The Determinants of the Usage of Accounting Information Systems toward Operational Efficiency in Industrial Revolution 4.0: Evidence from an Emerging Economy

, ,

, ,

Abstract

:1. Introduction

2. Literature Review

3. Theoretical Framework and Hypothesis Development

3.1. Theoretical Framework

3.1.1. Technology–Organization–Environment (TOE)

3.1.2. Diffusion of Innovations (DOI)

3.1.3. Resource Based View Theory (RBV)

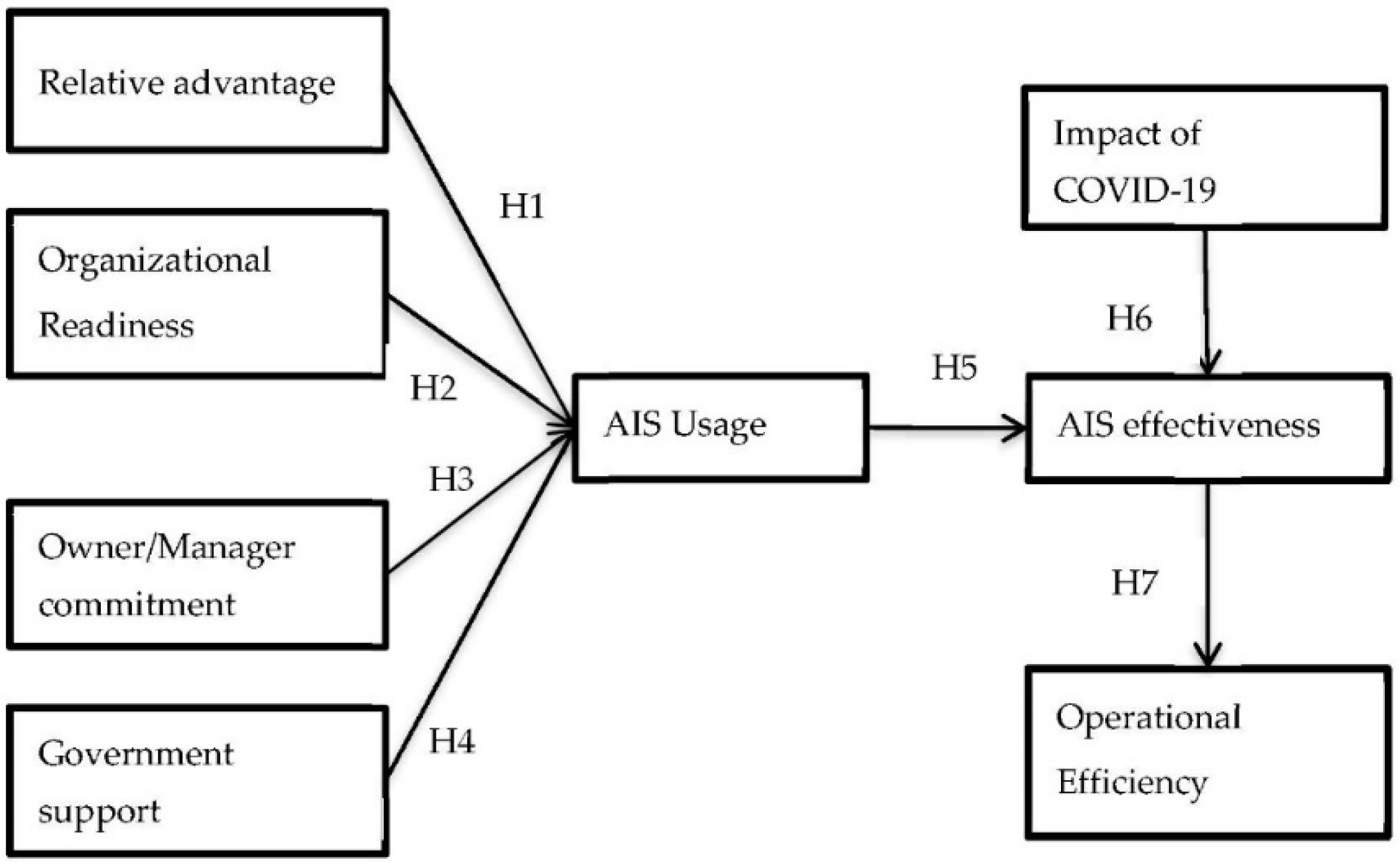

3.2. Hypothesis Development

4. Research Design

4.1. Scale and Structure of the Questionnaire

4.2. Methodology

4.3. Research Model

5. Results

5.1. Descriptive Statistics

5.2. Check Measurement

5.3. Structural Model

6. Discussion

7. Conclusions and Implications

7.1. Conclusions

7.2. Theorical Contribution

7.3. Practical Implications

7.4. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Study Measures | Measurement Items |

|---|---|

| RA Ali et al. (2012) | RA1. Using AIS can reduce our operation cost. RA2. Using AIS can reduce our operation time. RA3. Using AIS can provide useful information to make decisions. |

| RD Ali et al. (2012) | RD1. We are financially ready to use AIS. RD2. We have enough technological resources to use AIS. RD3. Our employees have adequate knowledge to use AIS. |

| OMC Lutfi et al. (2020) | OMC1. We consider AIS adoption important. OMC2. We are active engagement in planning and using AIS. OMC3. We support the management shows regarding the deployment and the planning of AIS. OMC4. We are committed to encourage and support the AIS usage by staff. OMC5. We are committed to correctly implement every available resource to use AIS successfully. OMC6. We overcome the hurdles present due to natural resistance to technology usage. |

| GS Lutfi et al. (2020) | GS1. Government support plays an important role in encouraging and promoting the use of AIS. GS2. Government policies and regulations vary from one industry to another that affect the use of AIS. GS3. Government policies and regulations vary from one country to another that affect the use of AIS. |

| AISU Lutfi et al. (2020) | AISU1. Information-related needs for reporting dissemination. AISU2. Non-economic information needs, information risk analysis. AISU3. Information needs related to business decisions. AISU4. Ability to respond to information related to business decisions. AISU5. The ability to respond to information related to notification dissemination. AISU6. Ability to respond to analytic risk and non-economic information. AISU7. The ability to reply to informational links to other issues. |

| AISE Lutfi et al. (2020) | AISE1. AIS is a data collection, storage, recording and processing system to generate information for decision managers. AISE2. Minimize uncertainty in decision making improve the ability to plan and control activities. AISE3. AIS supports SMEs growth in terms of sales, revenue and customers. Provide information to internal and external audiences. AISE4. Improve user satisfaction, reduce errors, and improve information availability. AISE5. Reduce costs, reduce time, save human resources for businesses to use. AISE6. AIS is a connection tool for management systems and operational systems. |

| CV Nagel (2020) | CV1. COVID-19 accelerating digital transformation work-from-anywhere (work from home, no global barrier, work-life balance, flexible work arrangement, time-saving as no commuting needed, …). CV2. COVID-19 accelerating digital transformation provides benefits of innovative business model (run business remotely, evolution of product, service and processes, online transaction improvement, driving innovative solutions, …). CV3. COVID-19 accelerating digital transformation provides benefits of technologies, automation and collaboration (telecommuting, virtual workplace, mobility, IT security, the wise use of scrum, …). |

| OE A Ali and AlSondos (2020) | OE1. Customer satisfaction. OE2. Employee Ethics. OE3. Enterprise market share. OE4. The growth of sales. OE5. Profits of the business. |

References

- A Ali, Basel J., and Ibrahim A. Abu AlSondos. 2020. Operational Efficiency and the Adoption of Accounting Information System (Ais): A Comprehensive Review of the Banking Sectors. International Journal of Management 11: 221–34. [Google Scholar]

- ACCA_GLOBAL. 2016. Professional Accountants—The Future: Drivers of Change and Future Skills. London: ACCA_GLOBAL. [Google Scholar]

- Acedo, Francisco José, Carmen Barroso, and Jose Luis Galan. 2006. The resource-based theory: Dissemination and main trends. Strategic Management Journal 27: 621–36. [Google Scholar] [CrossRef]

- Al Nahian Riyadh, Md, Shahriar Akter, and Nayeema Islam. 2009. The adoption of e-banking in developing countries: A theoretical model for SMEs. International Review of Business Research Papers 5: 212–30. [Google Scholar]

- Al-Alawi, Adel Ismail, and Faisal M. Al-Ali. 2015. Factors affecting e-commerce adoption in SMEs in the GCC: An empirical study of Kuwait. Research Journal of Information Technology 7: 1–21. [Google Scholar] [CrossRef]

- Ali, Azwadi, Mohd Shaari Abdul Rahman, and WNSW Ismail. 2012. Predicting continuance intention to use accounting information systems among SMEs in Terengganu, Malaysia. International Journal of Economics and Management 6: 295–320. [Google Scholar]

- Ali, B. J., Wan Ahmad Wan Omar, and Rosni Bakar. 2016. Accounting Information System (AIS) and organizational performance: Moderating effect of organizational culture. International Journal of Economics, Commerce and Management 4: 138–58. [Google Scholar]

- Ali, Basel J. A., Anas A. Salameh, and Mohammad Salem Oudat. 2020. The relationship between risk measurement and the accounting information system: A review in the commercial and islamic banking sectors. PalArch’s Journal of Archaeology of Egypt/Egyptology 17: 13276–90. [Google Scholar]

- Awa, Hart O., Ojiabo Ukoha, and Sunny R. Igwe. 2017. Revisiting technology-organization-environment (TOE) theory for enriched applicability. The Bottom Line 30: 2–22. [Google Scholar] [CrossRef]

- Barney, Jay. 1991. Firm resources and sustained competitive advantage. Journal of Management 17: 99–120. [Google Scholar] [CrossRef]

- Baumane-Vitolina, Ilona, and Igo Cals. 2013. Theoretical framework for using resource based view in the analysis of SME innovations. European Scientific Journal, 9. [Google Scholar]

- Beland, Louis-Philippe, Oluwatobi Fakorede, and Derek Mikola. 2020. Short-term effect of COVID-19 on self-employed workers in Canada. Canadian Public Policy 46: S66–S81. [Google Scholar] [CrossRef]

- Bhattacherjee, Anol. 2001a. An empirical analysis of the antecedents of electronic commerce service continuance. Decision Support Systems 32: 201–14. [Google Scholar] [CrossRef]

- Bhattacherjee, Anol. 2001b. Understanding information systems continuance: An expectation-confirmation model. MIS Quarterly 25: 351–70. [Google Scholar] [CrossRef]

- Churchill, Gilbert A., Jr. 1979. A paradigm for developing better measures of marketing constructs. Journal of Marketing Research 16: 64–73. [Google Scholar] [CrossRef]

- CISCO. 2020. Asia Pacific SMB Digital Maturity Study. Available online: https://www.cisco.com/c/dam/global/en_sg/solutions/small-business/pdfs/ebookciscosmbdigitalmaturityi5-with-markets.pdf (accessed on 11 November 2021).

- Damanpour, Fariborz, and Marguerite Schneider. 2006. Phases of the adoption of innovation in organizations: Effects of environment, organization and top managers. British Journal of Management 17: 215–36. [Google Scholar] [CrossRef]

- Fornell, Claes, and David F. Larcker. 1981. Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research 18: 39–50. [Google Scholar] [CrossRef]

- Grandon, Elizabeth E., and J. Michael Pearson. 2004. Electronic commerce adoption: An empirical study of small and medium US businesses. Information & Management 42: 197–216. [Google Scholar]

- Grover, Varun, and Martin D. Goslar. 1993. The initiation, adoption, and implementation of telecommunications technologies in US organizations. Journal of Management Information Systems 10: 141–64. [Google Scholar] [CrossRef]

- Hair, Joseph F., Jr., G. Tomas, M. Hult, Christian M. Ringle, and Marko Sarstedt. 2016. A Primer on Partial Least Squares Structural Equation Modeling, 2nd ed. Thousand Oaks: SAGE Publications, p. 390. [Google Scholar]

- Hair, Joseph F., Jr., Marko Sarstedt, Christian M. Ringle, and Siegfried P. Gudergan. 2017. Advanced Issues in Partial Least Squares Structural Equation Modeling. Thousand Oaks: SAGE Publications. [Google Scholar]

- Hair, Joseph F., Jr., G. Tomas, M. Hult, Christian M. Ringle, Marko Sarstedt, Nicholas P. Danks, and Soumya Ray. 2021. An introduction to structural equation modeling. In Partial Least Squares Structural Equation Modeling (PLS-SEM) Using R. Berlin/Heidelberg: Springer, pp. 1–29. [Google Scholar]

- Hansen, D., M. Mowen, and L. Guan. 2007. Cost Management: Accounting & Control, 6th ed. Mason: South-Western Cengage Learning. [Google Scholar]

- Henderson, Dave, Steven D. Sheetz, and Brad S. Trinkle. 2012. The determinants of inter-organizational and internal in-house adoption of XBRL: A structural equation model. International Journal of Accounting Information Systems 13: 109–40. [Google Scholar] [CrossRef]

- Hermann, Mario, Tobias Pentek, and Boris Otto. 2016. Design principles for industrie 4.0 scenarios. Paper presented at the 2016 49th Hawaii International Conference on System Sciences (HICSS), Koloa, HI, USA, January 5–8. [Google Scholar]

- Khairi, Mohammad Shadiq, and Zaki Baridwan. 2015. An empirical study on organizational acceptance accounting information systems in Sharia banking. The International Journal of Accounting and Business Society 23: 97–122. [Google Scholar]

- Koli, L. N., and B. Rawat. 2011. Measuring of operational efficiency and its impact on overall profitability. A Case Study of BPCL. BVIMR Management Egde 4: 105–14. [Google Scholar]

- Kouser, Rehana, Gul Rana, and Farasat Ali Shahzad. 2011. Determinants of AIS effectiveness: Assessment thereof in Pakistan. International Journal of Contemporary Business Studies 2: 6–21. [Google Scholar]

- Kozlenkova, Irina V., Stephen A. Samaha, and Robert W. Palmatier. 2014. Resource-based theory in marketing. Journal of the Academy of Marketing Science 42: 1–21. [Google Scholar] [CrossRef]

- Limayem, Moez, and Christy M. K. Cheung. 2008. Understanding information systems continuance: The case of Internet-based learning technologies. Information & Management 45: 227–32. [Google Scholar]

- Lutfi, Abd Alwali, Kamil Md Idris, and Rosli Mohamad. 2017. AIS usage factors and impact among Jordanian SMEs: The moderating effect of environmental uncertainty. Journal of Advanced Research in Business and Management Studies 6: 24–38. [Google Scholar]

- Lutfi, Abdalwali, Manaf Al-Okaily, Adi Alsyouf, Abdallah Alsaad, and Abdallah Taamneh. 2020. The impact of AIS usage on AIS effectiveness among Jordanian SMEs: A multi-group analysis of the role of firm size. International Journal of Sociology and Social Policy 40: 861–75. [Google Scholar] [CrossRef]

- Maryeni, Yen Yen, Rajesri Govindaraju, Budhi Prihartono, and Iman Sudirman. 2014. E-commerce adoption by Indonesian SMEs. Australian Journal of Basic and Applied Sciences 8: 45–49. [Google Scholar]

- Mcmahon, Richard G. P. 2001. Growth and performance of manufacturing SMEs: The influence of financial management characteristics. International Small Business Journal 19: 10–28. [Google Scholar] [CrossRef]

- Minishi-Majanja, Mabel K., and Joseph Kiplangat ’. 2005. The diffusion of innovations theory as a theoretical framework in library and information science research. South African Journal of Libraries and Information Science 71: 211–24. [Google Scholar] [CrossRef] [Green Version]

- Molino, Monica, Emanuela Ingusci, Fulvio Signore, Amelia Manuti, Maria Luisa Giancaspro, Vincenzo Russo, Margherita Zito, and Claudio G. Cortese. 2020. Wellbeing costs of technology use during COVID-19 remote working: An investigation using the Italian translation of the technostress creators scale. Sustainability 12: 5911. [Google Scholar] [CrossRef]

- Momani, Alaa M., Mamoun M. Jamous, and Shadi M. S. Hilles. 2017. Technology acceptance theories: Review and classification. International Journal of Cyber Behavior, Psychology and Learning 7: 1–14. [Google Scholar] [CrossRef]

- Nagel, Lisa. 2020. The influence of the COVID-19 pandemic on the digital transformation of work. International Journal of Sociology and Social Policy. [Google Scholar] [CrossRef]

- Nasiren, M. D. A., M. N. Abdullah, and Mohd Asmoni. 2016. Critical Success Factors on the BCM Implementation in SMEs. Journal of Advanced Research in Business and Management Studies 3: 105–22. [Google Scholar]

- Nastase, Carmen Eugenia, Ancuta Lucaci, and Carmen Chașovschi. 2020. Circular economy: A perspective for the transformation of rural built heritage in Europe. Paper presented at Competitiveness and Sustainable Development, Chişinău, Moldova, November 20. [Google Scholar]

- Nunnally, Jum C. 1978. Psychometric Theory, 2nd ed. New York: McGraw Hill. [Google Scholar]

- Pedró, Francesc. 2020. COVID-19 y educación superior en América Latina y el Caribe: Efectos, impactos y recomendaciones políticas. Análisis Carolina 36: 1–15. [Google Scholar] [CrossRef]

- Premkumar, G., and Margaret Roberts. 1999. Adoption of new information technologies in rural small businesses. Omega 27: 467–84. [Google Scholar] [CrossRef]

- Rahayu, Rita, and John Day. 2015. Determinant factors of e-commerce adoption by SMEs in developing country: Evidence from Indonesia. Procedia-Social and Behavioral Sciences 195: 142–50. [Google Scholar] [CrossRef] [Green Version]

- Ramdani, Boumediene, and Peter Kawalek. 2007. SME adoption of enterprise systems in the Northwest of England. Paper presented at IFIP International Working Conference on Organizational Dynamics of Technology-Based Innovation, Manchester, UK, June 14–16. [Google Scholar]

- Rogers, Everett M. 2010. Diffusion of Innovations. New York: Simon and Schuster. [Google Scholar]

- Rozzani, Nabilah, and Rashidah Abdul Rahman. 2013. Determinants of bank efficiency: Conventional versus Islamic. International Journal of Business and Management 8: 98–109. [Google Scholar] [CrossRef] [Green Version]

- Scherer, Ronny, Fazilat Siddiq, and Jo Tondeur. 2019. The technology acceptance model (TAM): A meta-analytic structural equation modeling approach to explaining teachers’ adoption of digital technology in education. Computers & Education 128: 13–35. [Google Scholar]

- Spurk, Daniel, and Caroline Straub. 2020. Flexible Employment Relationships and Careers in Times of the COVID-19 Pandemic. Amsterdam: Elsevier, p. 103435. [Google Scholar]

- Stuerz, Roland, Christian Stumpf, Ulrike Mendel, and Dietmar Harhoff. 2020. Digitalisierung durch Corona?—Verbreitung und Akzeptanz von Homeoffice in Deutschland: Ergebnisse zweier bidt-Kurzbefragungen. bidt Analysen und Studien. [Google Scholar]

- To, March L., and Eric W. T. Ngai. 2006. Predicting the organisational adoption of B2C e-commerce: An empirical study. Industrial Management & Data Systems 106: 1133–47. [Google Scholar]

- Tornatzky, Louis G., Mitchell Fleischer, and Alok K. Chakrabarti. 1990. Processes of Technological Innovation. Lanham: Lexington Books. [Google Scholar]

- Tu, Trương Văn. 2020. Nghiên cứu áp dụng hệ thống thông tin kế toán trong các doanh nghiệp nhỏ và vừa ở Việt Nam. Tạp Chí Tài Chính 4: 17–20. [Google Scholar]

- Vietnam News. 2021. Guidebook on Digital Transformation for Businesses Published. Vietnamnews, June 16. [Google Scholar]

- Wong, Ken Kwong-Kay. 2013. Partial least squares structural equation modeling (PLS-SEM) techniques using SmartPLS. Marketing Bulletin 24: 1–32. [Google Scholar]

- Word Bank. 2021. The Word Bank in Vietnam. Washington, DC: Word Bank. [Google Scholar]

- Zhu, Kevin, and Kenneth L. Kraemer. 2005. Post-adoption variations in usage and value of e-business by organizations: Cross-country evidence from the retail industry. Information Systems Research 16: 61–84. [Google Scholar] [CrossRef] [Green Version]

- Zhu, Kevin, Kenneth L. Kraemer, and Sean Xu. 2006. The process of innovation assimilation by firms in different countries: A technology diffusion perspective on e-business. Management Science 52: 1557–76. [Google Scholar] [CrossRef] [Green Version]

| Category | Percentage |

|---|---|

| Gender | |

| Female | 61.36% |

| Male | 38.64% |

| Total | 100% |

| Age | |

| 18–24 | 66.67% |

| 24–35 | 26.51% |

| 35–45 | 3.03% |

| 45 and above | 3.79% |

| Total | 100% |

| Work experience | |

| 5 years or less | 83.33% |

| 6–10 years | 9.85% |

| 11–15 years | 1.52% |

| More than 15 years | 5.30% |

| Total | 100% |

| Average income per month | |

| Under 10 million | 59.85% |

| 10–20 million | 29.55% |

| 20–40 million | 6.05% |

| Over 40 million | 4.55% |

| Total | 100% |

| Living place | |

| Ha Noi | 1.52% |

| TP.HCM | 86.36% |

| Đa Nang | 1.52% |

| Others | 10.60% |

| Total | 100% |

| Position | |

| Staff | 86.36% |

| Manager | 11.36% |

| Chief executive officer | 1.52% |

| Senior manager | 0.76% |

| Total | 100% |

| Academic level | |

| College | 5.30% |

| University | 89.40% |

| Post-university | 5.30% |

| Total | 100% |

| Type of business | |

| Mining industry | 9.85% |

| Retail | 23.48% |

| Repair of other cars and engines | 0.76% |

| Accommodation and food service | 48.48% |

| Water supply and waste treatment | 1.52% |

| Energy and mining | 2.27% |

| Transportation, warehousing, and construction | 6.06% |

| Electronic technology | 7.58% |

| Total | 100% |

| Age of business | |

| 1–5 years | 27.27% |

| 6–10 years | 22.73% |

| 11–20 years | 19.70% |

| More than 20 years | 30.30% |

| Total | 100% |

| Number of employees | |

| Under 10 people | 11.36% |

| 10–99 people | 27.27% |

| 100–199 people | 14.39% |

| 200–300 people | 9.10% |

| More than 300 people | 37.88% |

| Total | 100% |

| Var | Item | Factor Loading (>0.7) | AVE (>0.5) | CR (>0.7) | Cronbach’s Alpha (>0.7) |

|---|---|---|---|---|---|

| RA | RA1 | 0.899 | 0.734 | 0.892 | 0.819 |

| RA2 | 0.790 | ||||

| RA3 | 0.876 | ||||

| RD | RD1 | 0.900 | 0.790 | 0.918 | 0.869 |

| RD2 | 0.925 | ||||

| RD3 | 0.839 | ||||

| OMC | OMC1 | 0.841 | 0.727 | 0.941 | 0.924 |

| OMC2 | 0.870 | ||||

| OMC3 | 0.882 | ||||

| OMC4 | 0.891 | ||||

| OMC5 | 0.857 | ||||

| OMC6 | 0.769 | ||||

| GS | GS1 | 0.871 | 0.799 | 0.923 | 0.874 |

| GS2 | 0.903 | ||||

| GS3 | 0.908 | ||||

| CV | CV1 | 0.906 | 0.856 | 0.947 | 0.916 |

| CV2 | 0.939 | ||||

| CV3 | 0.930 | ||||

| AISU | AISU1 | 0.859 | 0.742 | 0.953 | 0.942 |

| AISU2 | 0.871 | ||||

| AISU3 | 0.870 | ||||

| AISU4 | 0.882 | ||||

| AISU5 | 0.872 | ||||

| AISU6 | 0.876 | ||||

| AISU7 | 0.796 | ||||

| AISE | AISE1 | 0.879 | 0.769 | 0.952 | 0.940 |

| AISE2 | 0.891 | ||||

| AISE3 | 0.902 | ||||

| AISE4 | 0.870 | ||||

| AISE5 | 0.871 | ||||

| AISE6 | 0.848 | ||||

| OE | OE1 | 0.871 | 0.690 | 0.917 | 0.887 |

| OE2 | 0.813 | ||||

| OE3 | 0.820 | ||||

| OE4 | 0.799 | ||||

| OE5 | 0.847 |

| AISE | AISU | CV | GS | OE | OMC | RA | RD | |

|---|---|---|---|---|---|---|---|---|

| AISE | 0.877 | |||||||

| AISU | 0.765 | 0.861 | ||||||

| CV | 0.683 | 0.630 | 0.925 | |||||

| GS | 0.548 | 0.572 | 0.558 | 0.894 | ||||

| OE | 0.585 | 0.593 | 0.607 | 0.530 | 0.831 | |||

| OMC | 0.706 | 0.688 | 0.665 | 0.644 | 0.647 | 0.853 | ||

| RA | 0.626 | 0.640 | 0.594 | 0.644 | 0.522 | 0.649 | 0.856 | |

| RD | 0.594 | 0.565 | 0.575 | 0.552 | 0.551 | 0.698 | 0.577 | 0.889 |

| Var | R Square Adjusted | |

|---|---|---|

| AISU | AIS Usage | 0.532 |

| AISE | AIS Effectiveness | 0.647 |

| OE | Operational Efficiency | 0.337 |

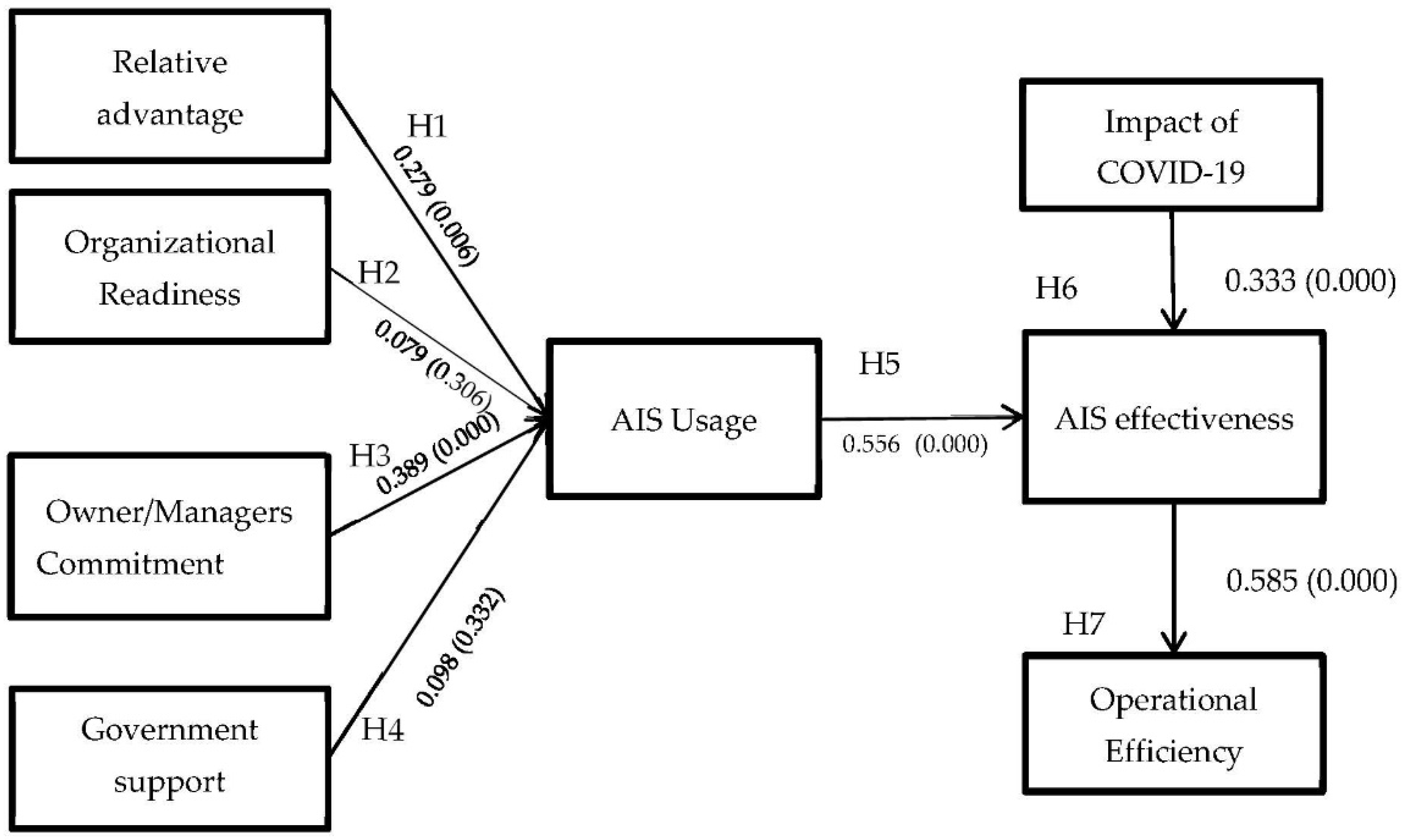

| Hypothesis | Path | Coefficient | T-Stat | p-Values | Conclusion |

|---|---|---|---|---|---|

| H1 | RA → AISU | 0.279 | 2.707 | 0.007 | Supported |

| H2 | RD → AISU | 0.079 | 1.035 | 0.301 | Not Supported |

| H3 | OMC → AISU | 0.389 | 3.700 | 0.000 | Supported |

| H4 | GS → AISU | 0.098 | 0.948 | 0.344 | Not Supported |

| H5 | AISU → AISE | 0.556 | 5.602 | 0.000 | Supported |

| H6 | CV → AISE | 0.333 | 3.507 | 0.000 | Supported |

| H7 | AISE → OE | 0.585 | 6.561 | 0.000 | Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Thuan, P.Q.; Khuong, N.V.; Anh, N.D.C.; Hanh, N.T.X.; Thi, V.H.A.; Tram, T.N.B.; Han, C.G. The Determinants of the Usage of Accounting Information Systems toward Operational Efficiency in Industrial Revolution 4.0: Evidence from an Emerging Economy. Economies 2022, 10, 83. https://0-doi-org.brum.beds.ac.uk/10.3390/economies10040083

Thuan PQ, Khuong NV, Anh NDC, Hanh NTX, Thi VHA, Tram TNB, Han CG. The Determinants of the Usage of Accounting Information Systems toward Operational Efficiency in Industrial Revolution 4.0: Evidence from an Emerging Economy. Economies. 2022; 10(4):83. https://0-doi-org.brum.beds.ac.uk/10.3390/economies10040083

Chicago/Turabian StyleThuan, Pham Quoc, Nguyen Vinh Khuong, Nguyen Duong Cam Anh, Nguyen Thi Xuan Hanh, Vo Huynh Anh Thi, Tieu Ngoc Bao Tram, and Chu Gia Han. 2022. "The Determinants of the Usage of Accounting Information Systems toward Operational Efficiency in Industrial Revolution 4.0: Evidence from an Emerging Economy" Economies 10, no. 4: 83. https://0-doi-org.brum.beds.ac.uk/10.3390/economies10040083