1. Introduction

The stock market becomes a crucial key for the development of the financial system in developing countries. The stock market provides opportunities for both new or experienced investors to increase their wealth [

1]. However, the stock market is risky given the unpredictable price of the market, and this makes stock trading attractive to aggressive or high-risk appetite investors, as they pursue the old advice of buying low and selling high. In Malaysia, the Chinese have the highest average wealth of RM 128,325, 76% and 47% higher than Malays and Indians, respectively [

2]. This evidence indicates the high correlation between ethnicity and investment behavior in relation to future financial decision-making [

3]. During the Covid-19 outbreak, many countries suffered an economic recession. Back on the 27 March 2020, the Malaysian government announced a national economic stimulus package, specifically known as the Prihatin Rakyat Economic Stimulus Package 2020 (PRIHATIN Package), allocating RM 250 billion to ease the financial burden of Malaysian citizens and another RM 10 billion to ease the financial burden of small and medium-sized enterprises (SMEs). Due to the uncertainties caused by the Covid-19 outbreak, major shareholders of some listed companies even disposed their shares during the first few trading days when the movement control order (MCO) was enforced [

4].

Over the years, the Malaysian government has tried to promote stock market investment among Malaysians who otherwise would generally deposit their money into various savings schemes that provide very little returns. Therefore, it is crucial to understand human behavior and decision-making from a financial perspective and examine factors that influence stock market investment intention among Malaysian working adults. In addition, investors need to develop a positive vision, foresight, patience, and drive [

5]. Many factors influence investment stock market participation, such as cognitive and emotional weaknesses, risk tolerance, financial well-being, financial literacy, overconfidence bias, demographic characteristics, herding behavior, social interaction, income level, and investment intention [

6]. There is a need to determine how these factors can influence stock market participation among the working adults in Malaysia.

According to the theory of planned behavior (TPB), behavioral achievement can be obtained through behavioral intention. Hence, when a behavior or situation affords a person complete control over behavioral performance, behavioral intention alone should be sufficient to predict the behavior [

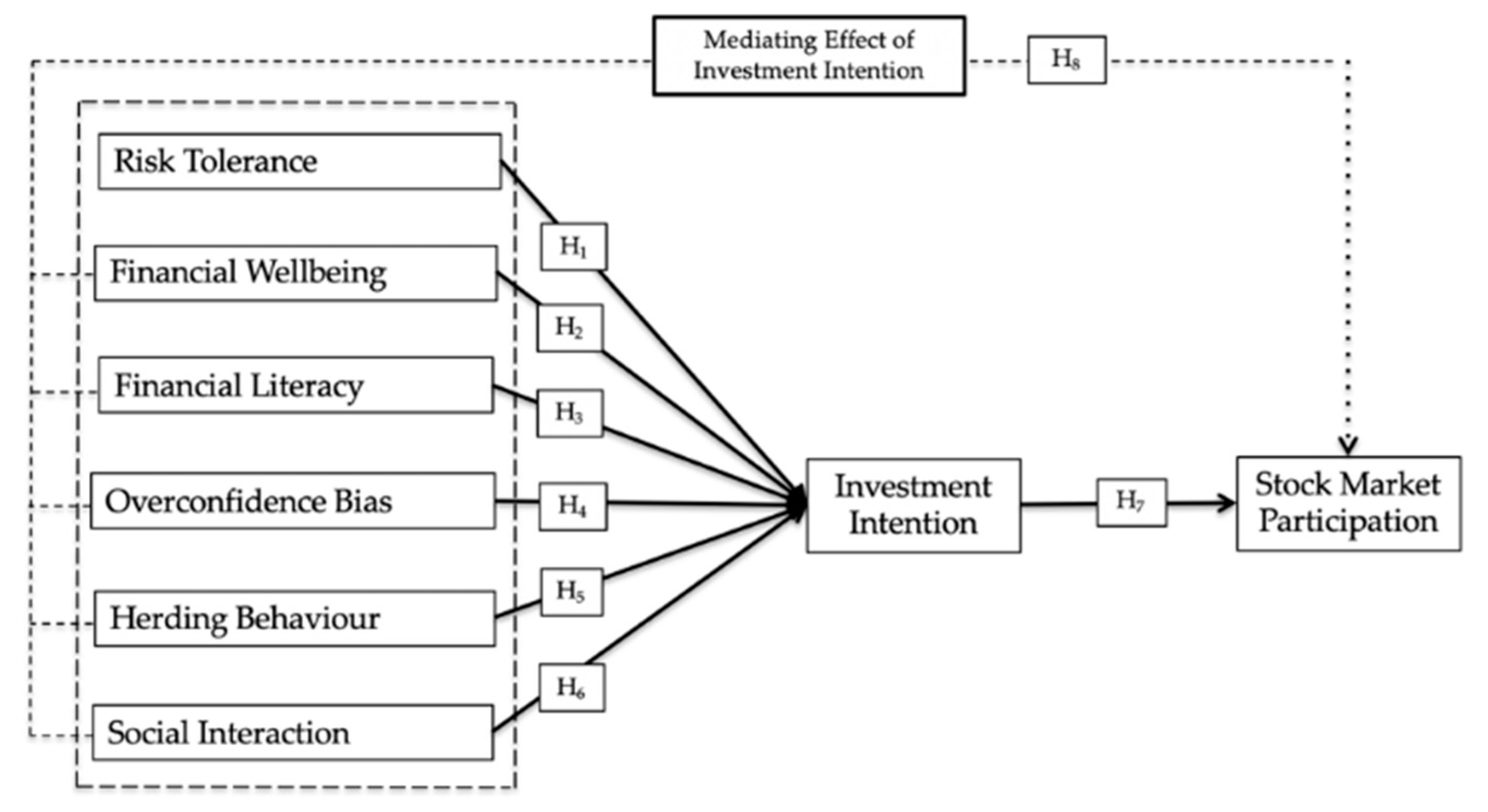

7]. Therefore, this study attempted to examine the relationships of risk tolerance, financial well-being, financial literacy, overconfidence bias, herding behavior, social interaction, stock market investment intention, and stock market participation within the Malaysian context.

5. Discussion

This study aimed to investigate the mediating effect of stock market investment intention on the relationships of selected constructs with stock market participation within the Malaysian context. This study verified the significant positive effect of risk tolerance on stock market investment intention, which is compatible with the findings of a study by Fauzi, Husniyah, and Amim [

14]. The study specifically stated that risk-takers tend to be involved in stock market investment. The perception towards one’s capability to control stock investment decisions is also important due to the influence of the individual’s confidence in the stock investment market. Besides that, the relationship between herding behavior and stock market investment intention was also found statistically significant. This particular finding is consistent with the finding of a prior study [

47]. Kumari et al. [

47] identified herding behavior as a specific investment-related behavior that an investor assumes in combating the volatility of the stock market. With the lack of knowledge and restricted information, many investors concurrently replicate the actions of other investors. Meanwhile, social interaction in this study was found to exhibit a significant effect on stock market investment intention. This particular finding supports the finding of a study by Wu et al. [

31], which stated that there is a major impact of social interaction on stock market investment intention. Inexperienced investors can acquire both higher utilitarian and hedonic values from social values, and stock market investment intention relies more on hedonic values. Meanwhile, experienced investors place greater emphasis on utilitarian values. In addition, Shanmugham and Ramya [

30] revealed that social interaction (e.g., social media and information from close friends) promotes stock market investment intention and subsequently increases stock market participation.

Furthermore, this study demonstrated the significant effect of stock market investment intention on stock market participation. Sarwar and Afaf [

15] stated that stock market investment intention plays a crucial role in the relationship between risk tolerance and herding behavior. However, this study demonstrated insignificant effects of financial well-being, financial literacy, and overconfidence bias on stock market investment intention. The findings of this study are not in line with the findings of previous studies [

12,

26]. These studies highlighted that understanding the factors that contribute to or detract from the acquisition of financial literacy among working adults can help in making policy interventions targeted at working adults for a higher level of financial well-being.

In addition, this study evidenced that the contradictory findings may be caused by the differences in demographic characteristics. The current study argued that female working adults generally possess higher financial literacy than male working adults. In most cases, a higher educational level was also found to be a significant indicator of higher financial knowledge, financial attitude, financial behavior, and financial literacy. Moreover, employment status, annual income, and financial socialization were also found to influence financial knowledge, financial well-being, overconfidence bias, and financial literacy at the individual level. In addition, this study argued the propensity of the Chinese to have a better understanding of investment for asset prospects in the future compared to other ethnic groups in Malaysia.

Adding to that, this study investigated the mediating effect of stock market investment intention. This study proved that stock market investment intention mediates the effects of risk tolerance and overconfidence bias on stock market participation within the context of developing countries. On the other hand, this study proved that the intention to invest among the majority of Malaysian working adults does not mediate the effects of certain factors on stock market participation, such as financial well-being, financial literacy, herding behavior, and social interaction.

Nonetheless, this study argued the different rates of stock market participation across countries, specifically between developing and developed countries, which generally increases with wealth. Moreover, at a higher wealth level, working adults in developing countries, such as Malaysia, do not hold stock, as they make a rational choice of not holding part of their assets in the stock market given their lack of financial literacy and inability to imitate the activities of other investors (of disregarding their own personal information and expectations). Meanwhile, working adults in developed countries have a better understanding of investing part of their assets in the stock market for higher income.

Majority of respondents in this study are employees with an annual income below RM 24,000, and the respondents in this study are dominated by young women with higher education graduates. These findings indicated that respondents in this study need a better understanding of stock market investment to gain their income and self-confidence. In addition, lack of investment knowledge and intentions become barriers for them to participate in the stock market. Perkins and Jones [

48] stress the importance of demographics and hypothesized that different demographics generally have a different outlook on finance and spending. These factors translate into market dynamics that can be leveraged while selecting a portfolio. They emphasize creating a consistent and habitual savings and investing plan. Therefore, based on the statistical correlation in this study, financial wellbeing, financial literacy, and overconfidence bias had no significant relationship on stock market investment among Malaysian working adults.

The majority of Malaysian working adults in this study is dominated by female worker around 18 to 30 years old, with 84.8%. These findings showed that the participation of women is more sensitive towards stock market investment in Malaysia. The participants of Chinese (92.8%) who hold a bachelor’s degree tend to have a better understanding of the stock market. Consequently, these results pointed out that Chinese employees had a greater intention to gain their knowledge, investment, and income. Moreover, based on received data from respondents, 58.2% of respondents in this study have an annual income below Rm.24.000. This indicated that Malaysia’s stock market investment has big potential to motivate Malaysian working adults with annual income under RM. 24.000 to invest their money or disposable income in the stock market to gain their income in SMI. Working adults in developing countries tend to score low on financial knowledge, financial attitude, financial behavior, and financial literacy. Therefore, an individual’s perception and financial opportunity recognition are important to obtain Malaysian working adults’ intentions in stock market investment. This finding is also supported in the study by Garg and Singh [

12], which stated that educational status, employment status, and family background play important factors to determine if high financial knowledge, financial attitude, financial behavior, and financial literacy of Participants.

6. Theory and Practical Implications

One of the major contributions of this study came from the development of stock market investment intention among working adults in relation to their investment decision-making processes from different behavioral perspectives. This study argued the importance of risk tolerance and overconfidence bias as predictors of working adult’s participation in the stock market through stock market investment intention. Practitioners need to develop a better understanding of the significant factors that affect stock market investment intention among working adults. Based on the findings of this study, it is suggested that increasing such investing capabilities can increase the willingness to invest in the stock market. Besides that, financial advisors may consider conducting financial training to equip working adults with knowledge before making any investment, and this may also encourage them to be more involved in their investment decisions. The nature of such training is important, as it provides information and a sense of connection to build involvement. Moreover, the findings of this study on stock market participation and the mediating effect of stock market investment intention within the context of working adults in developing countries have also extended the current literature on behavioral finance and behavioral theories, such as TPB. The practical contribution of this study is that the capital market and security authority have to put more events and workshops in place for Malaysian working adults. Moreover, the capital market and security authority (CMSA) need to motivate and provide adequate training, seminars, and awareness among working adults on the potential benefits of investing in the stock market in Malaysia. Thus that the individual has a better understanding of the stock market in the future. Other factors that might influence financial wellbeing, financial wellbeing, and overconfidence bias on stock market participation, such as income, mindset, culture, and gender, should be investigated. As a consequence, this will give more comprehensive results and influence more individuals to participate in the stock market.

,

,

{kind=link}