Exploring the Impact of Corporate Social Responsibility Communication through Social Media on Banking Customer E-WOM and Loyalty in Times of Crisis

,

,  ,

,  ,

,  ,

,  and

and

Abstract

:1. Introduction

2. Theory and Hypotheses

3. Methodology

3.1. Population, Sample, and the Handling of Social Desirability

3.2. Measures

4. Results and Analysis

Hypotheses Testing

5. Discussion and Implications

Limitations and Direction for Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Sharma, S.; Singh, S.; Kujur, F.; Das, G. Social Media Activities and its Influence on Customer-Brand Relationship: An Empirical Study of Apparel Retailers’ Activity in India. J. Theor. Appl. Electron. Commer. Res. 2020, 16, 602–617. [Google Scholar] [CrossRef]

- Shahbaznezhad, H.; Dolan, R.; Rashidirad, M. The Role of Social Media Content Format and Platform in Users’ Engagement Behavior. J. Interact. Mark. 2021, 53, 47–65. [Google Scholar] [CrossRef]

- Hajli, N. The impact of positive valence and negative valence on social commerce purchase intention. Inf. Technol. People 2019, 33, 774–791. [Google Scholar] [CrossRef]

- Hajli, N.; Featherman, M.S. Social commerce and new development in e-commerce technologies. Int. J. Inf. Manag. 2017, 37, 177–178. [Google Scholar] [CrossRef]

- Ma, L.; Zhang, X.; Ding, X.; Wang, G. How social ties influence customers’ involvement and online purchase intentions. J. Theor. Appl. Electron. Commer. Res. 2020, 16, 395–408. [Google Scholar] [CrossRef]

- Chatterjee, S.; Kar, A.K. Why do small and medium enterprises use social media marketing and what is the impact: Empirical insights from India. Int. J. Inf. Manag. 2020, 53, 102103. [Google Scholar] [CrossRef]

- Voorveld, H.A. Brand communication in social media: A research agenda. J. Advert. 2019, 48, 14–26. [Google Scholar] [CrossRef]

- Social, W.A. Digital 2020: 3.8 billion people use social media. Dostupné 2020, 15, 2020. [Google Scholar]

- Ahmad, N.; Naveed, R.T.; Scholz, M.; Irfan, M.; Usman, M.; Ahmad, I. CSR Communication through Social Media: A Litmus Test for Banking Consumers’ Loyalty. Sustainability 2021, 13, 2319. [Google Scholar] [CrossRef]

- Wang, R.; Huang, Y. Communicating corporate social responsibility (CSR) on social media. Corp. Commun. Int. J. 2018, 23, 326–341. [Google Scholar] [CrossRef]

- Sreejesh, S.; Sarkar, J.G.; Sarkar, A. CSR through social media: Examining the intervening factors. Mark. Intell. Plan. 2019, 38, 103–120. [Google Scholar] [CrossRef]

- Kucukusta, D.; Perelygina, M.; Lam, W.S. CSR communication strategies and stakeholder engagement of upscale hotels in social media. Int. J. Contemp. Hosp. Manag. 2019, 31, 2129–2148. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate social responsibility: Evolution of a definitional construct. Bus. Soc. 1999, 38, 268–295. [Google Scholar] [CrossRef]

- Barauskaite, G.; Streimikiene, D. Corporate social responsibility and financial performance of companies: The puzzle of concepts, definitions and assessment methods. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 278–287. [Google Scholar] [CrossRef]

- Mahmood, A.; Bashir, J. How does corporate social responsibility transform brand reputation into brand equity? Economic and noneconomic perspectives of CSR. Int. J. Eng. Bus. Manag. 2020, 12, 1847979020927547. [Google Scholar] [CrossRef]

- Kong, L.; Sial, M.; Ahmad, N.; Sehleanu, M.; Li, Z.; Zia-Ud-Din, M.; Badulescu, D. CSR as a potential motivator to shape employees’ view towards nature for a sustainable workplace environment. Sustainability 2021, 13, 1499. [Google Scholar] [CrossRef]

- George, N.A.; Aboobaker, N.; Edward, M. Corporate social responsibility and organizational commitment: Effects of CSR attitude, organizational trust and identification. Soc. Bus. Rev. 2020, 15, 255–272. [Google Scholar] [CrossRef]

- Ahmad, N.; Scholz, M.; Ullah, Z.; Arshad, M.; Sabir, R.; Khan, W. The Nexus of CSR and Co-Creation: A Roadmap towards Consumer Loyalty. Sustainability 2021, 13, 523. [Google Scholar] [CrossRef]

- Castro-González, S.; Bande, B.; Fernández-Ferrín, P.; Kimura, T. Corporate social responsibility and consumer advocacy behaviors: The importance of emotions and moral virtues. J. Clean. Prod. 2019, 231, 846–855. [Google Scholar] [CrossRef]

- Shabib, F.; Ganguli, S. Impact of CSR on consumer behavior of Bahraini women in the cosmetics industry. World J. Entrep. Manag. Sustain. Dev. 2017, 13, 174–203. [Google Scholar] [CrossRef]

- Sousa, B.; Silva, A.; Malheiro, A. Differentiation and market loyalty: An approach to cultural tourism in northern Portugal. In Crisis Management for Software Development and Knowledge Transfer; Metzler, J.B., Ed.; Springer: Singapore, 2019; pp. 681–690. [Google Scholar]

- Brady, M.K.; Bourdeau, B.L.; Heskel, J. The importance of brand cues in intangible service industries: An application to investment services. J. Serv. Mark. 2005, 19, 401–410. [Google Scholar] [CrossRef]

- Markovic, S.; Iglesias, O.; Singh, J.J.; Sierra, V. How does the perceived ethicality of corporate services brands influence loyalty and positive word-of-mouth? Analyzing the roles of empathy, affective commitment, and perceived quality. J. Bus. Ethic. 2015, 148, 721–740. [Google Scholar] [CrossRef]

- Grönroos, C. Adopting a service logic for marketing. Mark. Theory 2006, 6, 317–333. [Google Scholar] [CrossRef] [Green Version]

- Sierra, V.; Iglesias, O.; Markovic, S.; Singh, J.J. Does ethical image build equity in corporate services brands? The influence of customer perceived ethicality on affect, perceived quality, and equity. J. Bus. Ethic. 2015, 144, 661–676. [Google Scholar] [CrossRef]

- Balmer, J.M.T. The Three virtues and seven deadly sins of corporate brand management. J. Gen. Manag. 2001, 27, 1–17. [Google Scholar] [CrossRef]

- Raza, A.; Saeed, A.; Iqbal, M.K.; Saeed, U.; Sadiq, I.; Faraz, N.A. Linking corporate social responsibility to customer loyalty through co-creation and customer company identification: Exploring sequential mediation mechanism. Sustainability 2020, 12, 2525. [Google Scholar] [CrossRef] [Green Version]

- Sun, H.; Rabbani, M.; Ahmad, N.; Sial, M.; Guping, C.; Zia-Ud-Din, M.; Fu, Q. CSR, co-creation and green consumer loyalty: Are green banking initiatives important? A moderated mediation approach from an emerging economy. Sustainability 2020, 12, 10688. [Google Scholar] [CrossRef]

- Osakwe, C.N.; Yusuf, T.O. CSR: A roadmap towards customer loyalty. Total Qual. Manag. Bus. Excel. 2020, 1–17. [Google Scholar] [CrossRef]

- Poolthong, Y.; Mandhachitara, R. Customer expectations of CSR, perceived service quality and brand effect in Thai retail banking. Int. J. Bank Mark. 2009, 27, 408–427. [Google Scholar] [CrossRef]

- McDonald, L.M.; Rundle-Thiele, S. Corporate social responsibility and bank customer satisfaction. Int. J. Bank Mark. 2008, 26, 170–182. [Google Scholar] [CrossRef] [Green Version]

- McDonald, L.M.; Lai, C.H. Impact of corporate social responsibility initiatives on Taiwanese banking customers. Int. J. Bank Mark. 2011, 29, 50–63. [Google Scholar] [CrossRef]

- Ajina, A.S.; Japutra, A.; Nguyen, B.; Alwi, S.F.S.; Al-Hajla, A.H. The importance of CSR initiatives in building customer support and loyalty. Asia Pac. J. Mark. Logist. 2019, 31, 691–713. [Google Scholar] [CrossRef]

- Fatma, M.; Rahman, Z. Consumer responses to CSR in Indian banking sector. Int. Rev. Public Nonprofit Mark. 2016, 13, 203–222. [Google Scholar] [CrossRef]

- Fatma, M.; Rahman, Z. The CSR’s influence on customer responses in Indian banking sector. J. Retail. Consum. Serv. 2016, 29, 49–57. [Google Scholar] [CrossRef]

- Khan, I.; Fatma, M. Connecting the dots between CSR and brand loyalty: The mediating role of brand experience and brand trust. Int. J. Bus. Excell. 2019, 17, 439–455. [Google Scholar] [CrossRef]

- Tuan, L.T. Activating tourists’ citizenship behavior for the environment: The roles of CSR and frontline employees’ citizenship behavior for the environment. J. Sustain. Tour. 2018, 26, 1178–1203. [Google Scholar] [CrossRef]

- Blau, P.M. Social Exchange Theory; John Wiley & Sons: New York, NY, USA, 1964; Volume 3, p. 62. [Google Scholar]

- Gouldner, A.W. The Norm of Reciprocity: A Preliminary Statement. Am. Sociol. Rev. 1960, 25, 161. [Google Scholar] [CrossRef]

- Jarvis, W.; Ouschan, R.; Burton, H.J.; Soutar, G.; O’Brien, I.M. Customer engagement in CSR: A utility theory model with moderating variables. J. Serv. Theory Pr. 2017, 27, 833–853. [Google Scholar] [CrossRef]

- Fatma, M.; Khan, I.; Rahman, Z. CSR and consumer behavioral responses: The role of customer-company identification. Asia Pac. J. Mark. Logist. 2018, 30, 460–477. [Google Scholar] [CrossRef]

- Badenes-Rocha, A.; Ruiz-Mafé, C.; Bigné, E. Engaging customers through user-and company-generated content on CSR. Span. J. Mark. ESIC 2019, 23, 339–372. [Google Scholar] [CrossRef] [Green Version]

- Engerman, J.A.; Otto, R.F. The shift to digital: Designing for learning from a culturally relevant interactive media perspective. Educ. Technol. Res. Dev. 2021, 69, 301–305. [Google Scholar] [CrossRef] [PubMed]

- Mohammed, A.; Al-Swidi, A. The influence of CSR on perceived value, social media and loyalty in the hotel industry. Span. J. Mark. ESIC 2019, 23, 373–396. [Google Scholar] [CrossRef] [Green Version]

- Pérez, A.; Del Bosque, I.R. Corporate social responsibility and customer loyalty: Exploring the role of identification, satisfaction and type of company. J. Serv. Mark. 2015, 29, 15–25. [Google Scholar] [CrossRef]

- Moisescu, O.-I. From CSR to Customer Loyalty: An Empirical Investigation in the Retail Banking Industry of a Developing Country. Sci. Ann. Econ. Bus. 2017, 64, 307–323. [Google Scholar] [CrossRef] [Green Version]

- Shabbir, M.S.; Shariff, M.N.M.; Yusof, M.S.B.; Salman, R.; Hafeez, S. Corporate social responsibility and customer loyalty in Islamic banks of Pakistan: A mediating role of brand image. Acad. Account. Financ. Stud. J. 2018, 22, 1–6. [Google Scholar]

- Aramburu, I.A.; Pescador, I.G. The effects of corporate social responsibility on customer loyalty: The mediating effect of reputation in cooperative banks versus commercial banks in the Basque country. J. Bus. Ethic. 2019, 154, 701–719. [Google Scholar] [CrossRef]

- Prasad, S.; Garg, A.; Prasad, S. Purchase decision of generation Y in an online environment. Mark. Intell. Plan. 2019, 37. [Google Scholar] [CrossRef]

- Kollat, J.; Farache, F. Achieving consumer trust on Twitter via CSR communication. J. Consum. Mark. 2017, 34, 505–514. [Google Scholar] [CrossRef] [Green Version]

- Nyilasy, G. Word of mouth: What we really know and what we don’t. In Connected Marketing; Routledge: Abington, UK, 2006; pp. 161–184. [Google Scholar]

- Li, C.-Y. How social commerce constructs influence customers’ social shopping intention? An empirical study of a social commerce website. Technol. Forecast. Soc. Chang. 2019, 144, 282–294. [Google Scholar] [CrossRef]

- Romero, J.; Ruiz-Equihua, D. Be a part of it: Promoting WOM, eWOM, and content creation through customer identification. Span. J. Mark. ESIC 2020, 24, 55–72. [Google Scholar] [CrossRef]

- Tseng, T.H.; Lee, C.T. Facilitation of consumer loyalty toward branded applications: The dual-route perspective. Telemat. Inform. 2018, 35, 1297–1309. [Google Scholar] [CrossRef]

- Rialti, R.; Zollo, L.; Pellegrini, M.M.; Ciappei, C. Exploring the Antecedents of Brand Loyalty and Electronic Word of Mouth in Social-Media-Based Brand Communities: Do Gender Differences Matter? J. Glob. Mark. 2017, 30, 147–160. [Google Scholar] [CrossRef] [Green Version]

- Ngoma, M.; Ntale, P.D. Word of mouth communication: A mediator of relationship marketing and customer loyalty. Cogent Bus. Manag. 2019, 6, 1580123. [Google Scholar] [CrossRef]

- Ismagilova, E.; Slade, E.L.; Rana, N.P.; Dwivedi, Y.K. The Effect of Electronic Word of Mouth Communications on Intention to Buy: A Meta-Analysis. Inf. Syst. Front. 2020, 22, 1203–1226. [Google Scholar] [CrossRef] [Green Version]

- Alhulail, H.; Dick, M.; Abareshi, A. The Influence of Word of Mouth on Customer Loyalty to Social Commerce Websites: Trust as a Mediator. In Recent Trends in Data Science and Soft Computing, Proceedings of the 3rd International Conference of Reliable Information and Communication Technology (IRICT 2018), Kuala Lumpur, Malaysia, 23–24 June 2018; Saeed, F., Gazem, N., Mohammed, F., Busalim, A., Eds.; Springer: Cham, Switzerland, 2018; pp. 1025–1033. [Google Scholar]

- Khan, M.M.; Hashmi, H.B.A. Impact of interactivity of electronic word of mouth systems and website quality on customer e-loyalty. Pak. J. Commer. Soc. Sci. (PJCSS) 2016, 10, 486–504. [Google Scholar]

- Hajli, N. Social commerce constructs and consumer’s intention to buy. Int. J. Inf. Manag. 2015, 35, 183–191. [Google Scholar] [CrossRef]

- Nadeem, W.; Juntunen, M.; Shirazi, F.; Hajli, N. Consumers’ value co-creation in sharing economy: The role of social support, consumers’ ethical perceptions and relationship quality. Technol. Forecast. Soc. Chang. 2020, 151, 119786. [Google Scholar] [CrossRef]

- Chu, S.-C.; Chen, H.-T.; Gan, C. Consumers’ engagement with corporate social responsibility (CSR) communication in social media: Evidence from China and the United States. J. Bus. Res. 2020, 110, 260–271. [Google Scholar] [CrossRef]

- Fatma, M.; Ruiz, A.P.; Khan, I.; Rahman, Z. The effect of CSR engagement on eWOM on social media. Int. J. Organ. Anal. 2020, 28, 941–956. [Google Scholar] [CrossRef]

- Schaefer, S.D.; Terlutter, R.; Diehl, S. Talking about CSR matters: Employees’ perception of and reaction to their company’s CSR communication in four different CSR domains. Int. J. Advert. 2019, 39, 191–212. [Google Scholar] [CrossRef] [Green Version]

- Cheng, G.; Cherian, J.; Sial, M.; Mentel, G.; Wan, P.; Álvarez-Otero, S.; Saleem, U. The Relationship between CSR Communication on Social Media, Purchase Intention, and E-WOM in the Banking Sector of an Emerging Economy. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1025–1041. [Google Scholar] [CrossRef]

- Khan, Z.; Ferguson, D.; Pérez, A. Customer responses to CSR in the Pakistani banking industry. Int. J. Bank Mark. 2015, 33, 471–493. [Google Scholar] [CrossRef]

- Rastini, N.M.; Nurcaya, N. Customers trust mediation: Effect of CSR and service quality towards e-WOM. Int. Res. J. Manag. IT Soc. Sci. 2019, 6, 169–173. [Google Scholar] [CrossRef]

- Abbas, M.; Gao, Y.; Shah, S.S.H. CSR and Customer Outcomes: The Mediating Role of Customer Engagement. Sustainability 2018, 10, 4243. [Google Scholar] [CrossRef] [Green Version]

- Kuokkanen, H.; Sun, W. Companies, Meet Ethical Consumers: Strategic CSR Management to Impact Consumer Choice. J. Bus. Ethic. 2020, 166, 403–423. [Google Scholar] [CrossRef] [Green Version]

- Pang, A.; Lwin, M.O.; Ng, C.S.-M.; Ong, Y.-K.; Chau, S.R.W.-C.; Yeow, K.P.-S. Utilization of CSR to build organizations’ corporate image in Asia: Need for an integrative approach. Asian J. Commun. 2018, 28, 335–359. [Google Scholar] [CrossRef]

- Hur, W.M.; Kim, H.; Kim, H.K. Does customer engagement in corporate social responsibility initiatives lead to customer citizenship behaviour? The mediating roles of customer-company identification and affective commitment. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1258–1269. [Google Scholar] [CrossRef]

- Lacey, R.; Kennett-Hensel, P.A. Longitudinal Effects of Corporate Social Responsibility on Customer Relationships. J. Bus. Ethic. 2010, 97, 581–597. [Google Scholar] [CrossRef]

- Ng, S.; David, M.E.; Dagger, T.S. Generating positive word-of-mouth in the service experience. Manag. Serv. Qual. Int. J. 2011, 19, 229–242. [Google Scholar] [CrossRef]

- Popp, B.; Woratschek, H. Consumer–brand identification revisited: An integrative framework of brand identification, customer satisfaction, and price image and their role for brand loyalty and word of mouth. J. Brand Manag. 2017, 24, 250–270. [Google Scholar] [CrossRef]

- Kudeshia, C.; Kumar, A. Social eWOM: Does it affect the brand attitude and purchase intention of brands? Manag. Res. Rev. 2017, 40, 310–330. [Google Scholar] [CrossRef]

- Karjaluoto, H.; Munnukka, J.; Kiuru, K. Brand love and positive word of mouth: The moderating effects of experience and price. J. Prod. Brand Manag. 2016, 25, 527–537. [Google Scholar] [CrossRef]

- Khan, S.A.; Ramzan, N.; Shoaib, M.; Mohyuddin, A. Impact of word of mouth on consumer purchase intention. Age 2015, 18, 78. [Google Scholar]

- Serra-Cantallops, A.; Ramon-Cardona, J.; Salvi, F. The impact of positive emotional experiences on eWOM generation and loyalty. Span. J. Mark. ESIC 2018, 22, 142–162. [Google Scholar] [CrossRef]

- Chu, S.-C.; Chen, H.-T. Impact of consumers’ corporate social responsibility-related activities in social media on brand attitude, electronic word-of-mouth intention, and purchase intention: A study of Chinese consumer behavior. J. Consum. Behav. 2019, 18, 453–462. [Google Scholar] [CrossRef]

- Ogunmokun, O.A.; Timur, S. Effects of the Awareness of University’s CSR on Students’ Word-of-Mouth Intentions. In Proceedings of the Global Joint Conference on Industrial Engineering and Its Application Areas, Gazimagusa, North Cyprus, 2–3 September 2019; pp. 133–147. [Google Scholar]

- Van Asperen, M.; de Rooij, P.; Dijkmans, C. Engagement-based loyalty: The effects of social media engagement on customer loyalty in the travel industry. Int. J. Hosp. Tour. Adm. 2018, 19, 78–94. [Google Scholar] [CrossRef]

- Eisingerich, A.B.; Rubera, G.; Seifert, M.; Bhardwaj, G. Doing Good and Doing Better despite Negative Information?: The Role of Corporate Social Responsibility in Consumer Resistance to Negative Information. J. Serv. Res. 2010, 14, 60–75. [Google Scholar] [CrossRef]

- Kang, J.; Hustvedt, G. Building trust between consumers and corporations: The role of consumer perceptions of transparency and social responsibility. J. Bus. Ethic. 2014, 125, 253–265. [Google Scholar] [CrossRef]

- Dagger, T.S.; David, M.E.; Ng, S. Do relationship benefits and maintenance drive commitment and loyalty? J. Serv. Mark. 2011, 25, 273–281. [Google Scholar] [CrossRef]

- Iglesias, O.; Markovic, S.; Bagherzadeh, M.; Singh, J.J. Co-creation: A key link between corporate social responsibility, customer trust, and customer loyalty. J. Bus. Ethic. 2018, 163, 151–166. [Google Scholar] [CrossRef]

- Harman, H.H. Modern Factor Analysis; University of Chicago Press: Chicago, IL, USA, 1976. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Brown, T.J.; Dacin, P.A. The company and the product: Corporate associations and consumer product responses. J. Mark. 1997, 61, 68–84. [Google Scholar] [CrossRef] [Green Version]

- Latif, K.F.; Pérez, A.; Sahibzada, U.F. Corporate social responsibility (CSR) and customer loyalty in the hotel industry: A cross-country study. Int. J. Hosp. Manag. 2020, 89, 102565. [Google Scholar] [CrossRef]

- Tajvidi, M.; Wang, Y.; Hajli, N.; Love, P.E. Brand value Co-creation in social commerce: The role of interactivity, social support, and relationship quality. Comput. Hum. Behav. 2021, 115, 105238. [Google Scholar] [CrossRef] [Green Version]

- Han, H.; Al-Ansi, A.; Chi, X.; Baek, H.; Lee, K.-S. Impact of Environmental CSR, Service Quality, Emotional Attachment, and Price Perception on Word-of-Mouth for Full-Service Airlines. Sustainability 2020, 12, 3974. [Google Scholar] [CrossRef]

- D’Acunto, D.; Tuan, A.; Dalli, D.; Viglia, G.; Okumus, F. Do consumers care about CSR in their online reviews? An empirical analysis. Int. J. Hosp. Manag. 2020, 85, 102342. [Google Scholar] [CrossRef]

{kind=link}

| Demographic | Frequency | % |

|---|---|---|

| Gender | ||

| Male | 288 | 66.8 |

| Female | 143 | 33.2 |

| Age | ||

| 20–25 | 73 | 16.9 |

| 26–30 | 153 | 35.5 |

| 31–40 | 138 | 32.1 |

| Above 40 | 67 | 15.5 |

| Education | ||

| Intermediate | 77 | 17.9 |

| Graduate | 112 | 26.0 |

| Master | 183 | 42.4 |

| Higher | 59 | 13.7 |

| Total | 431 | 100 |

| Variable | Statement | Loading | AVE | CR |

|---|---|---|---|---|

| S–CSR | I consider this bank a socially responsible bank. | 0.71 | ||

| This bank is more beneficial to society’s welfare than other banks. | 0.74 | |||

| This bank contributes something to society. | 0.79 | |||

| I share this bank’s (CSR) posts on my own Facebook (or other social media) page. | 0.83 | |||

| I engage in conversations (CSR) on the Facebook (or other social media) page of this bank. | 0.82 | 0.61 | 0.88 | |

| E-WOM | I am likely to spread positive word of mouth about this bank (on social media). | 0.70 | ||

| I would recommend this bank’s products/services to my friends (on social media). | 0.77 | |||

| If my friends were looking to purchase banking services, I would tell them to try this bank (on social media). | 0.72 | 0.53 | 0.77 | |

| Loyalty | I consider this bank my first choice when I purchase the services they supply. | 0.73 | ||

| I am willing to maintain my relationship with this bank | 0.72 | |||

| I am loyal to this bank. | 0.84 | 0.59 | 0.81 |

| Variable | Mean | SD | S–CSR | E-WOM | Loyalty | Skewness | Kurtosis | |

|---|---|---|---|---|---|---|---|---|

| S–CSR | 3.88 | 0.58 | (0.781) | 0.27 ** | 0.24 ** | −0.56 | 0.47 | |

| E-WOM | 4.10 | 0.61 | (0.728) | 0.31 ** | −0.63 | 0.51 | ||

| Loyalty | 4.28 | 0.55 | (0.721) | −0.68 | 0.44 | |||

| (χ2/df = 4.09, RMSEA = 0.068, NFI = 0.924, CFI = 0.929, GFI = 0.925) | ||||||||

| Path | Beta Value | S.E | LLCI | ULCI | Decision |

|---|---|---|---|---|---|

| The Results of Hypothesis 1 and 2 | |||||

| S–CSR → Loyalty | 0.225 ** | 0.0442 | 0.293 | 0.537 | supported |

| S–CSR → E-WOM | 0.257 ** | 0.0371 | 0.310 | 0.583 | supported |

| (χ2/df = 3.394, RMSEA = 0.0578, NFI = 0.946, CFI = 0.949, and GFI = 0.947) *** | |||||

| The Results of Hypothesis 3 | |||||

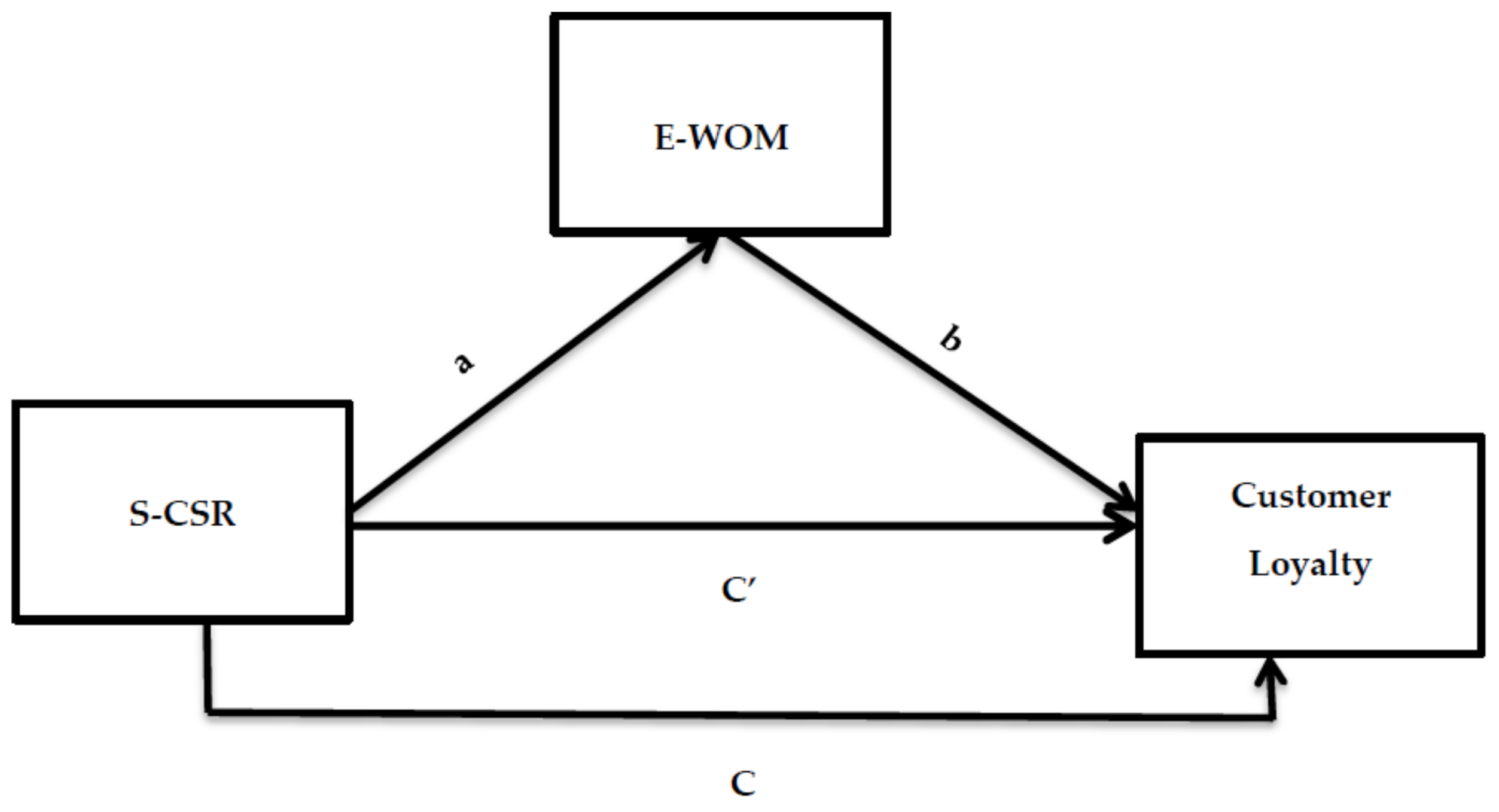

| S–CSR → E-WOM → Loyalty | 0.173 ** | 0.021 | 0.044 | 0.063 | supported |

| (χ2/df = 2.98, RMSEA = 0.0486, NFI = 0.952, CFI = 0.958, and GFI = 0.956) *** | |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, D.; Mahmood, A.; Ariza-Montes, A.; Vega-Muñoz, A.; Ahmad, N.; Han, H.; Sial, M.S. Exploring the Impact of Corporate Social Responsibility Communication through Social Media on Banking Customer E-WOM and Loyalty in Times of Crisis. Int. J. Environ. Res. Public Health 2021, 18, 4739. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph18094739

Zhang D, Mahmood A, Ariza-Montes A, Vega-Muñoz A, Ahmad N, Han H, Sial MS. Exploring the Impact of Corporate Social Responsibility Communication through Social Media on Banking Customer E-WOM and Loyalty in Times of Crisis. International Journal of Environmental Research and Public Health. 2021; 18(9):4739. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph18094739

Chicago/Turabian StyleZhang, Dianxi, Asif Mahmood, Antonio Ariza-Montes, Alejandro Vega-Muñoz, Naveed Ahmad, Heesup Han, and Muhammad Safdar Sial. 2021. "Exploring the Impact of Corporate Social Responsibility Communication through Social Media on Banking Customer E-WOM and Loyalty in Times of Crisis" International Journal of Environmental Research and Public Health 18, no. 9: 4739. https://0-doi-org.brum.beds.ac.uk/10.3390/ijerph18094739