1. Introduction

Energy has secured its place as one of the core needs in modern life [

1]. It plays a fundamental role in improving the standard of living and economic development of a country [

2,

3]. Modern life depends on reliable energy resources [

4,

5]. Proper energy supply plays a vital role in developing the economy [

6]. One of the prime benefits of reliable energy sources is eliminating the need and usage of fossil fuel, i.e., coal, oil, and natural gas for electricity generation [

7]. Besides, it is helpful for countries that do not have electricity access [

8,

9].

Recently, the energy demand has tremendously increased, and it is considered one of the world’s crucial problems [

10]. Energy shortage seriously affects people’s lives, professional and non-professional activities [

11]. The governments of developing countries are facilitating renewable energy expansion with policy strategies [

12]. Similar to other developing countries, Pakistan requires massive energy to support its industry and large population [

13]. The electricity gap between demand and supply has been uncontrolled in the past few years. The country faces the worst load shedding during the summer season, i.e., 10–12 h per day in urban areas and 16–18 h per day in rural areas [

14]. Pakistan is considered an energy-deficient country [

13]. In Pakistan, the available energy production sources are not enough to satisfy the country’s increasing energy demands. In the preceding years, the country’s power sector focused on generating energy from hydropower sources. Later, until 1994, the only electricity producer in the country was Water and Power Development Authority (WAPDA) [

15]. Independent Power Producers (IPPs) joined the system later. The focus of IPPs was to produce energy from thermal power plants operated on conventional fossil fuels. After 1994, the energy policy of Pakistan was introduced. The Private Power and Infrastructure Board (PPIB) was established to support the IPPs to satisfy energy needs.

Presently, 67% of the energy demand in Pakistan is met with non-renewable resources, which are increasing at more than 10% annually, and the annual average growth rate of energy demand will be 8.35% by 2050 [

16,

17]. Pakistan is facing an energy crisis due to two main reasons: first, energy policy and energy structure are mainly dependent on conventional energy sources, which are expensive and always under pressure due to shortages [

18,

19]. Second, Pakistan’s renewable energy sector only participates in 0.3% of overall energy needs, which is negligible [

20]. The country’s power production sources include natural gas (44%), oil (35.5%), hydropower (11%), coal (7%), nuclear (2%), and renewable energy (0.3%).

Severe energy crises have destructive impacts on the national economy of Pakistan [

21]. Solar energy resources are considered powerful, effective, and accessible on the Earth compared to other alternative energy sources [

22,

23]. The international energy agency explored that worldwide solar capacity was 402 gigawatts (GW) at the end of 2020 [

24]. Pakistan has a total estimated potential for solar energy of about 1600 GW, which can support the country’s energy needs if used effectively [

25]. The sustainable development of solar energy projects requires analyzing renewable energy policy and policy instruments to attract foreign direct investment and implement green technology strategies. There is a lack of green technology strategy for the sustainable development of solar power projects with financial analysis. Financial planning for assessing financial performance and improvement in solar power generation is needed by green technology to develop solar power projects.

As a result, the PPIB attracts the investors who installed the thermal power plants. Different phases of energy policy were introduced at subsequent periods in the country, but unfortunately, they cannot achieve the proposed targets. The energy policy of 2000 failed because it could not satisfy the country’s energy needs at the desired prices. As a result, the Alternate Energy Development Board (AEDB) was formed in 2003 to formalize alternate and renewable energy (ARE). The AEDB aims to support the private energy producers in the country. The country’s first energy policy regarding renewable energy was introduced in 2006 [

26]. The main objective of this policy was to convince IPPs to invest in renewable energy projects. In Pakistan, the first solar power project was introduced by the Pakistan Engineering Council (PEC) in 2010 with a capacity of 178 Kilowatt (kW) [

27]. After that, the Punjab Government initiated Quaid-e-Azam Solar Power Project to meet the country’s increasing energy demand. This project generated 1000 Megawatt (MW) in the initial phase. Similarly, the government of Pakistanis is also planning to establish more solar power projects in other parts of the country [

28]. Some solar power projects of Pakistan, along with project capacity, are presented in

Table 1.

Numerous investigations have been conducted on the energy crisis [

30,

31,

32,

33,

34,

35,

36,

37,

38,

39], solar power project installation, and site selections [

40]. Still, there is a lack of literature regarding energy project failures and sustainable development for solar energy projects with green technology strategy. There is also a lack of literature related to the impact of capital budgeting techniques on the performance of solar power projects by using green technology for sustainable development. Capital budgeting is a set of techniques used to analyze and decide a proposed investment in the new solar project or production line. Capital budgeting techniques are also known as analyzing and planning processes to determine the long-term investment of the industry and deciding strategies for new project investment, matching with expenditure and profit by considering critical factors such as capital return, the economic value of the project, availability of funds, accounting methods, and taxation. Solar firms also adopt traditional capital budgeting approaches, including internal rate of return, net present value, payback period, and profitability index. The financial performance of the energy projects can be assessed by applying these techniques. Financial performance is a subjective measure in which a solar firm can maintain the standards to use assets and generate revenue. The investor and analysts use the specific term to compare the same solar projects or firms as a general measure for the financial backbone of the firm at a particular time. Financial performance shows a snapshot of a solar project’s economic health and general well-being for investors and shareholders. A primary document is required to publish annually and reports the financial performance of the solar firm. A solar firm or project’s financial performance can be evaluated through financial statements, including cash flows, the income statement, and the balance sheet. The indicators of financial performance specify the economic position of the solar project.

Previous investigations regarding the energy sector in Pakistan have mainly pinpointed (i) energy gap between demand and supply, (ii) energy mix, (iii) evaluation of the country’s energy sector, (iv) the pros and cons of the introduction of renewable energy in the system, (v) future of energy sector, and (vi) renewable energy generation sources. Despite the long-standing interest of earlier researchers, specific gaps exist among all these studies, i.e., (i) there is a need to apply green technology strategy for the sustainable development of solar power projects through financial analysis using capital budgeting techniques, (ii) the lack of financial analysis of solar power projects discourage the investors and all type of investment, (iii) financial planning for assessment of the financial performance of solar power projects need to attract foreign direct investment, and (iv) enhancing and improving solar energy generation using green technology strategies for the sustainable development in Pakistan. The present study contributes to the existing research gaps by addressing the following questions: (i) examine the importance of green technology strategy for the sustainable development of solar power projects in Pakistan, (ii) highlight the importance of financial planning for the financial performance of solar power projects using capital budgeting techniques, and (iii) empirically investigate the moderating role of cost and riskiness of the methods on the sustainable development of solar power projects.

The remaining study is organized as follows:

Section 2 provides a brief literature review.

Section 3 deliberates research methodology.

Section 4 discusses the data analysis and results of the study.

Section 5 indicates the discussion and implication. Finally,

Section 6 concludes the research and provides study limitations.

2. Literature Review

The corporate financial policy includes various pillars, and investment decision tends to be one of them. The vast body of investment decisions is evident from multiple aspects, which in financial policies. These policies usually address the capital budgeting techniques and their usage among investment decisions [

14]. The establishment of capital budgeting indicates numerous factors influencing the specific areas of projects. Although different studies in developed economies are categorized, investment decisions are dominant over capital budgeting techniques. At the same time, interpreting solar energy technology in some other countries, various analyses were performed through statistical and financial means [

41]. Hence, a green technology strategy for the sustainable development of solar power projects is a possible solution to assess the financial performance of solar power projects through capital budgeting techniques. These analyses have dominantly stated the assessments through proper objectives of financial planning and improvements depicted in Pakistan. Usually, financial planning is more dominant in the projects initiated for a better profitability index [

42]. Therefore, the elements of financial planning have mainly improved in developing and developed countries [

43]. Capital budgeting techniques can closely assess the sustainable development of solar power projects. The improvement adapted to specific conditions of capital budgeting is closely associated with projected investment decisions. While enumerating the dominance of investment decisions, particular structures of capital budgeting techniques were described. These structures include debt–equity and the cost of capital, linking its association with investment decisions. Reasonable, sustainable efforts are depicted in the projects while emphasizing financial crisis with appropriate management decision making, assessments, and strategic planning [

44].

Solar power projects are the most highlighted innovation globally for energy production through different electrons and elements [

45]. The creation of technology will widely link with the structures of capital budgeting. Additional parameters were especially more emphasized to enumerate the association of financial planning. The association is a clear indication of financial planning assessment over various projects. The presentation clarifies the association of financial risks connected with the numerous infrastructure projects. Therefore, applying net present value (NPV) with other capital budgeting techniques helps establish uncertain situations prevailing in mitigation strategies. Financial planning usually depends on cash flows primarily used for budgeting and forecasting [

45]. Therefore, the assessments are more likely to be dominated by the factors of capital budgeting. The evaluation would not only help to capture the weak areas of performance but would also be beneficial for supporting the decision making process. Financial planning contains the complete process of assessment performed by many large companies and assessment agents. Usually, companies feel reluctant to have expert services essential in managing the financial planning for solar projects and others. This financial planning involves many factors that importantly assert a beneficial role for the capital budgeting techniques [

46]. Although companies cannot grow without adequate financial planning and management of their cash flows and company profits, in this context, the roles for assessing financial planning are described with the fair election of elements that could control the economic efficacy of companies. It is a complete process of planning, forecasting, and reporting with comprehensive analysis. Therefore, financial planning of solar power projects for sustainable development is important with a green technology strategy.

Corporate financial planning inserts their overall aspects to assert their objectives and financial performance. These objectives are more related to financial planning as well as operational decision making. Therefore, the company’s progress is the view with the limelight aspects of plans and goals designed under the capital budgeting context [

47]. Many obstacles were also grounded with the help of financial planning assessments that grow the company’s profits. Some critical issues were also eliminated with the economic evaluation and forecasting and considered an eye toward the company’s future. Financial planning includes income, investment, financial statements, expenses, taxes, and other financial affairs reviewed to strengthen capital budgeting [

48]. Thus, the elements of financial planning declare some factors that significantly influence the financial performance of various projects and businesses. Economic performance and the sustainable development of solar power project is only possible with financial planning. The importance of corporate or solar project-related companies is only with capital budgeting and financial planning elements. These elements comprise NPV, internal rate of return (IRR), payback period (PBP), and profitability index (PI), with significant consideration of risk and cost toward financial performance. The initial investment in the project is required to be analyzed to place the effectiveness of financial planning. This comparative assessment helps to maintain the expenses and knock the doors of profits through net present value. The potential of investment is prevalent in the internal rate of return that assesses the profitability among businesses of various companies [

49]. The investment could be a complete and extended channel for the assessment in capital budgeting for financial performance. Many projects are essential for the companies as well as the countries. Therefore, the companies primarily focused more upon the payback period for the sustainable development of the solar power projects.

The literature shows numerous studies conducted on the energy sector of Pakistan. For instance, [

50] focused on the energy mix of the Pakistani power sector. The energy sector was proposed that the transition from dominant hydro energy to thermal dominant energy mix was not financially suitable for the country and resulted in debt enhancement [

51]. The authors of [

52] discussed those factors associated with the gap between energy supply and demand and found the best renewable energy sources in Pakistan. They concluded that the government must prioritize the energy sector and formulate multidimensional policies to control the energy crisis. The authors of [

53] examined the present status and future of solar energy from the developing economies’ perspective. The study focused on the ongoing and upcoming renewable energy projects such as solar, wind, biogas, and hydropower. Research findings proposed changing the energy mix by giving more shares to solar energy in the system and by keeping in view the ongoing renewable energy projects, which will minimize the energy demand and supply gap with a green technology strategy. These outcomes support the sustainable development of renewable energy projects in Pakistan, and solar power projects were top rated.

Consequently, it is necessary to induce the appropriate measure of payback while executing proper financial assessment. The profitability index of the projects is more precisely crucial for the countries due to more investment towards other projects. Therefore, the formulated profitability index approach helps assert the business project’s significant performance [

54]. All of the factors are related to the assessment of green technology for the sustainable development of solar power projects with financial planning while considering the capital budgeting eminence. There is a broad association of risk factors with financial planning. These risk factors are uncertain due to some strange events and other safety environments and issues.

4. Data Analysis and Results

Our research employed the structural equation modeling (SEM) method for data analysis objectives [

113]. The study adopted this method to analyze the relational dimensions because it is a component-focused method [

114]. PLS-SEM has frequent usage and appropriateness, which is why the author adopted it in this study; the subsequent studies are evidence [

115,

116]. Structural equation modeling (SEM) is more advantageous than other methods of traditional statistical analysis. It is helpful for statistical analysis regarding efficiency, convenience, and accuracy [

117,

118]. SEM covers the problems of first-generation analysis, but it is a second-generation technique. SEM can assist in analyzing abundant variables at the same time because it is a multivariate analysis process. SEM is continuously popular in business research because it can simultaneously deal with complex and multiple relationships [

119].

The inappropriate adoption of analytical methods can cause inaccurate conclusions; however, an appropriate statistical technique is most important for management and social science research [

120]. Measurement and structural models are two-stage analysis approaches of PLS-SEM that include measurement results in two steps [

121]. Reliability and validity tests or the assessment of the inner model was included in the measurement assessment model for selected and currently working solar power projects in this study. Hypotheses and relationships testing, or the evaluation of the outer model, formed a structural assessment model for selected solar projects. The present research used PLS 3.0 software for primary data analysis and examined the links among the understudy variables. Additionally, partial least square path modeling has higher statistical power than covariance-based structural equation modeling. PLS-SEM is more advantageous to intercept relationships among the variables.

In addition, the smart-PLS for variance-based structural equation modeling (SEM) uses the partial least squares (PLS) path modeling method to examine the nexus among the variables [

122]. The purpose of smart-PLS is to hypothesize testing in the research, and the complex model research has adapted to it. The smart-PLS has two approaches: a measurement assessment model and a structural model for the analysis used in this study. The assessment measurement model includes the reliability and validity of the constructs checked with convergent and discriminant validity. The convergent validity related to the correlation among the items examined using the Chronbach Alpha, composite reliability (CR), and items loading. However, the discriminant validity is associated with the correlation among variables examined using Fornell Larcker, cross-loading, and Heterotrait–Monotrait ratio. In addition, the assessment of the measurement model includes the testing of hypotheses that were reviewed using path analysis—the analysis of the study discussed in the findings section.

The path analysis has shown the links among the variables in this study. The results revealed that capital budgeting techniques such as net present value, internal rate of return, payback period, and profitability index positively impact the selected and currently working solar power projects’ financial performance, and they accept H1, H2, H3, and H4. In addition, the findings also indicated that cost and riskiness of techniques significantly moderated among the nexus of internal rate of return, profitability index, and financial performance of the selected and working solar power projects mentioned in

Table 1, and they accept H6 and H8. Finally, the findings section of the measurement model has first shown the nexus’s convergent validity among the selected solar power project items in this study. The figures show that the loadings and average variance extracted (AVE) values are higher than 0.50, while Alpha and CR values are more significant than 0.70. These values have indicated that convergent validity is the valid and high connection among the items. The results of the research also include the assessment of correlation among items named convergent validity. The figures highlighted that the factor loadings are more significant than 0.50, Alpha values are more than 0.70, AVE values are also higher than 0.50, and CR values are also greater than 0.70. These values have indicated a high correlation among items and valid convergent validity. The results are reported in

Table 2.

4.1. Measurement Assessment Model

In the present research, measurement model evaluation was required to conduct reliability and validity tests for all the given constructs. The measurement model confirms the reliability and validity of the constructs and the factor loadings of all items approved by the model [

123]. The measurement evaluation model is consistent on reliability tests (item reliability and internal consistency reliability) and validity tests (convergent validity and discriminant validity) [

124]. Convergent validity has been measured over the AVE, internal consistency reliability has been measured over composite reliability (CR), and item reliability has been measured over outer loading in this study. All item loadings are well upstairs with the threshold value of 0.5 [

125]; see

Table 2. The analysis of the study verified that all of the averaged factor loadings were greater than 0.50, and each observation contributed to the constructed variable [

126]. AVE exceeds the suggested value of 0.5. The composite reliability value for each standard exceeds the cut-off point of 0.7, which displays that the measurements are reliable [

127]. The results of the current selected solar power projects designate that all the values of AVE are between 0.536 (cost and riskiness of methods) and 0.908 (internal rate of return method). CR values are between 0.820 (cost and riskiness of methods) and 0.975 (internal rate of return method). The values of all additional loadings are between 0.5 and 0.959.

All verified validity and reliability values in this measurement model are given below in

Table 3,

Table 4 and

Table 5. All the factor loading values are more significant than 0.50; thus, the convergent validity of all items is valid in the measurement assessment model.

The findings of this research also include the assessment of correlation among variables named as discriminant validity. First, a conventional method of Fornell–Larcker and cross-loading were used to test the discriminant validity (see

Table 3). These values indicated a low correlation among variables and verified the discriminant validity of the selected solar power projects. The bold values in

Table 4 show that all factors have a strong relationship but weak relationships with other factors. The bold values of the cross-loadings table were compared with other factors row-wise to check discriminant validity. The cost and riskiness method (CRM) values are greater than row-wise other factors and show strong discriminant validity in this study and so on. The other left and right values are smaller compared to bold values in

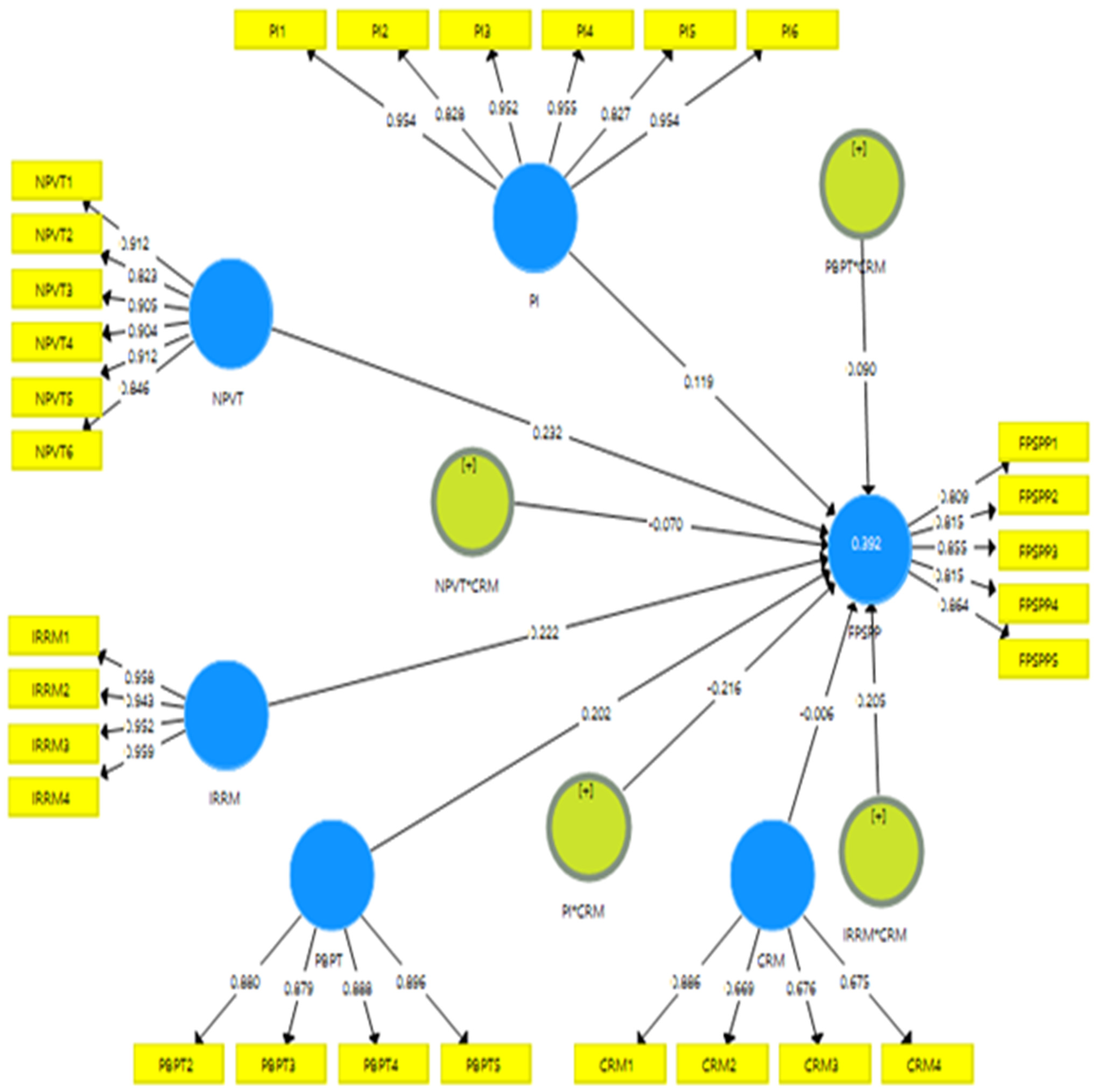

Table 4. The measurement assessment model is shown in

Figure 2, which indicates the factor loading of the variables.

The Heterotrait–Monotrait ratio of correlations (HTMT) for discriminant validity measure is considered more suitable due to different researchers’ criticism on the criteria of Fornell-Larcker [

128]. The value of discriminant validity confirms if it is less than 0.85 [

129] or 0.90 [

113]. All values are less than 0.90 in

Table 5. The findings section has also shown the discriminant validity that is about the nexus among the variables. First, cross-loadings and Fornell Larcker are used to test the discriminant validity. The figures have shown that the values that indicated the nexus with the variable itself are higher than those with other variables. These values explored that discriminant validity is the valid and low connection among the variables. All values are highlighted in

Table 5. Second, the latest method, such as the HTMT ratio, has been used to test the discriminant validity. The figures highlight that the figures of HTMT ratio are lower than 0.85. These values have indicated a low correlation among variables and valid discriminant validity (see

Table 5).

4.2. Structural Assessment Model

The smart-PLS have two steps. First, the measurement model, and second, the structural assessment model. The second step was applied here, which checked the relationship between exogenous and endogenous variables. The different types of statistical values are presented by the structural assessment model including effect size (f

2), t values, predictive relevance (Q

2), coefficient of determination (R

2), and path coefficient (β values). The PLS-SEM literature has provided the criteria to evaluate hypotheses and estimate the significance of path coefficients. The 5000 sub-samples were applied for bootstrapping process with a 5% significance level (one-tailed) to test the significance of the hypotheses [

124]. Results indicate that H4 and H7 are not accepted. NPV (β = 0.222, t = 2.331 > 1.64,

p < 0.05), NPV relationship (moderator), (β = 0.202, t = 3.441 > 1.64,

p < 0.05), internal rate of return (β = −0.205, t = 2.552 > 1.64,

p < 0.05), internal rate of return relationship (moderator), (β = 0.090, t = 1.660 > 1.64,

p < 0.05), payback period, (β = 0.232, t = 2.303 > 1.64,

p < 0.05), payback period relationship (moderator) (β = 0.119, t = 1.408 > 1.64,

p < 0.05), profitability index, (β = −0.070, t = 0.639 > 1.64,

p < 0.05), profitability index relationship (moderator) (β = 0.179, t = 2.681 > 1.64,

p < 0.05) have a positive and significant impact on the performance of selected and currently working solar power projects mentioned in

Table 1.

The R

2 value for NPVT → FPSPP is 0.458, indicating that the model has substantial explanatory power for increasing the financial performance of solar power projects. However, the R

2 value is not enough to be considered a suitable and effective method to assist a model [

130]. Consequently, the predictive relevance measurement Q

2 of the model is a suitable method. The value of Q

2 is more sophisticated than zero, which was indicated by the latent exogenous standards with excessive predictive relevance [

128]. The value of Q

2 is 0.245, which shows the model has significant predictive relevance and suggests the financial performance of solar power projects is increasing through CBTs. The f

2 has a typical value, including 0.02, 0.15, and 0.35, which indicate effects in three categories, small, medium, and large, respectively [

129]. Thus, the value of f2 assumed that effect size differs from medium to large (see

Table 6). Several kinds of statistical techniques are mentioned in

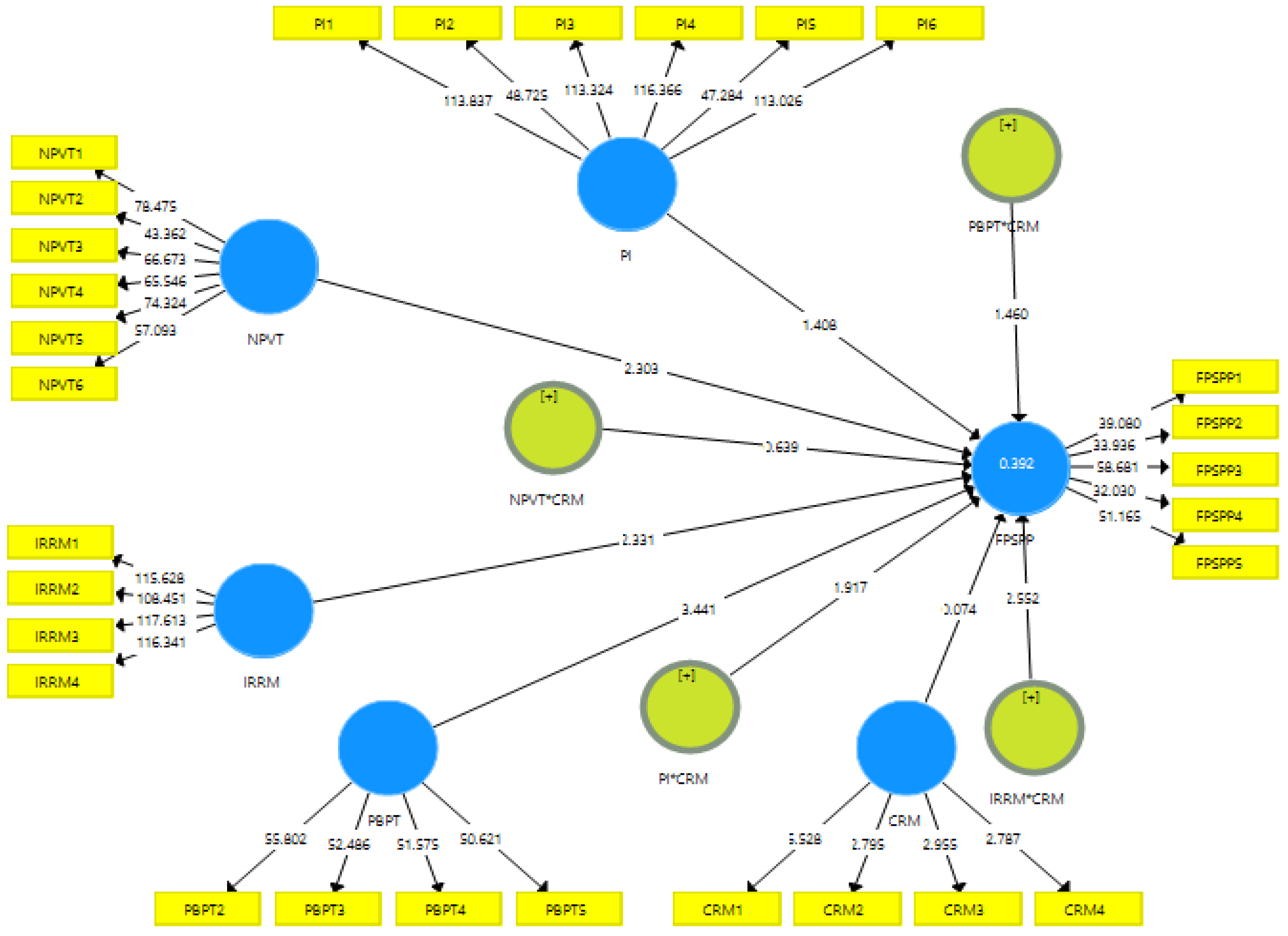

Table 6. The structural assessment model is shown in

Figure 3. The variables show a significant relationship in the model, the t values are more critical than 1.64, and the profitability index not positively impacts financial performance. The values of moderated variables have positive signs and show an entirely substantial relationship in the structural assessment model for solar projects in Pakistan.

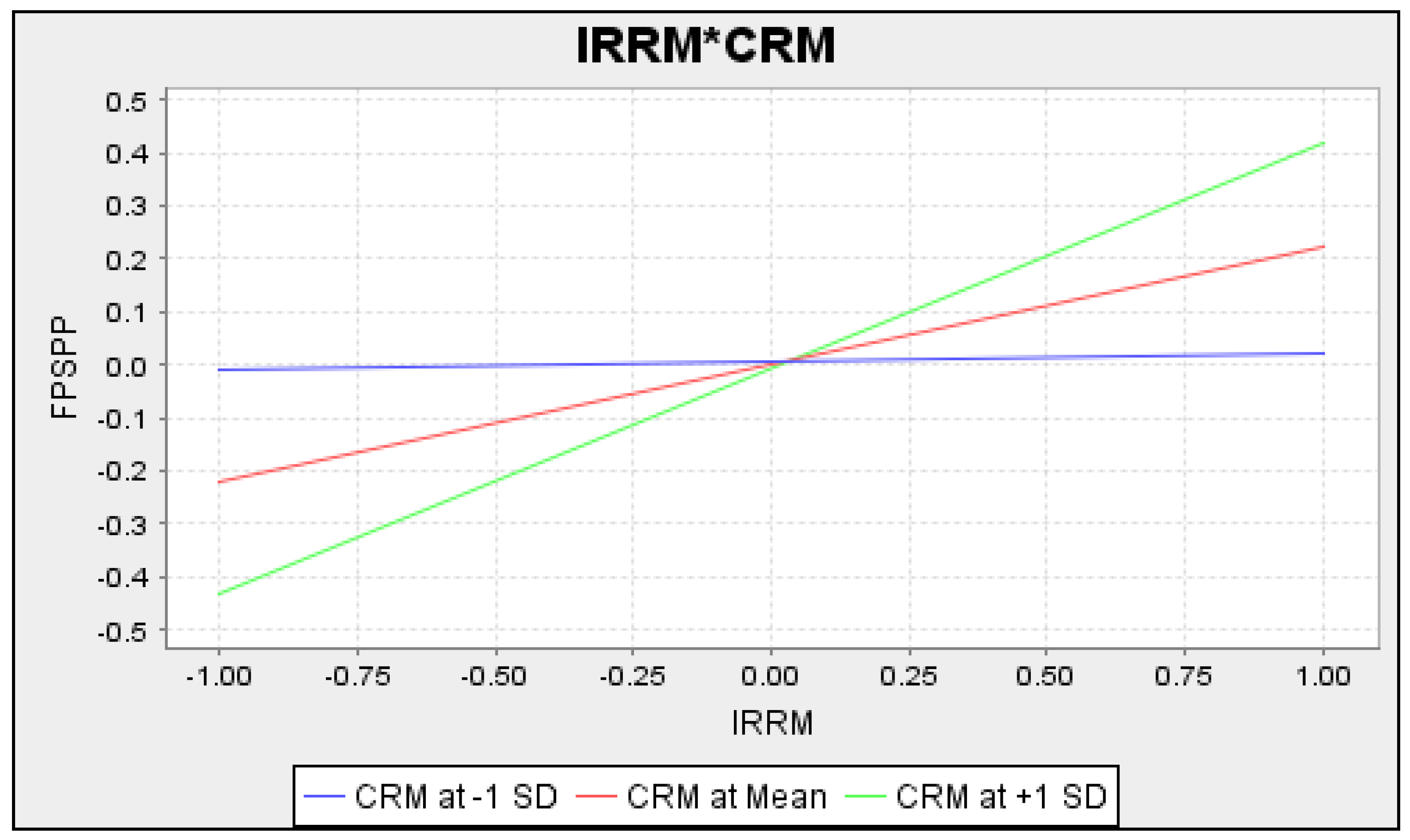

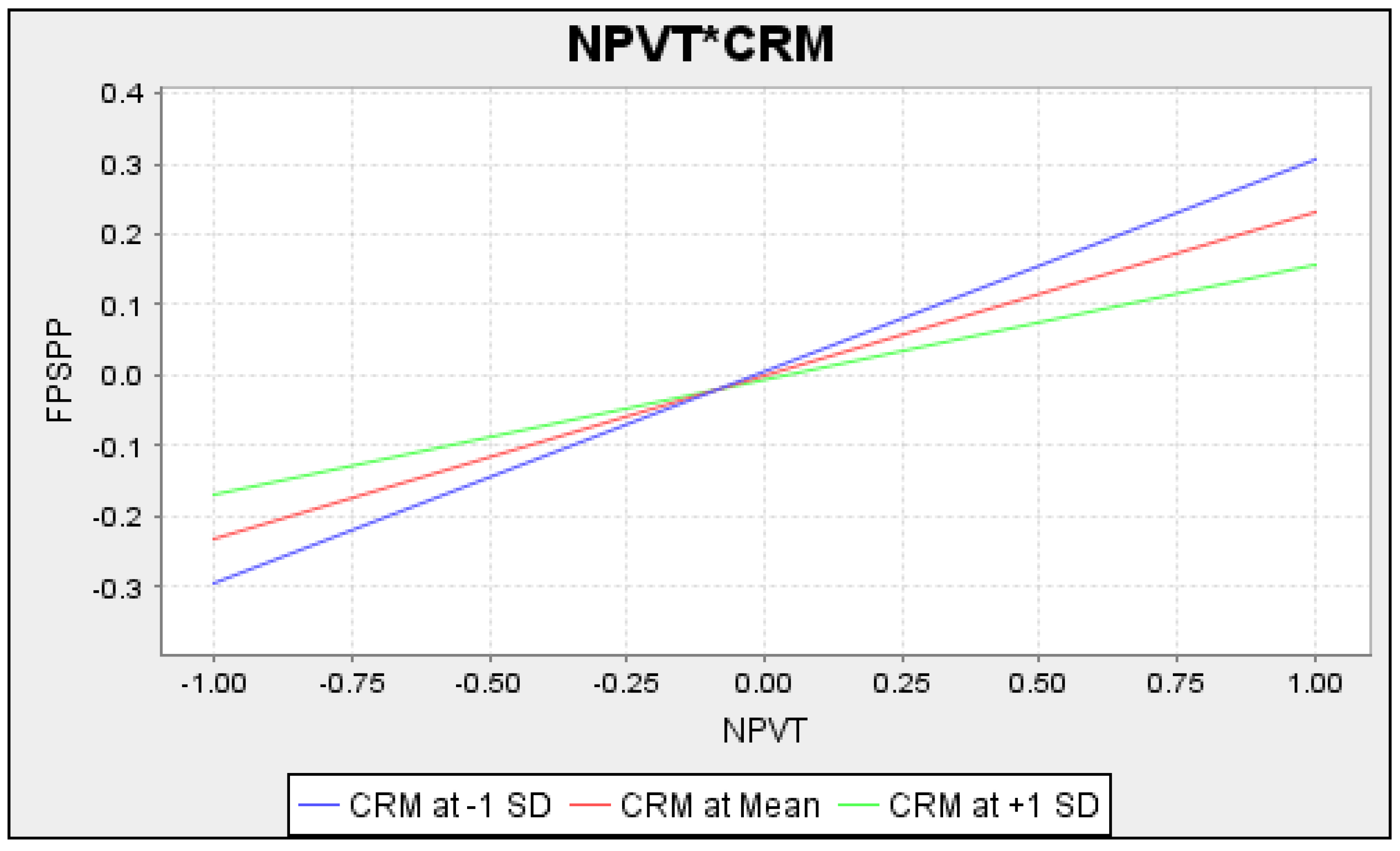

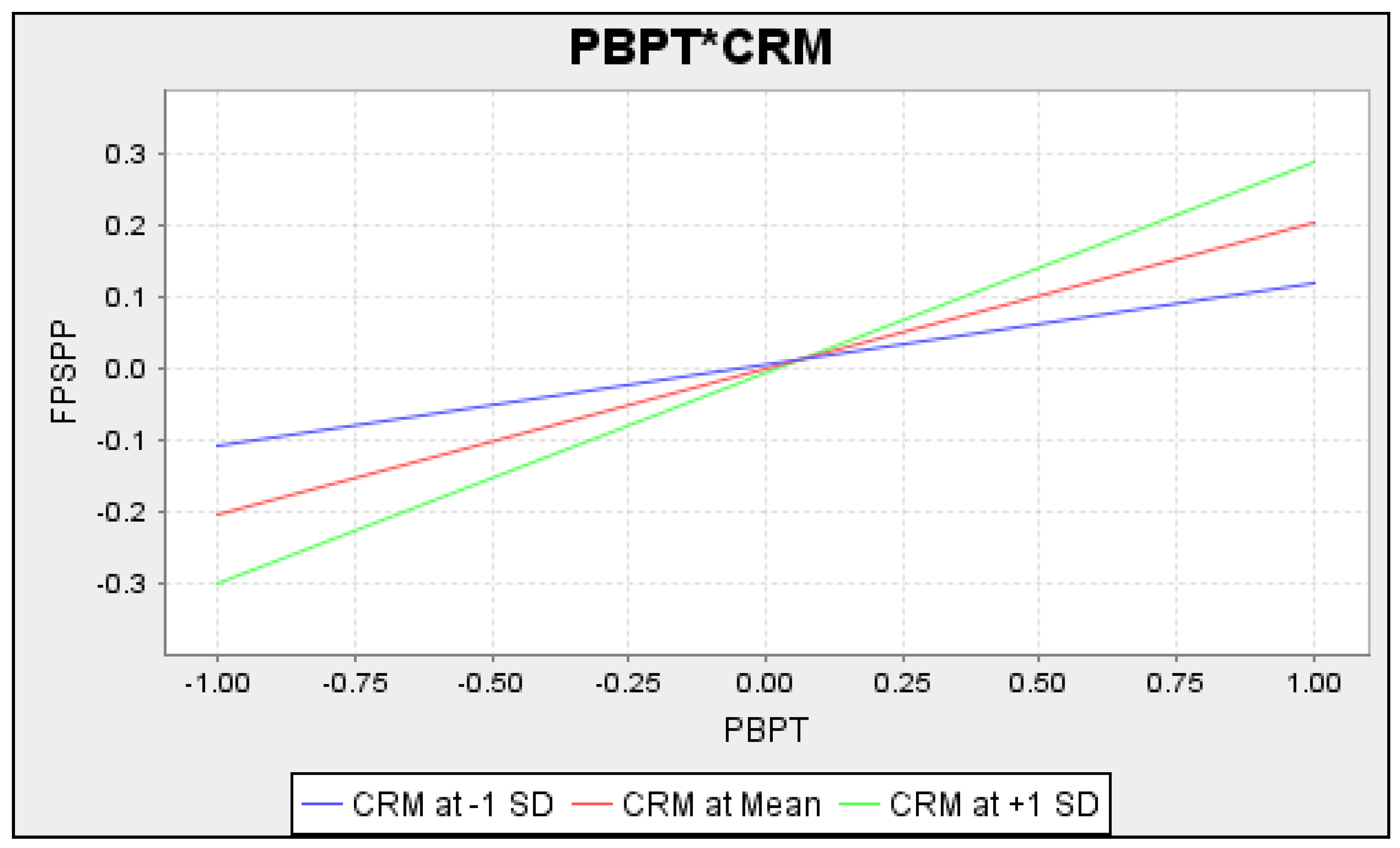

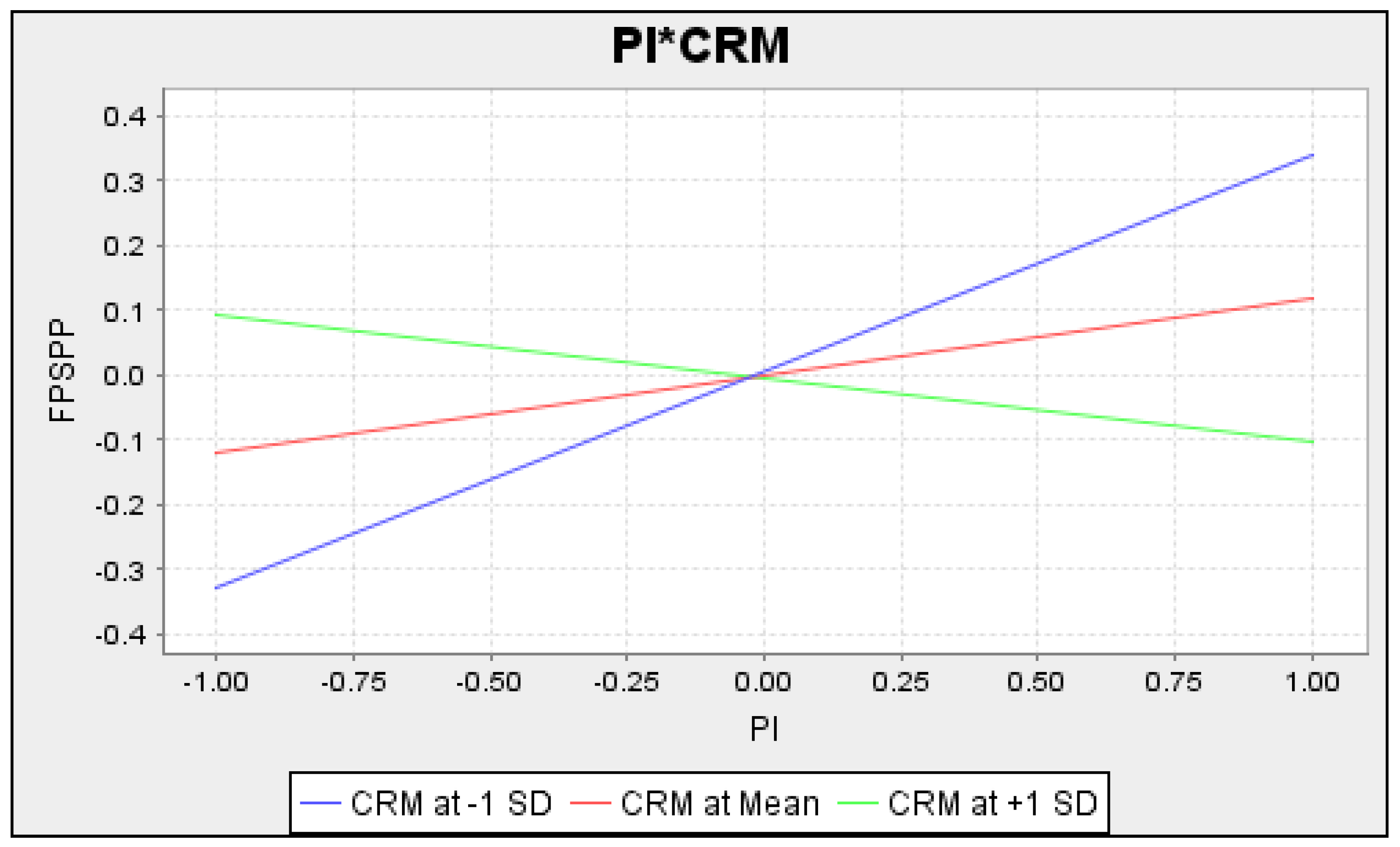

Figure 4 shows the results of moderations. The green line defines the positive or negative relationship among moderated variables of selected solar power projects in this study. After intersecting, if the green line is higher than red and blue, it shows a positive relationship. However,

Figure 4 shows the positive relationships among the moderate variables because the green line is upper than blue and red. In contrast,

Figure 5 shows the negative relationships among the moderate variables because the green line is lower than blue and red.

Figure 6 also shows the positive relationships among the moderate variables because the green line is upper to the blue and red line. Finally,

Figure 7 shows the negative relationships among the moderate variables because the green line is lower than the blue and red line.

5. Discussion and Implications

The study examines how financial planning can be assessed through capital budgeting techniques such as net present value. The results reveal that the NPV technique has a significant and favorable influence on the financial performance of solar power projects. The projects have a high performance when the capital invested is under the NPV technique. These results are in line with the past study of [

131]. In this regard, the research suggests that the NPV technique proves to be beneficial for the currently working solar power projects to attain higher financial performance.

Additionally, the study results have also indicated that the internal rate of return method for assessing financial planning has a positive link with the financial performance of the selected currently working solar power project in Pakistan. These results verify the results of a past study, highlighting the influences of the internal rate of return method on investment in different power projects [

132]. The present study implies that the internal rate of return method helps the management attain higher profitability on investment in different selected and currently working solar power projects. Furthermore, the study results indicate that the payback period method (one of the capital budgeting techniques) positively affects the financial performance of selected and currently working solar power projects. The study also indicates that the payback period technique significantly impacts solar power projects and shows better financial performance if it adopts the selected and currently working solar power projects. These results agree with the study results of [

133], which implies that applying the payback period technique for assessing financial planning while making investment decisions improves the financial performance of solar power projects. This study also aligns with past research that the investment based on periods can recover the investment cost and give a higher financial performance. Therefore, solar power projects have more investment and enjoy better financial performance; thus, there is a minor complication in the acquisition of solar projects in this case [

134]. Consequently, investment is increasing, and the financial performance of the solar power projects is growing.

The study makes both theoretical and empirical implications. This literary work is significant as it contributes to economic literature. The study deals with the influence of four factors: the NPV technique, MIRR, PBP technique, and PI to enhance the performance of selected and currently working solar power projects in the country. This study adds in literature to introduce capital budgeting techniques to minimize the cost and risk in solar power projects. The present study has provided the guidelines to the top management of the private and government sector in renewable energy to adopt capital budgeting techniques for better financial planning to enhance the performance of solar power projects. The study carries great importance to the economists of an emerging economy such as Pakistan because the guidance of this study improves the performance of selected and currently working solar power projects. The best financial planning can reduce the cost and risk of solar projects and enhance the financial performance of solar power projects. Hence, capital budgeting techniques can improve the financial position of the solar power projects if appropriate financial planning is adopted in the projects.

The results indicate that the profitability index has a positive relationship with the financial performance of the selected and currently working solar power projects. The improvement in the profitability index of the investment in particular solar power projects brings higher investment in such projects and drives higher financial performance. The previous study has approved these results [

135]. The capital budgeting technique, such as the profitability index, helps to make an investment considering the attainment of higher profitability on the investment in the future. The paper concludes that investment under the profitability index raises the performance level of solar power projects. The study results further reveal that the cost and riskiness of the capital budgeting method is not a perfect moderator between the NPV technique and the financial performance of the selected and currently working solar power project. The study suggests that the cost and riskiness of the NPV technique affect the financial performance of the selected and currently working solar power projects. These results comply with the study of [

132], indicating that the cost and riskiness of the method affect both the NPV technique and the financial performance of the solar power projects and their mutual association. The study results have also indicated that the cost and riskiness of the method is a considerable moderator between the internal rate of return method and the financial performance of the selected and currently working solar power projects in the country. These results align with the past study of [

76], which indicates that the cost and riskiness of the capital budgeting method, such as the internal rate of return method, affect the effectiveness of this method and the performance of solar power projects.

The study suggested that the NPV technique proves to be beneficial for selected and currently working solar power projects to attain higher financial performance. The internal rate of return method attains higher profitability, and assessing financial planning has positively linked the financial performance in selected and currently working solar power projects in Pakistan. The study results have indicated that the payback period method positively correlates with the financial performance of selected and currently working solar power projects. The profitability index is an effective technique that helps assess the investment’s profitability over different periods and allows the investors to make increased profits on the investment. The study analysis proves that the profitability index is a good source of the higher financial performance and payout of the selected and currently working solar power projects in Pakistan. The findings provide appreciated guidelines for the ministry of water and power, policymakers, government institutions, regulators, and top management of the alternative energy development board (AEDB) to adopt these capital budgeting techniques for selected and currently working solar power projects in the country. The competent authorities should consider NPV, PBP, IRR, and PI to reduce the cost and risk and enhance the performance of selected and currently working solar power projects in Pakistan.

These results also align with the past study, highlighting the cost occurrence and the riskiness involved in the internal rate of return. Still, this budgeting method improves the capital budgeting technique’s contribution to attaining the higher performance of solar power projects [

78]. Our results have shown that the cost and riskiness of the method have not played a moderating role between the payback period technique and the performance of the solar power projects. These results are in line with the previous study of [

131]. The study analyzes the influences of cost and riskiness on the effectiveness of the payback period method in power projects. It shows that the cost and riskiness of the technique prove to be a perfect moderator between the payback period method and the performance of the selected and currently working solar power projects in Pakistan. Furthermore, the results have revealed that the cost and riskiness of the process play a moderating role between the capital budgeting technique such as profitability index and the performance of selected and currently working solar power projects in the country. These results agree with the results of [

136], which show that the cost and riskiness of the method affect both the profitability index and the performance of solar power projects. Thus, the financial performance is also affected by selected and currently working solar power projects in Pakistan.

6. Conclusions and Limitations

The present study examined capital budgeting techniques for assessing financial planning and attaining the higher financial performance of selected and currently working solar power projects in Pakistan. In this regard, we scrutinized four capital budgeting techniques, such as the NPV technique, MIRR, PBP technique, and PI, concerning the financial performance of the selected and currently working solar power projects in this study. The NVP of the capital budgeting technique analyzed the cash inflows and outflows; it helps make profitable investments in different projects. Under this capital budgeting method, the level of investment in solar power projects is rising, raising their performance level.

The assessment of the period that an entity takes to cover the investment cost is a simple capital budgeting technique because the lack of complications obtains popularity among the investors and raises the financial sources and financial performance of solar power projects. Similarly, the profitability index is one of the effective capital budgeting techniques that help to assess the investment’s profitability over different periods. It allows the investors to make a good choice, resulting in increased profits on the investment. The study analyzed that the profitability index is a good source of the higher financial performance of the selected and currently working solar power projects in Pakistan. Besides, the study examined the cost and risks by adopting particular capital budgeting techniques, including the NPV technique, MIRR, PBP technique, and PI, concerning the selected and currently working solar power projects. As a result, the influence and effectiveness of the NPV technique attained the higher financial performance of the selected and currently working solar power projects in Pakistan.

Thus, the study shows that these capital budgeting techniques positively correlate with capital investment, return on capital, and cost and risk for sustainable development of the selected and currently working solar energy projects in Pakistan. The study also examined that these techniques are the best way to assess capital investment, return on investment, and capital investment before investing in a solar energy project in Pakistan. The present study has proved that capital budgeting techniques are more significant and better for green technology, return on capital, financial management, to assess cost and riskiness, and capital cost investing in selected and currently working solar energy projects in Pakistan. The R

2 value shown in

Table 6 for NPV is 0.458, which indicates that the model has substantial explanatory power for increasing the financial performance of selected and currently working solar power projects in Pakistan. The value of Q

2 is 0.245, which shows that the model has significant predictive relevance and suggests that the financial performance of selected and currently working solar power projects is increasing through CBTs. The variables show a meaningful relationship of a PBP of l in the model; the t values are more critical than (1.64), and the profitability index positively impacts financial performance. The importance of moderated variables has positive signs and shows an entirely substantial relationship in the structural assessment model for selected and currently working solar projects in Pakistan. The study has also disclosed that these techniques and their moderation adopted in this research have a positive and significant impact on the performance of selected solar energy projects in Pakistan.

Similarly, the study prompts introducing the cost and riskiness of the method as a moderator between the capital as mentioned-above budgeting techniques and the financial performance of the selected and currently working solar power projects. The study also proves which techniques are more profitable in different circumstances and improves the financial performance for sustainable development of selected and currently working solar power projects. Despite its theoretical and empirical implication, the current study has several limitations that future authors should recover. First, the study has analyzed the influences of four capital budgeting techniques such as the NPV technique, MIRR, PBP technique, and PI on the financial performance of selected and currently working solar power projects in Pakistan. At the same time, the other capital budgeting techniques, such as discounted payback period, modified internal rate of return, etc., and other economic factors affecting the financial performance of solar power projects have been completely neglected. Therefore, the authors in the future must also analyze the rest of the capital budgeting techniques and economic factors while replicating these study results.

Similarly, the study has kept the financial performance of selected and currently working solar power projects launched in Pakistan, a developing economy. Thus, the research is not equally valid in both developing and developed countries. Therefore, future authors must analyze the influences of capital budgeting techniques on the financial performance of solar power projects in developed economies.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}