1. Introduction

The COVID-19 pandemic started as an epidemic, with China being the first country reporting the disease. It was only 100 days until the declaration of the pandemic. After that, governments in every country implemented different measures to control the crisis, with a common structure: social distancing, lockdowns, stay-at-home orders, and travel restrictions, all of which had economic impacts. The whole world experienced a period in which the economy was not running efficiently, causing some businesses to collapse.

The recovery after the emergence of the pandemic evolved differently depending on the country and the sanitary situation, causing a global disruption in the commerce interchange and affecting the full value-added chain.

Commodities market prices reached their lowest level in decades, such as, for example, the crude oil and natural gas markets [

1]. Other commodities traded in futures exchanges, such as soft commodities and metals, also reacted sharply to this global crisis, with a vast shift in prices [

2], and the historical refuges of these stock markets also being affected [

3]. Copper, in particular, underwent a price decrease of almost 25%, from EUR 6200 at the beginning of 2020 to EUR 4627 per metric ton only 3 months after, with a lack of interest in the buying market and with most of the players trying to liquidate their long-held positions in official warehouses.

This COVID-19 pandemic has had by far the biggest influence on every market in recent times when base metals prices on commodities exchanges have been influenced by macroeconomic and microeconomic events. Each of these base metals shows different behaviors depending on its supply–demand situation, and how financialized each is.

Microeconomic and macroeconomic events have influenced commodities’ behaviors in different exchanges. Some of these macroeconomics variables, such as Gross Domestic Product (GDP), have been used to determine the effects on the 27 commodity futures traded on the Commodity Research Bureau (CRB) [

4], and the effect on the S&P 500 index has been tested using commodity price indexes [

5]. It is also informative to study currency volatility and the link between currency rates for 17 soft and hard commodities [

6]. Crude oil prices have also been analyzed by some authors, who found a vast range of variables affecting prices, such as the COVID-19 outbreak, the USD index, and Pacific Investment Management Company (PIMCO) Investment Grade Corporate bond index [

7], and US and BRICS (Brazil, Russia, India, China and South Africa) equities [

8]. Globally, it has been demonstrated that price cycles are affected by macroeconomic variables [

9].

The increase in financialization on the commodity market has been observable for a while [

10,

11], with commodities in general and base metals in particular being a refuge for investors trying to hedge their global exposure. In this regard, 2004 was pinpointed by some authors [

12] as the year in which financialization became more present, ultimately achieving inflows of up to USD 450 billion seven years later in 2011 [

13].

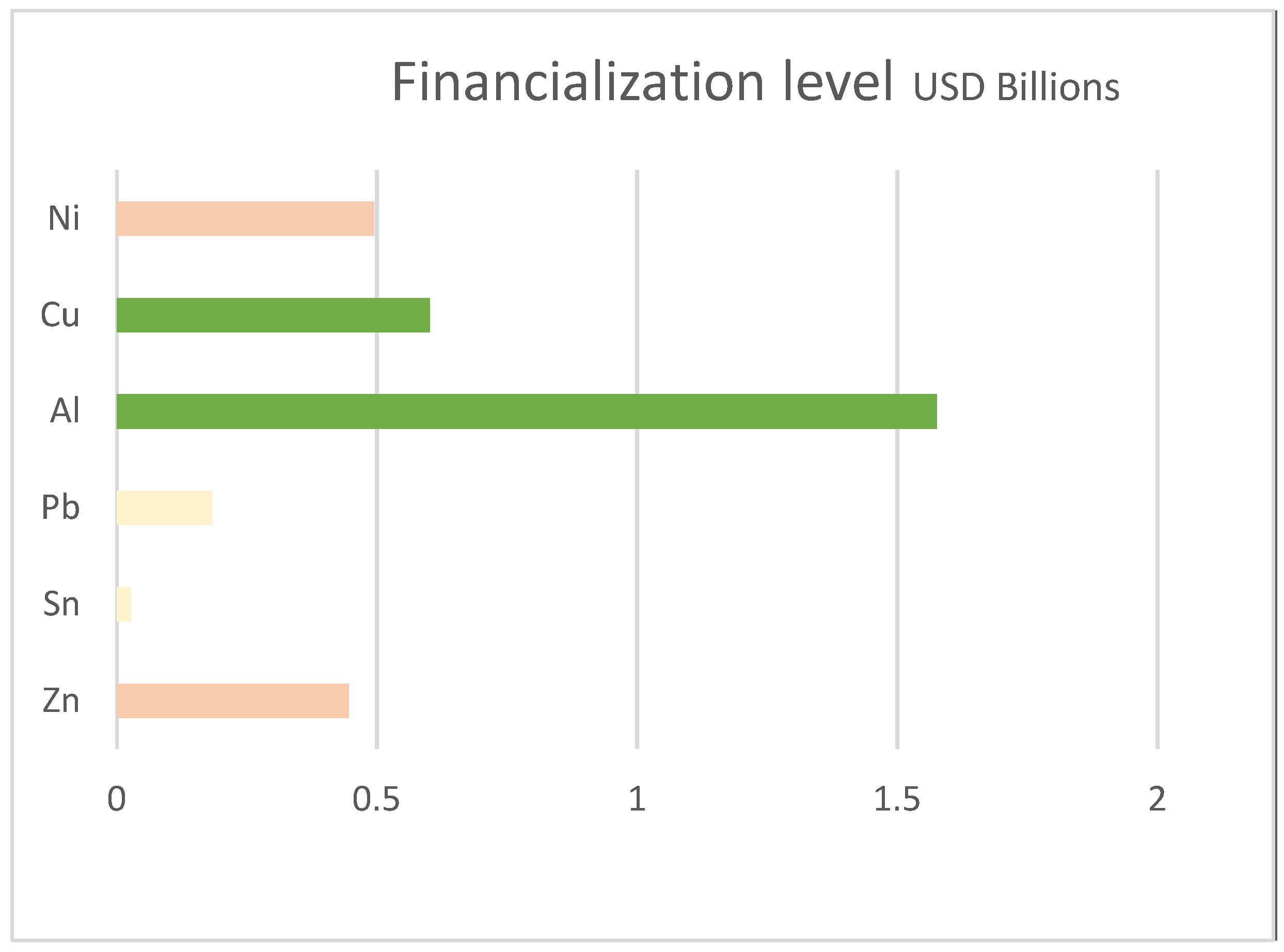

Specifically, we find that copper and aluminum are the two most highly financialized base metals, following the LME’s (London Metal Exchange) Commitment of Traders Report (see

Figure 1).

The so-called “normal backwardation” theory links the fundamental scarcity level of a commodity (physical supply and demand) with the appearance of a higher price in the short term than in the long term. This was first studied by [

14], looking generally at commodities [

15] and specifically at certain metals such as zinc [

16], and some have recently assessed financialization factors [

17]. Several trends in the data also reflect the disappearance of “normal backwardation” in specific periods of study and in different commodities [

18,

19].

The theory of normal backwardation is also established through the theory of storage and is related to the cost of carry (COC) model, as shown in [

20], where it was shown that risk premium could be used to determine a long-term pricing model. This theory of storage was used to study the levels of stocks in warehouses in different exchanges, which has always been one of the main factors of the fundamentals-based movements of contango and backwardation. The literature addressing this theory is broad [

21,

22,

23], and a model combining backwardation and storage has even been considered [

24]. We can also find evidence of normal backwardation in oil price curves [

24,

25,

26].

“Normal backwardation” is a theoretical framework that studies the futures price structure, whether it be backwardation or contango, wherein the fundamentals are the main drivers of prices in the short term. Said structure is also linked to several factors, such as the combination of lack of demand and excess of offer, indicating contango, and an absence of offer with a surplus of demand, indicating backwardation.

In this paper, the purpose is to follow and to check the link between the increase of LME warehouses’ stock and a high contango value on copper prices, which is evidence of the normal backwardation theory, related to an extreme event, such as COVID-19. This recent crisis has shocked the metals market, causing the whole value-added chain to slow down in the period immediately after the declaration of the pandemic. This slowing forced some market participants to increase their efforts to finance their sales to official warehouses. In the case of commodity sellers, the goods were directly moved to LME warehouses. Therefore, an increase in the stocks in warehouses was achieved at the same time as the pause in commerce, and the copper market futures prices developed into contango structure. Thus, we have analyzed prices and stocks data obtained from LME, and the number of deaths due to COVID-19 by geographical area, obtained from the World Health Organization (WHO), building data series to assess stationarity. Stationary tests have demonstrated stationarity or same level of non-stationarity, performing ADF (augmented Dickey–Fuller) [

27], PP (Phillips Perron) [

28], and KPSS (Kwiatkowski Phillips Schmidt Shin) tests [

29]. Subsequently, the cointegration between prices and deaths on the one hand, and contango structure and level of stocks in warehouses on the other hand, can be obtained by the Johansen approximation [

30] of the Engle and Granger causality theory.

The aim of this work is to clearly show that copper is a market linked to fundamentals, and is not only a refuge of investors, traders, and speculators—it is, for instance, a financialized market. The importance of copper to our daily lives makes the influences on offer and demand extremely important, and the situation during the first waves of COVID-19 in Europe offers evidence of this.

The contributions of this research include the findings of co-movements between the COVID-19 index of weekly deaths and the copper futures price structure during the first wave of contagions in Europe, and of evidence of normal backwardation with the development of such a futures price structure and the increase in stocks in official LME warehouses.

More specifically, we have completed an analysis of the development of contango in crisis situations and not only of the effects on prices (as in [

31]), which opposes the findings of some other authors (such as [

32,

33], which continued to see financialization throughout the COVID-19 crisis and other references such as [

17] that really focus on the paper of Financialization against Normal Backwardation).

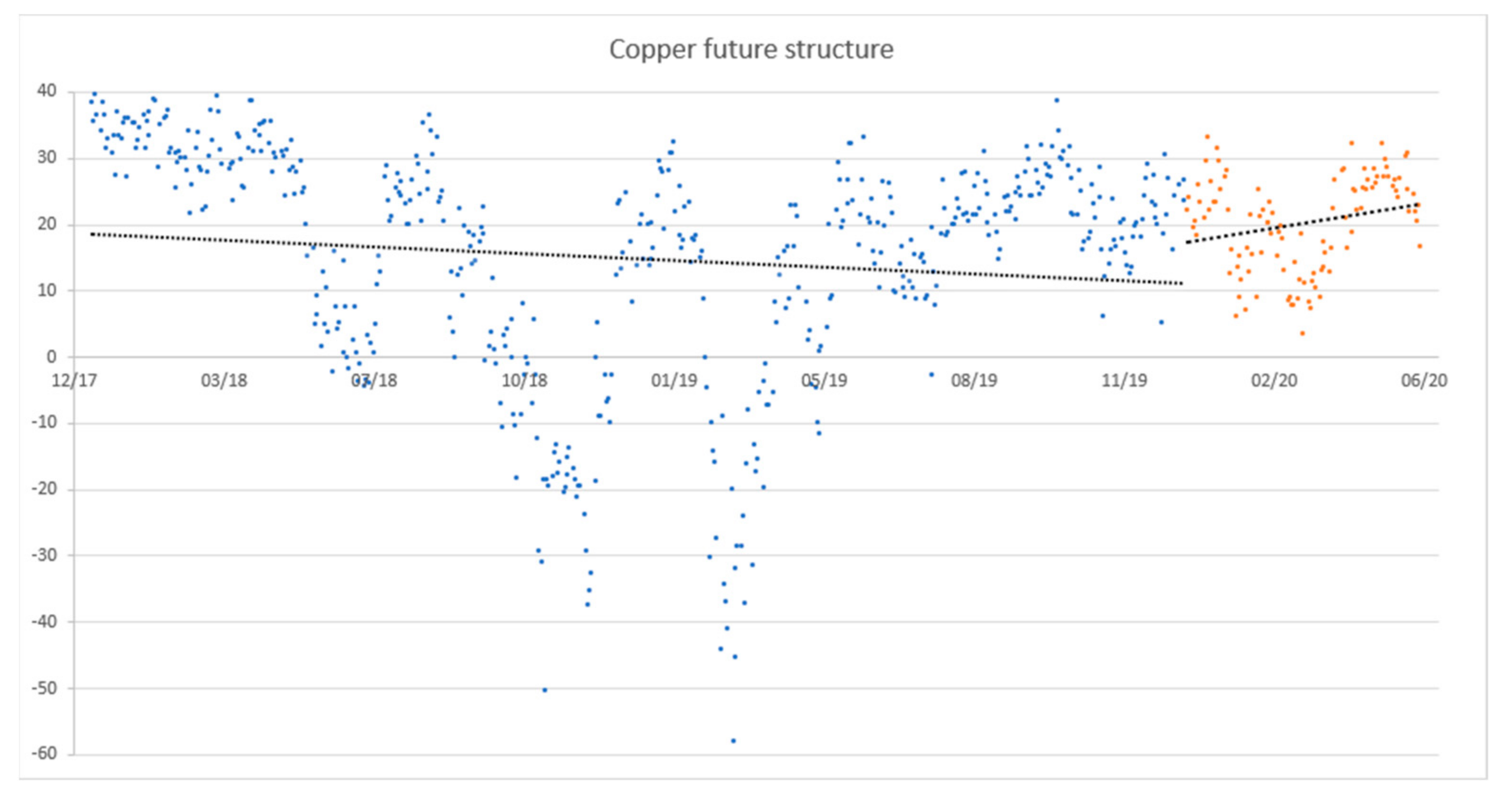

A better illustration of how COVID-19 has shocked the copper market in particular is offered by the descriptive change in tendency in the first half of 2020 (during the first wave of COVID-19 contagions in Europe) (see

Figure 2). The figure shows LME copper market evolution, in reference to its official historical price structure, and it can be seen, too, how the market had been in a negative (−0.0102) trend, then in a positive one (+0.0362), in both cases, using a linear regression approach.

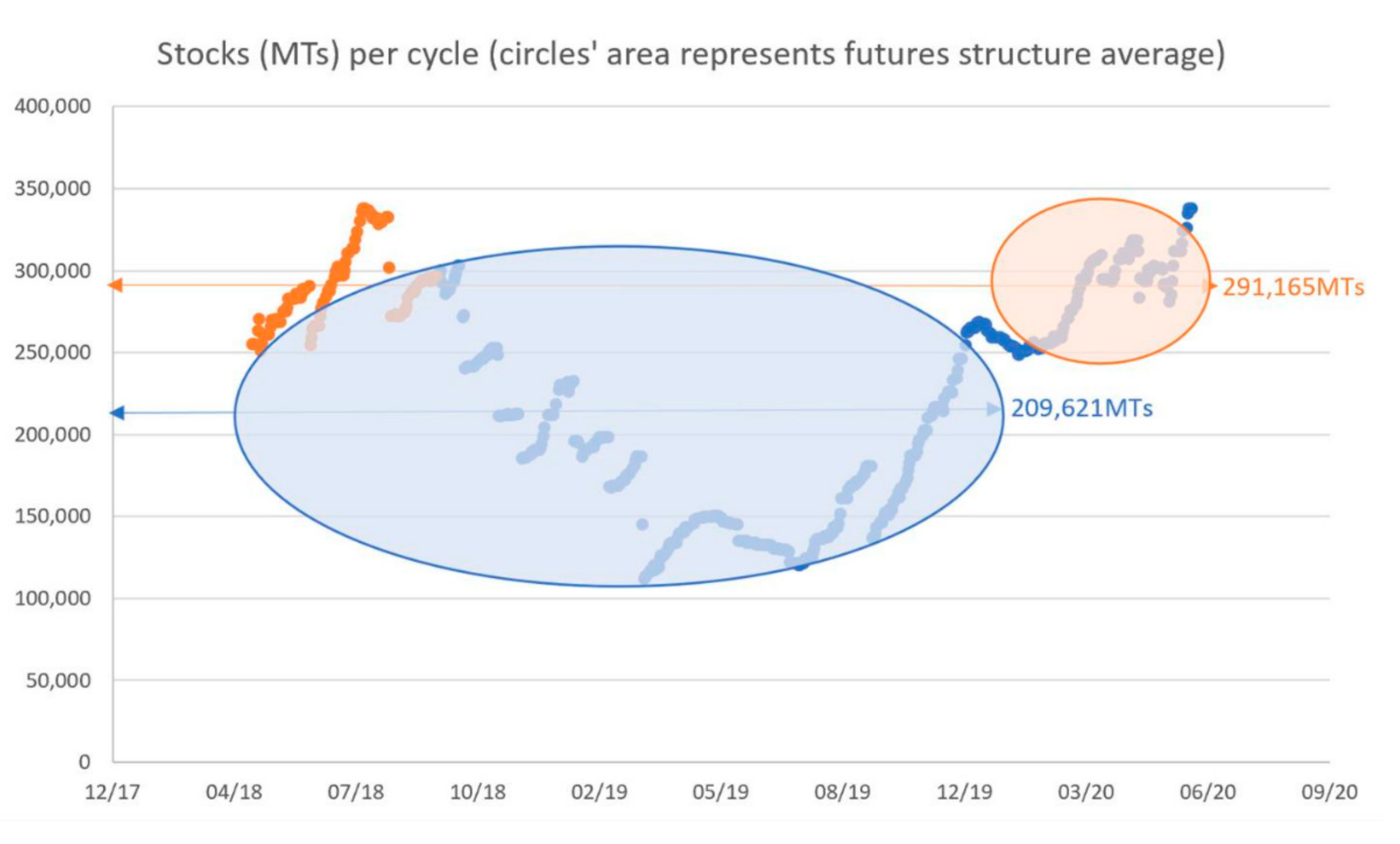

An additional illustration of the influence of the situation on stocks in the first half of 2020 is given by

Figure 3, representing the average levels of stocks in warehouses.

Copper stocks significantly changed, as volume went from 209,621 MTs, on average, during 2018–2019, to 291,165 MTs, on average, during the first half of 2020, which represents a 39% increase.

The remainder of this paper is organized as follows.

Section 2 reviews the relevant literature on cointegration, co-movements, copper, and the COVID-19 crisis. The data and methodology are reviewed in

Section 3. A description of the results and an analytical review are presented in

Section 4. Finally, conclusions and recommendations are discussed in

Section 5.

3. Data and Methodology

3.1. Data

The copper price data were obtained from the London Metal Exchange and have been used to establish the price structure upon official daily close of the market. The database includes 102 official LME calendar trading days, stretching between 13 January 2020 (day 44 of the pandemic, following [

68], with the first case identified in China) and 5 June 2020 (day 188, when the first wave in Europe was considered under control), as used for a descriptive analysis of the first wave of contagions in Europe as the growth rate moved to zero (this interval has also been used by some other authors [

69]). The COVID-19 data index we used was composed of the accumulated deaths collected each week in different regions of the world, according to the data published by the WHO, evaluating the number of cumulative deaths (weekly summarized) per population (10,000 habitants’ ratio) as per the United Nations World Populations Prospects 2019. These COVID-19 data were segmented by Date/Country/WHO_region/New_cases/Cumulative_cases/New_deaths/Cumulative deaths, and the different regions are shown in

Table 2 below.

3.1.1. WHO Weekly Mortality Index

We have used the percentage of increase in cumulative deaths, measured weekly as a percentage per 100,000 habitants, as cases detected during the first wave were not measured in the same diametric manner in every country (due to the different capacities to do so) and weekend data were usually not published on time by every country. The availability of tests and the differences in how countries report their figures have been amongst the biggest limitations to our data.

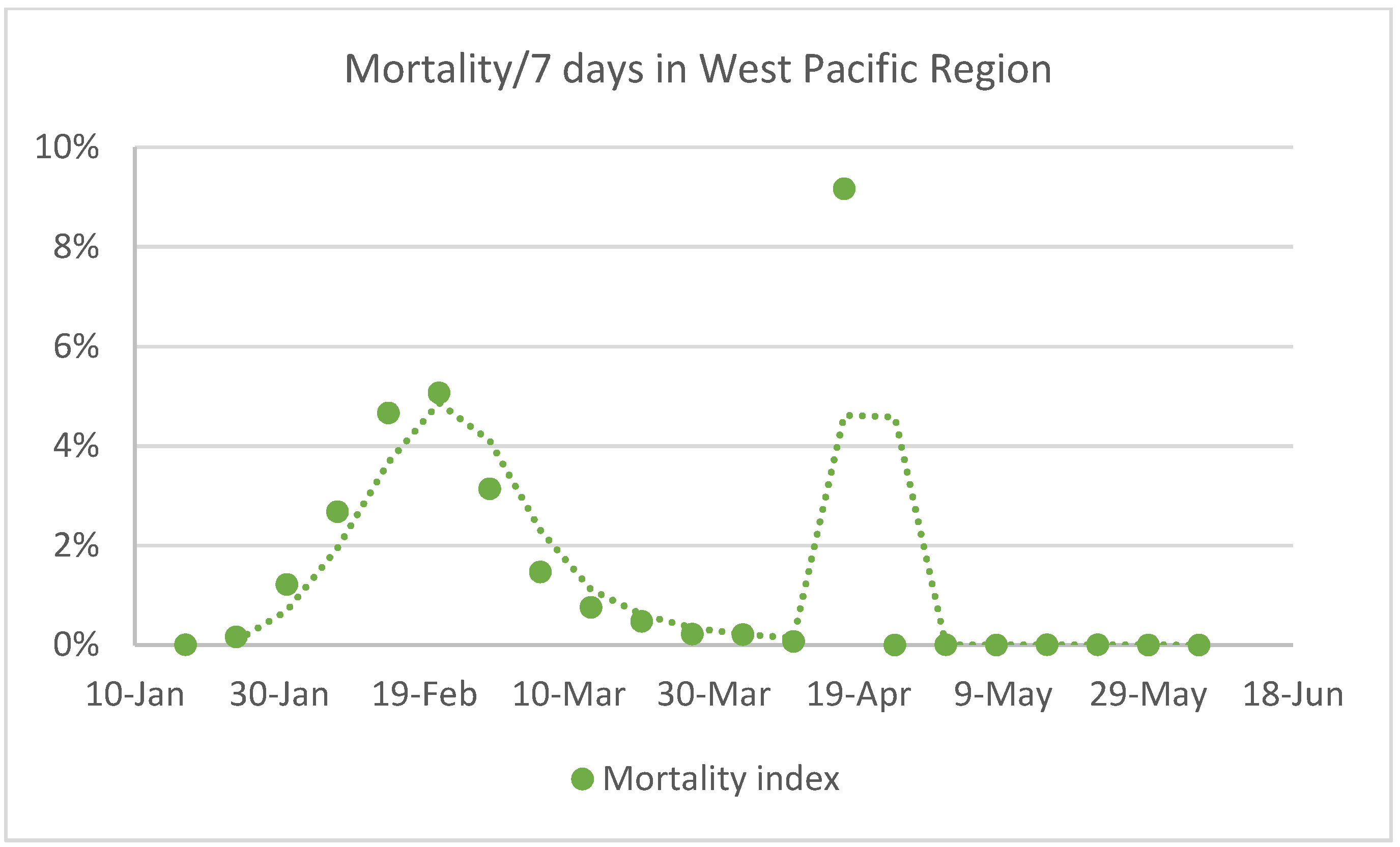

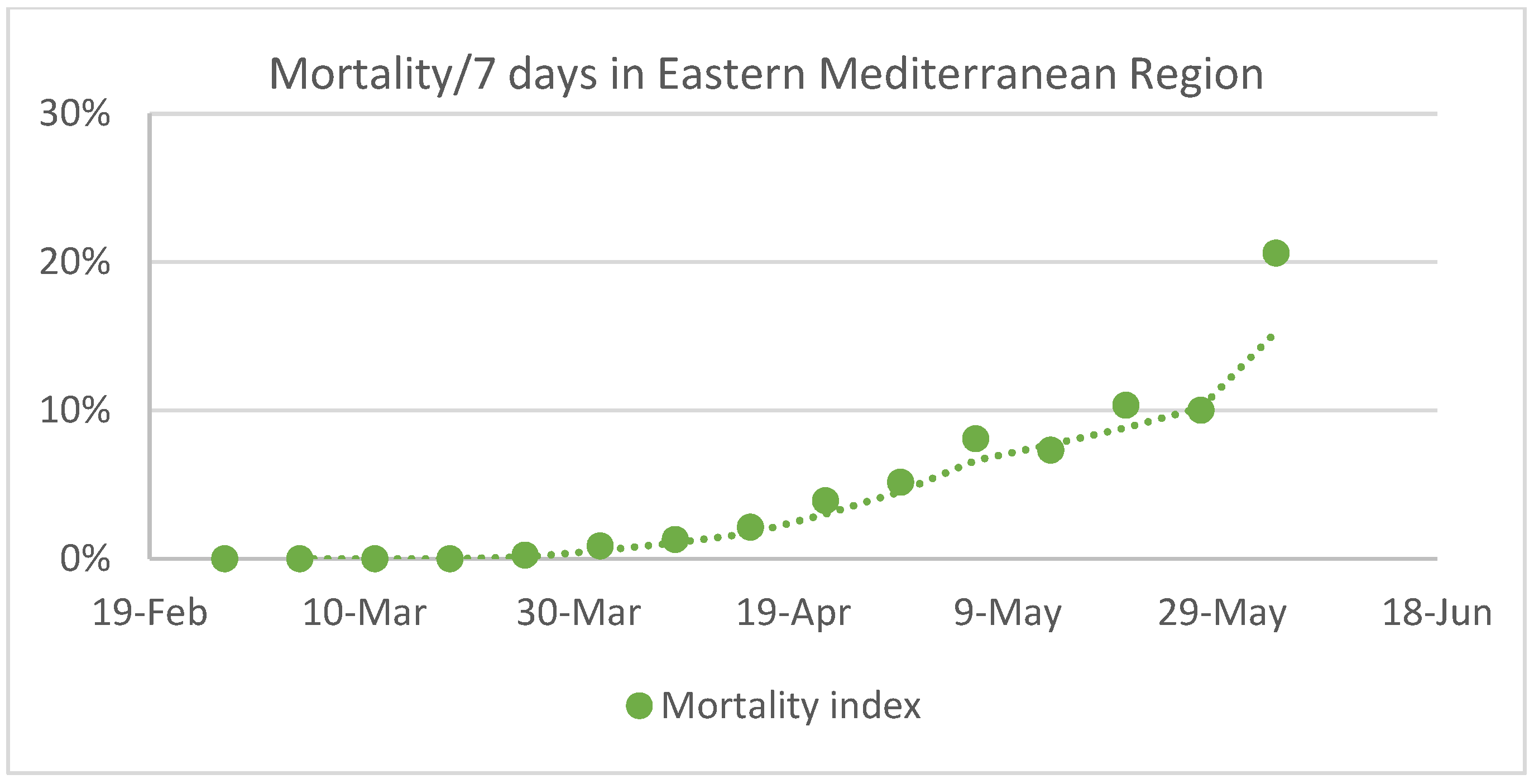

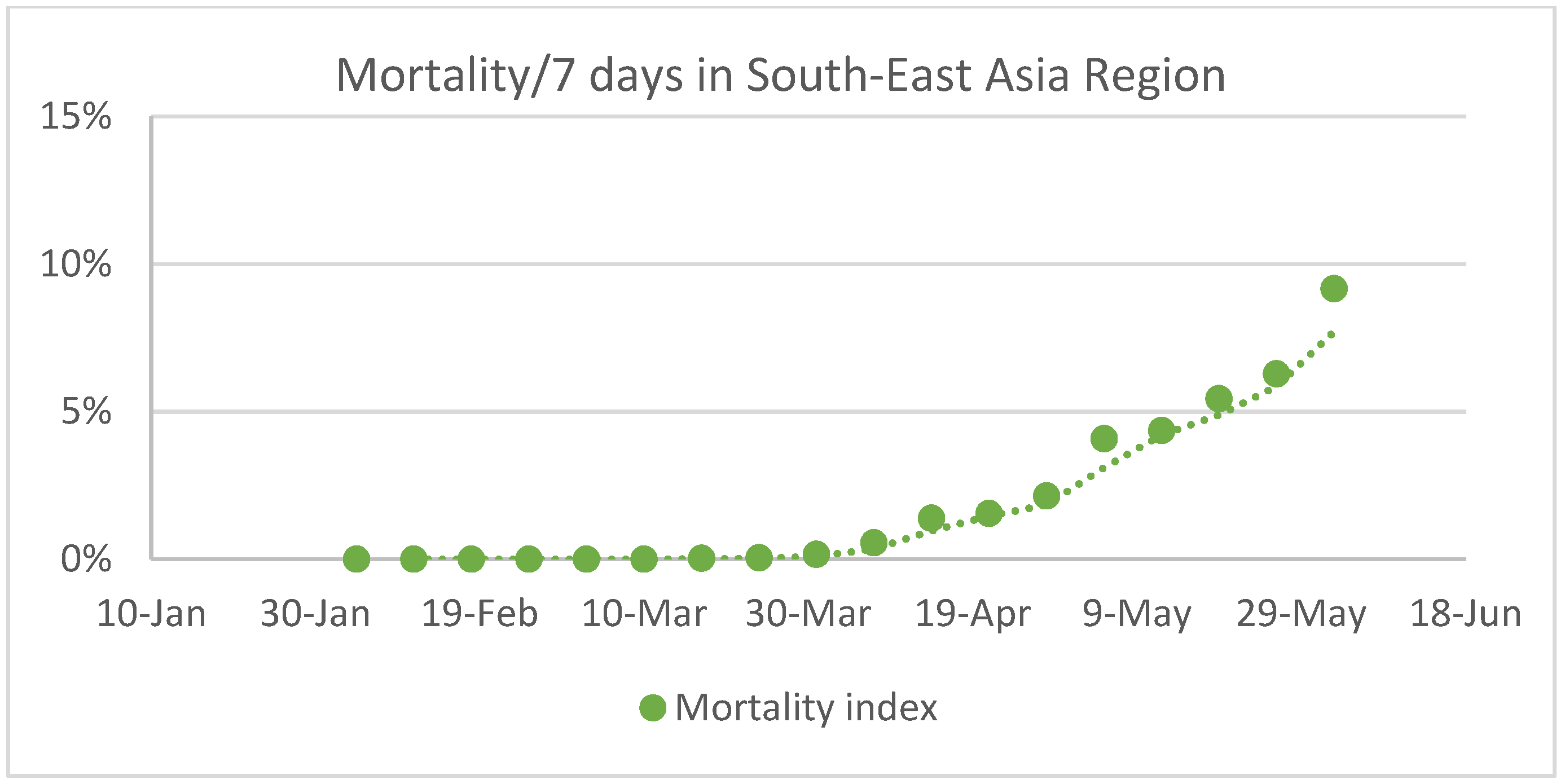

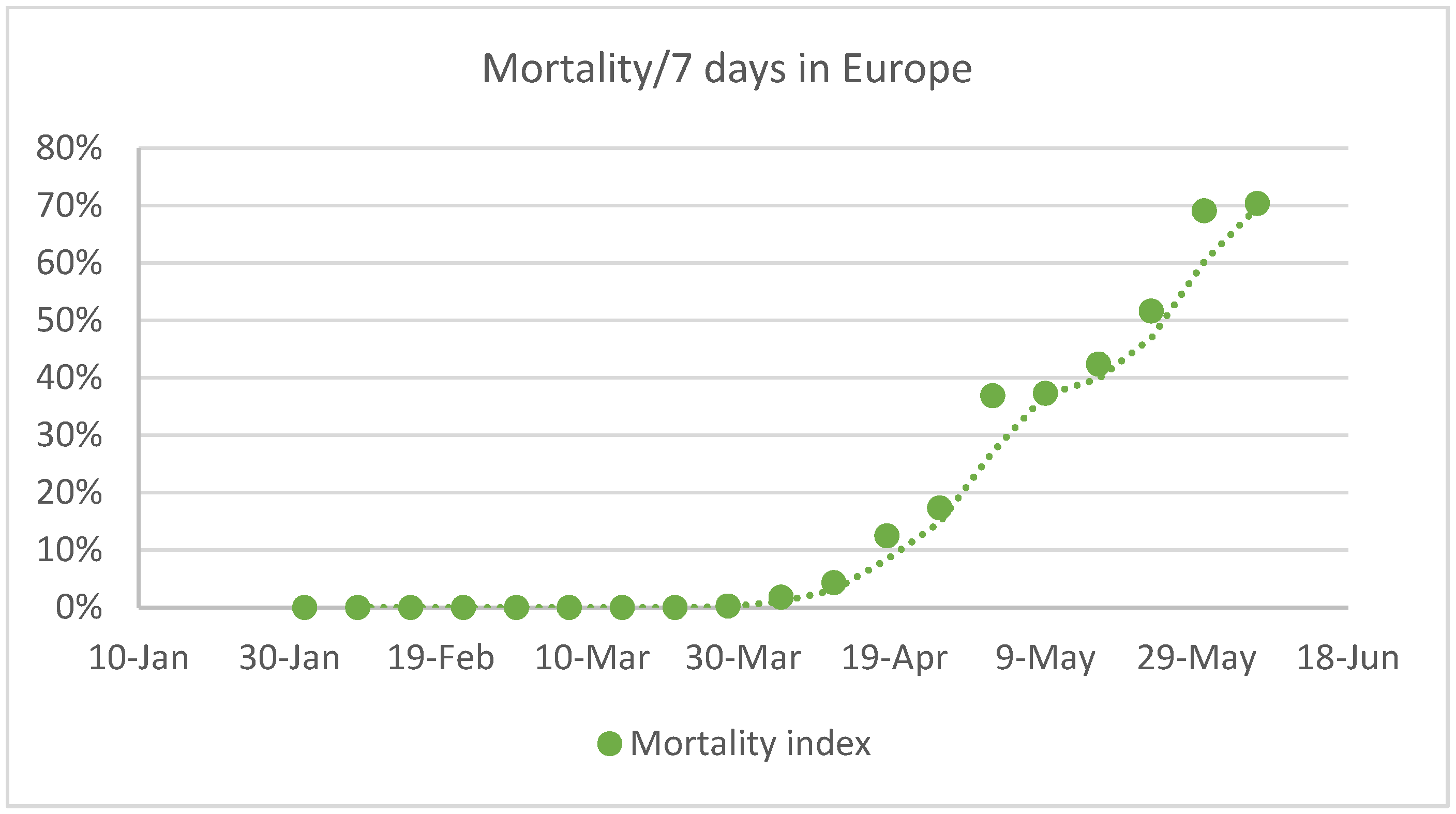

The figures show the data on the biggest countries in each WHO region to perform a descriptive analysis of the information available.

The COVID-19 weekly mortality index (represented by the time series COVIDt) was obtained through arithmetic assessments of the data given every Monday by WHO, focusing on the difference in cumulative deaths between one reference and that from the previous week. The percentage of growth shown by one reference over this period is the focus of our study. These data have been assessed for the number of inhabitants in every region. As such, we can establish:

Day 1 Cumulative deaths 1 Mortality assessed 1

Day 8 Cumulative deaths 2 Mortality assessed 2

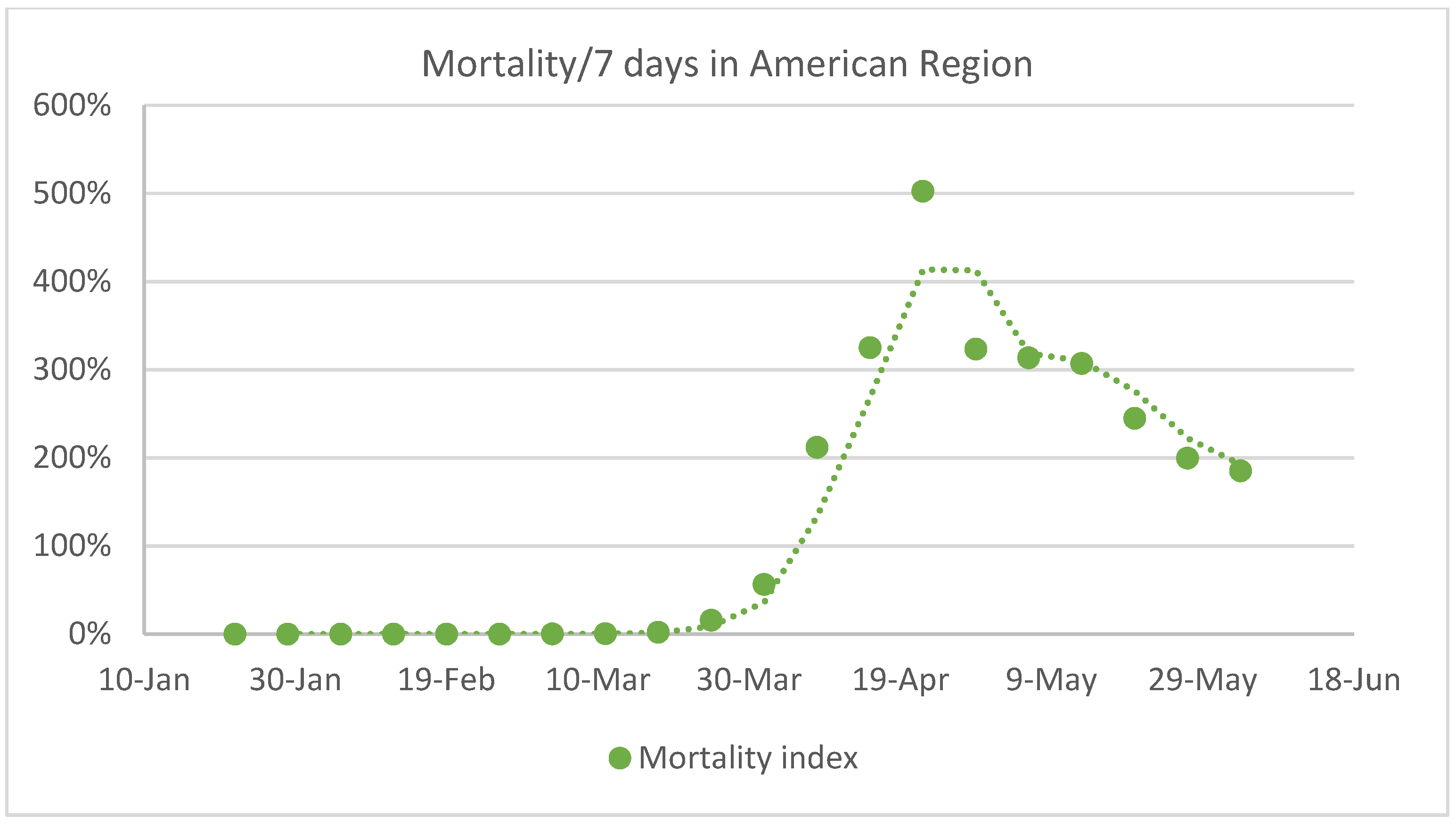

Cumulative deaths data from Monday to Sunday were calculated through the sum of daily deaths that were published. Even though Europe alone is the subject of our investigation, we display the results for the six areas (see

Figure 4,

Figure 5,

Figure 6,

Figure 7,

Figure 8 and

Figure 9).

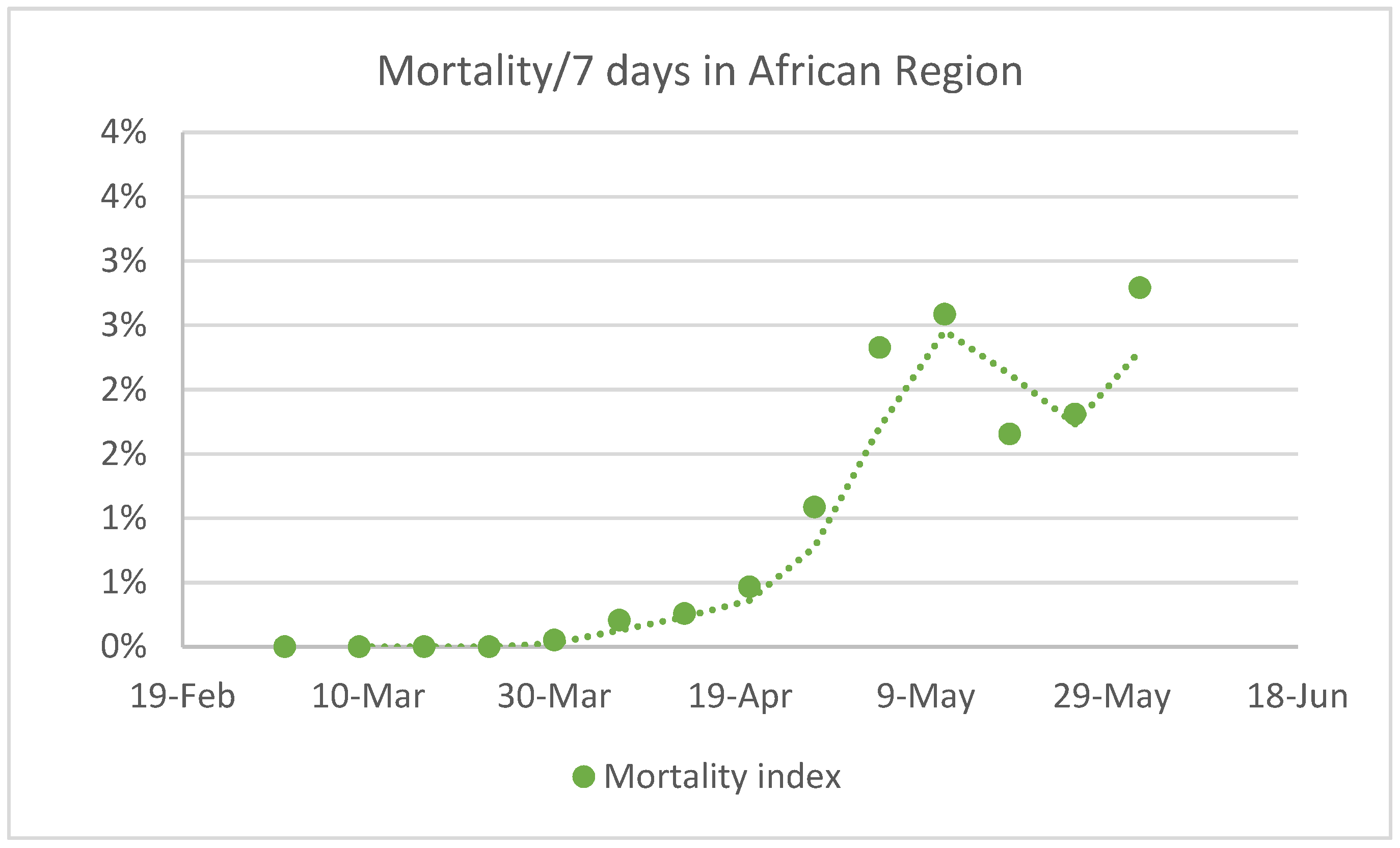

Low values were found in African and West Pacific regions during the first wave of contagions in Europe, and these are mainly related to the low ages of the populations in the main countries in the African area and to the heavy measures taken to control the pandemic in the West Pacific region.

Eastern Mediterranean, South-Eats Asia and Europe regions have shown constant increases, but Europe has shown a very significant constant increase in the seven days mortality index.

The American region has shown a constantly increasing ratio indicating an uncontrolled pandemic situation followed by a period of apparent control, with a substantial drop in the percentage of increase in deaths due to COVID-19; the reality, however, is that the increase was so big (achieving values of more than 500%) that the decrease appears as 200%.

3.1.2. LME Data: Prices and Warehouses’ Stocks

The allocation of the futures price structure is derived from the difference between the 3-month control reference and the cash or spot price. The 3-month basis is a liquid position [

70] and is that to which the whole market refers a large part of its operations; therefore, this metal’s structure refers to this difference, whereby a positive difference indicates contango and a negative one indicates backwardation.

The most common market structure should be contango, as the warehousing system is a regulator. Backwardation should only arise in a forced market, related to a lack of offer, an excess of demand, or a speculative global fund trading position. Nevertheless, this situation is becoming more and more frequent, with long periods of backwardation arising due to the developing super-cycle of metals [

71,

72].

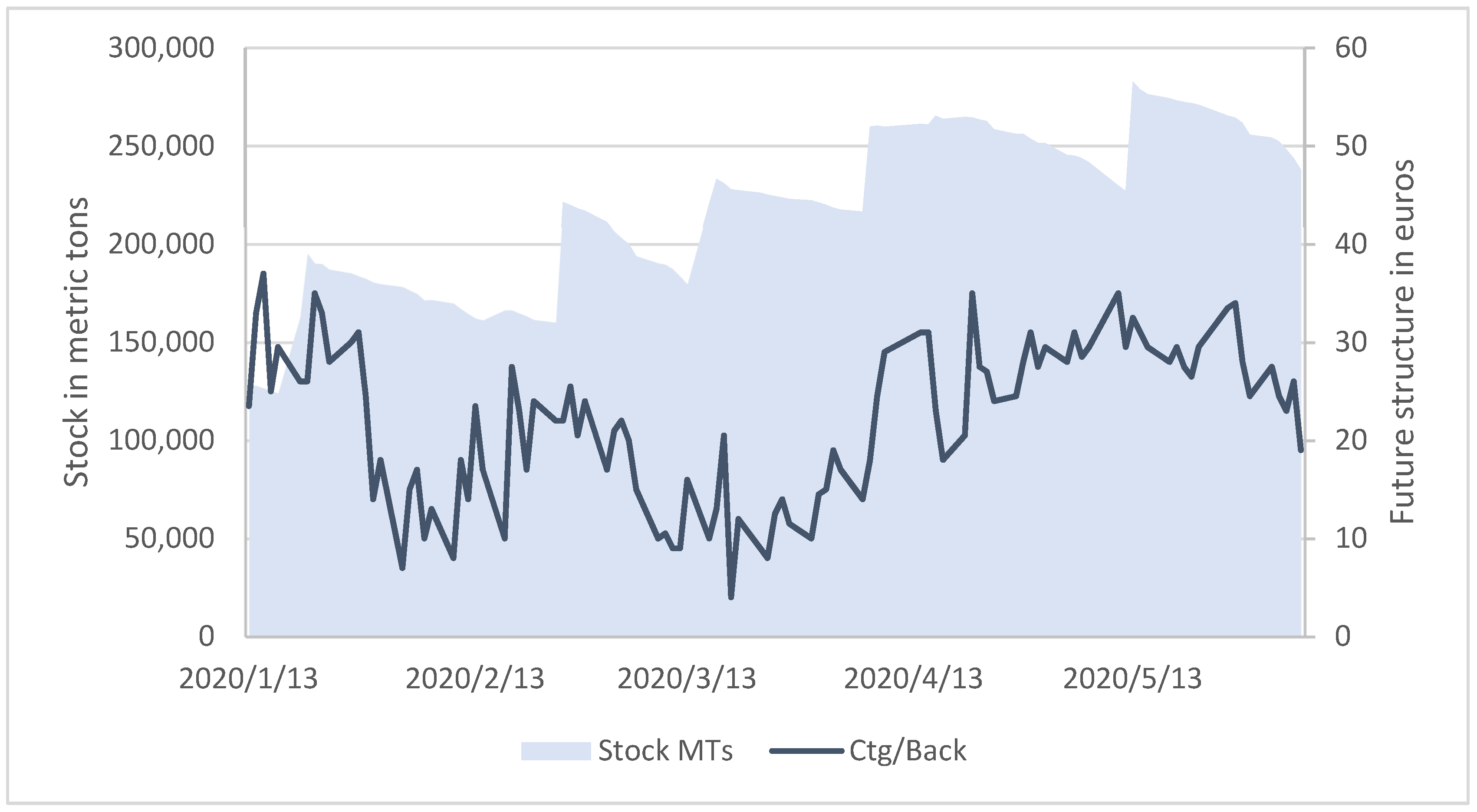

The copper futures price structure data were taken from the LME and warehouses stock for the same period; the LME uses a worldwide warehouse system to normalize different levels of metal demand and offers. Producers and traders can place large amounts of metal into these warehouses if its brand and quality are assured by the LME’s standards; this can be done through brokers, who also need to be listed under the LME’s standards. As the premium for introducing a metal into an LME warehouse is null, producers prefer to sell directly to the market so as to achieve a premium; therefore, it is usually only when the direct consumer market is not active or is sparse that metals arrive at these warehouses. Traders can also perform this type of operation to manipulate the structure of the prices or the forward curve in favor of their short- or long-term global positions. The levels of copper in LME’s warehouses and the structure of the copper futures prices are shown in

Figure 10.

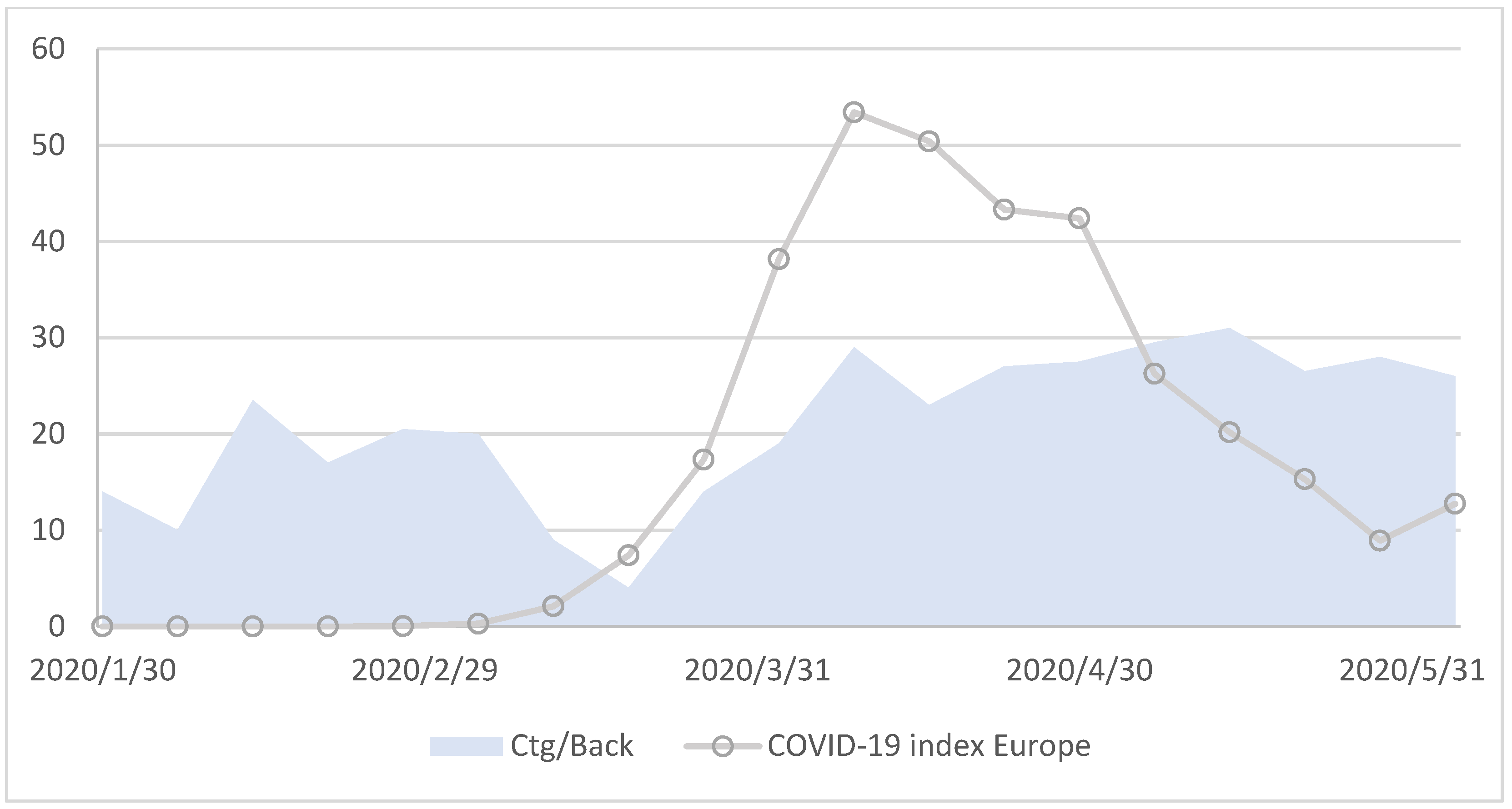

European data were chosen for this analysis for three reasons. First, Europe is one of the major economies outside of China; second, it is where the LME warehouses have been established; third, its markets are mostly based on fundamentals. Additionally, descriptive analysis also supports the strategy of using Europe as the basis of this study, as the same trends are shown in their COVID-19 indexes as in the changes in LME warehouses.

Both data series—the COVID-19 index in Europe and the LME copper futures price structure—are represented in

Figure 11.

3.2. Methodology

Unit root tests have been performed to ensure that the time series do not follow a random walk structure, ensuring that they are stationary and that causality tests can be used. In this regard, our aim was to identify the situation wherein series bind together, with no deviation from equilibrium in the long run.

In these types of unit root tests, the null hypothesis can be linked with the stationarity of the time series, as in the ADF and PP tests, as well as in different ones, such as KPSS tests.

Because the time series addressed in this study were non-stationary and exhibited non-constant variance, they were analyzed with the augmented Dickey–Fuller (ADF) [

27] unit root test, as recently deployed by [

73] and [

74].

The three regression models for ADF are set out below:

In these equations, the difference between two time values is a function of non-constant variance ut, with or without constant drift, µ, and a trend term, γt.

The symbols in the above expressions are defined below.

ΨADF, parameter determining the fulfilment or otherwise of the null hypothesis.

, sum of differentials in the value series multiplied by Ψ in p − 1 iterations.

p, maximum regression delay.

µ, constant.

γt, trend.

ut, process error, a function of the variance series.

The ADF and Phillips–Perron test that there is a unit root for a times series as a null hypothesis. The existence of a unit root implies that the process is non-stationary. KPSS tests the null hypothesis that there is stationarity in the series [

75].

Engle and Granger causality-based cointegration tests [

33] were performed on the transformed series. The latter yield the order of autoregressive vectors (VAR) [

76] and a basis for calculating

λmax using Johansen’s approximation, which is used to find at least one cointegration relationship between the two series.

The Granger causality theory (Johansen approximation [

30]) was used to analyze the relationship between the series

.

To resolve the equations shown below ((9)–(12)), Engle and Granger cointegration tests were conducted by applying ordinary Least Squares (OLS) to the transformed data series:

On the one hand,

where d is the number of delays used,

are the time series for which cointegration was to be determined,

α and

β are the parameters to be studied, and

εt and

ut are the errors or random disturbance, which are normally uncorrelated. It is necessary to fit a vector autoregressive (VAR) model to obtain the optimum lag model [

76].

On the other hand,

for the other pair of data series studied.

Finally, a robustness test was done, studying cointegration between the independent variables of the above analysis: COVIDt and STOCKt.

From a methodological point of view, once the series are transformed enough times to obtain stationarity, these series can be represented as a set of p iterations with consecutive values, as follows:

in which the values are corrected by a series of constants, such as

Ai, where

i = 1, …,

n; the input constant is

c, and the error vector is

et.

The

p-value of Equation (13) defines the VAR order of the series [

77]. Here, it was found with the Schwarz or Bayesian (BIC) and Akaike information criteria (AIC), as defined by [

78]:

where

L* is the Napierian logarithm of the likelihood function;

n is the number of observations, and

m is the number of estimated parameters.

The Johansen approximation yields α and β as the vectors:

where r is the number of cointegrating vectors, and p and m are the series vector components.

The premise underlying the maximum lambda and trace tests was described by [

79] as follows: “The maximum likelihood theory of systems of potentially cointegrated stochastic variables presupposes that the variables are integrated of order 1, or I(1), and that the data-generating process is a Gaussian vector autoregressive model of finite order l, or VAR(l), possibly including some determinant components”. The trace test is defined in the following terms:

where

λi are the eigenvalues in ascending order that deliver the solution to the “reduced rank regression problem”, and

r and

p form parts of values

α and

β, as above.

The test is run consecutively for r values of r = p − 1, …, 0 or r = 0, …, p − 1, up to the value at which the null hypothesis is first rejected, or to the end of the series if it is not rejected.

Instead of

r, the validity of the null hypothesis may also be determined from

r + 1, which constitutes the

λmax test, which is the one used here:

which is identical to the trace test when

p − r = 1.

Finally, it is necessary to determine whether one variable “Granger-causes” another. One variable causes the other if the past values of one are useful for predicting the other. See

Appendix B for an extensive explanation of the application of this methodology in different markets.

The residuals of the linear regressions built from the different data series are a matter of study in this paper, as assessed through the Durbin–Watson approach [

80,

81,

82].

Under this theory, the errors complete the definition of each time series, defined as

εt, and taking in this formula, the definition of the statistic D can be given as

where

t refers to the different observations of the time series.

The null and alternative hypotheses of this test are H0, where the errors are not correlated, and H1, where they are. With a p-value below the significance level, we can certify that the residuals are sufficient to use in the following tests on the time series.

4. Results

In this section, we give the relations between the structure of copper futures, the LME copper warehouses’ level, and the COVID-19 weekly mortality index during the first wave of contagions in Europe. We have also seen, in general, how extreme events are linked with big effects on the future price in comparison with the cash price, ultimately developing a contango structure, evidencing the theoretical background of so-called “normal backwardation”.

4.1. Relationship between LME Copper Warehouses’ Level and the Structure of Copper Futures Prices

Both series STOCK

t and st

rut have been shown to be non-stationary, even after Box–Cox [

83] transformations, and we also found non-stationarity at the following levels of both series. We confirmed this via ADF, PP, and KPSS tests to check the non-stationary of the two series, STOCK

t and st

rut, as can be seen in

Table 3, finding that both series are non-stationary to the same degree. In regard to causality, Johansen’s approximation of the cointegration test of Engel and Granger was performed (see

Table 4), obtaining cointegration between the STOCK

t and st

rut series in the time frame studied. This means that increases in contango and stocks are linked, giving evidence for the theory of normal backwardation.

This means that, under strongly adverse conditions in the consumption market, because of economic crises, sanitary catastrophes, low demand, or other extreme events, economic players, such as producers or traders, are forced to allocate their units to official warehouses instead of to final consumption markets. From a practical point of view, this means that copper producers cannot easily alter their volumes to adapt to rapid decreases in market consumption. This is also a characteristic of the commodity market, wherein a complex global system of warehouses is established specifically “to regulate the inflows with the outflows”. The specific definition of backwardation based on fundamentals refers to the lack of availability of metal on the market, and in general, to the feeling of scarcity; therefore, contango means the opposite, that is, the excess of availability. Our findings definitely support this fundamentals-based definition of contango, as under the conditions of a sanitary crisis, with a lack of consumption and the same production model, market inflows are higher than outflows, with a strongly positive offer–demand balance, excess being allocated to the official warehouses.

This theory can be used by market players when establishing their positions in favor of contango when such market disruptions are about to occur.

4.2. Relationship between COVID-19 Mortality Index and the Structure of Copper Futures Prices

As in the previous assessment of the series, we have also checked the stationarity of

strut, this being the futures copper price structure data series, finding (see

Table 5) that for both series (this one and the COVID-19 mortality data index), non-stationary conditions were achieved. After Box–Cox transformations, we also found non-stationarity in the following levels of both series.

Both data series, before and after being transformed, showed the same levels of non-stationarity, making it appropriate to use Johansen’s approximation of the Engel and Granger cointegration test to obtain co-movements between the COVID-19 index and the future price structure of copper (see

Table 6).

These results show that an event with a strong impact on demand (such as the increase in COVID-19 mortality rate) can cause market scarcity to disappear; in fact, it could generate a feeling of oversupply, thus developing a contango structure.

A producer that is starting to feel a lack of consumption interest from their customers due to a macro event, such as an incipient economic crisis or a sanitary emergency, could easily reassert their hedge position by selling their units using future due date prices instead of short-term prices. A good example of this has been the appearance of new variants of COVID-19, as a result of which the market could be preparing to restructure into a consistent contango. This approach, as others, is speculative by nature, so what is offered here is a better chance to prepare a strategy, as the market could have opposing drivers that would make the structures of copper futures prices fall into backwardation.

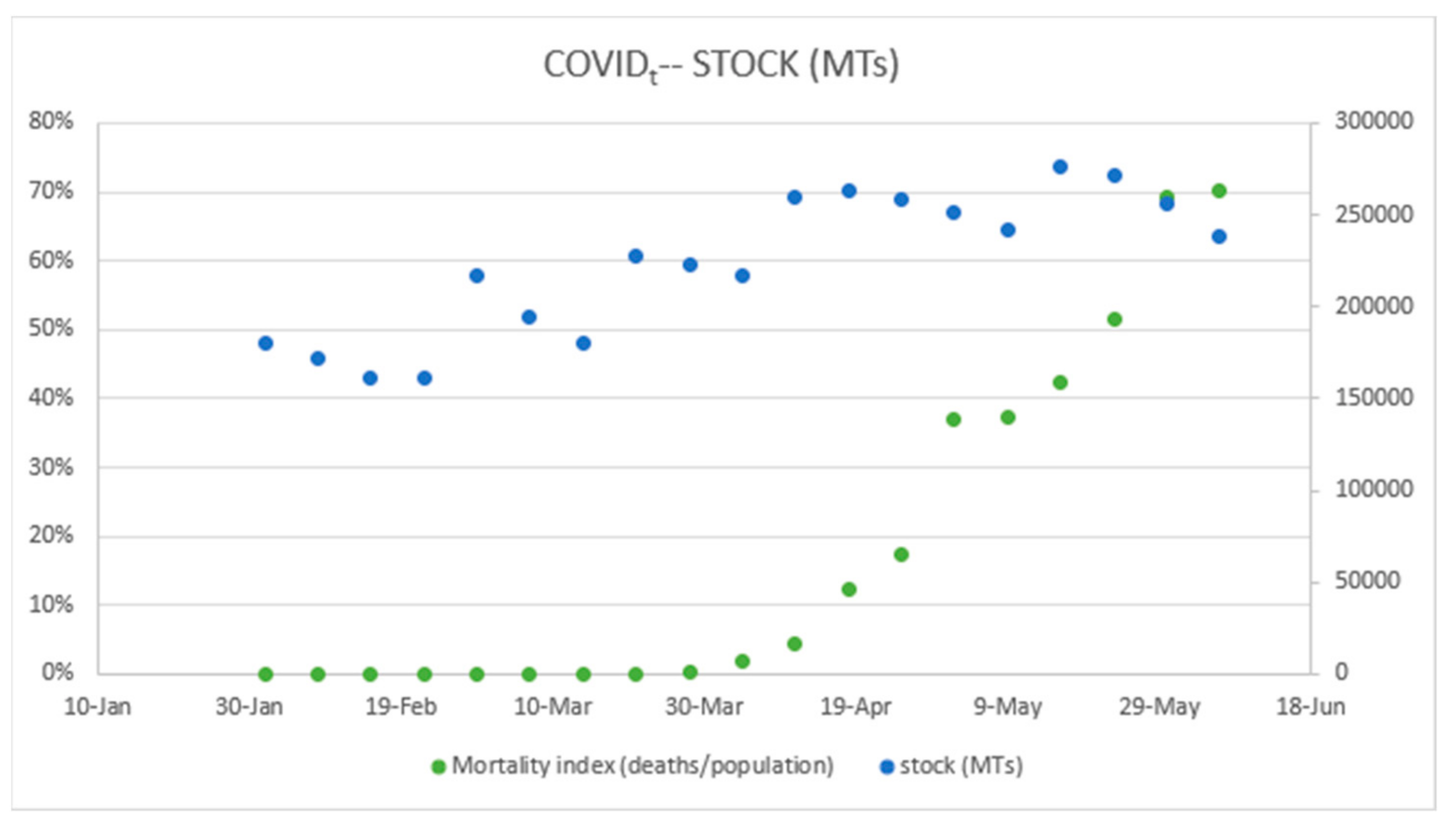

Relative to the joint evolution of COVIDt and LME warehouses stock series, as a robustness test, we have found that they are cointegrated. See

Figure 12 and

Table 7, showing

p-values of Engle and Granger test:

Finally, we tested the null hypothesis that residuals of the model are autocorrelated. Time series’ residuals have been checked via the Durbin–Watson test, trying to certify that these residuals are autocorrelated and the tendency is consistent. The results show (see

Table 8) that, in the case of the series: warehouse stocks, structure of daily dataset, and futures price structure, the p-value is less than the 1% and, in the case of the COVID-19 series, the

p-value is lower than the 5%, so the null hypothesis can be rejected.

5. Conclusions and Recommendations

The COVID-19 pandemic has thrown the world economy into turmoil, and commodity markets have lived through a tsunami since its beginning; its implications have led to a situation of strong normal backwardation.

This paper shows that the levels of stocks in warehouses are linked with the development of the commodity forward price (contango or backwardation). We proved that, in a multi-country lockdown scenario due to the first wave of COVID-19 infections in Europe, in a long-term backwardated context, copper stocks rose, and a contango structure appeared, indicating a cointegration between the data series representing these stocks and the contango structure.

In the same context, under the influence of macroeconomic events affecting commodity prices, the present findings confirm the existence of a relationship between COVID-19′s impact and the structure of copper futures prices, measured on the grounds of COVID-19 weekly mortality data.

In recent times, the financialization of commodities, especially copper, has been a matter of close study and investigation, as explored in the Introduction section, and we are finding that fundamentals are also interfering in the forward price compared with spot prices. Times are approaching where analyses and statistics are suggesting there will be a lack of copper units [

52,

53], so we can expect this commodity to be driven increasingly by fundamentals. The development of the EV (electric vehicle) and its higher level of copper usage for fabrication, the electrification of charging points, and the development of renewable energies are causing increases in optimism and a feeling that, again, fundamentals are playing an increasingly definitive role.

In this context, some highlights can be selected as policy recommendations, when market agents follow price structure strategies. Under normal backwardation theory, backwardation is the long-term trend; that implies that the spot price is higher than the 3-month price, so, depending on the position players have (short or long), they can try to move in favor of backwardation. However, an extreme event like COVID-19, that turned it into a contango, makes spot prices lower. This way, as contango appears, players should, then, set long term positions to optimize results.

Market players can benefit from changes in tendency and extreme events, such as the recent one studied here, related to the change from structural backwardation to contango. This fact can be used by volatility-based players to increase the weight of positions supported by extreme events, not only in terms of short-term contango or short-term backwardation, but also to set up a contango/backwardation structure change-based strategy. We have experienced, during the COVID-19 pandemic, different scenarios within the commodities market, showing the strongest contangos ever during the first phase of worldwide lockdowns, followed by several ups and downs in the future structure of base metals in particular, as related to extreme events (in our recent context, COVID-19): the arrival of a vaccine, the acceleration of the vaccination process, the appearance of new variants, countries’ herd immunity, new variants evading the protection of vaccines, new vaccines, new contagion waves, cross-relations between the variables under study, relations with other assets such as those in [

69], etc. There is no doubt that the analysis of the commodities market’s behavior in general, and that of copper’s in particular, under all these scenarios opens up a new line of research and constitutes the basis of new papers. Additionally, the relation between data from the WHO regions and aggregated data from around the world could be a new research focus, even if it would be a huge challenge to measure the integrity of the data given the speed of communication between each country.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}