Measuring Profitable Efficiency, Technical Efficiency, Technological Innovation of Waste Management Companies Using Negative Super-SBM–Malmquist Model

,

,  ,

,  ,

,

Abstract

:1. Introduction

2. Theoretical Foundations and Methodology

2.1. Literature Review

2.2. Method of Research

2.2.1. Research Process

2.2.2. Data Source

2.3. Mathematical Modeling

2.3.1. Negative Super-SBM Model

2.3.2. Negative Malmquist Model

3. Empirical Results

3.1. Pearson Correlation Coefficient

3.2. Profitable Efficiency

3.3. Technical and Technological Innovation

3.3.1. Technical Efficiency Change (Catch-Up Index)

3.3.2. Frontier-Shift Index (Technological Change)

3.3.3. Malmquist Productivity Index (MPI)

3.3.4. Cumulative Malmquist Index (CMI) and Adjusted Malmquist Index (AMI)

3.4. Discussion

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| DMUs | TA | COR | OE | TR | NI | TA | COR | OE | TR | NI |

|---|---|---|---|---|---|---|---|---|---|---|

| 2017 | 2018 | |||||||||

| 1 | 3,706,570 | 2,062,673 | 754,530 | 2,944,978 | 100,739 | 3,738,321 | 2,305,551 | 812,178 | 3,300,303 | 65,636 |

| 2 | 4,441,000 | 1,271,000 | 378,000 | 1,752,000 | 57,000 | 3,843,000 | 1,321,000 | 398,000 | 1,868,000 | 152,000 |

| 3 | 46,688,449 | 25,416,858 | 3,503,118 | 30,620,104 | 489,442 | 45,815,473 | 26,411,951 | 3,374,176 | 31,578,635 | 535,388 |

| 4 | 21,829,000 | 9,021,000 | 2,844,000 | 14,485,000 | 1,949,000 | 22,650,000 | 9,249,000 | 2,930,000 | 14,914,000 | 1,925,000 |

| 5 | 21,147,000 | 6,214,600 | 2,209,500 | 10,041,500 | 1,278,400 | 21,617,000 | 6,150,000 | 2,173,600 | 10,040,900 | 1,036,900 |

| 6 | 12,014,681 | 2,704,775 | 1,142,122 | 4,630,488 | 576,817 | 12,627,329 | 2,865,704 | 1,204,875 | 4,922,941 | 546,871 |

| 7 | 6,988,300 | 2,118,200 | 1,470,100 | 3,580,700 | 42,400 | 6,455,500 | 2,109,900 | 1,178,400 | 3,485,900 | −244,700 |

| 8 | 314,657 | 276,102 | 54,428 | 365,957 | 28,123 | 347,822 | 323,165 | 65,477 | 410,183 | 14,728 |

| 9 | 802,076 | 350,915 | 84,466 | 504,042 | 49,365 | 947,898 | 395,834 | 92,340 | 565,928 | 49,595 |

| 2019 | 2020 | |||||||||

| 1 | 4,108,904 | 2,387,819 | 794,915 | 3,412,190 | 97,740 | 4,131,520 | 2,137,751 | 755,010 | 3,144,097 | 134,837 |

| 2 | 3,715,000 | 1,371,000 | 407,000 | 1,870,000 | 10,000 | 3,706,000 | 1,420,000 | 396,000 | 1,904,000 | −28,000 |

| 3 | 49,991,086 | 27,820,803 | 3,401,354 | 33,135,684 | 761,584 | 55,286,346 | 26,960,501 | 3,338,589 | 31,699,045 | 108,223 |

| 4 | 27,743,000 | 9,496,000 | 3,205,000 | 15,455,000 | 1,670,000 | 29,345,000 | 9,341,000 | 3,399,000 | 15,218,000 | 1,496,000 |

| 5 | 22,683,800 | 6,298,400 | 2,198,400 | 10,299,400 | 1,073,300 | 23,434,000 | 6,100,500 | 2,211,800 | 10,153,600 | 967,200 |

| 6 | 13,737,695 | 3,198,757 | 1,290,196 | 5,388,679 | 566,841 | 13,992,364 | 3,276,808 | 1,290,036 | 5,445,990 | 204,677 |

| 7 | 6,437,000 | 2,134,400 | 1,055,100 | 3,308,900 | −346,800 | 5,581,900 | 1,622,400 | 897,600 | 2,675,500 | −57,300 |

| 8 | 471,314 | 349,603 | 81,963 | 421,764 | 8363 | 461,669 | 321,648 | 66,289 | 381,652 | 11,937 |

| 9 | 2,231,244 | 475,675 | 141,123 | 685,509 | 33,140 | 1,831,283 | 688,805 | 201,067 | 933,854 | −389,359 |

| TA | COR | OE | TR | NI | ||

|---|---|---|---|---|---|---|

| 2017 | DMU2 | 1,395,245.6 | 0.0 | 0.0 | 236,463.3 | 193,983.8 |

| DMU5 | 3,678,659.2 | 0.0 | 121,671.7 | 64,982.4 | 60,917.1 | |

| 2018 | DMU2 | 467,313.9 | 0.0 | 0.0 | 207,385.4 | 92,840.0 |

| DMU5 | 3,832,865.1 | 0.0 | 81,123.8 | 22,582.0 | 219,037.8 | |

| DMU7 | 0.0 | 0.0 | 462,165.9 | 0.0 | 651,374.0 | |

| 2019 | DMU2 | 324,965.1 | 0.0 | 0.0 | 181,877.5 | 167,337.5 |

| DMU5 | 2,634,726.3 | 0.0 | 0.0 | 6722.9 | 30,485.5 | |

| DMU7 | 0.0 | 0.0 | 331,946.3 | 84,728.9 | 684,925.5 | |

| 2020 | DMU2 | 0.0 | 0.0 | 0.0 | 143,997.1 | 170,948.7 |

| DMU9 | 0.0 | 3674.9 | 0.0 | 57,954.1 | 461,306.6 |

References

- Apsara, D.; Walahapitiya, P.; Perera, D.; Madushan, H.; Abeygunawardhana, L.; Ferdinando, D. Solid Waste Management in Textile Industry. J. Res. Technol. Eng. 2022, 3, 1–7. [Google Scholar]

- Demirbas, A. Waste management, waste resource facilities and waste conversion processes. Energy Convers. Manag. 2011, 52, 1280–1287. [Google Scholar] [CrossRef]

- Awuchi, C.; Awuchi, C.; Ikechukwu, A.; Victory, I. Industrial and Community Waste Management: Global Perspective. Am. J. Phys. Sci. (AJPS) 2020, 1, 1–16. [Google Scholar]

- Wang, C.N.; Hoang, Q.N.; Nguyen, T.K.L. Integrating the EBM Model and LTS(A,A,A) Model to Evaluate the Efficiency in the Supply Chain of Packaging Industry in Vietnam. Axioms 2021, 10, 33. [Google Scholar] [CrossRef]

- Kaza, S.; Yao, L.C.; Bhada-Tata, P.; Woerden, F.V. What a Waste 2.0: A Global Snapshot of Solid Waste Management to 2050; Urban Development; World Bank: Washington, DC, USA, 2018. [Google Scholar]

- Alliedmarketresearch. Available online: https://www.alliedmarketresearch.com/waste-management-market (accessed on 12 October 2021).

- Lichpinseo. Available online: https://linchpinseo.com/trends-waste-management-industry/ (accessed on 15 October 2021).

- The World Bank. Available online: https://www.worldbank.org/en/topic/urbandevelopment/brief/solid-waste-management (accessed on 28 February 2022).

- Papadakis, V.; Lioukas, S.; Chambers, D. Strategic decision-making processes: The role of management and context. Strateg. Manag. J. 1998, 19, 115–147. [Google Scholar] [CrossRef]

- Gollakota, A.R.K.; Gautam, S.; Shu, C.M. Inconsistencies of e-waste management in developing nations—Facts and plausible solutions. J. Environ. Manag. 2020, 261, 110234. [Google Scholar] [CrossRef]

- Gharfalkar, M.; Court, R.; Campbell, C.; Ali, Z.; Hillier, G.; Court, R. Analysis of waste hierarchy in the European waste directive 2008/98/EC. Waste Manag. 2015, 39, 305–313. [Google Scholar] [CrossRef]

- EURLex. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32008L0098 (accessed on 3 March 2022).

- EPA. Available online: https://www.epa.gov/rcra/resource-conservation-and-recovery-act-rcra-regulations (accessed on 3 March 2022).

- Kalulu, K.; Hoko, Z. Assessment of the performance of a public water utility: A case study of Blantyre Water Board in Malawi. Phys. Chem. Earth. 2010, 35, 806–810. [Google Scholar] [CrossRef]

- Bartolacci, F.; Paolini, A.; Quaranta, A.G.; Soverchia, M. Assessing factors that influence waste management financial sustainability. Waste Manag. 2018, 79, 571–579. [Google Scholar] [CrossRef]

- Charnes, A.A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision-making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Hotelling, H. The economics of exhaustible resources. J. Political Econ. 1931, 39, 137–175. [Google Scholar] [CrossRef]

- Banker, R.D.; Charnes, A.; Cooper, W.W. Some models for estimating technical and scale inefficiencies in data envelopment analysis. Manag. Sci. 1984, 30, 1078–1092. [Google Scholar] [CrossRef] [Green Version]

- Tone, K. A slacks-based measure of efficiency in data envelopment analysis. Eur. J. Oper. Res. 2001, 130, 498–509. [Google Scholar] [CrossRef] [Green Version]

- Tone, K. A slacks-based measure of super-efficiency in data envelopment analysis. Eur. J. Oper. Res. 2002, 143, 32–41. [Google Scholar] [CrossRef] [Green Version]

- Tone, K.; Chang, T.S.; Wu, C.H. Handling negative data in slacks-based measure data envelopment analysis models. Eur. J. Oper. Res. 2020, 282, 926–935. [Google Scholar] [CrossRef]

- Lee, Y.J.; Joo, S.J.; Park, H.G. An application of data envelopment analysis for Korean banks with negative data. Benchmarking 2017, 24, 1052–1064. [Google Scholar] [CrossRef]

- Nguyen, X.H.; Nguyen, T.K.L. Approaching the Negative Super-SBM Model to Partner Selection of Vietnamese Securities Companies. J. Asian Financ. Econ. Bus (JAFEB) 2021, 8, 527–538. [Google Scholar] [CrossRef]

- Cui, Q.; Jin, J.Y. Airline environmental efficiency measures considering negative data: An application of a modified network Modified Slacks-based measure model. Energy 2020, 207, 118221. [Google Scholar] [CrossRef]

- Färe, R.; Grosskopf, S.; Lindgren, B.; Roos, P. Productivity changes in Swedish pharmacies 1980–1989: A non-parametric Malmquist approach. J. Prod. Anal. 1992, 3, 85–101. [Google Scholar] [CrossRef]

- Egilmez, G.; McAvoy, D. Benchmarking road safety of U.S. states: A DEA-based Malmquist productivity index approach. Accid. Anal. Prev. 2013, 53, 55–64. [Google Scholar] [CrossRef]

- Pan, W.T.; Zhuang, M.E.; Zhou, Y.Y.; Yang, J.J. Research on sustainable development and efficiency of China’s E-Agriculture based on a data envelopment analysis-Malmquist model. Technol. Forecast. Soc. Chang. 2021, 162, 120298. [Google Scholar] [CrossRef]

- Wang, C.N.; Nguyen, T.L.; Dang, T.T.; Bui, T.H. Performance Evaluation of Fishery Enterprises Using Data Envelopment Analysis- A Malmquist Model. Mathematics 2021, 9, 469. [Google Scholar] [CrossRef]

- Bjurek, H. The Malmquist total factor productivity index. Scand. J. Econ. 1996, 98, 303–313. [Google Scholar] [CrossRef]

- Yahoo Finance. Available online: https://finance.yahoo.com/ (accessed on 29 June 2021).

- Wastetodaymagazine. Available online: https://www.wastetodaymagazine.com/article/waste-todays--top-50-haulers-list/ (accessed on 30 November 2021).

- Menikpura, S.N.M.; Gheewala, S.H.; Bonnet, S.; Chiemchaisri, C. Evaluation of the Effect of Recycling on Sustainability of Municipal Solid Waste Management in Thailand. Waste Biomass Valorization 2013, 4, 237–257. [Google Scholar] [CrossRef]

- Lohri, C.R.; Camenzind, E.J.; Zurbrügg, C. Financial sustainability in municipal solid waste management—Costs and revenues in Bahir Dar, Ethiopia. Waste Manag. 2014, 34, 542–552. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Cooper, W.W.; Seiford, L.M.; Tone, K. Data Envelopment Analysis-A Comprehensive Text with Models, Applications, References and DEA-Solver Software, 2nd ed.; Springer: Berlin/Heidelberg, Germany, 2006. [Google Scholar]

- Thore, S.; Kozmetsky, G.; Phillips, F. DEA of financial statements data: The U.S. computer industry. J. Product. Anal. 1994, 5, 229–248. [Google Scholar] [CrossRef]

- Tone, K. Advances in DEA Theory and Applications: With Extensions to Forecasting Models; John Wiley & Sons Ltd.: Hoboken, NJ, USA, 2017. [Google Scholar]

- Astuteanalytica. Available online: https://www.astuteanalytica.com/request-toc/waste-management-market (accessed on 5 March 2022).

- Tey, J.S.; Goh, K.C.; Kek, S.L.; Goh, H.H. Current practice of waste management system in Malaysia: Towards sustainable waste management. Environ. Eng. Manag. J. 2013, 6, 261–336. [Google Scholar]

- Recyclingtoday. Available online: https://www.recyclingtoday.com/article/nestle-veolia-plastic-recycling-cooperation/ (accessed on 12 December 2021).

| DMUs | Company Name | Headquarters |

|---|---|---|

| DMU1 | Clean Harbors, Inc. (CLH) | USA |

| DMU2 | Covanta Holding Corporation (CVA) | USA |

| DMU3 | Veolia Environment S.A. (VEOEY) | France |

| DMU4 | Waste Management, Inc. (WM) | USA |

| DMU5 | Republic Services, Inc. (RSG) | USA |

| DMU6 | Waste Connections, Inc. (WCN) | Canada |

| DMU7 | Stericycle, Inc. (SRCL) | USA |

| DMU8 | Heritage-Crystal Clean, Inc (HCCI) | USA |

| DMU9 | US Ecology, Inc. (ECOL) | USA |

| 2017 | 2018 | 2019 | 2020 | |||||

|---|---|---|---|---|---|---|---|---|

| Score | Rank | Score | Rank | Score | Rank | Score | Rank | |

| DMU1 | 1.062 | 5 | 1.087 | 4 | 1.098 | 4 | 1.127 | 4 |

| DMU2 | 0.361 | 9 | 0.858 | 8 | 0.792 | 8 | 0.799 | 8 |

| DMU3 | 1.400 | 1 | 1.380 | 2 | 1.349 | 2 | 1.426 | 2 |

| DMU4 | 1.312 | 4 | 1.339 | 3 | 1.214 | 3 | 1.229 | 3 |

| DMU5 | 0.974 | 8 | 0.922 | 7 | 0.989 | 7 | 1.015 | 7 |

| DMU6 | 1.046 | 7 | 1.034 | 6 | 1.044 | 5 | 1.018 | 6 |

| DMU7 | 1.318 | 3 | 0.070 | 9 | 0.092 | 9 | 1.025 | 5 |

| DMU8 | 1.386 | 2 | 1.541 | 1 | 1.716 | 1 | 1.680 | 1 |

| DMU9 | 1.056 | 6 | 1.060 | 5 | 1.032 | 6 | 0.144 | 9 |

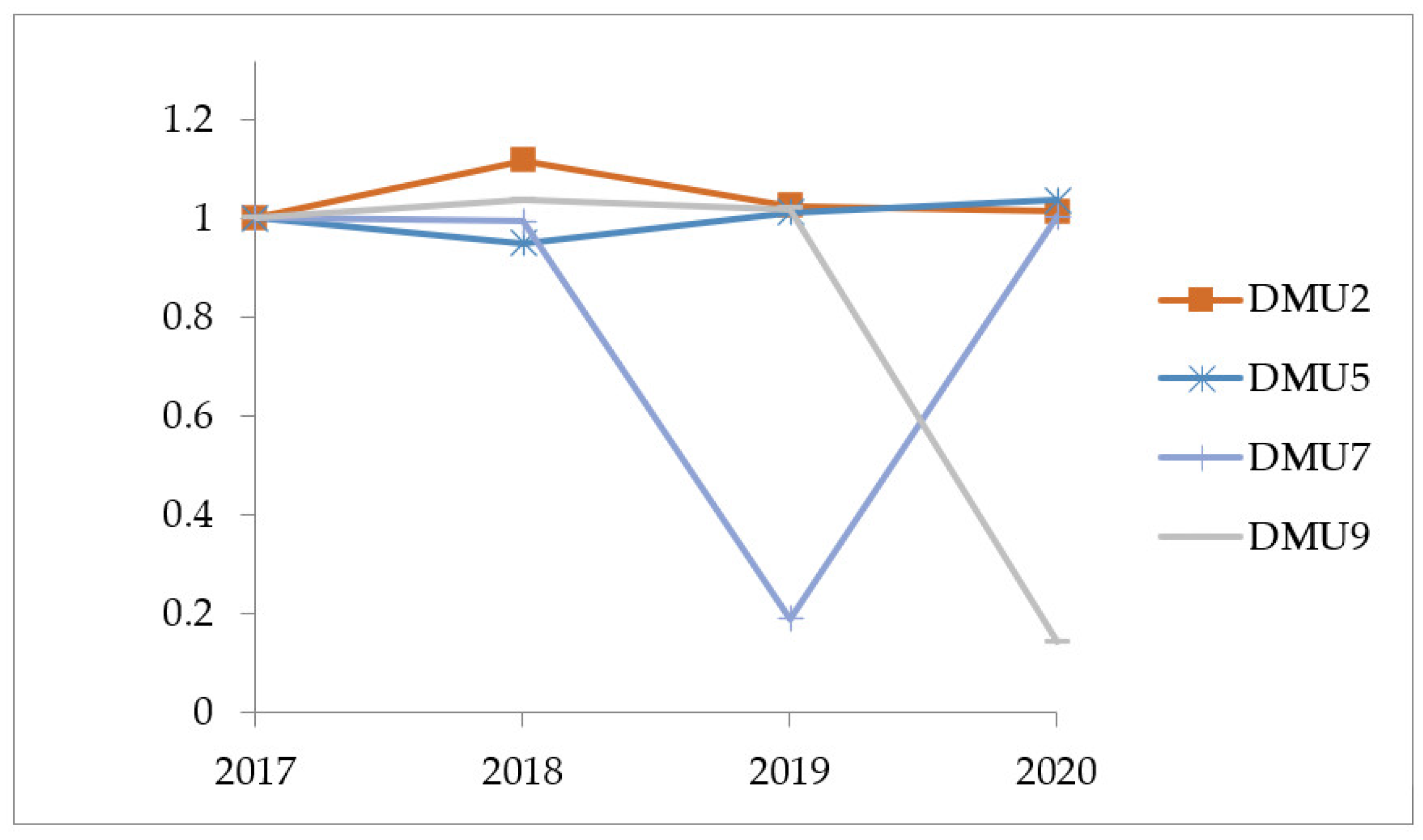

| Catch-up | 2017 => 2018 | 2018 => 2019 | 2019 => 2020 | Average |

|---|---|---|---|---|

| DMU1 | 1.029192 | 1.012638 | 1.033706 | 1.025179 |

| DMU2 | 1.116109 | 0.916079 | 0.990557 | 1.007581 |

| DMU3 | 1.000526 | 1.004000 | 0.996242 | 1.000256 |

| DMU4 | 1.061000 | 0.859401 | 1.023652 | 0.981351 |

| DMU5 | 0.949074 | 1.064716 | 1.025529 | 1.013107 |

| DMU6 | 0.992475 | 1.008661 | 0.960340 | 0.987158 |

| DMU7 | 0.992857 | 0.190107 | 5.311656 | 2.164873 |

| DMU8 | 1.000000 | 1.000000 | 1.000000 | 1.000000 |

| DMU9 | 1.036601 | 0.981614 | 0.139162 | 0.719126 |

| Average | 1.019759 | 0.893024 | 1.386760 | 1.099848 |

| Max | 1.116109 | 1.064716 | 5.311656 | 2.164873 |

| Min | 0.949074 | 0.190107 | 0.139162 | 0.719126 |

| SD | 0.048194 | 0.270305 | 1.499549 | 0.410407 |

| Frontier | 2017 => 2018 | 2018 => 2019 | 2019 => 2020 | Average |

|---|---|---|---|---|

| DMU1 | 1.048880 | 0.961287 | 0.965076 | 0.991748 |

| DMU2 | 0.987255 | 0.919907 | 0.971854 | 0.959672 |

| DMU3 | 1.020174 | 1.022377 | 0.725646 | 0.922732 |

| DMU4 | 0.962681 | 0.972562 | 0.939385 | 0.958209 |

| DMU5 | 1.027553 | 0.977746 | 0.967995 | 0.991098 |

| DMU6 | 0.990337 | 0.963644 | 0.871828 | 0.941936 |

| DMU7 | 0.663869 | 0.951609 | 0.981953 | 0.865810 |

| DMU8 | 1.011791 | 0.971227 | 0.980334 | 0.987784 |

| DMU9 | 0.955749 | 0.930389 | 1.002283 | 0.962807 |

| Average | 0.963143 | 0.963416 | 0.934039 | 0.953533 |

| Max | 1.048880 | 1.022377 | 1.002283 | 0.991748 |

| Min | 0.663869 | 0.919907 | 0.725646 | 0.865810 |

| SD | 0.116222 | 0.029483 | 0.086580 | 0.040263 |

| Malmquist | 2017 => 2018 | 2018 => 2019 | 2019 => 2020 | Average |

|---|---|---|---|---|

| DMU1 | 1.079499 | 0.973436 | 0.997605 | 1.016847 |

| DMU2 | 1.101884 | 0.842708 | 0.962677 | 0.969089 |

| DMU3 | 1.020711 | 1.026466 | 0.722919 | 0.923365 |

| DMU4 | 1.021404 | 0.835821 | 0.961604 | 0.939610 |

| DMU5 | 0.975224 | 1.041022 | 0.992707 | 1.002985 |

| DMU6 | 0.982885 | 0.971989 | 0.837251 | 0.930708 |

| DMU7 | 0.659127 | 0.180908 | 5.215798 | 2.018611 |

| DMU8 | 1.011791 | 0.971227 | 0.980334 | 0.987784 |

| DMU9 | 0.990731 | 0.913283 | 0.139479 | 0.681164 |

| Average | 0.982584 | 0.861873 | 1.312264 | 1.052240 |

| Max | 1.101884 | 1.041022 | 5.215798 | 2.018611 |

| Min | 0.659127 | 0.180908 | 0.139479 | 0.681164 |

| SD | 0.128542 | 0.265311 | 1.489230 | 0.375896 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, C.-N.; Hoang, Q.-N.; Nguyen, T.-K.-L.; Hsu, H.-P.; Dang, T.-T. Measuring Profitable Efficiency, Technical Efficiency, Technological Innovation of Waste Management Companies Using Negative Super-SBM–Malmquist Model. Axioms 2022, 11, 315. https://0-doi-org.brum.beds.ac.uk/10.3390/axioms11070315

Wang C-N, Hoang Q-N, Nguyen T-K-L, Hsu H-P, Dang T-T. Measuring Profitable Efficiency, Technical Efficiency, Technological Innovation of Waste Management Companies Using Negative Super-SBM–Malmquist Model. Axioms. 2022; 11(7):315. https://0-doi-org.brum.beds.ac.uk/10.3390/axioms11070315

Chicago/Turabian StyleWang, Chia-Nan, Quynh-Ngoc Hoang, Thi-Kim-Lien Nguyen, Hsien-Pin Hsu, and Thanh-Tuan Dang. 2022. "Measuring Profitable Efficiency, Technical Efficiency, Technological Innovation of Waste Management Companies Using Negative Super-SBM–Malmquist Model" Axioms 11, no. 7: 315. https://0-doi-org.brum.beds.ac.uk/10.3390/axioms11070315