Sustainable Debt Behaviour and Well-Being of Young Adults: The Role of Parental Financial Socialisation Process

Abstract

:1. Introduction and Background

2. Literature Review

2.1. Theoretical Background

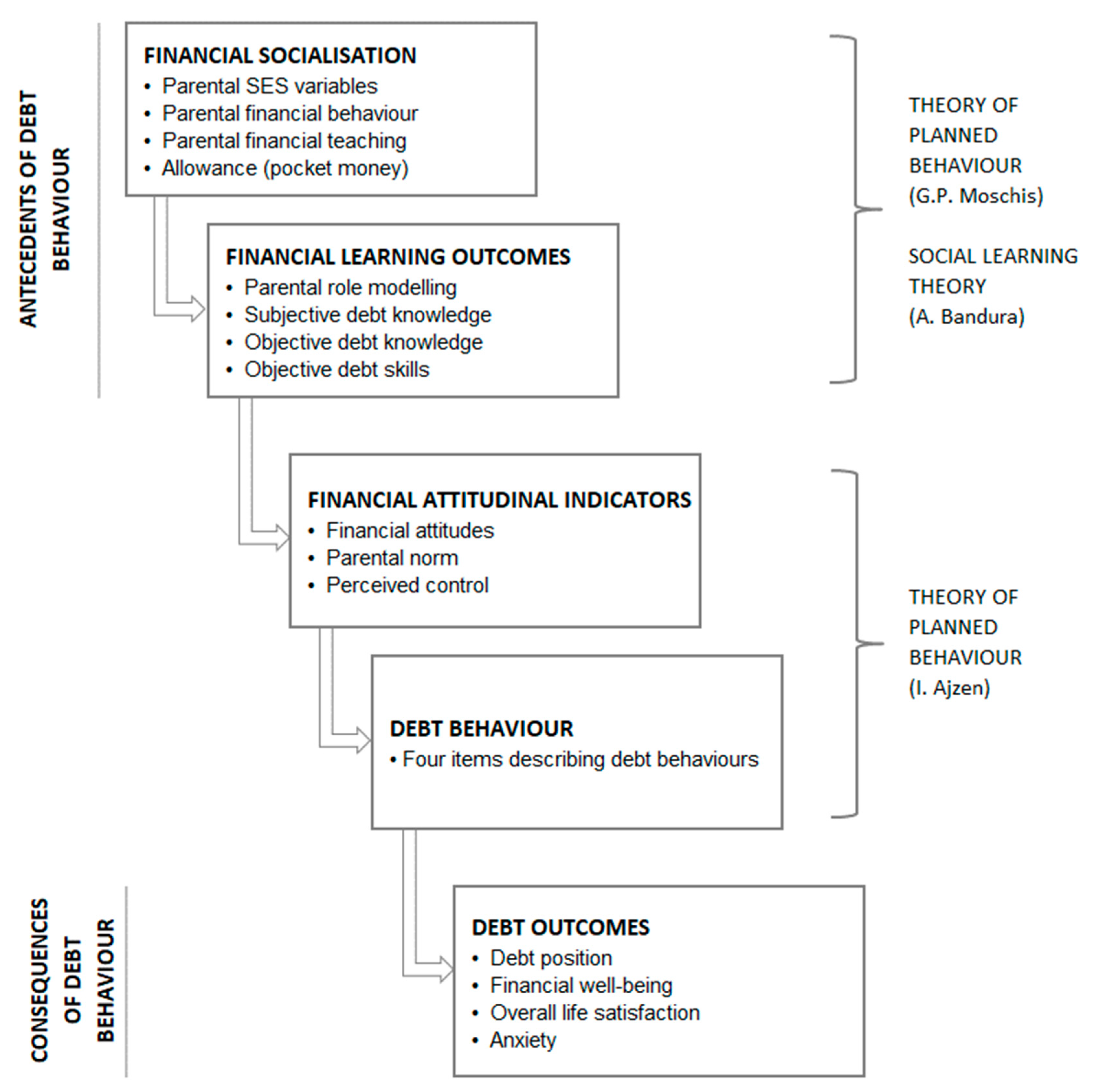

2.2. Conceptual and Analytical Framework

2.3. Previous Empirical Evidence on Indirect Effects

2.4. Previous Empirical Evidence on Direct Effects

3. Materials and Methods

3.1. Data

3.2. Measures

3.2.1. Financial Socialisation

3.2.2. Financial Learning Outcomes

- (a)

- One-time payment of PLN 500 in advance (at the beginning of the year), which means that PLN 4,500 will be effectively available for you on the day of grant.

- (b)

- One-time payment of PLN 500 at the end of the year, which means that PLN 5,500 will have to be returned to the lender on the day of repayment.

- (i)

- Option (a).

- (ii)

- Option (b).

- (iii)

- They are the same.

- (iv)

- Do not know.

- (v)

- Prefer not to answer.

3.2.3. Financial Attitudinal Indicators

3.2.4. Sustainable Debt Behaviour

3.2.5. Debt Behaviour Outcomes

3.3. Data Analysis Procedure

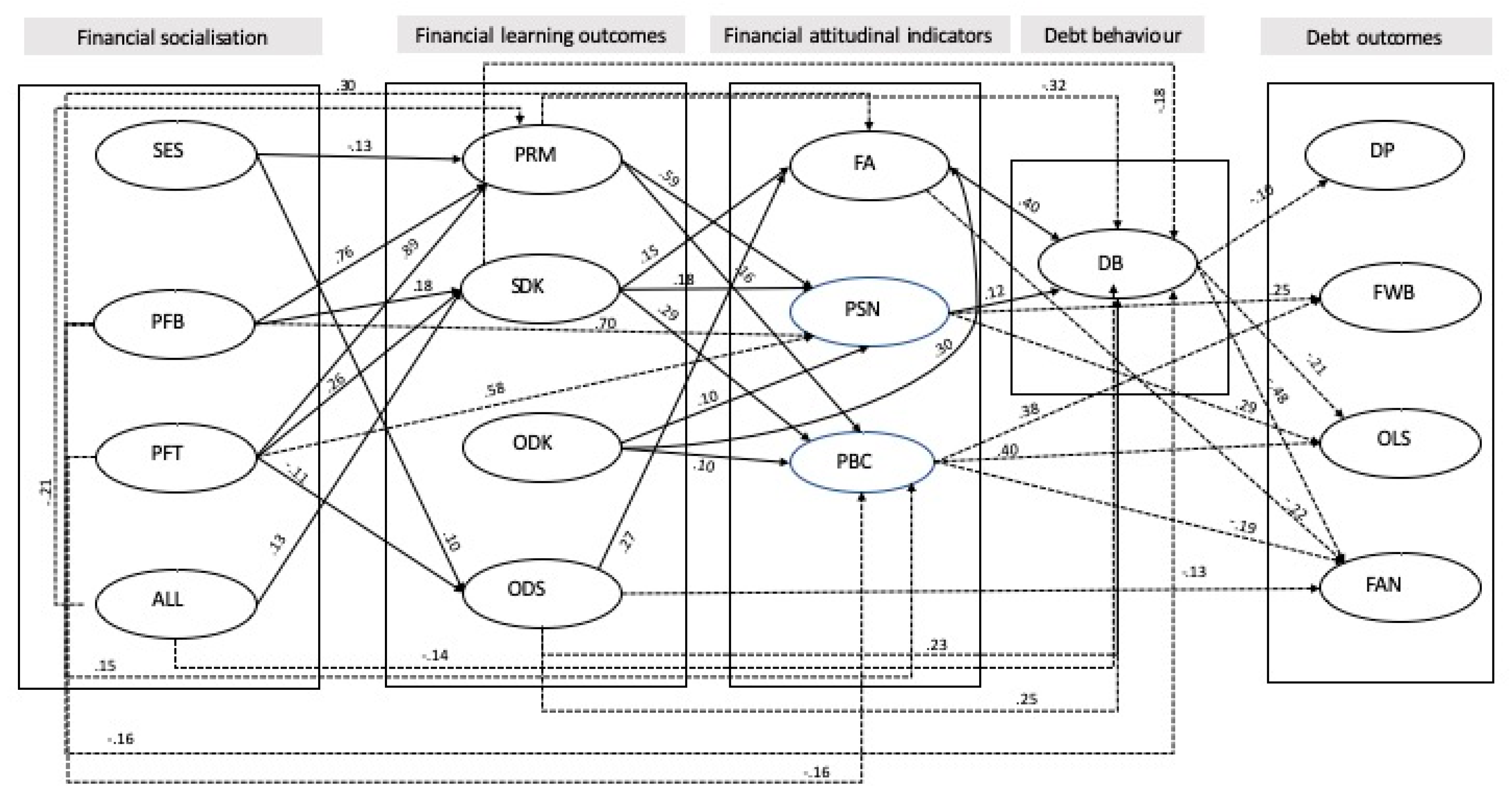

4. Results

4.1. The Hierarchical Relationship of Parental Financial Socialisation–Financial Learning Outcomes

4.2. The Hierarchical Relationship of Financial Learning Outcomes–Financial Attitudinal Indicators

4.3. The Hierarchical Relationship of Financial Attitudinal Indicators–Debt behaviour

4.4. The Hierarchical Relationship of Debt Behaviour–Debt Behaviour Outcomes

4.5. Maternally Conditioned versus Paternally Conditioned Respondents

5. Discussion

5.1. Overall Results: The Hierarchical Model

5.2. The Confirmed Effects: The Hierarchical Relationship of Literacy–Attitude–Behaviour

5.3. The Unconfirmed Effects

5.3.1. The Effect of Parental Financial Socialisation on Young Adults’ Financial Learning Outcomes

5.3.2. The Effect of Debt Behaviour on Well-Being Indicators

6. Conclusions, Limitations, and Future Research

Author Contributions

Funding

Conflicts of Interest

Appendix A. Debt Knowledge Test

{kind=link}

{kind=link}

| True | False | I Don’t Know | |

|---|---|---|---|

| Creditors are required to tell you the APY you will pay when you get a loan. | x | ||

| Your credit rating is not affected by how much you charge on your credit cards. | x | ||

| If the interest rate on an adjustable-rate mortgage loan goes up, your monthly mortgage payments will also go up. | x | ||

| Total amount of interest on a 15-year mortgage is lower than total amount of interest on the same, however a 30-year mortgage. | x | ||

| A 15-year mortgage typically requires higher monthly mortgage payments than the same, however 30-year mortgage. | x | ||

| The most important thing to look at when comparing a loan or credit offers is total amount of interest you will have to pay in the future. | x | ||

| Consumer can waive already granted loan during short-period of time after the day of grant. | x | ||

| Bank margin is another name for bank commission applied when granting loans to private individuals. | x | ||

| A list of warnings regarding dishonest lending institutions is maintained by the Polish National Bank. | x |

Appendix B. Debt Skills Test

- (1)

- 2 years

- (2)

- Less than 5 years (correct)

- (3)

- Between 5 and 10 years

- (4)

- More than 10 years

- (5)

- Do not know

- (1)

- Less than years

- (2)

- Between 5 and 10 years

- (3)

- Between 10 and 15 years

- (4)

- Never, continue to be in debt (correct)

- (5)

- Do not know

- (a)

- Pay 12 monthly instalments of PLN 100 each

- (b)

- Borrow at a 20% annual interest rate and payback PLN 1200 one year from now.

- (1)

- Option (a)

- (2)

- Option (b) (correct)

- (3)

- They are the same

- (4)

- Do not know

- (a)

- One-time payment of PLN 500 in advance (at the beginning of the year), which means that PLN 4,500 will be effectively available for you on the day of grant

- (b)

- One-time payment of PLN 500 at the end of the year, which means that PLN 5500 will have to be returned to the lender on the day of repayment.

- (1)

- Option (a)

- (2)

- Option (b) (correct)

- (3)

- They are the same

- (4)

- Do not know.

References

- Federal Reserve Bank of New York. Quarterly Report on Household Debt and Credit (2017:Q4); Federal Reserve Bank of New York: New York, NY, USA, 2018. [Google Scholar]

- International Monetary Fund. Global Financial Stability Report. Is Growth at Risk? International Monetary Fund: Washington, DC, USA, 2017. [Google Scholar]

- Lombardi, M.; Mohanty, M.; Shim, I. The Real Effects of Household Debt in the Short and Long Run; BIS Working Papers; Bank of International Settlements: Basel, Switzerland, 2017. [Google Scholar]

- Lusardi, A.; Tufano, P. Debt literacy, financial experiences, and overindebtedness. J. Pension Econ. Financ. 2015, 14, 332–368. [Google Scholar] [CrossRef] [Green Version]

- Buckley, N. Polish Banks Spared Forced Conversion of Swiss Franc Mortgages. Financial Times, 2 August 2016. [Google Scholar]

- Foy, H. Bankruptcy fears for Poland’s credit unions. Financial Times, 5 January 2015. [Google Scholar]

- Yeşin, P. Foreign Currency Loans and Systemic Risk in Europe; Federal Reserve Bank of St Louis: St. Louis, MO, USA, 2013; Volume 95, pp. 219–235. [Google Scholar]

- Hou, D.; Skeie, D. LIBOR: Origins, Economics, Crisis, Scandal, and Reform; Federal Reserve Bank of New York: New York, NY, USA, 2014. [Google Scholar]

- Neill, B.O.; Xiao, J.J.; Sorhaindo, B.; Garman, E.T. Financially Distressed Consumers: Their Financial Practices, Financial Well-being, and Health. Financ. Couns. Plan. 2005, 16, 73–87. [Google Scholar]

- Turunen, E.; Hiilamo, H. Health effects of indebtedness: A systematic review. BMC Public Health 2014, 14, 489. [Google Scholar] [CrossRef]

- Richardson, T.; Elliott, P.; Roberts, R. The relationship between personal unsecured debt and mental and physical health: A systematic review and meta-analysis. Clin. Psychol. Rev. 2013, 33, 1148–1162. [Google Scholar] [CrossRef] [Green Version]

- Lenton, P.; Mosley, P. Debt and Health; Sheffield Economic Research Papers; University of Sheffield: Sheffield, UK, 2008. [Google Scholar]

- Kadoya, Y.; Khan, M.S.R.; Hamada, T.; Dominguez, A. Financial literacy and anxiety about life in old age: Evidence from the USA. Rev. Econ. Househ. 2018, 16, 859–878. [Google Scholar] [CrossRef]

- Brown, S.; Gray, D. Household finances and well-being in Australia: An empirical analysis of comparison effects. J. Econ. Psychol. 2016, 53, 17–36. [Google Scholar] [CrossRef] [Green Version]

- Plagnol, A.C. Financial satisfaction over the life course: The influence of assets and liabilities. J. Econ. Psychol. 2011, 32, 45–64. [Google Scholar] [CrossRef] [Green Version]

- Shim, S.; Xiao, J.J.; Barber, B.L.; Lyons, A.C. Pathways to life success: A conceptual model of financial well-being for young adults. J. Appl. Dev. Psychol. 2009, 30, 708–723. [Google Scholar] [CrossRef]

- Modigliani, F.; Brumberg, R. Utility Analysis and the Consumption Function: An Interpretation of Cross-Section Data. In Post-Keynesian Economics; Kunihara, K.K., Ed.; Rutgers University Press: New Brunswicks, NJ, USA, 1954; pp. 388–436. [Google Scholar]

- Cecchetti, S.G.; Mohanty, M.S.; Zampolli, F. The Real Effects of Debt; BIS Working Papers; Bank of International Settlements: Basel, Switzerland, 2011. [Google Scholar]

- Ando, A.; Modigliani, F. The “Life Cycle” Hypothesis of Saving: Aggregate Implications and Tests. Am. Econ. Rev. 1963, 53, 55–84. [Google Scholar]

- FINRA. Financial Capability in the United States. Report of Findings from the 2012 National Financial Capability Study; FINRA: Washington, DC, USA, 2013. [Google Scholar]

- Global Financial Literacy Excellence Center and PwC. Millenials & Financial Literacy—The Struggle with Personal Finance; Global Financial Literacy Excellence Center and PwC: Washington, DC, USA, 2015. [Google Scholar]

- Moore, D. Survey of Financial Literacy in Washington State: Knowledge, Behavior, Attitudes, and Experiences; Technical Report 03-39; Washington State University, Social and Economic Sciences Research Center: Olympia, WA, USA, 2003. [Google Scholar]

- Disney, R.; Gathergood, J. Financial Literacy and Indebtedness: New Evidence for UK Consumers; University of Nottingham: Nottingham, UK, 2011. [Google Scholar]

- Gerardi, K.; Goette, L.; Meier, S. Financial Literacy and Subprime Mortgage Delinquency: Evidence from a Survey Matched to Administrative Data; Working Paper 2010-10; Federal Reserve Bank of Atlanta: Atlanta, GA, USA, 2010. [Google Scholar]

- Gerardi, K.; Goette, L.; Meier, S. Numerical ability predicts mortgage default. Proc. Natl. Acad. Sci. USA 2013, 110, 11267–11271. [Google Scholar] [CrossRef] [Green Version]

- Shim, S.; Barber, B.L.; Card, N.A.; Xiao, J.J.; Serido, J. Financial Socialization of First-year College Students: The Roles of Parents, Work, and Education. J. Youth Adolesc. 2010, 39, 1457–1470. [Google Scholar] [CrossRef]

- Ciemleja, G.; Lace, N.; Titko, J. Financial literacy as a prerequisite for citizens’ economic security: Development of a measurement instrument. J. Secur. Sustain. Issues 2014, 4, 29–40. [Google Scholar] [CrossRef] [Green Version]

- Sabri, M.F.; MacDonald, M.; Hira, T.K.; Masud, J. Childhood consumer experience and the financial literacy of college students in Malaysia. Fam. Consum. Sci. Res. J. 2010, 38, 455–467. [Google Scholar] [CrossRef]

- Xiao, J.J.; Tang, C.; Serido, J.; Shim, S. Antecedents and Consequences of Risky Credit Behavior Among College Students: Application and Extension of the Theory of Planned Behavior. J. Public Policy Mark. 2011, 30, 239–245. [Google Scholar] [CrossRef]

- Grohmann, A.; Kouwenberg, R.; Menkhoff, L. Childhood roots of financial literacy. J. Econ. Psychol. 2015, 51, 114–133. [Google Scholar] [CrossRef] [Green Version]

- Sansone, D.; Rossi, M.; Fornero, E. “Four Bright Coins Shining at Me”: Financial Education in Childhood, Financial Confidence in Adulthood. J. Consum. Aff. 2018, 53, 630–651. [Google Scholar] [CrossRef] [Green Version]

- van Ooijen, R.; van Rooij, M.C.J. Mortgage risks, debt literacy and financial advice. J. Bank. Financ. 2016, 72, 201–217. [Google Scholar] [CrossRef]

- Webley, P.; Nyhus, E.K. Economic socialization, saving and assets in European young adults. Econ. Educ. Rev. 2013, 33, 19–30. [Google Scholar] [CrossRef] [Green Version]

- Pracownia Badań i Innowacji Społecznych and Grupa IQS. Aktywność Finansowa Dzieci i Młodzieży w Polsce. Wyniki Badania Ilościowego; Pracownia Badań i Innowacji Społecznych and Grupa IQS: Warsaw, Poland, 2014. [Google Scholar]

- KRD Economic Information Bureau. Dlaczego Polacy się Zadłużają; KRD Economic Information Bureau: Wrocław, Poland, 2018. [Google Scholar]

- Almenberg, J.; Lusardi, A.; Säve-Söderbergh, J.; Vestman, R. Attitudes Toward Debt and Debt Behavior; National Bureau of Economic Research: Cambridge, MA, USA, 2018. [Google Scholar]

- Fernández, R.; Fogli, A.; Olivetti, C. Mothers and sons: Preference formation and female labor force dynamics. Q. J. Econ. 2004, 119, 1249–1299. [Google Scholar] [CrossRef]

- Morrill, M.S.; Morrill, T. Intergenerational links in female labor force participation. Labour Econ. 2013, 20, 38–47. [Google Scholar] [CrossRef]

- Eriksson, K.H.; Stenberg, A. Gender Identity and Relative Income within Households: Evidence from Sweden; IZA Discussion Paper Series, Discussion Paper No. 9533; The Institute for the Study of Labor (IZA): Bonn, Germany, 2015. [Google Scholar]

- Bandura, A. Social Learning Theory; Prentice-Hall: Englewood Cliffs, NJ, USA, 1977. [Google Scholar]

- Moschis, G.P. Consumer Socialization; Lexington Books: Lexington, KY, USA, 1987. [Google Scholar]

- Ajzen, I. The theory of planned behavior. Organ. Behav. Hum. Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Stolper, O.A.; Walter, A. Financial literacy, financial advice, and financial behavior. J. Bus. Econ. 2017, 87, 581–643. [Google Scholar] [CrossRef] [Green Version]

- Lachance, M.J. Young adults’ attitudes towards credit. Int. J. Consum. Stud. 2012, 36, 539–548. [Google Scholar] [CrossRef]

- Białowolski, P.; Cwynar, A.; Cwynar, W.; Węziak-Białowolska, D. Debt Attitudes in Gender Perspective: Is There an Effect of Debt Knowledge and Skills? 2018. Available online: https://ssrn.com/abstract=3325849 (accessed on 16 December 2019).

- Fishbein, M.; Ajzen, I. Belief, Attitude, Intention and Behaviour: An Introduction to Theory and Research; Addison-Wesley: Reading, MA, USA, 1975. [Google Scholar]

- Festinger, L. A theory of cognitive dissonance. Sci. Am. 1962, 207, 93–106. [Google Scholar] [CrossRef]

- Krugman, H.E. The Impact of Television Advertising: Learning Without Involvement. Public Opin. Q. 1965, 29, 349–356. [Google Scholar] [CrossRef]

- Ajzen, I. The Social Psychology of Decision Making. In Social Psychology: Handbook of Basic Principles; Higgins, E.T., Kruglanski, A.W., Eds.; Guilford Press: New York, NY, USA, 1996. [Google Scholar]

- Ali, A.; Rahman, M.S.A.; Bakar, A. Financial Satisfaction and the Influence of Financial Literacy in Malaysia. Soc. Indic. Res. 2015, 120, 137–156. [Google Scholar] [CrossRef]

- Livingstone, S.M.; Lunt, P.K. Predicting personal debt and debt repayment: Psychological, social and economic determinants. J. Econ. Psychol. 1992, 13, 111–134. [Google Scholar] [CrossRef]

- Hayhoe, C.R.; Leach, L.; Turner, P.R. Discriminating the number of credit cards held by college students using credit and money attitudes. J. Econ. Psychol. 1999, 20, 643–656. [Google Scholar] [CrossRef]

- Haultain, S.; Kemp, S.; Chernyshenko, O.S. The structure of attitudes to student debt. J. Econ. Psychol. 2010, 31, 322–330. [Google Scholar] [CrossRef]

- Chien, Y.-W.; Devaney, S.A. The effects of credit attitude and socioeconomic factors on credit card and installment debt. J. Consum. Aff. 2001, 35, 162–179. [Google Scholar] [CrossRef]

- Joo, S.-H.; Grable, J.E. An exploratory framework of the determinants of financial satisfaction. J. Fam. Econ. Issues 2004, 25, 25–50. [Google Scholar] [CrossRef]

- Godwin, D.D. Antecedents and consequences of newlyweds’ cash flow management. Financ. Couns. Plan. 1994, 5, 161–190. [Google Scholar]

- Xiao, J.J.; Tang, C.; Shim, S. Acting for happiness: Financial behavior and life satisfaction of college students. Soc. Indic. Res. 2009, 92, 53–68. [Google Scholar] [CrossRef]

- Archuleta, K.L.; Dale, A.; Spann, S.M. College Students and Financial Distress: Exploring Debt, Fiancial Satisfaction, and Financial Anxiety. J. Financ. Couns. Plan. 2013, 24, 50–62. [Google Scholar]

- Tay, L.; Batz, C.; Parrigon, S.; Kuykendall, L. Debt and Subjective Well-being: The Other Side of the Income-Happiness Coin. J. Happiness Stud. 2017, 18, 903–937. [Google Scholar] [CrossRef]

- Bernheim, B.D.; Garrett, D.M.; Maki, D.M. Education and saving: The long-term effects of high school financial curriculum mandates. J. Public Econ. 2001, 80, 435–465. [Google Scholar] [CrossRef]

- Jinhee Kim and Swarn Chatterjee Childhood Financial Socialization and Young Adults’ Financial Management. J. Financ. Couns. Plan. 2013, 24, 61–79.

- Hancock, A.M.; Jorgensen, B.L.; Swanson, M.S. College Students and Credit Card Use: The Role of Parents, Work Experience, Financial Knowledge, and Credit Card Attitudes. J. Fam. Econ. Issues 2013, 34, 369–381. [Google Scholar] [CrossRef]

- Norvilitis, J.M.; MacLean, M.G. The role of parents in college students’ financial behaviors and attitudes. J. Econ. Psychol. 2010, 31, 55–63. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Baby Boomer retirement security: The roles of planning, financial literacy, and housing wealth. J. Monet. Econ. 2007, 54, 205–224. [Google Scholar] [CrossRef] [Green Version]

- Yoong, J. Financial Illiteracy and Stock Market Participation: Evidence from the RAND American Life Panel; Pension Research Council Working Paper, PRC WP2010-29; Pension Research Council, University of Pennsylvania: Philadelphia, PA, USA, 2010. [Google Scholar]

- van Rooij, M.; Lusardi, A.; Alessie, R. Financial literacy and stock market participation. J. Financ. Econ. 2011, 101, 449–472. [Google Scholar] [CrossRef] [Green Version]

- Bucher-Koenen, T.; Ziegelmeyer, M. Who Lost the Most? Financial Literacy, Cognitive Abilities, and the Financial Crisis; European Central Bank Working Paper No. 1299; European Central Bank: Frankfurt am Main, Germany, 2011. [Google Scholar]

- Arrondel, L.; Debbich, M.; Savignac, F. Stockholding and financial literacy in the French population. Int. J. Soc. Sci. Humanit. Stud. 2012, 4, 285–294. [Google Scholar]

- Allgood, S.; Walstad, W.B. The effects of perceived and actual financial literacy on financial behaviors. Econ. Inq. 2016, 54, 675–697. [Google Scholar] [CrossRef]

- Alessie, R.; van Rooij, M.; Lusardi, A. Financial literacy and retirement preparation in the Netherlands. J. Pension Econ. Financ. 2011, 10, 527–545. [Google Scholar] [CrossRef]

- Crossan, D.; Feslier, D.; Hurnard, R. Financial Literacy and Retirement Planning in New Zealand. J. Pension Econ. Financ. 2011, 10, 619–635. [Google Scholar] [CrossRef]

- Hastings, J.S.; Mitchell, O.S. How Financial Literacy and Impatience Shape Retirement Wealth and Investment Behaviors; NBER Working Paper No. 16740; National Bureau of Economic Research: Cambridge, MA, USA, 2011. [Google Scholar]

- Sekita, S. Financial literacy and retirement planning in Japan. J. Pension Econ. Financ. 2011, 10, 637–656. [Google Scholar] [CrossRef] [Green Version]

- Lusardi, A.; Mitchell, O.S. Financial literacy and retirement planning in the United States. J. Pension Econ. Financ. 2011, 10, 509–525. [Google Scholar] [CrossRef] [Green Version]

- Jappelli, T.; Padula, M. Investment in financial literacy and saving decisions. J. Bank. Financ. 2013, 37, 2779–2792. [Google Scholar] [CrossRef] [Green Version]

- Behrman, J.R.; Mitchell, O.S.; Soo, C.K.; Bravo, D. How Financial Literacy Affects Household Wealth Accumulation. Am. Econ. Rev. 2012, 102, 300–304. [Google Scholar] [CrossRef] [Green Version]

- van Rooij, M.C.J.; Lusardi, A.; Alessie, R.J.M. Financial Literacy, Retirement Planning and Household Wealth. Econ. J. 2012, 122, 449–478. [Google Scholar] [CrossRef]

- French, D.; McKillop, D. Financial literacy and over-indebtedness in low-income households. Int. Rev. Financ. Anal. 2016, 48, 1–11. [Google Scholar] [CrossRef] [Green Version]

- Havighurst, R.J. Human Development and Education; Longmans, Green & Co.: New York, NY, USA, 1953. [Google Scholar]

- Kins, E.; Beyers, W.; Soenens, B.; Vansteenkiste, M. Patterns of Home Leaving and Subjective Well-Being in Emerging Adulthood: The Role of Motivational Processes and Parental Autonomy Support. Dev. Psychol. 2009, 45, 1416–1429. [Google Scholar] [CrossRef] [PubMed]

- Johnson, K.M. Parental Financial Assistance and Young Adults’ Relationships With Parents and Well-being. J. Marriage Fam. 2013, 75, 713–733. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Coleman, R.P. The Continuing Significance of Social Class to Marketing. J. Consum. Res. 1983, 10, 265–280. [Google Scholar] [CrossRef]

- Porto, N.; Xiao, J.J. Financial Literacy Overconfidence and Financial Advice Seeking. J. Financ. Serv. Prof. 2016, 70, 78–88. [Google Scholar]

- Cwynar, A.; Cwynar, W.; Wais, K. Debt Literacy and Debt Literacy Self-Assessment: The Case of Poland. J. Consum. Aff. 2019, 53, 24–57. [Google Scholar] [CrossRef]

- Hilgert, M.A.; Hogarth, J.M.; Beverly, S.G. Household Financial Management: The Connection between Knowledge and Behavior. Fed. Reserv. Bull. 2003, 89, 309–322. [Google Scholar]

- Huston, S.J. Measuring Financial Literacy. J. Consum. Aff. 2010, 44, 296–316. [Google Scholar] [CrossRef]

- Hung, A.A.; Parker, A.M.; Yoong, J.K. Defining and Measuring Financial Literacy; RAND Working Papers WR-708; RAND Corporation: Santa Monica, CA, USA, 2009. [Google Scholar]

- Remund, D.L. Financial literacy explicated: The case for a clearer definition in an increasingly complex economy. J. Consum. Aff. 2010, 44, 276–295. [Google Scholar] [CrossRef]

- Goedde-Menke, M.; Erner, C.; Oberste, M. Towards more sustainable debt attitudes and behaviors: The importance of basic economic skills. J. Bus. Econ. 2017, 87, 645–668. [Google Scholar] [CrossRef]

- Cohen, M.J. Consumer credit, household financial management, and sustainable consumption. Int. J. Consum. Stud. 2007, 31, 57–65. [Google Scholar] [CrossRef]

- Gardarsdóttir, R.B.; Dittmar, H. The relationship of materialism to debt and financial well-being: The case of Iceland’s perceived prosperity. J. Econ. Psychol. 2012, 33, 471–481. [Google Scholar] [CrossRef]

- Barton, C.; Fromm, J.; Egan, C. The Millennial Consumer: Debunking Stereotypes; The Boston Consulting Group: Boston, MA, USA, 2012. [Google Scholar]

- Gonzalez-Redin, J.; Polhill, J.G.; Dawson, T.P.; Hill, R.; Gordon, I.J. It’s not the ‘what’, but the ‘how’: Exploring the role of debt in natural resource (un) sustainability. PLoS ONE 2018, 13, e0201141. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Dew, J.; Xiao, J. The Financial Management Behavior Scale: Development and Validation. J. Financ. Couns. Plan. 2011, 22, 43–59. [Google Scholar]

- Polish Bank Association. Raport ZBP Info Kredyt; Polish Bank Association: Warsaw, Poland, 2017. [Google Scholar]

- Salter, J. The Borrowers: Looking beyond the Financial Impact of Debt…; Demos: London, UK, 2014. [Google Scholar]

- Hunter, J.L.; Heath, C.J. The Relationship Between Credit Card Use Behavior and Household Well-Being During the Great Recession: Implications for the Ethics of Credit Use. J. Financ. Couns. Plan. 2017, 28, 213–224. [Google Scholar] [CrossRef]

- Robb, C.A.; Babiarz, P.; Woodyard, A. The demand for financial professionals’ advice: The role of financial knowledge, satisfaction, and confidence. Financ. Serv. Rev. 2012, 21, 291–305. [Google Scholar]

- Diener, E.; Emmons, R.A.; Larsem, R.J.; Griffin, S. The Satisfaction With Life Scale. J. Pers. Assess. 1985, 49, 71–75. [Google Scholar] [CrossRef]

- Diener, E.; Oishi, S.; Lucas, R.E. Personality, culture, and subjective well-being: Emotional and cognitive evaluations of life. Annu. Rev. Psychol. 2003, 54, 403–425. [Google Scholar] [CrossRef]

- Proctor, C.L.; Linley, P.A.; Maltby, J. Youth life satisfaction: A review of the literature. J. Happiness Stud. 2009, 10, 583–630. [Google Scholar] [CrossRef] [Green Version]

- American Psychiatric Association. Diagnostic Statistical Manual-IV-TR, 4th ed.; American Psychiatric Association: Washington, DC, USA, 2000. [Google Scholar]

- Revelle, W. Psych: Procedures for Personality and Psychological Research; Northwestern University: Evanston, IL, USA, 2018. [Google Scholar]

- Rosseel, Y. Lavaan: An R package for structural equation modeling. J. Stat. Softw. 2012, 48, 1–36. [Google Scholar] [CrossRef] [Green Version]

- Strömbäck, C.; Lind, T.; Skagerlund, K.; Västfjäll, D.; Tinghög, G. Does self-control predict financial behavior and financial well-being? J. Behav. Exp. Financ. 2017, 14, 30–38. [Google Scholar] [CrossRef]

- Parker, A.M.; de Bruin, W.B.; Yoong, J.; Willis, R. Inappropriate Confidence and Retirement Planning: Four Studies with a National Sample. J. Behav. Decis. Mak. 2012, 25, 382–389. [Google Scholar] [CrossRef] [PubMed]

- Anderson, A.; Baker, F.; Robinson, D.T. Precautionary savings, retirement planning and misperceptions of financial literacy. J. Financ. Econ. 2017, 126, 383–398. [Google Scholar] [CrossRef] [Green Version]

- Jorgensen, B.L.; Savla, J. Financial literacy of young adults: The importance of parental socialization. Fam. Relat. 2010, 59, 465–478. [Google Scholar] [CrossRef]

- Kaiser, T.; Menkhoff, L. Does Financial Education Impact Financial Literacy and Financial Behavior, and If So, When? World Bank Econ. Rev. 2017, 31, 611–630. [Google Scholar] [CrossRef]

- Miller, M.; Reichelstein, J.; Salas, C.; Zia, B. Can You Help Someone Become Financially Capable? A Meta-Analysis of the Literature. World Bank Res. Obs. 2015, 30, 220–246. [Google Scholar] [CrossRef] [Green Version]

- Willis, L.E. Against Financial-Literacy Education. Iowa Law Rev. 2008, 94, 197–285. [Google Scholar]

- Aboagye, J.; Jung, J.Y. Debt Holding, Financial Behavior, and Financial Satisfaction. J. Financ. Couns. Plan. 2018, 29, 208–217. [Google Scholar] [CrossRef]

- Ameriks, J.; Caplin, A.; Leahy, J. Wealth accumulation and the propensity to plan. Q. J. Econ. 2003, 118, 1007–1047. [Google Scholar] [CrossRef]

- Ameriks, J.; Caplin, A.; Leahy, J.; Tyler, T.O.M. Measuring self-control problems. Am. Econ. Rev. 2007, 97, 966–972. [Google Scholar] [CrossRef] [Green Version]

| % | N | |

|---|---|---|

| Gender | ||

| Male | 55 | 330 |

| Female | 45 | 270 |

| All | 100 | 600 |

| Place of residence (inhabitants) | ||

| Village | 18.2 | 109 |

| Town up to 20,000 | 10.3 | 62 |

| City 20,001–50,000 | 18.8 | 113 |

| City 50,001–100,000 | 13.5 | 81 |

| City 100,001–200,000 | 14.5 | 87 |

| City 200,001–500,000 | 13.2 | 79 |

| City 500,001 or more | 11.5 | 69 |

| All | 100 | 600 |

| Educational attainment | ||

| Primary school | 0.5 | 3 |

| Junior high school | 1.7 | 10 |

| Basic vocational school | 3.7 | 22 |

| High school (upper secondary education) | 17.2 | 103 |

| Vocational school (upper vocational education) | 13 | 78 |

| Post high school | 9.3 | 56 |

| Higher school | 51.5 | 309 |

| PhD or higher | 3.2 | 19 |

| All | 100 | 600 |

| Income (PLN) | ||

| Less than 1500 | 22.6 | 136 |

| 1500–2500 | 29.3 | 176 |

| 2500–3500 | 23 | 138 |

| 3500–4500 | 10.5 | 63 |

| 4500–6000 | 7.1 | 43 |

| More than 6000 | 7.3 | 44 |

| All | 100 | 600 |

| Abbreviation | Variable | Min | Max | Median |

|---|---|---|---|---|

| SES | Parental socioeconomic status variables | 1.6 | 7 | 5 |

| PFB | Parental financial behaviour | 1 | 5 | 3.75 |

| PFT | Parental financial teaching | 1 | 5 | 3 |

| ALL | Allowance (pocket money) | 1 | 2 | 2 |

| PRM | Parental role modelling | 1 | 5 | 3 |

| SDK | Subjective debt knowledge | 1 | 5 | 3 |

| ODL | Objective debt knowledge | 0 | 9 | 4 |

| ODS | Objective debt skills | 0 | 4 | 1 |

| FAT | Financial attitudes | 1 | 5 | 4.5 |

| PSN | Parental subjective norms | 1 | 25 | 15 |

| PBC | Perceived behavioural control | 1 | 5 | 3 |

| DB | Debt behaviour | 1 | 5 | 4.25 |

| DP | Debt position | 0 | 3 | 1 |

| FWB | Financial well-being | 1 | 5 | 3 |

| OLS | Overall life satisfaction | 1 | 7 | 4 |

| FAN | Financial anxiety | 1 | 7 | 2.8 |

| Construct/Indicator | Items Comprising the Scale | Standardised Factor Loading | Cronbach’s Alpha |

|---|---|---|---|

| Parental SES | SES | 1.00 | N.A. |

| Parental financial behaviour | Spent within the budget | 0.594 | 0.66 |

| Saved money each month for the future | 0.783 | ||

| Paid bills on time | 0.572 | ||

| Insured against life contingencies | 0.62 | ||

| Parental financial teaching | Discussed family financial matters with me | 0.72 | 0.91 |

| Spoke to me about the importance of saving | 0.84 | ||

| Taught me how to be a smart shopper | 0.795 | ||

| Taught me how to use a credit card appropriately | 0.713 | ||

| Discussed how to establish a good credit rating | 0.66 | ||

| Discussed how to finance my college education with me | 0.75 | ||

| Allowance | ‘Yes/no’ question | 1.00 | N.A. |

| Parental role modelling | I make financial decisions based on what my parent(s) have done in similar situations | 0.86 | 0.93 |

| When it comes to managing money, I look to my parent(s) as my role models | 0.89 | ||

| My parent(s) are role models for me about how to manage financial matters | 0.878 | ||

| My parent(s) have a positive influence on me when it comes to managing money | 0.856 | ||

| Subjective debt knowledge | Self-assessment on a 5-point Likert scale | 1.00 | N.A. |

| Objective debt knowledge | Nine ‘True/false’ questions | 1.00 | N.A. |

| Objective debt skills | Four single-choice questions | 1.00 | N.A. |

| Financial attitudes | Spent within the budget | 0.76 | 0.83 |

| Saved money each month for the future | 0.86 | ||

| Paid bills on time | 0.74 | ||

| Insured against life contingencies | 0.62 | ||

| Parental subjective norm | Spent within the budget | 0.902 | 0.87 |

| Saved money each month for the future | 0.849 | ||

| Paid bills on time | 0.787 | ||

| Insured against life contingencies | 0.732 | ||

| Perceived behavioural control | Self-assessment on a 5-point Likert scale | 1.000 | N.A. |

| Debt behaviour | Borrowing money without thorough examination of all pros and cons as well as careful consideration of all available options | 0.597 | 0.87 |

| Borrowing money to repay former debts | 0.71 | ||

| Borrowing money simultaneously from more than one source (e.g., banks, personal loan/payday loan companies, instalment purchases, pawnshops, family etc.) | 0.83 | ||

| I get behind on bills payment or/and debt repayment | 0.705 | ||

| Debt position | Self-reported number of credits and loans | 1.000 | N.A. |

| Overall life satisfaction | In most ways, my life is close to my ideal | 0.82 | 0.86 |

| The conditions of my life are excellent | 0.77 | ||

| I am satisfied with my life | 0.86 | ||

| So far I have gotten the important things I want in life | 0.89 | ||

| If I would live my life over, I would change almost nothing | 0.76 | ||

| Financial well-being | Self-assessment on a 5-point Likert scale | 1.000 | N.A. |

| Financial anxiety | I feel anxious about my financial situation | 0.758 | 0.96 |

| I have difficulty sleeping because of my financial situation | 0.837 | ||

| I have difficulty concentrating on my school or work because of my financial situation | 0.844 | ||

| I am irritable because of my financial situation | 0.863 | ||

| I have difficulty controlling worrying about my financial situation | 0.936 | ||

| My muscles feel tense because of worries about my financial situation | 0.933 | ||

| I feel fatigued because I worry about my financial situation | 0.921 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cwynar, A.; Cwynar, W.; Baryła-Matejczuk, M.; Betancort, M. Sustainable Debt Behaviour and Well-Being of Young Adults: The Role of Parental Financial Socialisation Process. Sustainability 2019, 11, 7210. https://0-doi-org.brum.beds.ac.uk/10.3390/su11247210

Cwynar A, Cwynar W, Baryła-Matejczuk M, Betancort M. Sustainable Debt Behaviour and Well-Being of Young Adults: The Role of Parental Financial Socialisation Process. Sustainability. 2019; 11(24):7210. https://0-doi-org.brum.beds.ac.uk/10.3390/su11247210

Chicago/Turabian StyleCwynar, Andrzej, Wiktor Cwynar, Monika Baryła-Matejczuk, and Moises Betancort. 2019. "Sustainable Debt Behaviour and Well-Being of Young Adults: The Role of Parental Financial Socialisation Process" Sustainability 11, no. 24: 7210. https://0-doi-org.brum.beds.ac.uk/10.3390/su11247210