1. Introduction

According to the Intergovernmental Panel for Climate Change (IPCC), anthropogenic emission of greenhouse gases has contributed to a global temperature increase, rising sea levels, and more frequent occurrences of extreme weather events [

1]. The Paris Agreement puts forward a global plan to limit the growth in global temperature below 2 °C and to pursue the efforts to limit it to 1.5 °C to prevent further negative consequences of climate change [

2].

Recent work on the economic consequences of climate change provides quantification on the possible costs if climate change is not controlled. Using detailed data on a global scale where the unit of observation was 1° latitude by 1° longitude cells, Nordhaus [

3] finds a negative relationship between economic output and mean surface temperature. Using the estimated parameters and assuming an increase in the average temperature of 3 °C and a decrease in precipitation, he forecasts a reduction of economic activity between 0.9% and 3%. Based on the panel data of 100 most populous countries, Horowitz [

4] estimates that a rise in the surface temperature of 1 °C would reduce the world GDP between 2.7% and 4.2%, with the best estimate being 3.8%. Hsiang [

5] investigates the impact of variation of surface temperatures on the output of 28 Caribbean basin countries. After controlling for the effect of cyclones, he finds that a 1 °C rise in surface temperature is associated with a simultaneous decrease in GDP of 2.5%. He also finds that higher surface temperature is associated with a statistically significant decrease in economic output in three out of seven economic sectors. Dell et al. [

6] find large and negative effects of higher temperatures on economic growth: they estimate that a 1 °C rise in temperature in a given year reduces economic growth in that year by about 1.3%, though the relationship is more ambiguous for rich countries. The possibility that climate change does not harm rich countries has prompted some researchers to investigate this issue further. Burke et al. [

7] address this topic through the analysis of historical data to determine whether country-specific deviations from growth trends are related non-linearly to country-specific deviations from temperature and precipitation trends, after accounting for any disparities common to all countries. They find country-level economic production is smooth, non-linear, and concave in temperature, with a maximum at 13 °C. Both rich and poor countries exhibit similar non-linear responses to temperature. Therefore, the link between rich countries and temperature change is weaker primarily because rich countries exhibit lower temperatures. Lemoine and Kapnick [

8] also find that future warming could raise the expected rate of economic growth in rich countries, reduce the expected rate of economic growth in poor countries, and increase the fluctuation of growth by increasing the climate’s variability.

To limit the growth of surface temperature caused by anthropogenic emissions of CO

2, policymakers often put either a carbon tax or an emissions trading scheme in place. The application of such mechanisms has proven to have negative economic consequences. Adams [

9], by using a Computable General Equilibrium (CGE) model coupled with an electricity generation model, identified that the introduction of an Emissions Trading System (ETS) scheme in Australia would result in a real GDP decrease of 1.3% and a consumption loss of 1.4% by 2030. Real wages would decline by 3.3% and CO

2 emissions would be reduced by 21% compared to the baseline scenario. In a similar study, Adams et al. [

10] analyzed the impact of carbon pricing on the Australian economy as part of a global ETS scheme, which resulted in 25% lower emissions in 2030, resulting in a reduction of GDP by 1.1% compared to a base case scenario, together with a reduction in household disposable income by 2.3% and real private consumption by 1.3%. They also show that despite affecting most industries, a carbon pricing policy has positive effects on some sectors, notably forestry, electricity generation from renewables, and electricity generation from gas (due to a move away from coal) as well as iron, steel, and aluminum, which become more internationally competitive due to cheaper raw material. Lu et al. [

11] assess the impact of the introduction of a carbon tax on the Chinese economy and find that a carbon tax of up to 300 Chinese Yuan per ton of CO

2 (approximately 30 EUR in 2019) results in a relatively modest reduction of GDP of 1.1% compared to a scenario without a carbon tax. Similarly, Guo et al. [

12] investigate the impact of the introduction of a carbon tax and also find negative effects on most of the economic sectors as well as the overall GDP and returns to labor and capital. In the European context, Panagiotis et al. [

13] utilized an energy-system model with a CGE model to demonstrate that the Intended Nationally Determined Contribution (INDC) submitted by the European Union (EU-28) can be met with a minor GDP impact of 0.4% in 2030 and 1% in 2050 compared to the reference scenario.

Given research has shown that schemes to limit the emission of CO2 into the atmosphere such as a carbon tax or an emission trading scheme entail a reduction in GDP growth and consumption, the issue of distributional impacts of such schemes arises. For example, poorer households tend to live in less energy-efficient homes, own energy-inefficient vehicles and appliances, and have lower incomes. Therefore, the increase in prices of energy-related goods hurts poor households disproportionately more than rich ones. In addition, due to the rise in prices of energy-related goods, poor households have to reduce their consumption of other goods. To make carbon tax-related policies acceptable and equitable, it is important to consider how they affect different members of society and to ensure that these policies are not regressive.

Related research includes Goulder [

14], who emphasizes the importance of revenue recycling and tax interaction effects, both of which represent a fiscal interaction effect when assessing the cost-effectiveness of climate change policies. Revenue recycling refers to returning the revenues collected through climate change measures back to the economy, whilst tax interactions refer to the impact of climate policies on returns on factors of production. While the principles of revenue recycling effects are self-explanatory, the tax interactions argument states that climate policy measures increase the cost of carbon-related goods, hence driving up prices. This reduces the real wages of workers as well as returns to the owners of capital employing carbon-related inputs, both of which represent an efficiency loss. The efficiency loss could be reduced or even mitigated by applying appropriate fiscal policies such as the reduction of marginal tax rates on labor and capital, providing lump-sum transfers to households, or some combination of the above, depending upon the goals of the policymakers. Caron et al. [

15] provide a five-model assessment of distributional impacts of carbon pricing in the U.S. To alleviate distributional impacts on different households they evaluate the efficiency and equity (progressivity) of lump-sum household transfers, capital, and labor tax reductions. They find that lump-sum transfers to the household consumer are progressive, but come at the greatest costs, while capital tax reductions are mostly regressive and help the richest households. Labor tax credits are somewhere in between these two measures. Nevertheless, the authors conclude that by using a creative approach such as lump-sum transfers to the poorest households and capital tax reductions, the policymakers can reduce the progressivity of carbon pricing at a rather low cost. Reaños and Lynch [

16] evaluate the impact of a carbon tax in Ireland on sectors not covered by the ETS system. They also find that a carbon tax is regressive, hurting poor households the most. To alleviate the tax burden on households, they evaluate the impact of a flat rate and a targeted revenue recycling mechanism. Here they find poor households are better off receiving targeted support as opposed to a lump-sum payment, i.e., targeted measures are better suited to eliminate income inequality arising from the introduction of a carbon tax. In terms of administrative costs, they posit that a targeted approach would be more efficient as it would be conducted through the existing welfare system channels, while a lump-sum transfer to all households would require the establishment of a new channel to disburse the funds. Work by Tran et al. [

17] analyzed the impact of emission reduction in Australia by 2020 by using a static CGE model. Without revenue compensating mechanisms, they find a decline in Australia’s GDP by 0.285%–0.3% by 2020 as well as a decrease in welfare for all 20 household categories. To address the issue of welfare loss in different households, they assess the use of direct lump sum transfers, government transfers, and reductions in income tax. They find a trade-off between efficiency and equity. While income tax policies are the most efficient in the sense that they achieve the highest reductions in the GDP losses, they are the least equitable as they mostly benefit the wealthiest households. On the other hand, lump sum transfers aid the poorest households, while government transfer policy mostly aids middle-income households.

Finally, there is a group of studies focused on a tax reform that shifts the burden of taxation from conventional taxes, such as on labor or value-added tax (VAT), to environmentally damaging activities. Such reform is also known as environmental tax reform (ETR) or green tax (or budget) reform (GTR). Maxim and Zander [

18] analyzed the effects of substituting existing taxes by environmental taxes in European and non-European countries and found that an ETR has an average positive impact in employment for the European countries of 0.67% compared to the reference, but this number is highly dependent of the tax being substituted and varies from −0.15% for personal income tax (PIT) to 1.62% for VAT. Freire-González and Ho [

19] use a CGE model to assess the effects of an ETR in Spain for three different levels of carbon taxes and four revenue recycling scenarios and discover a positive economic output in all scenarios for a tax level of €10/tCO

2 and some scenarios for a tax level of €20/tCO

2. Streimikiene et al. [

20] researched on the impacts of environmental taxes in the Baltic region (Lithuania, Latvia, and Estonia) between 2005 and 2015 and revealed that an increase in the proportion of environmental taxes had a significant positive impact on sustainable energy development in that region.

In summary, the research up to date provides us with the following conclusions:

The historic effects of climate change on economic growth have been documented, and they affect not only the magnitude but also the rate of economic growth.

Unmitigated climate change results in significant negative environmental consequences that have negative repercussions on economic growth.

To mitigate the economic consequences of climate change, policymakers should enact policies that will eliminate and hopefully reverse the effects of climate change. But these policies come at a cost and are regressive in nature, mostly hurting poor households.

Policymakers have different options of revenue recycling mechanisms which fall in a range between efficient but inequitable (mitigation of negative effects of climate policies on economic output at the lowest costs but hurting poor households) and equitable but inefficient (a measure that supports more poor households than rich but comes at a higher cost).

Our paper adds to the current debate in several aspects. To our knowledge, this is the first comprehensive paper that addresses the consequences of the Paris Agreement on European economies, taking into account different pathways and their impacts on social disparities. In this sense, it expands the existing literature by making a multi-regional analysis of selected European countries between the years 2011 and 2050 while considering different emission targets inside and outside of the EU-28. Additionally, this work gives special attention to the distributional impacts from energy policies on different income groups by analyzing the income development, consumer behavior, and incidence of carbon prices for each income group.

A global multi-region recursive-dynamic CGE model with the household sector disaggregated into five income quintiles, similar to the approach from Bouet et al. [

21], was applied for this work. Additionally, we employed one reference scenario and four scenario variations with different degrees of CO

2 emissions cuts. The results indicate that higher emission reductions, compared to the reference scenario, lead to slower GDP growth, but also induce a more equitable increase of gross income. In this case, the gross income of the poorest quintile grows as much as, or even more in some cases, than the gross income of the richest quintile, given that the revenues from pricing carbon are paid back to the households.

2. Materials and Methods

In this work, we use the CGE model NEWAGE (National European World Applied General Equilibrium, for more details about the NEWAGE model, visit

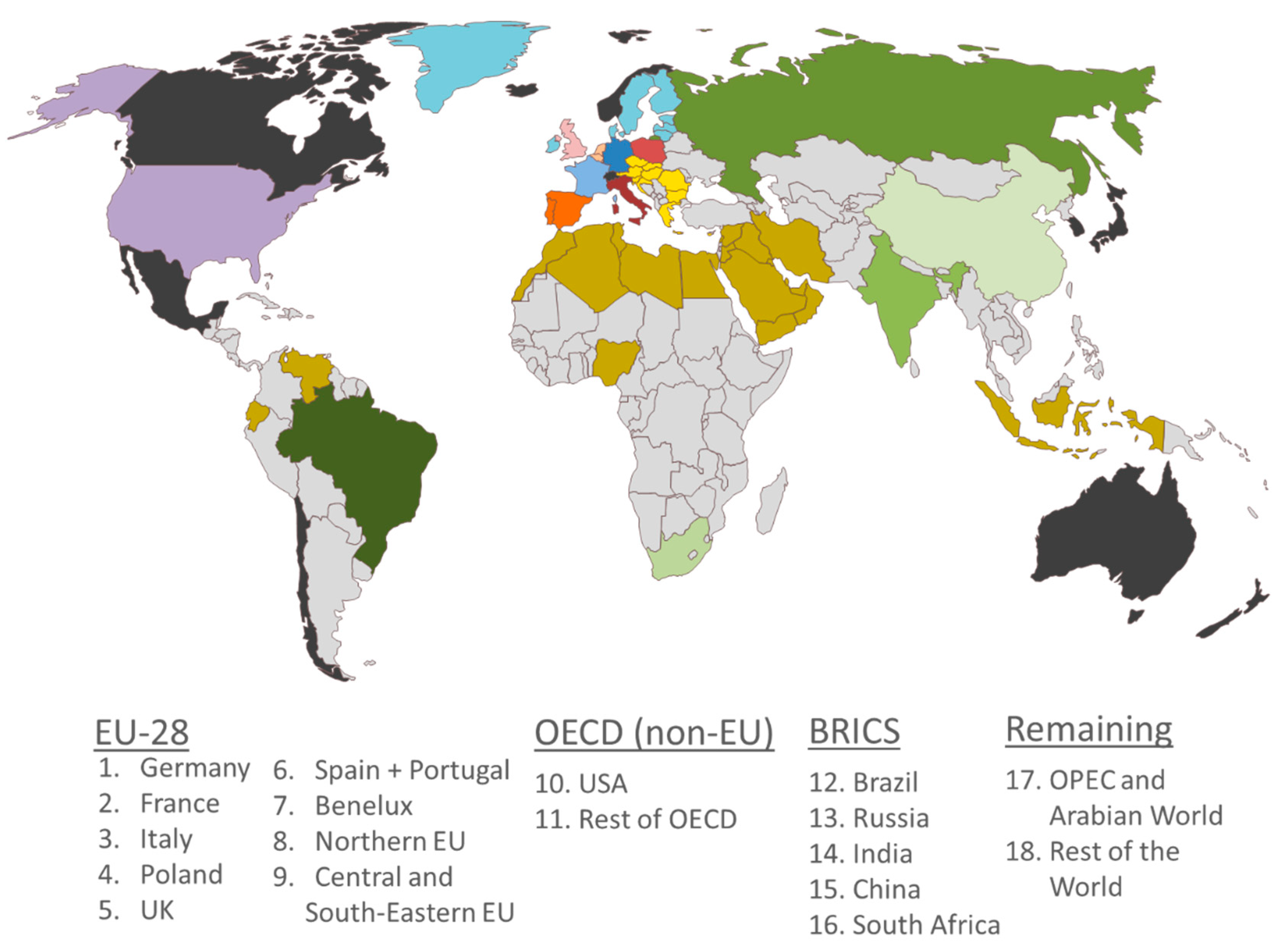

https://www.ier.uni-stuttgart.de/forschung/modelle/NEWAGE/index_en.html) to analyze different scenarios. NEWAGE is a multi-region, multi-sector, recursive-dynamic general equilibrium model that depicts the production and distribution of commodities in the global economy. A total of 18 regions of the world are modeled, as shown in

Figure A3, from which 9 regions are within EU-28, as shown in

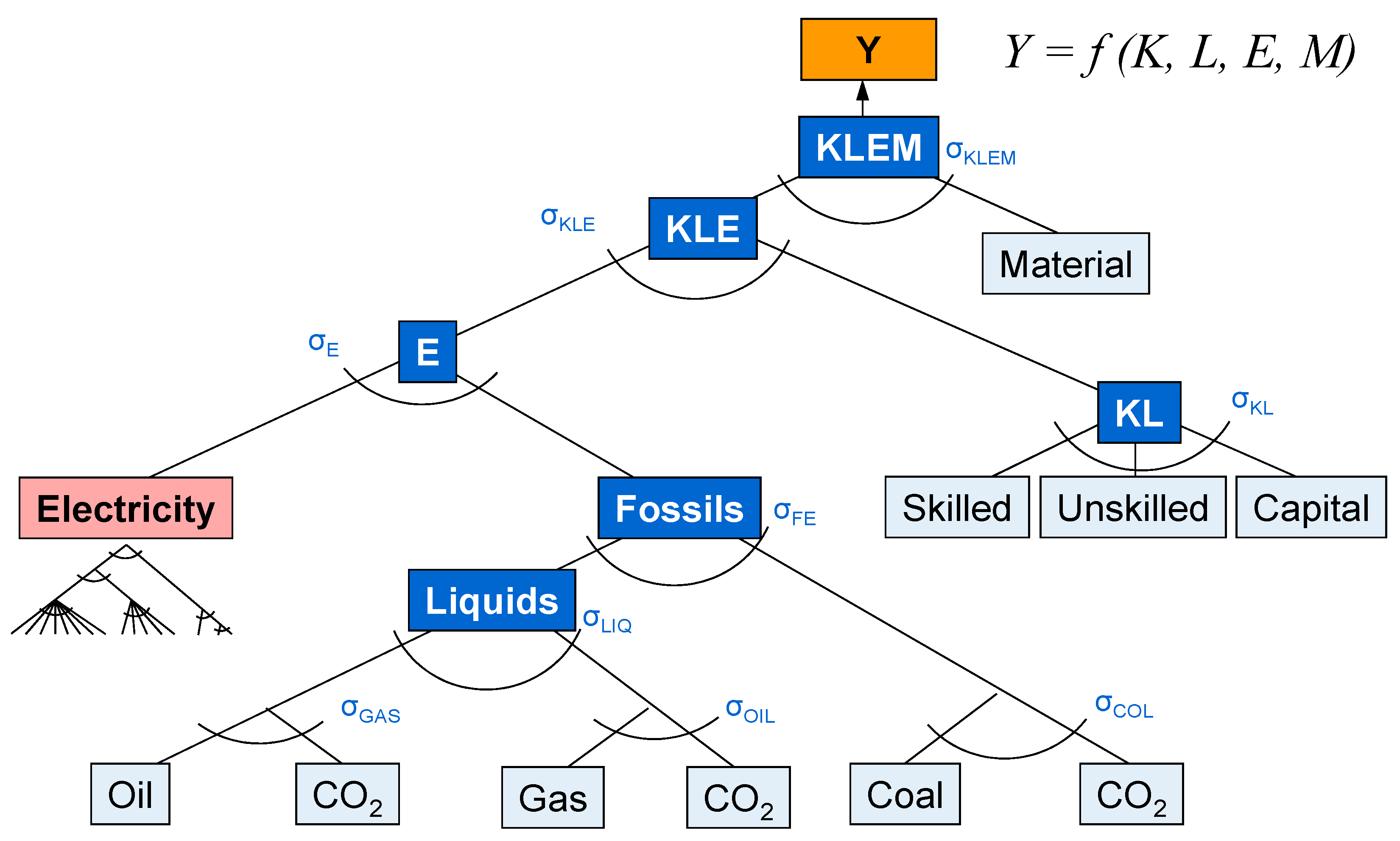

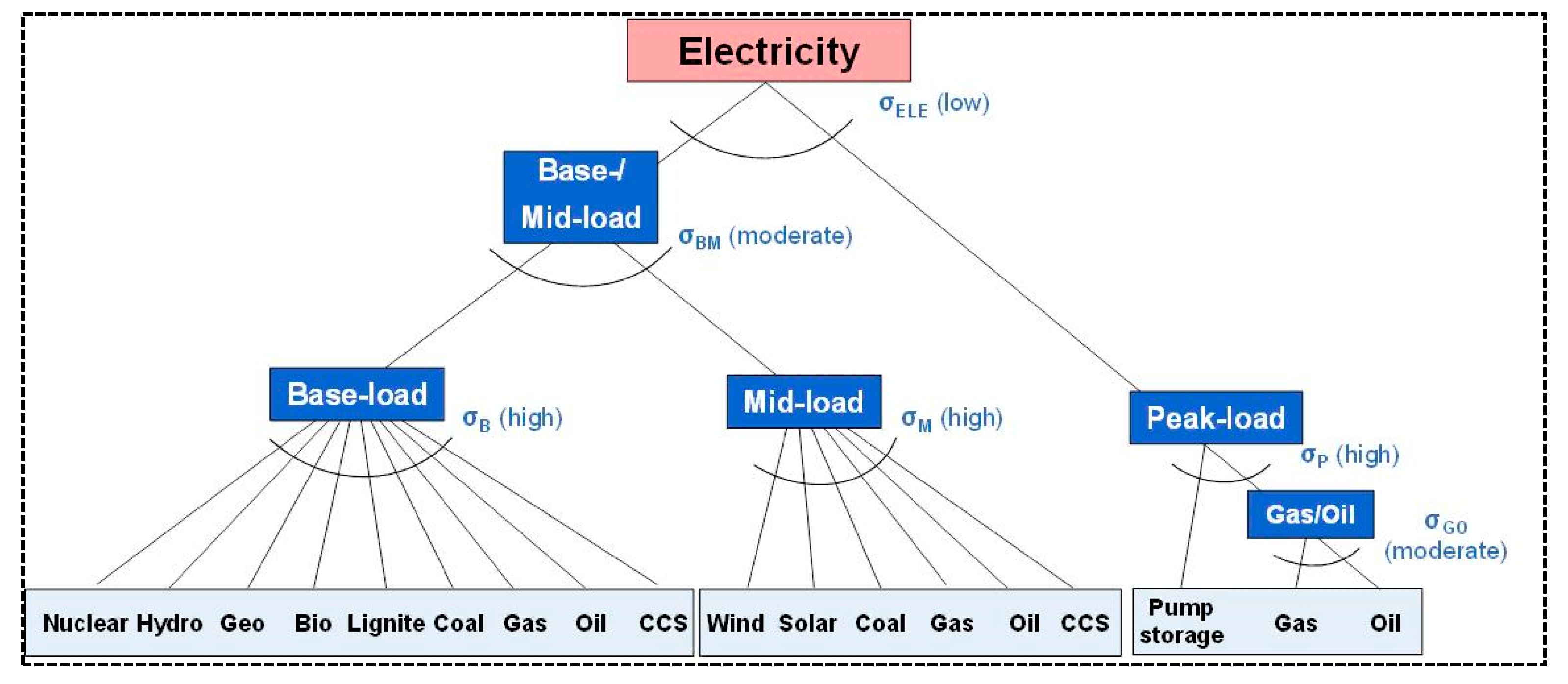

Table 1. The production sector is disaggregated into 5 energy production sectors, 6 energy-intensive industry sectors, 3 sectors representing the rest of the industry, and 4 sectors representing the rest of the economy. Additionally, it has a detailed representation of the electricity sector, consisting of 18 electricity generation technologies. Production possibilities are represented by Cobb-Douglas, Leontief, and Constant Elasticity of Substitution (CES) production functions. Detailed information regarding NEWAGE’s regional and sectoral structure, as well as the CES nesting for sectorial and electricity production, can be found in

Appendix A of this paper.

The framework of NEWAGE enables the analysis of the impacts of different political interventions on macro-economic indicators, such as GDP growth, employment, or competitiveness. In contrast, energy system models are usually unable to assess overall macro-economic costs because they usually lack the relationship with other actors of the economy, despite having a richer depiction of the technologies within the energy sector. Therefore, NEWAGE is a valuable tool for the analysis of energy policies and its implications to the rest of the economy, especially regarding effects on the households sector.

Despite being able to represent the relationship among different sectors of the economy, NEWAGE cannot endogenously calculate technology development. The model is capable of substituting energy purchases by capital in the current time-step using CES nesting, however, it is not capable of investing in technology development to improve the energy efficiency of specific production sectors and reduce its sectoral energy consumption in the next time-step. To overcome this limitation, NEWAGE applies exogenous assumptions for the technology development from 2011 to 2050 through the Autonomous Energy Efficiency Index (AEEI) parameter, which was developed based on the energy efficiency improvements provided by the EU Reference Scenario [

22]. For this work, the same set of AEEI was applied in all pathways, meaning that regardless of the environmental ambition, the rate of technology development remains the same. Additionally, the figures of electricity generation in the EU-28 between 2011 and 2050 utilized in this work were obtained through an iterative process that coupled the NEWAGE model with the energy system model TIMES-PanEU, as explained in [

23].

The present version of NEWAGE model perceives the gains and losses of any policy measure solely as a matter of profit and costs. It means that the model is not capable of accounting the non-financial impacts brought by different pathways, such as increased air quality and lower water pollution, in the cases where emission levels decrease, or higher temperatures, in the case where countries fail to reduce emissions.

A central assumption influencing the choice of production factors and technologies are the Elasticities of Substitution (EoS) of the production functions. They define how easily production factors, e.g., capital and labor, or different technologies, e.g., photovoltaics and wind turbines, can substitute for each other.

Figure A1 and

Figure A2 show a graphical representation of NEWAGE’s production functions. Substitution parameters vary between zero and infinity, with a value equal to zero meaning substitution is not possible. The higher the elasticity value, the easier it is to substitute the two respective factors. The elasticity parameters in NEWAGE, primarily based on reference [

24] and reference [

25], are summarized in

Table A3,

Table A4,

Table A5, and

Table A6.

In addition to the assumptions above, we use the following data sources for additional input parameters:

GTAP 9 Data Base [

26] for trade and energy data for the year 2011;

Electricity Information 2013 [

27] for electricity generation per country for the year 2011;

EU Reference Scenario 2016 [

22] for GDP growth for the EU-28 regions between years 2011 and 2050 and CO

2 emission for the EU-28 regions between years 2011 and 2050;

The Great Shift: Macroeconomic projections for the world economy at the 2050 horizon [

28] for GDP growth for the non-EU-28 regions between years 2011 and 2050 and CO

2 emissions for the non-EU-28 regions between years 2011 and 2050;

Household budget survey (HBS) [

29] for disaggregation of expenses;

Survey on income and living conditions (SILC) [

30] for income disaggregation.

In the context of CGE models, the representative agent is in many cases a combined depiction of government and households. It collects regional taxes, has a combined consumption of the two economic actors and represents and possesses endowments of three production factors: capital, labor and natural resources. Additionally, NEWAGE differentiates labor into two categories: skilled and unskilled, natural resources are divided into three categories: oil, natural gas, and coal, and adds CO2 allowances as a fourth production factor for the implementation of cap-and-trade policies.

For the task of analyzing distributional effects on households, we amended the present representation of the representative agent in NEWAGE by disaggregation into six new blocks: one for the government and five for each of the income quintiles. More specifically, we divided the households into five equally sized groups, containing 20% of the population each, according to their income sorted from lowest (hh1) to highest income (hh5), as shown in

Figure 1. No distinction between urban and rural populations was made and the calculus for income included gains from labor, capital, and government subsidies.

In order to perform the disaggregation of the household sector into five income groups, the first step was to separate the consumption of the representative agent between government and households, creating one block for each of these two agents. This task was executed by accessing the GTAP 9 database [

26] to apply the consumption values for both agents and, later, implementing the two blocks replacing the original representative agent. Afterwards, as the data available for consumption and income sources was aggregated on a national level, it was necessary to use Eurostat’s Household Budgets Survey (HBS) [

29] and Survey on Income and Living Conditions (SILC) [

30] to disaggregate it into income groups. The two later databases were granted to the Lithuanian Energy Institute by Eurostat to be used in the REEEM Project (For more information, see

reeem.org), to obtain data regarding the expenditure of households and their sources of income.

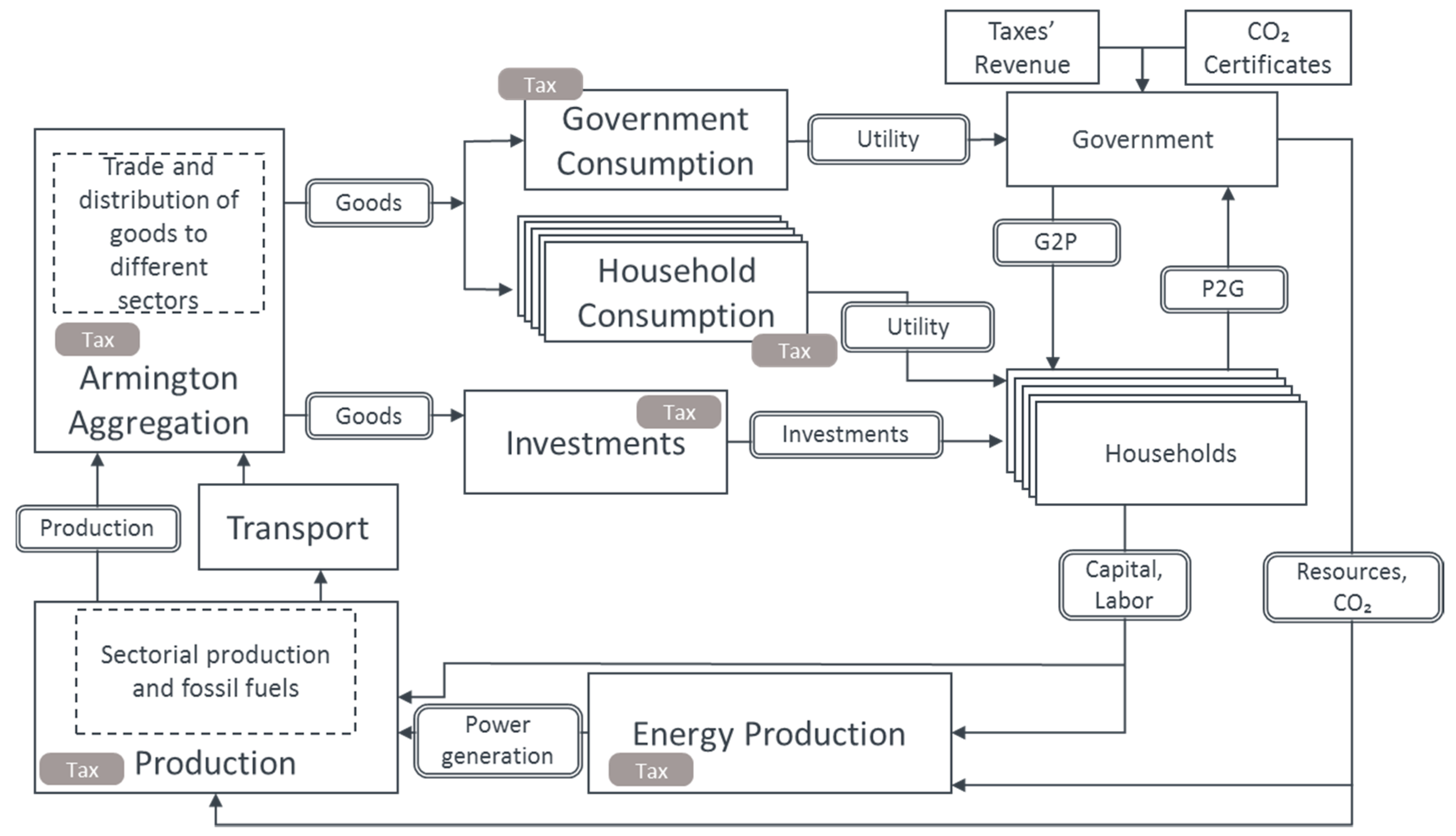

With the implementation of the six blocks representing the government and five income groups, the last step was to add the channels that allow for income flow between these blocks. This flow of income represents the taxation of income, from both labor and capital, from households to the government, and the payment of social benefits and pensions from the government to households.

Figure 2 shows a graph of the amended structure of NEWAGE containing a detailed representation of the new process of collecting and distributing tax revenues. The government receives tax revenues, as well as revenues from CO

2 allowances. Income taxes are paid by the households (P2G) and, in return, the government distributes some of the net revenues to the households (G2P) according to the shares that each income group is endowed to receive.

The first data processing step was the calculation of expenditure and income in different household groups of NEWAGE regions. To ensure the confidentiality of respondents and to make our calculations comparable to other datasets, all indicators are calculated at the decile level and, due to project requirements, aggregated to quintiles just before implementation in NEWAGE. To group individuals covered by the dataset to deciles, equivalized disposable income [

31] has been calculated by dividing the net income of a household by the equivalized household size (the number of adult equivalents in the household). Equivalized household size has been calculated using a modified OECD scale in which the first adult is equal to 1, the second and each subsequent person aged 14 and over is equal to 0.5, and each child aged under 14 is equal to 0.3. Finally, decile groups were formed taking into account equivalized income, household size, and sample weight.

The same methodology was applied for both SILC and HBS datasets. In the case of the HBS dataset, monetary net income (total monetary income from all sources minus income taxes, EUR_HH095) variable represents households’ disposable income, while for the SILC dataset total disposable household income (HY020) is applied.

The disaggregation of consumption expenditures by deciles was carried out assuming that total expenditure by commodity remains the same as in the aggregated version of NEWAGE. This assumption ensures the consistency of the model that relies on fully balanced GTAP data. Different consumption levels in different deciles were included as proportions of the total consumption expenditure calculated from HBS.

The shares in consumption expenditure on different commodities within each decile suffer mainly from data inconsistency and different classifications: The HBS deals with the classification of individual consumption by purpose (COICOP) [

32] categories, while the NEWAGE model uses an aggregated GTAP commodity classification. To gain consistency within the two datasets, a mapping matrix was developed. This matrix maps every commodity in the NEWAGE model with one or more COICOP categories within the HBS dataset. For instance, it is assumed that “oil” in NEWAGE represents “Fuels and lubricants for personal transport equipment” and “Liquid fuels” in the HBS data set. To get a balanced image of consumption structures among decile groups, iterative scaling (an RAS procedure) was performed by fixing total consumption by commodity-based on GTAP data and total consumption expenditure per household decile based on GTAP data on total consumption and consumption shares among deciles obtained from HBS microdata.

Income disaggregation was performed following the income categories represented in the new structure of NEWAGE. For this, we selected the most similar income categories in the SILC survey. In some cases, it was possible to get a rather good fit with the microdata (e.g., for skilled labor income), while in other cases like return on capital, microdata served only as a proxy since the SILC survey covers the income from rental of a property or land and interest, dividends, profit from capital investments in unincorporated business only. To get a more comprehensive and balanced view of income and consumption expenditure, aggregate propensities to consume by income quintile were calculated using HBS microdata. These values were applied as benchmarks with a focus on the poorest quintile and implemented in income disaggregation by using income taxes as a balancing element.

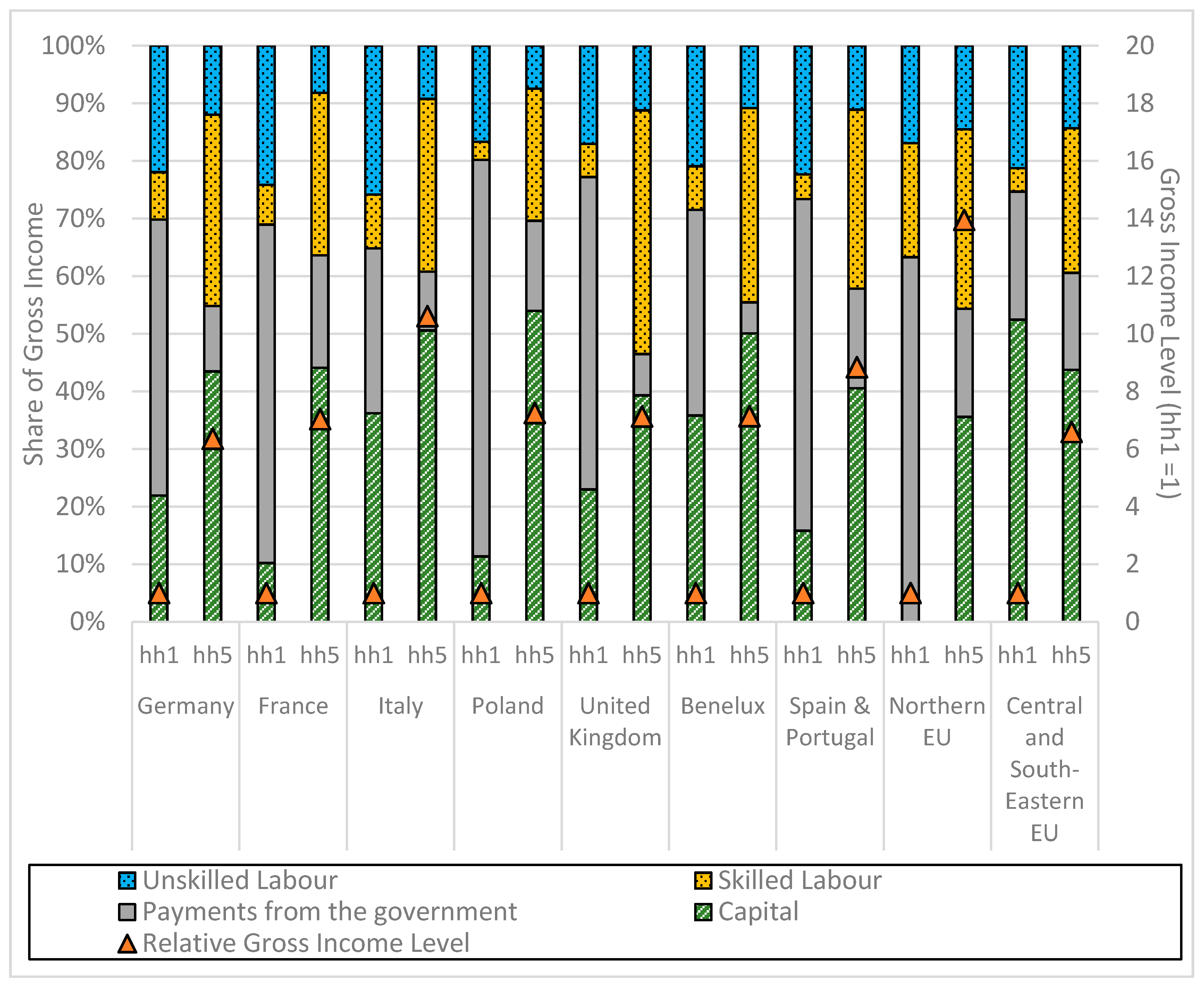

By the end of the disaggregation process,

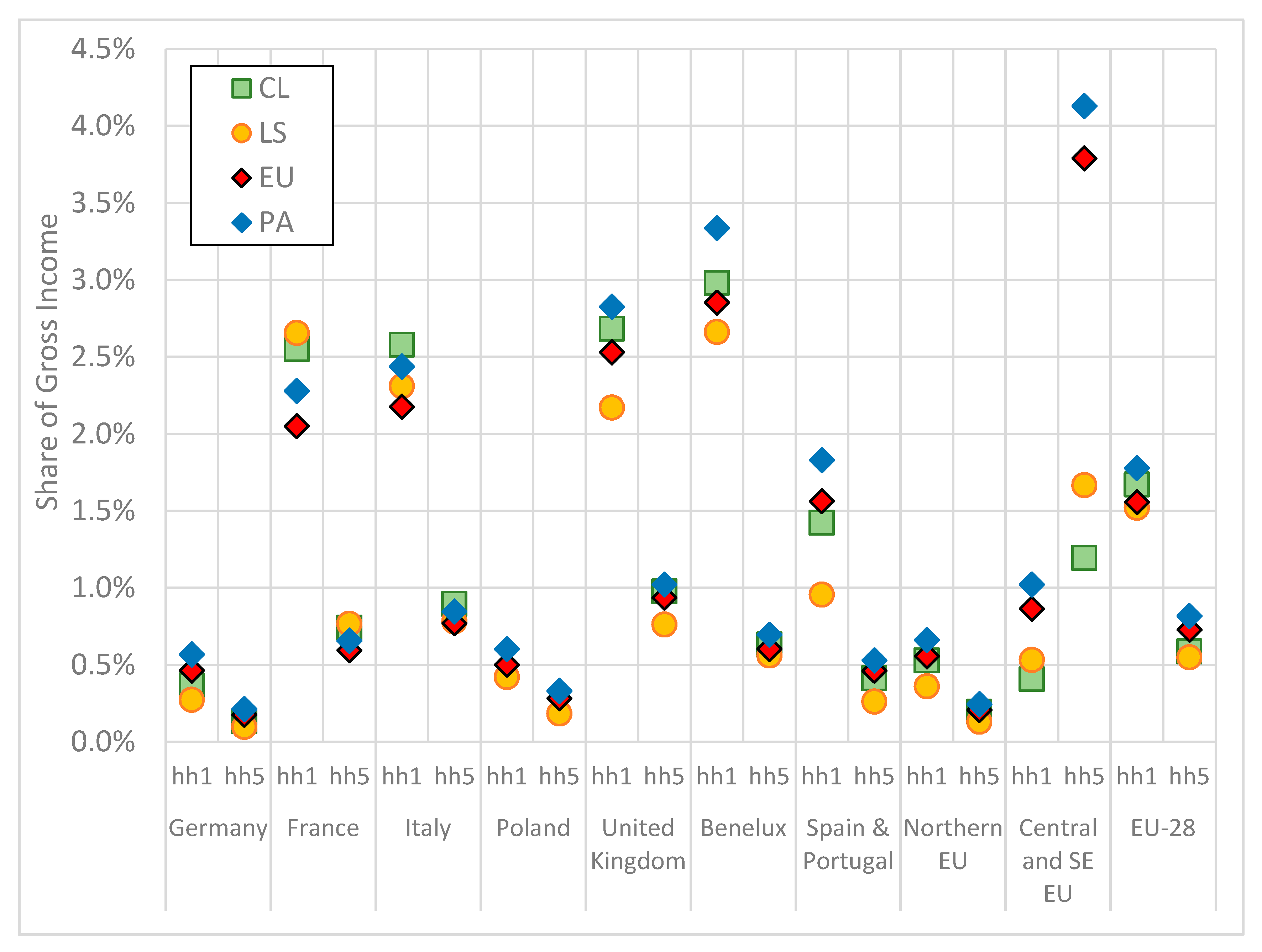

Figure 3 depicts the average composition of the gross income of the five income groups in the EU-28. The figure indicates that the lowest income group has a higher share of gross income from government payments or tax revenues, and the highest income group has the largest share of its gross income from capital revenues, followed by labor payments from skilled labor. Additionally, the regions or countries where the poorest quintile has the highest shares of government payments are the Northern EU, Poland, Spain, and Portugal, i.e., the low-income groups in these regions have the highest potential to benefit from a distribution of revenues from carbon pricing policies.

The disaggregation to quintile groups for each NEWAGE region imposes a methodological issue regarding regions that cover more than one country. This is the case for the region “Central and Eastern Europe”, where the disaggregation into quintile groups within this region means that a household from the lowest income group in the wealthiest country might fall to the highest income group on the regionally aggregated scale. The alternative approach, dealing with country-level income groups within the aggregated region, would result in a diversity of income levels within one group. Despite this disadvantage, we decided for the modeling to keep the actual regional disaggregation in this work, as presented in

Table 1, to ensure consistency with previous work conducted in the framework of the REEEM project with NEWAGE, such as [

33]. “Northern EU” also represents such a comparable case.

Figure 3 depicts the effects of this decision, as it is possible to see that the richest quintile, mostly composed by Sweden and Denmark, has a gross income level roughly 14 times higher than the poorest quintile, mostly composed by the Baltic countries.

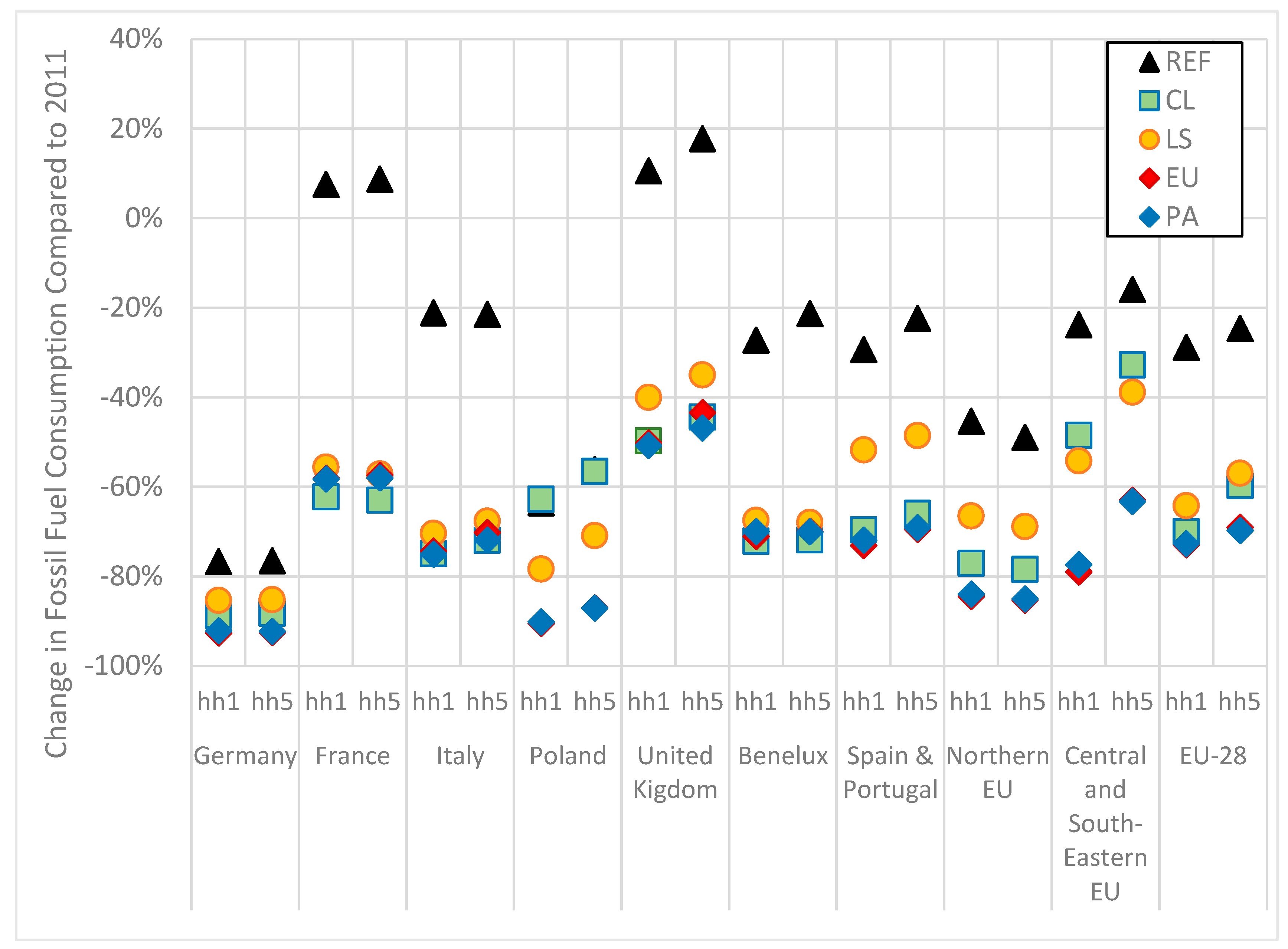

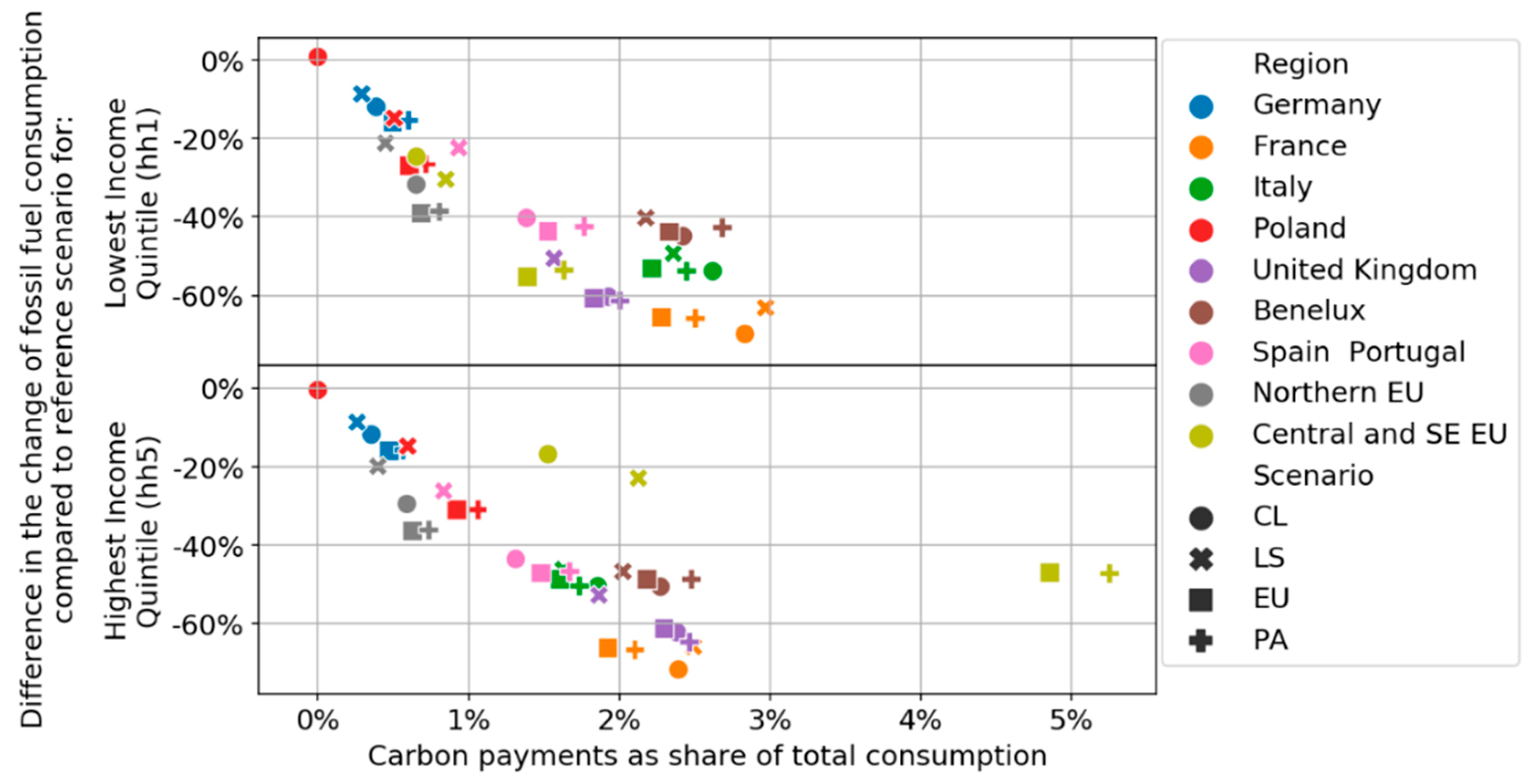

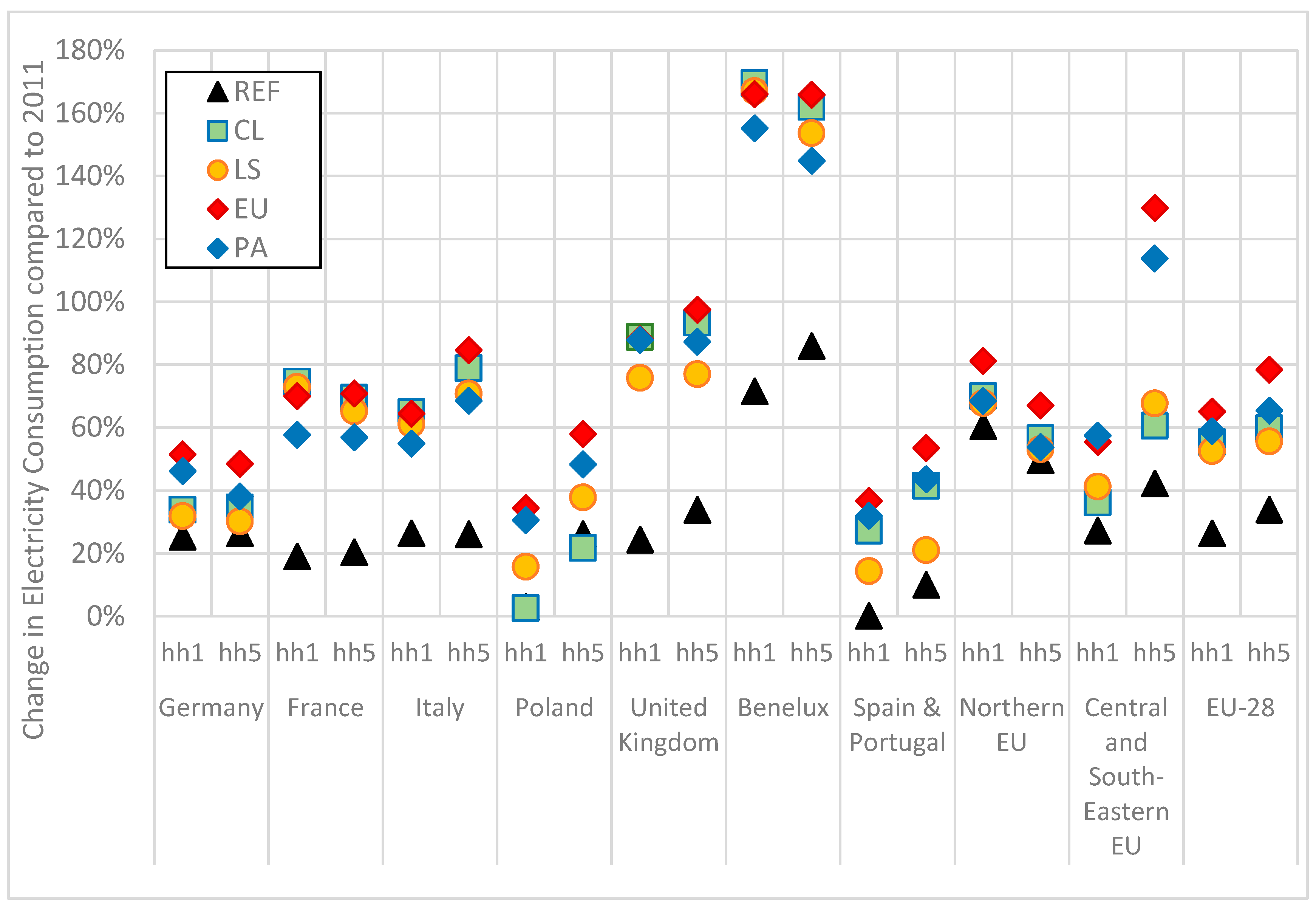

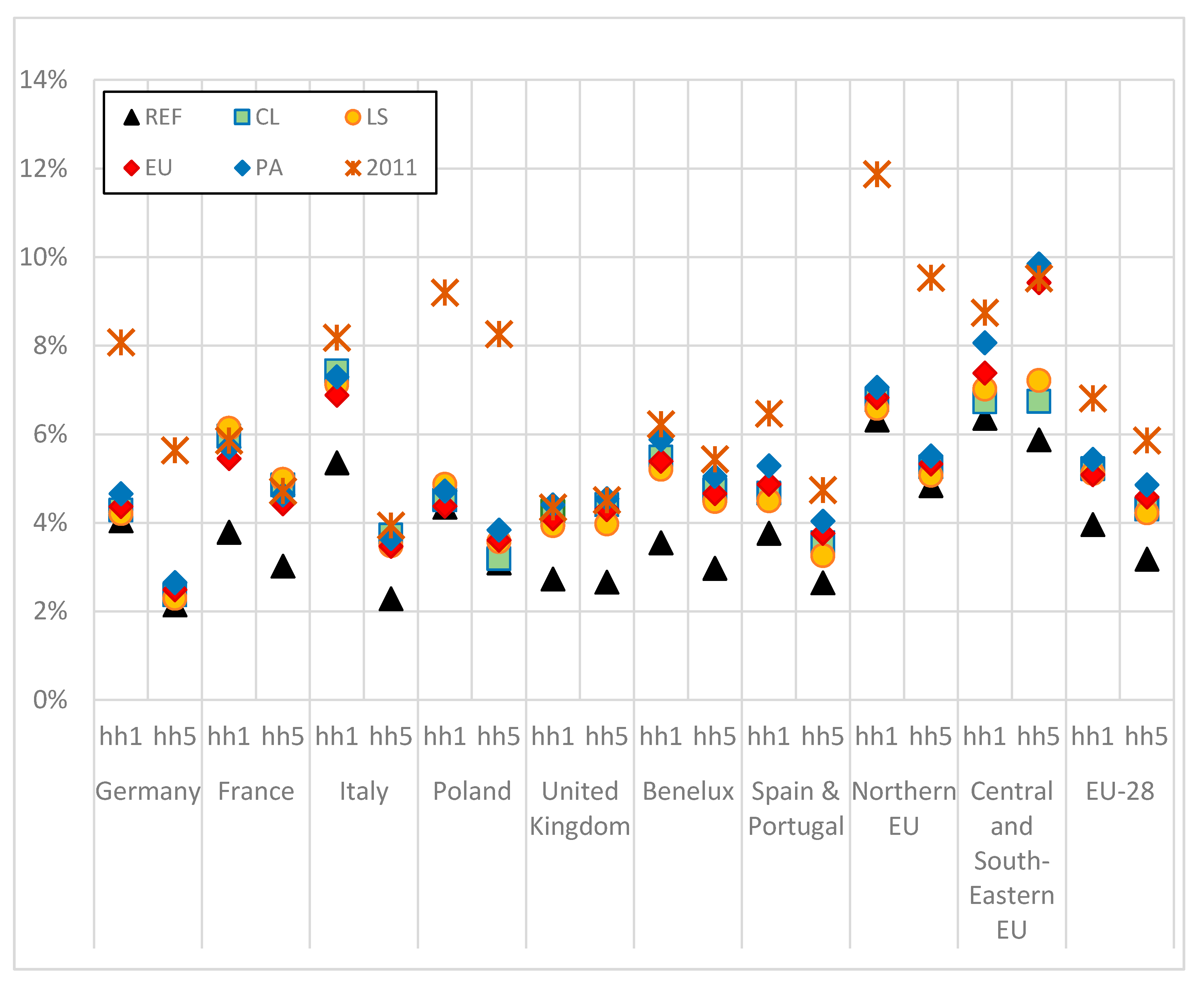

5. Conclusions

Throughout this work, different effects of energy policies based on the cap-and-trade system were analyzed by different parameters, namely GDP growth, consumption of energy goods, the incidence of a carbon price, and the development of income. The analysis was based on a reference scenario and four scenario variations: Coalitions (CL), Local Solutions (LS), EU-28 Going Alone (EU), and Paris Agreement (PA) pathways. They differed between one another in aspects such as sectoral coverage of carbon cap-and-trade scheme, reduction targets for 2050 and international cooperation against climate change. Additionally, the NEWAGE model had to be further developed to account for income quintiles and be able to assess the effects that carbon pricing has over consumption and income development for different income groups in multiple regions.

The results indicate the existence of a trade-off between economic growth and CO2 reduction and identified the cap-and-trade scheme and international commitment to reduce CO2 as key drivers for economic development. More specifically, a European cap-and-trade system where all the sectors of the economy are included produces a higher economic output for the majority of regions in the EU-28 and the higher the commitment of non-EU-28 to reduce their emissions, the lower their capacity to import European goods.

Additionally, it demonstrated that the cap-and-trade schemes analyzed in this work are regressive, but the one presented in EU and PA pathways provide an income increase for low-income households. These findings are relevant for the acceptance of carbon pricing measures in the household sector because they show that poorer households can obtain financial benefits from such energy policies when the revenue is redistributed to households and, as shown by Carattini et al. [

40], the proposed strategies to redistribute the revenues from such policies play a key role in obtaining voter acceptance.

As for future research based on the questions raised by this work, there are a few aspects that should be further studied. First, as non-European countries have a major influence over the economic development of the European economy, the development of different pathways regarding environmental policies implemented outside of the EU-28 and how to respond to them appropriately is especially important in a time of political instability and disagreements with countries such as the United States, Russia, and China. Secondly, it is crucial for a better understanding of the real impacts of policies to internalize environmental gains and losses as the costs of environmental measures, or lack thereof, would be more clearly perceived in economic parameters such as GDP and trade balances. Third, an aspect of the energy transition that could not be analyzed in detail is the level of investments made by households in energy efficiency. In the present version of NEWAGE, households can only substitute their fossil fuel consumption directly for electricity. Future work should expand their options to allow for direct investment in different technologies that decrease their energy consumption. Finally, this report considered that all pathways would have the same revenue recycling scheme for the carbon payments and, as it was shown that redistributing this revenue to households can have positive effects on diminishing income inequality, establishing new recycling schemes with a focus on low-income households and the substitution of existing taxes, such as on labor and capital, with environmental taxes through an ETR should be further studied.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}