A Semantic Model for Enhancing Data-Driven Open Banking Services

Abstract

:1. Introduction

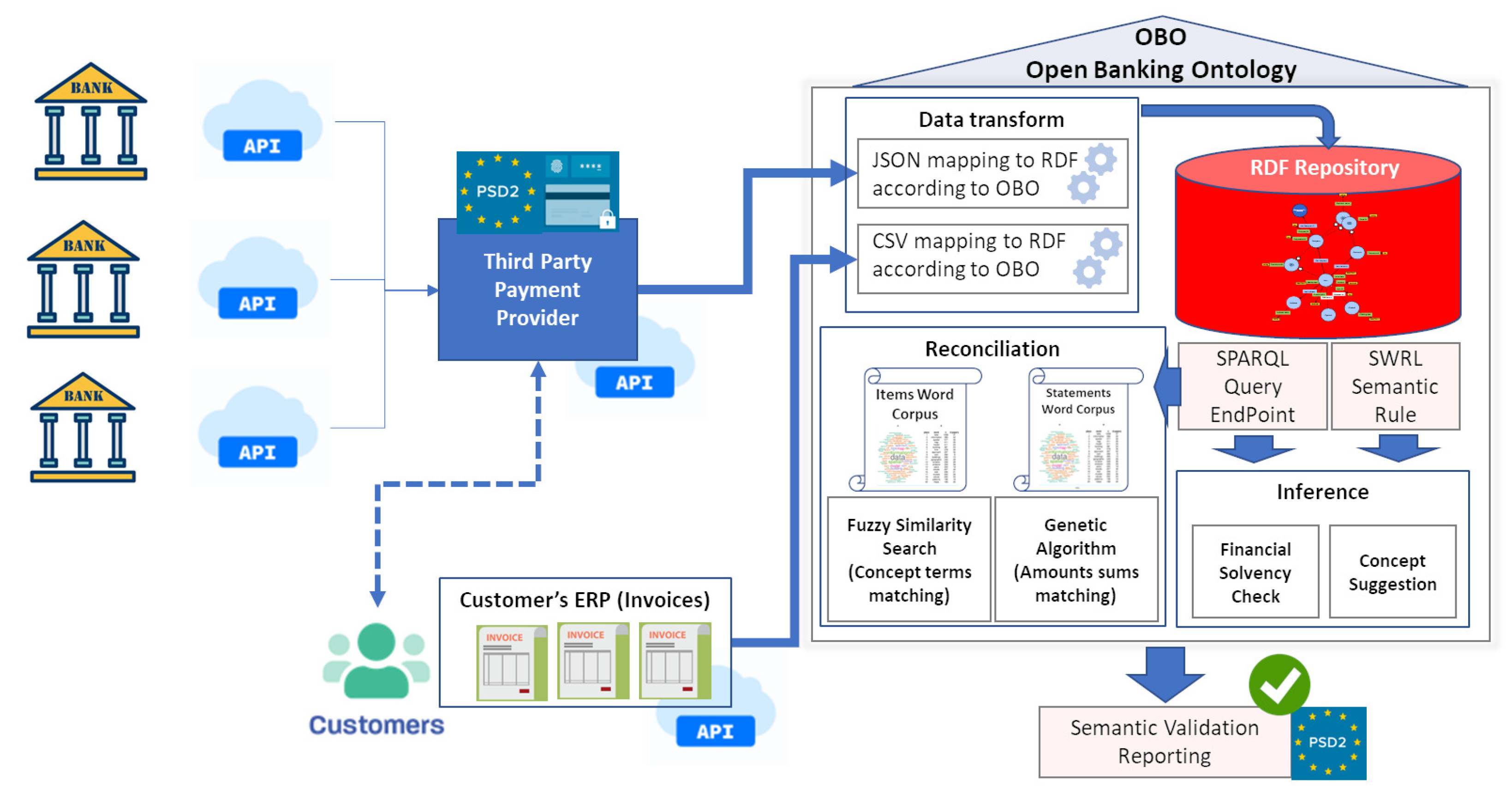

- An ontology is defined using Web Ontology Language (OWL 2) [13], for the first time for the semantic annotation of bank statement and invoice management operations in the context of PSD2 transactions. The proposal, called Open Banking Ontology (OBO), is used as a semantic integration data scheme for different information sources that enables data ingestion, querying, and reasoning in a structured and homogeneous way.

- According to the OBO definition, a semantic model is also developed for knowledge graph generation, which is populated by means of specific mapping functions for each different data source. The resulting graph comprising all the data instances is integrated into a repository using Resource Description Framework (RDF) [14], which allows querying with the same language (SPARQL). A series of reconciliation mechanisms were tested with data from more than 70,000 invoices and 33,000 open banking customers through multiple PSD2 operations.

- The proposal is validated through several real-world use cases, including intelligent matching bank statements with their corresponding invoices. Moreover, a set of SWRL reasoning rules is also specified for classifying the financial solvency of clients, including an automatic generation of concepts that would facilitate conciliation.

2. Background Concepts and Related Work

2.1. Preliminary Concepts

- -

- Ontology [15]. This is a description framework that provides a formal representation of the real world, shared by many users, by defining concepts and relationships between them. It defines a set of axioms and primitives to represent a specific domain of knowledge or discourse. In computer science, ontology refers to an artifact designed to allow the formal modeling of knowledge about a domain. Ontologies are part of the standards developed by the W3C consortium for the semantic web. In the semantic web, they are used to standardize vocabularies that facilitate the exchange of information between systems. This standard provides services to solve queries and to populate and publish knowledge graphs [16] so that they can be reusable and facilitate interoperability between heterogeneous systems and databases. Instances of ontology classes and properties annotate data or resources semantically. Furthermore, the reasoning capabilities of ontologies allow semantic web applications to infer implicit knowledge from explicitly expressed knowledge, enabling the creation of intelligent applications.

- -

- RDF [14]. To define an ontology in the context of web semantics, we used the standard language RDF, according to which resources are described in terms of properties and values. RDF statements are represented as triples, consisting of a subject, a predicate, and an object. RDFS (RDF Schema) [17] semantically extends RDF to define resource classes and the properties that those classes describe. RDFS provides the mechanisms for explaining the specific RDF vocabularies for each application. Although the expressiveness of RDFS is still insufficient for all applications, it is enough for data exchange and allows semantic languages to be built on top of it. However, for many other applications, it is necessary to have other characteristics, such as cardinality constraints, transitive properties, inverse properties, and range. When used for a specific class, it is able to express classes as unions or intersections of other classes. In addition, ontology languages should meet other requirements, such as having a well-defined syntax, being based on formal semantics necessary for reasoning, and supporting efficient reasoning mechanisms while maintaining expressiveness.

- -

- OWL [17]. Proposed by the W3C Ontology Working Group, this is a semantic markup language for publishing and sharing ontologies on the web. OWL is equivalent to a very expressive description logic, where an ontology corresponds to the Tbox [18]. This equivalence allows language to exploit the results of researchers in the logic of descriptions. OWL extends RDF and RDF Schema, with the main goal of bringing the expressiveness and reasoning power of description logic to the semantic web. OWL provides two sublanguages: OWL Lite for simple applications and OWL-DL, which represents the subset of the language equivalent to the logic of descriptions, the reasoning mechanisms of which are complex. A new version of this language is OWL 2 [13], which includes new functionalities, e.g., keys, property strings, data ranges, and qualified cardinality constraints. These new features are oriented towards increasing expressiveness.

2.2. Related Work

3. Semantic Model

3.1. Methodology

- Determine the domain and scope of the ontology. The ontology domain represents the different actors and the information generated in open banking services. More specifically, bank statements and invoice management systems are contextualised to allow for data reconciliation tasks.

- Consider reusing existing ontologies. After reviewing the literature, several ontologies were considered to describe accounting entries [8]. Still, none of them represents bank statements oriented to PSD2 format and other related aspects such as invoice contextual information. These ontologies usually contain a class Invoice, Receipt or other similar terms, but they do not ontologically describe an invoice, with relationships and components. In the proposed approach, the invoice concept plays an essential role since it allows considering all the meta-information, involving it to be further used in reconciliation mechanisms for linking with third-party bank statements. For example, those products or services the invoice refers to are usually unknown to the legal person or company that a given client has invoiced.

- Enumerate important terms in the ontology. As mentioned in the previous step, important terms in OBO correspond to data in invoices and bank statements, involving open banking service transactions. Examples of these terms are: companyId, customerId, issueDate, maturityDate, itemCurrencyAmt, and documentType, which are related to invoicing, as well as those related to bank statements, such as: Statement, Customer, Account number, Bank, Concept, and beneficiary.

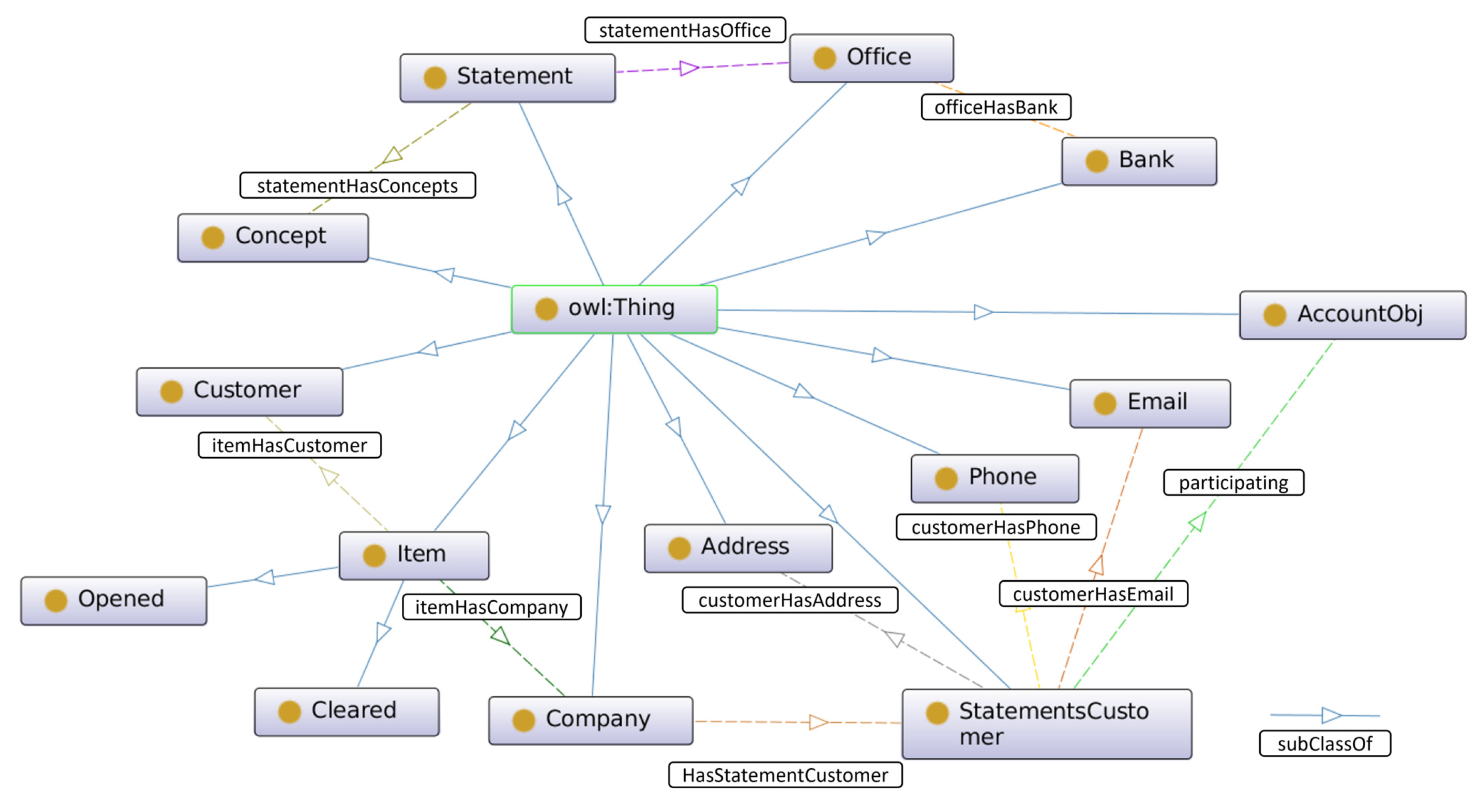

- Define the classes and the class hierarchy. From the relevant terms, we extract which of them are classes of ontology. Figure 1 shows the set of classes that have been defined to describe an open bank service. Examples of these classes are: Item, Statement, AccountObj, and Bank. The class Item comprises two subclasses, Opened and Cleared, for specifying whether Items are pending to be paid or not.

- Define the properties of classes. Object properties and data properties were created to connect instances of different classes and define their attributes. Examples of object properties are: participating, which connects a customer to the bank account; statementHasOffice, which relates a bank movement to the office in which it was registered; and ItemHasCompany, which connects an item with the company. Examples of data properties are: statementConcept, beneficiary, accountNumber itemIssueDate, itemAmount. Tables 2–6 describe details of these properties in description logic.

- Define the facets of the slots. In this step, cardinality and value constraints are defined. In the proposed ontology, examples of constraints are: the range of the property itemAmount has to be a decimal number; the range of the property itemIssueDate has to be a date; the concept of a statement has to be of type string, and so on.

- Create instances. The instances (or individuals) in the current approach are generated from the JSON documents containing actual PSD2 bank statements and the CSV files with data of the items (invoices). These data are transformed to RDF through mapping functions according to the classes and properties defined in OBO, and an RDF knowledge graph is then created.

3.2. Ontology Implementation

- The class Company represents those companies that take part in a given PSD2 transaction. For this class, 5 data properties were defined: businessName, to indicate the company name, companyId, which models the company identifier, corporationId to identify the corporation (when existing) to which the company belongs, currencyCode, which represents the currency the company works with, and fiscalId to store the tax identification number. In addition, the Company class has an object property, hasStatementCustomer, which links the company with its PSD2 bank statements. Table 2 describes the properties of the Company class in the description logic definition.

- The Customer class was included to annotate customers that participate in transactions with companies. A set of 3 data properties were defined for this class: businessName, which represents the customer’s name, customerId, which stores the customer identifier, and fiscalId to set the number of the client’s tax identification. Description logics of these properties can be found in Table 3.

- The Item class represents the invoices that customers should pay. Its main properties are defined in description logic in Table 4, comprising 7 data properties and 2 object properties. As for data properties, it is worth mentioning textititemAmount, which stores the invoice amount in the currency associated with the corresponding company, itemCurrencyAmt, to annotate the amount of the invoice, itemIssueDate, which describes the invoice issue date, currencyCode, which indicates the currency associated with the invoice and in which it is expressed, and indicator, which represents a series of descriptors associated with the invoice. The two object properties are: itemCompany, which links each invoice with its company, and ItemCustomer, which connects the invoice to the customer.

- The class Statement represents the bank statements carried out on a particular bank account. Among its main data properties, a set of 5 representatives ones is: statementAmount, to annotate the transaction amount, accountNumber, which indicates the bank account in which the statement was made, statementCurrency, which stores the currency associated with the statement, statementBeneficiary, representing the beneficiary of the bank statement, concept and statementValueDate, which indicate the concept and value date of the statement, respectively. The object property statementHasOffice was defined for this class to associate each transaction with the corresponding bank branch. Table 5 describes the properties of the Statement class.

- The Bank class models the bank information. A total of 3 data properties were defined for this class: bankGroupId, which stores the identifier of the bank group to which the bank belongs, bankId, to represent the identifier of the bank, and bankName, which stores the name of the bank. This class is important for annotating not only traditional banks, but also open banking entities that take part in PSD2 transactions with customers.

- The class StatementsCustomer represents the holders of the bank accounts in which the movements are made. For this class, a series of data properties were defined to store the customer’s identity document, name, date of birth, address, email, and telephone number, as described in Table 6. The customer is related to his/her/their bank accounts through the object property participating, specifying the role in which he/she/they participate(s) (owner or authorized). This is modeled using the AccountObj class.

3.3. Building the Knowledge Graph

- Mapping invoice data into RDF. These data are obtained from the ERP systems of the companies involved in CSV format, which comprise four different files: (1) for open invoices, (2) for closed invoices, (3) for companies that issue invoices to customers, and (4) for customer information, by means of the Customer class in OBO. In addition, contents regarding classes Item, Company, and Customer are also stored in the repository.

- Mapping PSD2 statements into RDF. Data concerning bank statements are collected from the corresponding APIs (of banking entities) in JSON format. The service client provides the user with an access token with which all bank movements can be accessed. Examples of JSON files in Code Listings A1 and A2 in Appendix A show information obtained from the PSD2-compliant API services of banks concerning the customers and their bank accounts. Classes StatementCustomer and Statement, among others, are populated in the form of semantic instances (individuals).

4. Reconciliation and Inference

4.1. Semantic Reconciliation

| Listing 1. Match by an exact amount. |

|

4.2. Semantic Inference

| Listing 2. Low debt. |

|

| Listing 3. Average debt. |

|

| Listing 4. High debt. |

|

| Listing 5. Debt Type. |

|

| Listing 6. Suggested concept. |

|

| Listing 7. Example of suggested concept query. |

|

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

| Listing A1. “Customer.json” sample (anonymized) file accessed from PSD2-compliant open banking API. |

|

| Listing A2. “Statement.json” sample (anonymized) file accessed from PSD2-compliant open banking API. |

|

References

- Polasik, M.; Huterska, A.; Iftikhar, R.; Mikula, Š. The impact of Payment Services Directive 2 on the PayTech sector development in Europe. J. Econ. Behav. Organ. 2020, 178, 385–401. [Google Scholar] [CrossRef]

- Gordon, T.F. An Overview of the Legal Knowledge Interchange Format. In Proceedings of the Business Information Systems Workshops, Berlin, Germany, 3–5 May 2010; Abramowicz, W., Tolksdorf, R., Węcel, K., Eds.; Springer: Berlin/Heidelberg, Germany, 2010; pp. 240–242. [Google Scholar]

- del Mar Roldán García, M.; García-Nieto, J.; Aldana-Montes, J.F. An ontology-based data integration approach for web analytics in e-commerce. Expert Syst. Appl. 2016, 63, 20–34. [Google Scholar] [CrossRef]

- Singarayan, T.; Jeganathan, A.; Leema, G. Semantic Integration of Classical and Digital Libraries. In Multimedia Information Extraction and Digital Heritage Preservation; World Scientific: Singapore, 2011; pp. 51–65. [Google Scholar] [CrossRef]

- Sobral, T.; Galvao, T.G.; Borges, J. An Ontology-based approach to Knowledge-assisted Integration and Visualization of Urban Mobility Data. Expert Syst. Appl. 2020, 150, 113260. [Google Scholar] [CrossRef]

- del Mar Roldán-García, M.; Uskudarli, S.; Marvasti, N.B.; Acar, B.; Aldana-Montes, J.F. Towards an ontology-driven clinical experience sharing ecosystem: Demonstration with liver cases. Expert Syst. Appl. 2018, 101, 176–195. [Google Scholar] [CrossRef]

- Castells, P.; Foncillas, B.; Lara, R.; Rico, M.; Alonso, J.L. Semantic Web Technologies for Economic and Financial Information Management. In Proceedings of the The Semantic Web: Research and Applications, Crete, Greece, 10–12 May 2004; Bussler, C.J., Davies, J., Fensel, D., Studer, R., Eds.; Springer: Berlin/Heidelberg, Germany, 2004; pp. 473–487. [Google Scholar]

- Bennett, M. The financial industry business ontology: Best practice for big data. J. Bank. Regul. 2013, 14, 255–268. [Google Scholar] [CrossRef]

- Tang, H.; Song, L. Ontologies in financial services: Design and applications. In Proceedings of the International Conference on Business Management and Electronic Information, Guangzhou, China, 13–15 May 2011; Volume 5, pp. 364–367. [Google Scholar] [CrossRef]

- Lara, R.; Cantador, I.; Castells, P. Semantic Web Technologies For The Financial Domain. In The Semantic Web: Real-World Applications from Industry; Cardoso, J., Hepp, M., Lytras, M.D., Eds.; Springer: Boston, MA, USA, 2008; pp. 41–74. [Google Scholar] [CrossRef]

- Bhasuran, B.; Murugesan, G.; Abdulkadhar, S.; Natarajan, J. Stacked ensemble combined with fuzzy matching for biomedical named entity recognition of diseases. J. Biomed. Inform. 2016, 64, 1–9. [Google Scholar] [CrossRef] [PubMed]

- Sehgal, N.; Crampton, A. Information Extraction for Additive Manufacturing Using News Data. In Proceedings of the International Conference on Advanced Information Systems Engineering, Cairo, Egypt, 23–25 August 2019; pp. 132–138. [Google Scholar] [CrossRef]

- Hitzler, P.; Krötzsch, M.; Parsia, B.; Patel-Schneider, P.F.; Rudolph, S. OWL 2 Web Ontology Language Primer, 2nd ed.; Available online: https://www.w3.org/TR/owl2-primer/ (accessed on 19 November 2022).

- Staab, S.; Studer, R. Handbook on Ontologies (International Handbooks on Information Systems); Springer: Berlin/Heidelberg, Germany, 2004. [Google Scholar]

- Gruber, T.R. A translation approach to portable ontology specifications. Knowl. Acquis. 1993, 5, 199–220. [Google Scholar] [CrossRef]

- Ehrlinger, L.; Wöß, W. Towards a Definition of Knowledge Graphs. Semantics 2016, 48, 2. [Google Scholar]

- Bechhofer, S.; Harmelen, F.V.; Hendler, J.A.; Horrocks, I.; McGuinness, D.L.; Patel-Schneider, P.F.; Stein, L.A. OWL Web Ontology Language Reference. Available online: https://www.w3.org/TR/owl-ref/ (accessed on 19 November 2022).

- Haase, P.; Stojanovic, L. Consistent Evolution of OWL Ontologies. In Proceedings of the European Semantic Web Conference, Crete, Greece, 29 May–1 June 2005; Volume 3532, pp. 182–197. [Google Scholar] [CrossRef] [Green Version]

- Fischer-Pauzenberger, C.; Schwaiger, W. The OntoREA Accounting Model: Ontology-based Modeling of the Accounting Domain. Complex Syst. Inform. Model. Q. 2017, 11, 20–37. [Google Scholar] [CrossRef] [Green Version]

- Guizzardi, G.; Wagner, G.; Almeida, J.P.; Andradea Guizzardi, R.S. Towards Ontological Foundations for Conceptual Modeling: The Unified Foundational Ontology (UFO) Story. Appl. Ontol. 2015, 10, 259–271. [Google Scholar] [CrossRef] [Green Version]

- Blums, I.; Weigand, H.H. Towards a Core Ontology for Financial Reporting Information Systems (COFRIS). In Proceedings of the OTM Workshops, Rhodes, Greece, 23–27 October 2017. [Google Scholar]

- Patel, A.; Debnath, N.; Mishra, A.; Jain, S. Covid19-IBO: A Covid-19 Impact on Indian Banking Ontology Along with an Efficient Schema Matching Approach. New Gener. Comput. 2021, 39, 647–676. [Google Scholar] [CrossRef] [PubMed]

- Noy, N. Ontology Development 101: A Guide to Creating Your First Ontology. Available online: https://protege.stanford.edu/publications/ontology_development/ontology101.pdf (accessed on 18 November 2022).

- Hyyrö, H. Bit-Parallel LCS-length Computation Revisited. In Proceedings of the 15th Australasian Workshop on Combinatorial Algorithms (AWOCA), Ballina Beach Resort, NSW, Australia, 7–9 July 2004; pp. 16–27. [Google Scholar]

- Benítez-Hidalgo, A.; Nebro, A.J.; García-Nieto, J.; Oregi, I.; Del Ser, J. jMetalPy: A Python framework for multi-objective optimization with metaheuristics. Swarm Evol. Comput. 2019, 51, 100598. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Abstract Syntax | DL Syntax | |

|---|---|---|

| Operators | ||

| Restrictions | for at least 1 value V from C | |

| for all values V from C | ||

| R is Symmetric | ||

| Class Axioms | A | |

| A |

| Object Properties | Description Logics |

|---|---|

| hasStastementCustomer | ∃ hasStastementCustomer |

| Thing ⊑ Company | |

| ⊤ ⊑ ∀ hasStastementCustomer | |

| StatementsCustomer | |

| Data Properties | Description logics |

| businessName | ∃ businessName Datatype Literal |

| ⊑ Company ⊤ ⊑ ∀ businessName | |

| Datatype string | |

| companyId | ∃ companyId Datatype Literal ⊑ Company |

| ⊤ ⊑ ∀ companyId Datatype int | |

| corporationId | ∃ corporationId Datatype Literal |

| ⊑ Company ⊤ ⊑ ∀ corporationId | |

| Datatype int | |

| currencyCode | ∃ currencyCode |

| Datatype Literal ⊑ Company | |

| ⊤ ⊑ ∀ currencyCode Datatype string | |

| fiscalId | ∃ fiscalId Datatype Literal ⊑ Company |

| ⊤ ⊑ ∀ fiscalId Datatype string |

| Data Properties | Description Logics |

|---|---|

| businessName | ∃ businessName Datatype Literal ⊑ Customer |

| ⊤ ⊑ ∀ businessName Datatype string | |

| customerId | ∃ customerId Datatype Literal ⊑ Customer |

| ⊤ ⊑ ∀ customerId Datatype int | |

| fiscalId | ∃ fiscalId Datatype Literal ⊑ Company |

| ⊤ ⊑ ∀ fiscalId Datatype string |

| Object Properties | Description Logics |

|---|---|

| itemHasCompany | ∃ itemHasCompany Thing ⊑ Item |

| ⊤ ⊑ ∀ itemHasCompany Company | |

| itemHasCustomer | ∃ itemHasCustomer Thing ⊑ Item |

| ⊤ ⊑ ∀ itemHasCustomer Customer | |

| Data properties | Description logics |

| indicator | ∃ indicator Datatype Literal ⊑ Item |

| ⊤ ⊑ ∀ indicator Datatype string | |

| itemAmount | ∃ itemAmount Datatype Literal ⊑ Item |

| ⊤ ⊑ ∀ itemAmount Datatype decimal | |

| itemCurrencyAmt | ∃ itemCurrencyAmt Datatype Literal ⊑ Item |

| ⊤ ⊑ ∀ itemCurrencyAmt Datatype decimal | |

| itemIssueDate | ∃ itemIssueDate Datatype Literal ⊑ Item |

| ⊤ ⊑ ∀ itemIssueDate Datatype dateTime | |

| itemMaturityDate | ∃ itemMaturityDate Datatype Literal ⊑ Item |

| ⊤ ⊑ ∀ itemMaturityDate Datatype dateTime | |

| currencyCode | ∃ currencyCode Datatype Literal ⊑ Item |

| ⊤ ⊑ ∀ currencyCode Datatype string | |

| itemId | ∃ itemId Datatype Literal ⊑ Item |

| ⊤ ⊑ ∀ itemId Datatype int |

| Object Properties | Description Logics |

|---|---|

| statementHasOffice | ∃ statementHasOffice Thing ⊑ Statement |

| ⊤ ⊑ ∀ statementHasOffice Office | |

| Data properties | Description logics |

| accountNumber | ∃ accountNumber Datatype Literal ⊑ Statement |

| ⊤ ⊑ ∀ accountNumber Datatype string | |

| statementAmount | ∃ statementAmount Datatype Literal |

| ⊑ Statement | |

| ⊤ ⊑ ∀ statementAmount Datatype int | |

| statementBeneficiary | ∃ statementBeneficiary Datatype |

| Literal ⊑ Statement | |

| ⊤ ⊑ ∀ statementBeneficiary Datatype string | |

| statementCurrency | ∃ statementCurrency Datatype Literal |

| ⊑ Statement | |

| ⊤ ⊑ ∀ statementCurrency Datatype string | |

| statementValueDate | ∃ statementValueDate Datatype |

| Literal ⊑ Statement | |

| ⊤ ⊑ ∀ statementValueDate Datatype dateTime | |

| concept | ∃ concept Datatype Literal ⊑ Statement |

| ⊤ ⊑ ∀ concept Datatype string |

| Object Properties | Description Logics |

|---|---|

| participating | ∃ participating Thing ⊑ StatementsCustomer |

| ⊤ ⊑ ∀ participating AccountObj | |

| Data properties | Description logics |

| customerBirthDate | ∃ customerBirthDate Datatype |

| Literal ⊑ StatementsCustomer | |

| ⊤ ⊑ ∀ customerBirthDate Datatype dateTime | |

| customerDocument | ∃ customerDocument Datatype |

| Literal ⊑ StatementsCustomer | |

| ⊤ ⊑ ∀ customerDocument Datatype string | |

| customerNames | ∃ customerNames Datatype |

| Literal ⊑ StatementsCustomer | |

| ⊤ ⊑ ∀ customerNames Datatype string | |

| address | ∃ address Datatype Literal |

| ⊑ StatementsCustomer ⊤ ⊑ ∀ address | |

| Datatype string | |

| ∃ email Datatype Literal ⊑ StatementsCustomer | |

| ⊤ ⊑ ∀ email Datatype string | |

| phone | ∃ phone Datatype Literal ⊑ StatementsCustomer |

| ⊤ ⊑ ∀ phone Datatype string |

| Step | Package | Language | Description | Reference |

|---|---|---|---|---|

| OBO Ontology | Protégé | OWL | Define Ontology | https://protege.stanford.edu/ (accessed on 25 November 2022) |

| JSON Mapping | RDFLib | Python | Translate JSON files and create RDF data | https://rdflib.dev/ (accessed on 24 November 2022) |

| CSV Mapping | RDFLib | Python | Translate CSV files and create RDF data | https://rdflib.dev/ (accessed on 24 November 2022) |

| RDF Repository | Stardog | SPARQL | Store and query the RDF data | https://www.stardog.com/ (accessed on 22 November 2022) |

| Fuzzy Similarity Search | RapidFuzz | Python | Calculate the strings similarity | https://maxbachmann.github.io/RapidFuzz/ (accessed on 26 November 2022) |

| Genetic Algorithm | jMetalPy | Python | Calculate the subset sum of the amounts | https://jmetalpy.readthedocs.io/ (accessed on 21 November 2022) |

| Inference | Pellet | Java | Reasoning with the elements and rules defined in the ontology | https://www.stardog.com/ (accessed on 22 November 2022) |

| SPARQL | Result |

|---|---|

| |

| |

| Semantic Attribute | Semantic Matching 1 | Semantic Matching 2 |

|---|---|---|

| URI Item | itemacffa | item55214 |

| URI Statement | statement55d2j | statementd27d4 |

| Item Descriptor | EXAMPLE COMPANY, S.L. | SERVICE FRANCE S.L.U. |

| Statement Descriptor | A FAVOR DE EXAMPLE COMPANY S.L | SERVICE FRANCE, SL |

| Score | 95 | 88 |

| Semantic Attribute | Semantic Matching 1 | Semantic Matching 2 |

|---|---|---|

| URI Item | itemb0e44 | item40f83 |

| URI Statement | statement14984 | statement41d07 |

| Item Descriptor | 1, EXP-JCR-100, CLIENT X | 1, S07220G, CLIENT Y |

| Statement Descriptor | PETER, FACT 22000-543 | CONTRACT 564, DOSSIER RISK |

| Amount | 241.16 | 5596.00 |

| Diff Days | −10 | 20 |

| Semantic Attribute | Subset Sum Result | |

|---|---|---|

| URI Item | item23dcb | item23dcb |

| URI Statement | statement335ad | statement5eb2b |

| Item Descriptor | HAPPY FRIENDS, S.A | HAPPY FRIENDS, S.A |

| Statement Descriptor | HAPPY FRIENDS S.A. | HAPPY FRIENDS |

| Score | 98 | 95 |

| Item Currency Amt | 1039.88 | 1039.88 |

| Statement Amount | 800.00 | 239.88 |

| Currency Code | EUR | EUR |

| Diff Days | 1 | 1 |

| Semantic Attribute | Subset Sum Result | |

|---|---|---|

| URI Item | item24b8b | item3069d |

| URI Statement | statement55d2d | statement55d2d |

| Item Descriptor | HAPPY FRIENDS S.A | HAPPY FRIENDS, S.A |

| Statement Descriptor | HAPPY FRIENDS | HAPPY FRIENDS, S.A. |

| Score | 98 | 95 |

| Item Currency Amt | 16637.50 | 5275.60 |

| Statement Amount | 21913.10 | 21913.10 |

| Currency Code | EUR | EUR |

| Diff Days | 1 | 1 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Paneque, M.; Roldán-García, M.d.M.; García-Nieto, J. A Semantic Model for Enhancing Data-Driven Open Banking Services. Appl. Sci. 2023, 13, 1447. https://0-doi-org.brum.beds.ac.uk/10.3390/app13031447

Paneque M, Roldán-García MdM, García-Nieto J. A Semantic Model for Enhancing Data-Driven Open Banking Services. Applied Sciences. 2023; 13(3):1447. https://0-doi-org.brum.beds.ac.uk/10.3390/app13031447

Chicago/Turabian StylePaneque, Manuel, María del Mar Roldán-García, and José García-Nieto. 2023. "A Semantic Model for Enhancing Data-Driven Open Banking Services" Applied Sciences 13, no. 3: 1447. https://0-doi-org.brum.beds.ac.uk/10.3390/app13031447