Characterisation of Impact Funds and Their Potential in the Context of the 2030 Agenda

, , ,

, , ,

Abstract

:1. Introduction

- What common elements allow us to characterise and compare different impact funds in such a way that we can assess their suitability as an SDG financing tool?

- Are impact funds not only an objective in themselves, but also an appropriate financing tool to achieve the Sustainable Development Goals under the 2030 Agenda?

- (a)

- Considering the 4 principles of The Global Impact Investing Network, a proposal for the classification of impact funds has been developed.

- (b)

- This classification considers aspects such as: size of investment, investor profile, target area of impact and resulting impact.

- (c)

- In the Results section, the Spanish impact funds have been selected, and the proposed classification has been applied to obtain data on how they operate in terms of investment, region, etc.

- (d)

- On the other hand, a subsection focused on the Creas Impacto case study has been added to the results. In addition, the funds have been related to the sustainable development goals of the 2030 Agenda.

- (e)

- Finally, the discussion and conclusions obtained are added.

2. Materials and Methods

2.1. Intentionality of the Investment in Its Positive Social and Environmental Contribution Together with a Financial Return

2.2. Use of Evidence and Impact Data When Designing the Investment

2.3. Management of Impact Development

2.4. Contribution to the Growth of Impact Investment

3. Results

3.1. Study Case: Creas Impacto

3.2. Impact Investing as a Financing Tool for Agenda 2030

3.3. Investment and Impact Funds: SDG 17

- 17.3 Mobilise additional financial resources from multiple sources for developing countries.

- 17.5 Adopt and implement investment promotion systems in favour of least developed countries.

- 17.16 Enhance the Global Partnership for Sustainable Development, complemented by multi-stakeholder partnerships that mobilise and exchange knowledge, expertise, technology, and financial resources to support the achievement of the Sustainable Development Goals in all countries, particularly developing countries.

- 17.17 Develop and promote effective partnerships in the public, public-private and civil society spheres, building on partnership experience and resource mobilisation strategies.

- 17.19 By 2030, build on existing initiatives to develop indicators to measure progress towards sustainable development and to complement gross domestic product, and support statistical capacity-building in countries in development.

4. Discussion

- i.

- Foundations are positioned as entities with a high potential to promote the creation of impact funds in Spain, which still continue to be a new product limited to operating in the most important cities.

- ii.

- Spanish impact funds focus only on impact investment with portfolios formed solely by social organisations with a positive and quantifiable impact on society/environment. However, only two of the funds have the “European Social Entrepreneurship Fund” label, which they recently obtained, confirming the novelty of the impact product. Perhaps this could act as a catalyst if other funds take them as a reference.

- iii.

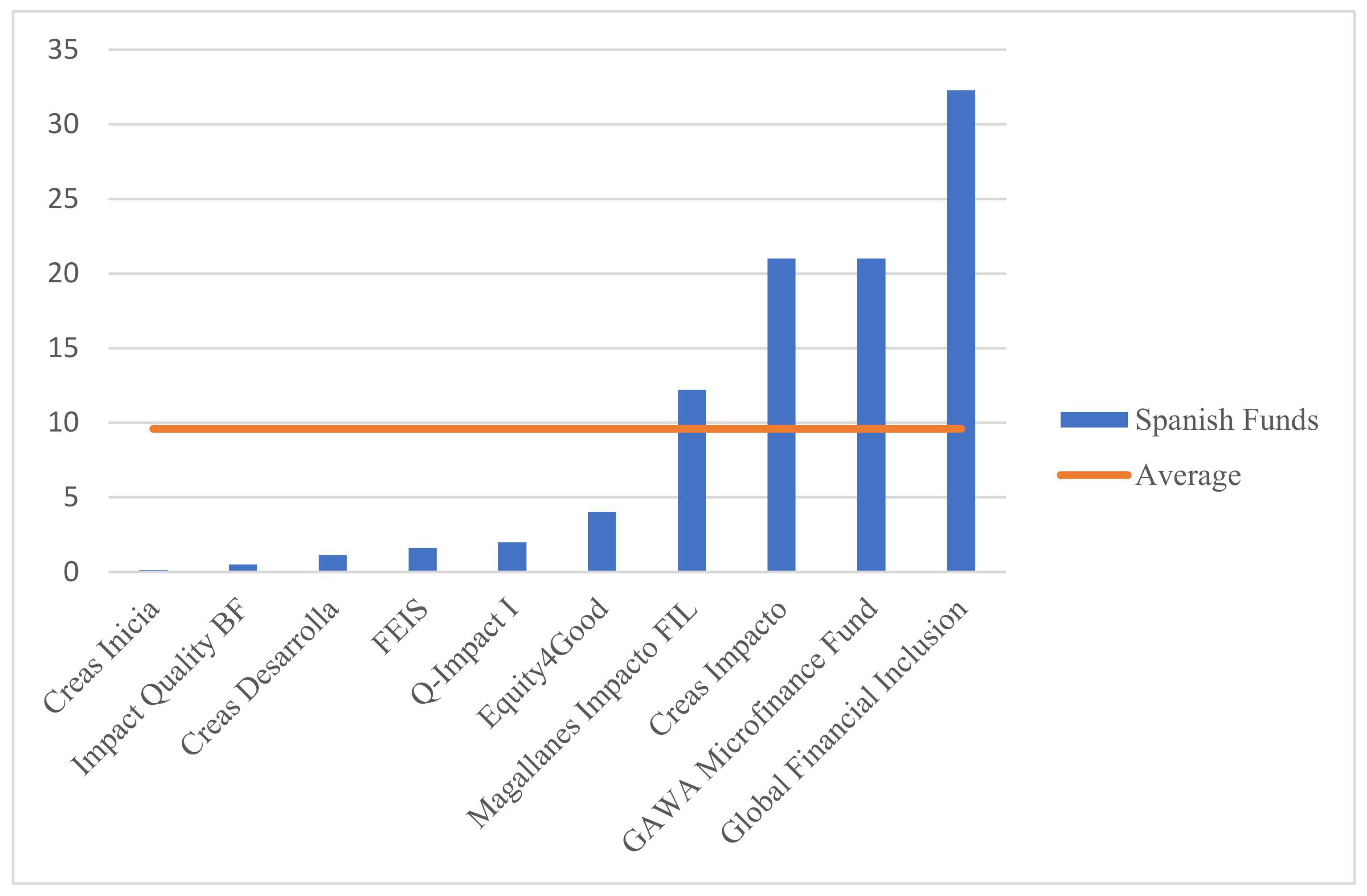

- The investment portfolios are very small and, proportionate to this, are the sizes of each investment. However, the financing tools they use offer diversity. Most of their capital comes from various private sector actors, although some public entities have been key to development.

- iv.

- The funds seek a balance between impact and profitability, but the data show rather low returns compared to those generally generated by traditional investment. The risk of investments is high, which is linked to being established as venture capital companies, where high risk is an intrinsic feature. The investment period ranges from 3 to 7 years. However, impact investment requires patient capital, with longer terms and continuous support. As identified in the Impact Forum report, patient capital is scarce because there are not enough players willing to assume the high risk involved in investing in social enterprises in their early stages: “companies with objectives of generating significant social impact need patient capital (more than ten years) with return expectations that reflect the additional costs and risks they face in achieving their objectives” [22].

- v.

- Moving on to the impact that Spanish funds seek to generate, these funds are not specialised in a specific topic, but rather the areas of impact are multiple with both social and environmental implications. These areas are not identified through the Sustainable Development Goals, nor are the results measured with the indices proposed by the Agenda but are carried out through those proposed by third parties. Therefore, based on the previous information, it is proposed as a main recommendation that the different funds unify and align their efforts in the same direction of work as the Agenda by including in the impact considerations, integrated throughout each of the stages that make up the investment process and the Sustainable Development Goals: objectives, targets and indicators.

- vi.

- Finally, the development phase of the target companies, in which a greater number of funds are concentrated, is the growth phase. As concluded in the report of Foro Impacto, new funds need to be created that focus on the pregrowth stages. There is a funding gap between the initial phase, when social enterprises outgrow the requirements to receive grants, but are nevertheless too small and too high risk for investors.

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Classification of Impact Funds | |

|---|---|

| Fund data | |

| Fund name: | Management company name: |

| Headquarter city: | Year of first closure: |

| The portfolio consists only of impact investment projects: | ☐ Yes ☐ No |

| Is labelled ESEF: | ☐ Yes ☐ No |

| Size of investment | |

| Size of the fund as a function of its total capital (EUR): | Size of each investment (EUR): |

| Financing instruments: | ☐ Debt/Loan ☐ Capital ☐ Donation ☐ Capital Hybrid Model |

| ☐ Venture Philanthropy Hybrid Model ☐ Other | |

| Investor profile | |

| Investor motivation: | ☐ Financial return ☐ Social and environmental impact |

| Financial return expectations (profitability): ____ % | Risk aversion (scale from 1 to 7): ____ |

| Investment timeline: | ☐ Short (< 1 year) ☐ Medium (1–5 years) ☐ Long (> 5 years) |

| Impact target area | |

| Main aim impact: | ☐ Environmental ☐ Social ☐ Both |

| Impact target: | ☐ One ☐ Multiple |

| What are they? | Are the impact areas identified by the fund through the sustainable development objectives? ☐ Yes ☐ No |

| Resulting impact | |

| Scale on which the impact is generated: | ☐ Local ☐ Regional ☐ National ☐ International ☐ Undetermined |

| Geographic location of impact: | ☐ Europe ☐ Asia ☐ Africa ☐ North America ☐ South America |

| The measurement of the impact is done by: | ☐ Fund-specific rates ☐ Objective rates of sustainable development |

| ☐ Rates established by another organisation. Which one? | |

| Other features | |

| State of development of the target company: | ☐ Seed ☐ Start ☐ Growth ☐ Maturity |

| Source of capital for the fund: | ☐ Public ☐ Private ☐ Both |

| Fund’s main investors: | |

References

- Global Impact Investment Network. Financing the Sustainable Development Goals: Impact Investing in Action. 2018. pp. 1–28. Available online: https://thegiin.org/assets/Financing%20the%20SDGs_Impact%20Investing%20in%20Action_Final%20Webfile.pdf (accessed on 18 August 2019).

- Impact Hub Madrid. Transformar la Ciudad a Través de la Inversión de Impacto; Impact Hub Madrid: Madrid, Spain, 2018. [Google Scholar]

- Unirisco. Available online: http://www.unirisco.com/ (accessed on 25 May 2019).

- Alonso, J.A. Movilizando los recursos y los medios de apoyo para hacer realidad la agenda de desarrollo post-2015. Coop. Esp. Madr. 2015, 53, 1689–1699. [Google Scholar] [CrossRef]

- PDNU (Programa de Desarrollo de las Naciones Unidas). Financing the 2030 Agenda; Programa de Desarrollo las Naciones Unidas: New York, NY, USA, 2018. [Google Scholar]

- Keeble, B.R. The Brundtland Report: “Our Common Future”. Med. War 1988, 4, 17–25. [Google Scholar] [CrossRef]

- Egelston, A.E. Sustainable Development: A History; Springer Science & Business Media: Berlin, Germany, 2013. [Google Scholar] [CrossRef] [Green Version]

- Gómez Gutiérrez, C.; Díaz Duque, J.A. Origen del Concepto de Desarrollo Sostenible; Universidad de Alcalá: Madrid, Spain, 2013; pp. 7–16. [Google Scholar]

- Sierra Montoya, J.E. Los Tres Pilares del Desarrollo Sostenible. 2019. Available online: http://www.i-ambiente.es/?q=blogs/los-tres-pilares-del-desarrollo-sostenible (accessed on 25 July 2019).

- Luengo Montero, M. El Futuro Será Sostenible o no Será. 2018. Available online: https://elpais.com/elpais/2018/09/11/eps/1536681073_060705.html (accessed on 25 March 2019).

- Razavi, S. The 2030 Agenda: Challenges of Implementation to Attain Gender Equality and Women’s Rights; Gender & Development: London, England, 2016; pp. 24–41. [Google Scholar]

- Sachs, J.D. From millennium development goals to sustainable development goals. Lancet 2012, 379, 2206–2211. [Google Scholar] [CrossRef]

- Lomazzi, M.; Borisch, B.; Laaser, U. The Millennium Development Goals: Experiences, achievements and what’s next. Glob. Health Act. 2014, 7 (Suppl. S1). [Google Scholar] [CrossRef] [PubMed]

- CEPAL, B. Agenda 2030 para el Desarrollo Sostenible. 2019. Available online: https://biblioguias.cepal.org/c.php?g=447204&p=6366258 (accessed on 15 July 2019).

- Clark, H. Openness for All: The Role for OGP in the 2030 Development Agenda; Open Government Partnership Summit: Washington, DC, USA, 2015. [Google Scholar]

- Colglazier, B.W.; Na, U. Sustainable development agenda: 2030. Science 2015, 349, 1048–1050. [Google Scholar] [CrossRef] [PubMed]

- UE. Reglamento UE No346/2013 del Parlamento Europeo y del Consejo de 17 de Abril de 2013 Sobre los Fondos de Emprendimiento Social Europeos; European Parliament: Strasbourg, France, 2013; pp. 18–38. [Google Scholar]

- Comisión Europea. Construir un Ecosistema para Promover las Empresas Sociales en el Centro de la Economía y la Innovación Sociales. Comunicación de La Comisión Al Parlamento Europeo Al Consejo, Al Comité Económico y Social Europeo y Al Comité de Las Regiones; European Parliament: Strasbourg, France, 2011. [Google Scholar]

- Rial, L. ¿Cómo Afecta el Tamaño de un Fondo de Inversión a la Rentabilidad? 2019. Available online: https://www.rankiapro.com/como-afecta-tamano-fondo-inversion-rentabilidad/ (accessed on 30 July 2019).

- BBVA. ¿Qué es el Horizonte Temporal en Una Inversión? 2018. Available online: https://www.bbvaassetmanagement.com/am/am/es/es/particular/actualidad/noticias/tcm:864-769645/horizonte-temporal-inversion (accessed on 25 July 2019).

- Sims, D.W.; Queiroz, N. Fish stocks: Unlimited by-catch limits recovery. Nature 2016, 531, 448. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Urriolagoitia, L.; Hehenberger, L. La Inversión de Impacto en España: Intermediación de Capital Una llamada a la Acción Para Impulsar el Mercado de las Inversiones de Impacto en España en el Marco del GSG; Foro Impacto: Madrid, Spain, 2019. [Google Scholar]

- Triodos Investment Management. Available online: https://www.triodos-im.com/ (accessed on 29 August 2019).

- Impact Forum. In Proceedings of the VI S2B Impact Forum, Barcelona, Spain, 25 October 2019.

- Amin, A.; Cameron, A.; Hudson, R. The social economy in context. Placing Soc. Econ. 2010, 1–15. [Google Scholar] [CrossRef]

- Cherrier, H.; Goswami, P.; Ray, S. Social entrepreneurship: Creating value in the context of institutional complexity. J. Bus. Res. 2018, 86, 245–258. [Google Scholar] [CrossRef]

- Dwivedi, A.; Weerawardena, J. Conceptualizing and operationalizing the social entrepreneurship construct. J. Bus. Res. 2018, 86, 32–40. [Google Scholar] [CrossRef]

- Hervieux, C.; Voltan, A. Framing Social Problems in Social Entrepreneurship. J. Bus. Ethics 2018, 151, 279–293. [Google Scholar] [CrossRef]

- Macke, J.; Sarate, J.A.R.; Domeneghini, J.; da Silva, K.A. Where do we go from now? Research framework for social entrepreneurship. J. Clean. Prod. 2018, 183, 677–685. [Google Scholar] [CrossRef]

- Sud, M.; Vansandt, C.V.; Baugous, A.M. Social entrepreneurship: The role of institutions. J. Bus. Ethics 2009, 85 (Suppl. S1), 201–216. [Google Scholar] [CrossRef]

- Félix González, M.; Husted, B.W.; Aigner, D.J. Opportunity discovery and creation in social entrepreneurship: An exploratory study in Mexico. J. Bus. Res. 2017, 81, 212–220. [Google Scholar] [CrossRef] [Green Version]

- McMullen, J.S.; Bergman, B.J. The promise and problems of price subsidization in social entrepreneurship. Bus. Horiz. 2018, 61, 609–621. [Google Scholar] [CrossRef]

| Impact Fund | Bibliography |

|---|---|

| GAWA Microfinance Fund | GAWA Capital, 2019 |

| Global Financial Inclusion Fund | GAWA Capital, 2019 |

| Magallanes Impacto FIL | Magallanes Value, 2019 |

| Q-Impact I | Qualitas Equity, 2019 |

| Fondo de Emprendimiento e Innovación Social | Seed Capital Bizkaia, 2019 |

| Creas Impacto | Creas, 2019 |

| Creas Desarrolla | Creas, 2019 |

| Creas Inicia | Creas, 2019 |

| Impact Equity S.L. | Ship2B, 2019 |

| Equity4Good S.L. | Ship2B, 2019 |

| Next Venture Capital | - |

| Rezinkers | - |

| Fund Data | 1 | Fund Name | GAWA Microfinance Fund | Creas Desarrolla | Creas Inicia | Global Financial Inclusion | Fondo de Emprendimiento e Innovación Social | Impact Equity BF | Creas Impacto | Magallanes Impacto FIL | Equity4Good | Q-Impact I |

| 2 | Management Company Name | GAWA Capital (Madrid) | Fundación Creas Valor Social | Fundación Creas Valor Social | GAWA Capital (Madrid) | Seed Capital Bizkaia | Fundación Ship2B | Self-managed | Magallanes Value Investors | Fundación Ship2B | Qualitas Equity | |

| 3 | Headquearters city | Luxemburgo | Zaragoza/Madrid | Zaragoza/Madrid | Luxemburgo | Bilbao | Barcelona | Madrid | Madrid | Barcelona | Madrid | |

| 4 | Year of First Closure | 2010 | 2012 | 2013 | 2014 | 2014 | 2016 | 2018 | 2018 | 2018 | 2019 | |

| 5 | Portfolio formed only by impact investment projects | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | Minimum 70% | |

| 6 | Owns FESE Label | No | No | No | No | No | No | Yes | No | No | Yes | |

| Investment Size | 7 | Size of the fund as a function of its total capital | 21 million | 750 thousand–1.5 million | 125 thousand | 32.3 million | 1.6 million | 0.5 million | 221 million 30 million (objective) | 12.2 million | 4 million | 2 million 30 million (objective) |

| 8 | Size of each investment | 1–3.5 million | 25–250 thousand | 10–25 thousand | 1–3.5 million | Maximum 600 thousand | 50–100 thousand | 500 thousand–3 million | n/a | 40–400 thousand | 500 thousand–3 million | |

| 9 | Financing instruments | Capital 35% and Debt 65% | Capital and Debt | Capital and Debt | Capital 35% and Debt 65% | Capital and Debt | Venture Philantropy | Capital, debt and quasi-capital | Unquoted debt | Venture Philantropy | Capital and Debt | |

| Investor Profile | 10 | Investor Motivation | n/a | Medium | Prioritizes impact | n/a | n/a | Medium | Medium | n/a | Medium | Medium |

| 11 | Profitability | 6.40% | 2.00% | No | 7.0–8.0% | 10.0–15.0% | 50.0% (x1.5) | 7.00% | 2.0–4.0% | 50.0% (x1.5) | 6.00% | |

| 12 | Risk aversion (scale from 1 to 7) | n/a | n/a | n/a | n/a | n/a | n/a | n/a | Big risk | n/a | 6 | |

| 13 | Investment timeline | 3–7 years | n/a | n/a | 3–7 years | Long | n/a | 3–7 years | 5 years | n/a | Long term | |

| Target Area of Impact | 14 | Impact with a main purpose | Social | Both | Both | Social | Both | Both | Both | Social | Both | Both |

| 15 | Impact target area | Unique | Multiple | Multiple | Unique | Mutiple | Mutiple | Mutiple | Unique | Mutiple | Mutiple | |

| 16 | Which are they? | Financial inclusion | n/a | n/a | Financial inclusion | Renewable energies, organic farming, bioconstruction, people at risk of social exclusion, development cooperation, fair trade | Environment, climate, health and social | Health and welfare, environmental sustainability, education, social innovation | Financial inclusion | Environment, climate, health and social | Sustainability, education, social inclusion | |

| 17 | Identified as SGSs | No | No | No | No | No | No | No | No | No | No | |

| Resulting Impact | 18 | Impact scale | n/a | n/a | n/a | n/a | Local: Bizkaia | n/a | n/a | n/a | n/a | n/a |

| 19 | Place where the impact is generated | Latin America, Asia, Sub-Saharan Africa | Spain | Spain | Latin America, Asia, Sub-Saharan Africa | Spain | Spain | Europe and Spain | Developing countries | Spain | Europe and Spain | |

| 20 | Impact measurement | IRIS (GIIN), The Social Performance Task Force, ODS | Theory of change | Theory of change | IRIS (GIIN), The Social Performance Task Force, ODS | n/a | Theory of change | EVPA and Theory of change | IRIS (GIIN), ODS | Theory of change | IRIS (GIIN) | |

| Other features | 21 | State of development of the target company | Growth | Start | Seed | Growth | All | Seed and start | Growth | Growth | Seed and start | Growth |

| 22 | Origin of the fund's capital | Private | Private | Private | Private and Public | Public | Private | Public | Private | Private and Public | Private | |

| 23 | The fund's main investors | Family offices, development institutions, individuals | Family offices and private investors | Donor partners | Family offices, development institutions, individuals, AECID | Provincial Council of Bizkaia | 36 investors | FEI, AXIS-ICO | n/a | European Investment Fund, Impact Equity | Investors of the Qualitas Equity funds |

| Creas Inicia | ||

|---|---|---|

| Social Enterprise | Description | Impact Area |

| iWOPI | Platform through which the user “donates” the km of sport he or she does to social projects that collaborate with the application | Health Funding |

| Civiclub | Encourage society to take sustainable actions through a points and rewards system | Social and environmental awareness |

| Disjob | Employment page for people with disabilities | Inclusion Work |

| Sensovida | Telecare system for the elderly | Health |

| Creas Desarrolla | ||

| Social Enterprise | Description | Impact Area |

| Koiki | “Last mile” delivery system by people in social centres | Inclusion Work Environment |

| Emzingo | Training program on innovation, responsible leadership and the connection between business performance and social and environmental impact | Education |

| Sadako | Robots with artificial intelligence that separate and recycle garbage in landfills | Technology |

| Jump Math | Mathematics education programme for primary and secondary school children | Education |

| Whats cine | Innovative audio-visual platform adapted for people with visual and hearing disabilities | Inclusion |

| Smileat | Locally produced organic baby food products and healthy recipes | Environment Nutrition Health |

| Classification of Impact Funds | |

|---|---|

| Fund data | |

| Fund name: Creas Impacto | Management company name: Self-management |

| Headquarter city: Madrid | Year of first closure: 2018 |

| The portfolio consists only of impact investment projects: | x Yes ☐ No |

| Is labelled ESEF: | x Yes ☐ No |

| Size of investment | |

| Size of the fund as a function of its total capital (EUR): 21 million (objective 30 million) | Size of each investment (EUR): 0.5–3 million |

| Financing instruments: | x Debt/Loan x Capital ☐ Donation x Capital Hybrid Model |

| ☐ Venture Philanthropy Hybrid Model ☐ Other | |

| Investor profile | |

| Investor motivation: | x Financial return ☐ Social and environmental impact |

| Financial return expectations (profitability): 7% | Risk aversion (scale from 1 to 7): - |

| Investment timeline: | ☐ Short (< 1 year) ☐ Medium (1–5 years) x Long (> 5 years) |

| Impact target area | |

| Main aim impact: | ☐ Environmental ☐ Social x Both |

| Impact target: | ☐ One x Multiple |

| What are they? Education, health and welfare, social innovation and environmental sustainability | Are the impact areas identified by the fund through the sustainable development objectives? ☐ Yes x No |

| Resulting impact | |

| Scale on which the impact is generated: | ☐ Local ☐ Regional ☐ National ☐ International x Undetermined |

| Geographic location of impact: | x Europe ☐ Asia ☐ Africa ☐ North America ☐ South America |

| The measurement of the impact is done by: | ☐ Fund-specific rates ☐ Objective rates of sustainable development |

| x Rates established by another organisation. Which one? EVPA | |

| Other features | |

| State of development of the target company: | ☐ Seed ☐ Start x Growth ☐ Maturity |

| Source of capital for the fund: | x Public ☐ Private ☐ Both |

| Fund’s main investors: | FEI and ICO |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Santamarta, J.C.; Storch de Gracia, M.D.; Carrascosa, M.Á.H.; Martínez-Núñez, M.; García, C.d.l.H.; Cruz-Pérez, N. Characterisation of Impact Funds and Their Potential in the Context of the 2030 Agenda. Sustainability 2021, 13, 6476. https://0-doi-org.brum.beds.ac.uk/10.3390/su13116476

Santamarta JC, Storch de Gracia MD, Carrascosa MÁH, Martínez-Núñez M, García CdlH, Cruz-Pérez N. Characterisation of Impact Funds and Their Potential in the Context of the 2030 Agenda. Sustainability. 2021; 13(11):6476. https://0-doi-org.brum.beds.ac.uk/10.3390/su13116476

Chicago/Turabian StyleSantamarta, Juan C., Mª Dolores Storch de Gracia, Mª Ángeles Huerta Carrascosa, Margarita Martínez-Núñez, Celia de las Heras García, and Noelia Cruz-Pérez. 2021. "Characterisation of Impact Funds and Their Potential in the Context of the 2030 Agenda" Sustainability 13, no. 11: 6476. https://0-doi-org.brum.beds.ac.uk/10.3390/su13116476