The Potential of Collaboration between India and Japan in the Hydrogen Sector

Graduate School of Media Governance, Keio University, Fujisawa 252-0082, Japan

*

Authors to whom correspondence should be addressed.

Energies 2023, 16(8), 3596; https://0-doi-org.brum.beds.ac.uk/10.3390/en16083596

Submission received: 14 March 2023

/

Revised: 14 April 2023

/

Accepted: 18 April 2023

/

Published: 21 April 2023

(This article belongs to the Special Issue Advances in Hydrogen Energy Ⅱ)

Abstract

:With growing concern about risks related to energy security around the world, the development of hydrogen cooperation between India and Japan has become very important to ensure the economic security of the two countries and to deepen economic cooperation. This report covers both public and private initiatives in the hydrogen area in both countries and visualizes the high potential and potential areas where both countries could cooperate in the hydrogen area, as well as the challenges that are necessary for cooperation. The following four factors are strong incentives for India and Japan to deepen cooperation in the hydrogen field: (1) India has a high potential hydrogen supply capacity, (2) India is very active in implementing hydrogen in society, (3) Japan is already conducting R&D in areas of high interest to India and (4) Japan will need to import hydrogen from other countries in the future. The issues of (1) cost visualization, including transportation costs, (2) harmonization of regulations, (3) harmonization of promotion measures between the two countries, (4) definition of “green hydrogen,” and (5) protection of intellectual property are main challenges to be overcome. Thus, disclosures of necessary data for cost visualization of hydrogen transportation, further inter-governmental cooperations between India and Japan, and facilitation of the discussions on hydrogen among various stakes are key actions for materializing various joint hydrogen projects between both countries.

1. Introduction

Hydrogen is getting attention around the world these days as an energy resource for reducing carbon dioxide emissions and enhancing energy security. As the supply of gas from Russia, the world’s second-largest producer of natural gas, has become more uncertain, there has been a growing debate on the resilience of the energy supply chain, especially in Europe, which has been highly dependent on gas supplies from Russia [1]. The argument that renewable energy improves energy security has existed for some time, and as global supply chain risks become more apparent, the need for the use of renewable energy is being advocated more and more [2]. As the introduction of renewable energy is accelerated from the perspective of both reducing greenhouse gas emissions and improving energy security, expectations for hydrogen with energy storage capabilities are increasing.

India is also enthusiastically implementing efforts to utilize hydrogen. India’s budget proposal for 2023 emphasizes the importance of hydrogen, and it is proposed that 2.4 billion USD * be allocated for the realization of the National Hydrogen Mission, India’s national strategy for the promotion of hydrogen [3]. (* In this paper, the exchange rate is fixed and calculated as described following: 1 USD = 130 JPY = 82 INR.) Indian government attaches great importance to reducing its trade deficit by decreasing gas and oil imports as well as improving energy security. Additionally, the significance of the National Hydrogen Mission is to facilitate energy transition and reduce dependence on fossil fuel imports [4]. As for Japan, it started discussions on utilizing hydrogen as an energy source before hydrogen attracted serious attention from around the world as an energy source. Since Japan formulated the “Basic Hydrogen Strategy” in 2017 and began a comprehensive study of a “Hydrogen society” that uses hydrogen as energy, many hydrogen-related technologies have been developed in Japan [5]. The Prime Minister of India, Narendra Modi, announced a national hydrogen mission on 15 August 2021 and started its promotion of hydrogen-related technologies [6]. Under these circumstances, the Prime Minister of Japan, Fumio Kishida, visited India in March 2022 and concluded an “India-Japan Clean Energy Partnership” to strengthen cooperation between India and Japan in the energy domain, including hydrogen [7]. On the other hand, at present, discussions on specific areas of cooperation have not been deepened, and concrete results of cooperation are expected to materialize.

The purpose of this paper is to fulfill the two objectives described following by listing representative efforts in both India and Japan and by discussing specific areas for collaboration; (1) To identify areas where the direction of both countries’ efforts are in line with each other and where there are high potentials for both countries to cooperate, (2) To identify barriers to cooperation between the two countries. Section 2 shows a discussion of hydrogen in the world that both countries need to consider when deepening their relationship. Section 3 then lists the potential implementation of hydrogen-related technologies in India from a scientific perspective and introduces specific initiatives in India. Section 4 lists Japanese initiatives that are underway in the areas considered by the Indian government. This is followed by a discussion of potential barriers to materializing collaboration between the two countries in Section 5.

2. Discussions on Hydrogen in The U.S., EU, UK, and Australia

The U.S. Department of Energy lists three important advantages of hydrogen for society: Energy Security, Public Health and Environment, and Fuel Storage. From the perspective of public health and the environment, hydrogen is important because, unlike gasoline and diesel, which emit nitrogen oxides, hydrogen only emits water, which contributes to reducing the burden on the environment and improving people’s health. Although hydrogen’s low energy density needs to be overcome in order for it to fulfill its role as energy storage, it is expected to be a new energy storage option and a technology that is certainly useful to society [8].

In the EU, in May 2022, the European Commission designated the three pillars of (1) saving energy, (2) producing clean energy, and (3) diversifying energy supplies as priority areas; REPowerEU has been announced to realize the green transition. Hydrogen is highlighted as an important part of this plan, and from the perspective of reducing LNG imports, it is clearly stated that the capacity of water electrolyzers will be expanded to 17.5 GW by 2025, aiming to produce 10 million tons/year of hydrogen from renewable energy sources. This is followed by an announcement to import 10 million tons/year of hydrogen derived from renewable energy sources from overseas by 2030 for a total goal of utilizing 20 million tons/year of hydrogen [9,10]. The United Kingdom has doubled its 2030 target for domestic low-carbon hydrogen production capacity from 5 GW to 10 GW, as stated in its hydrogen strategy, and has announced that more than half of this capacity will be derived from electrolytic hydrogen [11].

Australia has announced 2019 Australia’s National Hydrogen Strategy, which aims to develop a hydrogen industry as a hydrogen supplier country, backed by its abundant renewable energy potential. Success indicators include being one of the top three hydrogen suppliers in the Asian market, having a hydrogen industry that brings economic benefits and jobs, and enforcing an uncompromised and internationally recognized country-of-origin certification system [12]. Thus, policy measures are being taken around the world to promote the hydrogen industry in various contexts, such as reducing greenhouse gases, improving energy security, and fostering new industries.

2.1. List of Hydrogen Production Methods and Classifications

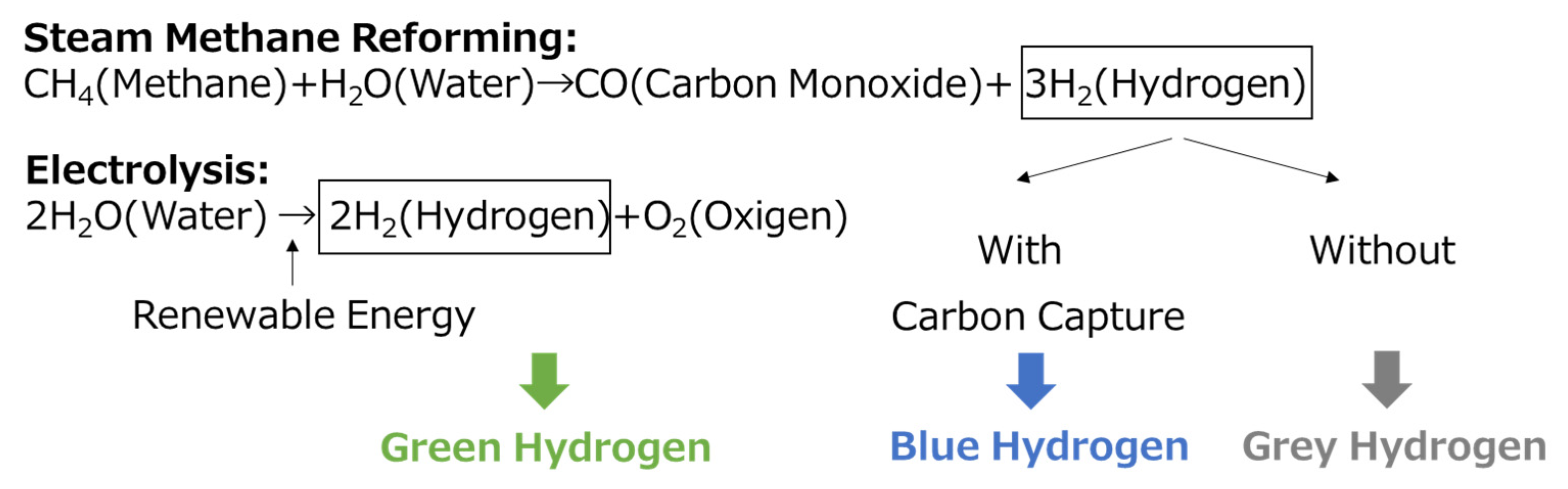

The utilization of hydrogen itself has long been considered, and specific hydrogen generation methods are broadly classified into Fuel Processing and Non-reforming Hydrogen production, under which they are categorized [13]. Hydrogen is nowadays generally classified into three types in Japan; hydrogen obtained through coal gasification and purification, hydrogen recovered from natural gas using a method called steam methane reforming (SMR: a technology in which natural gas and ultra-high-temperature steam are mixed in the presence of a catalyst to produce carbon monoxide and hydrogen through a chemical reaction), and hydrogen recovered from natural gas with CO2 generated in the hydrogen purification process. The hydrogen recovered from coal and natural gas using this method with carbon capture processes is generally defined as “blue hydrogen”, and the hydrogen recovered from the method without carbon capture processes is generally defined as “grey hydrogen”. Hydrogen that does not use fossil fuels in the production process and is produced by water electrolysis using renewable energy is defined as “green hydrogen” as Figure 1 shows [14]. In addition to these three representative categories, there is an ongoing discussion on the detailed coloring of hydrogen, including the classification of hydrogen produced through methane pyrolysis as turquoise and hydrogen produced using electricity generated by nuclear power as Pink [15,16].

2.2. Hydrogen Production in the World

The amount of hydrogen produced by low-emission technologies is very limited, accounting for less than 1% of the total hydrogen currently in circulation, and for the three years prior to 2021, it was less than 1% of the total emissions situation [17]. In terms of price, according to a 2018 IEA survey, the price of gray hydrogen in the U.S. has already achieved 1 USD/kgH, and given that the current price of green hydrogen, discussed below, is 3 USD/kgH, the price competitiveness of blue hydrogen at present is by far higher than that of green hydrogen [18].

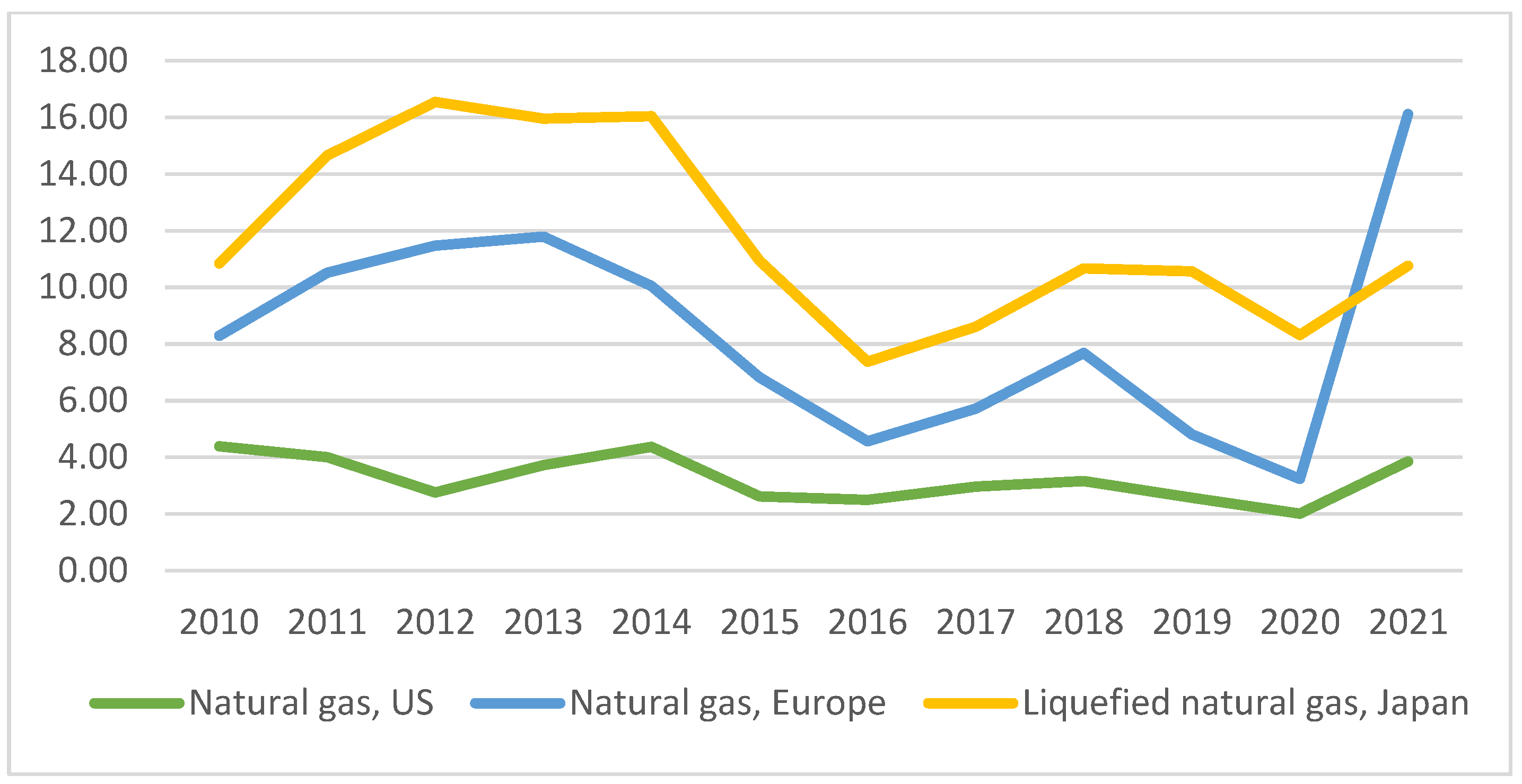

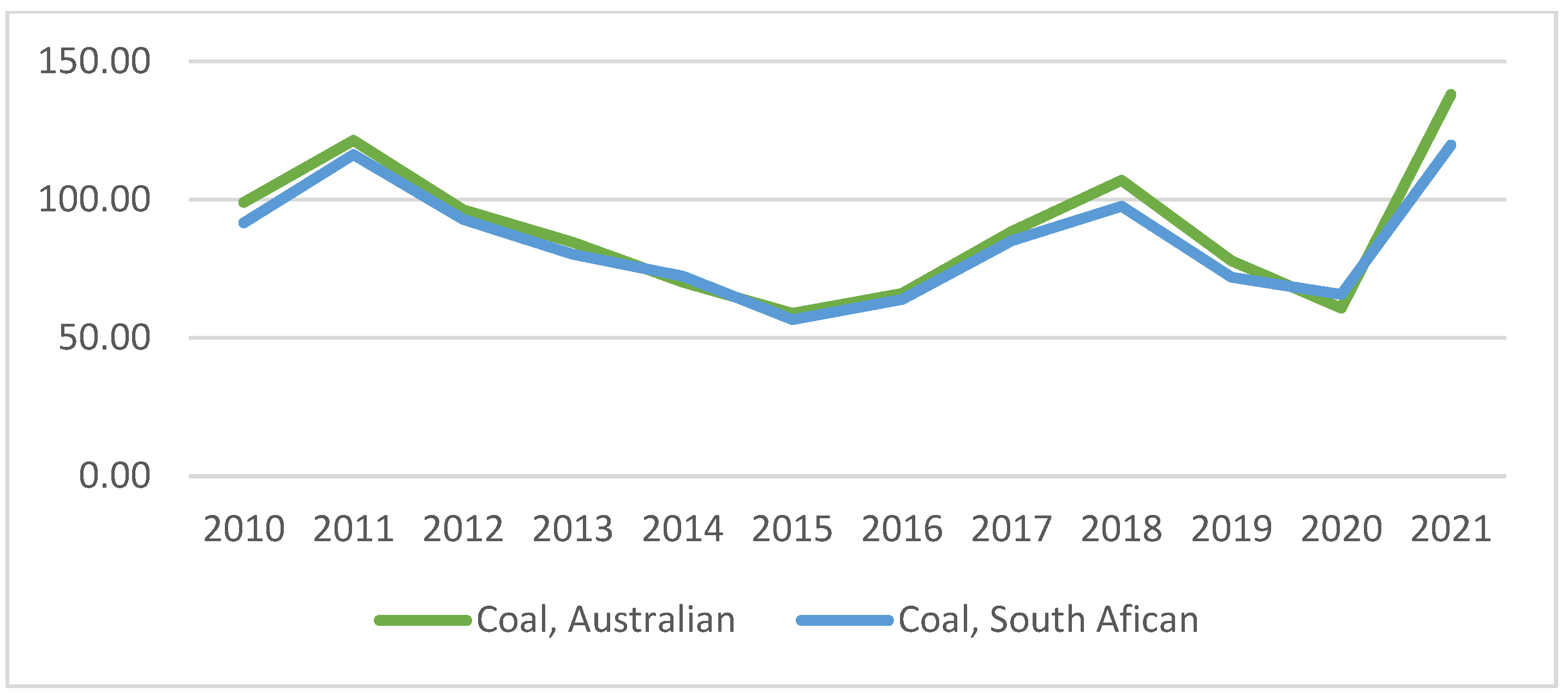

On the other hand, the prices of LNG and coal have been rising sharply in recent years as, Figure 2 and Figure 3 show [19]. Especially in Europe, where gas prices are rising sharply, hydrogen is attracting attention as an alternative energy source from the perspective of strengthening energy security. The outlook for the price of blue hydrogen, which is made from LNG, has become uncertain due to the protracted war in Ukraine, and expectations for green hydrogen have been rising.

IEA estimated that the price per unit of hydrogen is calculated for each price of electricity with fixed CAPEX; If more than 2000 h of electricity supply could be realized at a price below 20 USD/MWh, 2 USD/kgH could be realized. At this point in time, estimates have already been made that the production price of green hydrogen in China can realistically be produced at 3 USD/kgH. In the same report, IEA also calculates the theoretical hydrogen price for each country if the CAPEX price is fixed under the same conditions and a carbon dioxide emission cost of 25 USD/tCO2 is imposed on fossil fuel-derived hydrogen. Under the condition India is particularly competitive in the price of generating hydrogen with renewable energy, and if the lower theoretical limit is realized, green hydrogen production can be realized at a lower price than natural gas-derived hydrogen produced without carbon capture technologies in Australia. On the other hand, the cost of hydrogen generation from renewable energy sources in Japan will not fall below 4 USD/kgH even if the lower limit is realized [18]. Thus, calculations of global hydrogen production price estimates, given general assumptions, have progressed. These reference prices will be a very important benchmark in developing the arguments for realistically facilitating the distribution of hydrogen between India and Japan in the chapters that follow.

3. Discussions on Hydrogen in India

3.1. India’s Energy Mix and Current Policy Trends

3.1.1. India’s Energy Mix

India ranks third in energy consumption after China and the U.S. About 70% of India’s primary energy demand in the cross-section of FY 2019 is met by fossil fuels, and it is projected to exceed 70% in 2040. Specifically, demand for fossil fuels is expected to continue to increase along with economic development, and the IEA estimates that crude oil imports will double in 2040 from the 17% self-sufficiency rate in 2018. As for natural gas, the country is the world’s fourth-largest importer of LNG, and as for coal, it is the world’s second-largest importer of coal [20]. On the other hand, the Indian government continued to emphasize the acceleration of renewable energy installation as a key government policy and announced the implementation of 100 GW of renewable energy in August 2021. The India Central Electricity Authority’s 2030 installed capacity plan calls for 450 GW of renewable energy (280 GW solar PV, 140 GW wind, 10 GW biomass, and 5 GW small hydro). As for India, the country is currently dependent on imports of LNG, and every year Indian power plants face coal shortages and power outages that leave parts of the country in darkness and cripple industry [21]. For taking countermeasures, there is a great deal of interest in India to maximize the use of renewable energy and to generate green hydrogen using abundant renewable energy from the perspectives of energy security, industrial development, and trade deficit reduction.

3.1.2. India’s Long-Term Low Carbon Emissions Development Strategy

On 14 November 2022, the Government of India announced its Long-Term Low Carbon Emissions Development Strategy (LT-LEDS), India’s long-term transition plan to a decarbonized society, at the 27th Climate Change Conference (COP27) in Egypt. It sets the production of green hydrogen as the most important area of focus and states that measures will be implemented around the following six pillars. In particular, the LT-LEDS clearly links the production of hydrogen to nuclear power generation, and the content of the LT-LEDS is very strongly intended to develop hydrogen into a new export industry as a domestically produced energy source. In addition to being an export product, LT-LEDS also has very strong expectations from various angles as an alternative fuel for transportation and as a technology to realize the low-carbonization of the industrial sector [22].

3.1.3. India’s Environmental Regulations

Not only from the perspective of transitioning from a carbon-based society but also from the perspective of improving the living environment, environmental regulations are receiving increasing attention in India, and environmental regulations in India are beginning to become stronger. For example, the National Capital Region of Delhi (NCR) Department of Air Quality Management (CAQM) has had a significant impact on the manufacturing sector by tightening restrictions on economic activities based on the level of air pollution. The restrictions on generator use, which came into effect on 1 October 2022, were announced on 8 February 2022 to address air pollution in the Delhi metropolitan area. The regulation was announced on 8 February 2022 to address air pollution in the National Capital Region of Delhi. The regulation states that the use of generators will not be permitted unless the fuel for the generators is changed to liquefied petroleum gas (LPG) or natural gas or measures such as installation of exhaust gas purification equipment are taken. Japanese companies that have installed diesel generators in industrial parks as a countermeasure against power outages are facing a major problem, as these generators will no longer be able to be used after the new regulations come into effect. Currently, the latest action plan clearly states that the use of diesel generators will be prohibited if the AQI is 301 or above, and Japanese companies in the Delhi metropolitan area are forced to prepare for the conversion of generators to those that can use both diesel and natural gas, the introduction of gas generators, and the diversification of power supply sources. Many Japanese companies with plants in the Delhi metropolitan area are now preparing to convert their power generators to diesel and natural gas generators. Many companies with factories in the National Capital Region of Delhi own diesel generators and use them as backup power sources to cope with the unstable public power supply, but the CAQM has requested power companies to provide a stable power supply and has also asked industries to refrain from using diesel generators. The CAQM has also requested that industries refrain from using diesel generators. Air pollution is not just a general GHG reduction perspective; it is an issue that directly affects the quality of life of people living in India. Curbing wildfires that cause air pollution, desulfurization of transportation equipment, energy conservation, EVs, and cleaner said fuels have become major issues that both the central and state governments in India need to take action on [23].

3.2. India’s Hydrogen-Related Policies

3.2.1. National Hydrogen Mission of India

India announced its “National Hydrogen Mission” in August 2021. Subsequently, in February 2022, India’s Ministry of Power announced specific measures to provide incentives for renewable energy for green hydrogen and ammonia. For example, The Indian government plan to implement incentives that include no transmission charges from renewable energy generation facilities to green hydrogen and ammonia production sites for up to 25 years. According to press reports, the mission’s specific policies for the future include a Production Linked Incentive (PLI) scheme, which is the incentive scheme from the Indian government for promoting domestic manufacturing, for water electrolysis equipment and components, and enforcement for oil refiners and fertilizer manufacturers to replace a few percent of hydrogen used with green hydrogen [24].

After this policy announcement, NITI Aayog published “Harnessing Green Hydrogen” in June 2022. In this report, (1) The Future of Hydrogen in India chapter assesses manufacturing potential and forecasts demand, (2) Manufacturing Opportunities chapter states that domestic demand for water electrolyzers in India will grow to approximately $3.1 billion by 2050, and then mentions the maturity level of the Indian manufacturing industry, (3) Export Opportunity chapter discusses the potential of exporting water electrolyzers to India, and (4) The Future of Hydrogen in India chapter discusses the potential for manufacturing and demand. In the chapter on Export Opportunity, the comparison of the levelized cost of green hydrogen in selected countries introduces India as the country that can theoretically produce green hydrogen most cheaply in the cross-section of 2050 [25].

Indian central government has approved the budget for materializing the National Green Hydrogen Mission. The initial outlay for the mission will be 2.41 billion USD, including an outlay of 2.13 billion USD for the promoting investment in hydrogen infrastructures, 178.8 million USD for pilot projects, 48.78 million USD for R&D, and 47.32 million USD towards other Mission components. MNRE will formulate the scheme guidelines for the implementation of the respective components [3].

3.2.2. State Government Policies in India

As for the state government’s Solar PV incentive scheme, cases have been identified where this moment has become a system that discourages the proactive installation of hydrogen technology. For example, in the state of GJ, a geologically good state for hydrogen production, a solar PV preferential policy has been introduced, as well as a system (banking system) that considers the generated renewable energy as having been stored virtually and used at a different time than when it was generated [26]. As mentioned in the “National Hydrogen Mission” of India, GJ State has already started to implement a banking system for electricity generated by Solar PV in the industrial sector. The banking system is a scheme that allows the solar PV industry to bank electricity generated by the Solar PV system. The banking system is a very powerful incentive in terms of promoting the introduction of Solar PV in India, as it allows the use of electricity from Solar PV, which can be obtained at low cost, virtually at night, leading to lower electricity prices, as well as in terms of advocating the greening of production sites. On the other hand, the introduction of hydrogen technology is a very powerful incentive. On the other hand, when viewed from the perspective of introducing hydrogen technology, banking systems would rather reduce incentives to install hydrogen-related facilities. If banking systems and hydrogen-related devices compete on the economic side, especially in the early stages when the prices of both hydrogen generators and storage devices have not dropped significantly, it will reduce the motivation of operators to install hydrogen-related devices.

3.3. Hydrogen Production Potential and Deman in India

Table 1 shows the five states in India with the highest potential for generating renewable energy. Each total potentials of renewable energy generation are (1) Andhra Pradesh (113.749 GW), (2) Gujarat (178.531 GW), (3) Karnataka (152.576 GW), (4) Maharashtra (163.316 GW), (5) Rajasthan (270.111 GW) [27,28]. The potential for renewable energy is a very important indicator for the installation of hydrogen-related facilities. In addition, the proximity of potential hydrogen demand areas and the distance to ports are also important when considering the export of hydrogen. In the IEA’s report, India’s potential for producing hydrogen is competitive from the perspective of good wind conditions and high solar radiation and could produce hydrogen under the price of 1.5 USD/kg H2 [29]. While water issues are a concern in India, projects based on the desalination of seawater are also becoming a reality. Specifically, some studies have shown that the overall price may be in the negligible range. It has also been estimated that approximately 18 to 24 kg of water is needed to produce 1 kg of hydrogen [30].

On the other hand, in India, even if there is potential, the difficulty of project implementation due to the Inefficient maintenance of land records, Lack of a formal policy in certain key states, Delay in government land allotment under the Solar Park Scheme for ISTS projects, and Lack of digitization of land records make it important to consider whether the project has actually been implemented or not [31]. Table 2 shows the actual installed renewable energy capacity in states with high potential, indicating that Gujarat, Karnataka, and Rajasthan are aggressively introducing renewable energy by lending high potential. In addition, of the three, Gujarat and Karnataka have ports due to their oceanfront location, and both states have steel mills, fertilizer refineries, and refineries in the state that have been identified as major candidates for hydrogen demand [25].

In Harnessing Green Hydrogen, the potential for hydrogen production is analyzed in terms of energy sources and proximity to demand in various regions. The major demand areas for hydrogen expected in the report are (a) Refining, (b) Ammonia, (c) Methanol, (d) Steel, (e) Long-Haul Freight and Heavy-Duty Vehicles (HDVs), and (f) Power Sector.

3.3.1. Ammonia Sector

Ammonia is an important raw material for fertilizers, and until now, it has been mainly produced from natural gas. Recently, however, methods to produce fertilizers from renewable energy have been attracting attention, and companies such as Yara, a major Norwegian fertilizer company, are trying to take an advanced approach [32].

India is the world’s third largest fertilizer importer after the U.S. and Vietnam, and the total subsidy outgo for fertilizer in India reached about 20 billion USD during the fiscal year 2022 [33,34]. Thus, the switch to the domestic production of ammonia, which worsens the trade balance and the domestic fiscal balance, has become a very important issue for the Indian government.

Private companies are beginning to emerge in India that are trying to use renewable energy to produce ammonia. For example, Greenko, which is a big energy company in India, and Germany’s biggest gas trader Uniper, signed a Memorandum of Understanding (MoU) to supply 250,000 tonnes per annum of green ammonia from Greenko to Uniper [35].

Looking at the existing sector of ammonia, one could argue that India is at a good time to bring in new production facilities. In the ammonia sector of India, there are chemical plants that have existed for over 25 years and are likely to be replaced relatively soon, and the demand for hydrogen may pass at the time of facility upgrades during the replacement period [36].

3.3.2. Steel Sector

In the area of steel, Nippon Steel Corporation, through its Indian joint venture with ArcelorMittal Europe, will build two new blast furnaces in India, which will start operation sequentially from 2025. The total investment, including the cost of acquiring infrastructure such as ports, will exceed 1 trillion yen. The new blast furnaces and other measures will more than triple the current crude steel production capacity in India to 30 million tons per year by 2030. Japan’s demand for steel is expected to decline over the medium to long term, and India is positioned as one of the key growth drivers. By constructing blast furnaces in India, where demand is growing, the company will establish an integrated local production system and increase profitability. In the future, the company will also consider introducing “Hydrogen steelmaking” in India, which will reduce CO2 emissions [37]. Additionally, the Indian government expects, in Harnessing Green Hydrogen, that 160 GW of hydrogen production equipment is expected to be installed in the 2030 cross-section. On the other hand, 50 GW of this demand is expected to be in India, and 110 GW of the total installed capacity is assumed to be for export (including 69 GW of ammonia and 41 GW of hydrogen).

3.3.3. HDVs Sector

HDVs sector is an area of focus in India, as hydrogen buses will begin operating in Pune, an industrial city on the east coast near Mumbai, in August 2022 [38]. Discussions of collaboration between Indian and Japanese companies in this area have already begun. As for discussions of selling stacks to commercial vehicles, Toyota Kirloskar Motors, which is an Indian joint venture between Toyota Motor Corporation from Japan and Kirloskar Group from India, has already announced that they provide fuel cell modules to Ashok Leyland, a major local commercial vehicle manufacturer, in January 2023 [39]. In addition, India’s Railways Minister Vaishnav announced that the country’s first hydrogen-fueled train would be introduced by the end of the year. At a press conference following the budget announcement, the minister announced plans to begin operating hydrogen trains by December of 2023. The trains will first be introduced on routes connecting tourist attractions, such as between Kalika in the northern state of Haryana and Shimla in the northern state of Himachal Pradesh. The hydrogen trains will be designed and manufactured entirely in India [40].

3.3.4. Power Sector

In India, the utilization rate of gas power generation facilities, which are utilized as a major peak power source in Europe and Japan, has remained very low at around 20% [41]. In India, 72% of electricity (kWh basis) in FY2020 will be provided by coal power generation, partly because domestic production of natural gas is limited relative to demand [42]. Coal power generation capacity is expected to continue to increase until 2040 in India, and it is necessary to propose technologies and services that are in line with India’s desire to combine solar and coal power generation to supply electricity. As a project to address these issues, Adani and IHI Corporation have begun demonstration testing of an ammonia and coal co-firing power plant [43].

4. Discussions on Hydrogen in Japan

4.1. Japan’s Energy Mix and Current Policy Trends

When looking at sources of primary energy supply, Japan’s energy supply is dominated by oil (36.4%), coal (24.6%), natural gas (23.8%), nuclear (1.8%), hydropower (3.7%), and renewable energy excluding hydropower (9.7%). Japan’s dependence on fossil energy for primary energy supply in 2019 was 88.3%, a higher level than that of India (75.6%), and discussions related to fossil fuel phase-out in the country are very active. Looking at final energy consumption by sector, the industrial (45.6%), business (16.3%), residential (15.8%), and transportation (22.3%) sectors account for a high proportion of demand, and hydrogen technology is expected to advance decarbonization efforts in these areas. Hydrogen technology is expected to advance decarbonization efforts in these areas [44].

4.2. Japan’s Hydrogen-Related Policies

4.2.1. Japan’s Basic Hydrogen Strategy

Japan formulated the world’s first basic hydrogen strategy in December 2017 [5]. In October 2020, there was a declaration on achieving carbon neutrality in 2050, and since then, hydrogen has been positioned as one of the priority areas in the Green Growth Strategy. The annual installed capacity is expected to increase from the current 2 million tons to 3 million tons by 2030 and to 20 million tons by 2050. As for the cost, the current price is about 0.77 USD/Nm3, and the target is to reduce it to 0.23 USD/Nm3 by 2030 and 0.15 USD/Nm3 by 2050 [45,46].

4.2.2. Japan’s Hydrogen-Related Policies

Many companies are engaged in R&D in the hydrogen field, ranging from upstream hydrogen production technologies (water electrolyzers; alkaline type, PEM type), transportation technologies (liquefied hydrogen transportation, utilization of MCH as a hydrogen carrier, etc.), storage technologies, and downstream hydrogen utilization technologies (construction of hydrogen pipelines in port areas, hydrogen rail cars, FCVs, hydrogen co-firing, FCVs, hydrogen boilers, Hydrogen reduction technology in steelmaking, fuel cells, and hydrogen water heaters). Many companies are engaged in a wide range of R&D in the hydrogen field, and many technologies are nearing commercialization. For each of these areas, we will examine the potential for implementation in Indian society. In examining the potential for implementation, the potential and timing of implementation of both technologies that are designed to produce and transport hydrogen intensively and those that will be used on the spot will be discussed.

Japan has positioned hydrogen as one of its most important energy sources, and the development of technology and infrastructure to utilize hydrogen is progressing. On the other hand, Japan has limited power generation potential from renewable energy sources, and generating the electricity needed to produce hydrogen will be a major challenge. Based on a conservative estimate that considers business feasibility, the potential for the introduction of renewable energy in Japan is only about 340 GW [47]. In addition, renewable energy in Japan is expensive: as of 2022, the average cost of solar power is 0.092 USD per kWh, more than double the global average of 0.04 USD, and the cost of onshore wind power is 0.115 USD, nearly triple the global average 0.04 USD [48]. To address the shortage of hydrogen supply, the Japanese government has initiated discussions to support the private sector in promoting carbon neutrality and quickly securing sources of hydrogen imports and has opened discussions to realize a scheme to compensate the difference between the cost incurred to import hydrogen and the cost of purchasing conventional fossil fuels [49].

4.3. Areas Where Social Implementation of Hydrogen Related Technologies Is Progressing in Japan

Projects are underway in (b) Ammonia, (c) Methanol, (d) Steel, (e) HDVs, and (f) Power Sector, each of which is listed as an area where hydrogen is recommended to be actively utilized in Harnessing Green Hydrogen.

4.3.1. Ammonia Sector

In the ammonia area, private companies and universities are conducting demonstration tests to reduce the supply cost of ammonia to the upper 10 yen per Nm3 by 2030. As part of efforts to reduce ammonia supply costs, Chiyoda Corporation (Kanagawa, Japan), JERA Corporation (Tokyo, Japan), and Tokyo Electric Power Company Holdings, Inc. (Tokyo Japan) are developing new catalysts for ammonia production and conducting technology demonstrations related to the construction of a fuel ammonia supply chain [50].

The current ammonia production method, the Haber-Bosch process, requires a large amount of energy to produce ammonia because it reacts hydrogen and nitrogen under high temperature and high pressure. To improve this process, Idemitsu Kosan, the University of Tokyo, Tokyo Institute of Technology, Osaka University, and Kyushu University are developing green ammonia production technology at room temperature and under normal pressure [51]. In addition, demonstration studies are underway in the ammonia application area. The Japanese government is aiming for high mixing and dedicated combustion of ammonia (30 million tons/year of ammonia to be introduced in Japan by 2050) [52]. Specific projects include a demonstration study by IHI Corporation (Tokyo, Japan) and JERA Corporation (Tokyo, Japan) to establish technology for high ammonia co-firing at commercial thermal power plants [53]; a demonstration of high ammonia co-firing at thermal power plants by Mitsubishi Heavy Industries, Ltd. (Tokyo, Japan), and JERA Corporation using ammonia-dedicated burners [54]; and research and development of an ammonia-dedicated gas turbine by IHI Corporation, Tohoku University, and National Institute of Advanced Industrial Science and Technology (AIST) [55].

4.3.2. Methanol Sector

Currently, there is a process to produce LP gas by generating methanol from hydrogen and carbon monoxide, followed by a chemical transformation in the order of methanol, dimethyl ether (DME), and LP gas. This process has the advantages of generating less CO2 in the production process, being able to synthesize at lower temperatures than the Fischer-Tropsch reaction synthesis, which is expected to be a synthetic fuel production method, and not requiring a large amount of electricity for synthesis. However, the catalyst currently in use has a low production rate of about 30%, which poses a productivity challenge. Furukawa Electric Co., Ltd. has established a synthesis technology that will achieve a generation rate of 50% by FY2030 and is proceeding with development with the aim of commercialization [56].

4.3.3. Steel Sector

Japan Steel Corporation (Tokyo, Japan), JFE Steel Corporation (Tokyo, Japan), Kobe Steel, Ltd. (Hyogo, Japan), and the The Japan Research and Development Center for Metals (Tokyo, Japan) are conducting demonstrations to establish a hydrogen reduction technology that reduces CO2 emissions from the ironmaking process by 50% or more in the blast furnace process, a direct hydrogen reduction technology that reduces CO2 emissions by 50% or more in the direct reduction process compared to the current blast furnace process, and a technology to control the concentration of impurities in the electric furnace process to the level of the blast furnace process. The Center is also conducting a demonstration project to establish a technology to control the concentration of impurities in the electric furnace method to the same level as the blast furnace method [57].

4.3.4. HDVs Sector

In Japan, initiatives for HDVs are underway in the areas of commercial vehicles, ships, and aircraft, respectively. As for fuel cell buses, a typical example of commercial vehicles using hydrogen, the Tokyo Metropolitan Government has already introduced two fuel cell buses developed and commercialized by Toyota Motor Corporation and started commercial operation in February 2017, using them as route buses for the first time on the market [58]. As of October 2022, a total of 123 fuel cell buses are in widespread use, and discussions about commercial vehicles utilizing fuel cells are already developing in the commercial phase [59].

Demonstration tests are underway for ships. In Japan, both hydrogen-fueled centrifuges and ammonia-fueled ships are being studied. Kawasaki Heavy Industries, Ltd. (Tokyo, Japan), Yanmar Power Technology Co., Ltd. (Osaka, Japan), and Japan Engine Corporation (Hyogo, Japan) are developing marine hydrogen engines and marine hydrogen fuel systems for hydrogen-fueled ships. The companies plan to complete the engine lineup, which can be used for various applications, by around 2026, and conduct demonstration operations on actual vessels in cooperation with shipping companies and shipyards to implement the system in society [60].

For ammonia-fueled ships an integrated project for the development of ships equipped with ammonia-fueled domestic engines and the development and social implementation of ammonia-fueled ships is underway. The development of ships with ammonia-fueled domestic engines is being conducted by NYK Line (Tokyo, Japan), NIHON SHIPYARD CO., Ltd. (Tokyo, Japan), Japan Engine Corporation, and IHI Power Systems Corporation (Tokyo, Japan), with development commencing in December 2021. Specifically, the development and operation of an ammonia-fueled tug boat (A-Tug: Ammonia-fueled Tug Boat) is targeted to achieve an ammonia-fuel mixing ratio of 80% or higher by the time it enters service in FY2024, and efforts to improve the mixing ratio will be continued thereafter. In addition, the development and operation of an ammonia-fueled ammonia gas carrier (AFAGC) are being carried out in parallel, with the target of entering service in FY2026. The aim is to develop and operate an ammonia-fueled ammonia gas carrier, a concept that carries ammonia as cargo and runs on ammonia gas, which is vaporized from the cargo and cargo during the voyage [61]. AFAGC, for which research and development are continuing under this project, received Approval in Principle from Nippon Kaiji Kyokai in September 2022, and development toward social implementation is progressing smoothly [62].

ITOCHU Corporation (Tokyo, Japan), NIHON SHIPYARD Co., Ltd. (Tokyo, Japan), Mitsui E&S Machinery (Tokyo, Japan), Kawasaki Kisen Kaisha, Ltd. (Tokyo, Japan), and NS United Kaiun Kaisha, Ltd. (Tokyo, Japan) are engaged in the development of an integrated project for the development and social implementation of ammonia-fueled ships. The project aims to implement ammonia-fueled ships in society as early as possible, up to 2028, and to develop, own, and operate the systems and hulls [63].

Development is also underway for aircraft. Kawasaki Heavy Industries, Ltd. (Tokyo, Japan) is developing core technologies for hydrogen aircraft and is concurrently developing engine combustor and system technologies for hydrogen aircraft, developing liquefied hydrogen fuel storage tanks, and studying hydrogen aircraft airframe structures. Through these R&D efforts, the company is developing core technologies related to the airframe and engine necessary to realize next-generation aircraft and plans to conduct a ground-based demonstration test in 2030 [64].

4.3.5. Power Sector

In the power sector, in addition to the ammonia-based power generation methods, efforts are underway to implement green hydrogen in society. Asahi Kasei Corporation (Tokyo, Japan) and JGC Holdings Corporation (Kanagawa, Japan) are developing large-scale alkaline water electrolyzers and demonstrating green chemical plants. Additionally, the Yamanashi Prefectural Bureau of Public Enterprises (Yamanashi, Japan), Tokyo Electric Power Holdings, Inc., Ltd. (Tokyo, Japan), Toray Industries, Inc. (Tokyo, Japan), Hitachi Zosen Corporation (Osaka, Japan), Siemens Energy Corporation (Munich, Germany), and Miura Industry Co. (Ehime, Japan) are developing energy demand conversion and utilization technology using a PEM-type water electrolyzer.

The development of a large-scale alkaline water electrolyzer is underway with the aim of reducing the cost of alkaline water electrolyzers to 400 USD/kW by 2030, and the plan as of June 2022 is to construct a pilot test facility in March 2024 to conduct the verification tests necessary to design a 100 MW-class water electrolysis system. The pilot test facility is scheduled to be constructed in March 2024 to conduct the necessary verification tests for the design of a 100 MW water electrolysis system. As of June 2022, a modularized design policy that will help reduce the cost of systems that promote the decarbonization of large heat consumers has been decided, and discussions toward commercialization are progressing [65].

5. Challenges for Materializing the Collaboration between India and Japan

Cooperation between India, which has highly competitive green hydrogen supply potential, and Japan, which is conducting advanced demonstration research in sectors where India is prioritizing the introduction of hydrogen-related facilities (ammonia, methanol, iron, power generation, etc.), is highly significant. The challenge for the future is how quickly the technologies currently being researched and developed in Japan can be implemented in India, and at the same time, the infrastructure necessary for importing hydrogen from India can be developed.

5.1. Identifying the Costs for Transportation and Necessary Infrastructure for Hydrogen Export

While the IEA report has estimated the theoretical Production Cost of renewable energy, there has been no analysis of where and when this theoretical value will be realized in India and the costs required to transport the produced hydrogen to Japan. For the private sector to start trading in hydrogen, the costs and specific processes required to transport hydrogen need to be clarified.

There are already prior studies that should be referred to regarding the concept of cost estimation. For example, there is a paper that evaluates the cost of hydrogen transported from overseas to Japan as of 2030 by defining fixed values for the Levelized Cost of Hydrogen (LCOH) concept, assumptions for estimating renewable energy electricity costs, water electrolysis costs, and transportation cost estimates [66] and a paper that estimates the price of hydrogen for power generation and hydrogen for hydrogen stations if hydrogen is transported from Australia, China, Chile, Mexico, New Zealand, and the U.S. to the APEC region, based on necessary assumptions such as LCOH and water electrolysis costs, storage and transportation costs [67]. With reference to the concept of such studies, it is necessary to estimate the cost of transporting hydrogen to Japan from Gujarat and other areas with high potential for hydrogen production in India.

5.2. Harmonization of Regulations

In India’s National Hydrogen Mission, the importance of international harmonization of hydrogen-related regulations is mentioned, and although there is a statement that the MNRE will handle the issue centrally, no concrete scheme has yet been followed up and evaluated. On the other hand, in Japan, a study group has been meeting since 5 August 2022 to develop a hydrogen security strategy. With regard to the regulation of hydrogen, from the viewpoint of efficient social implementation of hydrogen, discussions are underway to review regulations, including those related to the handling of high-pressure gas [68]. In India, there is no law that specifically regulates hydrogen yet, and the handling of hydrogen is regulated by the same Static and Mobile Pressure Vessels (Unfired) Rules, along with other highly flammable gases such as natural gas and oxygen [69]. The rule provides guidelines for transportation, loading, and storage. Regulations are needed to address the unique characteristics of hydrogen, such as its flammability and hydrogen embrittlement; thus, the harmonization of regulations for hydrogen itself is very important from the perspective of ensuring the safe use of hydrogen and promoting its use in both India and Japan.

Harmonization is needed not only for regulations related to the handling of hydrogen itself but also for regulations related to the application of hydrogen. For example, one area where regulations may hinder the diversion of Japanese technology to India is the area of boilers. The Indian Boiler Regulation (IBR) exists as a safety regulation for boilers in India. From the perspective of ensuring boiler safety, boilers are required to undergo inspections to determine the strength of the steel used for boiler components and reviews of the design. The regulation also states that only boilers manufactured by welders certified by the Indian government can be used in India [70]. In Japan, boiler manufacturing is highly mechanized, and there are no reliable regulations for the introduction of the latest type of boilers capable of burning hydrogen into India, which means that under the current legal regulations, boilers capable of burning the latest type of hydrogen cannot be used in India.

Not only boilers, but also other areas such as steel, HDVs where specific results are expected between India and Japan and where special attention needs to be paid to ensure safety, are among the various applications required for the social implementation of hydrogen, and different regulations exist for each. These regulations need to be improved to business-friendly regulations that promote the use of hydrogen, and accelerated discussions on regulatory harmonization between India and Japan are needed.

5.3. Harmonization of Policies

Harmonization between India and Japan is needed not only in terms of regulations but also in terms of policies to promote the social implementation of hydrogen. India’s policy support is primarily focused on providing incentives for the manufacture of hydrogen-related equipment. The government’s National Hydrogen Mission, as of January 2023, has been reduced to a stance of monitoring the use of green hydrogen without penalties, which was initially considered a possibility to be implemented as part of the National Hydrogen Mission [25]. The situation lacks the provision of incentives for demand creation in the initial phase. In addition to this, there are even promotional measures that reduce incentives to introduce hydrogen, such as the banking system introduced in Gujarat state [26], making cooperation with India difficult. Japan is promoting facilitating hydrogen imports, and in order to solidify hydrogen cooperation between India and Japan, there is a need to harmonize at the policy level as well to compose a robust value chain that is beneficial to both countries.

5.4. Harmonization of Definitions of “Green Hydrogen”

The definition of “green hydrogen” also requires further discussion between India and Japan. For example, there is a worldwide debate on the color of hydrogen, with some defining “green hydrogen” as hydrogen produced exclusively from surplus renewable energy sources without any greenhouse gas emissions, “blue hydrogen” as hydrogen produced from fossil fuels using carbon capture and storage technology, and “pink hydrogen” as hydrogen produced from electricity generated by nuclear power. There is a movement to define hydrogen produced from fossil fuels using carbon capture and storage technology as “blue hydrogen” and hydrogen produced from electricity generated by nuclear power as “pink hydrogen [16]. There is a possibility of a conflict of opinions between India, which has strong incentives to define “green hydrogen” as hydrogen generated from electricity (electricity generated from other sources), and other countries that want to define “green hydrogen” as hydrogen generated from the electricity that does not emit greenhouse gases, such as wind power, including at night. In order to avoid supply chain breakdowns due to changes in international discussions, it is necessary for Japan, as an importing country, and India, as an exporting country, to create a definition of “green hydrogen” that can be accepted fairly by the world, while referring to discussions around the world, in order to realize a stable proposal with a low environmental impact. The definition of “green hydrogen” needs to be created in order to realize a stable and environmentally friendly proposal.

5.5. Establish an Environment in Which Intellectual Property Is Reliably Protected

One of the biggest barriers to investment in India for Japanese companies is concern over intellectual property protection. In a 2013 survey of 113 Japanese companies operating in India, 45.9% of SMEs reported some problems, compared to 29.7% of companies that said they had no problems and 24.3% that did not respond. The breakdown was as follows: slightly problematic (21.6%), problematic (10.8%), very problematic (8.1%), and extremely serious (5.4%) [71]. In addition, the Unfair Competition Prevention Law that exists in Japan is a law that is less effective than protection by patents and other intellectual property rights, but can be used to protect trade secrets by companies that do not want their information to be widely known or want to protect their secrets over the long term, does not exist in India [72]. Therefore, companies holding hydrogen technology as a trade secret can only rely on contractual and common law protection to protect their trade secrets. On the other hand, with patent protection, the invention is disclosed to the public, which means that the invention becomes known to many people, and once the patent term expires, the invention, etc., can, in principle, be freely used by anyone. In addition, it takes an average of 6.7 years to obtain a patent in India, making the process of obtaining a patent, one of the few measures of protecting business secrets, extremely difficult [73]. Although the Patent Prosecution Highway (PPH), a framework for expedited review by the patent authorities of both countries of procedures for obtaining patents in areas agreed upon by both countries, has already been introduced between India and Japan, it does not cover hydrogen-related technologies [74]. To distribute hydrogen and hydrogen-related technologies in both countries as quickly as possible, it is important to ensure an environment where intellectual property is properly protected in India and to create an environment where companies with cutting-edge hydrogen-related technologies can actively do business in India.

6. Future Directions to Develop the Potential of Collaboration

For concrete results to come to fruition, it is necessary to promote discussions between the two countries to resolve the issues of (1) cost visualization, including transportation costs, (2) harmonization of regulations, (3) harmonization of promotion measures between the two countries, (4) harmonization of the definition of “green hydrogen” and (5) protection of intellectual property.

The technologies related to hydrogen transportation are still in the developmental stage, and it takes time for hydrogen transportation projects to become profitable. Therefore, waiting for the private sector to act on the calculation of hydrogen transportation costs may take longer than necessary. It is desirable that the private companies involved in the hydrogen business and the governments of both countries actively disclose data, which does not affect corporate activities, necessary for the cost calculations so that a variety of institutions, including academia, think tanks, and NGOs, can conduct research on the (1) cost visualization.

Discussions on (2) harmonization of regulations, which take time to implement, should be initiated as soon as possible; although there is mention of this in the National Hydrogen Mission released in January 2023 [3], a specific scheme to promote harmonization of regulations has not yet been identified. A framework is needed to facilitate discussions between the governments of India and Japan on regulatory harmonization, including boilers and other peripheral equipment for utilizing hydrogen. In addition, to realize the export of hydrogen produced in India to Japan, visualization of the costs and challenges of the entire value chain required to import hydrogen from India and harmonization of the definition of hydrogen between the two countries will be very important issues to be discussed in the future.

Since discussions on (2) harmonization of regulations and (3) incentives in technologically new areas will be necessary, it will be important to develop discussions among academia in addition to the framework of intergovernmental and inter-industry dialogues. Not only the research in the natural science field that contributes to the development of hydrogen technology itself but also the studies which visualize the values and potentials of hydrogen technologies in our society are crucially important. For instance, calculation of the social cost of hydrogen technology, risk communication to enhance social acceptance of hydrogen, and measuring the contribution of hydrogen to carbon reduction are important for installing hydrogen technologies in our society.

(4) Harmonization of the definition of “green hydrogen” could be realized through the efforts of both India and Japan. It is important to create practical standards that will contribute to global carbon neutrality in a realistic manner through the promotion of concrete projects between the two countries and the actual activation of trade rather than discussions on only paper.

(5) Protection of intellectual property is a general issue that is not limited to the hydrogen domain. It is important to have an inter-governmental framework that facilitates the discussions for appropriately securing the intellectual properties of all stakes.

7. Conclusions

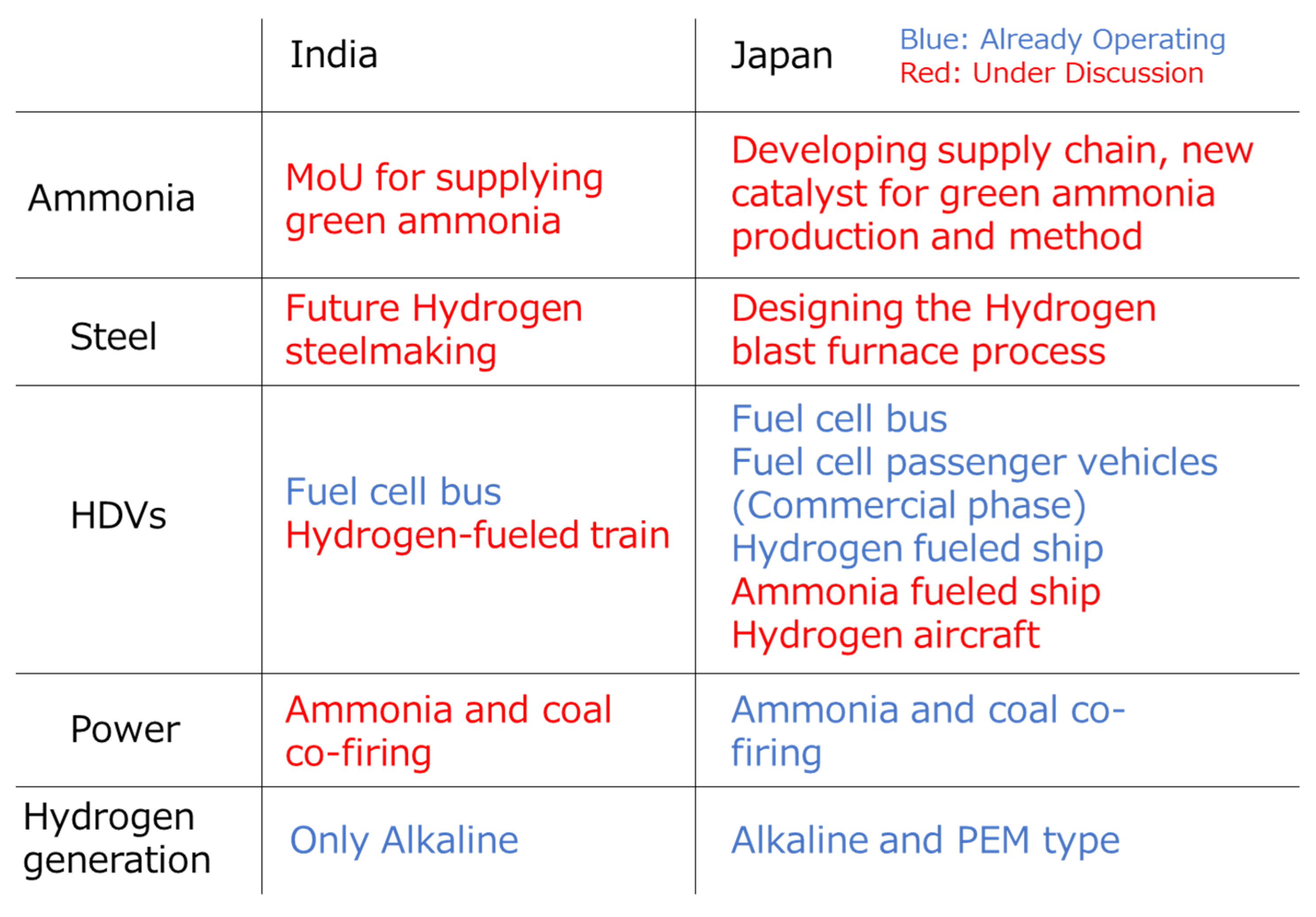

Around the world, discussions are being held on the utilization of hydrogen, and the certainty of the technology and the price required for its introduction into society are being verified from all angles. The following four factors are strong incentives for India and Japan to deepen cooperation in the hydrogen field compared with other areas: (1) India has a high potential hydrogen supply capacity, (2) India is very active in implementing hydrogen in society, (3) Japan is already conducting R&D in areas of high interest to India as Figure 4, which summarizes projects in the areas of particular interest to India listed in Section 3.3 and Section 4.2, shows and (4) Japan will need to import hydrogen from other countries in the future.

Given the fact that concrete demonstration projects are already underway in Japan in the Ammonia Sector, Steel Sector, HDVs, and Power Sector, which are India’s priority areas where hydrogen is actively being utilized. Discussions are needed to build up best practices in these areas.

The issues of (1) cost visualization, including transportation costs, (2) harmonization of regulations, (3) harmonization of promotion measures between the two countries, (4) definition of “green hydrogen,” and (5) protection of intellectual property are main challenges to be overcome. Thus, disclosures of necessary data for cost visualization of hydrogen transportation, further inter-governmental cooperations between India and Japan, and facilitations of the discussions on hydrogen among various stakes are key actions for materializing various joint hydrogen projects between both countries.

Author Contributions

Conceptualization, T.O. and R.S.; methodology, T.O. and R.S.; validation, T.O.; formal analysis, T.O.; investigation, T.O.; data curation, T.O.; writing—original draft preparation, T.O; writing—review and editing, R.S.; visualization, T.O.; supervision, R.S.; funding acquisition, R.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

No new data were created or analyzed in this study. Data sharing is not applicable to this article.

Acknowledgments

The authors acknowledge the support from India Japan Laboratory of Keio University.

Conflicts of Interest

The authors declare no conflict of interest.

References

- IEA. Russia’s War on Ukraine–Topics. 2022. Available online: https://www.iea.org/topics/russia-s-war-on-ukraine (accessed on 11 February 2023).

- Cox, S.; Beshilas, L.; Hotchkiss, E. Renewable Energy to Support Energy Security–NREL. 2019. Available online: https://www.nrel.gov/docs/fy20osti/74617.pdf (accessed on 11 February 2023).

- Ministry of New and Renewable Energy of India (MNRE). Cabinet Approves National Green Hydrogen Mission. Press Information Bureau. 4 January 2023. Available online: https://pib.gov.in/PressReleasePage.aspx?PRID=1888547 (accessed on 23 January 2023).

- Ministry of Environment, Forest and Climate Change (MoEFCC). India Stands Committed to Reducing Emissions Intensity of GDP by 45% by 2030 and Reach to Net-Zero by 2070, While Developing Sustainably: Shri Bhupender Yadav. Press Information Bureau. 2023. Available online: https://www.pib.gov.in/PressReleseDetail.aspx?PRID=1897093 (accessed on 11 February 2023).

- The Council of Ministers on the Renewable Energy and Hydrogen (TCMREH). Basic Hydrogen Strategy. The Council of Ministers on the Renewable Energy and Hydrogen. 2017. Available online: https://www.cas.go.jp/jp/seisaku/saisei_energy/pdf/hydrogen_basic_strategy.pdf (accessed on 22 January 2023).

- Ministry of New and Renewable Energy of India (MNRE). Increase in the Use of Green Hydrogen. Press Information Bureau of India. 2022. Available online: https://pib.gov.in/PressReleasePage.aspx?PRID=1883114#:~:text=In%20the%20Independence%20Day%20speech,and%20deployment%20of%20Green%20Hydrogen (accessed on 29 January 2023).

- Embassy of Japan in India (EoJ). India-Japan Clean Energy Partnership. 2022. Available online: https://www.in.emb-japan.go.jp/files/100319131.pdf (accessed on 29 January 2023).

- U.S. Department of Energy (USDoE). Hydrogen Benefits and Considerations. Alternative Fuels Data Center: Hydrogen Benefits and Considerations. 2023. Available online: https://afdc.energy.gov/fuels/hydrogen_benefits.html (accessed on 11 February 2023).

- European Commission. Repowereu: Affordable, Secure and Sustainable Energy for Europe. 2022. Available online: https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal/repowereu-affordable-secure-and-sustainable-energy-europe_en (accessed on 9 April 2023).

- European Commission. Commission Sets Out Rules for Renewable Hydrogen. 2023. Available online: https://ec.europa.eu/commission/presscorner/detail/en/ip_23_594 (accessed on 9 April 2023).

- Government of United Kingdom. Policy Paper British Energy Security Strategy. 2022. Available online: https://www.gov.uk/government/publications/british-energy-security-strategy/british-energy-security-strategy#hydrogen (accessed on 9 April 2023).

- Department of Industry, Innovation and Science of Australia. Australia’s National Hydrogen Strategy. 2019. Available online: https://www.dcceew.gov.au/energy/publications/australias-national-hydrogen-strategy (accessed on 9 April 2023).

- Holladay, J.D.; Hu, J.; King, D.L.; Wang, Y. An overview of Hydrogen production technologies. Catal. Today 2009, 139, 244–260. [Google Scholar] [CrossRef]

- Agency for Natural Resources and Energy of Japan (ANRE). Next generation energy “Hydrogen”, How can we generate?—Jisedai Enerugi “Suiso”, Somosomo Douyatte Tsukuru? Agency for Natural Resources and Energy of Japan. 12 October 2021. Available online: https://www.enecho.meti.go.jp/about/special/johoteikyo/suiso_tukurikata.html (accessed on 21 January 2023).

- World Economic Forum. Grey, Blue, Green—Why Are There So Many Colours of Hydrogen? 2021. Available online: https://www.weforum.org/agenda/2021/07/clean-energy-green-hydrogen/ (accessed on 9 April 2023).

- National Grid Group. The Hydrogen Colour Spectrum. 2023. Available online: https://www.nationalgrid.com/stories/energy-explained/hydrogen-colour-spectrum#:~:text=Hydrogen%20is%20an%20invisible%20gas,the%20different%20types%20of%20hydrogen (accessed on 9 April 2023).

- IEA. Hydrogen Supply, IEA, Paris. 2022. Available online: https://www.iea.org/reports/Hydrogen-supply (accessed on 9 April 2023).

- IEA. The Future of Hydrogen, IEA, Paris. 2019. Available online: https://www.iea.org/reports/the-future-of-Hydrogen (accessed on 21 January 2023).

- World Bank. Commodity Markets Annual Prices. Commodity Markets. January 2023. Available online: https://www.worldbank.org/en/research/commodity-markets (accessed on 21 January 2023).

- IEA. India Energy Outlook 2021, IEA, Paris. 2021. Available online: https://www.iea.org/reports/india-energy-outlook-2021 (accessed on 21 January 2023).

- Vanamali, K.V. Why does India Face a Recurring Power Shortage Despite Enough Coal Stock? Business Standard News. 2022. Available online: https://www.business-standard.com/podcast/economy-policy/why-does-india-face-a-recurring-power-shortage-despite-enough-coal-stock-122060100089_1.html (accessed on 22 January 2023).

- Ministry of Environment, Forest and Climate Change (MEFCC). India Submits Its Long-Term Low Emission Development Strategy to UNFCCC. 2022. Available online: https://pib.gov.in/PressReleasePage.aspx?PRID=1875816 (accessed on 22 January 2023).

- Japan External Trade Organization (JETRO). Diesel Generators in the Delhi Metropolitan Area Will Be Banned in Principle from October Onward (India). 2022. Available online: https://www.jetro.go.jp/biznews/2022/08/21ca073dc706c416.html (accessed on 22 January 2023).

- Ministry of Power of India (MoP). Green Hydrogen policy |Government of India| Ministry of Power. 2022. Available online: https://www.powermin.gov.in/en/content/green-Hydrogen-policy (accessed on 22 January 2023).

- NITI Aayog and RMI. Harnessing Green Hydrogen. 2022. Available online: https://rmi.org/insight/harnessing-green-Hydrogen/ (accessed on 22 January 2023).

- Government of Gujarat Energy and Petrochemicals Department (GGEPD). Gujarat Solar Power Policy 2021—Guvnl Suryagujarat. 2020. Available online: https://suryagujarat.guvnl.com/documents/2020/Gujarat%20Solar%20Power%20Policy%202021.pdf (accessed on 22 January 2023).

- Ministry of New and Renewable Energy of India (MNRE). Annual Report 2021–2022. 2021. Available online: https://mnre.gov.in/img/documents/uploads/file_f-1671012052530.pdf (accessed on 25 January 2023).

- Kumar, J.C.R.; Majid, M.A. Renewable Energy for Sustainable Development in India: Current status, future prospects, challenges, employment, and Investment Opportunities. Energy Sustain. Soc. 2020, 10, 7. [Google Scholar] [CrossRef]

- IEA. Global Hydrogen Review 2022 (p. 97), IEA, Paris. 2022. Available online: https://www.iea.org/reports/global-hydrogen-review-2022 (accessed on 25 January 2023).

- IRENA. Green Hydrogen Cost Reduction: Scaling up Electrolysers to Meet the 1.5 °C Climate Goal; International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2020. [Google Scholar]

- Gagal, V. Land Acquisition Continues to Be a Roadblock for Renewable Energy Projects & nbsp; The Hindu Business Line. 2022. Available online: https://www.thehindubusinessline.com/opinion/land-acquisition-continues-to-be-a-roadblock-for-renewable-energy-projects/article65809202.ece (accessed on 12 February 2023).

- Yara. Yara Clean Ammonia: Enabling the Hydrogen Economy: Yara International. 2022. Available online: https://www.yara.com/yara-clean-ammonia/ (accessed on 12 February 2023).

- Volza. India Fertilizer Imports–Volza. 2022. Available online: https://www.volza.com/p/fertilizer/import/import-in-india/ (accessed on 12 February 2023).

- Ministry of Chemicals and Fertilizers (MoCF). Year-End Review of the Department of Fertilizers-2022. Press Information Bureau. December 2022. Available online: https://pib.gov.in/PressReleasePage.aspx?PRID=1886054#:~:text=Total%20Subsidy%20Outgo&text=The%20Subsidy%20approved%20by%20Cabinet,(SSP)%20through%20freight%20subsidy (accessed on 12 February 2023).

- Pathak, K. Greenko to Supply 250K Tonnes Green Ammonia to Germany’s Uniper, 1st Indian Co to Start Exports from 2025. The Economic Times. 2023. Available online: https://economictimes.indiatimes.com/industry/renewables/germany-based-uniper-signs-pact-with-greenko-to-source-green-ammonia-from-india/articleshow/97698964.cms (accessed on 12 February 2023).

- IEA. Energy Technology Perspectives 2020 (P.60), IEA, Paris. 2020. Available online: https://www.iea.org/reports/energy-technology-perspectives-2020 (accessed on 12 February 2023).

- NIKKEI. Nippon Steel Corporation to Invest 1 Trillion Yen in India—Nittetsu, Indo de Icchyouen Toushi. 2022. Available online: https://www.nikkei.com/article/DGKKZO64706290Y2A920C2TB2000/ (accessed on 23 January 2023).

- The Economic Times. India’s First Hydrogen Fuel Cell Bus Unveiled in Pune—India’s First. The Economic Times. 2022. Available online: https://economictimes.indiatimes.com/industry/renewables/indias-first-hydrogen-fuel-cell-bus-unveiled-in-pune/indias-first/slideshow/93752486.cms?from=mdr (accessed on 12 February 2023).

- Toyota Kirloskar Motor (TKM). Toyota Kirloskar Motor Supplies Hydrogen Fuel Cell Module for a Proto Examination and Feasibility Study Purposes, Contributing to Nation’s Energy Self-Reliance and Carbon Neutral Goals. 2023. Available online: https://www.toyotabharat.com/news/2023/tkm-supplies-hydrogen-fuel-cell-module-for-a-proto-examination-and-feasibility.html (accessed on 12 February 2023).

- Paliwal, A. India’s 1st Hydrogen Train Will Come by Dec 2023 on Heritage Routes: Railway Min. Mint. 2023. Available online: https://www.livemint.com/news/india/indias-1st-hydrogen-train-will-come-by-dec-2023-on-heritage-routes-railway-minister-ashwini-vaishnaw-11675302269759.html (accessed on 12 February 2023).

- Central Electricity Authority of India (CEA). Draft Guidelines for Resource Adequacy Planning Framework for India. 2022. Available online: https://cea.nic.in/wp-content/uploads/irp/2022/09/Draft_RA_Guidelines___23_09_2022_final.pdf (accessed on 13 February 2023).

- IEA. Electricity Information—Data Product. IEA. 2022. Available online: https://www.iea.org/data-and-statistics/data-product/electricity-information#overview (accessed on 13 February 2023).

- IHI Corporation (IHI). IHI and Partners to Explore Ammonia Co-Firing at Indian Thermal Power Plant as Part of Japanese National Project. 2022. Available online: https://www.ihi.co.jp/en/all_news/2022/resources_energy_environment/1198023_3488.html (accessed on 13 February 2023).

- Agency for Natural Resources and Energy (ANRE). Energy White Paper. 2022. Available online: https://www.enecho.meti.go.jp/about/whitepaper/2022/html/2-1-1.html (accessed on 22 January 2023).

- Prime Minister’s Office of Japan (PMOJ). Global Warming Prevention Headquarters: 2020: A Day in the Life of the Prime Minister: News. PMOJ’s Web Site. 30 October 2020. Available online: https://www.kantei.go.jp/jp/99_suga/actions/202010/30ondanka.html (accessed on 23 January 2023).

- Ministry of Economy, Trade and Industry of Japan (METI). Green Growth Strategy through Achieving Carbon Neutrality in 2050. 2021. Available online: https://www.meti.go.jp/english/policy/energy_environment/global_warming/ggs2050/index.html (accessed on 23 January 2023).

- Ministry of the Environment of Japan (MoE). Japan’s Renewable Energy Deployment Potential. 2022. Available online: https://www.renewable-energy-potential.env.go.jp/RenewableEnergy/doc/gaiyou3.pdf (accessed on 13 February 2023).

- Ministry of Economy, Trade and Industry of Japan (METI). Current Status of Domestic and Foreign Renewable Energies and Draft Issues to be Discussed by the Procurement Price Calculation Committee this Fiscal Year. 2022. Available online: https://www.meti.go.jp/shingikai/santeii/index.html (accessed on 13 February 2023).

- Agency for Natural Resources and Energy of Japan (ANRE). Commercial Hydrogen and Ammonia Supply Chain Support Programs. 2022. Available online: https://www.meti.go.jp/shingikai/enecho/shoene_shinene/suiso_seisaku/index.html (accessed on 13 February 2023).

- JERA. Development of New Catalyst for Ammonia Production and Start of Technology Demonstration for Establishment of Fuel Ammonia Supply Chain—Adopted as Green Innovation Fund Project: Press Release (2022). 2022. Available online: https://www.jera.co.jp/information/20220107_824 (accessed on 22 January 2023).

- Idemitsu Kosan. Development of Ammonia Production Technology under Ambient Temperature and Pressure” Selected for NEDO Green Innovation Fund-Aiming to Realize Carbon-Free Ammonia Production Process: News Releases. 2022. Available online: https://www.idemitsu.com/jp/news/2021/220107.html (accessed on 22 January 2023).

- Agency for Natural Resources and Energy of Japan (ANRE). Research, Development, and Social Implementation Plan for the “Establishment of Fuel Ammonia Supply Chain”. 2021. Available online: https://www.nedo.go.jp/content/100937228.pdf (accessed on 22 January 2023).

- IHI Corporation. Adoption of Demonstration of Technology to Improve Ammonia Co-firing Rate at Hekinan Thermal Power Station ∣FY2021∣ News. 2022. Available online: https://www.ihi.co.jp/ihi/all_news/2021/resources_energy_environment/1197627_3345.html (accessed on 22 January 2023).

- Mitsubishi Heavy Industries (MHI). Development and Demonstration of High Ammonia Co-firing Technology in Coal Boilers. 2022. Available online: https://www.mhi.com/jp/news/22010702.html (accessed on 22 January 2023).

- Norihiko, I. Research and Development of Gas Turbine Using Ammonia as Fuel. J. 2022. Available online: https://www.jstage.jst.go.jp/article/sekiyu/2022/0/2022_10/_article/-char/en (accessed on 22 January 2023).

- Furukawa Electric. Establishment of a New Organization, the “Local Production for Local Energy Project Team,” for the Practical Application of Green LP Gas, which Contributes to the Realization of a Decarbonized Society. 2022. Available online: https://www.furukawa.co.jp/release/2022/kei_20220915.html (accessed on 22 January 2023).

- Ministry of Economy, Trade and Industry of Japan (METI). Research, Development, and Social Implementation Plan for the “Hydrogen Utilization in Ironmaking Processes” Project. 2021. Available online: https://www.nedo.go.jp/content/100937319.pdf (accessed on 22 January 2023).

- Tokyo Metropolitan Government (TMG). Toei Buses Starts Fuel Cell Bus Operation! First Commercial Operation by a Commercial Vehicle in Japan. Toei Buses Starts Fuel Cell Bus Operation. 2017. Available online: https://www.metro.tokyo.lg.jp/tosei/hodohappyo/press/2017/02/24/07.html (accessed on 23 January 2023).

- Ministry of Economy, Trade and Industry of Japan (METI). Study Group on Structural Changes in Mobility and the Direction of Automobile Policies for 2030 and Beyond. 2022. Available online: https://www.meti.go.jp/shingikai/mono_info_service/mobility_kozo_henka/index.html (accessed on 23 January 2023).

- Kawasaki Heavy Industries (KHI). “Development of Marine Hydrogen Engine and MHFS” Selected for NEDO Green Innovation Fund Project—Progress Toward Realization of Zero-Emission Ships. 2021. Available online: https://www.khi.co.jp/pressrelease/news_211026-2_2.pdf (accessed on 22 January 2023).

- Nippon Yusen Kabushiki Kaisha (NYK). Launch of a Demonstration Project for Social Implementation of Ships Equipped with Ammonia-Fueled Domestic Engines. 2021. Available online: https://www.nyk.com/news/2021/20211026_03.html (accessed on 23 January 2023).

- Nippon Yusen Kabushiki Kaisha (NYK). NYK Receives Basic Design Approval (AIP) for Ammonia Fueled Ammonia Carrier. 2022. Available online: https://www.nyk.com/news/2022/20220907_02.html (accessed on 23 January 2023).

- ITOCHU Corporation (ITOCHU). Adoption of the Green Innovation Fund Project for an Integrated Project for the Development and Social Implementation of Ammonia Fueled Ships. 2021. Available online: https://www.itochu.co.jp/ja/news/press/2021/211026.html (accessed on 23 January 2023).

- Kawasaki Heavy Industries (KHI). Development of Core Technologies for Hydrogen Aircraft’ Selected as NEDO Green Innovation Fund Project: Press Release. 2021. Available online: https://www.khi.co.jp/pressrelease/detail/20211105_1.html (accessed on 23 January 2023).

- New Energy and Industrial Technology Development Organization (NEDO). Green Innovation Fund Project/Hydrogen Production by Water Electrolysis Using Electricity Derived from Renewable Energies and Other Sources: Report of the WG for FY2022. 2022. Available online: https://www.meti.go.jp/shingikai/sankoshin/green_innovation/energy_structure/pdf/009_05_00.pdf (accessed on 22 January 2023).

- Nishi, M.; Yamamoto, H.; Takei, K. Cost Comparisons of Hydrogen Produced from Fossil Fuels and Renewable Energy in 2030. Proc. Int. Conf. Power Eng. ICOPE 2021, 15, 2021-0160. [Google Scholar] [CrossRef]

- Kan, S.; Shibata, Y. Evaluation of the economics of Renewable Hydrogen Supply in the APEC Region. 2018. Available online: https://eneken.ieej.or.jp/data/7944.pdf (accessed on 25 January 2023).

- Ministry of Economy, Trade and Industry of Japan (METI). Report of the Study Group on the Development of a Hydrogen Safety Strategy—Hydrogen Safety Strategy—(Draft). 2022. Available online: https://www.meti.go.jp/shingikai/safety_security/suiso_hoan/pdf/005_01_00.pdf (accessed on 25 January 2023).

- Ministry of Commerce and Industry of India (MoC). Static and Mobile Pressure Vessels (Unfired) (Amendment) Rules 2021 [G.S.R. 96(E)]: Petroleum & Explosive Safety Organisation. 2021. Available online: https://peso.gov.in/web/static-and-mobile-pressure-vessels-unfired-amendment-rules-2021-gsr-96e (accessed on 13 February 2023).

- Ministry of Commerce and Industry of India (MoC). The Indian Boiler Regulations, 2022. 2022. Available online: https://dpiit.gov.in/whats-new/indian-boiler-regulations-2022 (accessed on 14 February 2023).

- Sato, T. Small and Medium Enterprises’ Expansion into India—A Study Based on the 2013–2014 Questionnaire Survey. 2017. Available online: https://shokosoken.or.jp/shokokinyuu/2017/11/201711_2.pdf (accessed on 14 February 2023).

- Ministry of Economy, Trade and Industry of Japan (METI). Unfair Competition Prevention Law. 2022. Available online: https://www.meti.go.jp/policy/economy/chizai/chiteki/pdf/unfaircompetition_textbook.pdf (accessed on 15 February 2023).

- JETRO. Intellectual Properties Situation in India. WIPO. 2022. Available online: https://www.wipo.int/edocs/mdocs/mdocs/ja/wipo_webinar_wjo_2022_16/wipo_webinar_wjo_2022_16_pres.pdf (accessed on 15 February 2023).

- Ministry of Commerce and Industry of India (MoC). Procedure Guidelines for Patent Prosecution Highway (PPH). 2019. Available online: https://ipindia.gov.in/writereaddata/portal/news/591_1_pph_procedure_guideline_combined_20191128_final.pdf (accessed on 15 February 2023).

Figure 1.

Hydrogen classifications.

Figure 2.

Liquefied Natural Gas Price (USD/mmbtu) [19].

Figure 2.

Liquefied Natural Gas Price (USD/mmbtu) [19].

Figure 3.

Coal Price (USD/mt) [19].

Figure 3.

Coal Price (USD/mt) [19].

Figure 4.

Progress of projects in areas of particular interest to India.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| State Name | Wind Power Potential at 120 m (GW) | Small Hydro Power Potential (GW) | Solar Energy Potential (GW) | Total (GW) |

|---|---|---|---|---|

| Andhra Pradesh | 74.9 | 0.409 | 38.44 | 113.749 |

| Gujarat | 142.56 | 0.201 | 35.77 | 178.531 |

| Karnataka | 124.15 | 3.726 | 24.7 | 152.576 |

| Maharashtra | 98.21 | 0.786 | 64.32 | 163.316 |

| Rajasthan | 127.75 | 0.051 | 142.31 | 270.111 |

Table 2.

Installed capacities of renewable energy in high-potential states [27].

Table 2.

Installed capacities of renewable energy in high-potential states [27].

| State Name | Wind Power Installed as on 31 December 2021 (GW) | Small Hydro Power Installed as on 31 December 2021 (GW) | Grid Connected Solar Projects as on 31 December 2021 (GW) | Total (GW) |

|---|---|---|---|---|

| Andhra Pradesh | 4.096 | 0.162 | 4.292 | 8.55 |

| Gujarat | 9.007 | 0.085 | 6.206 | 15.298 |

| Karnataka | 5.077 | 1.28 | 7.497 | 13.854 |

| Maharashtra | 5.012 | 0.381 | 2.507 | 7.9 |

| Rajasthan | 4.326 | 0.024 | 9.98 | 14.33 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Otaki, T.; Shaw, R. The Potential of Collaboration between India and Japan in the Hydrogen Sector. Energies 2023, 16, 3596. https://0-doi-org.brum.beds.ac.uk/10.3390/en16083596

AMA Style

Otaki T, Shaw R. The Potential of Collaboration between India and Japan in the Hydrogen Sector. Energies. 2023; 16(8):3596. https://0-doi-org.brum.beds.ac.uk/10.3390/en16083596

Chicago/Turabian StyleOtaki, Takuma, and Rajib Shaw. 2023. "The Potential of Collaboration between India and Japan in the Hydrogen Sector" Energies 16, no. 8: 3596. https://0-doi-org.brum.beds.ac.uk/10.3390/en16083596

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.