1. Introduction

Environmental issues have attracted serious attention of governments around the world. These problems are closely related to the consumption of natural resources and the pollutant emissions of different industries. Among these environmental issues, high-polluting industries are important sources of pollutant emissions, and can even trigger some extreme weather events, such as sandstorms and smog. A recent study indicates that the frequency of smog in regions with concentrated high-polluting industries is much higher than that in other regions [

1]. However, high-polluting firms are also the main driving force for economic growth, especially in developing countries [

2]. There is an argument about whether we should protect the environment with restricting the operations of high-polluting firms, or destroy the environment with enhancing the role of high-polluting firms in economic growth. In order to solve this problem, high-polluting firms need to adopt technological innovations for reducing pollutant emissions, such as improving resource utilization and reducing energy consumption [

3].

During the economic development of developing countries, high-polluting industries play an important role in economic activities. Among developing countries, China is the biggest economy and has the largest population. High-polluting industries in China include thermal power, steel, metallurgy, building materials, mining and so on, and the contribution of high-polluting industries to China’s gross domestic product (GDP) is 36.1% in 2018 [

4]. The local governments demand high-polluting industries to support the development of regional economies, but high-polluting industries can also threaten the ecological environment by pollution emissions [

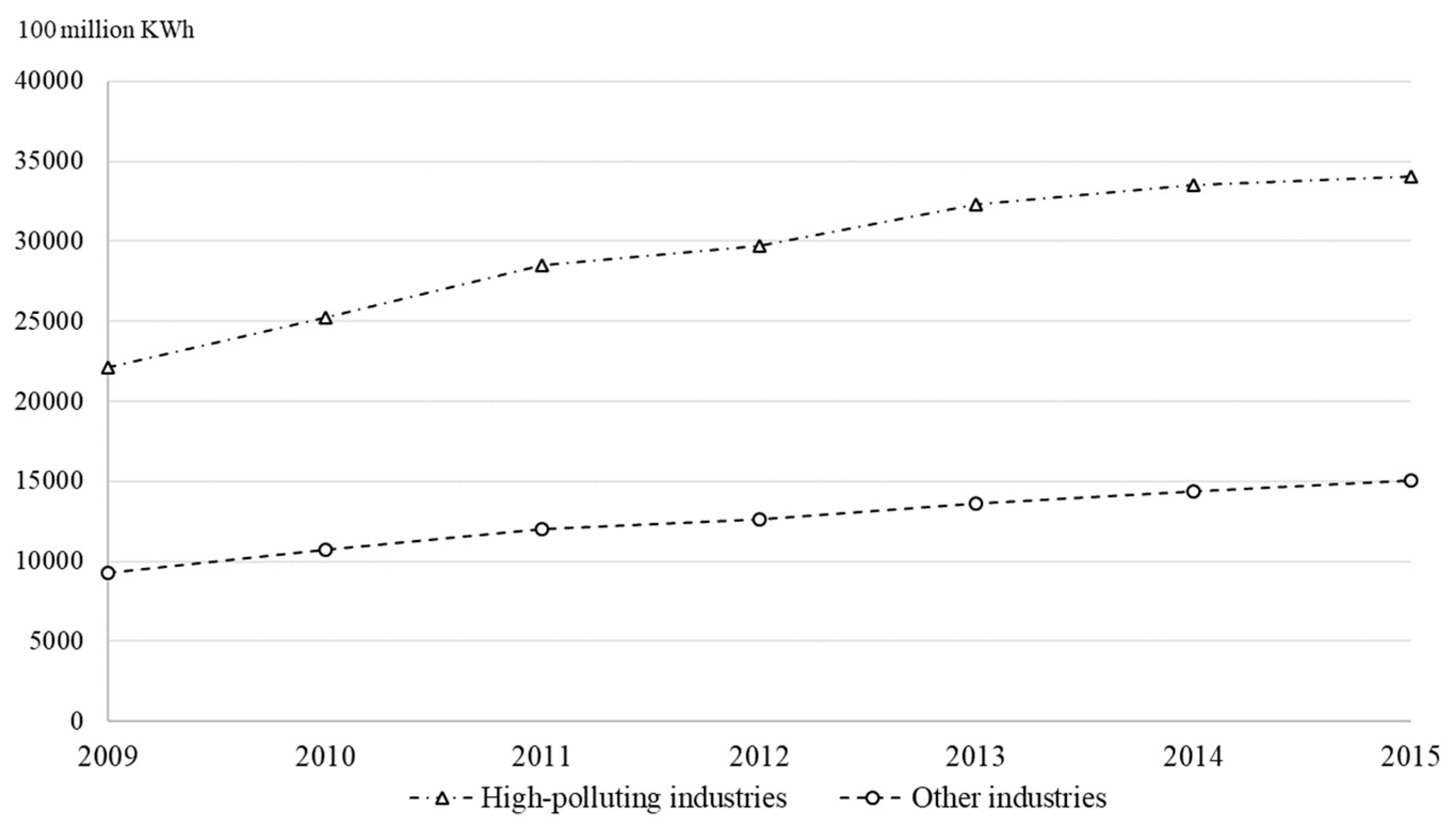

5]. As shown in

Figure 1, the energy consumption of China’s high-polluting industries has been rising in recent years [

4]. According to

Figure 2, the operations of high-polluting industries need to be supported by more and more electricity consumption, and the energy demand of high-polluting industries is much higher than that of other industries [

4]. Compared with other developing countries, China pays more attention to sustainable development, and has enacted many laws and regulations for environmental protection, such as the Law of Energy Conservation (2007), the Law of Cleaner Production Promotion (2012), the Law of Air Pollution Control (2018) [

6]. Faced with China’s sustainable development strategy, high-polluting firms bear huge pressure from environmental protection. In addition, the proportion of state-owned enterprises in China’s high-polluting industries is relatively large, and they suffer more due to strict environmental policy and energy resource constraints [

7]. State-owned enterprises in China can be backed by government, and focus on promoting the image of the central government. However, non-state-owned enterprises rely on the support of investors, and their behaviors in environmental protection can influence investors’ support [

8]. In this situation, how to resolve the conflict between environmental protection and environmental damage has become an important issue for China’s high-polluting firms.

In order to realize sustainable development, technological innovation can improve the growth of high-polluting firms with environmental benefits [

9]. The outcomes of technological innovation can reduce the pollutant emission and energy consumption of high-polluting firms. In addition, innovation performance can reflect the investments and efforts of firms’ technological innovation in different industries [

10]. In this paper, we focus on the outcomes of innovation, and use the number of patent to measure innovation performance. High-polluting firms can benefit from their innovation performance with resource utilization and energy consumption. The innovation performance of high-polluting firms can be driven by different factors, such as market factor, competitor factor, government factor and so on [

11]. Actually, high-polluting firms’ technological innovation may be affected by their proactive motivation or passive pressure. In terms of firms’ proactive motivation, corporate social responsibility requires firms to take responsibility for shareholders and environment during creating profits and bearing legal responsibilities [

3]. In the signal theory, corporate social responsibility can convey information about sustainable strategies to all stakeholders, and represent the firms’ actual activities for environmental protection and social contribution [

8]. Compared with other industries, corporate social responsibility performance of high-polluting firms can contain more information about corporate practices in environmental protection [

12]. Therefore, high-polluting firms are willing to use technological innovation to support corporate practices in social contribution, and obtain more environmental benefits [

13]. In terms of firms’ passive pressure, more and more people have paid attention to high-polluting industries due to pollutant emissions. Public attention, as the legitimacy-granting institution, can supervise the operations of high-polluting firms in real time [

14]. Some behaviors of high-polluting firms will be restricted by public attention, such as energy consumption and pollutant emission. This passive pressure can promote high-polluting firms to make more contributions to environmental protection and social stability [

15]. Based on the legitimacy theory, public attention can encourage high-polluting firms to concentrate on the practices of environmental protection [

14]. Combining the proactive motivation and passive pressure, the association among corporate social responsibility, public attention and innovation performance has become a key factor in promoting the innovation performance of high-polluting firms, as well as resolving the conflict between environmental protection and environmental damage.

This paper explores the influence factors of innovation performance for high-polluting firms, and provides a better understanding of the relationship among corporate social responsibility, public attention and innovation performance. A panel data model is constructed based on a sample of Chinese listed firms in high-polluting industries from 2011 to 2016. The empirical results show that there is a positive association between corporate social responsibility and innovation performance, as well as public attention. Considering different ownership structure, the public attention of state-owned enterprises has a stronger impact on their innovation performance, indicating that passive pressure can bring more motivations of innovation performance to such high-polluting firms. Moreover, corporate social responsibility plays a stronger role in promoting the innovation performance of non-state-owned enterprises, and these firms actively convey information about corporate practices for environmental protection and social contribution. The differences between state-owned enterprises and non-state-owned enterprises demonstrate that the ownership structure of high-polluting firms may affect their technological innovations. State-owned enterprises with more resources and policy supports face more pressure from public attention. Non-state-owned enterprises relying on the external investments emphasize the importance of corporate social responsibility in reflecting their sustainable strategies. After introducing the pressure of regional economies, the innovation performance of high-polluting firms is hindered, but the impacts of corporate social responsibility and public attention are significantly strengthened, indicating that local governments are potential factors for innovation performance in high-polluting industries.

Our paper makes several contributions. First of all, it constructs a novelty research framework to explore the influence factors of innovation performance for high-polluting firms. We use corporate social responsibility and public attention to reveal the proactive motivation and passive pressure of high-polluting firms. Secondly, it explores the differences between state-owned enterprises and non-state-owned enterprises, such as the impacts of corporate social responsibility and public attention. High-polluting firms with different ownership structure can develop various innovation strategies based on their specific advantages, which will help them to get more environmental benefits. Finally, considering the role of local governments in China, the impact of regional economic pressure on innovation performance is analyzed at the province level, and it will help high-polluting firms cope with the conflict between macro-economic objectives and micro-environmental contributions.

The structure of this paper is as follows:

Section 2 provides the background on innovation performance and the research hypotheses.

Section 3 introduces the research methods, including samples, variables, and research models.

Section 4 presents the empirical results, including the descriptive statistical analysis and the regression analysis.

Section 5 provides the discussion of empirical results. The conclusions and recommendations are drawn in

Section 6.

5. Discussion

Faced with the topics related to environmental deterioration, high-polluting firms need to take advantage of technological innovations to implement their sustainable strategies. In terms of social contributions, the corporate social responsibility of high-polluting firms can promote their innovation performance. Considering the social expectations of high-polluting industries, the public attention of high-polluting firms can motivate their innovation performance as well. Our empirical results are consistent with the findings of Cheng and Liu and Wu et al. [

14,

32]. Just like the discussion of government factors in Chen et al., the pressure of regional economies can inhibit the innovation performance of high-polluting firms, due to the pressure from local governments [

45]. It is worth noting that this kind of pressure can strengthen the positive impacts of corporate social responsibility and public attention, so that high-polluting firms should deal with the relationship between productivity losses and environmental benefits.

Considering the impact of ownership characteristics, corporate social responsibility and public attention can promote the innovation performance of state-owned enterprises, which supports the findings of Han et al. [

52]. Furthermore, the pressure of regional economies will inhibit the innovation performance of state-owned enterprises. This may be because local governments provide sufficient support for state-owned enterprises, and require them to achieve some economic goals. Faced with the pressure from local governments, state-owned enterprises may choose to expand the scale of production instead of promoting technological innovations. On the other hand, corporate social responsibility and public attention can also promote the innovation performance of non-state-owned enterprises. Comparing with the results of Huang et al., the pressure of regional economies cannot directly influence the innovation performance of non-state-owned enterprises [

15]. In this scenario, non-state-owned enterprises have significant differences with state-owned enterprises in terms of resource acquisition and policy support. Non-state-owned enterprises prefer to convey information about sustainable strategies, and promote their innovation performance to obtain more investments from all stakeholders [

65].

For high-polluting firms, technological innovation can help to implement sustainable strategies, and achieve long-term development. During the operations of high-polluting firms, their energy consumption and pollutant emission are closely related to environmental issues, and resolving these environmental problems will be the key step in their long-term development. High-polluting firms have to deal with the pressure of local governments, and satisfy the expectations of society. They need to rely on technological innovation to support their behaviors for environmental protection. During the operations of high-polluting firms, corporate social responsibility, as a proactive motivation, can convey information about environmental protection through technological innovation. Public attention, as a passive pressure, will bring more motivations for high-polluting firms to promote their innovation performance. From the perspective of sustainable development, it is necessary to take advantages of the relationship among corporate social responsibility, public attention and innovation performance for high-polluting industries. This relationship will provide guarantees for environmental benefits to all stakeholders of high-polluting firms.

6. Conclusions and Recommendations

6.1. Conclusions

Technological innovation is a key element of sustainable development for different firms, and has an important impact on resource utilization. High-polluting industries, as the main driving force of economic growth, have been closely linked to environmental issues for a long time. From the perspective of sustainable development, the debate between environment and economy is that whether we should protect the environment by reducing production, or destroy the environment for increasing revenue. In this situation, high-polluting firms need to explore the balance between profitability and sustainability, and the resource utilization and energy consumption become the key factors in this relationship. High-polluting firms should ameliorate their operations through technological innovation, thus achieving long-term development. Furthermore, the technological innovations of high-polluting firms can provide more environmental benefits and make more social contributions. The corporate social responsibility of high-polluting firms can convey information about corporate practices on environmental protection, and can be seen as a kind of signal for investors. High-polluting firms need to satisfy different social expectations, so that public attention has become a kind of legitimacy-granting institutions with informal supervision mechanism. Based on the signal theory and legitimacy theory, exploring the potential relationship among corporate social responsibility, public attention and innovation performance have become the determining factor of technological transition in the Chinese high-polluting industries.

In this study, we use a sample of listed high-polluting firms in the Chinese market from 2011 to 2016, and explore the impacts of corporate social responsibility and public attention on innovation performance. The Negative Binomial Regression method was chosen to empirically analyze the overall sample and subsamples (the subsample of state-owned enterprises and non-state-owned enterprises), and the impact of regional economies is also discussed. Empirically, we find that there is a positive relationship between corporate social responsibility and innovation performance of high-polluting firms, as well as public attention, indicating that the proactive motivation and passive pressure of high-polluting firms can promote their technological innovations. Corporate social responsibility is an important channel of delivering information about corporate activities for high-polluting firms, and reveals their social contribution and environmental protection. In order to gain more investors’ support, high-polluting firms need to try some new technological innovations to improve resource utilization, and reduce energy consumption. In addition, more and more people pay attention to the relationship between high-polluting industries and environmental issues. Public attention, as a passive pressure, has become a legitimacy-granting institution. Faced with this passive pressure, high-polluting firms should implement some sustainable strategies for reducing pollutant emission, thereby promoting the image of the central government. Furthermore, the pressure of regional economies cannot be ignored in the Chinese market, and the conflict between economy and environment may also have a corresponding impact on the innovation performance of high-polluting firms. Considering government factors, high-polluting firms should pay more attention to sustainable strategies, so as to promote technological innovations and maintain environmental benefits.

For high-polluting firms with different ownership structure, state-owned enterprises have obvious advantages in terms of the assets size and resource acquisition, so that they can receive sufficient support from local governments. Public attention will have a significant impact on the impression management of state-owned enterprises. Therefore, state-owned enterprises in high-polluting industries bear this passive pressure from social expectations. However, non-state-owned enterprises have difficulty in obtaining government resources, and their operations rely on the external investments. In order to gain investor’s support, non-state-owned enterprises need to convey information about social and environmental benefits to all stakeholders. In this situation, non-state-owned enterprises should pay more attention to corporate practices in environmental protection and social stability. In addition, state-owned enterprises suffer from the pressure of regional economies, which has a negative impact on their innovation performance. The pressure of regional economies can change the impacts of corporate social responsibility and public attention on the innovation performance of non-state-owned enterprises. High-polluting firms with different ownership structure should take advantage of proactive motivation or passive pressure to promote their innovation performance based on their specific advantages.

During exploring the influence factors of innovation performance in high-polluting industries, our results demonstrate that corporate social responsibility and public attention can significantly promote technological innovations. Corporate social responsibility can deliver more information about sustainable strategies of high-polluting firms, which is a signal of corporate environmental practices. Public attention, as a legitimacy-granting institution, can regulate the behaviors of high-polluting firms. The proactive motivation or passive pressure of high-polluting firms can promote technological innovation, and help to achieve the goal of improving resource utilization and reducing energy consumption.

6.2. Recommendations and Limitations

We focus on the innovation performance of high-polluting firms in our empirical analysis, and discuss the differences between the results of state-owned enterprises and non-state-owned enterprises. Considering the potential impact of local governments, high-polluting firms should deal with the relationship between environment and economy. Based on empirical results and conclusions, we propose the following recommendations:

First, high-polluting firms need to consider the influence factors of technological innovation from the perspective of firms’ proactive motivation. Corporate social responsibility can reflect the social contributions and environmental benefits of high-polluting firms for all stakeholders. High-polluting firms should balance the relationship between economic growth and environmental protection. Conveying information about innovation performance can help to get more and more support from investors, thus increasing the profitability of high-polluting firms.

Second, public attention can regulate the behaviors of high-polluting firms, and then motivate them to perform more environmental practices. High-polluting firms need to perform different socially expected activities, and take advantage of these social contracts to promote technological innovation. Understanding this passive pressure from social expectations can help high-polluting firms to achieve sustainable development.

There are also some limitations existing in this paper. In terms of time dimension, we select the data of listed companies from 2011 to 2016, and the time span may not fully demonstrate the relationship among corporate social responsibility, public attention and innovation performance. We obtain two subsamples, namely state-owned enterprises and non-state-owned enterprises. However, some non-state-owned enterprises are as good as state-owned enterprises, which makes the method of dividing samples imperfect. Combined with these limitations, future research on the innovation performance of high-polluting firms can consider a longer time span, and this will incorporate the impact of economic cycle into empirical analysis. In addition, the research sample can be divided into various subsamples by different methods, exhibiting the comprehensive relationship among corporate social responsibility, public attention and innovation performance of high-polluting firms.

,

,

{kind=link}

{kind=link}

{kind=link}