Executive Turnover and Founder CEO Experience: Effect on New Ventures’ R&D Investment

1

Department of International Business, Dongduk Women’s University, Seoul 02748, Korea

2

Department of Business Administration, Kyonggi University, Suwon 16227, Korea

3

Department of IT Management, Kyungmin University, Euijeongbu 11618, Korea

*

Author to whom correspondence should be addressed.

Economies 2022, 10(5), 97; https://0-doi-org.brum.beds.ac.uk/10.3390/economies10050097

Submission received: 2 March 2022

/

Revised: 13 April 2022

/

Accepted: 18 April 2022

/

Published: 19 April 2022

(This article belongs to the Special Issue Novel Insights in the Leadership in Business and Economics)

Abstract

:As the direction and strategies of new ventures depend on the top management team (TMT)’s stability and continuous efforts, we investigate the relationship between executive turnover and research and development (R&D) investment investment. Furthermore, we assess the moderating role of the founder chief executive officer (CEO)’s prior experiences to show that founders’ experiential knowledge mitigates the adverse side effects of executives’ departure. Our empirical analysis utilizes a large pool of firm-level survey datasets comprising 1897 Korean founder-led ventures. The empirical results show that executive turnover reduces R&D intensity, suggesting that new ventures’ longer-term investments may be affected by the instability of the management team. We also show that the negative effects of executive turnover weaken when the founder CEO has a longer prior work experience, prior business group experience, and founding experience. Our findings show that the founder CEO’s entrepreneurship based on valuable prior experiential knowledge mitigates the negative impact of organizational instability. While the TMT factor is essential for a new venture’s survival, our findings show that the manner in which leaders act should also be considered separately.

1. Introduction

New ventures are characterized by higher ambiguity about resources, routines, products, and environments due to new initiatives (Bradley et al. 2011; Ensley et al. 2002; Gartner et al. 1992). The entrepreneurship studies suggest that a demanding environment faced by a new venture increases the importance of the top management team (TMT) factors (Chandler et al. 2005; Cooper and Bruno 2000). While prior research has mostly provided insights into how the attributes of the TMT or interaction among TMT members affect performance (Ensley et al. 2002), this study seeks to contribute to the literature concerning the top management team’s issue in new ventures, focusing on executive turnover and the founder CEO’s experience. Discontinuity of executives managerial services is a concerning factor as it affects longer-term strategy such as R&D investment, the essential element in strengthening the core competencies of a new venture. To encourage the growth of new ventures, the effect of executive leave on new ventures’ innovation is an important question to address. We focus on executives (except for the CEO) to further test the boundary condition with regard to the founder CEO’s experiences. As founder CEOs are focal point of a new venture’s birth and continuous growth, we analyze how the founder CEOs’ prior experiences moderate the negative executive turnover effect. Finding the different impacts of the founder CEO and executives on the new venture’s innovation allows us to understand the new venture’s TMT dynamics.

Especially for new ventures, executives who possess valuable managerial skills or industrial expertise are a concerning factor in utilizing and further developing the inherently limited resources of new ventures. Prior entrepreneurship studies have further shown that the continuing managerial service provided by TMT is a vital factor for the innovation of venture firms as the ongoing R&D process and requires the continuous commitment and attention of executives (Cummings and Knott 2018). Discontinuity of managerial services by executives due to their leave implies losing the idiosyncratic tacit knowledge of a specific firm that supports the innovative process. It is not easy to find an adequate successor with similar skill sets or expertise perfectly compatible with the venture’s ongoing R&D process. Aside from the time and cost involved with the new recruitment, the newly elected executive also needs time to absorb new information to handle various business issues. Hence, we posit that an executive’s departure has a detrimental effect on new ventures’ continuous R&D investment efforts as they reduce the continuity of the innovation process and firm-specific knowledge assets.

While the executives are key human resources of venture firms, entrepreneurship research has focused on the value of an individual entrepreneur. Imprinting theory in entrepreneurship research asserts that entrepreneurs bring in a set of abilities and knowledge that are imprinted on a venture (e.g., Bamford et al. 2000; Johnson 2007). As new ventures suffer from scarce resources and business uncertainty, the founder CEO’s attributes are considered critical for venture survival. We argue that the founder CEO’s prior experiential knowledge moderates the negative impact of executive turnover on R&D investment. It is argued that the founder CEO’s previous experiences are likely to affect new ventures during the entrepreneurial process (Hashai and Zahra 2021; Shane and Venkataraman 2000; Westhead et al. 2005). Hence, when faced with a situation involving high uncertainty, founder CEOs are highly likely to make decisions based on managerial experiences they accumulated before founding the new ventures. As founder CEOs prior work-related experiences may shape their managerial skills, values, and goals, we suggest that previous work experience in general, prior business group work experience, and prior founding experience mitigate the negative impact of executives’ departure on R&D investment.

This study contributes to the literature by enhancing our knowledge of the effect of a new venture’s TMT instability on R&D investment strategies. While TMT characteristics have long been suggested to significantly influence the new venture’s performance, our results strengthen the argument that the TMT aspect is essential and provide further evidence that long-term strategic decisions (i.e., R&D investment) are affected by executive leave. Our results imply that new ventures’ steady investment may benefit from the stability of the management team and the continuous services provided by the executives. Furthermore, this study segregates TMT into executives and founder CEOs to show the combined effect of different aspects of TMT. We highlight the importance of the founder CEO’s role in early-stage investment in organizational instability after the executives’ departure. In particular, we show that the founder’s prior work-related experiences are related to relatively stronger organizational stability, which improves continuous investment.

The structure of this paper is as follows. Section 2 presents previous literature and hypotheses on the relationship between executive turnover and R&D investment. Section 3 explains the sample and variables for the empirical analysis. Section 4 presents the results of the empirical analysis, followed by Section 5 which discusses and summarizes the findings of this study.

2. Literature Review and Hypothesis Development

2.1. Executive Turnover and R&D Investment

As new firms face a higher propensity to fail due to liabilities of newness along with their inherent scarce resources, they have a unique challenge compared to the established firms (Eisenhardt and Schoonhoven 1990). New ventures operate in a dynamic business environment, and innovation strategies are the critical factor that can increase the longevity and growth of the organization. Prior innovation literature has pointed out that continuous innovation strategies increase knowledge accumulation, promoting persistent innovation (e.g., Costa et al. 2020; Suarez 2014). The organizational structure that promotes innovation and absorptive capacity is expected to increase the innovative outcomes at the organizational level. However, building a stable organizational structure from scratch under resource constraints is not an easy task (Kor and Mesko 2013). Executives rely heavily on the individuals that are crucial resources that possess firm-specific knowledge assets. Furthermore, establishing an innovation strategy and organizational structure for continuous innovation is disturbed when team cohesion is affected by the departure of executives from the company. Hence, we posit that an executive’s departure has a detrimental effect on new ventures’ continuous R&D investment efforts as it reduces the continuity of the innovation process and firm-specific knowledge assets.

Prior entrepreneurship studies have provided extensive evidence on how a new venture’s team characteristics affect strategies or outcomes. For example, Eva et al. (2019) highlight the role of the CEO in increasing performance, and Dai et al. (2019) show the relationship between the personality traits of new ventures’ TMTs and their performance. Although the importance of TMTs has been well established, there is little research on the strategic consequences of executive departure (Chandler et al. 2005). In particular, we have less understanding of how executive departures affect new ventures, which are organizations that mostly need managerial resources to survive. In this study, we examine how executive turnover affects innovation in new ventures by focusing on R&D investment, which is essential in strengthening the core competencies of new ventures and is executed from a long-term perspective.

As entrepreneurial firms are often dependent on strong executives with a vision and resources that enable them to grow (Lester et al. 2006), frequent turnover in the TMT may increase organizational instability. Turnover of executives implies several consequences. First, executive turnover hinders continuous efforts for innovation. One of the essential functions of the TMT is to utilize tacit knowledge to implement an effective strategy (Athanassiou and Nigh 2000; Nielsen 2010), and turnover implies the loss of valuable, tacit, and explicit knowledge. Executives are the core of firms’ technological resource development. It is difficult and costly to replace them, as they develop firm-specific idiosyncratic skills required for the knowledge creation process (Coff 1999). It is expected that a consistent focus on innovation is not achieved when executive turnover is high. As R&D investment from a long-term perspective requires expertise to understand not only the value of R&D but also the firm-specific context in the ongoing R&D process, consistent support from executives familiar with the ongoing process is needed (Cummings and Knott 2018).

Second, the executive turnover can be interpreted as less cohesion of TMT, which hinders the persistent effort on longer-term strategy. TMT cohesion affects the motivation and commitment of team members and is suggested to be the success factor of firms (Klein and Mulvey 1995). The cohesiveness of new venture TMT is essential due to the dynamic business environment they face. Ensley et al. (2002) explain that cohesive teams allow for efficient and effective management, as they have already gone through the process in which members share tacit knowledge and value in the organization. They promptly make decisions without revisiting conditions and goals. Such cohesive TMT is superior in solving problems and reacting quickly with the support of stable interpersonal relationships, and it leads to higher business performance (Smith et al. 1994). Hence, when team cohesion is interrupted, new ventures no longer enjoy the efficiency of a cohesive team.

Third, Dess and Shaw (2001) argue that executive turnover burdens the firm with additional costs because of the new recruitment and hiring of a successor and lower productivity during the vacancy period. The explicit and implicit costs of executive departure may be a financial burden. Also, while the newly hired executives may have managerial expertise, onboarding and developing firm-specific knowledge takes time. Thus, their expected contributions initially surpass the costs involved with their recruitment (Dai et al. 2011). New ventures are suffering from a lack of resources. The loss of critical human resources and related financial costs may put pressure on new ventures to maintain the level of R&D investment.

Based on the abovementioned arguments, we suggest:

Hypothesis 1 (H1).

Executive turnover is negatively related to R&D intensity.

2.2. Moderating Effect of Founder’s Prior Work Experience

Entrepreneurship studies suggest that the founder’s prior managerial experience is an essential source of learning and affects the decision-making of an entrepreneur (Cope 2005; Shepherd et al. 2003). Managerial experience can only be obtained when the founder CEO puts effort into making business decisions or understanding organizational routines (Cooper et al. 1994; De Cock et al. 2021). When making managerial decisions, accumulated experiential knowledge is the knowledge base for founder CEOs to discover or exploit business opportunities (Choi and Shepherd 2004; Shane 2000). The linkage between experiential knowledge and the performance is not only confined to new ventures, whether it is intensively addressed in prior research (e.g., Acquaah 2012; García-García et al. 2017). We posit that the value of the founder CEO’s experiential knowledge is higher, as ventures usually are not equipped with a structured management system. They are highly reliant on the founder’s performance capacity (Landstrom and Sexton 2000).

Based on the notion that the founder’s managerial experiences generate valuable experiential knowledge, we expect that founder CEOs with managerial experience can successfully lead a new venture even when executives’ departure increases organizational instability. Dencker and Gruber (2015) explain that experienced founders possess a valuable repertoire of potential strategic and organizational actions. Their responses to environmental changes are superior to those of less experienced founders. Hence, while executives’ turnover burdens new ventures with managerial challenges, experienced founder CEOs possess strong abilities to deal with such challenges and push firms to establish priorities by pursuing substantial R&D investments.

To analyze the value of founder CEOs’ prior managerial experiences, we propose three types of previous work experiences closely related to managerial expertise. First, the time invested in the industrial field itself is valuable to understanding the industry and market. Professional work experiences improve an entrepreneur’s strength to identify and pursue business opportunities (Roberts 1991), and prior work experience is an essential source of entrepreneurial action (Mathias et al. 2015).

As such, we offer our second hypothesis:

Hypothesis 2 (H2).

A founder’s prior work experience weakens the negative relationship between executive turnover and R&D intensity.

2.3. Moderating Effect of Founder’s Prior Business Group Experience

As the evaluation of risk and expected results for managerial decisions may vary based on the types of founder CEO work experience, we further focused on the effect of business group work experience. When faced with a situation with high uncertainty, the founder CEOs are more likely to make decisions that are comfortable and judged to be more appropriate, and this is likely to be similar to the corporate strategy experienced before (Simon 1978). A business group is a group of legally independent companies managed by the same controlling owner (Choi et al. 2015). In many emerging economies, including Korea, large business group firms are conglomerates that dominate the market. Compared to small firms, large business group firms have a relatively stable profit structure and a high level of structured organization. In addition, as business group firms are managed by controlling owners, such firm structures encourage the pursuit of long-term R&D investment to increase the level of business longevity and growth (Tribo et al. 2007). Chang et al. (2006) asserted that business groups have innovation-supporting institutions, and their persistent ties increase group coordination and transactions among them. As business group firms share group-level resources such as capital and technology, lower costs support their innovation. Hence, a founder CEO with business group experience is likely to have experiential knowledge of the effective innovation process and be more familiar with the consistent investment in technological capabilities. Also, working for a business group is closely related to an accumulation of industrial knowledge and the degree of business network, and a founder CEO with business group experience is more resourceful in navigating these types of difficult situations. Therefore, founder CEOs with business group experience are familiar with long-term perspectives and persistent investment strategies.

Thus, we suggest:

Hypothesis 3 (H3).

A founder’s prior business group experience weakens the negative relationship between executive turnover and R&D intensity.

2.4. Moderating Effect of Founder’s Prior Founding Experience

Lastly, we expect founder CEOs to understand the business cycle of new ventures better when they already have prior experience in founding other firms. Founding experience is related to knowing what needs to be done to manage a new firm successfully. It is accumulated by encountering problems specific to new firms, such as managing new employees and developing new products or services (Delmar and Shane 2006). Tzabbar and Margolis (2017) explain that prior entrepreneur experience forms tacit knowledge that can support new venture management in finding growth strategies and present a connection between entrepreneurial experience and innovation. Also, Geletkanycz and Hambrick (1997) asserted that such entrepreneurs’ various experiences allow them to identify more opportunities, thereby supporting the innovation process. Founding experience is associated with a higher understanding of the organization’s nature and growth strategy as it involves a knowledge of undergoing managerial challenges in newly established firms. Also, we can expect that a founder CEO with founding experience has a higher likelihood of having social ties with venture capitalists or industry experts which increases the utilization of valuable financial and managerial resources (Deb and Wiklund 2017). This suggests that experiences specific to new venture management would allow founder CEOs to be less affected by unexpected events, such as executive turnover. Such experiences make founder CEOs knowledgeable about formulating strategies and organizing activities with a strategic focus without the interruption of executive turnover.

Based on the abovementioned arguments, we propose:

Hypothesis 4 (H4).

A founder’s prior founding experience weakens the negative relationship between executive turnover and R&D intensity.

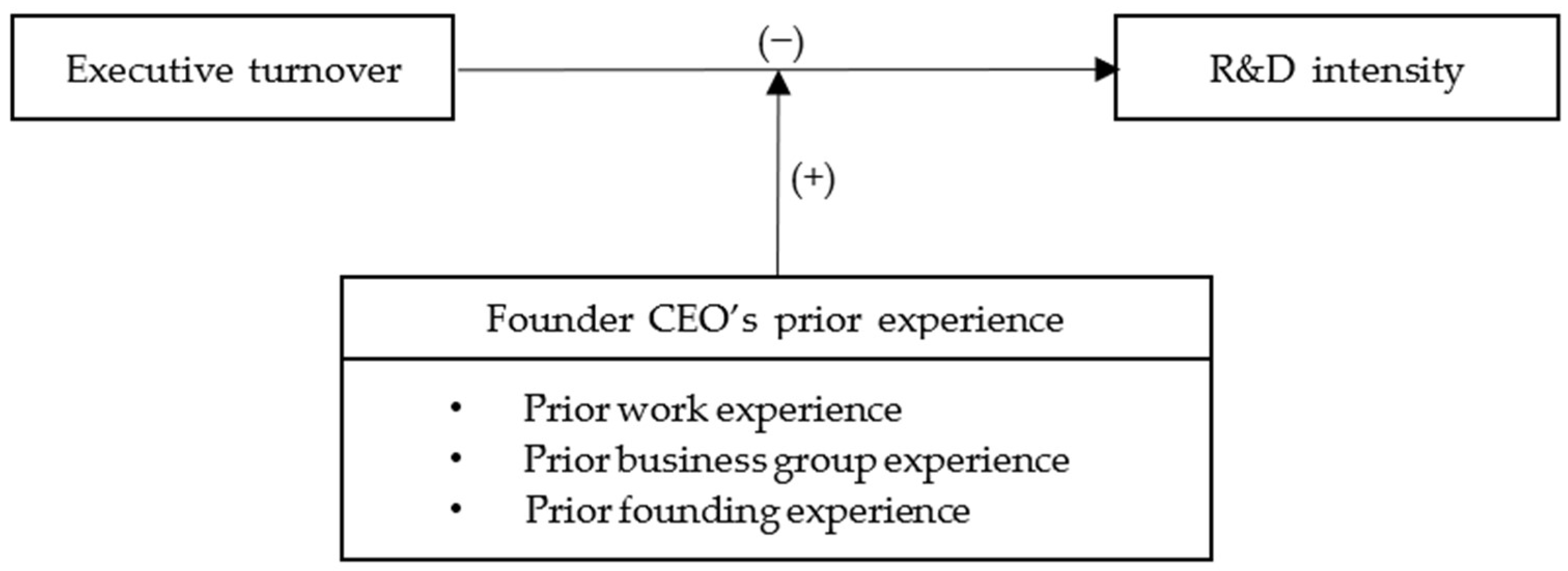

Based on the prior literature review and following the development of hypotheses, we propose a research model presented in Figure 1.

3. Method

3.1. Sample

Our empirical analysis is based on a unique firm-level survey dataset, a 2016–2020 survey conducted by the Ministry of SMEs and Startups and the Korea Venture Business Association based on the Act on Special Measures for the Promotion of Venture Businesses. The survey aims to understand how Korean ventures operate and evolve by collecting various information yearly, e.g., governance structure, employment, technological capabilities, financials, and supplier relations. Based on the Act on Special Measures for the Promotion of Venture Businesses, the Ministry of SMEs and Startups certify a firm as a venture firm based on specific criteria to devise effective policies and governmental support for nurturing ventures. For instance, having a loan based on technology evaluated by the technology credit bureau or having an investment of over 10 percent of equity from a venture capital firm validates the firm as a venture firm. Every year, 2000 venture firms are carefully selected as a sample from various sectors and firm sizes to reflect the original population of venture firms, and a structured questionnaire is distributed by online survey, fax, or email based on circumstances.

Most ventures are not listed firms, and this dataset is advantageous as it enables the collection of detailed information that is not easily accessible or undisclosed. In addition, as the survey contains responses only from venture firms, it provides an advantage in analyzing a large pool of new venture firms led by the founder. While the initial dataset contains 4163 firms, we only include 1897 new ventures eight years old or younger, following McDougall et al. (1994). The top three largest sectors in our sample are (1) food/fibers/non-metals/other manufacturing, (2) machinery/automobile/metal, and (3) software development/IT-based service. New ventures are frequently engaged in B2B sales, as it shows that nearly 90 percent of new ventures have B2B sales, and the average rate of B2B sales to total sales is 80%. Also, the sample shows that 67 percent of new ventures have intellectual properties (IPs), including patents, utility model rights, design rights, and trademark rights. The average of IPs possessed by new ventures is 5.76. When we look at capital raising type, 43 percent received policy support funds from the government, 31 percent had a bank loan, and two percent received venture capital investment. Only 1.5 percent raised capital by stock and bond issuance.

3.2. Measures

The dependent variable is R&D intensity, representing the ratio of R&D investment to total sales. As we investigate the effect of executive turnover on R&D intensity, we construct Executive turnover, measured as the ratio of executive leave to total employment size. To test the moderating effect of the founder’s prior experience, we include three measures, namely, Work experience, Business group experience, and Founding experience. The founder’s work experience is the number of working years before founding the new venture in question. A founder’s business group experience is a dichotomous variable coded as “1” if a founder has previously worked for a business group affiliated firm and “0” otherwise. Korean business groups are identified by the Korea Fair Trade Commissions board based on the total size of a business group affiliated firm. The founding experience is the number of firms founded before founding the new venture in question.

We also include several firm-specific control variables to control for other firm effects. Firm size is frequently a predictor of the size of resources firms can utilize, and it is suggested to influence a firm’s innovation (Forés and Camisón 2016). Hence, we include firm size, a logarithmic value of total assets (Hoskisson et al. 2002). Financial performance and status are closely related to the slack resources that can be used for innovation (Acharya and Xu 2017). We include ROA, the value of net income divided by total assets, and the Debt ratio is total debt divided by total assets. New ventures may be in different business cycles based on their age. We include Age, the number of years since the firm’s foundation. Also, Capital financing is included to control for the new financial slack that new ventures can utilize, which has a value of the size of capital raising divided by total assets. Finally, the year and industry effects are controlled. All control variables are lagged one year following prior research (e.g., Chrisman and Patel 2012). Appendix A Table A1 summarizes the definition of variables used for the analysis. In order to check the multicollinearity issue, we calculate variation inflation factor (VIF) values from regression analysis. For all variables in question, we obtained VIF values ranging from 1.04 to 1.37, which reject serious multicollinearity issues (O’brien 2007).

Table 1 shows the descriptive statistics for variables in the empirical model. In our sample, founder CEOs are likely to have work experience with an average of 11.5 years. Also, founder CEO without work experience only account for 9.7 percent of the total. It shows that the founding of a new firm is frequently initiated by the managerial skills obtained from work. Compared to work experience, founder CEOs have less business group experience or founding experience. Among founder CEOs, 16.2 percent of them have worked in a business group, and 18.7 percent have founded a firm before. Table 2 displays the correlation coefficients.

4. Empirical Results

We employ a pooled ordinary least squared (OLS) regression model to test these hypotheses. Table 3 presents the empirical results of this study. Model 1 shows test results for H1, which suggests the impact of executive turnover on the R&D investment of ventures. Executive turnover has a significant negative effect on R&D intensity, as shown in Model 1 (β = −0.062, p < 0.01). This result supports H1 and shows that the instability of the TMT leads to a strategic shift of new ventures. This research reinforces the importance of TMT for new venture firms in promoting innovation, as suggested in the previous research (e.g., Cummings and Knott 2018). Our empirical evidence suggests that among various TMT factors, the negative change in TMT dynamic due to the executive leave can affect TMT’s effectiveness.

Models 2, 3, and 4 show the moderating effect of three different types of founder CEO prior experiences. Model 2 displays the moderating effect of the founder CEO’s prior work experience on R&D intensity. We observe a significant and positive moderating impact of the founder CEO’s prior work experience, which weakens the negative influence of executive turnover on R&D investment. This result supports H2 (β = 0.005, p < 0.01), suggesting that founder CEO prior work experience is associated with a longer-term perspective in the investment of new ventures. Model 3 reports the moderating effect of founder CEOs’ prior business group experience on R&D intensity. The moderating effect of founder CEOs’ prior business group experience is significant (β = 0.084, p < 0.1), thus supporting Hypothesis 3. Model 4 tests the moderating effect of the founder CEO’s founding experience, and the coefficient is significant in Model 4 (β = 0.019, p < 0.05), thus supporting Hypothesis 4.

Overall, the empirical results show that organizational instability owing to executive departure has a lesser effect on the new venture when founder CEOs have the managerial experience to handle such instability. Our findings are in line with the prior research that proposes the connection between the founder’s attributes and the innovation (e.g., Tzabbar and Margolis 2017). Still, we further test the contingency in which the founder CEO’s managerial experience has a higher value.

5. Conclusions and Discussion

This research has two main research goals for understanding the relationship between the TMT factor and innovation of new ventures, as follows. First, it discusses the impact of executive departure on new ventures’ R&D investment. As researchers emphasized that R&D is a crucial determinant for owning competitive advantage, research on how organizational instability due to executives’ turnover will result in such R&D activities should be reinforced. Second, it explores the conditional effect of the founder CEO that changes the effect of executive turnover on new venture innovation. As the continuous efforts put into R&D investment are one of the factors that improve new venture’ competitiveness and survival, we provide insight into how the TMT factors change the new venture’s R&D investment. We provide empirical evidence that executive turnover reduces R&D investment due to the discontinuity in the managerial service and lack of cohesion in the TMT. However, a founder CEO’s prior managerial experience is a boundary condition that weakens the negative impact of executive turnover, implying the importance of an entrepreneur’s commitment and knowledge for the long-term investment.

5.1. Theoretical Contribution and Implications

This study offers several theoretical contributions and implications. First, our empirical results enhance our understanding of the effect of executive departure on new ventures. In entrepreneurship research, while the characteristics and dynamics of TMT have been well addressed, there is limited understanding of how organizational instability due to executive departure affects the innovation of new ventures. The results suggest that new ventures’ innovation may benefit from the stability of the management team and the continuous services provided by the executives. The results of this study show consistency with the studies of Xiong et al. (2021) and Qian et al. (2013) that TMT’s stability affects organizational innovation or R&D investment, respectively. We empirically confirmed the relationship between the executive departure and R&D investment in the venture business setting and presented the basis for a concrete explanation of this relationship. It contributes to entrepreneurship research by analyzing executive turnover and suggesting that TMT cohesion and stability promote continuous innovation efforts for new ventures.

Second, while prior research focuses on either the TMT as a whole or the CEO, we show a combined effect of executives and founder CEOs. Kor (2006) analyzed the effect of corporate governance on R&D investment strategy and reported that both the composition of the TMT and board of directors directly affect the intensity of R&D investment. In particular, it showed that the founder within the TMT had a positive effect on R&D investment. Still, it was not extended to analyzing the founder’s influence in an environment where the founder did not belong to TMT. In addition, Xiong et al. (2021) recently showed that the negative impact of CEO turnover on R&D investment is also prominent in family companies and non-state-owned companies, but cannot explain the effects of executives and founder CEO separately. However, we emphasized that the founder CEO is an entrepreneur who is at the center of the new venture’s formulation and growth and posited that it could influence the relationship between executives and firm performance. Our analysis proposes that while executives have a significant impact on R&D investment, the founder CEO is an influential factor that can change such an impact. The results imply that the founder CEO’s experiential knowledge accumulated from prior experience helps new ventures to focus more on innovative capabilities. This finding contributes to the imprinting theory in that the characteristics of the entrepreneur (here, founder CEO) bring a set of abilities and knowledge imprinted on ventures. Additionally, it suggests that, when analyzing the effect of TMT-related aspects on firm performance, acknowledging the difference between the entrepreneur and other executives may be beneficial for understanding the dynamics of TMT.

Third, while the importance of human and technological resources is especially high for new ventures due to their inherent dynamic environment, we propose a relationship between critical human resources (executives and founder CEO) and R&D investment. When we consider that executives and founder CEOs comprise the TMT, the changes and characteristics of the TMT jointly affect R&D investment. Although certain events such as turnover may negatively affect other factors, including the founder CEO can mitigate such effects.

Lastly, our findings widen our understanding of new venture entrepreneurship in the East Asian region. The East Asian market environment has been changing to support new venture growth, and these East Asian new ventures became important rivals of North American and European ventures. However, the prior research on new venture management has been predominantly focused on Western-based ventures (Hemmert et al. 2021). As the context for entrepreneurship occurrence and characteristics (Welter et al. 2017) matters, we apply the factors of entrepreneurship concerning the East Asian-based context. Our findings strengthen the idea that founder CEO and TMT-related factors have predictive power for the level of innovation and show that it also applies to the East Asian context. Furthermore, our incorporation of business group factors extends the discussion on the common organizational traits in the East Asian environment. We show that context-specific organizational factors should be considered in assessing a new venture’s behaviors and strategies.

5.2. Limitations and Future Research

This study has some limitations. First, executive departure can occur through the founder’s decision or voluntary leave. Future research is expected to analyze the impact on R&D investment by dividing it into voluntary and involuntary turnover, as in Xiong et al. (2021). In addition, while the information on the reason behind executive departure is unavailable, unexpected leave relative to voluntary leave may be a more concerning factor for new ventures. Future research should structure these types of turnovers to explore different aspects.

Second, in our study, executive turnover was measured through the ratio of executive leave to total employment size and then analyzed by using it as an independent variable. For this reason, the characteristics of each TMT member are not considered. Past research on TMT has focused on the CEO, but research has been spotlighted on individual TMT members, such as the chief financial officer, chief operating officer, chief technology officer (CTO), chief marketing officer, chief information officer, and chief strategy officer (Menz 2012). Even when evaluating the impact on venture R&D, it may be possible to reflect the characteristics of each sector by considering the type of TMT members. For example, Garms and Engelen (2019) showed that the CTO is a member of TMT that directly influences the R&D and innovation of a firm and analyzed the relationship between the characteristics of the CTO and the innovation commitment of other TMT members. It is expected that this aspect can also be considered when analyzing the relationship between executive turnover and R&D behaviors.

Third, cross-sectional data were used for the analysis. While our dataset provides an advantage in the sample size for new venture research, the time-variant aspect has not been addressed. This limitation necessitates further research using a longitudinal dataset.

Author Contributions

Conceptualization, H.C.; formal analysis, methodology, and validation, H.C.; writing–original draft preparation, H.C., P.L. and C.H.S.; writing–review and editing, P.L. and C.H.S.; project administration, P.L. and C.H.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Conflicts of Interest

The authors declare that they have no conflicts of interest.

Appendix A

{kind=link}

Table A1.

Variable definition.

| Variable | Definition |

|---|---|

| R&D intensity | the ratio of R&D investment to total sales |

| Executive turnover | the ratio of executive leave to total employment size |

| Work experience | the number of working years before founding the new venture |

| Business group experience | a dichotomous variable coded as “1” if a founder has worked for a business group affiliated firm before and “0” otherwise |

| Founding experience | the number of firms founded before founding the new venture |

| Firm size | a logarithmic value of total assets |

| ROA | a net income divided by total assets |

| Debt ratio | a total debt divided by total assets |

| Age | the number of years since the firm’s foundation |

| Capital financing | the size of capital raising divided by total assets |

Note. All variables are obtained from Korea Venture Business Association (https://venture.or.kr/#/home/home-main, accessed on 1 October 2021).

References

- Acharya, Viral, and Zhaoxia Xu. 2017. Financial dependence and innovation: The case of public versus private firms. Journal of Financial Economics 124: 223–43. [Google Scholar] [CrossRef] [Green Version]

- Acquaah, Moses. 2012. Social networking relationships, firm-specific managerial experience and firm performance in a transition economy: A comparative analysis of family owned and nonfamily firms. Strategic Management Journal 33: 1215–28. [Google Scholar] [CrossRef]

- Athanassiou, Nicholas, and Douglas Nigh. 2000. Internationalization, tacit knowledge and the top management teams of MNCs. Journal of International Business Studies 31: 471–87. [Google Scholar] [CrossRef]

- Bamford, Charles E., Thomas J. Dean, and Patricia P. McDougall. 2000. An examination of the impact of initial founding conditions and decisions upon the performance of new bank start-ups. Journal of Business Venturing 15: 253–77. [Google Scholar] [CrossRef]

- Bradley, Steven W., Dean A. Shepherd, and Johan Wiklund. 2011. The importance of slack for new organizations facing ‘tough’environments. Journal of Management Studies 48: 1071–97. [Google Scholar] [CrossRef]

- Chandler, Gaylen N., Benson Honig, and Johan Wiklund. 2005. Antecedents, moderators, and performance consequences of membership change in new venture teams. Journal of Business Venturing 20: 705–25. [Google Scholar] [CrossRef]

- Chang, Sea-Jin, Chi-Nien Chung, and Ishtiaq P. Mahmood. 2006. When and how does business group affiliation promote firm innovation? A tale of two emerging economies. Organization Science 17: 637–56. [Google Scholar] [CrossRef] [Green Version]

- Choi, Young Rok, and Dean A. Shepherd. 2004. Entrepreneurs’ decisions to exploit opportunities. Journal of Management 30: 377–95. [Google Scholar] [CrossRef]

- Choi, Young Rok, Shaker A. Zahra, Toru Yoshikawa, and Bong H. Han. 2015. Family ownership and R&D investment: The role of growth opportunities and business group membership. Journal of Business Research 68: 1053–61. [Google Scholar] [CrossRef]

- Chrisman, James J., and Pankaj C. Patel. 2012. Variations in R&D investments of family and nonfamily firms: Behavioral agency and myopic loss aversion perspectives. Academy of Management Journal 55: 976–97. [Google Scholar] [CrossRef]

- Coff, Russell W. 1999. When competitive advantage doesn’t lead to performance: The resource-based view and stakeholder bargaining power. Organization Science 10: 119–33. [Google Scholar] [CrossRef]

- Cooper, Arnold C., and Albert V. Bruno. 2000. Success among high technology firms. In Small Business: Critical Perspectives on Business Management. London and New York: Routledge, pp. 1183–91. [Google Scholar]

- Cooper, Arnold C., F. Javier Gimeno-Gascon, and Carolyn Y. Woo. 1994. Initial human and financial capital as predictors of new venture performance. Journal of Business Venturing 9: 371–95. [Google Scholar] [CrossRef]

- Cope, Jason. 2005. Toward a dynamic learning perspective of entrepreneurship. Entrepreneurship Theory Practice 29: 373–97. [Google Scholar] [CrossRef]

- Costa, Joana, Aurora A. C. Teixeira, and Anabela Botelho. 2020. Persistence in innovation and innovative behavior in unstable environments. International Journal of Systematic Innovation 6: 1–19. [Google Scholar] [CrossRef]

- Cummings, Trey, and Anne Marie Knott. 2018. Outside CEOs and innovation. Strategic Management Journal 39: 2095–119. [Google Scholar] [CrossRef]

- Dai, Guangrong, Kenneth P. De Meuse, and Dee Gaeddert. 2011. Onboarding externally hired executives: Avoiding derailment–accelerating contribution. Journal of Management & Organization 17: 165–78. [Google Scholar] [CrossRef]

- Dai, Shengli, Yingchun Li, and Wei Zhang. 2019. Personality traits of entrepreneurial top management team members and new venture performance. Social Behavior and Personality: An International Journal 47: 1–15. [Google Scholar] [CrossRef]

- De Cock, Robin, Petra Andries, and Bart Clarysse. 2021. How founder characteristics imprint ventures’ internationalization processes: The role of international experience and cognitive beliefs. Journal of World Business 56: 101163. [Google Scholar] [CrossRef]

- Deb, Palash, and Johan Wiklund. 2017. The effects of CEO founder status and stock ownership on entrepreneurial orientation in small firms. Journal of Small Business Management 55: 32–55. [Google Scholar] [CrossRef]

- Delmar, Frédéric, and Scott Shane. 2006. Does experience matter? The effect of founding team experience on the survival and sales of newly founded ventures. Strategic Organization 4: 215–47. [Google Scholar] [CrossRef]

- Dencker, John C., and Marc Gruber. 2015. The effects of opportunities and founder experience on new firm performance. Strategic Management Journal 36: 1035–52. [Google Scholar] [CrossRef]

- Dess, Gregory G., and Jason D. Shaw. 2001. Voluntary turnover, social capital, and organizational performance. Academy of Management Review 26: 446–56. [Google Scholar] [CrossRef]

- Eisenhardt, Kathleen M., and Claudia Bird Schoonhoven. 1990. Organizational growth: Linking founding team, strategy, environment, and growth among US semiconductor ventures, 1978–1988. Administrative Science Quarterly 35: 504–29. [Google Scholar] [CrossRef]

- Ensley, Michael D., Allison W. Pearson, and Allen C. Amason. 2002. Understanding the dynamics of new venture top management teams: Cohesion, conflict, and new venture performance. Journal of Business Venturing 17: 365–86. [Google Scholar] [CrossRef]

- Eva, Nathan, Alexander Newman, Qing Miao, Brian Cooper, and Kendall Herbert. 2019. Chief executive officer participative leadership and the performance of new venture teams. International Small Business Journal 37: 69–88. [Google Scholar] [CrossRef]

- Forés, Beatriz, and César Camisón. 2016. Does incremental and radical innovation performance depend on different types of knowledge accumulation capabilities and organizational size? Journal of Business Research 69: 831–48. [Google Scholar] [CrossRef] [Green Version]

- García-García, Raquel, Esteban García-Canal, and Mauro F. Guillén. 2017. Rapid internationalization and long-term performance: The knowledge link. Journal of World Business 52: 97–110. [Google Scholar] [CrossRef]

- Garms, Florian Peter, and Andreas Engelen. 2019. Innovation and R&D in the upper echelons: The association between the CTO’s power depth and breadth and the TMT’s commitment to innovation. Journal of Product Innovation Management 36: 87–106. [Google Scholar] [CrossRef] [Green Version]

- Gartner, William B., Barbara J. Bird, and Jennifer A. Starr. 1992. Acting as if: Differentiating entrepreneurial from organizational behavior. Entrepreneurship Theory and Practice 16: 13–32. [Google Scholar] [CrossRef]

- Geletkanycz, Marta A., and Donald C. Hambrick. 1997. The external ties of top executives: Implications for strategic choice and performance. Administrative Science Quarterly, 654–81. [Google Scholar] [CrossRef]

- Hashai, Niron, and Shaker Zahra. 2021. Founder team prior work experience: An asset or a liability for startup growth? Strategic Entrepreneurship Journal 16: 155–84. [Google Scholar] [CrossRef]

- Hemmert, Martin, Adam R. Cross, Ying Cheng, Jae-Jin Kim, Masahiro Kotosaka, Franz Waldenberger, and Leven J. Zheng. 2021. New venture entrepreneurship and context in East Asia: A systematic literature review. Asian Business Management, 1–35. [Google Scholar] [CrossRef]

- Hoskisson, Robert E., Michael A. Hitt, Richard A. Johnson, and Wayne Grossman. 2002. Conflicting voices: The effects of institutional ownership heterogeneity and internal governance on corporate innovation strategies. Academy of Management Journal 45: 697–716. [Google Scholar] [CrossRef]

- Johnson, Victoria. 2007. What is organizational imprinting? Cultural entrepreneurship in the founding of the Paris Opera. American Journal of Sociology 113: 97–127. [Google Scholar] [CrossRef]

- Klein, Howard J., and Paul W. Mulvey. 1995. Two investigations of the relationships among group goals, goal commitment, cohesion, and performance. Organizational Behavior Human Decision Processes 61: 44–53. [Google Scholar] [CrossRef]

- Kor, Yasemin Y. 2006. Direct and interaction effects of top management team and board compositions on R&D investment strategy. Strategic Management Journal 27: 1081–99. [Google Scholar] [CrossRef]

- Kor, Yasemin Y., and Andrea Mesko. 2013. Dynamic managerial capabilities: Configuration and orchestration of top executives’ capabilities and the firm’s dominant logic. Strategic Management Journal 34: 233–44. [Google Scholar] [CrossRef]

- Landstrom, Hans, and Donald L. Sexton. 2000. The Blackwell Handbook of Entrepreneurship. Oxford: Blackwell Business. [Google Scholar]

- Lester, Richard H., S. Trevis Certo, Catherine M. Dalton, Dan R. Dalton, and Albert A. Cannella Jr. 2006. Initial public offering investor valuations: An examination of top management team prestige and environmental uncertainty. Journal of Small Business Management 44: 1–26. [Google Scholar] [CrossRef]

- Mathias, Blake D., David W. Williams, and Adam R. Smith. 2015. Entrepreneurial inception: The role of imprinting in entrepreneurial action. Journal of Business Venturing 30: 11–28. [Google Scholar] [CrossRef]

- McDougall, Patricia Phillips, Jeffrey G. Covin, Richard B. Robinson Jr., and Lanny Herron. 1994. The effects of industry growth and strategic breadth on new venture performance and strategy content. Strategic Management Journal 15: 537–54. [Google Scholar] [CrossRef]

- Menz, Markus. 2012. Functional top management team members: A review, synthesis, and research agenda. Journal of Management 38: 45–80. [Google Scholar] [CrossRef]

- Nielsen, Sabina. 2010. Top management team internationalization and firm performance. Management International Review 50: 185–206. [Google Scholar] [CrossRef]

- O’brien, Robert M. 2007. A caution regarding rules of thumb for variance inflation factors. Quality & Quantity 41: 673–90. [Google Scholar] [CrossRef]

- Qian, Cuili, Qing Cao, and Riki Takeuchi. 2013. Top management team functional diversity and organizational innovation in China: The moderating effects of environment. Strategic Management Journal 34: 110–20. [Google Scholar] [CrossRef]

- Roberts, Edward B. 1991. The technological base of the new enterprise. Research Policy 20: 283–98. [Google Scholar] [CrossRef] [Green Version]

- Shane, Scott. 2000. Prior knowledge and the discovery of entrepreneurial opportunities. Organization Science 11: 448–69. [Google Scholar] [CrossRef]

- Shane, Scott, and Sankaran Venkataraman. 2000. The promise of entrepreneurship as a field of research. Academy of Management Review 25: 217–26. [Google Scholar] [CrossRef] [Green Version]

- Shepherd, Dean A., Andrew Zacharakis, and Robert A. Baron. 2003. VCs’ decision processes: Evidence suggesting more experience may not always be better. Journal of Business Venturing 18: 381–401. [Google Scholar] [CrossRef]

- Simon, Herbert A. 1978. Administrative Behavior. New York: The Free Press. [Google Scholar]

- Smith, Ken G., Ken A. Smith, Judy D. Olian, Henry P. Sims Jr., Douglas P. OBannon ’, and Judith A. Scully. 1994. Top management team demography and process: The role of social integration and communication. Administrative Science Quarterly 17: 412–38. [Google Scholar] [CrossRef]

- Suarez, Diana. 2014. Persistence of innovation in unstable environments: Continuity and change in the firm’s innovative behavior. Research Policy 43: 726–36. [Google Scholar] [CrossRef]

- Tribo, Josep A., Pascual Berrone, and Jordi Surroca. 2007. Do the type and number of blockholders influence R&D investments? New evidence from Spain. Corporate Governance: An International Review 15: 828–42. [Google Scholar] [CrossRef] [Green Version]

- Tzabbar, Daniel, and Jaclyn Margolis. 2017. Beyond the startup stage: The founding team’s human capital, new venture’s stage of life, founder–CEO duality, and breakthrough innovation. Organization Science 28: 857–72. [Google Scholar] [CrossRef]

- Welter, Friederike, Ted Baker, David B. Audretsch, and William B. Gartner. 2017. Everyday Entrepreneurship—A Call for Entrepreneurship Research to Embrace Entrepreneurial Diversity. Entrepreneurship Theory and Practice 41: 311–21. [Google Scholar] [CrossRef]

- Westhead, Paul, Deniz Ucbasaran, and Mike Wright. 2005. Decisions, actions, and performance: Do novice, serial, and portfolio entrepreneurs differ? Journal of Small Business Management 43: 393–417. [Google Scholar] [CrossRef]

- Xiong, Ran, Ping Wei, Jingyi Yang, and Luis Antonio Cristofini. 2021. Impact of top executive turnover on firms’ R&D investment: Evidence from China. Innovation 23: 400–24. [Google Scholar] [CrossRef]

Figure 1.

Theoretical Model.

Table 1.

Descriptive Statistics.

| Variable | Mean | St. Dev. | Min | Max |

|---|---|---|---|---|

| R&D intensity | 0.15 | 0.26 | 0 | 1.04 |

| Executive turnover | 0.02 | 0.13 | 0 | 2 |

| Work experience | 11.50 | 7.85 | 0 | 40 |

| Business group experience | 0.16 | 0.37 | 0 | 1 |

| Founding experience | 0.26 | 0.63 | 0 | 6 |

| Firm size | 7.58 | 1.44 | 2.04 | 12.95 |

| ROA | 0.01 | 0.12 | −0.30 | 0.14 |

| Debt ratio | 0.72 | 0.85 | −23.88 | 0.99 |

| Age | 5.51 | 1.33 | 2 | 7 |

| Capital financing | 0.27 | 0.93 | 0 | 13.32 |

Table 2.

Correlation Matrix.

| Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| 1. R&D intensity | |||||||||

| 2. Executive turnover | −0.01 | ||||||||

| 3. Work experience | −0.03 | 0.09 * | |||||||

| 4. Business group experience | −0.02 | 0.04 | 0.08 * | ||||||

| 5. Founding experience | 0.04 * | 0.03 | 0.11 * | −0.06 * | |||||

| 6. Firm size | −0.33 * | −0.06 * | 0.03 | 0.06 * | −0.00 | ||||

| 7. ROA | −0.42 * | −0.04 | 0.07 * | −0.01 | −0.05 * | 0.12 * | |||

| 8. Debt ratio | −0.17 * | −0.03 | 0.06 * | 0.01 | −0.04 * | 0.24 * | 0.25 * | ||

| 9. Age | −0.14 * | −0.04 | −0.03 | 0.03 | −0.04 | 0.21 * | 0.02 | 0.03 | |

| 10. Capital financing | 0.26 * | 0.02 | −0.08 * | −0.02 | 0.06 * | −0.27 * | −0.11 * | −0.42 * | −0.17 * |

Note: * p < 0.05.

Table 3.

Regression Results.

| Model 1 | Model 2 | Model 3 | Model 4 | |

|---|---|---|---|---|

| Executive turnover | −0.062 ** | −0.105 ** | −0.083 ** | −0.067 ** |

| (0.010) | (0.006) | (0.001) | (0.008) | |

| Executive turnover × Work experience | 0.005 ** | |||

| (0.009) | ||||

| Executive turnover × Business group experience | 0.084 † | |||

| (0.094) | ||||

| Executive turnover × Founding experience | 0.019 * | |||

| (0.047) | ||||

| Work experience | 0.001 † | |||

| (0.097) | ||||

| Business group experience | 0.001 | |||

| (0.105) | ||||

| Founding experience | 0.001 | |||

| (0.143) | ||||

| Firm size | −0.033 *** | −0.026 *** | −0.033 *** | −0.033 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| ROA | −0.646 *** | −0.341 *** | −0.646 *** | −0.647 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| Debt ratio | −0.033 | −0.023 * | −0.033 | −0.034 |

| (0.187) | (0.032) | (0.188) | (0.186) | |

| Age | −0.004 | −0.001 | −0.004 | −0.004 |

| (0.428) | (0.707) | (0.416) | (0.434) | |

| Capital financing | 0.197 *** | 0.112 *** | 0.197 *** | 0.197 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| Constant | 0.399 *** | 0.301 *** | 0.399 *** | 0.399 *** |

| (0.000) | (0.000) | (0.000) | (0.000) | |

| ∆R2 | 0.255 | 0.273 | 0.254 | 0.254 |

| F value | 23.92 | 30.13 | 18.56 | 18.09 |

Note. *** p < 0.001, ** p < 0.01, * p < 0.05, † p < 0.1.

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Cho, H.; Lee, P.; Shin, C.H. Executive Turnover and Founder CEO Experience: Effect on New Ventures’ R&D Investment. Economies 2022, 10, 97. https://0-doi-org.brum.beds.ac.uk/10.3390/economies10050097

AMA Style

Cho H, Lee P, Shin CH. Executive Turnover and Founder CEO Experience: Effect on New Ventures’ R&D Investment. Economies. 2022; 10(5):97. https://0-doi-org.brum.beds.ac.uk/10.3390/economies10050097

Chicago/Turabian StyleCho, Hyejin, Pyoungsoo Lee, and Choong Ho Shin. 2022. "Executive Turnover and Founder CEO Experience: Effect on New Ventures’ R&D Investment" Economies 10, no. 5: 97. https://0-doi-org.brum.beds.ac.uk/10.3390/economies10050097

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.