of compliance regarding corruption, bribes and unethical transactions. In terms of general disclosure principles, this reminds us that corruption disclosure reinforces corporation willingness, attitudes, motivations, acceptance, transparency and managerial quality regarding undocumented and unethical behavior. Additionally, RDT confirms that quality management is highly concerned about organizational trustworthiness and accountability, which is often what inspires them to disclose more CCD. We have also reported the negative moderating effect of political connectedness on the positive role of legal experts. The interaction result indicates that higher political connectedness indirectly reduces the influence of resourceful individuals and their participation in the fight against corruption in Bangladesh. The result of political connection may seem contradictory, but it indicates that developing country’s perspective corruption disclosure would be an effective mechanism to the management and politicians show their transparency and accountability regarding corruptions, bribes, money laundering and unethical behaviors to diverse stakeholders. At the same time, the legal experts’ positive contribution can be compromised by the political connection. Our empirical finding also suggests that effective stakeholder pressures (social and traditional media, NGO, civil society, peer group, regional and international organization) can highly influence the corporate behaviors that may encourage exhibiting more transparency and accountability through CCD. We suggest that a corporation requires strong safeguard against higher political influences and responsible behaviors from the political director. Moreover, the media plays an influential role; firms face much media scrutiny, which encourages them to report more CCD.

The empirical study has both theoretical and managerial implications. As a keyword-based study, the paper contributes to the present discussion of RDT and agency theory literature. Moreover, following stakeholder theory propositions, the study found that having particular experts on the board promotes professionalism and ethics for reinforcing personal, as well as corporate, reputation and accountability. Moreover, the legal expert on the board is a contributing variable, particularly in the developing country’s corruption perspective. Additionally, since the high political connection is a common phenomenon in the developing country’s business management, the study will enhance the political management literatures in the control of corruption. The research will also enhance the organizational behavior and ethics as the control of corruption enhances the transparency and accountability of the management. Last but not least, we can say that the study contributes to the theory of general disclosure, as well as to sustainability management literature. The study has significant managerial implications, especially regarding a developing country’s corporate governance and policy. ACCT and LEGE profoundly influence CCD practices and this study makes a good case for including more accounting and legal experts on company boards. More professional and resourceful persons in the corporate board significantly improve the transparency and accountability of the corporation. The study found that more accounting and legal experts in the decision-making process improve information flow that helps the internal and external communication strength to mitigate stakeholder’s pressure. Moreover, the professional accounting and legal experts can raise and solve many issues regarding financial and legal in relation to corruption, bribery, money laundering, taxation and audit. The study helps policymakers in the country to consider formulating a sound corporate governance regulation. Additionally, Securities and Exchange Commission and stock exchange listing authorities may want a mandatory provision of including legal and accounting experts on the board while restricting the higher political connections of the business management. We have also empirically shown that having a higher proportion of POLTC on the board diminishes the attitudes of the LEGE. Therefore, management should consider the implications of having higher political connections, as this negatively influences their motivation and mechanism for fighting corruption and bribery and increasing transparency and accountability.

Though it has significant contributions, this study also has some limitations. The limited number of firms, year observations and the fact the study only covers a single sector mean it cannot provide an overall picture of the country’s level of corruption. Therefore, future research should consider these questions by referring to a more complete list of sectors within the country to offer a more meaningful conclusion regarding CCD. Moreover, a cross-country examination would be another beneficial approach for gaining a better understanding of the culture differences in CCD.

{kind=link}