1. Introduction

Behind the accelerating pace and success of the world economy, there is the unavoidable adverse effect of a decrease in environmental quality in line with the rapid growth of industry, carbon retention, and other greenhouse gases which gradually increase over time [

1]. The Intergovernmental Panel on Climate Change (IPCC)—an institution formed as a result of collaboration between the United Nations and the World Meteorological Organization—is devoted to dealing with climate change problems. For the years 1906 to 2005, IPCC has gathered clear evidence that global temperatures have been increasing by an average of about 0.74 °C, with land temperatures higher than the oceans, and in the last 50 years, the average temperature has doubled compared to the last 100 years [

2]. In 2005, Indonesia was the fourth largest contributor to the world’s per capita emissions after China, the USA, and the European Union [

3]. According to the Ministry of Energy and Mineral Resources (2012), these emissions are mostly produced from mining and agricultural industry. The mining industry sector, such as oil, coal, and gas, uses 70% fossil energy from the total energy consumed. The mining industry is the biggest contributor to carbon emissions in developing countries, including Indonesia. Without exception, the agricultural industry also has contributed to the high carbon level growth of a 54% increase in total greenhouse gas (GHG) emissions since the year 2000.

To define the GHG emission totals, this study takes the definition from the World Bank website in the section of World Developments Indicators that expresses GHG totals in CO2 equivalent using the GWP100 metric of the Second Assessment Report of the IPCC. However, total greenhouse gas emissions in kt of CO2 equivalent are from the composition of CO2 totals obtained from biomass burning and all anthropogenic CH4 sources, N2O sources, and also F-gases (HFCs, PFCs, and SF6). This is leading to an increase in the Earth’s surface temperature, and to related effects on the climate and sea level.

Carbon dioxide (CO

2) makes up the largest share of the greenhouse gases contributing to global warming and climate change. Emissions of CO

2 come from burning oil, coal, and gas for energy use, burning wood and waste materials, and from industrial processes such as cement production. Data for carbon dioxide emissions include gases from fossil fuel combustion and cement manufacture, but exclude emissions from land use, such as deforestation. The burning of carbon-based fuels since the industrial revolution has rapidly increased concentrations of atmospheric carbon dioxide, increasing the rate of global warming and causing anthropogenic climate change. It is also a major source of ocean acidification, since it dissolves in water to form carbonic acid. This phenomenon leads to an increase in the Earth’s surface temperature and to related effects on the climate and rises in sea level [

4].

Due to the damaging effect on the environment, people from diverse professions, such as scientists, politicians, and business leaders have become concerned about the worsening gradual condition of the Earth and effect of global warming. The Kyoto Protocol—an environmental agreement, agreed upon and signed by the world leaders in 1997 and also by many of the parties to the United Nations Framework Convention on Climate Change (UNFCCC)—is working towards curbing CO2 emissions globally.

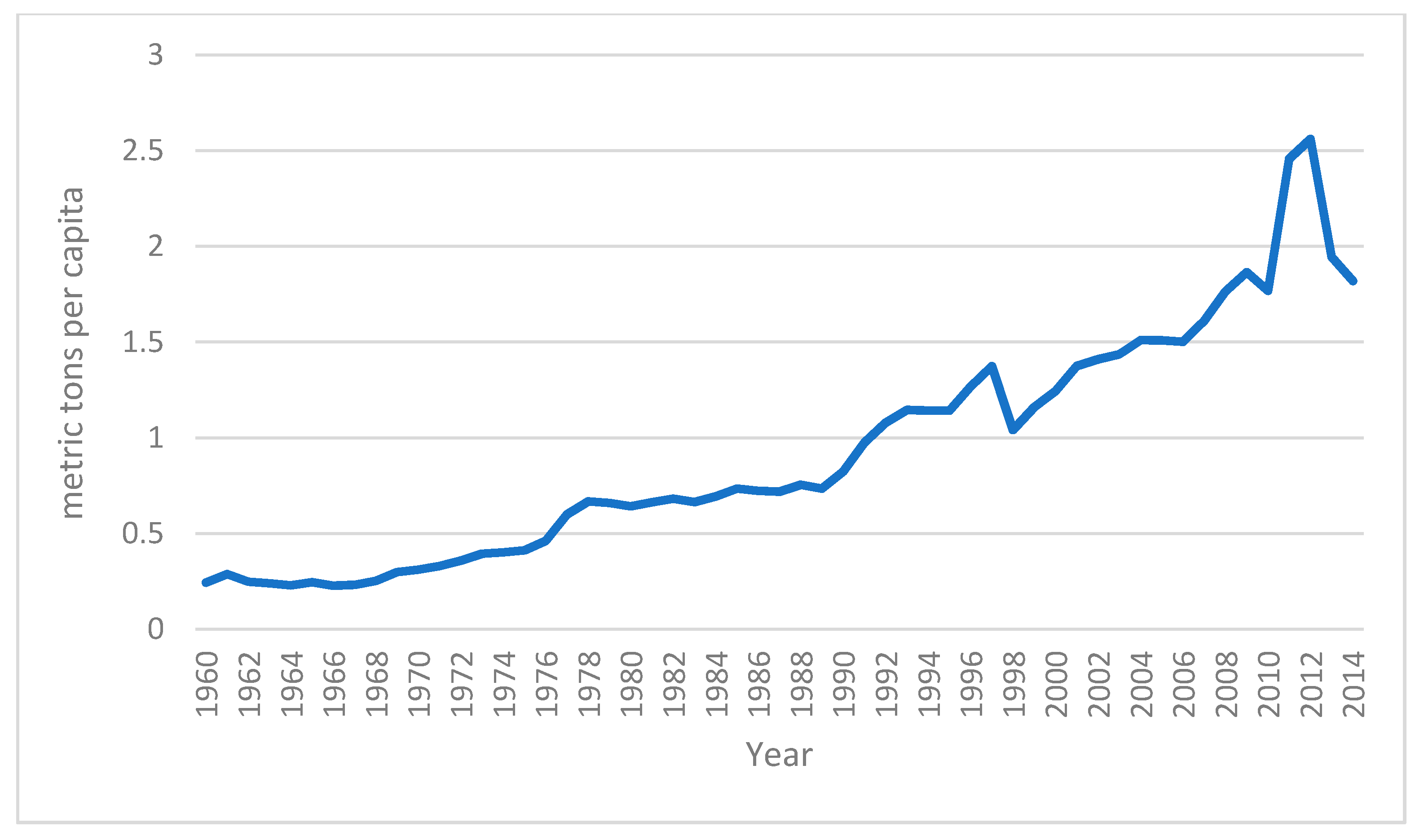

Figure 1 below is obtained from the World Development Indicators issued by the World Bank and shows the trend of Indonesia’s CO

2 emissions (metric tons per capita), provided from the years 1960 until 2014. From 1970, CO

2 emissions in Indonesia increased year by year. They reached a peak in the year 2012, but the trend has shown a decline since around 2013. The World Resources Institute (WRI) official website states that, in 2014, Indonesia’s rank as the world largest contributor country to carbon emissions has plunged to the 6th place after the United States, the European Union, China, India, and Russia, better than in 2005, when Indonesia ranked 4th as the largest contributor to the world’s per capita emissions after China, the USA, and the European Union.

The declining trend is probably caused by the government’s increasing urge to reduce carbon emissions by encouraging companies engaged in the industries with the highest contributions of carbon emissions to intensify their carbon emission management practices and disclose carbon emissions to the public. This urge is a form of realization for Indonesia as one of the countries that signed the Kyoto Protocol, and can be seen in the legislation that has been made, namely Law No. 17 in the year 2004 in which Indonesia ratified the Kyoto Protocol, which contained an agreement to reduce GHG (greenhouse gases) emission on a global scale. There are also other regulations that encourage GHG emission reduction, i.e., (1) Law No. 6, year 1994, wherein Indonesia ratified the convention on climate change; (2) Law No. 32, year 2009, concerning environmental protection and management; (3) Law No. 31, year 2009, concerning protection and management of the environment; (4) Presidential Regulation No. 61, year 2011, concerning the national action plan for the reduction of greenhouse gases, in which it was also stated that companies should participate in efforts to reduce GHGs; and (5) Presidential Regulation No. 71 year 2011 concerning the implementation of national greenhouse gas inventories.

Indonesia’s commitment was also shown by President Susilo Bambang Yudhoyono in his address to state leaders at the G-20 meeting in Pittsburgh, United States, 25 September 2009, in which he stated that Indonesia is voluntarily committed to reducing greenhouse gas (GHG) emissions by 26% by 2020 from Business as Usual (BAU) level by its own efforts, and reaching 41% if it gets international support [

5,

6,

7]. This commitment was conveyed mainly because Indonesia was determined to implement sustainable development as stated in the national development plan. The 2010–2014 Medium Term Development Plan states that sustainable development is mainstreaming, which means that every sector must implement sustainable development into policies and programs. The President’s commitment then becomes an important source of momentum to emphasize sectoral targets and programs that contribute to reducing emissions. With the commitment to reducing GHG emissions, Indonesia hopes that its voluntary action will drive other countries, especially developing countries, to reduce global GHG emissions. As a result, firms in given industries that are conducive to generating CO

2 emissions in their processes are now strongly encouraged to reduce and disclose carbon dioxide emissions to the public as part of the government’s sustainable development commitment.

Responding to this issue, this research paper will examine the factors that support the firms to disclose their carbon emissions. We used a sample of 305 firms listed on the Indonesian Stock Exchange (IDX) from the years 2011 to 2016. Those 305 firms were active in the sectors of Mining and Agricultural industry, both of which massively contribute to carbon emissions. This research is an extension of the research conducted by Gonzalez-Gonzalez and Zamora Ramirez (2016) entitled “Voluntary carbon disclosure by Spanish companies: an empirical analysis.” The difference between these studies has several points.

First, the research sample used in the Gonzalez-Gonzalez and Zamora Ramirez (2016) study was 48 companies in Spain registered in the FT500, DJSI, IBEX35 index [

8], while this study specifically focuses on mining and agricultural companies, numbering 305 firms listed on the Indonesian Stock Exchange (IDX) from the years 2011 to 2016. We chose to focus on those industries as they are categorized as industry sectors in Indonesia that are sensitive to environmental issues, largely in carbon emissions.

Secondly, the research period used by Gonzalez-Gonzalez and Zamora Ramirez (2016) began in 2015 [

8], whereas this research period runs from 2011 to 2016. The reason for the selection of the year period is that the latest regulation was made in 2011, namely, Presidential Regulation No. 71 year 2011, concerning the implementation of national greenhouse gas inventories. Additionally, as we can see in

Figure 1, Indonesia reached a higher level of CO

2 emissions in the year 2012, but then the trend starts to show a decline in the next year; however, the tail of the graph in 2014 seems to indicate that the decline will occur gradually in the following year. Hence, we added the next two years, as we believe that there will be a decline throughout 2016. Therefore, we presume the years 2011–2016 to be the impactful period of transition.

Third, the research conducted by Gonzalez-Gonzalez and Zamora Ramirez (2016) used variables of social pressure (firm size), market pressure (leverage), and pressure of the interests of shareholders (registered in the FT500, DJSI, IBEX35 index) [

8]. Based on the background of the problem above, we are interested in conducting research that aims to determine the influence of the firm size, corporate governance structure, and industry characteristics on carbon emission disclosure in the mining and agricultural companies listed on the Indonesian Stock Exchange (IDX) for the period of 2011 to 2016.

The compelling issue that this study provides is the prediction about board independence in voluntary carbon emission disclosures. Prior studies have mainly expected that having an independent board would positively influence and encourage carbon emission disclosure to a higher level. This study adds new evidence to the literature, as we document that the influence of having a greater proportion of independence is not always significantly positive on voluntary disclosure. On the contrary, it can be significantly negative, depending on industry sector and the corporate governance behavior of that particular country. Therefore, our results can inform policymakers about the capture of the mining and agricultural industries in Indonesia in terms of complying with the government’s sustainable development policies and program to reduce and disclose carbon emissions.

The remainder of this study is structured as follows:

Section 2 develops the research hypotheses;

Section 3 describes the sample and variables, along with the methodology;

Section 4 specifies the empirical models and presents the main results;

Section 5 summarizes the study and presents concluding remarks.

3. Data and Research Methodology

In this study, we used all firms from mining and agricultural industries that were listed on the Indonesia Stock Exchange (IDX) spanning the period 2011 to 2016 as our sample. We required no missing data for all variables used in this study. Our final sample consisted of 305 firm-year observations.

Table 1 presents the distribution of samples by year for both the mining and agricultural industries. It shows that, for the period 2011 to 2016 in Indonesia, the number of firms operating in the mining industry was greater than the number of firms in the agricultural industry.

To test the hypotheses, we employed several univariate and multivariate analysis methods. We used descriptive statistics to present the basic information related to each variable in this study. For univariate analysis, we employed a correlation matrix (Pearson correlation) to examine the relationship between each variable. With regard to multivariate analysis, we used ordinary least squared (OLS) regression and applied correct standard error to deal with the heteroscedasticity issue. We employed three regression equations as follows:

To test the relationship between firm size and CED:

To test the relationship between corporate governance structure and CED:

To test the relationship between industry and CED:

Our dependent variable was carbon emissions disclosure (CED). We hand-collected this data from the annual and sustainability reports. We followed Choi et al. (2013) in using a content analysis approach to construct this variable. Choi et al. (2013) developed some checklists given by the CDP (Carbon Disclosure Project) which were provided in the form of information request sheet. The information request sheet was used to determine how high or low the voluntary disclosures related to climate change and carbon emissions are carried out by the company were. There were five broad categories in determining the level of carbon emissions disclosure, namely: climate change (CC), greenhouse gas (GHG), energy consumption (EC), reduction and cost (RC), and accountability of cost and carbon emissions (ACC) [

50]. Each category included several items. There were 18 total items. The checklists are available in

Table A1.

We employed three interesting (independent) variables in this study. Our first interesting variable was firm size (FIRMSIZE). Firm size describes the number of assets owned by a company, which can be in the form of financial and non-financial assets. The independent variable in this study was the company size, which was calculated using natural logarithms (ln); because the total value of a company’s assets might have a value of millions or even billions of rupiahs, the total value requires simplification by converting it into logarithms.

The second independent variable was corporate governance structures. We addressed two issues on governance, firstly the size of the board of directors (BOARDSIZE), and second the level of independence (%INDDIR and %INDCOM). The BOARDSIZE is the total number of both directors and commissioners on the board. The %INDDIR is the number of independent directors divided by the total number of directors in the board. The %INDCOM is the number of independent commissioners divided by total number of commissioners on the board. In addition, we also constructed a dummy variable (MINING) to differentiate between firms in the mining and agricultural industry. MINING was defined 1 if the firm belonged to the mining industry, otherwise it was 0.

In addition, we controlled for leverage (LEVERAGE) and profitability (PROFIT) for the regression analysis. LEVERAGE is the ratio between total liabilities and total assets, which indicates the percentage of the creditors’ funds used to finance company assets [

50]. Leverage is a measurement of financial ratios calculated as total debt divided by total assets. Leverage is represented by a percentage. PROFIT is information related to financial performance [

50]. The greater the company’s profit, the stronger the company’s ability to generate earnings. Profitability can be measured by a variety of sizes, e.g., ROA, ROE, ROI, NPM (net profit margin). The pertinent formula in this study is measured using ROA.

4. Results and Analysis

Table 2 presents the descriptive statistics for all variables in this study. For CED, some firms did not disclose any information related to carbon emissions. The maximum score for disclosure was 17 out of 18 criteria. The maximum number of the board was 20 persons (directors and commissioners). The median of %INDCOM was 0.333, or, 33% of the commissioners were independent (median). The maximum value of %INDDIR was 0.667, or, the maximum percentage of independent commissioners was 67%. From this table, we can see that 70.2% of the observations were in the mining industry.

Table 3 presents the Pearson correlation matrix for all variables in this study. FIRMSIZE had a positive and significant correlation to the CED. In other words, larger firms will disclose more on carbon emissions. The coefficient of BOARDSIZE was 0.384 and significant at the 1% level. This indicates that firms with a larger number of people on their boards will have a higher level of carbon emissions disclosure (CED). Interestingly, both %INDDIR and %INDCOM had negative and positive correlations to CED. These indicate that a lower percentage of both independent directors and commissioners will have a higher level of carbon emissions disclosure. In addition, based on correlation matrix results, there were no significant correlations between MINING and CED.

Table 4 displays the mean difference between firms in the mining and agricultural industries. The finding shows that there was no significant difference in CED between the firms in these groups. Moreover, firms in the agricultural industry tended to have a larger number of people on their boards and more profitability than firms from the mining industry.

Table 5 presents the results of the regression for firm size (FIRMSIZE), corporate governance (BOARDSIZE, %INDDIR, and %INDCOM), and industry (MINING) to carbon emissions disclosure (CED). We controlled for fraction of debt to equity (LEVERAGE), profitability (PROFIT), and year-fixed effects in all specifications in this table. In specifications 1 and 2, we examined the relationship between firm size and the level of carbon emission disclosure. Based on prior findings, we predicted that firms with higher sizes would have a positive association to carbon emissions disclosure. In the first specification, we tested the first hypothesis using ordinary least square (OLS) regression. We found that the coefficient of FIRMSIZE was 2.238 and significant to the 1% level (t = 9.38). This finding indicates that firms with higher size are more likely to have a higher level of carbon emissions disclosure. This finding was robust even after we corrected the standard error in specification 2.

In specifications 3 and 4, we tested whether corporate governance had a significant impact on CED. We employed two issues of governance, namely the size of the board and the percentage of independent directors (or commissioners), to better capture of the relationship between corporate governance structures and emission disclosure. To examine hypothesis 2a, we used the total number of directors and commissioners as a proxy for board size. We predicted that a larger board would lead companies to disclose more on carbon emissions. As shown in

Table 5, specification 3, the coefficient of BOARDSIZE was 0.212 and was significant to the 10% level (t = 1.67). This shows that firms with larger board size are more likely to disclose more information related to carbon emissions.

In the second issue for governance, we examined whether the level of independence of the commissioners and directors affects the CED or not. We used the percentage of the number of independent commissioners and directors, scaled by the size of the boards. Interestingly, we found that the coefficients of %INDCOM and %INDDIR were −7.250 and −3.864, respectively. Both proxies were significant, to the 1 and 10% level, respectively. These results indicate that firms with a higher percentage of independent commissioners and directors are less likely to disclose information on carbon emissions. These findings imply that independent boards are more conservative when it comes to disclosing carbon-emission-related information to the stakeholders. Overall, those governance proxies increased the explanatory power of the research model by around 5% from the basic model. We found similar results (hypotheses 2a and 2b) even after we corrected the standard error (specification 4).

In addition, we examined whether the industry characteristic affected the firms’ disclosure of carbon emissions behavior. We added one dummy variable (MINING) to the model to capture whether firms in the mining industry have a different pattern of CED than firms in the agricultural industry. Since the mining industry has a higher scale and probability of producing carbon emissions, we predicted that firms in the mining industry would disclose more information on carbon emissions. In this study, we have not discussed whether disclosure is due to stakeholders’ pressure or voluntarily provided by the firms. We found that the coefficient of MINING was 2.370 and was significant to the 1% level (t = 3.53). This finding indicates that firms in the mining industry are likely to disclose more information related to carbon emissions. The finding was also robust after we corrected standard error. Overall, industry information increased the explanatory power by around 8% (R-squared from 26.2% to 34.2%) compared to the basic regression model (specification 1).

5. Conclusions and Suggestions

Indonesia’s 2010–2014 Medium Term Development Plan aims to achieve sustainable development for reducing carbon emissions, thus, every industry sector must implement sustainable development into their policies and programs, such as voluntary action to reduce global GHG emissions. Our contribution to the literature is that we have examined how the influence of firm size, corporate governance structure, and industry characteristics affect the level of voluntary carbon emission disclosure in response to Indonesia’s commitment to the program of emission reduction.

Based on the results and analysis in

Section 4, we find that the relationship between disclosure of carbon emissions and firm size has a positive and significant effect on the carbon emissions disclosure. In accordance with the legitimacy theory, larger firms are very vulnerable to higher pressure from the community and stakeholders, so they have a greater tendency to perform a higher level of carbon emissions disclosure to make the firms seem more legitimate in accordance with norms and values, based on applicable provisions regulated by the government.

Furthermore, larger firms make it possible to establish a larger board size; as we discovered, a larger board size has a positive impact on carbon emission disclosure, which is executed at a higher level. A larger board size enables firms to have a broad commissioners and directors’ way of thinking, as they seek to attain transparency to their stakeholders. This finding is also in conformity with stakeholder theory, which says that the company will seek satisfaction for its stakeholders when it contributes to economic resources that are important to the company, as the going concern of the company is dependent on the stakeholders.

However, still adrift on the corporate governance structure, we got an interesting result that is in contrast to most prior studies. Interestingly, we found that corporate boards whose independent board percentage was greater are somehow less likely to disclose more information on carbon emissions. As the situation stands in Indonesia, independent boards are more conservative on disclosing carbon-emission-related information to their stakeholders, and there is a lack of institutional ownership in Indonesia to improve corporate governance practices. Lastly, we found that that firms in the mining industry are more likely to disclose more information related to carbon emissions. We acknowledge that carbon emissions disclosures in this study are based on the authors’ own observations, and it is not yet known whether there really is a reduction of carbon in the companies’ activities. Examining the actual carbon emission reduction of the firms will extend the knowledge of the existing literature.

{kind=link}