Complexity Economics in a Time of Crisis: Heterogeneous Agents, Interconnections, and Contagion

, , ,

, , ,  and

and

Abstract

:1. Introduction

1.1. The Economics of Heterogeneity and Interconnections

… technological trajectories are a cumulative process of searching for “new ways to do things”, providing the reader with a framework to explain emerging behaviors such as lock-ins, ‘anti-commons’ problems… Since the 1960s, innovations began to be viewed as multi-interactive phenomenon, which entails a cumulative process between different agents and institutions, a fact ignored by standard economics… Once the cumulative process is understood, it is impossible to deny that there are differences in the ability of distinct firms to accumulate knowledge.

1.2. The Household Level: Theory and Simulation

Then an event—perhaps a change in government policy, an unexplained failure of a firm previously thought to have been successful—occurs that leads to a pause in the increase in asset prices. Soon, some of the investors who had financed most of their purchases with borrowed money become distress sellers of the real estate or the stocks because the interest payments on the money borrowed to finance their purchases are larger than the investment income on the assets. The prices of these assets decline below their purchase price and now the buyers are ‘under water’—the amount owed on the money borrowed to finance the purchase of these assets is larger than their current market value.

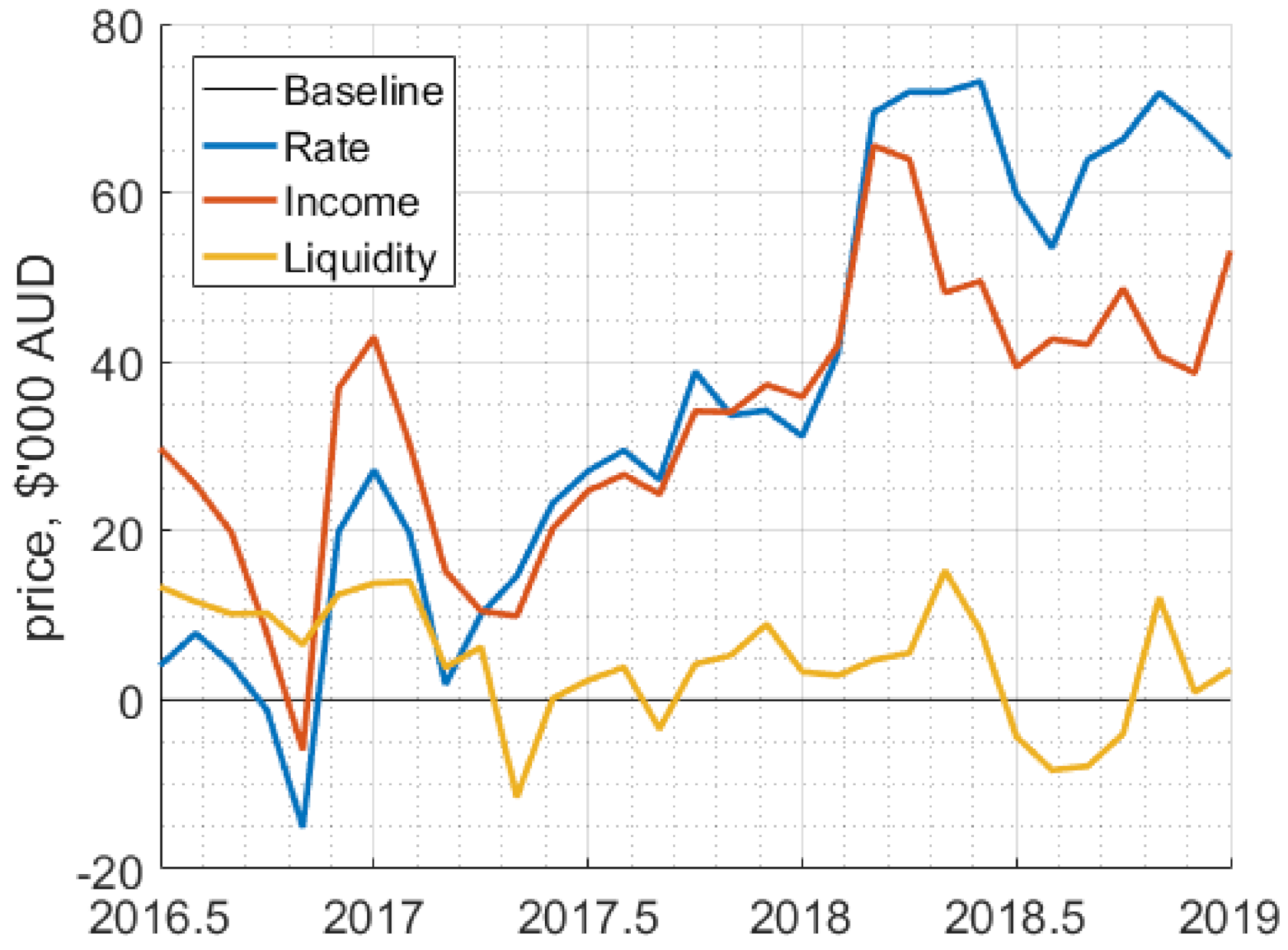

Increased housing market activity was driven by an expansive monetary policy and support through government policies such as Homebuilder and other state specific initiatives, as well as pent up demand (due to lower activity during the June quarter [2020] COVID-19 lockdown period). As auctions and open home inspections picked up in September quarter (with the easing of social distancing measures), greater demand than there was housing stock on the market saw property prices rebound

1.3. Financial Markets and Systemic Risks

1.4. Trade Networks: Internal and External Trade in Value Added

1.5. Business Sector Analysis

One reason for such acceleration in megaprojects can be gleaned from the projections of infrastructure to meet the world’s ever-increasing needs for economic growth and improvements. McKinsey (Garemo, Matzinger, & Palter, 2015) estimates that the world needs to spend about US$57 trillion on infrastructure by 2030 to keep up with the expected GDP growth. The Organisation for Economic Co-operation and Development (OECD) estimates that ‘global infrastructure investment needs of US$6.3 trillion per year over the period of 2016–2030 to support growth and development’, which exceeds the figure proposed by McKinsey.

1.6. The Structure of the Article

2. Periods of Financial Distress in an Agent Based Model

2.1. The Theoretical Framework

- Asset prices are updated using Equation (3),

- Agents realize profit/losses and update their wealth,

- Agents compute a new expected price.

2.2. Simulation Results

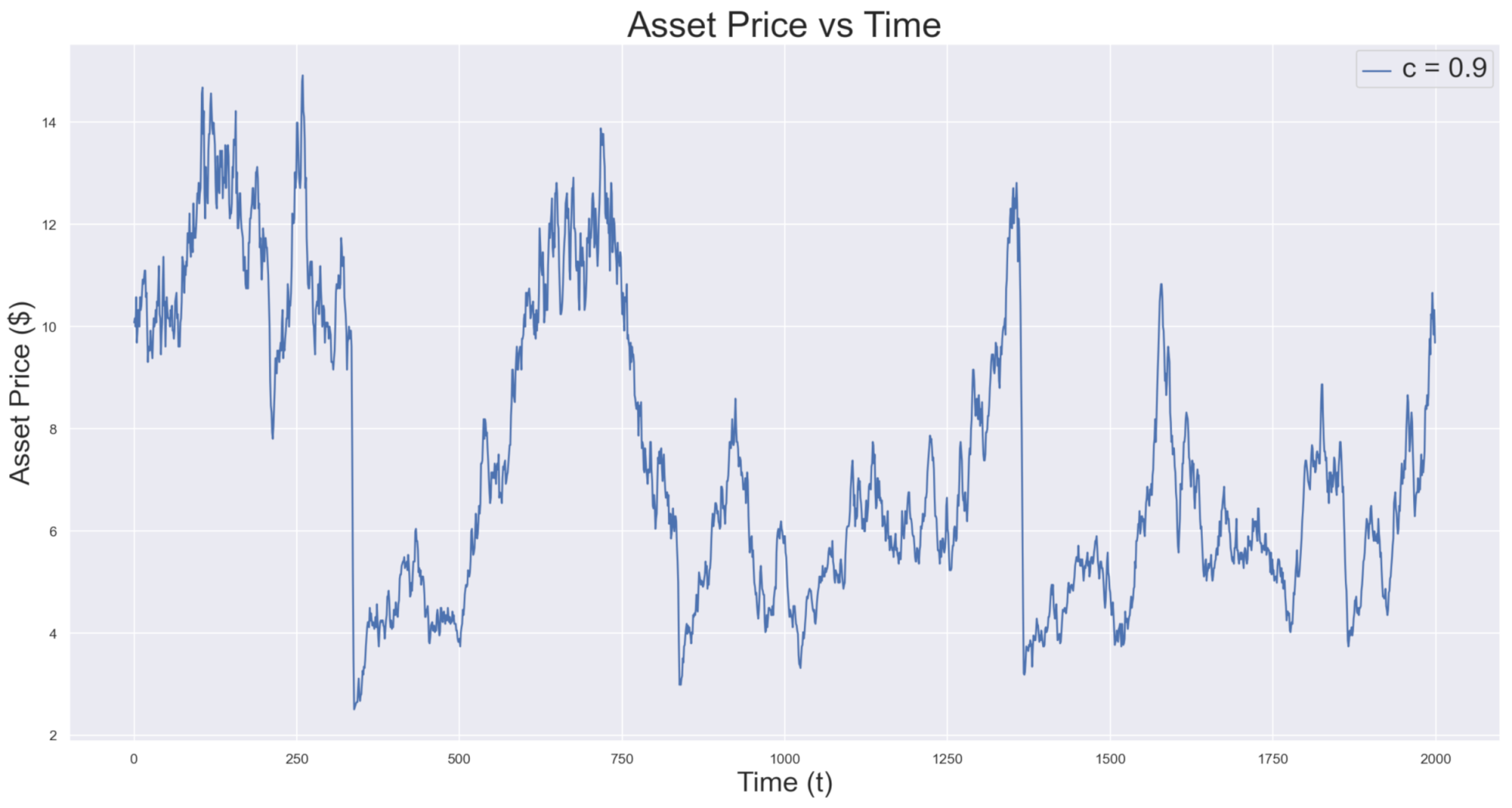

- A bubble characterized by a PFD is produced only when transaction costs are sufficiently high, see Figure 1. In the absence of high transaction costs no crashes are observed in the simulations.

- High financial costs cause a pattern of crashes in Figure 2. As a hypothesis for the cause of financial distress, high transaction costs have the drawback of causing repeatable patterns that are may not be realistic.

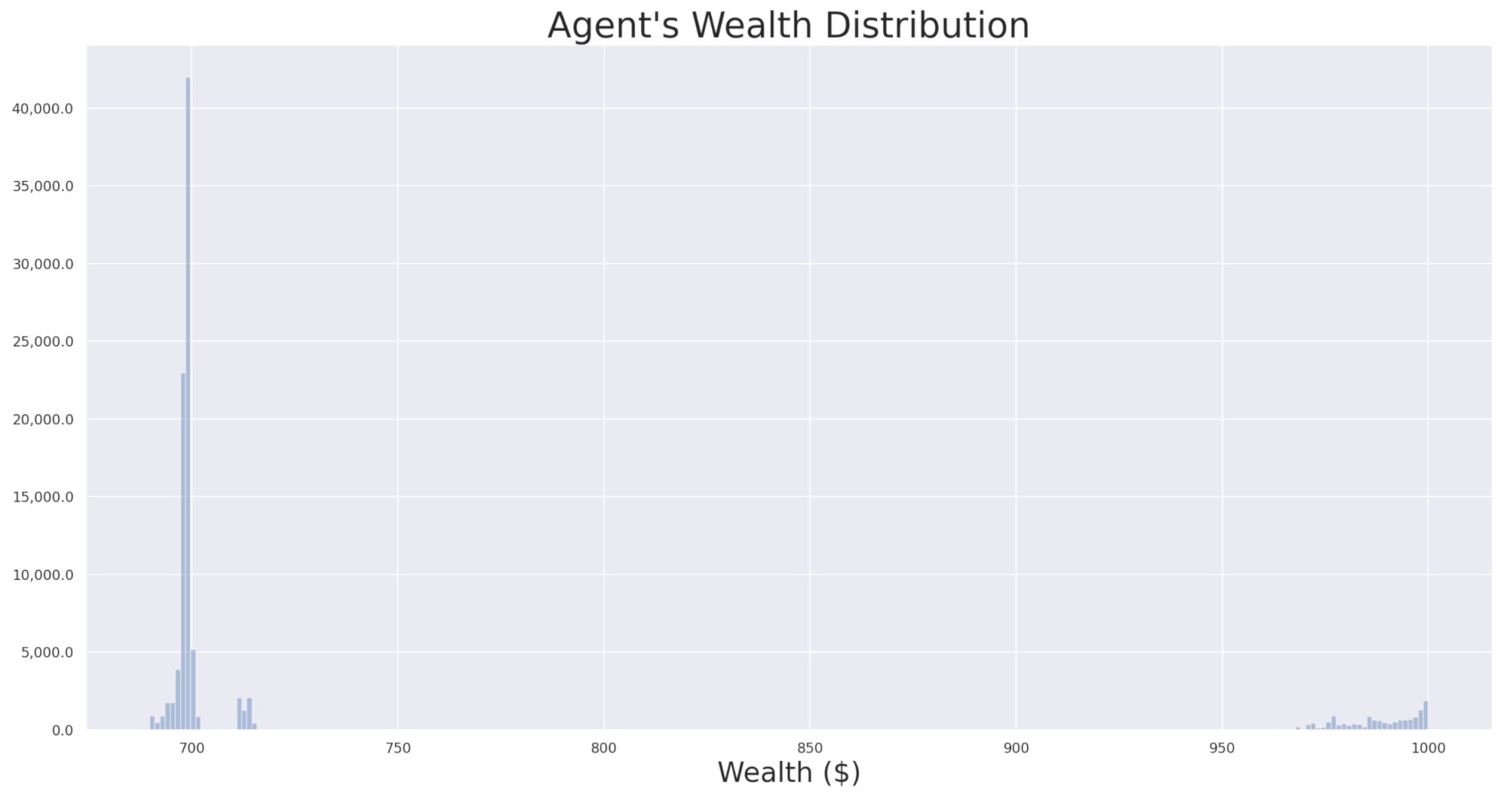

- The evolution of the wealth and the distribution of the agents explain the bubble (Figure 3). We can see two densities of wealth that correspond to the beginning of the simulation and right before the crash. It demonstrates that financial distress seems to be correlated with the occurrence of shocks.

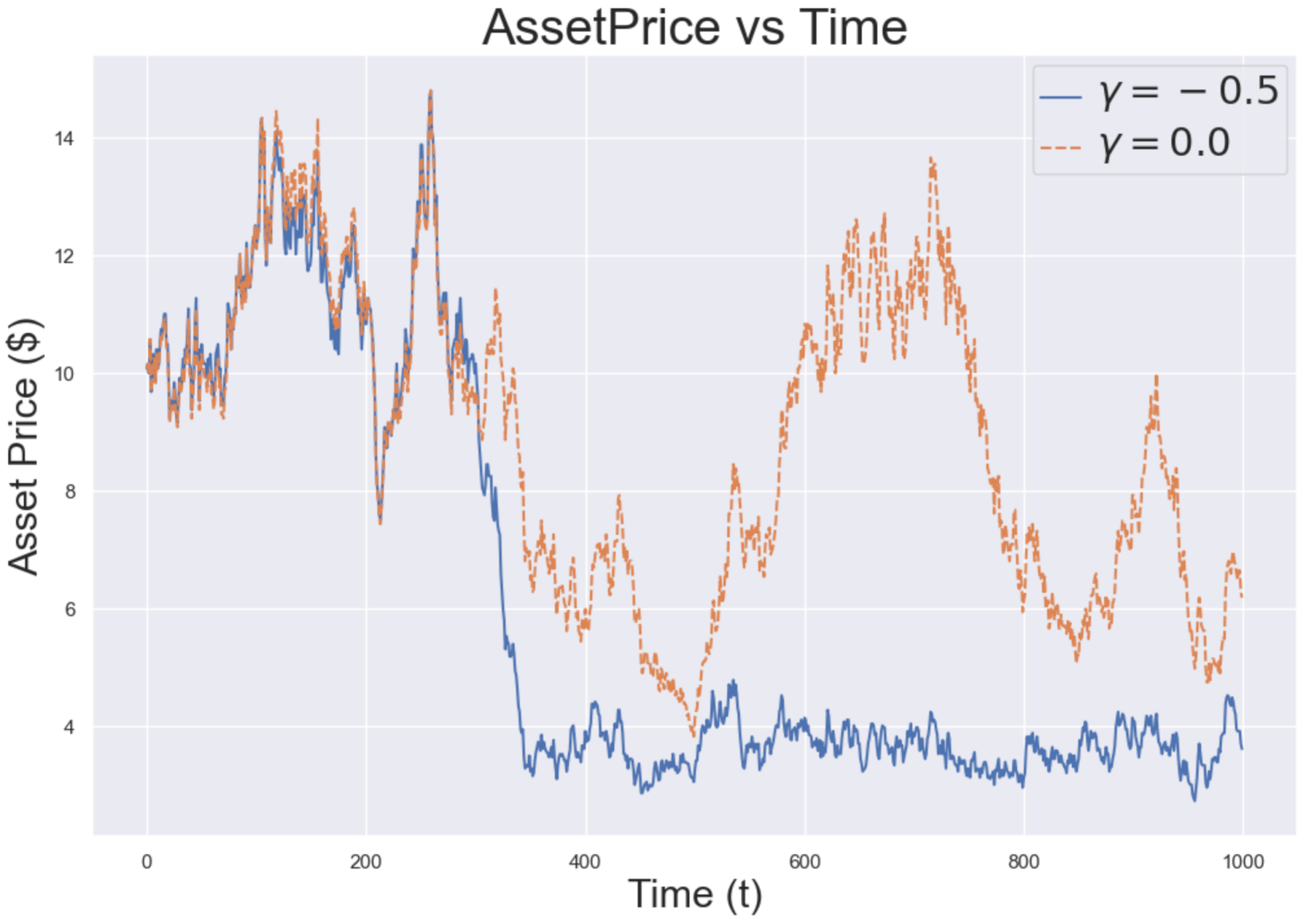

- Changes in the herding factor, J, affect the amplitude of the bubble, making social interaction an important component of how financial contagion spreads and how the shock ultimately unfolds into a crisis.

2.3. Remarks

3. Trading Houses: An Agent-Based Analysis of Stressed Markets

3.1. Simulation Results

3.2. Simple versus More Complex Agent-Based Models

4. Fluctuations in Equity Markets at Crises Points

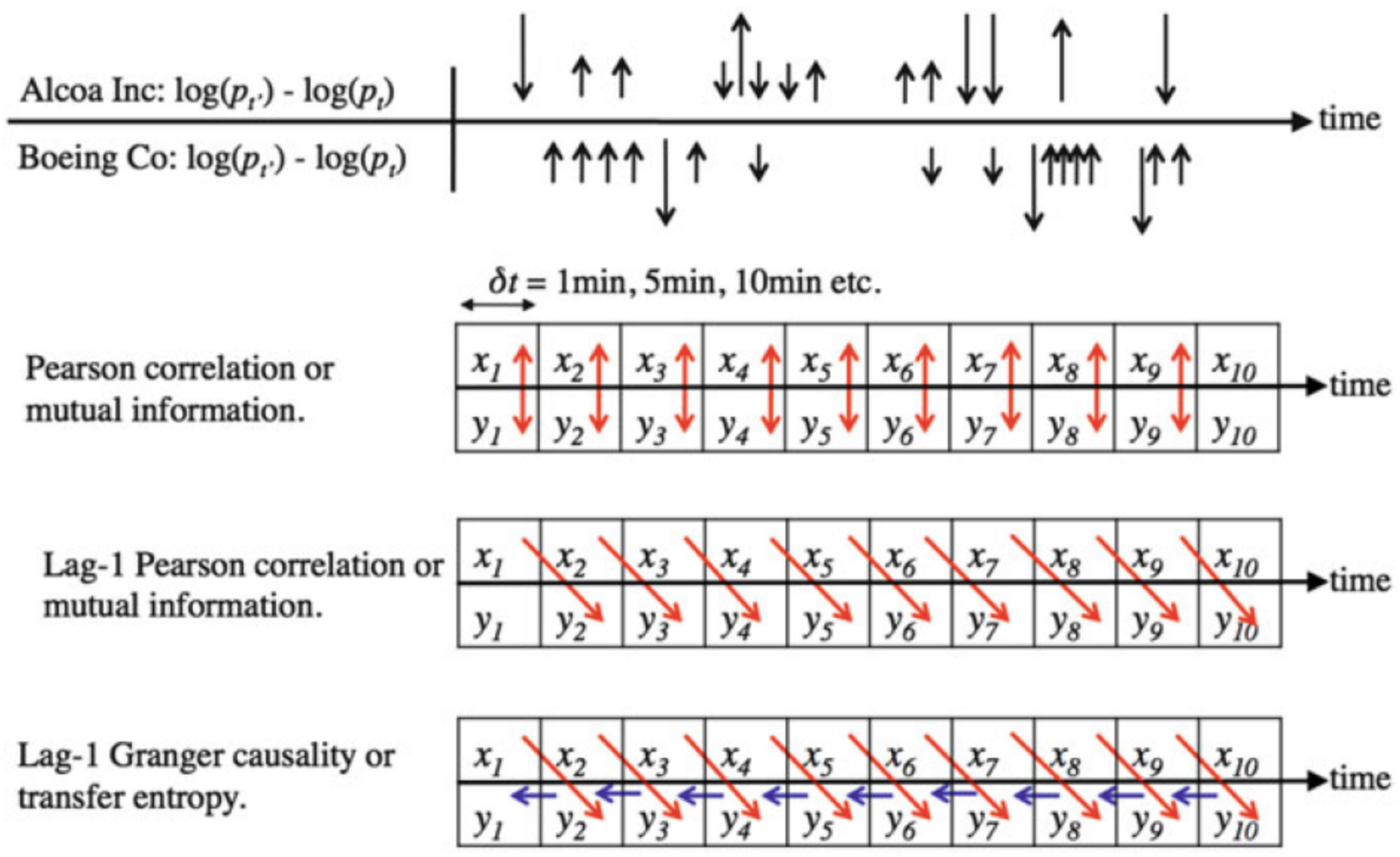

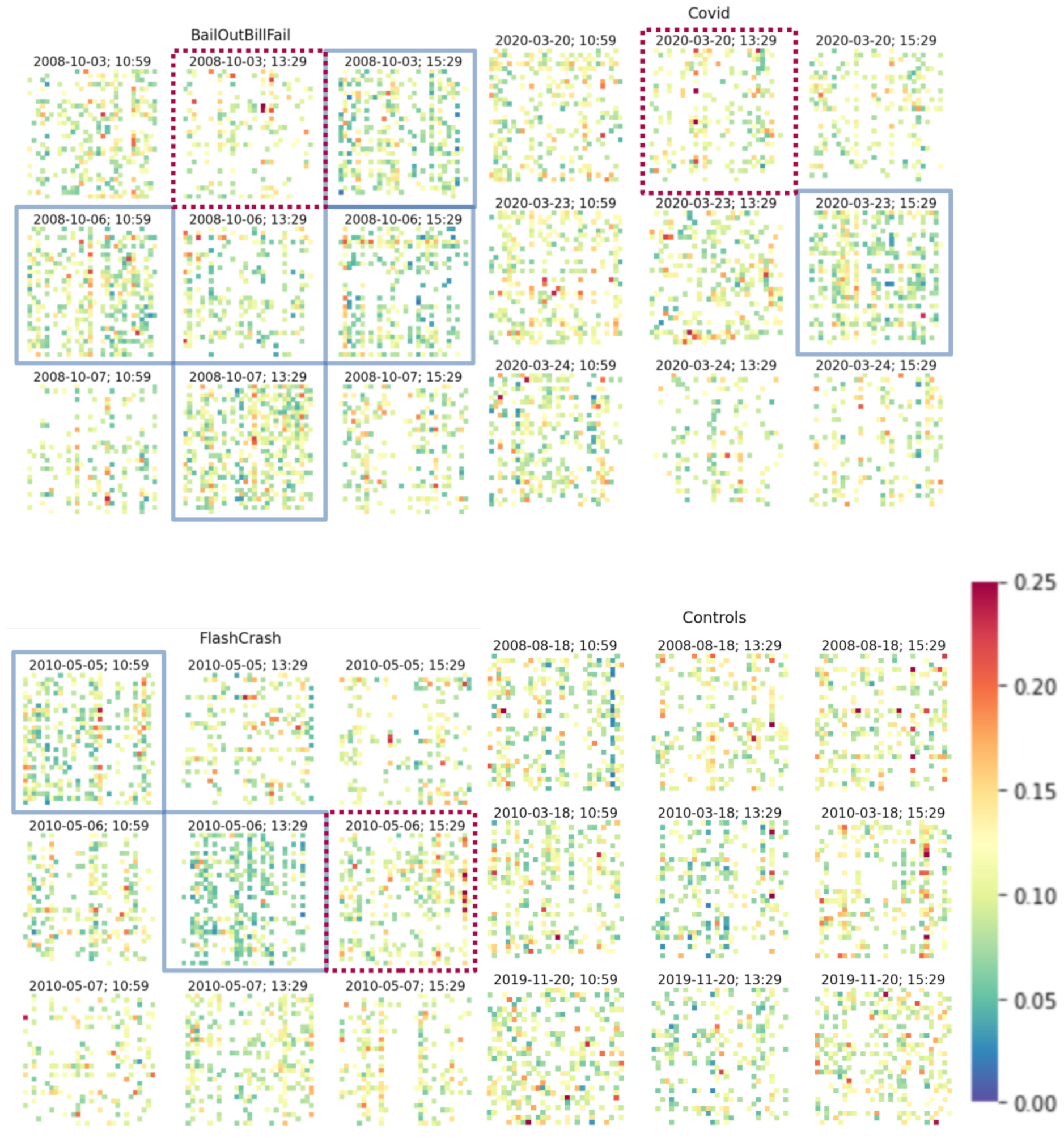

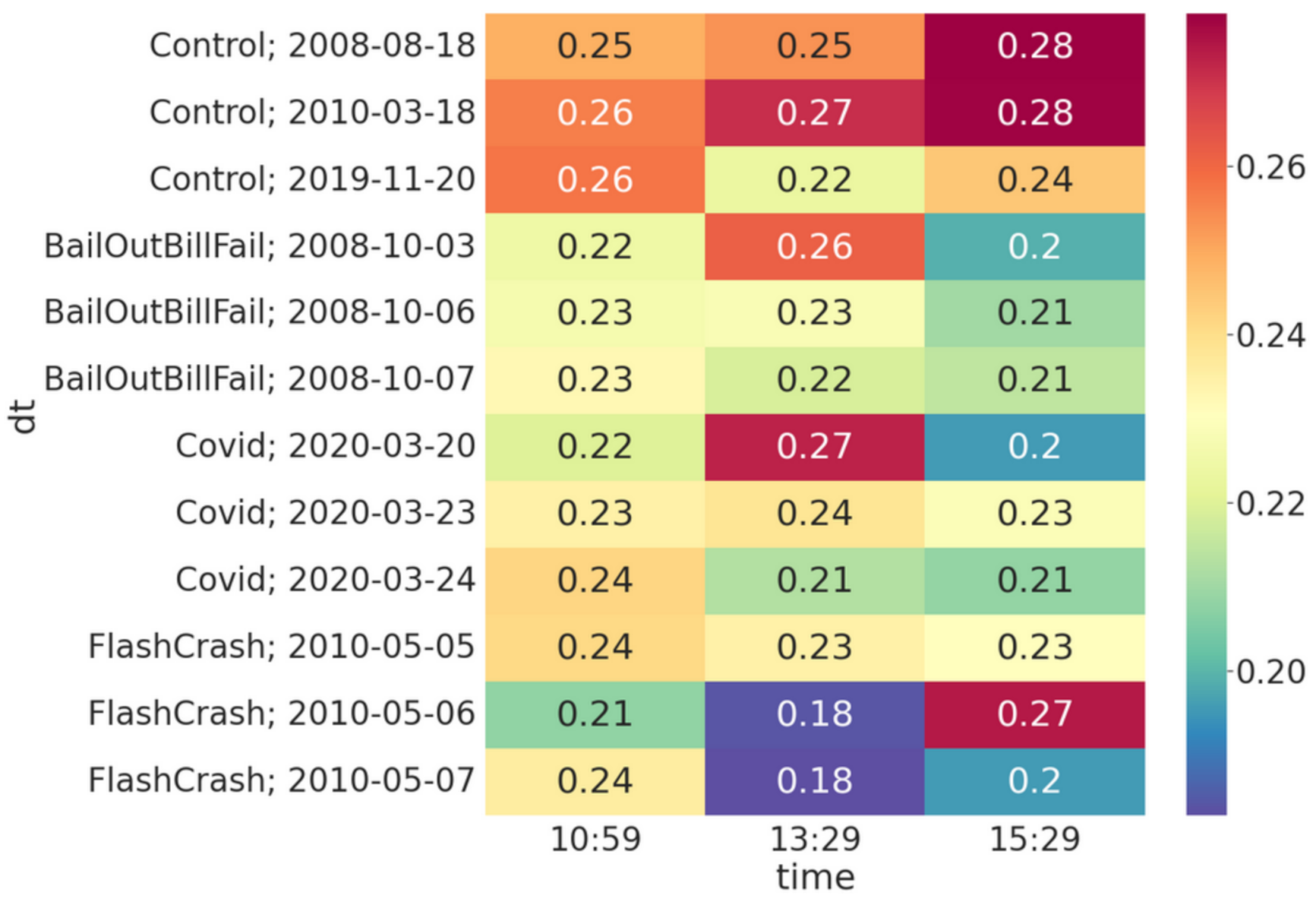

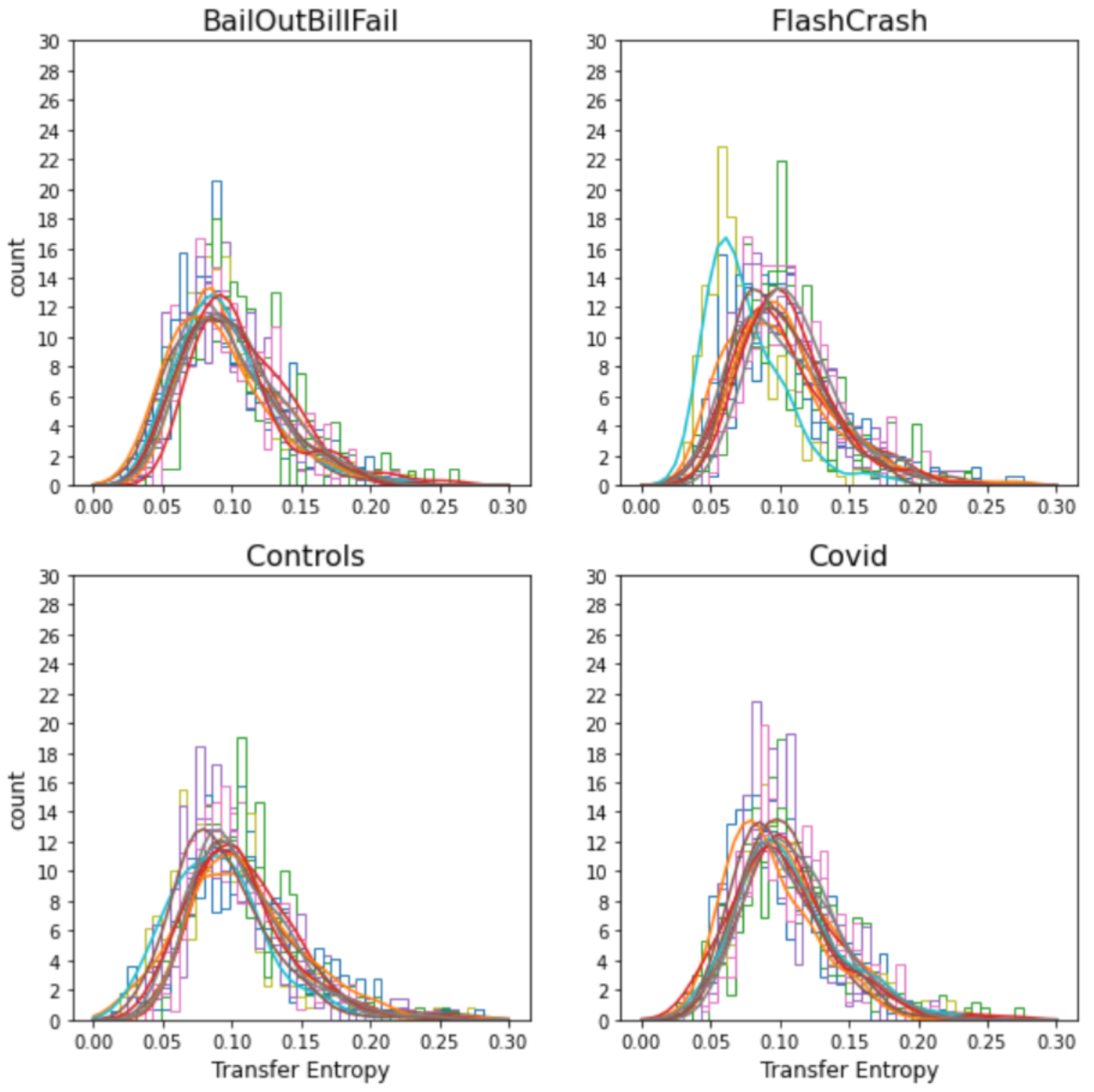

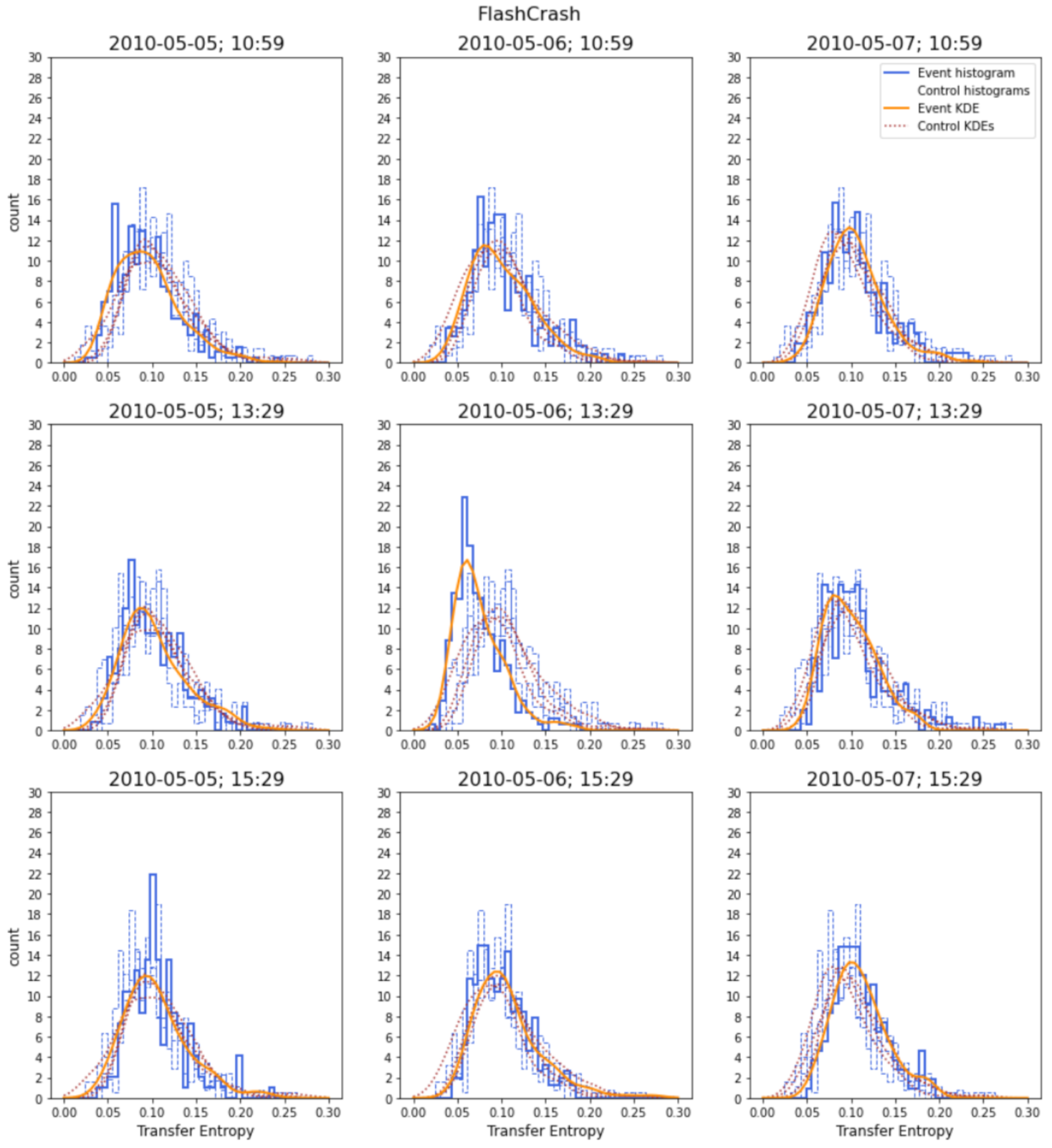

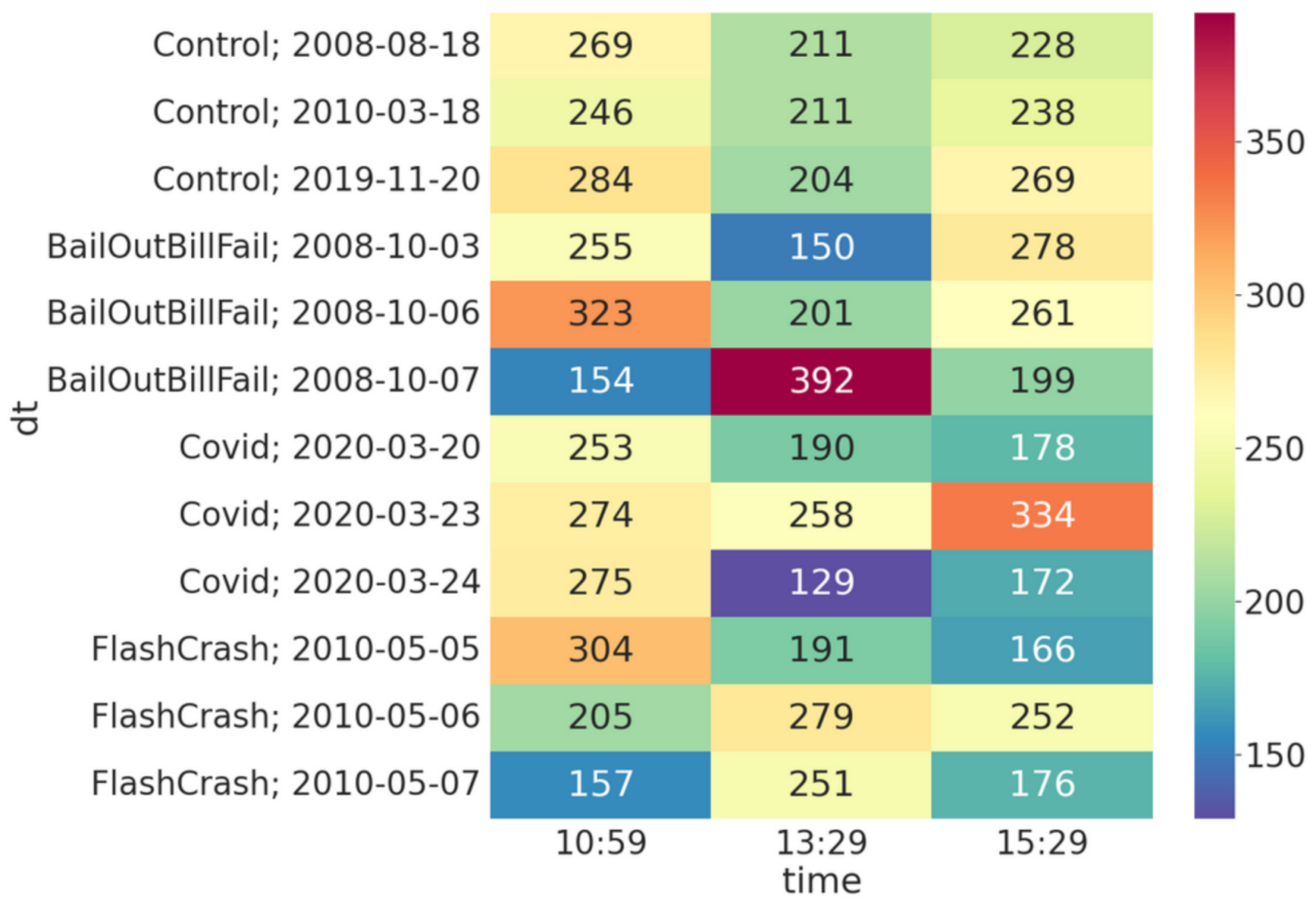

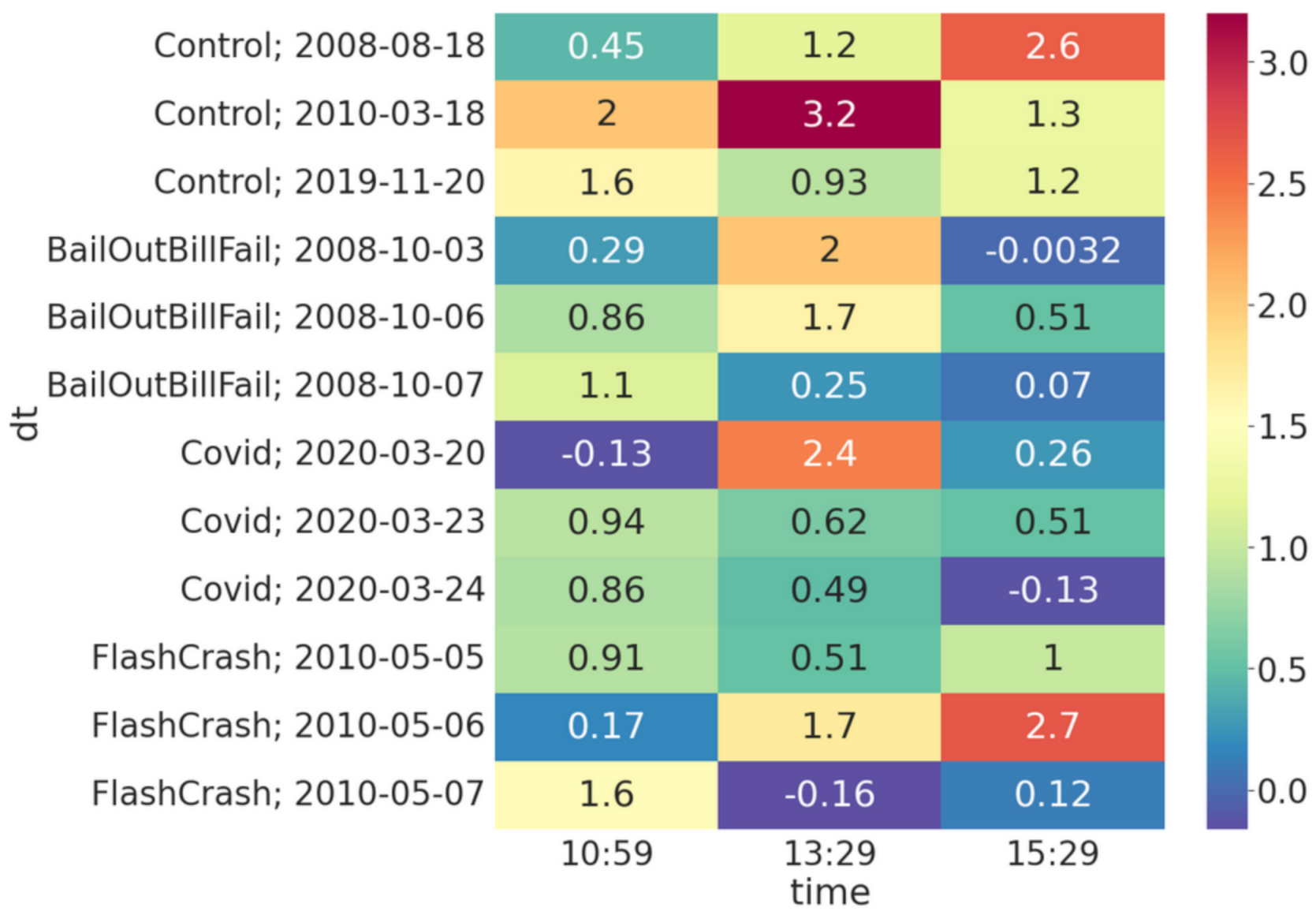

4.1. Analysis Using Transfer Entropy for the DJIA Market Shocks

4.2. Remarks

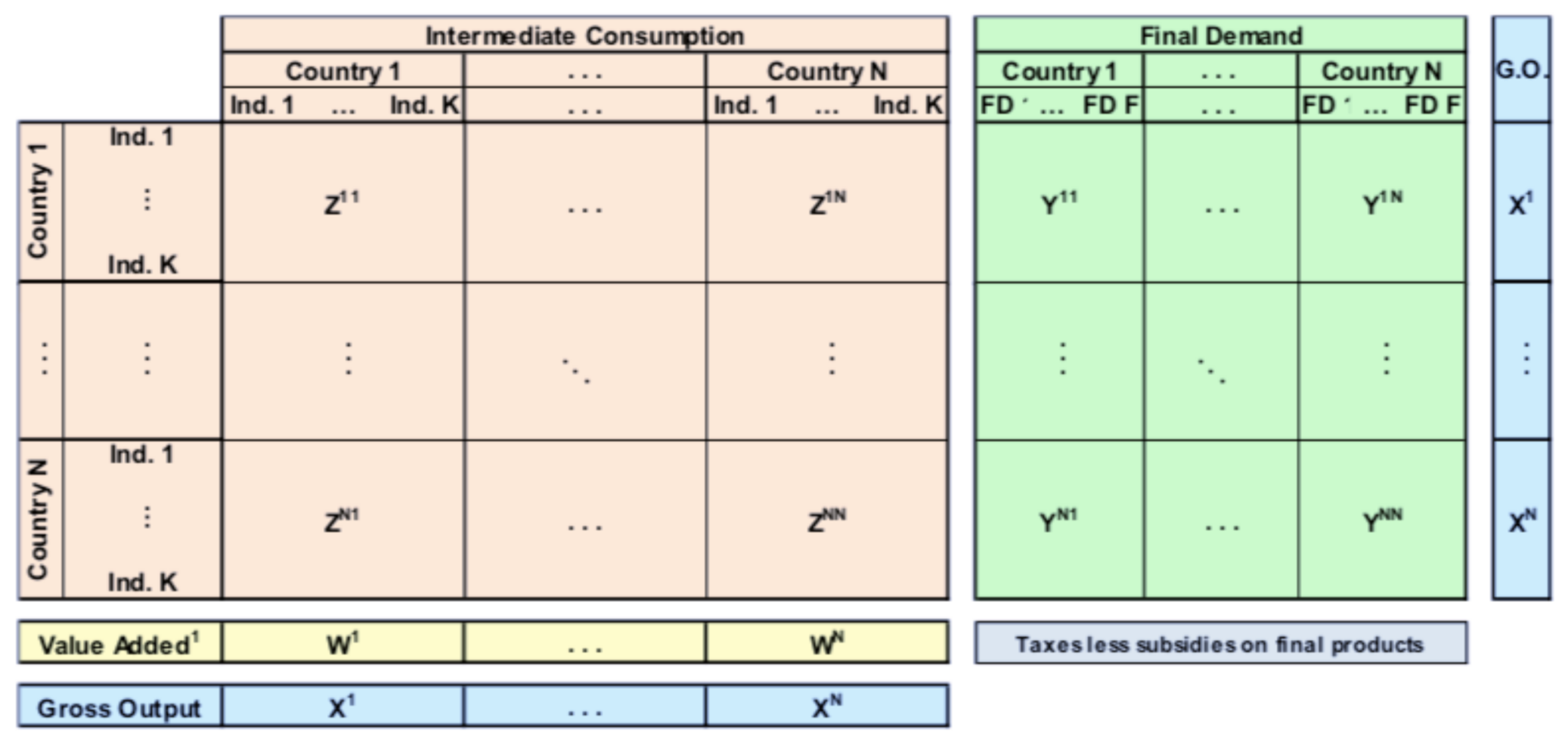

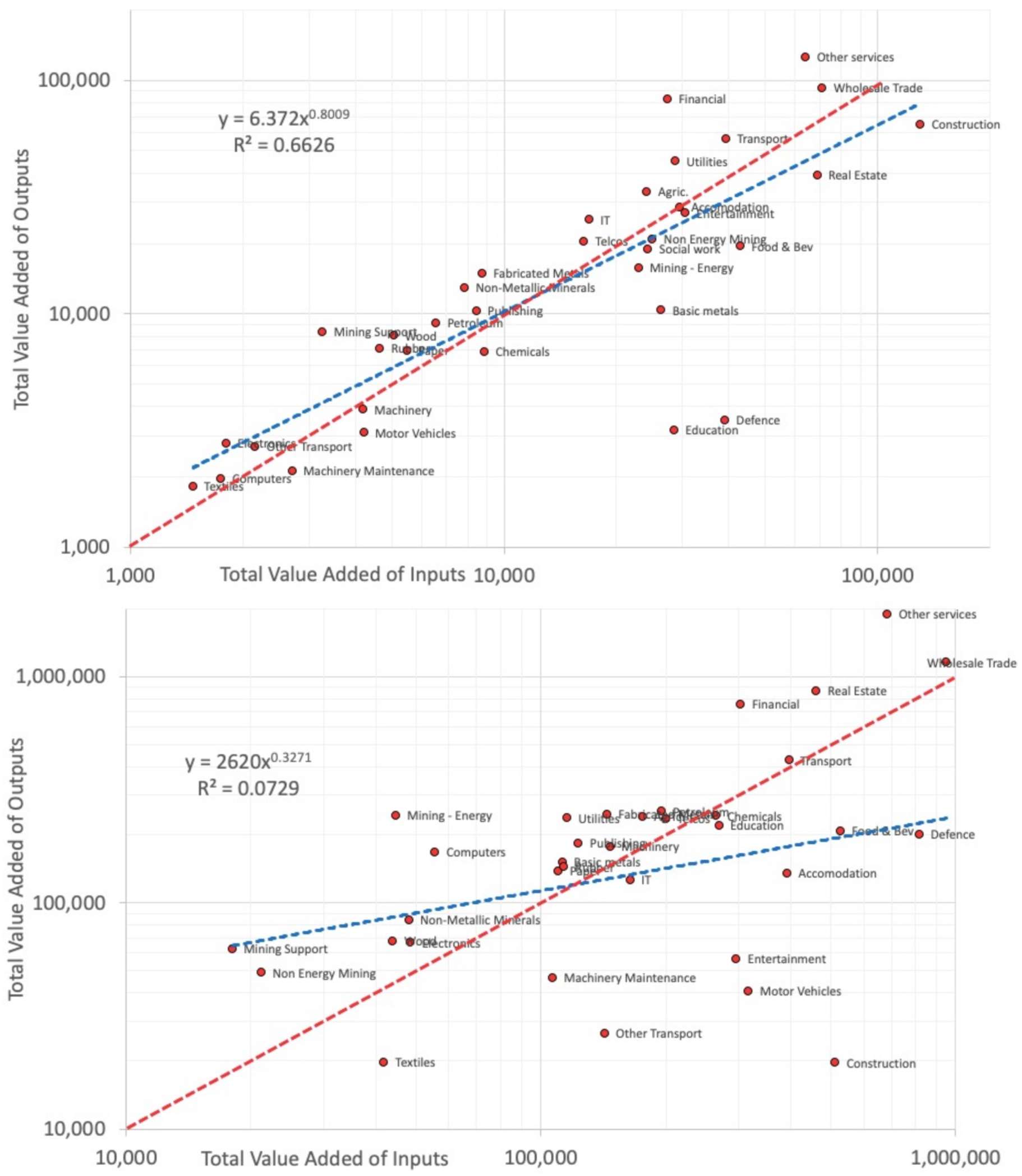

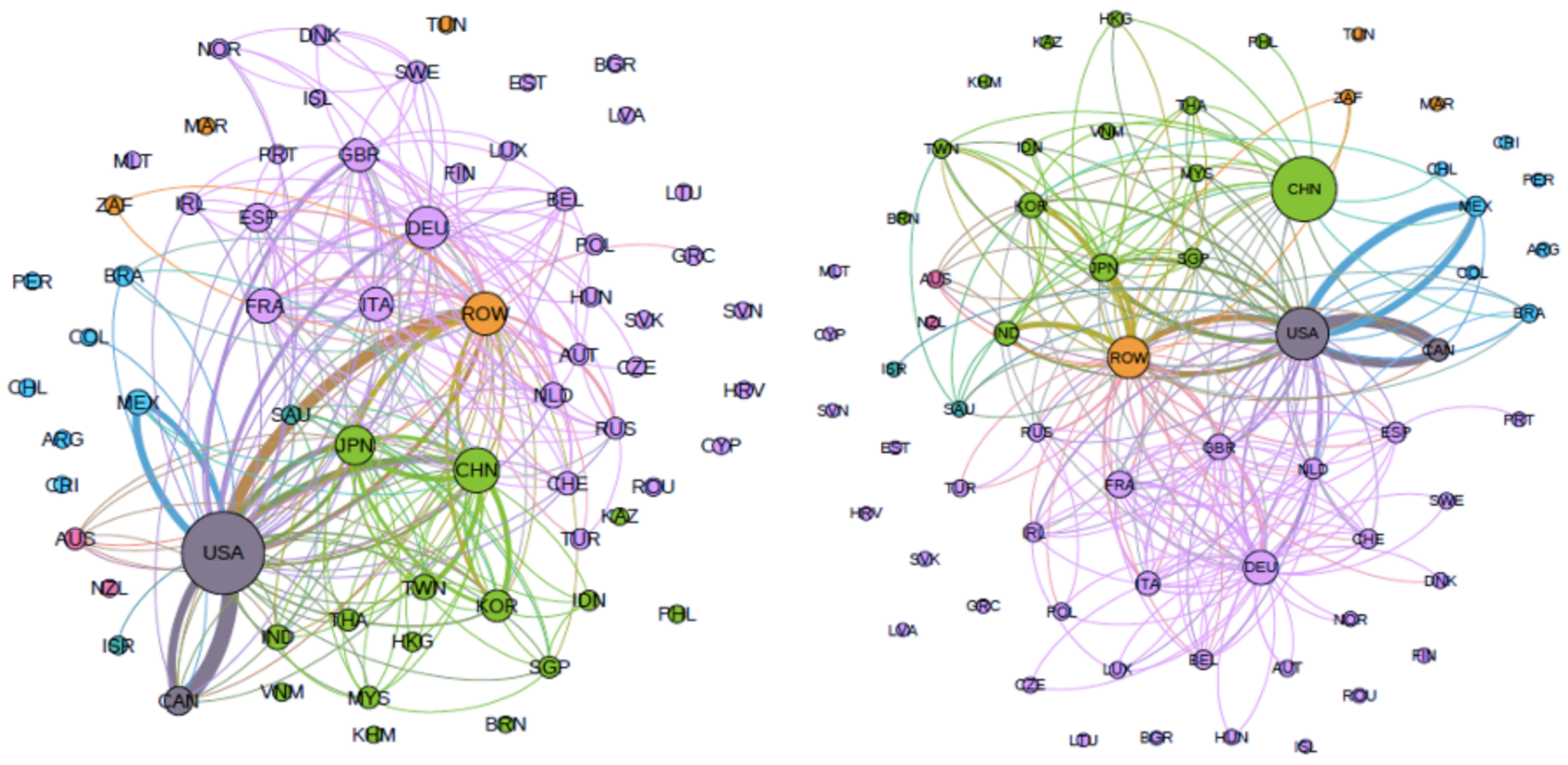

5. National and International Trade in Value Added

5.1. Value-Added Trade Networks

- supply-side reductions due to the closure of non-essential industries (which can be captured in part by the intermediate value added in TiVA tables), and

- demand-side changes caused by individuals immediate response to the pandemic, such as reduced demand for goods or services that are likely to place people at risk of infection (which is captured by final demand in TiVA tables).

5.2. Features of Australia’s Internal Trade Patterns

5.3. Predicting the Impacts of Exogenous Shocks

5.4. Features of Global Trade Patterns

5.5. Remarks

6. Project Economics and the Knock-On Macro-Effects of Their Delay, Cancellation, or Failure

6.1. Mega-Projects and the Economy

… such large sums of money ride on the success of megaprojects that company balance sheets and even government balance-of-payments accounts can be affected for years by the outcomes. The success of these projects is so important to their sponsors that firms and even governments can collapse when they fail.

6.2. COVID-19 at the Project Level

6.3. Remarks

7. Conclusions

Economic Research on a Global Scale

… fully vaccinating 50% of the population would have a larger effect than simultaneously applying all forms of containment policies in their most extreme form (closure of workplaces, public transport and schools, restrictions on travel and gatherings and stay-at-home requirements). For a typical OECD country, relaxing existing containment policies would be expected to raise GDP by about 4–5%.

… the poor and the young, especially those with children, should have received a larger [economic stimulus] check, which is an allocation that would have allowed for the same stimulus effect at half the cost of the actual allocation [as delivered by the US government].

- Stock markets initially ignored the pandemic (until 21 February), before reacted [sic] strongly to the growing number of infected people (23 February to 20 March), while volatility surged and concerns about the pandemic arose; following the intervention of central banks (23 March to 30 April), however, shareholders no longer seemed troubled by news of the health crisis, and prices rebound all around the world.

- Country-specific characteristics appear to have had no influence on stock market response.

- Investors were sensitive to the number of COVID-19 cases in neighbouring but mostly wealthy countries.

- Credit facilities and government guarantees, lower policy interest rates, and lockdown measures mitigated the decline in domestic stock prices

We also show that lockdowns can substantially reduce COVID-19 infections, especially if they are introduced early in a country’s epidemic. Despite involving short-term economic costs, lockdowns may thus pave the way to a faster recovery by containing the spread of the virus and reducing voluntary social distancing. [They were also able to show that the effect] … entail[s] decreasing marginal economic costs but increasing marginal benefits in reducing infections.

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | https://atlas.cid.harvard.edu, accessed on 13 October 2021. |

| 2 | https://oec.world/en/resources/about, accessed on 13 October 2021. |

| 3 | Also see Australian households and businesses amass $200 billion in savings during COVID-19 pandemic 9 News, 14 January 2021, and COVID-19 hit many Australians hard, but there were winners in the pandemic economy, ABC, 23 February 2021. |

| 4 | “Australia’s house prices soar to record highs over 2020”, https://www.domain.com.au/news/australias-house-prices-soar-to-record-highs-over-2020-1020487/, accessed on 13 October 2021. |

| 5 | A method for simplifying networks by using the minimum number of maximally weighted edges needed to connect all nodes without forming loops. |

| 6 | https://www.oecd.org/sti/ind/tiva/TiVA2018_Indicators_Guide.pdf, accessed on 13 October 2021. |

| 7 | https://www.oecd.org/sti/ind/measuring-trade-in-value-added.htm, accessed on 13 October 2021. |

| 8 | China’s and Mexico’s sub-classifications are aggregated (i.e., CNH, CN1, CN2, etc.). |

| 9 | See their website: https://covid.econ.cam.ac.uk, accessed on 13 October 2021. |

| 10 | https://www.reuters.com/world/us/us-house-approves-715-bln-infrastructure-bill-2021-07-01/, accessed on 13 October 2021. |

References

- Arthur, W.B. Complexity economics. In Complexity and the Economy; Oxford University Press: Oxford, UK, 2013. [Google Scholar]

- Hausmann, R.; Hidalgo, C.A.; Bustos, S.; Coscia, M.; Simoes, A. The Atlas of Economic Complexity: Mapping Paths to Prosperity; MIT Press: Cambridge, MA, USA, 2014. [Google Scholar]

- Hidalgo, C.A.; Klinger, B.; Barabási, A.L.; Hausmann, R. The product space conditions the development of nations. Science 2007, 317, 482–487. [Google Scholar] [CrossRef] [Green Version]

- Hidalgo, C.A.; Hausmann, R. The building blocks of economic complexity. Proc. Natl. Acad. Sci. USA 2009, 106, 10570–10575. [Google Scholar] [CrossRef] [Green Version]

- Turrell, A. Agent-based models: Understanding the economy from the bottom up. Bank Engl. Q. Bull. 2016, 4, 173–188. [Google Scholar]

- MacGee, J.J.; Pugh, T.M.; See, K. The Heterogeneous Effects of COVID-19 on Canadian Household Consumption, Debt and Savings; Technical Report; Bank of Canada: Ottawa, ON, Canada, 2020. [Google Scholar]

- Poledna, S.; Miess, M.G.; Hommes, C.H. Economic Forecasting with an Agent-Based Model. Available online: https://ssrn.com/abstract=3484768 (accessed on 4 February 2020). [CrossRef] [Green Version]

- Heise, A. Whither economic complexity? A new heterodox economic paradigm or just another variation within the mainstream? Int. J. Plur. Econ. Educ. 2017, 8, 115–129. [Google Scholar]

- Zhou, W.X.; Sornette, D. Self-organizing Ising model of financial markets. Eur. Phys. J. B 2007, 55, 175–181. [Google Scholar] [CrossRef]

- Schinckus, C. Ising model, econophysics and analogies. Phys. A Stat. Mech. Its Appl. 2018, 508, 95–103. [Google Scholar] [CrossRef]

- Plerou, V.; Gopikrishnan, P.; Stanley, H.E. Two-phase behaviour of financial markets. Nature 2003, 421, 130. [Google Scholar] [CrossRef] [PubMed]

- Brock, W.A.; Durlauf, S.N. Discrete choice with social interactions. Rev. Econ. Stud. 2001, 68, 235–260. [Google Scholar] [CrossRef]

- Aoki, M. New Approaches to Macroeconomic Modeling: Evolutionary Stochastic Dynamics, Multiple Equilibria, and Externalities as Field Effects; Cambridge University Press: Cambridge, UK, 1998. [Google Scholar]

- Mantegna, R.N.; Stanley, H.E. Turbulence and financial markets. Nature 1996, 383, 587–588. [Google Scholar] [CrossRef]

- Ghashghaie, S.; Breymann, W.; Peinke, J.; Talkner, P.; Dodge, Y. Turbulent cascades in foreign exchange markets. Nature 1996, 381, 767–770. [Google Scholar] [CrossRef]

- Milchtaich, I. Network topology and the efficiency of equilibrium. Games Econ. Behav. 2006, 57, 321–346. [Google Scholar] [CrossRef] [Green Version]

- Witt, U. Evolutionary Economics; Edward Algar Publishing: Aldershot, UK, 1993. [Google Scholar]

- Martin, R.; Sunley, P. Complexity thinking and evolutionary economic geography. J. Econ. Geogr. 2007, 7, 573–601. [Google Scholar] [CrossRef] [Green Version]

- Scatà, M.; Di Stefano, A.; La Corte, A.; Liò, P.; Catania, E.; Guardo, E.; Pagano, S. Combining evolutionary game theory and network theory to analyze human cooperation patterns. Chaos Solitons Fractals 2016, 91, 17–24. [Google Scholar] [CrossRef]

- Kasthurirathna, D.; Harre, M.; Piraveenan, M. Optimising influence in social networks using bounded rationality models. Soc. Netw. Anal. Min. 2016, 6, 1–14. [Google Scholar] [CrossRef]

- Arthur, W.B. Foundations of complexity economics. Nat. Rev. Phys. 2021, 3, 136–145. [Google Scholar] [CrossRef] [PubMed]

- Anderle, R.V. Modern Evolutionary Economics. Rev. Bras. Inov 2020, 19, 1–3. [Google Scholar] [CrossRef]

- Nelson, R.R.; Dosi, G.; Helfat, C.E.; Pyka, A.; Saviotti, P.P.; Lee, K.; Winter, S.G.; Dopfer, K.; Malerba, F. Modern Evolutionary Economics: An Overview; Cambridge University Press: Cambridge, UK, 2018. [Google Scholar]

- Carrère, C.; Mrázová, M.; Neary, J.P. Gravity Without Apology: The Science of Elasticities, Distance and Trade. Econ. J. 2020, 130, 880–910. [Google Scholar] [CrossRef]

- Isard, W. Location theory and trade theory: Short-run analysis. Q. J. Econ. 1954, 68, 305–320. [Google Scholar] [CrossRef]

- Anderson, J.E. A theoretical foundation for the gravity equation. Am. Econ. Rev. 1979, 69, 106–116. [Google Scholar]

- Bergstrand, J.H. The gravity equation in international trade: Some microeconomic foundations and empirical evidence. Rev. Econ. Stat. 1985, 67, 474–481. [Google Scholar] [CrossRef]

- Rauch, J.E. Business and social networks in international trade. J. Econ. Lit. 2001, 39, 1177–1203. [Google Scholar] [CrossRef] [Green Version]

- Rauch, J.E. Networks versus markets in international trade. J. Int. Econ. 1999, 48, 7–35. [Google Scholar] [CrossRef] [Green Version]

- Chaney, T. The network structure of international trade. Am. Econ. Rev. 2014, 104, 3600–3634. [Google Scholar] [CrossRef] [Green Version]

- Dalin, C.; Konar, M.; Hanasaki, N.; Rinaldo, A.; Rodriguez-Iturbe, I. Evolution of the global virtual water trade network. Proc. Natl. Acad. Sci. USA 2012, 109, 5989–5994. [Google Scholar] [CrossRef] [Green Version]

- Akerman, A.; Seim, A.L. The global arms trade network 1950–2007. J. Comp. Econ. 2014, 42, 535–551. [Google Scholar] [CrossRef] [Green Version]

- Edwards, J. Reconstruction: Australia after COVID; Penguin Random House Australia: Melbourne, Australia, 2021. [Google Scholar]

- Smillie, D. Regional Trade Agreements. The World Bank, Brief. 2018. Available online: https://www.worldbank.org/en/topic/regional-integration/brief/regional-trade-agreements (accessed on 14 October 2021).

- Sreedevi, R.; Saranga, H. Uncertainty and supply chain risk: The moderating role of supply chain flexibility in risk mitigation. Int. J. Prod. Econ. 2017, 193, 332–342. [Google Scholar] [CrossRef]

- Huang, Y.; Lin, C.; Liu, S.; Tang, H. Trade Networks and Firm Value: Evidence from the US-China Trade War. CEPR Discussion Paper No. DP14173. 2019. Available online: https://ssrn.com/abstract=3504602 (accessed on 14 October 2021).

- Levermann, A. Climate economics: Make supply chains climate-smart. Nat. News 2014, 506, 27. [Google Scholar] [CrossRef] [PubMed]

- Watts, D.J.; Strogatz, S.H. Collective dynamics of ‘small-world’networks. Nature 1998, 393, 440–442. [Google Scholar] [CrossRef] [PubMed]

- Barabási, A.L.; Albert, R. Emergence of scaling in random networks. Science 1999, 286, 509–512. [Google Scholar] [CrossRef] [Green Version]

- Bhattacharya, K.; Mukherjee, G.; Saramäki, J.; Kaski, K.; Manna, S.S. The international trade network: Weighted network analysis and modelling. J. Stat. Mech. Theory Exp. 2008, 2008, P02002. [Google Scholar] [CrossRef]

- Barigozzi, M.; Fagiolo, G.; Mangioni, G. Identifying the community structure of the international-trade multi-network. Phys. A Stat. Mech. Its Appl. 2011, 390, 2051–2066. [Google Scholar] [CrossRef] [Green Version]

- Fronczak, A.; Fronczak, P. Statistical mechanics of the international trade network. Phys. Rev. E 2012, 85, 056113. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Gallegati, M.; Keen, S.; Lux, T.; Ormerod, P. Worrying trends in econophysics. Phys. A Stat. Mech. Its Appl. 2006, 370, 1–6. [Google Scholar] [CrossRef]

- McCauley, J.L. Response to “worrying trends in econophysics”. Phys. A Stat. Mech. Its Appl. 2006, 371, 601–609. [Google Scholar] [CrossRef] [Green Version]

- Di Matteo, T.; Aste, T. No Worries: Trends in Econophysics. Eur. Phys. J. B 2007, 55, 121–122. [Google Scholar] [CrossRef]

- Arthur, W.B. Complexity and the economy. Science 1999, 284, 107–109. [Google Scholar] [CrossRef]

- LeBaron, B.; Arthur, W.B.; Palmer, R. Time series properties of an artificial stock market. J. Econ. Dyn. Control 1999, 23, 1487–1516. [Google Scholar] [CrossRef] [Green Version]

- Arthur, W.B. Inductive reasoning and bounded rationality. Am. Econ. Rev. 1994, 84, 406–411. [Google Scholar]

- Farmer, J.D.; Geanakoplos, J. The virtues and vices of equilibrium and the future of financial economics. Complexity 2009, 14, 11–38. [Google Scholar] [CrossRef] [Green Version]

- Rosser, J.B., Jr. The rise and fall of catastrophe theory applications in economics: Was the baby thrown out with the bathwater? J. Econ. Dyn. Control 2007, 31, 3255–3280. [Google Scholar] [CrossRef]

- Harré, M.; Bossomaier, T. Equity trees and graphs via information theory. Eur. Phys. J. B 2010, 73, 59–68. [Google Scholar] [CrossRef]

- Bossomaier, T.; Barnett, L.; Harré, M. Information and phase transitions in socio-economic systems. Complex Adapt. Syst. Model. 2013, 1, 1–25. [Google Scholar] [CrossRef] [Green Version]

- Kasthurirathna, D.; Piraveenan, M.; Harré, M. Influence of topology in the evolution of coordination in complex networks under information diffusion constraints. Eur. Phys. J. B 2014, 87, 1–15. [Google Scholar] [CrossRef]

- Harré, M.S.; Prokopenko, M. The social brain: Scale-invariant layering of Erdos–Rényi networks in small-scale human societies. J. R. Soc. Interface 2016, 13, 20160044. [Google Scholar] [CrossRef] [Green Version]

- Harré, M.; Bossomaier, T. Phase-transition–like behaviour of information measures in financial markets. EPL Europhys. Lett. 2009, 87, 18009. [Google Scholar] [CrossRef]

- Wolpert, D.H.; Harré, M.; Olbrich, E.; Bertschinger, N.; Jost, J. Hysteresis effects of changing the parameters of noncooperative games. Phys. Rev. E 2012, 85, 036102. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Harré, M.S.; Atkinson, S.R.; Hossain, L. Simple nonlinear systems and navigating catastrophes. Eur. Phys. J. B 2013, 86, 1–8. [Google Scholar] [CrossRef]

- Harré, M.S.; Bossomaier, T. Strategic islands in economic games: Isolating economies from better outcomes. Entropy 2014, 16, 5102–5121. [Google Scholar] [CrossRef] [Green Version]

- Harré, M.S.; Harris, A.; McCallum, S. Singularities and Catastrophes in Economics: Historical Perspectives and Future Directions. arXiv 2019, arXiv:1907.05582. [Google Scholar]

- Hopmere, M.; Crawford, L.; Harré, M.S. Proactively Monitoring Large Project Portfolios. Proj. Manag. J. 2020, 51, 656–669. [Google Scholar] [CrossRef]

- Slavko, B.; Glavatskiy, K.; Prokopenko, M. City structure shapes directional resettlement flows in Australia. Sci. Rep. 2020, 10, 1–11. [Google Scholar] [CrossRef] [PubMed]

- Glavatskiy, K.S.; Prokopenko, M.; Carro, A.; Ormerod, P.; Harré, M. Explaining herding and volatility in the cyclical price dynamics of urban housing markets using a large-scale agent-based model. SN Bus. Econ. 2021, 1, 1–21. [Google Scholar] [CrossRef]

- Evans, B.P.; Glavatskiy, K.; Harré, M.S.; Prokopenko, M. The impact of social influence in Australian real estate: Market forecasting with a spatial agent-based modell. J. Econ. Interact. Coord. 2021. [Google Scholar] [CrossRef]

- Crosato, E.; Prokopenko, M.; Harré, M.S. The polycentric dynamics of Melbourne and Sydney: Suburb attractiveness divides a city at the home ownership level. Proc. R. Soc. A 2021, 477, 20200514. [Google Scholar] [CrossRef]

- Wolpert, D.; Jamison, J.; Newth, D.; Harré, M. Strategic choice of preferences: The persona model. BE J. Theor. Econ. 2011, 11. [Google Scholar] [CrossRef] [Green Version]

- Harré, M.; Bossomaier, T.; Snyder, A. The perceptual cues that reshape expert reasoning. Sci. Rep. 2012, 2, 1–9. [Google Scholar] [CrossRef] [Green Version]

- Harré, M. The neural circuitry of expertise: Perceptual learning and social cognition. Front. Hum. Neurosci. 2013, 7, 852. [Google Scholar] [CrossRef] [Green Version]

- Gobet, F.; Snyder, A.; Bossomaier, T.; Harré, M. Designing a “better” brain: Insights from experts and savants. Front. Psychol. 2014, 5, 470. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Prokopenko, M.; Harré, M.; Lizier, J.; Boschetti, F.; Peppas, P.; Kauffman, S. Self-referential basis of undecidable dynamics: From the Liar paradox and the halting problem to the edge of chaos. Phys. Life Rev. 2019, 31, 134–156. [Google Scholar] [CrossRef]

- Harré, M. Entropy and Transfer Entropy: The Dow Jones and the Build Up to the 1997 Asian Crisis. In Proceedings of the International Conference on Social Modeling and Simulation, Plus Econophysics Colloquium 2014; Springer: Cham, Switzerland, 2015; pp. 15–25. [Google Scholar]

- Bossomaier, T.; Barnett, L.; Harré, M.; Lizier, J.T. An Introduction to Transfer Entropy; Springer: Cham, Switzerland, 2016; Volume 65. [Google Scholar]

- Prokopenko, M.; Barnett, L.; Harré, M.; Lizier, J.T.; Obst, O.; Wang, X.R. Fisher transfer entropy: Quantifying the gain in transient sensitivity. Proc. R. Soc. A Math. Phys. Eng. Sci. 2015, 471, 20150610. [Google Scholar] [CrossRef]

- Harré, M. Utility, revealed preferences theory, and strategic ambiguity in iterated games. Entropy 2017, 19, 201. [Google Scholar] [CrossRef] [Green Version]

- Harré, M.S. Strategic information processing from behavioural data in iterated games. Entropy 2018, 20, 27. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Bossomaier, T.; Barnett, L.; Steen, A.; Harré, M.; d’Alessandro, S.; Duncan, R. Information flow around stock market collapse. Account. Financ. 2018, 58, 45–58. [Google Scholar] [CrossRef]

- Harré, M.S. Information Theory for Agents in Artificial Intelligence, Psychology, and Economics. Entropy 2021, 23, 310. [Google Scholar] [CrossRef] [PubMed]

- Evans, B.; Prokopenko, M. A Maximum Entropy Model of Bounded Rational Decision-Making with Prior Beliefs and Market Feedback. Entropy 2021, 23, 669. [Google Scholar] [CrossRef] [PubMed]

- Gallegati, M.; Palestrini, A.; Rosser, J.B. The period of financial distress in speculative markets: Interacting heterogeneous agents and financial constraints. Macroecon. Dyn. 2011, 15, 60. [Google Scholar] [CrossRef] [Green Version]

- Rosser, J.B.; Rosser, M.V.; Gallegati, M. A Minsky-Kindleberger perspective on the financial crisis. J. Econ. Issues 2012, 46, 449–458. [Google Scholar] [CrossRef]

- Gordon, M.J. Towards a theory of financial distress. J. Financ. 1971, 26, 347–356. [Google Scholar] [CrossRef]

- Corbae, D.; Quintin, E. Leverage and the foreclosure crisis. J. Political Econ. 2015, 123, 1–65. [Google Scholar] [CrossRef] [Green Version]

- Haughwout, A.; Lee, D.; Tracy, J.S.; Van der Klaauw, W. Real Estate Investors, the Leverage Cycle, and the Housing Market Crisis. FRB of New York Staff Report, No. 514. 2011. Available online: https://ssrn.com/abstract=1926858 (accessed on 14 October 2021). [CrossRef] [Green Version]

- Bookstaber, R.M.; Paddrik, M.E. An Agent-Based Model for Crisis Liquidity Dynamics. Office of Financial Research Working Paper, No. 15-18. 2015. Available online: https://ssrn.com/abstract=2664230 (accessed on 14 October 2021). [CrossRef] [Green Version]

- Bookstaber, R.; Paddrik, M.; Tivnan, B. An agent-based model for financial vulnerability. J. Econ. Interact. Coord. 2018, 13, 433–466. [Google Scholar] [CrossRef]

- Kindleberger, C.P.; Aliber, R.Z. Manias, Panics and Crashes: A History of Financial Crises; Palgrave Macmillan: London, UK, 2011. [Google Scholar]

- Australian Government Department of Health. Coronavirus (COVID-19) Advice for International Travellers; Australian Government Department of Health: Canberra, Australia, 2021.

- Pacific, C.A. CoreLogic Quarterly Rental Review; CoreLogic: Sydney, Australia, 2020. [Google Scholar]

- Reserve Bank of Australia. Term Funding Facility–Reduction in Interest Rate to Further Support the Australian Economy; Media Releases–RBA: Sydney, Australia, 2020. [Google Scholar]

- Pacific, C.A. Housing Market Update; CoreLogic: Sydney, Australia, 2020. [Google Scholar]

- Australian Taxation Office A.G. JobKeeper Payment. 2021. Available online: https://www.ato.gov.au/general/jobkeeper-payment/ (accessed on 14 October 2021).

- Services Australia A.G. JobSeeker Payment. 2021. Available online: https://www.servicesaustralia.gov.au/individuals/services/centrelink/jobseeker-payment (accessed on 14 October 2021).

- Jribi, S.; Ismail, H.B.; Doggui, D.; Debbabi, H. COVID-19 virus outbreak lockdown: What impacts on household food wastage? Environ. Dev. Sustain. 2020, 22, 3939–3955. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Australian Bureau of Statistics. Household Impacts of COVID-19 Survey. 2021. Available online: https://www.abs.gov.au/statistics/people/people-and-communities/household-impacts-covid-19-survey/apr-2021 (accessed on 14 October 2021).

- Australian Bureau of Statistics. Insights of the Housing Market During COVID-19. 2021. Available online: https://www.abs.gov.au/articles/insights-housing-market-during-covid-19 (accessed on 14 October 2021).

- Lux, T.; Marchesi, M. Volatility clustering in financial markets: A microsimulation of interacting agents. Int. J. Theor. Appl. Financ. 2000, 3, 675–702. [Google Scholar] [CrossRef]

- Gopikrishnan, P.; Plerou, V.; Amaral, L.A.N.; Meyer, M.; Stanley, H.E. Scaling of the distribution of fluctuations of financial market indices. Phys. Rev. E 1999, 60, 5305. [Google Scholar] [CrossRef] [Green Version]

- Lux, T. Turbulence in financial markets: The surprising explanatory power of simple cascade models. Quant. Financ. 2001, 1, 632–640. [Google Scholar] [CrossRef]

- Zhou, W.X. Finite-size effect and the components of multifractality in financial volatility. Chaos, Solitons Fractals 2012, 45, 147–155. [Google Scholar] [CrossRef] [Green Version]

- Gidea, M.; Katz, Y. Topological data analysis of financial time series: Landscapes of crashes. Phys. A Stat. Mech. Its Appl. 2018, 491, 820–834. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Z.Q.; Xie, W.J.; Zhou, W.X.; Sornette, D. Multifractal analysis of financial markets: A review. Rep. Prog. Phys. 2019, 82, 125901. [Google Scholar] [CrossRef] [Green Version]

- Padash, A.; Chechkin, A.V.; Dybiec, B.; Pavlyukevich, I.; Shokri, B.; Metzler, R. First-passage properties of asymmetric Lévy flights. J. Phys. A Math. Theor. 2019, 52, 454004. [Google Scholar] [CrossRef]

- Arias-Calluari, K.; Alonso-Marroquin, F.; Harré, M.S. Closed-form solutions for the Lévy-stable distribution. Phys. Rev. E 2018, 98, 012103. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Alonso-Marroquin, F.; Arias-Calluari, K.; Harré, M.; Najafi, M.N.; Herrmann, H.J. Q-Gaussian diffusion in stock markets. Phys. Rev. E 2019, 99, 062313. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Arias-Calluari, K.; Alonso-Marroquin, F.; Najafi, M.N.; Harré, M. Methods for forecasting the effect of exogenous risks on stock markets. Phys. A Stat. Mech. Its Appl. 2021, 568, 125587. [Google Scholar] [CrossRef]

- Arias-Calluari, K.; Najafi, M.N.; Harré, M.; Yang, Y.; Alonso-Marroquin, F. Testing stationarity of the detrended price return in stock markets. Phys. A Stat. Mech. Its Appl. 2021, 126487. [Google Scholar] [CrossRef]

- Plerou, V.; Gopikrishnan, P.; Rosenow, B.; Amaral, L.A.N.; Guhr, T.; Stanley, H.E. Random matrix approach to cross correlations in financial data. Phys. Rev. E 2002, 65, 066126. [Google Scholar] [CrossRef] [Green Version]

- Plerou, V.; Gopikrishnan, P.; Rosenow, B.; Amaral, L.A.N.; Stanley, H.E. Universal and nonuniversal properties of cross correlations in financial time series. Phys. Rev. Lett. 1999, 83, 1471. [Google Scholar] [CrossRef] [Green Version]

- Onnela, J.P.; Chakraborti, A.; Kaski, K.; Kertesz, J. Dynamic asset trees and Black Monday. Phys. A Stat. Mech. Its Appl. 2003, 324, 247–252. [Google Scholar] [CrossRef] [Green Version]

- Onnela, J.P.; Chakraborti, A.; Kaski, K.; Kertesz, J.; Kanto, A. Asset trees and asset graphs in financial markets. Phys. Scr. 2003, 2003, 48. [Google Scholar] [CrossRef]

- Onnela, J.P.; Chakraborti, A.; Kaski, K.; Kertesz, J.; Kanto, A. Dynamics of market correlations: Taxonomy and portfolio analysis. Phys. Rev. E 2003, 68, 056110. [Google Scholar] [CrossRef] [Green Version]

- Onnela, J.P.; Saramäki, J.; Kertész, J.; Kaski, K. Intensity and coherence of motifs in weighted complex networks. Phys. Rev. E 2005, 71, 065103. [Google Scholar] [CrossRef] [Green Version]

- Barnett, L.; Lizier, J.T.; Harré, M.; Seth, A.K.; Bossomaier, T. Information flow in a kinetic Ising model peaks in the disordered phase. Phys. Rev. Lett. 2013, 111, 177203. [Google Scholar] [CrossRef] [Green Version]

- Granger, C.W. Testing for causality: A personal viewpoint. J. Econ. Dyn. Control 1980, 2, 329–352. [Google Scholar] [CrossRef]

- Schreiber, T. Measuring information transfer. Phys. Rev. Lett. 2000, 85, 461. [Google Scholar] [CrossRef] [Green Version]

- Simoes, A.J.G.; Hidalgo, C.A. The economic complexity observatory: An analytical tool for understanding the dynamics of economic development. In Proceedings of the Workshops at the Twenty-Fifth AAAI Conference on Artificial Intelligence, Palo Alto, CA, USA, 7–11 August 2011. [Google Scholar]

- Hartmann, D.; Guevara, M.R.; Jara-Figueroa, C.; Aristarán, M.; Hidalgo, C.A. Linking economic complexity, institutions, and income inequality. World Dev. 2017, 93, 75–93. [Google Scholar] [CrossRef] [Green Version]

- Lapatinas, A.; Garas, A.; Boleti, E.; Kyriakou, A. Economic Complexity and Environmental Performance: Evidence from a World Sample. Environ. Mod. Ass. 2021, 26, 251–270. [Google Scholar]

- Adam, A.; Garas, A.; Katsaiti, M.S.; Lapatinas, A. Economic complexity and jobs: An empirical analysis. Econ. Innov. New Technol. 2021, 1–28. [Google Scholar] [CrossRef]

- Dolfing, A.G.; Leuven, J.R.; Dermody, B.J. The effects of network topology, climate variability and shocks on the evolution and resilience of a food trade network. PLoS ONE 2019, 14, e0213378. [Google Scholar] [CrossRef]

- Fair, K.R.; Bauch, C.T.; Anand, M. Dynamics of the global wheat trade network and resilience to shocks. Sci. Rep. 2017, 7, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Schwartz, E.; Smith, J.E. Short-term variations and long-term dynamics in commodity prices. Manag. Sci. 2000, 46, 893–911. [Google Scholar] [CrossRef] [Green Version]

- Devalkar, S.K.; Anupindi, R.; Sinha, A. Integrated optimization of procurement, processing, and trade of commodities. Oper. Res. 2011, 59, 1369–1381. [Google Scholar] [CrossRef] [Green Version]

- Demirer, M.; Diebold, F.X.; Liu, L.; Yilmaz, K. Estimating global bank network connectedness. J. Appl. Econom. 2018, 33, 1–15. [Google Scholar] [CrossRef]

- Gemünden, H.G.; Lehner, P.; Kock, A. The project-oriented organization and its contribution to innovation. Int. J. Proj. Manag. 2018, 36, 147–160. [Google Scholar] [CrossRef]

- Flyvbjerg, B. What you Should Know about Megaprojects and Why: An Overview. Proj. Manag. J. 2014, 45, 6–19. [Google Scholar] [CrossRef] [Green Version]

- Ansar, A.; Flyvbjerg, B.; Budzier, A.; Lunn, D. Should we build more large dams? The actual costs of hydropower megaproject development. Energy Policy 2014, 69, 43–56. [Google Scholar] [CrossRef] [Green Version]

- Flyvbjerg, B.; Stewart, A. Olympic Proportions: Cost and Cost Overrun at the Olympics 1960–2012; SSRN Scholarly Paper ID 2238053; Social Science Research Network: Rochester, NY, USA, 2012. [Google Scholar] [CrossRef]

- Olds, K. Globalization and the production of new urban spaces: Pacific Rim megaprojects in the late 20th century. Environ. Plan. A 1995, 27, 1713–1743. [Google Scholar] [CrossRef]

- Zeković, S.; Maričić, T.; Vujošević, M. Megaprojects as an instrument of urban planning and development: Example of Belgrade Waterfront. In Technologies for Development: From Innovation to Social Impact; Springer: Cham, Switzerland, 2018; pp. 153–164. [Google Scholar] [CrossRef]

- Söderlund, J.; Sankaran, S.; Biesenthal, C. The Past and Present of Megaprojects; SAGE Publications: Los Angeles, CA, USA, 2017. [Google Scholar]

- Devenow, A.; Welch, I. Rational herding in financial economics. Eur. Econ. Rev. 1996, 40, 603–615. [Google Scholar] [CrossRef]

- Parker, W.D.; Prechter, R.R. Herding: An Interdisciplinary Integrative Review from a Socionomic Perspective. 2005. Available online: https://ssrn.com/abstract=2009898 (accessed on 14 October 2021). [CrossRef] [Green Version]

- Scheffer, M.; Bascompte, J.; Brock, W.A.; Brovkin, V.; Carpenter, S.R.; Dakos, V.; Held, H.; Van Nes, E.H.; Rietkerk, M.; Sugihara, G. Early-warning signals for critical transitions. Nature 2009, 461, 53–59. [Google Scholar] [CrossRef]

- Scheffer, M. Foreseeing tipping points. Nature 2010, 467, 411–412. [Google Scholar] [CrossRef]

- Seekell, D.A.; Carpenter, S.R.; Pace, M.L. Conditional heteroscedasticity as a leading indicator of ecological regime shifts. Am. Nat. 2011, 178, 442–451. [Google Scholar] [CrossRef] [Green Version]

- Dai, L.; Vorselen, D.; Korolev, K.S.; Gore, J. Generic indicators for loss of resilience before a tipping point leading to population collapse. Science 2012, 336, 1175–1177. [Google Scholar] [CrossRef] [Green Version]

- Slavko, B.; Glavatskiy, K.S.; Prokopenko, M. Revealing configurational attractors in the evolution of modern Australian and US cities. Chaos Solitons Fractals 2021, 148, 111079. [Google Scholar] [CrossRef]

- Staniek, M.; Lehnertz, K. Symbolic transfer entropy. Phys. Rev. Lett. 2008, 100, 158101. [Google Scholar] [CrossRef]

- Yao, W.; Wang, J. Multi-scale symbolic transfer entropy analysis of EEG. Phys. A Stat. Mech. Its Appl. 2017, 484, 276–281. [Google Scholar] [CrossRef]

- Wang, L.; Xue, W.; Li, Y.; Luo, M.; Huang, J.; Cui, W.; Huang, C. Automatic epileptic seizure detection in EEG signals using multi-domain feature extraction and nonlinear analysis. Entropy 2017, 19, 222. [Google Scholar] [CrossRef] [Green Version]

- Lenton, T.; Livina, V.; Dakos, V.; Van Nes, E.; Scheffer, M. Early warning of climate tipping points from critical slowing down: Comparing methods to improve robustness. Philos. Trans. R. Soc. A Math. Phys. Eng. Sci. 2012, 370, 1185–1204. [Google Scholar] [CrossRef] [PubMed]

- Tylianakis, J.M.; Coux, C. Tipping points in ecological networks. Trends Plant Sci. 2014, 19, 281–283. [Google Scholar] [CrossRef] [PubMed]

- Dakos, V.; Matthews, B.; Hendry, A.P.; Levine, J.; Loeuille, N.; Norberg, J.; Nosil, P.; Scheffer, M.; De Meester, L. Ecosystem tipping points in an evolving world. Nat. Ecol. Evol. 2019, 3, 355–362. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Barnett, L.; Barrett, A.B.; Seth, A.K. Granger causality and transfer entropy are equivalent for Gaussian variables. Phys. Rev. Lett. 2009, 103, 238701. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Lizier, J.T. JIDT: An information-theoretic toolkit for studying the dynamics of complex systems. Front. Robot. AI 2014, 1, 11. [Google Scholar] [CrossRef] [Green Version]

- Fagiolo, G.; Reyes, J.; Schiavo, S. On the topological properties of the world trade web: A weighted network analysis. Phys. A Stat. Mech. Its Appl. 2008, 387, 3868–3873. [Google Scholar] [CrossRef] [Green Version]

- Maeng, S.E.; Choi, H.W.; Lee, J.W. Complex networks and minimal spanning trees in international trade network. In International Journal of Modern Physics: Conference Series; World Scientific: Singapore, 2012; Volume 16, pp. 51–60. [Google Scholar]

- Barzel, B.; Barabási, A.L. Universality in network dynamics. Nat. Phys. 2013, 9, 673–681. [Google Scholar] [CrossRef] [Green Version]

- Ariu, A. Crisis-proof services: Why trade in services did not suffer during the 2008–2009 collapse. J. Int. Econ. 2016, 98, 138–149. [Google Scholar] [CrossRef] [Green Version]

- del Rio-Chanona, R.M.; Mealy, P.; Pichler, A.; Lafond, F.; Farmer, J.D. Supply and demand shocks in the COVID-19 pandemic: An industry and occupation perspective. Oxf. Rev. Econ. Policy 2020, 36, S94–S137. [Google Scholar] [CrossRef]

- Kelly, G.; La Cava, G. Value-added Trade and the Australian Economy. RBA Bull. 2013. Available online: https://www.rba.gov.au/publications/bulletin/2013/mar/ (accessed on 14 October 2021).

- Johnson, R.C.; Noguera, G. Accounting for intermediates: Production sharing and trade in value added. J. Int. Econ. 2012, 86, 224–236. [Google Scholar] [CrossRef] [Green Version]

- Deguchi, T.; Takahashi, K.; Takayasu, H.; Takayasu, M. Hubs and authorities in the world trade network using a weighted HITS algorithm. PLoS ONE 2014, 9, e100338. [Google Scholar]

- Zhu, Z.; Cerina, F.; Chessa, A.; Caldarelli, G.; Riccaboni, M. The rise of China in the international trade network: A community core detection approach. PLoS ONE 2014, 9, e105496. [Google Scholar] [CrossRef] [Green Version]

- Escaith, H.; Lindenberg, N.; Miroudot, S. International Supply Chains and Trade Elasticity in Times of Global Crisis; World Trade Organization (Economic Research and Statistics Division) Staff Working Paper ERSD-2010-08; WTO: Geneva, Switzerland, 2010.

- Turner, J. The Handbook of Project-Based Management, 2nd ed.; McGraw-Hill: London, UK, 1999. [Google Scholar]

- Geraldi, J.; Maylor, H.; Williams, T.M. Now, let’s make it really complex (complicated): A systematic review of the complexities of projects. Int. J. Oper. Prod. Manag. 2011, 31, 966–990. [Google Scholar] [CrossRef]

- Chipulu, M.; Neoh, J.G.; Ojiako, U.; Williams, T. A Multidimensional Analysis of Project Manager Competences. IEEE Trans. Eng. Manag. 2013, 60, 506–517. [Google Scholar] [CrossRef]

- Project Management Institute. PMI Lexicon of Project Management Terms; Technical Report; Project Management Institute: Newtown Square, PA, USA, 2017. [Google Scholar]

- Spanuth, T.; Heidenreich, S.; Wald, A. Temporary organisations in the creation of dynamic capabilities: Effects of temporariness on innovative capacity and strategic flexibility. Ind. Innov. 2020, 27, 1186–1208. [Google Scholar] [CrossRef]

- Schoper, Y.G.; Wald, A.; Ingason, H.T.; Fridgeirsson, T.V. Projectification in Western economies: A comparative study of Germany, Norway and Iceland. Int. J. Proj. Manag. 2018, 36, 71–82. [Google Scholar] [CrossRef]

- Turner, J.; Keegan, A. Mechanisms of governance in the project-based organization:: Roles of the broker and steward. Eur. Manag. J. 2001, 19, 254–267. [Google Scholar] [CrossRef]

- Caldas, C.; Gupta, A. Critical factors impacting the performance of mega-projects. Eng. Constr. Archit. Manag. 2017, 24, 920–934. [Google Scholar] [CrossRef]

- Flyvbjerg, B.; Bruzelius, N.; Rothengatter, W. Megaprojects and Risk: An Anatomy of Ambition; Cambridge University Press: New York, NY, USA, 2003. [Google Scholar]

- Bodrožić, Z.; Adler, P.S. The Evolution of Management Models: A Neo-Schumpeterian Theory. Adm. Sci. Q. 2018, 63, 85–129. [Google Scholar] [CrossRef]

- Hanusch, H.; Pyka, A. Principles of Neo-Schumpeterian Economics. Camb. J. Econ. 2006, 31, 275–289. [Google Scholar] [CrossRef] [Green Version]

- Locatelli, G. Why are Megaprojects, Including Nuclear Power Plants, Delivered Overbudget and Late? Reasons and Remedies. arXiv 2018, arXiv:1802.07312. [Google Scholar]

- Aritua, B.; Smith, N.J.; Bower, D. Construction client multi-projects–A complex adaptive systems perspective. Int. J. Proj. Manag. 2009, 27, 72–79. [Google Scholar] [CrossRef]

- Bousquin, J. $9.6B Worth of Infrastructure Projects Delayed or Canceled during COVID-19. 2020. Available online: https://www.constructiondive.com/news/96b-worth-of-infrastructure-projects-delayed-or-canceled-during-covid-19/582713/ (accessed on 14 October 2021).

- Premo Black, A. Impacts of COVID-19 on State and Local Transportation Revenues & Construction Programs; Technical Report; American Road & Transportation Builders Association; 2020; Available online: https://www.artba.org/wp-content/uploads/2020/11/202010.23_ARTBA_COVID19RevImpact_v22.pdf (accessed on 14 October 2021).

- Hopkirk, E. Projects Cancelled as Workloads and Income Hit by COVID-19 Pandemic, RIBA Survey Finds. 2020. Available online: https://www.building.co.uk/news/projects-cancelled-as-workloads-and-income-hit-by-covid-19-pandemic-riba-survey-finds/5105430.article (accessed on 14 October 2021).

- Steeman, M. Almost 200 Construction Projects Impacted by COVID-19. New Report Says|Stuff.co.nz. 2020. Available online: https://www.stuff.co.nz/business/property/120894743/almost-200-construction-projects-impacted-by-covid19-new-report-says (accessed on 14 October 2021).

- ConstructConnect. Delayed Projects Report-9 July 2021; Technical Report; Construct Connect: Cincinnati OH, USA, 2021; Available online: https://www.constructconnect.com/contact-us (accessed on 14 October 2021).

- AGC. State List of Construction Employment by Metropolitan Area or Division, September 2019–September 2020; Technical Report; AGC The Construction Association: Arlington, VA, USA, 2020. [Google Scholar]

- Jones, K. State of the Construction Industry: One Year Into the Pandemic; Construct Connect: Cincinnati OH, USA, 2021; Available online: https://www.constructconnect.com/blog/state-of-the-construction-industry-one-year-into-the-pandemic (accessed on 14 October 2021).

- Christelis, D.; Georgarakos, D.; Jappelli, T. Wealth shocks, unemployment shocks and consumption in the wake of the Great Recession. J. Monet. Econ. 2015, 72, 21–41. [Google Scholar] [CrossRef] [Green Version]

- Lupu, I. From the Financial Crisis to the Real Economy: The main channels of transmission through a theoretical perspective. Euro Econ. 2012, 31, 45–50. [Google Scholar]

- Padhan, R.; Prabheesh, K. The economics of COVID-19 pandemic: A survey. Econ. Anal. Policy 2021, 70, 220–237. [Google Scholar] [CrossRef]

- European University Institute|COVID-19 Research. 2021. Available online: https://www.eui.eu/Research/Library/ResearchGuides/Economics/Crisis (accessed on 14 October 2021).

- Eurostat|COVID-19|Economy. 2021. Available online: https://ec.europa.eu/eurostat/web/covid-19/economy (accessed on 14 October 2021).

- CEPR|Covid Economics. 2021. Available online: https://cepr.org/content/covid-economics-vetted-and-real-time-papers-0 (accessed on 14 October 2021).

- Turner, D.; Égert, B.; Guillemette, Y.; Botev, J. The Tortoise and the Hare: The Race between Vaccine Rollout and New COVID Variants; OECD Economics Department Working Papers; 2021; Available online: https://0-www-oecd--ilibrary-org.brum.beds.ac.uk/economics/the-tortoise-and-the-hare-the-race-between-vaccine-rollout-and-new-covid-variants_4098409d-en (accessed on 14 October 2021).

- Falcettoni, E.; Nygaard, V.M. A literature review on the impact of increased unemployment insurance benefits and stimulus checks in the United States. Covid Econ. 2021, 64, 186–201. [Google Scholar]

- Capelle-Blancard, G.; Desroziers, A. The stock market is not the economy? Insights from the COVID-19 crisis. In Insights from the COVID-19 Crisis (June 16, 2020). CEPR COVID Economics; VoxEU & CEPR Coverage of the Covid-19 Global Pandemic; 2020; Available online: https://voxeu.org/article/stock-market-and-economy-insights-covid-19-crisis (accessed on 14 October 2021).

- Caselli, F.; Grigoli, F.; Sandri, D. Protecting lives and livelihoods with early and tight lockdowns. BE J. Macroecon. 2021. [Google Scholar] [CrossRef]

- Mahase, E. COVID-19: What do we know about “long covid”? BMJ 2020, 370. [Google Scholar] [CrossRef] [PubMed]

- Hampshire, A.; Trender, W.; Chamberlain, S.R.; Jolly, A.E.; Grant, J.E.; Patrick, F.; Mazibuko, N.; Williams, S.C.; Barnby, J.M.; Hellyer, P.; et al. Cognitive deficits in people who have recovered from COVID-19. EClinicalMedicine 2021, 39, 101044. [Google Scholar] [CrossRef]

- Kupferschmidt, K.; Wadman, M. Delta Variant Triggers New Phase in the Pandemic. Science 2021, 372, 6549. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Demand Impacts | |||

|---|---|---|---|

| Industry Affected | Notional Value Affected | Industry Affected | Effect as % of Industry Total |

| Other services | −2850 | Non-Metallic Minerals | −9% |

| Wholesale Trade | −1667 | Wood | −8% |

| Non-Metallic Minerals | −1107 | Fabricated Metals | −6% |

| Supply Impacts | |||

|---|---|---|---|

| Industry Affected | Notional Value Affected | Industry Affected | Effect as % of Industry Total |

| Real Estate | −2337 | Real Estate | −3% |

| Other services | −533 | Wood | −2% |

| Defence | −514 | Utilities | −1% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Harré, M.S.; Eremenko, A.; Glavatskiy, K.; Hopmere, M.; Pinheiro, L.; Watson, S.; Crawford, L. Complexity Economics in a Time of Crisis: Heterogeneous Agents, Interconnections, and Contagion. Systems 2021, 9, 73. https://0-doi-org.brum.beds.ac.uk/10.3390/systems9040073

Harré MS, Eremenko A, Glavatskiy K, Hopmere M, Pinheiro L, Watson S, Crawford L. Complexity Economics in a Time of Crisis: Heterogeneous Agents, Interconnections, and Contagion. Systems. 2021; 9(4):73. https://0-doi-org.brum.beds.ac.uk/10.3390/systems9040073

Chicago/Turabian StyleHarré, Michael S., Aleksey Eremenko, Kirill Glavatskiy, Michael Hopmere, Leonardo Pinheiro, Simon Watson, and Lynn Crawford. 2021. "Complexity Economics in a Time of Crisis: Heterogeneous Agents, Interconnections, and Contagion" Systems 9, no. 4: 73. https://0-doi-org.brum.beds.ac.uk/10.3390/systems9040073