The eIDAS Regulation: A Survey of Technological Trends for European Electronic Identity Schemes

, , , , and

, , , , and

Abstract

:1. Introduction

- Security and Privacy:

- –

- Which are the standard authentication protocols adopted by the eID schemes?

- –

- Which are the crucial implementation choices taken to deploy the identified standard authentication protocols in the previous question by the eID schemes?

- Security and Usability:

- –

- Which are the adopted authentication methods for three levels of assurance?

- We extend our analysis regarding different authentication mechanisms chosen by MSs, adopted authentication standards and mobile-based authentication solutions by adding the recently notified eID schemes. More specifically, we add the eID schemes of the Czech Republic (MojeID, MEG), Austria (Austria ID), Sweden (BankID, Freja eID, EFOS), and Malta (Identity Malta);

- We discuss two new research questions to identify the trends for the eID schemes that provide solutions based on the OpenID Connect. In particular, we investigate the adopted OpenID Connect profiles and implementation choices for these solutions;

- We refine and extend a set of lessons learned by adding new considerations specific to solutions based on OpenID Connect; and

Paper Structure

2. Methodology

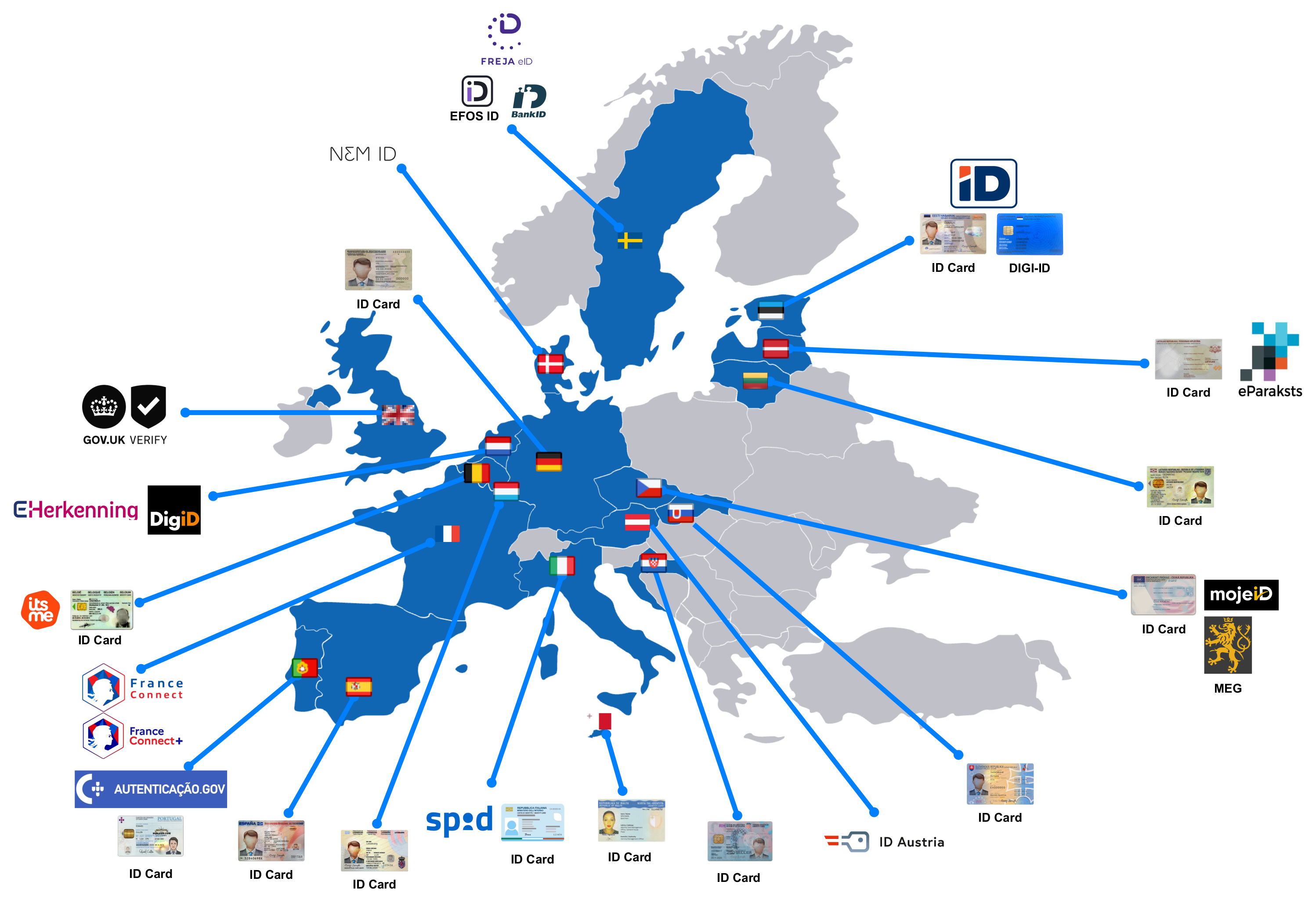

2.1. eID Schemes Selection

2.2. Research Questions

- RQ1. Based on the LoA (Low, Substantial, and High), what are the supported authentication methods in notified eID schemes?

- RQ2. Which standards are used to implement authentication solutions in notified eID schemes?

- RQ3. For the solutions based on OpenID Connect, which are the profiles followed by the notified eID schemes?

- RQ4. For the solutions based on OpenID Connect, which are the implementation choices considered by the notified eID schemes?

- RQ5. Which technologies are used to implement authentication solutions using mobile applications in notified eID schemes?

2.3. Data Source

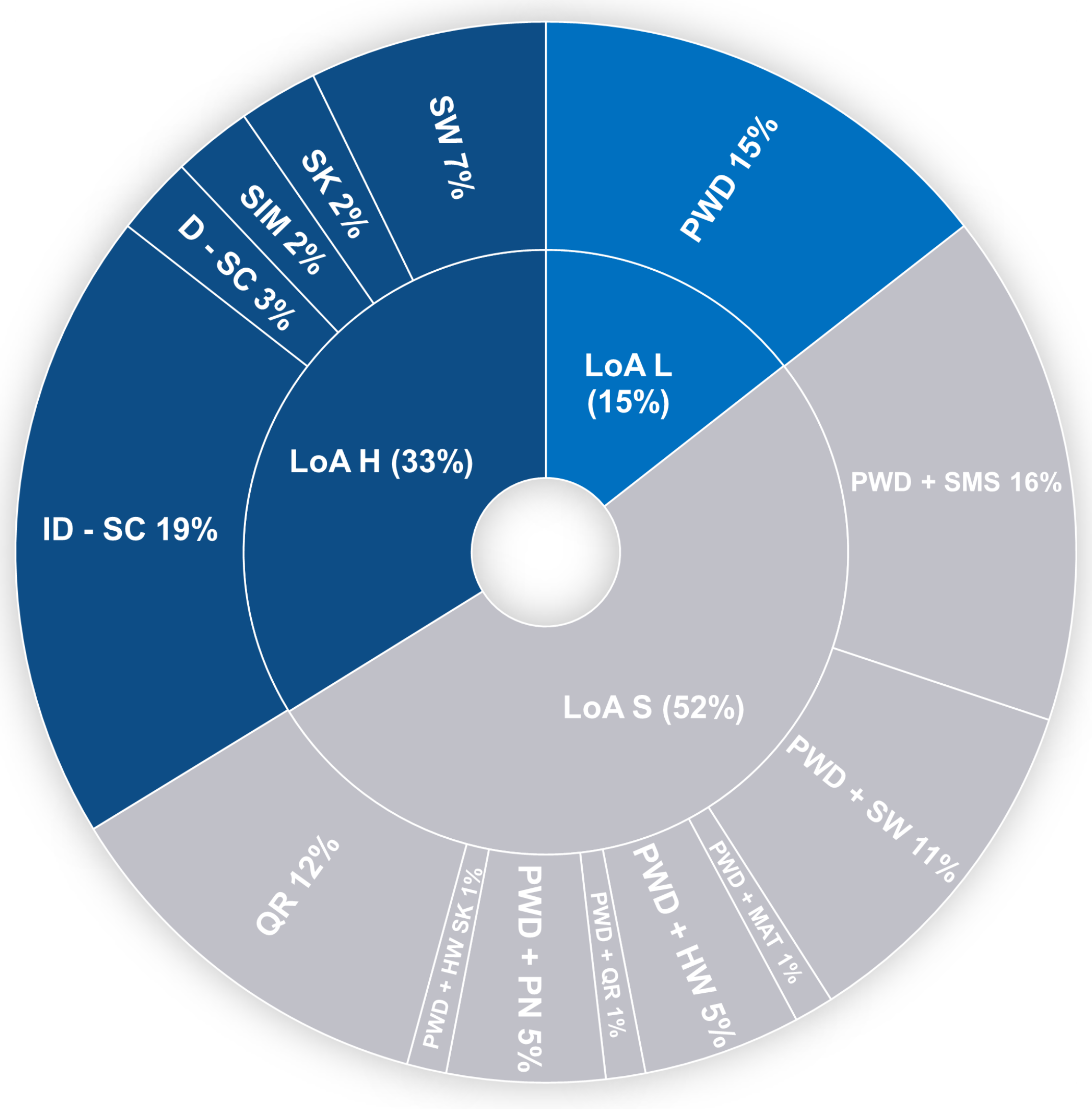

3. RQ1: Authentication Mechanisms Based on LoA

- LoA Low (L): comparable with LoA2 of ISO 29115, it provides a limited degree of confidence in the asserted identity of a person, single-factor authentication is acceptable.

- LoA Substantial (S): comparable with LoA3 of ISO 29115, at least two authentication factors should be used.

- LoA High (H): comparable with LoA4 of ISO 29115, at least two authentication factors should be used, and it should guarantee protection against duplication and tampering by attackers with high potential.

3.1. Authentication Mechanisms: LoA Low

3.2. Authentication Mechanisms: LoA Substantial

- PWD + SMS: username/password (knowledge factor) plus an OTP sent via SMS message to the registered phone number (possession factor) of the user;

- PWD + SW: username/password (knowledge factor) plus an OTP generated each time s/he requested it by an OTP software application (possession factor) installed on his/her phone;

- PWD + MAT: username/password (knowledge factor) plus a physical document (possession factor), also called “matrix”, with the list of codes (OTPs) that s/he has to use to reply to the randomly generated challenge from the online service;

- PWD + HW: username/password (knowledge factor) plus a physical electronic device (possession factor) which generates an OTP each time the user requests it;

- PWD + QR: username/password (knowledge factor) plus the scan of a QR code from a registered application (possession factor) that then generates an OTP to the online service;

- PWD + PN: username/password (knowledge factor) plus the sending of a Push Notification directly to a secure application on the user’s device (possession factor), alerting the user that an authentication attempt is taking place. Note that the user should provide a PIN (possession factor) or use biometrics (inherence factor) to complete the authentication after receiving the notification on the registered device;

- PWD + SK: username/password (knowledge factor) plus hardware security key (possession factor) that contains a private key (and the corresponding certificate) to send a signed OTP challenge to the authentication server. The user should provide a PIN (knowledge factor) or use biometrics (inherence factor) to complete the user authentication;

- QR: is an authentication capability that permits a registered device (possession factor) to scan a QR Code. Then, the user should provide a PIN (knowledge factor) or use biometrics (inherence factor) to complete the user authentication.

- Concerning the OTP implementation approaches, SMS (13 out of 20) is the most adopted approach, and PWD + Matrix, PWD + QR Code, and PWD + HW SK (1 out of 20 eID means) are the least adopted ones within the eID means;

- None of the eID means under analysis support the Email within their OTP implementation approach;

- Only 4 out of 20, and 10 out of 20 eID means under analysis support the push notification and Login with QR Code mechanism, respectively.

3.3. Authentication Mechanisms: LoA High

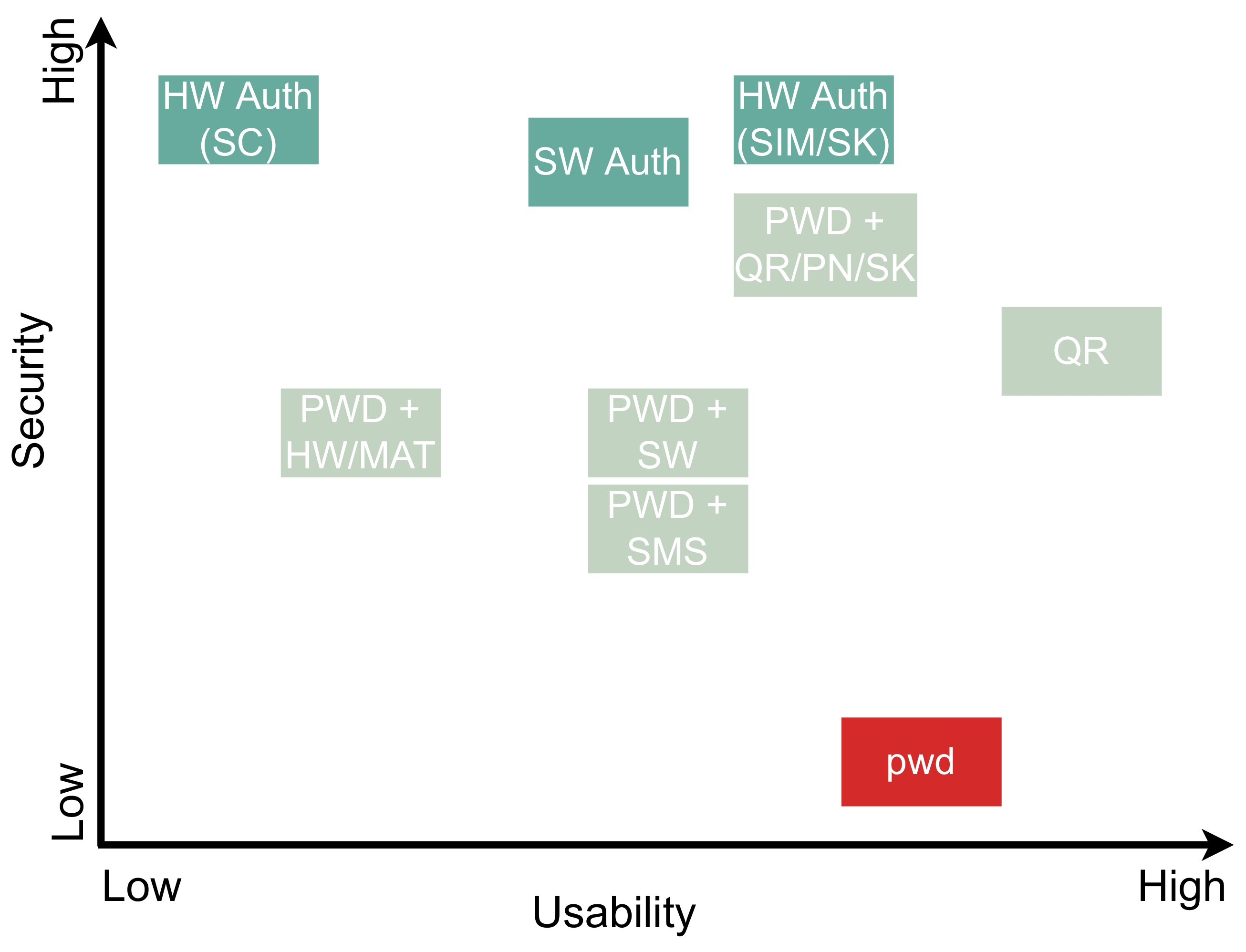

- Hardware Authenticator (HW Auth): indicates the support of login by using hardware authenticators (e.g., smart cards) by the eID means under analysis. Note that the hardware authenticator in LoA H refers to a hardware device that can securely store a client certificate. In contrast, the PWD + HW in LoA S refers to a hardware device capable of generating an OTP. We detected the following HW Auths:

- Smart card indicates the support of login by using a physical smart card (SC). In our analysis, we distinguish two types of SC, namely: dedicated SC (D-SC) and identity cards (ID-SC);

- SIM (Crypt SIM) indicates the use of SIM as a secure element to store secrets and electronic certificates, which are used during the authentication process. The Crypt SIM embeds additional applets (w.r.t. the ones used by network operators) to provide the functionalities for storing authentication and signature certificates;

- Security Key (SK) indicates the support of login by using a hardware security key (e.g., FIDO security key). The difference between SK in this category and the PWD + HW SK as defined in LoA S lies in the hardware requirements that the SK satisfies. To elaborate, let us consider the certification requirements defined for FIDO SKs in [48]. To be suitable for LoA H, the SK must have a restricted operating environment (e.g., Secure element), while this condition is not necessary for SKs that are recognized for LoA S;

- Software Authenticator (SW Auth): indicates the login support by using software authenticators storing the electronic certificate associated with the user’s digital identity. To elaborate, let us consider the SPID Poste Italiane eID means. In this scenario, a key pair is generated in the citizens’ device (PosteID app) that is protected by a user-selected 8-digit PIN during the setup phase.

- 18 eID means under analysis adopt login with a smart card (identity or dedicated) within their solutions;

- 6 eID means under analysis adopt the login with a software authenticator within their solutions;

- 2 eID means under analysis adopt the login with SK within their solutions.

4. RQ2: Authentication Standards

- SSO Protocols: Single Sign-On (SSO) is an authentication method that lets users access multiple applications and services using a single login credential. The adopted SSO standards based on our analysis are the following:

- SAML (Security Assertion Markup Language 2.0) [49]: is among the most widespread standards used to exchange authentication and authorization assertions (in XML formats). SAML requires that the User (called Principal) is registered with an Identity Provider (IdP), which, after receiving a request message from a Service Provider (SP), will respond with an authentication result (called assertion). An assertion contains information that SP uses to evaluate whether to give or deny the Principal access to a particular resource;

- OIDC (OpenID Connect) [3]: is a most recent authentication standard for user authentication that is designed for the same purpose as SAML. In contrast to SAML, which uses heavyweight XML messages, the OIDC uses the lightweight JSON message format. OIDC is an authentication layer developed on top of the OAuth 2.0 standard. It requires that the User (called Resource Owner in the context of OIDC) is registered with an IdP, which after receiving a request message from a relying party (RP in the context of OIDC) will respond with an authentication result (called ID Token). An ID Token is one of the main features that is added by the OIDC and contains information about the authentication process that enables the RP to evaluate whether to give or deny the resource owner access to a particular resource. In addition to the ID Token, the OIDC adds the userInfo endpoint into the OAuth standard as well, which is a protected OAuth Resource Server that releases identity-related claims to RPs (e.g., the email and address). The terms RP in the OIDC and SP in the SAML refer to the same entity. Hereafter, we use the term SP;

- FIDO (Fast Identity Online) [50]: is a protocol that uses standard public key cryptography techniques to provide stronger authentication. During the registration with an SP, the user’s device creates a new key pair. It retains the private key and registers the public key with the SP. Authentication is completed by the user’s device proving possession of the private key to the SP by signing a challenge. The user’s private keys can be used only after they are unlocked locally on the device. The local unlock is accomplished through a user–friendly and secure action, such as swiping a finger, entering a PIN, inserting a second–factor device, or pressing a button.

- SP-IdP Federated: indicates whether a federation is required through the registration phase of SP at the IdP to obtain SP-specific credentials and IdP metadata, where federation can be expressed as an agreement between parties that trust each other. The SP-IdP federation applies only in the case of SSO protocols.

- Direct Login: indicates whether the eID means under analysis does not use any federation mechanism, meaning that all identification and authentication communication occurs directly between the user and the SP.

- 72% of notified eID means use at least one of the SSO protocols;

- 62% of notified eID means use SAML standard within their solutions;

- German eID means is the only eID means that provides a hybrid solution to support both federated and direct authentication;

- The Swedish OIDC working group, in collaboration with Swedish eID means, is working on the definition of the Swedish OIDC profile. This profile is going to be adopted by the notified Swedish eID means [55];

- None of the notified eID means use Mobile Connect as an authentication standard. Mobile Connect [56] is an authentication mechanism based on OIDC, where the federated telco operators perform the user authentication;

- The eID means of Czech Republic (mojeID) and Sweden (EFOS) are the only available solutions that support FIDO [6].

5. RQ3: OpenID Connect Profiles

- OIDC Core Profile [3]: provides guidelines regarding the core OIDC functionality and how to achieve the baseline security;

- OIDC International Government Assurance (iGov) Profile [30]: is based on the OIDC Core and aims to increase baseline security, provide greater interoperability, and structure deployments for public administration and governmental domains;

- OIDC Financial Grade API (FAPI) Profile [57,58]: is a highly secured OIDC profile that aims to provide specific implementation guidelines for security and interoperability. This profile can be applied to any market area that requires a higher level of security than the one provided by standard OIDC Core;

- OIDC Identity Assurance (IDA) Profile [31]: aims to provide SPs with identity information, i.e., verified claims along with an explicit statement about the verification status of these Claims (what, how, when, according to what rules, using what evidence). It enables use cases requiring strong assurance, like compliance with regulatory requirements such as anti-money laundering laws or access to health data, risk mitigation, or fraud prevention.

- The Italian CIE and SPID eID means define their national OIDC specification based on the OIDC iGov profile, and they will be the only solutions within the eID means under analysis that follow the OIDC iGov;

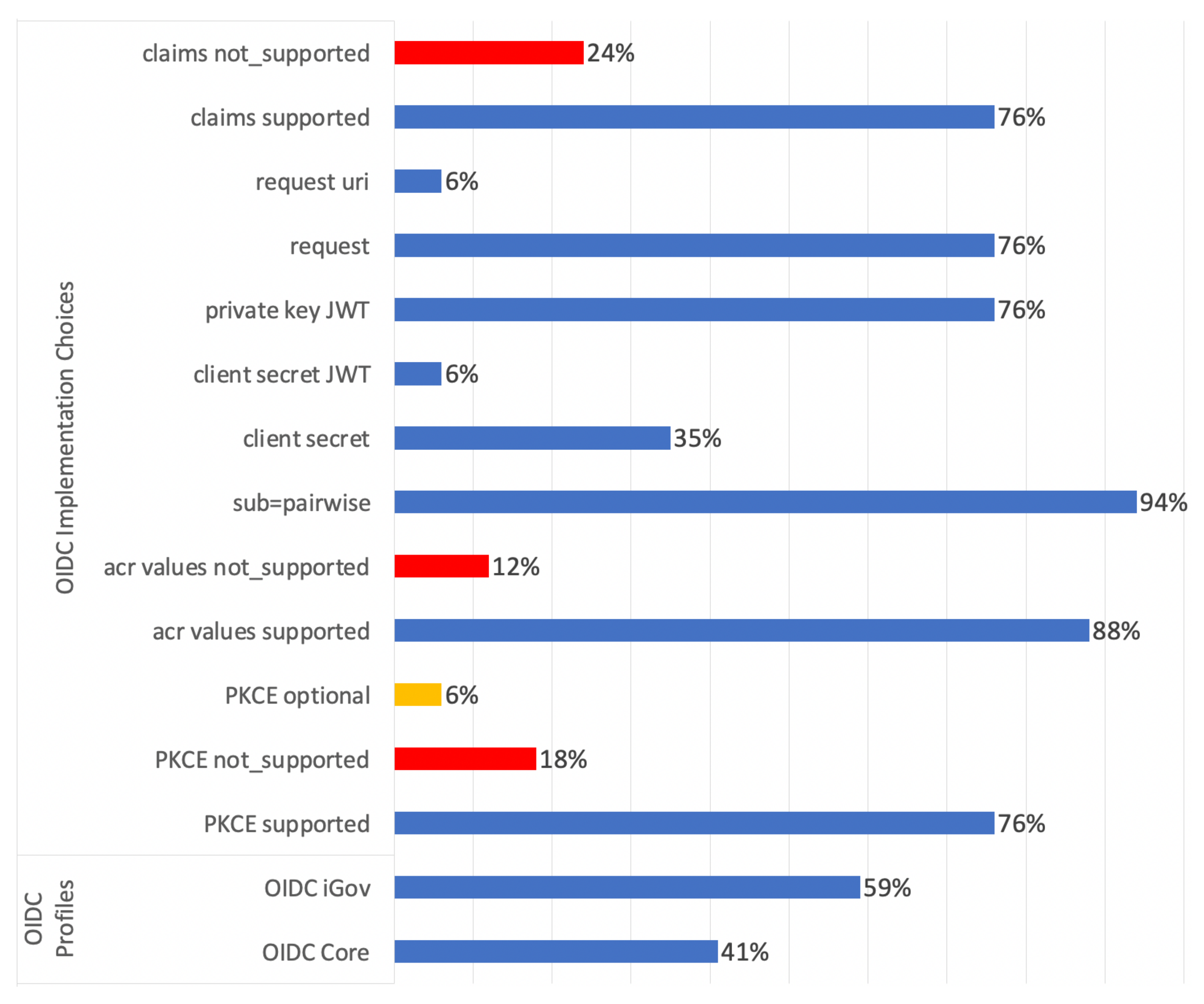

6. RQ4: OpenID Connect Implementation Choices

- Proof Key for Code Exchange (PKCE) [32]: indicates whether the eID means support PKCE. This extension was created to secure the OIDC implementations against several attacks such as code interception in the OIDC authorization code flow [3]. In simple words, code interception attack refers to scenarios in which the attacker can obtain the authorization code somehow and then sends it to an IdP to exchange it for an Access Token. An attacker may use several available ways to steal the code (Section 4 in OAuth Security BCPs [33]). To mitigate this attack, the PKCE extension introduced three query parameters to provide a way for the SP to prove to the IdP that the authorization code belongs to the SP, namely: (i) code_verifier, (ii) code_challenge, and (iii) code_challenge_method. The code_verifier is a dynamically created cryptographically random key, which is unique per request. The code_challenge is a transformation of the code_verifier by using the method that is declared in code_challenge_method (e.g., Plain or S256). Thus, an attacker needs to know the value of the code_verifier for the intercepted request to be able to exchange the authorization code for an Access Token, which is not as simple as code interception;

- acr_values [3]: indicates whether the eID means under analysis support acr_values to define the level of assurance within the authentication context, where acr_values enabling SPs to request IdPs strong authentication methods to harden intrusion attempts against users by mandating additional authentication factors;

- subject identifier (sub) = pairwise [30]: indicates whether the eID means under analysis adopt the pairwise value for the subject identifier, where the subject identifier is an attribute within the IdP for the User. The sub claim is returned from the IdP to SP either directly in the ID Token or as a response from the userInfo endpoint;

- client authentication method [3]: indicates the client authentication method used by the SP at the IdP token endpoint to authenticate the SP and avoid releasing Access/ID Tokens to a not legitimate SP. This feature can have the following values:

- client secret SP uses the client_secret received from the IdP during the registration phase to perform the client authentication;

- client secret JWT SP creates a JSON Web Token (JWT) using an HMAC SHA algorithm, which uses the client_secret issued by the IdP during the registration phase for the HMAC calculation that is used for the client authentication;

- private key JWT SP creates a JWT using asymmetric algorithms and signs the JWT with its private key to perform the client authentication;

- mTLS [59] SP provides a mechanism for authentication to the IdP using mutual TLS based on either self-signed certificates or public key infrastructure (PKI).

- request [3]: indicates whether the eID means under analysis support the request OIDC parameter. It provides a way to encapsulate all the authorization request query parameters inside a single object which can be signed and optionally encrypted to provide integrity;

- request_uri [3]: indicates whether the eID means under analysis support the request_uri OIDC parameter. In the same way as the OIDC request parameter, it provides a way to encapsulate all the authorization request query parameters inside a single object which can be signed and optionally encrypted to provide integrity. However,, in the case of request parameter, the object is directly included within the authorization request, in the case of request_uri, it is retrieved from the defined URL;

- Token Binding (DPoP/mTLS) [59,60]: indicates whether the eID means under analysis are using any techniques for binding the issued Access Tokens, such as: Demonstrating Proof of Possession (DPoP) or mutual TLS (mTLS) to avoid the misuse of a stolen Access Token by other SPs. DPoP is a JWT created by the SP and sent with an HTTP request using the DPoP header field to demonstrate to the IdP that the SP holds the private key that was used to sign the DPoP-proof JWT. DPoP enables IdP to bind issued Access Tokens to the corresponding public key. Furthermore, DPoP enables Resource Servers to verify the key-binding of Access Tokens that it receives, which prevents said tokens from being used by any entity that does not have access to the private key. mTLS is an alternative way to reach the same goal by using the application’s mutual-TLS certificate. Such a binding is accomplished by associating the certificate with the Access Token in a way that the protected resource can access. One possible way of doing this is to embed the certificate hash in the issued Access Token.

- claims [3]: indicates whether the eID means under analysis support the claims OIDC parameter, which enables the SP to explicitly request individual claims to be returned in the ID Token and/or userInfo response to satisfy data minimization. The top-level members of claims OIDC parameter JSON object are:

- userInfo: requests that the listed individual claims be returned from the userInfo endpoint. If present, the listed claims are being requested to be added to any claims that are being requested using the OIDC scope parameter. If not present, the claims being requested from the userInfo endpoint are only those requested using the values defined in the OIDC scope parameter;

- ID Token: requests that the listed individual claims be returned in the ID Token. If present, the listed claims are being requested to be added to the default claims in the ID Token. If not present, the default ID Token claims are requested.

- 76% of eID means support and mandate the usage of the PKCE within their solutions;

- Danish eID means (NemID) is the only solution that optionally supports the PKCE within its solution;

- 88% of the eID means under analysis support the usage of acr_values within their OIDC implementations;

- 94% of the eID means under analysis (for which we could find information) use the pairwise subject identifier;

- private_key_JWT and the client_secret are the two most widely used client authentication methods within eID means;

- None of the eID means support the mTLS client authentication method [59];

- 82% of eID means support either the request or request_uri OIDC parameters;

- 76% of the eID means under analysis (for which we could find information) support the usage of claim parameter within their solutions;

7. RQ5: Mobile-Based Authentication Solutions

- Mobile app protection: indicates whether the mobile application is protected with a security mechanism, such as biometrics (fingerprint, face recognition), and/or PIN;

- Secure storage for mobile apps: in the cases in which the mobile application leverages a cryptographic authenticator, we analyzed the storage location of the user’s private key. In our analysis, after the investigation of notified eID means, we identified the following locations:

- Keystore (Key SW): the private key of the user is stored in the user’s mobile phone within Keystore;

- SIM (crypt SIM): it is used to store secrets and electronic certificates to be used during authentication processes or, in this case, they embed additional applets than the ones used by network operators, for instance, to have a PKI-based SIM that stores authentication and signature certificates;

- Smart card: the NFC reader or Bluetooth connectivity of the mobile phone is used to interact with the smart card, which stores the private key;

- Security key: the user’s private key is stored in the hardware security key (e.g., FIDO security key). During the authentication, the user inserts the security key into the device and provides access to the private key by entering a PIN or using biometrics.

- Mobile browser to app to mobile browser (MB2App2MB): it represents the scenario where the user starts the authentication process within the mobile browser. S/he performs the login on the mobile browser and is redirected to an app for 2nd-factor authentication (e.g., using a national eID card). After the user successfully finishes this step, the app will redirect the user to the mobile browser to complete the authentication process and obtain the token to access the services.

- 4 eID means that provide card reader mobile applications do not have any mobile app protection mechanism;

- Concerning the secure storage solution used by mobile applications:

- –

- Estonian Mobiil-ID and Belgian itsme eID means are the only solutions that use cryptographic SIM to secure the PKI keys;

- –

- 8 eID means use the Mobile NFC or Bluetooth connectivity to read the information from the smart card;

- –

- 8 eID means for which we could find the information use the SW Keystore to secure the private key within their solutions;

- –

- None of the eID means for which we could find information uses either Secure Enclave/Element (SE) or Trusted Execution Environment (TEE) to secure the private key; SE would provide CPU hardware-level isolation and memory encryption by isolating application code and data; similarly, TEE would offer a secure area of the main processor, protecting the confidentiality and integrity of the executed data;

- –

- None of the eID means for which we could find information uses the security key to store the private key within their solutions;

- 10 eID means support the MB2App2MB scenarios.

8. Additional Information

- Denmark announces its new eID mean “MitID” that aims to address the development complexity of “NemID” and unify the two different systems that NemID provides for the public and private sectors. The scheme supports LoAs S and H and provides different authentication mechanisms, such as PWD + SW and PWD + HW. This eID scheme supports both SAML and OIDC authentication standards;

- Poland, Liechtenstein, and Bulgaria eID means—Trusted/personal profile, Li-eID, and Evrotrust eID—completed the peer-reviewed process in the eIDAS framework;

- The Norway eID means (BuypassID, BankID) completed the peer-reviewed process in the eIDAS framework and are in the process of becoming notified eIDAS solution. Both eID means are based on LoA H. Both eID means support the OIDC authentication standard and follow the OIDC Core profile.

9. Lessons Learned

9.1. Security Considerations

- All the eID means, independently of their adopted authentication factors, are not resistant against the (extremely powerful) MB attacker model;

- 12 eID means use PWD, which is the least secure authenticator and exposes these solutions to ES, SE, MB, and SS attacker models. However, it is worth mentioning that all the 12 eID means offer an additional authentication mechanism that provides a higher LoA, which can be used when necessary;

- Concerning the eID means with LoA S, the eID means that are using PWD + QR (1 eID mean) and/or PWD + PN (4 eID means) are more secure in comparison with the eID means that are using other authenticator types for LoA S (reported in Table 2). The main reasons are: (i) the number of successful attackers with higher risk is less than the other methods, and (ii) these methods are not susceptible to the ES attacker model, while this is not the case for the other available authenticator types for LoA S;

- Concerning the eID means with LoA S that are using PWD + SW and/or PWD + HW (13 eID means), the security of their solution can increase according to the features of the OTP generation provided by the SW/HW. In the case that the generation of OTP output is uniquely associated with the ongoing operation—dynamic linking [62]—the solution would be more secure in comparison to the one that does not consider dynamic linking. The main reason for the improvement of the security is related to the fact that: (i) the generated OTP is unique for that specific operation, and (ii) at the time of the operation, the identity of the demandant is displayed to the user and the user has to explicitly agree on the ongoing operation to generate the OTP;

- Concerning the eID means with LoA S that are adopting QR as an authenticator (10 eID means), the mobile app protection mechanism can affect the security level of the solution. Based on the results of our analysis using MuFASA, the usage of the fingerprint can improve the security w.r.t. the usage of PIN.

9.2. Privacy Considerations

9.2.1. General Considerations

- Accountability: in some use cases, the service providers may need additional information to precisely identify users to provide access to their resources. Thus, based on the form of identifier (e.g., pseudonymized identity) that is considered in the eID schemes, there could be greater accountability or privacy;

- Federated or Direct login: Federated solution means a centralized system exists to handle the identification and authentication. While it can simplify the management of authentication for the service providers, it will come with the cost of user tracking across the system if no other measures against that are in place. In the case of direct login, there is not a single entity that can know about a user’s authentication actions. Thus, in this way, it can increase the user’s privacy by preventing an entity from learning about all the user’s activity across different service providers. However, this comes with the cost of handling the authentication and all the relevant overhead that comes with it on service providers. Furthermore, it has the problem of interoperability issues with the other eID schemes. Regarding interoperability, the eIDAS framework implements a proxy to solve the problem, with the cost of creating a federation at the eIDAS level [27].

9.2.2. OIDC-Based Considerations

- Data Minimization: it means asking only for the required claims. Indeed, OIDC Core recommends minimizing the amount of information requested from the user. This is possible by the usage of the OIDC “Claim” parameter that returns the information explicitly declared using this parameter;

- Unlinkability: is to prevent users from being identified across different SPs. In the context of OIDC solutions, the users can be identified by SPs through the usage of subject identifier (sub) in the ID Token. Using the pairwise value for the subject type can help to protect the users against tracking by SPs as it will assign different values to the same user across different SPs. Thus, it can avoid user tracking across SPs.

9.3. Usability

10. eIDAS 2.0 Regulation

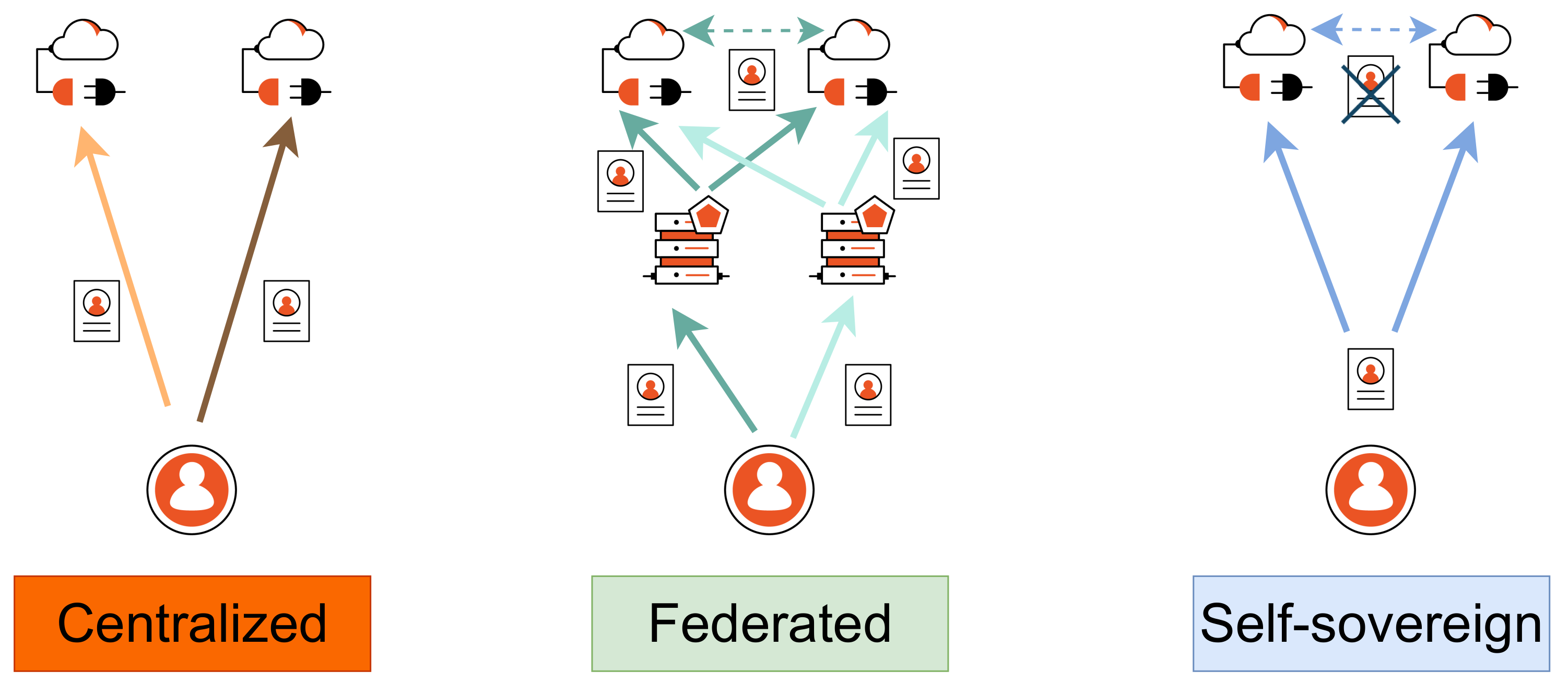

- Centralized identities: Entities such as administrators manage centralized identities at the system level (e.g., active directory). As a result, the user’s identity is determined by these entities and can only be deleted through them. Reliance on a centralized entity frequently leads to a lack of interoperability. The main reason is due to the fact that the user’s identity cannot be transferred without further ado, and it must be recreated for another service provider;

- Federated identities: aims to break down the hierarchies based on a single authority by providing a central-login solution (IdP) to enable the users to share their identities with different SPs using only one registered credential at the IdP. This solution can solve the problem of password fatigue by providing a Single Sign-On experience and interoperability, but, still, the problem of tracking users across multiple SPs remains unsolved. Indeed, it is possible for the IdP to aggregate information from numerous SPs to generate user profiles, which might cause several privacy issues [68];

- Self-sovereign identities: is the next and most recent stage of digital identity management that aims to solve the privacy issues in the previous models by giving the users back control of their own data. The main idea is to shift the control from the centers of the network to the edge of the network to enable direct interaction [69].

- Provide a highly secure and trustworthy electronic identity solution that enables the user to share only the minimum set of identity data needed by the SP to provide the service requested by the user;

- Introduce a so-called “European Digital Identity Wallet (EUDIW),” which may be provided by public authorities or by private entities recognized by MSs and link a citizen’s national digital identity to other personal attributes (e.g., driving license or bank account);

- Enhance privacy by decoupling credential issuance from its presentation to SPs; This can blind the IdP from the SP the user interacts with and vice versa.

- Persistent and unique identifier: Article 11a of eIDAS 2.0 regulation states that the minimum data set of user identification data shall contain a unique and persistent identifier for all European citizens and residents. This parameter should design carefully as it can create additional privacy risks and allows online services to track the user’s activity. A more privacy-friendly approach would be adopting a service-specific pairwise identifier model or pseudonymization;

- Standards and technology immaturity: To support the implementation of different functionality requirements of EUDIW, new standards and technologies are needed. There are different working groups, such as Decentralize Identity Foundation (DIF) (https://identity.foundation, accessed on 1 November 2022), OpenID Foundation (OIDF) (https://openid.net, accessed on 1 November 2022), World Wide Web Consortium (W3C) (https://www.w3.org/Consortium/, accessed on 1 November 2022), and ISO 18013-5 [72] to name a few of them, which are working on this dimension to provide the basic building blocks to build the EUDIW on top of it. However, most of these standards are in their early stages;

- Interoperability: It is worth mentioning that the current eID schemes that are operating within the MSs will continue to operate for quite some time after the final release of EUDIW. This can lead to potential challenges for SPs that are supporting several eIDs, including the EUDIW, for their services. A possible solution to this issue would be using an identity gateway (a.k.a broker) between the EUDIW and/or governmental eID means and the SPs. However, it is important to design the identity gateway based on privacy-by-design principles to prevent the identity gateway from profiling the user’s online activity. A potential solution can be the adoption of a blind broker architecture model [73].

11. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. eIDAS Identified Requirements per Assurance Level

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Assurance Level | Elements Needed |

|---|---|

| Low | The authentication mechanism should implement security mechanisms for the verification of eID means in a way that the authentication mechanism is resistant against guessing, eavesdropping, replay, or manipulation of communication by an attacker with enhanced-basic attack potential. |

| Substantial | The authentication mechanism should implement security mechanisms for the verification of eID means in a way that the authentication mechanism is resistant against guessing, eavesdropping, replay, or manipulation of communication by an attacker with moderate attack potential. |

| High | The authentication mechanism should implement security mechanisms for the verification of eID means in a way that the authentication mechanism is resistant against guessing, eavesdropping, replay, or manipulation of communication by an attacker with High attack potential. |

References

- European Union. Regulation (EU) No 910/2014 of the European Parliament and of the Council of 23 July 2014 on Electronic Identification and Trust Services for Electronic Transactions in the Internal Market and Repealing Directive 1999/93/EC. Off. J. Eur. Union L 2014. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2014.257.01.0073.01.ENG (accessed on 1 November 2021).

- European Union. Council regulation (EU) no 1502/2015 on setting out minimum technical specifications and procedures for assurance levels for electronic identification means pursuant to article 8(3) of regulation (eu) no 910/2014 of the european parliament and of the council on electronic identification and trust services for electronic transactions in the internal market. Off. J. Eur. Union L 2015. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=OJ:JOL_2015_235_R_0002 (accessed on 1 November 2021).

- Sakimura, N.; Bradley, J.; Jones, M.; De Medeiros, B.; Mortimore, C. OpenID Connect Core 1.0 Incorporating Errata Set 1. Specification; The OpenID Foundation: New York, NY, USA, 2014; Volume 335. [Google Scholar]

- Sharif, A.; Ranzi, M.; Carbone, R.; Sciarretta, G.; Ranise, S. SoK: A Survey on Technological Trends for (pre) Notified eIDAS Electronic Identity Schemes. In Proceedings of the 17th International Conference on Availability, Reliability and Security, Vienna, Austria, 23 August–26 August 2022; pp. 1–10. [Google Scholar]

- European Union. Regulation of the European Parliament and of The Council Amending Regulation (Eu) No 910/2014 as Regards Establishing a Framework for a European Digital Identity. Off. J. Eur. Union L 2021. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52021PC0281 (accessed on 1 November 2021).

- European Commission. Overview of Pre-Notified and Notified eID Schemes under eIDAS. 2022. Available online: https://ec.europa.eu/cefdigital/wiki/display/EIDCOMMUNITY/Overview+of+pre-notified+and+notified+eID+schemes+under+eIDAS (accessed on 1 September 2022).

- European Union. Council regulation (EU) no 1501/2015 on the interoperability framework pursuant to article 12(8) of regulation (eu) no 910/2014 of the european parliament and of the council on electronic identification and trust services for electronic transactions in the internal market. Off. J. Eur. Union L 2015. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32015R1501 (accessed on 1 November 2021).

- Grassi, P.A.; Garcia, M.E.; Fenton, J.L. Digital Identity Guidelines. NIST Spec. Publ. 2017, 800, 63. [Google Scholar]

- BelgianeID. Belgium eID Card. 2022. Available online: https://www.ibz.rrn.fgov.be/fr/documents-didentite/eid/ (accessed on 1 November 2021).

- BelgianMobileID. Itsme Developer Documentation-Authentication Service Documentation. 2022. Available online: https://belgianmobileid.github.io/slate/login.html (accessed on 1 November 2021).

- CzechGovernment. Czech Republic eCitizen. 2019. Available online: https://info.identitaobcana.cz/eop/ (accessed on 1 November 2021).

- CZNIC. MojeID Solution. 2022. Available online: https://www.mojeid.cz/en/egovernment/ (accessed on 1 September 2022).

- NemID. NemID eID Solution. 2019. Available online: https://www.nemid.nu/dk-en/get_started/index.html (accessed on 1 November 2021).

- BSI. German eID-Overview of the German eID System. 2017. Available online: https://www.bsi.bund.de/SharedDocs/Downloads/EN/BSI/EIDAS/German_eID_Whitepaper.pdf?__blob=publicationFile&v=1 (accessed on 1 November 2021).

- LithuanianGov. Lithuania Identity Card and Electronic Signature. 2019. Available online: https://www.nsc.vrm.lt/ (accessed on 1 November 2021).

- AMA. Authentication.gov-Authentication Provider of the Portuguese Public Administrator. 2021. Available online: https://www.autenticacao.gov.pt/documentos (accessed on 1 November 2021).

- SlovacianGovernment. Slovakia eID Card. 2019. Available online: https://www.slovensko.sk/sk/eid/_eid-karta/ (accessed on 1 November 2021).

- eHerkening. Eherkenning Overview. 2019. Available online: https://www.eherkenning.nl/leveranciersoverzicht (accessed on 1 November 2021).

- Whitley, E.A. Trusted Digital Identity Provision: GOV. UK Verify’s Federated Approach; Minister of UK: London, UK, 2018. [Google Scholar]

- FranceConnect. Franceconnect Documentation. 2021. Available online: https://api.gouv.fr/les-api/franceconnect (accessed on 1 November 2021).

- A-SIT. Austria ID Solution. 2021. Available online: https://www.a-sit.at/ (accessed on 1 September 2022).

- BankID. BankID Solution. 2022. Available online: https://www.bankid.com/en/utvecklare/guider/teknisk-integrationsguide/rp-introduktion (accessed on 1 September 2022).

- FrejaID. FrejaID Solution. 2022. Available online: https://frejaeid.com/en/home/ (accessed on 1 November 2022).

- EFOSID. EFOSID Solution. 2022. Available online: https://www.forsakringskassan.se/myndigheter-och-samarbetspartner/e-tjanster-for-myndigheter-och-samarbetspartner/e-identitet-for-offentlig-sektor-efos/allman-information-om-efos (accessed on 1 September 2022).

- SmartID. Smart ID Solution. 2021. Available online: https://www.smart-id.com/about-smart-id/ (accessed on 1 November 2021).

- ENISA. eIDAS Compliant eID Solutions: Security Considerations and the Role of ENISA. 2020. Available online: https://www.enisa.europa.eu/publications/eidas-compliant-eid-solutions/view/++widget++form.widgets.fullReport/@@download/ENISA+Report+-+eIDAS+Compliant+eID+Solution.pdf (accessed on 1 November 2021).

- Roelofs, F.; Verheul, E.; Jacobs, B. Analysis and Comparison of Identification and Authentication Systems under the eIDAS Regulation; European Commission: Brussels, Belgium, 2019. [Google Scholar]

- FutureTrust. Overview of eID Services. 2017. Available online: https://ec.europa.eu/research/participants/documents/downloadPublic?documentIds=080166e5b52e19d7&appId=PPGMS (accessed on 1 November 2021).

- Commission, E. Overview of Member States’ eID strategies v3.0. 2021. Available online: https://ec.europa.eu/digital-building-blocks/wikis/download/attachments/364643428/eID_Strategies_v4.0.pdf (accessed on 1 November 2021).

- Internet-Draft. International Government Assurance Profile (iGov) for OpenID Connect 1.0; Minister of UK: London, UK, 2018. [Google Scholar]

- Lodderstedt, T.; Fett, D. OpenID Connect for Identity Assurance 1.0; The OpenID Foundation, Specification: New York, NY, USA, 2022. [Google Scholar]

- Sakimura, N.; Bradley, J.; Agarwal, N. Proof Key for Code Exchange by OAuth Public Clients (RFC7636). Internet Eng. Task Force (IETF) 2015. Available online: https://www.rfc-editor.org/rfc/rfc7636 (accessed on 1 November 2021).

- Lodderstedt, T.; Bradley, J.; Labunets, A.; Fett, D. OAuth 2.0 Security Best Current Practice (draft-ietf-oauth-security-topics-21). Internet Eng. Task Force (IETF) 2022. Available online: https://www.ietf.org/archive/id/draft-ietf-oauth-security-topics-21.html (accessed on 1 September 2022).

- CzechGovernment. eGovernment Mobile Key. 2022. Available online: https://info.identitaobcana.cz/mep/, (accessed on 1 September 2022).

- EstonianGovernment. Estonian Digital ID (Digi-ID). 2018. Available online: https://www.politsei.ee/en/instructions/digital-id (accessed on 1 November 2021).

- EstonianGovernment. Mobiil-ID. 2018. Available online: https://www.politsei.ee/en/instructions/mobile-id (accessed on 1 November 2021).

- CroatianGovernment. Croatian Electronic Identity Card. 2018. Available online: https://www.eid.hr (accessed on 1 November 2021).

- LatvianGovernment. Latvian Electronic Identity Card. 2019. Available online: https://www.pmlp.gov.lv/lv/jaunums/eid-karte-erts-un-dross-personu-apliecinoss-dokuments (accessed on 1 November 2021).

- LVRTC. eParaksts. 2019. Available online: https://www.eparaksts.lv/en/ (accessed on 1 November 2021).

- LuxGov. The Luxembourg Electronic Identity Card. 2019. Available online: https://ctie.gouvernement.lu/en/dossiers/eID/eID.html (accessed on 1 November 2021).

- AMA. Chave Móvel Digital. 2021. Available online: https://www.ama.gov.pt/web/english/digital-mobile-key (accessed on 1 November 2021).

- ItalianGovernment. Italian eID Card. 2019. Available online: https://www.cartaidentita.interno.gov.it/en/citizens/cie-id/ (accessed on 1 November 2021).

- AGID. Public Digital Identity System (SPID). 2018. Available online: https://www.spid.gov.it (accessed on 1 November 2021).

- DutchGovernment. DigiD eID Scheme. 2020. Available online: https://www.digid.nl/en/ (accessed on 1 November 2021).

- DigIdentity. Digidentity 2018. Available online: https://www.digidentity.eu/en/govuk-verify/#how-it-works (accessed on 1 November 2021).

- MaltaGovernment. Maltese eID Card and E-Residence Documents. 2021. Available online: https://www.identitymalta.com/unit/e-id-cards-unit/ (accessed on 1 November 2021).

- ISO/IEC. Information Technology—Security Techniques—Entity Authentication Assurance Framework. 2013. Available online: https://www.iso.org/standard/45138.html (accessed on 1 November 2021).

- FIDO. Certified Authenticator Levels. 2021. Available online: https://fidoalliance.org/certification/authenticator-certification-levels/ (accessed on 1 November 2021).

- Cantor, S. SAML Version 2.0 Errata 05. Retriev. March 2012, 18, 2015. [Google Scholar]

- Alliance, F. Specifications Overview 2016. Available online: https://fidoalliance.org/specifications/overview (accessed on 1 November 2021).

- Chen, E.Y.; Pei, Y.; Chen, S.; Tian, Y.; Kotcher, R.; Tague, P. Oauth demystified for mobile application developers. In Proceedings of the 2014 ACM SIGSAC Conference on Computer and Communications Security, Scottsdale, AZ, USA, 3–7 November 2014; pp. 892–903. [Google Scholar]

- Sharif, A.; Carbone, R.; Sciarretta, G.; Ranise, S. Best current practices for OAuth/OIDC Native Apps: A study of their adoption in popular providers and top-ranked Android clients. J. Inf. Secur. Appl. 2022, 65, 103097. [Google Scholar]

- Sharif, A.; Carbone, R.; Ranise, S.; Sciarretta, G. A wizard-based approach for secure code generation of single sign-on and access delegation solutions for mobile native apps. In Proceedings of the 16th International Joint Conference on e-Business and Telecommunications-SECRYPT, Prague, Czech Republic, 26–28 July 2019; Volume 2, pp. 268–275. [Google Scholar]

- Yasuda, K.; Jones, M. Self-Issued OpenID Provider v2. 2022. Available online: https://openid.net/specs/openid-connect-self-issued-v2-1_0.html (accessed on 1 September 2022).

- OIDCSweden. Sweden OIDC Working Group. 2021. Available online: https://github.com/oidc-sweden/specifications (accessed on 1 September 2022).

- GSMA. Mobile Connect Universal Log-in Profile. 2021. Available online: https://mobileconnect.io/specifications/ (accessed on 1 November 2021).

- Sakimura, N.; Bradley, J.; Jay, E. Financial-grade API—Part 1: Baseline. Internet Eng. Task Force (IETF) 2021. Available online: https://openid.net/specs/openid-financial-api-part-1-1_0.html (accessed on 1 November 2021).

- Sakimura, N.; Bradley, J.; Jay, E. Financial-grade API—Part 2: Advanced. Internet Eng. Task Force (IETF) 2021. Available online: https://openid.net/specs/openid-financial-api-part-2-1_0.html (accessed on 1 November 2021).

- Campbell, B.; Bradley, J.; Sakimura, N.; Lodderstedt, T. OAuth 2.0 Mutual TLS Client Authentication and Certificate Bound Access Tokens (RFC8705). Internet Eng. Task Force (IETF) 2020. Available online: https://www.rfc-editor.org/rfc/rfc8705 (accessed on 1 November 2021).

- Fett, D.; Campbell, B.; Lodderstedt, T.; Jones, M.; Waite, D. OAuth 2.0 Demonstrating Proof-of-Possession at the Application Layer (DPoP) (draft-11). Internet Eng. Task Force (IETF) 2022. Available online: https://www.ietf.org/archive/id/draft-ietf-oauth-dpop-11.html (accessed on 1 September 2022).

- Sinigaglia, F.; Carbone, R.; Costa, G.; Ranise, S. Mufasa: A tool for high-level specification and analysis of multi-factor authentication protocols. In Proceedings of the International Workshop on Emerging Technologies for Authorization and Authentication, Luxembourg, 27 September 2019; Springer: Berlin, Germany, 2019; pp. 138–155. [Google Scholar]

- European Commission. European Banking Authority: Directive 2015/2366 of the European Parliament and of the Council on Payment Services in the Internal Market (PSD2). 2015. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32015L2366&qid=1653045761540&from=EN (accessed on 1 November 2021).

- Yong, K.S.; Chiew, K.L.; Tan, C.L. A survey of the QR code phishing: The current attacks and countermeasures. In Proceedings of the IEEE 2019 7th International Conference on Smart Computing & Communications (ICSCC), Sarawak, Malaysia, 28–30 June 2019; IEEE: Piscataway, NJ, USA, 2019; pp. 1–5. [Google Scholar]

- OWASP. QRLJacking—A New Social Engineering Attack Vector. 2020. Available online: https://github.com/OWASP/QRLJacking (accessed on 1 November 2021).

- Fox-Brewster, T. Watch as hackers hijack whatsapp accounts via critical telecoms flaws. Forbes, 1 June 2016. [Google Scholar]

- Lee, K.; Kaiser, B.; Mayer, J.; Narayanan, A. An Empirical Study of Wireless Carrier Authentication for SIM Swaps. In Proceedings of the Sixteenth Symposium on Usable Privacy and Security (SOUPS 2020), Boston, MA, USA, 10–11 August 2020; pp. 61–79. [Google Scholar]

- Security Standards Council. Information Supplement-Multi-Factor Authentication. 2017. Available online: https://www.pcisecuritystandards.org/pdfs/Multi-Factor-Authentication-Guidance-v1.pdf (accessed on 1 November 2021).

- Ehrlich, T.; Richter, D.; Meisel, M.; Anke, J. Self-sovereign Identity als Grundlage für universell einsetzbare digitale Identitäten. HMD Prax. Wirtsch. 2021, 58, 247–270. [Google Scholar] [CrossRef]

- Kubach, M.; Schunck, C.H.; Sellung, R.; Roßnagel, H. Self-sovereign and Decentralized identity as the future of identity management. In Open Identity Summit 2020; Springer: Berlin, Germany, 2020. [Google Scholar]

- European Commission. European Digital Identity Architecture and Reference Framework—Outline. 2022. Available online: https://digital-strategy.ec.europa.eu/en/library/european-digital-identity-architecture-and-reference-framework-outline (accessed on 1 September 2022).

- Zeit. Digitale Führerschein-App Defekt. 2021. Available online: https://www.zeit.de/mobilitaet/2021-09/verkehrsministerium-digitaler-fuehrerschein-app-defekt-andreas-scheuer (accessed on 1 November 2021).

- ISO. Personal Identification—ISO-Compliant Driving Licence—Part 5: Mobile Driving Licence (mDL) Application. 2021. Available online: https://www.iso.org/standard/69084.html (accessed on 1 September 2022).

- Boysen, A. Decentralized, self-sovereign, consortium: The future of digital identity in Canada. J. Frotiers Blockchain 2021, 4, 624258. [Google Scholar] [CrossRef]

- Sporny, M.; Longley, D.; Chadwick, D.; Terbu, O.; Zagidulin, D.; Zundel, B. Verifiable Credentials Implementation Guidelines 1.0. 2022. Available online: https://w3c.github.io/vc-imp-guide/ (accessed on 1 September 2021).

| MS | Ref | eID Scheme | ID | eID Means |

|---|---|---|---|---|

| BE | [9] | Belgian eID Scheme FAS/eCards | 1 | Belgian Citizen or Foreigner eCard |

| [10] | Belgian eID Scheme FAS/itsme | 2 | itsme Mobile app | |

| CZ | [11] | National identification scheme of the Czech Republic/eID Card | 3 | CZ eID Card |

| [12] | National identification scheme of the Czech Republic/MojeID | 4 | MojeID | |

| [34] | National identification scheme of the Czech Republic/MEG | 5 | MEG | |

| DK | [13] | NemID | 6 | NemID |

| DE | [14] | German eID based on Extended Access Control | 7 | ID/RP/EEA Card |

| EE | [6,29] | Estonian eID Scheme/eCards | 8 | ID/RP/Diplomatic/e-residencyCard |

| [35] | Estonian eID Scheme/Digi-ID | 9 | Digi-ID | |

| [36] | Estonian eID Scheme/Mobiil-ID | 10 | Mobiil-ID | |

| ES | [6,27,29] | Documento Nacional de Identidad electrónico (DNIe) | 11 | Spanish ID card (DNIe) |

| HR | [29,37] | National Identification and Authentication System (NIAS) | 12 | Personal Identity Card |

| LV | [26,38] | Latvian eID Scheme/eCards | 13 | eID/eparaksts card, eparaksts + card |

| [26,39] | Latvian eID Scheme/eParaksts | 14 | eParaksts | |

| LT | [15] | Lithuanian National identity card | 15 | Lithuanian National Identity card |

| LU | [40] | Luxembourg national identity card | 16 | Luxembourg national identity card |

| PT | [16] | Cartão de Cidadão | 17 | Portuguese national identity card |

| [41] | Chave Móvel Digital | 18 | Digital Mobile Key | |

| SK | [17] | National identity scheme of the Slovak Republic | 19 | Slovak Citizen eCard, Foreigner eCard |

| IT | [42] | Italian eID based on National ID card (CIE) | 20 | Italian eID Card |

| 21 | Aruba PEC SpA | |||

| 22 | Namirial SpA | |||

| 23 | InfoCert SpA | |||

| 24 | In.TE.S.A. SpA | |||

| [43] | SPID | 25 | Poste Italiane SpA | |

| 26 | Register.it SpA | |||

| 27 | Sielte SpA | |||

| 28 | Telecom Italia Trust Technologies S.r.l. | |||

| 29 | Lepida SpA | |||

| NR | [18] | Trust Framework for Digital Identity | 30 | eHerkenning |

| [44] | DigiD | 31 | DigiD | |

| UK | [19] | Gov.UK Verify/Post Office | 32 | Post Office |

| [45] | Gov.UK Verify/Digidentity | 33 | Digidentity | |

| FR | [20] | Franceconnect | 34 | Franceconnect |

| [20] | Franceconnect | 35 | Franceconnect+ | |

| AT | [21] | Austria ID | 36 | Austria ID |

| SE | [22] | Swedish eID/BankID | 37 | BankID |

| [23] | Swedish eID/Freja eID | 38 | Freja eID | |

| [24] | Swedish eID/EFOS | 39 | EFOS | |

| MT | [46] | Identity Malta | 40 | ID/e-residency Card |

| EE, LV, LT | [25] | SMART-ID | 41 | SMART-ID |

| MS | ID | LoA L | LoA S | LoA H | Authn Standard | Mobile Apps | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Authentication Mechanisms | Crypto Auth | SSO | Fed. | Prot. | Storage | |||||||||||||||||||||

| PWD | PWD + SMS | PWD + SW | PWD + MAT | PWD + HW | PWD + QR | PWD + PN | PWD + SK | QR | HW Auth | SW Auth | SAML | OIDC | FIDO | SP-IdP | Direct Login | Bio | PIN | Keystore | SIM | Smart Card | MB2App2MB | |||||

| ID-SC dd | D-SC | SIM | SK | |||||||||||||||||||||||

| BE | 1 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | Y | - | Y | - | - | - | - | - | - | - |

| 2 | - | - | - | - | - | - | - | - | - | - | - | Y | - | - | Y | Y | - | Y | - | Y | Y | - | Y | - | Y | |

| CZ | 3 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | - | - | - | Y | - | - | - | - | Y | - |

| 4 | Y | - | - | - | - | - | Y | Y | - | - | - | - | Y | - | Y | Y | Y | Y | - | - | - | - | - | - | - | |

| 5 | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | ? | ? | ? | ? | ? | Y | Y | ? | ? | - | - | |

| DK | 6 | - | - | Y | Y | Y | - | - | - | - | - | - | - | - | - | Y | Y | - | Y | - | Y | Y | - | - | - | - |

| DE | 7 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | Y | - | - | Y | Y | - | - | - | - | Y | - |

| 8 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | - | - | - | Y | - | - | - | - | Y | - | |

| EE | 9 | - | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | - | - | Y | - | - | - | - | Y | - |

| 10 | - | - | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | Y | - | ? | Y | - | Y | - | - | |

| ES | 11 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | - | - | - | Y | - | - | - | - | Y | - |

| HR | 12 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | Y | - | - | Y | - | - | - | - | - | - | - |

| LV | 13 | - | - | - | - | - | - | - | - | - | Y | Y | - | - | - | - | Y | - | Y | - | - | - | - | - | - | - |

| 14 | - | - | - | - | - | - | - | - | - | - | - | - | - | Y | - | Y | - | Y | - | Y | Y | Y | - | - | Y | |

| LT | 15 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | - |

| LU | 16 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | Y | - | - | Y | - | - | - | - | - | - | - |

| PT | 17 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | Y | - | - | Y | - | - | - | - | - | - | - |

| 18 | - | - | - | - | - | - | - | - | - | - | - | - | - | Y | Y | - | - | Y | - | - | Y | Y | - | - | Y | |

| SK | 19 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | Y | - | - | Y | - | - | - | - | - | - | - |

| IT | 20 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | Y | Y | - | Y | - | Y | - | - | - | Y | Y |

| 21 | Y | Y | Y | - | Y | - | - | - | - | Y | - | - | - | - | Y | Y | - | Y | - | Y | Y | - | - | Y | Y | |

| 22 | Y | Y | Y | - | Y | - | - | - | - | - | - | - | - | - | Y | Y | - | Y | - | - | Y | - | - | - | ? | |

| 23 | Y | Y | Y | - | - | Y | Y | - | Y | ? | ? | ? | - | ? | Y | Y | - | Y | - | Y | Y | ? | ? | ? | Y | |

| 24 | Y | Y | - | - | - | - | - | - | - | - | - | - | - | - | Y | Y | - | Y | - | - | - | - | - | - | - | |

| 25 | Y | Y | Y | - | - | - | Y | - | Y | - | - | - | - | Y | Y | Y | - | Y | - | Y | Y | Y | ? | - | Y | |

| 26 | Y | Y | - | - | - | - | - | - | - | - | - | - | - | - | Y | Y | - | Y | - | - | - | - | - | - | - | |

| 27 | Y | Y | Y | - | - | - | Y | - | - | ? | ? | ? | - | ? | Y | Y | - | Y | - | - | Y | ? | ? | ? | Y | |

| 28 | Y | Y | - | - | - | - | - | - | - | - | - | - | - | - | Y | Y | - | Y | - | - | - | - | - | - | - | |

| 29 | Y | Y | Y | - | - | - | - | - | Y | - | - | - | - | - | Y | Y | - | Y | - | - | Y | - | - | - | - | |

| NR | 30 | Y | Y | - | - | Y | - | - | - | Y | ? | ? | - | - | - | Y | - | - | Y | - | ? | ? | - | - | ? | - |

| 31 | - | Y | Y | - | - | - | - | - | Y | Y | - | - | - | - | Y | - | - | Y | - | - | Y | - | - | Y | - | |

| UK | 32 | - | Y | Y | - | - | - | - | - | Y | - | - | - | - | - | Y | - | - | Y | - | - | Y | - | - | - | - |

| 33 | - | Y | - | - | - | - | - | - | Y | - | - | - | - | Y | Y | - | - | Y | - | - | Y | Y | - | - | Y | |

| FR | 34 | Y | ? | - | ? | ? | - | - | - | - | - | - | - | - | - | - | Y | - | Y | - | ? | ? | - | - | ? | - |

| 35 | - | ? | - | ? | ? | - | - | - | - | - | - | - | - | - | - | Y | - | Y | - | ? | ? | - | - | ? | - | |

| AT | 36 | - | - | - | - | - | - | - | - | - | - | - | - | - | Y | Y | Y | - | Y | - | Y | Y | Y | - | - | Y |

| SE | 37 | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | - | - | - | - | Y | Y | Y | Y | - | - | ? |

| 38 | - | - | - | - | - | - | - | - | Y | - | - | - | - | - | - | - | - | - | Y | Y | Y | Y | - | - | ? | |

| 39 | - | - | - | - | - | - | - | - | - | Y | - | - | Y | - | - | - | Y | - | Y | - | - | - | - | - | - | |

| MT | 40 | - | - | - | - | - | - | - | - | - | Y | - | - | - | - | Y | - | - | Y | - | - | - | - | - | - | - |

| Baltic | 41 | - | - | - | - | - | - | - | - | - | - | - | - | - | Y | - | Y | - | Y | - | ? | Y | Y | - | - | - |

| Total | 12 | 13 | 9 | 1 | 4 | 1 | 4 | 1 | 10 | 16 | 2 | 2 | 2 | 6 | 25 | 20 | 2 | 32 | 9 | 11 | 19 | 8 | 2 | 8 | 10 | |

| MS | ID | OIDC | OIDC Implementation Choices | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Profiles | Client Authn Method | |||||||||||

| OIDC Core | OIDC iGov | PKCE | ACR Values | Sub=Pairwise | Client Secret | Client Secret JWT | Private Key JWT | Request | Request Uri | Claims | ||

| BE | 2 | Y | - | Y | Y | Y | - | - | Y | Y | - | - |

| CZ | 4 | Y | - | - | - | Y | Y | Y | Y | Y | - | Y |

| DK | 6 | Y | - | Y * | Y | Y | Y | - | - | Y | - | - |

| IT | 20 | - | Y | Y | Y | Y | - | - | Y | Y | - | Y |

| 21 | - | Y | Y | Y | Y | - | - | Y | Y | - | Y | |

| 22 | - | Y | Y | Y | Y | - | - | Y | Y | - | Y | |

| 23 | - | Y | Y | Y | Y | - | - | Y | Y | - | Y | |

| 24 | - | Y | Y | Y | Y | - | - | Y | Y | - | Y | |

| 25 | - | Y | Y | Y | Y | - | - | Y | Y | - | Y | |

| 26 | - | Y | Y | Y | Y | - | - | Y | Y | - | Y | |

| 27 | - | Y | Y | Y | Y | - | - | Y | Y | - | Y | |

| 28 | - | Y | Y | Y | Y | - | - | Y | Y | - | Y | |

| 29 | - | Y | Y | Y | Y | - | - | Y | Y | - | Y | |

| FR | 34 | Y | - | - | Y | Y | Y | - | - | - | - | - |

| 35 | Y | - | Y | Y | Y | Y | - | Y | - | Y | Y | |

| AT | 36 | Y | - | Y | - | Y | Y | - | - | - | - | Y |

| Baltic | 41 | Y | - | - | Y | ? | Y | - | - | ? | ? | ? |

| Total | 7 | 10 | 13 | 15 | 16 | 6 | 1 | 13 | 13 | 1 | 13 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sharif, A.; Ranzi, M.; Carbone, R.; Sciarretta, G.; Marino, F.A.; Ranise, S. The eIDAS Regulation: A Survey of Technological Trends for European Electronic Identity Schemes. Appl. Sci. 2022, 12, 12679. https://0-doi-org.brum.beds.ac.uk/10.3390/app122412679

Sharif A, Ranzi M, Carbone R, Sciarretta G, Marino FA, Ranise S. The eIDAS Regulation: A Survey of Technological Trends for European Electronic Identity Schemes. Applied Sciences. 2022; 12(24):12679. https://0-doi-org.brum.beds.ac.uk/10.3390/app122412679

Chicago/Turabian StyleSharif, Amir, Matteo Ranzi, Roberto Carbone, Giada Sciarretta, Francesco Antonio Marino, and Silvio Ranise. 2022. "The eIDAS Regulation: A Survey of Technological Trends for European Electronic Identity Schemes" Applied Sciences 12, no. 24: 12679. https://0-doi-org.brum.beds.ac.uk/10.3390/app122412679