Ammonia Production from Clean Hydrogen and the Implications for Global Natural Gas Demand

, , , and

, , , and

Abstract

:1. Introduction

1.1. The Global Natural Gas Market Context and Prospects in the Energy Transition

1.2. The Importance of Natural Gas for Global Ammonia Production

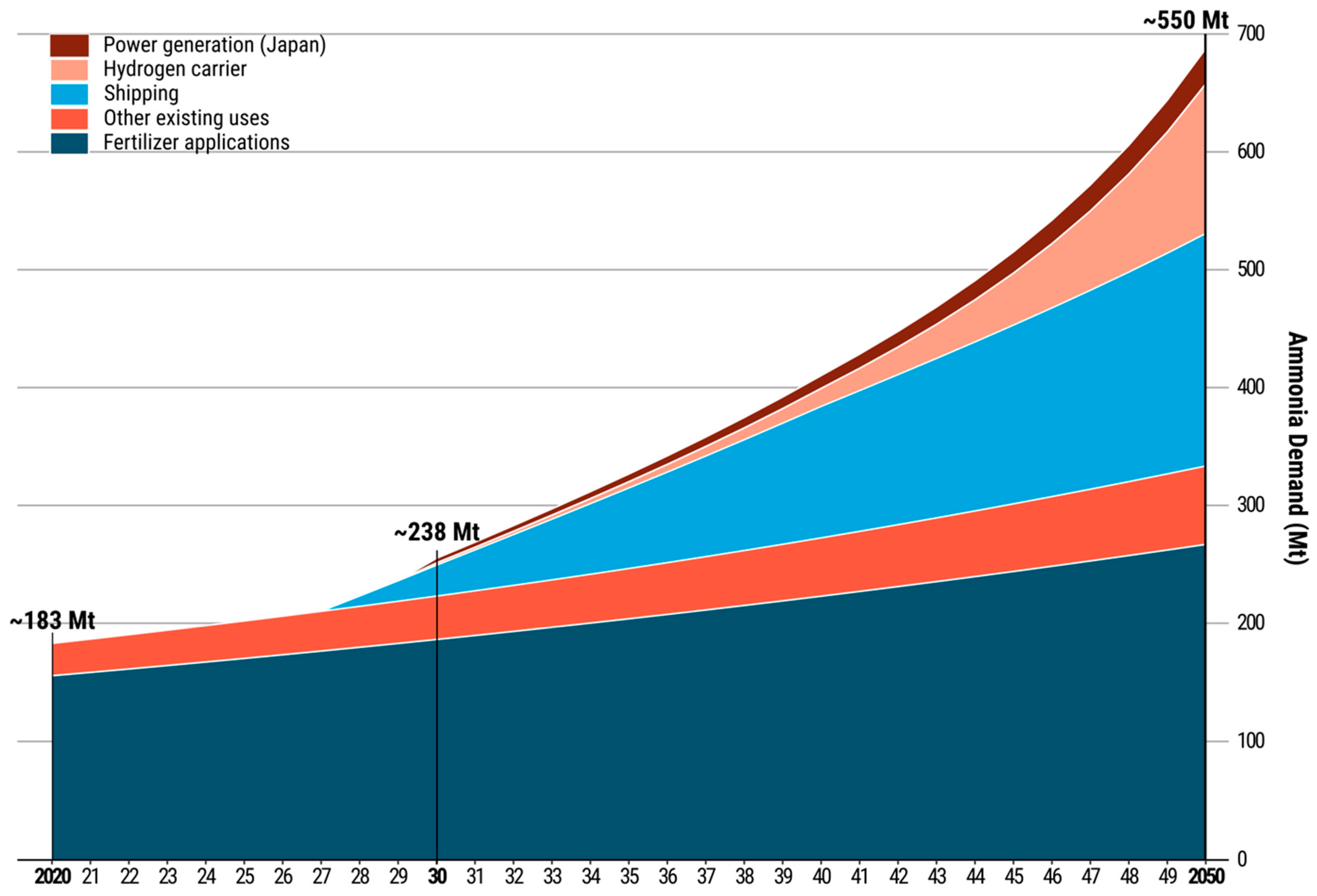

1.3. The Role of Ammonia in the Emerging Hydrogen Economy

1.4. Scope and Objective of This Paper

2. Latest Trends in the Global Ammonia Sector

3. Technical, Economic and Greenhouse Gas Emission Estimates of Ammonia Production Pathways

3.1. Energy Use and Greenhouse Gas Emissions of Ammonia Production

3.2. Production Costs of Ammonia

4. Discussion of System Implications and Technical Constraints in Utilizing Green Ammonia

4.1. Interactions with the Power System

4.2. Ammonia Production Aspects

- About 2% of the total electricity input is consumed at the inverter control system (0.072 MJ)

- Compression of hydrogen requires 4.32 MJ/kg hydrogen (0.085 MJ to compress 0.0197 kg hydrogen) [107]

- Nitrogen production (0.091 kg nitrogen is required for the equivalent amount of hydrogen compressed) requires 265 kWh/kg nitrogen electricity (0.087 MJ)

- Ammonia synthesis requires 600 kWh/t ammonia (0.238 MJ)

- Transport of ammonia over a 3000 km distance requires 0.936 MJ/kg ammonia (0.103 MJ)

- Cracking and purification steps require 0.4 kWh/kg ammonia (0.159 MJ) [107]

5. Discussion of Prospects for Green Ammonia Trade and Required Policies

5.1. Prospects for International Trade

5.2. Required Policies and Enabling Conditions

5.3. Climate and Environment

5.4. Innovation Policies

5.5. Regulations for Market Creation and Growth and Financing

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

| Unit | Assumed Value | References | |

| Hydrogen production | |||

| CAPEX: SMR | USD/kW | 910 | [124,125,126] |

| CAPEX: Electrolyzer | USD/kW | 750 | [127] |

| CAPEX: CCS | USD/t CO2/year | 300 | [69] |

| CAPEX: Onshore wind | USD/kW | 1150–3000 | [128,129] |

| CAPEX: Offshore wind | USD/kW | 2300–6300 | |

| CAPEX: Solar PV | USD/kW | 600–1750 | |

| CAPEX: Gas boiler | USD/kW | 500 | [130] |

| OPEX: SMR | % of CAPEX | 4.7 | [124,125] |

| OPEX: Electrolyzer | % of CAPEX | 2.5 | [127] |

| OPEX: CCS | % of CAPEX | 7 | [69] |

| OPEX: Renewable power | % of CAPEX | 2.5 | [128,129] |

| Gas boiler OPEX | % of CAPEX | 3 | [130] |

| Capacity factor: SMR | % | 90 | [124,125] |

| Capacity factor: Electrolyzer | % | 50 | [127] |

| Capacity factor: CCS | % | 90 | [69] |

| Capacity factor: Onshore wind | % | 28–38 | [128,129,130,131] |

| Capacity factor: Offshore wind | % | 38–57 | |

| Capacity factor: Solar PV | % | 12–23 | |

| Capacity factor: Gas boiler | % | 90 | [132] |

| SMR gas input | GJ/t H2 | [133] | |

| Feedstock | 140.7 | ||

| Fuel | 15.4 | ||

| SMR steam | GJ/t H2 | ||

| Import | 25.9 | ||

| Export | 37.2 | ||

| SMR electricity | GJ/t H2 | 1.14 | |

| Electrolyzer efficiency | % | 65 | [127] |

| Electrolyzer water demand | l/kg H2 | 15 | |

| CCS steam | GJ/t CO2 captured | 2.5 | [69] |

| CCS electricity | GJ/t CO2 captured | 0.4 | [69] |

| CCS capture rate | % | 90 | [69] |

| Gas-fired power plant efficiency | % | 30–90 | Assumption |

| Gas boiler efficiency | % | 90 | Assumption |

| Emission factor of natural gas | tons CO2/GJ | 0.056 | |

| Emission factor of grid electricity | g CO2/kWh | 0–1050 | Estimated based on data from [1] |

| Average methane emissions from natural gas | t CO2-eq/GJ | 0.015 | Estimated based on data from [1,22,63,71,82] |

| GHG emission reduction potential of methane abatement measures | % | Up to 16% | Estimated based on data from [1,71] |

| Nitrogen production | |||

| CAPEX: cryogenic air separation | USD/t N2/h | 1,500,000 | [56] |

| OPEX: cryogenic air separation | % of CAPEX | 2 | |

| Electricity | kWh/t N2 | 265 | [134] |

| Capacity factor | % | 90 | Assumption |

| Ammonia synthesis | |||

| CAPEX: ammonia synthesis | USD/t NH3/h | 3,450,000 | [17] |

| OPEX: ammonia synthesis | % of CAPEX | 2 | |

| Electricity for synthesis | kWh/kg NH3 | 0.65 | [16,57] |

| Utility prices | |||

| Natural gas price | USD/GJ | 1–10 | Assumption |

| Grid electricity | USD/kWh | 0.014–0.108 | Assumption |

| LCOE onshore wind | USD/kWh | 0.037–0.228 | Estimated based on above parameters |

| LCOE offshore wind | USD/kWh | 0.052–0.215 | |

| LCOE Solar PV | USD/kWh | 0.038–0.142 | |

| Water price | USD/L | 0.001 | Assumption |

| Annuity factor | |||

| Long-term interest rate (2019–2021) | % | −0.5–10 | [135] |

| Country credit ratings (August 2022) | - | - | [136] |

| Discount rate | % | 5–22 | Estimate |

| Economic lifetime of equipment | Years | 25 | Assumption |

References

- OECD/IEA. World Energy Balances Overview; International Energy Agency: Paris, France, 2021. [Google Scholar]

- IRENA. World Energy Transitions Outlook: 1.5 °C Pathway; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2022. [Google Scholar]

- OECD/IEA. World Energy Outlook 2021; International Energy Agency: Paris, France, 2021. [Google Scholar]

- Riahi, K.; Schaeffer, R.; Arango, J.; Calvin, K.; Guivarch, C.; Hasegawa, T.; Jiang, K.; Kriegler, E.; Matthews, R.; Peters, G.; et al. Mitigation Pathways Compatible with Long-Term Goals. In Climate Change 2022: Mitigation of Climate Change; Shukla, P., Skea, J., Slade, R., Khourdajie, A.A., Diemen, R., McCollum, D., Pathak, M., Some, S., Vyas, P., Fradera, R., et al., Eds.; Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2022. [Google Scholar]

- OECD/IEA. Ammonia Technology Roadmap; International Energy Agency: Paris, France, 2021. [Google Scholar]

- USGS. Nitrogen Statistics and Information. 2022. Available online: https://www.usgs.gov/centers/national-minerals-information-center/nitrogen-statistics-and-information (accessed on 29 November 2022).

- Dempsey, H.; Ivanova, P. European Gas Prices Soar after Russia Deepens Supply Cuts; Financial Times: London, UK, 2022. [Google Scholar]

- OECD. Why Governments should Target Support Amidst High Energy Prices. Available online: https://www.oecd.org/ukraine-hub/policy-responses/why-governments-should-target-support-amidst-high-energy-prices-40f44f78/ (accessed on 30 June 2022).

- OECD/IEA. Gas Market Report, Q3-2022; International Energy Agency: Paris, France, 2022. [Google Scholar]

- Lawson, C. Europe Nitrogen Capacity Closure and Cost Tracker. Available online: https://www.crugroup.com/knowledge-and-insights/insights/2022/europe-nitrogen-capacity-closure-and-cost-tracker (accessed on 25 August 2022).

- IAMM. Why are Ammonia Prices so High in 2022? Available online: https://www.iamm.green/ammonia-prices/ (accessed on 26 June 2022).

- The World Bank. World Bank Commodities Price Data (The Pink Sheet). Available online: https://thedocs.worldbank.org/en/doc/5d903e848db1d1b83e0ec8f744e55570-0350012021/related/CMO-Pink-Sheet-September-2022.pdf (accessed on 2 September 2022).

- Gielen, D.; Bazilian, M.D. Critically exploring the future of gaseous energy carriers. Energy Res. Soc. Sci. 2021, 79, 102185. [Google Scholar] [CrossRef]

- IRENA. Innovation Outlook: Renewable Ammonia; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2022. [Google Scholar]

- EU. Assessment of Hydrogen Delivery Options; European Union: Brussels, Belgium, 2021. [Google Scholar]

- Fasihi, M.; Weiss, R.; Savolainen, J.; Breyer, C. Global potential of green ammonia based on hybrid PV-wind power plants. Appl. Energy 2021, 294, 116170. [Google Scholar] [CrossRef]

- Armijo, J.; Philibert, C. Flexible production of green hydrogen and ammonia from variable solar and wind energy: Case study of Chile and Argentina. Int. J. Hydrog. Energy 2020, 45, 1541–1558. [Google Scholar] [CrossRef]

- Guerra, C.F.; Reyes-Bozo, L.; Vyhmeister, E.; Caparros, M.J.; Salazar, J.; Clemente-Jul, C. Technical-economic analysis for a green ammonia production plant in Chile and its subsequent transport to Japan. Renew. Energy 2020, 157, 404–414. [Google Scholar] [CrossRef]

- Salmon, N.; Bañares-Alcántara, R. Green ammonia as a spatial energy vector: A review. Sustain. Energy Fuels 2021, 5, 2814–2839. [Google Scholar] [CrossRef]

- Howarth, R.W.; Jacobson, M.Z. How green is blue hydrogen? Energy Sci. Eng. 2021, 9, 1676–1687. [Google Scholar] [CrossRef]

- Forster, P.; Storelvmo, T.; Armour, K.; Collins, W.; Dufresne, J.-L.; Frame, D.; Lunt, D.; Mauritsen, T.; Palmer, M.; Watanabe, M.; et al. 2021: The Earth’s Energy Budget, Climate Feedbacks, and Climate Sensitivity. In Climate Change 2021: The Physical Science Basis; Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change, Cambridge and New York; Cambridge University Press: Cambridge, UK, 2021; pp. 923–1054. [Google Scholar]

- OECD/IEA. Methane Emissions from Oil and Gas; International Energy Agency: Paris, France, 2021. [Google Scholar]

- Al-Aboosi, F.Y.; El-Halwagi, M.M.; Moore, M.; Nielsen, R.B. Renewable ammonia as an alternative fuel for the shipping industry. Curr. Opin. Chem. Eng. 2021, 31, 100670. [Google Scholar] [CrossRef]

- Allman, A.; Daoutidis, P.; Tiffany, D.; Kelley, S. A framework for ammonia supply chain optimization incorporating conventional and renewable generation. Process Syst. Eng. 2017, 63, 4390–4402. [Google Scholar] [CrossRef]

- Salmon, N.; Banares-Alcantara, R.; Nayak-Luke, R. Optimization of green ammonia distribution systems for intercontinental energy transport. iScience 2021, 24, 102903. [Google Scholar] [CrossRef]

- Zhao, H.; Kamp, L.M.; Lukszo, Z. The potential of green ammonia production to reduce renewable power curtailment and encourage the energy transition in China. Int. J. Hydrog. Energy 2022, 47, 18935–18954. [Google Scholar] [CrossRef]

- Sagel, V.N.; Rouwenhorst, K.H.R.; Faria, J.A. Renewable Electricity Generation in Small Island Developing States: The Effect of Importing Ammonia. Energies 2022, 15, 3374. [Google Scholar] [CrossRef]

- Saygin, D.; Gielen, D. Zero-Emission Pathway for the Global Chemical and Petrochemical Sector. Energies 2021, 14, 3772. [Google Scholar] [CrossRef]

- Patonia, A.; Poudineh, R. Global Trade of Hydrogen: What is the Best Way to Transfer Hydrogen over Long Distances? Oxford Institute for Energy Studies: Oxford, UK, 2022. [Google Scholar]

- MPP. Making Net-Zero Ammonia Possible: An Industry-Backed, 1.5oC-Aligned Transition Strategy; Mission Possible Partnership, 2022. [Google Scholar]

- OECD/IEA. Net Zero by 2050; International Energy Agency: Paris, France, 2021. [Google Scholar]

- Pekic, S. QatarEnergy to Build ‘World’s Largest Blue Ammonia Facility. 2022. Available online: https://www.offshore-energy.biz/qatarenergy-to-build-worlds-largest-blue-ammonia-facility/ (accessed on 18 January 2022).

- Rouwenhorst, K.H.; Travis, A.S.; Lefferts, L. 1921–2021: A Century of Renewable Ammonia Synthesis. Sustain. Chem. 2022, 3, 149–171. [Google Scholar] [CrossRef]

- IRENA. Global Hydrogen Trade to Meet the 1.5 °C Climate Goal: Part I—Trade Outlook for 2050 and Way Forward; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2022. [Google Scholar]

- Argus Media. Ammonia Market Update and CFR NW Ammonia Swaps—A New Risk Management Tool; Argus Media: London, UK, 2022. [Google Scholar]

- Thomas, W. Fertilizer Industry Takes Leap of Faith on Green Ammonia. Available online: https://www.crugroup.com/knowledge-and-insights/insights/2021/fertilizer-industry-takes-leap-of-faith-on-green-ammonia/ (accessed on 25 June 2021).

- Rai-Roche, S. ‘World’s Largest Green Ammonia Plant’ Planned for South Africa, Set to go Live in 2025. 2022. Available online: https://www.pv-tech.org/worlds-largest-green-ammonia-plant-planned-for-south-africa-set-to-go-live-in-2025/ (accessed on 18 January 2022).

- Atchison, J. Total: Renewable Ammonia Production in Egypt. 2022. Available online: https://www.ammoniaenergy.org/articles/total-renewable-ammonia-production-in-egypt/ (accessed on 26 May 2022).

- Construction Review Online. US$ 10.69bn Committed to Hydrogen & Green Ammonia Production Project in Guelmim-Oued Noun, Morocco. 2022. Available online: https://constructionreviewonline.com/news/us-10-69bn-committed-to-hydrogen-green-ammonia-production-project-in-guelmim-oued-noun-morocco/ (accessed on 29 January 2022).

- Atchison, J. Scatec Joins ACME’s Oman Green Ammonia Project. 2022. Available online: https://www.ammoniaenergy.org/articles/scatec-joins-acmes-oman-green-ammonia-project/ (accessed on 8 March 2022).

- IRENA. Global Hydrogen Trade to Meet the 1.5 °C Climate Goal: Part II—Technology Review of Hydrogen Carriers; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2022. [Google Scholar]

- Hatfield, O. Country Traded Ammonia Logistics and Storage, Present and Future. In Proceedings of the Ammonia Energy Conference 2021, Boston, MA, USA, 9–11 November 2021. [Google Scholar]

- Ghavam, S.; Vahdati, M.; Wilson, I.G.; Styring, P. Sustainable Ammonia Production Processes. Front. Energy Res. 2021, 9, 580808. [Google Scholar] [CrossRef]

- Wu, S.; Salmon, N.; Li, M.M.-J.; Banares-Alcantara, R.; Tsang, S.C.E. Energy decarbonization via green H2 or NH3? ACS Energy Lett. 2022, 7, 1021–1033. [Google Scholar] [CrossRef]

- NYK. Demonstration Project Begins for Commercialization of Vessels Equipped with Domestically Produced Ammonia-Fueled Engine. Available online: https://www.nyk.com/english/news/2021/20211026_03.html (accessed on 26 October 2021).

- IRENA. A Pathway to Decarbonize the Shipping Sector by 2050; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2021. [Google Scholar]

- IMO. Initial Imo Strategy on Reduction of GHG Emissions from Ships. Available online: https://wwwcdn.imo.org/localresources/en/OurWork/Environment/Documents/Resolution%20MEPC.304%2872%29_E.pdf (accessed on 13 April 2018).

- Kilemo, H.; Montgomery, R.; Leitão, A.M. Mapping of Zero Emission Pilots and Demonstration Projects; Getting to Zero Coalition: Copenhagen, Denmark, 2022. [Google Scholar]

- Lloyd’s List. Ammonia Retrofits for LNG-Fuelled Ships to Pick Up in 2030s. Available online: https://lloydslist.maritimeintelligence.informa.com/LL1135669/Ammonia-retrofits-for-LNG-fuelled-ships-to-pick-up-in-2030s (accessed on 4 February 2021).

- Mallouppas, G.; Ioannou, C.; Yfantis, E.A. A Review of the Latest Trends in the Use of Green Ammonia as an Energy Carrier in Maritime Industry. Energies 2022, 15, 1453. [Google Scholar] [CrossRef]

- Baresic, D. Ammonia as A Ship Fuel: Transition Pathways. In Proceedings of the Ammonia Energy Conference, Orlando, FL, USA, 12–14 November 2019. [Google Scholar]

- Atchison, J. JERA Targets 50% Ammonia-Coal Co-Firing by 2030. Ammonia Energy Association. Available online: https://www.ammoniaenergy.org/articles/jera-targets-50-ammonia-coal-co-firing-by-2030/ (accessed on 21 January 2022).

- METI. Transition Roadmap for Power Sector; Ministry of Economy, Trade and Industry: Tokyo, Japan, 2022.

- Brown, T. Japan’s Road Map for Fuel Ammonia. Available online: https://www.ammoniaenergy.org/articles/japans-road-map-for-fuel-ammonia/ (accessed on 25 February 2021).

- Atchison, J. South Korea Sets Targets for Hydrogen & Ammonia Power Generation. Available online: https://www.ammoniaenergy.org/articles/south-korea-sets-targets-for-hydrogen-ammonia-power-generation/ (accessed on 24 November 2021).

- Ikäheimo, J.; Kiviluoma, J.; Weiss, R.; Holttinen, H. Power-to-ammonia in future North European 100 % renewable power and heat system. Int. J. Hydrog. Energy 2018, 43, 17295–17308. [Google Scholar] [CrossRef]

- Nayak-Luke, R.; Bañares-Alcántara, R.; Wilkinson, I. “Green” Ammonia: Impact of Renewable Energy Intermittency on Plant Sizing and Levelized Cost of Ammonia. Ind. Eng. Chem. Res. 2018, 57, 14607–14616. [Google Scholar] [CrossRef] [Green Version]

- Rivarolo, M.; Riveros-Godoy, G.; Magistri, L.; Massardo, A.F. Clean Hydrogen and Ammonia Synthesis in Paraguay from the Itaipu 14 GW Hydroelectric Plant. ChemEngineering 2019, 3, 87. [Google Scholar] [CrossRef] [Green Version]

- Gomez, J.R.; Baca, J.; Garzon, F. Techno-economic analysis and life cycle assessment for electrochemical ammonia production using proton conducting membrane. Int. J. Hydrog. Energy 2020, 45, 721–737. [Google Scholar] [CrossRef]

- Bicer, Y.; Dincer, I.; Zamfirescu, C.; Vezina, G.; Raso, F. Comparative life cycle assessment of various ammonia production methods. J. Clean. Prod. 2016, 135, 1379–1395. [Google Scholar] [CrossRef]

- Singh, V.; Dincer, I.; Rosen, M.A. Life Cycle Assessment of Ammonia Production Methods. In Exergetic, Energetic and Environmental Dimensions, London, Ed.; Academic Press: New York, NY, USA, 2018; pp. 935–959. [Google Scholar]

- Liu, X.; Elgowainy, A.; Wang, M. Life cycle energy use and greenhouse gas emissions of ammonia production from renewable resources and industrial by-products. Green Chem. 2022, 22, 5751–5761. [Google Scholar] [CrossRef]

- OECD/IEA. The Oil and Gas Industry in Energy Transitions; International Energy Agency: Paris, France, 2020. [Google Scholar]

- Government of Alberta. Quest CO2 Capture Ratio Performance; Government of Alberta: Edmonton, AB, Canada, 2020. [Google Scholar]

- Bauer, C.; Treyer, K.; Antonini, C.; Bergerson, J.; Gazzani, M.; Gencer, E.; Gibbins, J.; Mazzotti, M.; McCoy, S.T.; McKenna, R.; et al. On the climate impacts of blue hydrogen production. Sustain. Energy Fuels 2022, 6, 66–75. [Google Scholar] [CrossRef]

- Dong, Z.Y.; Yang, J.; Yu, L.; Daiyan, R.; Amal, R. A green hydrogen credit framework for international green hydrogen trading towards a carbon neutral future. Int. J. Hydrog. Energy 2022, 47, 728–734. [Google Scholar] [CrossRef]

- Noussan, M.; Raimondi, P.P.; Scita, R.; Hafner, M. The Role of Green and Blue Hydrogen in the Energy Transition—A Technological and Geopolitical Perspective. Energies 2021, 13, 298. [Google Scholar] [CrossRef]

- Timmerberg, S.; Kaltschmitt, M.; Finkbeiner, M. Hydrogen and hydrogen-derived fuels through methane decomposition of natural gas—GHG emissions and costs. Energy Convers. Manag. 2020, 7, 100043. [Google Scholar] [CrossRef]

- Saygin, D.; Broek, M.; Ramirez, A.; Patel, M.K.; Worrell, E. Modelling the future CO2 abatement potentials of energy efficiency and CCS: The case of the Dutch industry. Int. J. Greenh. Gas Control. 2013, 18, 23–37. [Google Scholar] [CrossRef] [Green Version]

- OECD/IEA. Curtailing Methane Emissions from Fossil Fuel Operations—Pathways to a 75% cut by 2030; International Energy Agency: Paris, France, 2021. [Google Scholar]

- OECD/IEA. Methane Tracker 2020; International Energy Agency: Paris, France, 2020. [Google Scholar]

- IEAGHG. Reference Data and Supporting Literature Reviews for SMR Based Hydrogen Production with CCS.; IEA Greenhouse Gas R&D Programme: Cheltenham, UK, 2017. [Google Scholar]

- KBR. KBR Purifier™/PurifierPlus™ Process: A Superior Technology for Blue Ammonia Production; KBR: Houston, TX, USA, 2022. [Google Scholar]

- Liu, N. Increasing Blue Hydrogen Production Affordability; Hydrocarbon Processing: Houston, TX, USA, 2021. [Google Scholar]

- Hydrogen Council. Hydrogen Council. Hydrogen Decarbonization Pathways. In A Life-Cycle Assessment; Hydrogen Council: Brussels, Belgium, 2021. [Google Scholar]

- Ma, D.; Hasanbeigi, A.; Chen, W. Energy-Efficiency and Air-Pollutant Emissions-Reduction Opportunities for the Ammonia industry in China; Lawrence Berkeley National Laboratory: Berkeley, CA, USA, 2015. [Google Scholar]

- Appl, M. Ammonia: Principles and Industrial Practice; Wiley-VCH: Weinheim, Germany, 1998. [Google Scholar]

- Worrell, E.; Phylipsen, D.; Einstein, D.; Martin, N. Energy Use and Energy Intensity of the U.S. Chemical Industry; Ernest Orlando Lawrence Berkeley National Laboratory: Berkeley, CA, USA, 2000. [Google Scholar]

- European Commission. Large Volume Inorganic Chemicals—Ammonia, Acids and Fertilisers; Joint Research Centre: Brussels, Belgium, 2007. [Google Scholar]

- Noelker, K.; Ruether, J. Low-Energy Ammonia Production: Baseline Energy Consumption, Options for Energy Optimization. Dusseldorf, Germany. 2011. Available online: https://ucpcdn.thyssenkrupp.com/_legacy/UCPthyssenkruppBAIS/assets.files/download_1/ammonia_2/low_energy_consumption_ammonia_production_2011_paper.pdf (accessed on 15 April 2022).

- Brown, T. Innovations in Ammonia; US DOE, Hydrogen & Fuel Cell Technical Advisory Committee: Washington, DC, USA, 2018. [Google Scholar]

- OECD/IEA. Methane Tracker Data Explorer. 2022. Available online: https://www.iea.org/articles/methane-tracker-database (accessed on 1 June 2022).

- Egli, F.; Steffen, B.; Schmidt, T.S. Bias in energy system models with uniform cost of capital assumption. Nat. Commun. 2019, 10, 4588. [Google Scholar] [CrossRef] [Green Version]

- Cesaro, Z.; Ives, M.; Nayak-Luke, R.; Mason, M.; Bañares-Alcántara, R. Ammonia to power: Forecasting the levelized cost of electricity from green ammonia in large-scale power plants. Appl. Energy 2021, 282, 116009. [Google Scholar] [CrossRef]

- Nayak-Luke, R.M.; Banares-Alcantara, R. Techno-economic viability of islanded green ammonia as a carbon-free energy vector and as a substitute for conventional production. Energy Environ. Sci. 2020, 13, 2957–2966. [Google Scholar] [CrossRef]

- Pozo, C.A.; Cloete, S. Techno-economic assessment of blue and green ammonia as energy carriers in a low-carbon future. Energy Convers. Manag. 2022, 255, 115312. [Google Scholar] [CrossRef]

- Bogdanov, D.; Child, M.; Breyer, C. Reply to ‘Bias in energy system models with uniform cost of capital assumption’. Nat. Commun. 2019, 10, 1–2. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- IRENA. Green Hydrogen Cost Reduction: Scaling up Electrolysers to Meet the 1.5 °C Climate Goal; IRENA Publications: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Stones, J. MEPs Vote to Remove Additionality Principle for Renewable Hydrogen Production. Available online: https://www.icis.com/explore/resources/news/2022/09/14/10805502/meps-vote-to-remove-additionality-principle-for-renewable-hydrogen-production/ (accessed on 14 September 2022).

- Longden, T.; Beck, F.J.; Jotzo, F.; Andrews, R.; Prasad, M. ‘Clean’ hydrogen?—Comparing the emissions and costs of fossil fuel versus renewable electricity based hydrogen. Appl. Energy 2022, 306, 118145. [Google Scholar] [CrossRef]

- Cheema, I.; Krewer, U. Operating envelope of Haber–Bosch process design for power-to-ammonia. RSC Adv. 2018, 8, 34926–34936. [Google Scholar] [CrossRef] [Green Version]

- Zivar, D.; Kumar, S.; Foroozesh, J. Underground hydrogen storage: A comprehensive review. Int. J. Hydrog. Energy 2021, 46, 23436–23462. [Google Scholar] [CrossRef]

- Toktarova, A.; Göransson, L.; Johnsson, F. Design of Clean Steel Production with Hydrogen: Impact of Electricity System Composition. Energies 2021, 14, 8349. [Google Scholar] [CrossRef]

- Muhammed, N.S.; Haq, B.; Shehri, D.A.; Al-Ahmed, A.; Rahman, M.M.; Zaman, E. A review on underground hydrogen storage: Insight into geological sites, influencing factors and future outlook. Energy Rep. 2022, 8, 461–499. [Google Scholar] [CrossRef]

- Hévin, G. Underground Storage of Hydrogen in Salt Caverns; Paris, France. 2019. Available online: https://energnet.eu/wp-content/uploads/2021/02/3-Hevin-Underground-Storage-H2-in-Salt.pdf (accessed on 26 August 2022).

- Power, M. US DOE Closes $504.4 Million Loan to Advanced Clean Energy Storage Project for Hydrogen Production and Storage. Available online: https://power.mhi.com/regions/amer/news/20220609 (accessed on 9 June 2022).

- Gessel, S. Underground Hydrogen Storage; Geneva, Switzerland. 2021. Available online: https://unece.org/sites/default/files/2021-04/09_Serge_van_Gessel-Hydrogen_Storage_and_UNFC-UNECE_RM_Week-2021.pdf (accessed on 26 August 2022).

- RAG Austria A.G. Underground Sun Conversion—Renewable Gas Produced to Store Solar and Wind Power; RAG Austria AG: Vienna, Austria, 2018. [Google Scholar]

- HyChico. Underground Hydrogen Storage. 2018. Available online: http://www.hychico.com.ar/eng/underground-hydrogen-storage.html (accessed on 26 August 2022).

- Blanco, H.; Faaij, A. A review at the role of storage in energy systems with a focus on Power to Gas and long-term storage. Renew. Sustain. Energy Rev. 2018, 81, 1049–1086. [Google Scholar] [CrossRef]

- Perez, A.; Pérez, E.; Dupraz, S.; Bolcich, J. Patagonia Wind—Hydrogen Project: Underground Storage and Methanation. Zaragoza, Spain. 2016. Available online: https://hal-brgm.archives-ouvertes.fr/hal-01317467/document (accessed on 26 August 2022).

- Kruck, O.; Crotogino, F. Benchmarking of Selected Storage Options; KBB Underground Technologies GmbH: Hannover, Germany, 2013. [Google Scholar]

- Patonia, A.; Poudineh, R. Cost-Competitive Green Hydrogen: How to Lower the Cost of Electrolysers? Oxford Institute for Energy Studies: Oxford, UK, 2022. [Google Scholar]

- Service, R.F. Ammonia-a renewable fuel made from sun, air, and water—Could power the globe without carbon. Science 2018. [Google Scholar] [CrossRef]

- Smith, C.; Hill, A.K.; Torrento-Murciano, L. Current and future role of Haber–Bosch ammonia in a carbon-free energy landscape. Energy Environ. Sci. 2022, 13, 331–344. [Google Scholar] [CrossRef]

- Giddey, S.; Badwal, S.; Munnings, C.; Dolan, M. Ammonia as a Renewable Energy Transportation Media. ACS Sustainable Chem. Eng. 2017, 5, 10231–10239. [Google Scholar] [CrossRef]

- Ishimoto, Y.; Voldsund, M.; Neksa, P.; Roussanaly, S.; Berstad, D.; Gardarsdottir, S.O. Large-scale production and transport of hydrogen from Norway to Europe and Japan: Value chain analysis and comparison of liquid hydrogen and ammonia as energy carriers. Int. J. Hydrog. Energy 2020, 45, 32865–32883. [Google Scholar] [CrossRef]

- Morlanés, N.; Katikaneni, S.P.; Paglieri, S.N.; Harale, A.; Solami, B.; Sarathy, S.M.; Gascon, J. A technological roadmap to the ammonia energy economy: Current state and missing technologies. Chem. Eng. J. 2021, 408, 127310. [Google Scholar] [CrossRef]

- Frattini, D.; Cinti, G.; Bidini, G.; Desideri, U.; Cioffi, R.; Jannelli, E. A system approach in energy evaluation of different renewable energies sources integration in ammonia production plants. Renew. Energy 2016, 99, 472–482. [Google Scholar] [CrossRef]

- Ottosson, A. Integration of Hydrogen Production via Water Electrolysis at a CHP Plant—A Feasibility Study; Lulea University of Technolog: Lulea, Sweden, 2021. [Google Scholar]

- Cordonnier, J.; Saygin, D. Green Hydrogen Opportunities for Emerging and Developing Economies; OECD Publishing: Paris, France, 2022. [Google Scholar]

- Egerer, J.; Grimm, V.; Niazmand, K.; Runge, P. The Economics of Global Green Ammonia Trade—“Shipping Australian Wind and Sunshine to Germany”; Elsevier: Erlangen, Germany, 2022. [Google Scholar] [CrossRef]

- Lan, R.; Irvine, J.T.; Tao, S. Ammonia and related chemicals as potential indirect hydrogen storage materials. Int. J. Hydrog. Energy 2012, 37, 1482–1494. [Google Scholar] [CrossRef]

- Rissman, J.; Bataille, C.; Masanet, E.; Aden, N.; Zhou, W.M., III; Elliott, N.; Dell, R.; Heeren, N.; Huckestein, B.; Crescko, J.; et al. Technologies and policies to decarbonize global industry: Review and assessment of mitigation drivers through 2070. Appl. Energy 2020, 266, 114848. [Google Scholar] [CrossRef]

- Nilsson, L.; Bauer, F.; Ahman, M.; Andersson, F.; Bataille, C.; Can, S.R.; Ericsson, K.; Hansen, T.; Johansson, B.; Lechtenböhmer, S.; et al. An industrial policy framework for transforming energy and emissions intensive industries towards zero emissions. Clim. Policy 2021, 21, 1053–1065. [Google Scholar] [CrossRef]

- OECD. Framework for Industry’s Net-Zero Transition: Developing Financing Solutions in Emerging and Develoing Economies; OECD Publications: Paris, France, 2022. [Google Scholar]

- Saygin, D.; Rigter, J.; Caldecott, B.; Wagner, N.; Gielen, D. Power sector asset stranding effects of climate policies. Energy Sources Part B Econ. Plan. Policy 2019, 14, 99–124. [Google Scholar] [CrossRef]

- Warner, E.; Steinberg, D.; Hodson, E.; Heath, G. Potential Cost-Effective Opportunities for Methane Emission Abatement; The Joint Institute for Strategic Energy Analysis: Golden, CO, USA, 2015. [Google Scholar]

- Balcombe, P.; Heggo, D.A.; Harrison, M. Total Methane and CO2 Emissions from Liquefied Natural Gas Carrier Ships: The First Primary Measurements. Environ. Sci. Technol. 2022, 56, 9632–9640. [Google Scholar] [CrossRef]

- Newborough, M.; Cooley, G. Green hydrogen: Water use implications and opportunities. Fuel Cells Bull. 2021, 2021, 12–14. [Google Scholar]

- IRENA. Global Hydrogen Trade to Meet the 1.5 °C Climate Goal: Part III—Green Hydrogen Cost and Potential; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2022. [Google Scholar]

- Hasanbeigi, A.; Nilsson, A.; Mete, G.; Fontenit, G.; Shi, D. Fostering Industry Transition through Green Public Procurement: A “How to” Guide for the Cement & Steel Sectors; LeadIT: Stockholm, Sweden; UNIDO: Vienna, Austria; CEM: Paris, France, 2021. [Google Scholar]

- George, J.F.; Müller, V.P.; Winkler, J.; Ragwitz, M. Is blue hydrogen a bridging technology?—The limits of a CO2 price and the role of state-induced price components for green hydrogen production in Germany. Energy Policy 2022, 167, 113072. [Google Scholar] [CrossRef]

- Al-Qahtani, A.; Parkinson, B.; Hellgardt, K.; Shah, N.; Guillen-Gosalbz, G. Uncovering the true cost of hydrogen production routes using life cycle monetization. Appl. Energy 2021, 281, 115958. [Google Scholar] [CrossRef]

- OECD/IEA. Global Average Levelised Cost of Hydrogen Production by Energy Source and Technology, 2019 and 2050. 2020. Available online: https://www.iea.org/data-and-statistics/charts/global-average-levelised-cost-of-hydrogen-production-by-energy-source-and-technology-2019-and-2050 (accessed on 5 August 2022).

- Parkinson, B.; Balcombe, P.; Speirs, J.; Hawkes, A.; Hellgardt, K. Levelized cost of CO2 mitigation from hydrogen production routes. Energy Environ. Sci. 2019, 12, 19–40. [Google Scholar] [CrossRef]

- IRENA. Green Hydrogen Cost Reduction; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- IRENA. Renewable Power Generation Costs in 2021; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2022. [Google Scholar]

- IRENA. Renewable Power Generation Costs 2020; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2021. [Google Scholar]

- The World Bank. Global Solar Atlas. 2022. Available online: https://globalsolaratlas.info/map?c=11.609193,8.4375,3 (accessed on 5 August 2022).

- The World Bank. Global Wind Atlas. 2022. Available online: https://globalwindatlas.info/en (accessed on 5 August 2022).

- Saygin, D.; Gielen, D.J.; Draeck, M.; Worrell, E.; Patel, M.K. Assessment of the technical and economic potentials of biomass use for the production of steam, chemicals and polymers. Renew. Sustain. Energy Rev. 2014, 40, 1153–1167. [Google Scholar] [CrossRef]

- Spath, P.L.; Mann, M.K. Life Cycle Assessment of Hydrogen Production via Natural Gas Steam Reforming; National Renewable Energy Laboratory: Golden, CO, USA, 2001. [Google Scholar]

- Rouwenhorst, K.H.; Ham, A.G.; Mul, G.; Kersten, S.R. Islanded ammonia power systems: Technology review & conceptual process design. Renew. Sustain. Energy Rev. 2019, 114, 109339. [Google Scholar]

- OECD. Long-Term Interest Rates. 2022. Available online: https://data.oecd.org/interest/long-term-interest-rates.htm (accessed on 5 August 2022).

- Trading Economics. Credit Rating. 2022. Available online: https://tradingeconomics.com/country-list/rating (accessed on 5 August 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Feedstock/Production Route | [14] | [28] | [30] 1 |

|---|---|---|---|

| [Mt/Year] | [Mt/Year] | [Mt/Year] | |

| Green hydrogen | 550 | 400–450 | 387 |

| Natural gas with CO2 capture storage/use | 75 | - | 152 |

| Fossil fuel with CO2 capture storage/use | - | - | - |

| Biomass and other thermochemical | - | 100–150 | 17 |

| Fossil fuel with no capture | 40 | 100 | - |

| Other | - | - | 5 |

| Total | 665 | 650 | 561 |

| Production Pathway | Energy Use (GJ/t Ammonia) | Cradle-to-Factory Gate CO2 Equivalent (t CO2-eq/t Ammonia) | Ammonia Type | References |

|---|---|---|---|---|

| Coal Gasification | 56–64 | Fuel: 5.32–6.18 | Grey | Fuel use and related CO2 emissions [76] |

| SMR and ATR (without CCS) | 28–36 | Fuel: 1.51–2.02 Electricity: 0–1.05 Methane: 0.19–2.40 Total: 2.29–4.27 | Grey | Fuel use and CO2 related emissions: [77,78,79,80,81] Electricity and methane: See Appendix A for background data |

| SMR + CCS | 33 | Total: 1.34–3.68 | Blue | See Appendix A for background data |

| ATR + CCS | 29 | 0.65–0.70 | Blue | [14,75] |

| Renewables + Electrolyzer | 30–36 (electricity) | Green | Own estimate based on [16,17,56,57,58,59] |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Saygin, D.; Blanco, H.; Boshell, F.; Cordonnier, J.; Rouwenhorst, K.; Lathwal, P.; Gielen, D. Ammonia Production from Clean Hydrogen and the Implications for Global Natural Gas Demand. Sustainability 2023, 15, 1623. https://0-doi-org.brum.beds.ac.uk/10.3390/su15021623

Saygin D, Blanco H, Boshell F, Cordonnier J, Rouwenhorst K, Lathwal P, Gielen D. Ammonia Production from Clean Hydrogen and the Implications for Global Natural Gas Demand. Sustainability. 2023; 15(2):1623. https://0-doi-org.brum.beds.ac.uk/10.3390/su15021623

Chicago/Turabian StyleSaygin, Deger, Herib Blanco, Francisco Boshell, Joseph Cordonnier, Kevin Rouwenhorst, Priyank Lathwal, and Dolf Gielen. 2023. "Ammonia Production from Clean Hydrogen and the Implications for Global Natural Gas Demand" Sustainability 15, no. 2: 1623. https://0-doi-org.brum.beds.ac.uk/10.3390/su15021623