Time-Varying Causalities in Prices and Volatilities between the Cross-Listed Stocks in Chinese Mainland and Hong Kong Stock Markets

Abstract

:1. Introduction

2. Literature Review

2.1. Literature about Relationship between Different Prices of Cross-Listings

2.2. Literature about Time-Varying Granger Causality Analysis

3. Materials and Methods

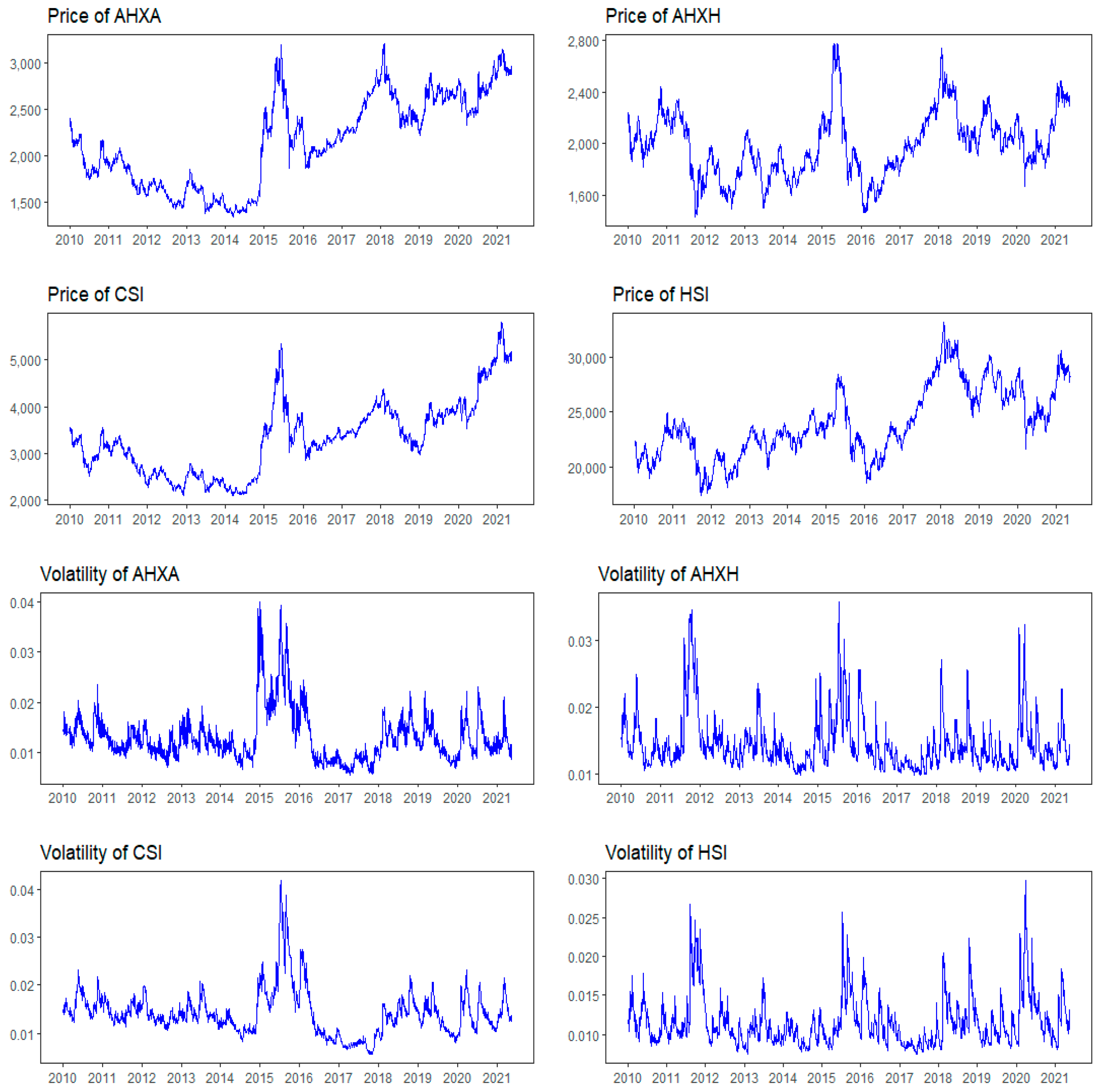

3.1. Data Description

3.2. Methodology

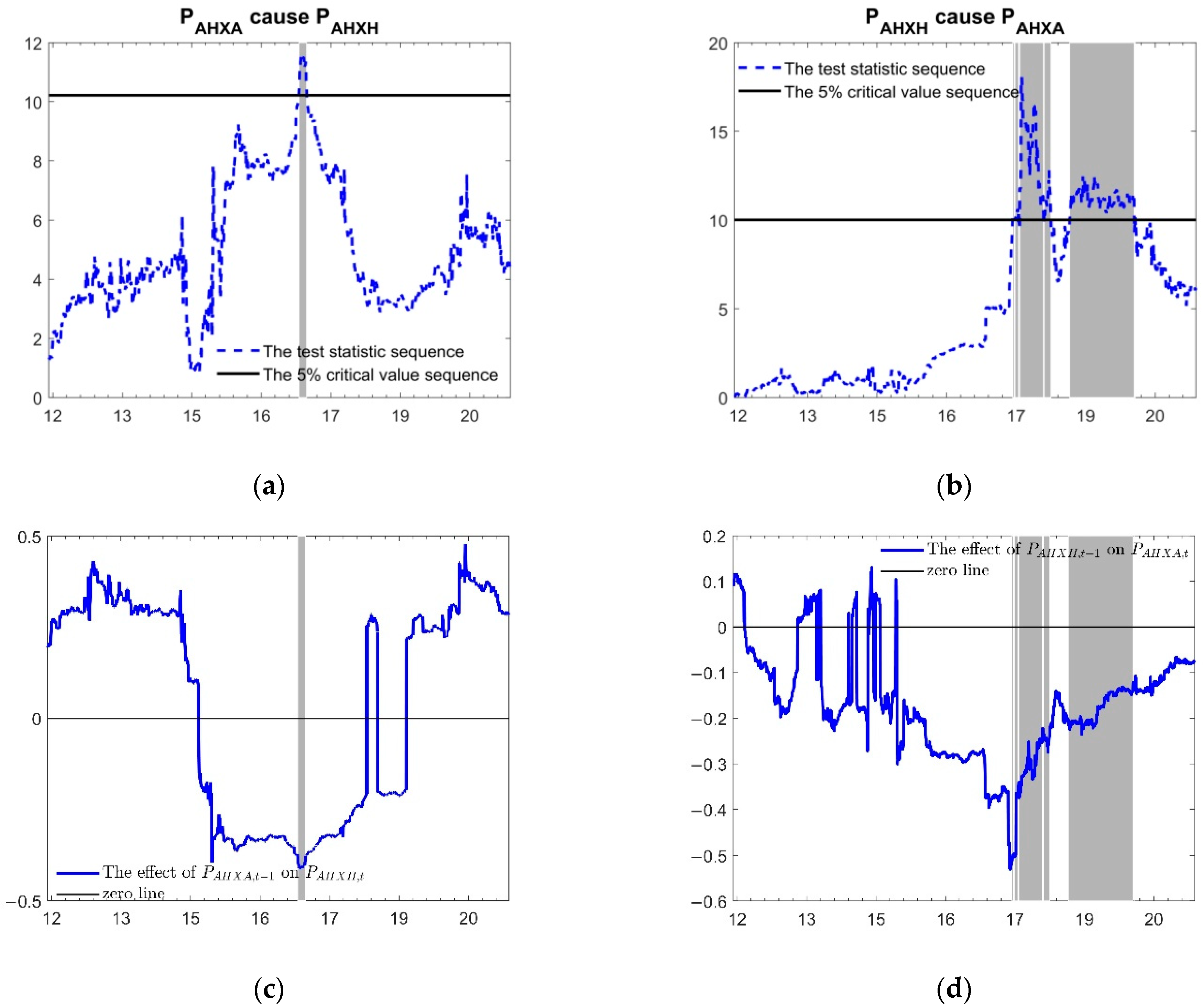

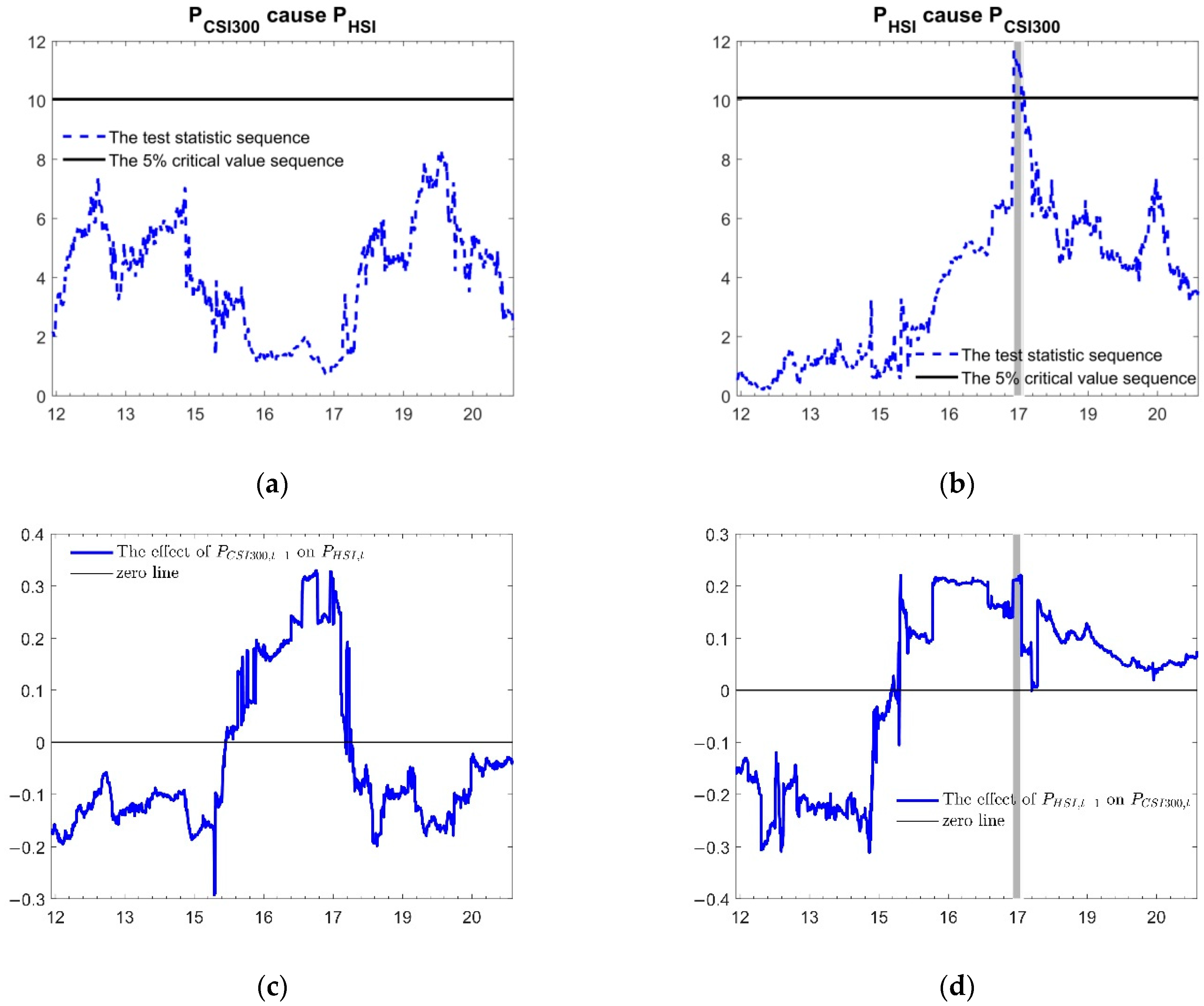

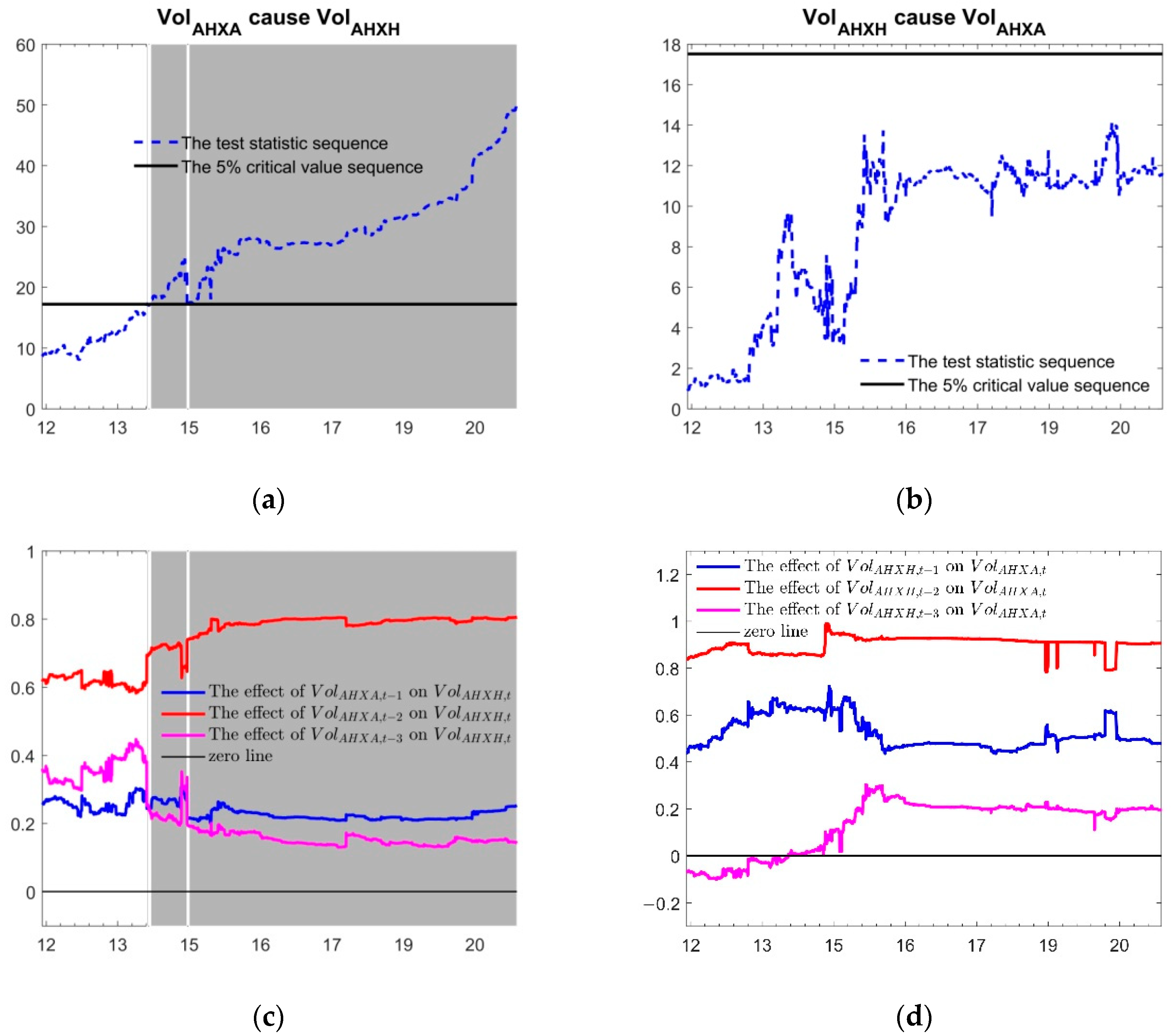

4. Results and Discussions

4.1. Maximum Order of Integration

4.2. Time Varying Granger Test between Price Series

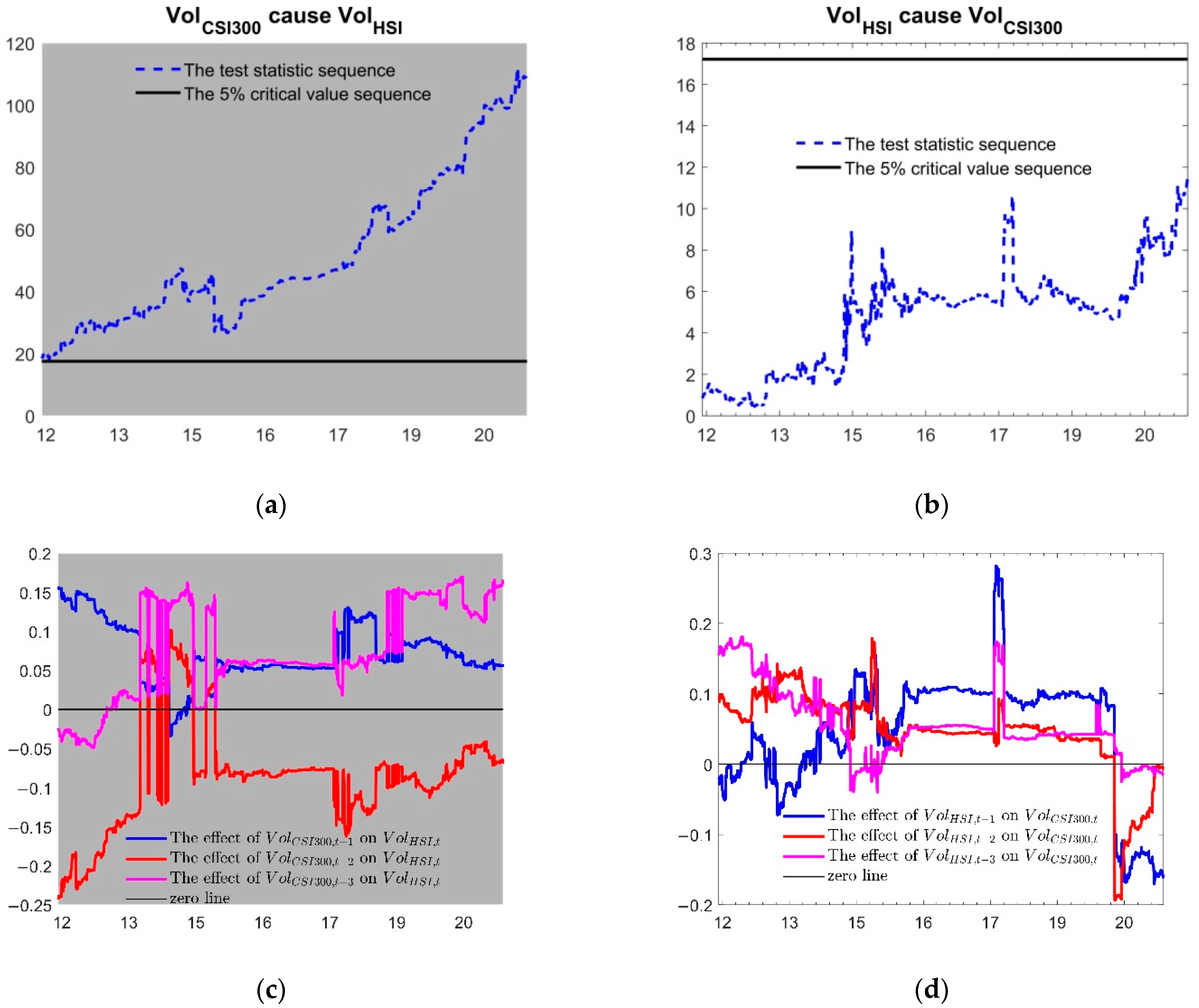

4.3. Time Varying Granger Test between Volatility Series

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Ding, Y.-J.; Feng, Y. The impact of market trading mechanism on A-H share price premium. Appl. Econ. Lett. 2018, 26, 594–600. [Google Scholar] [CrossRef]

- Hui, E.C.M.; Chan, K.K.K. Does the Shanghai-Hong Kong stock connect significantly affect the A-H premium of the stocks? Physica A 2018, 492, 207–214. [Google Scholar] [CrossRef]

- Pan, J.; Chi, J. How does the Shanghai-Hong Kong stock connect policy impact the A-H share premium? Emerg. Mark. Financ. Trade 2019, 57, 1912–1928. [Google Scholar] [CrossRef]

- Pavlidis, E.G.; Vasilopoulos, K. Speculative bubbles in segmented markets: Evidence from Chinese cross-listed stocks. J. Int. Money Financ. 2020, 109, 102222. [Google Scholar] [CrossRef]

- Luo, X.; Yu, X.; Qin, S.; Xu, Q. Option trading and the cross-listed stock returns: Evidence from Chinese A–H shares. J. Futures Mark. 2020, 40, 1665–1690. [Google Scholar] [CrossRef]

- Huang, Z.; Gao, W. Stock market liberalization and firm litigation risk—A quasi-natural experiment based on the Shanghai-Hong Kong stock connect policy. Appl. Econ. 2021, 53, 5619–5642. [Google Scholar] [CrossRef]

- Fan, Q.; Wang, T. The impact of Shanghai-Hong Kong stock connect policy on A-H share price premium. Financ. Res. Lett. 2017, 21, 222–227. [Google Scholar] [CrossRef]

- Deng, L.; Liao, M.; Luo, R.; Sun, J.; Xu, C. Does corporate social responsibility reduce share price premium? Evidence from China’s A- and H-shares. Pac.-Basin Financ. J. 2021, 67, 101569. [Google Scholar] [CrossRef]

- Cai, C.X.; McGuinness, P.B.; Zhang, Q. The pricing dynamics of cross-listed securities: The case of Chinese A- and H-shares. J. Bank. Financ. 2011, 35, 2123–2136. [Google Scholar] [CrossRef]

- Eun, C.S.; Sabherwal, S. Cross-border listings and price discovery: Evidence from US-listed Canadian stocks. J. Financ. 2003, 58, 549–575. [Google Scholar] [CrossRef] [Green Version]

- Frijns, B.; Indriawan, I.; Tourani-Rad, A. The interactions between price discovery, liquidity and algorithmic trading for U.S.-Canadian cross-listed shares. Int. Rev. Finan. Anal. 2018, 56, 136–152. [Google Scholar] [CrossRef]

- Wu, L.; Xu, K.; Meng, Q. Information flow and price discovery dynamics. Rev. Quant. Financ. Acc. 2020, 56, 329–367. [Google Scholar] [CrossRef]

- Bekhet, H.A.; Matar, A. Co-integration and causality analysis between stock market prices and their determinates in Jordan. Econ. Model. 2013, 35, 508–514. [Google Scholar] [CrossRef]

- Bahmani-Oskooee, M.; Ghodsi, S.H. Asymmetric causality between the U.S. housing market and its stock market: Evidence from state level data. J. Econ. Asymmetries 2018, 18, e00095. [Google Scholar] [CrossRef]

- Sun, X.; Fang, W.; Gao, X.; An, S.; Liu, S.; Wu, T. Time-varying causality inference of different nickel markets based on the convergent cross mapping method. Resour. Pol. 2021, 74, 102385. [Google Scholar] [CrossRef]

- Cai, C.X.; McGuinness, P.B.; Zhang, Q. Capital account reform and short- and long-run stock price leadership. Europ. J. Financ. 2015, 23, 916–945. [Google Scholar] [CrossRef] [Green Version]

- Dzhambova, K.; Tao, R.; Yuan, Y. Price leadership and asynchronous movements of multi-market listed stocks. Int. Rev. Finan. Anal. 2022, 79, 101970. [Google Scholar] [CrossRef]

- Shi, S.; Hurn, S.; Phillips, P.C.B. Causal change detection in possibly integrated systems: Revisiting the money-income relationship. J. Financ. Econ. 2020, 18, 158–180. [Google Scholar] [CrossRef] [Green Version]

- Shi, S.; Phillips, P.C.B.; Hurn, S. Change detection and the causal impact of the yield curve. J. Time Ser. Anal. 2018, 39, 966–987. [Google Scholar] [CrossRef] [Green Version]

- Shahzad, F.; Bouri, E.; Mokni, K.; Ajmi, A.N. Energy, agriculture, and precious metals: Evidence from time-varying Granger causal relationships for both return and volatility. Resour. Pol. 2021, 74, 102298. [Google Scholar] [CrossRef]

- Fang, L.; Chen, B.; Yu, H.; Qian, Y. The importance of global economic policy uncertainty in predicting gold futures market volatility: A GARCH-MIDAS approach. J. Futures Mark. 2018, 38, 413–422. [Google Scholar] [CrossRef]

- Kambouroudis, D.S.; McMillan, D.G.; Tsakou, K. Forecasting stock return volatility: A comparison of GARCH, implied volatility, and realized volatility models. J. Futures Mark. 2016, 36, 1127–1163. [Google Scholar] [CrossRef]

- Barucci, E.; Renò, R. On measuring volatility and the GARCH forecasting performance. J. Int. Finan. Mark. Inst. Money 2002, 12, 183–200. [Google Scholar] [CrossRef]

- Satchell, S.; Knight, J. Forecasting Volatility in the Financial Markets, 3rd ed.; Elsevier: Oxford, UK, 2007; pp. 101–119. [Google Scholar]

- Christopoulos, D.K.; Tsionas, E.G. Financial development and economic growth: Evidence from panel unit root and cointegration tests. J. Devel. Econ. 2004, 73, 55–74. [Google Scholar] [CrossRef]

- Calderón, C.; Liu, L. The direction of causality between financial development and economic growth. J. Devel. Econ. 2003, 72, 321–334. [Google Scholar] [CrossRef] [Green Version]

- Jalil, A.; Feridun, M. The impact of growth, energy and financial development on the environment in China: A cointegration analysis. Energy Econ. 2011, 33, 284–291. [Google Scholar] [CrossRef]

- Hsueh, S.; Hu, Y.; Tu, C. Economic growth and financial development in Asian countries: A bootstrap panel Granger causality analysis. Econ. Model. 2013, 32, 294–301. [Google Scholar] [CrossRef]

- Adekoya, O.B.; Oliyide, J.A. How COVID-19 drives connectedness among commodity and financial markets: Evidence from TVP-VAR and causality-in-quantiles techniques. Resour. Pol. 2021, 70, 101898. [Google Scholar] [CrossRef]

- Afshan, S.; Sharif, A.; Nassani, A.A.; Abro, M.M.Q.; Batool, R.; Zaman, K. The role of information and communication technology (internet penetration) on Asian stock market efficiency: Evidence from quantile-on-quantile cointegration and causality approach. Int. J. Financ. Econ. 2020, 26, 2307–2324. [Google Scholar] [CrossRef]

- Lin, A.; Shang, P.; Zhou, H. Cross-correlations and structures of stock markets based on multiscale MF-DXA and PCA. Nonlinear Dyn. 2014, 78, 485–494. [Google Scholar] [CrossRef]

- Ruan, Q.; Zhang, S.; Lv, D.; Lu, X. Financial liberalization and stock market cross-correlation: MF-DCCA analysis based on Shanghai-Hong Kong stock connect. Physica A 2018, 491, 779–791. [Google Scholar] [CrossRef]

- Harris, F.H.D.; McInish, T.H.; Shoesmith, G.L.; Wood, R.A. Cointegration, error correction, and price discovery on informationally linked security markets. J. Financ. Quant. Anal. 1995, 30, 563–579. [Google Scholar] [CrossRef]

- Kehrle, K.; Peter, F.J. Who moves first? An intensity-based measure for information flows across stock exchanges. J. Bank. Financ. 2013, 37, 1629–1642. [Google Scholar] [CrossRef]

- Su, Q.; Chong, T.T. Determining the contributions to price discovery for Chinese cross-listed stocks. Pac.-Basin Financ. J. 2007, 15, 140–153. [Google Scholar] [CrossRef]

- Ma, J.; Swan, P.L.; Song, F. Price discovery and information in an emerging market: Evidence from China. In Proceedings of the 2009 China International Conference in Finance, Guangzhou, China, 7 July 2009. [Google Scholar]

- Chan, M.K.; Kwok, S.S. Capital account liberalization and dynamic price discovery: Evidence from Chinese cross-listed stocks. Appl. Econ. 2015, 48, 517–535. [Google Scholar] [CrossRef]

- Li, M.L.; Chui, C.M.; Li, C.Q. Is pairs trading profitable on China AH-share markets? Appl. Econ. Lett. 2014, 21, 1116–1121. [Google Scholar] [CrossRef]

- Yuan, D.; Zhou, X.; Li, S. The dynamics of financial market integration between chinese A- and H-shares. Emerg. Mark. Financ. Trade 2018, 54, 2909–2924. [Google Scholar] [CrossRef]

- Chen, H.; Zhu, Y. An empirical study on the threshold cointegration of Chinese A and H cross-listed shares. J. Appl. Statist. 2015, 42, 2406–2419. [Google Scholar] [CrossRef]

- Tilfani, O.; Ferreira, P.; El Boukfaoui, M.Y. Dynamic cross-correlation and dynamic contagion of stock markets: A sliding windows approach with the DCCA correlation coefficient. Empir. Econ. 2019, 60, 1127–1156. [Google Scholar] [CrossRef]

- Eryiğit, M.; Eryiğit, R. Network structure of cross-correlations among the world market indices. Physica A 2009, 388, 3551–3562. [Google Scholar] [CrossRef]

- Ma, F.; Wei, Y.; Huang, D. Multifractal detrended cross-correlation analysis between the Chinese stock market and surrounding stock markets. Physica A 2013, 392, 1659–1670. [Google Scholar] [CrossRef]

- Cao, G.; Zhou, L. Asymmetric risk transmission effect of cross-listing stocks between mainland and Hong Kong stock markets based on MF-DCCA method. Physica A 2019, 526, 120741. [Google Scholar] [CrossRef]

- Xu, N.; Li, S. Segment stock market, foreign investors, and cross-correlation: Evidence from MF-DCCA and spillover index. Complexity 2020, 2020, 5836142. [Google Scholar] [CrossRef]

- Kaufmann, R.K.; Ullman, B. Oil prices, speculation, and fundamentals: Interpreting causal relations among spot and futures prices. Energy Econ. 2009, 31, 550–558. [Google Scholar] [CrossRef]

- Shrestha, K. Price discovery in energy markets. Energy Econ. 2014, 45, 229–233. [Google Scholar] [CrossRef]

- Hallack, L.N.; Kaufmann, R.; Szklo, A.S. Price discovery in Brazil: Causal relations among prices for crude oil, ethanol, and gasoline. Energ. Source Part B 2020, 15, 230–251. [Google Scholar] [CrossRef]

- Granger, C.W. Investigating causal relations by econometric models and cross-spectral methods. Econometrica 1969, 37, 424–438. [Google Scholar] [CrossRef]

- Thoma, M.A. Subsample instability and asymmetries in money-income causality. J. Econom. 1994, 64, 279–306. [Google Scholar] [CrossRef]

- Swanson, N.R. Money and output viewed through a rolling window. J. Monet. Econ. 1998, 41, 455–474. [Google Scholar] [CrossRef]

- Arora, V.; Shi, S. Energy consumption and economic growth in the United States. Appl. Econ. 2016, 48, 3763–3773. [Google Scholar] [CrossRef]

- Shi, G.; Liu, X.; Zhang, X. Time-varying causality between stock and housing markets in China. Financ. Res. Lett. 2017, 22, 227–232. [Google Scholar] [CrossRef]

- Si, D.; Li, X.; Jiang, S. Can insurance activity act as a stimulus of economic growth? Evidence from time-varying causality in China. Emerg. Mark. Financ. Trade 2018, 54, 3030–3050. [Google Scholar] [CrossRef]

- Phillips, P.C.; Shi, S.; Yu, J. Testing for multiple bubbles: Historical episodes of exuberance and collapse in the S&P 500. Int. Econ. Rev. 2015, 56, 1043–1078. [Google Scholar]

- Phillips, P.C.; Shi, S.; Yu, J. Testing for multiple bubbles: Limit theory of real-time detectors. Int. Econ. Rev. 2015, 56, 1079–1134. [Google Scholar] [CrossRef] [Green Version]

- Toda, H.Y.; Yamamoto, T. Statistical inference in vector autoregressions with possibly integrated processes. J. Econom. 1995, 66, 225–250. [Google Scholar] [CrossRef]

- Hammoudeh, S.; Ajmi, A.N.; Mokni, K. Relationship between green bonds and financial and environmental variables: A novel time-varying causality. Energy Econ. 2020, 92, 104941. [Google Scholar] [CrossRef]

- Emirmahmutoglu, F.; Denaux, Z.; Topcu, M. Time-varying causality between renewable and non-renewable energy consumption and real output: Sectoral evidence from the United States. Renew. Sust. Energ. Rev. 2021, 149, 111326. [Google Scholar] [CrossRef]

- Chen, C.; Chiang, S. Time-varying causality in the price-rent relationship: Revisiting housing bubble symptoms. J. Hous. Built Environ. 2020, 36, 539–558. [Google Scholar] [CrossRef]

- Hu, Y.; Hou, Y.G.; Oxley, L. What role do futures markets play in Bitcoin pricing? Causality, cointegration and price discovery from a time-varying perspective? Int. Rev. Finan. Anal. 2020, 72, 101569. [Google Scholar] [CrossRef]

- Raggad, B. Time varying causal relationship between renewable energy consumption, oil prices and economic activity: New evidence from the United States. Resour. Pol. 2021, 74, 102422. [Google Scholar] [CrossRef]

- Balcilar, M.; Ozdemir, Z.A.; Shahbaz, M. On the time-varying links between oil and gold: New insights from the rolling and recursive rolling approaches. Int. J. Finance Econ. 2019, 24, 1047–1065. [Google Scholar] [CrossRef]

- Zhang, X.; Jia, Y.; Lv, T. The impacts of the US dollar index and the investors’ expectations on the AH premium—A macro perspective. China Econ. Rev. 2020, 13, 249–269. [Google Scholar]

- Wang, W. Shanghai-Hong Kong stock exchange connect program: A story of two markets and different groups of stocks. J. Multinat. Finan. Manag. 2020, 55, 100630. [Google Scholar] [CrossRef]

- Li, S.; Chen, Q.A. Do the Shanghai-Hong Kong & Shenzhen-Hong Kong stock connect programs enhance co-movement between the mainland Chinese, Hong Kong, and U.S. stock markets? Int. J. Financ. Econ. 2020, 26, 2871–2890. [Google Scholar]

- Bacidore, J.M.; Sofianos, G. Liquidity provision and specialist trading in NYSE-listed non-US stocks. J. Financ. Econ. 2002, 63, 133–158. [Google Scholar] [CrossRef]

- Ding, W.; Levine, R.; Lin, C.; Xie, W. Corporate immunity to the COVID-19 pandemic. J. Financ. Econ. 2021, 141, 802–830. [Google Scholar] [CrossRef]

- Su, Z.; Liu, P.; Fang, T. Pandemic-induced fear and stock market returns: Evidence from China. Glob. Financ. J. 2021, 100644. [Google Scholar] [CrossRef]

- Corbet, S.; Hou, Y.; Hu, Y.; Oxley, L. The influence of the COVID-19 pandemic on asset-price discovery: Testing the case of Chinese informational asymmetry. Int. Rev. Finan. Anal. 2020, 72, 101560. [Google Scholar] [CrossRef]

- Baig, A.S.; Butt, H.A.; Haroon, O.; Rizvi, S.A.R. Deaths, panic, lockdowns and US equity markets: The case of COVID-19 pandemic. Financ. Res. Lett. 2021, 38, 101701. [Google Scholar] [CrossRef]

- Xue, S.; Zhou, S. Coping with the pandemic: Market segmentation and differential stock market reactions to COVID-19. 2021; Unpublished work. [Google Scholar]

- Gluzman, S. Nonlinear Approximations to Critical and Relaxation Processes. Axioms 2020, 9, 126. [Google Scholar] [CrossRef]

- Ge, X.; Lin, A. Dynamic causality analysis using overlapped sliding windows based on the extended convergent cross-mapping. Nonlinear Dyn. 2021, 104, 1753–1765. [Google Scholar] [CrossRef]

- Huo, R.; Ahmed, A.D. Return and volatility spillovers effects: Evaluating the impact of Shanghai-Hong Kong stock connect. Econ. Model. 2017, 61, 260–272. [Google Scholar] [CrossRef]

- Okorie, D.I.; Lin, B. Stock markets and the COVID-19 fractal contagion effects. Financ. Res. Lett. 2021, 38, 101640. [Google Scholar] [CrossRef] [PubMed]

- Shi, W.; Shang, P. Cross-sample entropy statistic as a measure of synchronism and cross-correlation of stock markets. Nonlinear Dyn. 2012, 71, 539–554. [Google Scholar] [CrossRef]

- So, M.K.P.; Chu, A.M.Y.; Chan, T.W.C. Impacts of the COVID-19 pandemic on financial market connectedness. Financ. Res. Lett. 2021, 38, 101864. [Google Scholar] [CrossRef]

- Zehri, C. Stock market comovements: Evidence from the COVID-19 pandemic. J. Econ. Asymmetries 2021, 24, e00228. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Index | Mean Model | GARCH Model |

|---|---|---|

| AHXA | Sparse ARMA(5,3) (AR2 and AR4 fixed at 0) | EGARCH(2,2) (Normal distribution) |

| AHXH | ARMA(1,0) | GJR-GARCH(2,1) (t distribution) |

| CSI | Sparse ARMA(4,4) (AR1, MA1, and MA2 fixed at 0) | EGARCH(1,1) (t distribution) |

| HSI | ARMA(2,2) | EGARCH(2,1) (t distribution) |

| Mean | Std. Dev. | Skewness | Kurtosis | JB | |

|---|---|---|---|---|---|

| Price | |||||

| CSI | 3320.952 | 787.512 | 0.567 * | 2.935 | 144.137 * |

| AHXA | 2158.179 | 486.335 | 0.046 | 1.795 * | 162.776 * |

| AHXH | 1971.335 | 250.006 | 0.410 * | 2.997 | 79.291 * |

| HSI | 24,064.616 | 3186.906 | 0.404 * | 2.422 * | 109.918 * |

| Return | |||||

| CSI | 0.000143 | 0.014934 | −0.654 * | 4.902 * | 2880.361 * |

| AHXA | 0.000083 | 0.014140 | −0.321 * | 6.215 * | 4366.804 * |

| AHXH | 0.000034 | 0.015164 | −0.064 | 2.779 * | 866.445 * |

| HSI | 0.000096 | 0.011932 | −0.318 * | 2.735 * | 882.803 * |

| Volatility | |||||

| CSI | 0.014 | 0.005 | 1.637 * | 8.355 * | 4406.751 * |

| AHXA | 0.013 | 0.005 | 1.881 * | 8.189 * | 4594.585 * |

| AHXH | 0.015 | 0.004 | 1.991 * | 7.668 * | 4210.519 * |

| HSI | 0.012 | 0.003 | 1.758 * | 6.779 * | 2979.322 * |

| Level | |||||||||

| ADF | Intercept | 0.6046 | 0.5956 | 0.0212 * | 0.2116 | <0.01 * | <0.01 * | <0.01 * | <0.01 * |

| Intercept and Trend | 0.2505 | 0.1942 | 0.0442 * | 0.0596 | <0.01 * | <0.01 * | <0.01 * | <0.01 * | |

| PP | Intercept | 0.8998 | 0.8834 | 0.0564 | 0.5175 | <0.01 * | <0.01 * | <0.01 * | <0.01 * |

| Intercept and Trend | 0.3944 | 0.3247 | 0.0312 * | 0.0368 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | |

| First difference | |||||||||

| ADF | Intercept | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * |

| Intercept and Trend | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | |

| PP | Intercept | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * |

| Intercept and Trend | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | <0.01 * | |

| Conclusion | |||||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lu, X.; Ye, Z.; Lai, K.K.; Cui, H.; Lin, X. Time-Varying Causalities in Prices and Volatilities between the Cross-Listed Stocks in Chinese Mainland and Hong Kong Stock Markets. Mathematics 2022, 10, 571. https://0-doi-org.brum.beds.ac.uk/10.3390/math10040571

Lu X, Ye Z, Lai KK, Cui H, Lin X. Time-Varying Causalities in Prices and Volatilities between the Cross-Listed Stocks in Chinese Mainland and Hong Kong Stock Markets. Mathematics. 2022; 10(4):571. https://0-doi-org.brum.beds.ac.uk/10.3390/math10040571

Chicago/Turabian StyleLu, Xunfa, Zhitao Ye, Kin Keung Lai, Hairong Cui, and Xiao Lin. 2022. "Time-Varying Causalities in Prices and Volatilities between the Cross-Listed Stocks in Chinese Mainland and Hong Kong Stock Markets" Mathematics 10, no. 4: 571. https://0-doi-org.brum.beds.ac.uk/10.3390/math10040571